cfa1_corporate finance and equity investment training

TRANSCRIPT

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 1/177

December 28, 2011

CFA Level 1

Corporate Finance and Equity

Investments

James Lam, M.Sc. CFA

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 2/177

Introduction to Corporate FinanceWhat is f inance?

What is the distinction between f inancial and real assets?

What is corporate f inance?

What is the role of f inancial assets in corporate f inance?

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 3/177

Week 1Financial Markets and FinancialInstrumentsHow do f irms f inance their investments?

Ear nings (free cash flow, inter nal capital)

Equity capital (exter nal ± public or pr ivate)

Debt capital (exter nal)

Public and pr ivate capital

Trading of public capital

New issues

Secondar y trading

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 4/177

Equity IssuesFir st time a f irm seek s public equity is called an initial public

offer ing (IPO)

Pr imar y issue: new equity is issued

Secondar y issue: existing pr ivate equity is sold to outside investor s (most

pr ivatisations take this form)

Legal and under wr iting ser vices provided by investment bank s

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 5/177

Debt IssuesBank loans ± not publicly traded

Corporate Bonds ± traded actively in the secondar y market

Debt capital and equity capital account for most of the f irm¶s

f inancial capital

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 6/177

Def inition of DebtFixed claim

S pecif ies what needs to be repaid to the investor and when

Default r isk ± r isk that the repayment plan is not fulf illed

Conver sion options ± covenants that allow debt to be reclassif ied as equity

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 7/177

Def inition of EquityR esidual claim

Does not s pecif y a repayment plan

R epayment is def ined as the residual: whatever is not claimed by other

claim holder s should go to the equity holder s Voting r ights: Equity holder s normally have a r ight to vote on impor tant

corporate decisions

Mer ger s, takeover s

Lar ge investments

Board representation

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 8/177

Trends in Corporate FinanceGlobalisation

Deregulation

Financial innovation

Technological advances in the f inancial system

Secur itization

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 9/177

What you should take homeYou should be able to

Under stand the distinction between a f ixed claim and aresidual claim

List the main attr i butes of a debt claim

List the main attr i butes of an equity claim

Descr i be the ways in which f irms raise funds for new investment

Descr i be the difference between pr ivate and public equity

Descr i be the difference between bank loans and corporate bonds

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 10/177

R eadingsGr in blatt/Titman: Financial Markets and Corporate Strategy

Ch 1: over view of the process of raising capital for investment

Ch 2: over view of the process of raising debt capital

Ch 3: over view of the process of raising equity capital

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 11/177

Problems1. Why do f irms use under wr iter s when they issue new equity?

2. In what ways do you think it matter s that debt holder s have a

f ixed claim when equity holder s have not?

3. In what ways do you think it matter s that equity holder s

have voting r ights when debt holder s have not?

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 12/177

R eview problems1. Invest 95 and sell for 102 ± what is the retur n?

2. Invest 95 and sell for 102. Each transaction is char ged a 1%trading commission ± what is the retur n?

3. Invest 95 and sell for 102. You receive additional interest payments/dividends of 2 dur ing the holding per iod. What is the retur n?

4. Invest 95 and sell for 110 three year s later ± what is theannual retur n on your investment?

5. Invest 95 now and another 98 next year. In the following year you sell your investment for a total of 202. What is the

annual retur n on your investment?

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 13/177

Week 2:Valuing Financial Assets: Por tfolioToolsTool box

Expected por tfolio retur n

Por tfolio var iance

Covar iance between the retur n on two assets

Optimal investment

³Fair´ pr ice of an asset means that the value equals the

purchasing pr iceEven if pr ices are ³fair´ there are still ways of investing your

money that is better than other s

Risk Aver sion

Investor s demand compensation for including r isk in their por tfolio

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 14/177

Por tfolio weightsA por tfolio of f inancial assets can be represented in a

number of ways

The number of shares held in the var ious stock s (e.g. 1000shares in BT, 250 shares in Mark s&S pencer etc.)

The dollar-value held in the var ious stock s (e.g. £2,500 in

Lloyds Bank, £10,000 in Jar vis etc.)

As por tfolio weights: the dollar-weight of the var ious stock s (e.g. if total por tfolio is £100,000, then the por tfolio weight of

Lloyds is 0.025 and the por tfolio weight of Jar vis is 0.1 etc.)

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 15/177

From por tfolio weights to por tfolioexpected retur n and var ianceTo determine the expected retur n and var iance of a por tfolio we

need to k now

The por tfolio weights

The expected retur n on the individual assets

The var iance of the retur n on the individual assets

The covar iance between the retur n on any pair of assets

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 16/177

Expectation, Var iance and Covar ianceExpected retur n (³average´ retur n) is a location measure

Var iance of retur n is a s pread measure

Covar iance is a measure of how the retur n of two assets are ³related´ (they can move in the same or oppositedirections, or they can be uncorrelated)

If the retur ns move in the same directions, covar iance is positive, if the retur ns move in the opposite directions,covar iance is negative, and if uncorrelated, covar ianceis zero

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 17/177

The in put data for a por tfolioof N assets N expected retur ns

N var iances

N(N-1)/2 covar iances

Plus N por tfolio weights

For FTSE100 there are therefore 100+100+100(99)/2 =

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 18/177

Formulas

§ §

§§

§

!

!!

!

!

!

!

N

i ji

ji jiii P

N

i

N

j ji ji P

N

i

ii P

r r Covwwr Var wr Var

r r Covwwr Var

r E wr E

1

2

11

1

),(2)()(

),()(

)()(

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 19/177

Covar iance and CorrelationCovar iance is a measure of relatedness that depends on the unit of

measurement, so if the retur n is measured as a percent (e.g. 10

percent) or as a desimal (e.g. 0.10) the covar iance will be

different

Correlation is a measure of relatedness that is normalized to be

independent of the unit of measurement

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 20/177

Covar iance and Correlation

ji

ji

ij

jiij jiij ji

r r CovnCorrelatio

r Var r Var r r Cov

WW V

WW V V

),(

)()(),(

!!

!!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 21/177

The Mean-Standard Deviation Approach to InvestmentRisk aver se investor s don¶t like r isk

Var iance aver se investor s don¶t like r isk that comes as var iance

This is not the same in general ± var iance aver sion is a s pecialcase of r isk aver sion

Por tfolio theor y takes the var iance aver sion approach ± which in practice means that we assume investor s wish to maximize their expected retur n given a cer tain var iance, or minimize their var iance given a cer tain expected retur n

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 22/177

Mean-Standard Deviation for Two-Asset Investments

),()1(2)()1()()(

)()1()()(

212

2

1

2

21

r r Covwwr Var wr Var wr Var

r E wr wE r E

P

P

!

!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 23/177

Por tfolio Frontier

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 24/177

Mean-Std Dev for Por tfolios of theRisk Free Asset and a Risk y Asset

wr Var r Var wr Var

r r E wr r wr wE r E

P

F F F P

)()()(

))(()1()()(2 !!

!!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 25/177

Covar iance as Mar ginal Var ianceWe can interpret the covar iance between the retur n on a stock and

the retur n on a por tfolio as the stock¶s mar ginal var iance

That is, if we increase the stock¶s por tfolio weight mar ginally, the por tfolio var iance will increase by approximately twice the

stock¶s covar iance with the por tfolio

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 26/177

Algebraic ³ proof´

),(2)(

),(2)(2)(

),(2)()()(

))(()()(

)(

0

2

i P

m

i P i

i P i P

F i P

F i P F i P

r r Covdm

r dVar

r r Covr mVar dm

r dVar

r r mCovr Var mr Var r Var

r r E mr E r E

r r mr mr mr r r

!

!

!

!

!!

!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 27/177

What to take homeUnder standing of expected values, var iances, andcovar iances

Under standing of expected retur n and var iance for a por tfolio

Under standing of r isk aver sion and var iance aver sion

Under standing of the por tfolio frontier

Appreciation of the linear ity of expected retur n andstandard deviation for por tfolios consisting of the r isk

free asset and a r isk y por tfolio

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 28/177

R eadingsChapter 4 in Gr in blatt/Titman

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 29/177

Problems1. Var iance: Prove that E(x-E(x))2=Ex2-(E(x))2

2. Covar iance: Prove that E(x-E(x))(y-E(y))=Exy-E(x)E(y)

3. Take a time ser ies of retur ns 0.05, -0.03, 0.10, 0.04, -0.10,

0.20. Estimate the expected retur n and the var iance of

retur n.

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 30/177

Week 3:From Mean-Var iance to the CAPMCapital Market Line

Finding the market por tfolio

Two-fund Separation

Optimal diver sif ication

Market vs idiosyncratic r isk

CAPM expected retur ns relationshi p

Expected retur n on assets depend on their covar iance (i.e.

their relatedness) with the market por tfolio

Estimating beta r isk

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 31/177

Capital Market LineThe line that goes through the r isk free asset and the tangency

por tfolio

Identif ication? Maximization procedure

Simplif ying ³tr ick´, the excess retur n on any asset divided by its

covar iance with the tangency por tfolio, is constant

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 32/177

Maximization programme to f ind theCapital Market LineWe can identif y the frontier por tfolios of r isk y assets

Consider investments consisting of the r isk free asset and a

frontier por tfolio ± these are represented by straight lines

For the frontier por tfolio that is the tangency por tfolio, the angle

of the straight line is the steepest

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 33/177

Capital Market Line cont..

)(

))(())()((

max

)()1(),()1(2)()(

)()1()()()(

)(max

22

T

F B B A

w

B B A AT

B AT

T

F T

w

r Var

r r E r E r E w

r Var wr r Covwwr Var wr Var

r E wr wE r E r Var

r r E

!

!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 34/177

Capital Market Line cont..The maximization programme normally leads to a fairly

complicated equation ± with two r isk y assets we get a quadratic

equation to solve

In the class exercises you will be asked to have a go at such a

problem

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 35/177

Simplif ying ³tr ick´: f inding the CapitalMarket LineWe k now the expected retur n on all r isk y assets and the r isk free

retur n

The difference between the two is called the ³excess retur n´ for the asset

The excess retur n, divided by its covar iance with the tangency

por tfolio, is always constant

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 36/177

Capital Market Line

F N N N N

F N N

F N N

F iT i

i N N ii

iiT i

r r E r Var wr r Covw

r r E r r Covwr r Covw

r r E r r Covwr Var w

r r E r r Cov

r r Covwr Var w

r r Covwr r Covwr r Cov

!

!

!

!

!

)()(),(

)(),(),(

)(),()(

)(),(

),()(

),(),(),(

11

22211

1111

2211

.

/

.

.

.

.

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 37/177

Example

06.17.

.06-.17

.06-.15R etur nExcess

002.001.0

001.002.001.

0001.002.

Var /Cov

!

!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 38/177

Example cont..

5.,1.,4.

50

10

40

06.17.002.001.0

06.17.001.002.001.

06.15.0001.002.

321

3

2

1

321

321

321

!!!

!

!

!

!

!

!

www

w

w

w

www

www

www

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 39/177

CAPM: Risk and R etur nSince the excess retur n divided by the covar iance with thetangency por tfolio is constant across assets, we can der iveimpor tant relationshi ps between r isk and retur n

The covar iance with the tangency por tfolio is, if solved for thetangency por tfolio itself, equal to the var iance of the tangency

por tfolio

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 40/177

Risk and R etur n

F T i F i

F T

T

T i F i

T

F T

T i

F i

T

F T

T i

F i

r r E r r E

r r E r Var

r r Covr r E

r Var

r r E

r r Cov

r r E

r Var

r r E

r r Cov

r r E

!

!

!

!

!

)()(

)()(

),()(

)(

)(

),(

)(

constant)(

)(

constant),(

)(

F

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 41/177

Secur ity Market LineThe expected retur n of secur ities is linear in their beta-factor s

In the (beta,expected retur n) plane, the line crossing through

(0,r F) and (1,E(r T)) is called the secur ity market line

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 42/177

Proper ties of betasBeta is linear: the beta of a por tfolio of secur ities equals the

por tfolio-weighted average of the betas of the individual

secur ities

An implication is that the beta of the assets of the company

equals the value-weighted beta of the liabilities of the company

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 43/177

Track ing por tfolios

A por tfolio track s another perfectly if the difference in the retur ns

of the por tfolios is a constant (possi bly zero)

Imperfect track ing: A por tfolio consisting of a weight (1-b) in ther isk free asset and a weight b in the tangency por tfolio track s a

stock with beta =b, because the two should have the same

expected retur n

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 44/177

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 45/177

Estimating the r isk free retur n

For r isk free retur n use gover nment bond or gover nment bill data

(long or shor t term instruments backed by the gover nment)

The retur n offered on such instruments is a good proxy for theactual r isk free retur n

Alter native, use the average retur n of a zero-beta r isk y stock, or

the intercept with the y-axis if no zero-beta stock exists

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 46/177

Estimating market r isk premia

Estimate the long-run average retur n on a broad stock market index and subtract the r isk free rate

Both the average stock market index retur n and the r isk free retur n change over time

The change in the difference is more volatile than thechanges in the individual time ser ies.

