ch04 beechy ism

TRANSCRIPT

CHAPTER 4

Wholly Owned Subsidiaries:Reporting Subsequent to Acquisition

This chapter deals exclusively with the subsequent reporting of wholly owned subsidiaries, with the emphasis on purchased subsidiaries as a follow-up to the discussion of business combinations in Chapter 3. Unlike the preceding two chapters and Chapter 5, Chapter 4 is procedurally oriented as it goes through the mechanics of subsequent-year consolidations.

An especially important topic in this chapter is the elimination of intercompany transactions and balances, including unrealized profit on intercompany sales of inventory. Other topics discussed in this chapter include the acquisition adjustment (to record fair values and goodwill), amortization of FVAs, equity reporting, and the consolidated statements of income and cash flows. The financial statement impacts of equity reporting and of consolidation are compared.

This chapter uses the direct approach, while the worksheet approach is available on the companion website to this text. Some students prefer one approach while others prefer another. They should experiment with both approaches to discover which method they prefer.

A very brief discussion of goodwill impairment is included in the chapter. Appendix 4A addresses income tax allocation issues subsequent to acquisition, a follow-up to Appendix 3A. Appendix 4B addresses the goodwill impairment test in more detail.

SUMMARY OF ASSIGNMENT MATERIAL

Case 4-1: Growth Limited This is a brief discussion case that focuses on two aspects of the costs versus benefits to private companies to comply with IFRS: (1) testing for impairment of goodwill and (2) future income taxes. The setting is a very small company that is providing audited statements to a bank in compliance with a loan agreement.

Case 4-2: Pelican Systems Inc.In this case students must consider the users’ objectives in evaluating the accounting policies that were followed in the preparation of the prior year financial statements.

Case 4-3: Brand Drug LimitedIn this case, students are asked to discuss the issues surrounding a company’s decision to change from equity to cost in reporting an investment. Circumstances have changed, but the case can be argued either way. A good class discussion can be stimulated by having

Copyright © 2014 Pearson Canada Inc. 139

Chapter 4 – Wholly Owned Subsidiaries

half the class argue for the change and half against.

Case 4-3: Exotic Bean Bags Inc.This case requires students to consolidate the translated financial statements of a 100% owned foreign subsidiary with the financial statements of the parent and to suitably account for the investment in an associate. The case also requires students to assess the appropriateness of using consolidated versus separate entity SCI to assess the profitability of the parent.

The investment in the associate resulted from the sale of the 80% ownership of the retail business previously owned by the parent. As part of the sale agreement, the parent has assured the majority owner of the retail business that it will reimburse the retail business the shortfall if the latter’s profit is less compared to the profit on the parent’s consolidated IFRS based SCI. The parent is also seeking a bank loan for expansion purposes. The bank has asked the parent for its IFRS based consolidated SCI.

P4-1 (20 minutes, medium) Consolidation-related adjusting entries in relation to the inter-company sale of inventory and unrealized gains in one year and the realization of those gains in the subsequent year are required.

P4-2 (30 minutes, medium) Preparation of a simple statement of comprehensive income and statement of financial position for a parent-founded subsidiary after one year. Includes unrealized profits, an intercompany loan, and intercompany interest payments and accrual.

P4-3 (40 minutes, medium) This problem follows on from P4-1, which should be solved first. Both upstream and downstream sales are present in the second year of operations, as is an intercompany sale of land. A statement of financial position and statement of comprehensive income are required.

P4-4 (40 minutes, medium) Consolidation one year subsequent to a business combination. Only a statement of financial position is required. The one challenging element is the presence of a sale of an asset with a fair value increment.

P4-5 (60 minutes, medium)This problem requires preparation of a consolidated statement of comprehensive income and a statement of financial position one year after acquisition. The problem requires some thought on the part of the student, but it is not “tricky”.

P4-6 (90 minutes, difficult)A problem set two years after acquisition, it requires computation of selected amounts, including consolidated earnings and equity basis earnings. It does not require consolidated statements.

P4-7 (90 minutes, medium)

Copyright © 2014 Pearson Canada Inc. 140

Chapter 4 – Wholly Owned Subsidiaries

This problem requires two sets of parent company financial statements: (1) a statement of financial position and statement of comprehensive income prepared on the equity basis, and (2) a consolidated statement of financial position, statement of comprehensive income and statement of changes in retained earnings, one year following the acquisition. A comparison of consolidation techniques under equity recording vs. cost recording is also required. This is a very comprehensive problem that brings the students up to speed on consolidation technique.

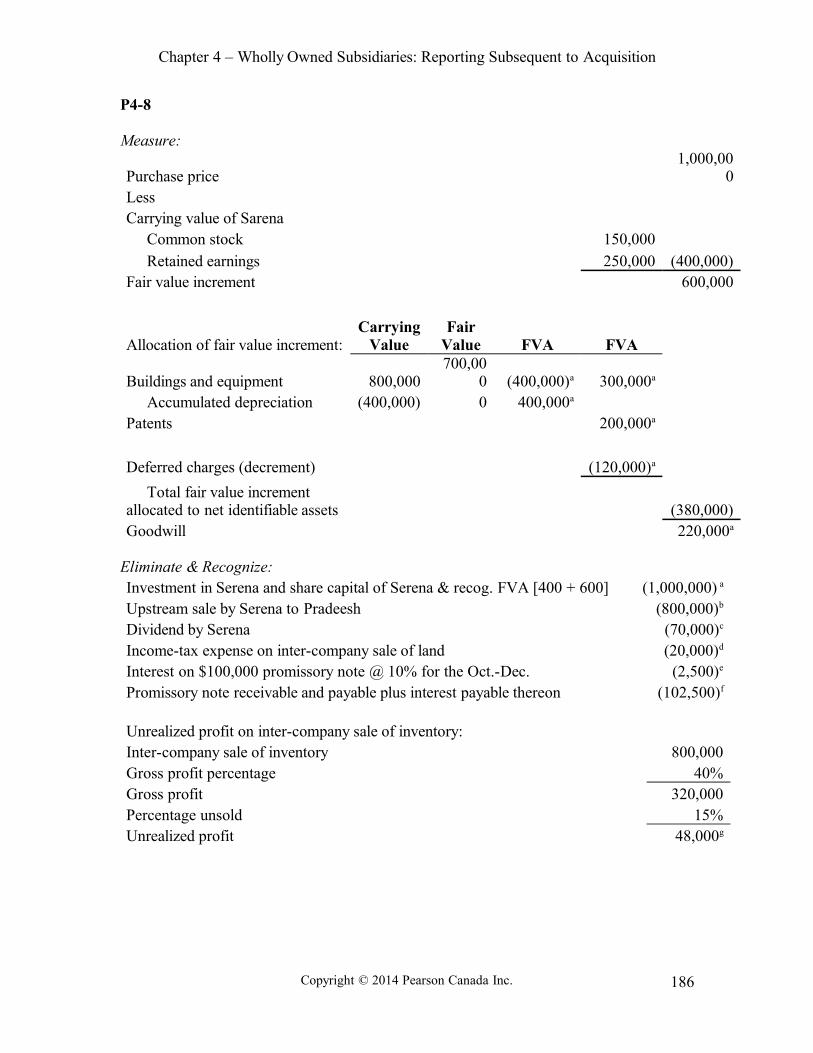

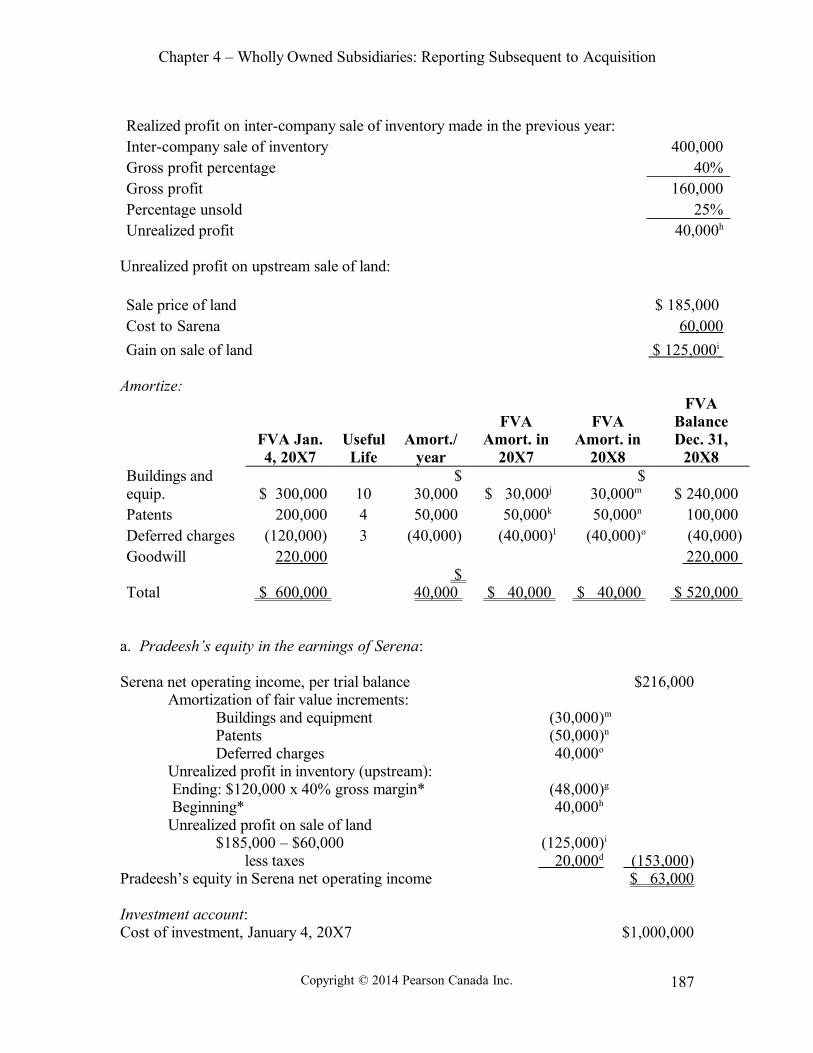

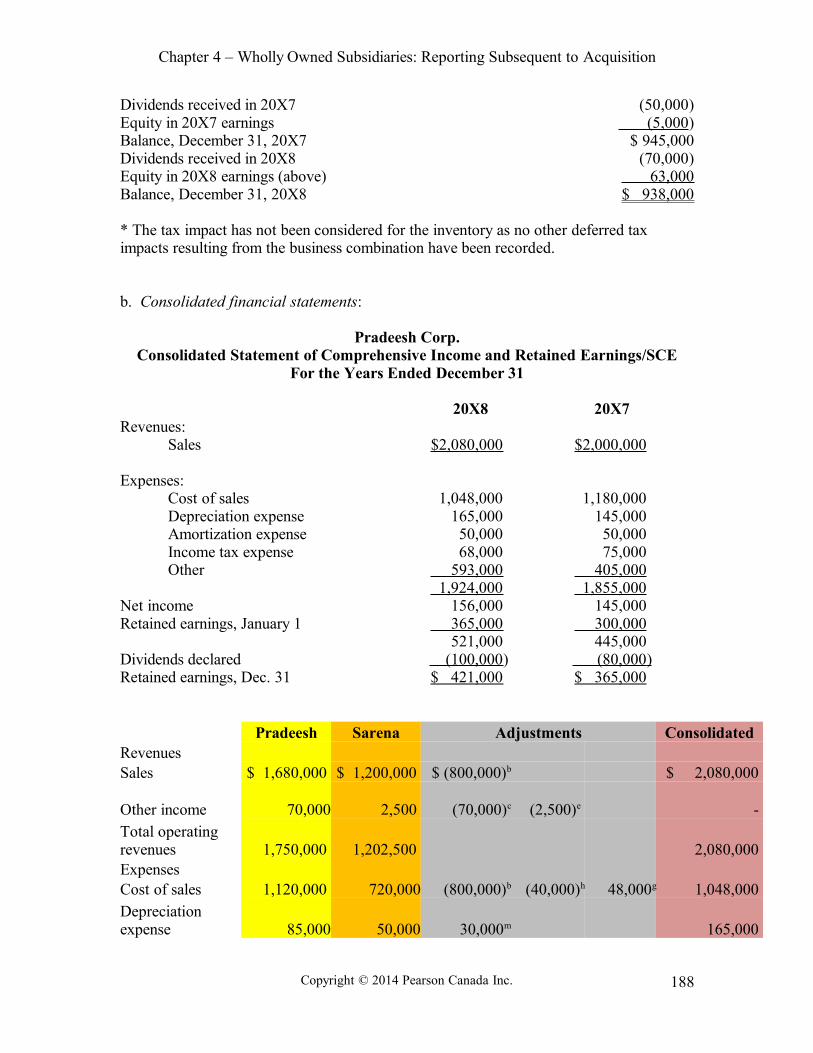

P4-8 (120 minutes, difficult) The second in the series, P4-8 carries on from P4-7 for the second year after the business combination. A full set of consolidated statements is required, prepared on a comparative basis. The students are also required to determine the parent’s equity in the earnings of the subsidiary and the balance in the investment account, if the equity method was used.

