chevron corporation - washburn · pdf filechevron billie jean bergmann jacob krause the...

TRANSCRIPT

Student Investment Fund Stock Report Analysts: Billie Jean Bergmann & Jacob Krause

HIGHLIGHTS

CVX is the world's largest producer of geothermal energy1.

CVX is diversifying their sources of energy in order to meet the world's growing demand in an environmentally sound way.

CVX is diversified geographically with operations in over 100 countries worldwide.

CVX’s investment in new technology and renewable energy initiatives ensure future stability and growth in revenues and profits.

CVX's efforts to protect the environment were recognized in 2008 with awards from the National Ocean Industries Association and the California Department of Oil, Gas and Geothermal Resources.

Recommendation: BUY

Market Cap: $132.3 B

Chevron Corporation NYSE: CVX

Recent Price: $66.87 (05/01/09)

Target Price: $79.11

Sector: Energy

Sub‐Sector: Integrated Oil & Gas

BUSINESS SUMMARY Chevron Corporation is one of the world's largest integrated energy companies. The company is headquartered in San Ramon, California and conducts business in more than 100 countries. CVX is engaged in every aspect of the crude oil and natural gas industry, including exploration and production, manufacturing, marketing and transportation, chemical manufacturing and sales, geothermal and power generation. CVX is a world leader in renewable energy investment and advanced energy technology. Chevron’s commitment to technological development provides ways that help the business increase energy efficiency. CVX is taking steps to form partnerships to help improve the overall quality of life and health of people in emerging markets.

INVESTMENT THESIS

Growth in worldwide energy consumption is increasing the need to develop innovative sources of renewable energy and additional supplies of traditional energy. CVX is strategically positioned and diversified to meet the world’s growing demand for renewable and traditional energy.

CVX has a strong historical and projected dividend growth compared to its key competitors, evidenced by its steady and consistent growth in free cash flow per share and 21 consecutive years of growing dividends.

ROA, ROE, and ROIC are all sufficiently high to ensure CVX remains on pace for shareholder value creation in the long term, even if the company’s future operating environment becomes more challenging than it’s been in the recent past.

Our conservative model projects a relatively small spread between the ROIC and WACC, but one that is consistent with long‐term value creation.

FINANCIAL STATISTICS VS. SELECTED COMPETITORS & INDUSTRY

Metric CVX XOM COP Industry S&P 500

ROA, 5‐Yr. Avg. 13.5% 17.7% 5.8% 11.4% 8.4%

ROE, 5‐Yr. Avg. 26.4% 34.5% 10.6% 22.1% 20.4%

ROIC, 5‐Yr. Avg. 22.4% 25.4% 11.9% 15.1% 11.3%

DPS, 2008 $2.52 $1.55 $1.87 ‐ ‐

FCF/share, 5‐Yr. Avg. $3.67 $6.35 ($0.28) ‐ ‐

EPS, 2008 $11.72 $9.14 ($10.42) ‐ ‐

5‐YR Insider Selling $262 M $432 M $96 M ‐ ‐

ONE‐YEAR PRICE PERFORMANCE

CVX has outperformed the S&P 500 in the past year.

1. A renewable resource that generates reliable power while producing virtually no greenhouse gas emissions.

S&P 500

CVX

Chevron Billie Jean Bergmann

Jacob Krause

MACROECONOMIC THESIS Worldwide energy consumption is projected to rise more than 50% by 2030, fueled by growth in the global

population. Higher energy demand will be driven by rapid growth rates in emerging economies such as China

and India, which will continue to develop into more energy‐hungry economies (similar to the United States

and Europe).

Energy demand will rise with economic output and improved standards of living, which in turn will put

added pressure on energy supplies. As economies become increasingly industrialized they drive their cars

more each year and live in houses that are equipped with an increasing array of energy‐demanding appliances,

computers and other conveniences.

The combined aspects listed above will lead to an increase in the need to develop innovative, renewable

energy sources and additional supplies of traditional energy. Even if the use of renewable energy supplies

double or triple over the next 25 years, the world will still depend on fossil fuels for as much as 85% of its

energy needs. (Projections reported by the National Petroleum Council)

President Obama’s plan to cut $35 billion in U.S. oil preferences over the next 10 years will have little effect on Chevron’s revenues due to the company’s geographic diversification and strategic positioning, which is further discussed below in the global presence section.

BUSINESS SEGMENTS CVX's Upstream segment (26.9% of 2008 total sales revenue) includes the exploration, production and sale of crude oil and natural gas. Earnings for the upstream segment closely follow industry price levels for crude oil and natural gas. Crude oil and natural gas prices are subject to external factors over which the company has no control, including product supply and demand connected with global economic conditions and industry inventory levels. Besides the impact of the fluctuation in prices for crude oil and natural gas, the longer‐term trend in earnings for the upstream segment is also a function of other factors, including the company’s ability to find, acquire and efficiently produce crude oil and natural gas; changes in fiscal terms of contracts; changes in tax rates on income; and the cost of goods and services. The United States accounted for 46.9% of upstream sales revenues in 2008; whereas, international sales accounted for 53.1% of upstream revenues. CVX's Downstream segment (71.8% of 2008 total sales revenues) includes refining and marketing of petroleum products and other products derived from crude oil. Additionally, it includes the transportation of products. Earnings for the downstream segment are closely tied to margins on the refining and marketing of products such as gasoline, diesel and jet fuel, lubricants, fuel oil and feedstock for chemical manufacturing.

Chevron Billie Jean Bergmann

Jacob Krause

The energy industry's margins are often volatile, and can be affected by the global and regional supply and demand balance for refined products and by changes in the price of crude oil used for refinery feedstock. Industry margins can also be influenced by refined‐product inventory levels, geopolitical events, refinery maintenance programs and disruptions at refineries resulting from unplanned outages due to severe weather or other operational events. Other factors affecting profitability for downstream operations include the reliability and efficiency of CVX’s refining and marketing network, the effectiveness of the crude oil and product supply functions and the economic returns on invested capital. Profitability can also be affected by the volatility of tanker‐charter rates for the company’s shipping operations, which are driven by the industry’s demand for crude oil and product tankers. Other factors beyond the company’s control include the general level of inflation and energy costs to operate the company’s refinery and distribution network. The company’s most significant marketing areas are the West Coast of North America, the U.S. Gulf Coast, Latin America, Asia, Southern Africa and the United Kingdom. In 2008, 42.2% of downstream sales revenues were based in the United States with international sales accounting for 57.8% of downstream sales revenues. CVX's Chemicals segment (0.7% of 2008 total sales revenues) includes the manufacture and sale of additives for lubricants and fuel. Chevron’s 50‐50 joint venture, Chevron Phillips Chemical Company LLC, is one of the world’s leading manufacturers of commodity petrochemicals. Chevron Oronite markets more than 500 performances enhancing products and supplies, which is ¼ of the world’s fuel and lubricant additives. Earnings in the petrochemicals business are closely tied to global chemical demand, industry inventory levels and plant capacity utilization. Feedstock and fuel costs, which tend to follow crude oil and natural gas price movements, also influence earnings in this segment. In 2008, United States sales accounted for 26.4% of sales revenues in CVX’s chemicals segments, with 73.6% of the sales revenues driven by international markets. CVX's Other Businesses segment (0.6% of 2008 total sales revenues) includes coal mining operations, power generation businesses, insurance operations, real estate activities and technology companies. 95.3% of the other businesses revenues were based in the United States; 4.7% of the sales revenues were international.

