chart of accounts - dairybase/media/dairybase/dairybase... · the standard chart of accounts...

TRANSCRIPT

Chart of accountsExplanatory guide

Disclaimer

Whilst all reasonable efforts have been taken to ensure the accuracy of the Standard Chart of Accounts Explanatory Guide, use of the information contained herein is at one’s own risk. To the fullest extent permitted by Australian law, Dairy Australia disclaims all liability for any losses, costs, damages and the like sustained or incurred as a result of the use of or reliance upon the information contained herein, including, without limitation, liability stemming from reliance upon any part which may contain inadvertent errors, whether typographical or otherwise, or omissions of any kind.

© Dairy Australia Limited 2015. All rights reserved.

ISBN 978-1-925347-04-3

Dairy Australia standard chart of accounts | Explanatory guide 1

Contents

Purpose 2

Introduction 3

Explanation of terms 4

Descriptions 5

Key physical number 6

Options 7

GST selection 8

Appendix - Standard chart of accounts 9

2

This explanatory guide has been developed as a resource to assist in understanding and interpreting the Standard Chart of Accounts developed by Dairy Australia to be utilised by the Australian Dairy Industry.

The aim of this document and the Standard Chart of Accounts (SCoA) is to drive consistency across the Australian dairy industry in how we discuss, describe, calculate and report farm business performance.

There has been a significant amount of work undertaken by a number of groups within the Australian dairy industry over a long period of time and the culmination of this work and the assessment of previous documents has resulted in this guide and the Standard Chart of Accounts being developed.

Some of the major contributors over recent years have been Murray Dairy through the development of their Financial Records Guide and the Department of Economic Development, Jobs, Transport and Resources (DEDJTR) formerly known as the DPI, through the Dairy Farm Monitor Project (DFMP) that started in the 2006/07 financial year.

More recently the work undertaken to establish DairyBase, the new Dairy Australia web based Farm Business Management tool, has resulted in a further review of terminology utilised in farm business management and the logical flow of income and expenses as it is interpreted in management accounts.

The original Financial Records Guide for Dairy Farms was produced by Murray Dairy for all dairy farmers to provide assistance with establishing and maintaining a Chart of Accounts following the introduction of the GST in 2000.

It was designed to enable dairy farmers to improve financial and farm management decisions through the better use of financial data to monitor costs or benchmark performance.

The original guide was developed in response to a group of dairy farmers seeking assistance regarding the establishment of their Chart of Accounts.

In response, Murray Dairy established a Reference Team comprised of dairy farmers, consultants, extension officers, accountants and rural counsellors to provide dairy farmers with information on establishing and maintaining a Chart of Accounts. Murray Dairy subsequently revised and updated the guide to bring it into line with changes in the Dairy Industry.

With the recent release (May, 2015) of DairyBase, the Financial Records Guide for Dairy Farms has again been updated to ensure consistency with DairyBase and the Dairy Farm Monitor Project.

This version of the Guide provides a complex Chart of Accounts, which should satisfy the requirement of the most detailed record keeper and a truncated version providing the minimum requirement to complete a DairyBase analysis.

Purpose

Dairy Australia standard chart of accounts | Explanatory guide 3

Whilst one of the main aims of a Standard Chart of Accounts is to drive consistency across the Australian dairy industry in how we discuss, describe, calculate and report farm business performance it also meets many other goals.

The Standard Chart of Accounts enables dairy farmers to manage the flow of financial information through their business and establish an efficient system for paying bills and complying with Australian tax regulations. Whilst ensuring tax compliance, the Standard Chart of Accounts can also be converted to management accounts with relative ease to enable farmers to make informed decisions in their businesses. The management accounts enable farmers to complete end of year and comparative analysis on their business by ensuring a consistent approach to the allocation of financial information and financial terminology used within the Dairy industry. It will also enable conversion to a regular cashflow and could be utilised for budgeting within businesses.

The Standard Chart of Accounts has not been established as a rigid tool to prescribe the exact setup of farm accounts on all dairy farms, it has merely been developed as a guide to the way a dairy farmer can keep financial records but, if used correctly, will give consistency in record keeping. As well as providing farmers with data to make informed financial and farm management decisions, the Chart of Accounts will allow farmers to effectively benchmark their business. The use of “benchmarks” by some sectors of the dairy industry can only be accurate if each business doing the comparisons have put their income and expenses in the same category in their financial recording system.

Introduction

4

The Dairy Industry, including, farmers, service providers and the computer software packages used by all these groups use various terms to refer to accounts listed under the headings of Income and Expenses. For the purpose of this guide we have used the terms “Category”, “Sub-Category” and “Sub-sub Category”.

For example, under the heading Expenses there are Categories of Herd, Shed and Feed. These categories may have sub-categories eg. Feed, sub Agistment. Sub-categories may also be expanded into Sub-sub-categories eg. Agistment, sub Cartage etc.

For example if you paid $200.00 to W. Black for cartage of heifers to agistment you would enter this in Cartage which is a Sub-sub category of Agistment which is a Sub category of Feed which is one of the main expense Categories.

Where sub or sub-sub categories exist, the income or expense must be entered in the lowest sub category. For example if you have sub-sub categories within Herd Costs and you were entering a Herd Test expense then you need to enter it under the sub-sub category of Herd Test, rather than directly under the sub-category of AI & Herd Test of the Category of Herd Costs.

