canadian banks 2012 - perspectives on the canadian - pwc

TRANSCRIPT

www.pwc.com/ca/canadianbanks

Canadian Banks 2012Perspectives on the Canadian banking industry

2 Canadian Banks 2012

The firms of the PricewaterhouseCoopers global network (www.pwc.com) provide industry-focused assurance, tax and advisory services to build public trust and enhance value for clients and their stakeholders.

More than 169,000 people in 158 countries across our network share their thinking, experience and solutions to develop fresh perspectives and practical advice.

In Canada, PricewaterhouseCoopers LLP (www.pwc.com/ca) and its related entities have more than 5,700 partners and staff in offices across the country.

Perspectives on the Canadian banking industry 3

PwC is pleased to present the 2012 edition of Canadian Banks.

This edition of Canadian Banks reviews the 2011 financial results for the Big Six. We also take an in-depth look at some of the business impacts of regulatory changes.

Canada’s banks continued to perform well despite the turmoil in Europe over rising sovereign debt levels and the economic uncertainty in the United States. Canadian banks posted their third consecutive year of higher earnings following the 2008 global financial crisis. Many banks reported record profits.

Regulatory reform continues to increase costs and create uncertainty as various new regulations get finalized. Basel III, Dodd-Frank including the Volcker Rule, and FATCA will require banks to adapt to a changing regulatory landscape with capital, business model and resource implications. As you know, Canadian banks are actively reviewing the implications and taking action in order to meet these new regulatory requirements.

We hope you find this publication helpful and look forward to your feedback.

Bill McFarland CEO and Canadian Senior Partner PwC Canada

A message from our CEO and senior partnerBill McFarland

4 Canadian Banks 2012

ContentsPerspectives

Consumer lending survey 2012

2011 economic highlights

Analysis of 2011 results

Continued capital strength

Credit losses

Results by business segment

Market capitalization

Snapshot of the Big Six

Outlook

Appendix

Financial Services publications

Financial Services leadership team

06162026293235404257607678

Perspectives on the Canadian banking industry 5

Perspectives01

Regulatory risk is significant and banks are devoting considerable resources towards these new rules.

Perspectives on the Canadian banking industry 7

The occurrence of a financial crisis is nothing new. History has taught us that economies are prone to sharp market declines, bank runs and loss of consumer confidence. Deflating speculative bubbles are also not a new concept. The stock market crash of 1929, the dot-com bubble in 2000, and even Dutch tulip mania of the 1600s all shared similar characteristics. This all might lead one to wonder why market observers couldn’t have seen and prevented the recent financial crisis from taking shape.

The Group of Twenty (G20) countries was formed in 1999 to specifically address financial stability concerns arising from another financial crisis, in particular the 1997 Asian financial crisis. The group’s aim was to “broaden the dialogue on key economic and financial policy issues among systemically significant economies and promote cooperation to achieve stable and sustainable world economic growth that benefits all.”

Changes in technology, government trade policies, and the expansion of emerging markets had created new demands on government policy. Specifically, there was a growing need to address risks created by the integration of the global economy and financial markets. These risks did not diminish over the next decade and as the 2008 financial crisis demonstrated, the risk of events happening at one end of the globe can instantly impact markets thousands of miles away.

After meetings in Washington in November 2008 and in London in April 2009, the G20 agreed to expand the Financial Stability Forum, which was created by the G7 in 1999. The mandate of the new Financial Stability Board (FSB) included, among other aspects, assessing vulnerabilities in the financial system, promoting co-ordination between authorities responsible for financial stability, and advising on

market developments and their implications for regulatory policy. One clear theme of the mandate was that regulators could no longer act alone as the integrated global market required an enhanced, coordinated approach.

In September 2009, the FSB released its framework on Improving Financial Regulation. Early in the report, the FSB called out on G20 leaders to support international policy development and to “signal their determination to implement fully and consistently the reforms at national levels.” The details proposed changes to the quality and quantity of banks’ capital, reducing the moral hazard posed by systemically important institutions, strengthening the over-the-counter (OTC) derivatives market, and improving global liquidity.

With that began a tsunami of regulatory reform, being thrust upon the global integrated market economy. However, despite the importance of global consistency being stressed, what we are now seeing a little more than two years later is that protectionist pressures, driven by differences in legal frameworks, is having a significant impact on each country’s ability to implement these reforms. As a result, many are taking a jurisdictional approach for the actual implementation, rather than a global approach.

8 Canadian Banks 2012

Basel III

One of the cornerstones of the regulatory reform is the implementation of Basel III, developed by the Basel Committee on Banking Supervision. Basel III raises both the quality and quantity of the required regulatory capital base and enhances the risk coverage of the Basel II capital framework to capture major on-and off-balance sheet risks. It also strengthens the quality, consistency, and transparency of the capital base by defining and limiting the types of eligible capital instruments. Furthermore, it introduces significant new regulatory requirements for bank liquidity, net stable funding, leverage, counterparty credit risk, and conservation. Countercyclical buffers which “dampen” the pro-cyclical effects of Basel II minimum capital requirements were also introduced. One of the drawbacks noted of Basel II was that provisions increased in bad times but fell in good times. This prevented banks from building up an appropriate level of protection to prepare for economic downturns.

Basel III also addresses systemic risk and lack of transparency within the financial sector, including strong incentives for banks to move exposures to central clearing parties. It places higher risk weights on highly correlated exposures to financial institutions and adds measures to mitigate reliance on external credit ratings, and additional loss-absorbing capacity for systemically important banks.

While the Basel III rules may be global, it is up to each local regulator to oversee its implementation. With a January 1, 2013 start date for the phased in implementation, a lot of work is left to be done. Global debates are currently ongoing, discussing how the impacts of Basel III will be felt by each country. In Canada, the Office of the Superintendent of Financial Institutions (OSFI) is expected to release draft regulations in May 2012, with final guidance before the end of 2012.

Basel III will be challenging to implement, but Canadian banks are starting from a good position to adopt the provisions of Basel III compared to other international banks. The concept of deleveraging to meet these targets for some banks can lead to reduced credit availability in that country, hampering attempts at economic recovery. In Europe, European banks are purchasing sovereign debt at the request of the European Central Bank. These purchases will make it harder for those banks to meet Basel III targets if the quality of the debt does not improve. It also is counter-intuitive with the premise under Basel III of reducing risk, as additional capital will be required to be set aside to cover the potential for losses in riskier assets such as European sovereign debt.

Basel III phase-in will commence in Canada starting on January 1, 2013.

Perspectives on the Canadian banking industry 9

With banks being required to hold higher quality and greater levels of capital, there will be business implications. Larger levels of higher quality capital on the balance sheet of a bank generally produces lower levels of return. With banks holding greater levels of this capital, shareholder returns could be impacted. In terms of the type of capital being issued, Canadian banks last February responded to an OSFI release regarding the phase-out of certain non-qualifying capital instruments. These instruments contained redemption rights which could be triggered if a regulatory event occurred which changed their capital treatment. The banks clarified that they would not be redeeming these instruments during the Basel III phase-in period. By the time Basel III is fully implemented, these innovative capital instruments will no longer be recognized as regulatory capital, and as a result can no longer be issued by the banks seeking to increase their regulatory capital levels.

While still in the implementation stage for Basel III and with many hurdles still to be passed, the global market appears to be attempting to meet the FSB’s goal of having consistency at national levels. However, the same cannot be said for other regulations being developed on a country-by-country basis.

Regulatory Change

Key existing or emerging areas of regulatory direction also include the creation of living wills to ensure an orderly resolution process should a bank fail to protect the financial system. European proposed regulations such as the European Markets Infrastructure Regulation (EMIR) and the Markets in Financial Instruments Directive (MiFID) II to address OTC and trading reform have been designed with a view to strengthen market infrastructure and enhance transparency and disclosure.

The American Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank), enacted in July 2010, promises to impact almost every segment of the US financial services sector. However, it required significant rulemaking to take place to allow the implementation of the framework described in the act to occur. Dodd-Frank impacts not only every segment of the US financial services industry, but also impacts financial institutions that deal with banks with US operations in ways that may not have been fully anticipated. This can be seen most recently in discussions relating to one aspect of Dodd-Frank, the Volcker Rule.

10 Canadian Banks 2012

Volcker Rule

The Volcker Rule places prohibitions on banking entities from engaging in proprietary trading and certain relationships with hedge funds and private equity funds. Running throughout the Volcker Rule is the presumption that acting as “principal” is “speculating,” except where the rule says it is not. As a result, this could significantly change the economics of firms’ capital markets and trading businesses.

The comment period for the rule closed in January 2012 with significant feedback being received from financial institutions globally. OSFI and the five major Canadian banks delivered comment letters on the proposed rule to the US lawmakers expressing a number of concerns that would impact their banking operations.

OSFI conveyed that the proposal as it currently stands could potentially “hinder the ability of foreign financial institutions to efficiently manage their risks” as a number of the core systems utilized by the Canadian banks are US-based and therefore would be impacted by the Volcker Rule. This includes systems used for clearing and settling US transactions, US exchanges, and US-owned infrastructure.

In addition, OSFI noted that the current rule would only allow proprietary trading by banking entities in US Treasury, state, and municipal general, limited and pass-through obligations. Other foreign government securities currently don’t have an exemption.

The rule sees these types of transactions in the light of a “principal” relationship or “speculation” as they are trading for profit while putting their own capital at risk. However, as the Canadian banks play a key role in market-making for government securities in Canada, these transactions are multi-purpose. Restrictions in this area could impact liquidity and funding requirements.

The five largest Canadian banks expressed that rules relating to the definition of a “covered fund” would restrict the ability for investors, that might reside in the US, such as “snowbirds”, to continue to invest in certain Canadian bank-sponsored mutual funds.

OSFI and the five major Canadian banks delivered comment letters on the proposed rule to the US lawmakers expressing a number of concerns that would impact their banking operations.

Perspectives on the Canadian banking industry 11

FATCA

In an effort to stem increasing cases of income tax evasion by US persons subject to US tax and the difficulty of accessing foreign-based information due to foreign law privacy constraints, the US Government passed the Hiring Incentives to Restore Employment Act (HIRE) in 2010. Included in the legislation was the Foreign Account Tax Compliance Act (FATCA). FATCA’s objective is identifying US persons who

(i) directly own financial accounts at or investments in non-US financial institutions to earn income from the underlying investments, or

(ii) own directly or indirectly non-US entities having such accounts or investments.

Under this legislation, foreign financial institutions are broadly defined to include those accepting deposits, holding financial assets for the account of others, or engaged primarily in the business of investing or reinvesting in securities or derivatives.

Such institutions are subject to 30% withholding tax on the receipt of US source income (e.g., interest and dividends) and gross proceeds from the sale of US debt or equity interest (collectively “withholdable payments”) unless the institution enters into an agreement with the Internal Revenue Service (IRS) to identify and report on its existing and new US accountholders. Upon review of the institution’s client data and after application of specified due diligence procedures, those with actual or potential US indications who do not clarify their status, US persons refusing to provide privacy waivers, and other foreign financial institutions not entering into such agreements with the IRS will be subject to withholding on payments made to them by the financial institution. Some limited categories of foreign financial institutions considered at low risk for use by US persons for tax evasion will be exempt from FATCA withholding on payments they receive. An example of this latter category includes wholly owned government instrumentalities and certain pension plans.

