chapter 3 (continued) state and local spending states redirect funds to local (municipal or county)...

TRANSCRIPT

Chapter 3 (Continued)

State and Local Spending States redirect funds to local (municipal or

county) level

40% of local government spending primary and secondary education

Other big spending: social welfare (4%), hospitals (5%), police (5.6%)

Local Govt. Budgets

Various budget processes depending on location

Likewise various types of control mechanisms, generallyRanking of prioritiesLimits on expansion of servicesSpecific dollar level ceilings

State Budget Processes

Depends on state

1. Not all states have executive budgets, may entirely at discretion of legislature

2. Flexibility in terms of both legislative budget decisions and governor’s. Some states have part-time legislatures and grant executive discretion during non-meeting periods.

3. May have various mechanisms for dealing with periods when a budget cannot be passed. Can include continuing resolutions, special sessions, etc.

4. Most states have line-item veto power.

State and Local Deficits

Typically state/local govts. do not have large deficitslimited access to the capital marketRestricted ability to impact macroeconomy Most have budget stabilization funds to

accommodate difficult financial periods

Chapter 4Budget Methods & Practice

OVERVIEW

1. Preparation of budget requests2. Review of agency requests3. Construction of final executive budgets4. Management of budget execution5. Audits

Budget Requests

1. Contains a narrative – justifying the planned agency action

2. Detailed schedule – specifies objectives into budget requests

3. Cumulative schedule – aggregates new initiatives into existing activities

Surprisingly, the descriptive element is usually more important than the numbers since it provides the justification

Budget justification

A narrative explanation of spending needs Should avoid jargon and abbreviations Must be factual and provide documentation Should clearly explain the current need If requesting an increase, justify reason Finally, provide the benefits that will result

from fulfilling the request

Example Budget Narrative

The Bloomington Youth Center provide a safe supervised environment for teens. This budget request would provide for five years of operating costs and part-time staff. The city is a focal point for runaways in the region, and the number of teens has increased from approximately 300 in 1995 to 500 in 2003. Additional funds are requested for 3-days professional counseling training for volunteer staff.

Cost Estimation

Provides estimates of numeric costs for fulfilling agency mission

Includes: Personnel Costs

Non-personnel Costs

Personnel Costs

DIRECT COMPENSATION - Wages and salaries

Calculated by hours assigned to task

(hourly, monthly, yearly, etc).

NON-WAGE – Fringe benefits Pensions, health, life insurance, payroll

tax payments, etc.

Designing a Budget Schedule

Includes all line item costs May be assigned a code corresponding to a

standardized system (rather than “Social Security payroll deductions” would be “4056”).

May or may not include a schedule illustrating the timing of each expenditure

Can be organized according to department, objective or function

Example Basic Budget

High School

Annual

Budget

A More Advanced Budget Schedule

Break-even Analysis

Tells the point at which operating costs and revenue will equal, or break-even

Used to estimate such things as the minimal level of clients necessary to provide a service, whether a particular activity is a net gain or loss, or if an activity is even worth the investment

Plots costs against revenues as the quantity of output varies and compares to total costs.