Other Business

FY2008

Sales $1.82B

0.6% of Total Sales

13.1% Growth from 2007

Downstream

FY2008

Sales $219.94B

71.8% of Total Sales

23.4% Growth from 2007

Upstream

FY2008

Sales $82.32B

26.9% of Total Sales

26.2% Growth from 2007

Chemicals

FY2008

Sales $2.17B

0.7% of Total Sales

10.8% Growth from 2007

Chevron Billie Jean Bergmann

Jacob Krause

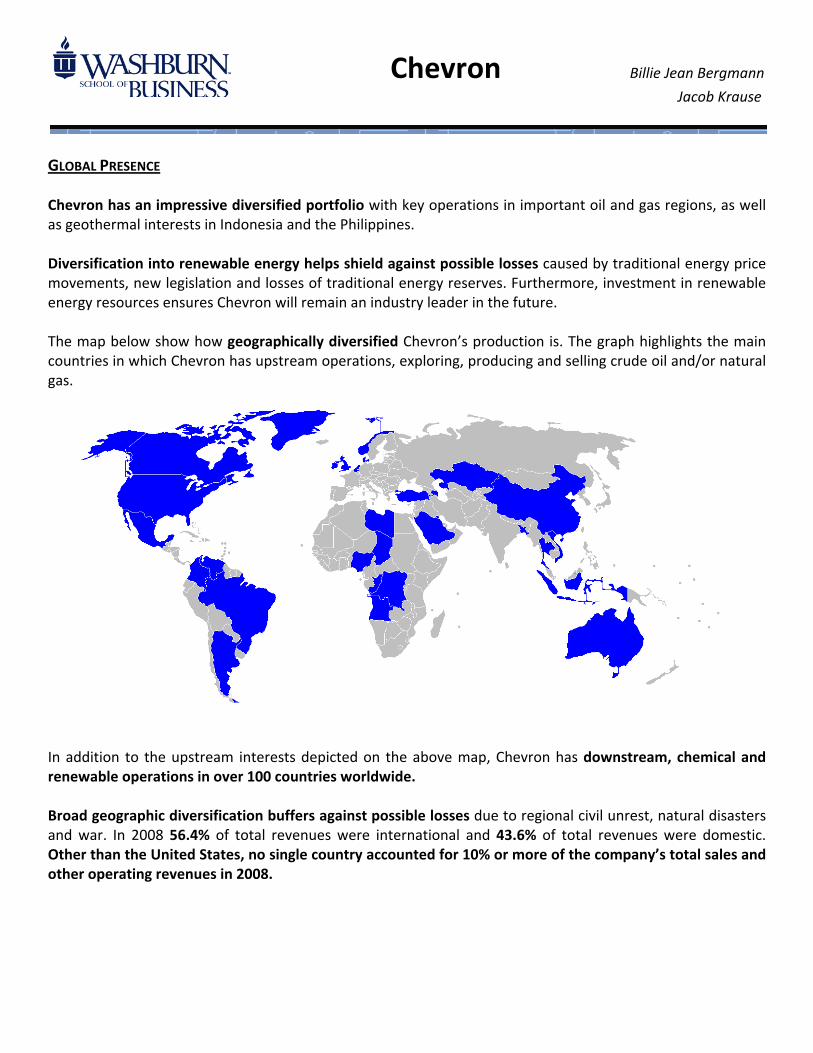

GLOBAL PRESENCE Chevron has an impressive diversified portfolio with key operations in important oil and gas regions, as well as geothermal interests in Indonesia and the Philippines. Diversification into renewable energy helps shield against possible losses caused by traditional energy price movements, new legislation and losses of traditional energy reserves. Furthermore, investment in renewable energy resources ensures Chevron will remain an industry leader in the future. The map below show how geographically diversified Chevron’s production is. The graph highlights the main countries in which Chevron has upstream operations, exploring, producing and selling crude oil and/or natural gas.

In addition to the upstream interests depicted on the above map, Chevron has downstream, chemical and renewable operations in over 100 countries worldwide. Broad geographic diversification buffers against possible losses due to regional civil unrest, natural disasters and war. In 2008 56.4% of total revenues were international and 43.6% of total revenues were domestic. Other than the United States, no single country accounted for 10% or more of the company’s total sales and other operating revenues in 2008.

Chevron Billie Jean Bergmann

Jacob Krause

VALUATION Our valuation model analyzes CVX's historical financials (2004‐2008) and explicitly forecasts all income statement and balance sheet items as a percent of sales over a 10 year horizon (model shown in appendix). Using conservative assumptions, a discounted cash flow (DCF) model suggests that CVX is slightly undervalued. The model returns a fair value of $79.11 for 2009 and supports a 12‐month target price of $86.61. CVX’s closing price on May 01, 2009 was $66.87. Our model suggests that CVX’s DCF price could grow as high as $169.81 by 2018 (11.05% annual returns, in addition to the stock's 3.9% dividend yield). Inputs:

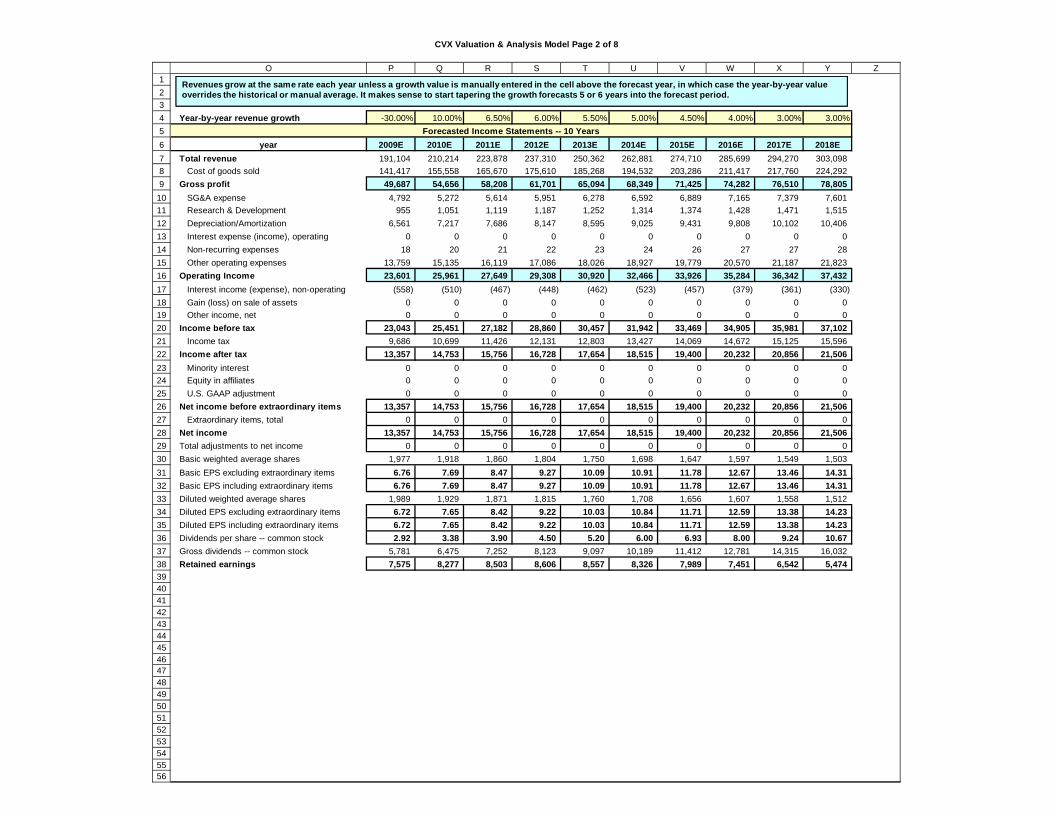

Revenue growth is modeled on a year‐by‐year basis to better reflect CVX’s prospects (see technical appendix). Despite CVX’s historical 5‐year growth rate average of 15.1%, the revenue growth forecast we used forecasted a decline in energy demand due to the global economic downturn and the volatility of prices in the industry. Our average 10‐year projected growth rate is therefore a conservative 5.26%. Revenues are projected to grow ‐30% in 2009, 10% in 2010, 6.5% in 2011, 6% in 2012, 5.5% in 2013, 5% in 2014, 4.5% in 2015, 4% in 2016 and then taper off to a long‐term sustainable rate of 3% in 2017 and beyond. Our long‐term forecasted growth rate of 3% is significantly more conservative than Thomson‐Reuters and the analysts' consensus, both of whom project a long‐term growth of 7%.

Cost of Goods Sold was conservatively forecasted to be slightly higher than the 5‐year average of 74%, contrary to the historical decline in COGS and further predicted decline in costs (Argus Research). Our forecast assumes that higher input costs will accompany the global economic recovery.

Other Operating Expenses are adjusted 0.3% higher from the historical average. CVX has a historical trend of slightly increasing other expenses. By adjusting the expenses above the historical average to 7.2% our forecast continues a trend that offsets future increases in operating expenses.

Share Growth/Diluted Share Growth is set at ‐3.0%, which is lower than the historical average of ‐0.9%. CVX has historically bought back shares, as represented in the negative historical average. The ‐3.0%% rate ensures that earnings per share and intrinsic value per share are modeled conservatively.

Dividend growth is adjusted down 0.4% from the historical average. CVX has a recent trend of a slower dividend growth. The 12.0% dividend growth rate reflects CVX's historical commitment to growing dividends faster than peer firms such as Exxon‐Mobil and Conoco‐Phillips.

Net Property Plant and Equipment is modeled on a year‐by‐year basis to better reflect CVX’s net PPE as a percent of sales. We anticipate that future exploration of oil will be more capital intensive. Therefore, we based our PPE projections off of historic growth in PPE/Sales. The historic growth from 2005‐2008 in PPE/Sales is 13.0%. To keep our model conservative and account for the impact the projected ‐30.0% revenue growth in 2009 had on PPE/Sales we projected a 7.0% increase in Net PPE year‐by‐year out to 2015. Forecasted year‐by‐year PPE/Sales, 51.39% in 2009, 49.99% in 2010, 50.22% in 2001, 50.70% in 2012, 51.42% in 2013, 52.40% in 2014, 52.50% in 2015 and 2016, and holding the PPE/Sales at 53.00% in 2017 and 2018. The historical average of 32.5% compared to the forecasted average of 51.71% shows our large increase in Net PPE.

Chevron Billie Jean Bergmann

Jacob Krause

Cash is modeled slightly higher than the historical average. Although CVX’s cash/sales have been decreasing, we increased the cash to help keep our model conservative and compress forecasted ROIC.

Receivables are modeled slightly lower than the historical average. CVX’s receivables/sales have declined significantly recently from 10.2% in 2007 to 5.8% in 2008. CVX is reducing the amount held in receivables; therefore, we forecasted receivables/sales lower than the historical average.

WACC and Beta. The model uses a WACC at 10.40%. Our estimates of CVX's historical beta vs. the S&P 500 was 0.84. We used a much higher beta of 1.15 to allow for reversion to the mean and possible increases in the volatility of CVX’s stock price. The higher beta increases the cost of capital, which compresses the value of the stock price. The cost of capital was calculated using a risk‐free rate of 4%, which is higher than the current rate of 2.75%, and market risk premium of 6%.