To combat the use of non-US entities by US persons to own financial assets, a withholding agent will be required to withhold 30% on withholdable payments unless the entity certifies that it has no substantial US owners or provides the identification of such persons. Withholding agents will provide the ownership information to the IRS.

12 Canadian Banks 2012

While the legislation is relatively straightforward, the proposed regulations released on February 8, 2012 still leave many issues unanswered and contentious areas are deferred for additional industry consultation. What is clear is that, while the regulations attempt to take in to account industry comments to make the application of FATCA more practical, the drive for transparent government reporting is gaining momentum internationally. The FATCA regulations provide financial institutions with sufficient clarity to move forward to enter into agreements with the IRS and make the necessary systems and processes changes for an expected effective date of July 1, 2013.

Implementing FATCA may result in financial institutions incurring costs to:

• Change customer on-boarding systems and processes to include new data and supporting documentation necessary to classify the customer’s FATCA status;

• Examine existing client account data to identify US persons;

• Develop new or expanded withholding and reporting systems;

• Develop systems to calculate and publish quarterly information regarding the composition of US and non-US assets;

• Educate personnel and customers regarding the new requirements; and

• Update derivative contracts to address FATCA withholdings and confirm the counterparty’s FATCA status.

OTC derivatives

In relation to OTC derivatives, the G20 leaders agreed in September 2009 that “All standardized OTC derivative contracts should be traded on exchanges or electronic trading platforms, where appropriate, and cleared through central counterparties by end-2012 at the latest. OTC derivative contracts should be reported to trade repositories. Non-centrally cleared contracts should be subject to higher capital requirements.”

The aim of these requirements was to “improve transparency in the derivatives markets, mitigate systemic risk, and protect against market abuse.” Each country must take steps to ensure that their jurisdiction can ensure compliance with the G20 agreement.

Perspectives on the Canadian banking industry 13

Rather than focus on the progress being made by Canada and other jurisdictions, we will focus on the potential business and market implications of the anticipated changes. One such impact is that for those companies that use derivatives, either to take exposure or mitigate risk, the cost of doing so will increase. This could be the result of needing to post margin with a central counterparty for centrally cleared transactions or providing collateral to an individual counterparty for bilateral transactions, where previously no collateral may have been posted.

As margin or collateral is generally required to be in a liquid form, for example, cash or liquid highly rated securities, this will require an ability for derivative users to turn assets into cash or equivalents to meet these margin or collateral requirements, potentially on short notice. While this ability has generally been required for banks today, expanding this to include all derivative counterparties will require this ability to be replicated at non-bank financial institutions and corporates alike.

The ability to manage collateral effectively will be a skill required by all companies that use derivatives and will be an ongoing cost going forward.

14 Canadian Banks 2012

Operational risk

Under Basel, banks can use one of three approaches to measure their level of operational risk. One of these approaches is the Advanced Measurement Approach (AMA), which many of the Canadian banks are working towards. The purpose of AMA is to enhance operational risk measurement and management. The AMA framework requires effective governance, risk capture and assessment, and quantification of operational risk exposure. The benefits of using AMA include a potential reduction in the operational risk capital charge as capital will be based on risk exposures and not income levels, improved risk culture and understanding of the risks faced by the institution, and improved reputation amongst stakeholders through the use of more advanced risk-management methodologies.

Given the pace of regulatory change, operational risk management is at a crucial point in its development. While institutions are struggling to make AMA fully effective and embedded into the day-to-day management of the business, regulatory change may further increase the operational risk profile for many institutions.

However, there could be unsuspected advantages in the upheaval across the financial world. Under AMA, operational risk-capital modeling allows for the understanding of the institution’s level of exposure to operational risk. One component of the capital model is the business environment and internal control factors which provide a more forward-looking view, recognizing both improvements and deterioration in operational-risk profiles. As a result, management actions, such as the investment in internal controls can be reflected in the operational-risk capital.

While regulatory change is pushing institutions into a more general overhaul of internal compliance systems, procedures, and internal controls, it is also a “cleansing” opportunity to have a more streamlined regime that focuses on efficient and effective internal controls. By taking a strategic approach to internal controls under AMA, many institutions have the opportunity to benefit by a reduction in operational risk capital.

As new regulation increases capital costs, the need to boost returns by reducing expenses and bolstering revenues will intensify. 15th Annual Global CEO Survey – Banking and Capital Markets sector summary

Perspectives on the Canadian banking industry 15

Summary

The level and pace of regulatory change impacting Canadian banks is significant. Currently, Canadian banks are assessing the potential impacts of these regulations, the emerging rules, and responding in several ways:

• Undertaking analysis of the potential operating and strategic implications, for their businesses, products, customers, and the Canadian financial system;

• Responding to proposed regulations via comments to the relevant regulatory bodies to ensure their views are heard on unintended consequences as individual banks and on an industry basis;

• Liaising with government bodies such as OSFI and the Bank of Canada where proposals would negatively impact the Canadian economy, such as the Volcker rule, to provide their perspectives and ask for their engagement on the issue; and

• Preparing for changed processes, systems and business models based on views formed on the proposed regulations.

Ryan Leopold

Audit and Assurance Partner

416 869 2594

Jason Boggs

Consulting & Deals Partner

416 941 8311

Michael Bondy

Banking and Capital Markets Tax Leader

416 365 2724

Elisabeth Burke

Consulting & Deals Partner

416 687 8589

Rani Turna

Consulting & Deals Partner

416 869 2911

Overall, the banks have demonstrated their ability to weather the changes in the economic and regulatory environment to date. This is demonstrated by the $23.6 billion in profits earned during 2011 by the largest six Canadian Banks. Their capital levels remain strong which helps provides stability in uncertain times. The uncertainty created by the vast range of regulatory changes and proposals adds significant layers of complexity to the system. This can make basic planning decisions difficult for the banks, let alone dealing with the ever changing macro-economic environment. However, as the rules are finalized, additional clarity will be provided. Until that point is reached we will see banks operating in an evolving landscape, both in Canada and abroad.

The weight of the proposed regulatory changes, including new capital and liquidity demands, is going to be a key factor in determining business plans, changing the cost profile of many banking products. 15th Annual Global CEO Survey – Banking and Capital Markets sector summary

Consumer lending survey 201202

Perspectives on the Canadian banking industry 17

Canadians continue to feel confident about their debt levels. However, this confidence has somewhat softened in the last year, according to our annual consumer lending survey. They appear to be more concerned about the level of debt they carry and have indicated that they intend to reduce their debt level over the next year.

The survey of 1,200 Canadians, which was conducted by Leger Marketing, finds that 59% of respondents think their debt level is about right. One-third think it’s too high while 4% say it’s too low and another 4% did not answer the question. The results are interesting considering data from the Bank of Canada indicating that consumer debt is at an all time high and Statistics Canada reporting that the debt-to-income ratio of Canadians has reached a record high of 153% in the third quarter of 2011. Consumers still seem to be relatively comfortable despite having a debt-to-income ratio that’s similar to levels in the United States. This comfort could be in part due to the economic and structural differences between the US and Canadian markets. Furthermore, the trends in other key indicators such as the debt-to-asset or debt servicing ratios are more favourable.

Compared to last year, the survey results indicate a softening of confidence as we observed a three percentage point increase in the number of Canadians who believe that their debt level is too high.

Confidence levels vary by demographic: most concerned are people aged 25 to 55 (41% think it’s too high). Those who earn more are more confident about their debt levels. Sixty-four percent of those surveyed with household incomes above $100,000 say their debt levels are about right.

Respondents seem to be listening to Bank of Canada governor Mark Carney, who has warned Canadians about rising consumer debt levels. The majority of those surveyed – 63% – want to decrease the amount of debt they carry over the next year. Nearly one-third intend to maintain their debt levels, while 4% actually intend to go deeper into debt. The intent to reduce debt was present regardless of the respondent’s comfort level with their debt.

18 Canadian Banks 2012

65%forego buying

new electronics

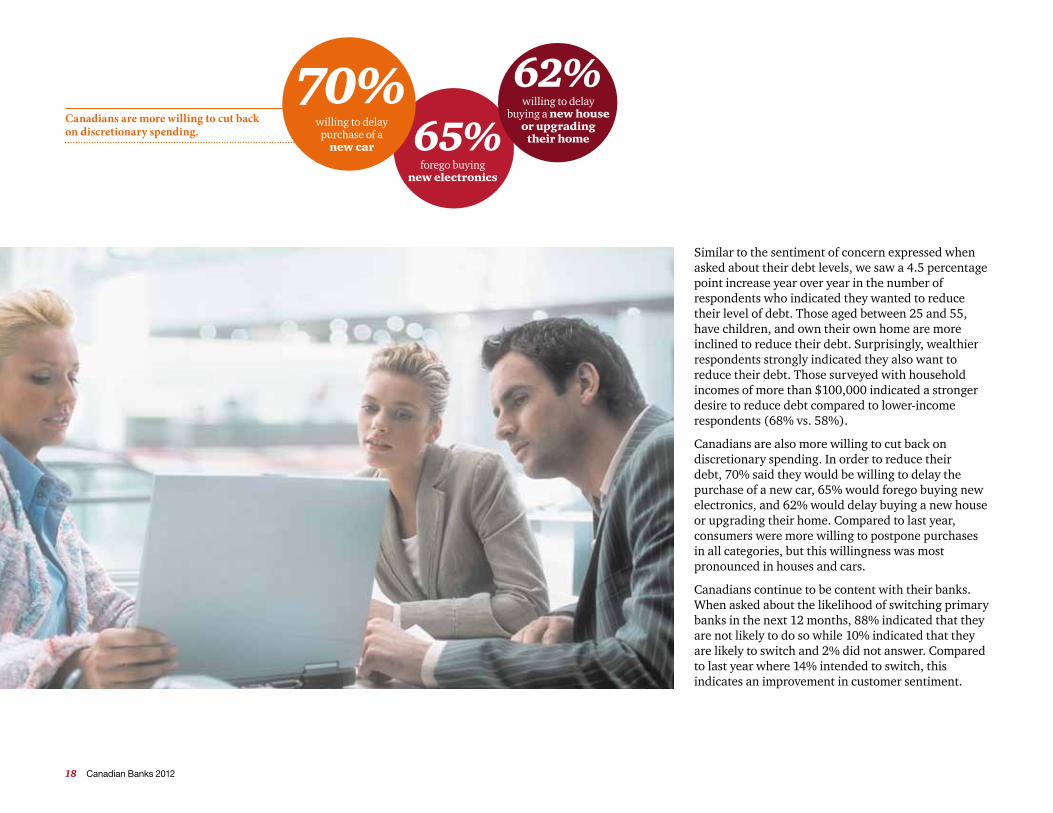

Similar to the sentiment of concern expressed when asked about their debt levels, we saw a 4.5 percentage point increase year over year in the number of respondents who indicated they wanted to reduce their level of debt. Those aged between 25 and 55, have children, and own their own home are more inclined to reduce their debt. Surprisingly, wealthier respondents strongly indicated they also want to reduce their debt. Those surveyed with household incomes of more than $100,000 indicated a stronger desire to reduce debt compared to lower-income respondents (68% vs. 58%).