Explanation of terms

Dairy Australia standard chart of accounts | Explanatory guide 5

The description section is the key to the correct placement of income and expenses in the accounts. Read the descriptions carefully and become familiar with the concept of why each expense should be in a particular category.

It is important to be specific about the allocation of expenses. Categories such as “Hardware”, “Tools”, “Farm Supplies”, and “Miscellaneous” should not be used at all. The items that have previously been put in these should be thought about carefully and put into the category that they actually relate to. This will mean that merchandise store accounts/invoices must be broken down expense by expense and allocated accordingly. You must ask yourself “what did I do with this item?” and allocate it accordingly.

For example, poly pipe fittings and a ball valve for a water trough would go into OVERHEADS sub REPAIRS & MAINTENANCE sub-sub STOCK WATER.

Other expenses that are usually not allocated properly are “Contractors” and “Cartage/Freight”.

If a payment is made to a “contractor”, then you need to work out what that contractor was paid to do and then allocate this expense accordingly. For example, if the contractor repaired fences then the expense goes into sub-sub ‘R&M Fencing’, under Sub category ‘Repairs and Maintenance’ within the ‘Overheads’ Category. If the contractor baled hay then the expense goes to sub-sub category Hay Making, under sub category Hay & Silage Making within the Home Grown Feed Costs category.

Similarly with cartage the expense needs to be allocated to the sub-category to which the expense applies. For example, the cartage for dry cows transported to agistment should be allocated to sub-sub category Dry Cows under sub category Agistment within the Purchased Feed Costs category.

To enable accurate evaluation of farm business performance the guide separates “farm income”, defined as “income generated by or directly related to the operation of the farm business”, from “off-farm income”. It also separates “farm expenses”, defined as “expenses directly related to the operation of the farm business”, from “off-farm expenses”.

Descriptions

Dairy Australia standard chart of accounts | Explanatory Guide 5

6

Whilst collecting the financial information is the most important component of a standard chart of accounts there are particular income and expense categories that require physical details for tax purposes and others where a quantity makes farm business analysis a more straightforward process. There is a column in the standard Chart of Accounts for the Key Physical Number whereby users can input these numbers both for tax purposes and any further analysis of their business.

For tax purposes dairy farmers are required to include the number of animals for both livestock sales and purchases as part of the overall livestock trading account whilst also recording the litres purchased for diesel for the diesel fuel rebate.

To enable any future farm business analysis it is also recommended that users collect physical details for feed and fertiliser whereby this information can be collected as tonnes dry matter, tonnes wet or in bales for feeds such as silage and hay.

It is also worthwhile collecting data such as megalitres for irrigation and the number of animal’s agisted.

Key physical number

Dairy Australia standard chart of accounts | Explanatory guide 7

Dairy farmers can choose the layout of the Chart of Accounts that best suits their business. It allows farmers to utilise the basic level 1 format with all the major categories or to step through to Level 3 which has a detailed breakdown of each category, sub- category and sub-sub category. Alternatively, farmers can also tailor the Chart of Accounts specifically to suit their business by electing to have sub-sub categories for some expenses whilst only have sub categories for others.

For example, you may elect to have sub-sub categories (Level 3) for all the Home Grown and Purchased feed costs whilst only having sub categories (level 2) for Herd and Shed Costs. The end result must still be that the expense or income concerned is in the sub-category that aligns with the correct category outlined in the standard Chart of Accounts.

For the Guide to be an effective record-keeping and/or comparative analysis tool, the main “Categories and sub-categories” should not be varied.

`

Options

8

The Standard Chart of Accounts has a suggested GST description for each sub-category. More than one description is suggested when the GST application differs according to the individual circumstances e.g. farm leases. Changes to GST legislation and application may occur. It is important to confirm your GST descriptions with your Accountant before allocating tax codes to your Chart of Accounts. A Y in the GST column indicates that GST is applicable where an N indicates the income or expense is GST free. A D indicates the income or expense item may incur GST or may be GST free depending on individual circumstances.

GST selection

Dairy business standard chart of accountsVersion 1.01

Key Physical

GST Number Description

1.0 Income All income associated with dairy farming activities

1.1 Milk Income Y Quantity Gross Milk Income – i.e Butterfat and Protein income, step-ups, retrospective payments and colostrums sales. Record other items on factory milk statement in appropriate income or expense categories or sub-categories not here under milk income

1.2 Livestock Sales Y Number Sales of stock from normal herd management practices, not from one-off sales such as major reductions as these are considered as CAPITAL INCOME sub SALES-BREEDERS.

1.2.1 Calves Y Number Bull calves, beef cross calves, heifer calves not kept for herd replacements

1.2.2 Culls Y Number Culled stock, chopper cows, heifers, bulls etc. culled and sold for slaughter

1.2.3 Other Livestock Sales Y Number Beef cattle, horses, bulls, breeding stock e.g. bulls, cows, heifers if they are regularly sold to others for use for breeding, milking, sires not stock from a major reduction sale or dispersal sale as these sales would be under CAPITAL INCOME

1.3 Feed Sales Y Quantity Sales of feed produced within the dairy business

1.3.1 Hay Sales Y Quantity Income from hay sales

1.3.2 Silage Sales Y Quantity Income from silage sales

1.3.3 Other Feed Sales Y Quantity Income from other feed sales such as grain

1.4 Water Sales Y ML Sales of water from normal water management practices, not from one-off sales such as major reductions as these are considered as CAPITAL INCOME