P4-9 (60 minutes, medium)What makes this problem challenging is the disposition of FVAs on current assets, the FVA on bonds payable, and both upstream and downstream sales of inventory. The problem requires a consolidated statement of comprehensive income (for the second year after acquisition) and the calculation of selected statement of financial position amounts.

P4-10 (120 minutes, difficult)No consolidated financial statements are required in this problem. Nonetheless, this is a difficult problem since it requires the calculation of many consolidation and equity method related amounts relating to the first two years after acquisition.

P4A-1 (25 minutes, medium)This is a continuation of P4-1 that requires all consolidation-related adjusting entries, including deferred tax entries in relation to the unrealized and realized gains on the upstream sale of inventory in the year of such sale and the succeeding year.

P4A-2 (90 minutes, difficult)This is a continuation of P4-7. The requirements are the same as in P4-7 except that the deferred tax consequences of consolidation adjustments have to be considered as well.

P4A-3 (150 minutes, difficult)This is a continuation of P4-8. The requirements are the same as in P4-8 except that the deferred tax consequences of consolidation adjustments have to be considered as well.

ANSWERS TO REVIEW QUESTIONS

Q4-1: The acquisition adjustment has the effect of (1) eliminating the initial cost of the investment, (2) establishing the fair value adjustments on the net assets acquired, and (3) establishing the goodwill, if any.

Q4-2: The acquisition adjustment for a parent-founded subsidiary will not include fair

Copyright © 2014 Pearson Canada Inc. 141

Chapter 4 – Wholly Owned Subsidiaries

value adjustments nor goodwill.

Q4-3: Goodwill is not amortized. Goodwill is tested for impairment on an annual basis for each cash-generating unit. Qualifying entities can elect to adopt provisions under GAAP for private companies and test goodwill for impairment only when an event or circumstance indicates that the fair value of the reporting unit may be less than its carrying value.

Q4-4: The fair value adjustments are really just a part of the cost of the assets and liabilities at the time of acquisition, which is equal to their fair values. As with the cost of any asset, the cost (including the fair value adjustments) must be depreciated or amortized over the expected useful life of the asset.

Q4-5: The profit on intercompany transactions must be eliminated when the profit has not been realized by a subsequent sale to an outside third party or by using up the asset or services transferred in the normal productive activities of the company.

Q4-6: There are a great deal of estimates and judgments required by management in order to determine the fair value of a cash-generating unit as fair value is a function of an entity’s estimated future earnings. The estimates and judgments required by management to determine the fair value of a cash-generating unit directly impact the goodwill impairment test.

Q4-7: Qualifying entities may elect to test goodwill for impairment only when an event or circumstance indicates that the fair value of a reporting unit may be less than its carrying value.

Q4-8: When intercompany sales are eliminated in consolidation, the full amount of the sales is deducted both from sales (for the selling company) and from purchases or cost of goods sold (for the buying company). If some of these goods have not yet been sold, then the ending inventory component of cost of goods sold must also be adjusted, otherwise the ending inventory will be overstated by the amount of the intercompany profit. The act of reducing the ending inventory component of cost of goods sold has the apparent effect of increasing the cost of goods sold. Remember that increasing a cost will reduce net income therefore eliminating intercompany profit.

Q4-9: The acquisition adjustment relates to the date of the purchase transaction. Operations adjustments are for post-acquisition activities and events.

Q4-10: The equity method includes all of the same types of adjustments to earnings that would be required if the investee corporation were consolidated with the parent. Therefore, the method is sometimes called the consolidation method of equity reporting.

Q4-11: A parent company’s net assets are the same amount under equity reporting as they would be on consolidated statements. The difference between equity reporting and consolidation is that under consolidation, the investment in the subsidiary is disaggregated into the component assets and liabilities, but the net assets remain the same.

Copyright © 2014 Pearson Canada Inc. 142

Chapter 4 – Wholly Owned Subsidiaries

Q4-12: Under equity reporting, discontinued operations reported by the investee are reported as discontinued operations on the statement of comprehensive income of the investor only if the items represent discontinued operations to the parent by satisfying the requirements at the level of the parent. Nevertheless, income from the discontinued operations of associates has to be separately disclosed. Regardless of the treatment, such income is not included in the one-line equity pick-up of the subsidiaries earnings.

Q4-13: Any unrealized profit in beginning inventories that has been realized through sales in the current year will increase consolidated earnings for the year.

Q4-14: IFRS 3 requires the acquirer to disclose such information which enables users of its financial statements to evaluate the nature and financial effect of a business combination that occurred either 1) in the current reporting period or, 2) after the end of the reporting period but before the issue of its financial statements. The acquirer is also further required to disclose information which enables users to evaluate the financial effects of adjustments recognized in the current reporting period relating to the business combinations which occurred either in the current period or previous reporting periods. Specifics regarding such information are provided in Appendix B of the standard. Additional information not required under Appendix B but which is required to meet the reporting objectives as stated above should also be disclosed. The disclosures should cover the following:

• a description including the name of the acquired subsidiary, the date of acquisition, percentage of the voting shares acquired, primary reason for the business combination and how control was obtained,

• qualitative description of the factors giving rise to the goodwill and intangible assets not separately identifiable from goodwill,

• the amount of any contingent consideration recognized, and arrangement and basis for arriving at such amount,

• amounts of the major classes of assets and liabilities acquired,• fair value on the acquisition date of the purchase consideration transferred and of

each major class of consideration,• the amount and reason for a gain from bargain purchase if present,• the amount and measurement basis of the non-controlling interest if less than 100

percent of the acquiree is acquired.

For acquisitions that are individually immaterial, similar information should be disclosed in the aggregate.

Q4-15: Consolidation of a parent-founded subsidiary generally will be simpler than consolidation of a purchased subsidiary because it will not include fair value adjustments nor goodwill.

Q4-16: When one corporation directly acquires the assets and liabilities of another corporation (rather than indirectly through the purchase of shares), the assets and recorded liabilities acquired will be recorded on the acquirer’s books of account and will henceforth be included in the acquirer’s trial balances. No consolidation will be necessary because there is no separate legal entity to consolidate.

Copyright © 2014 Pearson Canada Inc. 143

Chapter 4 – Wholly Owned Subsidiaries

CASE NOTES

Case 4-1: Growth Limited

Objectives of the Case

This case presents a brief scenario of a very small company that has limited users of its financial statements. It gives students practice at relating accounting practices to the needs of both the preparer and the users. The case originally appeared on the 1987 UFE as a 15 mark (36 minute) question. This case is also a good example of when private enterprise GAAP reporting options are appropriate.

Objectives of Financial Reporting

So far as we can discern from the case, we need to consider only two users of the statements, the president of the company and the bank. The company is quite small, having sales of only $1,800,000, and therefore is unlikely to require an audit unless a specific user has requested one. The audit is being provided, for the first time, for the bank’s benefit, who wants it in order to test compliance with the loan agreement (which no doubt includes other explicit covenants that we are not told about). The most likely objectives of the preparer are contract compliance and performance evaluation. The banker, who is the main user of the financial statements, will be interested in contract compliance and cash flow prediction. The banker will likely be the primary user since the company requires the loan to support its expansion plans.

Discussion

Goodwill

While goodwill was required to be amortized a few years ago under then extant Canadian standards, under IFRS goodwill has to be tested for impairment on an annual basis and not amortized. We can presume that the goodwill was acquired in a business combination involving a purchase of the net assets of another company (otherwise, the opening goodwill balance would constitute internally generated goodwill and thus should not have been capitalized in the first place). Acquired goodwill is different from the sort of goodwill that the president is talking about, the goodwill that is built up through quality of operations. A company is not allowed to capitalize or record goodwill unless there has been a business combination. It appears that the new goodwill was also recorded as a result of a business combination.

The president does not want to test goodwill for impairment as he does not believe the goodwill has declined in value, The bank may not be concerned with the goodwill on the statement of financial position as banks often disregard the goodwill number in their calculations, as demonstrated by the comment in respect of the deferred tax balance. The president could adopt provisions for goodwill under GAAP for private enterprises which only require an impairment test when an event or circumstance indicates the fair value of

Copyright © 2014 Pearson Canada Inc. 144

Chapter 4 – Wholly Owned Subsidiaries

the goodwill is less than its carrying value.

Deferred income taxes

It is not an unusual practice for bankers to negate the impact of deferred income taxes by adding the DIT balance to retained earnings. However, if the bank is not also adding the deferred portion of income tax expense back to earnings, they are doing only half the job. By not calculating deferred income taxes at all, the company has removed the need for the bank to make adjustments. Thus the objectives of cash flow prediction and contract compliance seem to be better served by not following income tax allocation.

On the other hand, deferred income taxes can represent future cash flows in a small business. Small companies usually have very uneven capital expenditures, with only occasional large outlays for capital equipment. In such circumstances, it is quite likely that the CCA/depreciation temporary difference will reverse in the future, and higher cash outflows for income tax will result. Nevertheless, as long as the bank is uninterested in tax allocation, there seems little point in calculating deferred income taxes unless the company intends to go public. Once again, the president could adopt provisions under private enterprise GAAP - this time to account for income taxes using the taxes payable method. This would meet with both users’ needs.

IFRS versus Accounting Standards for Private Enterprises

The underlying issue in this case is that of IFRS versus Canadian Accounting Standards for Private Enterprises. Students must be able to recognize that this is a very small company, and that accounting principles that are appropriate for a large, publicly accountable enterprise may not be appropriate for a small, private enterprise.

[CICA, adapted]

Case 4-2: Pelican Systems Inc.

Objectives of the Case

In this case students must consider significant accounting issues relating to the prior year financial statements of a new audit. The accounting issues covered include revenue recognition, acquisition of equipment, financing fees, sale of a subsidiary, a 10% investment and the acquisition of a subsidiary. This case is to be written in memo format.

Memo to: Partner, Sharp & Ipson

Users and Objectives

PSI is a publicly accountable enterprise where aggressive accounting policies have been used. In contrast, the board and the shareholders would have wanted the financial statements to present an accurate reflection of management’s performance.

The CEO appears to be interested in maximizing PSI’s net income over a three-year

Copyright © 2014 Pearson Canada Inc. 145

Chapter 4 – Wholly Owned Subsidiaries

period as his bonus is directly tied to net income. Hence, the CEO has a bias to overstate net income. The CEO has also indicated he expects an increase in both revenue and EPS and will wish to meet those indicators, providing another bias to increase revenue and income.

The creditor would be interested in both future cash flows for payment of the interest and principal on the loan and compliance with debt covenants if any.

The securities commission would be another user of the financial statements. It would be very concerned with changes in accounting policies and why those changes are being made. As a result, there could be negative issues with respect to the securities commission listing and/or legal repercussions.

Evaluation of Accounting Policies

A. Sales Leasing

PSI’s policy appears to recognize revenue on the sale of the equipment to the financial institution. At this point, the title of the equipment is transferred to the financial institution and the equipment is delivered to the lessee, indicating that PSI has completed its performance obligations. In addition, payment is received from the financial institution.

However, PSI retains a risk if the lessee defaults since PSI has guaranteed the lessee’s payments. If the lessee defaults, PSI is obligated to pay the financial institution. The result is that PSI has retained the risk associated with the collection. This is evident in the first year where $400,000 or 20% of the lease payments were not collected by the financial institution. These customers are classified as a high credit risk which makes this obligation even riskier. In addition, PSI may not be able to accurately measure the revenue at the time of the sale to the financial institution since the value of payments it will need to make under the guarantee is not known. PSI also has the right to purchase the lease receivables at any time, which it may decide to exercise to obtain title to the equipment so it has some collateral. At the present time, PSI holds the risk and has no collateral to offset the risk.

If PSI is able to estimate the value of the payment guarantees it will be required to make, it could recognize revenue at this point. However, it is unlikely the payment guarantees can be estimated given the lack of history and the high credit risk.

Based on the above analysis, the revenue recognition policy used for the preparation of the 20X5 financial statements was very aggressive and does not meet the IFRS criteria for revenue recognition. Even though this meets management’s objective of higher revenue, net income and EPS, it is not acceptable. In addition, the shareholders are not provided with a clear picture as PSI has guaranteed the payment stream and no accrual has been set up for this. It is as if PSI is the lessor itself.

Alternate points of revenue recognition include:

- Installment-sales method, thereby recognizing revenue as collections are received, due to the high risk of non-collection. The cost recovery method is also an option but is

Copyright © 2014 Pearson Canada Inc. 146

Chapter 4 – Wholly Owned Subsidiaries

overly conservative.

- Transfers of receivables if PSI has surrendered control over the receivables. It has not done that at this point as it has retained the risks and right to purchase. Therefore, it would not meet the sale criteria and would be accounted for as a borrowing.