Canadians are also more willing to cut back on discretionary spending. In order to reduce their debt, 70% said they would be willing to delay the purchase of a new car, 65% would forego buying new electronics, and 62% would delay buying a new house or upgrading their home. Compared to last year, consumers were more willing to postpone purchases in all categories, but this willingness was most pronounced in houses and cars.

Canadians continue to be content with their banks. When asked about the likelihood of switching primary banks in the next 12 months, 88% indicated that they are not likely to do so while 10% indicated that they are likely to switch and 2% did not answer. Compared to last year where 14% intended to switch, this indicates an improvement in customer sentiment.

70%willing to delay

purchase of a new car

62%willing to delay

buying a new house or upgrading

their home

Canadians are more willing to cut back on discretionary spending.

Perspectives on the Canadian banking industry 19

Banks may not have much pricing leeway to compete for customers on price so they will have to focus their attention on customer experience and product innovation.

Interestingly, the majority of respondents feel that their financial institution should play a role in helping them manage their level of debt. Eighty-two percent of respondents say banks should play a role in both determining the maximum amount of debt someone can responsibly take on and hold them to that limit. This was especially true of those with household incomes of more than $100,000 a year compared to those making less (85% vs. 71%).

Based on what Canadians have told us, we believe that banks will experience a slowdown in lending growth over the next 12 months, which will only serve to intensify competition for volume. Given the prolonged low interest rate environment, banks may not have much pricing leeway to compete for customers on price so they will have to focus their attention on customer experience and product innovation as means of differentiation. Furthermore, banks need to do so while being more efficient by managing the cost of delivery.

We will be releasing more detailed results from our second annual consumer lending survey later in March 2012. Visit www.pwc.com/ca/banking for more.

John MacKinlay

National Financial Services Consulting & Deals Leader

416 815 5117

Perspectives on the Canadian banking industry 20

Economic highlights03

While economic activity rebounded vigorously in the third quarter as these temporary factors were resolved, the economy continued to show signs of deceleration in the latter part of 2011.

Perspectives on the Canadian banking industry 21

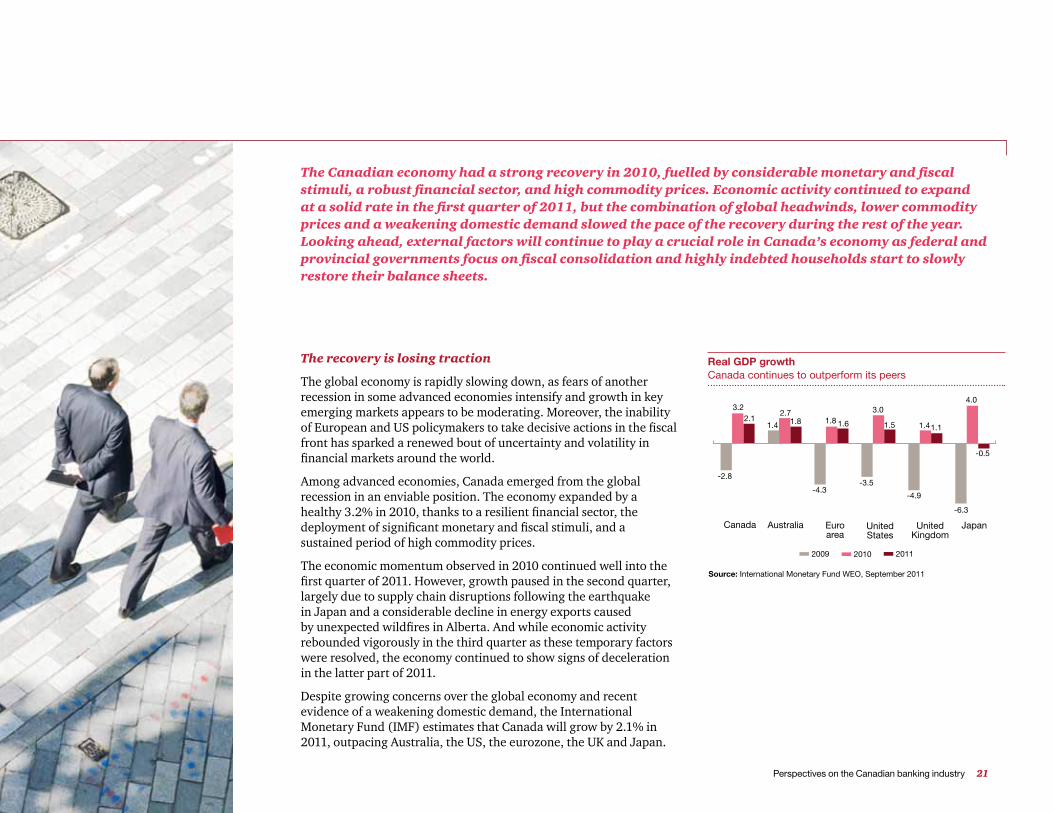

The Canadian economy had a strong recovery in 2010, fuelled by considerable monetary and fiscal stimuli, a robust financial sector, and high commodity prices. Economic activity continued to expand at a solid rate in the first quarter of 2011, but the combination of global headwinds, lower commodity prices and a weakening domestic demand slowed the pace of the recovery during the rest of the year. Looking ahead, external factors will continue to play a crucial role in Canada’s economy as federal and provincial governments focus on fiscal consolidation and highly indebted households start to slowly restore their balance sheets.

-8-7-6-5-4-3-2-101234

2010 20112009

Canada

-2.8

3.22.1

1.4

2.71.8 1.8 1.6

-4.3-3.5

-4.9

-6.3

1.41.1

4.0

-0.5

1.5

3.0

Australia Euroarea

UnitedKingdom

UnitedStates

Japan

Source: International Monetary Fund WEO, September 2011

Real GDP growth Canada continues to outperform its peers

The recovery is losing traction

The global economy is rapidly slowing down, as fears of another recession in some advanced economies intensify and growth in key emerging markets appears to be moderating. Moreover, the inability of European and US policymakers to take decisive actions in the fiscal front has sparked a renewed bout of uncertainty and volatility in financial markets around the world.

Among advanced economies, Canada emerged from the global recession in an enviable position. The economy expanded by a healthy 3.2% in 2010, thanks to a resilient financial sector, the deployment of significant monetary and fiscal stimuli, and a sustained period of high commodity prices.

The economic momentum observed in 2010 continued well into the first quarter of 2011. However, growth paused in the second quarter, largely due to supply chain disruptions following the earthquake in Japan and a considerable decline in energy exports caused by unexpected wildfires in Alberta. And while economic activity rebounded vigorously in the third quarter as these temporary factors were resolved, the economy continued to show signs of deceleration in the latter part of 2011.

Despite growing concerns over the global economy and recent evidence of a weakening domestic demand, the International Monetary Fund (IMF) estimates that Canada will grow by 2.1% in 2011, outpacing Australia, the US, the eurozone, the UK and Japan.

22 Canadian Banks 2012

Strong global headwinds ahead

As a small open economy, the fate of Canada depends in large part on the prospects of the global economy. In the near term, Canada faces several risks to its external environment, including growing concerns over the possibility of debt and banking crises in Europe, uncertainty surrounding economic growth in the US, and lower-than-expected economic activity in China and other large emerging markets.

The European sovereign debt crisis continued to unfold during 2011 and is threatening to spread into larger economies such as Italy and Spain. Europe’s inability to contain the crisis could pose a serious threat to the stability of the world banking system and global trade.

South of the border, Canada’s largest trading partner continues to struggle with a sluggish recovery; US growth in 2011 is estimated at a mere 1.6%. Moreover, the combination of a fragile labour market, a depressed housing market and a prolonged household deleveraging process is likely to hold back domestic demand well into 2012.

Finally, China and other emerging economies began to experience more sustainable rates of growth in the second half of 2011, in part thanks to monetary policy tightening policies introduced in the early part of the year. All these developments have also been reflected in lower demand for commodities and softer prices.

Some risks persist at home

In addition to successful accommodative fiscal and monetary policies, Canada was able to exit the global recession on firm footing thanks to strong private demand. Domestic consumption continued to be the engine of growth in 2011, albeit at a more moderate pace than in 2010. The unemployment rate, which reached a peak in August 2009 of 8.7%, continued to retreat gradually during the year, but still remains above pre-crisis levels.

The financial and corporate sectors retained a strong position during 2011. Bank profits are now back to pre-Lehman levels and business credit continues to grow, as firms take advantage of historically low funding costs. Additionally, capital ratios have remained at healthy levels and non-performing loans are well under control.

Canada was able to exit the global recession on firm footing.

Perspectives on the Canadian banking industry 23

On the other hand, Canadian households came out of the recession burdened by high levels of debt and lower levels of wealth, with household debt to disposable income reaching 152.98% in the third quarter of 2011. This, coupled with tepid growth in disposable income and a sharp reduction in commercial credit, led to lower levels of consumer spending in 2011. Furthermore, residential construction activity started to moderate in the second half of the year, as policies to tighten mortgage lending standards came into effect.

Going forward, the persistence of subdued household consumption and a cooling housing market could dampen domestic demand further, reversing the downward unemployment trend observed in 2010 and 2011.

Achieving the right policy mix

After deploying an effective and sizable fiscal stimulus during 2009 and 2010, estimated at 4% of gross domestic product (GDP), Canada is now shifting its focus towards fiscal consolidation. The Canadian government has expressed its intention to bring the budget back into surplus before 2016, as it plans to address long-term fiscal challenges.

Conversely, monetary policy is expected to remain highly accommodative in the medium term in light of renewed global uncertainties. The Bank of Canada, which has maintained the overnight interest rate at 1% since September 2010, is expected to stay on the sidelines well into 2012, reflecting subdued inflationary pressures, a relatively strong Canadian dollar and exceptionally low interest rates in the US.Primary balance = Primary net lending/borrowing

Source: IMF estmates. International Monetary Fund WEO, September 2011

60

55

50

70

80

75

90

85

65

-3

-4

-5

0

-1

-2

1

23

60

80

100

-5-4-3-2-10123

2006

2008

2010

2012

(f)

2013

(f)

2014

(f)

2015

(f)

2011

(f)