PROFITABILITY

Margins. The forecast model projects no growth in margins over the 10‐year forecast period. This helps to compensate for some of the current economic uncertainty. CVX has shown average Gross, Operating and Net Profit Margins for 2004‐2008 of 27.9%, 14.5%, and 8.4%, respectively. When we employ conservative forecasting assumptions the average forecasted margins compress to 26% for Gross Margins, 12.3% for Operating Margins and 7.1% for Net Profit Margins.

Dividends Per Share. One of the key factors in choosing a mega‐oil stock was the ability of a company to grow its dividends. CVX’s potential to grow DPS is substantially better than its key competitors due to CVX’s ability to steadily and consistently grow their FCF per share. Even with conservative assumptions, CVX has the ability to grow its dividend as high as $10 per share in the long term, whereas their key competitors cannot, which benefits the tax‐free status of the student investment fund. Historical Avg Forecasted Avg $2.01 $6.04

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

Dividends Per Share

XOM CVX COP

0%

5%

10%

15%

20%

25%

30%

35%

Gross Margin Operating Margin Net Margin

Chevron Billie Jean Bergmann

Jacob Krause

Free Cash Flow Per Share. The stability in FCF per share supports CVX’s ability to grow its dividends. XOM’s FCF/Share is higher historically, and COP’s has the chance to be higher in the future, but CVX’s FCF/Share has undeniable stability that suits our selection criteria for a big oil stock, as shown in the historic average of $3.67 per share and forecasted average of $6.46 per share.

Historical Avg Forecasted Avg

$3.67 $6.46

Return on Assets, Return on Equity and Return on Invested Capital. CVX has earned strong and sustainable ROA, ROE and ROIC for 2004‐2008, with an average of 13.5%, 26.4%, and 22.4%, respectively. In employing conservative forecasting assumptions, these metrics compress to 13‐14% for ROE and ROIC and 9% for ROA. The forecasted averages are all sufficiently high enough to ensure CVX remains on pace for shareholder value creation in the long term, even if the company’s future operating environment becomes more challenging than it’s been in the recent past.

Historical Avg Forecasted Avg ROA 13.5% 8.8% ROE 26.4% 13.7% ROA 22.4% 12.9%

($10)

($5)

$0

$5

$10

$15

$20 Free Cash Flow Per Share

XOM CVX COP

0%

5%

10%

15%

20%

25%

30%

35%

Return on Assets Return on Equity Return on Invested Capital

Chevron Billie Jean Bergmann

Jacob Krause

VALUE CREATION METRICS

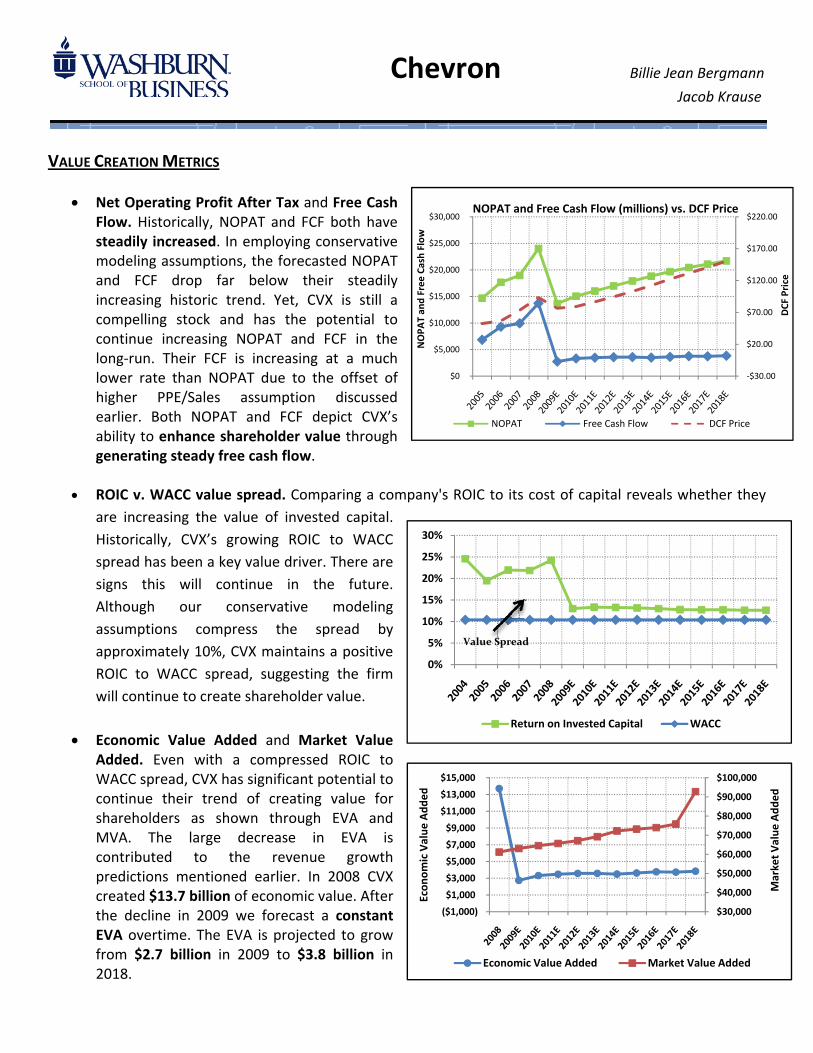

Net Operating Profit After Tax and Free Cash Flow. Historically, NOPAT and FCF both have steadily increased. In employing conservative modeling assumptions, the forecasted NOPAT and FCF drop far below their steadily increasing historic trend. Yet, CVX is still a compelling stock and has the potential to continue increasing NOPAT and FCF in the long‐run. Their FCF is increasing at a much lower rate than NOPAT due to the offset of higher PPE/Sales assumption discussed earlier. Both NOPAT and FCF depict CVX’s ability to enhance shareholder value through generating steady free cash flow.

ROIC v. WACC value spread. Comparing a company's ROIC to its cost of capital reveals whether they

are increasing the value of invested capital.

Historically, CVX’s growing ROIC to WACC

spread has been a key value driver. There are

signs this will continue in the future.

Although our conservative modeling

assumptions compress the spread by

approximately 10%, CVX maintains a positive

ROIC to WACC spread, suggesting the firm

will continue to create shareholder value.

Economic Value Added and Market Value Added. Even with a compressed ROIC to WACC spread, CVX has significant potential to continue their trend of creating value for shareholders as shown through EVA and MVA. The large decrease in EVA is contributed to the revenue growth predictions mentioned earlier. In 2008 CVX created $13.7 billion of economic value. After the decline in 2009 we forecast a constant EVA overtime. The EVA is projected to grow from $2.7 billion in 2009 to $3.8 billion in 2018.

‐$30.00

$20.00

$70.00

$120.00

$170.00

$220.00

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

DCF Price

NOPAT an

d Free Cash Flow

NOPAT and Free Cash Flow (millions) vs. DCF Price

NOPAT Free Cash Flow DCF Price

0%

5%

10%

15%

20%

25%

30%

Return on Invested Capital WACC

Value Spread

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

($1,000)

$1,000

$3,000

$5,000

$7,000

$9,000

$11,000

$13,000

$15,000 Market Value Added

Economic Value Added

Economic Value Added Market Value Added

Chevron Billie Jean Bergmann

Jacob Krause

CVX had a MVA of $61.2 billion in 2008. Our projections show steady increase overtime from $63.1 billion to $92.8 billion. This evidences CVX’s ability to create value for the market beyond the value of contributed capital as Chevron effectively controls and manages its assets.

RELATIVE VALUATION

We do not just rely on one valuation metric to measure the intrinsic market value of price. We also look at the historic valuation multiples which include:

o Price/Sales o Price/EBITDA o Enterprise Value/EBITDA o Price/Earnings

We compressed the historic multiples and compare forecasted multiple prices to our estimated DCF valuation. Our DCF price tracks closer to the extrapolated multiples prices, which shows the DCF share price is consistent with the multiples value estimates, which often reflects the market price.

Current Price/Earnings, Price/Sales, Enterprise Value/EBITDA and Price/Book indicated that CVX is priced at a slightly lower premium compared to XOM, suggesting favorable relative valuation compared to competitors and the industry.

INSIDER SELLING

An additional metric we look at is the pattern of

net insider purchases/sales. We prefer companies

where executives are heavily invested in their own

stock. The net insider selling strongly favors CVX

over XOM. Since 2004, XOM's insiders have

divested roughly $432 million, whereas CVX's

insiders have divested only $262 million.

Relative Valuation CVX XOM COP Industry

P/E Ratio 6.53 8.94 ‐5.26 6.60

Price/Sales 0.57 0.88 0.34 0.63

Value/EBITDA 2.97 4.17 17.02 ‐

Price/Book 1.54 2.93 ‐ 1.59

$20 $30 $40 $50 $60 $70 $80 $90 $100 $110 $120 $130 $140 $150 $160 $170 $180

Forecasted Value Per Share

Forecasted Per Share Stock Values

Low Price DCF Price High Price

($525,000)

($450,000)

($375,000)

($300,000)

($225,000)

($150,000)

($75,000)

$0

Net Insider Tran

sactions

Net Insider Purchases (Sales) , $, in thousands

XOM CVX

Chevron Billie Jean Bergmann

Jacob Krause

RISKS

There is no stock in the current environment where everything is positive. Some risks we are concerned with include:

Governmental policies regulating how companies are structured and where and how companies conduct their operations and formulate their products, which could hinder CVX’s ability to outperform their competitors. Government imposed price controls on refined products such as gasoline or diesel fuel could have an adverse effect on the operations of CVX. Strained relations between the government and CVX may also impact the company’s operations.

