capital markets and portfolio theory, roland portait

TRANSCRIPT

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 1/102

Capital Markets and PortfolioTheory

Roland PortaitFrom the class notes taken by Peng Cheng

Novembre 2000

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 2/102

2

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 3/102

Table of Contents

Table of Contents

PART I Standard (One Period) Portfolio Theory . . . . . . . . . . . . . . . . . . . . . 1

1 Portfolio Choices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21.A Framework and notations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

1.A.i No Risk-free Asset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21.A.ii With Risk-free Asset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

1.B Efficient portfolio in absence of a risk-free asset . . . . . . . . . . . . . . . . . . . . . . 61.B.i Effi ciency criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61.B.ii Effi cient portfolio and risk averse investors . . . . . . . . . . . . . . . . . . . . . . . . . . . 81.B.iii Effi cient set . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91.B.iv Two funds separation (Black) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 0

1.C Efficient portfolio with a risk-free asset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111.D HARA preferences and Cass-Stiglitz 2 fund separation . . . . . . . . . . . . . . 14

1.D.i HARA (Hyperbolic Absolute Risk Aversion) . . . . . . . . . . . . . . . . . . . . . . . . 141.D.ii Cass and Stiglitz separation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 5

2 Capital Market Equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172.A CAPM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

2.A.i The Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 7

2.A.ii Geometry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 92.A.iii CAPM as a Pricing and Equilibrium Model . . . . . . . . . . . . . . . . . . . . . . . . . 192.A.iv Testing the CAPM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 1

2.B Factor Models and APT. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212.B.i K -factor models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 12.B.ii APT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 22.B.iii Arbitrage and Equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 42.B.iv References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 5

PART II Multiperiod Capital Market Theory : theProbabilistic Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

3 Framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 273.A Probability Space and Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 273 .B Asse t Pr ices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

3.B.i DeÞ nitions and Notations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 83.C Portfolio Strategies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

3.C.i Notation: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 93.C.ii Discrete Time . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 93.C.iii Continuous Time . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 0

i

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 4/102

Table of Contents

4 AoA, Attainability and Completeness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 324.A DeÞ n i t i ons . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 324.B Propositions on AoA and Completeness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

4.B.i Correspondance between Q and Π : Main Results . . . . . . . . . . . . . . . . . . . 354.B.ii Extensions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 8

5 Alternative Speci Þ cations of Asset Prices . . . . . . . . . . . . . . . . . . . . . . . . . . 395.A Ito Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 395.B Diff us ions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 405.C Diff usion state variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

5.D Theory in the Ito-Di ff usion Case . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 415.D.i Framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 15.D.ii Martingales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 2

5.D.iii Redundancy and Completeness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 25.D.iv Criteria for Recognizing a Complete Market . . . . . . . . . . . . . . . . . . . . . . . . 44

PART III State Variables Models: the PDE Approach . . . . . . . . . . . . . . . . 45

6 Framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

7 Discounting Under Uncertainty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

7.A Ito’s lemma and the Dynkin Operator . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 487.B The Feynman-Kac Theorem .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

8 The PDE Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 508.A Continuous Time APT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

8.A.i Alternative decompositions of a return . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 508.A.ii The APT Model (continuous time version) . . . . . . . . . . . . . . . . . . . . . . . . . . 51

8.B One Factor Interest Rate Models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 538.C Discounting Under Uncertainty. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

9 Links Between Probabilistic and PDE Approaches . . . . . . . . . . . . . . . 55

9.A Probability Changes and the Radon-Nikodym Derivative . . . . . . . . . . . 559.B Girsanov Theorem. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 569.C Risk Adjusted Drifts: Application of Girsanov Theorem . . . . . . . . . . . . 56

PART IV The Numeraire Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

10 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

11 Numeraire and Probability Changes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6111.AFramework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

11.A.i Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 1

ii

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 5/102

Table of Contents

11.A.ii Numeraires . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 111.B Correspondence Between Numeraires and Martingale Probabilities . 62

11.B.i Numeraire →Martingale Probabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6211.B.ii Probability →Numeraire . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 3

11.CSummary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

12 The Numeraire (Growth Optimal) Portfolio . . . . . . . . . . . . . . . . . . . . . . . 6512.ADeÞ nition and Characterization ... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

12.A.i DeÞ nition of the Numeraire (h , H ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 512.A.ii Characterization and Composition of (h , H ) . . . . . . . . . . . . . . . . . . . . . . . . 6512.A.iii The Numeraire Portfolio and Radon-Nikodym Derivatives . . . . . . . . . . . . 69

12.B First Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6912.B.i CAPM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 012.B.ii Valuation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 0

PART V Continuous Time Portfolio Optimization . . . . . . . . . . . . . . . . . . . . 72

13 Dynamic Consumption and Portfolio Choices (The MertonModel) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7313.AFramework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

13.A.i The Capital Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 313.A.ii The Investors (Consumers)’ Problem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 4

13.B The Solution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7413.B.i Sketch of the Method . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 413.B.ii Optimal portfolios and L + 2 funds separation . . . . . . . . . . . . . . . . . . . . . . 7713.B.iii Intertemporal CAPM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 8

14 THE ”EQUIVALENT” STATIC PROBLEM (Cox-Huang,Karatzas approach) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8014.ATransforming the dynamic into a static problem . . . . . . . . . . . . . . . . . . . . 80

14.A.i The pure portfolio problem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 014.A.ii The consumption-portfolio problem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 2

14.BThe solution in the case of complete markets. . . . . . . . . . . . . . . . . . . . . . . . 8314.B.i Solution of the pure portfolio problem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8314.B.ii Examples of speci Þ c utility functions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 514.B.iii Solution of the consumption-portfolio problem . . . . . . . . . . . . . . . . . . . . . . 8614.B.iv General method for obtaining the optimal strategy x∗∗ . . . . . . . . . . . . . . . 87

14.CEquilibrium: the consumption based CAPM . . . . . . . . . . . . . . . . . . . . . . . . 88

PART VI STRATEGIC ASSET ALLOCATION . . . . . . . . . . . . . . . . . . . . . . . 90

15 The problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

16 The optimal terminal wealth in the CRRA, mean-variance

iii

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 6/102

Table of Contents

and HARA cases . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9216.A Optimal wealth and strong 2 fund separation....................... 9216.B The minimum norm return . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

17 Optimal dynamic strategies for HARA utilities in two cases . . . . 9317.A The GBM case . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9317.B Vasicek stochastic rates with stock trading . . . . . . . . . . . . . . . . . . . . . . . . . 93

18 Assessing the theoretical grounds of the popular advice . . . . . . . . . 9418.AThe bond/stock allocation puzzle . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9418.B The conventional wisdom. .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

REFERENCES 95

iv

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 7/102

PART IStandard (One Period)

Portfolio Theory

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 8/102

Chapter 1 Portfolio Choices

Chapter 1Portfolio Choices

1.A Framework and notations

In all the following we consider a single period or time interval (0 1), hence twoinstants t = 0 and t = 1

Consider an asset whose price is S (t) (no dividends or dividends reinvested).The return of this asset between two points in time (t = 0 , 1) is:

R =S (1) −S (0)

S (0)

We now consider the case of a portfolio. and distinguish the case where ariskless asset does not exist from the case where a risk free asset is traded.

1.A.i No Risk-free Asset

There are N tradable risky assets noted i = 1 ,...,N :

• The price of asset i is S i (t), t = 0 , 1.

• The return of asset i is

R i =S i (1) −S i (0)

S i (0)

2

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 9/102

Chapter 1 Portfolio Choices

• The number of units of asset i in the portfolio is n i . The portfolio is describedby the vector n (t); n i can be > 0 (long position) or < 0 (short position).

• Then the value of the portfolio, denoted by X (t), is

X (t) = n 0 · S (t )

with n (0) = n (1) = n (no revision between 0 and 1), the prime denotes atranspose. S (t ) stands for the column vector (S 1(t),...,S N (t))0

• The return of the portfolio is:

RX =X (1) −X (0)

X (0)

• Portfolio X can also be de Þ ned by weights, i.e.

xi (0) = xi =n i S (0)X (0)

(Note that xi (1) 6= x i ). Besides the weights sum up to one:

x 0 · 1=1

where x= ( x1, x2,...,x N )0 and 1 is the unit vector .

• The return of the portfolio is the weighted average of the returns of itscomponents:

RX = x 0R

3

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 10/102

Chapter 1 Portfolio Choices

Proof

1 + RX =X (1 )X (0)

=n 0S (1 )X (0)

=N

Xi = 1

n i S i (1 )X (0)

·S i (0)S i (0)

=N

Xi = 1

xi ·S i (1 )S i (0)

=N

Xi = 1

xi · (1 + R i )

= 1 +N

Xi = 1

xi R i

Q.E.D.