1.4.1 Temporary Y ML Sales of temporary water

1.4.2 Other Water Sales Y ML Income from any other water sales

1.5 Other Farm Income D Various sources of farm income resulting from farm operations

1.5.1 Interest N Interest received on farm operating bank accounts and short term deposits with bank accounts or factories and any other interest money received because of the operation of the farm business, not interest on off-farm or non-farm investments and personal bank account interest as these go in NON FARM INCOME

1.5.2 Contracting Y Income earned off-farm using the business farm machinery, equipment e.g. hay mower, hay roller, hay/silage processing

1.5.3 Milk Company Dividends D Factory, co-op dividends, not dividends from off farm or non-farm investments

1.5.4 Incentives N Trade incentives, discounts on purchases, vat purchase incentives

1.5.5 Leases D Cows, farming land, machinery etc. that is leased out to others

1.5.6 Rebates - Fuel D Fuel rebates

1.5.7 Rebates - Fertiliser D Fertiliser Rebates

1.5.8 Rebates - Other D Other rebates, including Semen, Factory or Volume Charge rebates

1.5.9 Government Payments N Government payments in the form of subsidies and support payments

1.5.10 Other Farm Income D Any other farm income resulting from farm operations such as farm house rental

2.0 Herd Costs All expenses relating to maintaining herd quality and assisting herd management2.1 AI & Herd Test Y All Artificial Insemination and Herd Test expenses

2.1.1 AI/Semen Y Artificial Insemination technician, semen, embryo, ET drugs, gloves, nitrogen for semen tank, vet services, fees and drugs associated with ET work, CIDR, PG and induction

2.1.2 Herd Test Y Herd test charges

2.1.3 Other Breeding Costs Y Tags for calves, heifers and cow identification, freeze branding of all classes of stock

2.2 Animal Health Y All Animal Health expenses including drugs and veterinary fees but excluding any AI expenses

2.2.1 Drugs Y Drench, drench guns, lice and parasite treatment and prevention – minerals and vitamins injected to all classes of stock – vaccines, injections (usually preventative) drugs and other treatments not restricted to purchase from vets

2.2.2 Veterinary Fees Y Vet visits, operations, drugs restricted to purchase from a Veterinary Surgeon or requiring Veterinary sanction

2.3 Calf Rearing Y Any expenses incurred for feeding, treating and maintaining calves up to the time they are weaned

2.3.1 Calf Feed Y Grain, pellets and growth promotants, for calves up to the time they are weaned

2.3.2 Milk Powder Y Milk powder and milk additives for calves up to the time they are weaned

2.3.3 Bedding Y Rice hulls or other bedding material

2.3.4 Other Calf Rearing Costs Y Drenching and other calf shed treatments for calves up to the time they are weaned

2.4 Other Herd Costs Y Short term lease of cows, heifers and bulls for periods of less than 12 months as these have a different tax implication to leases in excess of 12 months. Registrations, transfers, classifications, photos, show entry fees

3.0 Shed Costs All expenses relating to milk harvesting3.1 Shed Power Y Electricity, gas fuel for heating, cooling lighting milking

3.2 Dairy Supplies Y Chemicals, detergents used for washing, sterilizing, cleaning, fly control. Inflations, rubber tubes, filter socks, strainers, vacuum pump oil, isolated purchases of cups, claws and bowls etc.

3.3 Other Shed Costs Y

4.0 Home Grown Feed Costs All costs associated with growing feed on land under control of the business4.1 Fertiliser Y Quantity All NPKS and trace element fertiliser products and compounds including blending, mixing, cartage, bin hire and spreading

4.1.1 PKS Y Quantity All PKS and trace element fertiliser products and compounds including blending, mixing, cartage, bin hire and spreading

Dairy business standard chart of accountsVersion 1.01

Key Physical

GST Number Description

4.1.2 Urea Y Quantity All urea including cartage, bin hire and spreading

4.1.3 Nitrogen Blends Y Quantity All nitrogen blends including blending, mixing, cartage, bin hire and spreading

4.1.4 Lime & Gypsum Y Quantity Lime & Gypsum including blending, mixing, cartage, bin hire and spreading

4.1.5 Effluent Spreading/Disposal Y Costs associated with spreading effluent

4.1.6 Other Y Other fertiliser products

4.2 Irrigation Y All costs associated with irrigation in the dairy business but not new structures used in new land forming and pasture establishment as these major expenses should be entered into CAPITAL EXPENSES. Maintenance of Irrigation structures and physical channel cleaning should be entered in OVERHEADS sub REPAIRS & MAINTENANCE sub IRRIGATION

4.2.1 Water Authority Rates N Water rates for supply and drainage relating to farm irrigation water

4.2.2 TWE Purchases D Purchase of temporary water transfers in addition to water right or allocation

4.2.3 Pumping Costs - Electricity Y Electricity costs for pumping irrigation water

4.2.4 Pumping Costs - Diesel Y Diesel costs for pumping irrigation water

4.2.5 Other Irrigation Costs Y

4.3 Hay & Silage Making Y Costs for on-farm hay and silage making, including twine, plastic wrap and contractors

4.3.1 Hay Making Y Cutting, twine, net wrap, pressing, baling, hay inoculants, cartage on hay and freight on twine etc.

4.3.2 Silage Making Y Harvesting, transport, plastic wrap, pressing, baling, wrapping, chopping, covering, compacting contractors for silage, silage inoculants, cartage of silage purchases and freight on plastic covering etc

