cfa institute research challenge de manila university student research concepcion industrial...

TRANSCRIPT

CFA Institute Research Challenge hosted by

CFA Society of the Philippines Ateneo de Manila University

Ateneo de Manila University Student Research

Concepcion Industrial Corporation (CIC) This report is published for educational purposes only by students Industrial Sector, Electrical Component & Equipment Industry competing in the CFA Institute Research Challenge. Philippine Stock Exchange (PSE)

DATE: 11/28/2014 PRICE: PHP 41.00 RECOMMENDATION: BUY (23.14% UPSIDE) TICKER: CIC.PM (BLOOMBERG) TARGET PRICE: PHP 50.49

MARKET SNAPSHOT

Outstanding Shares 339.6 mn

Free Float Level 29%

Market Capitalization Php 13.6 bn

Listing Date 11/27/2013

Par Value Php 1.00

External Auditor Isla Lipana Co.

Adj. 52 week High: Php 43.69/share

Adj. 52 week Low: Php 16.54/share

Dividend Yield (NTM) 1.87%

Source: Philippine Stock Exchange

TRAILING RETURN

CIC PSEi

1 month 2.50% 3.22%

3 month 1.23% 2.73%

6 month 45.23% 7.46%

12 month 105.00% 18.22% Source: Thomson Reuters, Bloomberg

SUBSIDIARIES OF CIC

SUBSIDIARY MAIN PRODUCTS

Concepcion-Carrier Air Conditioning Company (CCAC)

Air Conditioners, Commercial Refrigerators

Concepcion Durables Inc. (CDI)

Residential Refrigerators

Concepcion Otis Philippines Inc. (COPI)

Elevators, Escalators, Moving Walkways

Concepcion Midea Inc. Philippines (CMIP)

Consumer Appliances

Source: Team Estimates

TARGET PRICE BREAKDOWN

SUBSIDIARY VALUE PER SHARE1

CCAC 35.74

CDI 11.42

COPI 3.10

CMIP 0.24

CIC 50.49 1Value per share attributable to CIC (in Php) Source: Team Estimates

EARNINGS PER SHARE (IN PHP)

Source: Team Estimates

CIC: There’s Something Cool in the Air

We issue a BUY recommendation on Concepcion Industrial Corporation (CIC) with a target price of Php 50.49/sh using Sum-of-Parts Valuation method and Discounted Free Cash Flow to Firm (DCF) analysis. This presents an upside of 23% from the closing price of Php 41.00/sh on November 28, 2014. We expect its EPS to grow at a compound annual growth rate (CAGR) of 12%, from Php 2.03/sh in 2014 to Php 4.08/sh in 2020, driven by its market leadership with proven track record, strong growth potential in underpenetrated markets, and financial flexibility to pursue new ventures. MARKET LEADERSHIP WITH PROVEN TRACK RECORD CIC is the number one seller and manufacturer of air conditioners and refrigerators in the country with a market share of 37% and 25% respectively. This is backed by a long operational history of over 50 years, its above-market performance, and its highly recognized brands such as Carrier, Condura, Kelvinator, and Toshiba. We believe that CIC can at least sustain its market leadership through margin expansion (reaching 20% EBITDA margin in 2020) driven by strong research and development capability, cost reduction efforts, and flexible operations. STRONG GROWTH POTENTIAL IN UNDERPENETRATED MARKETS CIC’s sales is expected to grow at a CAGR of 10% for the years 2014 to 2020. This will be driven by the country’s robust economic growth leading to increasing purchasing power and booming real estate industry. These factors will propel the demand for air conditioners and refrigerators as Philippines’ penetration rates are only at 6% and 35%, respectively, one of the lowest among its ASEAN neighbors. As the market leader, CIC is poised to capitalize on this growth. FINANCIAL FLEXIBILITY TO SUSTAIN BUSINESS AND PURSUE NEW VENTURES CIC can sustain its current business and pursue mergers and acquisitions (M&As) with its strong cash flows and underleveraged position. It is able to return value to its shareholders via dividends and finance its capital expenditures through internally generated funds as evidenced by its average free cash flows of around Php 1.1 bn annually for the next five years. CIC’s debt ratio has been consistently low at 14%, further highlighting the company’s low risk and capacity to acquire loans at a lower marginal cost of debt. The company’s strong cash flows and underleveraged position gives CIC the financial flexibility to seek new ventures in line with its long-term goal of being the leading provider of comprehensive consumer and building solutions. Recently, the company entered into joint ventures (JVs) with Otis Philippines and Midea to expand the company’s business into the people-moving products (e.g. elevators, escalators, moving walkways) and the Php 60-bn consumer appliance market. Moving forward, CIC intends to acquire fire, security, and lighting solutions as it strives to be a one-stop shop for both its individual and institutional clients.

KEY FINANCIAL RATIOS

2014E 2015F 2016F 2017F 2018F 2019F 2020F

Sales YoY Growth Rate (%) 19.55 10.86 10.29 9.95 9.68 9.49 9.27

EBITDA Margin (%) 18.44 17.70 18.30 18.87 18.97 19.08 19.71

Net Income Margin (%) 12.26 11.76 12.21 12.65 12.75 12.90 13.39

Cash Ratio 0.62 0.77 0.94 1.12 1.30 1.48 1.66

Debt Ratio (%) 14.18 12.27 10.72 9.35 8.22 7.25 6.39

Return on Equity (%) 30.34 27.20 25.68 24.34 22.68 21.42 20.82

Earnings per Share 2.03 2.17 2.48 2.87 3.17 3.51 4.08

EPS Growth (%) 27.27 6.68 14.22 16.01 10.54 10.59 16.18

Free Cash Flow per Share 1.92 2.44 2.87 3.28 3.65 4.03 4.60

0%

5%

10%

15%

20%

0.0

2.0

4.0

6.0

20

14E

20

15F

20

16F

20

17F

20

18F

20

19F

20

20

F

YoY

Gro

wth

EP

S (

in P

hp)

EPS YoY Growth

Ateneo de Manila University Student Research | 2

FIGURE 1. MARKET SHARE OF LOCAL PLAYERS IN AIR CONDITIONING INDUSTRY,

BY VOLUME (2013)

Source: Company Data

FIGURE 2. MARKET SHARE OF LOCAL PLAYERS IN THE REFRIGERATION

INDUSTRY, BY VOLUME (2013)

Source: Company Data

FIGURE 3. CIC REVENUE BREAKDOWN, BY SEGMENT (2013)

Source: Company Data

FIGURE 4. CIC’S EFFECTIVE OWNERSHIP IN ITS SUBSIDIARIES

Source: Company Data

FIGURE 5. GDP (IN PHP TN) AND GDP PER

CAPITA GROWTH RATES

Source: World Bank

Business Description Operating for more than 50 years, Concepcion Industrial Corporation (CIC) is Philippines’ leading supplier and manufacturer of air conditioning and refrigeration appliances. Currently, it is expanding into other consumer appliances and building solutions (see Appendix A-2). It caters to two market segments namely, consumer solutions and business & industrial solutions (see Appendix A-3), which accounts for 80% and 20% of 2013 revenues respectively. CIC's Business Model Canvas is shown in Appendix A-4.

MARKET LEADER IN AIR CONDITIONING AND REFRIGERATION CIC is a holding company that primarily operates through two of its subsidiaries, Concepcion-Carrier Air Conditioning Company (CCAC) and Concepcion Durables Inc. (CDI), the country’s leading suppliers of air conditioning at 37% volume share (see Figure 1) and refrigeration appliances at 25% volume share (see Figure 2) respectively. Air conditioning sales made up 65% of the company’s 2013 revenues, refrigeration sales accounted for 31%, and after-sales revenues made up 4% (see Figure 3). CCAC manufactures, sells, distributes, installs, and provides comprehensive air conditioning and commercial refrigeration products and services. This comprises 69% of 2013 sales. It employs a multi-brand strategy to target consumers from different segments, with Carrier and Toshiba catering to the high-end segment, Condura targeting the mid-tier segment, and Kelvinator targeting the entry level segments. On the other hand, CDI manufactures, assembles, wholesales, and retails residential refrigeration appliances through its market-leading brands, Kelvinator and Condura. It focuses solely on the residential and light commercial (RLC) segment, which accounted for 31% of the company’s sales in 2013 (see Figure 3). Both subsidiaries operate a manufacturing plant in Cabuyao, Laguna, with a combined production area of 35,000 sq. meters This is equivalent to an annual production capacity of 500,000 units for air conditioners and 300,000 units for refrigerators given 1-2 production shifts per day, making CIC the largest air conditioning and refrigeration manufacturer in the country. The management does not see the need to increase the plant capacity in the near future given its current utilization rate of 56% for CCAC and 78% for CDI, and that operations may scale up to 3-4 production shifts per day.

