capital improvement board of managers - gfoa.netgfoa.net/cafr/coa2012/marioncountycapitol... ·...

TRANSCRIPT

Capital Improvement Board of Managers (of Marion County, Indiana)

(A Component Unit of the Consolidated City of Indianapolis - Marion County)

Comprehensive Annual Financial Report For the Fiscal Year Ended December 31, 2012

Comprehensive Annual Financial Report

Fiscal Year Ended December 31, 2012 Capital Improvement Board of Managers (of Marion County, Indiana) - a Component Unit of the Consolidated City of Indianapolis- Marion County Indianapolis, Indiana

Prepared by:

Finance Department Ann Lathrop, President

Capital Improvement Board of Managers (of Marion County, Indiana)

(A Component Unit of the Consolidated City of Indianapolis-Marion County)

December 31, 2012

Contents

Introductory Section (Unaudited) Letter of Transmittal .......................................................................................................................................... 2 Certificate of Achievement for Excellence in Financial Reporting .................................................................. 11 Organization Table ........................................................................................................................................... 12 Principal Officers and Management ................................................................................................................. 13

Financial Section Independent Auditor’s Report on Financial Statements ................................................................................... 15 Management’s Discussion and Analysis .......................................................................................................... 17 Financial Statements

Balance Sheets ............................................................................................................................................ 30 Statements of Revenues, Expenses and Changes in Net Position ............................................................... 32 Statements of Cash Flows .......................................................................................................................... 33 Notes to Financial Statements .................................................................................................................... 35

Other Supplementary Information Balance Sheet Information ......................................................................................................................... 65 Analysis of Revenues, Expenses and Changes in Net Position ................................................................. 66 Analysis of Certain Operating Expenses ................................................................................................... 67

Statistical Section (Unaudited)