4.3.3 Crop Harvesting Y Harvesting and storage of crops including crop purchases and cartage and freight etc

4.3.4 Other Hay & Silage Making Costs Y Any other costs incurred in making hay and silage on farm

4.4 Pasture & Cropping Y Costs associated with pasture renovation and cropping such as seed, weed & pest and contractor costs. Not new land forming and the associated new pasture establishment as these major expenses should be entered under CAPITAL EXPENSE sub DEVELOPMENT

4.4.1 Seed Y Seed purchases

4.4.2 Weed & Pest Control Y Chemicals and contractors for the control of weeds and pests in pastures, roadsides and channels. Chemicals, baits, ammunition, contractors used to control vermin

4.4.3 Other Pasture & Cropping Costs Y Ploughing, ripping, discing, power harrowing, seedbed preparation, seed for crop and pasture sowing and pasture renovation, direct drilling contractor, oversowing and planting

4.5 Fuel & Oil Y Fuel used for vehicles, equipment, motors used for feed production

4.5.1 Diesel Y Litres Diesel costs except those for irrigation

4.5.2 Unleaded Y Unleaded petrol

4.5.3 Gas Y Gas

4.5.4 Oil/Grease Y Oil, grease

4.6 Other Feed Costs Y Includes any other feed costs that have not been included elsewhere here. These may include the cost of washing out or altering grain contracts and cartage costs not already accounted for

5.0 Purchased Feed Costs All purchased feeds including cartage, feed additives and agistment5.1 Concentrates Y Quantity Purchased concentrates (pellets, grain mixes etc)

5.1.1 Concentrate 1 Y Quantity Grain, grain mixes and pellets

5.1.2 Concentrate 2 Y Quantity Legumes and protein meals

5.1.3 Concentrate 3 Y Quantity

5.1.4 Concentrate 4 Y Quantity

5.1.5 Concentrate 5 Y Quantity

5.1.6 Concentrate 6 Y Quantity

5.2 Purchased Fodder Y Quantity Purchased fodder costs inluding hay and silage

5.2.1 Purchased Fodder 1 Y Quantity Hay purchases

5.2.2 Purchased Fodder 2 Y Quantity Silage Purchases

5.2.3 Purchased Fodder 3 Y Quantity Haylage Purchases

5.2.4 Purchased Fodder 4 Y Quantity

5.2.5 Purchased Fodder 5 Y Quantity

5.2.6 Purchased Fodder 6 Y Quantity

5.3 ByProducts Y Quantity Purchased byproducts

5.3.1 ByProduct 1 Y Quantity Brewers grain

5.3.2 ByProduct 2 Y Quantity Citrus Pulp

5.3.3 ByProduct 3 Y Quantity Other byproduct

5.3.4 ByProduct 4 Y Quantity

5.4 Other purchased feeds Y Any other purchased feed costs

5.4.1 Other purchased feed 1 Y Additives

5.4.2 Other purchased feed 2 Y

Dairy business standard chart of accountsVersion 1.01

Key Physical

GST Number Description

5.4.3 Other purchased feed 3 Y

5.4.4 Other purchased feed 4 Y

5.5 Agistment Y Number Agistment and short term land leases (less than 12 months), contract rearing of all classes of stock after weaning, cartage to and from agistment

5.5.1 Milkers Y Number Agistment or the purchase of standing feed grazed by the milking herd including cartage to and from the agistment should all be entered in this category

5.5.2 Dry Cows Y Number Agistment or the purchase of standing feed grazed by dry cows including cartage to and from the agistment should all be entered in this category

5.5.3 ReplacementY Number

Agistment, contract rearing, contract growing, weight gain agistment or the purchase of standing feed grazed by the replacements including cartage to and from the agistment should all be entered in this category

5.5.4 OtherY Number

Agistment, contract rearing, contract growing, weight gain agistment or the purchase of standing feed grazed by the other livestock including cartage to and from the agistment should all be entered in this category

