calgary toronto moscow almaty/atyrau caracas rio de janeiro anti-corruption in international...

TRANSCRIPT

Calgary Toronto Moscow Almaty/Atyrau Caracas Rio de Janeiro

Anti-Corruption in International Mining Projects: Practical Risk Management and Compliance Strategies

Date: November 29, 2010

Presenter: Janne Duncan, Partner, Toronto office

Tel.: +1 416 202 6715Email: [email protected]

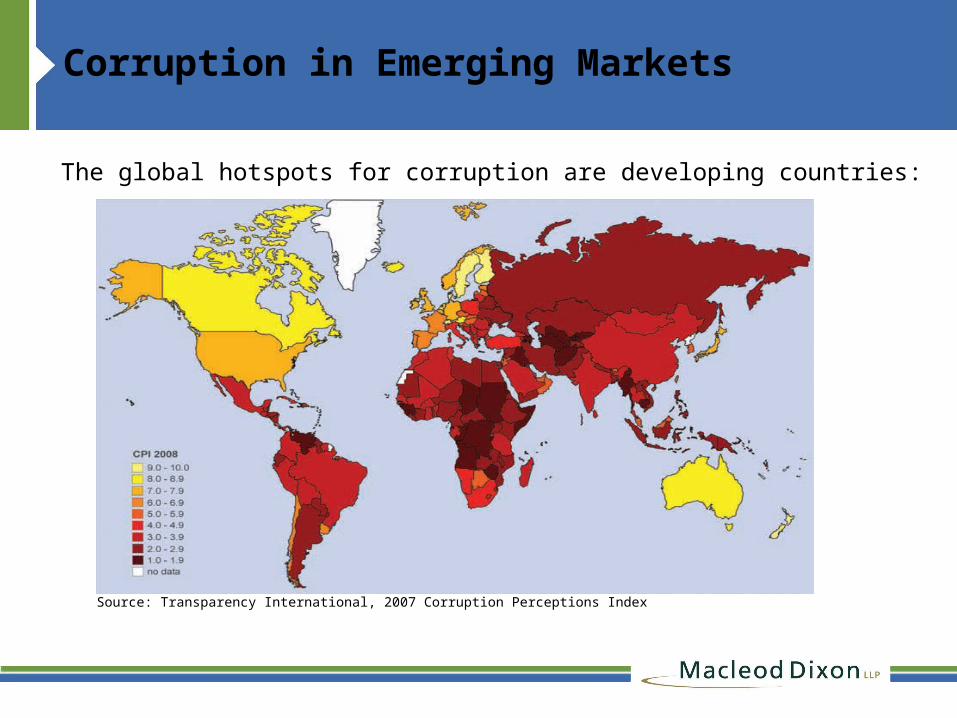

Corruption in Emerging Markets

The global hotspots for corruption are developing countries:

Source: Transparency International, 2007 Corruption Perceptions Index

Mining: An At-Risk Industry

• Why is mining an at-risk industry?

– operates in countries where there is a perceived high risk of corruption or where corruption is viewed as acceptable local practice

– mining industry typically requires discretionary government-issued licenses, concessions, planning consent and permits which requires regular dealings with government officials to

– mining companies are often involved in joint ventures or production-sharing agreements with foreign governments or state-owned enterprises in high-risk countries

OECD Convention

Convention on Combating Bribery of Foreign Public Officials in International Business Transactions (OECD Convention)

– establishes legally binding standards to criminalize bribery of foreign public officials in international business transactions

– adopted by the 33 OECD member countries and 5 non-member countries

Key Legislation in US, UK and Canada

US Foreign Corrupt Practices Act (FCPA)

UK Bribery Act, 2010[Not retroactive so prior legislation still relevant]

Canadian Foreign Corrupt

Practices Act (CFCPA)

Illegal to bribe a foreign official or political party with the intent to obtain or retain business

Illegal to bribe a foreign official, or accept a bribe, with the intent to obtain or retain business

Similar to US

Issuers (issued securities registered in US or files reports with SEC)- must keep accurate books and records of transactions- must maintain reasonable internal controls to prevent bribery

Strict (automatic) liability corporate offence of failing to prevent bribery by “associated person” – could include joint venture partners of the corporateDefense to show “adequate procedures” in place

None

Facilitation payments are permitted

Facilitation payments are NOT permitted

Similar to US

Voluntary disclosure None None

Key Legislation in US, UK and Canada: Jurisdiction – who is covered?