• DeÞ ne µi = E [R i] and µ = ( µ1, µ2,...,µ N )0

, then:

µX = E (RX ) = x 0µ

• Denote the variance-covariance matrix of returns Γ N × N = ( σ ij ), whereσ ij = cov (R i , R j ), then:

var (RX ) = var (x 0R )= x0Γ x

=N

Xi=1

N

X j =1

xix j σ ij

1.A.ii With Risk-free Asset

We now have N +1 assets, with asset 0 being the risk-free asset, and the remainingN assets being the risky assets.

4

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 11/102

Chapter 1 Portfolio Choices

• S 0 (1) = S 0 (0) · (1 + r ) with r a deterministic interest rate.

• Again we can de Þ ne the portfolio in units, with n = ( n0, n 1, n 2,...,n N )0

• The portfolio can be similarly de Þ ned in weights:

x i =n iS (0)X (0)

for the N risky assets (i = 1 , 2,...,N ), and

x0 = 1 −N

Xi=1

x i

Note that now

x 0 · 1 6= 1

where x= ( x1, x2,...,x N )0 denotes the weights in the N risky assets.

• The return of the portfolio is:

RX = x0r +N

Xi=1

x i R i = r +N

Xi=1

xi (R i −r )

The term (R i −r ) is the excess return of asset i over r . Moreover:

µX = E (RX ) = r + x 0π

where π is the risk premium vector of the E (R i −r )

• Also denote Γ N × N as the variance-covariance matrix of the risky assets, then:

var (RX ) = x 0Γ x

Γ is always positive semi-de Þ nite (meaning that ∀x , x 0Γ x ≥0). In some casesit is positive de Þ nite (

∀

x 6= 0 , x 0Γ x > 0).

De Þ nition 1 Assets i = 1 , 2,...,N are redundant if there exist N scalars λ 1 , λ 2 ,..., λ N such that PN

i = 1 λ i R i = k, where k is a constant. Then the portfolio λ is risk-free.

Proposition 1The N assets i = 1 , 2,...,N are not redundant iff Γ is positive de Þ nite (i.e. non-singular or invertible).

5

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 12/102

Chapter 1 Portfolio Choices

Proof

Assume that the assets are redundant, then there exist N scalars λ 1 , λ 2 ,..., λ N such that

PN i = 1 λ i R i = k. Consider the portfolio de Þ ned by the weights λ . The variance of its return =

var (k) = 0 = λ 0Γ λ , i.e. Γ is singular and not positive de Þ nite. Conversely if Γ is singular and not positive de Þ nite there exist a non 0 vector λ such that λ 0Γ λ = 0 ; Then the return of portfolio λ has zero variance and PN

i = 1 λ i R i = k

Q.E.D.

Remark 1 In the following sections we will assume that the assets are non-redundant (it is

always possible to “drop” redundant assets if any).

1.B E ffi cient portfolio in absence of a risk-free asset

1.B.i E ffi ciency criteria

De Þ nition 2 Portfolio (x∗, X ∗) is e ffi cient if ∀y , σY < σX ∗

⇒µY < µ X ∗ and σ Y =σ X ∗

⇒µY ≤µX ∗

Consider any e fficient portfolio ( x∗, X ∗) and let variance (RX ) = kx∗ solves the optimization program (P ) :

maxx

E [RX ] s.t. x 0Γ x = k ; x 01 = 1

The Lagrangian is:

Lµx ,θ2 , λ¶= x0µ −

θ2x0Γ x −λ x 01

The Þ rst order condition ¡∂ L∂ x = 0¢writes:

µ −θ Γ x∗−λ 1 = 0

or equivalently, for i = 1 , . . ,N :

µi = λ + θN

X j =1

x∗ j σ ij

6

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 13/102

Chapter 1 Portfolio Choices

Remark that these Þ rst order conditions are necessary and also su fficient for thesolution being a maximum since the second order conditions hold ( L(x ) is strictlyconcave -Γ positive de Þ nite).

Theorem 1A portfolio (x , X ) is e ffi cient iff there exist two scalars λ and θ such that for all i = 1 , 2,...,N :

µi = λ + θ · cov (Rx , R i )

Proof

The necessary and su ffi cient condition for x to be e ffi cient is that it satis Þ es the Þ rst order condition: for all i: µi = λ + θP

N j = 1 x∗j σ ij . We then have:

µi = λ + θN

Xj = 1

x∗j cov (R i , R j )

= λ + θ · cov R i,

N

Xj = 1

x∗j R j

= λ + θcov (R i , RX )

Q.E.D.

Remark 2 The second term can be considered as the additional required rate of return (risk premium), proportional to cov (R i , RX ).

Remark 3 If cov (R i , RX ) = 0 , then µi = λ .

Remark 4 Also note:

var (RX ) =N

Xi = 1

N

Xj = 1

x i x j σ ij

=N

Xi = 1x i · cov R i ,

N

Xj = 1xj R j

=N

Xi = 1

x i · cov (R i , R X )

The covariance term cov (R i , RX ) indicates the contribution of asset i to the total risk of the portfolio. Therefore, additional required rate of return should be proportional to this induced risk which is what is stated in the theorem. Moreover cov (R i , RX ) appears to be the relevant measure of risk for any asset i embedded in the portfolio X.

7

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 14/102

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 15/102

Chapter 1 Portfolio Choices

1.B.iii E ffi cient set

De Þ nition 3 The E ffi cient Set is the set of all x ∗ that obey the Þ rst order condition. Equiv-alently, it is the set of all x ∗ that solve the optimization program (P 0) ∀θ ≥0.

Recall that the Þ rst order condition for (P 0) is:

µ −θ Γ x∗−λ 1 = 0

DeÞ ne risk tolerance

bθ as the inverse of risk aversion, i.e.

bθ =1θ

Then x∗ can be solved as:

x∗ = bθΓ − 1¡µ −λ 1¢To Þ nd λ , use the constraint 10x∗ = 1 , i.e.

1 = 10x∗

= 10

· bθΓ − 1

¡µ −λ 1¢Then:

bθ10Γ − 1µ − bθλ 10Γ − 1 1 = 1

or:

bθ10Γ − 1µ − bθλ 10Γ − 1 1 = bθθ

This solves for λ :

λ =10Γ − 1µ

−θ

10Γ − 11

Then:

x∗ = bθΓ − 1¡µ −λ 1¢= bθΓ − 1µµ −

10Γ − 1µ −θ

10Γ − 1 1·1¶

=Γ − 11

10Γ − 11+

bθΓ − 1µµ −

10Γ − 1µ

10Γ − 1 1·1¶

9

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 16/102

Chapter 1 Portfolio Choices

We recognize in the Þ rst term the minimum variance portfolio ( k1) and we callk 2 the second term:

k1 =Γ − 11

10Γ − 11

k2 = Γ − 1·µ −10Γ − 1

µ

10Γ − 1 1·1¸

Then the solution of (P ) writes:

x∗ = k 1 +

bθk 2

Note that k 011 = 1 and x∗01 = 1 , therefore k 021 = 0 . Any efficient portfolio is thusthe sum of k 1 (the minimum variance portfolio) and k 2 which is a zero weight(zero investment) portfolio. As it could be expected, an investor with a zero risktolerance will hold only k 1; If he has a positive risk tolerance bθ he will add a risktaking the form bθk2 in order to increase the expected return. The e ffi cient set cannow be caracterized as:

ES = nx∗|x∗ = k1 + bθk 2 ∀ bθ > 0oSince the expected return x∗0µ is linear in

bθ and the variance is quadratic in

bθ, in

the (σ2, R ) space the effi cient portfolios are represented by the e fficient frontier,which is a parabola. Each point on the e fficient frontier corresponds to a given θ,the slope of the parabola at this point being equal to θ

2 (the shadow price in (P )of the constraint on variance).

In the (σ , R ) space the efficient frontier is an hyperbola.

1.B.iv Two funds separation (Black)

Theorem 2Consider any two e ffi cient portfolio x and y :

1. Any convex combination of x and y is effi cient, i.e.∀u∈[0, 1] , ux+ (1 −u) y∈ES

2. Any efficient portfolio is a combination of x and y (not necessarily a convexcombination)

3. The whole parabola (e fficient and ine ffi cient frontier) is generated by (all)combinations of x and y

10

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 17/102

Chapter 1 Portfolio Choices

Proof

• Since x∈ES and y∈ES , for some positive bθX and bθY , we have:

x = k 1 + bθX k 2

y = k 1 + bθY k 2

Let z = ux + (1 −u)y , then:

z = [uk1 + (1

−u) k 1] +

hu

bθX + (1

−u)

bθY

ik 2

= k 1 + bθZ k 2

With bθZ > 0, we can conclude that z∈ES.

• Let z∈ES , then z = k1 + bθZ k2 for some bθZ > 0. For any x

∈ES andy∈ES :

ux + (1 −u) y = k 1 + hu bθX + (1 −u) bθY ik2

By equating

bθZ to u

bθX + (1

−u)

bθY we get:

u∗ = bθZ − bθY

bθX − bθY

Then the combination u∗x + (1 −u∗) y = z

Q.E.D.