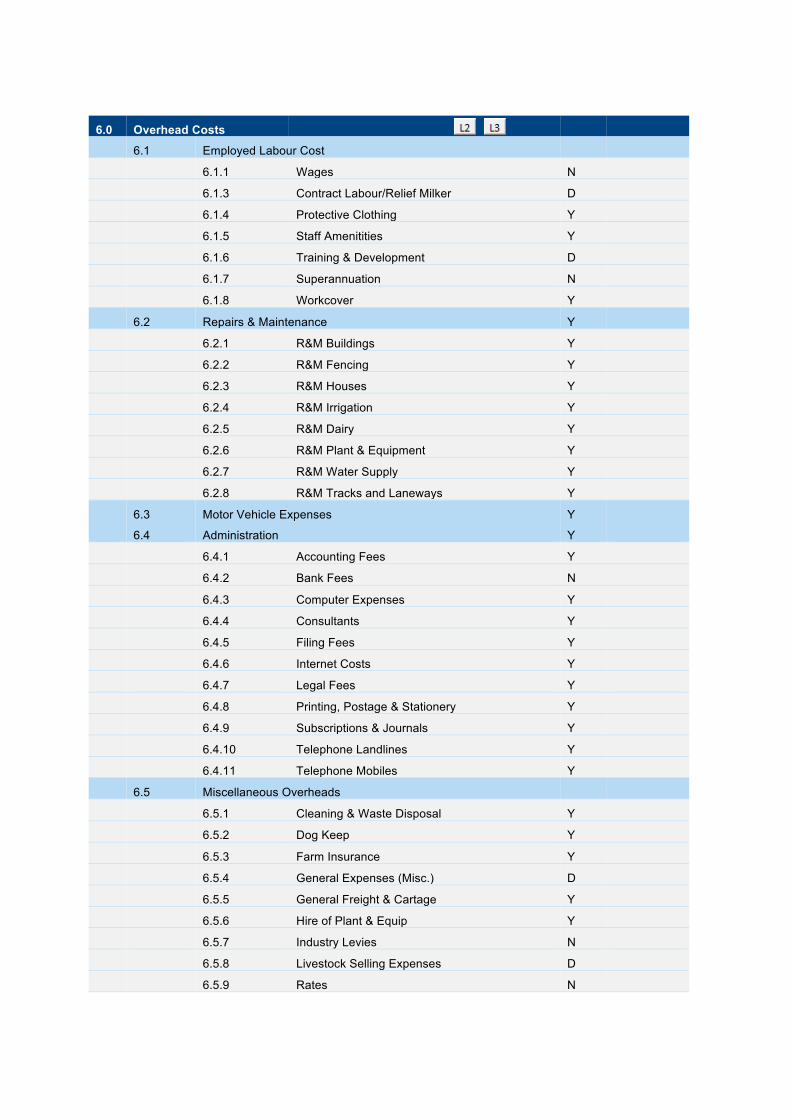

6.0 Overhead Costs Expenses related to the management of the farm business operation6.1 Employed Labour Cost Permanent labour and casual labour. Note: Contractors and contracting should be entered under the category that relates to the work carried out

6.1.1 Wages N Permanent farm employees either full-time or part-time and casual farm employees

6.1.2 Sharefarmer D Share paid to sharefarmer

6.1.3 Contract Labour/Relief Milker D

6.1.4 Protective Clothing Y Apron, gloves, Gum boots, waterproof clothes etc

6.1.5 Staff Amenitities Y Includes things like tea and coffee and light meals provided to staff

6.1.6 Training & Development D Fees for courses, seminars, workshops etc. that relate to the farm business (including travel, meals, accommodation, materials) for permanent and casual employees

6.1.7 Superannuation N Superannuation contributions for permanent and casual employees

6.1.8 Workcover Y Workcover for permanent and casual employees

6.2 Repairs & Maintenance Y Repairs and maintenance on farm improvements and plant and equipment this does not include capital improvements which should be entered under CAPITAL EXPENSES

6.2.1 R&M Buildings Y Maintenance of farm buildings and structures. The fixtures that would be considered to be part of the farm when/if it is sold

6.2.2 R&M Fencing Y Fencing contractors, yards, gates, insulators, gate tapes, fence reels, posts, wire, yard mesh, hinges, gate chains etc

6.2.3 R&M Houses Y Repairs to farm houses

6.2.4 R&M Irrigation Y Maintenance of irrigation structures and channel cleaning. Note:Structures used in new landforming and pasture establishment should be entered under CAPITAL EXPENSE sub DEVELOPMENT.

6.2.5 R&M Dairy Y Vat repair, platform repair, sludge pump repair

6.2.6 R&M Plant & Equipment Y Repairs and maintenance to farm equipment, plant and machinery

6.2.7 R&M Water Supply Y Repairs and maintenance of water troughs, poly pipe, pipe and trough fittings, pressure pumps for stock water supply

6.2.8 R&M Tracks and Laneways Y Repairs and maintenance to tracks and laneways

6.3 Motor Vehicle Expenses Y Motor vehicle expenses

6.3.1 Fuel & Oil Y Fuel and oil not directly related to the conservation or feeding of feed

6.3.2 R&M Servicing Y Repairs and maintenance on vehicles

6.3.3 Registrations N Registrations on farm vehicles

6.3.4 Vehicle Insurance Y Vehicle Insurance

6.4 Administration Y

6.4.1 Accounting Fees Y Professionals used for accounting advice in relation to the farm business

6.4.2 Bank Fees N Bank generated charges, account keeping fees, reference fee, stop cheque fee. Costs related to borrowing funds for farm use – Fees to establish farm related loans

6.4.3 Computer Expenses Y Computer expenses, including anti-virus software

6.4.4 Consultants Y Professionals used for financial,business management and production advice in relation to the farm business

6.4.5 Filing Fees Y Filing fees, including those paid to ASIC

6.4.6 Internet Costs Y Email and internet

6.4.7 Legal Fees Y Legal fees in relation to the farm business

6.4.8 Printing, Postage & Stationery Y Stationery, postage, printing, stamps, postal charges, post office box rental, envelopes, paper supplies, pens, pencils etc. for use in farm office

6.4.9 Subscriptions & Journals Y Farm Journals, Rural Newspapers and Magazines etc

6.4.10 Telephone Landlines Y Office and home landline

6.4.11 Telephone Mobiles Y Mobile phones

6.5 Miscellaneous Overheads

6.5.1 Cleaning & Waste Disposal Y Charges relating to rubbish removal and pickup

6.5.2 Dog Keep Y Food, drugs, veterinary attention, collars, chains for working dogs.

6.5.3 Farm Insurance Y Farm insurance package including stock, plant, fodder, buildings, sickness, accident and trauma insurance. Portion of house insurance as determined by your accountant

6.5.4 General Expenses (Misc.) D General farm expenses that do not fit within another expense code

6.5.5 General Freight & Cartage Y General freight & cartage not including to and from agistment which should be entered under Agistment

