china’sinsurancemarket:opportunity,competitionand … · with the people’s bank of china during...

TRANSCRIPT

China's Insurance Market: Opportunity, Competition andMarket Trends

by Yiming Shen�

China represents the largest insurance market in the world that is both closed and under-served. With more than 20 per cent of the world's population and a high level of domesticsavings, China is considered an ideal opportunity for foreign insurers: one quarter of theworld's population accounting for less than 1% of its premium spending. For the past twodecades, the highly centralized planned economic system and the state social insurancesystem has operated to prevent commercial insurance from ful®lling the role that it plays incountries where insurance is highly developed. This situation is now changing. While theinsurance industry in China is still, in essence, a new and developing industry (having justunder two decades of insurance experience as compared to more than a hundred years'experience for developed countries). Chinese regulatory authorities predict the market willdouble by 2004 to more than $30 billion. From 1992 until 1999 only nine foreign companieswere granted licences and their operations were restricted to the city of Shanghai, with theexception of one American company permitted to operate in Guangzhou. In 1999, four moreforeign companies were selected by the government for business in China.1 In November1999 the U.S. Government completed bilateral talks on China's accession to the World TradeOrganization (WTO). It is expected that China's WTO accession will lead to an elimination ofgeographic restrictions, greater market access, and more lines of business permitted forforeign insurers over the next several years. Life insurers strongly praised the agreement, asAmerican Council of Life Insurance President Carroll Campbell said, `̀ it gives insurers theopportunity to grow into a new and largely untapped market.''2

This article starts with a general introduction of the Chinese insurance market withstatistic reports, that offer a basis for further analysis of market pro®les and prospects. Thesecond part it provides an overview of the market competition status in China with specialfocus on the entry and operating issues for foreign insurers. The third part summarizes theinsurance aspects of the U.S.±China WTO agreement and predicts its implementation. Thearticle concludes with a general discussion of relevant legal and regulatory issues, followed bya projection of development trends and strategic recommendations to foreign insurers whowant to tap this emerging market.

� Dr Shen LL.B., LL.M. (Fudan University, China) JSD (Osgoode Hall Law School, Canada), is a Director andAssociate Counsel at Manulife International based in Hong Kong. Prior to joining Manulife Financial, he internedwith the People's Bank of China during 1995±1996.

1 In April 1999, licences were awarded to four companies ± the Chubb Group and John Hancock Mutual LifeInsurance of the U.S., the U.K.'s Prudential and Canada's Sun Life Assurance Company.

2 See S. Brostoff, `Insurers Praise Pact For China To Enter WTO', National Underwriter (Life & Health/Financial Services Edition), 22 November 1999.

The Geneva Papers on Risk and Insurance Vol. 25 No. 3 (July 2000) 335±355

# 2000 The International Association for the Study of Insurance Economics.

Published by Blackwell Publishers, 108 Cowley Road, Oxford OX4 1JF, UK.

1. Market pro®le3

The emergence of powerful local players and the arrival of foreign insurers aretransforming China's insurance industry at a remarkable speed. The industry is gearing upto meet the unprecedented demand for insurance generated by continuing market reforms. Itis estimated that the market could reach RMB 250 billion (US$ 30.1 billion) by the year 2004,and RMB 420 billion (US$ 50.6 billion) by the year 2010, with projected annual increases inthe region of 20 to 30 per cent and possibly even more for life insurance. Even though themarket share captured by foreign insurers is not expected to exceed 5 per cent by year 2000,this tiny slice of the Chinese insurance market could be worth RMB 10 billion (US$ 1.2billion) to RMB 12.5 billion (US$1.5 billion) annually ± a highly attractive prospect forforeign insurers with saturated domestic markets.

The insurance industry has shown rapid growth within the past few years, particularly inthe life insurance market, as Chinese citizens' average annual income grew an average of 23per cent during the past four years. In addition, the increase in private businesses, coupledwith the decline of job opportunities in the state sector as a direct result of China's statereforms, has sparked people's interest in buying all types of insurance ranging from propertyto life. In 1998, the total amount of life and property insured was RMB 124.73 billion (US$15.06 billion). China's insurance sector reported a premium income of RMB139.3 billionyuan (US$17.07 billion) in 1999, up 10 per cent from 1998.4 Among these premiums, 52.1billion yuan was from property insurance, up nearly 3 per cent from 1998, and 87.2 billionyuan from life and health insurance, up 15 per cent. Insurers paid out 28 billion yuan inliabilities on property policies and 23 billion yuan for life and health policies. Ma Yongwei,chairman of the China Insurance Regulatory Commission (`̀ CIRC''), attributed the stablegrowth of the insurance sector to the regulators' efforts to improve market order. China'sinsurance sector is expected to earn total annual premium of US$30 billion by the year 2004,as estimated by Wu Xiaoping, Vice-Chairman of CIRC.5

3 See P. Lim and E. Bai, `China ± Insurance Industry', National Trade Data Bank, Market Reports, 1 August1998.

4 `China's Insurance Sector Reports Double Digit Premium Growth', Asia Pulse (26 January 2000).5 `China Insurance Premium will reach $30 billion at 2004' (12 December 1999) on line: khttp:dailynews.-

muzi.coml

Table 1:Major China Economic Indicators (1995±1999)

YearGDP growth

(%)GNP (US$)

(billion)Per capitaGNP (US$)

1995 10.2 686 571.51996 9.7 812.6 667.41997 8.8 893.3 726.11998 8 981 7851999 7.8 1100 871

Source: China Statistical Yearbook.