US Foreign Corrupt Practices Act (FCPA)

UK Bribery Act, 2010 Canadian Foreign Corrupt Practices

Act (CFCPA)

Issuers (issued securities registered in US or files reports with SEC) and Domestic Concerns (US Citizens, residents and companies) regardless of where offence

UK citizens, residents and companies regardless of where the offence occurs

No jurisdiction over Canadian citizens, Canadian residents or Canadian companies where act takes place outside Canada

Any non-US nationals or companies if it causes, directly or through agents, an act in furtherance of a corrupt payment to take place in the US

Any non-UK nationals or companies if an act or omission forming part of the offence took place within the UK

US parent companies can be liable for acts of foreign subsidiaries where authorized activity

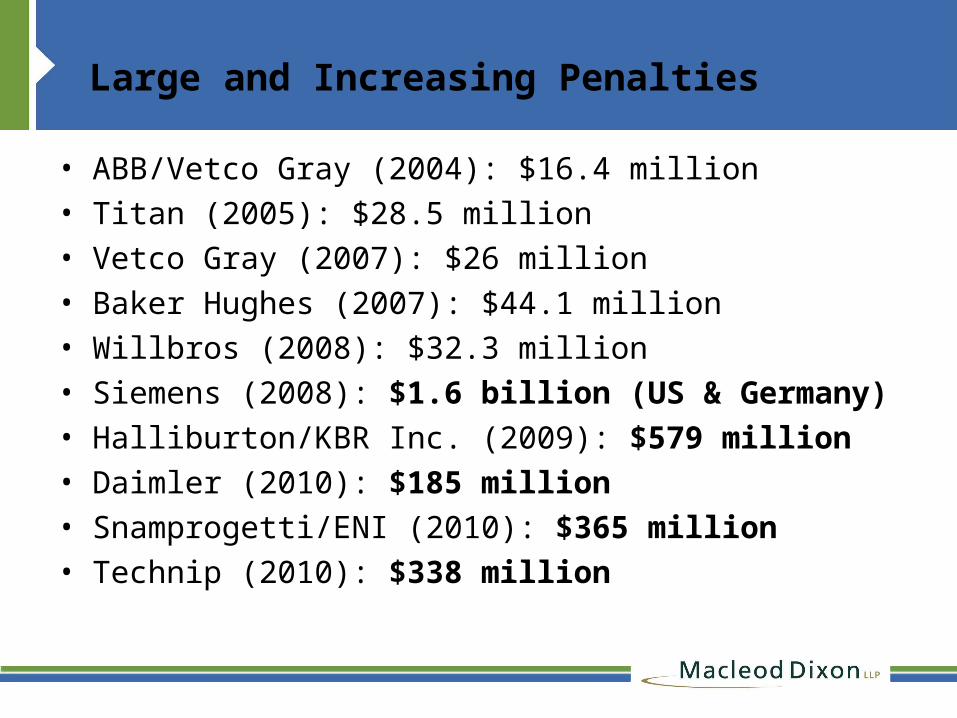

Large and Increasing Penalties

• ABB/Vetco Gray (2004): $16.4 million• Titan (2005): $28.5 million• Vetco Gray (2007): $26 million• Baker Hughes (2007): $44.1 million• Willbros (2008): $32.3 million• Siemens (2008): $1.6 billion (US & Germany)• Halliburton/KBR Inc. (2009): $579 million• Daimler (2010): $185 million• Snamprogetti/ENI (2010): $365 million• Technip (2010): $338 million

International Finance Institutional Efforts

• World Bank Group

– project agreements incorporate Anti-Corruption Guidelines by reference

– failure to comply can result in sanctions including debarment

• European Bank for Reconstruction & Development; Inter-American Development Bank Group; Asian Development Bank; African Development Bank Group (together “Multinational Development Banks”)

– with European Investment Bank Group and International Monetary Fund, agreed in September 2006 - Uniform Framework for Preventing and Combating Fraud and Corruption:

– April 2010, the Multinational Development Banks signed an agreement to cross-debar firms

Questions to ask

• If company is doing a financing, how to respond to due diligence questions from investors? Investment bankers?