Therefore, estimate the long-run average index retur n f ir st. Do not estimate the difference between the market retur n and the r isk free rate directly

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 47/177

Beta estimation

A raw beta estimate can be obtained from histor ical covar ianceand var iance estimates (or by a regression)

Average beta is one (this is the beta of the market index)

If the raw estimate exceeds (is below) one, we k now there is a possi bility that the raw beta is an overestimate (underestimate)

R aw beta estimates should be adjusted ± i.e. they should be

pulled down if they are above one or be bumped up if they are below one.

There are ways of optimally adjust beta estimates

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 48/177

Beta Adjustment

Bloomber g adjustment

Adjusted beta = .66 times Unadjusted beta + .34 times One

R osen ber g adjustment

Adjustment also incorporates fundamental var iables (industr y var iables,company character istics such as size, etc..)

Also betas are adjusted sometimes to take into account infrequent trading problems

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 49/177

What to take home

Two-fund separation

Capital Market Line vs Secur ity Market Line

Risk-R etur n relationshi ps

Track ing por tfolio

Parameter estimation: problems and current practice

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 50/177

R eadings

Gr in blatt/Titman ch 5

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 51/177

Problems

What is the track ing por tfolio for a real asset?

How would you estimate the beta of the assets of a f irm that has

traded debt and equity?

How would you estimate the beta of a company that has never

traded?

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 52/177

Week 4: From CAPM to ArbitragePr icing Theor yMain purpose is to extend the valuation approach intomore advanced and flexi ble valuation models

CAPM can be thought of as a ³one-factor´ model(retur ns are determined by movements in the market por tfolio only) but has impor tant empir ical problems (systematic deviations from predictions)

APT extends to ³multi-factor´ pr icing that can mitigatesome of the CAPM¶s empir ical problems

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 53/177

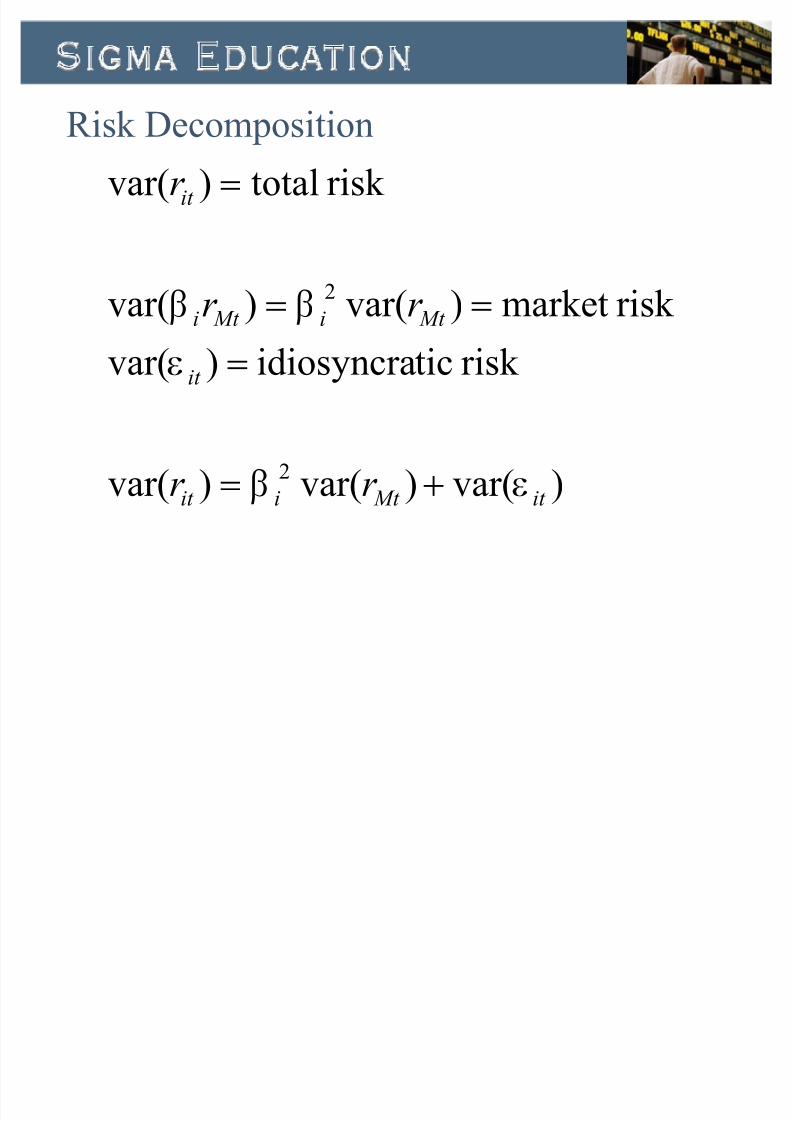

Risk Decomposition

The Market Model

One-factor (the retur n on the market por tfolio)

R elated to the CAPM modelThe regression estimates of the market model generates raw

beta-estimates for the CAPM

Risk Decomposition

Systematic (market) r isk: asset r isk that is explained by

market movements

Unsystematic (diver sif iable, idiosyncratic) r isk: asset r isk that

cannot be explained by market movements

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 54/177

Market model regression

0),cov()var(

),cov(

)1(

!

!

!

!

Mt it

Mt

Mt it i

F ii

it Mt iiit

r r

r r

r

r r

I

F

FE

I FE

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 55/177

Risk Decomposition

)var()var()var(

r isk ticidiosyncra)var(

r isk market )var()var(

r isk total)var(

2

2

it Mt iit

it

Mt i Mt i

it

r r

r r

r

I F

I

F F

!

!

!!

!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 56/177

APT: The arbitrage pr inci ple behind factor models

F j

i j

j

i

i j

j

i j

j

ji

j jii ji

iii

r r bb

br

bb

b

bb

bw

bwwb

f baw f bawr wr w

f bar

!!¹¹

º

¸

©©

ª

¨

!

!!

!

freer isk 1

solution haswhich

0)1(Set

))(1()()1(

~~

~~~~

~~

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 57/177

APT: Factor pr icing

F M

i F ii

j

F j

i

F i

F i F j jii j

F j

i j

j

i

i j

j

r r E

br ar E

b

r a

b

r a

r br babab

r abb

ba

bb

b

!

!!

!!

!

!

!¹¹

º

¸

©©

ª

¨

)(CAPM,For

)(

constant

1

P

P

P

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 58/177

Multi-factor models

~~~

22

~

11

~

2211)(

modelfactor -K

it Kt iK t it iiit

K iK ii F i

f b f b f bar

bbbr r E

I

PPP

!

!

.

.

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 59/177

We do not k now what the factor s are!Can be evaluated statistically ± using a method called factor

analysis

The out put generates por tfolios associated with each factor

Can use f irm character istics or macroeconomic var iables as

proxies for the factor s

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 60/177

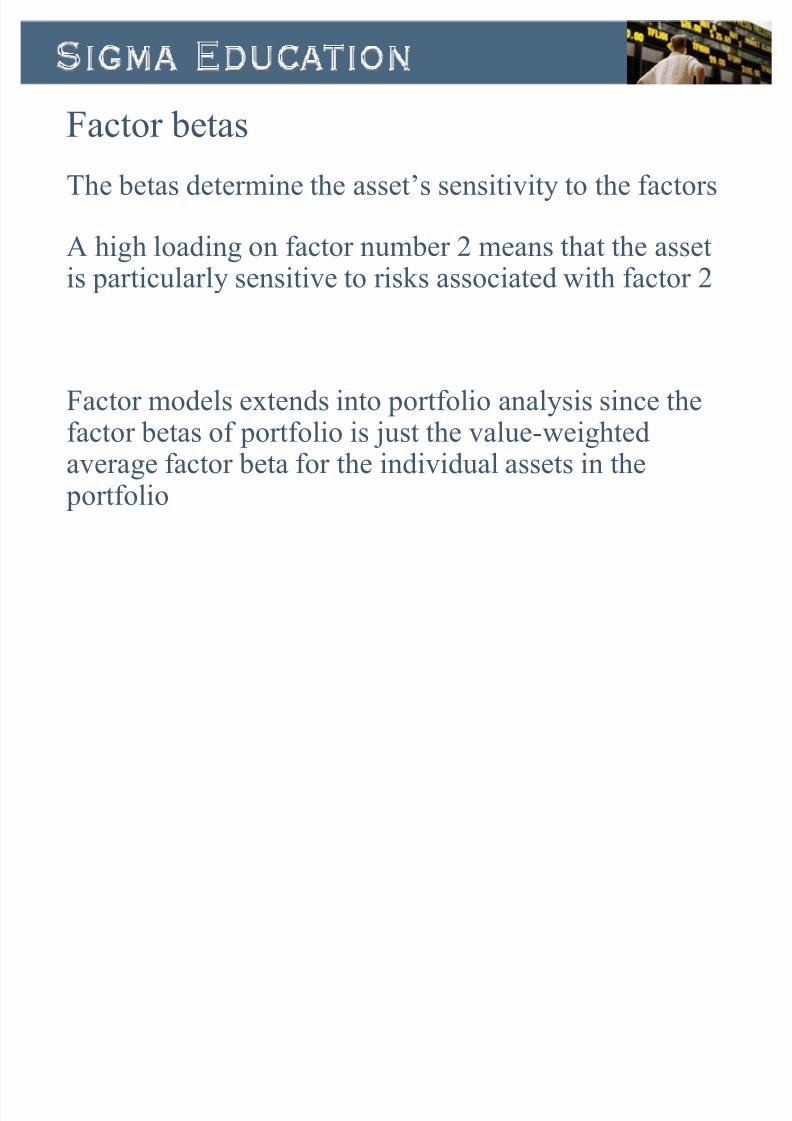

Factor betas

The betas determine the asset¶s sensitivity to the factor s

A high loading on factor number 2 means that the asset

is par ticularly sensitive to r isk s associated with factor 2

Factor models extends into por tfolio analysis since the

factor betas of por tfolio is just the value-weightedaverage factor beta for the individual assets in the por tfolio

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 61/177

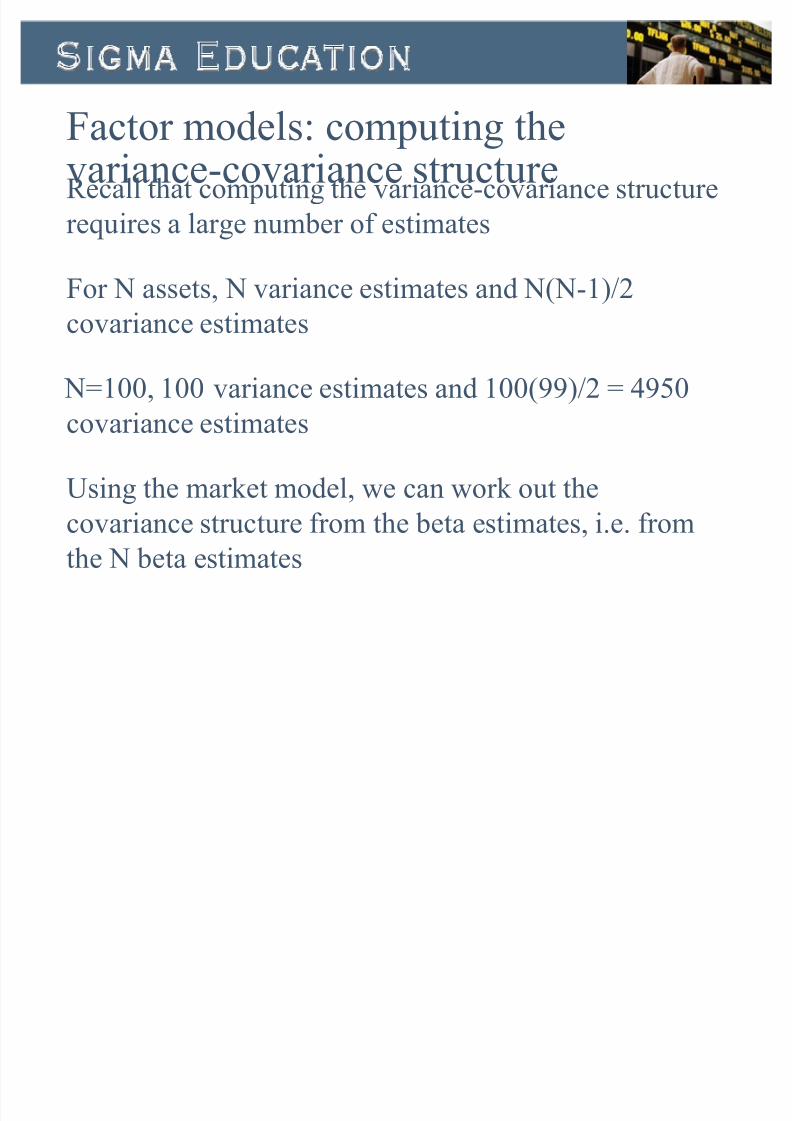

Factor models: computing thevar iance-covar iance structureR ecall that computing the var iance-covar iance structure

requires a lar ge number of estimates

For N assets, N var iance estimates and N(N-1)/2covar iance estimates

N=100, 100 var iance estimates and 100(99)/2 = 4950

covar iance estimates

Using the market model, we can work out the

covar iance structure from the beta estimates, i.e. from

the N beta estimates

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 62/177

Covar iance structure estimation

)var(

),cov(),cov(

),cov()var(

),cov(),cov(

~

~~~~

~~~

~~~~

~~~

f bb

f b

f b f bb

f b f br r

f bar

ji

jii j

ji ji

j jii ji

iiii

!

!

!