2009

2007

Primary balance (right scale)Gross debt

% o

f GD

P

Gross public debt and primary balance – shifting towards fiscal consolidation

0

2

1

4

3

5%

0

1

2

3

4

5

2008

2009

2010

2011

2008

2008

-220

08-4

2008

-620

08-8

2008

-920

08-1

120

0920

09-3

2009

-420

09-6

2009

-820

09-1

020

09-1

120

1020

10-3

2010

-520

10-6

2010

-820

10-1

020

10-1

220

1120

11-3

2011

-520

11-7

2011

-820

11-1

020

11-1

2

Last observation: December 23, 2011 Source: Bank of Canada

Target for overnight rate – awaiting further developments

24 Canadian Banks 2012

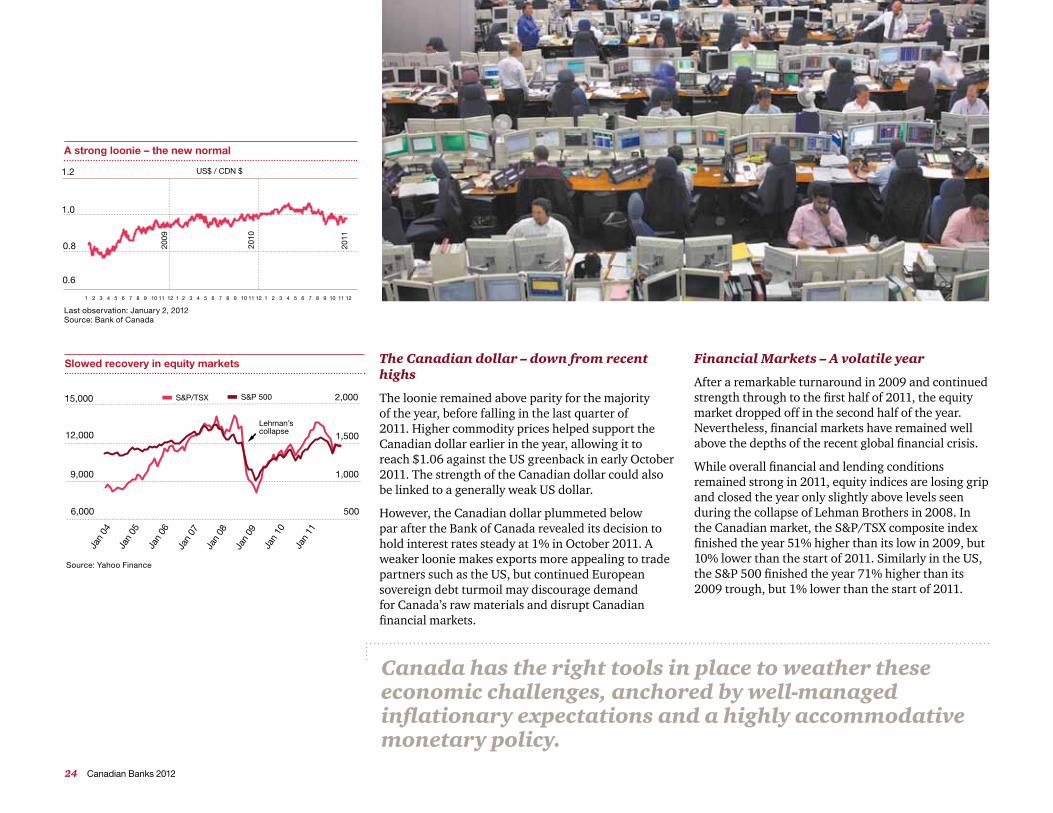

The Canadian dollar – down from recent highs

The loonie remained above parity for the majority of the year, before falling in the last quarter of 2011. Higher commodity prices helped support the Canadian dollar earlier in the year, allowing it to reach $1.06 against the US greenback in early October 2011. The strength of the Canadian dollar could also be linked to a generally weak US dollar.

However, the Canadian dollar plummeted below par after the Bank of Canada revealed its decision to hold interest rates steady at 1% in October 2011. A weaker loonie makes exports more appealing to trade partners such as the US, but continued European sovereign debt turmoil may discourage demand for Canada’s raw materials and disrupt Canadian financial markets.

Financial Markets – A volatile year

After a remarkable turnaround in 2009 and continued strength through to the first half of 2011, the equity market dropped off in the second half of the year. Nevertheless, financial markets have remained well above the depths of the recent global financial crisis.

While overall financial and lending conditions remained strong in 2011, equity indices are losing grip and closed the year only slightly above levels seen during the collapse of Lehman Brothers in 2008. In the Canadian market, the S&P/TSX composite index finished the year 51% higher than its low in 2009, but 10% lower than the start of 2011. Similarly in the US, the S&P 500 finished the year 71% higher than its 2009 trough, but 1% lower than the start of 2011.

Canada has the right tools in place to weather these economic challenges, anchored by well-managed inflationary expectations and a highly accommodative monetary policy.

6,000

9,000

12,000

15,000

500

1,000

1,500

2,000

6000

9000

12000

15000

500

1000

1500

2000

Jan

04

Jan

06

Jan

08

Jan

10

Jan

11

Jan

09

Jan

07

Jan

05

S&P 500S&P/TSX

Lehman’scollapse

Source: Yahoo Finance

Slowed recovery in equity markets

0.6

0.8

1.0

1.2

0.6

0.8

1.0

1.2

US$ / CDN $20

09

2010

2011

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12

Last observation: January 2, 2012 Source: Bank of Canada

A strong loonie – the new normal

Perspectives on the Canadian banking industry 25

Contributing economists:

Diego Mesa Puyo

Economics and Statistics Practice, Vancouver

604 806 7119

Jessica Yu

Economics and Statistics Practice, Vancouver

604 806 7521

1 Bank of Canada Monetary Policy Report, January 2012

0

1

2

3

4

5

0

1

2

3

4

5

0

1

2

3

4

5

6

0

1

2

3

4

5

6

6%

3-month Canadian dollar offering rate5 year debt swaped into 3 month floating rate debt

3-month overnight index swap

Jul 0

7O

ct 0

7Ja

n 08

Apr 0

8Ju

l 08

Oct

08

Jan

09Ap

r 09

Jul 0

9O

ct 0

9Ja

n 10

Apr 1

0Ju

l 10

Oct

10

Jan

11Ap

r 11

Jul 1

1

Notes: The 3-month CDOR is the average bid-side rate for Canadian bankers’ acceptances determined daily from a survey of market makers and can be used as a proxy for the cost of 3-month bank funding. Five-year debt swapped into 3-month floating rate debt is an indicator of the rate for senior deposit notes, and provides an indication of the longer-term cost of bank funding. The 3-month OIS rate represents the expected overnight interest rate over the 3-month period and can be used as a point of reference to compare the two measures of the cost of wholesale bank funding.

Source: Bank of Canada

3-month overnight index swap

Notes: The effective interest rate for households is a weighted-average of various mortgage and consumer credit interest rates. The weights are derived from residential mortgage and consumer credit data, adjusted for additional information provided by financial institutions. The effective interest rate for businesses is a weighted-average borrowing rate for new lending to non-financial businesses, estimated as a function of bank and market interest rates. The weights are derived from business credit data.

Source: Bank of Canada

3

4

5

6

7

8%

3

4

5

6

7

8

3

4

5

6

7

8

Jan

07Ap

r 07

Jul 0

7O

ct 0

7Ja

n 08

Apr 0

8Ju

l 08

Oct

08

Jan

09Ap

r 09

Jul 0

9O

ct 0

9Ja

n 10

Apr 1

0Ju

l 10

Oct

10

Jan

11Ap

r 11

Jul 1

1O

ct 1

1

Business effective interest rate

Household effective interest rate

Weekly effective interest rates

Outlook for the Canadian economy

As a result of weakening external demand and moderating household spending, the outlook for the Canadian economy has darkened compared to the prospects faced in early 2011. Continued risks from financial markets turmoil, linked to the European debt crisis, along with high levels of household indebtedness and fiscal consolidation are likely to hamper consumer and business confidence in the near term. Moreover, the persistent strength of the Canadian dollar, coupled with a very fragile recovery in the US and moderating growth in key emerging economies could restrain export performance in 2012, further tempering the speed of economic growth.

However, Canada has the right tools in place to weather these economic challenges, anchored by well-managed inflationary expectations and a highly accommodative monetary policy. The Bank of Canada is calling for growth of 2.0% in 2012 followed by 2.8% in 2013. Canadian banks are expected to remain well capitalized in 2012, with high levels of liquidity and easily accessible funding at relatively low rates by global standards.

Analysis of 2011 results04

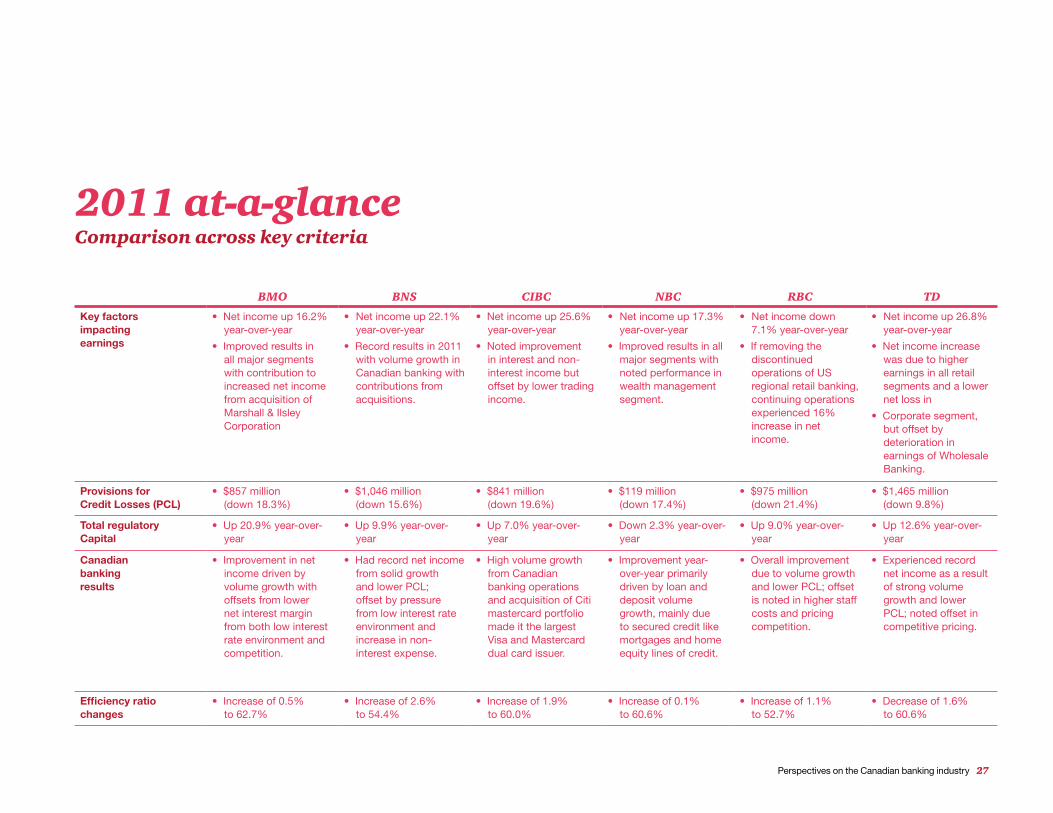

Comparison across key criteria2011 at-a-glance

BMO BNS CIBC NBC RBC TD

Key factors impacting earnings

• Net income up 16.2% year-over-year

• Improved results in all major segments with contribution to increased net income from acquisition of Marshall & Ilsley Corporation

• Net income up 22.1% year-over-year

• Record results in 2011 with volume growth in Canadian banking with contributions from acquisitions.

• Net income up 25.6% year-over-year

• Noted improvement in interest and non-interest income but offset by lower trading income.

• Net income up 17.3% year-over-year

• Improved results in all major segments with noted performance in wealth management segment.

• Net income down 7.1% year-over-year

• If removing the discontinued operations of US regional retail banking, continuing operations experienced 16% increase in net income.

• Net income up 26.8% year-over-year

• Net income increase was due to higher earnings in all retail segments and a lower net loss in

• Corporate segment, but offset by deterioration in earnings of Wholesale Banking.