STRATEGIC PARTNERSHIPS AND ACQUISITIONS Last November 2013, CIC entered into a joint venture with Midea Group, one of the largest consumer appliance manufacturers and distributors in the world, to form Concepcion Midea Inc. Philippines (CMIP). CIC’s 40% share (see Figure 4) of CMIP allows it to broaden its reach in the Php 60-bn consumer appliance market. Last March 2014, CIC engaged in a joint venture agreement with UTC-Asia Pte. Ltd., a subsidiary of United Technologies Corp., to take 51% equity stake (see Figure 4) in Concepcion Otis Philippines Inc. (COPI). COPI sells and services elevators, escalators, and moving walkways, thus broadening the building and industrial solutions (BIS) that CIC can offer to its institutional clients. CIC plans to capitalize its current relationships with tier one real estate developers to drive growth in COPI’s revenues.

OWNERSHIP STRUCTURE CIC is owned by the public and three major shareholders. The three major shareholders are Foresight Realty and Development Corp., formerly Concepcion Holdings Inc., Hyland Realty and Development Corp., and Horizons Realty Inc. The Concepcion family, who has been operating the business for more than 50 years, owns these major shareholders, which comprise 71.4% of the total shares. The public owns the remaining 28.6%.

CORPORATE GOVERNANCE CIC believes in conducting its business and operations in accordance with the principles and best practices of good corporate governance. It aims to engender a good reputation in the market place, leading to long-term sustainability and success. Top management is comprised of experts with a proven track record of over 20 years of experience in the field to lead CIC to sustained growth. Further discussion on Corporate Governance is detailed in Appendix F.

Industry Overview and Competitive Positioning INDUSTRY OVERVIEW: STRONG GROWTH POTENTIAL Rise in Infrastructure Driven by Economic Growth The Philippines has enjoyed unprecedented economic growth over the years, with GDP per capita growth of around 7% from 2011 to 2013 (see Figure 5). Following this trend, the expected rise in GDP per capita will translate into more infrastructures such as housing, offices, and shopping malls. New office supply in the major commercial business districts is expected to grow at a CAGR of 8.3%, while the supply of residential units is expected to grow at a CAGR of 10.4% for the next three years. This rise in infrastructure translates into stronger demand for consumer appliances and industrial building solutions.

Wider Market Base Due to Demographic Shift and Increasing Household Income With the country’s low median age of 22.9 years old (see Figure 6), the working population is expected to grow rapidly. Coupled with a decreasing unemployment rate (see Figure 7), this translates into a growing middle class that is forecasted to comprise 61% of the population in 2017. In addition, the steady influx of overseas remittances further increases household disposable income at a CAGR of 7% from 2013 to 2020, outgrowing the forecasted inflation rate of 4% (see Figure 8). This demographic shift and rising household income will increase the size of CIC’s potential market.

37%

22%

9%

7%

6%

19%

CIC Panasonic Samsung Korur LG Others

25%

22%

12%

12%

11%

18%

CIC Panasonic LG Haier Sharp Others

51%

31%

14%

4%

CCAC-AC: Residential & Light Commercial CDI-Ref: Residential & Light Commercial CCAC-AC: Commercial & Industrial After-market Sales

CIC

CCAC

60%

Otis

51%

Midea

40%

CDI

100%

2.2%

10.3%

6.0% 7.0% 7.4%

0.0

3.0

6.0

9.0

12.0

20

09

20

10

20

11

20

12

20

13

GDP

GDP per capita Growth Rate

in Php

tn

Ateneo de Manila University Student Research | 3

FIGURE 6. AGE-SEX PYRAMID OF THE PHILIPPINES (2010)

Source: Philippine Statistical Authority

FIGURE 7. LABOR FORCE POPULATION (IN MN) AND UNEMPLOYMENT RATE

Source: World Bank, Philippine Statistics Authority, Philippine Institute for Development Studies

FIGURE 8. HOUSEHOLD ANNUAL DISPOSABLE INCOME IN PHP ‘000

Source: Bangko Sentral ng Pilipinas

FIGURE 9. AIR CONDITIONING AND REFRIGERATION PENETRATION RATES

Source: Euromonitor, World Bank

FIGURE 10. PORTER'S FIVE FORCES ANALYSIS

Source: Team Analysis

Growth Potential from Increasing Penetration Rate The penetration rates of air conditioners and refrigerators in the country are 6% and 35%, respectively, which are some of the lowest in the ASEAN region (see Figure 9). However, these rates are expected to increase over the years due to the booming real estate industry and the increasing purchasing power of the Filipinos. Together, these three factors directly contribute to the increasing demand for air conditioning and refrigeration units. With strong brand recognition and innovative solutions, CIC is geared to tap into these growing markets and grow the sales of CCAC, CDI, COPI, and CMIP at a CAGR of 9.83%, 10.21%, 13.58%, and 10.40% respectively for the years 2014 to 2020.

CIC and the ASEAN With the upcoming ASEAN economic integration, new competitors are expected to enter the country’s consumer appliance market. However, the industry analysis (see Table 8) indicates that CIC will remain as a market leader through its active M&A strategy and distinctive competencies. With a long operational history, CIC has the first-mover advantage and brand loyalty from consumers. Moreover, we do not expect the ASEAN economic integration to result into a price war. Through the ASEAN Trade in Goods Agreement (ATIGA), member nations are already implementing preferential tariff rates of 0% for imported air conditioners, refrigerators, and primary raw materials since February 2009. With CIC’s commitment to efficiency, active efforts in cost reduction, and vast distribution network, we expect CIC to withstand increasing competition in the industry.

Porter’s Five Forces Analysis A summary of our industry analysis is shown in Figure 10 and Table 8. A more extensive discussion is presented in Appendix C-1.

TABLE 8. PORTER’S FIVE FORCES ANALYSIS

PORTER’S FORCE

LEVEL DESCRIPTION

Bargaining Power of Buyers

Moderate to

Significant

Given the low switching cost, consumers drive quality and innovation of products in the industry. They pressure the manufacturers to provide differentiated products by incorporating features such as energy efficiency and environmental sustainability at affordable cost.

Bargaining Power of Suppliers

Low

Despite the high importance of quality and the lack of available substitutes for the raw material inputs, supplier power is low primarily due to minimal switching costs from undifferentiated raw material inputs and the large supplier size relative to the number of manufacturers.

Threat of New Entrant

Low Barriers to entry in the industry are very high due to the capital intensity, high fixed costs, heavy investments in R&D, and high significance of economies of scale.

Threat of Substitute

Low to Moderate

Electric and cooling fans are possible substitute products for air conditioners. As for refrigeration appliances, there are no clear substitute products, but consumers may choose to purchase their food on a per need basis. Despite the presence of cheaper alternatives, these do not provide its users the same level of utility as with air conditioners and refrigerators.

Rivalry of Existing

Competitors

Significant

The list of CIC’s key competitors for each market segment is summarized in Table 1. The presence of both local and international players intensifies the competition within the market. Buyers having moderate to significant bargaining power, price wars, high exit cost for the firms imply that the rivalry of existing competitors is significant.

Source: Team Analysis

COMPETITIVE POSITIONING: MARKET LEADERSHIP A detailed discussion of CIC’s strengths is presented below. The summary of the SWOT Analysis is shown in Appendix C-2.

Leading and Trusted Brands to Capture Different Market Segments Having operated for more than 50 years in the industry, CIC has a strong reputation in the country and a loyal customer base. CIC believes that holding numerous trusted brands in its portfolio allows it to achieve its leadership position in both air conditioning and refrigeration industries. CIC employs a multi-brand strategy in the market for air conditioners and refrigerators: Carrier and Toshiba for high-end segment, Condura as mid-tier brand, Kelvinator for entry to mid-tier segment, and Midea as an entry-level brand (see Table 9). This strategy allows CIC to capture a broader customer base by offering products with varying features and price points. This strategy is highly suitable for the country’s growing middle class.

Strong Local Knowledge and R&D Capability to Defend Market Leadership CIC prides itself in its strong local knowledge, which enables it to differentiate its products from its competitors. With its eight self-owned R&D laboratories, more than 30 engineers, and design teams, it develops customized product solutions, next-generation products, latest technology, and best practices that specially target local consumers (see Table 2). An example of its product innovation is the patented energy-saving plug built into Carrier air conditioners, which automatically switches the fan on when the air conditioner shuts down. This innovation is intended to allow consumers to save on electricity costs, as the electricity cost in the country is among the highest in Asia. Furthermore, the company’s strong R&D facility allows it to engage in cost reduction efforts such as product re-engineering to drive margin expansion.

