ch05 beechy ism

TRANSCRIPT

CHAPTER 5

Consolidation of Non-Wholly Owned Subsidiaries

The function of this chapter is to extend the discussion in the previous two chapters to subsidiaries that are acquired in a business combination but where a non-controlling interest continues to be held by outside parties. The discussion of non-controlling or minority interest has purposely been delayed to this point in the text in order to try to prevent students from becoming confused between alternative approaches to consolidation on the one hand and alternative approaches to reporting non-controlling interest on the other. This chapter begins with a discussion of why a parent corporation may own less than 100% of a subsidiary’s shares. The chapter then introduces alternative methods for consolidating non-wholly owned subsidiaries, including a conceptual discussion of the alternatives.

The chapter then presents consolidations using the current IFRS approach recommended in IFRS 3 and IFRS 10. The chapter illustrates consolidation at the date of acquisition and in the two subsequent years using the MEAR steps to consolidation, and is parallel to the consolidations illustrated in Chapters 3 and 4 for wholly owned subsidiaries. The same example is used in both Chapters 4 and 5 so that students can compare the results and see the impact of a non-controlling interest on the consolidated statements.

The existence of a non-controlling interest raises the issue of how to report this interest on the consolidated statement of financial position of the majority shareholder, and this is the focus of the last part of the chapter.

Chapter 5 has two appendices that focus on the effect of changes in ownership interest by the investor corporation. Appendix 5A discusses the impact of an increase in ownership interest and then, using an example, the approach. Appendix 5B identifies and discusses circumstances which may result in a decrease in or loss of an investor’s ownership interest and the accounting for this decrease or loss, with an example. In this document, solutions for review questions and problems in the appendices are included after the solutions to the problems in the main part of the chapter.

Copyright © 2014 Pearson Canada Inc. 212

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Copyright © 2014 Pearson Canada Inc. 213

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

SUMMARY OF ASSIGNMENT MATERIAL

Case 5-1: Metro Utility Workers’ UnionThis case requires students to play the role of an accounting advisor to a labor union that is planning for impending wage negotiations with the employer, a public limited company. The advisor is provided with preliminary cost basis financial statements of the employer and is required to appropriately account for its 40% ownership of another company. The advisor is required to analyze the provided financial statements and the statements prepared by him/her and advice the union on the true financial situation of the employer and the appropriate stance to adopt during the wage negotiation. The advisor is also required to elaborate on the different motivating factors and objectives which might drive the employer while preparing its financial statements to be issued to the public for the year.

Case 5-2: McIntosh Investments Ltd.This is a case that involves interrelationships between two significantly influenced investee corporations. This case includes a purchase price allocation for an equity investment and raises the issue of how to treat unrealized profits between the two significantly influenced entities.

Case 5-3: Simpson Ltd.In this case, students must decide what fair values must be assigned to the buildings acquired as part of a business combination; two different appraised values are given. The selection of fair values should be consistent with the parent’s reporting objectives. Students are asked to determine the impact of the business combination on the parent’s SFP, but a consolidated statement is not required.

Case 5-4: Proctor IndustriesThe student is placed in a unique role of having to report to the audit committee on significant accounting issues. One of these issues involves a business combination and the allocation of negative goodwill. If desired, the required could be altered to ask for accounting and auditing issues to provide a case that integrates more than one syllabus area.

P5-1 (25 minutes, easy)This problem presents six independent cases and requires students to calculate for each case the 1) gain from bargain purchase, if present, 2) net fair value adjustment, 3) fair value adjustment allocated to net identifiable assets, and 4) goodwill.P5-2 (25 minutes, easy)In this problem students are required to provide the balance in the investment account at the end of the first year in relation to a 20% shareholding in another company assuming the investment is classified as 1) a FVTPL investment, 2) an investment in an associate, and 3) a FVTOCI investment. The problem also requires students to calculate the total

Copyright © 2014 Pearson Canada Inc. 214

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

income reported in net income and OCI, including the gain on the sale of the entire investment, by the investor in year 3 assuming that the investment is classified as above.

P5-3 (50 minutes, medium) This problem illustrates (1) the difference between a purchase of assets and a purchase of 75% of the shares, and (2) the different approaches to consolidation when a non-controlling interest exists.

P5-4 (15 minutes, easy) Calculation of the consolidated balances of land, goodwill and non-controlling interest immediately after purchase of 70% of a subsidiary. There is negative goodwill on the combination that must be allocated.

P5-5 (15 minutes, easy) Preparation of a simple consolidated statement of financial position at date of acquisition of 70% interest, under both entity and parent-company extension methods.

P5-6 (25 minutes, easy) Calculation of selected balances on a consolidated statement of financial position immediately following acquisition of 70% ownership and an explanation of what non-controlling interest represents.

P5-7 (20 minutes, medium)This problem is a simple illustration of consolidating indirect holdings (i.e., a subsidiary of a subsidiary) by focusing on a single item: Non-controlling interest in the parent’s statement of financial position.

P5-8 (25 minutes, easy) Prepare eliminating entries for consolidation of a 70%-owned subsidiary one year after acquisition. The problem focuses on the amortization of FVIs and goodwill.

P5-9 (40 minutes, medium)In this problem a consolidated statement of comprehensive income and selected statement of financial position amounts are required at the end of the first year after acquisition. It includes upstream and downstream inventory sales and an upstream sale of land.

P5-10 (75 minutes, medium)A consolidated statement of comprehensive income and selected statement of financial position accounts are required for the second year after the acquisition of a 90% owned subsidiary.

P5-11 (85 minutes, difficult) A bargain purchase is present in the problem. Students are first required to prepare consolidated statements at the time of acquisition under the proportionate method for a 80% owned subsidiary. Next, students are required to calculate the consolidated retained

Copyright © 2014 Pearson Canada Inc. 215

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

earnings and the non-controlling interests balance two years after acquisition. Finally, students are required to calculate the adjusted incomes of the parent and the subsidiary respectively for the second year after acquisition.

P5-12 (90 minutes, difficult) This problem is the same as P4-6 except that the subsidiary is now 80% owned. The problem is set two years after acquisition; it requires computation of selected amounts, including consolidated earnings and equity basis earnings. It does not require consolidated statements.

P5-13 (30 minutes, medium)A consolidated statement of comprehensive income has been provided which needs to be corrected. There is an upstream unrealized profit on a capital asset sale and a downstream unrealized profit on inventory.

P5-14 (45 minutes, medium)An investment classified as a fair value through OCI investment in the first year becomes a significantly influenced investment in the second year. Associated entries and calculations are required in both years. This problem tests students’ grasp of concepts relating to FVTOCI and significantly influenced investments, and can be used as an exam question.

P5-15 (65 minutes, medium)Select SCI and SFP amounts, such as NCI interest in income, separate entity net income of the parent, NCI balance, investment account under the equity method are required to be calculated in relation to a 75% investment made two years ago. This problem tests students’ grasp of concepts relating to the reporting of an investment in a non-wholly owned subsidiary two years after such investment, and can be used as an exam question.

P5-16 (120 minutes, difficult)This problem is the same as P4-10 except that the subsidiary is now 80% owned. No consolidated financial statements are required in this problem. Nonetheless, this is a difficult problem since it requires the calculation of many consolidation and equity method related amounts relating to the first two years after acquisition.

P5-A1 (15 minutes, easy) This is an exercise in the reporting of an investment in common shares when there has been a two-step acquisition. Appropriate reporting under the cost, fair value, and equity methods is required.

P5-A2 (30 minutes, medium)The balance in the investment account is required using the equity method after an increase in share ownership.

P5-A3 (40 minutes, medium)

Copyright © 2014 Pearson Canada Inc. 216

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

The balances in the patent, goodwill and non-controlling interest accounts are required following a two-step purchase. Also required is the balance in the investment account using the equity method.

P5-B1 (20 minutes, medium)This problem is basically quite simple. What increases its level of difficulty is that at least half of the information presented in the problem is irrelevant, and students must be able to identify which information is relevant. Some students will get very frustrated!

P5-B2 (30 minutes, medium)The consolidated net income, gain/loss on sale of shares and consolidated retained earnings must be calculated two years after purchase. The question is complicated by a reduction in share ownership.

P5-B3 (30 minutes, medium)The balance in the investment account is required using the equity method after a decrease in share ownership. In addition, the required asks for the calculation of the gain/loss on the sale of the shares.

P5-B4 (30 minutes, medium)Three unrelated changes in subsidiary shares are described, (1) a stock split, (2) a new issue of subsidiary shares, and (3) a subsidiary’s retirement of its own shares. The first two are easy, but the third requires some thought, as it is not explicitly dealt with in the text.

ANSWERS TO REVIEW QUESTIONS

Q5-1:a. Non-controlling interest is the general term for shareholders that do not enable the shareholder to control the enterprise. Usually this will be less than 50% of the voting shares.

b. Non-controlling interest was formerly called minority interest. This term is no longer used in IFRS. Minority interest is a narrower definition of non-controlling interest where less than 50% of the voting shares of a subsidiary are owned by shareholders outside of the consolidated entity. Minority interest is the most common type of non-controlling interest.

c. When proportionate consolidation is used, a subsidiary’s assets, liabilities, revenues and expenses are combined with the parent’s only to the extent of the parent’s ownership interest. If only 60% is owned, then only 60% is included in the parent’s financial statements. This is one of the two alternatives currently allowed under IAS 31 to report joint ventures, the other being the equity method. However, under IFRS 11, the equity method is the only appropriate method available to report joint ventures.

Copyright © 2014 Pearson Canada Inc. 217

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

d. Under the parent-company method of consolidating financial statements, all of the subsidiary’s assets, liabilities, revenues and expenses are combined with those of the parent. However, to the extent that the assets and liabilities have fair values on the date of acquisition that differ from the subsidiary’s book values, only the parent’s proportionate share of those fair value increments or decrements is reported in the consolidated amounts.

e. Under the parent-company extension method of consolidating financial statements, the subsidiary’s identifiable assets and liabilities at fair values, and revenues and expenses are combined with those of the parent. However, goodwill is included only to the extent of the parent’s proportionate share. f. Under the entity method of consolidating financial statements, all of the subsidiary’s assets and liabilities, including goodwill, at fair values, and revenues and expenses are combined with those of the parent.

Q5-2: Less than full ownership enables the parent to obtain the benefits of control without having to invest the full amount of the subsidiary’s capital base. It may also allow the parent to spread the ownership risk, provide an avenue to develop links with other corporate shareholders and maintain a market for the subsidiary’s shares.

Q5-3: While the parent does not own 100% of the subsidiary’s shares, it can control the resources within the subsidiary. The consolidated statements are intended to portray substance over form or control over resources, not just ownership interest.

Q5-4: Recognition of less than 100% ownership is given by allocating to the non-controlling interest its proportionate share of the separate-entity earnings of the subsidiary, after making suitable consolidation related adjustments.

Q5-5: Under a “pure” application of the entity method, goodwill on the consolidated statement of financial position is “grossed up” to assign a value to the goodwill for non-controlling interest that is proportional to the value of the goodwill purchased by the controlling interest.

Q5-6: The parent-company extension approach modifies the entity approach by not allocating or assigning any value to goodwill for the non-controlling interest. The reasons are that (1) the controlling interest’s goodwill was actually paid for, while there has been no similar transaction to establish the value of goodwill for the non-controlling interest, and (2) the controlling interest’s goodwill can be ascribed to the value of gaining control, while there is no comparable benefit to the non-controlling shareholders and thus no implicit goodwill relating to the non-controlling interest.

Q5-7: The parent-company approach is a strict application of the historical cost basis of accounting. It shows a) the historical cost of the parent’s separate entity assets (book value), b) the historical cost to the parent of its share of the subsidiary’s assets (fair

Copyright © 2014 Pearson Canada Inc. 218

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

value) and c) the historical cost to the subsidiary of the net assets not purchased by the parent (book value).

Q5-8: Under the entity method, at the date of acquisition, non-controlling interest is measured at its proportionate share of the fair value of the acquired company’s net assets, including goodwill. In contrast, on the date of acquisition, the non-controlling interest is measured at its proportionate share of the fair value of the acquired company’s net assets, excluding goodwill, under the parent-company extension method.