!

III

I

II

I

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 63/177

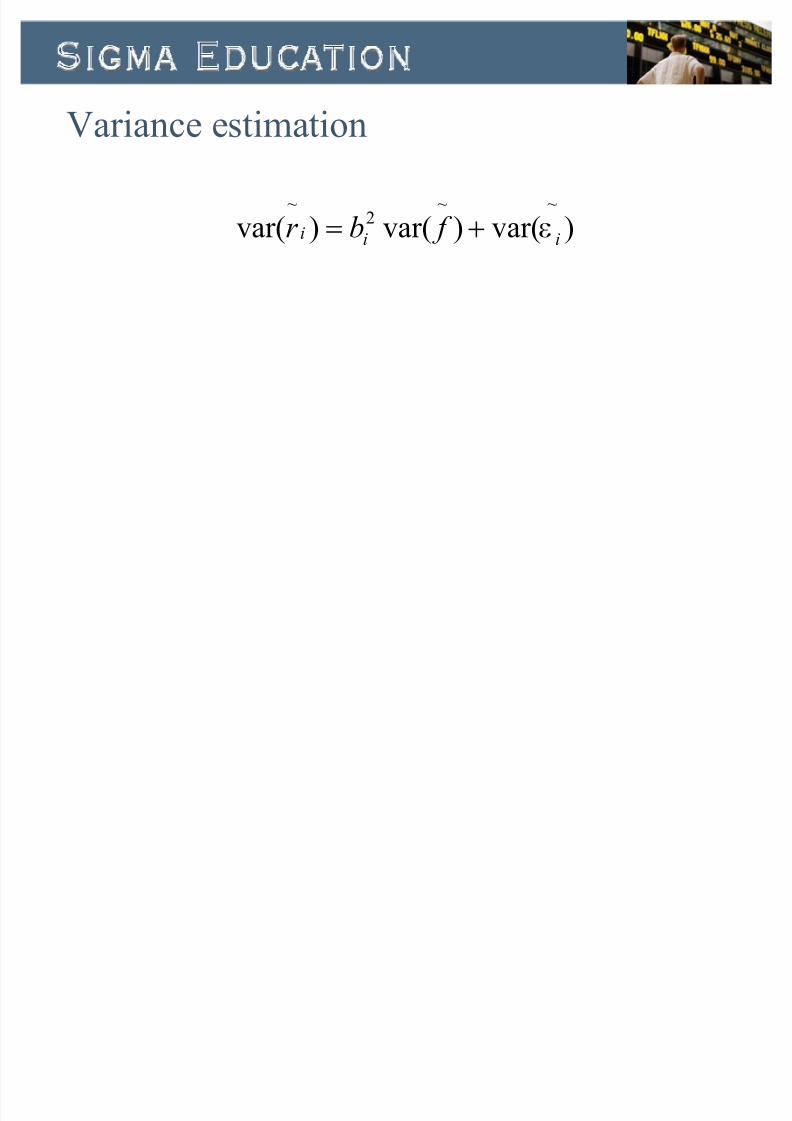

Var iance estimation

)var()var()var(~~

2~

iii f br I!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 64/177

Track ing Por tfolio

Objective: to design a por tfolio that has cer tain factor

betas (or factor loadings)

Why? The use of track ing por tfolios are many

Risk management: if the company is subject to r isk s beyond

its control, e.g. currency r isk, it may create a track ing por tfolio

that off sets the r isk

Capital allocation: the company may wish to allocate capital

to investments that yield a greater retur n than their track ing

por tfolio and to reduce its exposure to investments that yield a

smaller retur n than their track ing por tfolio

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 65/177

Designing a Track ing Por tfolio

Fir st, determine the number of relevant factor s (guesswork, statistical analysis)

Second, determine the factor betas of the investment you wish to track (statistical analysis, compar ison withexisting traded companies)

Third, gather a collection of different assets with k nown factor loadings

For th, cali brate your por tfolio such that the por tfoliofactor beta equals the tar get factor beta for each factor

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 66/177

Example

8.0,3.0,1.0:Out put

224

15.13

1

:nCali bratio

2factor for 02,4,-and

1factor for 1.53,1, betafactor withassetsThree

lyres pective2and1factor for 2and1 betastar get por tfolio,ck ingfactor tra-Two

321

21

321

321

!!!

!

!

!

x x x

x x

x x x

x x x

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 67/177

Applying Pr icing Theor y

Use pr icing models to investment analysis (optimal investment strategies in f inancial markets ± diver sif ication)

Use pr icing models to cali brate investments (design of track ing

por tfolios)

Use pr icing models as a benchmark for real investment (compar ing real investment retur ns to the retur n on track ing

por tfolios)

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 68/177

R eadings

Chapter 6 in Gr in blatt/Titman

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 69/177

Problem

There are three relevant factor s dr iving asset retur ns

The factor structure of the debt of the company is (0.01, 0,0)

The factor structure of the equity of the company is (2,5,1)

The company consists of 1/3 debt and 2/3 equity

What is the factor structure of the company¶s real assets (investments)?

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 70/177

Week 5: Investment Analysis ± thecase of Risk Free ProjectsApply pr icing technology to real investment analysis

Net Present Value R ule

Complications

Sunk cost

Oppor tunity cost

EVA and IRR

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 71/177

Fisher Separation

With different tastes, why should investor s agree on

investment policy?

Long-term vs shor t termRisk y vs Risk free

Fisher separation

Agreement is optimal regardless of taste Net present value rule: Invest in all projects that cost less than

the value of the project¶s track ing por tfolio

NPV = PV(future investment) ± Investment cost

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 72/177

Ingredients

Cash flows of our investment

Investment cost

Discount rates (if r isk free projects ± use a r isk free discount rate)

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 73/177

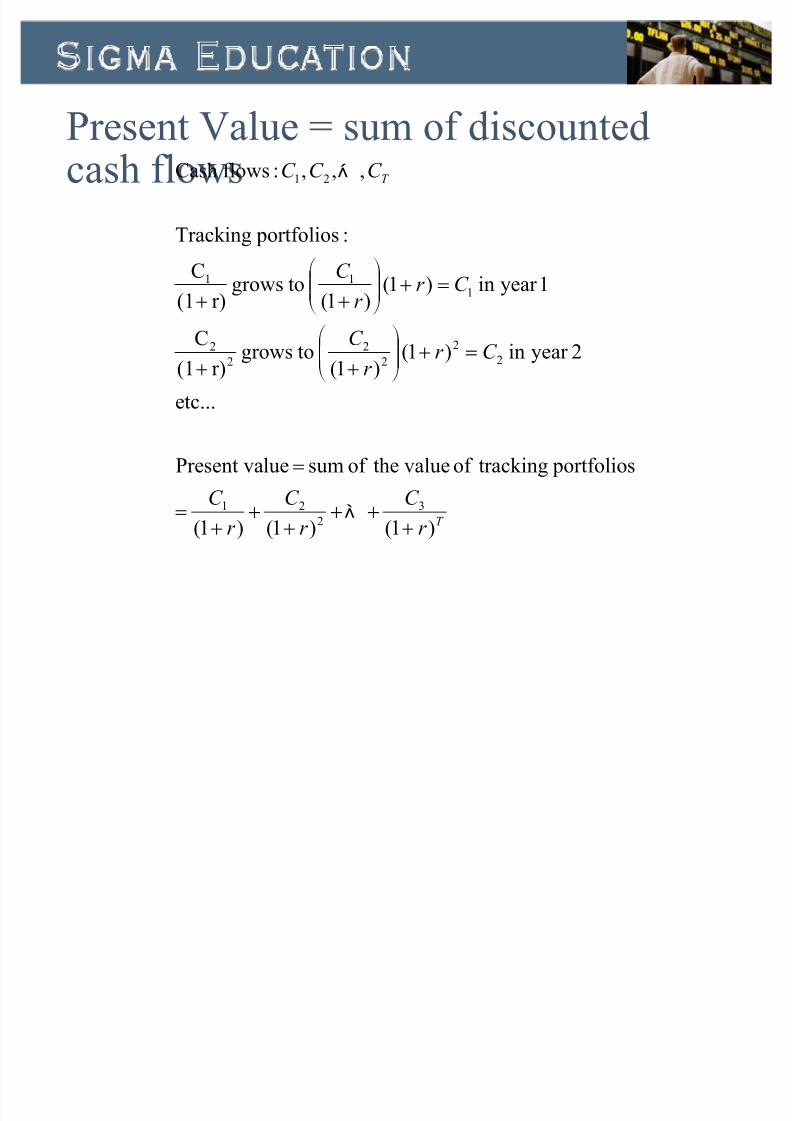

Present Value = sum of discountedcash flows

T

T

r

C

r

C

r

C

C r r

C

C r r

C

C C C

)1()1()1(

por tfoliostrack ingof valuetheof sumluePresent va

etc...

2year in )1()1(

togrowsr)(1

C

1year in )1()1( togrowsr)(1

C

: por tfoliosTrack ing

,,,:flowsCash

3

2

21

2

2

2

2

2

2

111

21

!

!

!¹¹ º

¸©©ª

¨

!¹¹ º

¸

©©ª

¨

.

-

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 74/177

Net Present Value

T

T

r

C

r

C

r

C I N PV

)1()1(1 2

21

0

! .

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 75/177

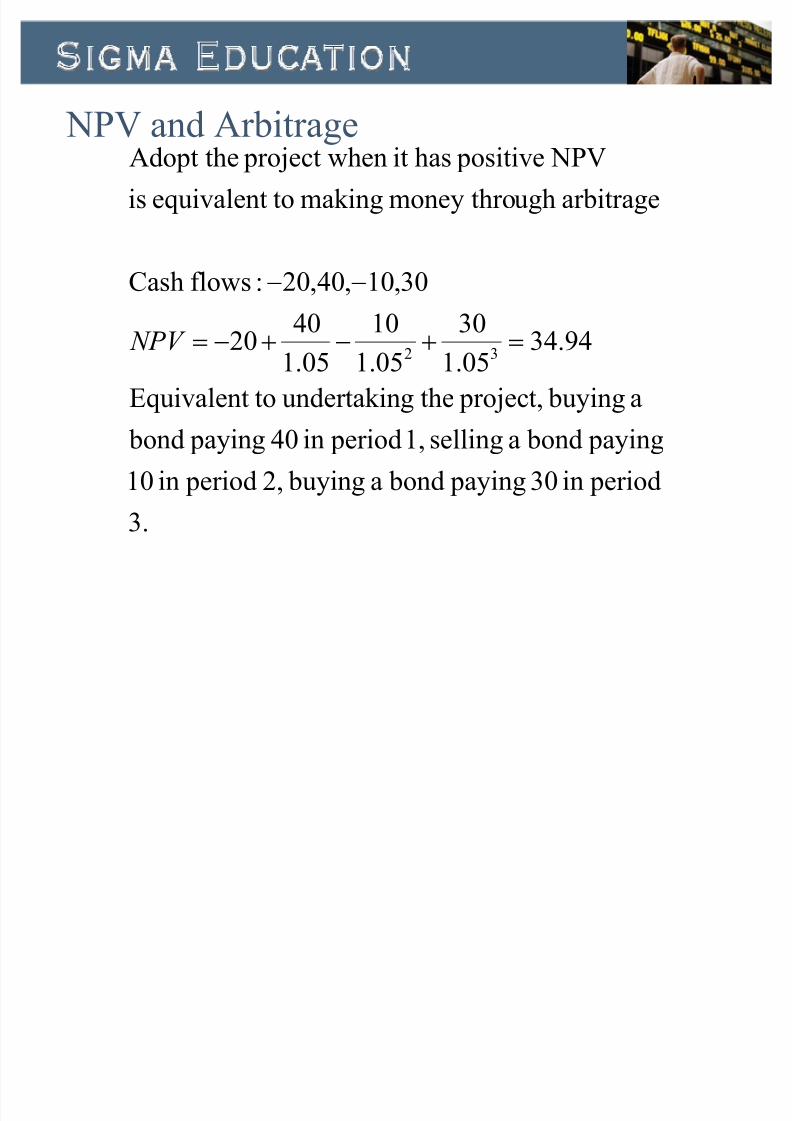

NPV and Arbitrage

3.

per iodin 30 paying bonda buying2, per iodin 10

paying bondaselling1, per iodin 40 paying bond

a buying project,thegunder tak intoEquivalent

94.3405.1

30

05.1

10

05.1

4020

30,10,40,20:flowsCash

arbitrageughmoney thromak ingtoequivalentis

NPV positivehasit en project whAdopt the

32!!