Provisions for Credit Losses (PCL)

• $857 million (down 18.3%)

• $1,046 million (down 15.6%)

• $841 million (down 19.6%)

• $119 million (down 17.4%)

• $975 million (down 21.4%)

• $1,465 million (down 9.8%)

Total regulatory Capital

• Up 20.9% year-over-year

• Up 9.9% year-over-year

• Up 7.0% year-over-year

• Down 2.3% year-over-year

• Up 9.0% year-over-year

• Up 12.6% year-over-year

Canadian banking results

• Improvement in net income driven by volume growth with offsets from lower net interest margin from both low interest rate environment and competition.

• Had record net income from solid growth and lower PCL; offset by pressure from low interest rate environment and increase in non-interest expense.

• High volume growth from Canadian banking operations and acquisition of Citi mastercard portfolio made it the largest Visa and Mastercard dual card issuer.

• Improvement year-over-year primarily driven by loan and deposit volume growth, mainly due to secured credit like mortgages and home equity lines of credit.

• Overall improvement due to volume growth and lower PCL; offset is noted in higher staff costs and pricing competition.

• Experienced record net income as a result of strong volume growth and lower PCL; noted offset in competitive pricing.

Efficiency ratio changes

• Increase of 0.5% to 62.7%

• Increase of 2.6% to 54.4%

• Increase of 1.9% to 60.0%

• Increase of 0.1% to 60.6%

• Increase of 1.1% to 52.7%

• Decrease of 1.6% to 60.6%

Perspectives on the Canadian banking industry 27

28 Canadian Banks 2012

13.7217.29

11.414.47

23.1020.13

With the exception of CIBC and RBC, all banks reported higher revenues when compared to prior year.

1Total revenue is defined as net interest income plus other income.

Total revenue1 ($ billions)

With the exception of RBC and BMO, all banks experienced an increase in ROE.

0 5 10 15 20 25

12.9%13.9%

21.3%

14.0%19.1%

17.7%

BMOBNS

CIBCNBCRBC

TD

Return on equity (ROE) (%)

0 1 2 3 4 5 6 7 8

3.216.45

7.32

5.284.62

6.93

BMOBNS

CIBCNBCRBC

TD

CIBC and RBC had noted decreases to their EPS; all other banks recorded increases.

Earnings per share (EPS) ($)

Net income for all banks increased from prior year except RBC.

0 1 2 3 4 5 6

4.855.89

3.27

3.085.18

1.21

BMOBNS

CIBCNBCRBC

TD

Net income ($ billions)

14.9%13.9%

18.4%16.9%

15.3%16.0%

Most banks recorded an increase in Tier 1 capital ratio except BMO and NBC.

Total capital ratio (%)

0 3 6 9 12 15

BMOBNS

CIBCNBCRBC

TD14.45

13.08

8.61

7.359.56

2.92

All banks reported higher expenditures than prior year.

Non-interest expense (NIE) ($ billions)

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

2.082.61

3.51

2.802.05

2.74

BMOBNS

CIBCNBCRBC

TD

BMO is the only bank to remain unchanged; all other banks increased their dividend declared.

Dividends declared ($ per share)

2011 key metrics

Perspectives on the Canadian banking industry 29

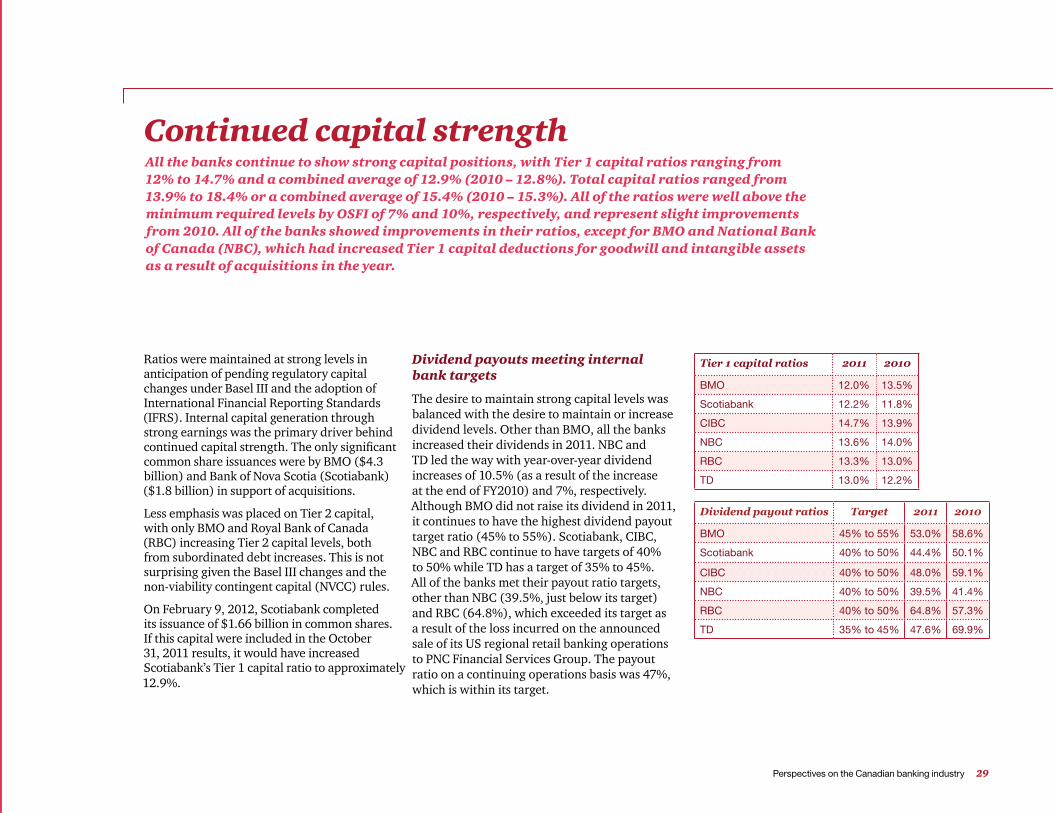

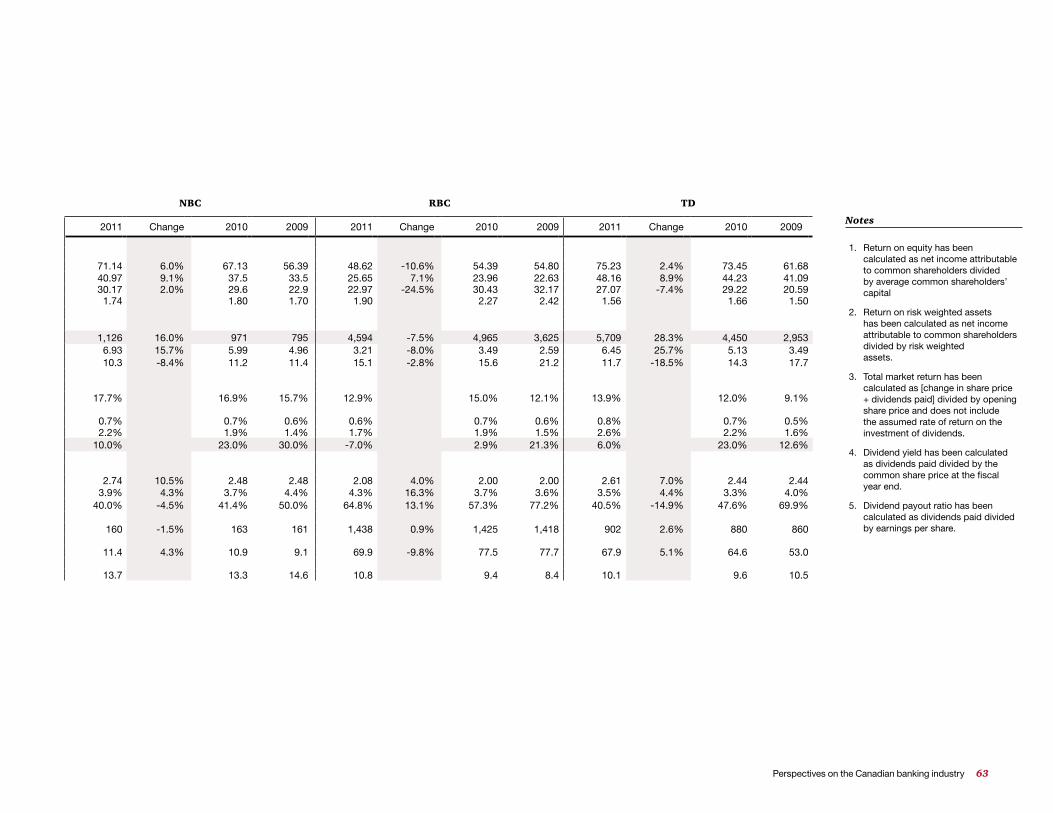

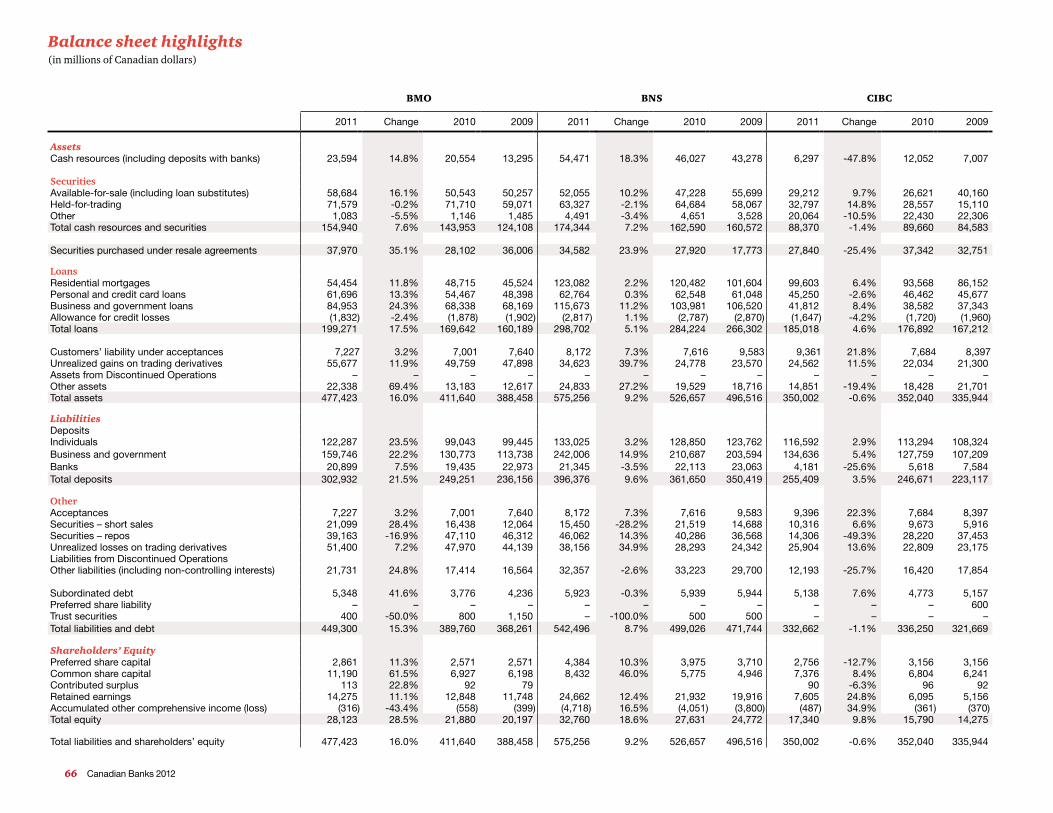

Ratios were maintained at strong levels in anticipation of pending regulatory capital changes under Basel III and the adoption of International Financial Reporting Standards (IFRS). Internal capital generation through strong earnings was the primary driver behind continued capital strength. The only significant common share issuances were by BMO ($4.3 billion) and Bank of Nova Scotia (Scotiabank) ($1.8 billion) in support of acquisitions.