Q5-9: One year after the date of acquisition, the non-controlling interest will consist of the proportionate share of the net fair value of the subsidiary’s net assets at the date of acquisition (using the entity method), plus the NCI share of the subsidiary’s net adjusted income less dividends for the year just ended, plus/minus the NCI’s proportionate share of the amortization of the FVI. The only difference under the parent-company extension method is that the NCI value on the SFP will disregard the value of its share of goodwill and any related impairment losses if any.

Q5-10: Any unrealized profit on upstream sales is removed from the consolidated earnings. Therefore, the amount allocated to the NCI as its share of the adjusted separate entity earnings of the subsidiary will also be reduced by the NCI’s share of the unrealized profit on the upstream sales.

Q5-11: Unrealized profits from downstream sales do not affect the NCI’s share of earnings because the profit is effectively being deducted from the parent’s earnings, not the subsidiary’s.

Q5-12: The non-controlling shareholders should not react at all because the reduction does not actually affect their equity in the subsidiary. The non-controlling shareholders will evaluate the subsidiary’s performance by using the financial statements of the subsidiary, not those of the parent. There is no impact on the subsidiary’s statements from eliminations made for consolidation purposes by the parent company.

Q5-13: Since unrealized profit in beginning inventories is normally realized during the ensuing year, the impact on the NCI is for its allocated share of the current year earnings to increase by the proportionate share of the previously unrealized profit on upstream sales.

Q5-14: The portion of dividends that is paid by the subsidiary to shareholders other than the parent represents a payment to the non-controlling interest and is deducted therefrom. Subsidiary dividends will not appear at all on the parent’s consolidated statement of retained earnings, although the dividends paid to non-controlling interests will appear on the consolidated cash flow statement as an outflow of cash from the consolidated entity.

Q5-15: Under both the parent-company method and the parent-company extension method, the subsidiary’s assets and liabilities are fully consolidated. However, under the parent-company method any discrepancies between carrying values and fair values of the

Copyright © 2014 Pearson Canada Inc. 219

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

individual assets and liabilities (FVIs) at the date of acquisition are included in the consolidated net assets only to the extent of the parent’s ownership share. Under the parent-company extension method, while the full extent of the FVIs, relating to the net identifiable assets at the date of acquisition, including the parent’s and the NCI’s share, are included in the consolidated statements, only the parent’s share of goodwill is included in the consolidated statements. Therefore, under both methods, the total consolidated amount will vary (due to the fair value increments and decrements) depending on the percentage share purchased by the parent.

CASE NOTES

Case 5-1 Metro Utility Workers’ Union (MUWU)

Role:MUWU is a not-for-profit workers’ union, whose members can be assumed to be moderately sophisticated users of accounting information. My task, as required by Ms. François Dubois, is to prepare the financial statements of MU that appropriately accounts for its investment in OU, and to advice the union on the financial status of MU such that they can obtain as good a wage settlement as possible. Before I do this I have to elaborate on the various users of MU’s financial statements and their objectives. Next, I will then detail the basis of my choice of accounting to account for MU’s investment in OU. Finally, I will explain the implications of the accounting choices made by MU and my choice on the financial situation of MU and its implications on MUWU’s aim to get the best wage settlement possible.

MU (Note that the question requires the following analysis only in relation to MU and not MUWA):

Critical Success Factors:Arriving at a wage settlement which favors MUWU or at best a fair wage settlement.

Constraints:MU as well as OU are public limited companies. Therefore, IFRS is a constraint. There do not appear to exist other constraints. Tax law is not assumed to be a constraint, since in all probability MU will maintain separate books to that extent.

Users & Objectives

InvestorsTheir shares are presumably traded widely on the TSX. Therefore, MU’s and OU’s investors are important users of MU’s and OU’s financial statements. Since they are retired these investors depend on the regular dividends paid by these companies for the cash flow needs. Therefore, their main objective in looking at the FS of these two

Copyright © 2014 Pearson Canada Inc. 220

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

companies would be cash flow prediction mainly, followed by performance evaluation and evaluation of the management of MU and OU respectively.In addition, MU will also be a user of OU’s FS since the former owns 40% of the latter. However, MU may also have access to other books of OU given its significant shareholding in the latter and representation on the BOD of the latter. At first glance, it appears that MU has significant influence on OU.

Top Management of MUThe top management of MU gets a bonus based on its net income. Thus, other things being equal, these individuals will be interested in maximizing net income to increase their bonuses. They also have the goal of stewardship reporting to their investors. To that extent they may want to portray as positive a picture as possible about their managerial ability. Further, they also know that MUWU will make use of the financial statements of MU during wage negotiations in 20X9. Therefore, to dissuade MUWU from adopting too aggressive a wage negotiation stance, the management of MU may be interested in portraying as negative a picture as possible about MU’s operations and financial situation. To the extent IFRS based FS are used for tax purposes, tax minimization will also be a goal. Since MU is an established company income smoothing can also be a reporting objective of MU’s management. Finally, minimum compliance does not appear to be an important goal of the management given the wide shareholding of MU’s shares. Thus, obviously, the goals of the top management of MU conflict with each other.

MUWUMUWU is an important user of MU’s FS. They would like to obtain as clear a picture as possible of MU’s true affairs so that they can bargain for a fair wage settlement. However, it is not necessarily the case that MU will view MUWU as an important user. Even if it does, MU may in fact try to conceal its true status as discussed above (i.e. portray a more negative picture of MU than existing) vis-à-vis MUWU to weaken the latter’s bargaining position.

OthersA bank loan may exist and to that extent the bank would be a user.

Ranking of Users and Objectives:Note that this ranking is being done from the viewpoint of MU. If MU’s management adopts aggressive accounting measures they benefit by obtaining higher bonuses. This may fool unsophisticated investors into thinking that MU is doing better than it actually is. Aggressive accounting will also benefit the union since it can ask for a better wage settlement. Thus, adopting aggressive accounting measures to boost short term profits may not be optimal in the long run. Investors may not like it if the management ends up making too many concessions to the union. Thus, management may make use of conservative accounting measures to portray a negative picture of MU; however, this will cost them in terms of reduced bonuses. Therefore, alternatively, they

Copyright © 2014 Pearson Canada Inc. 221

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

may try and take a big bath in 20X8 so that they can use these FS to enter into a wage settlement which favors MU, hoping to earn bigger bonuses in the future (they could also have increased 20X7 profits at the cost of 20X8 profits). Finally, instead of being overly aggressive or conservative they may decide that the best course is to provide as correct a picture of MU as possible, since this will be the best long term solution for all concerned. Given the CSF above, MU’s management will either be conservative or use the correct accounting choices. However, it is hard to decide which of these alternatives will be actually chosen by MU’s management. Therefore, I will keep the above discussion in mind while offering my advice. MUWU should also remember this point at the time of actual wage negotiation.

MU’s investment in OU [see Exhibit 1 for the FS]:MU owns 40% of OU. It has also been buying 70% of OU’s output. Finally, MU controls one of the eight BOD of OU. Under IFRS this strongly suggests the presence of significant influence. However, it would be very difficult to conclude that control exists based on these facts. While 70% of OU’s sales are to MU, this by itself does not suggest the existence of control. Further, the availability of new markets means that OU will be free to sell to others in North America. Further, since MU owns only 40% of OU, and also given that it controls only one of the eight BOD of OU, MU appears incapable of controlling OU without the cooperation of the other shareholders of OU. Therefore, it is safe to assume that MU has significant influence over OU. Under IFRS public companies should account for their significantly influenced investments using the equity method. This means that MU will include its portion of OU’s accumulated and current year’s earnings on its FS. Its portion of OU’s current year earnings will be included as equity in the earning s of OU on its IS. MU’s investment in OU will be valued at the original purchase consideration plus MU’s portion of OU’s adjusted unremitted earnings. If current year’s dividends have been accounted for as income, such income has to be eliminated. Finally, MU’s retained earnings should also be adjusted for its portion of OU’s adjusted unremitted earnings. Thus, in total, the equity method will mean adjustments to four accounts on MU’s FS: Equity in earnings of OU, dividend income from OU, investment in OU, and retained earnings. This is also known as a one-line consolidation, since MU’s investment in OU is shown on MU’s FS via a single account – investment in OU account. We call this a one line consolidation since we make all adjustments needed under regular consolidation which would affect the income statement and retained earnings of MU in a single account—equity in the earnings of the associate.

MU has in good faith provided MUWU with its separate entity financial statements wherein it has accounted for its investment in OU under the cost method. It is not clear why it provided you with these financial statements. This choice would make sense if OU is making a lot of profits, much of which is not being remitted via dividends; and the management of MU prefers to show relatively less income on its FS. In this scenario, under the cost basis the dividend income from OU recognized by MU would be much less than the amount it might have to recognize under the equity method. However the truth is the opposite. In 20X8, the unadjusted net income of OU is $11,200. In contrast, OU declared a dividend of $20,000. Further, when all required adjustments needed under the equity method are done, OU’s adjustment income actually becomes negative so much

Copyright © 2014 Pearson Canada Inc. 222

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

so that MU’s portion of the OU’s income is ($2,391). This is compounded by the negative unremitted retained earnings of OU. MU’s portion after all adjustments is a ($50,591). This suggests that MU may have overpaid for its investment in OU. It also appears that MU did indeed provide its cost basis FS to MUWU in good faith. In any case, the performance of OU appears to be irrelevant for MUWU’s objective of obtaining a fair wage settlement. MU’s workers should be paid on the operating performance of MU and not on the results of its investment activity, which in the present case is not very good. Therefore, MUWU would be better off during wage negotiations by using the separate entity FS provided by MU, in which its investment in OU is accounted for using the cost basis. Do understand though that the management of MU will point out that the $8,000 dividend income from OU should be eliminated while assessing the profitability of MU since it does not pertain to MU’s operation.

The information provided suggests that OU now will attempt to sell its output to other customers. This may mean that MU itself will have to pay more to get its raw materials. Therefore, in future the operations of MU may in fact deteriorate. Therefore, the results of 20X8 should not be used to extrapolate into the future to predict MU’s operating results in the future.

Financial Statements/Calculations:

Equity in earnings of OU: 40% share of unadjusted earnings $4,480 40% share of amortization of FVA allocated to capital assets (3,200)40% share of amortization of FVA allocated to patents (4,000)40% share of excess depreciation on capital asset sold upstream 1,600 40% share of realized profit on upstream sale of inventory in the previous year 3,911 40% share of unrealized profit on upstream sale of inventory sold in the current year remaining unsold at the end of the year (5,182)Equity in earnings of OU ($2,391)

Note: Since the loan to OshKosh has not being eliminated, the corresponding interest expense is also not being eliminated. This would offset the interest income shown on MU’s IS and therefore would be a wash anyway.

Share of adjusted change in retained earnings of OU in previous years 40% share of retained earnings 20X7 end $22,720 40% Share of retained earnings at acquisition 34,000 40% share of change in RE since acquisition (11,280)Less 40% share of amortization of FVA allocated to inventory (13,000)Less 40% share of amortization of FVA allocated to capital assets (6,400)Less 40% share of amortization of FVA allocated to patents (8,000)Less 40% share of unrealized gains on upstream sale of capital assets in previous year (8,000)Less 40% share of unrealized profit in beginning inventory (3,911)

Copyright © 2014 Pearson Canada Inc. 223

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Share of adjusted change in retained earnings of OU ($50,591)

Adjusting entry required to report under the equity method given recording is under the cost method:Dividends revenue 8,000 Retained earnings 50,591 Equity in earnings of OU 2,391 Investment in OU 60,982

Equity Basis Separate Entity Statement of Comprehensive Income of OshKosh Utility for 20X8

Revenues $800,000 Cost of goods sold 625,000 Gross profit 175,000Depreciation 50,000 Other expenses 45,000 Interest expense 50,000 Equity in earnings of OU 2,391 Net income before taxes 27,609 Taxes 11,400 Net income 16,209 Beginning retained earnings $137,809 Dividends 15,000 Ending retained earnings $139,018

AssetsCash $300,000 AR 225,000 Inventory 95,000 Loan to OshKosh 200,000 Capital assets 450,000 Investment in OshKosh Utility 119,018

TOTAL ASSETS$1,389,01

8 Liabilities and Owners’ EquityCurrent liabilities $400,000 Long-term liabilities 600,000 Shareholders' equity 250,000 Retained earnings 139,018

TOTAL LIABILITIES AND OWNERS’ EQUITY$1,389,01

8

Copyright © 2014 Pearson Canada Inc. 224

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Case 5-2: McIntosh Investments Ltd.