1.C E ffi cient portfolio with a risk-free asset

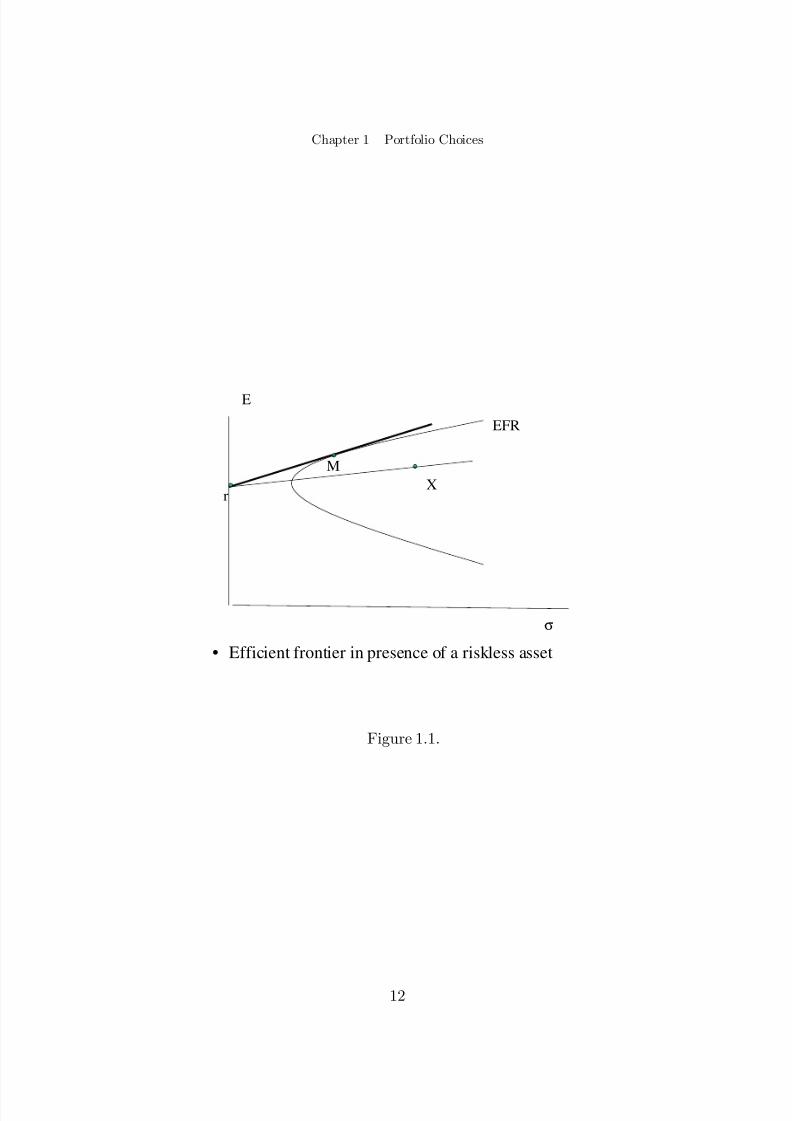

Consider Þ gure 1 where the upper branch of the hyperbola EFR represents, in the(σ , E ) space, the efficient portfolios in absence of a riskless asset. Assume now thatexists a risk free asset 0 yielding the certain return r. M stands for the tangencypoint of the hyperbola EFR with a straight line drown from r representing asset 0.Point M represents a portfolio composed only of risky assets, called the tangentportfolio.

11

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 18/102

Chapter 1 Portfolio Choices

• Efficient frontier in presence of a riskless asset

σ

E

r

MX

EFR

Figure 1.1.

12

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 19/102

Chapter 1 Portfolio Choices

Proposition 2

1. Asset 0 is efficient2. Consider any portfolio X . Any combination of 0 and X yielding

R = uR X + (1 −u) r , lies on the straight line connecting 0 and X in the ( σ , E )space

3. Any feasible portfolio which representative point is not on r −M (such as X )is dominated by portfolios in r −M. The straight line r −M is the effi cientfrontier and is called the Capital Market Line

4. (Tobin’s Two-fund Separation ) Any effi cient portfolio is a combination of anytwo efficient portfolios, for instance 0 and M

5. Any efficient portfolio writes:

x∗ = bθΓ − 1¡µ −r 1¢6. The tangent portfolio (m ,M ) is:

m = bθM Γ− 1¡µ −r 1¢

bθM =1

10Γ − 1¡µ −r 1¢Proof

1, 2, 3, 4 are standard and easy to prove. Let us proove 5 and 6: x∗

∈ES solves:

max 1r + x∗0¡µ −r 1¢−θ2

x∗0Γ x∗

The Þ rst order condition is:

µ −r 1 = θ Γ x∗

Then:

x∗ =1

θΓ − 1

¡µ −r 1¢= bθΓ − 1¡µ −r 1¢The tangent portfolio is an e ffi cient portfolio, therefore, m = bθM Γ − 1 ¡µ −r1¢. Also: m 01 = 1 ,then:

bθM =1

10Γ − 1¡µ −r 1¢Q.E.D.

13

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 20/102

Chapter 1 Portfolio Choices

Remark 5 Given a risk tolerance

bθ:

• bθ < bθM , the portfolio is long in 0 and m

• bθ > bθM , the portfolio shorts 0

Remark 6 We de Þ ne later the market portfolio as a portfolio containing all the risky assets present in the market (and only risky assets). In absence of riskless asset the market portfolio is e ffi cient iif its representative point belongs to the hyperbola EFR. In presence of a risk free asset the necessary and su ffi cient condition for the market portfolio to be e ffi cient is that it coincides with the tangent portfolio m (which is the only e ffi cient portfolio of EFR, in presence of a risk free asset). Would all investors face the same e ffi cient frontier (it would be the case under

homogeneous expectations and horizon) and would they all follow the mean-variance criteria,they would all hold combinations of 0 and M and the tangent portfolio M would necessarily coincide with the market portfolio.

1.D HARA preferences and Cass-Stiglitz 2 fund separation

A rational agent (in the sense of Von Neumann-Morgenstern) should maximizethe expected utility of wealth E [U (W )].

1.D.i HARA (Hyperbolic Absolute Risk Aversion)

A utility function U (W ) belongs to HARA class if it writes:

U (W ) =γ

1 −γ · bθ +W γ ¸1− γ

Some restrictions are imposed on the coe fficients γ and

bθ and the domain of

deÞ nition.

The absolute risk tolerance (ART) and absolute risk aversion (ARA) are:

ART =1

ARA

= −U 0

U 00

=

bθ +

W γ

14

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 21/102

Chapter 1 Portfolio Choices

and the relative risk tolerance (RRT) is:

RRT = bθW +

1γ

In particular:

1. bθ = 0 ⇒U (W ) =

W 1− γ

1 −γ

We obtain CRRA, i.e. constant relative risk aversion.A limit case of CRRA is obtained for γ = 1 which can be showed to beequivalent to the Log utility

2. γ = −1⇒

U (W ) = W −W 2

2 bθi.e. the quadratic utility function.

3. Using a quadratic utility function implies a mean-variance criteria; Indeed:

min var (RX ) s.t. E [RX ] = bE (and x 01 = 1)

⇔min E [R2X ] s.t. E [RX ] = bE (and x 01 = 1)

⇔min E [X 2 (1)] s.t. E [X (1)] = X (0) ·h1 + bE i⇔min E [X 2 (1)] −λE [X (1)]

⇔max E £X (1) − 1λ X 2 (1)¤4. Three undesirable features of the quadratic utility:

— Saturation at W = bθ (for that wealth U (W ) = W −W 2

2 bθis maximum; U (W ) decreases

for W >

bθ!)

— ARA increasing with wealth (it is commonly admitted that ARA decreases for most agents).

— Indi ff erence to skewness (only the two Þ rst moments of W matter), whereas most investors actually like skewness.

1.D.ii Cass and Stiglitz separation

Cass and Stiglitz showed that all HARA investors sharing the same exponential

15

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 22/102

Chapter 1 Portfolio Choices

parameter γ can build their optimal portfolios by mixing the two same funds.When a risk free asset exists it can be chosen as one of the two funds. Since allquadratic (mean-variance) investors exhibit the same γ (= −1) Tobin and Black2 fund separation are particular cases of Cass and Stiglitz separation. Cass andStiglitz conditions on the utility functions for separation to hold for investorssharing the same exponential parameter are summarized in the following table

Complete Market Incomplete Market @r (under complete markets ∃r ) quadratic or CRRA 2

∃r class wider than HARA HARA

2 in the particular case of CRRA one fund su ffi ces (for a given γ the portfolio is the same for all W

16

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 23/102

Chapter 2 Capital Market Equilibrium

Chapter 2Capital Market Equilibrium

2.A CAPM

2.A.i The Model

Consider again N risky assets (a risk free asset may exist or not). The marketvalue of asset i is V i , then (by de Þ nition of the market portfolio) it’s weight in themarket portfolio is:

m i =V i

PN i=1 V i

The return of the market portfolio is:

RM = m0

R

Hypothesis 1 (H ) : The market portfolio M is e ffi cient.

