china ppp overview - un escap › sites › default › files › 2. hua tan... · 2019-09-23 ·...

TRANSCRIPT

Smart Connections for All

The Transport and ICTGlobal Practice

CHINA PPP OVERVIEW

Hua Tan

Senior Transport Specialist, Transport and ICT Global Practice

China, Mongolia, and Central Asia, World Bank Group

September 12, 2018

Guiyang City, Guizhou Province

1

Local Government UDIC

Bank

Developer Land reserve A Land reserve B

Apply for loan by collateralizing land lease revenue

Issue loan

Obta

in a

loan to

invest

in in

frastru

ctu

re

Auctioning land development rights

Pay la

nd tra

nsactio

n fe

es

and ta

xes

part of the transaction fees goes to UDIC to

repay principal and interests 2

3

4

56

7

Repayment of principal and interests8

• This financing mode is no longer permitted under the new Budget Law.

Prior to 2015, local government financing vehicles (LGFVs) / UDIC were responsible

for infrastructure financing with implicit government guarantees mostly

collateralized by future land revenues

To mitigate financial risks, starting in 2014, the central government introduced a

series of reform policies

2

• Improve local government budget management

• Improve debt management

• Standardize transfer payment

New Budget Law

• Regulate the relationship between local government and LGFVs

• Transition UDICs into independent commercial entities

No. 43rd Decree of

the State Council

• Conduct extensive inventory of existing local government debt

• Manage the total amount of local government debt

• Reduce the cost of debt

Debt investigation

and replacement

Better manage fiscal budget

Mitigate financialrisks

Standardize municipal financing

Policy Objectives

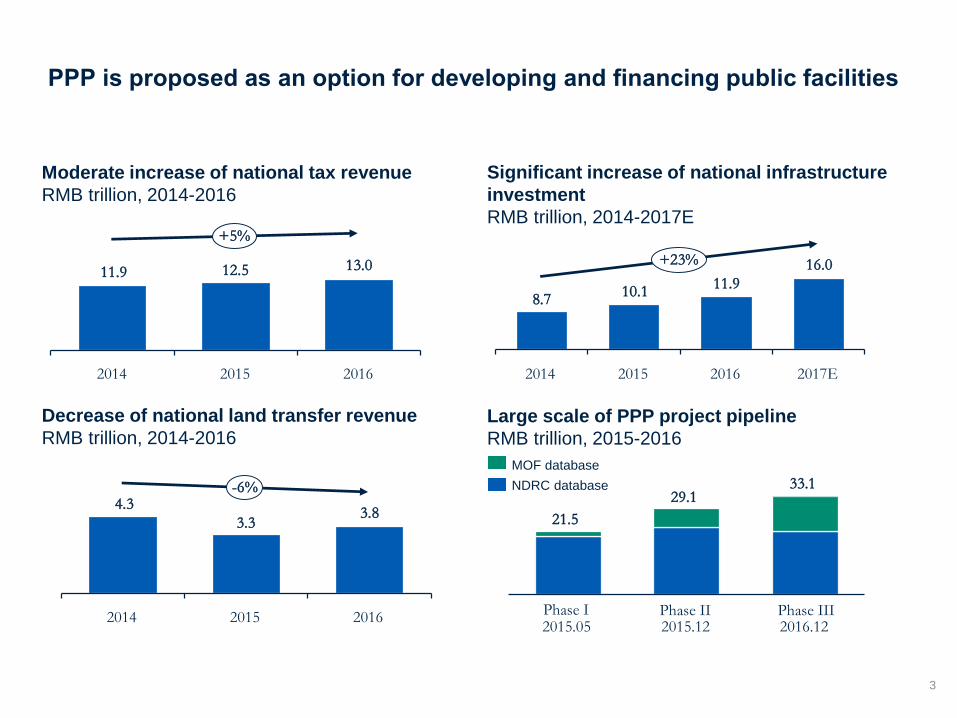

Large scale of PPP project pipeline

RMB trillion, 2015-2016

PPP is proposed as an option for developing and financing public facilities

3

Phase III

33.1

Phase II

29.1

Phase I

21.5

NDRC database

MOF database

2015.05 2015.12 2016.12

11.9 12.5 13.0

+5%

201620152014

Moderate increase of national tax revenue

RMB trillion, 2014-2016

Decrease of national land transfer revenue

RMB trillion, 2014-2016

4.33.3

3.8

-6%

201620152014

Significant increase of national infrastructure

investment

RMB trillion, 2014-2017E

8.7 10.1 11.916.0+23%

2017E201620152014

PPP is promoted as an alternative procurement model to help alleviate local

government financial burden and improve delivery of public services

4

Past Present

• UDIC model

– Local governments inject assets, including land, to UDICs which invest, build, and operate public infrastructure on behalf of local governments