Objectives of the Case

This case incorporates the purchase of a 30% interest in a company that is a supplier of another investee subject to significant influence. There are a number of intercompany transactions between the two enterprises. Fair value increments and goodwill on the purchase must be determined.

Objectives of Financial Reporting

McIntosh Investments Ltd. (MIL) is a publicly traded investment company. Although 30% of the shares are publicly held, the remaining 70% are owned by the president and her brothers, giving virtually complete control of the company to Loraine McIntosh.

Compliance reporting will be an objective due to the public holdings of the shares and possibly due to the existence of at least some bank loans. Cash flow prediction could be an objective, but due to the nature of the company as essentially a personal holding company, such an objective is not likely. The tax status of an investment company, in terms of its taxable income, is fairly clear, and thus tax deferral is not likely to be an important objective except in controlling (or influencing) dividend flows from the investee companies.

Impact of EAPI on MIL Financial Statements

MIL clearly has significant influence, but not control, over the affairs of EAPI. The significant influence is demonstrated by MIL’s involvement in increasing EAPI’s efficiency and increased business with CCC. MIL does not control EAPI: it cannot control EAPI without the cooperation of others since its interest is only 30%. Therefore, equity reporting of the investment would be appropriate. The objectives of compliance with contracts and minimum disclosure may be the only really meaningful reporting objectives in this case, and would call for adherence to IFRS requirements. Using accounting standards for private enterprises is not an option since 30% of the shares of MIL are widely held. While the use of the equity method may be appropriate, it is not completely clear how it would be applied. Certainly a starting point for the equity pick-up of earnings would be 30% of EAPI’s reported net income of $300,000 or $90,000.

Adjustments to that figure will be necessary, however, for amortization of the fair value increment on the equipment, long-term investment, and debentures, disposition of the fair value increment on beginning inventory and perhaps unrealized profit. The

Copyright © 2014 Pearson Canada Inc. 225

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

amortization of the fair value increments on equipment and debentures is fairly straightforward, and depends on the remaining lives of these items and the depreciation and amortization methods being used. The fair value increment on the long-term investment will be adjusted when the investment is sold or there is an impairment. The fair value increment of the inventory at the date of acquisition will be charged to operations for fiscal 20X7. Therefore, MIL’s share of EAPI’s net income will decrease by 30% of $(40,000), or $12,000.

Another issue that students will have to evaluate is the treatment of unrealized profits. There are no transactions between MIL and EAPI; the transactions are between CCC and EAPI. CCC (Candide Cars Corporation) is another significantly-influenced affiliate of MIL; CCC is 40% owned by MIL. The question is whether profits generated by sales between significantly-influenced investee corporations should be eliminated if the items sold are still unsold to outside third parties or are unused. Since MIL was not a party to the transactions between EAPI and CCC, and since there is also no direct ownership link between EAPI and CCC, there is no clear obligation to eliminate unrealized profits, as long as the transactions that did occur can be viewed as arm’s-length transactions. If MIL has profit maximization as a reporting objective, then it would make sense to leave the profits in EAPI without adjustment.

A contrary view is that while there is no direct link between EAPI and CCC, the case makes it quite clear that MIL’s management is actively involved in both affiliates. The spectre of income manipulation arises because of the dramatic increase in inventories purchased by CCC from EAPI during the year. If unrealized profits are not eliminated, then MIL could bolster its earnings (as well as the earnings of EAPI) by “influencing” CCC to acquire excess inventory from EAPI. In view of the manipulative possibilities and the compliance reporting objective, elimination seems appropriate.

If the unrealized earnings are eliminated, then one must decide what percentage applies to MIL: the 30% interest in EAPI or the 40% interest in CCC. The answer is really quite straightforward, although it may not be obvious to the students. What is being eliminated is profit that MIL may report as its equity in an affiliate’s earnings. The unrealized profits in CCC’s ending inventory have been recorded as profits on the books of EAPI, and MIL picks up 30% of EAPI’s earnings; as a result, the elimination of unrealized profit would be 30% of the 35% gross profit on $300,000 inventory, or $31,500. The beginning inventory was acquired before MIL acquired its interest in EAPI. The unrealized profit in EAPI’s opening inventory therefore need not be given any consideration in the determination of MIL’s share of earnings in EAPI.

In summary, MIL’s equity in the earnings of EAPI can be determined as follows: 30% of EAPI earnings available to common shareholders $90,000Adjustments:

FVI – Beginning inventory (12,000)Unrealized profit (before income tax) (31,500)

Tax effect ($31,500 x EAPI’s tax rate) ?

Copyright © 2014 Pearson Canada Inc. 226

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Amortization of FVI on equipment ?Amortization of debenture FVI ?

MIL’s equity in the earnings of EAPI ???

The equity pick-up will be reported on MIL’s statement of comprehensive income and will increase the investment account on the statement of financial position. The dividend received by MIL will be treated as a distribution of MIL’s investment and, therefore, credited to the Investment in EAPI account, in the amount of: $1.50 x 18,000 shares = $27,000

Case 5-3: Simpson Ltd.

This is a business combination question. It contains a few variables, however, to see if candidates are able to apply their knowledge rather than simply replicate the textbook approach. Specifically, a decision is required on which value within a feasible range to assign to buildings; the decision will affect the amount of goodwill. The decision should relate to the owner’s stated objective of maximizing net income.

Allocating FVI when fair value of buildings is $8,400,000, no bargain purchase, goodwill present:

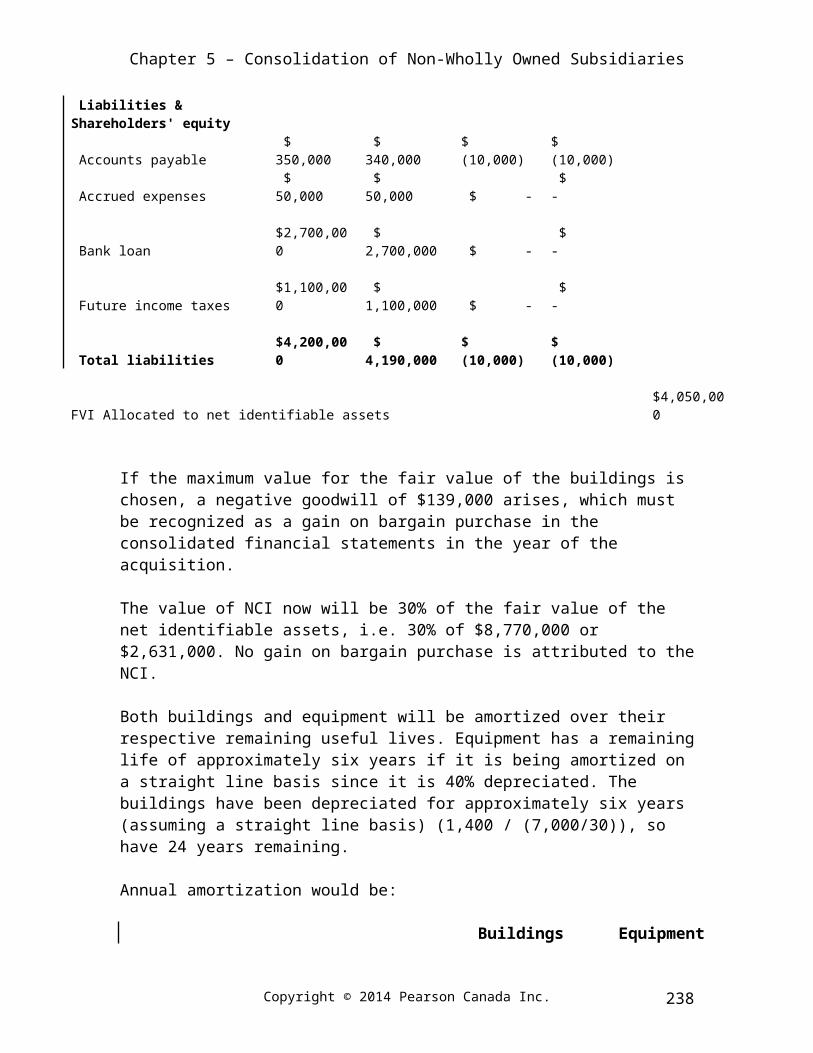

Purchase consideration $6,000,000 Grossed-up value of Ong based on purchase price $ 8,571,429 Carrying value of Ong net assets $ 4,700,000 Fair value increment $ 3,871,429 FVI Allocation: Ong Book FMV FVI FVI Allocated Assets Cash $ 200,000 $ 200,000 $ - $ - Accounts receivable $ 100,000 $ 100,000 $ - $ - Inventories -- raw materials and supplies $1,200,000 $ 1,180,000 $ (20,000) $ (20,000) Buildings $7,000,000 $ 8,400,000 $1,400,000 $ 1,400,000 Accumulated depreciation $(1,400,000) $ - $1,400,000 $ 1,400,000 Equipment $3,000,000 $ 1,980,000 $(1,020,000) $ (1,020,000) Accumulated depreciation $(1,200,000) $ - $1,200,000 $ 1,200,000 Total Assets $8,900,000 $11,860,000 $2,960,000 $ 2,960,000 Liabilities & Shareholders' equity Accounts payable $ 350,000 $ 340,000 $ (10,000) $ (10,000) Accrued expenses $ 50,000 $ 50,000 $ - $ - Bank loan payable $2,700,000 $ 2,700,000 $ - $ - Deferred income taxes $1,100,000 $ 1,100,000 $ - $ - Total liabilities $4,200,000 $ 4,190,000 $ (10,000) $ (10,000) FVI Allocated to net identifiable assets $ 2,970,000 Goodwill @ 100% $ 901,429

Copyright © 2014 Pearson Canada Inc. 227

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Therefore, the NCI value will be 30% × $8,571,429 = $2,571,429.

Allocating FVI when fair value of buildings is $9,500,000, gain on bargain purchase of $139,000 present:

Purchase consideration $6,000,000 Fair value of 70% of net identifiable assets: $6,139,000 Gain on bargain purchase $ 139,000 FVI Allocation: Ong Book FMV FVI FVI Allocated Assets Cash $ 200,000 $ 200,000 $ - $ - Accounts receivable $ 100,000 $ 100,000 $ - $ - Inventories -- raw materials and supplies $1,200,000 $ 1,180,000 $ (20,000) $ (20,000) Buildings $7,000,000 $ 9,500,000 $2,500,000 $ 2,500,000 Accumulated depreciation $(1,400,000) $ - $1,400,000 $ 1,400,000 Equipment $3,000,000 $ 1,980,000 ($1,020,000) $ (1,020,000) Accumulated depreciation $ (1,200,000) $ - $1,200,000 $ 1,200,000 Total Assets $8,900,000 $12,960,000 $4,060,000 $ 4,060,000 Liabilities & Shareholders' equity Accounts payable $ 350,000 $ 340,000 $ (10,000) $ (10,000) Accrued expenses $ 50,000 $ 50,000 $ - $ - Bank loan $2,700,000 $ 2,700,000 $ - $ - Future income taxes $1,100,000 $ 1,100,000 $ - $ - Total liabilities $4,200,000 $ 4,190,000 $ (10,000) $ (10,000) FVI Allocated to net identifiable assets $4,050,000

If the maximum value for the fair value of the buildings is chosen, a negative goodwill of $139,000 arises, which must be recognized as a gain on bargain purchase in the consolidated financial statements in the year of the acquisition.

The value of NCI now will be 30% of the fair value of the net identifiable assets, i.e. 30% of $8,770,000 or $2,631,000. No gain on bargain purchase is attributed to the NCI.

Both buildings and equipment will be amortized over their respective remaining useful lives. Equipment has a remaining life of approximately six years if it is being amortized on a straight line basis since it is 40% depreciated. The buildings have been depreciated for approximately six years (assuming a straight line basis) (1,400 / (7,000/30)), so have 24 years remaining.