- Lease approach. As noted above, PSI has retained the risks of a lessor and is, in substance, the lessor.

a. Installment-sales method

The installment-sales method permits the recognition of a portion of the gross profit when a payment is received. This would be appropriate due to the possibility the lessees may not pay, as they are high credit risk customers. Under this approach, $5,400K × $1,600/$12,000) or $720K gross margin would be recognized rather than $5,400K in 20X5.

b. Transfers of receivables A liability would be set up to the financial institution for the amount of the loan provided to the lessee and a corresponding receivable from the lessee. PSI may be able to offset the obligation, since the obligation and receivable are expected to be settled simultaneously and neither are legally PSI’s. However, it is unlikely the receipts will match the required payments as can be seen from the shortfall of $400K in 20X5, which means offsetting would not be appropriate.

c. Lease approach Due to the high risk of collection, the lease would not meet the criteria to be considered a finance lease by the lessor and would, therefore, be considered an operating lease. As such, the sale of the equipment would not be recorded. The equipment would remain on PSI’s books and be amortized. Lease payments would be recorded as income when received.

Based on the above analysis, I do not believe the accounting policy used in 20X5 was consistent with IFRS. PSI should use the installment-sales method to recognize revenue in 20X6 and apply this on a retroactive basis. This will decrease net income by $5,400K - $720K = $4,680K, which will also decrease equity.

B. Financing Fee Arrangement

The 10% fee paid to the financial institution is being deferred and recognized over the three-year period of the leases. This policy did not match the costs incurred (the 10% fee) to the revenue, which was being recognized up front.

The fee is compensation to the financial institution for a lower interest rate for the lessee and, therefore, facilitates a sale. It is, therefore, a direct cost of the sale and should be matched to the revenue earned. Given my recommendation for revenue recognition, this would be matched as a cost against the installment sale revenue earned each year. That is, for 20X5, $1,200K × $1,600/$12,000 = $160K would be charged to cost of sale. The rest would remain in deferred charges until more installments are received. This allows for the

Copyright © 2014 Pearson Canada Inc. 147

Chapter 4 – Wholly Owned Subsidiaries

matching of the related expense to the revenue earned, if the installment-sales method to recognize income is followed.

C. Acquisition of Equipment

Under IAS 16, equipment has to be initially recognized at its cost to the entity. In this case, there is no laid down cost but a contingent payment obligation. PSI is treating the payments similar to a royalty expense that is expensed when paid. This is an example of off-statement of financial position financing (off-balance sheet financing).

The contingent payments cover a three-year period and the life of the equipment is expected to be five years. The cost price of the property, plant and equipment is to be allocated over the useful life of the equipment to match to the revenues earned. The current policy does not do this, as the useful life is different than the period of the contingent payments.

Generally, the fair value of what is given up is used as the value of the asset. However, this is difficult to measure in this case, as the payments are contingent upon the gross margin earned in subsequent years on a particular product. The cost could be estimated using the predicted margins for the three-year period and the contract cost percentage, which gives a value of $3,900K (see Exhibit I). This assumes that the supplier of the equipment agrees with PSI’s definition of gross margin. If the expected sale and gross margin vary from the information provided, this would be treated as a change in estimate and adjusted from that point forward. The fair value of $3,900K would then be amortized over the expected useful life of five years. Alternately, the equipment could be recognized at its fair value of $3,000K, which has been provided. In both cases, an equivalent credit to a payable account would have to be entered.

While the recognition of the equipment as an asset does not match the expense with the cash flow, it does match, through depreciation, the cost of the equipment with the revenue it produces, which permits the shareholders to evaluate management’s performance. Both assets and liabilities will be increased and net income will decrease.

D. Sale of Subsidiary

The gain on the sale of the subsidiary is the result of a management decision and is significant. IAS 1, para 97 requires that an entity shall disclose the nature and amount of items of income or expense that are material. Further, IAS 1, para 98 the circumstances that would give rise to separate disclosure of items of income and expense include, among others, disposals of investments. Therefore, the gain on the sale of the subsidiary should be separated from S, G & A in the statement of comprehensive income and be reported as another item. This would permit the shareholders to have a higher-quality prediction of future operations. This treatment is evidence of aggressive reporting and manipulation by the CEO with the apparent objective of increasing his bonus.

If the subsidiary was in a separate line of business and would be considered a business component, it may also qualify as a discontinued operation to be reported below income from continuing operations.

Copyright © 2014 Pearson Canada Inc. 148

Chapter 4 – Wholly Owned Subsidiaries

E. Investment in H & P

Under the new IFRS 9, Financial instruments, equity instruments have to be carried at fair value. Management can either classify the equity instruments as Fair Value Through Profit and Loss (FVTPL) or Fair Value Through Other Comprehensive Income (FVTOCI). In both cases, the investment has to be valued on the SFP at the fair value of $20 per share on December 31, 20X5. Therefore, there is an unrealized gain of $19 per share. If management chooses to classify the shares as a FVTPL investment, the unrealized gain can be recognized as a gain in net income. Alternatively, if management chooses to classify the investment as FVTOCI, such a classification is irrevocable, and all gains and losses have to be taken directly to equity. Cumulative holding and realized gains or losses can never be reclassified into profit and loss. Thus, the unrealized gain would be included as an increase to other comprehensive income, which is part of equity.

The decrease in the value of H&P shares constitute a non-adjustment event after the reporting period. $ 40,000,000 is clearly material. According to Paragraph 21 of IAS 10 Events after Reporting Period, “If non-adjusting events after the reporting period are material, non-disclosure could influence the economic decisions that users make on the basis of the financial statements. Accordingly, an entity shall disclose the following for each material category of non-adjusting event after the reporting period:(a) the nature of the event; and(b) an estimate of its financial effect, or a statement that such an estimate cannot be made.”

Therefore, PSI has to appropriately disclose the decrease in the value of its investment in H&P after the SFP date. F. Acquisition of ATI

The acquisition of ATI should be recorded at its cost which includes the $6 million plus the value of the stock options (less the $1.5 million allocated to intangibles). Information has not been provided to calculate the value of the stock options. The allocation of the $1.5 million to the employment contract is accurate. However, intangibles are to be amortized if there is a limited useful life. While the stock options may indicate a longer-term interest in PSI, the legal life is three years and the useful life cannot exceed three years unless it is renewable at little or no cost. In this case, that is unlikely and the intangible should be amortized over a three-year period. This will result in an amortization charge of $167K ($1,500K ÷ 36 × 4).

Overall Conclusion on Accounting

The adjustments to net income will have a negative impact on the bonus paid to the CEO. This will reverse a small portion of the changes to net income.

As a result of the aggressive accounting policies used in 20X5, the CEO received a nice bonus. However, the objectives of the shareholders, board and the creditor were not met by these aggressive accounting polices. The financial statements will need to be restated.

Copyright © 2014 Pearson Canada Inc. 149

Chapter 4 – Wholly Owned Subsidiaries

PSI will need to contact both the securities commission and the creditor to advise them of the planned restatement. Disclosure of the changes in accounting policies will be required. Transparency will be key for all users.

Copyright © 2014 Pearson Canada Inc. 150

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

Exhibit I

To estimate the dollar value of the contingent payment of the equipment.

Sales20X6 $19,500,00020X7 27,300,00020X8 18,200,000

$65,000,000

Expected gross margin at 40% $26,000,000Cost at 15% of gross margin $ 3,900,000

Based on the information provided, the purchase price will be $3,900,000 over the three-year period. The time value of money will also have to be considered and the present value of the payments for 20X7 and 20X8 calculated.

Case 4-3: Brand Drug Limited

Objectives of the Case

This case requires students to consider qualitative characteristics that indicate whether an investment should be accounted for as a strategic investment (significant influence) or as a passive investment.

Overview

In this case, it appears that the investor corporation has lost its significant influence over the affairs of the investee corporation, and therefore the investor has switched from the equity to the cost basis of reporting the investment. All may not be as it seems, however, and students are required to investigate the substance of the situation and make a recommendation accordingly.

It is possible for a student to conclude either that the investment is passive and therefore BDL is not correct in changing to the cost method and should have instead changed to the fair value method, or that significant influence continues to exist and therefore BLD should return to the equity method. In either case, the student should complete his or her analysis along the path that he or she chose.

Discussion

The managers of Brand Drug Limited (BDL) are planning a share issue and do not want their company’s earnings impaired by the poor performance of National Pharmaceuticals Limited (NPL). BDL has changed from the equity method just prior to the release of potentially very poor earnings results by NPL, which raises questions about Brand’s motivations. Not only is NPL suffering from generic drug competition, the company also has further depressed earnings by writing off its intangible assets.

Copyright © 2014 Pearson Canada Inc. 151

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

[Note: it is a fairly common occurrence for companies to write down their assets during a major loss year; the theory seems to be that if operating losses are going to occur, it will not further damage the stock prices to write off assets. After the write-off, the company will then be in a better position to post strong earnings in subsequent years because there will be no asset amortization to charge against earnings. This earnings management technique is called a “big bath”.]

On the other hand, the relationship between BDL and NPL seems, at least on the surface, to be uncooperative. Intercompany sales are down, BDL has left the NPL board of directors, and NPL is refusing to supply information to CA and is being uncooperative with BDL in supplying year-end information. Thus, the investment by BDL in NPL seems to be passive and no longer strategic.

Accounting for the Investment

The choice of the appropriate method to account for the NPL investment depends primarily on whether BDL has significant influence over NPL. In assessing significant influence, the following factors should be considered:

• BDL’s ownership meets the 20% guideline;

• BDL had membership on the board of directors and voluntarily gave it up;

• intercompany transactions have declined and are no longer material;

• dividends have not been paid recently, and perhaps earnings of NPL will not accrue to BDL; and,

• given the uncooperative nature of NPL and BDL’s relationship, it does not appear that BDL has significant influence over NPL.

If BDL is able to exert significant influence over NPL, then the equity method of accounting for the investment remains appropriate. If not, the investment is passive. Under IFRS 9 passive investments in equity should be accounted for using the fair value method. BDL has the choice to treat the passive investment as either a fair value through profit and loss (FVTPL) investment or as a fair value through other comprehensive income (FVTOCI) investment. In either case, the cost method is not generally appropriate. IFRS 9 allows the use of cost as an appropriate estimate of fair value in limited circumstances such as when i) insufficient recent information exists to determine fair value, or ii) a wide range of possible fair value measures exist and cost is the best estimate of fair value within that range. Thus, BDL appears to be having an incorrect understanding of the accounting method allowed under IFRS for reporting passive equity investments.

The circumstances surrounding this investment have changed; however, it is difficult to determine whether management of BDL manipulated that change by ceasing to trade with NPL and removing the BDL representative from NPL’s board of directors.

Copyright © 2014 Pearson Canada Inc. 152

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

Fair Value Method

If it is determined that significant influence has been lost BDL is required to measure its continuing investment in NPL at its fair value on the date such influence was lost. BDL is required to recognize in profit or loss the difference between the fair value of its investment in NPL and the carrying amount in its books of its investment in NPL under the equity method. Thus, BDL’s retroactive reversal of its share of NPL 2005 earnings is incorrect. Also, the beginning of year unrealized inventory profits should be recognized.

BDL’s investment in NPL is most probably a FVTOCI investment since it has the intent to hold the investment for a period of time. The use of the fair value method requires a determination of the market value of the investment at year end. The investment in NPL would be recorded on the SFP at its fair value. The loss on the deemed sale of the investment would be recognized in profit and loss. The market price for the shares at August 31, 20X6 is $12 per share giving a total market price of $24 million ($12 × 2 million). The difference between the $24 million and the equity value at the time of the change in investment type of $3.4 million ($27.4 – $24.0) should be recognized as a loss in net income. This situation will require detailed note disclosure to enable the users to understand BDL’s financial statements.

Equity Method

BDL must reflect its share of NPL’s current loss, but the investment cannot be valued at less than $0. As shown below, the equity method would decrease BDL’s earnings by about $27 million.

Equity Valuation(in thousands of dollars)

Carrying value per draft $ 25,000Add back adjustment 2,400

27,400Equity adjustments:22% of CPL loss $(30,800)Realized upstream $5,500,000 × 0.22 1,210Unrealized upstream $1,500,000 × 0.22 (330) (29,920)Equity valuation (cannot be negative) $ 0

Copyright © 2014 Pearson Canada Inc. 153

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

Case 4-4: Exotic Bean Bags

Objectives of the CaseThis case requires students to consolidate the translated financial statements of a 100% owned foreign subsidiary with the financial statements of the parent and to suitably account for the investment in an associate. The case also requires students to assess the appropriateness of using consolidated versus separate entity SCI to assess the profitability of the parent.

Role:To prepare a memo addressed to the partner including the financial information requested by Ada and Erin and the analysis requested by them, including:• Preparing the consolidated SCI of EBBI after appropriately accounting for EBBI’s

stake in ERI.