# 2000 The International Association for the Study of Insurance Economics.

336 SHEN

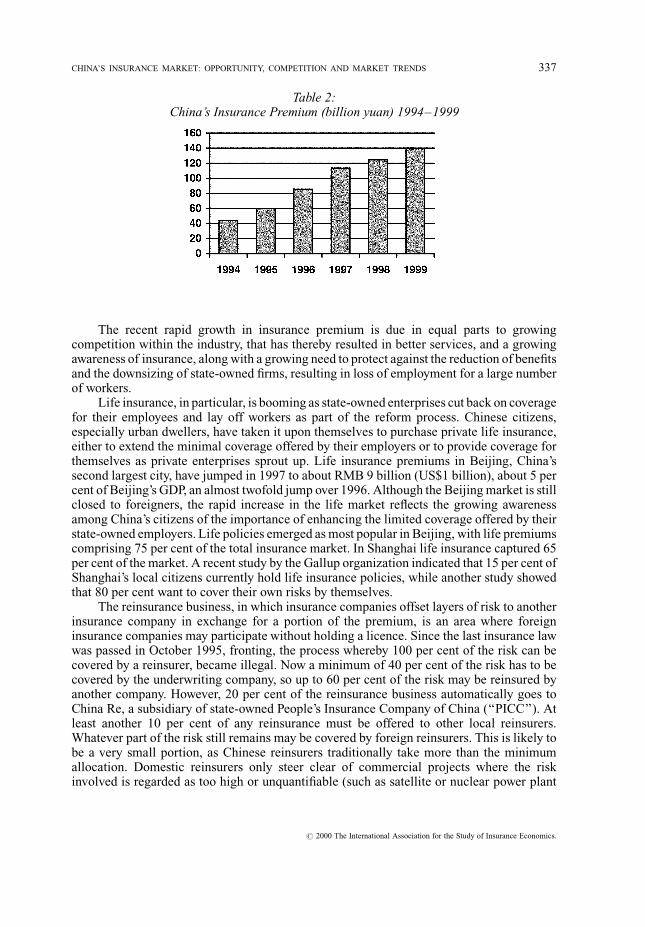

The recent rapid growth in insurance premium is due in equal parts to growingcompetition within the industry, that has thereby resulted in better services, and a growingawareness of insurance, along with a growing need to protect against the reduction of bene®tsand the downsizing of state-owned ®rms, resulting in loss of employment for a large numberof workers.

Life insurance, in particular, is booming as state-owned enterprises cut back on coveragefor their employees and lay off workers as part of the reform process. Chinese citizens,especially urban dwellers, have taken it upon themselves to purchase private life insurance,either to extend the minimal coverage offered by their employers or to provide coverage forthemselves as private enterprises sprout up. Life insurance premiums in Beijing, China'ssecond largest city, have jumped in 1997 to about RMB 9 billion (US$1 billion), about 5 percent of Beijing's GDP, an almost twofold jump over 1996. Although the Beijing market is stillclosed to foreigners, the rapid increase in the life market re¯ects the growing awarenessamong China's citizens of the importance of enhancing the limited coverage offered by theirstate-owned employers. Life policies emerged as most popular in Beijing, with life premiumscomprising 75 per cent of the total insurance market. In Shanghai life insurance captured 65per cent of the market. A recent study by the Gallup organization indicated that 15 per cent ofShanghai's local citizens currently hold life insurance policies, while another study showedthat 80 per cent want to cover their own risks by themselves.

The reinsurance business, in which insurance companies offset layers of risk to anotherinsurance company in exchange for a portion of the premium, is an area where foreigninsurance companies may participate without holding a licence. Since the last insurance lawwas passed in October 1995, fronting, the process whereby 100 per cent of the risk can becovered by a reinsurer, became illegal. Now a minimum of 40 per cent of the risk has to becovered by the underwriting company, so up to 60 per cent of the risk may be reinsured byanother company. However, 20 per cent of the reinsurance business automatically goes toChina Re, a subsidiary of state-owned People's Insurance Company of China (`̀ PICC''). Atleast another 10 per cent of any reinsurance must be offered to other local reinsurers.Whatever part of the risk still remains may be covered by foreign reinsurers. This is likely tobe a very small portion, as Chinese reinsurers traditionally take more than the minimumallocation. Domestic reinsurers only steer clear of commercial projects where the riskinvolved is regarded as too high or unquanti®able (such as satellite or nuclear power plant

Table 2:China's Insurance Premium (billion yuan) 1994±1999

# 2000 The International Association for the Study of Insurance Economics.

CHINA'S INSURANCE MARKET: OPPORTUNITY, COMPETITION AND MARKET TRENDS 337

projects). Foreign reinsurers face other ®nancial disincentives including a tax of 8.55 per centon any business that goes offshore. China's non-life insurance market, on which reinsurersmust subsist, only amounted to RMB 45 billion in 1998. In the absence of a sophisticatedreinsurance infrastructure in China, a large number of domestic non-life insurance ®rms donot reinsure at all. Foreign reinsurers would like to get involved, but cannot because the lawprevents them from engaging in local currency or RMB business. Due to the fact that theChinese local currency is not convertible, the reinsurance business is also not convertible onthe international market. Catastrophe is one coverage in which local underwriters have hugeexposure in local currency and must absorb heavy ¯ooding insurance losses every year. Mostcatastrophe reinsurance is for foreign currency exposure. China's reinsurance business isfuelled by the growth in large-scale projects in which multinational companies have beendeeply involved, especially in the construction, energy, satellite, aviation, and power sectors.The bottom line is that foreign reinsurers must make do with China's non-life, foreigncurrency-denominated insurance business, which was a ballpark US$1 billion at the end of1998.

Actuarial services are still primitive, with many companies going to Hong Kong foractuarial expertise. The brokerage market is still restricted, as there is only one licensedforeign broker, U.K.-based Sedgwick Group, along with several Chinese brokers.

2. Competition in China's insurance market

Domestic competition

Insurance in China is still dominated by domestic companies, due largely to theprotectionist policies of the central government. Of the 13 domestic companies, the top three,PICC, China Paci®c and Ping An are national companies with the freedom to operate all overChina. Other local companies such as Huatai and Guotai have more restrictive businesslicences, limiting them to particular regions.

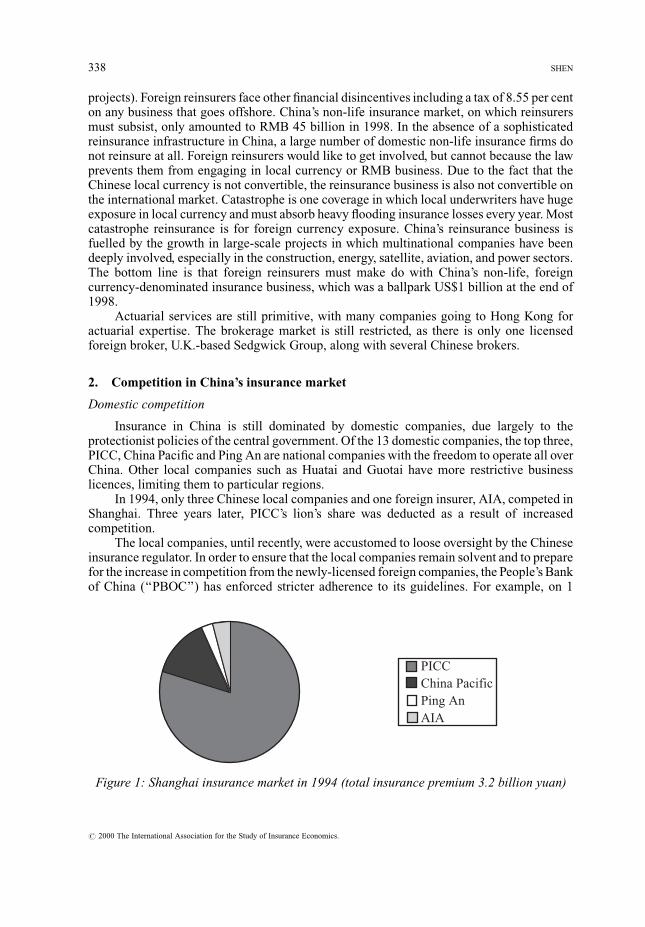

In 1994, only three Chinese local companies and one foreign insurer, AIA, competed inShanghai. Three years later, PICC's lion's share was deducted as a result of increasedcompetition.