Change in prices, which are generally determined by the supply and demand of oil could adversely impact operations. OPEC production levels are the major factor in determining worldwide supply of oil. Demand driven by the condition of local, national, and global economies, weather patterns and taxation relative to other energy sources can have an adverse effect on the price of oil.

A longer recession than forecasted could continue to put downward pressure on oil and gas prices.

Production and distribution disruptions from either natural or human causes could have an adverse effect on the operations of CVX. Hurricanes, floods, fire, earthquakes, and other forms of severe weather would impact CVX’s ability to generate future revenues. Additionally, war, civil unrests, acts of violence, and other political events could adversely impact CVX’s operations.

If Chevron is not successful in replacing the crude oil and natural gas it produces with good prospects for future production, the company’s business will decline. Creating and maintaining new projects depends on many factors including: obtaining and renewing rights to explore, developing and producing hydrocarbons, drilling success, ability to bring long‐lead‐time, capital‐intensive projects to completion on budget and schedule, and efficient and profitable operation of mature properties.

Activities that could result in liability, either as a result of an accidental, unlawful discharge or as a result of new conclusions on the effects of the company’s operations on human health or the environment.

Regulation of greenhouse gas emissions could increase CVX’s operational costs and reduce the demand for CVX’s products.

The risk we are most concerned with is an ongoing environmental damage lawsuit filed by Ecuador. Chevron management cannot currently estimate a range of possible loss from the case, but believes the case lacks legal and factual merit and plans to fight it. Chevron has also recently hired William “Jim” Haynes II, who ran one of the largest law departments in the U.S. federal government. We feel the addition of his world‐class legal talent and leadership will ensure minimal loss to the company.

Chevron Billie Jean Bergmann

Jacob Krause

OWNERSHIP CVX’s institutional & mutual fund ownership is 64%. Top holders summarized below.

TOP INSTITUTIONAL HOLDERS Holder Shares % Out Value Reported

STATE STREET CORPORATION 103,764,672 5.18 $7.68 B 31-Dec-08Barclays Global Investors UK Holdings Ltd 84,863,132 4.23 $6.28 B 31-Dec-08VANGUARD GROUP, INC. (THE) 67,001,647 3.34 $4.96 B 31-Dec-08Capital World Investors 57,122,806 2.85 $4.23 B 31-Dec-08AXA 47,709,066 2.38 $3.53 B 31-Dec-08FMR LLC 39,225,546 1.96 $2.90 B 31-Dec-08Capital Research Global Investors 36,181,589 1.8 $2.68 B 31-Dec-08Bank of New York Mellon Corporation 30,293,763 1.51 $2.24 B 31-Dec-08WELLINGTON MANAGEMENT COMPANY, LLP 28,269,935 1.41 $2.09 B 31-Dec-08NORTHERN TRUST CORPORATION 25,520,500 1.27 $1.89 B 31-Dec-08

TOP MUTUAL FUND HOLDERS Holder Shares % Out Value Reported

WASHINGTON MUTUAL INVESTORS FUND 27,846,800 1.39 $2.06 B 31-Dec-08VANGUARD 500 INDEX FUND 19,224,064 0.96 $1.42 B 31-Dec-08SPDR TRUST SERIES 1 18,764,198 0.94 $1.55 B 30-Sep-08VANGUARD TOTAL STOCK MARKET INDEX FUND 17,375,518 0.87 $1.29 B 31-Dec-08INVESTMENT COMPANY OF AMERICA 13,572,278 0.68 $1.00 B 31-Dec-08INCOME FUND OF AMERICA INC 12,885,000 0.64 $953 M 31-Dec-08

VANGUARD INSTITUTIONAL INDEX FUND 12,604,863 0.63 $932 M 31-Dec-08AMERICAN BALANCED FUND 11,900,000 0.59 $880 M 31-Dec-08

COLLEGE RETIREMENT EQUITIES FUND 10,960,852 0.55 $811 M 31-Dec-08VANGUARD/WELLINGTON FUND INC. 10,110,200 0.5 $799 M 30-Nov-08

SHORT SELLING TRENDS IN CVX STOCK CVX’s downward trending days‐to‐cover indicates a general positive sentiment towards the stock. The short sellers have not set their sights on CVX throughout the economic downturn. If anything, CVX's days to cover ratio exhibits a slight downward trend.

0

2

4

6

8

10

12

14

Days to Cover Ratio

Days to Cover Ratio (Short Interest ÷ Volume)

Days to Cover

Chevron Billie Jean Bergmann

Jacob Krause

OTHER VALUATION MEASURES Piotroski’s Financial Fitness Scorecard Piotroski’s Financial Fitness Scorecard gives a company a maximum of 11 points based on items on the income statement and balance sheet. Historically, CVX’s scored an average 8 out of the 11. The forecasted average scored an average of 9 out of 11, which indicates we are projecting CVX to become more financially stable. Altman’s Probability of Bankruptcy Test The Altman Z‐Score uses eight different variables from a company’s income statement and balance sheet to predict a company’s probability of failure. In 2008, CVX scored a 4.55 indicating the company is well‐above the safe zone and should not go bankrupt in the near future.

Analysts' Consensus Recommendations If analysts' recommendations were ranked on a scale of 1 to 5, 1 being a strong buy and 5 being a strong sell, CVX's mean recommendation would have averaged a steady 2.2 for the past two weeks indicating a buy, but not a strong buy, signal from analysts. Graham and Dodd Relative Valuation Graham and Dodd is a Thomson‐Reuters relative valuation metric. It measures the premium investors are paying for future earnings compared to all stocks in the S&P 500. CVX ranked in the 5th Decile of Graham and Dodd, indicating the stock sells for an average premium, and is not overvalued.

Chevron Billie Jean Bergmann

Jacob Krause

Earnings Momentum When we began screening for stocks one of the criteria was for the company to have convincing earnings momentum, because growing profits in the current economic environment would be a sign of even stronger prospects when the global economy eventually recovers. CVX has better earnings momentum than 82% of the stocks in the S&P 500. Based on our forecasts, this strong earnings momentum is likely to continue. RECOMMENDATION: “BUY” We believe every portfolio has a place for a big energy stock. We like CVX in terms of its relative and discounted cash flow valuation, strong dividend per share growth, ability to create shareholder value and financial stability:

CVX is undervalued at its current price of $66.87 (05/01/2009), compared to our conservative DCF valuation of $79.11.

CVX’s has strong historical and projected DPS growth compared to its key competitors, evidenced by its steady and consistent growth in FCF per share and 21 consecutive years of growing dividends.

ROA, ROE, and ROIC are all sufficiently high enough to ensure CVX remains on pace for shareholder value creation in the long term, even if the company’s future operating environment becomes more challenging than it’s been in the recent past.

Our conservative model projects a relatively small spread between the ROIC and WACC, CVX is still able to create value, as evidenced by its increasing EVA and MVA.

CVX’s proven financial stability, evidenced by Piotroski’s Financial Fitness Scorecard, Altman’s Probability of Bankruptcy test, NOPAT and FCF.

The growth in worldwide energy consumption will lead to an increase in the need to develop innovate, renewable energy and develop additional supplies of traditional energy. CVX is strategically positioned through diversification to meet the world’s growing demand in renewable and traditional energy.

CVX Valuation & Analysis Model Page 1 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

394041424344454647484950515253545556

A B C D E F G H I J K L M N

Enter Firm Ticker CVX

Enter first financial statement year in cell B6 2004 2005 2006 2007 2008 2004 2005 2006 2007 2008 Average Manual

Total revenue 155,300 198,200 210,118 220,904 273,005 Revenue Growth 27.6% 6.0% 5.1% 23.6% 15.1%

Cost of goods sold 114,237 148,750 149,034 155,575 192,700 COGS % of Sales 73.6% 75.1% 70.9% 70.4% 70.6% 72.1% 74.0%

Gross profit 41,063 49,450 61,084 65,329 80,305

SG&A expense 4,557 4,828 5,093 5,841 5,734 SG&A % of Sales 2.9% 2.4% 2.4% 2.6% 2.1% 2.5%

Research & Development 697 743 1,364 1,323 1,169 R&D % of Sales 0.4% 0.4% 0.6% 0.6% 0.4% 0.5%

Depreciation/Amortization 4,935 5,913 7,506 8,708 9,528 D&A % of Sales 3.2% 3.0% 3.6% 3.9% 3.5% 3.4%

Interest expense (income), operating 0 0 0 0 0 Inc. Exp. Oper. 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Non-recurring expenses 0 0 0 85 22 Exp. Non-rec 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Other operating expenses 9,832 12,191 14,624 16,932 20,795 Other exp. 6.3% 6.2% 7.0% 7.7% 7.6% 6.9% 7.2%