• Ascertaining whether Erin’s assertion, that the profitability of EBBI on its IFRS based consolidated SCI would be higher than that of ERI, is correct and if incorrect analyzing the reasons for the dissimilarity between the assertion and the actual results.

• Discussing the appropriate financial statement (separate entity or consolidated SCI) to use for determining whether or not the guarantee by EBBI to ERI holds.

• While not explicitly required to do so, explaining why the bank wants the consolidated SCI and what the bank will make of EBBI’s consolidated SCI.

Report:

ToThe Partner,

I have provided below the financial information requested by Ada and Erin as well as the analyses required by them. Overview:

The bank as well as the agreement between EBBI and ERI requires that the financial statements of EBBI be prepared following IFRS. Obtaining the bank loan is a critical success factor for EBBI. It is also equally critical for EBBI to correctly determine whether or not ERI’s profits are less than those of EBBI so as to find out whether or not EBBI needs to fulfil its guarantee to ERI in relation to its profit percentage in 20X8. The correct determination of this issue is critical since it can significantly impact the ongoing business relationship between Ada and Erin.

Users & Objectives:

Users:

Copyright © 2014 Pearson Canada Inc. 154

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

• Ada

• Erin

• Bank

Objectives:

Ada:• The consolidated SCI of EBBI should portray as positive a picture about its

operations as possible so that that the bank is persuaded to sanction the loan to EBBI.

• Consolidated SCI of EBBI should show a profit percentage less than that of EBI so that EBBI is not forced to act upon its guarantee.

• Notwithstanding the above objective, in the long run it is crucial for Ada that the relationship between EBBI and EBI and Erin remains strong. Hence, to ensure that Erin does not feel cheated Ada would like EBBI’s Consolidated SCI to reflect its true economic income.

• Performance evaluation of EBBI and comparing its performance with that of ERI. Would also want to assess the soundness of the sale of the retail operations to Erin.

Erin:• The consolidated SCI of EBBI should truly reflect its real economic income.

• Other things being equal, Erin would alternatively want EBBI’s consolidated SCI to show high profits such that it is forced to fulfil its guarantee relating to ERI’s profits. Therefore, Erin also has incentive to reduce the income of ERI.

Bank:• Would want the consolidated SCI of EBBI to truly reflect its earnings, cash flows, and

ability to service debt including paying interest on the debt and repaying the debt.

Ranking of Users & Objectives:• Clearly, the most common objective is for the consolidated SCI to fairly reflect the

true operating results of EBBI. While Ada has both an income increasing as well as an income decreasing motive, achieving either has costs. Increasing the income too much might mean that EBBI will have to fulfil its guarantee to ERI when in reality it does not have to. Thereby, EBBI will unnecessarily loose cash in an attempt to get the loan. Of course, EBBI can increase income, but just enough to achieve a profit percentage that is slightly below the profit percentage of ERI. In contrast, Erin would like EBBI’s income to be as high as possible such that it is forced to fulfil its guarantee to ERI. On our part, satisfying Ada’s preferred goal will mean dissatisfying Erin and vice-versa. We have a fiduciary duty to both Ada and Erin. Further, the bank is a known user of the consolidated SCI of EBBI prepared by us. Thus, all in all it appears best for us to prepare a consolidated SCI that fairly reflects the true operating results of EBBI.

Copyright © 2014 Pearson Canada Inc. 155

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

Notwithstanding the previous discussion, IFRS does not offer much leeway in terms of the availability of different accounting alternatives for accounting for the investments in EBBCL and ERI respectively. However, bias may still be present in the separate entity financial statements of both EBBI and ERI, specifically to reduce the net incomes of both entities.

Discussion:1. The sum of the cost of goods sold and ending inventory amounts of EBBI exactly

matches the sales amount of EBBCL, indicating that the entire ending inventory of EBBI was purchased from EBBCL.

2. The beginning inventory of ERI:a. Does not include any unrealized profit from sales to ERI by EBBI since no

sales were made by EBBI to ERI prior to the current year. Therefore, unrealized profits in the beginning inventory of ERI if present would represent profits related to sales made by EBBCL in the prior year to EBBI.

b. However, the deemed sale/purchase rule applies when control over a subsidiary is lost. EBBI lost control of ERI last year when 80% of the shares owned it were sold to Erin. Therefore, all unrealized profits in the beginning inventory of ERI will have been deemed to have been realized by Dec. 31, 20X7.

c. Even if it assumed that unrealized profits still exist in the beginning inventory of ERI, following proprietary theory, which needs to be applied under IFRS while accounting for an investment in an associate, only 20% should be held back.

3. Ending inventory of ERI: While the facts provided do not allow the calculation of the proportion of the ending inventory of ERI purchased from EBBI, they nonetheless allow the calculation of the maximum unrealized amount under the assumption that all of the ending inventory of ERI was indeed purchased from EBBI. Alternatively, at the other extreme, it can also be assumed that the entire ending inventory of ERI was purchased from others and not from EBBI. The amount of unrealized profits that has to be held back will depend on the assumption made regarding the proportion of the ending inventory of ERI purchased from EBBI.

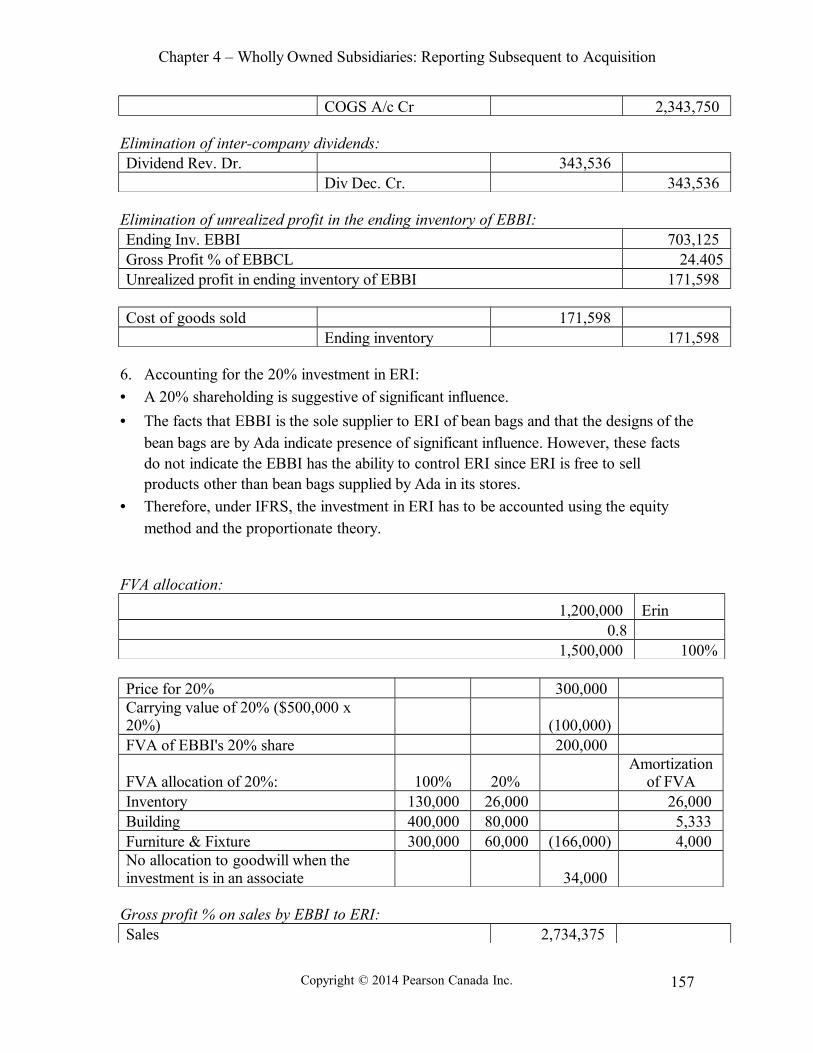

4. The gross profit percentage on the sales by EBBCL to EBBI is calculated below:

Gross Profit 571,992 Sales 2,343,750 24.405%

5. Consolidation-related adjustments and eliminations required in relation to consolidating EBBCL’s translated SCI with EBBI’s SCI:

Elimination of inter-company sales:Sales A/c Dr 2,343,750

Copyright © 2014 Pearson Canada Inc. 156

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

COGS A/c Cr 2,343,750

Elimination of inter-company dividends:Dividend Rev. Dr. 343,536

Div Dec. Cr. 343,536

Elimination of unrealized profit in the ending inventory of EBBI:Ending Inv. EBBI 703,125 Gross Profit % of EBBCL 24.405Unrealized profit in ending inventory of EBBI 171,598

Cost of goods sold 171,598 Ending inventory 171,598

6. Accounting for the 20% investment in ERI:

• A 20% shareholding is suggestive of significant influence.

• The facts that EBBI is the sole supplier to ERI of bean bags and that the designs of the bean bags are by Ada indicate presence of significant influence. However, these facts do not indicate the EBBI has the ability to control ERI since ERI is free to sell products other than bean bags supplied by Ada in its stores.

• Therefore, under IFRS, the investment in ERI has to be accounted using the equity method and the proportionate theory.

FVA allocation:

1,200,000 Erin0.8

1,500,000 100%

Price for 20% 300,000 Carrying value of 20% ($500,000 x 20%) (100,000)FVA of EBBI's 20% share 200,000

FVA allocation of 20%: 100% 20%Amortization

of FVAInventory 130,000 26,000 26,000 Building 400,000 80,000 5,333 Furniture & Fixture 300,000 60,000 (166,000) 4,000 No allocation to goodwill when the investment is in an associate 34,000

Gross profit % on sales by EBBI to ERI:Sales 2,734,375

Copyright © 2014 Pearson Canada Inc. 157

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

COGS 1,640,625 Gross Profit 1,093,750 40%

Calculation of unrealized gain in the ending inventory of ERI;20%

EI of ERI 136,719 Less unrealized gain in EI @ 40% (54,688) (10,938)Cost to EBBI 82,031 Unrealized gain on sales from EBBCL* (20,020) (4,004)

Since EBBCL, EBBI, and ERI are all related, the amount of the unrealized gains present in ERI’s ending inventory which should be eliminated includes not only EBBI’s profits but also EBBCL’s profits as well.

100% 20%SE income of ERI for 20X8 391,798 78,360 Less FVI amortization for the year (176,667) (35,333)Adjusted income of ERI for 20 X8 215,131 43,026 Share of EBBLess unrealized gain in EI on sale from EBBI (54,688) (10,938)Less unrealized gain in EI on sale from EBBCL (20,020) (4,004)Equity in the Earnings of ER 140,423 28,085

When there is loss of control a deemed sale/purchase is supposed to have occurred. Therefore, all unrealized profit in ending inventory @ 20X7 is assumed to be realized. Hence no unrealized gain is present in the beginning inventory of ERI.

If ending inventory of ERI is not assumed to be purchased from EBBI, $10,938 and $4,004 need to be added back, thus equity in the earnings will instead be $43,026.

Consolidated SCI for EBBI for 20X8 EBBI EBBCL Con. Adj. Con St.

Sales 2,734,375 2,343,75

0 (2,343,750

) 2,734,375

COGS 1,640,625 1,771,75

8 (2,343,750

) 171,598 1,240,231 Gross Profit 1,093,750 571,992 1,494,145 Salaries 240,625 164,063 404,688 Rent 235,726 235,726 Amortization building 337,500 337,500 Amortization furniture & fixtures 225,000 115,000 340,000 Overheads 142,188 98,438 240,625 Dividend Income from EBBCL 343,536 (343,536) 0

Copyright © 2014 Pearson Canada Inc. 158

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

Equity in the Earnings of ER 28,085 28,085 Exchange loss on NMA 68,814 68,814

Net Income before Taxes 491,974 (110,048) (315,452)(171,598) (105,123)

Income Taxes 93,729 83,320 177,049 Net Income after Taxes 398,245 (193,368) (282,172)

7. Calculation of comparative profit percentages:

EBBI Consolidated SCINet income before taxes (105,123)Sales 2,734,375Profit percentage -3.84%

EBBI Separate Entity SCINet income before taxes 491,974 Sales 2,734,375 Profit percentage 17.992%

ERI SCINet income before taxes 602,765 Sales 3,996,394 Profit percentage 15.083%

EBBI Consolidated, removing unrealized and forex lossAdjusted net income 135,289 Sales 2,734,375Profit percentage 4.95%

8. Accuracy of Erin’s assertions and reasons for difference:As the above analysis clearly shows, Erin is not correct in assuming that the profit percentage will be the same if based on the consolidated SCI of EBBI as when it is based on the separate entity SCI of EBB. There are four major reasons why a difference exists between these two profit figures:

1) Loss on foreign currency translation of $68,8142) Elimination of inter-company dividends of $343,536, replaced instead by

($110,048) income before taxes. Further, only the inter-company transactions were eliminated but expenses of both entities, EBBCL and EBBI are retained. Thus, there are additional expenses on the consolidated SCI as compared to the separate entity SCI of EBBI, thereby reducing net income.