Remark 7 The market portfolio would be e ffi cient if all investors would hold e ffi cient port- folios (since a combination of e ffi cient portfolios is e ffi cient).

Theorem 3(General CAPM )

1. If (H ) is true, then there exist θ and λ such that, for i = 1 ,...,N :

µi = E [R i ]= λ + θcov (RM , R i )

2. Conversely, if there exist θ and λ such that, for i = 1 ,...,N : µi =λ + θcov (RM , R i), then (H ) is true.

17

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 24/102

Chapter 2 Capital Market Equilibrium

Proof

The proof comes directly from Theorem 1.

Q.E.D.

Remark 8 θ can be interpreted as the risk aversion of the average (representative) investor.

Remark 9 CAPM holds for any portfolio ( x , X ).

Indeed, call RX its return and consider the case where no risk free asset exists(x01 = 1) :

E [RX ] =N

Xi=1

xi µi

=N

Xi=1

xi (λ + θcov (RM , R i ))

=N

Xi=1

xi λ + θN

Xi=1

x i cov (RM , R i)

= λ + θcovÃRM ,

N

Xi=1x iR i

!= λ + θcov (RM , R X )

Remark 10 The proof follows the same lines when the portfolio contains a risk free asset with weight x0

Remark 11 λ and θ are the same for all assets or portfolios

Remark 12 For the market portfolio:

µM = λ + θcov (RM , RM )= λ + θσ 2

M

Therefore:

θ =µM −λ

σ 2M

Then:

µi = λ + θcov (RM , R i )

= λ + ·µM −λσ 2

M ¸cov (RM , R i )

18

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 25/102

Chapter 2 Capital Market Equilibrium

De Þ ne:

β i =cov (RM , R i )

σ 2M

Then we may write the CAPM equation in the alternative form:

E [R i ] = λ + β i (µM −λ )

Consider any portfolio z with β Z = 0 :

β Z = 0

⇔ cov (RM , RZ ) = 0

⇔ cov (m0

R , z0

R ) = z0Γ m = 0

⇐⇒z⊥Γ m

⇔ z∈[vect (Γ m )]⊥

vect [v 1, v 2, ..., v N ] is the set of all linear combinations of v 1, v 2, ..., v N , or linearsubspace generated by v 1, v 2, ..., v N . The dimension of [vect (Γ m )]⊥ is thus N −1and there are an in Þ nity of 0-beta portfolios. Now, from the general CAPM, wewould have: λ = µZ ; Thus:

Corollary 1 ( 0−beta CAPM) If M is e ffi cient, for any zero beta portfolio or asset Z : E [R i ] =µZ + β i (µM

−µZ )

Corollary 2 (Standard CAPM ) : If there exists a risk-free asset yielding r (which is a par-ticular zero beta asset)

E [R i ] = r + β i (µM −r )

Note that µZ = r for any zero beta portfolio or asset.

2.A.ii Geometry

missing

2.A.iii CAPM as a Pricing and Equilibrium Model

• For a security delivering eV (1) at time 1(the pdf of eV (1) is given, thusE (

eV (1)) and cov(

eV (1) , RM ) are known), what is its price V (0) at time 0?

19

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 26/102

Chapter 2 Capital Market Equilibrium

Let’s assume that there exists a risk-free asset, then:

E heV (1)iV (0)= E [1 + R] = 1 + r + θcovÃeV (1)

V (0), R M !

with

θ =µM −r

σ2M

Then:

E heV (1)i= (1 + r ) V (0) + θcov³eV (1) , RM

´and

V (0) =E heV (1)i−θcov³eV (1) , R M ´1 + r

i.e. V (0) is the present value of its certainty equivalent at time 1 discountedat the risk-free rate.However this asset may be an element of the market portfolio M (unless thisclaim is in zero net supply ..) and therefore the previous pricing formula isnot a closed form general equilibrium relation.

• In fact CAPM is an equilibrium condition stemming from the demand side;The equilibrium price can only be otained by specifying the supply side (inthe previous example the supply was a right on an exogeneous cash ß ow X ).General equilibrium requires a speci Þ cation of the supply of all securitiestraded in the market.

— Consider the N risky assets together and we look for their equilibrium prices. We assume Þ rst an inelastic supply. Assume that asset i delivers

eV i (1 ), an exogenous cash

ß ow, at time 1 , what is its price at time 0?

E heV i (1 )iV i (0)= 1 + r + ·µM −r

σ 2M ¸covÃeV i (1 )

V i (0), RM !

For i = 1 , 2,...,N . We have N equations with N unknowns V i (0) ( i = 1 ,...,N ).( 1 + RM = PN

i = 1 eV i (1)

PN i = 1 V i (0) allows to compute µM , σ 2

M ,cov³eV i (1)V i (0) , R M ´as functions of the

V i (0))

— Consider again the N risky assets and an elastic supply with constant returns to scale,where the joint pdf of the R i is given and independent of the scale V i (0) to be invested in ”technology i”. The CAPM determines the scale V i (0) of investment in technology i

20

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 27/102

Chapter 2 Capital Market Equilibrium

by the equations:

µi = E [R i ] = r + ·µM −rσ2

M ¸cov (RM , R i )

and

1 + RM = PN i = 1 V i (0) · (1 + R i )

PN i = 1 V i (0)

2.A.iv Testing the CAPM

One remark about this important empirical topic.Testing the CAPM is equivalent to testing (H ). However, how should we de Þ nethe market portfolio and how to measure the market return?Usually the market portfolio is proxied by stock (plus bond) indices. But resultson stock indices do not include all assets in M (non tradable assets, art,..). Hencewe test the e fficiency of the index and not that of M (Roll’s Critique).

2.B Factor Models and APT

2.B.i K -factor models

Hypothesis 2 There exist K factors, F k , k = 1 , 2,...K with

1. F i⊥F j

2. E [F k ] = 0

3. var (F k ) = σ2k

such that for i = 1 , 2,...,N :

R i = µi +K

Xk = 1

β ik F k + ² i

where E [² i ] = 0 and ² i ⊥² j ⊥F k . In vector form:

R N × 1 = µ + β N × K F K × 1 + ² = µ +K

Xk = 1

β 0k F k + ²

21

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 28/102

Chapter 2 Capital Market Equilibrium

with β k being the kth row of β .

• In practice, we should have large N and small K , so that in estimating thevariance-covariance matrix,

cov (R i , R j ) =K

Xk =1

β ik β jk σ2k

we only need to estimate K terms of σ2k and run N regressions for estimating

the β ik

.

• In CAPM or in the Markowitz model, without the factor decomposition, weneed to estimate N (N −1) / 2 terms.

• A Particular case: K = 1 boils down into the market model that writes:

R i = µi + β iF + ² i

Then:

RM =N

Xi=1

m i µi + F N

Xi=1

m i β i +N

Xi=1

m i ² i

= µM + F

Since the innovation terms diversify and β M = PN i=1 m i β i = 1 :

F = RM −µM

and

R i = µi + β i [RM −µM ] + ² i

Note that the R i are linked through [RM −µM ] (since cov (R i , R j ) = β i β j σ2M ).Also, β i [RM −µM ] is the systematic risk, and ² i is the unsystematic (diversi Þ able)risk; only systematic risk should be priced (CAPM).

2.B.ii APT

We assume that the returns are generated by a K factors linear process previouslydeÞ ned that writes:

22

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 29/102

Chapter 2 Capital Market Equilibrium

R = µ + + β F + ² = µ +K

Xk =1

βkF k + ²

Recall that βk

is an N dimensioned column vector with an i th component equalto β ik

De Þ nition 4 A zero investment portfolio, de Þ ned by the amount of wealth, x , invested in each asset, satis Þ es:

x 01 = 0

V (0) = 0V (1 ) = x 0R

The last equation can be veri Þ ed since:

V (1) =N

Xi=1

xi (1 + R i ) =N

Xi=1

xi +N

Xi=1

x iR i = x 0R

De Þ nition 5 An arbitrage portfolio is a zero investment portfolio with x 0R ≥ 0 almost

surely and E [x0R ] > 0.Absence of arbitrage (AOA) prevails if no arbitrage portfolio can be constructedi.e:x01 = 0 and x0R ≥0 a.s. implies x0R = 0 a.s. (or equivalently implies E (x0R ) =0)

Theorem 4(APT ) In AoA there exist K + 1 scalars such that:

µ = λ 0 1 + λ 1β1 + ... + λ K β K

or µi = λ 0 + λ 1 β i 1 + ... + λ K β iK

• λ 0 is the required rate of return without systematic risk.

• λ k is the market price of risk k.

• λ k β ik is the risk premium imposed to security i because it has a risk k of intensity β ik .