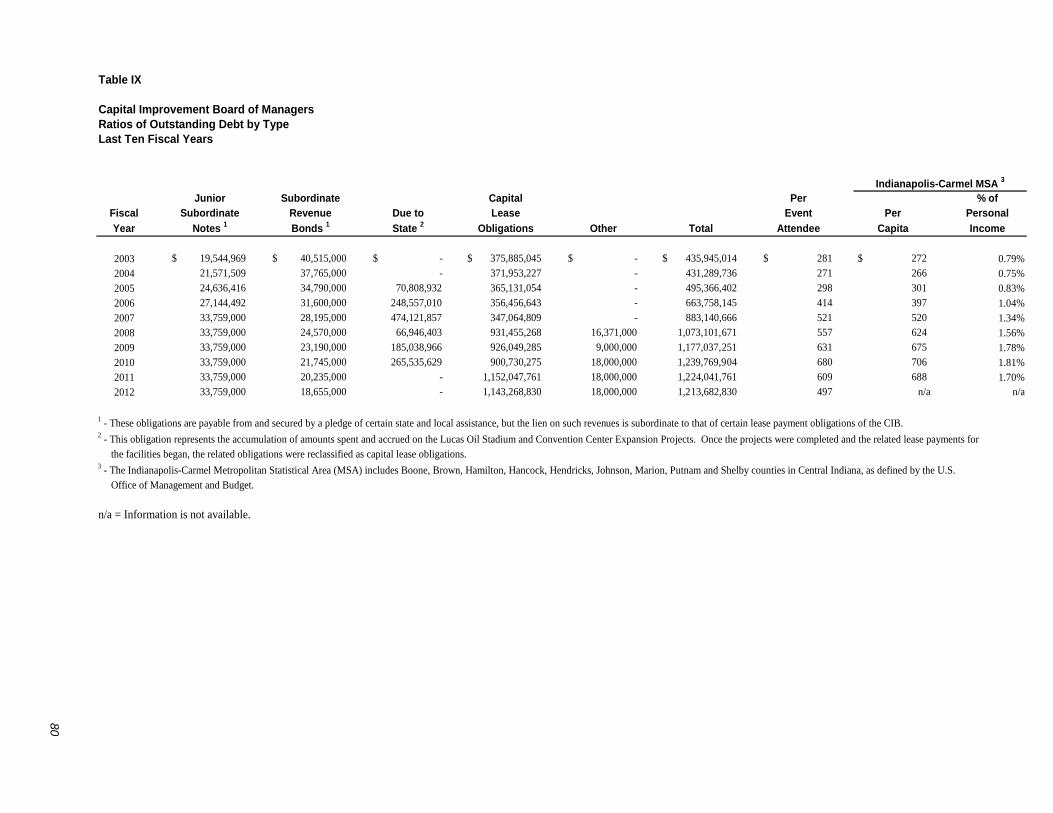

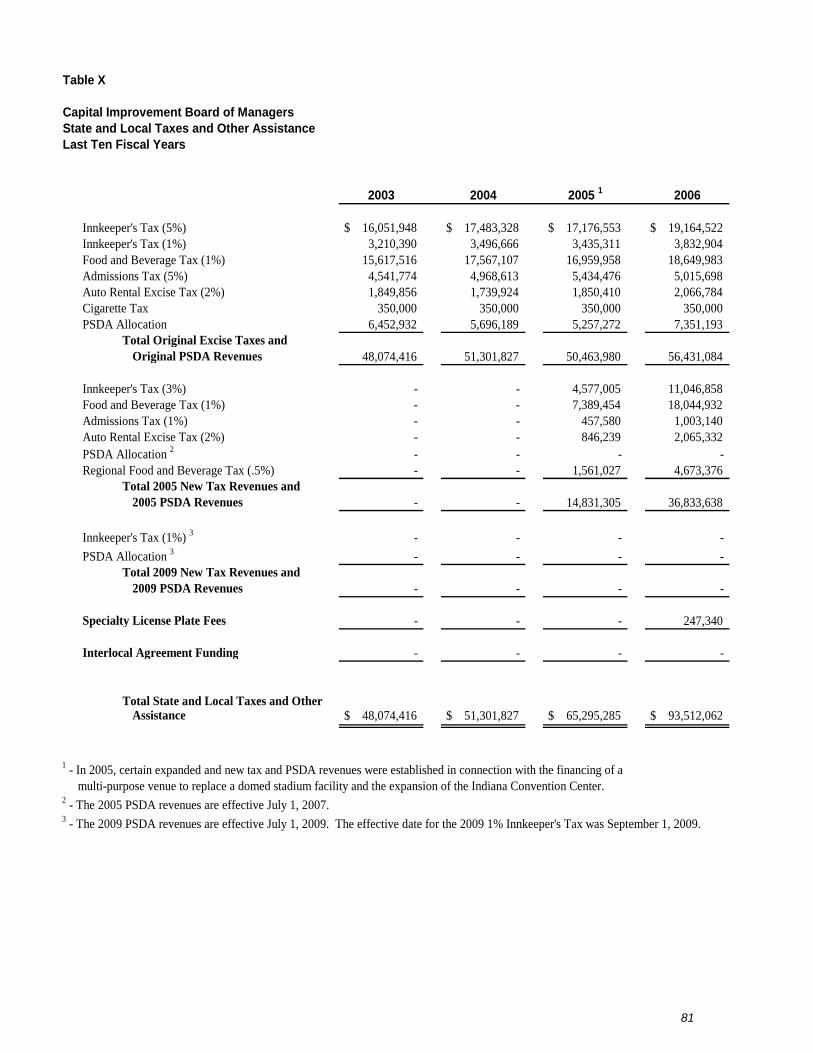

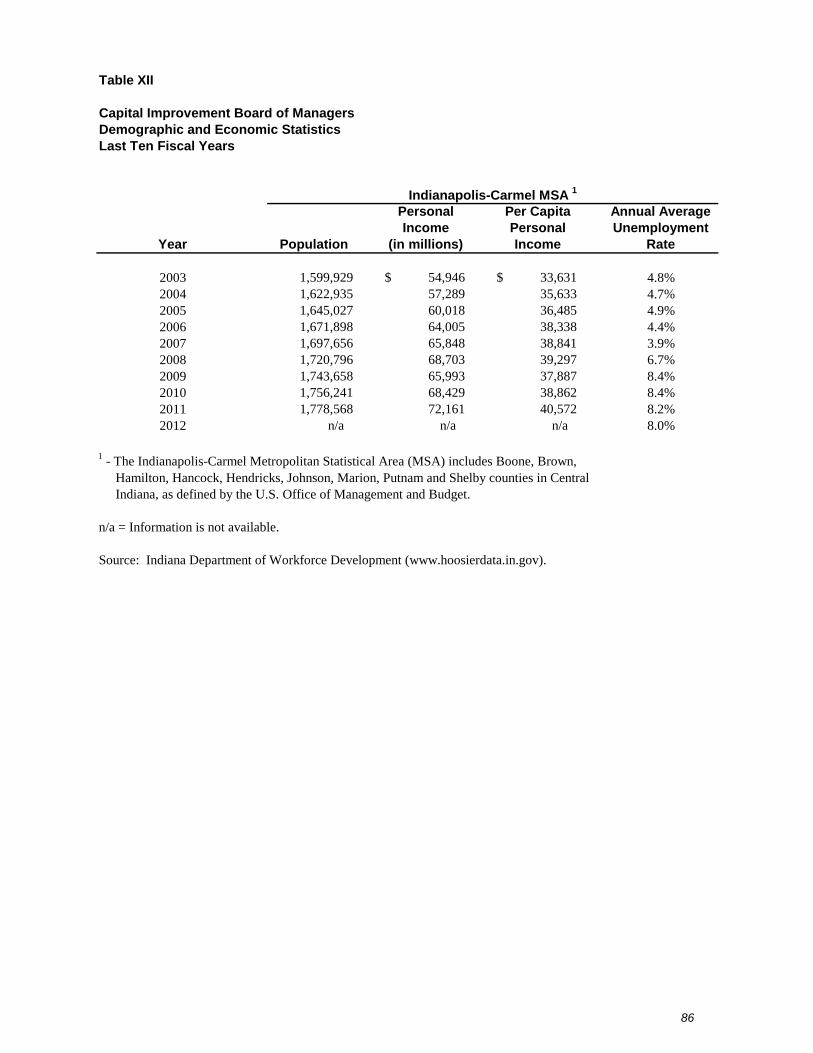

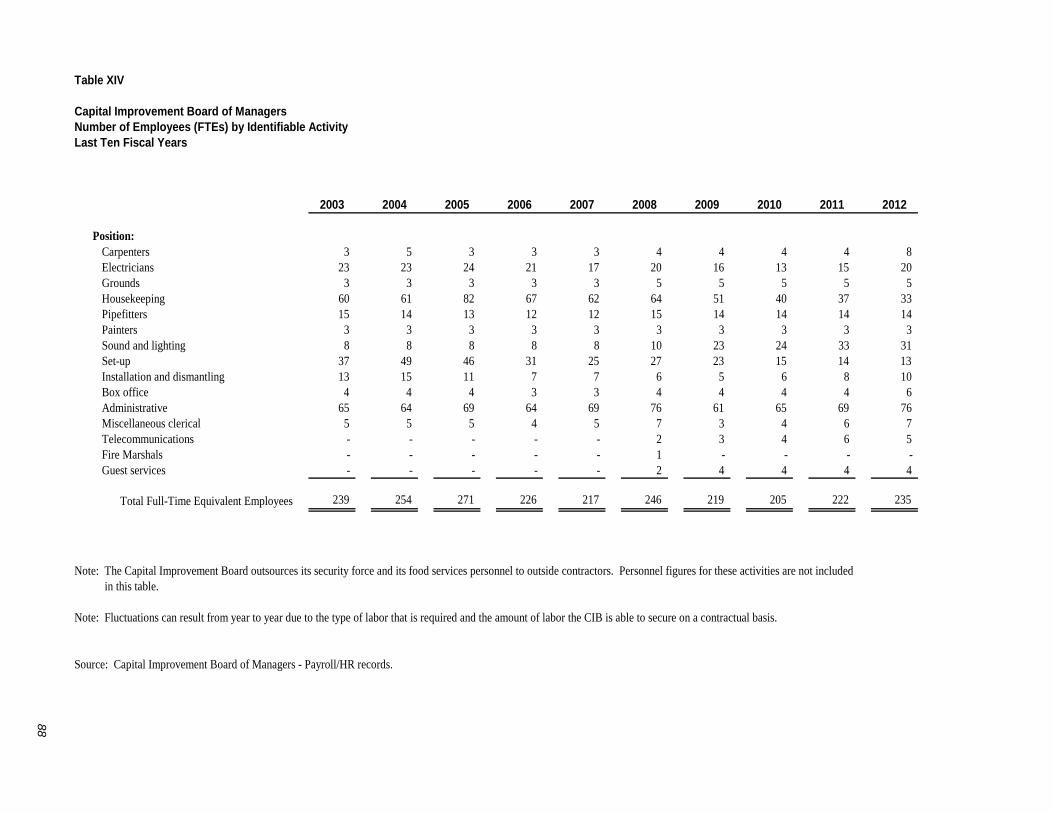

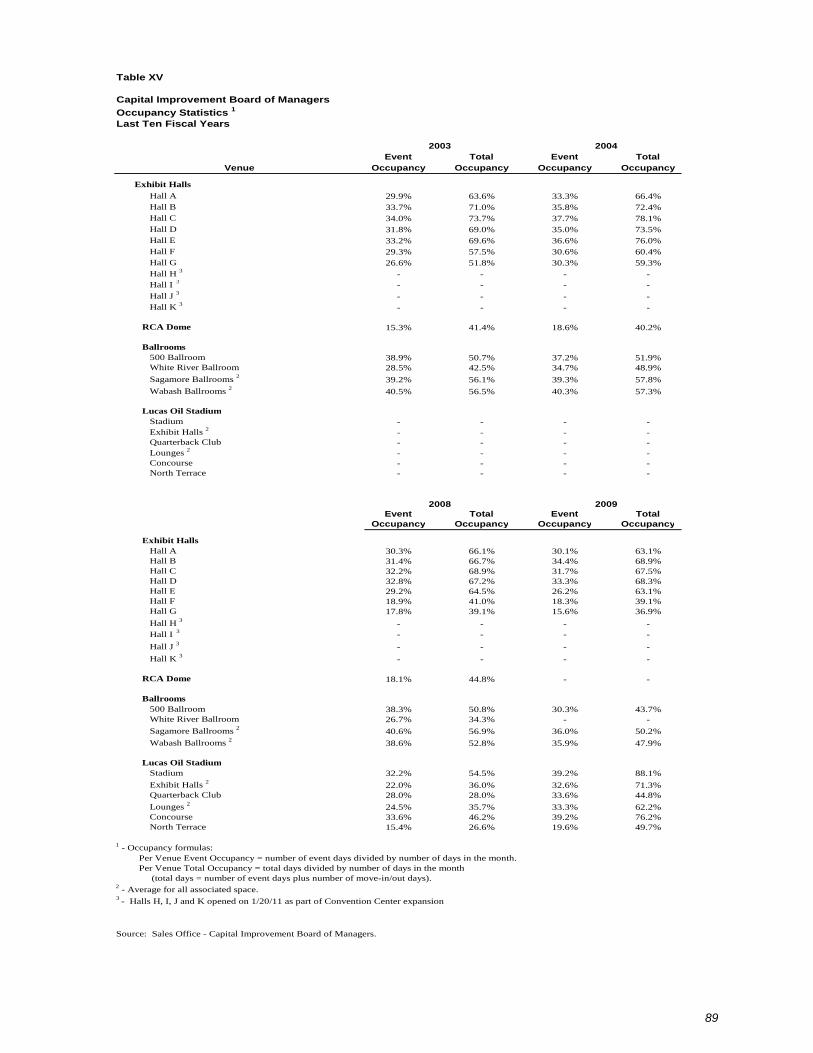

Table I - Net Position by Component ............................................................................................................... 69 Table II - Changes in Net Position ................................................................................................................... 71 Table III - Event Statistics ................................................................................................................................ 73 Table IV - Largest Customers .......................................................................................................................... 75 Table V - Rate Schedule - Exhibits .................................................................................................................. 76 Table VI - Rate Schedule - Meetings ............................................................................................................... 77 Table VII - Rate Schedule - Hourly Labor Reimbursement Rates ................................................................... 78 Table VIII - Food Service and Concession Revenues ...................................................................................... 79 Table IX - Ratios of Outstanding Debt by Type .............................................................................................. 80 Table X - State and Local Taxes and Other Assistance ................................................................................... 81 Table XI - Pledged Revenue Coverage ............................................................................................................ 83 Table XII - Demographic and Economic Statistics .......................................................................................... 86 Table XIII - Principal Employers ..................................................................................................................... 87 Table XIV - Number of Employees (FTEs) by Identifiable Activity ............................................................... 88 Table XV - Occupancy Statistics ..................................................................................................................... 89

(THIS PAGE INTENTIONALLY LEFT BLANK)

Introductory

Section

2

May 31, 2013 Capital Improvement Board of Managers (of Marion County, Indiana) Indianapolis, Indiana We are pleased to present the Comprehensive Annual Financial Report of the Capital Improvement Board of Managers (of Marion County, Indiana) (“CIB”), for the fiscal year ended December 31, 2012.

The financial statements of the CIB are prepared in accordance with accounting principles generally accepted in the United States of America, and we believe they present the CIB's financial affairs in a manner designed to fairly set forth the financial position and results of operations of the CIB. We also believe that all disclosures necessary to enable the reader to gain an understanding of the CIB's financial affairs have been included. Responsibility for both the accuracy of the presented data and the completeness and fairness of the presentation, including all disclosures, rests with the CIB. The financial statements have been audited by the Indiana State Board of Accounts and the independent auditor’s report has been included in this report.

Management’s discussion and analysis (MD&A) immediately follows the independent auditor’s report and provides a narrative introduction, overview and analysis of the basic financial statements. The MD&A complements this letter of transmittal and should be read in conjunction with it.

Profile of the CIB

Structure and Reporting Entity: The CIB is a municipal body of Marion County created pursuant to the provisions of Indiana Code (IC) 36-10-9. The CIB has no stockholders or equity holders and all revenues and other receipts must be deposited and disbursed in accordance with provisions of such statute. The board is composed of nine members. Six of the nine board members are appointed by the Mayor of the City of Indianapolis, one is appointed by the Marion County Board of Commissioners, one is appointed by the City-County Council of the Consolidated City of Indianapolis-Marion County, a unified form of government commonly referred to as “Unigov” (“City-County Council”) and one is appointed jointly by majority vote of a body consisting of one member of the board of the county commissioners of each county in which a food and beverage tax is in effect under IC 6-9-35 on January 1 of the appointment. The board of county commissioners that has the greatest population of all counties in which a food and beverage tax is in effect under IC 6-9-35 on January 1 of the year of the appointment shall convene the meeting to make the joint appointment. Each county in which a food and beverage tax is in effect under IC 6-9-35 on January 1 of the year of the appointment is entitled to be represented at the meeting by one member of the county’s board of county commissioner, who shall be selected by that county’s board of county commissioners. One of the members appointed by the Mayor must be engaged in the hotel or motel business in the county. Not more than four of the members appointed by the Mayor may be affiliated with the same political party.

3

The CIB is authorized by the statute to finance, construct, equip, operate and maintain any capital facilities or improvements of general public benefit or welfare which would tend to promote convention, cultural, entertainment and recreational activities and thereby positively impact the wider public and civic well-being of the community. While the CIB receives certain excise tax revenue, the CIB has no taxing power. The exercise of any taxing power requires the action of the Indiana General Assembly and, in certain instances when so authorized by the Indiana General Assembly, the enactment by ordinance of the City-County Council. Additionally, certain of these taxes are statutorily restricted to limited purposes. The CIB operates facilities used in convention, cultural, entertainment and recreational activities in downtown Indianapolis. Such activities are maintained, for accounting and reporting purposes, in a single enterprise fund. Based upon the provisions of Governmental Accounting Standards Board Statement No. 14, The Financial Reporting Entity, the CIB has determined that it is a component unit of the Consolidated City of Indianapolis-Marion County as further explained in the notes to the financial statements.

CIB Operating Model: As an operating model, the CIB’s public purposes are achieved by operating capital facilities, which are an important driver to underlying the economic vitality of historically strong and growing convention, cultural, entertainment and recreational businesses (public and private) serving the public and civic interests and well-being of the State of Indiana and particularly the central Indiana region. The public and civic interests and well-being are directly and indirectly served by the investment and activity of the CIB and its growth fostering effect on the larger economy, including most directly the MSA Indianapolis public and private sector hospitality industry. Additionally, the broader private and public sector is benefited by leisure, amenity and employment opportunities. The hospitality industry is an important element and has played a central role in stabilizing the core of the City of Indianapolis, thereby generally transmitting a rippling benefit throughout the region and the State. This model, ever expanding since its inception in 1965, has become an important element to the success story that is the central Indiana region.

At the core of this operating model is an understanding that the CIB’s activities work in tandem with the private sector to foster diverse economic growth. The CIB’s assets, activities and ancillary amenities allow a larger private hospitality industry to operate. In turn, the hospitality industry mutually develops and services the region’s significant convention, cultural, entertainment and recreational activity and amenities. This understanding of the hospitality industry, as a significant driver allowing the region to enjoy amenities and activities beyond the means of the region to be supported by just its citizens, supports viewing it as an element that fosters non-hospitality economic growth and quality of life in the region. Viewed in this context, an operating model that permits the generation of non-operating revenue (from both the industry’s customers as well as regional users and beneficiaries of these activities and amenities) to support and subsidize the CIB’s capital and operating costs can be seen as thoughtful and balanced taxation policy. Tax policy impacting the CIB is managed by the Indiana General Assembly and the City-County Council. Working in harmony, this operating model has allowed the region to benefit from a thriving downtown Indianapolis and allows the State to enjoy the fruits of a growing tax base which extends past the borders of Indiana. Ultimately, the CIB operations serve to protect and support a region that has thrived and competes well in comparison to other similar cities in the nation.

Internal Control Structure: In developing and evaluating the CIB's accounting system, we have given consideration to the adequacy of the internal control structure, designing it to provide reasonable, but not absolute, assurance regarding: (1) the safeguarding of assets against loss from unauthorized use or disposition; and (2) the reliability of financial records for preparing financial statements and maintaining accountability for assets. The concept of reasonable assurance recognizes that: (1) the cost of a control should not exceed the benefits likely to be derived; and (2) the valuation of costs and benefits requires estimates and judgments by management.

4

All internal control evaluations occur within the above framework. We believe that the CIB's internal accounting controls adequately safeguard assets and provide reasonable assurance of proper recording of financial transactions.

Budget: The CIB maintains budgetary controls. The objective of these budgetary controls is to ensure compliance with legal provisions embodied in the annual approved budget. The Department Directors, in conjunction with the Administrative staff, develop budgets for the individual departments.

(1) Using these departmental budgets, the Chief Financial Officer prepares the budget for review and approval by the members of the governing board of the CIB.

(2) The budget is advertised in two local newspapers.

(3) The CIB’s board approves and submits the budget to the City-County Council for its review.