Annual amortization would be:

Buildings Equipment Fair value $ 9,500,000 $ 1,980,000 Depreciation per year $ 395,833 $ 330,000

Copyright © 2014 Pearson Canada Inc. 228

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Fair value $ 8,400,000 Depreciation per year $ 350,000

If the lower value is chosen, there will be goodwill of $631,000, which is not amortized but tested for impairment on an annual basis. Assuming there is no impairment, the charge to the statement of comprehensive income will be less. Therefore, the objective of maximizing earnings will be achieved if the minimum fair value is assigned to the buildings and the remainder allocated to goodwill.

Simpson’s individual consolidated assets and liabilities would be increased by 100% of the fair value increments and decrements of Ong’s assets and liabilities (and by the goodwill, if any of the purchase price is allocated to goodwill). The offsetting changes would be to decrease cash by $1.5 million and increase long-term liabilities by $4.5 million, the purchase price of acquiring Ong. Specifically, the impact on Simpson’s statement of financial position would be as follows (assuming there is no allocation to goodwill):

Acquisition cost:Cash $1,500,000 cr.Secured debt 4,500,000 cr.

$6,000,000

The acquisition-related adjusting and eliminating entries (not required) will be as follows:

When FMV of buildings is $9,500,000

Common shares 1,000,000

Retained earnings 3,700,000

Buildings 2,500,000

Buildings -- accumulated depreciation 1,400,000

Equipment -- accumulated depreciation 1,200,000

Accounts payable 10,000

Inventories - raw materials and supplies 20,000

Equipment 1,020,000

Cash 1,500,000

Secured debt 4,500,000

Non-controlling interest 2,631,000

Copyright © 2014 Pearson Canada Inc. 229

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Gain on bargain purchase 139,000

Total 9,810,000 9,810,000

When FMV of buildings is $8,400,000

Common shares 1,000,000

Retained earnings 3,700,000

Buildings 1,400,000

Buildings – accumulated depreciation 1,400,000

Equipment – accumulated depreciation 1,200,000

Accounts payable 10,000

Goodwill 901,429

Inventories—raw materials and supplies 20,000

Equipment 1,020,000

Cash 1,500,000

Secured debt 4,500,000

Non-controlling interest 2,571,429

Total $ 9,611,429 $ 9,611,429

Therefore, regardless of whether or not there is a bargain purchase, the net identifiable assets of Ong are always included at their fair market values in the consolidated financial statements. Therefore, for each asset and liability line item, the impact of Ong’s assets and liabilities will be as follows, when the building FMV is $8,400,000:

Ong FMV Identifiable Assets Cash $ 200,000 Accounts receivable 100,000 Inventories -- raw materials and supplies 1,180,000 Buildings 8,400,000 Accumulated depreciation — Equipment 1,980,000 Accumulated depreciation — Total Identifiable Assets $11,860,000 Identifiable Liabilities Accounts payable $ 340,000 Accrued expenses 50,000 Bank loan 2,700,000 Future income taxes 1,100,000 Total Identifiable liabilities $ 4,190,000

Copyright © 2014 Pearson Canada Inc. 230

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Goodwill $ 901,429

The above will be matched by these other line-item changes on the consolidated financial statements: Non-controlling interest $ 2,571,429 Secured debt $ 4,500,000 Decrease in cash $ 1,500,000

When the building FMV is instead 9,500,000, the line-item changes will be as follows:

Ong. FMV Identifiable Assets Cash $ 200,000 Accounts receivable 100,000 Inventories -- raw materials and supplies 1,180,000 Buildings 9,500,000 Accumulated depreciation — Equipment 1,980,000 Accumulated depreciation — Total Identifiable Assets $12,960,000 Identifiable Liabilities Accounts payable $ 340,000 Accrued expenses 50,000 Bank loan 2,700,000 Future income taxes 1,100,000 Total liabilities $ 4,190,000

Matched by these other line-item changes on the consolidated financial statements:

Non-controlling interest $ 2,631,000 Secured debt $ 4,500,000 Decrease in cash $ 1,500,000Increase in retained earnings due to gain on bargain purchase $ 139,000

Case 5-4: Proctor Industries

Objectives of the Case

This case asks the students to consider accounting issues to report to the audit committee. The students will carefully have to think about their role and realize that even though audit terminology is being used and that they are the auditor of PI, they are asked to provide accounting advice. The issues involve accounting policies for investments and accounting for a business combination.

Objectives of Financial Reporting

Copyright © 2014 Pearson Canada Inc. 231

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

PI requires audited financial statements therefore IFRS is a constraint. PI is a large public company. Therefore, it is likely that compliance with securities legislation is an objective. With its recent acquisition of CI it is possible that it has some creditors that are interested in cash flow prediction.

Accounting Issues

Minor Inc.The results of MI will need to be consolidated with PI. PI has a 60% interest that indicates control. The non-controlling interest of 40% must be recorded on the SFP. PI will require a clean opinion on MI unless their operations are immaterial to PI. Therefore, the revenue recognition issue will need to be resolved. IFRS requires the use of uniform accounting policies for reporting similar transactions and other events in similar circumstances. Therefore, if an entity within a group uses accounting policies different from those adopted in the consolidated financial statements for similar transactions and events in similar circumstances, appropriate adjustments are required to be carried out during the consolidation procedure.

However, it is not necessary that the revenue recognition policy for PI and MI be the same. There may be valid reasons why there are different risks and rewards, e.g. different country, different products. Nevertheless, it appears that MI is being very aggressive with the revenue recognition policy being when goods are produced. Even though there may be a high demand there are potential risks until delivery, and uncertainty in prices. It would be easier if MI had the same policy as PI for consolidation. This issue must be resolved as soon as possible. If this cannot be resolved and it is material to PI’s operations, suitable adjustments to match up with PI’s revenue recognition policy will have to be made during the consolidation process. A $320,000 loss would be recorded in the consolidated financial statements. PI will not have to take a hit for the entire loss however: 40% of the loss will be attributed to the non-controlling interest.

Chemicals Inc.PI purchased 100% of CI’s common shares. Therefore, its results will be consolidated with PI using the acquisition method. The large discrepancy between the purchase price and the present net carrying value must be investigated and a reason documented. The allocation of this amount will have a large impact on the consolidated financial statements. Assuming that the SFP did not change significantly from the date of purchase two months ago and assuming the carrying values fairly approximate fair values the difference is:

Net carrying value $1,300,000Purchase price 100,000Negative goodwill $1,200,000

The negative goodwill of $1.2 million should be recognized as a gain on a bargain purchase. However, the chemical dumping could be the reason for the negative goodwill

Copyright © 2014 Pearson Canada Inc. 232

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

and some should be allocated to this contingent liability, thereby reducing the gain on the bargain purchase. In any case, the fair values of all the identifiable assets and liabilities have to be determined, and the full fair value decrement relating to such identifiable net assets have to be first allocated to be before determining the gain from bargain purchase.

The difference in year-end dates is a minor issue. PI may want to arrange for CI to change its year-end date to be consistent with that of PI to make it easier for consolidation. If not changed, following IAS 27, CI will have to prepare, for consolidation purposes, additional financial statements on the financial statements date of PI, unless preparation of such additional statements is not practical. Notwithstanding the previous, the difference of a month between the reporting dates of the two companies is within the three month maximum difference allowed under IFRS. If additional statements are not prepared by CI, adjustments have to be carried out during consolidation to remove the effects of significant transactions or events that occurred between CI’s reporting date and that of CI. Further, details regarding the different reporting date of CI and the reason for using a different date should be disclosed in the consolidated financial statements.

Legal LetterThe chemical dumping is a contingent liability. This letter needs to be followed up on. Contingent liabilities are not recognized under IAS 37. Rather, IAS 37 requires entities to disclose contingent liabilities, unless the possibility of an outflow of economic resources is remote. CI has denied these allegations, which do not appear to be determinable. However, it sold the company for $1.2 million less than the financial statements indicate it is worth.

Allowance for Doubtful AccountsOur assessment indicates that this allowance is understated. The amount and possible impact needs to be discussed with the audit committee. Our best estimate is that it should be at least $250,000. PI may not want to make an adjustment to this account. It may argue that it is just an estimate and it is a matter of judgment.

Buy-Back of CIA note must be included in PI’s financial statements disclosing the possible buy back provision for CI.

SOLUTIONS TO PROBLEMS

P5-1Fair value of percentage acquired $100 $64 $120 $96 $80 $80 Is there a gain from a bargain purchase? No No Yes Yes No NoAmount of gain from bargain purchase $20 $16 $0

Copyright © 2014 Pearson Canada Inc. 233

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Extrapolated fair value/fair value of net indefinable assets $120 $150 $120 $120 $100 $100 Carrying value of 100% of net identifiable assets 80 100 80 100 120 120Net fair value increment/(fair value decrement) $40 $50 $40 $20

($20)

($20)

Fair value adjustment allocation to net identifiable assets 20 (20) 40 20 (40) (20)Goodwill $20 $70 $0 $0 $20 $0

P5-21.a.

FV end of year 1: $22 × 25,000 shares = $550,000

b.Cost $500,000 Add Income:Year 1 $400,000 20% of Year 1 Income × 20% 80,000Less Dividends:Year 1 200,000 20% of Year 1 Dividends × 20% (40,000)Less share of amortization of FVA relating to Year 1:$50,000 x 20% = $10,000 (10,000)Balance in investment account end of Year 1: $530,000

c.

FV end of year 1: $22 × 25,000 shares = $550,000

2.a. Year 1 Year 2 Year 3Dividends $40,000 $16,000 $30,000 Unrealized gains 50,000 (25,000) 50,000 Total net income $90,000 ($9,000) $80,000

b. Year 1 Year 2 Year 3

Copyright © 2014 Pearson Canada Inc. 234

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Share of net income of Panther $80,000 ($20,000) $50,000 Less: Share of amortization of FVA (10,000) (10,000) (10,000)Share of adj. net income 70,000 (30,000) 40,000 Gain on sale of associate 81,000 Total share of net income of associate $70,000 ($30,000) $121,000

c. Year 1 Year 2 Year 3Dividends $40,000 $16,000 $30,000 Total net income 40,000 16,000 30,000 OCI: Unrealized & realized gains 50,000 (25,000) 50,000