The local companies, until recently, were accustomed to loose oversight by the Chineseinsurance regulator. In order to ensure that the local companies remain solvent and to preparefor the increase in competition from the newly-licensed foreign companies, the People's Bankof China (`̀ PBOC'') has enforced stricter adherence to its guidelines. For example, on 1

PICCChina PacificPing AnAIA

Figure 1: Shanghai insurance market in 1994 (total insurance premium 3.2 billion yuan)

# 2000 The International Association for the Study of Insurance Economics.

338 SHEN

October 1997, the domestic insurers signed an agreement stating that they will followguidelines on premiums, agents' commissions and operational limitations. Althoughcommission rates were limited to 10 per cent of the premium, actual rates paid to agentswere much higher, due to some cut-throat competition. Later in the year, on 1 December,PBOC set new life interest rates that fell below the national savings interest rate, and for the®rst time, required all Chinese insurers to conform to those rates. Returns on life productspreviously averaged between 7.5 per cent and 9.0 per cent, two to three percentage pointshigher than the interest paid on a one-year savings deposit. Further rate cuts in early 1998 havehad little impact on the sales of life insurance policies, but they have squeezed the potential forcorporate pro®ts.

Domestic companies still enjoy certain freedoms unavailable to foreign companies. Forexample, domestic companies are able to offer various kinds of products, with a minimalapproval process, whereas foreign companies are required to submit an application for eachnew product. Furthermore, vehicular insurance, a lucrative market due to the growth inprivate ownership and mandatory compliance by all owners, is off-limits to foreigncompanies. Vehicular insurance accounted for 55 per cent of PICC Property's total income,and they captured 80 per cent of the domestic market for auto insurance in 1997.

People's Insurance Company of China

Since its resurrection in 1979, the People's Insurance (Group) Company (PICC) hascontinuously dominated the insurance industry throughout China. After the promulgation ofthe 1995 Insurance Law, PICC divided its operations into three divisions: life, non-life andreinsurance. Rather than suffer from the competition of foreign companies into the Shanghailife market, PICC has actually bene®ted as their total premiums have risen, despite the loss inmarket share. PICC (Life) captured 44.7 per cent of the Shanghai life market in 1997,compared to 79.7 per cent in 1994. Premium income, in both life and general grew from RMB1.1 billion (US$133 million) in 1991 to RMB 6.7 billion (US$810 million) in 1997.

Taking a cue from its foreign competitors, PICC is seeking growth by improving itsservices and offering more products. In 1997, PICC (Life) Shanghai recently expanded itsbusiness distribution by signing agreements with local banks empowering them to provideservices on behalf of PICC.

As the largest insurer in China, PICC was also involved in covering US $57 million worthof risk in the Three Gorges Dam project, the world's largest hydroelectric project. PICC was

PICCChina PacificPing AnAIATian AnDa Zhongother

Figure 2: Shanghai insurance market in 1997 (total premium income 9 billion yuan)

# 2000 The International Association for the Study of Insurance Economics.

CHINA'S INSURANCE MARKET: OPPORTUNITY, COMPETITION AND MARKET TRENDS 339

given a BBB credit rating by Standard & Poor's Corporation and was recently listed as the 15thlargest insurance company in the world.

Ping An Insurance Company of China

Headquartered in Shenzhen and founded in 1988, Ping An has been quick to follow inPICC's footsteps. It has already surpassed PICC as the number one life insurer in Beijing andShenzhen. In addition to overtaking China Paci®c Insurance Company as the number twoinsurer in China, Ping An possesses the unusual ability to deal in other ®nancial services.Because it began operations as an insurance company offering other types of ®nancialservices, Ping An retained these rights although the Insurance Law of 1995 strictly prohibitsthis practice. Consequently, Morgan Stanley and Goldman Sachs have each taken a 6 per centstake in Ping An Insurance Company. Morgan Stanley views Ping An as a strategic partnerand is working with Ping An to research asset management, human resource management andimprove products. Ping An has also set up a joint venture company with Lincoln National todevelop an annuity project. Ping An's chairman states that Ping An, unlike PICC, welcomescompetition, as Ping An itself was founded in order to offer a choice to the then monopolisticPICC.

China Paci®c Insurance Company

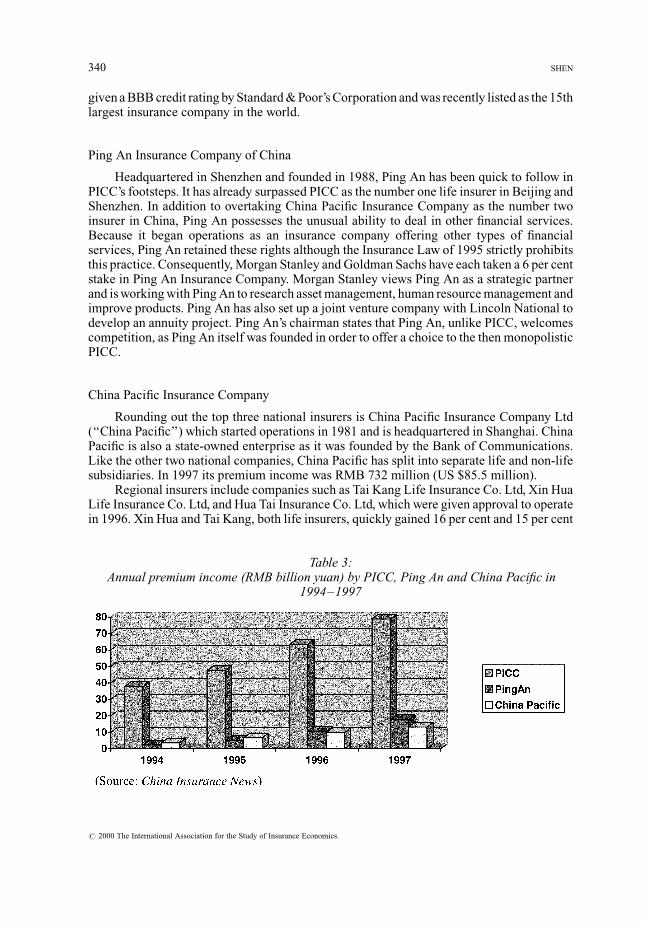

Rounding out the top three national insurers is China Paci®c Insurance Company Ltd(`̀ China Paci®c'') which started operations in 1981 and is headquartered in Shanghai. ChinaPaci®c is also a state-owned enterprise as it was founded by the Bank of Communications.Like the other two national companies, China Paci®c has split into separate life and non-lifesubsidiaries. In 1997 its premium income was RMB 732 million (US $85.5 million).