Operating Income 21,042 25,775 32,497 32,440 43,057

Interest income (expense), non-operating 0 0 0 0 0 Int. inc. non-oper. 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Gain (loss) on sale of assets 0 0 0 0 0 Gain (loss) asset sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Other income, net 0 0 0 0 0 Other income, net 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Income before tax 21,042 25,775 32,497 32,440 43,057

Income tax 7,517 11,098 14,838 13,479 19,026 Tax rate 35.7% 43.1% 45.7% 41.6% 44.2% 42.0%

Income after tax 13,525 14,677 17,659 18,961 24,031

Minority interest 0 0 0 0 0 Minority interest 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Equity in affiliates 0 0 0 0 0 Equity in affiliates 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

U.S. GAAP adjustment 0 0 0 0 0 U.S. GAAP adjust. 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Net income before extraordinary items 13,525 14,677 17,659 18,961 24,031

Extraordinary items, total 294 0 0 0 0 Extrordinary items

Net income 13,819 14,677 17,659 18,961 24,031

Total adjustments to net income 3 2 1 0 0 Adjustments to NI

Basic weighted average shares 2,116 2,144 2,186 2,118 2,038 Share growth 1.3% 1.9% -3.1% -3.8% -0.9% -3.0%

Basic EPS excluding extraordinary items 6.39 6.85 8.08 8.95 11.79

Basic EPS including extraordinary items 6.53 6.85 8.08 8.95 11.79

Diluted weighted average shares 2,122 2,155 2,197 2,132 2,050 Diluted share growth 1.6% 2.0% -3.0% -3.8% -0.9% -3.0%

Diluted EPS excluding extraordinary items 6.37 6.81 8.04 8.90 11.72

Diluted EPS including extraordinary items 6.51 6.81 8.04 8.90 11.72

Dividends per share -- common stock 1.53 1.76 2.01 2.26 2.53

Gross dividends -- common stock 3,236 3,778 4,396 4,791 5,162 Dividend growth 16.7% 16.4% 9.0% 7.7% 12.4% 12.0%

Retained earnings 10,583 10,899 13,263 14,170 18,869

Data Source: Thomson/Reuters

values in millions

Too unpredictable to forecast, set to zero in the forecast

Too unpredictable to forecast, set to zero in the forecast

Forecasting PercentagesHistorical Income Statements

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

CVX Valuation & Analysis Model Page 2 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

394041424344454647484950515253545556

O P Q R S T U V W X Y Z

Year-by-year revenue growth -30.00% 10.00% 6.50% 6.00% 5.50% 5.00% 4.50% 4.00% 3.00% 3.00%

year 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E

Total revenue 191,104 210,214 223,878 237,310 250,362 262,881 274,710 285,699 294,270 303,098

Cost of goods sold 141,417 155,558 165,670 175,610 185,268 194,532 203,286 211,417 217,760 224,292

Gross profit 49,687 54,656 58,208 61,701 65,094 68,349 71,425 74,282 76,510 78,805

SG&A expense 4,792 5,272 5,614 5,951 6,278 6,592 6,889 7,165 7,379 7,601

Research & Development 955 1,051 1,119 1,187 1,252 1,314 1,374 1,428 1,471 1,515

Depreciation/Amortization 6,561 7,217 7,686 8,147 8,595 9,025 9,431 9,808 10,102 10,406

Interest expense (income), operating 0 0 0 0 0 0 0 0 0 0

Non-recurring expenses 18 20 21 22 23 24 26 27 27 28

Other operating expenses 13,759 15,135 16,119 17,086 18,026 18,927 19,779 20,570 21,187 21,823

Operating Income 23,601 25,961 27,649 29,308 30,920 32,466 33,926 35,284 36,342 37,432

Interest income (expense), non-operating (558) (510) (467) (448) (462) (523) (457) (379) (361) (330)

Gain (loss) on sale of assets 0 0 0 0 0 0 0 0 0 0

Other income, net 0 0 0 0 0 0 0 0 0 0

Income before tax 23,043 25,451 27,182 28,860 30,457 31,942 33,469 34,905 35,981 37,102

Income tax 9,686 10,699 11,426 12,131 12,803 13,427 14,069 14,672 15,125 15,596

Income after tax 13,357 14,753 15,756 16,728 17,654 18,515 19,400 20,232 20,856 21,506

Minority interest 0 0 0 0 0 0 0 0 0 0

Equity in affiliates 0 0 0 0 0 0 0 0 0 0

U.S. GAAP adjustment 0 0 0 0 0 0 0 0 0 0

Net income before extraordinary items 13,357 14,753 15,756 16,728 17,654 18,515 19,400 20,232 20,856 21,506

Extraordinary items, total 0 0 0 0 0 0 0 0 0 0

Net income 13,357 14,753 15,756 16,728 17,654 18,515 19,400 20,232 20,856 21,506

Total adjustments to net income 0 0 0 0 0 0 0 0 0 0

Basic weighted average shares 1,977 1,918 1,860 1,804 1,750 1,698 1,647 1,597 1,549 1,503

Basic EPS excluding extraordinary items 6.76 7.69 8.47 9.27 10.09 10.91 11.78 12.67 13.46 14.31

Basic EPS including extraordinary items 6.76 7.69 8.47 9.27 10.09 10.91 11.78 12.67 13.46 14.31

Diluted weighted average shares 1,989 1,929 1,871 1,815 1,760 1,708 1,656 1,607 1,558 1,512

Diluted EPS excluding extraordinary items 6.72 7.65 8.42 9.22 10.03 10.84 11.71 12.59 13.38 14.23

Diluted EPS including extraordinary items 6.72 7.65 8.42 9.22 10.03 10.84 11.71 12.59 13.38 14.23

Dividends per share -- common stock 2.92 3.38 3.90 4.50 5.20 6.00 6.93 8.00 9.24 10.67

Gross dividends -- common stock 5,781 6,475 7,252 8,123 9,097 10,189 11,412 12,781 14,315 16,032

Retained earnings 7,575 8,277 8,503 8,606 8,557 8,326 7,989 7,451 6,542 5,474

Forecasted Income Statements -- 10 Years

Revenues grow at the same rate each year unless a growth value is manually entered in the cell above the forecast year, in which case the year-by-year value overrides the historical or manual average. It makes sense to start tapering the growth forecasts 5 or 6 years into the forecast period.Revenues grow at the same rate each year unless a growth value is manually entered in the cell above the forecast year, in which case the year-by-year value overrides the historical or manual average. It makes sense to start tapering the growth forecasts 5 or 6 years into the forecast period.

CVX Valuation & Analysis Model Page 3 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

394041424344454647484950515253545556

AA AB AC AD AE AF AG AH AI AJ AK AL AM AN

Enter Firm Ticker CVX

year 2004 2005 2006 2007 2008 2004 2005 2006 2007 2008 Average Manual

Assets PPE Growth 43.3% 8.1% 14.2% 16.8% 13.0%

Cash & equivalents 9,291 10,043 10,493 7,362 9,347 Cash % of Sales 6.0% 5.1% 5.0% 3.3% 3.4% 4.6% 5.5%

Short term investments 1,451 1,101 953 732 213 ST Invest. % of Sales 0.9% 0.6% 0.5% 0.3% 0.1% 0.5%

Receivables, total 12,429 17,184 17,628 22,446 15,856 Receivables % Sales 8.0% 8.7% 8.4% 10.2% 5.8% 8.2% 6.0%

Inventory, total 2,983 4,121 4,656 5,310 6,854 Inventory % of Sales 1.9% 2.1% 2.2% 2.4% 2.5% 2.2%

Prepaid expenses 2,349 1,887 2,574 3,527 4,200 Pre. Exp. % of Sales 1.5% 1.0% 1.2% 1.6% 1.5% 1.4%

Other current assets, total 0 0 0 0 0 Other CA % of Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Total Current Assets 28,503 34,336 36,304 39,377 36,470

Property, plant and equipment (net) 44,458 63,690 68,858 78,610 91,780 Net PPE % of Sales 28.6% 32.1% 32.8% 35.6% 33.6% 32.5%

Goodwill 0 4,636 4,623 4,637 4,619 Goodwill % of Sales 0.0% 2.3% 2.2% 2.1% 1.7% 1.7%

Intangibles 0 0 0 0 0 Intangibles % of Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Long term investments 14,389 17,057 18,552 20,477 20,920 LT Invest. % of Sales 9.3% 8.6% 8.8% 9.3% 7.7% 8.7%

Notes receivable -- long term 1,419 1,686 2,203 2,194 2,413 Notes Rec. % of Sales 0.9% 0.9% 1.0% 1.0% 0.9% 0.9%

Other long term assets, total 4,439 4,428 2,088 3,491 4,963 Other LT ass. % Sales 2.9% 2.2% 1.0% 1.6% 1.8% 1.9%

Other assets, total 0 0 0 0 0 Other assets % Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Total assets 93,208 125,833 132,628 148,786 161,165

Liabilities and Shareholders' Equity

Accounts payable 10,747 16,074 16,675 21,756 16,580 Acc. Payable % Sales 6.9% 8.1% 7.9% 9.8% 6.1% 7.8%

Payable/accrued 0 0 0 0 0 Pay/accured % Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Accrued expenses 3,410 3,690 4,546 5,275 8,077 Acc. Exp. % of Sales 2.2% 1.9% 2.2% 2.4% 3.0% 2.3%