Less emphasis was placed on Tier 2 capital, with only BMO and Royal Bank of Canada (RBC) increasing Tier 2 capital levels, both from subordinated debt increases. This is not surprising given the Basel III changes and the non-viability contingent capital (NVCC) rules.

On February 9, 2012, Scotiabank completed its issuance of $1.66 billion in common shares. If this capital were included in the October 31, 2011 results, it would have increased Scotiabank’s Tier 1 capital ratio to approximately 12.9%.

Dividend payouts meeting internal bank targets

The desire to maintain strong capital levels was balanced with the desire to maintain or increase dividend levels. Other than BMO, all the banks increased their dividends in 2011. NBC and TD led the way with year-over-year dividend increases of 10.5% (as a result of the increase at the end of FY2010) and 7%, respectively. Although BMO did not raise its dividend in 2011, it continues to have the highest dividend payout target ratio (45% to 55%). Scotiabank, CIBC, NBC and RBC continue to have targets of 40% to 50% while TD has a target of 35% to 45%. All of the banks met their payout ratio targets, other than NBC (39.5%, just below its target) and RBC (64.8%), which exceeded its target as a result of the loss incurred on the announced sale of its US regional retail banking operations to PNC Financial Services Group. The payout ratio on a continuing operations basis was 47%, which is within its target.

Continued capital strengthAll the banks continue to show strong capital positions, with Tier 1 capital ratios ranging from 12% to 14.7% and a combined average of 12.9% (2010 – 12.8%). Total capital ratios ranged from 13.9% to 18.4% or a combined average of 15.4% (2010 – 15.3%). All of the ratios were well above the minimum required levels by OSFI of 7% and 10%, respectively, and represent slight improvements from 2010. All of the banks showed improvements in their ratios, except for BMO and National Bank of Canada (NBC), which had increased Tier 1 capital deductions for goodwill and intangible assets as a result of acquisitions in the year.

Tier 1 capital ratios 2011 2010

BMO 12.0% 13.5%

Scotiabank 12.2% 11.8%

CIBC 14.7% 13.9%

NBC 13.6% 14.0%

RBC 13.3% 13.0%

TD 13.0% 12.2%

Dividend payout ratios Target 2011 2010

BMO 45% to 55% 53.0% 58.6%

Scotiabank 40% to 50% 44.4% 50.1%

CIBC 40% to 50% 48.0% 59.1%

NBC 40% to 50% 39.5% 41.4%

RBC 40% to 50% 64.8% 57.3%

TD 35% to 45% 47.6% 69.9%

30 Canadian Banks 2012

Transition to IFRS will reduce capital levels

All of the banks presented preliminary opening IFRS reconciliations as of November 1, 2010, their opening balance sheet date. Decreases in shareholder’s equity ranging from 3.5% (Scotiabank) to 9.1% (RBC) are expected on the transition to IFRS. Increases in assets-to-capital multiples are also anticipated. However, the impact to regulatory capital and the multiples are cushioned by OSFI’s transitional guidance, permitting the banks to phase in the impact of IFRS on Tier 1 capital over a five-quarter period beginning in Q1 2012. OSFI’s transitional relief to exclude residential mortgages from Canada Mortgage and Housing Corporation (CMHC) securitizations prior to March 31, 2010, recognized back on balance sheet under IFRS, will also reduce the impact to assets-to-capital multiples.

Basel III

Although full Basel III implementation is not until January 1, 2019, the transitional arrangements commence January 1, 2013. OSFI is expected to release updated guidance in Spring 2012. The banks continue to prepare for these enhanced capital requirements both in terms of quality of capital and quantity of capital, but they are well positioned for the Basel III requirements thanks to their strong capital positions and historical profitability.

OSFI issued guidance in August 2011, outlining NVCC requirements for instruments issued by Canadian banks. All instruments issued after December 31, 2012 must meet these NVCC requirements to qualify as regulatory capital. Existing instruments need to be assessed or amended to meet NVCC criteria. Only CIBC ($881 million of its non-cumulative preferred shares) and TD (certain instruments issued by its US subsidiaries) have indicated that some of its instruments will be treated as NVCC under Basel III. Non-common share capital that does not meet Basel III requirements will be subject to grandfathering provisions, with recognition as regulatory capital phased out over a 10-year period beginning January 1, 2013. This is expected to apply to all of the banks. CIBC and TD are the only ones that have indicated they expect to exercise a regulatory event redemption right only in FY2022 for non-common capital instruments that will not qualify and have not matured by that date.

Perspectives on the Canadian banking industry 31

Other Basel II changes

Before Basel III is effective, institutions will also be affected by revisions to Basel II. Effective as of January 1, 2012, banks are required to implement market risk guidelines to include stressed value-at-risk and an incremental risk charge in market risk capital. These changes will result in increases to risk-weighted assets.

Also effective at the beginning of 2012, insurance subsidiaries held prior to January 1, 2007 will be deducted 50% from Tier 1 capital and 50% from Tier 2 capital, as opposed to deducting 100% from Tier 2 capital. The impact of this change will result in reductions to Tier 1 capital but not to total capital.

Dodd-Frank’s capital implications

While the Dodd–Frank Wall Street Reform and Consumer Protection Act was enacted in the US in July 2010, many of its provisions have not been written yet. The banks have been closely monitoring and commenting on the potential implications to date, such as the limits on interchange fees, regulation of over-the-counter derivatives markets, and the restrictions on proprietary trading and sponsorship of private investment funds (the much debated Volcker Rule).

Effective as of January 1, 2012, banks are required to implement market risk guidelines to include stressed value-at-risk and an incremental risk charge in market risk capital.

However, Dodd-Frank also has potential implications to capital requirements. On December 20, 2011, the US Federal Reserve proposed steps to strengthen regulation and supervision of banks with more than US$50 billion in assets. The proposal, with comments requested by March 31, 2012, includes a wide range of measures such as capital, liquidity, credit exposure, stress testing, risk management, and early remediation requirements. Sound similar to Basel III? Many of the proposed requirements have a phased-in approach with the intention to converge with Basel III, but the Federal Reserve also indicated that it’s carefully considering what changes to the standards it may recommend to Basel III based on the results of this observation. Canadian banks will need to be mindful of the potential implications of these standards on their US subsidiaries.

32 Canadian Banks 2012

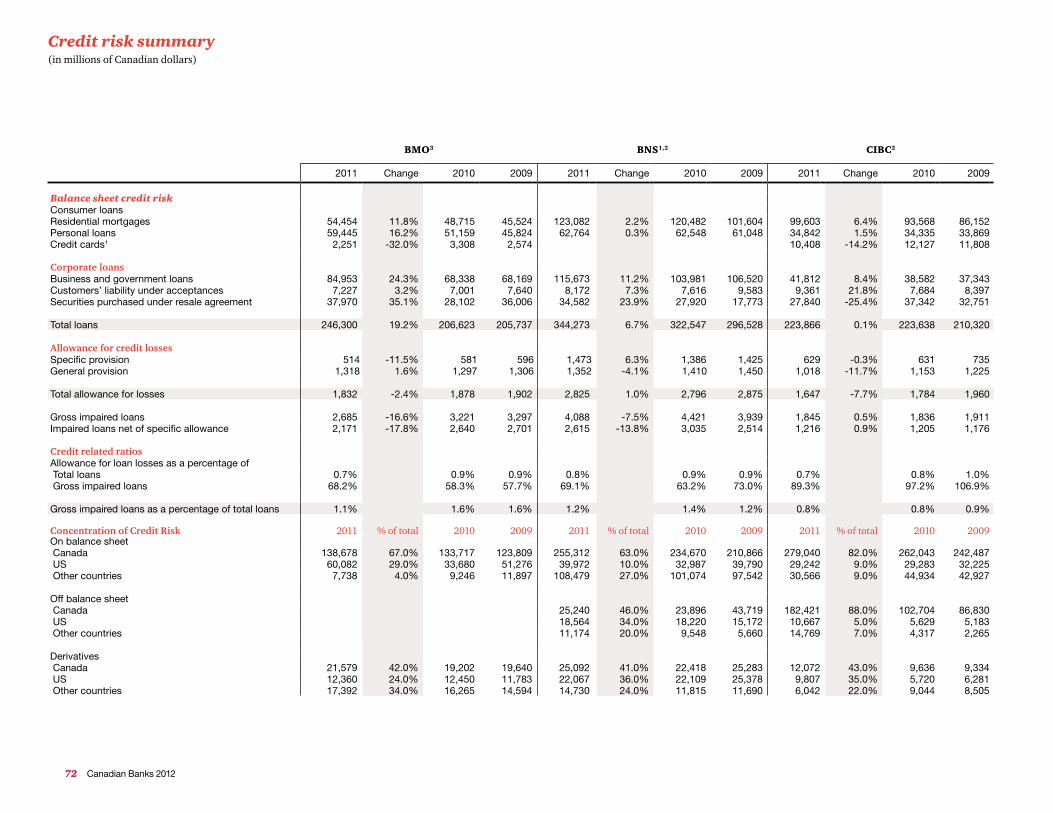

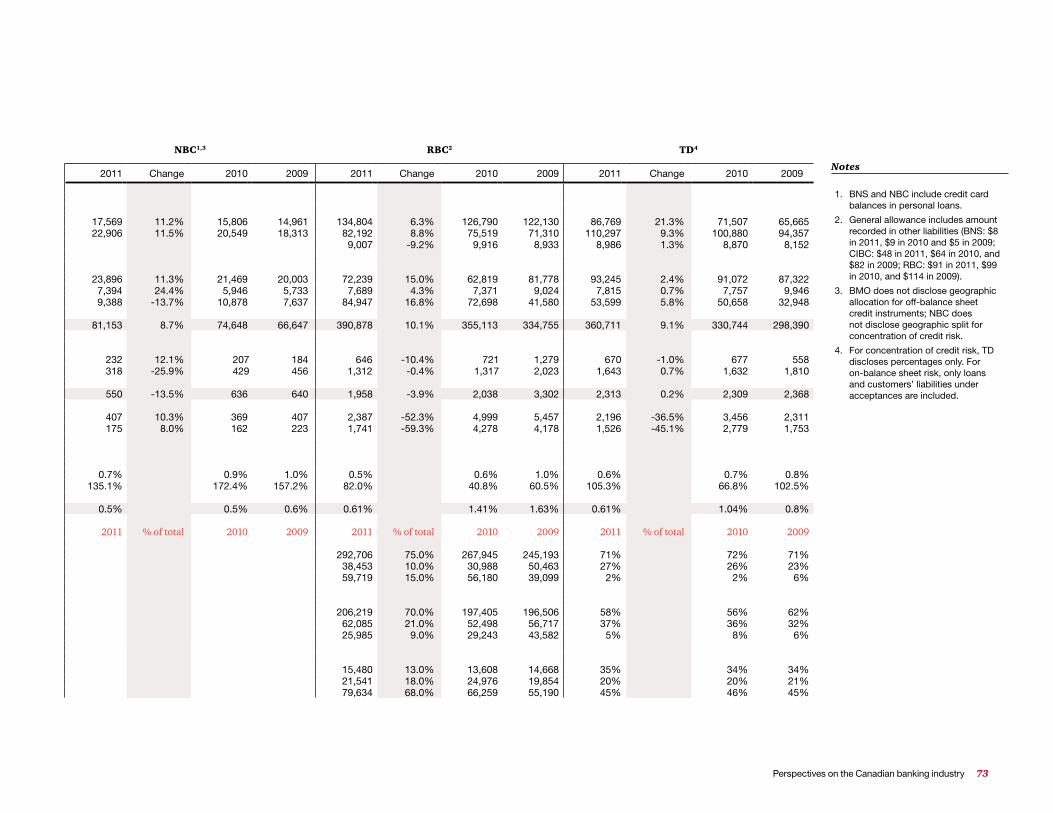

Gross impaired assets also decreased, dropping 25.6% to $13.6 billion as of October 31, 2011 from $18.3 billion as of October 31, 2010. Some banks did see an increase in gross impaired assets and impaired loan formation from Q3 to Q4, although this did not consistently occur in the same portfolios when comparing different banks. Across the banks, total provisions for credit losses decreased 2.2% year over year to $11.1 billion from $11.4 billion, although the trend wasn’t consistent between all banks, with Scotiabank and TD bucking the trend with 1.1% and 0.2% increases in their respective provisions. NBC recorded the largest proportional decline at 13.5%.