3) Further, the unrealized gain in ending inventory of EBBI purchased from EBBCL of $171,598 was eliminated while arriving at the consolidated SCI.

4) 20% of unadjusted income of ERI is $120,553, however 20% of adjusted income

Copyright © 2014 Pearson Canada Inc. 159

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

of ERI recognized as equity in the earnings of ERI by EBBI in its consolidated SCI is only $28,085. The separate entity SCI of EBBI does not include any portion of the results from the operations of ERI as the latter has not declared any dividends. Thus, the net income on the consolidated SCI of EBBI is no doubt higher as compared to the net income on EBBI’s separate entity SCI consequent to the inclusion of its share of the adjusted earnings of ERI of $28,085. Nonetheless, if no consolidation adjustments were made to EBBI’s share of the net income of ER, the increase in the consolidated income of EBBI would have been that much higher.

9. Better reflection of the true economics of EBBITo answer the question about which of the two statements of comprehensive income, separate entity or consolidated, is a better reflection of the real economic operations of Canada, we need to first define what the term “real economic operations of EBB” is. Ada and Erin need to be clear on whether such operations should include the impact of the operations of EBBCL. From the facts provided it appears that the operations of EBBCL are more or less determined by EBBI, thus EBBCL is nothing but the purchasing arm of EBBI. Therefore, it is safe to conclude that the operations of EBBI should include the impact of the operations of EBBCL. However, the question still remains whether such a reflection should be restricted to the dividends received from EBBCL as shown in the separate entity SCI of EBBI or to the net income of EBBCL as reflected in the Consolidated SCI of EBBI. Given the extent to which the operations of EBBCL are controlled by EBBI it would appear that the entire income of EBBCL should be reflected in the SCI of EBBI, not just the dividends declared by the former. On this count the consolidated SCI of EBBI provides a better reflection of the true economic operations of EBBI since intercompany transactions, and related unrealized gains are removed.

However, it can be argued that the loss on the foreign currency translation of $68,814 should be excluded since it is a reflection of the accounting exposure to foreign exchange changes and not the real economic exposure due to such changes. Specifically, Ada notes that the decrease in the value of Kas will be beneficial to EBBI. The loss of $68,814 does not reflect this assertion (assuming that the assertion is correct).

Also, note the impact the amortization of FVAs has on the portion of the adjusted income of ERI recognized in the consolidated SCI of EBB. Only $28,085, EBBI’s share of the adjusted net income of ERI is included in the consolidated SCI of EBB, whereas 20% of the unadjusted earnings would be $120,553. If ERI’s operations were still a part of EBBI, this excess amortization would have been absent, since amortization would have been based on the book values of the related assets. While no portion of ERI income is recognized in the cost basis separate entity SCI of EBBI, to reflect the true economic circumstance of EBB, such income should be included as done on its consolidated SCI.

Thus, the consolidated SCI of EBBI suitably adjusted for the previous two points (i.e. after adding back the loss on the foreign currency translation of $68,814 and fair value adjustment amortization on ERI’s assets) would provide a better reflection of the true economic operations of EBBI.

Copyright © 2014 Pearson Canada Inc. 160

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

10. What the bank will look for in the consolidated SCI of EBBI:The bank may want to see the overall income of EBBI available for servicing interest payments as well as its existing sources of income and reasons for expenses. While the SFP of EBBI would no doubt provide an idea of the assets owned by EBBI that can be used as collateral, the bank may not be interested in taking over those assets of EBBI in the event it defaults on its loan. Repossessing assets means the bank now has the headache of trying to sell them to recoup its money. A bank would much rather prefer a company to service and repay its debt in the normal course of its business.

While the separate entity SCP is good for looking at the collateral available to the bank, the consolidated SCI provides a better reflection of the true profits and cash flows of EBBI. It better represents the risk of the entire operations of EBBI. Further, the consolidated SCI is a better reflection of EBBI’s total operations since EBBCL is only an extension of EBBI. Additionally, the consolidated SCI also includes EBBI’s equity in the earnings of ERi, thereby providing a complete picture of EBBI’s total operations.

The consolidated SCI of EBBI shows a loss. Therefore, at first blush the operating performance of EBBI does not look positive. However, amortization expenses, which are noncash expenses, are a significant proportion of the expenses on the consolidated SCI. Therefore, even though its earnings are negative EBBI may still be able to service its debt since it looks as if it is cash flow is positive.

A huge portion of the loss is because of the negative foreign exchange loss on translation. Hopefully, the future operating results of EBBI will be better since as Ada states, consequent to the depreciation in the Kas, her costs are down. Ada should also point out to the bank that the FVA amortization also has a significant negative impact on EBBI’s share of the adjusted income of ER. These additional amortization expenses, which again are noncash, were absent in prior years when ER’s operations were part of EBBI.

Copyright © 2014 Pearson Canada Inc. 161

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

SOLUTIONS TO PROBLEMS

P4-11. Consolidation-related adjusting entries required in 20X5 and 20X6 relating to the sale

of Okavango to its 100% owned subsidiary Serengeti:

20X5Eliminate inter-company sale:Sales 10,000 Cost of goods sold 10,000

Eliminate unrealized profit:Cost of goods sold 2,000 Ending inventory 2,000

20X6Capture impact of prior-year consolidation entry:Beginning retained earnings 2,000 Beginning inventory 2,000

Recognize realization of profits in current year:Beginning inventory 2,000 Cost of goods sold 2,000

Alternatively, net entry required in 20X6:Beginning retained earnings 2,000 Cost of goods sold 2,000

2. The consolidation-related adjusting entries would be identical to those shown in relation to Part 1) above if instead the sale of inventory was upstream, i.e. from Serengeti to Okavango. This results ensures since Serengeti is a 100% owned subsidiary of Okavango, and, therefore, the full amount of the unrealized profit on the inter-company sale of inventory has to be eliminated and is attributable to the shareholders of Okavango. Thus, when the sale is between a parent and its wholly owned subsidiary, the direction of the sale, upstream or downstream, is irrelevant when making consolidation-related adjustments. In contrast, if the sale had been between Okavango and its non-wholly owned subsidiary, the direction of the sale, upstream or downstream does matter while making consolidation-related adjusting entries, an issue which is discussed in further detail in Chapter 5.

P4-2

Copyright © 2014 Pearson Canada Inc. 162

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

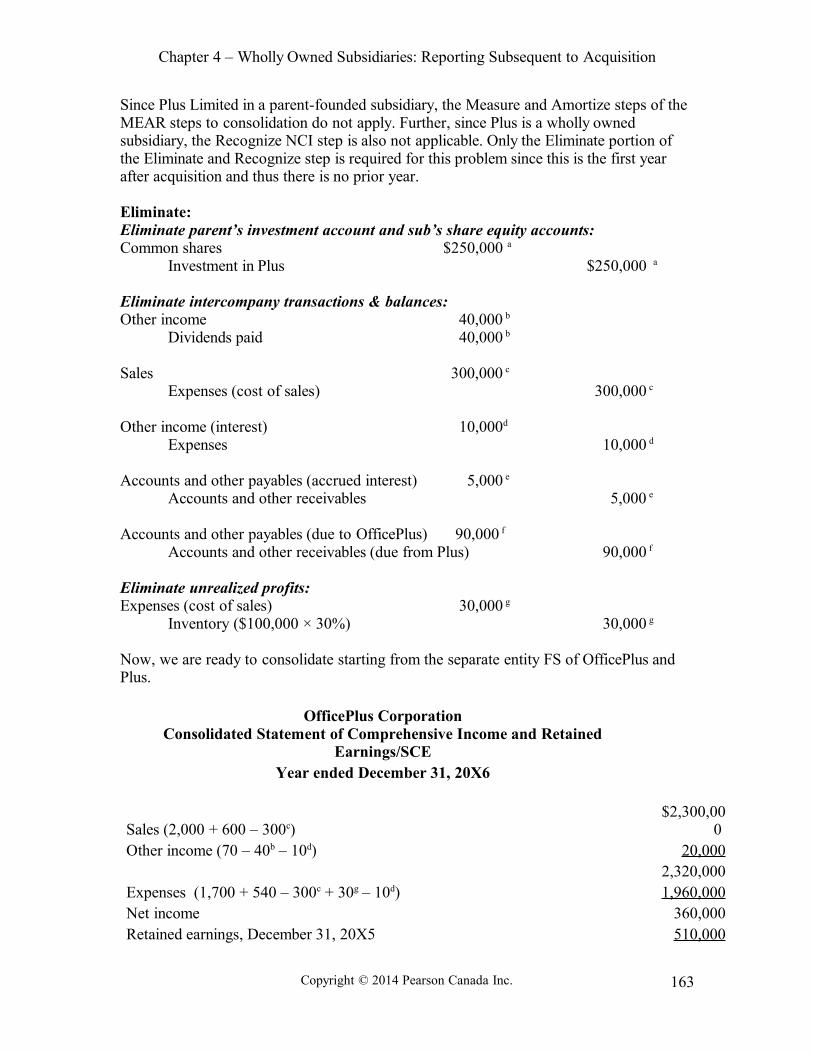

Since Plus Limited in a parent-founded subsidiary, the Measure and Amortize steps of the MEAR steps to consolidation do not apply. Further, since Plus is a wholly owned subsidiary, the Recognize NCI step is also not applicable. Only the Eliminate portion of the Eliminate and Recognize step is required for this problem since this is the first year after acquisition and thus there is no prior year.

Eliminate:Eliminate parent’s investment account and sub’s share equity accounts:Common shares $250,000 a

Investment in Plus $250,000 a

Eliminate intercompany transactions & balances:Other income 40,000 b

Dividends paid 40,000 b

Sales 300,000 c

Expenses (cost of sales) 300,000 c

Other income (interest) 10,000d

Expenses 10,000 d

Accounts and other payables (accrued interest) 5,000 e

Accounts and other receivables 5,000 e

Accounts and other payables (due to OfficePlus) 90,000 f

Accounts and other receivables (due from Plus) 90,000 f

Eliminate unrealized profits:Expenses (cost of sales) 30,000 g

Inventory ($100,000 × 30%) 30,000 g

Now, we are ready to consolidate starting from the separate entity FS of OfficePlus and Plus.

OfficePlus CorporationConsolidated Statement of Comprehensive Income and Retained

Earnings/SCEYear ended December 31, 20X6

Sales (2,000 + 600 – 300c)$2,300,00

0 Other income (70 – 40b – 10d) 20,000

2,320,000Expenses (1,700 + 540 – 300c + 30g – 10d) 1,960,000Net income 360,000Retained earnings, December 31, 20X5 510,000

Copyright © 2014 Pearson Canada Inc. 163

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

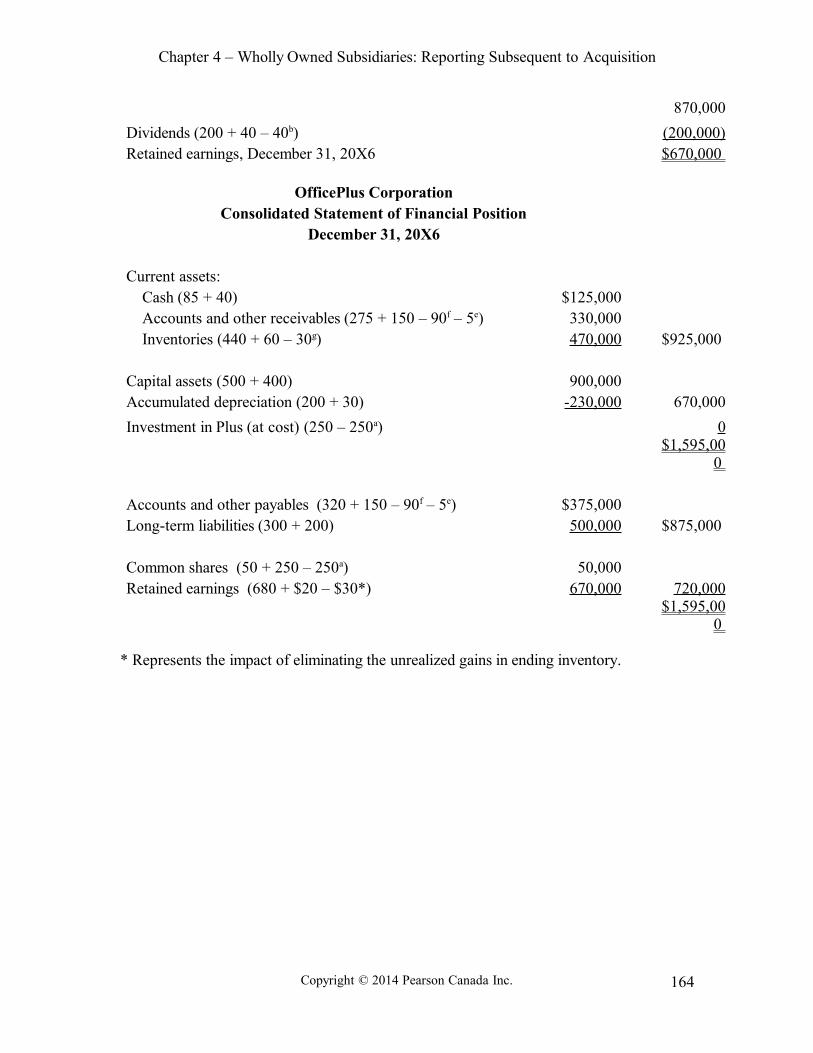

870,000

Dividends (200 + 40 – 40b) (200,000)Retained earnings, December 31, 20X6 $670,000

OfficePlus CorporationConsolidated Statement of Financial Position

December 31, 20X6

Current assets:Cash (85 + 40) $125,000 Accounts and other receivables (275 + 150 – 90f – 5e) 330,000Inventories (440 + 60 – 30g) 470,000 $925,000

Capital assets (500 + 400) 900,000Accumulated depreciation (200 + 30) -230,000 670,000

Investment in Plus (at cost) (250 – 250a) 0$1,595,00

0

Accounts and other payables (320 + 150 – 90f – 5e) $375,000 Long-term liabilities (300 + 200) 500,000 $875,000

Common shares (50 + 250 – 250a) 50,000Retained earnings (680 + $20 – $30*) 670,000 720,000

$1,595,000

* Represents the impact of eliminating the unrealized gains in ending inventory.