(4) The Municipal Corporations Committee of the Council holds public hearings on the budget of the CIB and forwards it for approval to the City-County Council.

(5) The budget of the CIB is reviewed and approved by the City-County Council.

(6) The overall adopted budget of the City (of which the CIB’s budget is a part) is reviewed by the County Tax Adjustment Board (“CTAB”) at a public meeting. The CTAB can reduce the City budget but not increase the operating expenses included in it and must complete its review by November 1.

(7) The Indiana Department of Local Government Finance (“DLGF”) makes the final review of the City’s budget. It can revise, reduce or restore, on appeal, funds and tax rates removed by the CTAB. It may not increase a budget above the level originally advertised. The DLGF certifies the City’s budget by February 15. The CIB’s budget is reviewed in the context of the larger City budget and, accordingly, the City’s budget review includes the review by the CTAB and DLGF. The CIB’s Act only requires review and approval by the City-County Council, not the review or approval of the CTAB and DLGF.

CIB Facilities: Among the facilities managed by the CIB are the multi-purpose Indiana Convention Center (“ICC”) and the state-of-the-art Lucas Oil Stadium (“LOS”). With the expansion of the Convention Center completed in January 2011, the expanded structure covers a 6 city block area in downtown Indianapolis. The LOS site covers a 6½ city block area just south of the expanded Convention Center and is connected by internal and covered structures, allowing combined use opportunities.

Since opening in 1972, the Indiana Convention Center has had four major expansions, with the fourth being completed in January 2011. With this latest expansion, the Indiana Convention Center now contains 566,300 square feet of clear span convention and exhibition space, 71 meeting rooms and three ballrooms. The 11 exhibit halls range in size from 36,300 square feet to 88,900 square feet. The Sagamore Ballroom, with 33,335 square feet, can be divided into seven different sections. The 500 Ballroom has 13,536 square feet and an adjoining reception room. The 10,202 square foot Wabash Ballroom features a 24’ ceiling and may be divided into three separate sections.

5

LOS features a retractable roof, offering spectacular views of the Indianapolis skyline. In addition, LOS has an infill playing surface, 7 locker rooms, exhibit space, meeting rooms, operable north window, dual two-level club lounges, 137 suites, retractable sideline seating, house reduction curtains, two large video boards, ribbon boards, spacious concourses, interior and exterior plaza space, 11 indoor docks and 2 vehicle ramps to the event level. In January 2011, LOS was connected to the expanded Convention Center and several hotels and entertainment options by a pedestrian connector. Tradeshows can take advantage of an indoor 30,000 square foot loading dock with 11 bays, retractable seating and operable walls to utilize up to 183,000 contiguous square feet of space. Football games can be played indoors or outdoors using the retractable roof and operable north window. The house reduction curtain system covers the entire Terrace Level seating, reducing capacity from 63,000 to approximately 41,000. Basketball and other mini-stadium events have the option of playing in the round for up to 71,000 fans or in a much smaller configuration with a house reduction curtain system. Concerts may be played indoors or outdoors in full stadium or reduced house configurations. Seating configurations range in size from 15,000 to 71,000.

In addition to managing the Indiana Convention Center & Lucas Oil Stadium, the CIB also maintains Victory Field and Bankers Life Fieldhouse.

Victory Field, home to the Indianapolis Indians AAA baseball team, has often been referred to as, “the most beautiful AAA ball park in the country,” by those who have enjoyed seeing a baseball game from this magnificent spot. It is constructed on a 13-acre site in White River State Park, which is subleased to, and operated by, the Indianapolis Indians franchise. Located on the southwest corner of West and Maryland streets, the ballpark is in close proximity to the Indiana Convention Center & Lucas Oil Stadium. Victory Field seats approximately 14,200 people, which includes an open-air stadium seating area and the very popular grassy berms in the outfield areas, which offer inviting, lawn seating. This grassy area, around the outfield wall, can accommodate up to 2,000 people. The park's main deck of seats wraps from behind home plate to the foul poles in left and right field. When fans enter the ballpark, they can walk down the steps to their seats in a lower seating bowl, or up to their seats in the upper bowl. There are 12,200 seats with back and arm rests. The ballpark also features many modern-day amenities, such as 29 luxury suites and cup holders at most seats.

Bankers Life Fieldhouse (formerly Conseco Fieldhouse), widely acknowledged as one of the finest sports and civic arenas in the country, is home to the National Basketball Association’s Indiana Pacers and the Women’s National Basketball Association’s Indiana Fever (2012 WNBA Champions). With a basketball-seating capacity of 18,165 that includes 71 suites and 2,667 club seats, Bankers Life Fieldhouse occupies approximately 750,000 square feet between Delaware and Pennsylvania Streets at Georgia Street in the warehouse district of downtown Indianapolis. The first retro-styled facility in the NBA, Bankers Life Fieldhouse has three seating levels: Lower Level, Krieg DeVault Club Level and Balcony Level; and the concourses on each level evoke memories of a traditional Indiana basketball Fieldhouse, complemented by state-of-the art amenities. Highlighting the inner bowl of the Fieldhouse are the windows that support the 14-story (140 foot), exposed steel roof. Throughout the day, and during select events, the curtains to these windows are lowered; giving fans not only a view to the outside, but a beautiful view of downtown Indianapolis. The window theme is continued on both the Pennsylvania and Delaware Street sides of the Indiana University Health Entry Pavilion, home to the 18 ticket windows and retro-styled ticker board announcing the upcoming events. A true tribute to the game of basketball in Indiana, the sightlines were designed for the best viewing of a basketball game; but also give patrons a great view for the many other events held at the Fieldhouse. From concerts, hockey, high school and college sports to the circus and even the World Swimming Championship, the Fieldhouse is also highly acclaimed for both the number and variety of non-basketball events it holds each year. Its many meeting rooms, restaurants and multi-use spaces also make the Fieldhouse ideal for the smaller corporate gatherings and ceremonies held daily. Located in the heart of downtown Indianapolis, the Fieldhouse is located within walking distance of Circle Centre Mall, the Indiana Convention Center, Lucas Oil Stadium, Victory Field, the State Capitol Building and the City-County Building.

6

Economic Condition

State and Local Economy: Intellectual capital, public support, academic partnerships, workforce excellence and business and industry collaborations are the driving force behind Indiana’s life sciences industry. For more than a century, Indiana has been a center of innovations in the life sciences, pharmaceutical and medical device industries. Indiana is home to more than 1,000 businesses in the medical device, pharmaceutical, drug development, diagnostic and agriculture-biotech sectors. The State has long been a world leader in life sciences and is home to such industry giants as Eli Lilly and Company, Biomet, Cook Group Inc., Roche Diagnostics and Zimmer. Indiana boasts the second-largest medical school in the United States, the Indiana University School of Medicine. Indiana is also home to the Indiana University Emerging Technologies Center, a highly successful business incubator which houses many biosciences companies. Indiana's life sciences industry succeeds through a collaboration of partnerships between industry, academia and government which creates new jobs and economic growth.

The production of motor vehicles, parts and transportation equipment is a cornerstone element of Indiana’s manufacturing culture. Indiana is home to major assembly plants for Toyota, Subaru, Honda and General Motors. The state is also home to hundreds of vehicle parts manufacturers, including Chrysler, Cummins, Delphi, Allison Transmission, ArvinMeritor, NTN, Mitsubishi, KYB, Keihin, Enkei, Toa, Tomasco USSteel, Tower Automotive, PPG and the North American headquarters of Aisin U.S.A. According to the US Bureau of Economic Analysis, Indiana’s motor vehicle industry is the 2nd largest in the United States. Indiana is home to more than 630 automotive companies producing more than 11% of all automobiles produced in the United States.

Indiana's advanced Logistics industry is a driving force in today's economy and offers a sustainable competitive advantage to manufacturers and distributors. The State is also home to information technology businesses, including Hurco Companies, Inc., search engine ChaCha, Sony Digital Audio, Hitachi, ExactTarget, and Interactive Intelligence, which maintain a clear focus on building a strong information technology workforce. Indiana’s academic and industrial partners have created an environment that encourages and sustains growth in the clean technology sector; Indiana’s clean energy jobs grew by nearly 18 percent between 1998 and 2007, ranking the state first in the industrial Midwest in overall job growth in the clean energy industry. Agriculture also plays a vital role in Indiana’s economy. With more than 15 million acres of farmland, Indiana is a leading producer of corn, soybeans, hogs, poultry, popcorn and tomato products.

Motorsports companies have also developed a clear industry cluster in the region. After all, no other place on the globe can boast the number and variety of major racing events that are held in Indianapolis and other parts of the state, annually. Commonly referred to as the “Racing Capital of the World”, Indianapolis is home to the Indianapolis Motor Speedway. In 2011, the Indianapolis Motor Speedway celebrated the 100th anniversary of the 500 mile race, which was first run in 1911 and which has been broadcast live on the radio, in its entirety, by the Indianapolis Motor Speedway Radio Network since 1953. Beginning in 2007, this wonderful event was first broadcast in HD. Indianapolis hosts two of the largest single-day sporting events in the world ~ the Indianapolis 500, often referred to as the “Greatest Spectacle in Racing,” which will be run on Sunday, May 26th, and the Brickyard 400, which will take place on Sunday, July 28th. And, on Sunday, August 18th, the IMS will host the Red Bull Indianapolis GP. The motorsports industry attracts a highly skilled and mobile workforce and, among other benefits, is an important asset in Indiana’s effort to retain and attract college graduates and other creative and skilled individuals.

There are a number of other notable players in the Indiana economy, among which is the Indianapolis Airport Authority. In 2012, the Indianapolis International Airport (IND) served 7.3 million domestic and international passengers. IND is the eighth largest cargo facility in the nation, and internationally it ranks 22nd largest in the world. In 2012, 1 million tons of cargo were transported from this facility. On average, there were 135 daily departures. In addition to 32 nonstop locations, there are 31 additional destinations from IND.

7

The passenger terminal is approximately 1.2 million square feet, with two concourses, each having 20 gates. Two gates are for international arrivals and lead to a dedicated federal inspection area and baggage claim. This beautiful state-of-the-art facility is an important contributor to central Indiana’s growing economy. As a part of the Airport’s economic impact, and based upon the most recent data available from the Aviation Association of Indiana, IND’s annual economic impact is $3.3 billion dollars. Key business partners include 9 commercial airlines, FAA, TSA, U.S. Customs & Border Patrol, 58 concessionaires (rental car, retail and other service providers), and tenants including FedEx Corporation, AAR, Express Scripts, Comlux, Hawker Beechcraft Services and Signature Flight Support. About 10,000 people work at the airport each day. No property taxes were or are used to operate and manage IND.

Indiana benefits from its proximity to major markets and population centers - both nationally and internationally. Through Indiana’s three ports, businesses can access markets and population centers in the north, through Lake Michigan and the Great Lakes - St. Lawrence Seaway; and to the south, through the Ohio and Mississippi rivers. Sometimes referred to as, “the Crossroads of America,” Indianapolis is at the center of America’s heartland, with more interstates converging in Indianapolis than in any other city in the United States. More than 50% of the population in the U.S. lives within a one day’s drive of Indianapolis.

Indianapolis is the nation’s 12th largest city. According to the U.S. Census Bureau’s Statistics for 2011, the estimated population of Marion County is 911,296 and 1,778,568 for the Indianapolis Metropolitan Area. Indianapolis is well known for the multitude of cultural, educational, sporting, shopping and dining opportunities offered to its residents and visitors. Indianapolis is the home of “Hoosier Hospitality” the perfect blend of Midwest, small town welcome and big city attractions and opportunities. Employers and employees discover that a dollar goes farther here. In other words, lower operating and living costs allow more to be done with less. Residents and business owners alike enjoy an extremely competitive cost of living, along with a high quality of life.