This was the second year banks’ profits have benefited from decreases in their PCLs after peaking during the financial crisis in 2008. This industry-wide decrease was achieved despite an $88 billion (or 7%) increase in gross loan balances and was driven by continuing year-over-year improvements in the credit quality of the banks’ lending portfolios.

As expected, despite being the largest single lending portfolio for each of the Canadian banks, credit losses and associated provisions for Canadian residential mortgages remain immaterial to the results of the banks, generally being below 5% of total PCLs. This historically low level of losses reflects the more conservative underwriting standards of Canadian

banks compared to their US peers, the fact that many are insured through programs such as CMHC, and the full recourse nature of Canadian mortgages, which impacts customer behaviour.

US lending portfolios continue to experience a higher rate of credit losses than Canadian portfolios. This affects TD’s and BMO’s results compared to their peers given their proportionally larger US portfolios, with disclosed US credit risk concentrations of 27% and 29% for TD and BMO, respectively. Other major banks are all at 10% or less. As a consequence, US credit losses are generally also relatively immaterial in the context of each bank’s results, with the

0.00.10.20.30.40.50.60.70.8

0.52%

PCLs / Loans LLPs / Loans

0.40%

0.76%

0.68%

20102011

Credit losses

Credit lossesThe major banks again benefited from a year-over-year improvement in provisions for credit losses (PCLs) hitting their P&L, with total PCLs down $1.0 billion or 16.4% year over year ($5.3 billion in 2011 down from $6.3 billion in 2010). PCLs decreased year over year by 12 bps to 0.40% from 0.52%, and loan loss provisions (LLPs) on the balance sheet dropped to 0.68% from 0.76% as a percentage of loans with each bank seeing year-over- year improvements in these metrics.

Perspectives on the Canadian banking industry 33

exception of TD and BMO. TD reported continuing improvement in the performance of its US portfolio, offset by portfolio growth with the net effect being that its provision related to its US book remained flat. BMO reported an $86 million increase in its PCLs, with this largely driven by its acquisition of Marshall & Ilsley and the resultant increase in its portfolio size.

The bulk of retail banking credit losses relate to the unsecured credit card and personal lending portfolios. In general, the banks saw year-over-year improvements in the credit quality of these portfolios. However, there is some indication that this trend stopped in Q4, with arrears rates either stabilizing or deteriorating slightly compared to Q3.

The other large driver of credit losses is commercial lending. Most banks reported a year-over-year improvement in commercial lending credit losses. Having said that, as with unsecured personal lending, there was some divergence in trends between banks from Q3 to Q4. Some banks continued to see improvements in certain portfolios while others saw slight declines in credit quality.

The divergence in trends from Q3 to Q4 in PCL ratios at a consolidated level are detailed below:

The majority of the banks don’t publish credit-related information segmented by province and territory, but mortgage arrears information collated by the Canadian Bankers Association shows that the year-over-year improvement in mortgage arrears has been consistent in all provinces and territories. Having said that, it is interesting to note that as of September 2011, the percentage of mortgages over 30 days in arrears in Alberta remains substantially higher at 0.75%, compared to British Columbia at 0.47%, Quebec at 0.34%, and Ontario at 0.29%. Other provinces and territories account for a relatively small proportion of lending balances, but their mortgage arrears rates are similarly also lower than those seen in Alberta.

In relation to Europe, the Canadian banks have generally made an effort to reduce their exposure to peripheral Europe (Portugal, Italy, Ireland, Greece and Spain). They have also made voluntary disclosures to the market in relation to their European holdings, generally segmented by region and nature of exposure. In short, direct credit losses have been very limited to date and it appears that the banks are closely managing the exposures that they do have.

The impact the European debt crisis is having on credit losses is less direct. The prolonged period of uncertainty has had a negative impact on business and consumer confidence globally, impacting levels of business and consumer spending. The Canadian and US economies are still forecast to grow in 2012, but not as quickly as may have been the case in the absence of this uncertainty.

BMO BNS CIBC NBC RBC TD

Canada Stable Improved Improved Deteriorated Improved Deteriorated

International* Improved Deteriorated Deteriorated n/a Improved Improved

* In the case of TD and BMO, this primarily represents their US businesses.

34 Canadian Banks 2012

The indirect impact on credit quality is that we’re seeing indications that arrears rates are bottoming out at a level higher than may otherwise have been the case. The credit card delinquency rate (90 days and over) stood at 1.05% in July 2011, slightly above the average from 2004 to 2007 of 0.82%. A similar trend holds for the percentage of mortgages in arrears by more than 30 days (0.39% as at September 2011 vs. a 0.26% average for 2004-2007). Still, it is interesting to note that the rate is already below the average since 1990 of 0.42%.

There is some divergence in views about what will happen to credit losses in 2012, although this divergence is likely just a matter of timing. Canada’s economic fundamentals remain sound and there has been some positive data coming out of the US. Unfortunately, the uncertainty surrounding Europe continues to dampen business and consumer confidence, which is having a real impact on spending and investment decisions.

This year also marked the banks’ final year of reporting under pre-IFRS Canadian GAAP. As noted in our previous publication, both IFRS and GAAP require the use of an incurred loss provisioning model. The banks have largely refined their provisioning models to comply with IFRS and none have indicated that they expect any significant adjustments. Credit loss metrics will be impacted where securitized loans are brought back onto the balance sheet under IFRS. But given that the level of insurance on mortgages securitized under the CMHC’s securitization programs typically results in very low losses being suffered by lenders in the event of default, there will, however, be a change in presentation and classification with IFRS requiring provisions for credit losses to be presented based on whether they have been assessed collectively or individually.

Perspectives on the Canadian banking industry 35

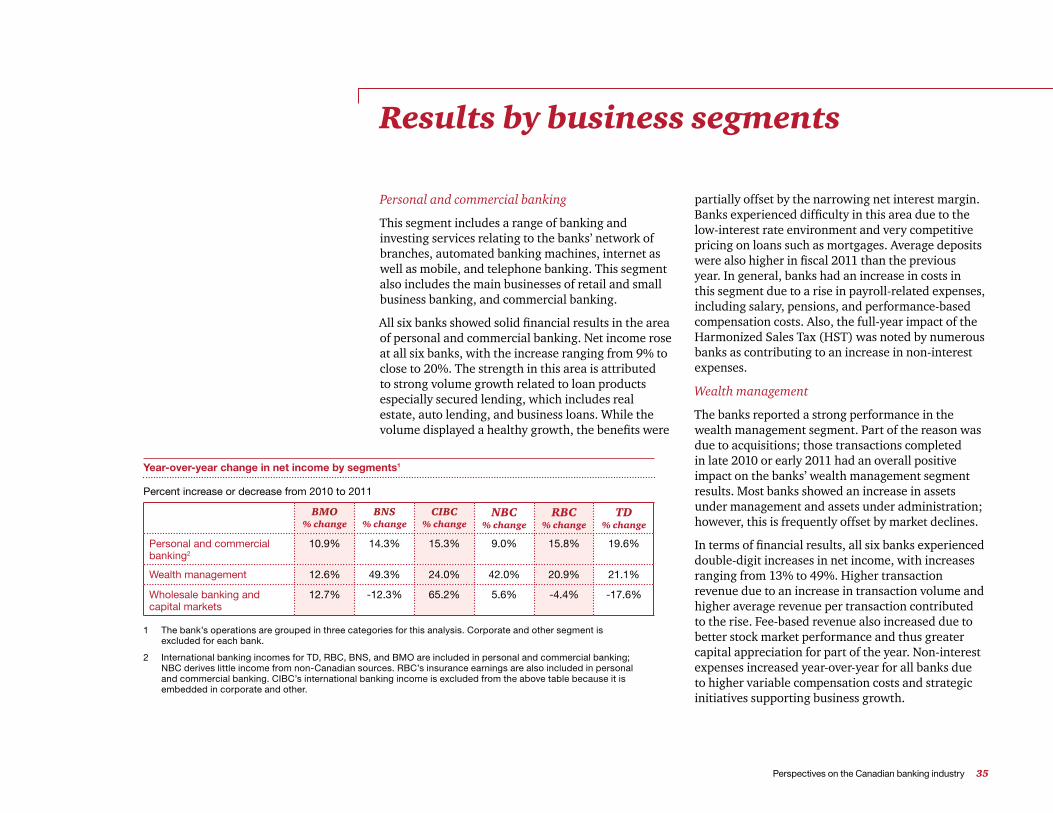

Personal and commercial banking

This segment includes a range of banking and investing services relating to the banks’ network of branches, automated banking machines, internet as well as mobile, and telephone banking. This segment also includes the main businesses of retail and small business banking, and commercial banking.

All six banks showed solid financial results in the area of personal and commercial banking. Net income rose at all six banks, with the increase ranging from 9% to close to 20%. The strength in this area is attributed to strong volume growth related to loan products especially secured lending, which includes real estate, auto lending, and business loans. While the volume displayed a healthy growth, the benefits were

partially offset by the narrowing net interest margin. Banks experienced difficulty in this area due to the low-interest rate environment and very competitive pricing on loans such as mortgages. Average deposits were also higher in fiscal 2011 than the previous year. In general, banks had an increase in costs in this segment due to a rise in payroll-related expenses, including salary, pensions, and performance-based compensation costs. Also, the full-year impact of the Harmonized Sales Tax (HST) was noted by numerous banks as contributing to an increase in non-interest expenses.

Wealth management

The banks reported a strong performance in the wealth management segment. Part of the reason was due to acquisitions; those transactions completed in late 2010 or early 2011 had an overall positive impact on the banks’ wealth management segment results. Most banks showed an increase in assets under management and assets under administration; however, this is frequently offset by market declines.