Copyright © 2014 Pearson Canada Inc. 164

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

P4-3

Since Plus Limited in a parent-founded subsidiary, the Measure and Amortize steps of the MEAR steps to consolidation do not apply. Further, since Plus is a wholly owned subsidiary, the Recognize NCI step is also not applicable. Since this the second year after the creation of Plus, both the Eliminate and Recognize portions of the Eliminate and Recognize step are required.

Eliminate:Eliminate parent’s investment account and sub’s share equity accounts:Common shares $ 250,000a

Investment in Plus $ 250,000a

Eliminate intercompany transactions & balances:Other income 45,000b

Dividends paid 45,000b

Sales 400,000c

Expenses (cost of sales) 400,000c

Sales 127,000d

Expenses (cost of sales) 127,000d

Other income (interest) 5,000e

Expenses 5,000e

Eliminate unrealized profits:Expenses (cost of sales) 40,000f

Inventory 40,000f

{Unrealized profit on downstream sales, [400× 25% × 40%]

Expenses (cost of sales) 27,000g

Inventory 27,000g

[Unrealized profit on upstream sales ($127,000 – $100,000)]

Other income 40,000h

Capital assets (land) 40,000h

Recognize realized profits:Beginning Retained Earnings 30,000i

Expenses (cost of sales) 30,000i

[To realize profit in beginning inventory]

OfficePlus CorporationConsolidated Statement of Comprehensive Income and Retained

Earnings/SCE

Copyright © 2014 Pearson Canada Inc. 165

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

Year ended December 31, 20X7

Sales (2,300 + 700 – 400c – 127d)$2,493,00

0

Other income (100 – 45b – 5e – 40h) 10,0002,503,000

Expenses (2,100 + 650 - 400c – 127d – 5e + 40f + 27g – 30i) 2,255,000 Net income 248,000

Retained earnings, December 31, 20X6 (680 + $20 – 30i) 670,000 918,000

Dividends (220 + 45 – 45b) (220,000)Retained earnings, December 31, 20X7 $698,000

OfficePlus CorporationConsolidated Statement of Financial Position

December 31, 20X7

Current assets:Cash (50 + 60) $110,000 Accounts and other receivables (210 + 60) 270,000

Inventories (440 + 195 – 40f – 27g) 568,000

948,000

Capital assets (560 + 520 – 40h) 1,040,000 Accumulated depreciation (230 + 60) (290,000)

750,000

Investment in Plus (at cost) (250 – 250a) 0 Other Investments (140 + 0) 140,000

$1,838,000

Accounts and other payables (360 + 250) $610,000 Long-term liabilities (250 + 230) 480,000

1,090,000

Common shares (50 + 250 – 250a) 50,000 Retained earnings* 698,000

748,000 $1,838,000

* $760,000 + $45,000 – $40,000 – $27000 – $40,000

Copyright © 2014 Pearson Canada Inc. 166

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

P4-4

Measure:

Consideration given: $15,000,000 Consideration received:NCV of assets, January 1, 20X6 $12,000,000 Fair value adjustments:

Buildings and equipment (1,800,000)Inventory 450,000 Investments 1,950,000 Goodwill (from prev. acquisition) (1,200,000) 11,400,000

Goodwill $3,600,000

Eliminate:

Eliminate inter-company balances and transactions

Investment in Small & owners' equity of Small($15,000,000

)Upstream sales (1,500,000)

Receivable/payable (600,000)Dividend declared by Small (600,000)

Eliminate unrealized gains and recognize realized gains

Unrealized gain in EI on upstream sale (750,000)

Amortize FVIs:

FVI Allocated

Amort. Period

Amort.Amort./

impairment loss during 20X6

Balance of FVI

remaining at the end of 20X6per year

Inventory $450,000 ($450,000) $0

Copyright © 2014 Pearson Canada Inc. 167

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

Buildings and equipment

(1,800,000) 10

(180,000) 180,000 (1,620,000)

Investments 1,950,000 (360,000) 1,590,000 Goodwill 3,600,000 3,600,000

Total $4,200,000 ($630,000) $498,400

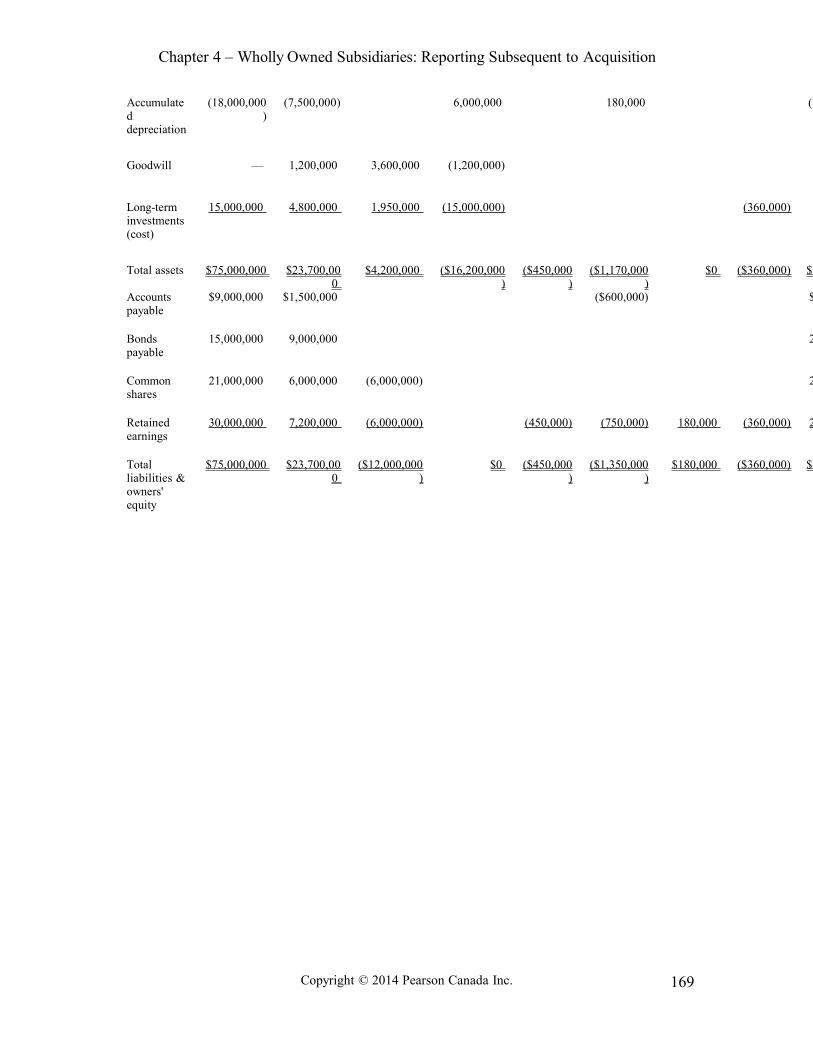

Big Inc.Consolidated Statement of Financial Position

December 31, 20X6

Current assets: Cash $ 3,900,000Accounts receivable 5,400,000Inventories 8,550,000 $ 17,850,000

Plant and equipment 76,200,000Accumulated depreciation (19,320,000 ) 56,880,000

Goodwill 3,600,000Long-term investments 6,390,000

$84,720,000

Liabilities: Accounts payable $ 9,900,000Bonds payable 24,000,000 $33,900,000

Shareholders’ equity: Common shares 21,000,000Retained earnings 29,820,000 50,820,000

$84,720,000

Statements of Financial Position December 31, 20X6

Big SmallAcquisition

Adj.Acquisition

Adj.Operatin

g Adj.Operating

Adj.Operating

Adj.Operating

Adj.Cash $3,000,000 $900,000

$3,900,000 Accounts receivable

4,800,000 1,200,000 (600,000)

Inventories 7,200,000 2,100,000 450,000 (450,000) (750,000)

Plant and equipment

63,000,000 21,000,000 (1,800,000) (6,000,000) 76,200,000

Copyright © 2014 Pearson Canada Inc. 168

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

Accumulated depreciation

(18,000,000)

(7,500,000) 6,000,000 180,000 (19,320,000

Goodwill — 1,200,000 3,600,000 (1,200,000)

Long-term investments (cost)

15,000,000 4,800,000 1,950,000 (15,000,000) (360,000)

Total assets $75,000,000 $23,700,000

$4,200,000 ($16,200,000)

($450,000)

($1,170,000)

$0 ($360,000) $84,720,000

Accounts payable

$9,000,000 $1,500,000 ($600,000) $9,900,000

Bonds payable

15,000,000 9,000,000 24,000,000

Common shares

21,000,000 6,000,000 (6,000,000) 21,000,000

Retained earnings

30,000,000 7,200,000 (6,000,000) (450,000) (750,000) 180,000 (360,000) 29,820,000

Total liabilities & owners' equity

$75,000,000 $23,700,000

($12,000,000)

$0 ($450,000)

($1,350,000)

$180,000 ($360,000) $84,720,000

Copyright © 2014 Pearson Canada Inc. 169

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

Supporting computations:

CostAccum. Depr.

Plant and equipment:Big $63,000,000 $18,000,000

Small, per books 21,000,000 7,500,000 Less accum. depr. at acquisition (6,000,000) (6,000,000)

Less FV decrement at December 31, 20X6 (1,800,000) (180,000)

$76,200,000 $19,320,000

Long-term investments: Small, per books $4,800,000

FVI at acquisition 1,950,000

Less FVI on investment sold (360,000)

$6,390,000

Retained earnings:

Big $30,000,000 Small per books 7,200,000 Less Small balance at acquisition (6,000,000)Fair value increments charged to income:

Investment sold (360,000)

FVI on beginning inventory (450,000)Amortization of FVD on buildings and equipment 180,000

Unrealized profit in ending inventory (750,000)$29,820,000

Copyright © 2014 Pearson Canada Inc. 170

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

Notes:

1. The intercompany inventory at the date of acquisition needs no adjustment, since the companies were not related at the time of the intercompany sale; it was assumed to be an arm’s-length transaction.

2. No adjustment is required for the intercompany dividend. The inclusion of the dividend in Big’s retained earnings is offset by an equal reduction in Small’s retained earnings.