6.0 4.0 2.0 0.0 2.0 4.0 6.0

5- 10-14

20-24 30-34 40-44 50-54 60-64 70-74 80-84

Male (in mn) Female (in mn)

Age

7.4% 7.5%

7.3%

7.0% 7.0% 7.1%

0

10

20

30

40

50

20

08

20

09

20

10

20

11

20

12

20

13

Labor Force Population (in mn)

Unemployment Rate (% of labor force)

in mn

0

100

200

300

400

500

600

700

20

08

20

09

20

10

20

11

20

12

20

13

20

14E

20

15F

20

16F

20

17F

4% inflation rate

in Php

'000

0

20

40

60

80

100

0%

20%

40%

60%

80%

100%

PH

L

IND

TH

A

MLY

SIN

GD

P p

er C

apita

(in U

SD

'00

0)

Peentr

ation R

ate

Air Conditioning Refrigeration GDP per capita, PPP (in USD '000)

0

1

2

3

4

5

Bargaining Power of Buyers

Threat of Substitute Products

Bargaining Power of Suppliers

Rivalry of Existing Competitors

Threat of New

Entrants

Ateneo de Manila University Student Research | 4

TABLE 1. COMPETITORS OF CIC

MARKET SEGMENT COMPETITOR

RLC Air Conditioning

Panasonic

Samsung

Hitachi

Commercial and Industrial Air Conditioning

Mitsubishi

Trane

York

Hitachi

LG

RLC Refrigeration

Panasonic

Samsung

Sharp

LG

Whirlpool

Commercial and Industrial Refrigeration

Grasso

GNQ

KR

Zikor

Ruey Shing Source: Company Data

TABLE 2. STRONG R&D CAPABILITY

STRONG R&D CAPABILITY

Philippines' Largest Air Conditioning and Refrigeration Lab

8 Self-Owned R&D Laboratories

Vibration Laboratory and Sound Room

Simulation and Environment Laboratory

3 Psychometric Laboratories

Thermal Cycling Room

Thermal Calibration Machine

Comprehensive Engineering and Design Team

30 Engineering and Design Teams

Source: Company Data

FIGURE 11. CIC EBITDA MARGIN VS. COMPETITORS IN 2012

Source: Thomson Reuters, Company Data

FIGURE 12. PRODUCT CYCLE

Source: Company Data

TABLE 3. DISTRIBUTION NETWORK

Nationwide Logistic Network

Distribution Across the Philippines

Nationwide Retail Coverage

90% Retail Store Coverage

In-Store Merchandisers

Over 1,000+ Merchandisers

Source: Company Data

TABLE 9. CIC'S AWARDS AND RECOGNITIONS

BRAND MARKET

SEGMENT AWARDS AND RECOGNITIONS

High-End

Philippines’ best-selling air conditioner brand in 2010 Reader’s Digest Trusted Brand for the past 17 years

Mid-Tier

Leading domestic air conditioning and refrigeration brand Reader’s Digest Trusted Brand for the past 9 years for air conditioners Reader’s Digest Trusted Brand for the past 2 years for refrigerators

Entry to Mid-Tier

Leading air conditioner and refrigerator brand internationally Introduced the world’s first automatic-control refrigerator

High-End Leading consumer brand globally Introduced the first inverter air conditioner

Entry Level

Leading appliance brand globally No.1 manufacturer of major home appliances for 2012 and 2013

Source: Company Data

Cost Leadership and Lean Manufacturing Operations Result to Immense Savings CIC has had consistently high EBITDA margins compared to its competitors in the past (see Figure 11). With CIC’s strong commitment to efficiency, strong profitability is expected to continue, as they are able to maintain an OPEX-to-sales percentage of 17% that is superior to its competitors. In 2013, the company adopted efforts to improve its operational efficiency, which is expected to amount to total savings of Php 73 mn from engineering, purchasing, and manufacturing activities.

Flexible Operations due to Unique Outsourcing Strategy Enables CIC to Supply Growing Demand CIC employs a unique outsourcing strategy that enables both of its air conditioning and refrigeration plants to maintain lean manufacturing systems. Certain stages in the manufacturing process are outsourced to “negosyo partner corporations”, which are cooperatives comprised mostly of former CIC employees. This strategy provides CIC’s production the flexibility to scale up or down depending on the demand and simultaneously controls costs.

Offering of Customized End-to-End Solutions to Cultivate Brand Loyalty CIC’s integrated operations, from manufacturing to after-sales services, allow it to adapt to changing consumer needs. It does not only offer air conditioning and refrigeration products, but also develop solutions that cater to the entire life cycle of its products (see Figure 12). Unlike other manufacturers, CIC enters as early as the planning and designing stage of real estate projects. Having its own manufacturing plant in the country and a strong R&D facility, CIC is able to customize air conditioner and refrigerator designs based on the needs of its clients. CIC believes that this unique end-to-end business model and its ability to custom-fit designs allow it to develop customer loyalty.

Extensive After-Sales Support and Strong Tier One Relationships to Mobilize COPI Growth CIC currently has a strong relationship with seven of the top ten tier one real estate developers in the country. Moreover, its after-sales network is also considered as the largest in the country (see Table 4). Its air conditioning business includes partnerships with over 170 installer companies, 70 service centers, and 8 dedicated parts stores, while its refrigeration business has 69 service centers nationwide. After-sales is considered to be COPI’s key driver for profitability as it has larger profit margins of around 30% to 40%. CIC’s joint venture to form COPI allows the latter to capitalize on CIC’s existing customer relationships and leverage on CIC’s strong after-sales support system, making it the preferred choice of consumers and clients in both the residential and commercial segment.

Wide-Scale Sales Distribution Network and Strong Brand Image to Propel CMIP Growth CIC has a wide-scale distribution network that places its products in approximately 90% of all appliance outlets in the country (see Table 3). This, together with its strong brand image, allows CMIP to increase its sales and build the Midea brand. CIC believes that its multi-channel presence and distribution are key to strengthening its relationships and partnerships with consumers and retailers by ensuring the availability of its products.

Corporate Key Directions and Growth Strategy STRENGTHENING MARKET LEADERSHIP Cost Reduction Efforts to Improve Profitability As CIC expands its current core business, it seeks to further strengthen cost leadership through unlocking potential synergies such as shared back end support systems and various cost reduction efforts. For the year ended 2013, CIC saved roughly Php 73 mn, amounting to 4% of the year’s COGS and OPEX. The list of cost reduction projects implemented in 2013 is presented in Appendix C-3. It is expected that the company will save up another Php 70 mn by the end of 2014 and Php 120 mn in the year 2015. CIC’s cost reduction efforts are focused on the following aspects:

• Purchasing Savings - trade discounts on bulk purchases, price hedging on raw materials

• Engineering-Related Savings - driven by the company’s strong research and development in increasing material productivity through altering product designs, down gauging, and material substitution

• Productivity Savings - increased efficiency and utilization rate of both equipment and employees

• Logistics Savings - optimization of distribution routes, maximization of container capacity

• Supplier Chargebacks - payment of replacement costs, penalties, and damages from suppliers due to defective raw materials

0%

5%

10%

15%

20%

CIC Panasonic Daikin Sampo

Designing Stage

Equipment Scoping and

Selection

Supply Installation

Testing and Commissioning

After-Sales

Ateneo de Manila University Student Research | 5

TABLE 4. AFTER-SALES SUPPORT

24/7 Customer Care

24/7 Contact Center

Nationwide Service & Install Capability

In-House Technicians

Service Center Finder

Carrier Certified Installer

Highly Trained Service Technicians

Training and Audit Partners - TESDA & Don Bosco

Dedicated Parts Stores

8 Totaline Parts Stores Strategically Located

Source: Company Data

FIGURE 13. INCREASING REFRIGERATOR PENETRATION RATE AS GDP PER CAPITA

INCREASES

Source: Euromonitor, World Bank

FIGURE 14. INCREASING AIR CONDITIONER PENETRATION RATE AS GDP PER CAPITA

INCREASES

Source: Euromonitor, World Bank

FIGURE 15. CCAC AND CDI OPERATING CASH FLOW

Source: Team Estimates

FIGURE 16. CIC DEBT-TO-ASSET RATIO

Source: Team Estimates

Diversifying Into Specialized Turnkey Solutions With a strong foothold in the retail segment of the air conditioning and refrigeration market, CIC aims to diversify its business into specialized turnkey solutions. Capitalizing on the company’s strong R&D capability and relationship with tier one real estate developers, CIC aims to provide custom-fit air conditioner and refrigerators to its institutional clients. This will enable the company to have an established after-sales customer base and tap a different distribution channel that has high volume demand.

TAPPING THE UNDERPENETRATED MARKET Multi-Brand Strategy to Capture Different Market Segments Holding numerous trusted brands in its portfolio, CIC implements a multi-brand strategy in the market for air conditioners and refrigerators: Carrier and Toshiba for high-end segment, Condura as mid-tier brand, Kelvinator for entry to mid-tier segments, and Midea as entry-level brand (see Table 9). The company believes its multi-brand strategy will allow it to continue to expand its product portfolio with varying features and price points, meeting the needs of a broader range of customers, especially in terms of the growing Philippine middle class.