Notes payable/short term debt 816 739 2,159 1,162 2,818 Notes payable % Sales 0.5% 0.4% 1.0% 0.5% 1.0% 0.7%

Current portion of LT debt/Capital leases 0 0 0 0 0 Curr. debt % of Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Other current liabilities 3,822 4,508 5,029 5,605 4,548 Other curr liab % Sales 2.5% 2.3% 2.4% 2.5% 1.7% 2.3%

Total Current Liabilities 18,795 25,011 28,409 33,798 32,023

Long term debt, total 10,456 12,131 7,679 6,070 6,083 LT debt % of Sales

Deferred income tax 7,268 11,262 11,647 12,170 11,539 Def. inc. tax % Sales 4.7% 5.7% 5.5% 5.5% 4.2% 5.1%

Minority interest 172 200 209 204 469 Min. Int. % of Sales 0.1% 0.1% 0.1% 0.1% 0.2% 0.1%

Other liabilities, total 11,287 14,553 15,749 19,456 24,403 Other liab. % of Sales 7.3% 7.3% 7.5% 8.8% 8.9% 8.0%

Total Liabilities 47,978 63,157 63,693 71,698 74,517

Preferred stock (redeemable) 0 0 0 0 0

Preferred stock (unredeemable) 0 0 0 0 0

Common stock 1,706 1,832 1,832 1,832 1,832

Additonal paid-in capital 4,160 13,891 14,124 14,288 14,448Retained earnings (accumluated deficit) 45,414 55,738 68,464 82,329 101,102Treasury stock -- common (5,124) (7,870) (12,395) (18,892) (26,376)ESOP Debt Guarantee 0 0 0 0 0Other equity, total (926) (915) (3,090) (2,469) (4,358)

Total Shareholders' Equity 45,230 62,676 68,935 77,088 86,648Total Liabilities and Shareholders' Equity 93,208 125,833 132,628 148,786 161,165Diluted weighted average shares 2,122 2,155 2,197 2,132 2,050 Diluted share growth 1.6% 2.0% -3.0% -3.8% -0.9% -3.0%Total preferred shares outstanding 0 0 0 0 0 Preferred share growth

values in millions

Historical Balance Sheets

Set to last historical year's level throughout the forecasts.Set to last historical year's level throughout the forecasts.

LT debt is manually adjusted for AFN in the pro formas

Forecasting Percentages

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

The model uses the more conservative diluted common shares number for total shares outstanding.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

The model uses the more conservative diluted common shares number for total shares outstanding.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

The model uses the more conservative diluted common shares number for total shares outstanding.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

The model uses the more conservative diluted common shares number for total shares outstanding.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

The model uses the more conservative diluted common shares number for total shares outstanding.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

The model uses the more conservative diluted common shares number for total shares outstanding.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

The model uses the more conservative diluted common shares number for total shares outstanding.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

The model uses the more conservative diluted common shares number for total shares outstanding.

CVX Valuation & Analysis Model Page 4 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

394041424344454647484950515253545556

AO AP AQ AR AS AT AU AV AW AX AY AZ

0.07 98,205 105,079 112,434 120,305 128,726 137,737 147,379 157,695 168,734 180,545

Year-by-year PPE/Sales 51.39% 49.99% 50.22% 50.70% 51.42% 52.40% 52.50% 52.50% 53.00% 53.00%

year 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E

Assets

Cash & equivalents 10,511 11,562 12,313 13,052 13,770 14,458 15,109 15,713 16,185 16,670

Short term investments 899 989 1,053 1,117 1,178 1,237 1,293 1,344 1,385 1,426

Receivables, total 11,466 12,613 13,433 14,239 15,022 15,773 16,483 17,142 17,656 18,186

Inventory, total 4,254 4,679 4,984 5,283 5,573 5,852 6,115 6,360 6,551 6,747

Prepaid expenses 2,608 2,869 3,056 3,239 3,417 3,588 3,750 3,900 4,017 4,137

Other current assets, total 0 0 0 0 0 0 0 0 0 0

Total Current Assets 29,739 32,713 34,839 36,929 38,960 40,908 42,749 44,459 45,793 47,167

Property, plant and equipment (net) 98,205 105,079 112,434 120,305 128,726 137,737 144,223 149,992 155,963 160,642

Goodwill 3,184 3,502 3,730 3,954 4,171 4,380 4,577 4,760 4,903 5,050

Intangibles 0 0 0 0 0 0 0 0 0 0

Long term investments 16,677 18,345 19,537 20,709 21,848 22,941 23,973 24,932 25,680 26,450

Notes receivable -- long term 1,793 1,972 2,100 2,226 2,348 2,466 2,577 2,680 2,760 2,843

Other long term assets, total 3,625 3,988 4,247 4,501 4,749 4,987 5,211 5,419 5,582 5,749

Other assets, total 0 0 0 0 0 0 0 0 0 0

Total assets 153,222 165,598 176,886 188,624 200,803 213,418 223,309 232,242 240,680 247,901

Liabilities and Shareholders' Equity

Accounts payable 14,863 16,350 17,412 18,457 19,472 20,446 21,366 22,220 22,887 23,574

Payable/accrued 0 0 0 0 0 0 0 0 0 0

Accrued expenses 4,421 4,863 5,179 5,490 5,792 6,082 6,355 6,610 6,808 7,012

Notes payable/short term debt 1,332 1,465 1,560 1,654 1,745 1,832 1,914 1,991 2,050 2,112

Current portion of LT debt/Capital leases 0 0 0 0 0 0 0 0 0 0

Other current liabilities 4,331 4,764 5,074 5,378 5,674 5,958 6,226 6,475 6,669 6,869

Total Current Liabilities 24,947 27,442 29,226 30,979 32,683 34,317 35,862 37,296 38,415 39,567

Long term debt, total 8,800 7,878 7,074 6,678 6,871 7,872 6,667 5,262 4,907 4,335

Deferred income tax 9,800 10,780 11,481 12,170 12,839 13,481 14,088 14,651 15,091 15,543

Minority interest 220 242 258 273 288 302 316 329 339 349

Other liabilities, total 15,232 16,755 17,844 18,915 19,955 20,953 21,895 22,771 23,454 24,158

Total Liabilities 58,999 63,097 65,882 69,015 72,636 76,925 78,828 80,309 82,206 83,952

Preferred stock (redeemable) 0 0 0 0 0 0 0 0 0 0

Preferred stock (unredeemable) 0 0 0 0 0 0 0 0 0 0

Common stock 1,832 1,832 1,832 1,832 1,832 1,832 1,832 1,832 1,832 1,832

Additonal paid-in capital 14,448 14,448 14,448 14,448 14,448 14,448 14,448 14,448 14,448 14,448Retained earnings (accumluated deficit) 108,677 116,955 125,458 134,064 142,621 150,947 158,936 166,387 172,929 178,402Treasury stock -- common (26,376) (26,376) (26,376) (26,376) (26,376) (26,376) (26,376) (26,376) (26,376) (26,376)ESOP Debt Guarantee 0 0 0 0 0 0 0 0 0 0Other equity, total (4,358) (4,358) (4,358) (4,358) (4,358) (4,358) (4,358) (4,358) (4,358) (4,358)

Total Shareholders' Equity 94,223 102,501 111,004 119,610 128,167 136,493 144,482 151,933 158,475 163,948Total Liabilities and Shareholders' Equity 153,222 165,598 176,886 188,624 200,803 213,418 223,309 232,242 240,680 247,901Total common shares (diluted) 1,989 1,929 1,871 1,815 1,760 1,708 1,656 1,607 1,558 1,512Total preferred shares outstanding 0 0 0 0 0 0 0 0 0 0AFN (interactive with 3 items below) 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0Adjustment to LT Debt (use Goal Seek) 2,716.7 (921.6) (803.8) (396.2) 193.0 1,000.5 (1,204.6) (1,405.4) (354.5) (572.2)Issue Common Stock to Fund AFNSet Balance Sheet Cash Lower to Fund AFN

Forecasted Balance Sheets -- 10 Years

Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49

CVX Valuation & Analysis Model Page 5 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

394041424344454647484950515253545556

BA BB BC BD BE BF BG BH BI BJ BK BL BM BN BO BPEnter Firm Ticker CVX

2004 2005 2006 2007 2008 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E

Liquidity

Current 1.52 1.37 1.28 1.17 1.14 1.19 1.19 1.19 1.19 1.19 1.19 1.19 1.19 1.19 1.19

Quick 1.36 1.21 1.11 1.01 0.92 1.02 1.02 1.02 1.02 1.02 1.02 1.02 1.02 1.02 1.02

Net Working Capital to Total Assets 0.10 0.07 0.06 0.04 0.03 0.03 0.03 0.03 0.03 0.03 0.03 0.03 0.03 0.03 0.03

Asset Management

Days Sales Outstanding 29.21 31.65 30.62 37.09 21.20 21.90 21.90 21.90 21.90 21.90 21.90 21.90 21.90 21.90 21.90

Inventory Turnover 52.06 48.10 45.13 41.60 39.83 44.92 44.92 44.92 44.92 44.92 44.92 44.92 44.92 44.92 44.92

Fixed Assets Turnover 3.49 3.11 3.05 2.81 2.97 1.95 2.00 1.99 1.97 1.94 1.91 1.90 1.90 1.89 1.89