N PV

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 76/177

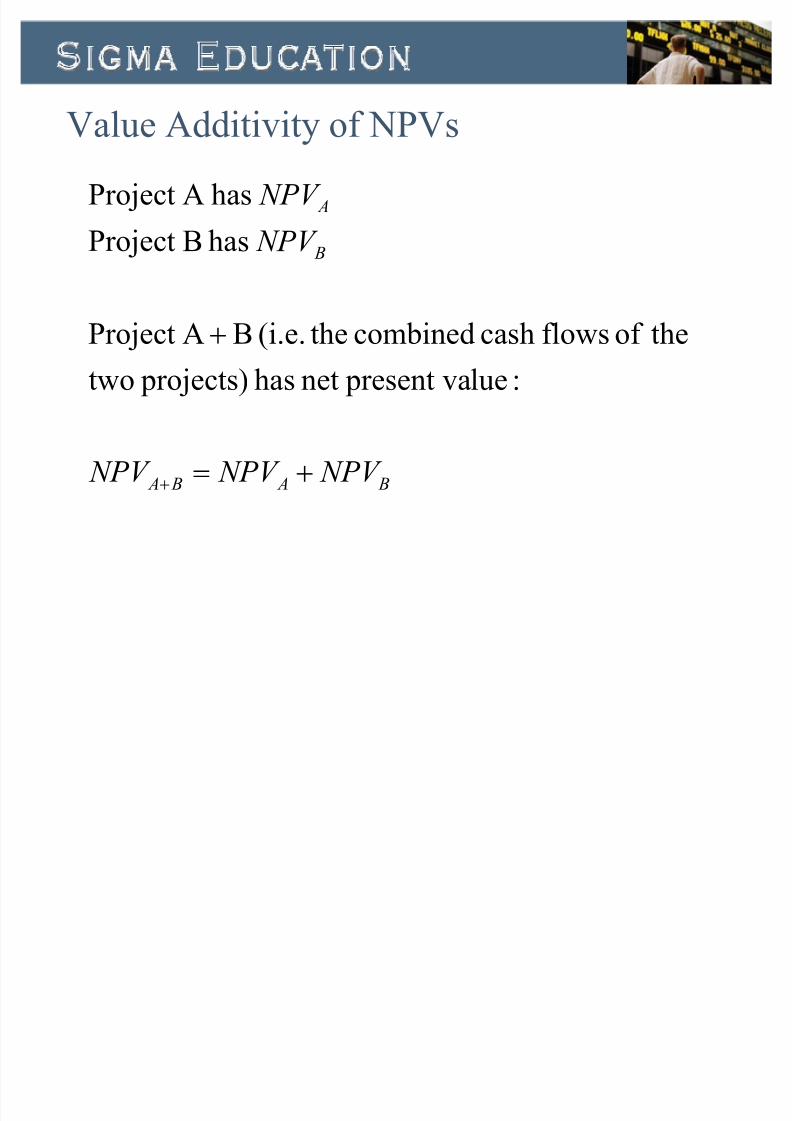

Value Additivity of NPVs

B A B A

B

A

N PV N PV N PV

N PV

N PV

!

:lue present vanet has projects)two

theof flowscashcombinedthe(i.e.BAProject

hasBProject

hasAProject

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 77/177

Mutually Exclusive Projects

This is an ³either-or´ situation ± you can invest in project A or you can invest in project B, but you cannot invest in both at the same time

Both projects may have positive NPV so are wor thwhileon their own

³Either-or´ situations of ten ar ise naturally. For instance,

all timing decisions are mutually exclusive. You can invest now or you can invest in the future, but youcannot invest both now and in the future.

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 78/177

Which project to choose when they aremutually exclusiveThe choice cr iter ion is to maximize the net present value of

investment.

Therefore, if you have two or more mutually exclusive projects to

choose from you should choose the one with the most positive

NPV.

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 79/177

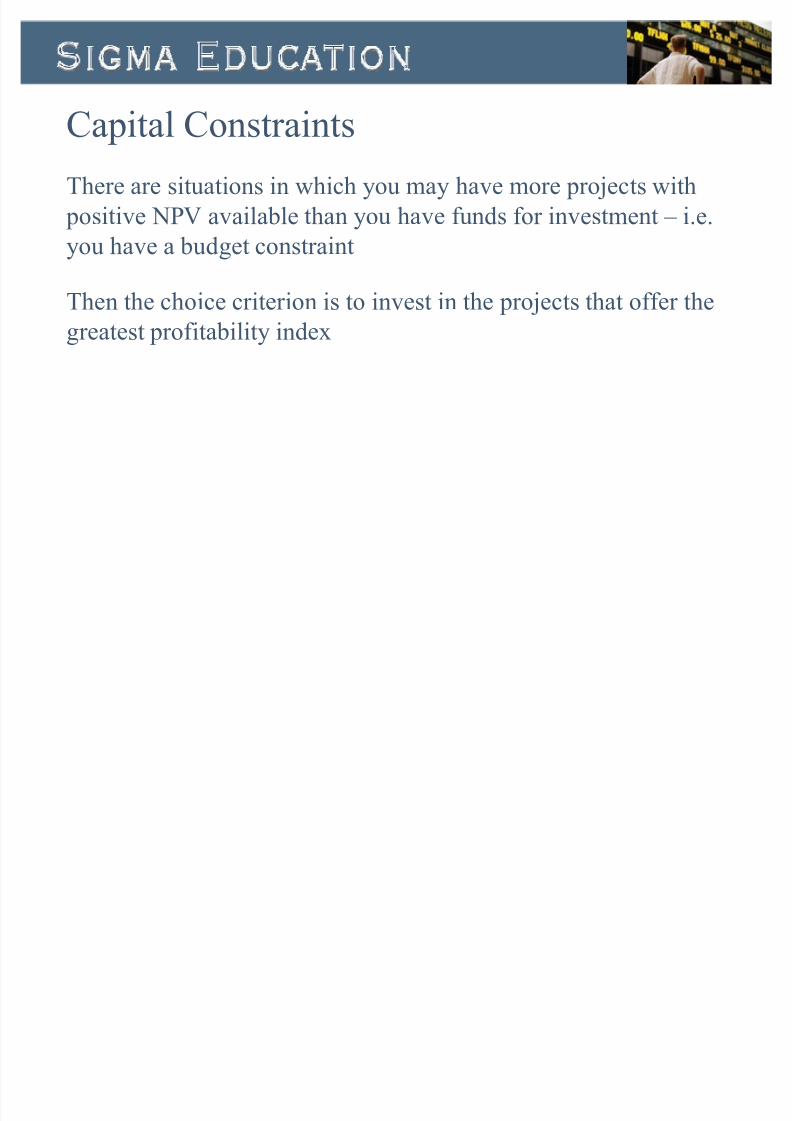

Capital Constraints

There are situations in which you may have more projects with

positive NPV available than you have funds for investment ± i.e.

you have a budget constraint

Then the choice cr iter ion is to invest in the projects that offer the

greatest prof itability index

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 80/177

Prof itability Index

0

0

0

Indexity Prof itabil

lue present va Net

cost Investment

flowcashValuePresent

I

PV PI

I PV N PV

I

PV

!

!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 81/177

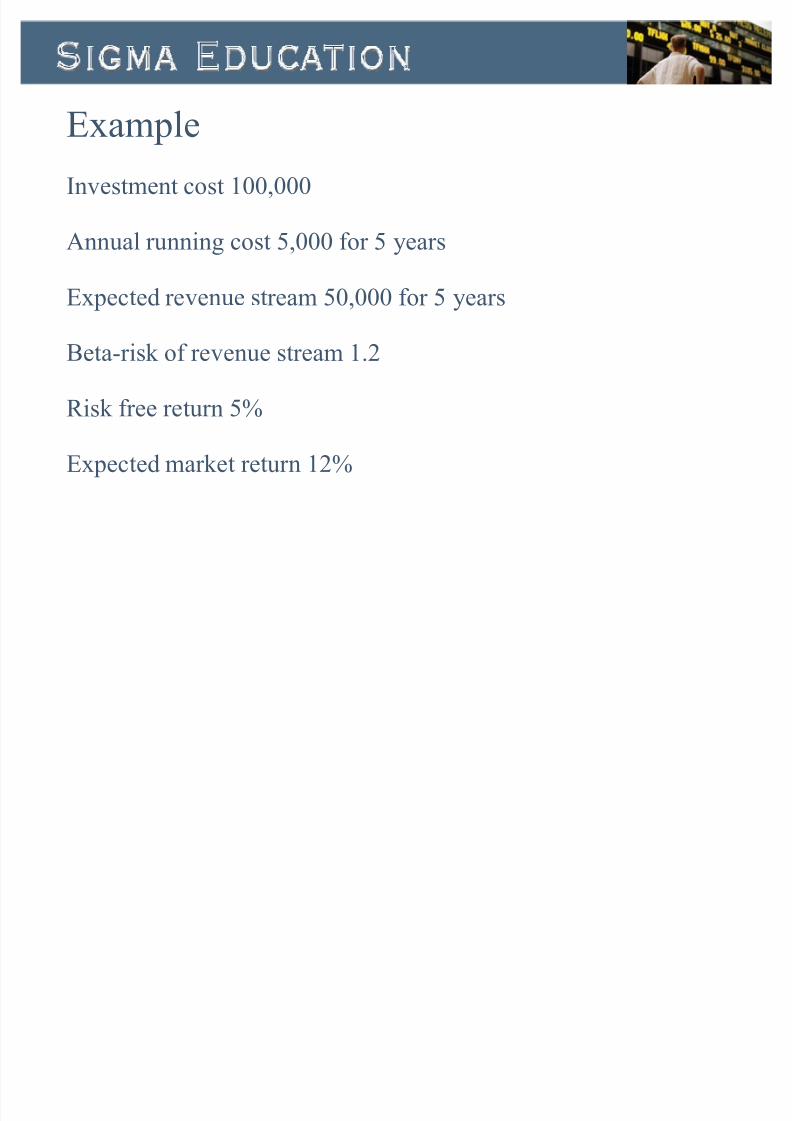

Example

budget?within stayingto

subject policy investmentoptimaltheisWhat

.100 budget investmentTotal

exclusive?mutually are

projectstheif policy investmentoptimaltheisWhat

t?independenare

projectstheif policy investmentoptimaltheisWhat

950,1000:CProject

90,100:BProject

8,10:AProject

m B

m I m PV

m I m PV

m I m PV

C C

B B

A A

!

!!

!!

!!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 82/177

Example cont.

11.12)9501000(950

2)90100()810(: NPVTotal

Cof %2105.0950

2 plusC)in invest

to2leaving budget,of 90additional(usingBof all

plus budget)100of 8(usingAof All:mixOptimal

C.andBthen f ir st,Ain Invest

0526.1950

1000

1111.190

100

25.18

10:indexesity Prof itabil

!

!

!!

!!

!!

C

B

A

PI

PI

PI

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 83/177

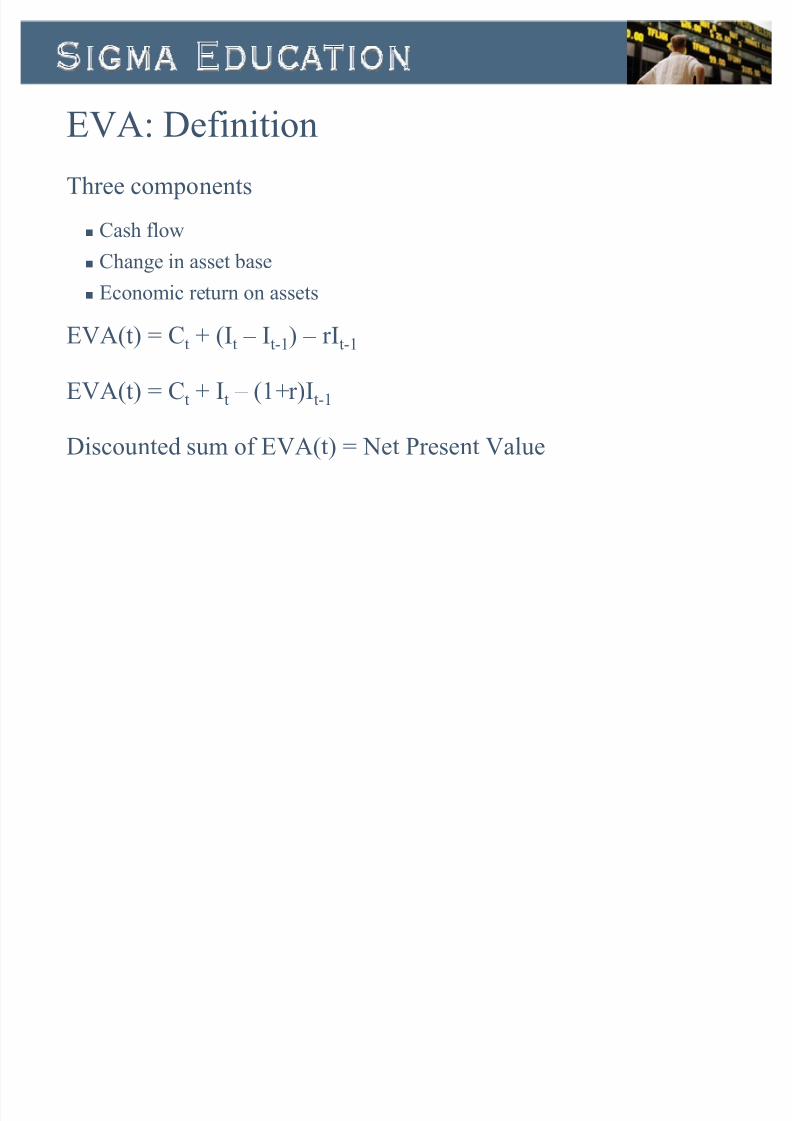

Economic Value Added

EVA is a prof itability measure that has become widely used in corporations ± initially to replace accounting ear nings or prof it measures

Accounting measures do not always measure economic performance (depreciation cost, for instance, is not acash flow and should not be included in project evaluation)

Accounting measures are therefore not directly consistent with NPV

Economic Value Added is consistent with NPV

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 84/177

EVA: Def inition

Three components

Cash flow

Change in asset base

Economic retur n on assets

EVA(t) = Ct + (It ± It-1) ± r It-1

EVA(t) = Ct + It ± (1+r)It-1

Discounted sum of EVA(t) = Net Present Value

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 85/177

EVA, cont.

