capital budgeting last update 2015.02.11 1.1.0 copyright kenneth m. chipps ph.d. 2013 - 2015 1

TRANSCRIPT

Capital Budgeting

Last Update 2015.02.11

1.1.0

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

1

What is Capital Budgeting

• Capital budgeting is the process of deciding the amounts of available funding to set aside for the purchase of fixed assets

• It is also the process the requester goes through in order to receive approval for a capital expenditure

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

2

What is Capital Budgeting

• Capital budgeting is a cost-benefit analysis• It asks a single question

– If we purchase this fixed asset, will the benefits to the company be greater than the cost of the asset

• As this asset will function over a period of time a complicating factor is that the inflows and outflows may not be comparable

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

3

What is Capital Budgeting

• The cash outflows – the costs - are typically concentrated at the time of the purchase, while cash inflows – the benefits – arrive irregularly over time

• The time value of money principle states that dollars today are worth more than dollars in the future

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

4

What is Capital Budgeting

• The solution is to place all of the funds on both sides on a present value basis which puts them all in today’s dollar value

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

5

Capital Budgeting Analysis

• A capital budgeting analysis conducts a test to see if the benefits – the cash inflows - are large enough to repay the company for three things– The cost of the asset– The cost of financing the asset– The required rate of return

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

6

Cost of the Asset

• The cost of the asset is just that, how much must we pay for it

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

7

Cost of Financing

• The financing cost is the interest cost charged for borrowing the money to pay for the asset or the interest foregone by taking the money out of the bank

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

8

Required Rate of Return

• The rate of return is the risk premium that accounts for any errors made when estimating cash flows that will occur in the distant future

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

9

Capital Budgeting Methods

• Let's take a look at the basic methods used for this type of analysis– Hurdle Rate– Payback Period– Net Present Value– Internal Rate of Return– Profitability Index

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

10

Hurdle Rate

• The hurdle rate is the return we could earn by doing nothing with the funds, just leave them sitting in a safe location such as an insured bank account or government securities

• It consists of two numbers– The cost of capital– Risk of the investment

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

11

Hurdle Rate

• The cost of capital is– If withdrawn, the interest given up– If borrowed, the interest rate

• The risk factor is– The assumption that the funds are safe

• This number is based on experience• It is usually from 1 to a few points• It is a guess• It is often called a discount rate

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

12

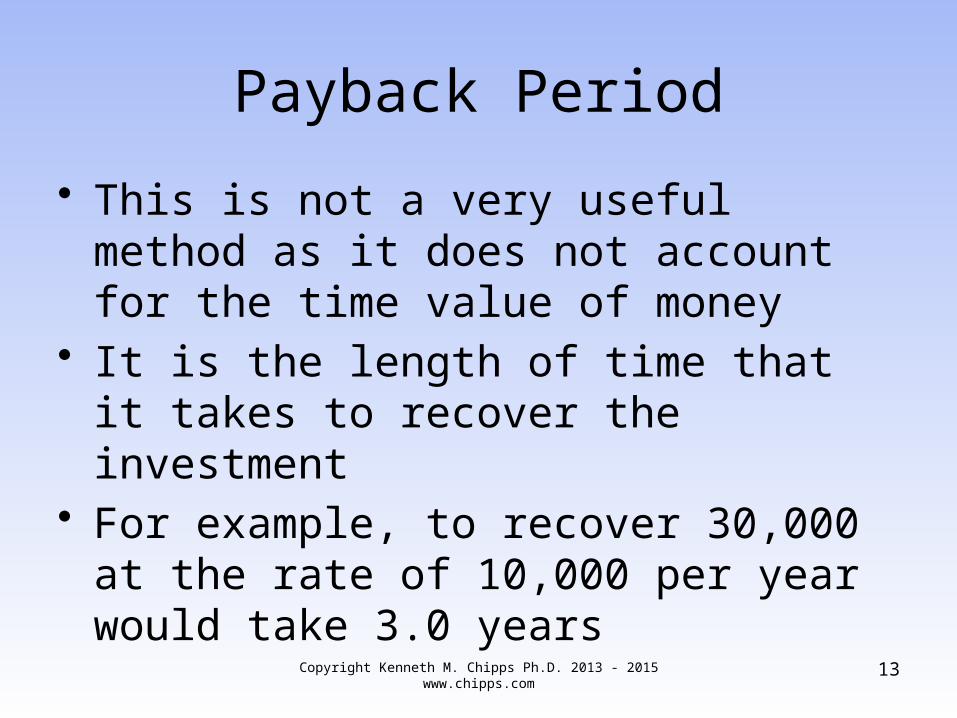

Payback Period

• This is not a very useful method as it does not account for the time value of money