The hallmarks of the Indianapolis economy have long been its diversity and steady growth, which is part of the foundation of Indy’s strong performance during the past several years. Indianapolis can boast of diverse strengths in the manufacturing, distribution, retail and service sectors. Economic diversity keeps Indianapolis on a steady growth track. Additionally, Indiana’s real estate availability affords a wide selection of available land, existing office space and industrial parks. Finally, many of the city’s accomplishments, such as Victory Field, Bankers Life Fieldhouse, Circle Centre Mall, Lucas Oil Stadium, and the expanded Convention Center were all the result of successful partnerships between private and public sectors.

The stable economy and many attractions of Indianapolis, along with its central location within the nation, make it a prominent convention and tourist center. The Indianapolis 500 Mile Race, the Brickyard 400, the Red Bull Indianapolis GP, the NFL’s Indianapolis Colts, the NBA’s Indiana Pacers, the WNBA’s Indiana Fever and the AAA Indianapolis Indians baseball team are among the city’s prominent sporting attractions, not to mention countless amateur sporting events, including the Big Ten Championship Football Game, the NCAA® Men’s and Women’s Final Four Basketball Championship and the Men’s and Women’s Big Ten Basketball Tournaments. In February 2012, Indianapolis hosted the NFL Super Bowl®. Circle Centre Mall, White River State Park, the NCAA Headquarters and Hall of Champions, the Indianapolis Zoo, the Indianapolis Motor Speedway Museum, the Indiana State Museum, the Indianapolis Children’s Museum, the Indianapolis Museum of Art, the Eiteljorg Museum of American Indian and Western Art, the American Cabaret Theatre, the Indiana Repertory Theatre, the Indianapolis Symphony Orchestra and the White River State Park have also become popular attractions, along with many outstanding downtown restaurants and sports bars.

8

The current brand strategy of Visit Indy, Inc. (Visit Indy) is based on the competitive spirit found in the people of Indiana and offers a brand position that lives within the people of our great state. Around the world, Indianapolis’ name is synonymous with the very spirit of competition. With every structure we build, every event we stage, and every attraction we display, we set new national standards: always planning ahead for our next big opportunity - and consistently raising the game. In the development of this brand strategy, Visit Indy has been speaking in terms of certain primary factors which come into play. The first has to do with the restless dissatisfaction that describes the Hoosier spirit, one that never rests on its laurels and past successes. This is evident with the Col. H. Weir Cook Terminal at the Indianapolis International Airport, Lucas Oil Stadium, the expanded Indiana Convention Center and the recently completed JW Marriott. The JW Marriott Indianapolis is the city’s largest, full-service convention hotel with 104,000 square feet of meeting and event space and 1,005 guest rooms. With the addition of these new hotel rooms, the Indiana Convention Center now has over 4,700 rooms that are connected to the convention center. Indianapolis now has more rooms connected to its convention center than any other city in the country. The dynamic convention and meetings market and a vibrant tourism and hospitality industry are at the core of all of this exciting growth. Our industry is powered by over 70,000 dedicated service employees who help deliver an annual economic impact to Indianapolis MSA of approximately $3.5 billion. Significant growth will take place in the future for the convention and meetings market along with steady growth in leisure business to our city and region. In Visit Indy parlance, here’s to a bright future and additional guests visiting our great city in the years ahead.

Major Initiatives of the CIB: The Indiana Convention Center & Lucas Oil Stadium are excellent venues that have hosted very diverse groups - NCAA® Men’s and Women’s Final Four® Basketball Championships, North American Christian Annual Convention, Drum Corp International World Championship, Indiana Black Expo and VFW Annual National Convention. Groups leading the Top 20 Conventions, based on direct visitor spending for 2012, include Super Bowl XLVI® and NFL Experience, Fire Department Instructors Conference, Do It Best Corporation, National FFA Organization Convention, Gen Con LLC, Custom Electronic Design & Installation Association, Episcopal Church, The American Legion, Big Ten Football Championship and International Motorsports Industry Show.

The CIB’s primary objective, aside from the management and maintenance of its various facilities, is to build on the momentum of its convention and trade show business and continue to attract national and international sporting and other events to its facilities. A breakdown of current year events hosted and future events scheduled follows:

Current Year Events

JAMfest Super Nationals, Super Bowl XLVI®, NFL Experience, 2012, Dealernews International Powersports Dealer Expo, Pumper Cleaner Environmental Expo, Work Truck Show and NTEA Annual Convention, M-PACT 2012, International Sleep Products Assn. EXPO 2012, Nike MEQ Volleyball, National Science Teachers Association National Convention, Fire Department Instructors Conference, American Occupational Therapy Association Annual Meeting, American Coatings Shows & Conference-Biennial, 500 Festival Mini-Marathon Packet Pick-up and Expo, Indiana Conference of the United Methodist Church Annual Conference, IUPUI Commencement, Indiana Black Expo 2012 Summer Celebration, Gen Con "The Best Four Days in Gaming", Do it Best Corporation May and October Markets, National Forensic League National Tournament, American Legion National Convention, CEDIA Expo 2012, American Industrial Hygiene Association Annual Convention, 2012 WSF Cheer & Dance Nationals “Indy Showdown,” Young Champions Cheer Competition, NBM Shows, National Black MBA Association Annual Conference, Revive Our Hearts 2012 TRUE WOMAN Conference, Episcopal Church Triennial General Convention, 2012 Pokémon U.S. National Championships, American Association of Diabetes Educators Annual Meeting, Sports Inc. June Athletic Show, North American Die Casting Association CASTEXPO, National FFA Convention 2012, National Missionary Annual & Joint Youth Convention, Kenny Chesney Concert, DCI World Championships, Performance Racing Industry PRI Show, ISSMA State Marching Band Finals, Music For All Regional and Grand National Championships, Circle City Classic, Big Ten Football Championship Game, Big Ten Football Fanfest, and Indianapolis Colts Football.

9

Major Events Scheduled for 2013

National Precast Concrete Association, Circle of Stars Gymnastics Invitational, National Soccer Coaches Association Annual Convention, JAMfest Super Nationals, Capitol Sports Volleyball Central Zone Invitational, 2013 Monster Jam, 2013 Dealer Expo, National Football Scouting Combine, Pumper Cleaner Environmental Expo, Work Truck Show and NTEA Annual Convention, 2013 Supercross, Higher Education Users Group Alliance 2013, Nike Mideast Qualifier Volleyball, National Society of Black Engineers Annual National Convention, NCAA® Midwest Regional Basketball, WQA Aquatech USA, Just Give Me Jesus, National AfterSchool Association Annual Conference 2013, Association of College & Research Libraries Biennial, M-PACT 2013, Fire Department Instructors Conference, Do it Best Corporation May and October Markets, 2013 NCAA® Division I Men's Lacrosse Championship Quarterfinals, American College of Sports Medicine Annual Meeting, NBM Shows, Indiana Conference of the United Methodist Church Annual Conference, Church of the Nazarene General Assembly, lia sophia Annual Conference, Shriners of North America Imperial Council Session, 2013 Pokémon U.S. National Championships, Signature Equipo Vision LLC Summer Convention, ADSA-ASAS Joint Annual Meeting, Scentsy Annual Convention, Indiana Black Expo 2013 Summer Celebration, Pentecostal Assemblies of the World Annual Summer Assembly, DCI World Championships, Gen Con "The Best Four Days in Gaming", American Chemical Society National Meeting & Expo, Railway Interchange, Society of Hispanic Professional Engineers Annual, National Association for Gifted Children Annual Convention, Walk in the Word - Harvest Bible Chapel, Percussive Arts Society International Convention, Music For All Grand National Championship, National Federation for Catholic Youth Ministry Conference, Circle City Classic, Big Ten Football Championship Game, Big Ten Football Fanfest, SEMA/PRI Show, and Indianapolis Colts Football.

Major Events for 2014

American Football Coaches Association Annual Convention, 2014 Monster Jam, Circle of Stars Gymnastics Invitational, Pumper Cleaner Environmental Expo, 2014 Supercross, Work Truck Show and NTEA Annual Convention, Public Library Association National Convention, Property Loss Research Bureau Annual Claim Conference, Nike Mideast Qualifier Volleyball, American College Personnel Association Annual Convention, M-PACT 2014, Fire Department Instructors Conference, Nat'l. Rifle Assn. of America Annual Mtg./Exhibits, Do it Best Corporation May and October Markets, Business Professionals of America National Leadership Conference, National NeedleArts 2014 Summer Trade Show, Association for Iron & Steel Technology AISTECH 2014, BBI 2014 International Fuel Ethanol Workshop & Expo, NBM Shows, American Society for Engineering Educational Annual Conference & Exposition, lia sophia Annual Conference 2014, National Athletic Trainers' Association Annual Meeting, North American Christian Convention Annual Convention, Indiana Black Expo 2014 Summer Celebration, Gen Con "The Best Four Days in Gaming", National Association College Admission Counseling Annual Conference, Emergency Nurses Assn. Annual Scientific Conference, Music For All Grand National Championship, Percussive Arts Society International Convention, Circle City Classic, Big Ten Football Championship Game, Assemblies of the Lord Jesus Christ National Youth, Big Ten Football Fanfest, SEMA/PRI Show and Indianapolis Colts Football.

10

Awards and Acknowledgements

Independent Audit: The CIB has an annual audit of its financial statements performed by the Indiana State Board of Accounts. The independent auditor’s report on the CIB’s financial statements is included in the financial section of this report.

Awards: The Government Finance Officers Association of the United States and Canada (“GFOA”) awarded a Certificate of Achievement for Excellence in Financial Reporting to the CIB for its comprehensive annual financial report for the fiscal year ended December 31, 2011. This was the 27th consecutive year that the CIB has achieved this prestigious award. In order to be awarded a Certificate of Achievement, a government must publish an easily readable and efficiently organized comprehensive annual financial report. This report must satisfy both accounting principles generally accepted in the United States of America and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe that our current comprehensive annual financial report continues to meet the Certificate of Achievement Program requirements and we are submitting it to the GFOA to determine its eligibility for another certificate.

Acknowledgements: This report could not have been prepared without the assistance of numerous staff members and the Indiana State Board of Accounts.

