chapter 3 cash flows and financial analysis © 2000 south-western college publishing

TRANSCRIPT

Chapter 3Chapter 3

Cash Flows andCash Flows and

Financial AnalysisFinancial Analysis

© 2000 South-Western College Publishing

FINANCIAL INFORMATIONFINANCIAL INFORMATIONResults of operations in money terms

Basis for projecting future results

Responsibility of management

USERS OF FINANCIAL INFORMATION

Investors Make judgments about the firm's securities

Financial Analysts report to investment community

Vendors

Sell to the firm on credit

Management Highlight areas in which attention will improve performance

TM 3-1 Slide 1 of 3

SOURCES OF FINANCIAL SOURCES OF FINANCIAL INFORMATIONINFORMATION

Annual ReportManagement's report card to

stockholders on its own

performance

Tends to be favorably biased

Other SourcesBrokerage firms, credit bureaus

TM 3-1 Slide 2 of 3

ORIENTATION OF FINANCIAL ORIENTATION OF FINANCIAL ANALYSTSANALYSTS

Critical and investigative

Looking for current or potential problems

Looking for the physical reasons behind financial results

TM 3-1 Slide 3 of 3

CASH FLOWCASH FLOW Businesses run on cash, not on accounting profits.

It's possible to go out of business while making a profit.

THE STATEMENT OF CASH FLOWS

Shows where money actually comes from and goes to

Developed from the basic income statement and balance sheet

Other Terminology

Funds flow

Sources and uses (applications) of cash or funds

Statement of changes in financial position

TM 3-2 Slide 1 of 2

BASIC APPROACHBASIC APPROACH

Adjust net income for non cash items

Analyze changes in balance sheet accounts between beginning and end of year as sources or uses of cash

Organize and sum

Free Cash Flows

Available after reinvestments needed for growth

and to replace worn-out equipment

TM 3-2 Slide 2 of 2

CASH FLOW RULESCASH FLOW RULES

Asset Increase = Use

Asset Decrease = Source

Liability Increase = Source

Liability Decrease = Use

TM 3-3

CASH FLOWS IN A BUSINESSCASH FLOWS IN A BUSINESS

Organized into three activities

Operating Activities Routine running of the company

Sales, collections, inventories, wages, etc.

Paying interest on debt

TM 3-4 Slide 1 of 2

Investing ActivitiesInvesting Activities

Commitment of long term capital

Usually buying or selling fixed assets

Investing Activities Equity and long term debt transactions

Selling stock and paying dividends

Borrowing and repaying loans

(Note: Interest payment in operating activities)

TM 3-4 Slide 2 of 2

A GRAPHIC PORTRAYAL OF BUSINESS CASH FLOWSA GRAPHIC PORTRAYAL OF BUSINESS CASH FLOWS

Figure 3.1 Business Cash Flows

Cash to vendors

Cash to

vendors

Cash to

employees

Stock

Cash price Cash from

from/to customers

stockholders

Cash Cash to IRS to/from Repayment lenders

TM 3-5

Operating Activities

Accrual

Pay Wages

Payable

Buy Inventory

Product

Sale

Receivable

Pay Taxes

CASH

Investing Activities

Financing Activities

Purchase Fixed Assets

Stock Equity

Bonds DebtLoan

Intrst

Divs

ANOTHER VISUAL REPRESENTATIONANOTHER VISUAL REPRESENTATION THE CASH CONVERSION CYCLE THE CASH CONVERSION CYCLE

(RACETRACK DIAGRAM)

Figure 3-2 The Cash Conversion Cycle: The Racetrack Diagram TM 3-6

A/R

Cash Sale

Inventory

Labor

Assets, Taxes, Profits...

BUILDING THE STATEMENT OF CASH FLOWSBUILDING THE STATEMENT OF CASH FLOWSBelfry Company

Balance SheetFor the Period Ended 12/31/00

ASSETS12/31/99 12/31/00

Cash $1,000 $1,400Accts. Receivable 3,000 2,900Inventory 2,000 3,200CURRENT

ASSETS $6,000 $7,500Fixed Assets

Gross $4,000 $6,000Accum. Depr. (1,000) (1,500)Net $3,000 $4,500

TOTAL ASSETS $9,000 $12,000LIABILITIES

Accts. Payable $1,500 $2,100Accruals 500 400CURRENT LIABIL. $2,000 $2,500Long-term debt $5,000 $6,200Equity 2,000 3,300TOTAL CAPITAL $7,000 $9,500TOTAL LIABILITIES AND EQUITY $9,000 $12,000