Regional insurers include companies such as Tai Kang Life Insurance Co. Ltd, Xin HuaLife Insurance Co. Ltd, and Hua Tai Insurance Co. Ltd, which were given approval to operatein 1996. Xin Hua and Tai Kang, both life insurers, quickly gained 16 per cent and 15 per cent

Table 3:Annual premium income (RMB billion yuan) by PICC, Ping An and China Paci®c in

1994±1997

# 2000 The International Association for the Study of Insurance Economics.

340 SHEN

market shares respectively in Beijing during the ®rst half of 1997. Xin Hua Insurance even hasa website selling life policies.

Foreign players in China6

At the beginning of 1998, there were a total of 106 foreign insurance companies from 15foreign cities and regions with 189 representative of®ces in China waiting for regulatoryapproval. Most of the companies are from Japan, followed by European companies. Mostrepresentative of®ces are located in big cities such as Beijing, Shanghai, Guangzhou,Shenzhen, Qingdao, Dalian and Tianjin.

The China Insurance Regulatory Commission claims that the sector will open onceChinese companies have matured enough to compete fairly with their foreign counterparts. Inaddition, the CIRC also wants to build up its own supervision system and set up industryguidelines. Since granting licences to American International Assurance Company Ltd. andAIU Insurance Company, member companies of American International Group (AIG), in

6 See Goldman Sachs, `China Insurance Market', 1998 [unpublished report].

Figure 3: Life insurance market share by PICC, Ping An and China Paci®c in 1997

Figure 4: Property and casualty insurance market share by PICC, Ping An and China Paci®cin 1997

# 2000 The International Association for the Study of Insurance Economics.

CHINA'S INSURANCE MARKET: OPPORTUNITY, COMPETITION AND MARKET TRENDS 341

Guangzhou, the government has recently only granted licences to companies in Shanghai'sPudong New District, which has been declared a test site for ®nancial experiments. This areais also being developed as China's ®nancial centre, so banks and insurance companies arerequired to set up home bases there. Consequently, the CIRC (Shanghai) will step upsupervision of the insurance industry. Guangzhou, by contrast, has been designated amanufacturing centre and may be best considered as a secondary entry point for companiesfollowing a licence granted ®rst in Shanghai.

China realizes that opening its insurance market to more foreign competition is arequisite for eventual entry into the World Trade Organization. However, the opening of themarket may proceed slowly as China embarks on an ambitious three-year plan to overhaul its®nancial sector in order to reduce debt risk and improve ®nancial management. China cannotdeny that foreign companies have helped to promote the reform of the entire insurance systemand advance the development of the insurance market. Not only have foreign companiesbrought in new business products, marketing systems, and management experience, they havealso helped to increase total insurance premiums for the industry. It remains to be seenwhether China will reconsider the positive bene®ts of competition and weigh them against itscurrent conservative policies.

Foreign companies are all vying for the coveted licence to provide underwriting servicesin China. So far, at least one company from each of the large countries has a licence. Decisionsare politically motivated as the State Council seems determined to spread out licences infairness to the different countries. In order to secure a licence, companies undertake activitiesto show their long-term commitment to China. When coming to China foreign insurers bring awealth of information, experience, and know-how which China's young and immatureinsurance market desperately needs. In their bids to land operating licences many foreigninsurers have tried to make this point, and taken measures to address it by setting up orendowing various insurance training programs and institutions. The Chinese government usesvarious criteria in deciding which foreign ®rms will be granted a licence, and one of theimportant ones is a demonstrated commitment to the country by the applicants. Hopefulforeign insurers have attempted to demonstrate their commitment to China by gettinginvolved with these training institutes, but not all have restricted themselves quite so narrowly.Other means of building goodwill have included investing in Chinese industries andcontributing to museums and schools. For example, one company has invested money inboth energy and infrastructure projects. Another has also provided free medical treatment toimpoverished children. Yet a third company has provided money for university scholarshipfunds while another one has set up investment funds for investing in China. In China, thebuilding of good relations and goodwill is essential at all stages of doing business, and if aforeign insurer is to be successful in the Chinese market it cannot afford to ignore this way ofdoing business. After China's accession to the WTO, it is likely that licences will be given onthe basis not of a political trade-off, but according to size, international experience, businessplan and overall competence.

There are restrictions on the type of investment vehicle foreign insurers can use to enterthe Chinese market. A foreign insurance company is allowed to incorporate as a joint stocklimited company. It is also allowed to take the form of either a branch of®ce or an equity jointventure. However, the relevant government departments are said to be reluctant to allowforeign life insurance companies to establish branches in China, preferring to see themestablish joint ventures or take up equity shares in joint stock insurers. The government has,however, continued to allow non-life insurers to set up branch of®ces, although they arerestricted to underwriting policies for foreign-invested operations.

# 2000 The International Association for the Study of Insurance Economics.

342 SHEN

Equity investment in Chinese domestic joint stock insurers will conceivably give foreigncompanies a simpler and quicker route into the market, as approval for equity companies isrelatively more rapid than that for joint ventures. Currently, the maximum equity stakepossible for foreign insurance companies in joint ventures is 50 per cent, and at least one of the