GROWTH IN NEW VENTURES Comprehensive Product Lineup in Consumer Solutions Group CIC aims to become the largest consumer appliance company in the country. To achieve this, CIC plans to offer a comprehensive product lineup that caters to different market segments in the consumer appliance industry. This will allow CIC to maintain its leadership position in the core markets, broaden the company’s product range, and mitigate the risk of losing market share to differently priced substitutes. CIC’s recent joint venture agreement to form CMIP gives the company the access to penetrate the consumer appliance market and fill in the gaps in its product portfolio.

Complete Customized End-to-End Business and Industrial Solutions Provider CIC aims to provide complete end-to-end building and industrial solutions by eyeing strategic acquisitions and joint ventures in the field of security systems, lighting fixtures, and fire safety. Few of CIC’s possible acquisitions or JVs are United Technologies’ brands such as Chubb, leading provider of security and fire-safety solutions, and Kidde, leading manufacturer of residential smoke alarms, carbon monoxide (CO) alarms, and fire extinguishers. See Appendix C-4 for a list of UTC’s building and industrial system brands and products.

Investment Summary We issue a BUY recommendation on Concepcion Industrial Corporation (CIC) with a target price of Php 50.49/sh using Sum-of-Parts Valuation method and Discounted Free Cash Flow to Firm (DCF) analysis. This presents an upside of 23% from the closing price of Php 41.00/sh on November 28, 2014. We expect its EPS to grow at a CAGR of 12%, from Php 2.03/sh in 2014 to Php 4.08/sh in 2020, driven by its market leadership with proven track record, strong growth potential in underpenetrated markets, and financial flexibility to pursue new ventures.

DOMINANT MARKET POSITION SUPPORTED BY LOCAL KNOWLEDGE AND PRESENCE CIC is the market leader in its core businesses namely air conditioning and refrigeration garnering market share of 37% and 25% respectively. It can strengthen its market position through margin expansion (reaching 20% EBITDA margin in 2020) driven by strong R&D capability, cost reduction efforts, and flexible operations. With its long operational history of over 50 years, CIC has built its highly reputable brands such as Carrier, Condura, Kelvinator, and Toshiba through its commitment to product innovation and adaptability to local consumer preferences. With its products available in 90% of all appliance stores nationwide, CIC has a strong market presence and a comprehensive after-sales support.

SOLID TOPLINE GROWTH IN UNDERPENETRATED MARKETS We expect CIC’s sales to grow at a CAGR of 10% for the next five years due to growing demand for air conditioners and refrigerators. Increasing purchasing power, as evidenced by a GDP per capita growth rate of 8% year-over-year, is expected to push penetration rates of air conditioners and refrigerators, which are currently at 6% and 35% respectively. With an expanding middle class and a steady influx of overseas remittances, household income is expected to grow by 7% year-over-year from 2013 to 2020. With the Philippines at a tipping point relative to its ASEAN neighbors (see Figure 13 and Figure 14), CIC aims to further increase its revenues through capitalizing the booming real estate industry that is growing at a CAGR of 9.3% from 2013 to 2020 using its relationships with tier one real estate developers.

HEALTHY CASH FLOW TO FUND OPERATIONS AND FUTURE MERGERS AND ACQUISITIONS CIC’s long-term goal is to provide comprehensive solutions for both its consumer and business & industrial segments, which it intends to achieve by sustaining its current business and pursuing strategic acquisitions and joint ventures. Moving forward, CIC plans to further strengthen its building and industrial solutions by acquiring businesses specializing in security systems, lighting fixtures, and fire safety. CIC aims to become the one-stop shop for real estate developers to drive sustainable sales growth thereby strengthening its leadership position and providing potential upside. CIC has the option to sustain its current business and finance its new ventures with internally generated funds and borrowings. With strong cash flows that average at Php 1.1 bn annually from 2015 to 2020 (see Figure 15), CIC can return value to its shareholders via dividends and support its capital expenditures through internally generated funds. Moreover, as of the third quarter of 2014, CIC is in a net cash position and has a gross debt-to-equity ratio of only 27%. CIC’s debt-to-asset ratio has also been consistently low at 14% (see Figure 16) highlighting the company’s low risk and enabling the company to fund its future mergers and acquisitions with debt at a low marginal cost of capital.

0%

20%

40%

60%

80%

100%

120%

0 20 40 60 80

GDP per Capita, PPP (in USD '000)

Other Asian Countries

Philippines

Trend Line

0%

25%

50%

75%

100%

125%

150%

0 20 40 60 80

GDP per Capita, PPP (in USD '000)

Other Asian Countries

Philippines

Trend Line

0

300

600

900

1200

1500

20

14E

20

15F

20

16F

20

17F

20

18F

20

19F

20

20

F

Thousa

nds

CCAC CDI

in Php mn

0.00%

4.00%

8.00%

12.00%

16.00%

20

14E

20

15F

20

16F

20

17F

20

18F

20

19F

20

20

F

Ateneo de Manila University Student Research | 6

TABLE 5. TARGET PRICE BREAKDOWN

SUBSIDIARY VALUE PER SHARE1

CCAC 35.74

CDI 11.42

COPI 3.10

CMIP 0.24

CIC 50.49 1Value attributable to CIC (in Php)

Source: Team Estimates

FIGURE 17. CIC FORECASTED FCF TO FIRM

Source: Team Estimates

FIGURE 18. CCAC AND CDI SALES GROWTH RATES

Source: Team Estimates

FIGURE 19. CCAC AND CDI SALES FORECAST

Source: Team Estimates

FIGURE 20. CCAC AND CDI EBITDA MARGINS

Source: Team Estimates

VALUATION METHODS We used the Sum-of-Parts Valuation method and Discounted Free Cash Flow to Firm (DCF) analysis to arrive at our target price of Php 50.49/sh, which presents an upside of 23.14%. CIC operates through its four subsidiaries, namely CCAC, CDI, COPI, and CMIP. Its revenues are independently forecasted using weighted key driver growth rates with a premium, which slowly decreases over the years. The free cash flows derived from the sales forecasts are then discounted using their respective WACCs. We computed a moving WACC for CCAC ranging from 9.54% to 9.63%, based on a targeted capital structure of 10% debt and 90% equity. On the other hand, a constant WACC of 10.40% for CDI, COPI, and CMIP is applied, based on a 100%-equity capital structure. Lastly, we calculated a terminal growth rate of 2.60% 2.13%, 3.25%, and 3.31% for CCAC, CDI, COPI, and CMIP, respectively.

POSSIBLE INVESTMENT RISKS CIC experiences market risk in the form of volatilities in exchange rates, interest rates, and commodity prices. Aside from this, investors must also be aware of the industry risk like the intense rivalry in competition. Operational risks that CIC may face include unplanned breakdown of plant and equipment and the disruption of manufacturing and sales due to its heavy dependence on importation of raw materials and commercial units. A detailed discussion of the risks, together with the company’s response to mitigate these, is presented in the Investment Risk section and is followed by a Sensitivity and Scenario Analysis.

FIGURE 24. SHARE PRICE MOVEMENT AND NEWS FLOW

Source: Company Data, Thomson Reuters

Valuation

SUM OF PARTS - DCF VALUATION STRUCTURE We used the Sum-of-Parts Valuation method and Discounted Free Cash Flow to Firm (DCF) analysis in order to arrive at our target price of Php 50.49/s (see Table 5 and Figure 17), which presents an upside of 23.14% (see Appendix D-1). Using the Sum-of-Parts valuation structure, the forecast of CIC’s financials is divided into four business units, namely CCAC, CDI, COPI, and CMIP, which are treated independently.

ECONOMIC OUTLOOK AND COMPETENCIES SIGNAL GROWTH AND MARGIN EXPANSION IN CIC Core Business: CCAC and CDI The sales of CCAC and CDI are forecasted using two components – (1) weighted key driver growth rates and (2) a premium. We derived the weighted key driver growth rates by decomposing CIC’s key business segments, namely consumer solutions and building and industrial solutions. These segments are further divided into different categories where growth drivers are determined and weighted according to their impact on the business segment (see Appendix D-6). After which, a regression analysis is conducted to show the statistical significance and explanatory power of the key drivers used (see Appendix D-12). As both CCAC and CDI sales are growing above the industry average for the past decade, a premium is calculated for each of the subsidiaries to account for this faster growth rate. Operating in an underpenetrated market, we believe that both subsidiaries will continue to enjoy the benefits of a premium that slowly decreases from 2.80 for CCAC and 2.41 for CDI in 2014 to 0 at the terminal phase in 2021 (see Appendix D-13). The resulting industry growth rates, without the premium, are 8.88% and 9.50% for air conditioners and refrigerators respectively. Incorporating the premium yields a growth rate of 11.68% and 11.91% for CCAC and CDI respectively, both of which are at a diminishing marginal rate of decline thereafter until it reaches a sustainable growth in 2021 (see Figure 18). The growth rate components of CCAC and CDI are outlined in Appendix D-7 and D-8. CIC’s core businesses rely heavily on importing commodities such as steel, copper, and aluminum. To take into account the fluctuations of the prices of these commodities, we have adjusted the COGS margin of CCAC and CDI to match the forecasted movement of the market (see Appendix D-18), resulting to a COGS margin of 60.83% for CCAC and 80.92% for CDI. With CIC’s flexibility in operations and strong commitment towards efficiency through its cost reduction efforts, CCAC’s EBITDA margin is expected to be 22%, which is significantly higher than the industry average of 10%. As for CDI, EBITDA margin is expected to reach 8% by 2014-2016, 10% by 2017-2019, and 12% from 2020 onwards (see Figure 20).