Belfry CompanyBalance Sheet

For the Period Ended 12/31/00

Sales $10,000COGS 6,000Gross Margin $ 4,000

Expense $ 1,600Depreciation 500EBIT $ 1,900Interest 400EBT $ 1,500Tax 500Net Income $ 1,000

TM 3-7

OPERATING ACTIVITIESOPERATING ACTIVITIES

Net income $1,000Depreciation 500Net changes in current accounts (600)Cash from operating

activities $ 900

Detail of Changes in Current AccountsDetail of Changes in Current Accounts

Account Source/(Use)Receivables $ 100Inventory (1,000)Payables 600Accruals (100)

$ (600)

INVESTING ACTIVITIESINVESTING ACTIVITIESPurchase of fixed assets ($2,000)

(Note: excludes cash)

TM 3-8 Slide 1 of 2

FINANCING ACTIVITIESFINANCING ACTIVITIES

Increase in long-term debt $1,200

Sale of stock 800Dividend paid (500)

Cash from financing activities $1,500

UNDERSTANDING THE EQUITY ACCOUNTUNDERSTANDING THE EQUITY ACCOUNTAmount Activity

Net income $1,000 OperatingStock sale 800 FinancingDividend (500) Financing

Change in equity $1,300

TM 3-8 Slide 2 of 2

RATIO ANALYSISRATIO ANALYSIS

Pairs of numbers from the financial statements formed into ratios

Each ratio high-lights a particular aspect of running the business

Example: The current ratio measures liquidity, the ability to pay bills in the short run

Current Assets: Money coming in within a year

Current Liabilities: Money going out within a year

For solvency need: Current ratio >> 1.0

TM 3-9 Slide 1 of 3

Current ratio = current assetscurrent liabilities

COMPARISONSCOMPARISONSRatios are most meaningful when compared with similar figures

History

Prior performance - look for trends

Competitors

Identify strong or weak spots relative to similar businesses

Plan

Is performance better or worse than expected?