Sincerely,

Augustus B. Levengood, Executive Director Ann Lathrop, President

11

Capital Improvement Board of Managers of Marion County, Indiana

Organizational Table

12

13

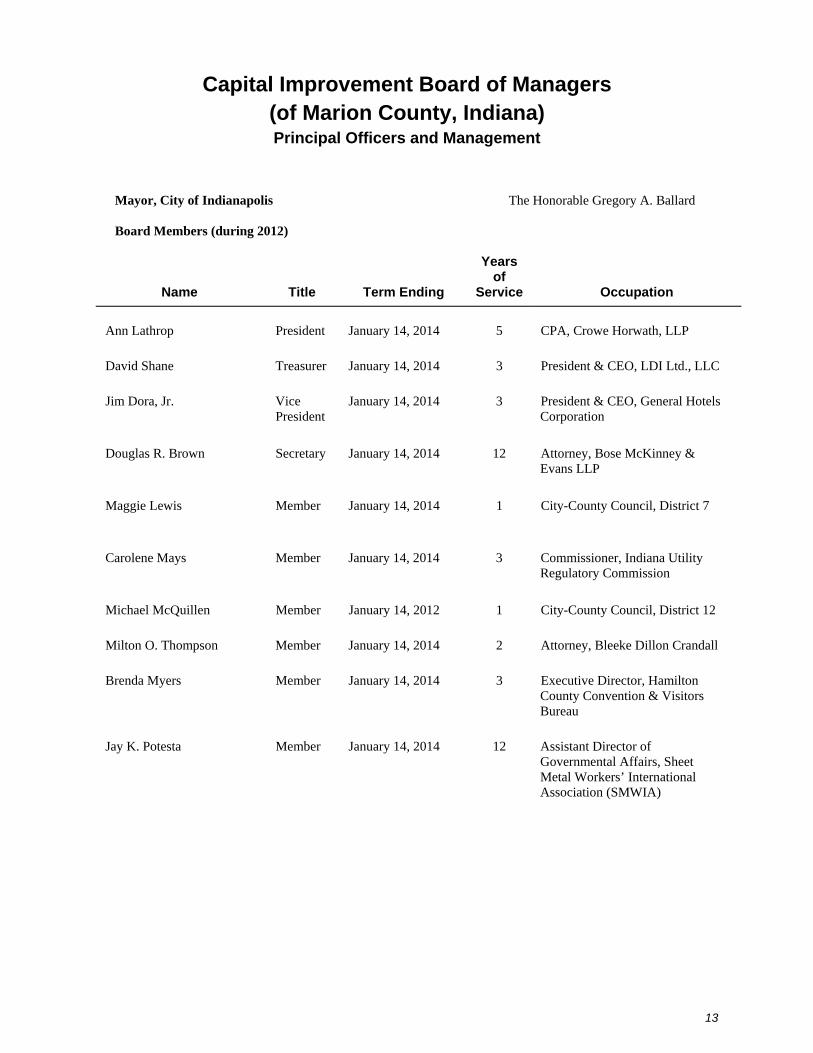

Capital Improvement Board of Managers (of Marion County, Indiana) Principal Officers and Management

Mayor, City of Indianapolis The Honorable Gregory A. Ballard Board Members (during 2012)

Name

Title

Term Ending

Years of

Service

Occupation

Ann Lathrop President January 14, 2014 5 CPA, Crowe Horwath, LLP

David Shane Treasurer January 14, 2014 3 President & CEO, LDI Ltd., LLC

Jim Dora, Jr. Vice President

January 14, 2014 3 President & CEO, General Hotels Corporation

Douglas R. Brown Secretary January 14, 2014 12 Attorney, Bose McKinney & Evans LLP

Maggie Lewis Member January 14, 2014 1 City-County Council, District 7

Carolene Mays Member January 14, 2014 3 Commissioner, Indiana Utility Regulatory Commission

Michael McQuillen Member January 14, 2012 1 City-County Council, District 12

Milton O. Thompson Member January 14, 2014 2 Attorney, Bleeke Dillon Crandall

Brenda Myers Member January 14, 2014 3 Executive Director, Hamilton County Convention & Visitors Bureau

Jay K. Potesta Member January 14, 2014 12 Assistant Director of Governmental Affairs, Sheet Metal Workers’ International Association (SMWIA)

14

Capital Improvement Board of Managers (of Marion County, Indiana)

Principal Officers and Management (Continued)

Administrative Personnel

Name

Position

Years of Service

Barney Levengood Executive Director 22

Linda G. Addaman Director of Marketing 17

Dan Huge, CPA Chief Financial Officer 3

Patti Dean Controller 3

Major E. Gardner Event Manager 32*

Michael A. Fox Stadium Director 28

Thomas L. Boyle Director of Operations 18 Counsel to the Board Bingham Greenebaum Doll, LLP Indianapolis, Indiana * Major E. Gardner employed January 1, 2012 - November 2, 2012

Financial Section

STATE OF INDIANA

AN EQUAL OPPORTUNITY EMPLOYER STATE BOARD OF ACCOUNTS 302 WEST WASHINGTON STREET ROOM E418 INDIANAPOLIS, INDIANA 46204-2765

Telephone: (317) 232-2513 Fax: (317) 232-4711 Web Site: www.in.gov/sboa

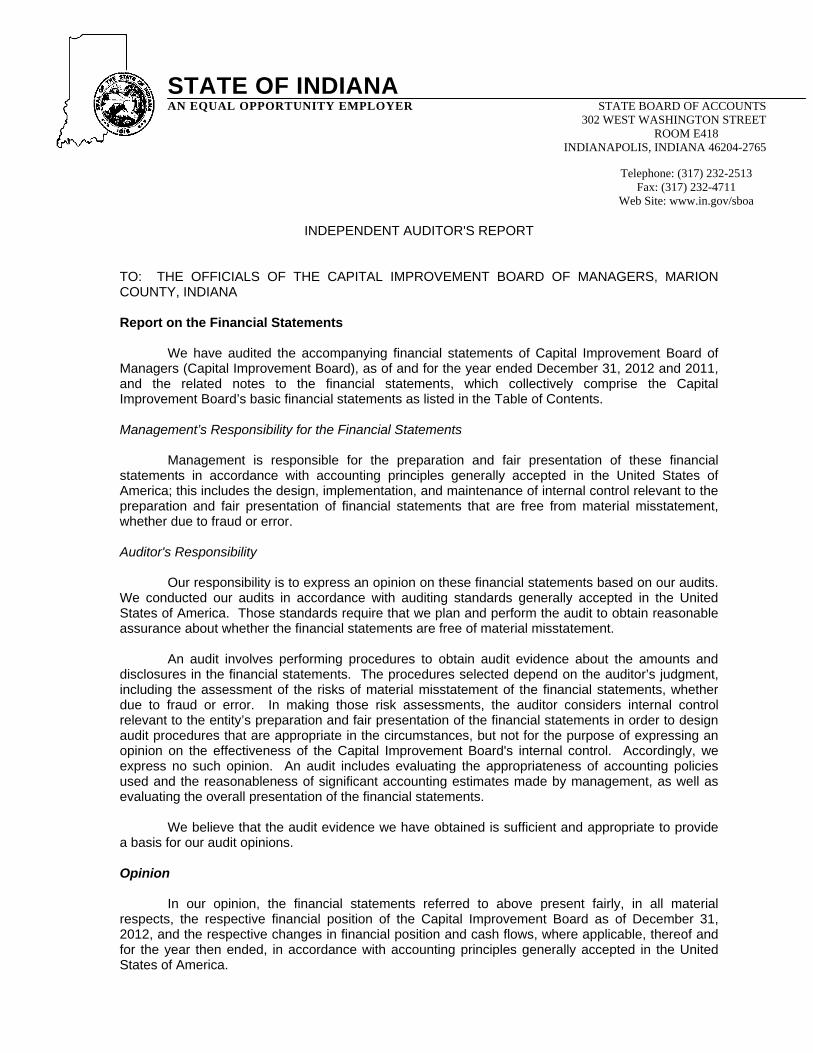

INDEPENDENT AUDITOR'S REPORT

TO: THE OFFICIALS OF THE CAPITAL IMPROVEMENT BOARD OF MANAGERS, MARION COUNTY, INDIANA Report on the Financial Statements We have audited the accompanying financial statements of Capital Improvement Board of Managers (Capital Improvement Board), as of and for the year ended December 31, 2012 and 2011, and the related notes to the financial statements, which collectively comprise the Capital Improvement Board’s basic financial statements as listed in the Table of Contents. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor's Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Capital Improvement Board's internal control. Accordingly, we express no such opinion. An audit includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the Capital Improvement Board as of December 31, 2012, and the respective changes in financial position and cash flows, where applicable, thereof and for the year then ended, in accordance with accounting principles generally accepted in the United States of America.

16

Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the Management’s Discussion and Analysis as listed in the table of contents be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Capital Improvement Board basic financial statements. The accompanying Balance Sheet Information (Combining Statements), Analysis of Revenues, Expenses and Changes in Net Position, and Analysis of Certain Operating Expenses are presented for purposes of additional analysis and are not a required part of the basic financial statements. The schedules listed above are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the combining and analysis schedules listed above are fairly stated, in all material respects, in relation to the basic financial statements as a whole. The Introductory and Statistical Sections have not been subjected to the auditing procedures applied in the audit of the basic financial statements, and accordingly, we do not express an opinion or provide any assurance on these sections.

Bruce Hartman, CPA State Examiner May 23, 2013

17

MANAGEMENT’S DISCUSSION AND ANALYSIS

(Unaudited)

Introduction

The management of Capital Improvement Board of Managers of Marion County, Indiana (“CIB”), which is a component unit of the Consolidated City of Indianapolis-Marion County (“City”) and conducts its business in the City, offers readers of the CIB’s financial statements this narrative overview and analysis of the financial activities of the CIB for the fiscal year ended on December 31, 2012. This Management’s Discussion and Analysis is being presented to provide additional information regarding the activities of the CIB in connection with its financial statements and to meet the requirements of Governmental Accounting Standards Board (“GASB”) Statement No. 34, Basic Financial Statements - and Management’s Discussion and Analysis - for State and Local Governments.

The CIB is organized and operated to acquire, construct, finance, lease, operate, promote and publicize capital improvements and thereby serve the convention and visitor industry and the commercial, industrial and cultural interests of Indiana and its citizens. This presently occurs principally through its operation of the Indiana Convention Center & Lucas Oil Stadium, and its use arrangements related to Victory Field and Bankers Life Fieldhouse.

Financial Highlights

The following are some highlights from the CIB’s financial statements for the year ended December 31, 2012:

The CIB experienced an increase in Total assets of about $1.8 million, or .12% in 2012. Current assets - restricted increased by about $8.1 million primarily due to increases in the stadium and convention center sublease investment accounts. Current assets - unrestricted increased about $11.6 million due to an increase in cash reserves, which was largely the result of tax receipts designated for operating purposes in excess of the 2012 cash outlay. Capital assets decreased by about $34.4 million. This represents depreciation expense less additions in 2012. Other assets increased $16.5 million related to loans and advances,

Total liabilities decreased by about $14.9 million, or 1.2% in 2012. Current liabilities increased about $5.3 million in 2012 largely due to an increase in the current portion of long-term debt related to capital leases, while Noncurrent liabilities decreased about $20.2 million due to decreases in capital leases, and bonds and notes payable.

Net position increased by about $16.7 million, or 7.0% in 2012, primarily due to an increase in cash and investments, and note receivable, as well as a decrease in capital leases payable and a decrease in capital assets due to depreciation expense.

Operating revenues increased by about $1.7 million, or 6.4% in 2012, primarily due to labor reimbursements related to the Super Bowl.

Nonoperating revenues increased by about $10.1 million, or 7.8%. State and local taxes and other assistance increased by about $10.0 million due to fluctuations in the underlying activities from which such tax revenues are derived.

18

Operating expenses increased by about $11.0 million, or 14.6%, in large part due to additional labor and other expenses related to the Super Bowl, as well as, other new events. In addition, depreciation and amortization expense increased by $4.0 million.

Nonoperating expenses increased by about $1.0 million, or 1.5%. Interest expense increased by about $2.1 million and loss on sale/disposal of capital assets decreased by $1.0 million.

Overview of Financial Statements

This financial report of the CIB includes the following financial statements for the calendar years 2012 and 2011:

• Balance Sheets

• Statements of Revenues, Expenses and Changes in Net Position

• Statements of Cash Flows

Also included are notes to the financial statements that provide more detailed data. These financial statements are prepared in accordance with accounting principles generally accepted in the United States of America promulgated by GASB.