– UDICs pledge assets such as land as collateral for bank loans to finance infrastructure projects

– Banks assume implicit government guarantee to loans issued to UDICs, which are backed by local governments.

– UDIC loans are not included in local government budget (off balance sheet)

– UDIC is responsible for loan repayment and infrastructure operations

• PPP model

– Private partners areresponsible for financing, building, and operating public infrastructure

– Local government financial obligations to the PPP projects are accounted for in its annual budget

– Total local government financial obligations to PPP projects cannot exceed 10% of the annual general public expenditure budget

Improvements in PPP legal framework

processes

“ Notice on the promotion of PPP ” (MOF, No.76, 2014-9-23)

• Defines the basic framework

“Guiding opinions on the promotion of PPP in the field of social

service” (State Council, No. 4, 2015-5-22)

• Defines regulation, fiscal, supervision, and pricing systems

“ Guiding opinions on innovation of investment and financing

mechanisms in key sectors and incentives for social investment”

(State Council, No. 60, 2014-11-26)

• Defines financing principles, tools and policies

“Notice on improvements of PPP projects” (MOF, No. 57, 2015-6-

25)• Establish the PPP information platform of the Ministry of Finance

“Notice on the guidelines for the implementation of PPP projects in

the field of traditional infrastructure” (NDRC, No. 2231, 2016-10-24)• Outlines the selection of social investors, project evaluation, and project

implementation

“Demonstration guidelines on fiscal affordability of PPP project”(MOF, No. 21, 2015-4-7)• Outlines the two major risk assessment methods: VfM and fiscal

affordability

demonstration mechanism and

information disclosure

project evaluation and risk management

financing

system

PPP framework

“Notice on further regulating the debt financing behaviors of local

governments ” (MOF, No. 50, 2017-4-26)• Prohibits local governments from providing guarantees for UDIC debt and

pledging future land sale proceeds to bolster UDIC creditworthiness

local government debt control

Improvements in PPP legal framework

performance-based payment

“ Notice on promoting asset-backed securitization for PPP projects”

(NDRC, No.268, 2016-12-21)

“ Notice on conducting asset-backed securitization for PPP projects in

a regulated manner ” (MOF, No.55, 2017-6-7)

• Promotes ABS as an innovative financing tool for PPP projects

“Notice on mandatory use of PPP model in wastewater treatment

and solid waste treatment projects” (MOF, No. 455, 2017-7-1)• Mandates the use of PPP model in all new wastewater and solid waste

treatment projects.

“Notice on regulating management of PPP integrated information

platform database” (MOF, No. 92, 2017-11-10)• Increases the threshold for PPP projects entering the national database

• Requires 30% of government payments made on performance basis

“Guidelines on the issuance of PPP project bonds” (NDRC, No. 730,2017-4-25)• Introduces PPP project bonds as a new financing tool for refinancing

PPP projects in operation

mandate PPP in wastewater and solid

waste sectors

PPP project bonds

Asset-backed Securitization (ABS)

“Notice on strengthening risk control of State-owned Enterprises in

PPP sector” (SASAC, No. 192, 2017-11-17)• Prohibits SOEs who has a debt ratio over 85% from participating in PPPs

SOE debt control

“PPP Law in the Infrastructure and Public Service Sectors (Draft for

Comment)” (State Council, 2017-7)

• A draft of the proposed law that consists 7 chapters and 50 articles has

been handed to China's cabinet as well as local authorities

PPP legislation

Ministry of Finance (MOF) and National Development and Reform Commission

(NDRC) regulate PPP project development

7

Legislative Affairs Office of the State Council

MOF NDRC

Role Regulator Regulator

Responsible Sectors

Public Services:

• Primarily social services and small

scale infrastructure projects

• Energy, transport, municipal

infrastructure, agriculture, forestry,

water, environmental protection,

social welfare projects, health

care, elderly care, education,

science and technology, culture,

sports, tourism, etc.