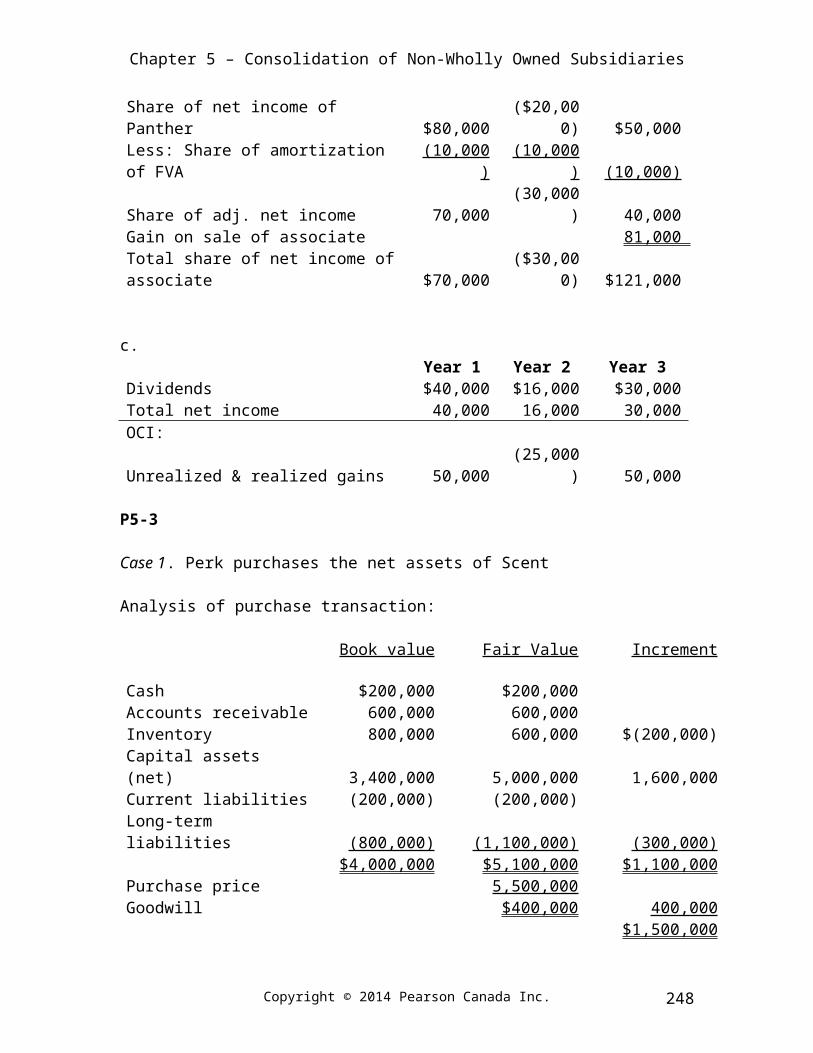

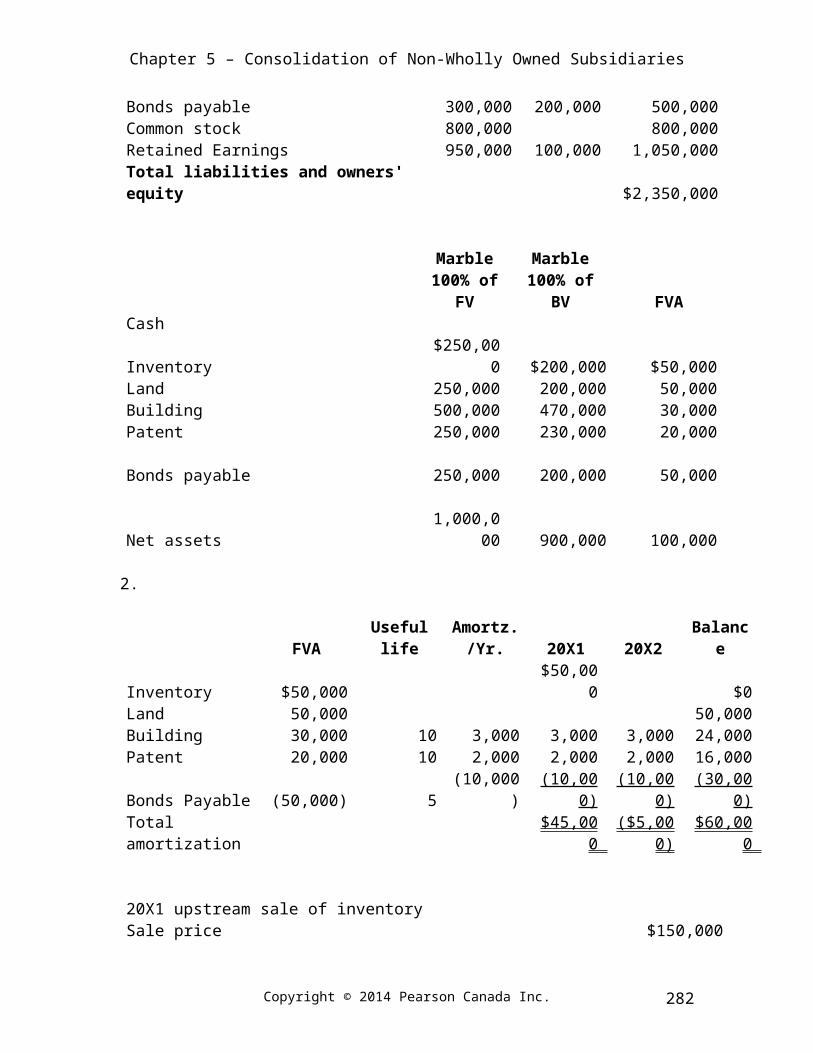

P5-3

Case 1. Perk purchases the net assets of Scent

Analysis of purchase transaction:

Book value Fair Value Increment

Cash $200,000 $200,000Accounts receivable 600,000 600,000Inventory 800,000 600,000 $(200,000)Capital assets (net) 3,400,000 5,000,000 1,600,000Current liabilities (200,000) (200,000)Long-term liabilities (800,000) (1,100,000) (300,000)

$4,000,000 $5,100,000 $1,100,000Purchase price 5,500,000Goodwill $400,000 400,000

$1,500,000

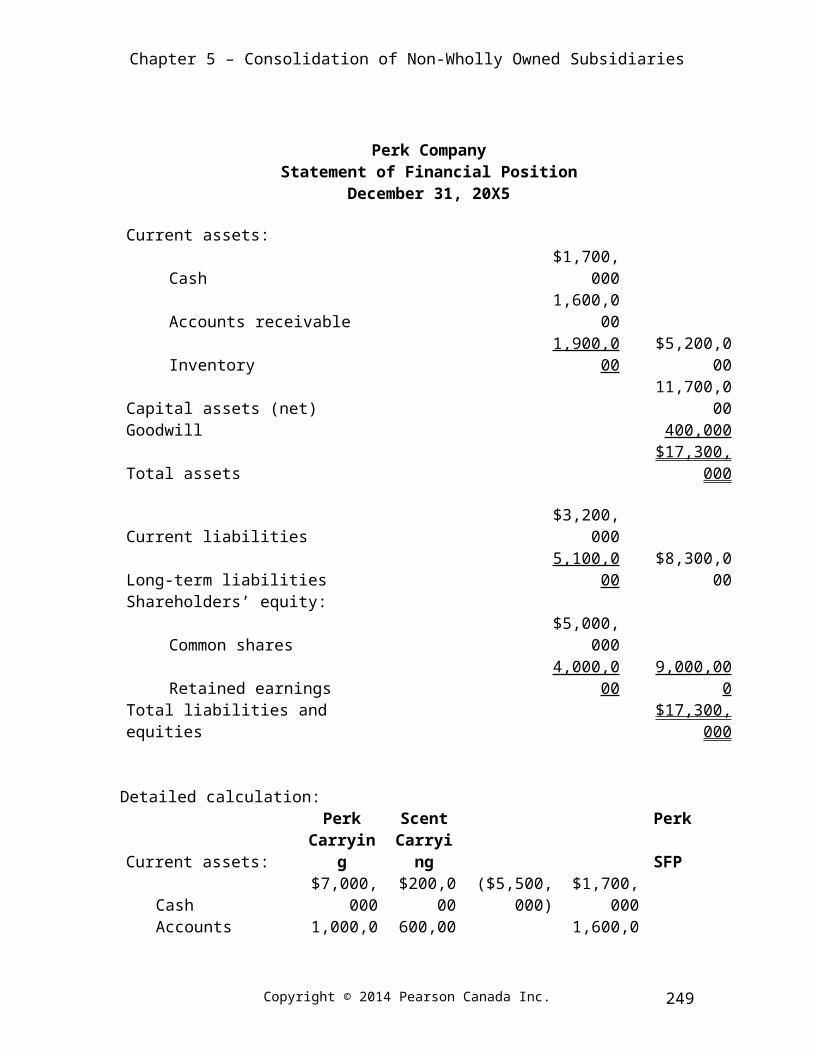

Perk CompanyStatement of Financial Position

December 31, 20X5

Current assets: Cash $1,700,000Accounts receivable 1,600,000Inventory 1,900,000 $5,200,000

Capital assets (net) 11,700,000Goodwill 400,000Total assets $17,300,00

Copyright © 2014 Pearson Canada Inc. 235

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

0

Current liabilities $3,200,000Long-term liabilities 5,100,000 $8,300,000Shareholders’ equity:

Common shares $5,000,000Retained earnings 4,000,000 9,000,000

Total liabilities and equities$17,300,00

0

Detailed calculation:Perk Scent Perk

Current assets: Carrying Carrying SFP

Cash$7,000,00

0 $200,000 ($5,500,000

)$1,700,00

0 Accounts receivable 1,000,000 600,000 1,600,000 Inventory 1,300,000 800,000 (200,000) 1,900,000 $5,200,000

Capital assets (net) 6,700,000 3,400,00

0 1,600,000 11,700,000 Goodwill 400,000

Total assets$17,300,00

0

Current liabilities$3,000,00

0 $200,000 $3,200,00

0 Long-term liabilities 4,000,000 800,000 300,000 5,100,000 $8,300,000 Shareholders’ equity:

Common shares 5,000,000 5,000,000 Retained earnings 4,000,000 4,000,000 9,000,000

Total liabilities and equities

$17,300,000

Case 2. Perk purchases 75% of Scent’s voting shares

Analysis of purchase transaction:

Book value Fair Value FVI Book value Fair Value FVI75% 75% 75% 100% 100% 100%

Cash $150,000 $150,000 $0 $200,000 $200,000 $0Accounts receivable 450,000 450,000 0 600,000 600,000 0Inventory 600,000 450,000 (150,000) 800,000 600,000 (200,000)Capital assets (net) 2,550,000 3,750,000 1,200,000 3,400,000 5,000,000 1,600,000Current liabilities (150,000) (150,000) 0 (200,000) (200,000) 0

Copyright © 2014 Pearson Canada Inc. 236

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Long-term liabilities (600,000) (825,000) (225,000) (800,000) (1,100,000) (300,000)$3,000,000 $3,825,000 $825,000 $4,000,000 $5,100,000 $1,100,000

Purchase Price for 75% $4,500,000Goodwill 75% $675,000Grossed-up value of 100% of Scent based on purchase price paid by Perk $6,000,000Goodwill 100% $900,000

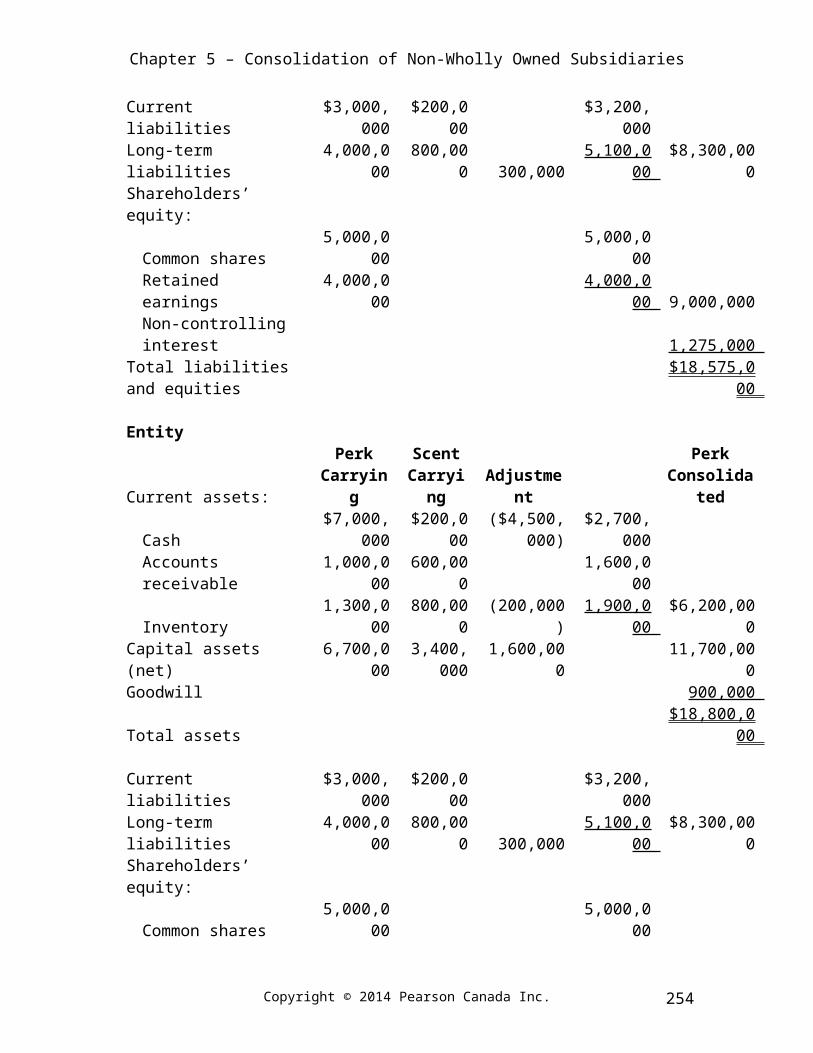

Perk CompanyConsolidated Statements of Financial Position

December 31, 20X5

1 2 3 4

Proportionateconsolid.