20

14E

20

15F

20

16F

20

17F

20

18F

20

19F

20

20

F 0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

8.0%

9.0%

10.0%

11.0%

12.0%

20

14E

20

15F

20

16F

20

17F

20

18F

20

19F

20

20

F

CCAC CDI

0

2

4

6

8

10

20

14E

20

15F

20

16F

20

17F

20

18F

20

19F

20

20

F

CCAC CDI

in Php bn

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

20

14E

20

15F

20

16F

20

17F

20

18F

20

19F

20

20

F

CCAC CDI

Semi-Annual Dividend

Declaration

Finalized JV with Otis

Annual Report Release

Quarterly Report Release

News Release about JV

with Midea

Annual Stockholder's

Meeting

0%

50%

100%

150%

200%

250% 11

/27/

13

12/1

1/13

12/2

5/1

3

1/8/1

4

1/22/1

4

2/5

/14

2/1

9/1

4

3/5

/14

3/1

9/1

4

4/2

/14

4/1

6/1

4

4/3

0/1

4

5/1

4/1

4

5/2

8/1

4

6/1

1/14

6/2

5/1

4

7/9/1

4

7/23/1

4

8/6

/14

8/2

0/1

4

9/3

/14

9/1

7/14

10/1

/14

10/1

5/1

4

10/2

9/1

4

11/1

2/1

4

11/2

6/1

4

CIC

Share

Pri

ce a

nd P

SE

i

(as

% o

f 11

/27/

13 V

alu

es)

CIC PSEi

Ateneo de Manila University Student Research | 7

FIGURE 21. COPI NET PROFIT MARGINS

Source: Team Estimates

FIGURE 22. COPI FORECASTED SALES, IN PHP MN

Source: Team Estimates

FIGURE 23. CMIP REVENUE FORECAST,

IN PHP MN

Source: Team Estimates

TABLE 6. WACC COMPUTATIONS (2014)

INPUT VALUE METHODOLOGY

Beta 1.02 Peers’ Beta

Risk-free Rate

4.75% T-Bond rate (25 years)

Market Premium

5.56% Bloomberg

Cost of Equity

10.40% Team Computations

Cost of Debt

2.63% Prevailing cost of debt

Debt to Equity Ratio

10:90 Forecasted Capital Structure

WACC 9.54% (2014)

Team Computations

Source: Team Analysis

TABLE 7. TERMINAL GROWTH RATES

SUBSIDIARY TERMINAL GROWTH

RATE

CCAC 2.60%

CDI 2.13%

CMIP 3.25%

COPI 3.31% Source: Team Analysis

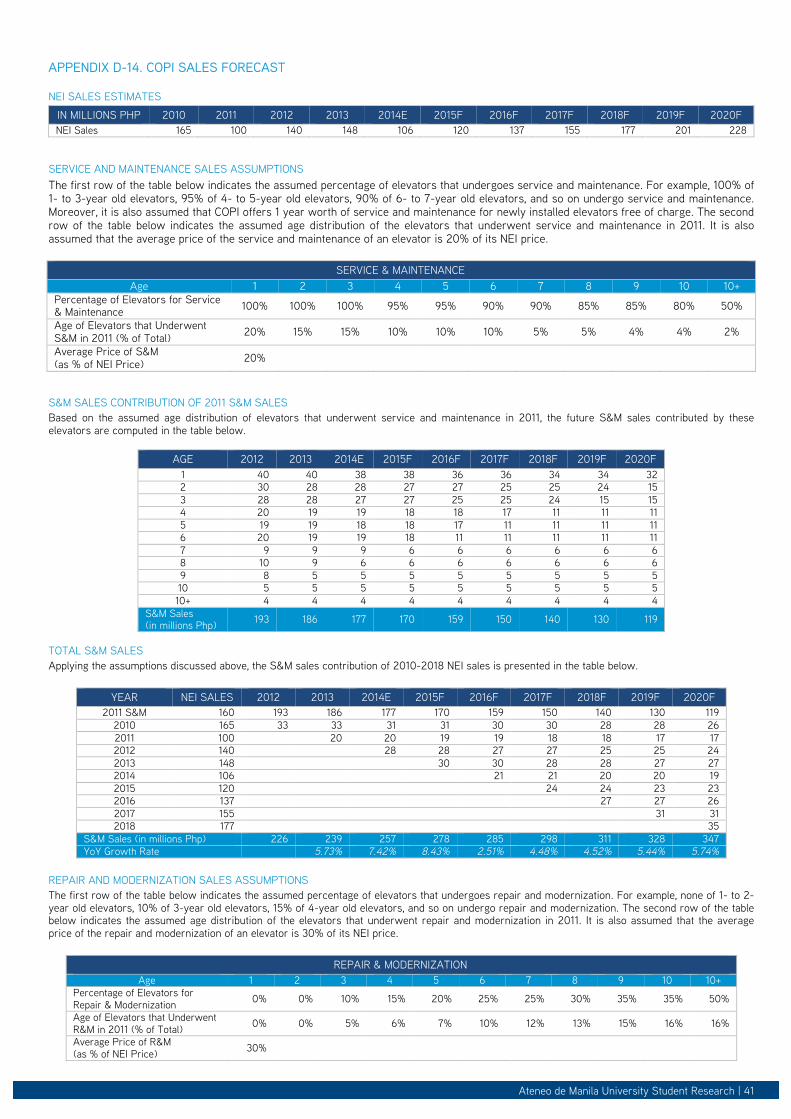

Growth and Expansion Business: COPI COPI has three revenue streams, namely new equipment and installation (NEI), services and maintenance (S&M), and repair and modernization (R&M). The 13.58% growth rate of COPI’s NEI is based on the country’s booming residential and non-residential building industry growth rate of 11.40% plus a premium of 2.18% (see Appendix D-9). This growth rate is backed by CIC’s extensive after-sales support and strong relationship with tier one real estate developers. We expect a 9% net profit margin from NEI sales, which is consistent with Otis’ historical performance. In forecasting S&M and R&M sales, a rainfall model is built to take into account the decreasing retention rate of customers who avail of after-sales services as their equipment ages, and the increasing probability for older machines to break down (see Appendix D-14). The net profit margins of S&M and R&M are expected to be at 20%-30% in 2014-2020 (see Figure 21). CIC expects COPI’s revenues to reach Php 342 mn (see Figure 22), which is equivalent to 3.8% of CIC’s forecasted total revenue in 2014.

Growth and Expansion Business: CMIP As a distributor of a relatively new brand in the country, CMIP is not expected to be profitable in its first two years of operations as current efforts are focused on building the Midea brand. It is expected to incur a loss in 2014, and break even in 2015. However, CIC’s wide-scale distribution network and strong brand reputation are expected to drive CMIP’s sales by a CAGR of 10.40% (see Appendix D-10) from 2014 to 2020, reaching Php 452 mn in sales (see Figure 23). The sales growth rate is calculated by adding a 2.18% premium to the country’s consumer appliance CAGR of 8.22%. We expect CMIP’s net profit margin to reach 2% in 2016, 3% in 2017, 4% in 2018, 6% in 2019 and stabilize at 7% thereafter. This net profit margin is highly comparable to similar firms such as Midea Group China, which has an EBITDA margin of around 8.65% (see Appendix D-20). CMIP’s net profit margin is expected to be lower since it does not manufacture its products locally. CMIP is estimated to generate Php 250 mn sales, which is equivalent to 2.76% of CIC’s forecasted total revenue for the year 2014.

CAPITAL EXPENDITURE CIC’s annual capital expenditure is composed of maintenance CAPEX and growth CAPEX. CIC’s maintenance capital expenditure is expected to be stable at around Php 55 mn every year under the assumption that CIC reinvests back its annual depreciation expense as maintenance CAPEX. For its growth CAPEX, the management does not see the need to increase the plant manufacturing capacity despite the expected increase in sales. It currently operates with two working shifts, and can be increased to three or four shifts should the need arise. However, the company incurs Php 20 mn in growth CAPEX every five years for its grill modernization project. This project aims to keep CIC’s air conditioner grill designs up to date.