Traditional infrastructure Projects:

• Primarily large-scale traditional

infrastructure projects

• Energy, transport, water,

environmental protection,

agriculture, forestry, and major

municipal infrastructure

Life-cycle Management

• 5 phases with a total of 19 steps

• For PPP project approval,

requires VfM analysis and fiscal

affordability assessment

• Follows the normal project

management process

• For PPP project approval,

requires the feasibility study to

include VfM analysis and fiscal

affordability assessment

Major Law Government Procurement Law Bidding and Tendering Law

MOF requires VfM Assessment and Fiscal Affordability Assessment

8

VfM

Assessment

Qualitative

Analysis

Quantitative

Analysis

(optional)

Life cycle integration

Risk identification and allocation

Performance oriented and incentives for innovation

Potential competition

Capability of governmental institutions

Feasibility of financing

Supplementary evaluation metricsEquity investment present value

Operation subsidy present value

Risk premium present value

government counterpart funds present value

Construction and O&M net cost

Comparative adjusted value

Total project risk premium

Present Value of

Life-cycle Project

Cost

PSC

VfM Assessment is qualitative rather than quantitative

Fiscal affordability assessment combines qualitative and quantitative analyzes

FAA (Fiscal

Affordability

Assessment)

Expenditure Estimate

Capability Assessment

Government equity investment

Operation subsidy

Risks

Government counterpart funds

Fiscal expenditure assessment

Industry and sector balance assessment

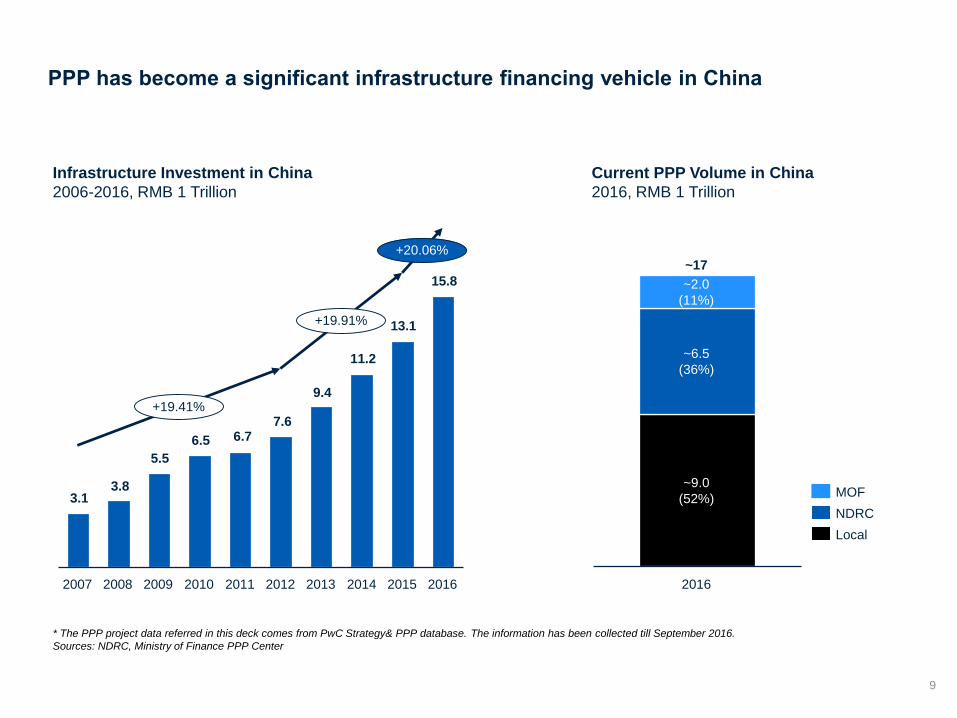

PPP has become a significant infrastructure financing vehicle in China

9

3.13.8

5.5

6.5 6.77.6

9.4

11.2

13.1

15.8

201120102007 2015201420132012

+19.41%

+20.06%

+19.91%

201620092008

Infrastructure Investment in China

2006-2016, RMB 1 Trillion

2016

~17

~9.0

(52%)

~6.5

(36%)

~2.0

(11%)

Current PPP Volume in China

2016, RMB 1 Trillion

Local

NDRC

MOF

* The PPP project data referred in this deck comes from PwC Strategy& PPP database. The information has been collected till September 2016.