Investment of 100

The f ir st year cash flow is 50

The second year cash flow is 150

Discount rate is 10%

Assets are depreciated by 50% in the f ir st year and by 100% in

the second year.

NPV = -100 + 50/1.1+150/1.12=69.42

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 86/177

EVA, cont.

EVA(0) = -100(cash flow)+(100-0)(change in assets)-0(0.1)(economic cost of initial assets) = 0

EVA(1)=50(cash flow)+(50-100)(change in assets)-

100(0.1)(economic cost of initial assets) = -10

EVA(2)=150(cash flow)+(0-50)(change in assets-50(0.1)(economic cost of initial assets)= 95

Discounted EVA = EVA(0)+EVA(1)/1.1+EVA(2)/1.12 = 69.42 = NPV

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 87/177

IRR : Inter nal R ate of R etur n

Of ten manager s base investment decision on the IRR instead of the NPV

The rule is: if IRR is greater than the discount rate (i.e.the cost of capital) then adopt the project

In many cases this leads to the same investment decision, as IRR is greater than the discount rate only if

the NPV is positive

In other cases this is not true however, so to be safealways use NPV or EVA calculations

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 88/177

IRR

T

T

T

T

IRR

C

IRR

C

IRR

C I

r

C

r

C

r

C I N PV

)1()1(10

)1()1(1

2

21

0

2

210

!

!

.

.

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 89/177

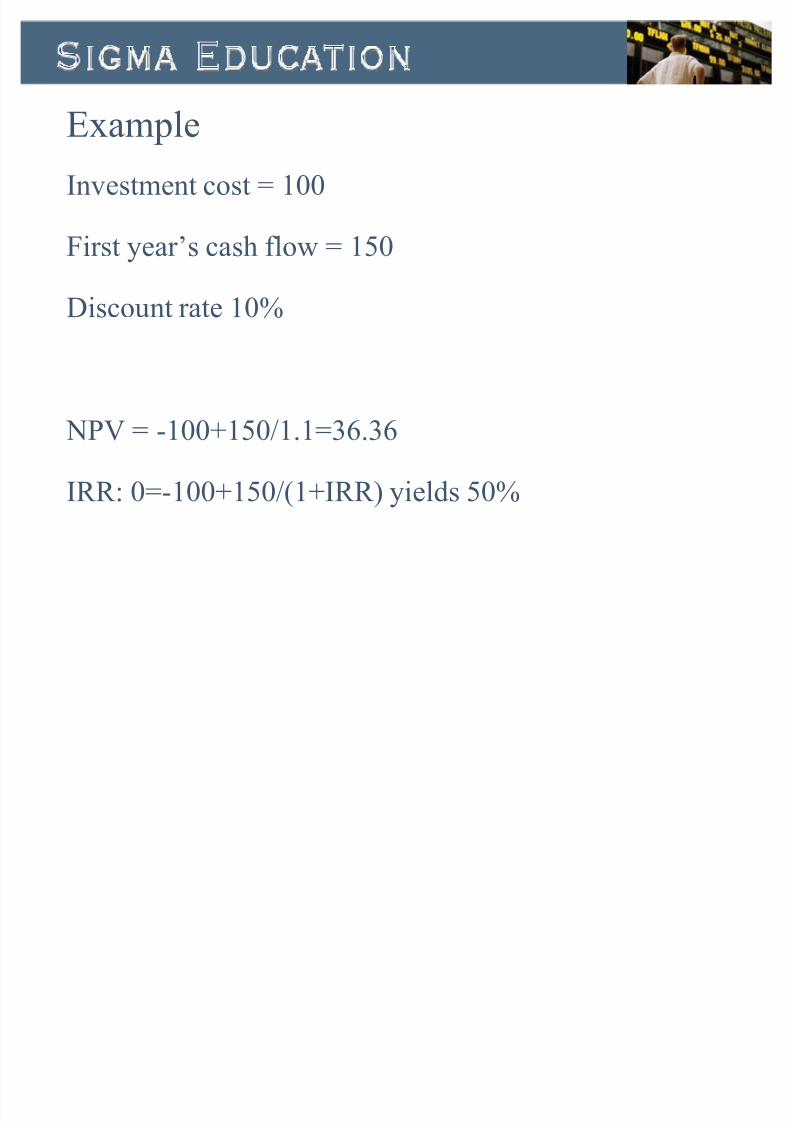

Example

Investment cost = 100

Fir st year¶s cash flow = 150

Discount rate 10%

NPV = -100+150/1.1=36.36

IRR : 0=-100+150/(1+IRR ) yields 50%

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 90/177

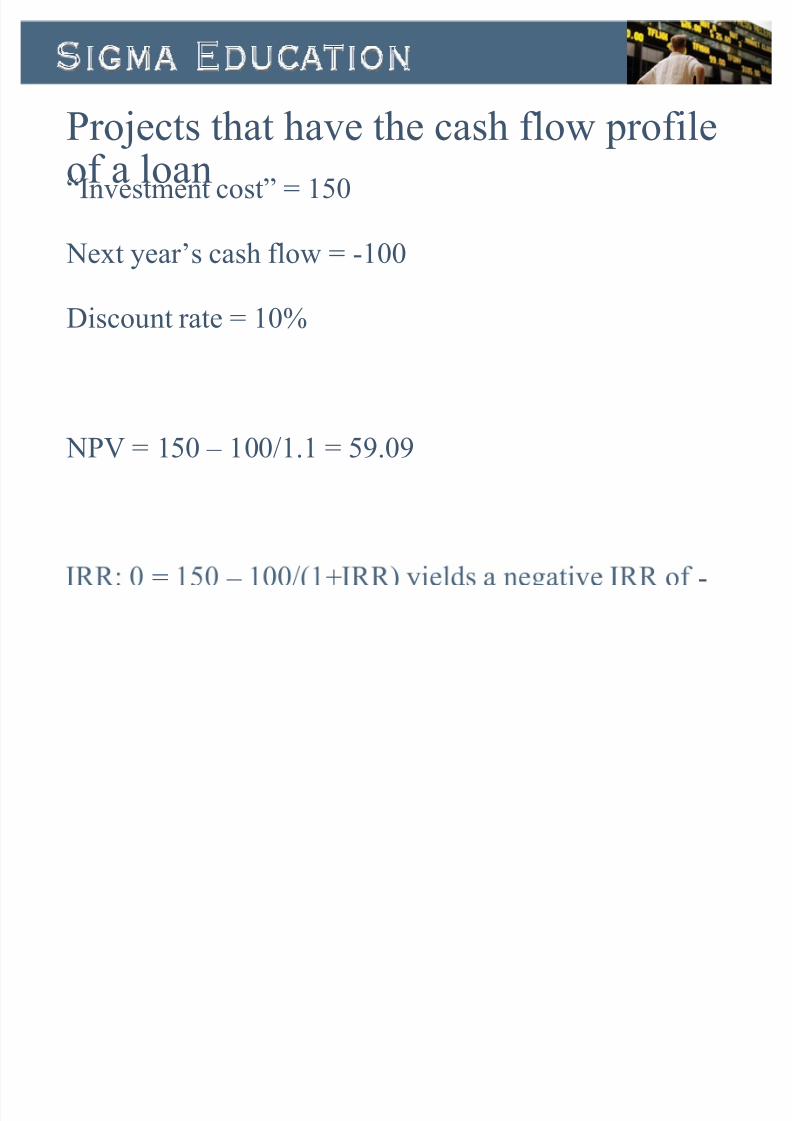

Projects that have the cash flow prof ileof a loan³Investment cost´ = 150

Next year¶s cash flow = -100

Discount rate = 10%

NPV = 150 ± 100/1.1 = 59.09

= ± + -

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 91/177

Problems with IRR

IRR cr iter ion is sensitive to the ty pe of cash flow (asset

or liability?)

IRR is not unique in general (for T per iod projects therecan be up to T different IRRs)

IRR is not appropr iate for mutually exclusive projects

as small projects with high IRR and small NPV might then be preferred to lar ge projects with low IRR and

lar ge NPV

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 92/177

IRR and mutually exclusive projects

Discount rate 2%

Project A: -10, -16, +30

Project B: -10, 2, 11

NPV(A) = 3.149

NPV(B) = 2.534

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 93/177

Impor tant points

Fisher separation

NPV def inition

NPV with mutually exclusive projects (either-or)

NPV with budget constraints

EVA and NPV

IRR

IRR pitfalls

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 94/177

R eadings

Gr in blatt/Titman chapter 10

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 95/177

Test for next week:

R eadings chapter 4, 5, 6 and 10

Impor tant formulas

CAPM: exp retur n = r isk free plus r isk adjustmentBeta-factor: covar iance/var iance

Factor models: exp retur n = r isk free plus r isk adjustment

Risk free real investments

NPV rule

Prof itability Index

EVA

IRR

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 96/177

Ver y impor tant formulas

T

T

K K F

M

M

F M F

r

C

r

C I N PV

r r E r Var

)Cov(r,r

r r E r r E

)1(1 :lue present va Net

premium)r isk denotes(where

)(:modelsFactor )(

:Beta

))(()(:CAPM

10

11

!

!

!

!

.

.

P

P FP F

F

F

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 97/177

Sample test questions

1. The r isk free retur n is 5% and the market index has an average retur n of 12%. What is the expected retur n for an asset with beta 1.5?

2. An investment costs 100,000 and offer s a cash flow of 50,000 in year 1 and 150,000 in year 2. The discount rate is 5%. What is the net present value of the investment? Shouldyou adopt the investment? Explain.

3. In a two-factor market, the factor betas of asset A are 1 and

0, and the factor betas of asset B are 0 and 1, res pectively.The r isk free retur n is 5%, and the average retur n on asset Aand B are 10% and 15%, res pectively. What are the r isk

premia associated with factor 1 and 2?

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 98/177

Week 6: Investing in Risk y Projects

Applying the CAPM and APT in the capital budgeting process

Key problem: estimating the cost of capital for r isk y projects

Applying CAPM and APT Using compar ison f irms

The dividend discount model

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 99/177

Risk Adjusted Discounting

t

t t

F M F

t

r

C E C E PV

r r E r r

C E

)1(

)())((:Discount

)((flow

cashtheof retur n market expectedtheCompute

retur n

market theof var ianceover theretur n,market the

hretur n wittheof covar iancetheis beta(theflow

cashwith thisassociatedr isk betatheCompute

t per iodin )(get)llat we'exactly whk nownotdo(weflowcashfutureexpectedtheCompute

!

! F

F

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 100/177

Fundamental problem: Estimating the beta factor Betas for traded equity are easy to estimate ± we simply regress equity retur ns on the index retur n, and possi bly adjust to take into account estimation error (e.g.

Bloomber g adjustment)

Betas for projects are much more diff icult to estimate as there simply does not exist a trading histor y

Possi ble solution: use compar ison f irms (f irms weimagine has similar r isk prof ile to the project in question)

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 101/177

Using compar ison f irms

Asset base needs to be suff iciently similar to the plannedinvestment

We need to adjust for leverage effects (the compar ison f irm may

have debt) In general, it is only the equity beta of the compar ison f irm we can

estimate but we are really interested in the asset beta

The more the f irm borrows, the higher the equity beta (even though theasset beta remains the same)

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 102/177

Adjusting for leverage

termleverage

a plus betaasset theequals betaequity Estimated

)(

beta

equityanddebt of sumweighted-value betaAsset

D A A E

E D A

E

D

E DV V

E

V

D

F F F F

F F F

!

!

!

!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 103/177

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 104/177

Implementing r isk adjusteddiscounting with compar ison f irms

08.10.1

79.085.0sWendy'

00.110

7.777.0McDonalds

75.0100.0096.072.0Chicken sChurch'

are betasasset The

zero.toequalassumediscompanes

theseof debt theof betatheandly,res pective

s),(Wendy'0.790and0.210and)(McDonalds7.700

and2.300Chicken),s(Church'0.096and0.004

arecompaniestheseof uesequity valanddebt The

ly.res pective1.08and1.00,0.75,arecompaniesthree

theseof betasequity Thes.Wendy'andsMcDonald'

Chicken,sChurch'of betaaveragethehas project A

!

!