WEIGHTED AVERAGE COST OF CAPITAL (WACC) Using pure-play method, we computed CIC’s beta by adjusting the average unlevered beta of its peers based on CIC’s capital structure and arrived at a value of 1.02 (see Appendix D-16). With a market premium of 5.56% and a risk-free rate of 4.75%, we obtained a 10.40% cost of equity (see Table 6). On the other hand, CIC’s cost of debt is subject to the fluctuations of the country’s interest rates as we expect its short-term debt to be rolled over to finance the company’s future acquisitions. CIC’s prevailing cost of debt is around 2.63% in 2014, which is expected to move to as high as 3.92% in 2018, and eventually dip down to 3.07% at the terminal phase. Accounting for interest rate fluctuations, we arrived at a moving WACC ranging from 9.54% to 9.63% for CCAC, based on the capital structure of 10% debt and 90% equity (see Table 6 and Appendix D-19). With a 100%-equity capital structure, a constant WACC of 10.40% is used for CDI, COPI, and CMIP.

TERMINAL GROWTH RATE The terminal growth rates for CCAC, CDI, and CMIP are based on the growth rates of mature air conditioning, refrigeration, and consumer appliance markets, respectively. The selection of such markets is based on their geographic location and penetration rates. The terminal growth rate for COPI is based on the sales growth rates of selected elevator companies that operate in mature markets. The terminal growth rate used for CCAC, CDI, COPI, and CMIP are 2.60%, 2.13%, 3.25%, and 3.31% respectively (see Table 7). A detailed discussion on the computation of these growth rates is presented in Appendix D-17.

RELATIVE VALUATION

TABLE 10. PEER COMPARABLE RATIOS

COMPANY P/E PRICE/ FCF EV/ EBITDA EV/ SALES PEG RATIO

CIC 20.90 4.53 9.72 1.72 0.65

Ree (VNM) 8.80 7.71 11.96 2.69 0.42

Singer (THA) 14.06 36.64 10.32 1.77 1.20

Daikin (JPN) 21.04 23.56 10.65 1.48 1.33

Mitsubishi (JPN) 16.25 8.64 6.93 0.71 2.60

Toshiba (JPN) 29.72 33.60 8.33 0.62 2.28

Hitachi (JPN) 13.67 120.79 7.70 0.83 1.22

Peer Median 15.16 28.58 9.33 1.16 1.27 Legend: Favorable Unfavorable Source: Bloomberg, Team Estimates

A relative valuation analysis is conducted among Asian peers of CIC (see Appendix D-15 for Peer Selection Criteria). CIC posted a relatively higher P/E (TTM) ratio of 20.90x compared to its peers trading at 15.16. However, this high P/E ratio is justified by its PEG (TTM) ratio of 0.65x, which is significantly lower than that of the industry, thus supporting our BUY recommendation.

0%

5%

10%

15%

20%

25%

30%

20

14E

20

15F

20

16F

20

17F

20

18F

20

19F

20

20

F

New Equipment and Installation

Service and Maintenance

Repair and Modernization

0%

5%

10%

15%

0

200

400

600

800

20

14E

20

15F

20

16F

20

17F

20

18F

20

19F

20

20

F

YoY

Gro

wth

Rate

CO

PI S

ale

s (i

n P

hp m

n)

Repair and Modernization Service and Maintenance New Equipment and Installation

-200

-100

0

100

200

300

400

500

600

20

14E

20

15F

20

16F

20

17F

20

18F

20

19F

20

20

F

Revenues Net Income (Loss)

in Php

mn

Ateneo de Manila University Student Research | 8

Financial Analysis

TABLE 11. CCAC AND CDI KEY RATIOS

KEY RATIOS CCAC CDI

Industry Median

2012 2013 2014E 2015F 2016F 2012 2013 2014E 2015F 2016F

Profitability Ratios

Gross Profit Margin (%) 29.65 39.22 38.01 39.40 38.35 39.36 17.39 19.47 19.38 18.18 19.29

EBITDA Margin (%) 10.08 20.20 22.53 22.64 21.63 22.61 4.24 5.47 8.01 7.85 7.72

Net Income Margin (%) 6.30 13.59 15.31 15.37 14.64 15.33 1.86 2.29 4.50 4.50 4.50

Liquidity Ratios

Quick Ratio 0.91 1.95 1.89 1.29 1.52 1.80 0.73 1.39 1.42 1.41 1.44

Current Ratio 1.78 2.42 2.45 1.60 1.85 2.14 1.08 2.15 2.11 2.10 2.13

Activity Ratios

Days of Sales Outstanding 79.33 87.46 81.39 79.31 85.62 85.82 114.66 122.89 113.38 114.02 114.25

Days of Inventory on Hand 74.00 73.24 68.89 69.03 66.06 67.27 57.76 76.96 73.39 70.76 71.88

Number of Days Payables 54.62 109.19 113.04 107.16 103.81 105.72 124.87 129.94 97.59 113.22 115.00

Cash Conversion Cycle 89.74 51.50 37.25 41.18 47.88 47.37 47.55 69.92 89.18 71.56 71.13

Cash Flow Ratios

Cash Flow-to-Revenue 0.11 0.14 0.14 0.04 0.03

Cash Return-on-Equity 0.28 0.30 0.28 0.11 0.10

Cash Flow per Share 1.90 2.66 3.05 0.30 0.31

Dividend Coverage Ratio 2.64 3.31 3.60 2.99 2.73

DuPont Analysis

Tax Burden 0.63 0.70 0.70 0.70 0.70 0.70 0.67 0.65 0.70 0.70 0.70

Interest Burden 1.06 1.00 1.00 0.98 0.98 0.98 0.98 0.88 1.00 1.00 1.00

EBIT Margin (%) 6.26 19.73 22.26 22.40 21.35 22.36 2.71 3.70 6.43 6.43 6.43

Asset Turnover 0.91 1.62 1.63 1.44 1.21 1.15 1.79 1.63 1.71 1.68 1.68

Leverage 2.39 1.59 1.66 1.80 1.82 1.69 6.52 2.80 1.79 1.82 1.82

Return on Equity (%) 13.24 35.78 42.28 39.72 32.36 29.78 20.83 9.69 13.76 13.71 13.72 Source: Team Estimates

FIGURE 25. CIC FORECASTED SALES, IN PHP BN

Source: Team Estimates

FIGURE 26. CCAC AND CDI EBITDA MARGIN VS. INDUSTRY MEDIAN

Source: Company Data, Team Estimates

FIGURE 27. CIC CASH RATIO VS. INDUSTRY MEDIAN

Source: Company Data, Team Estimates

SUSTAINABLE GROWTH OF CORE BUSINESS CIC posted revenues of Php 7.5 bn and net earnings of Php 866 mn in 2013. With the strong growth potential of the air conditioning and refrigeration markets in the country, we expect CIC to double its revenues to Php 16 bn by 2020 (see Figure 25), translating into net earnings of Php 2.1 bn. With rising GDP per capita and a booming real estate industry, we expect CCAC’s revenues to grow at a CAGR of 9.83% from 2014 to 2020 and CDI’s sales to rise at a CAGR of 10.21% from 2014 to 2020.

EXPANDING BUSINESS THROUGH M&A CIC’s recent ventures on COPI and CMIP are expected to contribute revenues of Php 1 bn or 6.43% of total sales, and net income of Php 138 mn or 6.57% of total net income in 2020. Furthermore, this expansion is expected to drive CIC’s profitability to a 19.71% EBTIDA margin with COPI’s high-margin after-sales services having a net income margin of 30% in 2020. These subsidiaries are also expected to contribute 6.50% of CIC’s CFO in 2020.

HIGH OPERATIONAL EFFICIENCY LEADS TO SUPERIOR MARGINS CIC has a strong commitment to operational efficiency with its adoption of UTC’s Achieving Competitive Excellence (ACE) System that ensures the efficiency and effectiveness of its manufacturing operations. This is evident in CIC’s increasing fixed asset turnover, reaching 83.13 in 2020, and its total asset turnover of 1.45 in 2014, which is 59% higher than the peer median of 0.91. It also employs operational strategies to protect its profits such as its outsourcing to “negosyo partners.” Moreover, CIC’s aggressive efforts in cost reduction are expected to contribute Php 120 mn in savings in 2015, driving EBITDA margins to 19.71%. With these, we expect CIC to achieve EBITDA margins of around 22% for CCAC and 10% for CDI starting 2017 (see Figure 26).

CASH-GENERATING ENGINE ENABLING FINANCIAL FLEXIBILITY CIC is highly liquid with a cash ratio of 0.62 in 2014, which is 51% higher than the peer median of 0.41. Its strong liquidity position is supported by its well-managed inventory and strong bargaining power against suppliers, as exhibited by its CCC of 50 days, which is 44% lower than the peer median. This strong liquidity position enables CIC to fulfill its 30% dividend policy with a dividend coverage ratio of around 3.7x starting 2014. Furthermore, with a CFO/CAPEX of 22x in 2016, CIC has the flexibility to internally finance its operations and capital expenditures. We expect this to be sustained with CIC’s reliable cash flows, as reflected in its high Cash Flow Ratio (CFO/Average Current Liabilities) of 0.37 in 2014, which is 95% higher than the peer median (see Figure 27). The reliability of CIC’s cash flows is further supported by the company’s high level of profitability. Its strong financial position highlights the company’s financial flexibility to expand its business through internally generated funds.