Total Assets Turnover 1.67 1.58 1.58 1.48 1.69 1.25 1.27 1.27 1.26 1.25 1.23 1.23 1.23 1.22 1.22

Debt Management

Long-Term Debt to Equity 23.1% 19.4% 11.1% 7.9% 7.0% 9.3% 7.7% 6.4% 5.6% 5.4% 5.8% 4.6% 3.5% 3.1% 2.6%

Total Debt to Total Assets 12.1% 10.2% 7.4% 4.9% 5.5% 6.6% 5.6% 4.9% 4.4% 4.3% 4.5% 3.8% 3.1% 2.9% 2.6%

Times Interest Earned N/A N/A N/A N/A N/A 42.3 50.9 59.2 65.4 66.9 62.0 74.2 93.1 100.8 113.4

ProfitabilityGross Profit Margin 26.4% 24.9% 29.1% 29.6% 29.4% 26.0% 26.0% 26.0% 26.0% 26.0% 26.0% 26.0% 26.0% 26.0% 26.0%

Operating Profit Margin 13.5% 13.0% 15.5% 14.7% 15.8% 12.3% 12.3% 12.3% 12.3% 12.3% 12.3% 12.3% 12.3% 12.3% 12.3%

Net After-Tax Profit Margin 8.9% 7.4% 8.4% 8.6% 8.8% 7.0% 7.0% 7.0% 7.0% 7.1% 7.0% 7.1% 7.1% 7.1% 7.1%

Total Assets Turnover 1.67 1.58 1.58 1.48 1.69 1.25 1.27 1.27 1.26 1.25 1.23 1.23 1.23 1.22 1.22

Return on Assets 14.8% 11.7% 13.3% 12.7% 14.9% 8.7% 8.9% 8.9% 8.9% 8.8% 8.7% 8.7% 8.7% 8.7% 8.7%

Equity Multiplier 2.06 2.01 1.92 1.93 1.86 1.63 1.62 1.59 1.58 1.57 1.56 1.55 1.53 1.52 1.51

Return on Equity 30.6% 23.4% 25.6% 24.6% 27.7% 14.2% 14.4% 14.2% 14.0% 13.8% 13.6% 13.4% 13.3% 13.2% 13.1%

Free Cash Flow Per Share ($2.60) $5.70 $5.95 $5.63 $3.88 $3.88 $4.37 $4.75 $5.13 $5.48 $7.70 $8.89 $9.49 $11.05

EPS (using diluted shares, excluding extraordinary items) 6.37 6.81 8.04 8.90 11.72 6.72 7.65 8.42 9.22 10.03 10.84 11.71 12.59 13.38 14.23

DPS (dividends per share) 1.53 1.75 2.00 2.25 2.52 2.91 3.36 3.88 4.48 5.17 5.97 6.89 7.95 9.19 10.61

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

NOPAT (net operating profit after tax) 13,525 14,677 17,659 18,961 24,031 13,680 15,048 16,026 16,988 17,922 18,818 19,665 20,452 21,065 21,697

ROIC (return on invested capital) 24.6% 19.5% 22.0% 21.9% 24.2% 13.0% 13.4% 13.3% 13.2% 13.0% 12.8% 12.8% 12.8% 12.6% 12.6%

EVA (economic value added) 7,804 6,848 9,295 9,944 13,716 2,744 3,324 3,486 3,578 3,587 3,499 3,626 3,771 3,731 3,843

FCF (free cash flow) N/A (5,593) 12,519 12,678 11,548 7,709 7,480 8,175 8,629 9,027 9,352 12,749 14,283 14,783 16,698

Weighted Average Cost of Capital 10.4% 10.4% 10.4% 10.4% 10.4% 10.4% 10.4% 10.4% 10.4% 10.4% 10.4%

Net Operating Working Capital (NOWC) 10,546 11,584 11,556 8,087 7,400 6,947 7,641 8,138 8,626 9,101 9,556 9,986 10,385 10,697 11,017

Operating Long Term Assets 44,458 63,690 68,858 78,610 91,780 98,205 105,079 112,434 120,305 128,726 137,737 144,223 149,992 155,963 160,642

Total Operating Capital 55,004 75,274 80,414 86,697 99,180 105,152 112,720 120,572 128,931 137,827 147,293 154,208 160,377 166,659 171,659

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018Long-term Horizon Value Growth Rate (user-supplied) 3.00%PV of Forecasted FCF, discounted at 10.40% $147,193 $154,793 $163,413 $172,235 $181,520 $191,373 $201,925 $210,177 $217,754 $225,619 $247,512Value of Non-Operating Assets $9,560 $11,410 $12,551 $13,367 $14,169 $14,948 $15,695 $16,402 $17,058 $17,570 $18,097Total Intrinsic Value of the Firm $156,753 $166,203 $175,964 $185,602 $195,689 $206,321 $217,620 $226,579 $234,811 $243,188 $265,609Intrinsic Market Value of the Equity $147,852 $157,302 $167,063 $176,701 $186,788 $197,420 $208,719 $217,678 $225,910 $234,287 $256,708Per Share Intrinsic Value of the Firm $72.12 $79.11 $86.61 $94.44 $102.92 $112.14 $122.23 $131.42 $140.61 $150.33 $169.81MVA (market value added) $61,204 $63,079 $64,563 $65,697 $67,178 $69,253 $72,226 $73,196 $73,977 $75,813 $92,759

Item Value Percent Cost Weighted Cost Risk Free Rate 4.00%ST Debt (from most recent balance sheet) 2,818 2.00% 3.78% 0.04% Beta 1.15LT Debt (from most recent balance sheet) 6,083 4.31% 5.77% 0.14% Market Risk Prem. 6.00%MV Equity (look up stock's mkt. cap and enter in cell BB53) 132,320 93.70% 10.90% 10.21% Cost of Equity 10.90%Weighted Average Cost of Capital 10.40%

Source: Yahoo (3/8/09)http://finance.yahoo.com/bonds/composite_bond_rates

Weighted Average Cost of Capital Calculations

Valuation Metrics Trend Analysis (NOPAT, EVA, MVA, FCF and Capital in millions)

Forecasted Ratios and Valuation Model -- 10 Years

Capital Asset Pricing Model

Forecasted Valuation Metrics -- 10 Years

values in millions

Historical Ratios and Valuation Model

Valuation (in millions) -- through year 2018

CVX Valuation & Analysis Model Page 6 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

394041424344454647484950515253545556

BQ BR BS BT BU BV BW BX BY BZ CA CB CC CD CE CF CG CH

Inputs 2004 2005 2006 2007 2008 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E

Per share value (hist. & DCF est.) $52.51 $56.77 $73.53 $93.35 $76.52 $79.11 $86.61 $94.44 $102.92 $112.14 $122.23 $131.42 $140.61 $150.33 $169.81

Market capitalization $111,114 $121,726 $160,737 $197,675 $155,948 $156,381 $166,085 $175,666 $185,694 $196,264 $207,497 $216,404 $224,588 $232,916 $255,205

EBITDA $26,271 $31,688 $40,003 $41,148 $52,585 $20,497 $22,500 $23,930 $25,344 $26,733 $28,084 $29,309 $30,440 $31,340 $32,263

Enterprise Value $113,267 $124,753 $160,291 $197,749 $155,971 $156,222 $164,108 $172,245 $181,247 $191,398 $203,045 $210,192 $216,456 $224,027 $245,330

Multiples

Price/Sales 0.72 0.61 0.76 0.89 0.57 0.82 0.79 0.78 0.78 0.78 0.79 0.79 0.79 0.79 0.84

Price/EBITDA 4.23 3.84 4.02 4.80 2.97 7.63 7.38 7.34 7.33 7.34 7.39 7.38 7.38 7.43 7.91

Price/Free Cash Flow N/A -21.48 12.59 16.10 14.03 20.29 22.21 21.49 21.52 21.74 22.19 16.97 15.72 15.76 15.28

Enterprise Value/EBITDA 4.31 3.94 4.01 4.81 2.97 7.62 7.29 7.20 7.15 7.16 7.23 7.17 7.11 7.15 7.60

Price/Earnings 8.24 8.33 9.15 10.49 6.53 11.78 11.32 11.22 11.17 11.18 11.27 11.22 11.17 11.23 11.94

Dividend Yield 2.90% 3.09% 2.72% 2.41% 3.29% 3.68% 3.88% 4.10% 4.35% 4.61% 4.88% 5.24% 5.66% 6.11% 6.25%

Historical Override

Valuation Estimates Based On: Average w/Manual 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E

Price/Sales 0.71 $68.44 $77.61 $85.21 $93.12 $101.28 $109.63 $118.11 $126.63 $134.47 $142.78

Price/EBITDA 3.97 $41.18 $46.60 $51.10 $55.79 $60.67 $65.71 $70.69 $75.69 $80.34 $85.26

Price/Free Cash Flow 5.31 15.00 $58.49 $58.51 $65.92 $71.74 $77.37 $82.64 $116.14 $134.14 $143.12 $166.66

Enterprise Value/EBITDA 4.01 $41.53 $47.00 $51.53 $56.27 $61.18 $66.26 $71.29 $76.33 $81.02 $85.99