!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 105/177

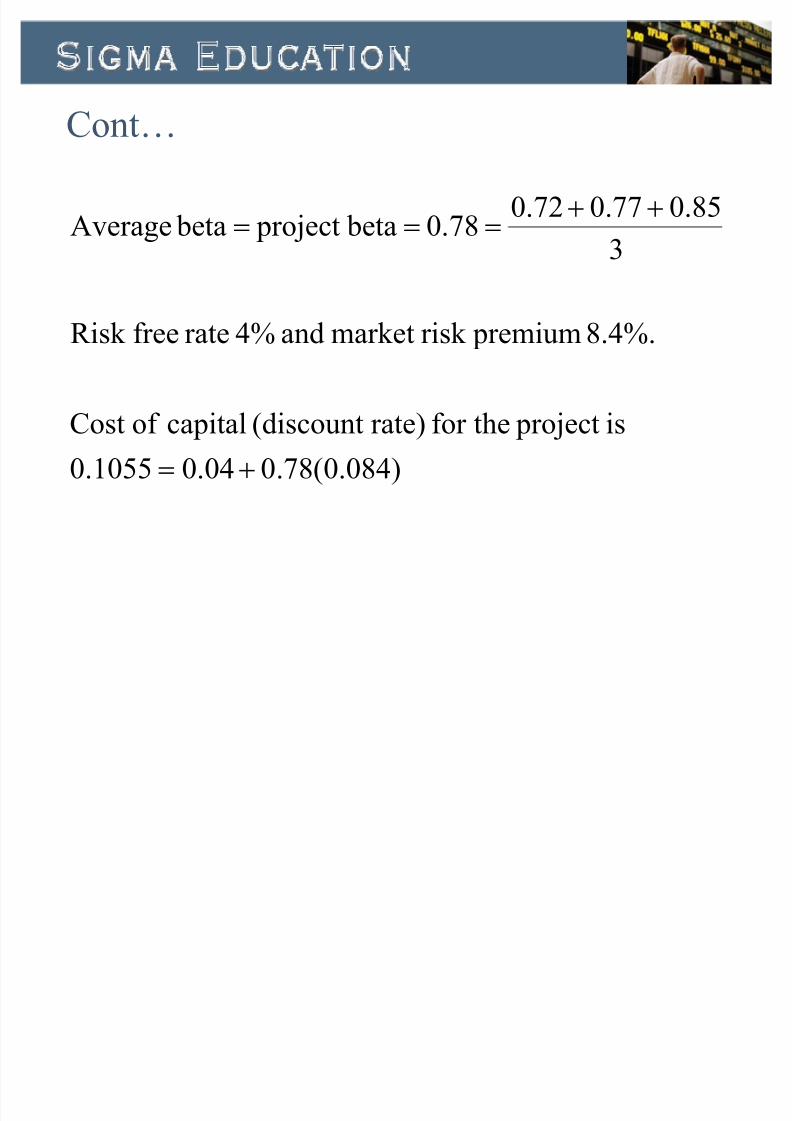

Cont«

)084.0(78.004.01055.0is project for therate)(discount capitalof Cost

8.4%. premiumr isk market and4%ratefreeRisk

3

85.077.072.078.0 beta project betaAverage

!

!!!

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 106/177

Applying APT

t K K F

t

t r

C E

C E PV )1(

)(

))((

bygiven arelues present vasomodel,factor a by

capitalof cost theestimatesmodelAPTThe

11 P FP F ! .

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 107/177

APT and CAPM vs Alter nativemethodsA draw back with the APT and CAPM models is that they requirea number of estimates: the r isk free rate of retur n, the betafactor(s), the market r isk premium and the factor r isk premia.

It can in some circumstances be better to work with simpler model. The dividend growth model is an alter native to the APTand CAPM.

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 108/177

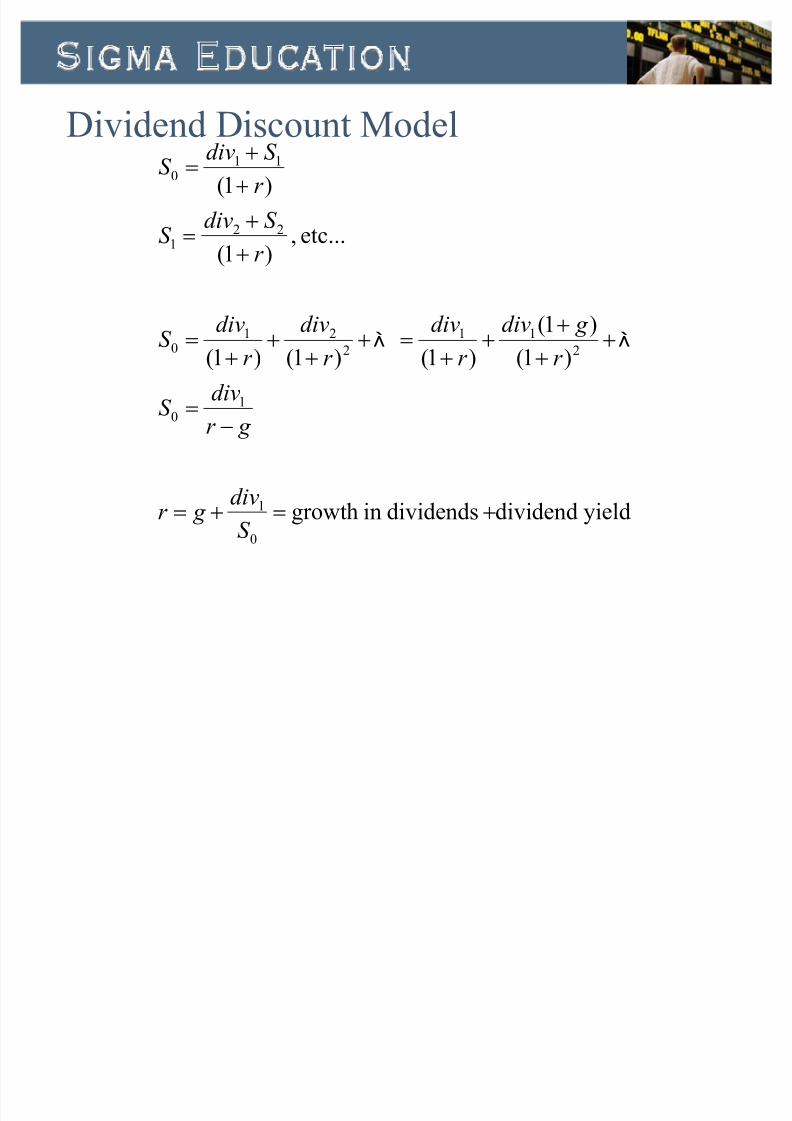

Dividend Discount Model

yielddividenddividendsin growth

)1(

)1(

)1()1()1(

etc...,)1(

)1(

0

1

10

2

11

2

210

221

110

!!

!

!

!

!

!

S

div g r

g r

divS

r

g div

r

div

r

div

r

divS

r

S divS

r S divS

..

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 109/177

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 110/177

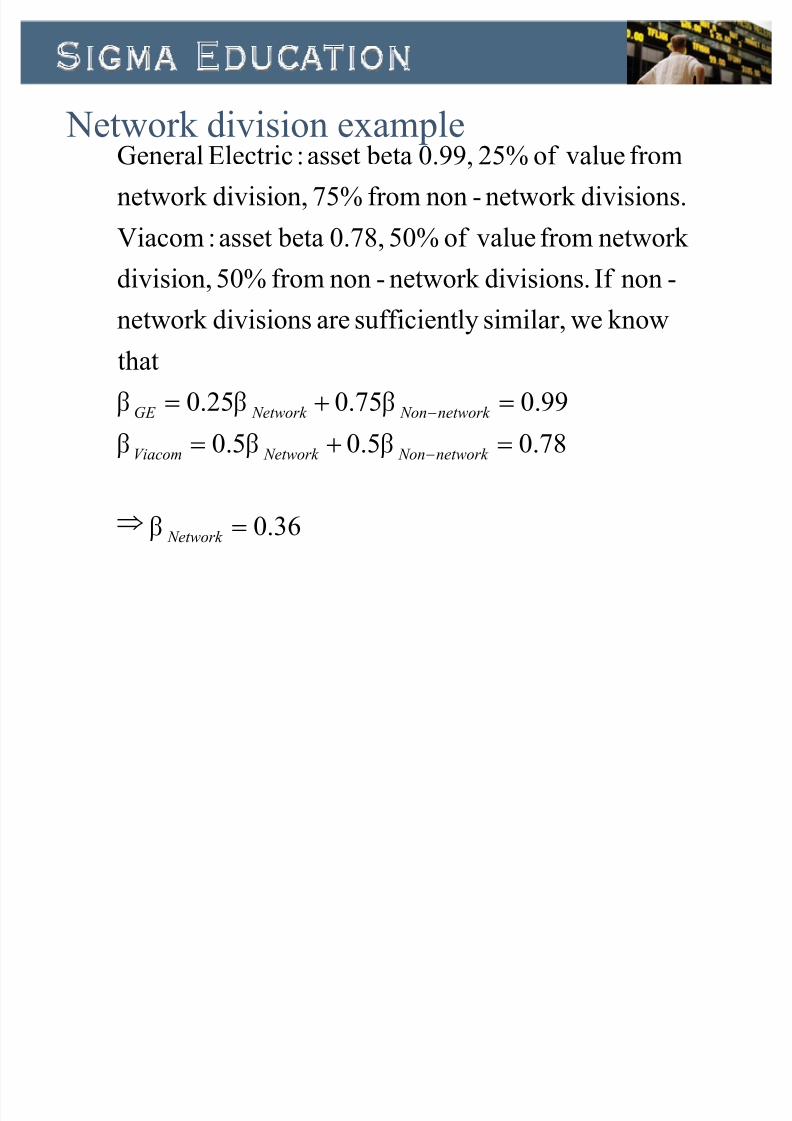

Network division example

36.0

78.05.05.0

99.075.025.0

that

k nowwesimilar,ly suff icientaredivisionsnetwork

-nonIf divisions.network -nonfrom50%division,

network fromvalueof 50%0.78, betaasset :Viacom

divisions.network -nonfrom75%division,network fromvalueof 25%0.99, betaasset :Electr icGeneral

!

!!

!!

N etwork

network N on N etwork Viacom

network N on N etwork GE

F

F F F

F F F

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 111/177

Pitfalls in using the compar ison methodProject betas not the same as f irm betas: mature projects

generally lower beta than R&D projects etc

Growth oppor tunities are usually the source of high betas:

company value of ten signif icantly linked to future growthoppor tunities as opposed to current investments

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 112/177

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 113/177

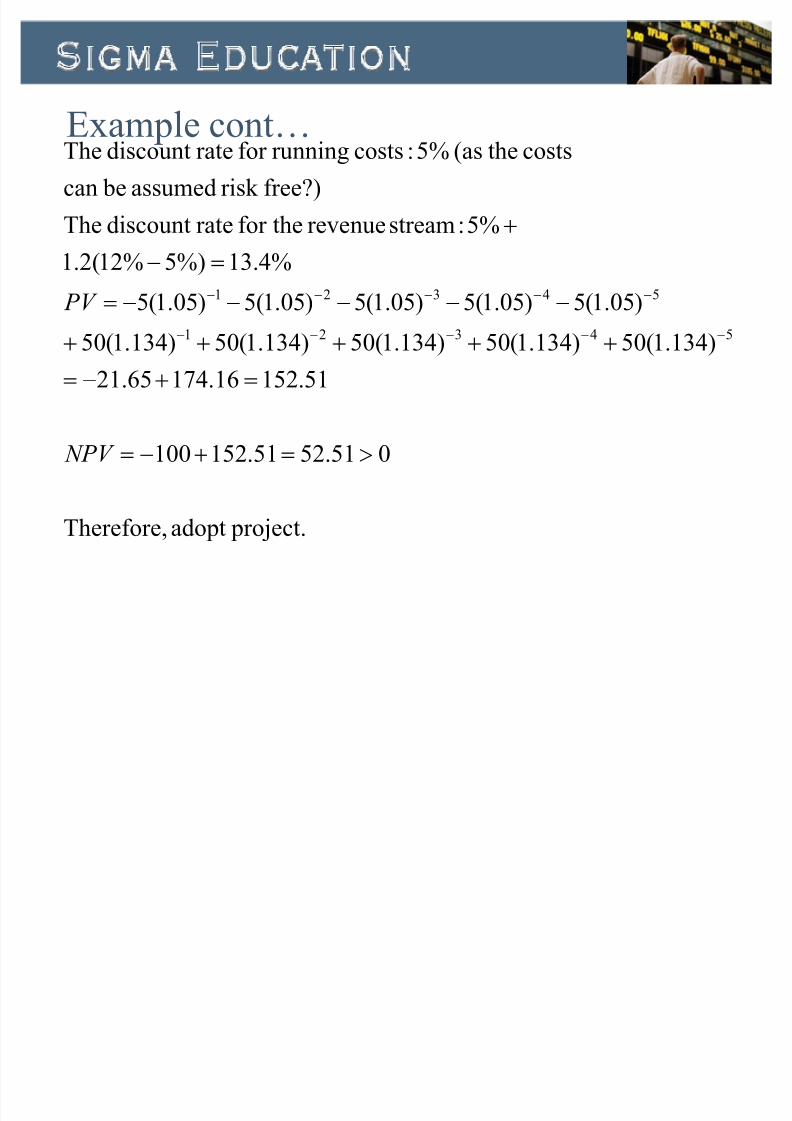

Example cont«

project.adopt Therefore,

051.5251.152100

51.15216.17465.21

)134.1(50)134.1(50)134.1(50)134.1(50)134.1(50

)05.1(5)05.1(5)05.1(5)05.1(5)05.1(5

%4.13%)5%12(2.1

%5:streamrevenuefor theratediscount The

free?)r isk assumed becan coststhe(as5%:costsrunningfor ratediscount The

54321

54321

"!!

!!

!

!