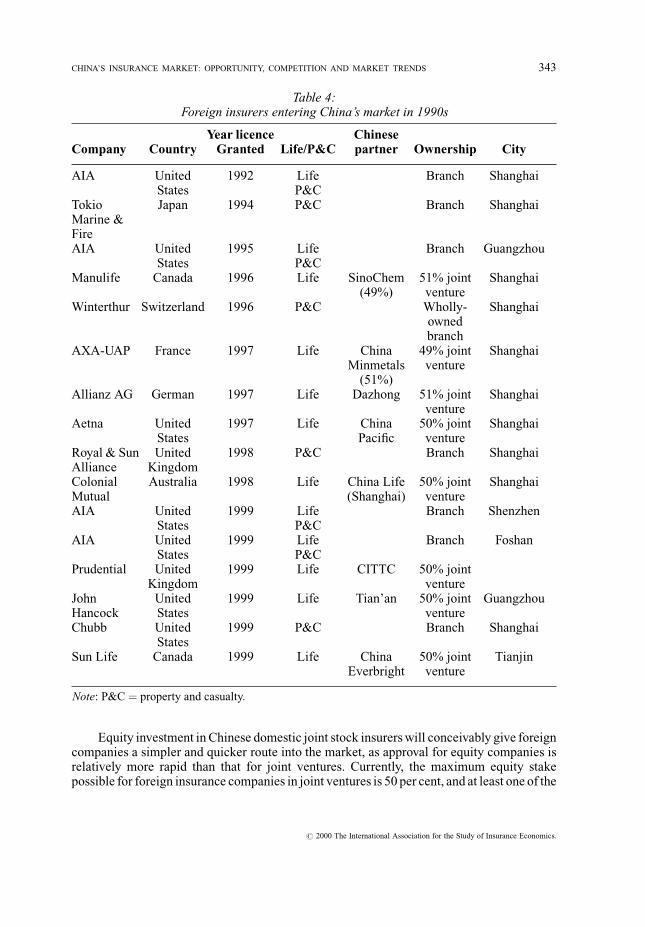

Table 4:Foreign insurers entering China's market in 1990s

Company CountryYear licence

Granted Life/P&CChinesepartner Ownership City

AIA UnitedStates

1992 LifeP&C

Branch Shanghai

TokioMarine &Fire

Japan 1994 P&C Branch Shanghai

AIA UnitedStates

1995 LifeP&C

Branch Guangzhou

Manulife Canada 1996 Life SinoChem(49%)

51% jointventure

Shanghai

Winterthur Switzerland 1996 P&C Wholly-ownedbranch

Shanghai

AXA-UAP France 1997 Life ChinaMinmetals

(51%)

49% jointventure

Shanghai

Allianz AG German 1997 Life Dazhong 51% jointventure

Shanghai

Aetna UnitedStates

1997 Life ChinaPaci®c

50% jointventure

Shanghai

Royal & SunAlliance

UnitedKingdom

1998 P&C Branch Shanghai

ColonialMutual

Australia 1998 Life China Life(Shanghai)

50% jointventure

Shanghai

AIA UnitedStates

1999 LifeP&C

Branch Shenzhen

AIA UnitedStates

1999 LifeP&C

Branch Foshan

Prudential UnitedKingdom

1999 Life CITTC 50% jointventure

JohnHancock

UnitedStates

1999 Life Tian'an 50% jointventure

Guangzhou

Chubb UnitedStates

1999 P&C Branch Shanghai

Sun Life Canada 1999 Life ChinaEverbright

50% jointventure

Tianjin

Note: P&C � property and casualty.

# 2000 The International Association for the Study of Insurance Economics.

CHINA'S INSURANCE MARKET: OPPORTUNITY, COMPETITION AND MARKET TRENDS 343

partners must be a Chinese insurance company.7 As for equity investment, current policyallows foreign insurers an ownership stake of up to 25 per cent in domestic insurance com-panies with, however, each individual overseas insurer restricted to a maximum 5 per centshare.8

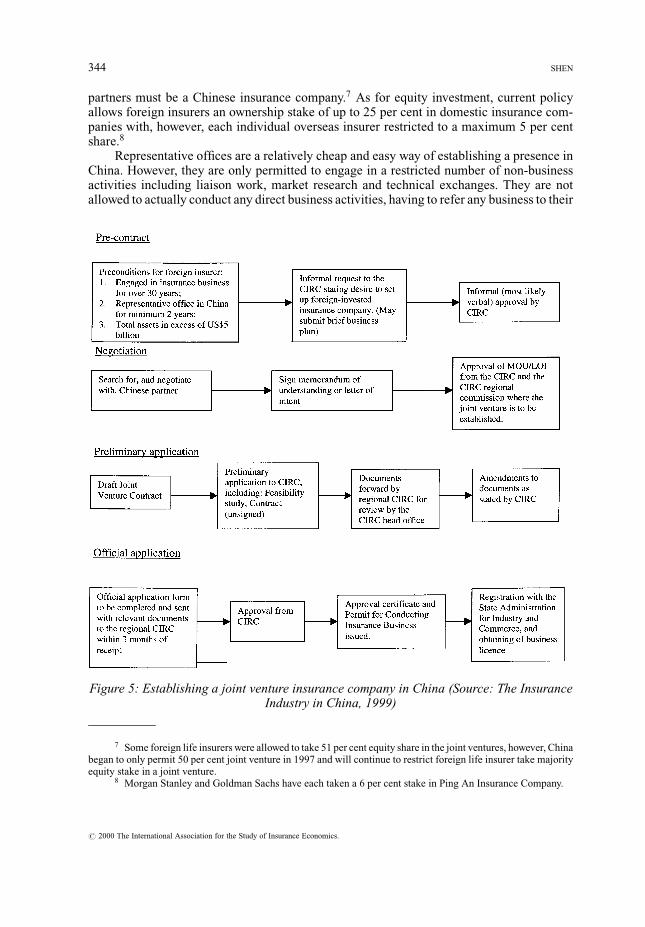

Representative of®ces are a relatively cheap and easy way of establishing a presence inChina. However, they are only permitted to engage in a restricted number of non-businessactivities including liaison work, market research and technical exchanges. They are notallowed to actually conduct any direct business activities, having to refer any business to their

Figure 5: Establishing a joint venture insurance company in China (Source: The InsuranceIndustry in China, 1999)

7 Some foreign life insurers were allowed to take 51 per cent equity share in the joint ventures, however, Chinabegan to only permit 50 per cent joint venture in 1997 and will continue to restrict foreign life insurer take majorityequity stake in a joint venture.

8 Morgan Stanley and Goldman Sachs have each taken a 6 per cent stake in Ping An Insurance Company.

# 2000 The International Association for the Study of Insurance Economics.

344 SHEN

parent companies. The incentive for establishing a representative of®ce is the legalrequirement that a foreign insurer to maintain a representative of®ce in the country for aminimum of two years before being eligible to apply to set up formal business operations.

Equity joint ventures are limited liability companies incorporated and registered inChina, having legal person status and their own independent management structure. TheChinese and foreign parties in equity joint ventures share the risks and pro®ts in proportion totheir respective capital contributions in the joint venture. As Chinese authorities have clearlyindicated that all future foreign life insurance operations must be in the form of a joint venture,foreign insurers have been obligated to seek out prospective local partners to boost theirchances for approval. No clear written rules governing the establishment of joint ventureinsurance companies exist. When the ®rst Sino-foreign joint venture insurance company,Manulife-SinoChem Life Insurance Company Limited (formerly known as Zhong Hong LifeInsurance Company Limited), was established in November 1996, its approval set many of theprecedents for subsequent applications by foreign life insurers. Figure 5 brie¯y summarizesthe procedures involved as derived from the Manulife-SinoChem precedent.