23

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 30/102

Chapter 2 Capital Market Equilibrium

Proof

Consider any well-diversi Þ ed zero investment portfolio satisfying:

x 01 = 0 or x⊥1x0β k = 0 or x⊥

βk for k = 1 ,...,K

hence:

x is any element of hvect³1 ,β 1 , β2 ,..., β

K ´i⊥Also x0² = 0 (since it is well diversi Þ ed); Then:

RX = x 0R

= x 0µ +

K

Xk = 1

F k x 0βk + x 0

²

= x 0µ

Since x 0µ is certain, in AoA x 0µ must be zero (if x 0µ > 0 then x is an arbitrage portfolioand if x 0µ < 0 then −x is an arbitrage portfolio). Thus: x0µ = 0 or x⊥µ , which means that µ is orthogonal to any element x of [vect(1 , β 1 , β 2 ,..., β K )]

⊥ , i.e.

µ∈vect(1 , β 1 , β 2 ,..., β K )

implying that exist K + 1 scalars such that : µ = λ 0 1 + λ 1β 1 + ... + λ K β K

Q.E.D.

• In the particular case where there is a risk-free asset, then:

µ0 = λ 0 = r

and

µi = r + λ 1β i1 + ... + λ K β iK

2.B.iii Arbitrage and Equilibrium

• Equilibrium implies AoA, but the inverse is not true.

• AoA conditions do not involve utility functions.

24

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 31/102

Chapter 2 Capital Market Equilibrium

2.B.iv References

Dumas-Allaz, 1995 ; Demange-Rochet, 1992.

25

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 32/102

PART IIMultiperiod CapitalMarket Theory : the

Probabilistic Approach

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 33/102

Chapter 3 Framework

Chapter 3Framework

3.A Probability Space and Information

We consider the usual probability triplet (Ω , F , P ), where F is a σ-algebra on Ω

representing the observable events at time T .

Information in the period [0, T ] is represented by a Þ ltration F t t∈[0,T ], where F tis the set of observable events at time t (represented by a σ−algebra), and thesequence F t t∈[0,T ] satis Þ es the ”usual” conditions:

F 0 = null events and a.s. event (s < t ) ⇔ (F s⊂F t )

F T = F F s = \t>s

F t

In the discrete time setting, all transactions take place at discrete points, i.e.,t = 1 , 2,...,T . In the continuous time setting, transactions take place continuously,i.e., t∈[0, T ].

We assume a frictionless market, continuously open in the continuous time frame-work.

27

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 34/102

Chapter 3 Framework

3.B Asset Prices

3.B.i De Þ nitions and Notations

There are N + 1 assets traded in the market, one being the locally risk-free as-set, denoted by 0, and the remaining N being the risky assets. The prices of those assets are noted S i (t) ( for i = 0 , 1,...,N ); S(t) = ( S 1(t), . . ,S N (t))0 or(S 0(t), S 1(t), . . ,S N (t))0 (depending on the context) is the N (or N + 1 ) dimen-

sional column vector of asset prices. Without loss of generality it will generallybe assumed that S i (0) = 1It is assumed for the time being that there is no dividend, or that a dividend isreinvested in the asset that delivers it.1. In the discrete time case S 0(t) = S 0(t −1)[1 + r (t −1)], with r (t −1) beingthe locally risk-free rate in [t −1, t] , known at time t −1 but unknown before.Remark that S 0(t + 1) = S 0(t)(1+ r (t)) is random at t −1 since r (t) is unknown.2. In the continuous time context:

• r (t) is stochastic but F t -adapted.

For a risk-free asset:

dS 0 = S 0rdt

or

S 0 (t) = eR t0 r (u )du

with S 0 (0) = 1 .

• For a risky asset we will usually assume that prices follow Ito processes:dS i = S i µidt + S i σ i

0dw

with risk induced by w , the vector of standard Brownian Motions.

Technical conditions (e.g., the integrability conditions) apply.If S i follows Ito process, we preclude jumps. If jumps are involved, however, thena rather general assumtion is that S i follows a semi-martingale process. A slightlymore speci Þ c assumption is that asset prices follow processes that yield a.s. RightContinuous and Left Limited (RCLL) paths. When considering the possibility of

28

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 35/102

Chapter 3 Framework

jumps we will assume RCLL processes for the asset prices to avoid the so Þ sticationof semi martingales 3.

• It is worthwhile to note that Ito processes ⊂RCLL ⊂Semi −martingales .

• Most of the results of the next chapter (On AOA and completeness) hold inthe semi-martingale case.

3.C Portfolio Strategies

3.C.i Notation:

• n (N +1) × 1 the vector of the N+1 numbers of assets ; xN × 1 the vector of N weights on risky assets

• S (N +1) × 1 the vector of the N+1 asset prices

• X (t) = n 0(t)S(t) the value of the portfolio at t

• (n ,X ) or (x ,X ) a strategy

3.C.ii Discrete Time

[t −1, t[ is period t −1;at time t S (t) is set and, just after, n(t) is choosen

• During period t −1, the value of the portfolio will evolve:X (t) −X (t −1) = n 0(t)S(t)−n 0(t −1)S(t −1)

= n 0(t −1) [S(t) −S(t−1)] + S0(t) [n (t) −n (t −1)]

The Þ rst term in the right hand side of the equation, n 0(t −1) [S(t) −S(t−1)], isthe gain during the period [t −1, t[ , and is represented as g(t −1, t).3 Consider the integral: R φ (u ) dS . In a regular integral of this form dS is inÞ nitesmal, while in a

jump process it can assume some Þ nite value somewhere.

29

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 36/102

Chapter 3 Framework

The second term can be deemed as the net cash in ß ow added to the portfolio attime t. Indeed it can be decomposed into two terms: −S0(t)n (t −1), the value of assets sold at time t, and S0(t)n (t), the algebric value of assets purchased (maybe < 0 if sales> purchases).

• The cumulative gain in [0, t], deÞ ned for t = 1 ,...,T , can be represented as:

G(t) =t

Xu =1

g(u −1, 1)

De Þ nition 6 (Self- Þ nancing Portfolio ) When at each time t the net in ß ow is 0, the strategy is said to be self- Þ nancing, i.e., if (n ,X ) is self- Þ nancing, then:

X (t) −X (t −1 ) = g(t −1 , t ) = n 0(t −1 ) [S (t) −S(t−1)]

and

X (t) = X (0) + G(t)

• Let S i (t) be the value of asset i at time t, and S 0(t) be the numeraire, thenthe discounted value of i is:

S di =S i (t)S 0(t)

• Self-Þ nancing is independent of the numeraire used; In particular (n ,X )self-Þ nancing implies:

X d(t) −X d (t −1) = n 0(t −1)£Sd (t) −S d (t −1)¤3.C.iii Continuous Time

• The gain process in [t, t + dt) is deÞ ned as:

dG(t) = n 0(t)dS(t)

and

G(t) = Z t

0dG(u) = Z t

0n 0(u)dS(u)

30

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 37/102

Chapter 3 Framework

• The change of the portfolio value is found to be:

dX = d (n 0(t)dS(t))= n 0(t)dS(t)+ S0(t)dn 0(t)+ dn 0(t)dS(t)= n 0(t)dS(t)+ dn 0(t) [S(t)+ dS(t)]

with the Þ rst term in the right hand side of the equation being the period gaindG(t) and the second term the net in ß ow at t + dt.

• Again, in a self- Þ nancing strategy: dX (t) = dG(t), and X (t) = X (0) + G(t);As in the discrete time case, the self Þ nancing property as well as theexpression of the gain do not depend on the choosen numeraire .

31

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 38/102

Chapter 4 AoA, Attainability and Completeness

Chapter 4AoA, Attainability andCompleteness

4.A De Þ nitions

De Þ nition 7 strategy (n ,X ) is admissible if:

1. n (t) is F t adapted and satis Þ es some technical conditions 4.

2. X (t)∈L1,2.

3. (This is an additional condition imposed sometimes) X (t) is bounded frombelow to avoid doubling Strategies 5 .

De Þ nition 8 A is the set of admissible strategies

De Þ nition 9 A0 = Self- Þ nancing and admissible strategies

We now work with A0, i.e., ∀(n ,X )∈A0, dX = n 0dS .4 Technical conditions on n ( t ) :

, when asset prices follow RCLL processes(a) G(t) = R t

0 n 0(u)dS(u) must be de Þ ned for S(t)∼RCLL

(b) (Integrability )

i.

R t

0 kn 0(u)k2 du< ∞a.s.

ii. R t

0 |n0(u)| du< ∞a.s.

(c) (predictability of n (t))n (t)∼LCRL so that if there is a jump in S(t), rebalancing must takeplace in t+ but never in t− , the latter being equivalent to insider trading,i.e., a rebalancing, or jump, in n (t) takes the advantage of a jump in S(t)that has just occured. This condition is not necessary when S(t) iscontinuous.

5 In a Doubling Strategy the gambler bets 2 when losing 1 and bets 4 when losing 2...

32

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 39/102

Chapter 4 AoA, Attainability and Completeness

It is also possible to de Þ ne a strategy by a vector of weights x N × 1. The weight of the risk-free asset in the portfolio is then 1 −x01 .

De Þ nition 10 (a ,A) is an arbitrage if:

1. (a ,A)∈A0.