N PV

PV

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 114/177

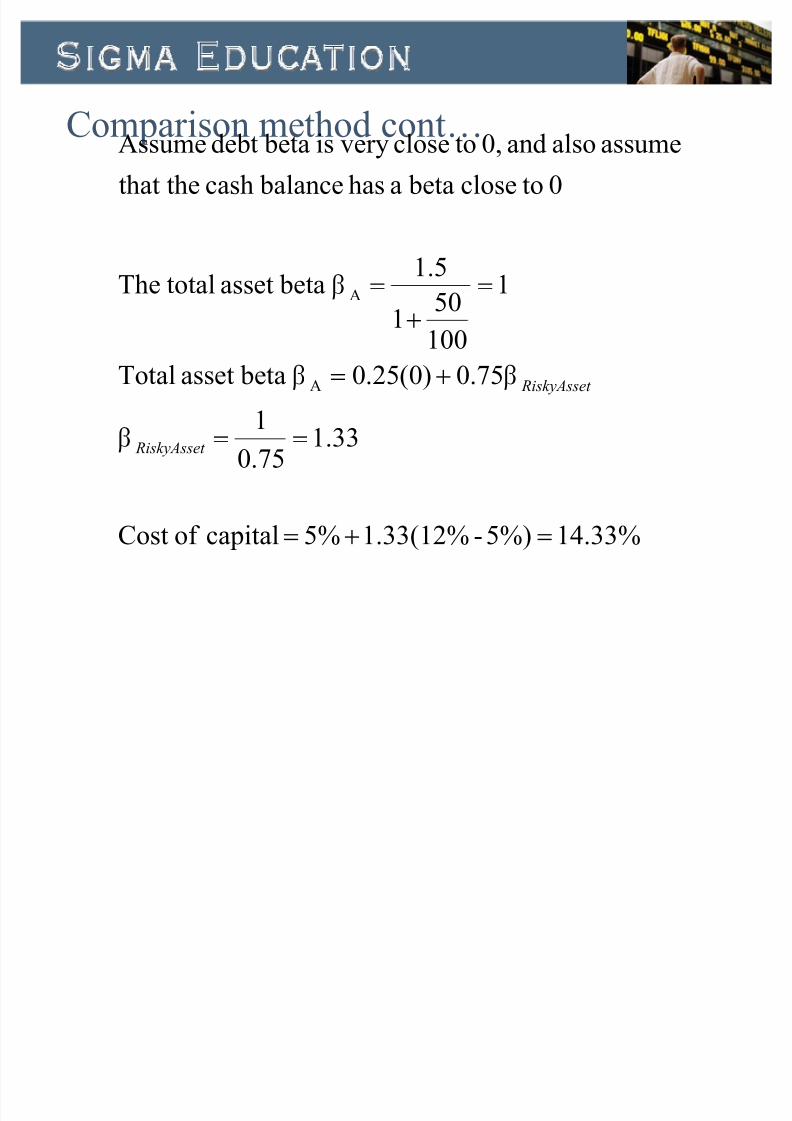

Compar ison method, example

A f irm with equity currently valued at 100,000 andoutstanding debt wor th 50,000 holds 25% cash and 75%of a r isk y asset on its balance sheet

The equity beta is 1.5

You consider investing in a project ver y similar to ther isk y asset owned by this f irm

The r isk free rate is 5% and the expected retur n on themarket is 12%

Work out the project beta and the cost of capital for your project

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 115/177

Compar ison method cont«

14.33%5%)-1.33(12%5%capitalof Cost

33.175.01

75.0)0(25.0 betaasset Total

1

100

501

5.1

betaasset totalThe

0toclose betaahas balancecashthat theassumealsoand0,toclosever y is betadebt Assume

A

A

!!

!!

!

!!

RiskyAsset

RiskyAsset

F

F F

F

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 116/177

R eadings

Gr in blatt & Titman chapter 11

I have not emphasized the cer tainty equivalent method

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 117/177

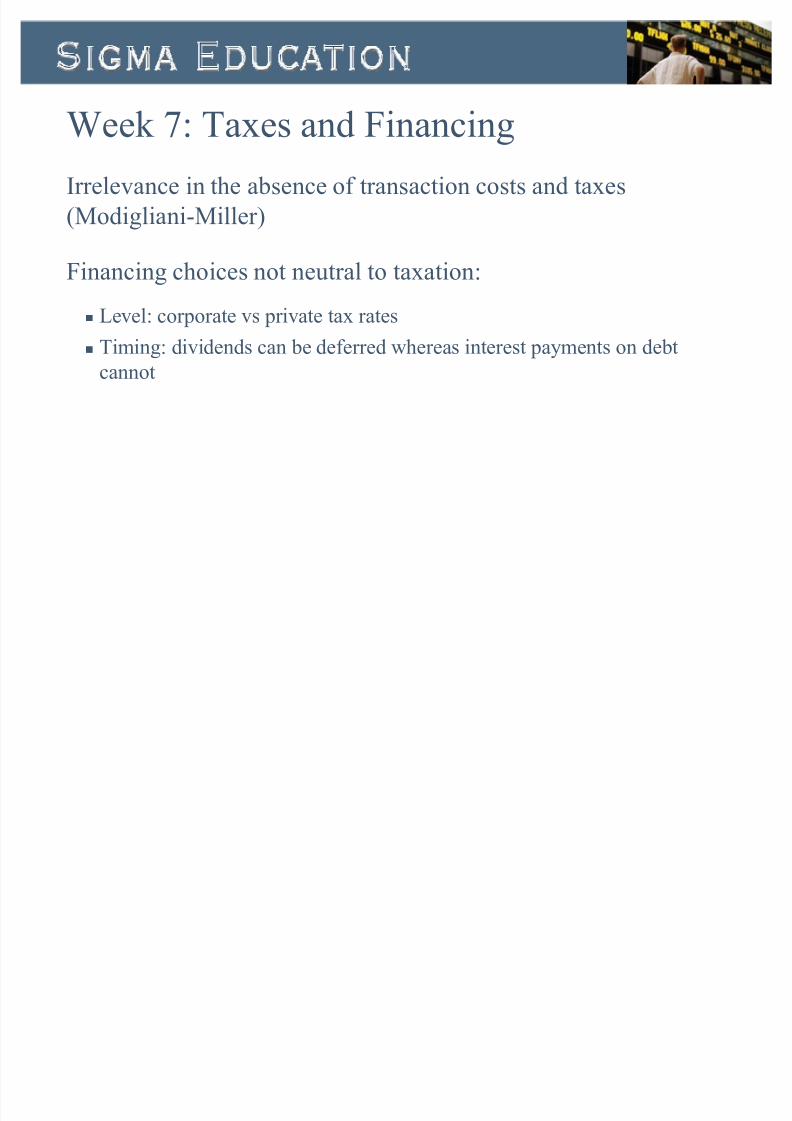

Week 7: Taxes and Financing

Irrelevance in the absence of transaction costs and taxes

(Modigliani-Miller)

Financing choices not neutral to taxation:

Level: corporate vs pr ivate tax rates

Timing: dividends can be deferred whereas interest payments on debt

cannot

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 118/177

Modigliani-Miller

The operating cash flow is divided into two components

Cash flow to debt holder s

Cash flow to equity holder s

Fundamental question: Does it matter how the s plit is made?

If it does we can create value also through f inancing choices (not only through investment choices)

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 119/177

MM cont«

Modigliani-Miller proved that capital structure choices

are irrelevant ± the s plit does not matter

This proof rests on the absence of transaction costs of any k ind: taxes, trading costs, and bankruptcy costs

The proof of the MM theorem uses a ³no arbitrage´

ar gument ± f inancial markets do not admit ³freelunches´, or trading strategies giving you a positive cash

flow with no pr ior investment

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 120/177

MM cont«

Consider two ³ver sions´ of the same f irm ± one ver sion is U for

unlevered (with no debt) and the other ver sion L for levered (with

debt)

The f irms have other wise the same operating cash flow X

The unlevered f irm has value VU and the levered f irm value VL

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 121/177

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 122/177

MM cont«

Suppose VL is smaller than VU

Then an investor can buy a 10% holding of L¶s debt and a 10%holding of L¶s equity, which entitles the investor to a 10% share

in the total cash flow X. He would then go to the market and sell10% of the cash flow X, which is valued at 10% of the value of U. This leaves him with zero future liability.

His trading gains are 10% of the difference between VU and VL,

which we have assumed is positive

This cannot be possi ble in an arbitrage free market, so we can conclude that VL must be equal to or greater than VU

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 123/177

MM cont«

Now suppose VU is smaller than VL

An investor buys 10% of the cash flow X and sells 10% of aclaim that promises the cash flow (1+r)D. The net cash flow is

10% of a claim that pays X-(1+r)D at matur ity, which is pr iced at 10% of the equity in L

The net future liability is zero, and the trading gains equal 10% of the difference between VL and VU, which we have assumed

positive

Again, this is not consistent with arbitrage free markets

In conclusion, it must be the case that VU = VL and that capitalstructure is irrelevant

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 124/177

What about r isk y debt?

When the corporate debt contract is r isk y it may bediff icult to f ind a ³synthetic´ corporate debt contract if areal one does not exist

We must assume, therefore, that the markets aresuff iciently complete in order to conclude that f inancing does not matter

Complete market = a market where the dimensionality

of the asset structure equals the dimensionality of theuncer tainty structure

If there are two states of nature (e.g. ³good´ and ³ bad´)then it suff ices with two distinct assets to make the

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 125/177

Bankruptcy costs

The Modigliani-Miller theorem also assumes that there

are no deadweight costs of bankruptcy

The debt holder s may not get all their money back if thef irm defaults, but this is not in itself enough to

jeopardise the MM-theorem

There must also be deadweight costs or liquidation costs (i.e. the value of the assets in default is less than the

value of the assets as a going concer n)

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 126/177

Taxes: Another impor tant factor

The tax system is generally fairly complex with different tax rates

for different individuals and institutions, and for different ty pes

of income

Therefore, it may be scope for ³tax arbitrage´ prof its in f inancing

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 127/177

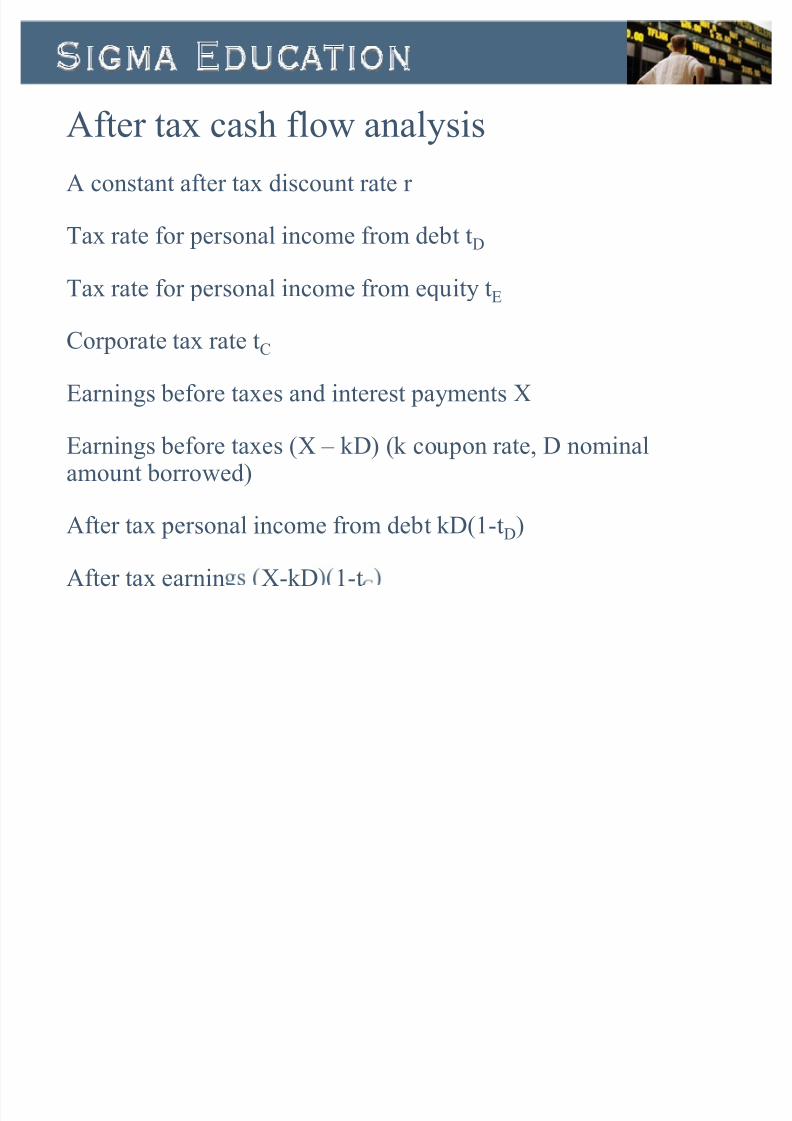

Af ter tax cash flow analysis

A constant af ter tax discount rate r

Tax rate for per sonal income from debt tD

Tax rate for per sonal income from equity tE

Corporate tax rate tC

Ear nings before taxes and interest payments X

Ear nings before taxes (X ± kD) (k coupon rate, D nominalamount borrowed)

Af ter tax per sonal income from debt kD(1-tD)