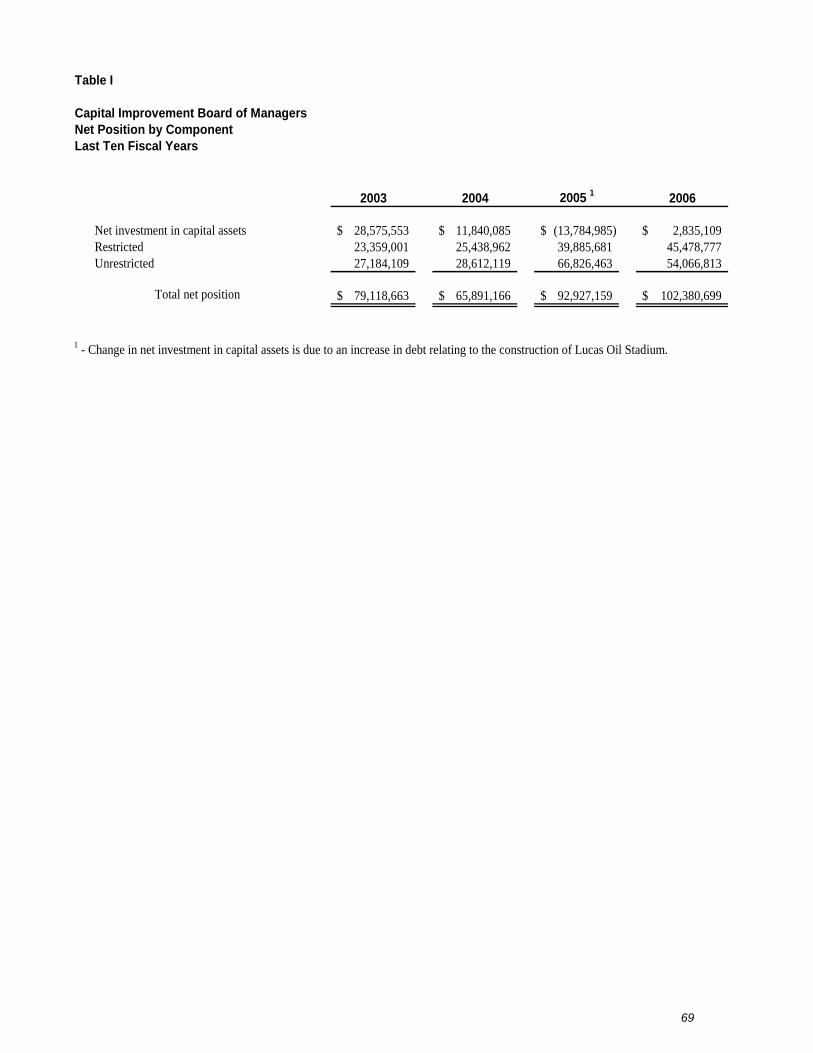

The net position of the CIB is composed of three categories:

Net investment in capital assets - this reflects the CIB’s investment in capital assets (e.g. land, buildings, machinery and equipment), less any related debt used to acquire those assets that is still outstanding. The CIB uses these capital assets to provide services to the public; consequently, these assets are not available for future spending. Although the CIB’s investment in its capital assets is reported net of related debt, it should be noted that the resources to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities.

Restricted - this represents resources that are subject to external restrictions (which principally relate to trust agreements under which capital lease obligations and bonded indebtedness were incurred) on how they may be used.

Unrestricted - this represents resources that may be used to meet the CIB’s ongoing obligations to the public and creditors.

The Balance Sheets reflect the assets and liabilities of the CIB using the accrual basis of accounting, which is similar to the accounting used by most private-sector companies. The CIB’s net position represents one way to measure the CIB’s financial health. In a general way, changes in net position that occur over time may also serve as an indicator of whether the financial position of the CIB is strengthening or softening. However, to assess the overall fiscal health of the CIB, readers of the CIB’s financial statements should consider additional nonfinancial factors such as the ability of the CIB to retain and attract conventions, trade shows, tourism, sporting and cultural events and other activities that utilize the capital assets of the CIB; the general economic health and outlook in Indianapolis-Marion County in the hotel and motel, retail food and beverage and rental car industries, which are subject to certain local taxes that are committed to and financially support the CIB; and the general economic health and outlook locally (that is, Indianapolis-Marion County and the surrounding region) as well as nationally with regard to consumer appetite for scheduling, attending and supporting the events and activities at the facilities of the CIB.

19

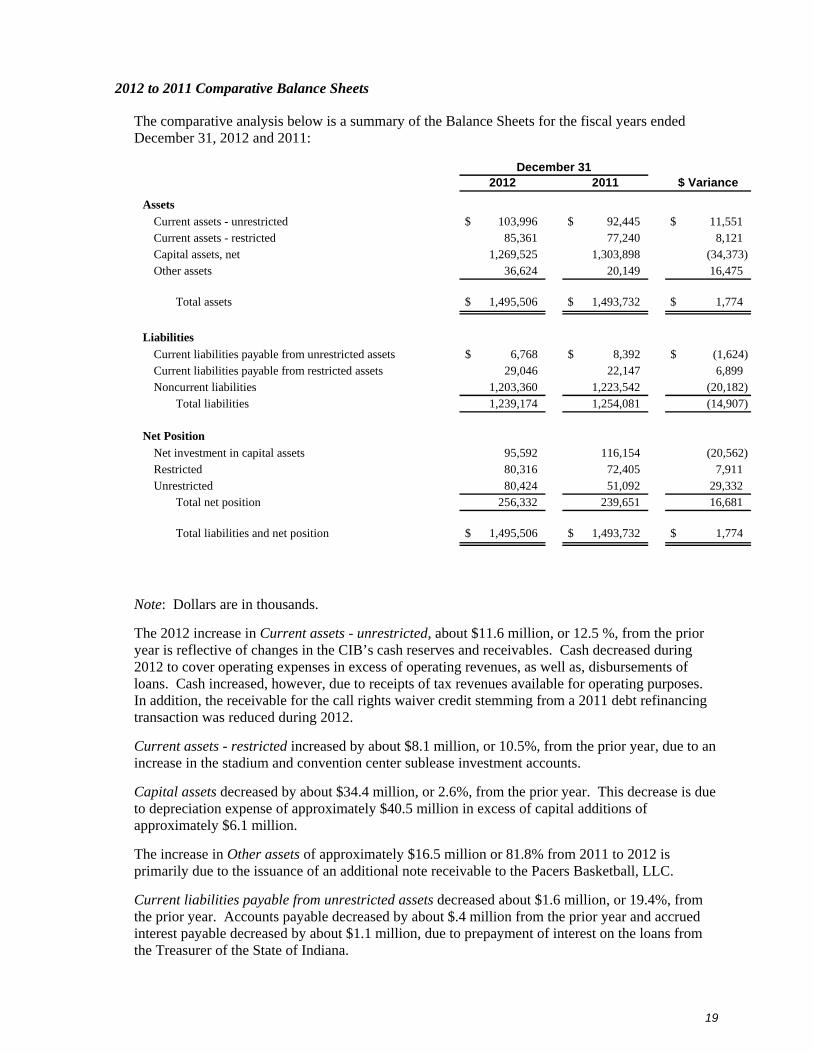

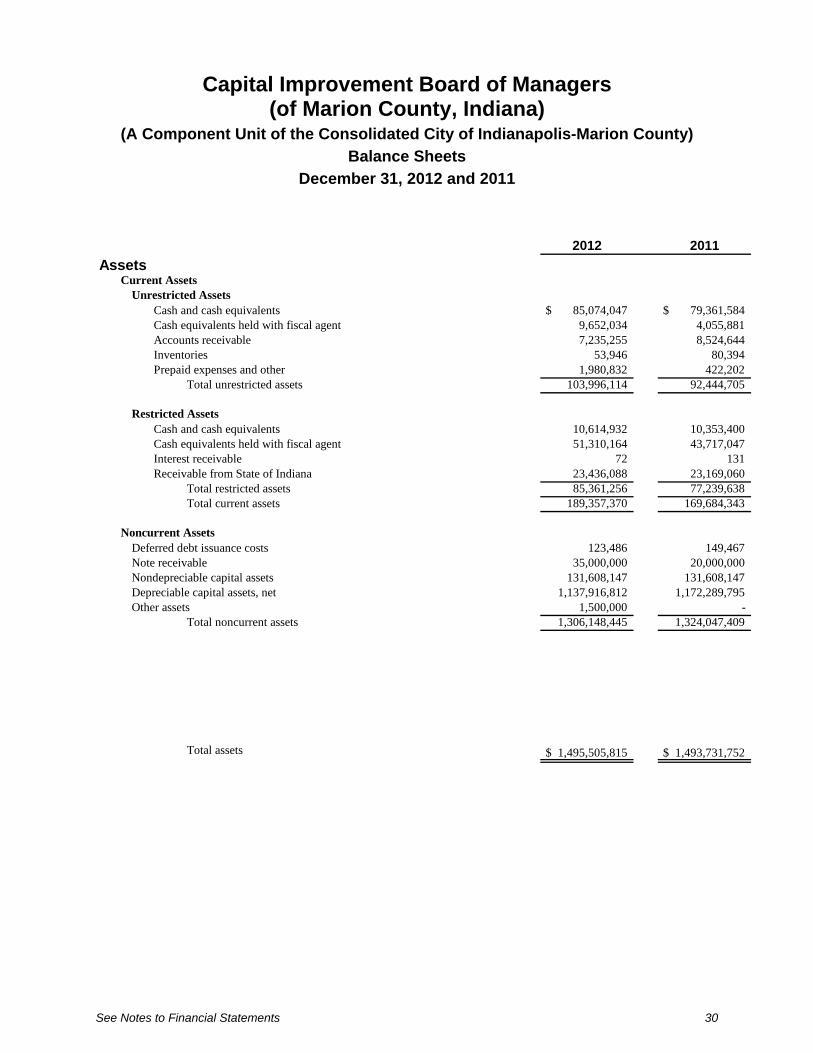

2012 to 2011 Comparative Balance Sheets

The comparative analysis below is a summary of the Balance Sheets for the fiscal years ended December 31, 2012 and 2011:

2012 2011 $ Variance

Assets

Current assets - unrestricted $ 103,996 $ 92,445 $ 11,551 Current assets - restricted 85,361 77,240 8,121 Capital assets, net 1,269,525 1,303,898 (34,373)Other assets 36,624 20,149 16,475

Total assets $ 1,495,506 $ 1,493,732 $ 1,774

Liabilities

Current liabilities payable from unrestricted assets $ 6,768 $ 8,392 $ (1,624)Current liabilities payable from restricted assets 29,046 22,147 6,899 Noncurrent liabilities 1,203,360 1,223,542 (20,182)

Total liabilities 1,239,174 1,254,081 (14,907)

Net Position

Net investment in capital assets 95,592 116,154 (20,562)Restricted 80,316 72,405 7,911 Unrestricted 80,424 51,092 29,332

Total net position 256,332 239,651 16,681

Total liabilities and net position $ 1,495,506 $ 1,493,732 $ 1,774

December 31

Note: Dollars are in thousands.

The 2012 increase in Current assets - unrestricted, about $11.6 million, or 12.5 %, from the prior year is reflective of changes in the CIB’s cash reserves and receivables. Cash decreased during 2012 to cover operating expenses in excess of operating revenues, as well as, disbursements of loans. Cash increased, however, due to receipts of tax revenues available for operating purposes. In addition, the receivable for the call rights waiver credit stemming from a 2011 debt refinancing transaction was reduced during 2012.

Current assets - restricted increased by about $8.1 million, or 10.5%, from the prior year, due to an increase in the stadium and convention center sublease investment accounts.

Capital assets decreased by about $34.4 million, or 2.6%, from the prior year. This decrease is due to depreciation expense of approximately $40.5 million in excess of capital additions of approximately $6.1 million.