3. Insurance aspects of the U.S.±China WTO agreement9

On 15 November 1999, World Trade Organization Director-General Mike Moorewarmly welcomed the U.S.±China accord on Chinese accession to the WTO. Althoughsubstantial work remains before China becomes a member of the organization, the DirectorGeneral expressed con®dence that this work could be completed in a relatively short period oftime. The bilateral agreement on market access is signi®cant, Mr Moore said, given the sizeand importance of the two economies:

`̀ This is a major step forward in China's accession to the WTO. I have said many timesthat we are not a World Trade Organization until China has joined. China must still reachagreement with other member governments and we need to complete importanttechnical talks before China can take her rightful place at the table of great tradingnations. A door to history has been opened and now member governments must walkthrough it together.''10

The following is a summary of news releases from the White House, American Councilof Life Insurance and CIRC, and information placed on www.china-insurance.com (aChinese language website on insurance in China) concerning China's commitment to openingits insurance market on accession to the WTO. Some uncertainties still remain, and awaitfurther clari®cation by the CIRC.11

Number of licences

There will be no economic needs testing or numeric/quantitative restrictions on thenumber of operating licences to be issued to foreign insurance companies on accession.

9 This section was presented by the author at Global Insurance Forum (American Council of Life Insurance) on6 December 1999 in San Francisco.

10 Press release of the World Trade Organization (emphasis added). On line: khttp://www.wto.org/wto/new/press148.html

11 Clifford Chance, Asian Financial Market Newsletter (December 1999 edition).

# 2000 The International Association for the Study of Insurance Economics.

CHINA'S INSURANCE MARKET: OPPORTUNITY, COMPETITION AND MARKET TRENDS 345

Licencing requirements:

In order to qualify for a licence, foreign insurers must meet the following criteria: (a) 30years of experience as an insurer; (b) US$ 5 billion in total assets; and (c) a representativeof®ce in China established for the past two years.

Operating licences will not, however, be issued in an uncontrolled manner; the CIRC willutilize `̀ prudence'' based assessments in conjunction with the qualifying requirements toprovide a further re®ned evaluation of which foreign insurers will be suitable marketparticipants.

Geographic restrictions

Until now, life joint ventures and non-life branches have been restricted to operating inShanghai and Guangzhou, though China has recently indicated that it is prepared to open the®rst group of cities: Dalian, Chengdu, Chongqing, Fuzhou, Xiamen, Ningbo, Wuhan,Shenzhen, Tianjin, Shenyang, and Beijing.

Immediately on accession, foreign non-life insurers will be allowed to write `̀ large-scalerisks'' on a nationwide basis. Cities which American insurance companies are primarilyinterested in will be opened within two to three years after accession. Opening the market inthe north-western region will be given priority.

All geographic restrictions on the market for foreign insurers are to be eliminated withinthree years of China's accession.

Ownership and form of establishment

Life insurers may have a 50 per cent joint venture partnership with a Chinese partner oftheir own choice upon accession (some Chinese reports suggest that 51 per cent may beavailable within ®ve years). Non-life insurers may have a 51 per cent joint venture or branchesupon accession, and 100 per cent wholly owned subsidiaries within two years after accession.Internal branches will be permitted consistent with the phase-out of geographic restrictions.

Scope of business/insurance lines

Foreign life insurers may sell individual products to both Chinese and foreign nationalsupon accession. Foreign non-life insurers are currently only allowed to write business forforeign invested enterprises. Restrictions on the scope of business and geographic operationsof foreign invested property insurance companies will be relaxed gradually. For example, theycan insure large-scale commercial risks with no geographic restrictions and provide insurancefor enterprises abroad, property insurance, related liabilities insurance and credit insurancefor foreign ®rms upon accession. Foreign insurers may sell health insurance within four yearsof China's accession. Foreign insurers may sell pension and group lines of insurance within®ve years of China's accession.

Reinsurance

This market will be fully opened (100 per cent, with no restrictions) upon accession. It isnot clear whether this refers to abolishing restrictions on reinsuring offshore or allowing 100per cent ownership of subsidiaries/branches in China by foreign reinsurers, or both. The CIRC

# 2000 The International Association for the Study of Insurance Economics.

346 SHEN

is reported to be considering lowering the statutory reinsurance rate (20%) and preference forreinsuring with domestic companies, as well as establishing a national reinsurance market,possibly in Shanghai, with the participation of domestic and foreign insurers, reinsurancecompanies and brokers.

Grandfathering

China will grandfather all existing current market access and activities includingownership in insurance sectors. This will protect existing foreign insurance services in China,including those operating under contractual or shareholder agreements or a licence, fromrestrictions as Chinese commitments phase in.

Some insurers comment that the elimination of geographical restrictions is crucial andwill have a huge effect on the development of the market. However, most insurers think thebiggest impact will be the expanded scope for insurance business. The Agreement opens upgroup, health and pension lines within ®ve years. These lines account for 85 per cent of totalpremiums in China. Opening group insurance lines is particularly important because bene®tsin China are commonly supplied through employers, especially for large state-ownedenterprises. It will provide foreign insurers tremendous opportunities in this particular nichemarket after China's WTO accession, since most Chinese companies would rather use foreigninsurers like AIG, or Manulife, on employee bene®ts than their own domestic insurers.12 IfChina joins the WTO as expected, possibly by the end of 2000 will have to make substantialchanges to its insurance regulations, particularly those regulations governing access to themarket by foreign insurers. In the same way that Mexican regulators had to end barriers toforeign access to Mexico in the years following the implementation of the North AmericanFree Trade Agreement in 1994, Chinese regulatorswill have to remove many of the restrictionson foreign insurers. Currently, a handful of foreign insurers have limited licences to sellinsurance in a few areas of the country. After China's accession to the WTO, the regulators willlikely, among other things, have togive foreign insurers access to all areas of Chinawithin threeyears, permit 100 per cent foreign ownership of domestic insurers within two years and endwithin two years the 20 per cent compulsory reinsurance cessions to a Chinese state-ownedreinsurer for companies that are fully foreign-owned. `̀ There will be a huge change'',commented Kevin Cronin, president and chief executive of®cer of the International InsuranceCouncil.13 Already, the CIRC is making changes in order to bring domestic and foreigninsurers and brokers into compliancewith its existing regulations. In conclusion, the CIRC hasmade it clear that during the forthcoming ®ve years licensed foreign insurers in China will begiven national treatment in terms of product variety, clientele and operating regions.