UNLEVERAGED POSITION ENABLES CIC TO FINANCE NEW VENTURES CIC is highly unleveraged with no long-term debt from 2011 to 2013. It currently has a short-term debt of Php 1 bn that is expected to roll over, pegging its debt-to-asset ratio to 11% in 2016, which is 56% lower than the peer median of 25%. With its minimal debt and superb credit rating, CIC has the ability to acquire new debt at a low marginal cost of capital to fund its future mergers and acquisitions.

0.0

5.0

10.0

15.0

20.0

20

14E

20

15F

20

16F

20

17F

20

18F

20

19F

20

20

F

CCAC CDI COPI CMIP

in Php

bn

0%

5%

10%

15%

20%

25%

2012 2013 2014E 2015F 2016F

CCAC CDI Industry Median

0%

10%

20%

30%

40%

50%

20

14E

20

15F

20

16F

20

17F

20

18F

20

19F

20

20

F

CIC Industry Median

Ateneo de Manila University Student Research | 9

FIGURE 28. RISK MATRIX

IMP

AC

T

High

h OR1

Mediu

m

OR2 IR1 MR3

OR4 MR1 IR2

OR3 MR2

Low

w

Low Medium High

PROBABILITY

Source: Team Analysis

TABLE 12. RISK ANALYSIS

RISKS MITIGATING FACTORS

Market Risk

Foreign Exchange Risk

Acquisition of future and forward contracts for price hedging

Short Term Locked-In Exchange Rate

Reinvestment Rate Risk

Good credit rating

Solid company financials

Commodity Price Risk

Price hedging of raw materials

60-days supplier contracts to lock-in prices

Industry Risk

Intense Rivalry in the Competition

Cost Reduction

Strong Track Record

Leading and Trusted Brands

Continuous Product Development

Increasing Electricity Costs

Energy Efficient Air Conditioning Units and Refrigerators

Operational Risk

Unplanned Breakdown of Plant and Equipment

Leading and Trusted Brands

Continuous Product Development

Heavy Dependence on Importation

Increasing Capacity of Production Plant

Multi Sourcing Strategy

Corporate Governance

Two Independent Board Members

Strong Talent Acquisition Programs

Execution Risk

Implementation of Industry Best Practices

Hiring of Abled and Experienced Professionals

Source: Team Analysis

Investment Risks The investment risks are summarized in Figure 28 and its mitigating factors are outlined in Table 12.

MARKET RISK | FOREIGN EXCHANGE RISK (MR1) A substantial portion of CIC’s raw materials is imported from suppliers abroad. Major sources include Taiwan and China for aluminum; Malaysia and China for copper; and Taiwan, China, Korea, and Italy for steel. Given this, fluctuations in the exchange rate between the Philippine Peso and foreign currencies may increase the company’s expenses and reduce profitability. This could adversely affect the company’s business, financial condition, and results of operations. To counter this impending risk, the company invests in future and forward contracts to hedge on foreign currency exchanges.

MARKET RISK | REINVESTMENT RATE RISK (MR2) Based on the financial statements of the company, CIC only has short-term loans. The management may opt to roll this over in the future, thus needing to renew their current rate. This exposes CIC to reinvestment rate risk as the current interest rate in the market is rising. However, due to CIC’s good credit standing, the management will be able to bargain for lower rate.

MARKET RISK | COMMODITY PRICES RISK (MR3) As a manufacturer, CIC requires certain raw materials such as copper, aluminum, and steel. The prices of these raw materials heavily fluctuate due to the global market conditions. Any increase in the raw material prices will significantly increase the company’s cost of goods sold, but CIC cannot readily increase its selling retail price and pass on these additional costs. This, in effect, would decrease the company’s margins. To mitigate this risk, CIC engages in price hedging activities and locks-in prices with its suppliers for certain raw materials.

INDUSTRY RISK | INTENSE RIVALRY IN THE COMPETITION (IR1) With the intense competition in the air conditioning and refrigeration industry at hand, CIC’s ability to maintain or increase its market share and profitability may be limited. To be able to thrive in an increasingly competitive market, CIC is implementing continuous cost reduction measures and numerous product developments in both its air condition and refrigeration manufacturing facilities.

INDUSTRY RISK | INCREASING ELECTRICITY COSTS DUE TO SHORTAGE (IR2) Air conditioners and refrigerators are few of the household appliances known to have high electricity consumption. The impending increase in electricity costs discourages consumers to buy air conditioners and refrigerators. To address this issue, CIC is continuously developing energy-efficient air conditioners and refrigerators such as the Carrier Optima that provides uncompromised cooling with low electricity consumption, and additional 40% cost savings with the company’s patented Energy Savings Plug.

OPERATIONAL RISK | UNPLANNED BREAKDOWN OF PLANT AND EQUIPMENT (OR1) CIC currently produces all of its residential air conditioners and refrigerators at a single factory location in Light Industry and Science Park in Cabuyao, Laguna, Philippines. Due to lack of geographical diversification, CIC’s manufacturing operations is exposed to greater risks of interruptions from plant or equipment breakdown. Any unexpected circumstance such as power shortage, natural disasters, or equipment breakdown that may cause CIC’s entire manufacturing operations to stop can drastically affect CIC’s supply of air conditioners and refrigerators. To prevent any downtime caused by equipment breakdown, CIC invests approximately Php 50 mn to Php 60 mn annually to rehabilitate and maintain the company’s manufacturing facility.

OPERATIONAL RISK | HEAVY DEPENDENCE ON IMPORTS (OR2) CIC imports roughly 70% of the raw materials and component parts used in the production of air conditioners and refrigerators. Moreover, CIC imports all of its commercial air conditioning and refrigeration units. Given this, the price, availability, and timely delivery of the various raw materials and component parts largely affect CIC’s operations. To mitigate such risk, the company uses multiple sourcing strategies, with supply forecasts set every three to six months and pricing terms set annually, depending on the supplier.

OPERATIONAL RISK | CORPORATE GOVERNANCE RISK (OR3) CIC started as a family business of the Concepcions. As the company starts to venture out and be a public entity, issues may arise such as building credibility and ensuring transparency and accountability. To be able to address this problem, CIC is taking necessary actions to ensure the presence of strong and independent elements in the board such as hiring two independent auditors and acquiring talents both locally and from abroad.

OPERATIONAL RISK | EXECUTION RISK (OR4) CIC’s recent joint venture and acquisition, COPI and CMIP, are still in the transition and gestation period with the new management. With this, there are still uncertainties whether CIC’s new management can turn around the business and induce growth into the new JVs. To ensure the success of these new business ventures, CIC implements industry best practices and hires professionals with more than 20 years of industry experience to manage the business.

Sensitivity and Scenario Analysis To determine the effect of certain investment risks on the intrinsic value of CIC, a sensitivity and scenario analysis is conducted. The first part of the conducted sensitivity analysis determines the minimum changes in certain variables that may shift our recommendation (see Table 15 and Table 16). After conducting such, we evaluate the impact of possible changes in the weighted cost of capital, industry sales growth, and commodity price growth rate to the target price (see Table 14, Table 17, and Table 18).