Price/Earnings 8.55 $57.76 $65.77 $72.41 $79.26 $86.23 $93.24 $100.71 $108.28 $115.07 $122.33

Low Price $41.18 $46.60 $51.10 $55.79 $60.67 $65.71 $70.69 $75.69 $80.34 $85.26

High Price $68.44 $77.61 $85.21 $93.12 $101.28 $109.63 $118.11 $134.14 $143.12 $166.66

DCF Price $79.11 $86.61 $94.44 $102.92 $112.14 $122.23 $131.42 $140.61 $150.33 $169.81

Forecasted Stock Prices Based on Historical Multiples -- 10 Years

Historical Ratios and Valuation Forecasted Ratios and Valuation

In this section we are going to examine historical and forecasted ratios (or "multiples") typically used to value stocks ‐‐ P/CF, Enterprise Value/EBITDA, etc. We first want to compare the historical trends in these ratios to the trends in their forecasted values. If our forecasted multiples are systematically increasing or decreasing our forecasts may be too optimistic or pessimistic, and our forecast assumptions may have to be adjusted. Second, we want to compare our discounted cash flow valuation estimates with those derived from the various multiples. Once again, if there is a large discrepancy between our DCF valuation estimate of the company's stock and the range of values obtained from the various multiples, we may want to adjust our forecast assumptions. 1. You will need to look up the company's year‐end stock prices and enter them in the first 5 (historical) years of the "per share value" category.2. Use the estimated DCF price per share in the forecasted period (link to your forecasted prices in cells BG47‐BP47.3. Market capitalization will be calculated as basic weighted shares x historical year‐end prices and then forecasted basic weighted shares x DCF forecasted prices.4. As with previous calculations, historical multiples use actual historical values and forecasted multiples use forecasted values.

$20

$45

$70

$95

$120

$145 Forecasted Value Per Sh

are

Forecasted Per Share Stock Values

Low Price DCF Price High Price

$20

$40

$60

$80

$100

$120

$140

$160

$180

0

5

10

15

20

25

30

35

DCF Price

P/S and Ent. Value/EBITDA

Price/Sales and Enterprise Value/EBITDA vs. Price

Price/Sales Enterprise Value/EBITDA DCF Price

In this section we are going to examine historical and forecasted ratios (or "multiples") typically used to value stocks ‐‐ P/CF, Enterprise Value/EBITDA, etc. We first want to compare the historical trends in these ratios to the trends in their forecasted values. If our forecasted multiples are systematically increasing or decreasing our forecasts may be too optimistic or pessimistic, and our forecast assumptions may have to be adjusted. Second, we want to compare our discounted cash flow valuation estimates with those derived from the various multiples. Once again, if there is a large discrepancy between our DCF valuation estimate of the company's stock and the range of values obtained from the various multiples, we may want to adjust our forecast assumptions. 1. You will need to look up the company's year‐end stock prices and enter them in the first 5 (historical) years of the "per share value" category.2. Use the estimated DCF price per share in the forecasted period (link to your forecasted prices in cells BG47‐BP47.3. Market capitalization will be calculated as basic weighted shares x historical year‐end prices and then forecasted basic weighted shares x DCF forecasted prices.4. As with previous calculations, historical multiples use actual historical values and forecasted multiples use forecasted values.

$20

$45

$70

$95

$120

$145 Forecasted Value Per Sh

are

Forecasted Per Share Stock Values

Low Price DCF Price High Price

$20

$40

$60

$80

$100

$120

$140

0

5

10

15

20

25

30

35

DCF Price

P/S and Ent. Value/EBITDA

Price/Sales and Enterprise Value/EBITDA vs. Price

Price/Sales Enterprise Value/EBITDA DCF Price

In this section we are going to examine historical and forecasted ratios (or "multiples") typically used to value stocks ‐‐ P/CF, Enterprise Value/EBITDA, etc. We first want to compare the historical trends in these ratios to the trends in their forecasted values. If our forecasted multiples are systematically increasing or decreasing our forecasts may be too optimistic or pessimistic, and our forecast assumptions may have to be adjusted. Second, we want to compare our discounted cash flow valuation estimates with those derived from the various multiples. Once again, if there is a large discrepancy between our DCF valuation estimate of the company's stock and the range of values obtained from the various multiples, we may want to adjust our forecast assumptions. 1. You will need to look up the company's year‐end stock prices and enter them in the first 5 (historical) years of the "per share value" category.2. Use the estimated DCF price per share in the forecasted period (link to your forecasted prices in cells BG47‐BP47.3. Market capitalization will be calculated as basic weighted shares x historical year‐end prices and then forecasted basic weighted shares x DCF forecasted prices.4. As with previous calculations, historical multiples use actual historical values and forecasted multiples use forecasted values.

$20 $30 $40 $50 $60 $70 $80 $90

$100 $110 $120 $130 $140 $150 $160 $170 $180

Forecasted Value Per Sh

are

Forecasted Per Share Stock Values

Low Price DCF Price High Price

$20

$40

$60

$80

$100

$120

$140

$160

$180

0

5

10

15

20

25

DCF Price

P/S and Ent. Value/EBITDA

Price/Sales and Enterprise Value/EBITDA vs. Price

Price/Sales Enterprise Value/EBITDA DCF Price

CVX Valuation & Analysis Model Page 7 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

394041424344454647484950515253545556

CI CJ CK CL CM CN CO CP CQ CR CS CT CU CV CW CX CY CZ DA DB

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

‐5

0

5

10

15

20

25

30

35

Dividend Yield

Price/Earnings Ratio

Price/Earnings Ratio and Dividend Yield

Price/Earnings Ratio Dividend Yield

0%

10%

20%

30%

40%

50%

Gross M

argin

Gross, Operating and Net Profit Margins

Gross Margin Operating Margin Net Margin

0%

5%

10%

15%

20%

25%

30%

35%

40%

ROA, R

OE an

d ROIC

Return on Assets, Equity and Invested Capital

Return on Assets Return on Equity Return on Invested Capital

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000 NOPAT an

d Free Cash Flow

NOPAT and Free Cash Flow (millions)

NOPAT Free Cash Flow

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$0 $50

$100 $150 $200 $250 $300 $350 $400 $450 $500 $550 $600

Market Value Added

Economic Value Added

Economic Value Added & Market Value Added (millions)

Economic Value Added Market Value Added

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

EPS an

d DPS

Earnings and Dividends Per Share

Earnings Per Share Dividends Per Share

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

‐5

0

5

10

15

20

25

30

35

Dividend Yield

Price/Earnings Ratio

Price/Earnings Ratio and Dividend Yield

Price/Earnings Ratio Dividend Yield

0%

10%

20%

30%

40%

50%

Gross M

argin

Gross, Operating and Net Profit Margins

Gross Margin Operating Margin Net Margin

0%

5%

10%

15%

20%

25%

30%

35%

40%

ROA, R

OE an

d ROIC

Return on Assets, Equity and Invested Capital

Return on Assets Return on Equity Return on Invested Capital

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000 NOPAT an

d Free Cash Flow

NOPAT and Free Cash Flow (millions)

NOPAT Free Cash Flow

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$0 $50

$100 $150 $200 $250 $300 $350 $400 $450 $500 $550 $600

Market Value Added

Economic Value Added

Economic Value Added & Market Value Added (millions)

Economic Value Added Market Value Added

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

EPS an

d DPS

Earnings and Dividends Per Share

Earnings Per Share Dividends Per Share

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

2

4

6

8

10

12

14

Dividend Yield

Price/Earnings Ratio

Price/Earnings Ratio and Dividend Yield

Price/Earnings Ratio Dividend Yield

0%

5%

10%

15%

20%

25%

30%

35%

Gross M

argin

Gross, Operating and Net Profit Margins

Gross Margin Operating Margin Net Margin

0%

5%

10%

15%

20%

25%

30%

35%

ROA, R

OE an

d ROIC

Return on Assets, Equity and Invested Capital

Return on Assets Return on Equity Return on Invested Capital

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

NOPAT an

d Free Cash Flow

NOPAT and Free Cash Flow (millions)

NOPAT Free Cash Flow

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

($1,000)

$1,000

$3,000

$5,000

$7,000

$9,000

$11,000

$13,000

$15,000

Market Value Added

Economic Value Added

Economic Value Added & Market Value Added (millions)

Economic Value Added Market Value Added

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

EPS an

d DPS

Earnings and Dividends Per Share

Earnings Per Share Dividends Per Share

CVX Valuation & Analysis Model Page 8 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

394041424344454647484950515253545556

DC DD DE DF DG DH DI DJ DK DL DM DN DO DP DQ DR DS DT DU DV

0

1

2

3

4

5

Days to Cover Ratio

Days to Cover Ratio (Short Interest ÷ Volume)

Days to Cover

3,000

6,000

9,000

12,000

15,000

18,000

21,000

24,000

27,000

Short Interst (thousands)

Short Interest (thousands of shares)

Short Interest (thousands of shares)

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Avg. D

aily Volume

Average Daily Trading Volume (thousands)

Average Daily Volume (thousands of shares)

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

Historical P/E Ratio

Historical Trends: Price/Earnings Ratio

Yum Brands McDonalds0.9

1.0

1.0

1.1

Historical P/S Ratio

Historical Trends: Price/Sales Ratio

YUM Brands McDonalds

0

1

2

3

4

5

Days to Cover Ratio