Sources: NDRC, Ministry of Finance PPP Center

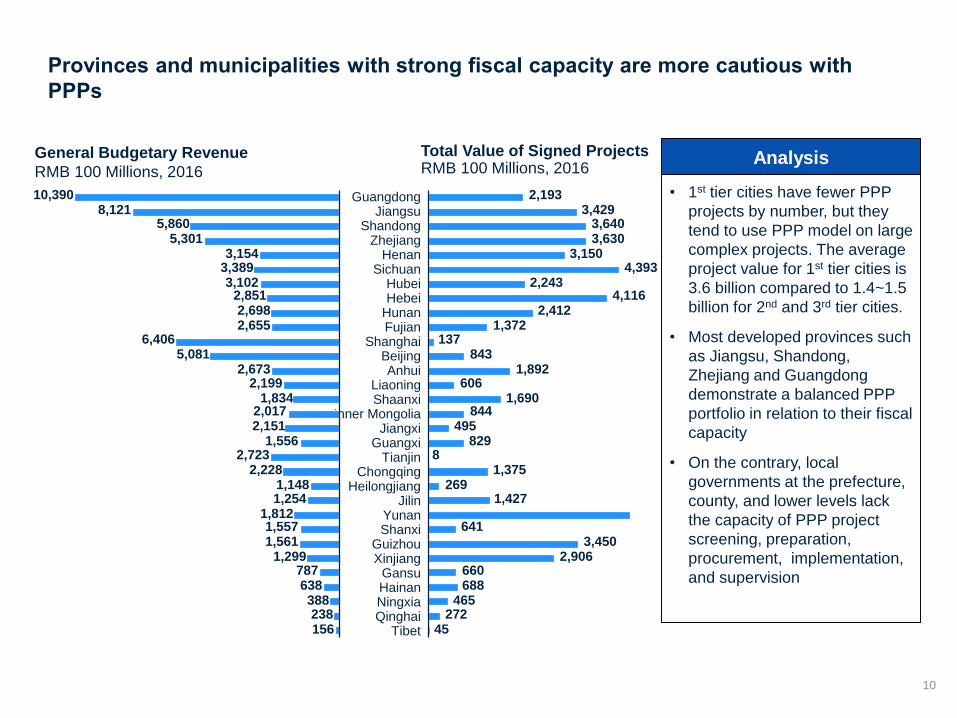

Provinces and municipalities with strong fiscal capacity are more cautious with

PPPs

10

2,1933,429

3,6403,630

3,1504,393

2,2434,116

2,4121,372

137843

1,892606

1,690844

495829

81,375

2691,427

6413,450

2,906660688

465272

45TibetQinghaiNingxiaHainanGansu

XinjiangGuizhou

ShanxiYunan

JilinHeilongjiang

ChongqingTianjin

GuangxiJiangxi

Inner MongoliaShaanxiLiaoning

AnhuiBeijing

ShanghaiFujianHunanHebeiHubei

SichuanHenan

ZhejiangShandong

JiangsuGuangdong10,390

8,1215,860

5,3013,154

3,3893,102

2,8512,6982,655

6,4065,081

2,6732,199

1,8342,0172,151

1,5562,723

2,2281,1481,254

1,8121,5571,561

1,299787638388238156

General Budgetary Revenue

RMB 100 Millions, 2016Analysis

• 1st tier cities have fewer PPP

projects by number, but they

tend to use PPP model on large

complex projects. The average

project value for 1st tier cities is

3.6 billion compared to 1.4~1.5

billion for 2nd and 3rd tier cities.