Eliminations (not required):(based on information provided—statement of financial position only)

Acquisition adjustments:

Common shares 6,000,000

Retained earnings 6,000,000Inventory 450,000

Investments 1,950,000Goodwill 3,600,000

Goodwill 1,200,000

Plant and equipment 1,800,000

Investment 15,000,000

Accumulated depreciation 6,000,000

Plant and equipment 6,000,000

Operating adjustments:

Cost of sales 750,000

Inventory 750,000

[Unrealized profit on upstream sales, 1,500,000 × 50%]

Accounts payable 600,000

Copyright © 2014 Pearson Canada Inc. 171

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

Accounts receivable 600,000

Plant and equipment acc. Dep (1,800,000 ÷10) 180,000Amortization expense 180,000

Gain on sale of investment 360,000Investments 360,000

Cost of sales 450,000

Inventory 450,000

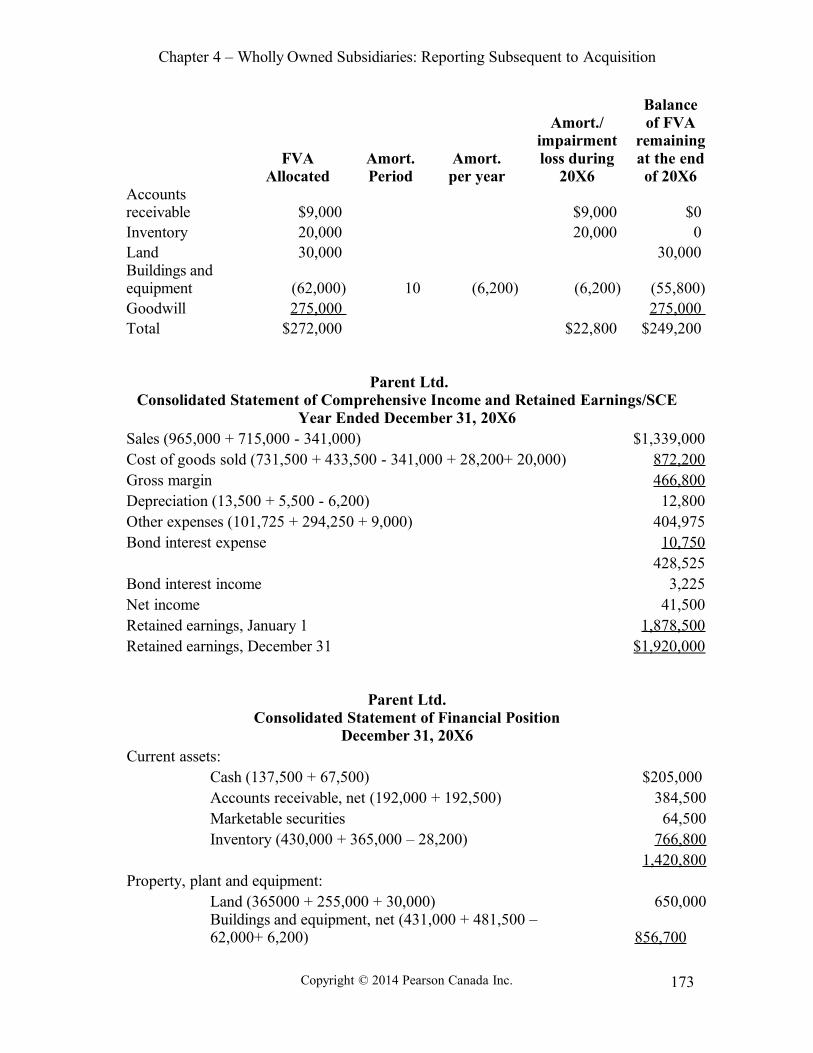

P4-5

Measure:Purchase price $1,400,000

Common shares $200,000 Retained earnings 983,000 Carrying value $1,183,000 Accounts receivable 9,000 Inventory 20,000 Land 30,000 Buildings and equipment (62,000)Goodwill (55,000)Fair value of net assets acquired 1,125,000Goodwill $275,000

Eliminate inter-company balances and transactions

Upstream sales (341,000)

Eliminate unrealized gains and recognize realized gains

Unrealized gain in EI on upstream sale (28,200)

Amortize FVAs:

Copyright © 2014 Pearson Canada Inc. 172

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

FVA Allocated

Amort. Period

Amort.per year

Amort./ impairment loss during

20X6

Balance of FVA

remaining at the end of 20X6

Accounts receivable $9,000 $9,000 $0 Inventory 20,000 20,000 0 Land 30,000 30,000 Buildings and equipment (62,000) 10 (6,200) (6,200) (55,800)Goodwill 275,000 275,000 Total $272,000 $22,800 $249,200

Parent Ltd.Consolidated Statement of Comprehensive Income and Retained Earnings/SCE

Year Ended December 31, 20X6Sales (965,000 + 715,000 - 341,000) $1,339,000Cost of goods sold (731,500 + 433,500 - 341,000 + 28,200+ 20,000) 872,200Gross margin 466,800Depreciation (13,500 + 5,500 - 6,200) 12,800Other expenses (101,725 + 294,250 + 9,000) 404,975Bond interest expense 10,750

428,525Bond interest income 3,225Net income 41,500Retained earnings, January 1 1,878,500Retained earnings, December 31 $1,920,000

Parent Ltd.Consolidated Statement of Financial Position

December 31, 20X6Current assets:

Cash (137,500 + 67,500) $205,000 Accounts receivable, net (192,000 + 192,500) 384,500Marketable securities 64,500Inventory (430,000 + 365,000 – 28,200) 766,800

1,420,800Property, plant and equipment:

Land (365000 + 255,000 + 30,000) 650,000Buildings and equipment, net (431,000 + 481,500 – 62,000+ 6,200) 856,700

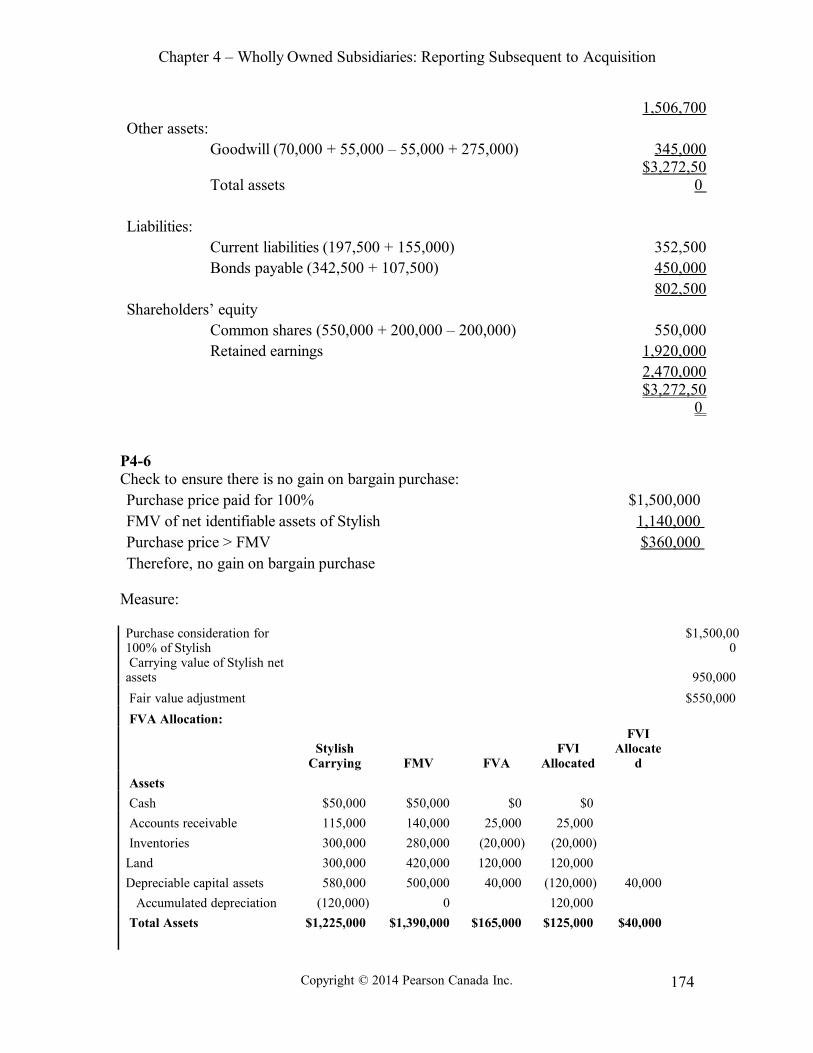

Copyright © 2014 Pearson Canada Inc. 173

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

1,506,700Other assets:

Goodwill (70,000 + 55,000 – 55,000 + 275,000) 345,000

Total assets$3,272,50

0

Liabilities:Current liabilities (197,500 + 155,000) 352,500Bonds payable (342,500 + 107,500) 450,000

802,500Shareholders’ equity

Common shares (550,000 + 200,000 – 200,000) 550,000Retained earnings 1,920,000

2,470,000$3,272,50

0

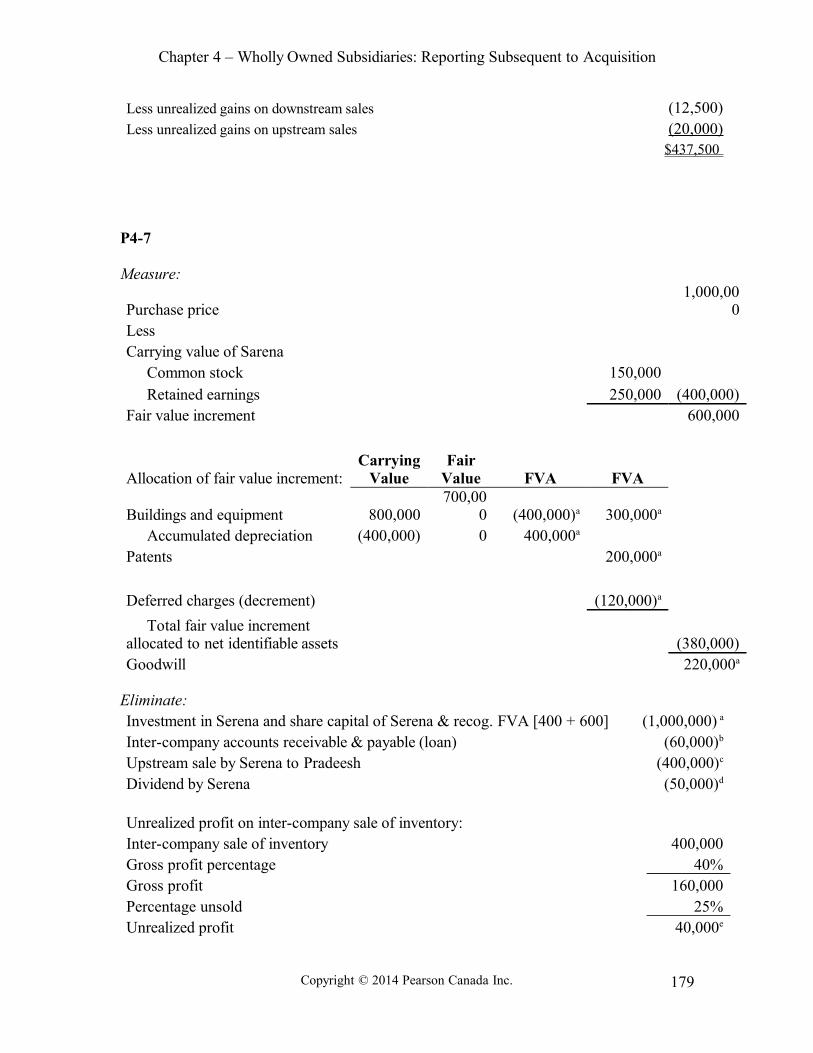

P4-6Check to ensure there is no gain on bargain purchase:Purchase price paid for 100% $1,500,000 FMV of net identifiable assets of Stylish 1,140,000 Purchase price > FMV $360,000 Therefore, no gain on bargain purchase

Measure:

Purchase consideration for 100% of Stylish

$1,500,000

Carrying value of Stylish net assets 950,000

Fair value adjustment $550,000

FVA Allocation:

Stylish

Carrying FMV FVAFVI

Allocated

FVI Allocate

d

Assets

Cash $50,000 $50,000 $0 $0

Accounts receivable 115,000 140,000 25,000 25,000

Inventories 300,000 280,000 (20,000) (20,000)

Land 300,000 420,000 120,000 120,000

Depreciable capital assets 580,000 500,000 40,000 (120,000) 40,000

Accumulated depreciation (120,000) 0 120,000

Total Assets $1,225,000 $1,390,000 $165,000 $125,000 $40,000

Copyright © 2014 Pearson Canada Inc. 174

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

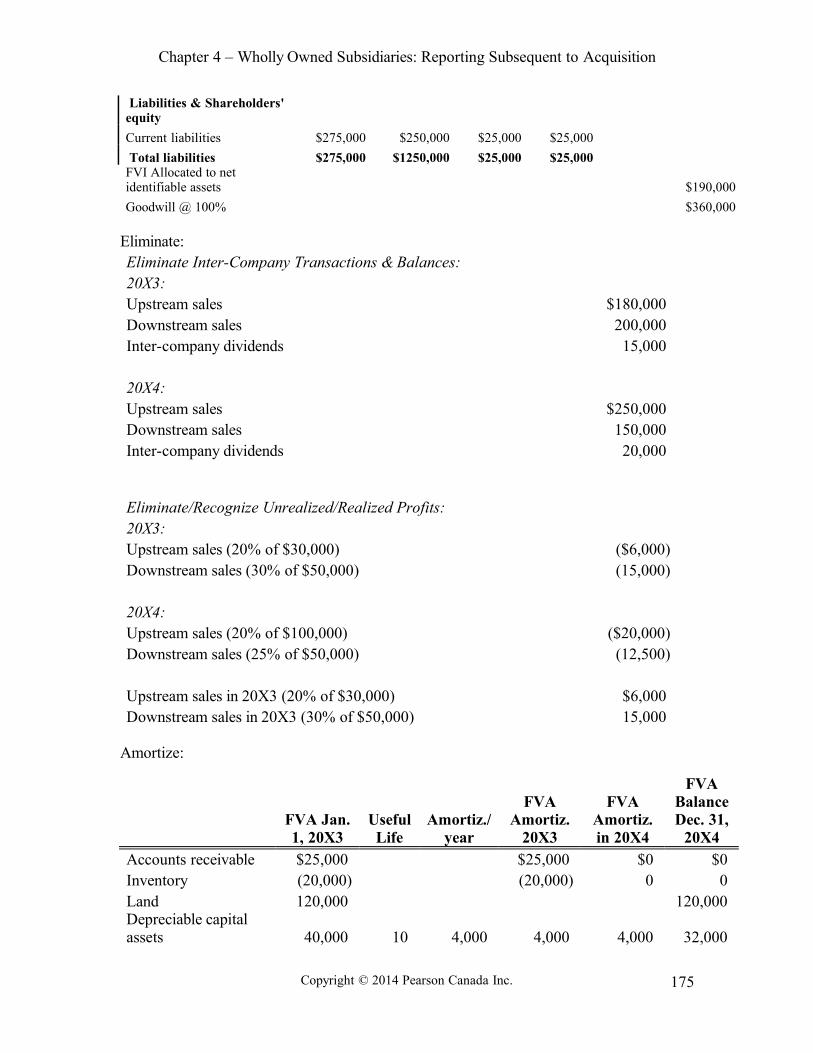

Liabilities & Shareholders' equity

Current liabilities $275,000 $250,000 $25,000 $25,000

Total liabilities $275,000 $1250,000 $25,000 $25,000 FVI Allocated to net identifiable assets $190,000