Need both equation representing revenue and one representing costs

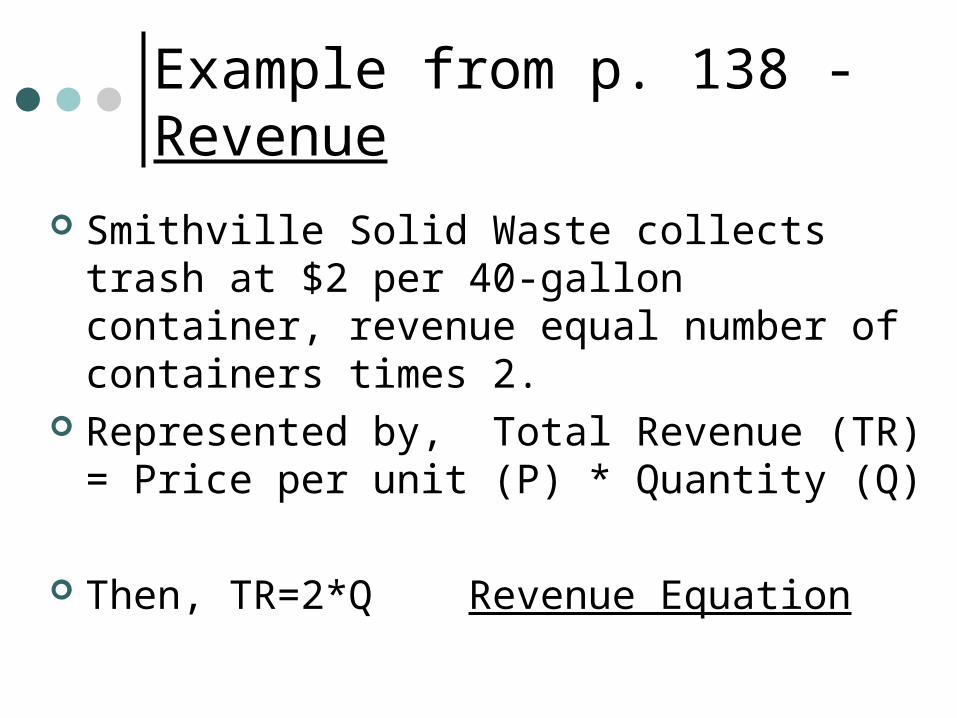

Example from p. 138 - Revenue

Smithville Solid Waste collects trash at $2 per 40-gallon container, revenue equal number of containers times 2.

Represented by, Total Revenue (TR) = Price per unit (P) * Quantity (Q)

Then, TR=2*Q Revenue Equation

Costs

Two types of costs: Fixed and Variable Fixed-any cost that remains constant no matter

what level of service is being provided. Ex: Building maintenance, Support staff, Equipment leasing, Advertising, etc.

Variable – costs that change as additional units of a good are produced. Ex: Material (# of flu vaccines given, unit of water sanitized, fuel used, etc.), labor (hours of counseling, additional staff)

Total costs:

Fixed Costs:Administration (staff, utilities, etc.) $ 35,000Equipment lease 85,000

Total Fixed Costs: $120,000

Variable Costs (per unit):Landfill charge $ 1.00Equipment operations 0.15Collection crew payments 0.25

Total Variable Costs: $ 1.40

Total Costs

Represented as, TC = FC + (VC * Q)

Where TC=total costs, FC=Fixed costs, VC=Variable costs, Q=Quantity supplied

So, TC = 120,000 + 1.40Q

Break-even point

= where the total costs (TC) equals the total revenues (TR)

Set the two equations equal, TR=TCwhere TR= P*Q and TC = FC + (VC * Q), so

2Q = 120,000 + 1.40Q, solve for Q

The Break-even point is where Q=200,000. So at least 200,000 clients will need to be served in order for revenues to cover costs.

Graphic Example

Data Example

Quantity Total Revenue Total Costs

Q 2Q 120000+1.4Q

0 0 120000

10 20 120014

50 100 120070

1,000 2000 121400

10,000 20000 134000

100,000 200000 260000

200,000 400,000 400,000

400,000 800000 680000

600,000 1200000 960000

800,000 1600000 1240000

Class Exercise You are planning a Halloween party on a very limited

budget. You plan to charge $2 per person. How many people do you need to invite in order to not lose any money? Use the following information to determine the break-even point.

Fixed costs Keg = $ 75 Ice bucket = 10 Tikki torches = 15

Variable costs Cups = 0.05 Ice = 0.02

Deficit Reduction Avoidance Mechanisms

1. Using Rosy scenarios

2. Including one-shot revenue sources

3. Inter-budget manipulation

Deficit Reduction Avoidance Mechanisms (continued…)

4. Bubbles & timing

5. Ducking the decision

6. Use the Intergovernmental System

7. “Magic asterisk”

Managing Budget Execution

Managerial Controls Qualified personnel Segregated responsibilities Separate operations and accounting Assign responsibility Maintain controlled proofs and security Record transactions and safeguard

assets

Audits and Evaluation

Audit – both internal and external. Ensures that the funds were spend in the appropriate manner and that all revenues and costs are reported. Accounting standard.

Evaluation – measures whether funds were used efficiently. Main concern is efficiency.

Types of audit “irregularities” Ghosting – theft through phantom resources, either

staff that does not exist or supplies and services that are not delivered

Bid rigging – collusion with private firms to raise the price of a service delivered

Shoddy material – rather than raising price of the bid, lower the quality resources for normal bid price

Honest graft – use of insider information for private profit

Diversion of public resource –public resource for private use

Kickbacks – Side payments to public officials for preferential treatment