Ateneo de Manila University Student Research | 10

1 9.54% for CACC 2014

TABLE 13. RATING GUIDE

RATING GUIDE

BUY HOLD SELL

Greater Than 10% upside

0 to 10% Upside

Negative Returns

> Php 45.1/sh Php 41 – 45.1/sh < Php

41/share Source: Team Analysis

TABLE 14. WACC SENSITIVITY ANALYSIS

WEIGHTED COST OF CAPITAL

PRICE/SHARE

14.00% 30.62

13.00% 33.92

12.00% 37.94

11.56% 40.00

11.00% 42.92

10.81% 44.01

10.00% 49.26

9.54% 50.49

9.00% 57.59

8.00% 69.01

7.00% 85.60 Source: Team Analysis

FIGURE 29. WACC SENSITIVITY ANALYSIS

Source: Team Analysis

TABLE 15. VALUATION WITHOUT CMIP AND COPI

CCAC 35.74

CDI 11.42

CIC 47.15

(15% Upside) Source: Team Analysis

TABLE 16. SENSITIVITY ANALYSIS ON ASSUMPTIONS

CHANGES IN VARIABLES TO SHIFT RECOMMENDATION TO HOLD/SELL

Variable Base Case Hold Change in

Percentage Points

Sell Change in

Percentage Points

Industry Growth Rate for CCAC 8.88% 6.03% (2.85%) 4.01% (4.87%)

Industry Growth Rate for CDI 9.50% 1.60% (7.90%) (6.80%) (16.30%)

Weighted Cost of Capital 9.54%1 10.81% 1.27% 11.56% 2.02%

CCAC Terminal Growth Rate 2.60% 0.44% (2.16%) (1.70%) (4.30%)

CDI Terminal Growth Rate 2.13% (17.80%) (19.93%) (100%) (102.13%) Source: Team Analysis

TABLE 17. SCENARIO ANALYSIS: CCAC AND CDI SALES GROWTHS

INDUSTRY SALES GROWTH FOR CCAC

IN

DU

STR

Y S

ALE

S

GR

OW

TH

FO

R C

DI

10.0% 9.0% 8.88% 8.0% 7.0% 5.0% 3.0% 1.0%

11.0% 54.99 52.43 52.13 50.01 47.73 43.53 39.80 36.48

10.0% 53.88 51.32 51.02 48.91 46.62 42.43 38.69 35.37

9.5% 53.35 50.79 50.49 48.38 46.09 41.90 38.16 34.84

9.0% 52.84 50.28 49.98 47.86 45.58 41.38 37.65 34.32

5.0% 49.26 46.7 46.40 44.28 42.00 37.81 34.07 30.75

3.0% 47.79 45.23 44.92 42.81 40.53 36.33 32.60 29.27

1.0% 46.49 43.94 43.63 41.52 39.24 35.04 31.30 27.98 Source: Team Analysis

We also conducted a sensitivity analysis on the fluctuations of the commodity prices of steel, aluminum, and copper. Historically, these commodity prices fluctuate within ±200 basis points. Table 18 shows the impact of commodity price growth changes on CIC’s target price. A 100 basis point increase in commodity price growth rate translates to a 100 basis point decrease in CIC’s share price. Thus, a ±200 basis point change in the commodity price growth will not change our BUY recommendation.

TABLE 18. SCENARIO ANALYSIS: COMMODITY PRICE GROWTH RATE

CHANGE IN COMMODITY PRICES GROWTH RATE

COGS MARGIN CIC SHARE PRICE CCAC CDI

(200 basis points) 59.99% 80.01% 51.89

(100 basis points) 60.41% 80.46% 51.19

Base Case 60.83% 80.92% 50.49

+100 basis points 61.25% 81.38% 49.79

+200 basis points 61.67% 81.83% 49.09

Source: Team Analysis One of the variables that will significantly affect our valuation is the WACC. The current moving WACC used to discount CIC’s free cash flows ranges from 9.54% to 9.63% depending on the Philippine interest rates for the corresponding years. Based on the sensitivity analysis conducted, WACC should increase by 127 basis points reaching 10.81% before our recommendation changes to hold. Moreover, WACC should reach as high as 11.56% for our recommendation to change from buy to sell (see Table 14 and Figure 29). As mentioned above, CIC is exposed to execution risk with the company’s recent JVs, COPI and CMIP. CIC expects to turn around its recent joint ventures in the years 2014 to 2015. Despite the company’s efforts to integrate COPI and CMIP into its core business, there are still uncertainties regarding how these recent joint ventures will fare in the succeeding years. Our base case valuation indicates that both COPI and CMIP contribute roughly Php 3.34 per share. Without both, the target price of CIC will fall to Php 47.15 per share, representing 15% upside from the Php 41 per share closing price last November 28, 2014 (see Table 15).

0

20

40

60

80

100

7.00% 12.00% 17.00%

CIC

Share

Pri

ce (

Php)

WACC

Buy Sell Hold

Ateneo de Manila University Student Research | 11

Table of Contents APPENDIX A: COMPANY OVERVIEW ............................................................................................................................................ 12

Appendix A-1. Glossary of Terms ................................................................................................................................................................................... 12 Appendix A-2. CIC Subsidiaries ...................................................................................................................................................................................... 14 Appendix A-3. Overall Distribution ................................................................................................................................................................................. 15 Appendix A-4. Business Model Canvas .......................................................................................................................................................................... 15

APPENDIX B: FINANCIAL STATEMENTS ..................................................................................................................................... 16 Appendix B-1. Consolidated Balance Sheet ................................................................................................................................................................... 16 Appendix B-2. Consolidated Income Statement ............................................................................................................................................................ 16 Appendix B-3. Consolidated Cash Flow Statement ........................................................................................................................................................ 17 Appendix B-4. Consolidated Statement of Retained Earnings ....................................................................................................................................... 17 Appendix B-5. CCAC Balance Sheet .............................................................................................................................................................................. 18 Appendix B-6. CCAC Income Statement ........................................................................................................................................................................ 19 Appendix B-7. CCAC Cash Flow Statement ................................................................................................................................................................... 19 Appendix B-8. CCAC Statement of Retained Earnings ................................................................................................................................................. 19 Appendix B-9. CDI Balance Sheet .................................................................................................................................................................................. 20 Appendix B-10. CDI Income Statement .......................................................................................................................................................................... 20 Appendix B-11. CDI Cash Flow Statement ..................................................................................................................................................................... 21 Appendix B-12. CDI Statement of Retained Earnings ................................................................................................................................................... 21 Appendix B-13. COPI Balance Sheet .............................................................................................................................................................................. 22 Appendix B-14. COPI Income Statement ........................................................................................................................................................................ 22 Appendix B-15. COPI Statement of Cash Flows ............................................................................................................................................................ 22 Appendix B-16. COPI Statement of Retained Earnings ................................................................................................................................................. 23 Appendix B-17. CMIP Income Statement ....................................................................................................................................................................... 23

APPENDIX C: INDUSTRY OVERVIEW AND COMPETITIVE POSITIONING .................................................................................. 24 Appendix C-1. Porter’s Five Forces Analysis ................................................................................................................................................................ 24 Appendix C-2. SWOT Analysis ....................................................................................................................................................................................... 26 Appendix C-3. Cost Reduction Methods ......................................................................................................................................................................... 27 Appendix C-4. Possible Mergers and Acquisitions ........................................................................................................................................................ 27

APPENDIX D: VALUATION ............................................................................................................................................................. 30 Appendix D-1. Summary of Sum of Parts and DCF Methods ....................................................................................................................................... 30 Appendix D-2. CCAC Free Cash Flow and Valuation .................................................................................................................................................... 31 Appendix D-3. CDI Free Cash Flow and Valuation ........................................................................................................................................................ 31 Appendix D-4. COPI Free Cash Flow and Valuation ..................................................................................................................................................... 31 Appendix D-5. CMIP Free Cash Flow and Valuation ..................................................................................................................................................... 31 Appendix D-6. Key Drivers for Growth .......................................................................................................................................................................... 32 Appendix D-7. CCAC Growth Rate ................................................................................................................................................................................. 33 Appendix D-8. CDI Growth Rate ..................................................................................................................................................................................... 34 Appendix D-9. COPI Growth Rate .................................................................................................................................................................................. 34 Appendix D-10. CMIP Growth Rate ................................................................................................................................................................................ 34 Appendix D-11. Summary of Growth Rates ................................................................................................................................................................... 35 Appendix D-12. Regression Backing .............................................................................................................................................................................. 36 Appendix D-13. Premium ................................................................................................................................................................................................ 40 Appendix D-14. COPI Sales Forecast ............................................................................................................................................................................. 41 Appendix D-15. Criteria for Peers Selection .................................................................................................................................................................. 42 Appendix D-16. Beta Calculation ..................................................................................................................................................................................... 42 Appendix D-17. Terminal Growth Rate Calculation ....................................................................................................................................................... 43 Appendix D-18. Commodity Price Adjustment ............................................................................................................................................................... 44 Appendix D-19. Moving WACC ........................................................................................................................................................................................ 45 Appendix D-20. Peer Group of CMIP ............................................................................................................................................................................. 45

APPENDIX E: FINANCIAL ANALYSIS ............................................................................................................................................ 46 Appendix E-1. CIC Key Ratios ........................................................................................................................................................................................ 46 Appendix E-2. CCAC Key Ratios ..................................................................................................................................................................................... 47 Appendix E-3. CDI Key Ratios ......................................................................................................................................................................................... 48 Appendix E-4. COPI Key Ratios ...................................................................................................................................................................................... 49 Appendix E-5. Key Ratios of Peers ................................................................................................................................................................................ 49

APPENDIX F: CORPORATE GOVERNANCE .................................................................................................................................. 50 Appendix F-1. Summary of Corporate Governance and Social Responsibility ............................................................................................................ 50 Appendix F-2. Board of Directors .................................................................................................................................................................................. 51 Appendix F-3. Senior Management ................................................................................................................................................................................ 52

Ateneo de Manila University Student Research | 12

Appendix A: Company Overview APPENDIX A-1. GLOSSARY OF TERMS

CIC: CONCEPCION INDUSTRIAL CORPORATION