Goodwill @ 100% $360,000

Eliminate:Eliminate Inter-Company Transactions & Balances:20X3:Upstream sales $180,000 Downstream sales 200,000 Inter-company dividends 15,000

20X4:Upstream sales $250,000 Downstream sales 150,000 Inter-company dividends 20,000

Eliminate/Recognize Unrealized/Realized Profits:20X3:Upstream sales (20% of $30,000) ($6,000)Downstream sales (30% of $50,000) (15,000)

20X4:Upstream sales (20% of $100,000) ($20,000)Downstream sales (25% of $50,000) (12,500)

Upstream sales in 20X3 (20% of $30,000) $6,000 Downstream sales in 20X3 (30% of $50,000) 15,000

Amortize:

FVA Jan. 1, 20X3

Useful Life

Amortiz./ year

FVA Amortiz.

20X3

FVA Amortiz. in 20X4

FVA Balance Dec. 31,

20X4Accounts receivable $25,000 $25,000 $0 $0 Inventory (20,000) (20,000) 0 0 Land 120,000 120,000 Depreciable capital assets 40,000 10 4,000 4,000 4,000 32,000

Copyright © 2014 Pearson Canada Inc. 175

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

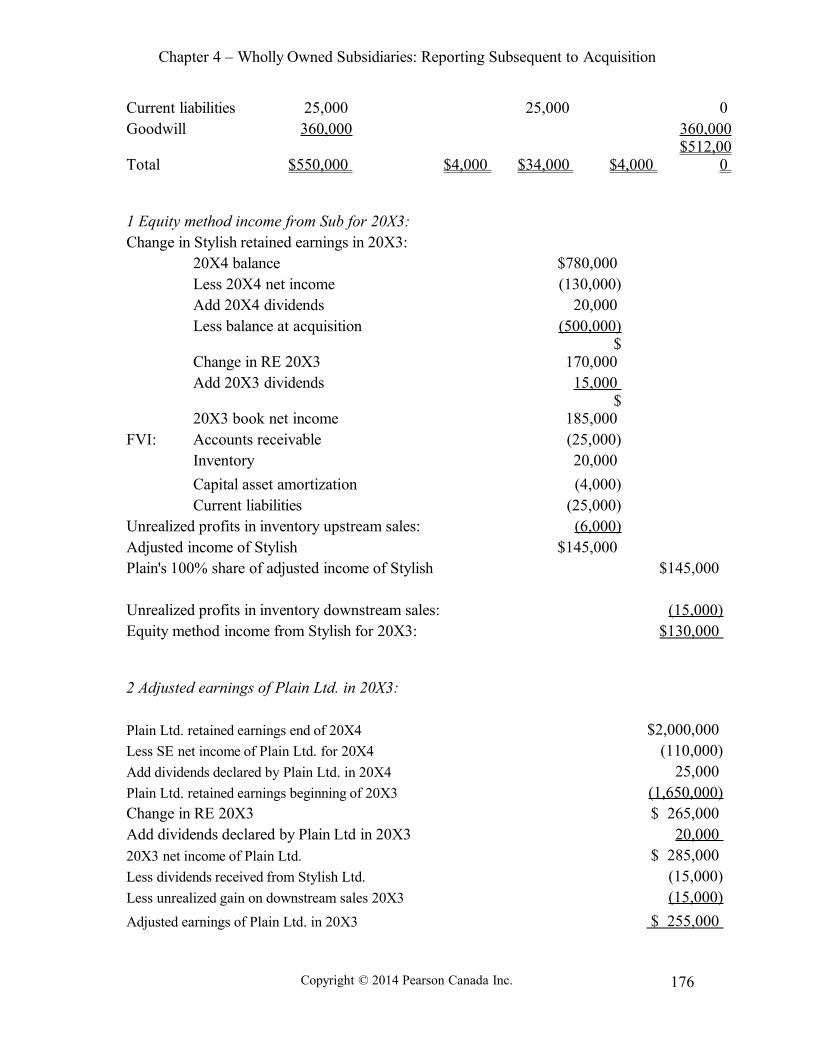

Current liabilities 25,000 25,000 0 Goodwill 360,000 360,000

Total $550,000 $4,000 $34,000 $4,000 $512,00

0

1 Equity method income from Sub for 20X3:Change in Stylish retained earnings in 20X3:

20X4 balance $780,000 Less 20X4 net income (130,000)Add 20X4 dividends 20,000 Less balance at acquisition (500,000)

Change in RE 20X3 $

170,000 Add 20X3 dividends 15,000

20X3 book net income $

185,000 FVI: Accounts receivable (25,000)

Inventory 20,000

Capital asset amortization (4,000)Current liabilities (25,000)

Unrealized profits in inventory upstream sales: (6,000)Adjusted income of Stylish $145,000 Plain's 100% share of adjusted income of Stylish $145,000

Unrealized profits in inventory downstream sales: (15,000)Equity method income from Stylish for 20X3: $130,000

2 Adjusted earnings of Plain Ltd. in 20X3:

Plain Ltd. retained earnings end of 20X4 $2,000,000 Less SE net income of Plain Ltd. for 20X4 (110,000)Add dividends declared by Plain Ltd. in 20X4 25,000 Plain Ltd. retained earnings beginning of 20X3 (1,650,000)Change in RE 20X3 $ 265,000 Add dividends declared by Plain Ltd in 20X3 20,000 20X3 net income of Plain Ltd. $ 285,000 Less dividends received from Stylish Ltd. (15,000)Less unrealized gain on downstream sales 20X3 (15,000)

Adjusted earnings of Plain Ltd. in 20X3 $ 255,000

Copyright © 2014 Pearson Canada Inc. 176

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

3 Consolidated net income for 20X4:Plain Ltd. net income $110,000 Unrealized profits, end of year downstream sales: (12,500)Unrealized profits, beg. of year downstream sales: 15,000Dividends revenue from Stylish (20,000)Adjusted income of Plain 92,500

Stylish Ltd. net income $130,000 Unrealized profits, end of year upstream (20,000)Unrealized profits, beg. of year upstream: 6,000Amortizations:

Capital asset FVI (4,000)Adjusted income of Stylish 112,000Consolidated net income for 20X4 $204,500

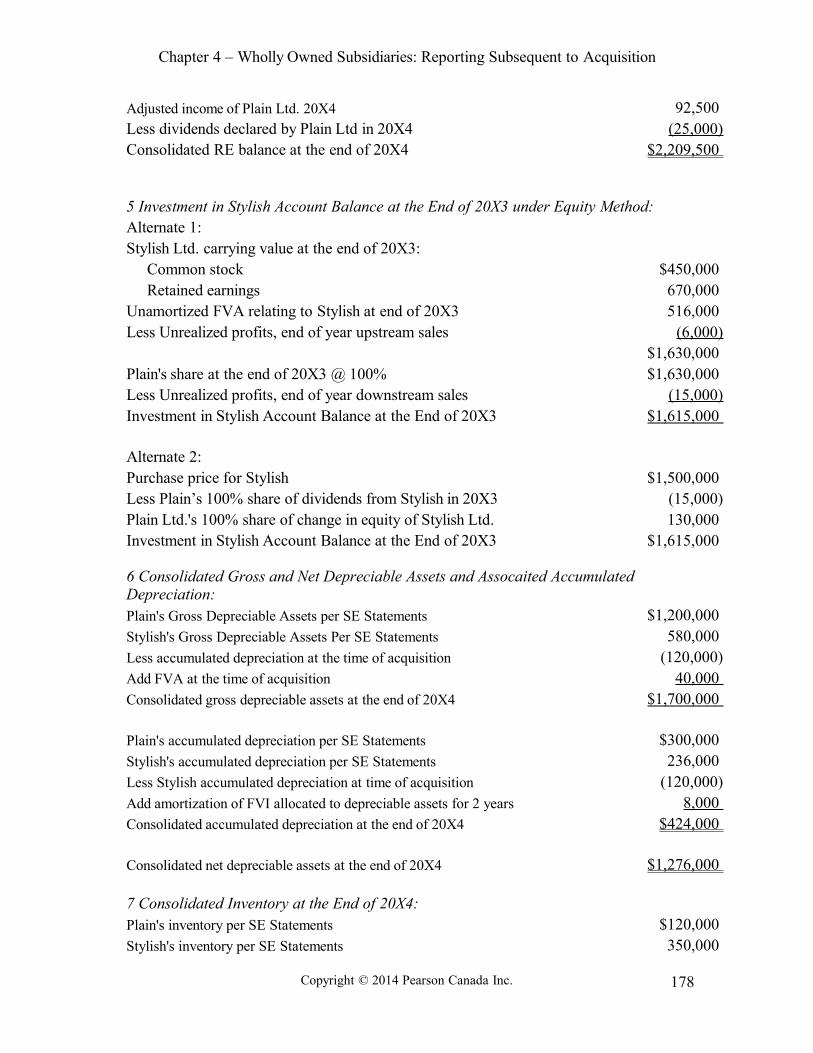

4 Consolidated RE balance at the end of 20X4:Alternate 1:Separate entity RE of Plain Ltd. end of 20X4 $2,000,000 Less Unrealized profits, end of year downstream sales (12,500)Separate entity RE of Stylish Ltd. end of 20X4 $780,000 Separate entity RE of Stylish Ltd. at the time of its acquisition (500,000)Change in RE of Stylish Ltd. from its acquistion to end of 20X4 $280,000 Less FVA amortization:Accounts receivable (25,000)Inventory 20,000 Capital asset amortization ($4,000 x 2) = (8,000)Current liabilities (25,000)Less Unrealized profits, end of year upstream sales (20,000)Adjusted Change in RE of Stylish Ltd. $222,000 Plain Ltd.'s 100% share of adj. change in RE of Stylish Ltd. 222,000 Consolidated RE balance at the end of 20X4 $2,209,500

4 Consolidated RE balance at the end of 20X4:Alternate 2:

Retained earnings balance of Plain Ltd. 20X3 Beg. $1,650,000 Plain's 100% share of adjusted income of Stylish 145,000 Adjusted earnings of Plain Ltd. in 20X3 255,000 Less dividends declared by Plain Ltd in 20X3 (20,000)Consolidated RE balance at the beginning of 20X4 $2,030,000 Plain Ltd.'s 100% share of adjusted inc. of Stylish 20X4 112,000

Copyright © 2014 Pearson Canada Inc. 177

Chapter 4 – Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition

Adjusted income of Plain Ltd. 20X4 92,500 Less dividends declared by Plain Ltd in 20X4 (25,000)Consolidated RE balance at the end of 20X4 $2,209,500

5 Investment in Stylish Account Balance at the End of 20X3 under Equity Method:Alternate 1:Stylish Ltd. carrying value at the end of 20X3: Common stock $450,000 Retained earnings 670,000 Unamortized FVA relating to Stylish at end of 20X3 516,000 Less Unrealized profits, end of year upstream sales (6,000)

$1,630,000 Plain's share at the end of 20X3 @ 100% $1,630,000 Less Unrealized profits, end of year downstream sales (15,000)Investment in Stylish Account Balance at the End of 20X3 $1,615,000

Alternate 2:Purchase price for Stylish $1,500,000 Less Plain’s 100% share of dividends from Stylish in 20X3 (15,000)Plain Ltd.'s 100% share of change in equity of Stylish Ltd. 130,000 Investment in Stylish Account Balance at the End of 20X3 $1,615,000