• If company is the target in an M&A transaction, how to respond to due diligence questions from a [US? UK?] bidder?

• If company is entering into a joint venture, how to respond to due diligence questions from a [US? UK?] JV partner?

• How to cover due diligence questions from investors, investment bankers, a bidder in an M&A transaction or a potential JV partner about suppliers? JV partners? Foreign subsidiaries?

Best Practices to Minimize Corruption Risk: Effective Compliance Programs

Effective Anti-corruption Compliance Program

Essentials• Tone from the top – establish the right culture• Clear and well known written policy• Regular training of staff and related parties• Strong internal controls• Consistent and fair enforcement• Monitoring and revisions when needed

- US Sentencing Guidelines Manual, §8B2.1

Compliance – Prevention is better than cure…

• Create and Maintain Clear, Practical and Accessible Polices & Procedures

• Business Conduct Guidelines– active and passive bribery– anti-money laundering procedures– policy on gifts and hospitality– mandate transparent documentation of

expenses– whistle-blowing procedures and

disciplinary consequences

Compliance – Prevention is better than cure…

Top Level Commitment• Senior personnel should be responsible for

compliance• Program and direct reporting relationship to the

Board

Regular Risk Assessment• identifies the likely and potential corruption an

organization faces • risk assessments should extend beyond the

company (i.e. transaction risk, country risk, partnership risk)

Compliance – Prevention continued…

Training Best Practices• policy only effective if understood and adhered to

– periodic training of all managers and employees– in local language or involving locals– use real life examples that are relevant to job

function• monitor attendance and track results• update training practices according to changes in

the law and in the business• ensure access and availability to materials• annual reaffirmation of understanding and

commitment to Business Conduct Guidelines• use of questionnaires recommended

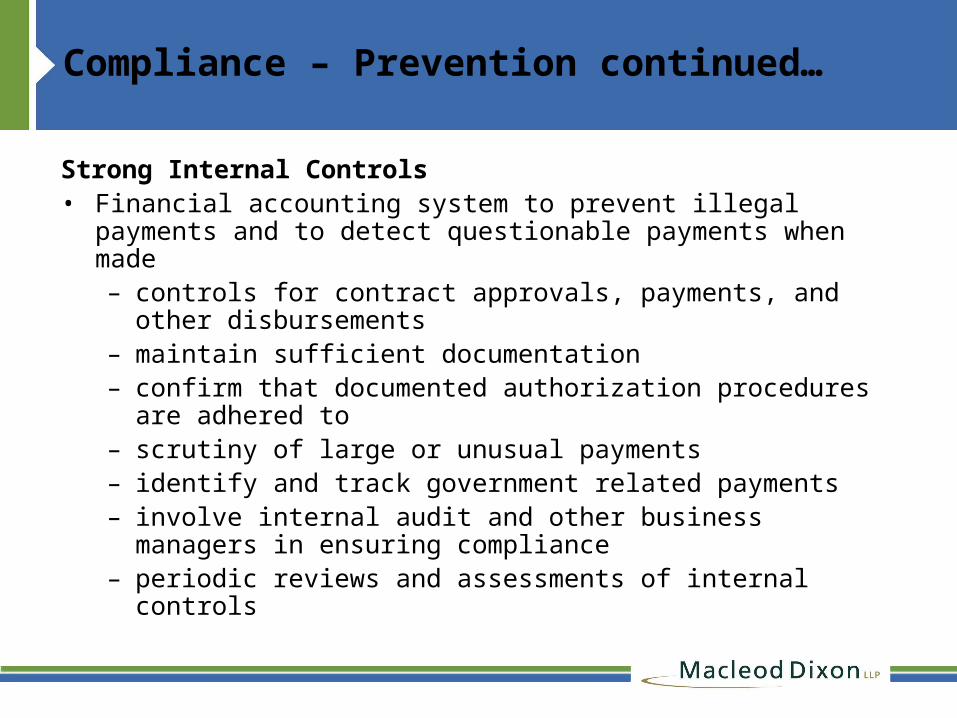

Compliance – Prevention continued…

Strong Internal Controls• Financial accounting system to prevent illegal payments