• Most developed provinces such

as Jiangsu, Shandong,

Zhejiang and Guangdong

demonstrate a balanced PPP

portfolio in relation to their fiscal

capacity

• On the contrary, local

governments at the prefecture,

county, and lower levels lack

the capacity of PPP project

screening, preparation,

procurement, implementation,

and supervision

Total Value of Signed Projects RMB 100 Millions, 2016

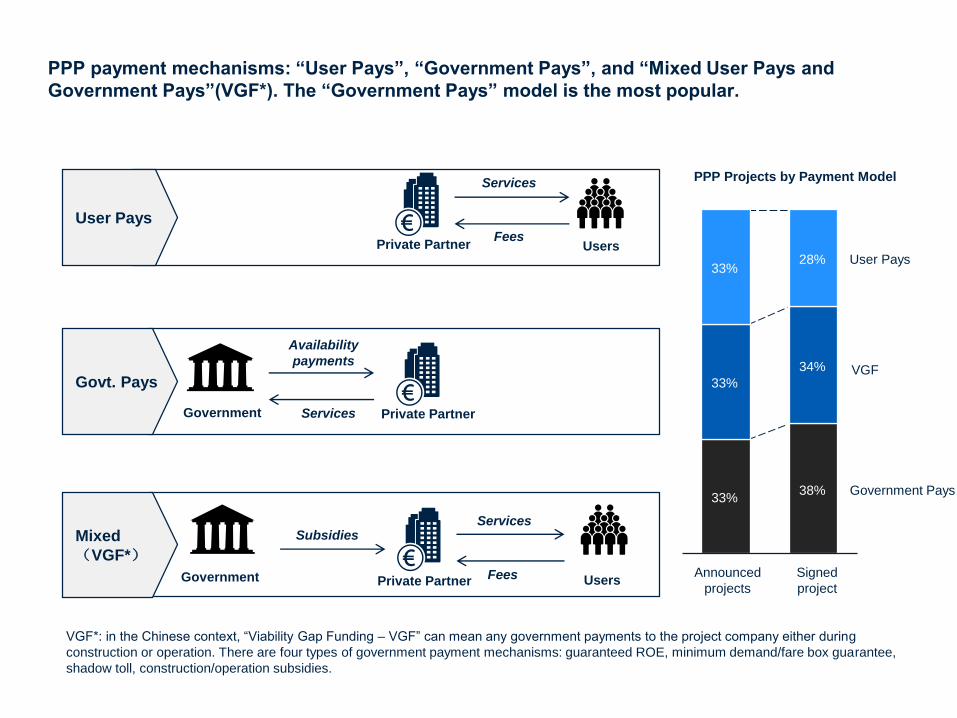

PPP payment mechanisms: “User Pays”, “Government Pays”, and “Mixed User Pays and

Government Pays”(VGF*). The “Government Pays” model is the most popular.

User Pays

Govt. Pays

Mixed

(VGF*)

Government

Users

Users

Private Partner

Services

Fees

Services

Fees

Availability

payments

Services

Subsidies

Government Private Partner

Private Partner

PPP Projects by Payment Model

VGF

Government Pays33%

33%

33%

34%

28%

Announced

projects

User Pays

Signed

project

38%

VGF*: in the Chinese context, “Viability Gap Funding – VGF” can mean any government payments to the project company either during

construction or operation. There are four types of government payment mechanisms: guaranteed ROE, minimum demand/fare box guarantee,

shadow toll, construction/operation subsidies.

Ownership of private partners: SOEs are dominant in the PPP market

12

76.0%

Led by SOE

24.0%

Led by private

companies

31%

69%

100%

Project Value Leading Companies

SOE

Private

Source: BRIdata. (2017). 2017 Annual Report on PPP Development in China. Available from http://www.bridata.com/front/pdf/detail?id=1537

Leading large-scale EPC SOEs

Leading domestic listed companies specializing in EPC and real estate

Amount Ownership

China State Construction Engineering

Corporation

857 Central

China Communications Construction

Company

585 Central

China Railway Construction Corporation 428 Central

Metallurgical Corporation of China 370 Central

China Railway Group 359 Central

China Fortune Land Development Co., Ltd 289 Private

Power Construction Corporation of China 236 Central

China Gezhouba Corporation 193 Central

Yunnan Construction Engineering Group 115 Local SOE

Beijing Orient Landscape 95 Private

Recent PPP winners, RMB billion

contract

signed

under

development

Type of private partners: primarily contractors, lack of experienced operators

13

6.9%

12.6%

2.6%

72.2%

3.1%

2.6%

100%

PPP winners’ background,

As of October 2017

Leading Companies Capacities

• Large-scale SOEs

• Mostly contractors

• Leading commercial banks

• Investment arms of large-scale SOEs

• Equipment supplier

• Operators

contractors

banks

funds

OEM

operatorsothers

Source: PwC Strategy& PPP Database. Not publicly available.