2. A(0) = n 0(0)S(0) =0 , (i.e., zero initial investment).

3. A(T ) ≥0 a.s. (i.e., non-negative cash ß ow at the end).

4. E [A(T )|F 0] > 0

There is an arbitrage opportunity each time that a strategy (x, X ) in A0 dominatesanother strategy (y, Y ) in A0 (i.e. X (T ) ≥Y (T ) a.s. and E [X (T )] ≥E [Y (T )] forthe same initial investment X (0) = Y (0); or X (T ) = Y (T ) a.s. with X (0) < Y (0)).Arbitrage is built by being long in (x, X ) and short in (y, Y ).

Example 1 X (T ) ≥S 0 (T ) = eR T

0 r ( u )du a.s. ; E (X (T ) −S 0 (T )) > 0 and X (0) = 1

Example 2 X (T ) = K , a constant, while X (0) < KB T (0) where BT (0) denotes the value

at time 0 of a zero-coupon bond yielding 1 at time T.

The previous considerations imply:

Proposition 3In AoA, all self- Þ nancing and admissible portfolios yielding a.s. the same terminal value must require the same initial investment, i.e. ∀(x ,X ) ∈A0 and ∀¡y ,Y ¢∈A0

with X (T ) = Y (T ) a.s. , then in AoA: X (0) = Y (0).

DeÞ

nition 11 eC T is a contingent claim if

1. eC T is F T measurable.

2. eC T ∈L1,2 (Þ nite mean and variance).

3. (goes with hypothesis on admissible strategies) eC T is bounded from below.

De Þ nition 12 C , the set of contingent claims

33

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 40/102

Chapter 4 AoA, Attainability and Completeness

Example 3 The terminal values of N + 1 primitive assets are contingent claims.

Example 4 ∀A∈F T , the indicator function 1 A is a contingent claim.

De Þ nition 13 eC T ∈C is attainable if ∃(c ,C )∈A0 with C (T ) = eC T a.s. . We say eC T is

attained by (c,C ) or (c,C ) yields eC T .

De Þ nition 14 Ca = attainable contingent claims

De Þ nition 15 Cn = non-attainable contingent claims

De Þ nition 16 The market is (dynamically) complete when all contingent claims are attain-able, i.e., Ca = C or Cn = ∅.

Remark 13 Market completeness is unrealistic in discrete time, but less unrealistic in con-tinuous time. In continuous time the possibility of rebalancing at each point of time allows a much larger spanning. When completeness is obtained through continuous rebalancing, the market is said “dynamically” complete.

De Þ nition 17 A pricing formula π maps C onto R. To be viable, π must satisfy:

1. π is linear, i.e., ∀λ 1, λ 2, eC T ∈C, and eC 0T ∈

C:

π ³λ 1eC T + λ 2eC 0T ´= λ 1π ³eC T ´+ λ 2π³eC 0T ´2. ∀eC T ∈

C

(a)

eC T ≥0 a.s. ⇒π³

eC T ≥0

(b) eC T = 0 a.s. ⇒π

³eC T

´= 03. (Viability or Compatibility Condition) ∀(x ,X ) attaining eC T (i.e., X (T ) = eC T

a.s. ):

π³eC T ´= X (0)

De Þ nition 18 Π = π |π viable

34

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 41/102

Chapter 4 AoA, Attainability and Completeness

De Þ nition 19 Two probability measures P and Q are equivalent if they have the same null sets (the impossible as well as the certain events are the same for P and Q)

De Þ nition 20 An adapted stochastic process is a martingale if at each point of time the (conditional) expectation of a future value is the current value i.e:

Z (t) is a martingale if E [Z (t)/F s ] = Z (s) for any s and t such that 0 ≤s ≤ t ≤T

De Þ nition 21 Q = nQ|Q∼P and ∀(x ,X )∈A0, E Q hX (T )S 0 (T ) |F 0i= X (0 )

S 0 (0) o. Equivalently,Q is a set of P -equivalent probability measures Q under which the asset 0 discounted asset prices X d (T ) = X ( T )

S 0 ( T ) are martingales.

It should be noted that X (0) 6= E P

hX (T )S 0 (T ) |F 0ibecause investors are risk-averse

and expect a return di ff erent than the risk-free rate r (usually higher since, ingeneral, holding a risky asset increases the risk of their portfolio). However, thisdoes not mean that there is no such a probability measure as Q that yields Q-martingale discounted prices.

In the following we will consider the problems:

• Are Q and Π empty?

• What is the relation between Q and Π ?

4.B Propositions on AoA and Completeness

Recall in the following that S 0 (0) = 1

4.B.i Correspondance between Q and Π : Main Results

Theorem 5Assume Q and Π are not empty. There exists a one-to-one relation between Q and Π .

• Q →π Q , deÞ ned by:

∀eC T ∈C : π Q ³eC T ´= E Q "eC T

S 0 (T )|F 0#

35

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 42/102

Chapter 4 AoA, Attainability and Completeness

• π

→Qπ , deÞ ned by:

∀A∈F T : Qπ (A) = E Q [1A ] = π (1A · S 0 (T ))

Proof

Let us begin by showing that π Q is a viable pricing system. Indeed:

1. π Q is linear (because the expectation operator E is linear), i.e., ∀

eX T ∈

Ca

and ∀

eY T ∈

Ca :

π Q ³λ eX T + µeY T ´ = E Q "λ eX T + µeY T

S 0 (T ) #= E Q "λ eX T

S 0 (T )#+ E Q "µeY T

S 0 (T )#= λπ Q ³eX T ´+ µπ Q ³eY T ´

2. ∀

eC T ≥0 a.s. , π Q ³

eC T ≥0;Indeed:

eC T > 0⇒π Q ³eC T ´= E Q "eC T

S 0 (T )#> 0

and

eC T = 0 a.s.⇒π Q ³eC T ´= E Q "eC T

S 0 (T )#= 0

3. (Compatibility Condition) ∀(x ,X ) attaining

eC T , i.e., X (T ) =

eC T a.s. .,

π Q

³eC T

´= X (0); Indeed:

π Q ³eC T ´ = E Q "eC T

S 0 (T )#= E Q ·X (T )

S 0 (T )¸= E Q £X d(T )|F 0¤= X (0)

since Q yields martingale discounted prices

36

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 43/102

Chapter 4 AoA, Attainability and Completeness

4. It has been shown that π Q is a viable pricing formula that maps Q into Π .Moreover, this mapping is injective, i.e., ∀Q

0 6= Q and Q0, Q∈Q, π Q 0 6= π Q .Indeed:

Q0 6= Q

⇒ ∃A∈F T s.t. Q0(A) 6= Q (A)

⇐⇒E Q0

[1A ] 6= E Q [1A ]

Consider a contingent claim 1A S 0 (T ):

π Q (1A S 0 (T )) = E Q

·1A S 0 (T )

S 0 (T )

¸= E Q [1A ]

and

π Q 0 (1A S 0 (T )) = E Q0 ·1A S 0 (T )

S 0 (T ) ¸= E Q

0

[1A ]

Therefore we obtain di ff erent prices for this particular contingent claim,hence, π Q 0 6= π Q .

5. The proof ends by checking that when π is a viable price systemQ (A) = π (1A · S 0 (T )) deÞ nes a probability measure which has the samenull sets than P .

Q.E.D.

Corollary 3 Q = ∅⇐⇒π = ∅

Corollary 4 Q is a singleton

⇐⇒

π is a singleton

Theorem 61. In AoA, a viable pricing formula on Ca exists and is unique.

2. Market is complete and AOA ⇐⇒Q is a singleton ⇐⇒

Π is a singleton

3. AoA⇐⇒Q 6= ∅⇐⇒

Π 6= ∅Proof :

37

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 44/102

Chapter 4 AoA, Attainability and Completeness

1. Assume AoA and consider any

eC T

∈

Ca attained by (x ,X ). Because thecompatibility condition it is only possible to de Þ ne the price of eC T by π³eC T ´=

X (0). If another strategy ¡y ,Y ¢attains fC T , X (0) = Y (0) because AOA, Hencethere is only one viable pricing of an attainable claim under AOA.2. Under AOA, if the market is complete all claims are attainable, hence there isone and only one viable price for any contingent claim in C .3. Under AOA and incomplete markets there are an in Þ nite number of viableprices for a non-attainable contingent claim ( Π 6= ∅but is not a singleton). WhenAOA does not prevail no pricing system meets the compatibility condition, henceΠ is empty.

4.B.ii Extensions

4.B.ii.a Extension I.

Consider eC T ∈Ca attained by (x ,X ) and consider Q∈

Q:

• — At time 0, π³eC T ´= E Q heC T

S 0 ( T ) |F 0i· S 0 (0) = E Q heC T

S 0 ( T ) |F 0i= X (0)

— At time s∈[0, T ]:

π s ³eC T ´ = E Q ·X (T )S 0 (T )

|F s¸· S 0 (s)

=X (s)S 0 (s)

· S 0 (s)

= X (s)

4.B.ii.b Extension II.