and to detect questionable payments when made– controls for contract approvals, payments, and other

disbursements– maintain sufficient documentation– confirm that documented authorization procedures are

adhered to– scrutiny of large or unusual payments– identify and track government related payments – involve internal audit and other business managers in

ensuring compliance– periodic reviews and assessments of internal controls

Compliance – Prevention continued…

Best Practices For Engaging Third Parties• Research the business reputation of third party• Conduct reasonable due diligence• Require formal application process• Obtain a list of references and interview them• Require approval of third party contracts by

centralized authority at the corporate level• Include anti-bribery provisions in third party

contracts• Monitor third parties and require additional

periodic certifications and audit• Remove decision-making authority in “grey

areas” (i.e. travel; entertainment; gifts)

Compliance – Prevention continued…

Watch for red flags during DD:

• secret or nontransparent details• payment to third country, third

party, or multiple accounts• relationship between agent and

foreign official• lack of sufficient resources (i.e.

staff) or competence to perform services offered

• requests for payments in cash or "bearer" securities

• foreign official recommends agent

• cash transactions or “off-book” payments

• use of side letters or stand alone consultant agreements

• lack of written agreements• payment to entity run by

former governmental officials • third party is a shell company

or use of unnecessary intermediaries

• unusually high commission payment or large increase in anticipated fee

• large dollar travel, gifts, entertainment or gratuities

Compliance – Prevention continued…

Research the reputation of foreign business partners

• Use official sources (i.e. Embassies or Consulates)• Review all publicly available information• Review incorporation documents to assess ownership

and ensure no governmental interest [if possible]• Determine if the company has been subject to past

corruption-related investigations• Interview proposed partner’s clients and customers• Determine whether further investigation is warranted

Compliance 2 – Implementation

Reporting• Provide ways for internal & external

parties to report compliance violations• Ensure employee whistle-blowers, who act

in good faith, are not disadvantaged• Periodic audits of remote offices

Investigate• Whether reported violations or due

diligence of agents, JVs partners etc

Compliance 2 – Implementation

Discipline• Impose appropriate penalties for compliance violations, as

sanctioned by labour laws• Ensure awareness of disciplinary procedure during training

Consistent and Fair Enforcement• Ensure policies are consistently enforced

– no special treatment for certain clients or senior level executives, officers or directors

• Ensure appropriate discipline and remedial action is taken• Promptly investigate concerns raised, particularly anonymous

hotline complaints– will serve to prevent whistleblower claims– assists in establishing a culture of compliance and encourage

more internal reporting

Compliance 3 – Monitor, Review, Respond

Prepare Response to Potential Incidents

• Determine whether and what to investigate

• Determine who will investigate• Agree on investigation plan• Self-reporting

Who We Are

Calgary, Toronto

CaracasMoscow

Macleod Dixon LLP is a global law firm with offices in seven key centers of the energy industry: Canada (Calgary and Toronto), Venezuela, Colombia, Brazil, Russian Federation and Kazakhstan. Nine lawyers from Macleod Dixon have just been ranked as leading practitioners by Who's Who Legal, Mining 2010 - the highest number of any Canadian-based firm. PLC Which Lawyer has also just ranked Macleod Dixon as the #1 Energy firm in Canada and Venezuela for 2010.

Macleod Dixon LLP is a global law firm with offices in seven key centers of the energy industry: Canada (Calgary and Toronto), Venezuela, Colombia, Brazil, Russian Federation and Kazakhstan. Nine lawyers from Macleod Dixon have just been ranked as leading practitioners by Who's Who Legal, Mining 2010 - the highest number of any Canadian-based firm. PLC Which Lawyer has also just ranked Macleod Dixon as the #1 Energy firm in Canada and Venezuela for 2010.

AlmatyRio de Janeiro

Bogota