• The local government will designate a representative entity to invest in the project company with equity contributions between 5-30% of the total equity contribution

• Debt financing depends on the strength of private

partners’ balance sheets and the implicit guarantee in

the form of government representation in the project

company

• As of 2017, 72% of all the established PPP Project

Companies has a local government as a shareholder

either directly or through a UDIC type company

China’s practice differs from international practice in that governments

participate in PPP projects through a ‘platform company’

14

China PracticeInternational Practice

Local

Government

Private

Partner

Project CompanyFinancial

Institute

Local

Government

Project CompanyFinancial

Institute

Platform

Company

(e.g. UDIC)

debt

Private

Partner

debt

investShareholder agreement

contract

designate

investinvest

contract

Shareholder agreement

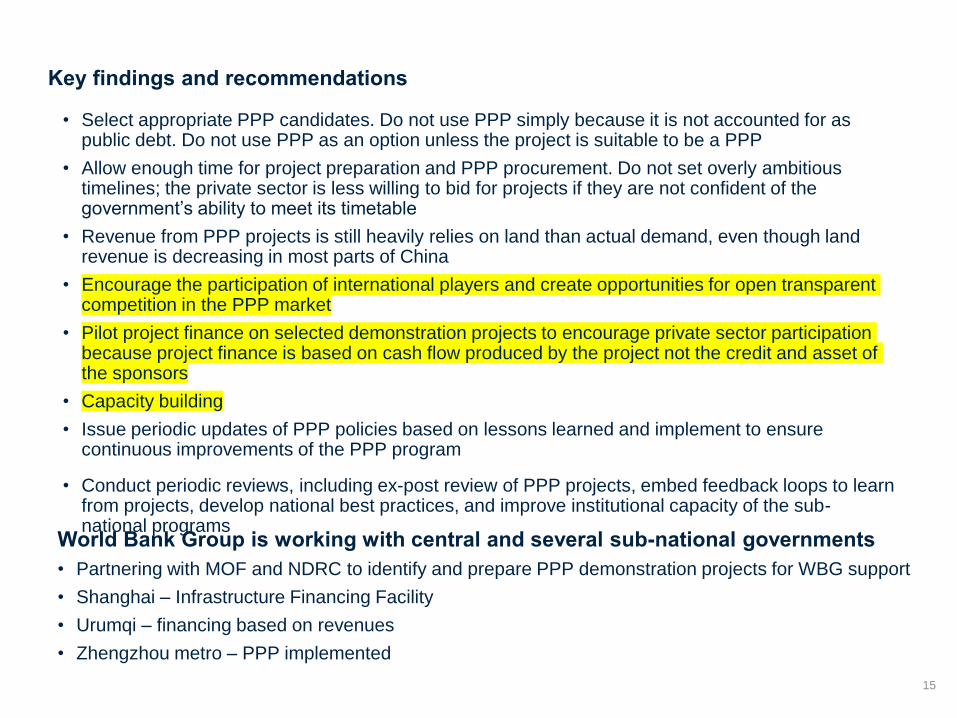

Key findings and recommendations

15

• Select appropriate PPP candidates. Do not use PPP simply because it is not accounted for as public debt. Do not use PPP as an option unless the project is suitable to be a PPP

• Allow enough time for project preparation and PPP procurement. Do not set overly ambitious timelines; the private sector is less willing to bid for projects if they are not confident of the government’s ability to meet its timetable

• Revenue from PPP projects is still heavily relies on land than actual demand, even though land revenue is decreasing in most parts of China

• Encourage the participation of international players and create opportunities for open transparent competition in the PPP market

• Pilot project finance on selected demonstration projects to encourage private sector participation because project finance is based on cash flow produced by the project not the credit and asset of the sponsors

• Capacity building

• Issue periodic updates of PPP policies based on lessons learned and implement to ensure continuous improvements of the PPP program

• Conduct periodic reviews, including ex-post review of PPP projects, embed feedback loops to learn from projects, develop national best practices, and improve institutional capacity of the sub-national programs

World Bank Group is working with central and several sub-national governments

• Partnering with MOF and NDRC to identify and prepare PPP demonstration projects for WBG support

• Shanghai – Infrastructure Financing Facility

• Urumqi – financing based on revenues

• Zhengzhou metro – PPP implemented