The portfolio is not self-Þ

nancing:

• — Assume an adapted and integrable dividend payment δ (t) in [t, t + dt], then:

X (0) = E Q0 (Z T

0 hδ (t) e− R t

0 r ( u ) du idt + X (T ) e− R T

0 r ( u ) du ) — Assume a cumulative dividend stream dD (t) in [t, t + dt], then:

X (0) = E Q0 (Z T

0 hdD (t) e− R t

0 r (u )du idt + X (T ) e− R T

0 r ( u ) du )38

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 45/102

Chapter 5 Alternative Speci Þ cations of Asset Prices

Chapter 5Alternative Speci Þ cations of AssetPrices

5.A Ito Process

There are N + 1 assets in the market:

• r (t) being the adapted, locally risk-free rate, asset 0 is the correspondingrisk-free asset with:

dr = α r (t) dt + σ 0r (t) dw

dS 0 (t) = S 0 (t) r (t) dt⇔S 0 (t) = eR t0 r (u )du

At t : dr (t) is not known, but dS 0 is known.

• The N risky assets follow the process:

dS = α (t) dt + Ω (t) dw

⇔ S (t) = S (0) + Z t

0α (u) du + Z t

0Ω (u) dw

or for the i th asset

dS i= α i (t) dt + Ω 0i (t) dw

where w M × 1 is the vector of standard Brownian Motions and α N × 1 (t) andΩ

N × M (t) are the two adapted processesΩ 0

i is the ith

row of Ω

. The coeffi

cientsof all these Ito processes are stochastic processes that satisfy integrabilityconditions.

• In terms of returns:

dR i =dS iS i

= µi (·) dt + σ 0i (·) dw

or in vector form:

dR = µ (·) dt+ Σ (·) dw

39

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 46/102

Chapter 5 Alternative Speci Þ cations of Asset Prices

where σ 0i is the ith row of Σ , the diff usion matrix.

Equivalently:

S i (t) = S i (0) eR t0 [µ i (.)− 1

2 kσ i (.)k2 ]du +R t0 σ 0

i ( .)dw

The integrability conditions on the coe fficients are:(IC ) R t

0 |µi(.)| du and R t0 kσ i (.)k

2 du deÞ ned a.s fori = 1 ,...,N They will be refered as the integrability conditions (IC ) in the followingchapters

• Ito process yields continuous sample paths, but they are not necessarily

Markovian.

5.B Di ff usions

• S(t) follows a diff usion process if:

dS = α (t, S (t) , r (t)) dt + Ω (t, S (t) , r (t)) dw

or

dS i= α i (t, S (t) , r (t)) dt + Ω 0i (t, S i (t) , r (t)) dw

or

dR = µ (t, S (t) , r (t)) dt+ Σ (t, S (t) , r (t)) dw

or, equivalently

S i (t) = S i (0) eR t0 [µ i − 1

2 kσ i k2 ]du +R t0 σ 0

i dw

The process for the risk-free rate is:

dr = µr (t,r, S) dt + σ0r (t,r, S) dw

with the coe fficients ( α (·) , µ (·) , Ω (·) , ..), being a deterministic function of stochastic variables r, S and the deterministic t.

• The di ff usion process is an Ito process, hence it exhibits continuous samplepaths. Moreover it is Markovian since the next increment depends on t andS(t) , r (t) only.

• Technical conditions to be satis Þ ed bythe coefficients of a diff usion process arethe Lipschitz condition and the linear growth condition.

40

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 47/102

Chapter 5 Alternative Speci Þ cations of Asset Prices

5.C Di ff usion state variables

The state of the economy is de Þ ned by L state variables Y obeying the di ff usionSDE: dY = α Y (t, Y (t)) dt + Ω Y (t, Y (t)) dw(the coefficients meet the integrability conditions). The dynamics of all the Þ nan-cial variables depend on (t, Y (t)) ,i.e:dR = µ (t, Y (t)) dt+ Σ (t, Y (t)) dw ; dr = µr (t, Y ) dt + σ0

r (t, Y ) dwRemark that- The processes are Markovian- The simple di ff usion case is a particular case of the state variable di ff usion case(where S and r are the state variables); the state variable di ff usion case is aparticular case of the Ito case.

5.D Theory in the Ito-Di ff usion Case

All the results on AOA, martingale measures, viable prices, completeness,.., pre-sented in the case of RCLL asset prices and LCRL strategies hold of course whenthey follow Ito or di ff usion processes (which are continuous). We present in thefollowing some speciÞ c results valid in these last cases.

5.D.i Framework

• Assume the usual probability triplet [Ω , F , P ] .

• Let w M × 1 denote the sources of uncertainties. The observable eventsat t are the events w (t0) ≤ a for all t0 ≤ t and all the real vectors a:roughly, information at t is represented by the path of w between 0 andt. F t , t∈[0, T ] ≡F w is then called the Þ ltration generated by w .

• dR = µ (t)dt+ Σ (t)dw and dS i = S i µi dt + S i σ 0idw ; dr = α r (t) dt + σ 0

r (t) dw; the coefficients ( µ (t), Σ (t), ..) are F w −adapted and satisfy the integrabilityconditions.

• Let Γ (·) denote the instantaneous variance-covariance matrix, then:

Γ =dR dR 0

dt

=Σ dw · dw 0Σ 0

dt= ΣΣ 0

41

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 48/102

Chapter 5 Alternative Speci Þ cations of Asset Prices

• Let C be the set of contingent claims de Þ ned as L2, as previously. If X, Y

∈

C,then E [XY ] is a scalar product and C is an Hilbert space

• A strategy can be de Þ ned by weights on risky-assets xN × 1. The strategy willbe denoted by (x ,X ) and the weight of the risk-free asset in the portfoliowould be x0 = 1 −x 01

• (x ,X ) is self-Þ nancing iff

dX X

= x0rdt + x 0dR

= rdt + x0(dR −rdt 1)

i.e., the increment in value comes only from returns. Equivalently:dX X

= µX dt + x 0Σ dw

with

µX = rdt + x 0¡µ −r1¢5.D.ii Martingales

Theorem 7(martingale representation theorem, stated without proof). Consider any F w -adapted Martingale Z (t) : there exists an integrable process β M × 1 (·) such that, for t∈(0T ) :Z (t) = Z 0 + R t

0 β 0(.)dw ⇐⇒ dZ = β 0(t)dw (t)

In particular, for any (x , X ) in A0, under any Q∈Q: dX d

X d = β 0dw (X d = X/S 0)and dX

X = r (t)dt+ β 0dwWe will see later that the probability change (from P to Q for instance) changes

only the drift of the process but not the diff

usion term (this follows from Girsanovtheorem stated further on). Since this di ff usion part would be x 0Σ dw for aportfolio (x , X ),we can write under Q: dX d

X d = x0Σ dw and dX X = r (t)dt + x 0Σ dw

5.D.iii Redundancy and Completeness

De Þ nition 22 The N + 1 assets are redundant at time t if there exists a non zero N -dimensional vector λ (t) = ( λ 1 , λ 2 ,..., λ N )0 such that λ 0dR = α (t) dt a.s. , i.e., a linear combina-tion of risky assets gives a locally risk-free result.

42

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 49/102

Chapter 5 Alternative Speci Þ cations of Asset Prices

• Without losing generality, assume λ 01=1

• In AoA, α (t) = r (t)

Proposition 4The assets are not redundant iff Rank (Σ ) = N, or, equivalently, iff the N rows of Σ are linearly independent, or iff Γ is a positive de Þ nite (invertible) matrix for all t a.s. .

Proof

Assume that the assets are redundant, i.e., λ 0dR = PN i = 1 λ i dR i = α (t) dt . Then de Þ ning

θi = −λ i

λ N gives:

dRN = γ dt +N − 1

Xi = 1

θi dR i

Apply the processes followed by R i :

µN dt + σ 0N dw =

eγ dt +

N − 1

Xi = 1

θi σ 0i dw

For all dw; This implies:

σ 0N =

N − 1

Xi = 1

θi σ 0i

i.e., the N th row of Σ is a linear combination of the other rows. Therefore, Rank (Σ ) < N .

Q.E.D.

Remark 14 A result follows directly: a necessary condition for the assets to be non-redundant is M ≥N.

Theorem 8Assume AOA, that M = N , that the coe ffi cients are adapted w.r.t. the Þ ltration F wgenerated by w and that the N + 1 assets are non-redundant (hence Rank (Σ ) = N ∀ta.s. .), then the market is complete w.r.t. . the Þ ltration F w .