• It is the length of time that it takes to recover the investment

• For example, to recover 30,000 at the rate of 10,000 per year would take 3.0 years

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

13

Payback Period

• Companies that use this method will set some arbitrary payback period for all capital budgeting projects, such as a rule that only projects with a payback period of 2.5 years or less will be accepted

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

14

Net Present Value

• Using a minimum rate of return known as the hurdle rate, the net present value of an investment is the present value of the cash inflows minus the present value of the cash outflows

• A more common way of expressing this is to say that the NPV - net present value is the PVB - present value of the benefits minus the PVC - present value of the costs

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

15

Net Present Value

• PVB – PVC = NPV• By using the hurdle rate as the discount

rate, we are conducting a test to see if the project is expected to earn our minimum desired rate of return

• Here are the decision rules

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

16

Net Present Value

NPV Is Benefits v Costs Above Return Rate

Accept or Reject

Positive Benefits > Costs Yes Accept

Zero Benefits = Costs Equal To Indifferent

Negative Benefits < Costs No Reject

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

17

IRR

• The IRR - Internal Rate of Return is the rate of return that an investor can expect to earn on the investment

• Technically, it is the discount rate that causes the present value of the benefits to equal the present value of the costs

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

18

IRR

• According to surveys of businesses, the IRR method is actually the most commonly used method for evaluating capital budgeting proposals

• This is probably because the IRR is a very easy number to understand because it can be compared easily to the expected return on other types of investments

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

19

IRR

• If the internal rate of return is greater than the project's minimum rate of return, we would tend to accept the project

• The calculation of the IRR, however, cannot be determined using a formula; it must be determined using a trial-and-error technique

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

20

Which Basic Method to Use

• As the payback period is not a useful technique the question is which of the basic methods is better - NPV or IRR

• NPV is better than the IRR• It is superior to the IRR method for at least

two reasons

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

21

Which Basic Method to Use

– Reinvestment of Cash Flows• The NPV method assumes that the project's cash

inflows are reinvested to earn the hurdle rate; the IRR assumes that the cash inflows are reinvested to earn the IRR

• Of the two, the NPV's assumption is more realistic in most situations since the IRR can be very high on some projects

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

22

Which Basic Method to Use

– Multiple Solutions for the IRR• It is possible for the IRR to have more than one

solution• If the cash flows experience a sign change, such

as a positive cash flow in one year and a negative in the next, the IRR method will have more than one solution

• In other words, there will be more than one percentage number that will cause the PVB to equal the PVC

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

23

Profitability Index

• The profitability index is a ratio of the present value of the benefits to the present value of the costs

• The index is used instead of Net Present Value when evaluating mutually exclusive proposals that have different costs

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

24

Source

• The material just above is for the most part from online lecture notes by Dr. Larry Guin Professor of Finance (Retired)

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

25

Q Sort

• Q-Sort is a simple method for ranking ideas on different dimensions

• Ideas are put on cards• For each dimension being considered, the

cards are stacked in order of their performance on that dimension

• Several rounds of sorting and debate are used to achieve consensus about the projects

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

26

Conjoint Analysis

• Conjoint Analysis estimates the relative value individuals place on attributes of a choice

• Individuals given a card with products or projects with different features and prices

• Individuals rate each in terms of desirability or rank them

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

27

Conjoint Analysis

• Multiple regression is then used to assess the degree to which an attribute influences rating

• These weights quantify the trade-offs involved in providing different features

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

28

DEA

• Data Envelopment Analysis uses linear programming to combine measures of projects based on different units, such as rank vs. dollars, into an efficiency frontier

• Projects can be ranked by assessing their distance from efficiency frontier

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

29

DEA

• As with other quantitative methods, DEA results only as good as the data utilized; managers must be careful in their choice of measures and their accuracy

Copyright Kenneth M. Chipps Ph.D. 2013 - 2015 www.chipps.com

30