AVERAGE OR ENDING BALANCES

Ending when measuring a status

Average when measuring an activity

Distinction important when growth is rapid

TM 3-9 Slide 2 of 3

CATEGORIES OF RATIOSCATEGORIES OF RATIOS

• Liquidity• Asset Management• Debt Management

• Profitability• Market Value

Ratios Don't Provide Answers

They Help You Ask The Right Questions

TM 3-9 Slide 3 of 3

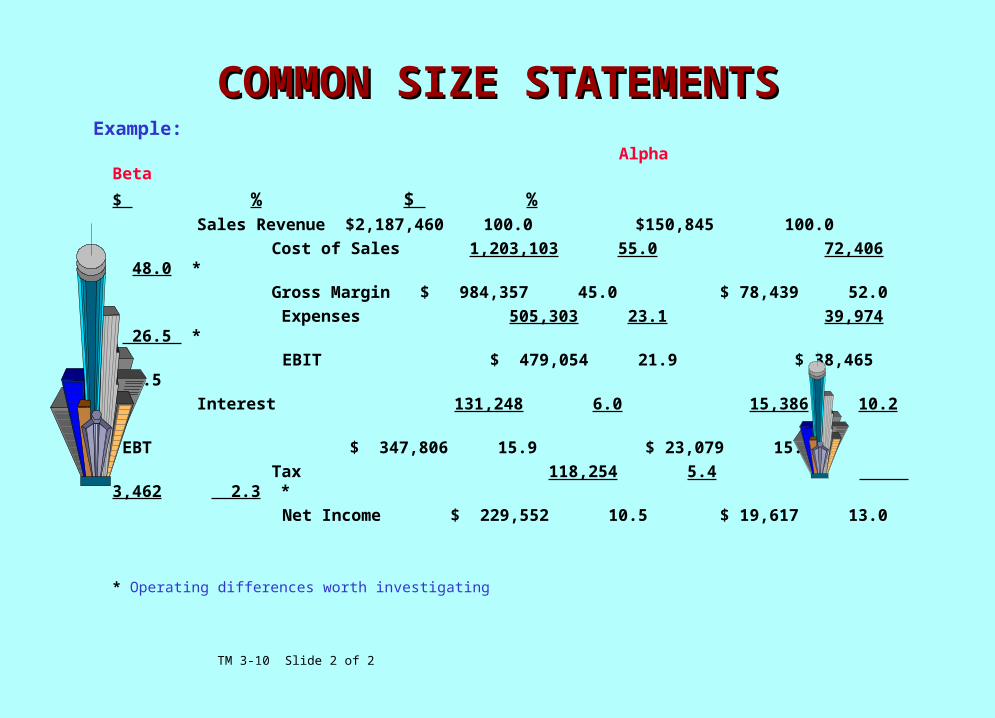

COMMON SIZE STATEMENTSCOMMON SIZE STATEMENTS

Ratios of income statement line items

to sales revenue

Facilitates operating comparisons

over time and between

companies of different sizes

TM 3-10 Slide 1 of 2

COMMON SIZE STATEMENTSCOMMON SIZE STATEMENTS Example: Alpha Beta

$ % $ % Sales Revenue $2,187,460 100.0 $150,845 100.0

Cost of Sales 1,203,103 55.0 72,406 48.0 *

Gross Margin $ 984,357 45.0 $ 78,439 52.0

Expenses 505,303 23.1 39,974 26.5 *

EBIT $ 479,054 21.9 $ 38,465 25.5

Interest 131,248 6.0 15,386 10.2 *

EBT $ 347,806 15.9 $ 23,079 15.3

Tax 118,254 5.4 3,462 2.3 *

Net Income $ 229,552 10.5 $ 19,617 13.0

* Operating differences worth investigating

TM 3-10 Slide 2 of 2

LIQUIDITY RATIOSLIQUIDITY RATIOS

Measure the ability to meet short term obligations

(Use ending balances)

(Examples from Belfry Company)

Current Ratio

TM 3-11 Slide 1 of 2

current ratio = current assetscurrent liabilities

current ratio = $7,500

$2,500 = 3.0

Quick Ratio (Acid Test)Quick Ratio (Acid Test)

Removes inventory which may be problematic in

generating cash

TM 3-11 Slide 2 of 2

1.72$2,500

$3,200$7,500= Ratio Quick

sliabilitiecurrent inventoryassestscurrent = Ratio Quick

=

ASSET MANAGEMENT RATIOSASSET MANAGEMENT RATIOS (Use average balances)

AVERAGE COLLECTION PERIOD (ACP)AVERAGE COLLECTION PERIOD (ACP) How long does it take to collect on credit sales?

Interpretation: All customers paying slow or there are old receivables which may never be collected.

TM 3-12 Slide 1 of 2

days 106.2 = 360 $10,000$2,950 = ACP

360 sales

receivable accounts = ACP

sales daily averagereceivable accounts = ACP

INVENTORY TURNOVERINVENTORY TURNOVER

Measures inventory used to support production and operations

(COGS)

(Sales)

Interpretation: Too much inventory is expensive to carry. Too little causes stockouts: inefficient production and lost sales.

TM 3-12 Slide 2 of 2

3.8 = $2,600

$10,000 =turnover Inventory

2.3 = $2,600$6,000 =turnover Inventory

inventorysales =turnover Inventory

OR inventory

sold goods ofcost =turnover Inventory

FIXED ASSET TURNOVER AND TOTAL ASSET FIXED ASSET TURNOVER AND TOTAL ASSET TURNOVERTURNOVER

Measures effectiveness of assets in generating sales

Interpretation: Are there idle or inefficient assets?

Are promotional efforts effective?

TM 3-13

.95 = $10,500$10,000 =turnover asset Total

2.7 = $3,750

$10,000 =turnover asset Fixed

assets totalsales =turnover asset Total

assets fixedsales =turnover asset Fixed

DEBT MANAGEMENT RATIOSDEBT MANAGEMENT RATIOS

Measures the firm's debt level relative to assets, equity, and income (Use ending balances)

DEBT RATIO

TM 3-14 Slide 1 of 2

Debt ratio = long- term debt + current liabilities

total assets

Debt ratio = $6,200 + $2,500

$12,000 = 72.5%

DEBT TO EQUITY RATIODEBT TO EQUITY RATIO

Debt to Equity Ratio = Long Term Debt : Equity

Debt to Equity = $6,200 : $3,300

= 1.9 : 1

(Stated as 1.9 to 1, since $6,200/$3,300 = 1.9)

Interpretation: Too much debt as a percentage of assets or

equity is an indication that financial risk may

be making the firm unstable.