The increase in Other assets of approximately $16.5 million or 81.8% from 2011 to 2012 is primarily due to the issuance of an additional note receivable to the Pacers Basketball, LLC.

Current liabilities payable from unrestricted assets decreased about $1.6 million, or 19.4%, from the prior year. Accounts payable decreased by about $.4 million from the prior year and accrued interest payable decreased by about $1.1 million, due to prepayment of interest on the loans from the Treasurer of the State of Indiana.

20

Current liabilities payable from restricted assets increased about $6.9 million, or 31.2%, from the prior year. Current portion of long-term debt and rental deposits increased by approximately $6.5 million and $.5 million, respectively.

Noncurrent liabilities decreased by about $20.2 million, or 1.6%, from the prior year. The net decrease in noncurrent liabilities in 2012 is due to reductions of the capital lease obligations and other debt in excess of new debt acquired during the year. With the completion of the ICC expansion project in 2011, the 2012 additions to debt were minimal compared to the scheduled payment reductions during the year.

Invested in Capital assets, net of related debt decreased about $20.6 million, or 17.7%, in 2012, as a result of reductions of debt and depreciation expense in excess of newly acquired capital assets. Restricted net position increased about $7.9 million, or 10.9%, in 2012, as a result of an increase in cash equivalents held with fiscal agent. This represents tax revenues received to be used to pay the capital lease obligations related to Lucas Oil Stadium and the ICC expansion. The approximate $29.3 million increase, or 57.4%, from the prior year in Unrestricted net position is primarily due to the continued increase of tax revenues available for operating purposes.

2011 to 2010 Comparative Balance Sheets

The comparative analysis below is a summary of the Balance Sheets for the fiscal years ended December 31, 2011 and 2010:

2011 2010 $ Variance

Assets

Current assets - unrestricted $ 92,445 $ 73,055 $ 19,390 Current assets - restricted 77,240 68,371 8,869 Capital assets, net 1,303,898 1,321,956 (18,058)Other assets 20,149 10,177 9,972

Total assets $ 1,493,732 $ 1,473,559 $ 20,173

Liabilities

Current liabilities payable from unrestricted assets $ 8,392 $ 5,436 $ 2,956 Current liabilities payable from restricted assets 22,147 40,195 (18,048)Noncurrent liabilities 1,223,542 1,218,572 4,970

Total liabilities 1,254,081 1,264,203 (10,122)

Net Position

Net investment in capital assets 116,154 118,659 (2,504)Restricted 72,405 66,209 6,196 Unrestricted 51,092 24,488 26,604

Total net position 239,651 209,356 30,295

Total liabilities and net position $ 1,493,732 $ 1,473,559 $ 20,173

December 31

Note: Dollars are in thousands.

21

The 2011 increase in Current assets - unrestricted, about $19.4 million, or 26.5 %, from the prior year is reflective of changes in the CIB’s cash reserves and an additional receivable for call rights waiver credits stemming from a 2011 debt refinancing transaction. Cash decreased during 2011 to cover operating expenses in excess of operating revenues, however, increased due to an $8 million receipt of funds from the interlocal agreement and other tax revenues designated for operating purposes.

Current assets - restricted increased by about $8.9 million, or 13.0%, from the prior year, due to an approximate increase of $2.8 million in the renewal and replacement reserve, $2.5 million in box office funds and $3.6 million in taxes receivable from the State of Indiana.

Capital assets decreased by about $18.0 million, or 1.4%, from the prior year. In 2011, this decrease is due to depreciation expense in excess of capital additions since the ICC expansion project was placed into service in 2011.

The increase in Other assets of approximately $10.0 million or 98.0% from 2010 to 2011 is due to the issuance of an additional note receivable to the Pacers Basketball, LLC.

Current liabilities payable from unrestricted assets increased about $3.0 million, or 54.4%, from the prior year. Accounts payable increased by about $2.3 million, or 57.2%, from the prior year due to various capital projects. Accrued interest payable increased by about $.67 million, due to interest on loans from the Treasurer of the State of Indiana.

Current liabilities payable from restricted assets decreased about $18.0 million, or 44.9%, from the prior year. Current unearned contribution revenue decreased by $12.5 million due to the recognition of such amounts as revenue in 2011. Current portion of long-term debt decreased by $5.9 million, the real estate rentals payable decreased $1.85 million, and funds held for others - box office increased $2.5 million.

Noncurrent liabilities increased about $5.0 million, or .4%, over the prior year. The amount due to the State of Indiana was reclassified as a capital lease payable since the ICC project was placed into service in 2011. The net increase in noncurrent liabilities in 2011 is due to additional expenditures on LOS and the ICC, net of scheduled reductions for the capital lease obligations.

Net investment in capital assets decreased about $2.5 million, or 2.1%, in 2011, as a result of capital asset and related debt activity in connection with the LOS and ICC projects. Restricted increased about $6.2 million, or 9.4%, in 2011, as a result of an increase in the renewal and replacement fund and box office funds, and an increase in the accrual of state and local tax assistance. The approximate $26.6 million increase, or 108.7%, from the prior year in Unrestricted is primarily due to the receipt of $8 million from the interlocal agreement and new tax revenues created in 2009 designated for operating expenses.

22

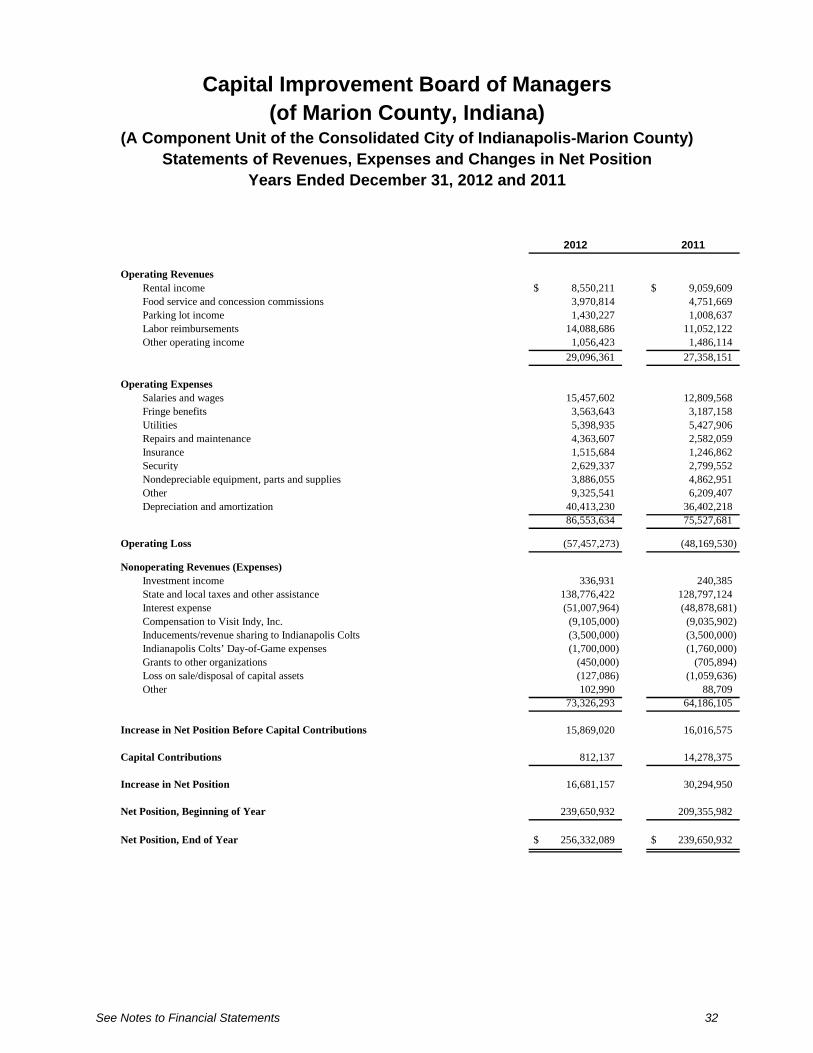

2012 to 2011 Comparative Statements of Revenues, Expenses and Changes in Net Position

The comparative analysis below is a summary of the Statements of Revenues, Expenses and Changes in Net Position for the fiscal years ended December 31, 2012 and 2011:

2012 2011 $ Variance % Variance

Operating Revenues

Rental income $ 8,550 $ 9,060 $ (510) (5.6) %Food service and concession commissions 3,971 4,752 (781) (16.4)

Parking lot income 1,430 1,009 421 41.7

Labor reimbursements 14,089 11,052 3,037 27.5

Other operating income 1,056 1,486 (430) (28.9)

Total operating revenues 29,096 27,359 1,737 6.4

Nonoperating Revenues

Investment income 337 240 97 40.2

State and local taxes and other assistance 138,777 128,797 9,980 7.7

Other 103 89 14 16.1

Total nonoperating revenues 139,217 129,126 10,091 7.8

Total revenues 168,313 156,485 11,828 7.6

Operating Expenses

Salaries and wages 15,458 12,810 2,648 20.7

Fringe benefits 3,564 3,187 377 11.8

Utilities 5,399 5,428 (29) (0.5)

Repairs and maintenance 4,364 2,582 1,782 69.0

Insurance 1,516 1,247 269 21.6

Security 2,629 2,800 (171) (6.1)

Nondepreciable equipment, parts and supplies 3,886 4,863 (977) (20.1)

Other 9,325 6,209 3,116 50.2

Depreciation and amortization 40,413 36,402 4,011 11.0

Total operating expenses 86,554 75,528 11,026 14.6

Nonoperating Expenses

Interest expense 51,008 48,879 2,129 4.4

Compensation to Visit Indy, Inc. 9,105 9,036 69 0.8

Colts inducements/Revenue Sharing and Day-of-Game expenses 5,200 5,260 (60) (1.1)

Other 577 1,765 (1,188) 100.0

Net nonoperating expenses 65,890 64,940 950 1.5

Total expenses 152,444 140,468 11,976 8.5

Income Before Capital Contributions 15,869 16,017 (148) (0.9)

Capital Contributions 812 14,278 (13,466) (94.3)

Increase in Net Position 16,681 30,295 (13,614) (44.9)

Net Position, Beginning of Year 239,651 209,356 30,295 14.5

Net Position, End of Year $ 256,332 $ 239,651 $ 16,681 7.0

December 31

Note: Dollars are in thousands.

Total operating revenues increased about $1.7 million, or 6.4%. Labor reimbursements increased about $3 million, or 27.5%, mainly related to the Super Bowl. All other operating revenues decreased a total of approximately $1.3 million, in part due to normal fluctuations in event activity and partially due to the lack of availability of space for other events during the Super Bowl time frame.

23

Total nonoperating revenues increased about $10.1 million, or 7.8%. State and local taxes and fees increased about $10.0 million, or 7.7%. The 2005 New Tax revenues increased about $4.9 million and all other Excise Tax revenues increased approximately $5.2 million in 2012.

Total operating expenses increased by $11.0 million, or 14.6%. Salaries and wages increased by about $2.6 million, or 20.7%, and fringe benefits increased about $.4 million, or 11.8%. Much of this increase was related to the Super Bowl. Repairs and maintenance costs increased about $1.8 million, or 69.0%, due to several large projects during 2012. Nondepreciable equipment, parts and supplies decreased about $1.0 million, or 20.1%, due to 2011 expenses relating to the ICC expansion. Other expenses increased by about $3.1 million, or 50.2%, due primarily to costs related to public safety for the Super Bowl. Depreciation and amortization increased about $4.0 million, or 11.0%, due to 2012 being the first full year for depreciation for the ICC expansion project which was placed into service in 2011.