Dairy business standard chart of accountsVersion 1.01

Key Physical

GST Number Description

6.5.6 Hire of Plant & Equip Y Hire of plant and equipment

6.5.7 Industry Levies N DA levy, UDV Levy,

6.5.8 Livestock Selling Expenses D Government levies, Yard dues and Cartage

6.5.9 Rates N Shire rates and charges, domestic water rates where applicable. Note: Irrigation water rates are entered in FEED sub IRRIGATION sub WATER AUTHORITY RATES

7.0 Finance Costs Expenses relating to financing the operation of the business

7.1 Interest N Note: Interest – separate sub-categories should be set up for each loan or hire purchase. There should be a corresponding sub-category for the Principal portion for each loan or hire purchase under the CAPITAL EXPENSE category

7.1.1 Interest on Loans N Interest on major additions and/or alterations to the land, buildings, livestock, plant and equipment

7.1.2 Interest on Overdraft N Interest charged for overdraft on farm operating account, often shown as “debit interest” on bank statement and interest on any other bank accounts but not interest on loans as these are entered in their own category under INTEREST ON LOANS

7.1.3 Other Interest N Include any other interest paid here

7.2 Leases Leases over 12 months on land, water, livestock, plant & equipment

7.2.1 Leases Plant & Equipment D Leases on plant & equipment

7.2.2 Leases Livestock D Leases on livestock

7.2.3 Leases Land & Water D Leases on land and water

8.0 Capital Transactions Capital costs on items that are part of the management and development of the farm business8.1 Livestock Purchases Y Number Livestock purchases

8.1.1 Milkers Y Number Cow purchases

8.1.2 Replacements Y Number Replacement purchases

8.1.3 Bulls/Other Y Number Bulls or other stock purchases

8.2 Other Capital Purchases Y

8.2.1 Other Capital Purchase 1 Y Improvements: Major additions and/or alterations to the dairy building and dairy plant

8.2.2 Other Capital Purchase 2 Y Plant, Equipment & Vehicles: Tractor, mower, slasher etc. for use on the farm. Milk vat purchase. Farm related vehicles

8.2.3 Other Capital Purchase 3 Y Development: Land forming, recycle systems, pasture establishment and the associated irrigation structures, pumps, motors etc. Any major farm development or works

8.2.4 Other Capital Purchase 4 Y Land: Land purchased for use by the farm business

8.2.5 Other Capital Purchase 5 Y Water: HRWS,LRWS or bore water purchases

8.2.6 Other Capital Purchase 6 Y Share Equity: Factory share purchases, usually taken directly from milk receipts

8.2.7 Other Capital Purchase 7 Y Other capital purchases that relate to the dairy farm business

8.2.8 Farm Management Deposits N Cash amount despoited into FMDs

8.2.9 Farm Management Deposits - Withdrawals N FMDs that become available for use

8.2.10 Capital Introduced N Capital permanently introduced from non farm business activities

8.3 Capital Sales Sale of items that have a permanent impact on the balance sheet

8.3.1 Land Y Sale of land utilised in the dairy farm business

8.3.2 Permanent Water Y Sale of water utilised in the dairy farm business

8.3.3 Equipment /Machinery Y Sale of plant and equipment used in the dairy farm business

8.4 Loan Principal Repayments NLoan repayments. Note: Loan payments/Hire Purchases – if a loan or hire purchase exists on a capital expenditure item below, a separate sub-category should be set up for the Principal portion and defined as Principal or HP. e.g. HP DAIRY PLANT or PRINCIPAL LAND. There should be a corresponding sub-category for the Interest portion for each loan or hire purchase under the FINANCE sub INTEREST category. If a loan, the Loan Funds Received should also similarly be entered in CAPITAL INCOME sub LOANS in a corresponding sub-category name