Parentcompany

Parent co.extension. Entity

Cash $2,650,000 $2,700,000 $2,700,000 $2,700,000Accts. receivable 1,450,000 1,600,000 1,600,000 1,600,000Inventory 1,750,000 1,950,000 1,900,000 1,900,000Capital assets (net) 10,450,000 11,300,000 11,700,000 11,700,000Goodwill 675,000 675,000 675,000 900,000Total assets $16,975,000 $18,225,000 $18,575,000 $18,800,000

Current liabilities $3,150,000 $3,200,000 $3,200,000 $3,200,000Long-term liability 4,825,000 5,025,000 5,100,000 5,100,000Common shares 5,000,000 5,000,000 5,000,000 5,000,000Non-controlling interest — 1,000,000 1,275,000 1,500,000Retained earnings 4,000,000 4,000,000 4,000,000 4,000,000Total liabilities and equities $16,975,000 $18,225,000 $18,575,000 $18,800,000

Detailed calculations:Proportionate Consolidation

Perk Scent Perk

Current assets: Carrying Carrying AdjustmentConsolidate

d

Cash $7,000,000 $150,000 ($4,500,000

)$2,650,00

0 Accounts receivable 1,000,000 450,000 1,450,000 Inventory 1,300,000 600,000 (150,000) 1,750,000 $5,850,000

Capital assets (net) 6,700,000 2,550,00

0 1,200,000 10,450,000

Copyright © 2014 Pearson Canada Inc. 237

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Goodwill 675,000 Total assets $16,975,000

Current liabilities $3,000,000 $150,000 $3,150,00

0 Long-term liabilities 4,000,000 600,000 225,000 4,825,000 $7,975,000 Shareholders’ equity:

Common shares 5,000,000 5,000,000 Retained earnings 4,000,000 4,000,000 9,000,000

Total liabilities and equities $16,975,000

Parent CompanyPerk Scent Perk

Current assets: Carrying Carrying AdjustmentConsolidate

d

Cash$7,000,00

0 $200,000 ($4,500,000

)$2,700,00

0 Accounts receivable 1,000,000 600,000 1,600,000 Inventory 1,300,000 800,000 (150,000) 1,950,000 $6,250,000

Capital assets (net) 6,700,000 3,400,00

0 1,200,000 11,300,000 Goodwill 675,000 Total assets $18,225,000

Current liabilities$3,000,00

0 $200,000 $3,200,00

0 Long-term liabilities 4,000,000 800,000 225,000 5,025,000 $8,225,000 Non-controlling interest 1,000,000 Shareholders’ equity:

Common shares 5,000,000 5,000,000 Retained earnings 4,000,000 4,000,000 9,000,000

Total liabilities and equities $18,225,000

Parent Company ExtensionPerk Scent Perk

Current assets: Carrying Carrying AdjustmentConsolidate

d

Cash$7,000,00

0 $200,000 ($4,500,000

)$2,700,00

0

Copyright © 2014 Pearson Canada Inc. 238

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Accounts receivable 1,000,000 600,000 1,600,000 Inventory 1,300,000 800,000 (200,000) 1,900,000 $6,200,000

Capital assets (net) 6,700,000 3,400,00

0 1,600,000 11,700,000 Goodwill 675,000 Total assets $18,575,000

Current liabilities$3,000,00

0 $200,000 $3,200,00

0 Long-term liabilities 4,000,000 800,000 300,000 5,100,000 $8,300,000 Shareholders’ equity:

Common shares 5,000,000 5,000,000 Retained earnings 4,000,000 4,000,000 9,000,000 Non-controlling interest 1,275,000

Total liabilities and equities $18,575,000

EntityPerk Scent Perk

Current assets: Carrying Carrying AdjustmentConsolidate

d

Cash$7,000,00

0 $200,000 ($4,500,000

)$2,700,00

0 Accounts receivable 1,000,000 600,000 1,600,000 Inventory 1,300,000 800,000 (200,000) 1,900,000 $6,200,000

Capital assets (net) 6,700,000 3,400,00

0 1,600,000 11,700,000 Goodwill 900,000 Total assets $18,800,000

Current liabilities$3,000,00

0 $200,000 $3,200,00

0 Long-term liabilities 4,000,000 800,000 300,000 5,100,000 $8,300,000 Shareholders’ equity:

Common shares 5,000,000 5,000,000 Retained earnings 4,000,000 4,000,000 9,000,000 Non-controlling interest 1,500,000

Total liabilities and equities $18,800,000

P5-4

Copyright © 2014 Pearson Canada Inc. 239

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Purchase Price $190,000Net carrying value of net assets (100,000 + 60,000 – 15,000) x 70%

101,500

FVA Land $150,000 Building 60,000 Equipment (30,000) Goodwill (20,000) Bonds Payable 10,000

$170,000 x 70% 119,000Negative Goodwill (30,500)Recognize as gain on bargain purchase

30,500

$ NIL

a. Land: 100% Carrying value

$ 30,000100% of FVI

150,000

$180,000

b. Goodwill: $ 0

c. Non-controlling interest: 30% of FV of Zoe’s net identifiable assets of $315,000 (carrying value of $145,000 plus FVI of $170,000)

$ 94,500

Note: The value of goodwill (of zero) and the NCI are the same under both the entity and the parent-company extension methods given that there is a gain on bargain purchase. Further, land is valued at its full fair value under both the entity and the parent-company extension methods and is thus same under both methods.

Copyright © 2014 Pearson Canada Inc. 240

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

P5-5

Analysis of purchase transaction:

Fair value of Lethbridge's net identifiable assets @ 100% $427,500Fair value of Lethbridge's net identifiable assets @ 70% 299,250Purchase price for 70% 315,000Goodwill @ 70% $15,750Therefore, there is no bargain purchaseGrossed-up value of Goodwill @ 100% $22,500Grossed-up value of 100% of Lethbridge based on purchase price of $315,000 for 70%

$450,000

Allocation of fair value adjustment:Carrying

value Fair ValueFVI

Adjustment

Current assets $210,000 $210,000 $0Land 135,000 225,000 90,000 Building, net 322,500 300,000 (22,500)Equipment, net 90,000 135,000 45,000 Current liabilities (105,000) (105,000) 0 Bonds payable (315,000) (337,500) (22,500)

$337,500 $427,500 $90,000Fair value of Lethbridge's 100% net identifiable assets

$427,500

Goodwill @ 100% under entity method $22,500Goodwill @ 70% under parent-company extension method $15,750

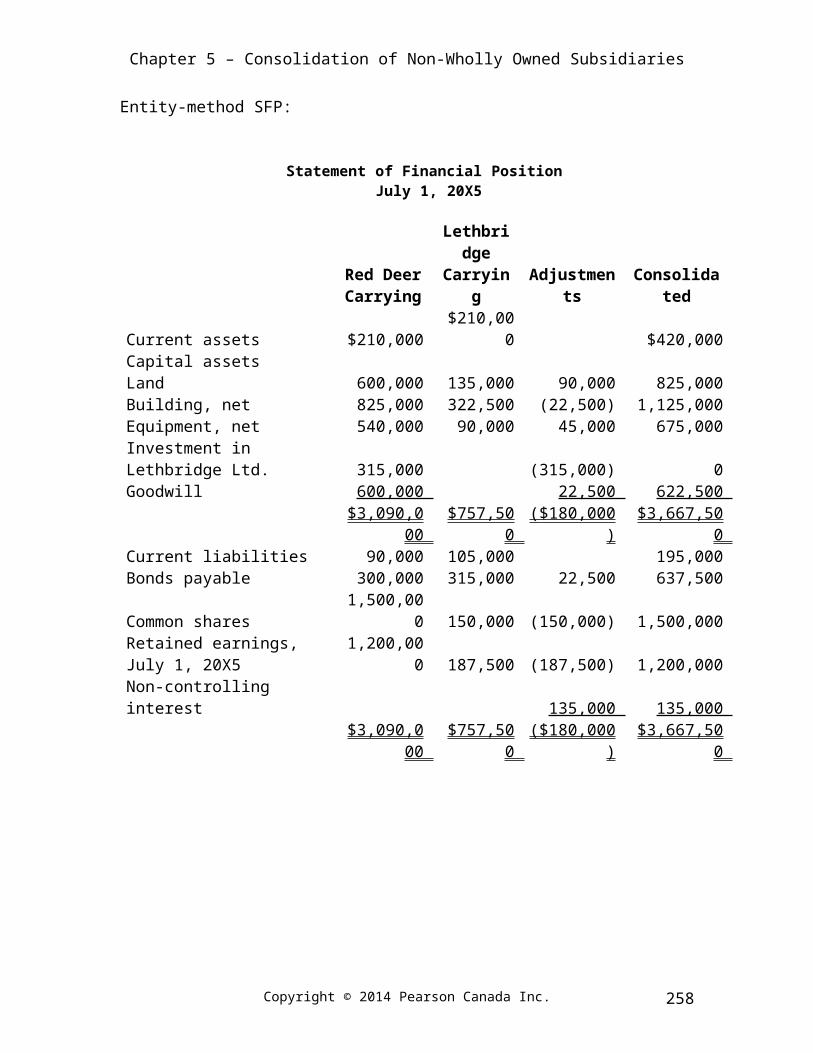

Entity-method SFP:

Statement of Financial Position July 1, 20X5

Red Deer Carrying

Lethbridge Carrying

Adjustments Consolidated

Current assets $210,000 $210,000 $420,000 Capital assetsLand 600,000 135,000 90,000 825,000 Building, net 825,000 322,500 (22,500) 1,125,000 Equipment, net 540,000 90,000 45,000 675,000 Investment in Lethbridge Ltd. 315,000 (315,000) 0 Goodwill 600,000 22,500 622,500

Copyright © 2014 Pearson Canada Inc. 241

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

$3,090,000 $757,500 ($180,000) $3,667,500 Current liabilities 90,000 105,000 195,000 Bonds payable 300,000 315,000 22,500 637,500 Common shares 1,500,000 150,000 (150,000) 1,500,000 Retained earnings, July 1, 20X5 1,200,000 187,500 (187,500) 1,200,000 Non-controlling interest 135,000 135,000

$3,090,000 $757,500 ($180,000) $3,667,500

Parent-company extension method SPF:

Statement of Financial Position July 1, 20X5

Red Deer Carrying

Lethbridge Carrying

Adjustments Consolidated

Current assets $210,000 $210,000 $420,000 Capital assets

Copyright © 2014 Pearson Canada Inc. 242

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Land 600,000 135,000 90,000 825,000 Building, net 825,000 322,500 (22,500) 1,125,000 Equipment, net 540,000 90,000 45,000 675,000 Investment in Lethbridge Ltd. 315,000 (315,000) 0 Goodwill 600,000 15,700 615,700

$3,090,000 $757,500 ($186,750) $3,660,750 Current liabilities 90,000 105,000 195,000 Bonds payable 300,000 315,000 22,500 637,500 Common shares 1,500,000 150,000 (150,000) 1,500,000 Retained earnings, July 1, 20X5 1,200,000 187,500 (187,500) 1,200,000 Non-controlling interest 128,250 128,250

$3,090,000 $757,500 ($186,750) $3,660,750

Copyright © 2014 Pearson Canada Inc. 243

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

P5-6

Measure:Maui Ltd.’s identifiable assets & liabilities at fair values:

Current assets $170,000 Current liabilities $130,000 Land 150,000 Bonds payable 140,000 Building (net) 360,000 Equipment (net) 60,000 Total $740,000 $270,000 Fair value of net identifiable assets $470,000

Fair value of 70% of net identifiable assets $329,000 Purchase Price paid by Oahu for its 70% 371,000 Goodwill @ 70% $42,000 Goodwill @ 100% $60,000 Grossed-up value of Maui Ltd. $530,000

1.

a. Goodwill (100%) $60,000 b. Land (100% FMV of Maui Ltd.) 150,000c. Equipment (100% FMV of Maui Ltd.) 60,000d. Common shares (of Oahu Ltd.) 960,000e. Retained earnings (of Oahu Ltd.) 1,420,000f. NCI @ 30% of $530,000 159,000

Copyright © 2014 Pearson Canada Inc. 244

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

2.