Total nonoperating expenses increased about $1.0 million, or 1.5%. Interest expense increased approximately $2.1 million. This represents a combination of decreased interest expense in 2012 related to savings on certain debt refinancing transactions, as well as increased expense in 2012 on other debt issues due to debt refinancing savings recognized in 2011. In addition, the ICC expansion debt had a significant increase in interest expense in 2012. Other nonoperating expenses decreased about $1.2 million. This is the result of approximately $1.1 million of loss on sale/disposal of capital assets, primarily related to the replacement of carpet in the ICC included in 2011.

Capital contributions recognized of approximately $.8 million represent capital additions at Victory Field paid for by the Indianapolis Indians. The capital contributions of about $14.3 million in 2011 consist of contributions relating to the ICC expansion. The majority of this amount was classified as unearned contribution revenue in 2010 and recorded as a capital contribution in 2011 when the expansion was placed into service

24

2011 to 2010 Comparative Statements of Revenues, Expenses and Changes in Net Position

The comparative analysis below is a summary of the Statements of Revenues, Expenses and Changes in Net Position for the fiscal years ended December 31, 2011 and 2010:

2011 2010 $ Variance % Variance

Operating Revenues

Rental income $ 9,060 $ 6,313 $ 2,747 43.5%

Food service and concession commissions 4,752 3,071 1,681 54.7

Parking lot income 1,009 1,499 (490) (32.7)

Labor reimbursements 11,052 7,780 3,272 42.1

Other operating income 1,486 414 1,072 258.9

Total operating revenues 27,359 19,077 8,282 43.4

Nonoperating Revenues

Investment income 240 207 33 15.9

State and local taxes and other assistance 128,797 120,583 8,214 6.8

Other 89 92 (3) (3.3)

Total nonoperating revenues 129,126 120,882 8,244 6.8

Total revenues 156,485 139,959 16,526 11.8

Operating Expenses

Salaries and wages 12,810 10,376 2,434 23.5

Fringe benefits 3,187 2,848 339 11.9

Utilities 5,428 5,414 14 0.3

Repairs and maintenance 2,582 1,120 1,462 130.5

Insurance 1,247 1,117 130 11.6

Security 2,800 3,310 (510) (15.4)

Nondepreciable equipment, parts and supplies 4,863 4,124 739 17.9

Other 6,209 4,620 1,589 34.4

Depreciation and amortization 36,402 32,532 3,870 11.9

Total operating expenses 75,528 65,461 10,067 15.4

Nonoperating Expenses

Interest expense 48,879 48,650 229 0.5

Compensation to Visit Indy, Inc. 9,036 9,192 (156) (1.7)

Colts inducements/Revenue Sharing and Day-of-Game expenses 5,260 4,940 320 6.5

Other 1,765 - 1,765 100.0

Net nonoperating expenses 64,940 62,782 2,158 3.4

Total expenses 140,468 128,243 12,225 9.5

Income Before Capital Contributions 16,017 11,716 4,301 36.7

Capital Contributions 14,278 6,893 7,385 107.1

Increase in Net Position 30,295 18,609 11,686 62.8

Net Position, Beginning of Year 209,356 190,747 18,609 9.8

Net Position, End of Year $ 239,651 $ 209,356 $ 30,295 14.5

December 31

Note: Dollars are in thousands.

25

Total operating revenues increased about $8.3 million, or 43.4%. Rental income increased about $2.7 million, or 43.5%, food service and concession income increased about $1.7 million, or 54.7% and labor reimbursements increased about $3.3 million, or 42.1%. All of these increases were directly related to the increased size and capacity of the expanded ICC. The expansion allowed the ICC to hold larger conventions with greater headcount than in previous years. Other operating income increased about $1.1 million mainly due to reimbursements of previous utility costs related to the LOS construction and ICC expansion.

Total nonoperating revenues increased about $8.2 million, or 6.8%. State and local taxes and fees increased about $8.2 million, or 6.8%. This was the result of the 2009 Marion County Innkeeper’s Tax and the 2009 PSDA Revenue increasing about $2.7 million, as well as the Original Excise Tax revenues increasing approximately $4.9 million in 2011.

Total operating expenses increased by $10.1 million, or 15.4%. Salaries and wages increased by about $2.4 million, or 23.5%, and fringe benefits increased about $.3 million, or 11.9%, due to additional labor related to the increased operating income from new and larger events. Repairs and maintenance costs increased about $1.5 million, or 130.5%, largely due to work done to repair parking lots. Insurance costs increased about $.1 million, or 11.6%. Security costs decreased about $.5 million, or 15.4%, due to two additional Colts playoff games in January 2010 versus one in January 2011. Nondepreciable equipment, parts and supplies increased about $.7 million, or 18.0%, due to renovations at Bankers Life Fieldhouse. Other expenses increased by about $1.6 million, or 34.4%, due to an increase in advertising and promotion and labor set-up fees. Depreciation and amortization increased about $3.9 million, or 11.9%, due to the ICC expansion project being placed into service in 2011.

Total nonoperating expenses increased about $2.2 million, or 3.4%. Other nonoperating expenses increased about $1.8 million. This is a result of grants to other organizations of approximately $.7 million in 2011 which were not similarly made in 2010, as well as, approximately $1.1 million of loss on sale/disposal of capital assets, primarily related to the replacement of carpet in the ICC.

Capital contributions of about $14.3 million in 2011 consist of contributions relating to the ICC expansion. The majority of this amount was classified as unearned contribution revenue in 2010 and recorded as a capital contribution in 2011 when the expansion was placed into service. The capital contributions of about $6.9 million in 2010 were relating to the LOS construction.

26

Overall Financial Analysis

The CIB’s financial position continued to improve in 2012. As was the case in 2010 and 2011, the CIB ended 2012 with a positive net cash flow and an increase in operating cash balances. The CIB’s 2013 budget anticipates meeting 2013 expenditures with budgeted revenues and cash reserves.

Capital Asset and Debt Administration

Capital Assets

As discussed, the CIB is organized and operated to acquire, construct, lease, finance, operate, promote and publicize capital improvements and thereby serve the convention and visitor industry and the commercial, industrial and cultural interests of Indiana and its citizens. Because these assets are leased from the other governments and ownership of the assets ultimately reverts to the CIB upon expiration or termination of these leases, they are accounted for as property owned under capital leases and are depreciated along with other assets owned by the CIB. Readers are referred to footnotes 3 and 4 to the financial statements for more detailed information on capital asset activity. These capital improvements (capital assets) consist primarily of the following:

Indiana Convention Center & Lucas Oil Stadium

Among the facilities managed by the CIB is a multi-purpose sports and convention facility, the Indiana Convention Center & Lucas Oil Stadium. Over the years, the ICC has been expanded to meet the ever-growing demand for convention space in Indianapolis, the Capitol City of Indiana. As the lure of the City’s many tourist, cultural and sports attractions grows around the country, so grows the appeal of Indianapolis for convention and trade show organizers. The Indiana Convention Center & Lucas Oil Stadium hosts numerous state and national conventions, trade shows, cultural and sporting events each year, bringing millions of visitors to Indianapolis and central Indiana.

The Indiana Convention Center & Lucas Oil Stadium was constructed, expanded and improved using a mix of private and public funds, including the proceeds from a number of tax-exempt and taxable bond offerings by Marion County Convention and Recreational Facilities Authority (“MCCRFA”) and the Indiana Finance Authority (“IFA”). Lease agreements relating to these facilities secure the related bonds, along with certain state and local taxes which are used by the CIB to pay lease rentals. Such state and local taxes also secure certain bond and note indebtedness of the CIB and other lease obligations of the CIB related to other facilities.

In 2005, the CIB entered into a lease and other agreements with the Colts extending their relationship and commitment with the City of Indianapolis and setting forth the terms of their use of the CIB’s facilities. The Colts will play their home NFL games in Indianapolis through their 2034 season. The CIB is obligated to operate, maintain and insure the Indiana Convention Center & Lucas Oil Stadium at its expense.

The CIB has not adopted any planned actions that would significantly impact the planned use or life of the ICC or LOS.

27

Bankers Life Fieldhouse (formerly Conseco Fieldhouse)

Bankers Life Fieldhouse (including a connected parking facility) was completed in 1999 and is used for a variety of sporting events, concerts and other special events. The Pacers Basketball, LLC’s, a National Basketball Association franchise (the Pacers), is the exclusive operator of the facility, which operation and use occurs under its operating and financial agreements (as recently amended) with the CIB. Other frequent users include the Indiana Fever (a Women’s National Basketball Association basketball franchise).

Bankers Life Fieldhouse was built using a mix of private and public funds, including the proceeds from a 1997 tax-exempt and taxable bond offering of MCCRFA. A lease agreement (between MCCRFA, as lessor, and the CIB, as lessee) related to Bankers Life Fieldhouse secures the related bonds, along with certain state and local taxes which are committed by the CIB to pay lease rentals. The CIB is obligated to cause certain on-going capital maintenance and repair items to be undertaken, if necessary, to maintain the condition of Bankers Life Fieldhouse.

In 2010, the CIB entered into an Amendment to the Operating Agreement with the Pacers. In this amendment, the CIB agreed to provide $3.5 million dollars of capital improvements to Bankers Life Fieldhouse. The capital improvements were provided in full from 2010 through 2012.

The CIB has not adopted any planned actions that would significantly impact the planned use or life of Bankers Life Fieldhouse.

Victory Field

MCCRFA completed construction of Victory Field in 1995. Victory Field is home to the Indianapolis Indians (“Indians”), a AAA minor league baseball franchise affiliated with the Pittsburgh Pirates organization.

Victory Field was built using a mix of public and private funds, including the proceeds from a taxable bond offering of MCCRFA. A lease agreement (between MCCRFA, as lessor, and the CIB, as lessee) related to Victory Field also secures the related bonds, along with certain state and local taxes which are committed by the CIB to pay lease rentals. The CIB is obligated to cause Victory Field to be operated, maintained and insured; those obligations are undertaken by the Indians. The novelty/gift shop area at Victory Field was renovated in 2009. All renovation costs were paid for by the Indians. There are currently no commitments for additional significant construction.

The CIB has not adopted any planned actions that would significantly impact the planned use or life of Victory Field.

Long-Term Debt

The CIB’s long-term debt is comprised of capital lease obligations, bond indebtedness and note indebtedness.

The CIB has acquired certain of its existing capital assets (namely the previously existing ICC, Bankers Life Fieldhouse and Victory Field) through capital leasing arrangements involving MCCRFA and, in 2005, began acquiring other capital assets (namely LOS and an expansion of the ICC) through capital leasing arrangements involving the Indiana Office of Management and Budget (“IOMB”), the Indiana Stadium and Convention Building Authority (“ISCBA”), and the IFA (collectively and individually their interests being referred to in this discussion as “the State Leasing Entities”).

28

MCCRFA’s revenue bonds are payable solely from the respective trust estates under which they were issued and rely upon the receipt of debt service lease rentals to provide for their payment. The CIB’s lease payments to MCCRFA are funded and secured by a pledge of certain state and local tax revenues that varies depending on which debt is involved. More specific information concerning these financing and security arrangements related to CIB’s facilities can be found in footnotes 4, 5 and 7 to the financial statements.

The IFA’s revenue obligations are payable from and secured by ISCBA obligations that are supported by the ISCBA’s leases with IOMB, as lessee, who in turn receives rent under subleases with the CIB, as sublessee. The CIB’s lease payments to IOMB are funded and secured by a pledge of certain state and local tax revenues. More specific information concerning these financing and security arrangements related to CIB’s facilities can be found in footnotes 4 and 7 to the financial statements.