4. Transparent regulation and fair regulatory standards

The new regulatory regime began in November 1998 when the CIRC took over insuranceregulation from the People's Bank of China. The new regulator has a much larger staff than theinsurance regulator at the PBOC, and many of the staff have insurance experience. UntilNovember 18, 1998, in accordance with the stipulations of the Insurance Law, the PBOC was

12 See Gene Linn, `US Insurers Expected To Bene®t When China Wins WTO Admittance', Journal ofCommerce (3 May 1999).

13 Gavin Souter, `Changes seen in China; Regulatory crackdown anticipates WTO membership', BusinessInsurance (14 February 2000).

# 2000 The International Association for the Study of Insurance Economics.

CHINA'S INSURANCE MARKET: OPPORTUNITY, COMPETITION AND MARKET TRENDS 347

the primary authority in charge of regulating the insurance industry. However, in a move toimplement the principle of separate regulatory and business functions for government unitsarticulated during the National People's Congress in March 1998, the PBOC's powers over theinsurance industry were withdrawn and transferred to the newly created China InsuranceRegulatory Commission. Created under the State Council, the CIRC is mandated to formulatepolicy for the insurance industry, enforce laws, penalize wrongdoing, protect the rights andinterests of policyholders and establish a risk evaluation system. It will therefore beresponsible for vetting application to establish new insurance institutions and supervisingexisting domestic and foreign-invested insurance companies. The new regulator has eightdepartments, including international, legislative, life insurance and property insurancedepartments, and employ approximately 100 of®cials at its headquarters in Beijing. Mostof those of®cials come from the former insurance department of the PBOC and the PICC.14

The creation of a specialized body to supervise the insurance industry has been welcomed byall players as it promises to centralize and simplify regulation. Under the old system thePBOC had primary responsibility for overseeing the industry, but the Ministry of Finance andthe State Auditing Administration also had some input, contributing to a sometimesfragmented and inef®cient regulatory regime. With one single specialized regulator thesystem should become more ef®cient and having the CIRC report directly to the State Councilshould also serve to raise the pro®le of insurance at the highest levels of government.

There is an urgent need for effective implementation of the Insurance Law,15 and for thepromulgation of detailed implemention of regulations to enhance the enforceability of the Lawand establish an integrated insurance market in China. The Insurance Law was the culminationof approximately ®ve years' work by various committees which involved liaison and in-depthobservations and visits to some 13 countries to study various approaches to insurancelegislation in both Western and Asian environments. The Insurance Law was the ®rst statutepassed inan effort tobring order to the country's commercial insurance operations, and markedthe ®rst step in constructing a much-needed legal framework for the industry.

Overall, most people who have studied the ®nal result give it high marks as a major stepforward in transforming insurance regulation in China towards: (1) international standards ofaccountability of management; (2) balance in protecting insured and insurer rights; and (3)de®ning the role of the regulator.16

As a senior executive of a major Chinese insurance company noted, `̀ the competitive-ness of Chinese domestic insurers can only be achieved when a properly regulated marketwhich embraces fair competition rules is in place.'' The Insurance Law provides thatinsurance companies shall observe the principle of fair competition (Article 7). It prohibitsinsurance companies from engaging in improper competition by promising to pay thepolicyholders, insured and bene®ciaries premium rebates and other bene®ts in addition tothose provided in the insurance contracts (Article 105). It also provides that the basic terms forpolicies and premium rates for the main types of commercial insurance shall be set andregulated by the Supervisory Authority. The terms of policies and premium rates provided bythe insurance companies for other types of insurance shall be reported to the SupervisoryAuthority for the record (Article 106).

14 A. Allen, The Insurance Industry in China (Hong Kong: Asia Information Associates Ltd, 1999) at 10.15 The Insurance Law was promulgated on 30 June 1995 at the Fourteenth Session of the Standing Committee

of the 8th National People's Congress of China and became effective on 1 October 1995.16 Ian Lancaster (Chubb China Operation), `Insurance Law Commentary', article online: www.chubb.com/

China/laws/inslaw-commentary.htm.

# 2000 The International Association for the Study of Insurance Economics.

348 SHEN

It is widely accepted that the competition rules are unlikely to be complied with and awell-regulated market cannot be expected to emerge if there are no follow-up procedures ordetailed implemention guidelines in place. For example, the liquidity requirements promul-gated in the Insurance Law have not yet been effectively implemented. In the words of anexecutive director of a major Chinese insurance company, `̀ the compulsory reinsurance of anyunit risk whichexceeds 10 per cent of the actual assets plus accumulation funds has been hardlysupervised, while supervision has been skewed towards 20 per cent compulsory reinsurance.''As a result, to capture a bigger market share, some Chinese local insurance companies, andespecially those new insurers, diverted reserves and accumulation funds into underwritingliabilities which are sometimes more than ten times their actual assets and accumulation funds.`̀ The guarantee reserve (20 per cent of the total amount of an insurance company's registeredcapital) for repaying the debts of the company upon liquidation will be a far cry from saving aninsurance company from bankruptcy once struck by natural or man-made catastrophes.''

Among measures being urged for implementation are regulations on social insurance,regulations on reinsurance and regulation on insurance intermediaries. China is stillformulating the regulations and creating the mechanisms needed to supervise the industry.The accompanying supporting legislation and implementing regulations are still in theprocess of being drafted and promulgated. Since the Insurance Law, the government has onlyissued the Regulations for the Administration of Insurance Agents (for Trial Implementa-tion), the Provisional Regulations for the Administration of Insurance, and the ProvisionalRegulations for the Administration of Insurance Brokers, as well as a small number of minorpieces of legislation. Much remains to be done ± and some of the legislation will requirecontinued amendments and improvements as it is implemented.

On 13 January 2000 the CIRC issued a decree on regulating insurance ®rms, which wasdue to take effect from 1 March 2000. There are ten chapters in the decree. These includeprovisionsontheestablishmentof insurance®rms, theoperationof insurers, insurancepoliciesandpremium, theuseofpremium income andreinsurance, aswell as supervision.According tothe decree, the establishment of insurance ®rms and branch of®ces by insurance ®rms must beapproved by the CIRC. Insurance ®rms must have a customer service department and lines thatwill look after potential complaints. The terms and premium of major insurance policies mustbe ®xed by the CIRC. Other policies must also be approved by the CIRC. Foreign-fundedinsurance ®rms shall also be subject to regulations stipulated in the decree.17 Since Chinaresumed insurance business in the early 1980s, it has come forth with an insurance law anddecrees on the management of insurance brokers and insurance agents. Most foreign insurancecompanies welcome this latest step taken by China in improving its insurance law system.