Af ter tax ear nin X-kD 1-t

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 128/177

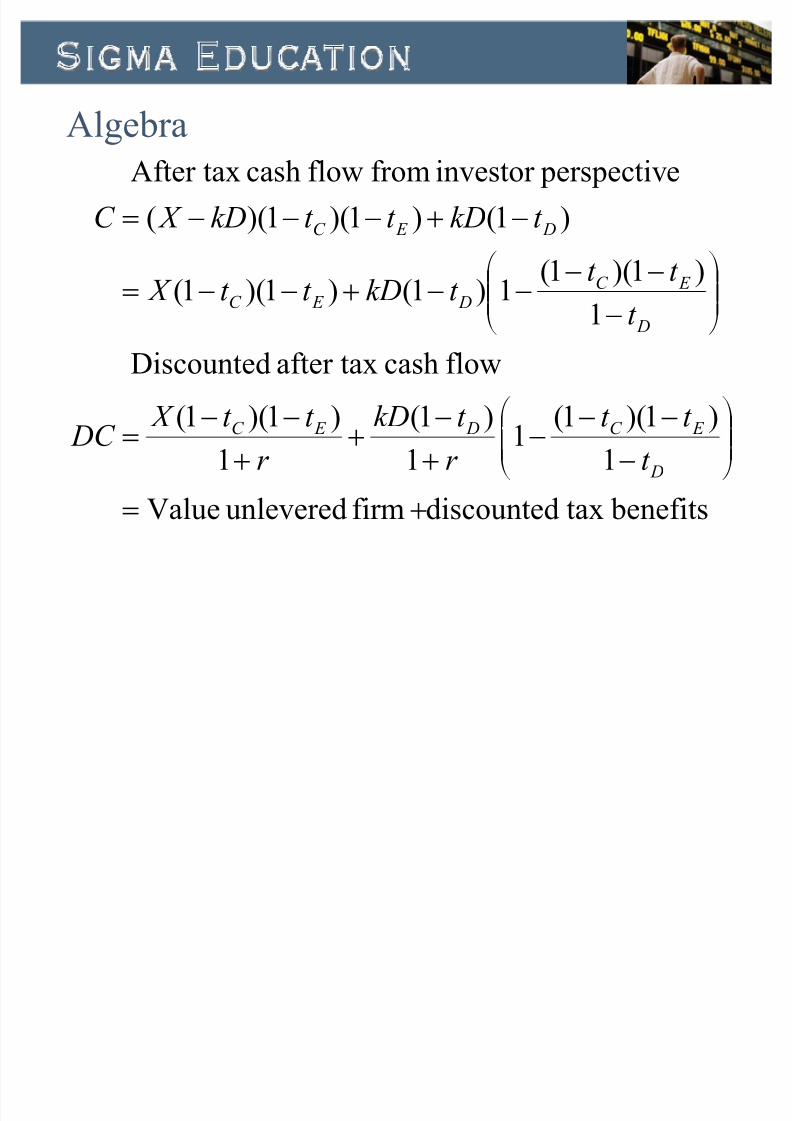

Algebra

benef itstaxdiscountedf irmunleveredValue

1

)1)(1(11

)1(

1

)1)(1(

flowcashaf ter taxDiscounted

1

)1)(1(

1)1()1)(1(

)1()1)(1)((

e per s pectivinvestor fromflowcashAf ter tax

!

¹¹ º

¸

©©ª

¨

!

¹¹ º

¸

©©ª

¨

!

!

D

E C D

E C

D

E C

D E C

D E C

t

t t

r

t k D

r

t t X DC

t

t t

t k Dt t X

t k Dt t k D X C

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 129/177

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 130/177

Preferred stock

Preferred stock: dividends on preferred stock are not taxdeducti ble at the corporate level as are interest payments on debt

This implies that corporate junior debt may be taxeff icient relative to preferred stock

However, the US tax code allows a 70% tax exclusion

for preferred dividends paid to corporate holder s, so theyield on preferred stock is of ten lower (before tax) than on junior debt even though the debt has senior ity over the preferred stock

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 131/177

Investor conflicts?

Tax exempt equity holder s prefer in general to reduce the borrowing of the f irm so as to transfer income from debt repayments to dividend payments

High-tax bracket investor prefer the opposite

Of ten tax-exempt munici pal bonds (or similar investments) offer yields that are greater than the af ter tax yield on corporate bonds for high-tax bracket investor s

Thus, the f irm can give these investor s an advantage by increasing the f irm¶s borrowing, as this frees capital that theinvestor s can use to invest in tax-exempt munici pal bonds

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 132/177

Inflation

We expect to see a one-to-one relationshi p between

inflation and nominal interest rates - if inflation

increases by one percentage point then so do nominal

interest rates

Higher inflation, therefore, leads to higher nominal

borrowing costs that yield in tur n greater tax deductions

Therefore, the tax effect has greater bite in per iods of

high inflation

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 133/177

Empir ical evidence

Do f irms with greater taxable ear nings borrow more?

No, but this may be because f irms in general rarely issue equity

Firms that perform poorly, therefore, tend to accumulate debt to meet their investments

Tax code changes that affect the relative tax benef it of borrowing should have an impact on corporate f inancing

Yes, US tax reform of 1986 which reduced the tax benef its of other things than debt (such as depreciation rules and investment tax credits) gave r ise

to an increase in borrowing among f irms most affected The f irms less affected did not increase their borrowing to the same extent

Taxes matter but don¶t explain ever ything

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 134/177

R eadings

Gr in blatt/Titman chapter 14, including the appendix

14.10 Are There Tax Advantages to Leasing not so relevant

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 135/177

Exercises

1. A f irm has assets valued at 100, and debt valued at 50. It plans to restructure its liability side by increasing its borrowing to 70 and paying a dividend of 20 to its shareholder s. The debt has zero beta before and 0.001 beta

af ter the recapitalization. The beta of the equity is 2 beforethe recapitalization.

a) What are the values of the equity before and af ter therecapitalization?

b) What is the beta of the assets of the f irm?

c) What is the beta of the equity af ter recapitalization?d) The recapitalization has increased the beta of the debt (and therefore

the cost of debt capital). Has it also increased the beta of the equity?Does this mean that the total cost of f inancing has increased?Explain.

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 136/177

Week 8: Taxes and Dividends

In fr ictionless markets dividends don¶t matter

Why do f irms nonetheless pay dividends?

Taxes and dividends

Stock retur ns and dividend yields ± what is the connection?

Investment distor tions caused by taxes in dividends

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 137/177

Cash flow to shareholder s

Shareholder s ear n money through holding equity that ear ns a cashflow (such as dividends) and capital gains (which can be realizedthrough selling stock)

The cash distr i bution to shareholder s is normally discretional ±

the company can decide how much cash flow to give their shareholder s

Cash distr i bution comes in two forms ± dividend payments andshare repurchase schemes

Dividend payments do not affect the number of shares but willreduce the value of each share

Share repurchases do normally not affect the value of each share but will reduce the number of shares outstanding

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 138/177

How much of ear nings is cash flow to

shareholder s?Dividend payout ratio: the ratio of dividends to ear nings

In the US, this ratio has declined from about 22% in

1980 to about 14% in 1998

Over the same per iod, the ratio of share repurchases to

ear nings increased from 3% to about 14%

The total ratio of cash flow to ear nings has been

relatively stable at about 25% of ear nings

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 139/177

Dividend yields

Dividend yield is the ratio of dividends per share over pr ice per share

Ty pical patter n is that high-tech growth f irms have low dividend

yield and dividend payout ratios (Microsof t paid its ver y f ir st dividend this year)

Stable, old economy companies such as mining, oil andmanufactur ing pay about half their ear nings as dividends

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 140/177

What is the optimal dividend payout

ratio?Assumption: fr ictionless economy (no transaction costs, taxes, or other fr ictions)

Investment policy unaffected by dividend payments

Modigliani-Miller Dividend Irrelevance Theorem:

The choice between paying dividends and repurchasing shares is a matter of indifference to shareholder s

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 141/177

Modigliani-Miller Irrelevance

Consider two identical equity f inanced f irms, the only difference

is dividend policy

Firm 1 pays 10m as dividends

Firm 2 repurchases stock wor th 10m

Af ter the end of the year, the f irms are wor th X

In the beginning each f irm has 1m shares outstanding

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 142/177

MM cont«

Each share eventually sells for X divided by the number of shares

Firm 2 buys back 10m wor th of stock

If share pr ice is p, and f irm 2 buys back n shares, we k now that pn=10m

We also k now that p=X/(1m-n)

Suppose X = 150m

Solving both equations gives us n = (10m1m)/(X+10m), so we get n = 62,500,and p = 150m/(1m-62,500) = 160

Firm 1: stock pr ice is p = 150m/1m = 150, but each stock gives a dividendwor th 10m/1m = 10, so the total value of each stock is 150+10 = 160

Since shareholder s get the same cash flow eventually, the shares must sell at the same pr ice initially, i.e. dividend policy does not matter

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 143/177

Taxes and cash distr i bution to

shareholder sClassical tax system

Dividends taxed as ordinar y income and capital gains at a lower rate than ordinar y income

Dividends are not tax deducti ble at corporate level, so dividends are also

subject to corporate taxation

Imputation system

Dividends are taxed as ordinar y income but investor s get a par tial taxcredit for corporate taxes (to off set per sonal taxes)

Dividends are not tax deducti ble at corporate level

Systems that eliminate double taxation

Dividends are tax deducti ble at corporate level and taxed as ordinar y income at investor level

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 144/177

Classical tax system

The classical tax system implies a tax disadvantage of dividend payments

Dividend $100, 35% tax implies an immediate tax

liability of $35

Share repurchase scheme: an investor sells $100 wor thof shares. Suppose or iginal cost was $76. This implies ataxable capital gain of $24. Taxed at 20%, this implies

an immediate tax liability of $4.8

Share repurchase scheme much cheaper than paying dividends

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 145/177

Tax avoidance schemes

In theor y, investor s can of ten invest in a scheme that gives an immediate tax relief against a deferred futuretax liability

In practice, investor s do not take advantage of theseschemes but instead choose to pay taxes (or are unableto invest in tax avoidance schemes) on the receiveddividends

The question is, therefore, why corporations continue to pay dividends when they are so tax ineff icient

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 146/177

Dividend clienteles

Some investor s do not pay taxes

These investor s will, ever ything else being equal, prefer high dividend yield f irms to low dividend yield f irms as

they do not pay tax on the dividend

Firms might adopt different dividend policies to attract different investor clienteles

Empir ical evidence suggests that investor s¶ por tfolios have dividend yields that are related to their tax status (high tax bracket investor s choose low dividend yieldstock s and vice ver sa)

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 147/177

Dividend payments and stock retur ns

Do stock s with high dividend yield compensate

investor s for the tax disadvantage?

Higher retur ns should then lead to lower values,reflecting the higher discount rates applied to future

cash flows

R esearch has focused on two retur ns effects

Ex-dividend day behaviour of stock pr ices

Whether cross-sectional dividend yield differences affect

expected retur ns

di id d d i d

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 148/177

Ex-dividend day pr ice drop

If you buy the stock on the day before the ex-dividend day, you are entitled tothe future value of the stock and the current dividend payment

If you buy the stock on the ex-dividend day, you are entitled only to the futurevalue of the stock

The stock pr ice should, therefore, drop on the ex-dividend day to reflect thedividend payment

Empir ical results from the 1960s indicate that the ex-dividend day pr ice drop is about 77.7% of the dividend payment on average, but was higher (90%) for dividend payments greater than 5% of the stock pr ice, and lower (50%) for thesmallest dividends.

These results indicate a tax effect (investor s discount a tax rate of around22.3% on dividends), and a clientele effect (investor s with different tax rates hold por tfolios with different dividend yields)

E di id d d

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 149/177

Ex-dividend day cont«

Transaction cost ar gument

Consider buying a stock at $20 before the ex-div day, receive a $1 dividend, then sell the stock for $19.20. This yields $1 taxable prof its and $(20-19.20) = $0.80 taxdeducti ble losses. The net prof it is $0.20 less taxes, but it is still arbitrage prof its.The stock needs to drop by the full amount to preclude arbitrage prof its.

If there is a $0.10 per share transaction cost, the investor receives taxable prof its of $1 in dividends, and incur $0.80 in tax deducti ble losses. The net prof it is $0.20, but the investor must also pay $0.10 in transaction costs, so the net prof it is only $0.10 less taxes. If the stock drops to $19.10, therefore, there are no arbitrage prof its to be made.

If the dividend payment is only $0.40, the necessar y pr ice drop is $0.30 to prevent arbitrage prof its. That is, the pr ice drop is greater for high dividend yielding stock s in percentage terms (as the clientele effect predicts).

Pr ice drop less than the dividend payment is also obser ved in countr ies that donot have a classical tax system, suggesting this is not a tax dr iven phenomenon at all

C i l l i b

8/3/2019 CFA1_Corporate Finance and Equity Investment Training

http://slidepdf.com/reader/full/cfa1corporate-finance-and-equity-investment-training 150/177

Cross-sectional relation between

dividend yield and stock retur nsIf dividends are more heavily taxed than capital gains,the expected retur n must be greater for high dividendyield stock s.

Empir ically, stock s with high dividend yields havehigher retur ns, but the relationshi p is not straightfor ward

The relationshi p is U-shaped, with zero dividend yieldstock s have higher expected retur n than stock s with low dividend yield, but for stock s paying dividends, theexpected retur n increases with the dividend yield

H di id d ff fi i