TM 3-14 Slide 2 of 2

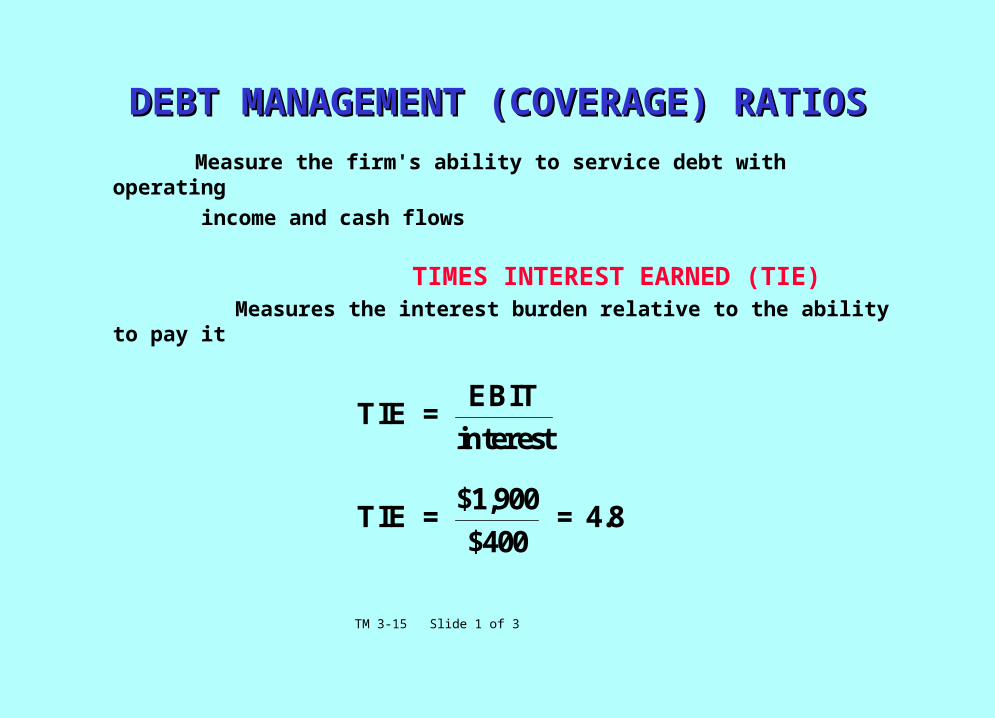

DEBT MANAGEMENT (COVERAGE) RATIOSDEBT MANAGEMENT (COVERAGE) RATIOS

Measure the firm's ability to service debt with operating

income and cash flows

TIMES INTEREST EARNED (TIE) Measures the interest burden relative to the ability to pay it