Oahu Ltd. includes in its consolidated statement of financial position all the net assets over which it has control, including 100% of Maui’s net assets. However, Oahu actually owns only 70% of Maui’s shares. Since all of the net assets are consolidated, these must be partially offset by a non-controlling interest that represents the outside owners’ 30% equity in the consolidated Maui net assets. The NCI does not represent a liability to Oahu or a part of Oahu’s ownership; it is an outside ownership interest in assets controlled by but not owned by Oahu Ltd.

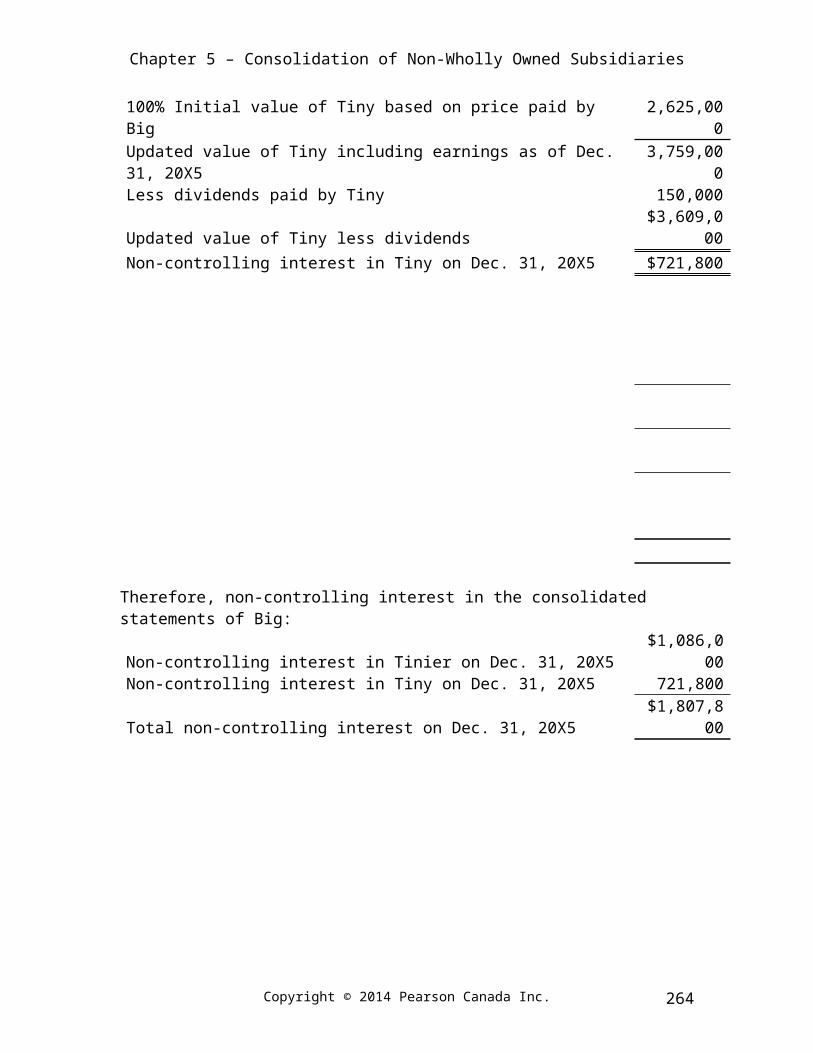

P5-7

Non-controlling interest on Huge’s consolidated statement of financial position will consist of two components:

1. 40% non-controlling interest in Tinier, plus2. 20% non-controlling interest in Tiny.

40% non-controlling interest in Tinier:Tinier

Purchase price $1,395,000 Grossed-up value based on price paid $2,325,000 Income less dividends during the year 390,000Total $2,715,000

Non-controlling interest in Tinier on Dec. 31, 20X5 $1,086,000

Copyright © 2014 Pearson Canada Inc. 245

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

20% non-controlling interest in Tiny:Tiny net income on cost basis $900,000 Less Tiny's portion of dividends from Tinier 36,000Tiny's separate entity earnings for the year 864,000Add share of income of Tinier 270,000Consolidated earnings attributable to shareholders of Tiny 1,134,000100% Initial value of Tiny based on price paid by Big 2,625,000Updated value of Tiny including earnings as of Dec. 31, 20X5 3,759,000Less dividends paid by Tiny 150,000Updated value of Tiny less dividends $3,609,000

Non-controlling interest in Tiny on Dec. 31, 20X5 $721,800

Therefore, non-controlling interest in the consolidated statements of Big:Non-controlling interest in Tinier on Dec. 31, 20X5 $1,086,000Non-controlling interest in Tiny on Dec. 31, 20X5 721,800Total non-controlling interest on Dec. 31, 20X5 $1,807,800

Copyright © 2014 Pearson Canada Inc. 246

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

P5-8

Measure:Purchase consideration $ 553,000 Grossed-up value of Sub based on purchase price $ 790,000 Carrying value of Sub net assets $ 540,000 Fair value increment $ 250,000 FVI Allocation: Sub Book FMV FVI FVI Allocated Assets Cash $ 40,000 $ 40,000 $ - $ - Inventory 40,000 30,000 (10,000) (10,000) Equipment, net 120,000 100,000 (20,000) (20,000) Building, net 300,000 360,000 60,000 60,000 Land 50,000 160,000 110,000 110,000 Total Assets $ 550,000 $ 690,000 $ 140,000 $ 140,000 Liabilities Liabilities $ 10,000 $ 14,000 $ 4,000 $ 4,000 Total liabilities $ 10,000 $ 14,000 $ 4,000 $ 4,000 FVI Allocated to net identifiable assets $ 136,000 Goodwill @ 100% $ 114,000

Amortize FVIs:

FVI Allocated Amort. PeriodAmort.

per year

Amort./ impairment loss

during 20X5

Balance of FVI remaining at the end of

20X5Inventory $ (10,000) $ (10,000) $ 0Equipment (20,000) 10 $ (2,000) (2,000) (18,000)Building 60,000 20 3,000 3,000 57,000Land 110,000 110,000Goodwill 114,000 114,000Liabilities (4,000) (4,000) 0Total $ 250,000 ($13,000) $263,000

Note: The various adjustments and eliminations are being presented as entries below.The at-the-time-of-acquisition adjusting and eliminating entries are:

Building $ 60,000 Land 110,000Common shares 250,000Retained earnings 290,000Goodwill 114,000

Investment in Sub Ltd. $553,000Inventory 10,000Equipment 20,000Liabilities 4,000Non-controlling interest 237,000

Copyright © 2014 Pearson Canada Inc. 247

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

The consolidation related adjustments and eliminations for the current year of 20X5 are:

Inventory 10,000Cost of Sales 10,000

Depreciation expense 1,000Accumulated depreciation – equipment 2,000

Accumulated depreciation – building 3,000

Liabilities 4,000Income Summary/Expenses (20X5) 4,000

Note: The adjustment for the liabilities fair value debit decrement may cause some confusion. If the liability was liquidated at $14,000 as the fair value implies, then the entry to record the payment on the books of Sub would appear as follows:

Liability $10,000Loss (or increase of expense) 4,000

Cash $14,000

The consolidation worksheet adjustment then offsets the recorded loss of $4,000. If the liability was actually settled for $10,000, then the $14,000 fair value estimate was wrong and the fair value debit must be charged to income when the error is detected in 20X5. Thus, regardless of the actual amount for which the liability is settled, the fair value increment must be credited to 20X5 net income.

P5-91.

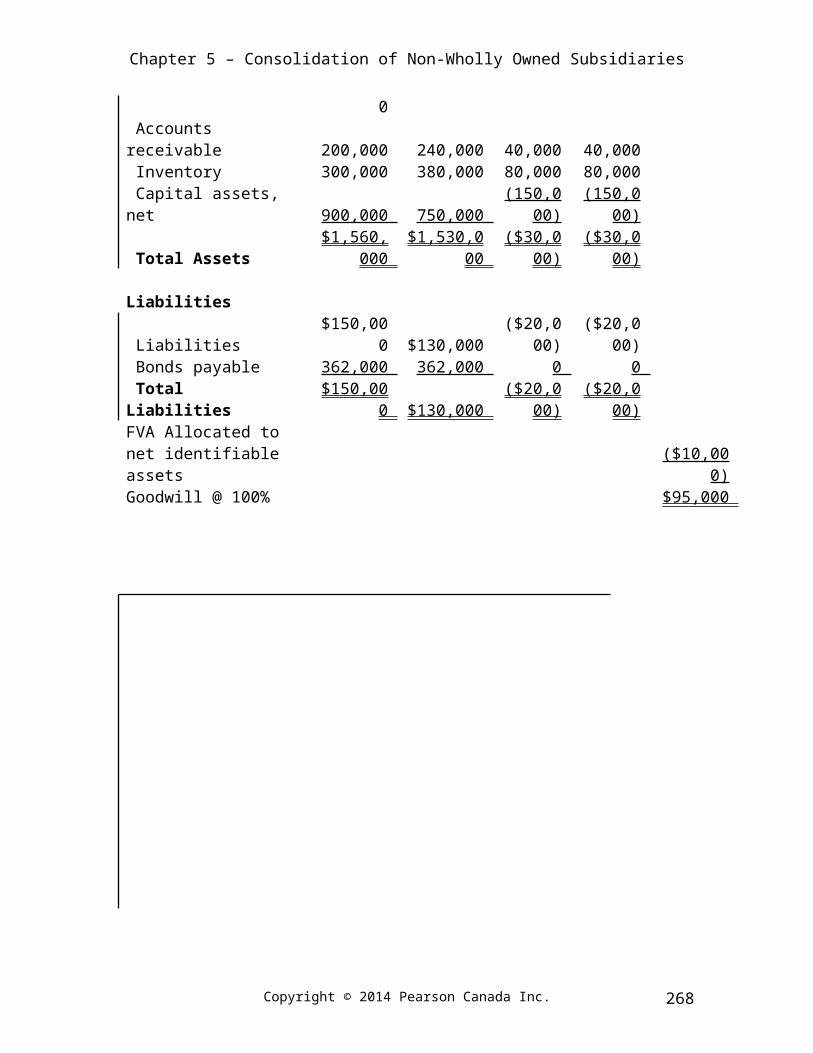

Measure Step:Purchase consideration $906,400 Grossed-up value of Sub based on purchase price $1,133,000 Carrying value of Sub net assets 1,048,000 Fair value adjustment 85,000 FVA Allocation:

Sub

Carrying FMV FVA

FVA Allocate

d Assets Cash $160,000 $160,000 $0 $0 Accounts receivable 200,000 240,000 40,000 40,000

Copyright © 2014 Pearson Canada Inc. 248

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Inventory 300,000 380,000 80,000 80,000 Capital assets, net 900,000 750,000 (150,000) (150,000) Total Assets $1,560,000 $1,530,000 ($30,000) ($30,000)

Liabilities Liabilities $150,000 $130,000 ($20,000) ($20,000) Bonds payable 362,000 362,000 0 0 Total Liabilities $150,000 $130,000 ($20,000) ($20,000)FVA Allocated to net identifiable assets ($10,000)Goodwill @ 100% $95,000

Non-controlling interest $226,600

Eliminate Intercompany Transactions:Downstream sale of inventory by Par to Sub $ (140,000)Upstream sale of inventory by Sub to Par (250,000)

Eliminate Unrealized Gains:Calculation of unrealized gain on downstream sale:

Copyright © 2014 Pearson Canada Inc. 249

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Sale price $ 140,000Cost 100,000Gross profit 40,000Inventory remaining unsold 20%Unrealized gain on downstream sale 8,000

Calculation of unrealized gain on upstream sale:Sale price $ 250,000Cost 200,000Gross profit 50,000Inventory remaining unsold 30%Unrealized gain on upstream sale 15,000

Therefore, the following unrealized gains have to be eliminated: Unrealized gain on downstream sale $ (8,000)Unrealized gain on upstream sale (15,000)Unrealized gain on upstream sale of land by Sub to Par (60,000)

Amortize FVIs:

FVA Allocated

Amort. Period

Amort.per year

Amort./ impairment loss

during 20X5Balance of FVA remaining at the

end of 20X5 Accounts receivable $ 40,000 $ 40,000 $ - Inventory 80,000 80,000 0

Capital assets, net (150,000) 10$

(15,000) (15,000) (135,000) Current liabilities 20,000 20,000 - Goodwill 95,000 95,000Total $ 85,000 $ 125,000 $ (40,000)

To clarify the treatment of the fair value decrement relating to current liabilities, note that its carrying value in Sub’s books is $150,000, however, if its fair market value of $130,000 is accurate, Sub. will recognize a gain of $20,000 on retiring the liability at its FMV of $130,000. However, from the consolidated perspective there is no gain since the carrying value at the consolidated level is already at $130,000. Therefore, the amortization expense relating to the fair value decrement of $20,000 will offset the gain of $20,000 recognized by the Sub.