In terms of financial results, all six banks experienced double-digit increases in net income, with increases ranging from 13% to 49%. Higher transaction revenue due to an increase in transaction volume and higher average revenue per transaction contributed to the rise. Fee-based revenue also increased due to better stock market performance and thus greater capital appreciation for part of the year. Non-interest expenses increased year-over-year for all banks due to higher variable compensation costs and strategic initiatives supporting business growth.

Results by business segments

BMO % change

BNS % change

CIBC % change

NBC % change

RBC % change

TD % change

Personal and commercial banking2

10.9% 14.3% 15.3% 9.0% 15.8% 19.6%

Wealth management 12.6% 49.3% 24.0% 42.0% 20.9% 21.1%

Wholesale banking and capital markets

12.7% -12.3% 65.2% 5.6% -4.4% -17.6%

1 The bank’s operations are grouped in three categories for this analysis. Corporate and other segment is excluded for each bank.

2 International banking incomes for TD, RBC, BNS, and BMO are included in personal and commercial banking; NBC derives little income from non-Canadian sources. RBC’s insurance earnings are also included in personal and commercial banking. CIBC’s international banking income is excluded from the above table because it is embedded in corporate and other.

Year-over-year change in net income by segments1

Percent increase or decrease from 2010 to 2011

36 Canadian Banks 2012

Wholesale banking and capital markets

This segment – which includes investment banking, corporate banking, capital markets, and other services – slowed down from the 2010 highs. The first six months of the year displayed stronger results and higher investor confidence. However, in the last six months of the year, market uncertainty contributed to a low-confidence environment that is expected to continue due to unresolved complications relating to Europe’s debt crisis. While analysts’ expectations were low for this segment’s results, the banks pleasantly surprised the market with better-than-expected results.

NBC and BMO came out ahead with 6% and 13% year-over-year increases, respectively. CIBC displayed a significant 65% increase from 2010 due to higher equity sales and new issuances. The banks with positive growth in net income benefited from an increase in corporate and investment banking and lower provisions for credit losses. However, the below-trend performance of the market is still evident in some banks’ financial results. Three of the six

banks (RBC, TD, and Scotiabank) saw a moderate decrease to net income ranging from 4% to 18% in the wholesale banking and capital markets segment. Banks felt the pressure of the global economic situation. All six banks experienced declines in the global fixed-income business, especially related to the US and Europe.

Results by geographic segments

The large Canadian banks ended the 2011 fiscal year on a very positive note. All banks presented solid results with the majority of them performing above analysts’ expectations; some banks experienced record or close to record income for the year. The benefit is mainly due to an increase in Canadian retail banking and growth in loan portfolios. However, 2012 began with a tone of great domestic competition; the first spark starting with BMO offering a record low rate on mortgages, which caused quick responses from the other banks. This is a sign of intense competition for new customers and to compensate for tight margins by expanding loan volumes.

Perspectives on the Canadian banking industry 37

While all the Canadian banks have a significant focus in Canada, for some, their foreign operations also form an integral part of their business model, some more significantly than others. The banks have varying degrees of foreign involvement and differ markedly in their approach to international operations. Certain banks actively focus on enhancing their international presence by way of acquisition, expanding their existing foreign operations, and entering emerging markets. Some banks decided to pull out of certain markets and focus their efforts in another area. Other banks focused on the domestic market with limited foreign operations.

However, the recent global economic situation has many of the banks skeptical about the future. The banks acknowledge that growth will be challenging given uncertainty over the resolution of Europe’s debt issues. However, some have said that the turmoil may

produce new business opportunities as their foreign competitors are forced to give up market share to the more financially sound Canadian banks. Nevertheless, international developments will cause difficulties for Canadian banks on the international front. Recent US legislative changes, such as Dodd-Frank, will ultimately affect all financial institutions operating in the US; many Canadian banks have subsidiaries and other significant operations there. The US is not alone in making changes. The European Commission is reviewing the Markets in Financial Instruments Directive (MiFID). Also, Basel III is expected to be enacted in the near future. The laws are expected to increase compliance costs, add to legal risks, and restrict the banks’ ability to earn income the way they previously had. While the banks had a strong performance in 2011 and seem relatively shielded from the circumstances around them, Canadian banks are not unaffected by the recent reforms.

The large Canadian banks ended the 2011 fiscal year on a very positive note.

38 Canadian Banks 2012

Scotiabank is Canada’s most international bank, operating in more than 55 countries worldwide and currently generates the largest share of net income outside of Canada, deriving more than 35% of its net income from foreign sources for 2011. It concentrates in high-growth emerging markets, positioning itself in Mexico, the Caribbean, Asia, and Central, Latin and South America. A number of significant transactions occurred in 2011 in Asian and South American markets: announcing the purchases of a 19.99% interest in China’s Bank of Guangzhou and a 51% stake in Colombia’s Banco Colpatria as well as the completion of the acquisition of Dresdner Bank in Brazil and Nuevo Banco Comercial S.A. in Uruguay. Due to the recent reforms in Cuba, Canadian banks are considering what opportunities are available. Among the first to act is Scotiabank, applying to the Central Bank of Cuba for a representative office licence in December 2011. Its medium-term goal is to generate an equal amount of net income from its Canadian and foreign operations.

In 2011, RBC pulled back on its US operations and is currently working to sell its US regional retail banking arm to PNC Financial Services Group. However, RBC’s global presence remained strong, focusing on corporate, institutional and high net worth clients in its capital markets and wealth management segments.

RBC strengthened its ties with Asia, launching a new trading floor in Hong Kong in late 2010 and appointed a new head of Asia capital markets in mid-2011. The European and Caribbean arms of RBC, however, faced challenges. The European fixed-income trading business is experiencing difficulties due to the European debt crisis. Its Caribbean banking business faces pressure due to a slowdown in the tourism industry and the local economy. Its joint venture with Dexia, RBC Dexia Investor Services with clients in 15 countries, faces stress due to the stability of its joint venture partner. Despite all this, RBC’s international banking arm still managed a CAD$81 million increase in net income after discontinued operations due to higher earnings at RBC Dexia. Future developments for RBC may include Cuba, where RBC is in the early stages of considering this market.

TD operates a large network of branches in the US with more than 1,200 “stores”. It has the largest US retail arm of all the Canadian banks. TD also owns about 45% of online brokerage TD Ameritrade. Its recent acquisition of 100% of Chrysler Financial, renamed TD Auto Finance US, further increased TD’s operations in the US. The integration of the recently acquired South Financial Group also occurred in 2011. The US retail banking sector is a highly competitive environment. Combined with the changes in regulations, TD will have to focus on product evolution where products are in compliance with new regulations while delivering value to customers. On the international front, TD Waterhouse International operates in the UK and Europe.

Perspectives on the Canadian banking industry 39

In 2011, BMO completed the acquisition of Marshall & Ilsley (M&I) in July. This new acquisition will contribute mainly to BMO’s US personal and commercial banking, private client and corporate service segments. M&I was combined with BMO’s existing US-based Harris Bank to form BMO Harris Bank, which more than doubles the US branch network to 679 branches in 2011 from 312 in 2010. This acquisition gives BMO a significant market presence in eight US states, mostly in the Midwest.

CIBC is more focused on domestic operations. However, in 2011, it completed another transaction in a series of strategic investment over the last two years, purchasing a 41% equity interest in American Century Investments, a US asset management company. CIBC also opened a new wholesale banking office in London, England and a new corporate credit products office in Houston, Texas. CIBC’s international banking operations are comprised of CIBC FirstCaribbean,

joint venture CIBC Mellon and the Bank of N.T. Butterfield & Son Ltd. In 2011, CIBC’s international banking operations performed relatively worse than the prior year due to low gains on the sale of securities and a strong Canadian dollar.

NBC’s operations are primarily focused in the province of Quebec where it earns 70% of its revenue. NBC is leveraging its distribution network to grow its presence outside of Quebec into the rest of Canada, which currently represents 27% of revenue earned. Internationally, NBC’s activities are limited in comparison to its other large Canadian bank peers at only 3%. NBC operates under Natbank in Florida and owns Putnam Lovell NBF, a US-based investment bank acquired in 2002. While Scotiabank and RBC are considering or acting on opportunities in Cuba, NBC has already been operating in the country for more than 15 years.

Some have said that the turmoil may produce new business opportunities as their foreign competitors are forced to give up market share to the more financially sound Canadian banks.

40 Canadian Banks 2012

Four of the Big Six banks realized a drop in the value of their common share price compared to the year-ago period. The most significant decline of 16.6% was recognized by RBC to $48.62 from $54.39, followed by CIBC with a 4% drop to $75.10, Scotiabank with a 3.9% decrease to $52.53, and BMO with a drop of 2.2% and ending value of $58.89. Increases were posted by NBC of 6% to $71.14 and TD of 2.3% to $75.23. While the price of Scotiabank and BMO shares fell, the market cap of both banks rose because both issued stock, offsetting the decline.

TCE ratios ranged from 19.6% for TD at the high end to 11.7% for BMO at the low end as of October 31, 2011. Overall, ratios stayed relatively consistent with the prior year, which had a TCE ratio range of 19.0% for TD to 10.8% for Scotiabank. It’s important to note that this ratio compares tangible common equity to risk-weighted assets as opposed to total assets, which some analysts point out would remove the judgment required in determining the likelihood of the assets going bad and result in significantly lower ratios.

Potential earnings are inhibited by the fact that the industry is currently seeing smaller margins on loans and with a ceiling on consumer lending in Canada, the banks are not able to simply increase portfolios to maintain profits. Furthermore, the continual global economic uncertainty is projected by some analysts to have an impact on growth in Canada, which is likely one of the factors that led two of the banks to lay off a significant amount of employees during the quarter

As of October 31, 2011, RBC continued to register as Canada’s largest bank with a market capitalization of $69.9 billion. However, this is a decline of 9.8% from October 31, 2011 and a 9.7% decline from October 31, 2009, making RBC the only one of the Big Six that has seen a decrease compared to both the 2010 and 2009 comparatives. TD stood a close second, registering a market capitalization of $67.9 billion, an increase of 5.1% over the prior year. Scotiabank followed with a modest 0.4% rise and a market value of $57.2 billion and BMO with an increase of 10.4% and a market capitalization of $37.6 billion. CIBC ranked fifth at $30.1 billion, and although this was a decrease of 2.1% from the prior year, it was a 26.3% rise over the two-year period. NBC, the smallest of the Big Six, was valued at $11.4 billion, an increase of 4.1% from the prior year. The total market capitalization as of October 31, 2011 for the six banks in Canada was $274.1 billion, overall holding very steady from $274.8 billion in the prior year. Subsequent activity in market capitalization saw TD edge ahead of RBC on November 9, 2011, showing how close the race is for the top spot. This was a short lived move; RBC has since regained and maintained top spot.

Market capitalization

The last two years have seen some variability in the market capitalization, tangible common equity (TCE) ratios, and stock prices of Canada’s Big Six.

Perspectives on the Canadian banking industry 41

ending October 31, 2011. RBC had 585 fewer full-time positions and BMO had 435 fewer full-time positions as compared to the end of fiscal Q3.

Despite challenges faced by the Canadian banks, there are reasons to be optimistic. The quarter ending October 31, 2011 saw record earnings of $6.5 billion for the big six banks.