8.4.1 Principal Payments - Loans N Principal repayments on loans

8.4.2 Principal Payments - HP's or CM's N Principal repayments on Hire Purchase or Chattel Mortgages

9.0 Non Farm Income N9.1 Wages N Wages, salaries earned by family members working off-farm.

9.2 Rent N Rent received

9.3 Personal Income N Personal income

9.4 Non farm Dividends N Dividends from off farm investments

10.0 Non Farm Operating Expenses Personal expenses that are not tax deductible. 10.1 Drawings 1 N

10.1.1 Living N

Dairy business standard chart of accountsVersion 1.01

Key Physical

GST Number Description

10.1.2 Education N

10.1.3 Insurance N

10.1.4 Medical N

10.2 Other Non Farm Expenses

10.3 Other Non Farm Expenses

11.0 Tax N11.1 GST N GST amounts

11.2 PAYG N Pay as you go tax

11.3 PAYG Withheld N Taxheld PAYG for permanent and casual employees

11.4 EOY N End of year tax

Dairy business standard chart of accounts – Example 1 – Detailed Breakdown

Key Physical

GST Number

1.0 Income

1.1 Milk Income Y Quantity

1.2 Livestock Sales Y Number

1.2.1 Calves Y Number

1.2.2 Culls Y Number

1.2.3 Other Livestock Sales Y Number

1.3 Feed Sales Y Quantity

1.4 Water Sales Y ML

1.5 Other Farm Income D

1.5.1 Interest N

1.5.2 Contracting Y

1.5.3 Milk Company Dividends D

1.5.4 Incentives N

1.5.5 Leases D

1.5.6 Rebates - Fuel D

1.5.7 Rebates - Fertiliser D

1.5.8 Rebates - Other D

1.5.9 Government Payments N

1.5.10 Other Farm Income D

2.0 Herd Costs

2.1 AI & Herd Test Y

2.1.1 AI/Semen Y

2.1.2 Herd Test Y

2.1.3 Other Breeding Costs Y

2.2 Animal Health Y

2.2.1 Drugs Y

2.2.2 Veterinary Fees Y

2.3 Calf Rearing Y

2.4 Other Herd Costs Y

3.0 Shed Costs

3.1 Shed Power Y

3.2 Dairy Supplies Y

3.3 Other Shed Costs Y

4.0 Home Grown Feed Costs

4.1 Fertiliser Y Quantity

4.1.1 PKS Y Quantity

4.1.2 Urea Y Quantity

4.1.3 Nitrogen Blends Y Quantity

4.1.4 Lime & Gypsum Y Quantity

4.1.5 Effluent Spreading/Disposal Y

4.1.6 Other Y

4.2 Irrigation Y

4.3 Hay & Silage Making Y

4.4 Pasture & Cropping Y

4.4.1 Seed Y

4.4.2 Weed & Pest Control Y

4.4.3 Other Pasture & Cropping Costs Y

4.5 Fuel & Oil Y

4.5.1 Diesel Y Litres

4.5.2 Unleaded Y

4.5.3 Gas Y

4.5.4 Oil/Grease Y

4.6 Other Feed Costs Y

5.0 Purchased Feed Costs

5.1 Concentrates Y Quantity

5.1.1 Wheat Y Quantity

5.1.2 Canola Meal Y Quantity

5.1.3 Lupins Y Quantity

5.1.4 Classic Dairy Pellets Y Quantity

5.2 Purchased Fodder Y Quantity

5.2.1 Vetch Hay Y Quantity

5.2.2 Oaten Hay Y Quantity

5.2.3 Maize Silage Y Quantity

5.4 Other purchased feeds Y

5.4.1 Minerals Y

5.5 Agistment Y Number

5.5.2 Dry Cows Y Number

5.5.3 Replacements Y Number

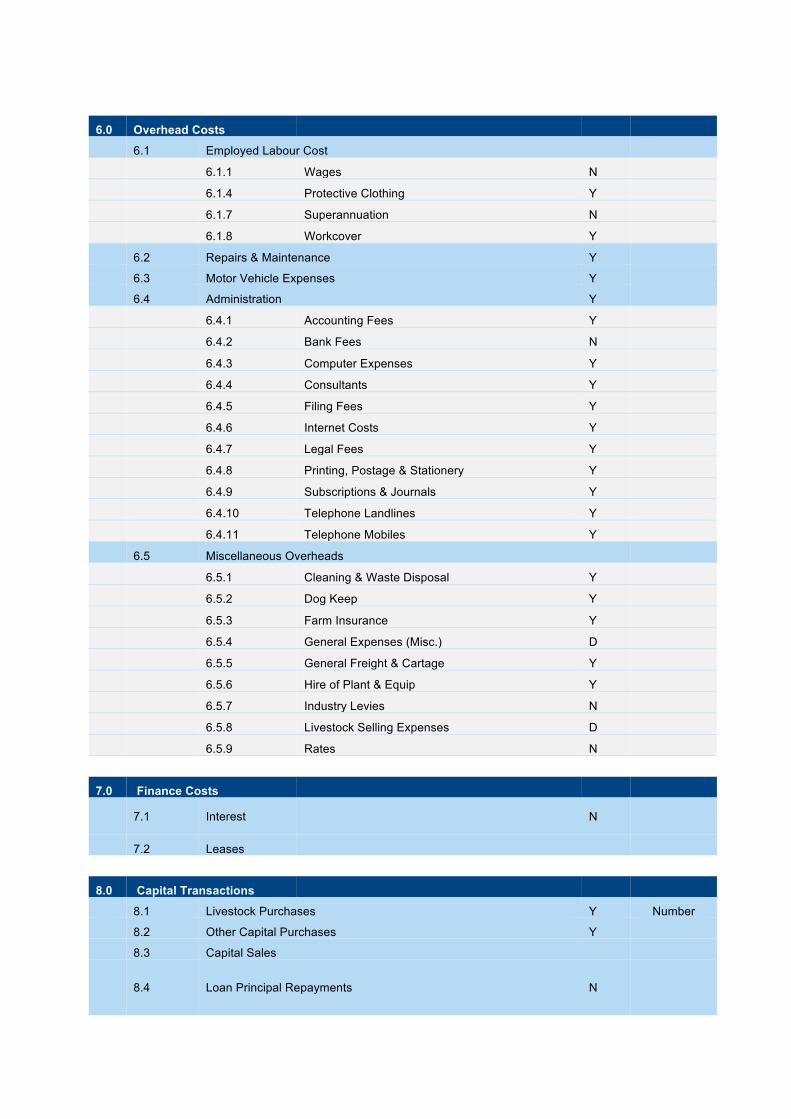

6.0 Overhead Costs

6.1 Employed Labour Cost

6.1.1 Wages N

6.1.3 Contract Labour/Relief Milker D

6.1.4 Protective Clothing Y

6.1.5 Staff Amenitities Y

6.1.6 Training & Development D

6.1.7 Superannuation N

6.1.8 Workcover Y

6.2 Repairs & Maintenance Y

6.2.1 R&M Buildings Y

6.2.2 R&M Fencing Y

6.2.3 R&M Houses Y

6.2.4 R&M Irrigation Y

6.2.5 R&M Dairy Y

6.2.6 R&M Plant & Equipment Y

6.2.7 R&M Water Supply Y

6.2.8 R&M Tracks and Laneways Y

6.3 Motor Vehicle Expenses Y

6.4 Administration Y

6.4.1 Accounting Fees Y

6.4.2 Bank Fees N

6.4.3 Computer Expenses Y

6.4.4 Consultants Y

6.4.5 Filing Fees Y

6.4.6 Internet Costs Y