TM 3-15 Slide 1 of 3

TIE = EBIT

interest

TIE = $1,900

$400 = 4.8

CASH COVERAGECASH COVERAGE

A variation on TIE to better get at cash flow

TM 3-15 Slide 2 of 3

Cash coverage = EBIT + depreciation

interest

Cash coverage = $1,900 + $500

$400 = 6.0

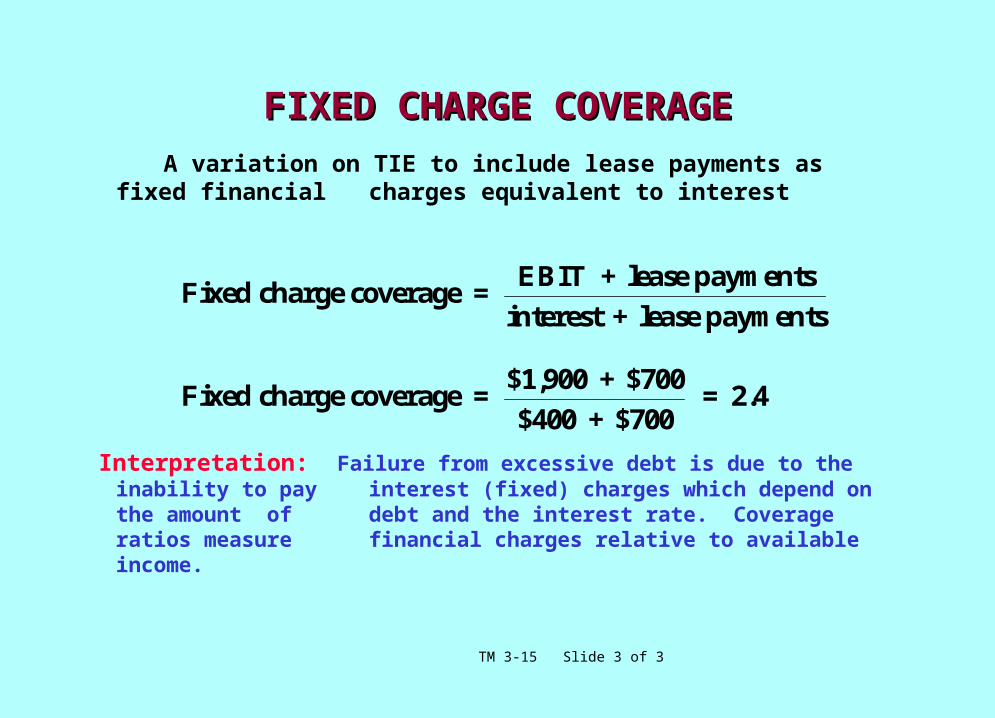

FIXED CHARGE COVERAGEFIXED CHARGE COVERAGE

A variation on TIE to include lease payments as fixed financial charges equivalent to interest

Interpretation: Failure from excessive debt is due to the inability to pay interest (fixed) charges which depend on the amount of debt and the interest rate. Coverage ratios measure financial charges relative to available income.

TM 3-15 Slide 3 of 3

Fixed charge coverage = EBIT + lease payments

interest + lease payments

Fixed charge coverage = $1,900 + $700

$400 + $700 = 2.4

PROFITABILITY RATIOSPROFITABILITY RATIOSMeasure profitability relative to sales, assets, and the owners'

investment (equity) (Use average balances)

RETURN ON SALES (ROS)RETURN ON SALES (ROS)

Interpretation: Measures control of pricing, costs, and expenses

TM 3-16 Slide 1 of 3

ROS = net income

sales

ROS = $1,000

$10,000 = 10%

RETURN ON ASSETS (ROA)RETURN ON ASSETS (ROA)

Interpretation: Measures control of pricing, costs, and expenses

and asset utilization

TM 3-16 Slide 2 of 3

ROA = net income

total assets

ROA = $1,000

$10,500 = 9.5%

RETURN ON EQUITY (ROE)RETURN ON EQUITY (ROE)

Interpretation: Measures control of pricing, costs, and expenses and asset utilization, and the use of leverage

TM 3-16 Slide 3 of 3

ROE = net income

equity

ROE = $1,000

$2,650 = 37.7%

MARKET VALUE RATIOSMARKET VALUE RATIOS Measure the market's opinion of the stock as an investment based on

its price (Use ending balances)

PRICE/EARNINGS RATIO (P/E)

Interpretation: The amount investors will pay for each dollar of earnings

Based primarily on expected growth

TM 3-17 Slide 1 of 2

11.4 = $3.33$38 = P/E

$3.33 = 300

$1,000 = EPS

EPSprice stock = Ratio P/E

MARKET TO BOOK VALUE RATIOMARKET TO BOOK VALUE RATIO

Interpretation: Identifies the going concern value of the firm as perceived by investors

TM 3-17 Slide 2 of 2

Market to book value ratio = stock price

book value per share

Market to book value ratio = $38

$11 = 3.5

DU PONT EQUATIONSDU PONT EQUATIONS

Identify relationships between ratios

TM 3-18 Slide 1 of 3

ROA = net income

total assets

sales

sales

ROA = net income

sales

sales

total assets

ROA = ROS total asset turnover

Extended Du Pont EquationExtended Du Pont Equation

ROE = net income

equity

sales

sales

total assets

total assets

ROE = net income

sales

sales

total assets

total assets

equity

ROE = ROS total asset turnover equity multiplier

ROE = ROA equity multiplier

TM 3-18 Slide 2 of 3

Using the Du Pont Equations to Analyze ProblemsUsing the Du Pont Equations to Analyze Problems

ROA = ROS Total Asset Turnover

Pillbox Inc. 12% 6% 2

Industry 15% 5% 3

Focus attention on revenue or assets rather

than on cost or expense

TM 3-18 Slide 3 of 3