Recognize NCI share of earnings:Unadjusted income of Sub. $74,000Unrealized gain on upstream sale of inventory (15,000

Copyright © 2014 Pearson Canada Inc. 250

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

)

Unrealized gain on upstream sale of land(60,000

)

Amortization of FVI allocated to Inventory(80,000

)Amortization of FVD allocated to capital assets 15,000

Amortization of FVD allocated to current liabilities(20,000

)

Amortization of FVI allocated to accounts receivable(40,000

)$

(200,000)

Adjusted income of Sub.$

(126,000)Non-controlling interest share $ (25,200)

We also need to remember to eliminate Sub.’s at-the-time of acquisition share equity accounts and Par.’s Investment in Sub. account.

[Par Ltd. owns 80% of Sub Ltd.—Direct Method]Consolidated Statement of Comprehensive Income

Year Ended December 31, 20X5

Sales [2,000,000 + 2,000,000 – 140,000 – 250,000] $3,610,000 Cost of sales [1,400,000 + 1,700,000 – 140,000 – 250,000 +15,000 + 8,000 + 80,000] 2,813,000 Gross Margin 797,000 Depreciation Expense [100,000 + 90,000 – 15,000] 175,000 Interest expense [63,000 + 44,000] 107,000 Other expenses [124,000 +78,000 + 20,000 + 40,000] 262,000 Total Expenses 544,000 253,000 Investment Income [37,000 + 60,000 – 60,000] 37,000 290,000 Income Tax [140,000 + 74,000] 214,000 Net Income and Comprehensive Income $ 76,000 Net income attributable to: Owners of the parent $101,200 Non-controlling interests (25,200)

Retained Earnings Section of the Consolidated Statement of Changes in EquityYear Ended December 31, 20X5

Retained earnings Jan. 1. 20X5* $2,001,000Net income 101,200

Copyright © 2014 Pearson Canada Inc. 251

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Retained earnings Dec. 31 20X5 $2,102,200

* Note: Beginning retained earnings is a calculated amount based on the income for 20X5 and the ending retained earnings for 20X5 given in the problem. Thus, beginning retained earnings equals $2,211,000 – $210,000 = $2,001,000.

2. Consolidated SFP amounts, December 31, 20X5

a.Net capital assets: (Buildings and equipment)*Par $1,200,000Sub 900,000FMV Increment (150,000)Amortization 15,000Less: gain (60,000)

$1,905,000*assume land is included in this line item

b.Goodwill:Par $ 0Sub 0FMV Increment 95,000

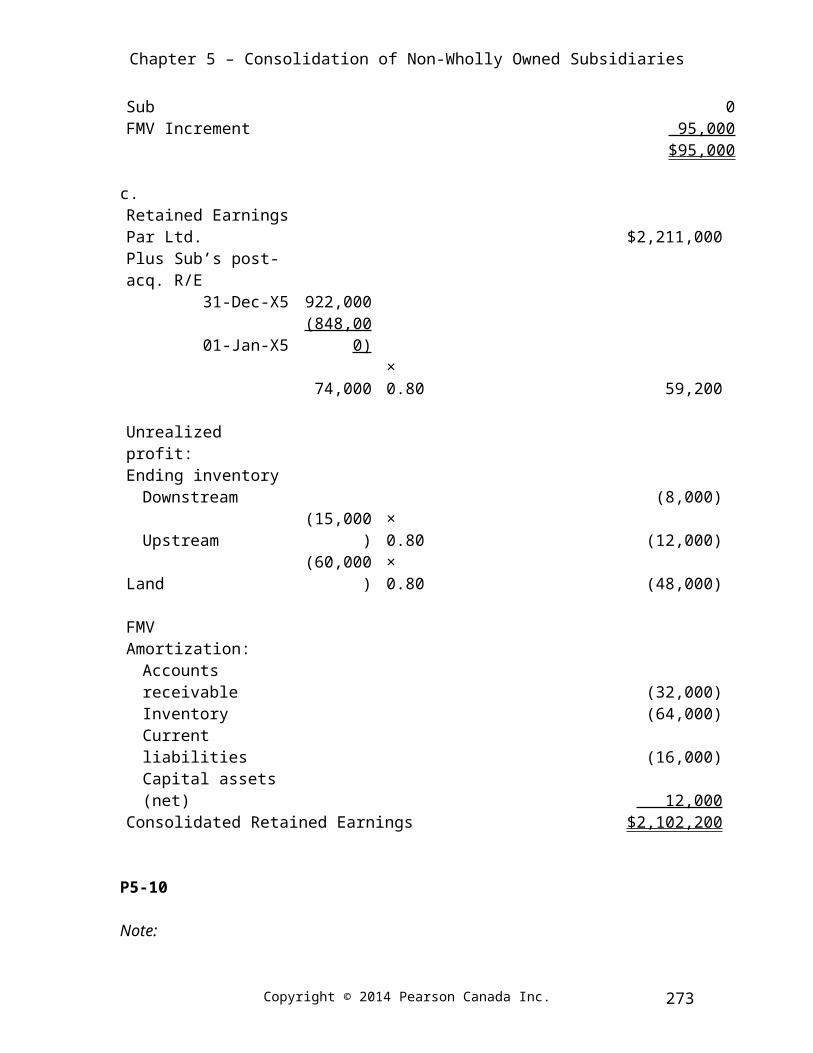

$95,000

c.Retained EarningsPar Ltd. $2,211,000Plus Sub’s post- acq. R/E

31-Dec-X5 922,00001-Jan-X5 (848,000)

74,000 × 0.80 59,200

Unrealized profit:Ending inventory

Downstream (8,000)Upstream (15,000) × 0.80 (12,000)

Land (60,000) × 0.80 (48,000)

FMV Amortization:Accounts receivable (32,000)Inventory (64,000)

Copyright © 2014 Pearson Canada Inc. 252

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Current liabilities (16,000)Capital assets (net) 12,000

Consolidated Retained Earnings $2,102,200

P5-10

Note:

Measure Step:

Purchase consideration $972,000

Grossed-up value of Sub based on purchase price $ 1,080,000

Carrying value of Sub net assets 1,020,000

Fair value adjustment $60,000

FVA Allocation:

Sub Book FMV FVA FVA

Allocated

Assets

Cash $60,000 $60,000 $0 $0

Accounts receivable 120,000 160,000 40,000 40,000

Inventory 180,000 220,000 40,000 40,000

Capital assets, net 1,500,000 1,350,000 (150,000) (150,000)

Goodwill 100,000 (100,000) (100,000)

Total Assets $1,960,000 $1,790,000 ($170,000) ($170,000)

Liabilities

Current liabiliies $140,000 $140,000 $0 $0

Bonds payable 800,000 850,000 50,000 50,000

Total liabilities $940,000 $990,000 $50,000 $50,000 FVI Allocated to net identifiable assets (220,000)

Goodwill @ 100% $ 280,000

Non-controlling interest @ 10% of $ 1,080,000 $ 108,000

Copyright © 2014 Pearson Canada Inc. 253

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

Eliminate Intercompany Transactions:Downstream sale of inventory by Parent to Sub ($ 275,000)Dividends paid by Sub ($60,000)

Eliminate Unrealized Gains & Recognize Realized Gains:Calculation of unrealized gain on downstream sale:Sale price $ 275,000Cost 200,000Gross profit 75,000Inventory remaining unsold by end of 20X5 35%Unrealized gain on downstream sale 26,250

Calculation of realized gain in 20X5 on upstream sale made in 20X4:Sale price $ 320,000Cost 260,000Gross profit 60,000Inventory remaining unsold by end of 20X4 25%Profit in beginning inventory realized in 20X5 15,000

Therefore, the following unrealized gains have to be eliminated: Unrealized gain on downstream sale $ (26,250)Realized gain on upstream sale 15,000

Amortize FVIs:

FVI Allocated

Amort. Period Amort.

Amort./ impairment in previous

Amort./ impairment loss during

Balance of FVI

remaining

Copyright © 2014 Pearson Canada Inc. 254

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

years of 20X4 20X5 at the end

of 20X5per year

Accounts receivable $40,000 $40,000 $0

Inventory 40,000 40,000 0

Capital assets, net (150,000) 10 (15,000) (15,000) (15,000) (120,000)

Liabilities (50,000) 10 (5,000) (5,000) (5,000) (40,000)

Goodwill 280,000 280,000

Total $160,000 $60,000 ($20,000) $120,000

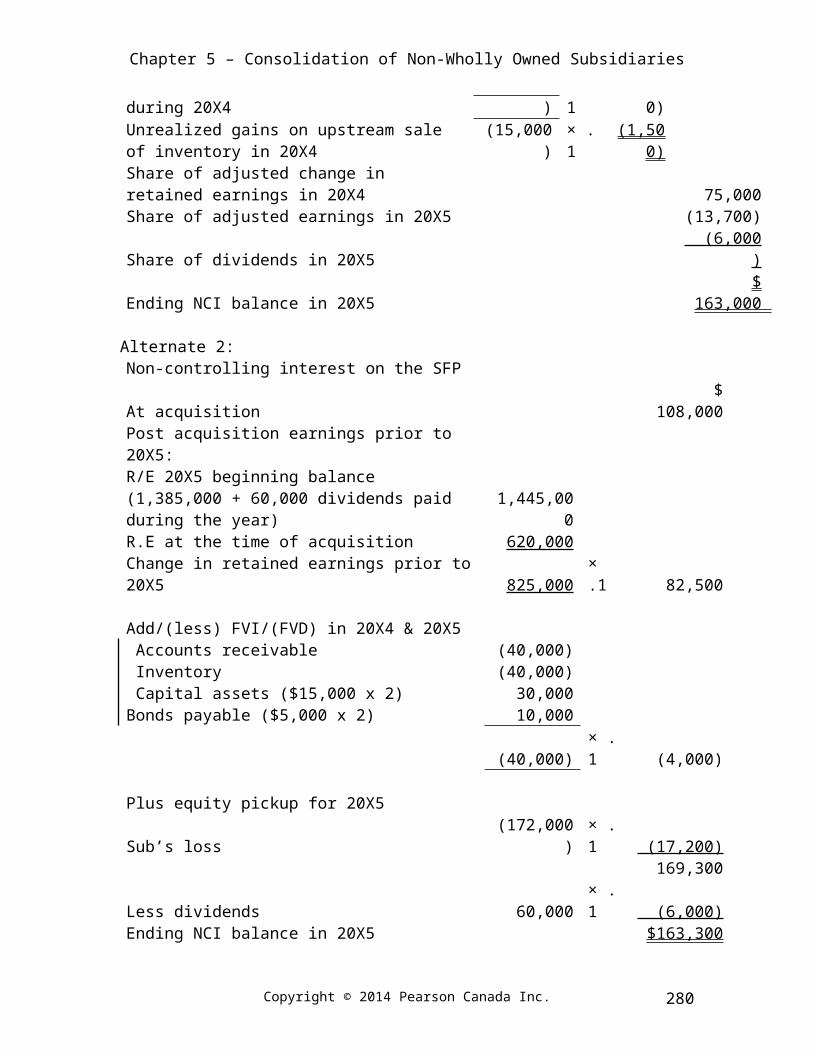

Recognize NCI share of earnings:Unadjusted income of Sub. $ (172,000)Realized gain on upstream sale of inventory $ 15,000Amortization of FVD allocated to capital assets 15,000Amortization of FVD allocated to bonds payable 5,000 $35,000Adjusted income of Sub. $ (137,000)Non-controlling interest share $ (13,700)

Copyright © 2014 Pearson Canada Inc. 255

Chapter 5 – Consolidation of Non-Wholly Owned Subsidiaries

1. [Parent Ltd. owns 90% of Sub Ltd.—Direct Method]Consolidated Statement of Comprehensive Income

Year Ended December 31, 20X5