6.4.7 Legal Fees Y

6.4.8 Printing, Postage & Stationery Y

6.4.9 Subscriptions & Journals Y

6.4.10 Telephone Landlines Y

6.4.11 Telephone Mobiles Y

6.5 Miscellaneous Overheads

6.5.1 Cleaning & Waste Disposal Y

6.5.2 Dog Keep Y

6.5.3 Farm Insurance Y

6.5.4 General Expenses (Misc.) D

6.5.5 General Freight & Cartage Y

6.5.6 Hire of Plant & Equip Y

6.5.7 Industry Levies N

6.5.8 Livestock Selling Expenses D

6.5.9 Rates N

7.0 Finance Costs

7.1 Interest N

7.2 Leases

8.0 Capital Transactions

8.1 Livestock Purchases Y Number

8.1.1 Milkers Y Number

8.1.2 Replacements Y Number

8.1.3 Bulls/Other Y Number

8.2 Other Capital Purchases Y

8.3 Capital Sales

8.4 Loan Principal Repayments N

9.0 Non Farm Income N

9.1 Wages N

9.2 Rent N

9.3 Personal Income N

9.4 Non farm Dividends N

10.0 Non Farm Operating Expenses

10.1 Drawings 1 N

10.1.1 Living N

10.1.2 Education N

10.1.3 Insurance N

10.1.4 Medical N

10.2 Other Non Farm Expenses

10.3 Other Non Farm Expenses

11.0 Tax N

11.1 GST N

11.2 PAYG N

11.3 PAYG Withheld N

11.4 EOY N

Dairy business standard chart of accounts – Example 2

Key Physical

GST Number

1.0 Income

1.1 Milk Income Y Quantity

1.2 Livestock Sales Y Number

1.3 Feed Sales Y Quantity

1.4 Water Sales Y ML

1.5 Other Farm Income D

1.5.1 Interest N

1.5.3 Milk Company Dividends D

1.5.6 Rebates - Fuel D

2.0 Herd Costs

2.1 AI & Herd Test Y

2.2 Animal Health Y

2.3 Calf Rearing Y

2.4 Other Herd Costs Y

3.0 Shed Costs

3.1 Shed Power Y

3.2 Dairy Supplies Y

3.3 Other Shed Costs Y

4.0 Home Grown Feed Costs

4.1 Fertiliser Y Quantity

4.2 Irrigation Y

4.3 Hay & Silage Making Y

4.4 Pasture & Cropping Y

4.5 Fuel & Oil Y

4.6 Other Feed Costs Y

5.0 Purchased Feed Costs

5.1 Concentrates Y Quantity

5.2 Purchased Fodder Y Quantity

5.3 ByProducts Y Quantity

5.4 Other purchased feeds Y

5.5 Agistment Y Number

6.0 Overhead Costs

6.1 Employed Labour Cost

6.1.1 Wages N

6.1.4 Protective Clothing Y

6.1.7 Superannuation N

6.1.8 Workcover Y

6.2 Repairs & Maintenance Y

6.3 Motor Vehicle Expenses Y

6.4 Administration Y

6.4.1 Accounting Fees Y

6.4.2 Bank Fees N

6.4.3 Computer Expenses Y

6.4.4 Consultants Y

6.4.5 Filing Fees Y

6.4.6 Internet Costs Y

6.4.7 Legal Fees Y

6.4.8 Printing, Postage & Stationery Y

6.4.9 Subscriptions & Journals Y

6.4.10 Telephone Landlines Y

6.4.11 Telephone Mobiles Y

6.5 Miscellaneous Overheads

6.5.1 Cleaning & Waste Disposal Y

6.5.2 Dog Keep Y

6.5.3 Farm Insurance Y

6.5.4 General Expenses (Misc.) D

6.5.5 General Freight & Cartage Y

6.5.6 Hire of Plant & Equip Y

6.5.7 Industry Levies N

6.5.8 Livestock Selling Expenses D

6.5.9 Rates N

7.0 Finance Costs

7.1 Interest N

7.2 Leases

8.0 Capital Transactions

8.1 Livestock Purchases Y Number

8.2 Other Capital Purchases Y

8.3 Capital Sales

8.4 Loan Principal Repayments N

9.0 Non Farm Income N

9.1 Wages N

9.2 Rent N

9.3 Personal Income N

9.4 Non farm Dividends N

10.0 Non Farm Operating Expenses

10.1 Drawings 1 N

10.2 Other Non Farm Expenses

10.3 Other Non Farm Expenses

11.0 Tax N

11.1 GST N

11.2 PAYG N

11.3 PAYG Withheld N

11.4 EOY N

Dairy Australia Limited ABN 60 105 227 987

Level 5, IBM Centre60 City Road, Southbank VIC 3006 AustraliaT + 61 3 9694 3777 F + 61 3 9694 3701E [email protected]

0357

| A

ug 2

015