Proof

43

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 50/102

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 51/102

PART IIIState Variables Models:

the PDE Approach

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 52/102

Chapter 6 Framework

Chapter 6Framework

The state of the economy depends on a vector Y of state variables

• Let w M × 1 denote the M -Brownian Motions vector and Y L × 1 denote theL-state variables vector with

dY = µ Y (t, Y (t))dt + Ω L × M ³t ,Y (t)´dw

Y (t) represent the random variable, Y t will denote a particular realization att

• We consider N + 1 ”primitive” securities (one risk-free, N risky). The returnsof the N risky assets follow the di ff usion process:

dR N × 1= µ (t , Y (t))dt + Σ N × M (t, Y (t))dw

or, for a single asset:

dR i =dS iS i

= µi (t, Y (t)) dt + σ 0i (t, Y (t)) dw

(σ 0i is the ith row of Σ )

• The risk-free rate follows the di ff usion process:

dr (t) = µ0 (t, Y (t)) dt + σ 0r (t, Y (t)) dw

The price of the locally riskless asset follows:

dS 0 = r (t) S 0 (t) dt

46

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 53/102

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 54/102

Chapter 7 Discounting Under Uncertainty

Chapter 7Discounting Under Uncertainty

7.A Ito’s lemma and the Dynkin Operator

Recall that we consider the variables Y satisfying;

dY = µ Y (t, Y )dt + Ω L × M (t , Y ) dw

Consider v (t, Y ) : [0, T ] × RL →R, with v∈C 1 w.r.t. t and v∈C 1,2 w.r.t. Y .Ito’s lemma writes in alternative forms:

dv =∂ v∂ t

dt + µ∂ v∂ Y¶0

dY +12

dY 0 ∂ 2v∂ Y ∂ Y 0dY

This gives:

dv = "∂ v∂ t

+L

Xi=1

∂ v∂ Y i

µY i +12

L

Xi=1

L

X j =1

∂ 2v∂ Y i ∂ Y j

V ij#dt +L

Xi=1

∂ v∂ Y i

M

X j =1

ωij dw j

with V ij being the common term of V , ΩΩ 0.

DeÞ ne the Dynkin operator as:

D tY v =

E t [dv]dt

=∂ v∂ t

+L

Xi=1

∂ v∂ Y i

µY i +12

L

Xi=1

L

X j =1

∂ 2v∂ Y i ∂ Y j

V ij

then the dynamics of v can be simpli Þ ed in notations as:

dv = ( DtY v)dt + µ∂ v

∂ Y¶0

Ω dw

7.B The Feynman-Kac Theorem

Consider Y and v (t, Y ) as previously de Þ ned. For given functions of bµ (t, Y (t)) ,δ (t, Y (t)), and l (Y ), we try to Þ nd the solution to the following problem (PDE

48

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 55/102

Chapter 7 Discounting Under Uncertainty

with its limit condition):

P DE DtY v + δ = bµv

v (T, Y ) = l (Y )

Feynman-Kac theorem: The solution of the previous P DE can be writtenas an expectation:

v (t, Y t ) = E P ½Z T

tδ (u) · e− R u

t bµ (x )dx du + l (Y T ) · e− R Tt bµ (x )dx |Y (t) = Y t¾

The Þ nancial interpretation of this is:

• v is the price of a Þ nancial asset giving a dividend stream of δ and a terminalvalue of l (Y )

• bµ is the required rate of return

• D tY v+ δ

v is the expected instantaneous return with ( DtY v)dt being the capital

gain and δ (t)dt the dividend during the period [t, t + dt].

The PDE states that the expected return is equal to the required

bµ; Its solution

is the conditional expected value of the ”discounted” stream of dividends + theterminal value, the discount rate being bµ. This is also CIR(1985), lemma III .

Feynman-Kac theorem provides a link between the PDE approach and the mar-tingale approach. However since we do not know the required expected return bµthe PDE or its solution interpreted as a discounting at rate bµ does not give thevalue v. But in the following we are going to provide an APT condition on bµ.

49

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 56/102

Chapter 8 The PDE Approach

Chapter 8The PDE Approach

8.A Continuous Time APT

8.A.i Alternative decompositions of a return

Consider an asset yielding a dividend stream of δ and a terminal value of l (Y ).We have derived that:

dv = ( DtY v)dt + µ∂ v

∂ Y¶0Ω dw

Divide both sides by v gives:

dv

v=

1

v¡Dt

Y v

¢dt +

1

vµ∂ v

∂ Y¶0

Ω dw

= µv dt + σ 0vdw

Here µv = 1v Dt

Y v can be considered as the expected rate of return and σ 0v =

¡σ1v , σ2

v , ..., σM v ¢the volatility vector or sensitivity w.r.t. . w .

Also, deÞ ne

ψ = µv

−1

vµ∂ v

∂ Y¶0

µY

then

dvv

= µvdt +1vµ∂ v

∂ Y¶0Ω dw

= µvdt +1vµ∂ v

∂ Y¶0

£dY −µY dt¤= ψdt +

1vµ∂ v

∂ Y¶0

dY

50

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 57/102

Chapter 8 The PDE Approach

More explicitly we get two alternative decompositions of the return:

dvv

= µvdt +M

Xi=1

σ ivdwi

= ψdt +1v

L

Xi=1

∂ v∂ Y i

dY i

• σ iv is the sensitivity of the return of asset v w.r.t. w i and 1

v∂ v∂ Y i the sensitivity

w.r.t. Y i .

8.A.ii The APT Model (continuous time version)

In the following (·) denotes (t, Y (t)) .The following proposition is the continuous time version of APT and can be justi Þ ed as the discrete time version.

Proposition 5(APT)

1. There exist M scalars: λ 1 (·) , λ 2 (·) , ..., λ M (·) such that, for any asset (value vreturn stream = δ , required expected instantaneous return = µ):

δ v

(·) + µ (·) = r (·) +M

Xi=1

λ i (·) σ iv (·)

λ i (·) is the market price of the risk wi and is the same for all assets. Theequation above can be deemed as a decomposition of the expected rate of return into the riskless rate and M risk premiums: λ i (·) is the market price of risk (MPR) wi ; The MPR vector λ is the same for all assets.

2. There exist L scalars: θ1 (·) , θ2 (·) ,..., θL (·) s.t. , for any asset:δ v

(·) + µ (·) = r +L

X j =1

θ j (·)1v

(·)∂ v∂ Y j

(·)

This is an alternative decomposition of the expected rate of return with L riskpremia (relative to risks Y ). θ j is the market price of risk (MPR) Y j , and isalso the same for all assets.

We will drop (·) in the following for simplicity

51

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 58/102

Chapter 8 The PDE Approach

A direct result then follows:

θ L × 1= Ω L × M λ M × 1

• In the particular case that L = M and then Ω is invertible, λ can be solved as:

λ = Ω − 1θ

• Furthermore, if we apply APT to the ith primitive asset:

dR i = µi dt + σ 0i dw

µi = r + σ0i λ

where σ 0i is the ith row of Σ .

• In vector form:

µ = r · 1+ Σ λ

This equation may be used in two ways:- To obtain the required returns µ for a given MPR λ .Then, the returns of the primitive risky assts follow:dR = [r (.)1 + Σ (.)λ (.)]dt + Σ (.))dw

- To obtain (or estimate) the MPR λ assuming that the risk premiums µ −r 1are known (or estimated). This is only possible when Σ is invertible ( M = N and non redundant assets, implying market completeness), in which case:

λ = Σ − 1¡µ −r 1¢Under incomplete markets an in Þ nite number of MPR vectors λ are compatiblewith the risk premia on the primitive securities.

• It is important to note that:

DtY v + δ v

= r + 1vµ∂ v

∂ Y¶0

θ

This PDE means that the expected rate of return equals the required rate of return. It must be followed by any asset in a world described by Y . The onlydiff erence between assets is the boundary condition v (T, Y ) = l (Y ) speciÞ cto each asset.

Example 5 In the Black-Schole’s framework Y = S, L = M = N = 1 , for a call: l(Y ) =(Y −K )+ , λ = ( µ −r )/ σ

52

8/3/2019 Capital Markets and Portfolio Theory, Roland Portait

http://slidepdf.com/reader/full/capital-markets-and-portfolio-theory-roland-portait 59/102

Chapter 8 The PDE Approach

Example 6 A one factor interest rate model with a stochastic risk-free rate r , which is also the state variable. Only bonds are considered and one bond is su ffi cient (the others are redundant), therefore, L = M = N = 1 . We consider such models in the following section.

8.B One Factor Interest Rate Models

• — L = M = 1 , and now Y 1 = r

— dS 0 = S 0 r (t) dt — Let BT (t, r (t)) be the price of a zero coupon bond at t that delivers 1 at T . The

duration of the bond is then T −t

— Several BT may be traded (but they are redundant).

— dr = a [b−r ]dt + σ r (t, r )dw. In Vasicek model σ r (t, r ) = σ constant, and in CIR model σ r = σ√ r

• Write the expected rate of return by applying APT:

Dtr BT

BT = r +

1BT

∂ BT

∂ rθ

This gives:

∂ BT

∂ t+

12

σ2r

∂ 2BT

∂ r 2 + a (b−r )∂ BT

∂ r= rB T +

∂ BT

∂ rθ

with the boundary condition that BT (T ) = 1 ∀T .

• The PDE can be solved in both Vasicek and CIR settings.

8.C Discounting Under Uncertainty

Consider the PDE:

D tY v + δ = rv + µ∂ v

∂ Y¶0

θ ; LC : v(T, Y ) == l(Y )