According to related sources, the CIRC is now working on `̀ Regulations GoverningForeign Insurance Companies'', while additional regulations on business scope for foreigninsurance companies will be drafted separately.18 The ®rst regulation on foreign insurers ±the Provisional Measures on the Administration of Insurance Institutions with ForeignInvestment in Shanghai ± was issued in 1992.

CIRC has already made changes to bring domestic and foreign insurers and brokers intocompliance with its existing regulations. In May 1999, it suspended the activities of severalforeign brokerages in China, alleging trading irregularities, including the operation ofunlicensed businesses. The commission ordered Jardine Insurance Brokers Ltd to close its

17 `China Issues Insurance Firm Regulations', KPMG Insurance Insider (13 January 2000).18 See `China Paci®c Insurance to Invite Foreign Investment for JV', Asia Pulse (21 February 2000).

# 2000 The International Association for the Study of Insurance Economics.

CHINA'S INSURANCE MARKET: OPPORTUNITY, COMPETITION AND MARKET TRENDS 349

Beijing and Guangzhou of®ces, and banned for life the chief representatives at each, WangJiacong and Chen Jiehong, from any future work in the industry. Jardine was the secondBritish-based brokerage accused of exceeding the terms of its licence. London-basedSedgwick Insurance & Risk Management Consultants (China) Ltd was suspended for threemonths earlier in 1999 after being found guilty of several infractions. Sedgwick is a unit ofMarsh & McLennan Cos of New York. The regulator also sent a letter to all insurers, agentsand brokers, stating it would enforce existing laws that previously had been ¯outed by manydomestic and foreign organizations. Later in 1999, American International Assurance Co.Ltd, a Chinese unit of American International Group Inc., stopped writing life insurancepolicies marketed to employees of companies after it was instructed by the CIRC that itspolicies were considered group life coverage, which the AIA was not licensed to sell. Fourdomestic insurers have been penalized by China's Insurance Regulatory Commission forengaging in illegal practices and other misconduct.

Two are units of People's Insurance Co. of China, the state-run giant of the industry, inGuizhou and Shandong provinces. The others are branches of Shanghai-based China Ping'anInsurance Co. in Hunan province and Beijing. Of®cials said the four companies had chaoticmanagement, incomplete procedures and offered outdated policies or obsolete ®nancialsystems in providing vehicle coverage. Both PICC units and one of Ping'an's were ordered tosuspend business for three months. The Ping'an ®rm in Beijing was criticized in a publicnotice. `̀ The aim of standardizing the market is to prevent risks and strengthen management,and the effort will help spur the sound development of China's insurance industry'', said WuDingfu, Vice-Chairman of the regulatory body.

5. Market trends

A survey of 14 Chinese cities showed that 25.7 per cent of the residents intend to buyinsurance policies in 2000, 10.1 percentage points more than in 1999. The number of peoplebuyinginsurancepolicies isexpected togrowby64.7percentover1999, AsiaPulse reported.19

The number of people buying home property insurance, medical insurance and femaleserious sickness bene®t insurance will double and people buying endowment insurance,serious bene®t insurance and accidental bene®t insurance will increase by over 70 per cent.The survey showed that 39.9 per cent of the residents had bought commercial insurancepolicies by the end of 1999. The people bought policies mainly for endowment assurance, lifeinsurance and medical insurance. Of the people in the 14 cities, 19.3 per cent boughtendowment assurance, 17.5 per cent bought life insurance, 17.2 per cent bought medicalinsurance, 7.0 per cent bought insurance for children, 5.1 per cent bought accident and deathbene®t insurance and 4.9 per cent bought serious ill bene®t insurance, 3.8 per cent boughtproperty insurance and 2.0 per cent bought motor insurance.

Life insurance is one of the best sales prospects in China

Registered foreign companies are allowed to sell life policies to both locals andexpatriates. Furthermore, the market potential is quite large, as 99.5 per cent of the populationstill does not own any life insurance, other than the minimal amount that the state will provide.

19 `More Chinese Intend to Buy Insurance Policies in 2000' (18 March 2000) on line: khttp://dailynews.mu-zi.coml

# 2000 The International Association for the Study of Insurance Economics.

350 SHEN

China's current population stands at 1.22 billion people. According to the Gallup study on theinsurance industry conducted in 1997, 13 per cent of the upper income group in urban areasowned life policies in 1997. Only 9 per cent of this group had life insurance in 1996. Theaverage cost of a life policy is RMB 300 (US $36) per year.

Life insurance is growing most quickly in cities such as Beijing and Shanghai. Part ofthis is due to the door-to-door sales approach which was introduced by AIA in the 1990s.Consumers expect life insurance to pay for children's education, protect against illness or®nancial disaster and provide for retirement. Surveys indicate that Chinese consumers favourproducts tailored to their speci®c needs, reasonable prices, solid reputation, and good service.

Reinsurance offers yet another opportunity for foreign companies to enter the market

Local companies often cannot cover all the risks associated with large-scale projects, sothey need to reinsure part of them with foreign companies. One potentialwinner is Hong Kongand its role as a reinsurance centre. The opening up of the enormous mainland market mayprovide opportunities for Hong Kong's reinsurance market. China's deal for gainingmembership to the WTO allows even quicker market access for foreign reinsurers than otherinsurance categories. According to the terms of the agreement, the reinsurance sector will be`̀ completely open'' when China accedes to the WTO. One positive development in thedirection of a free market was the decision by the CIRC to establish a China ReinsuranceExchange Centre. The move is in anticipation of the entry of foreign reinsurance companies toChina. The chosen location will be a `̀ cosmopolitan city with a highly developed insurancemarket'', probably Shanghai. Along with the of®cial stance on deregulation, several seniorforeign reinsurance representatives are optimistic that their ®rms will soon be allowed to openbranch of®ces in China and engage in renminbi business. It is rumoured that at least onecontinental European reinsurer is likely to receive a branch of®ce licence in 2000. From theCIRC's point of view it makes sense to allow at least one foreign reinsurer in order to assess theeffect on the domestic industry. CIRC is also making plans to lower the ratio for compulsorysecession to China Re at the appropriate time. Such a move will weaken the monopoly ofChina Re, reveal Beijing's sincerity in opening up insurance markets to foreign investors, andalso minimize the risk of China's insurance carriers.

Property insurance is growing due to reforms in the state industrial sector

Immediately upon China's accession to the WTO, foreign non-life insurers will beallowed to write `̀ large scale risks'' on a nationwide basis. Foreign non-life insurers arecurrently only allowed to write business for foreign invested enterprises. Restrictions onthe scope of business and geographic operations of foreign invested property insurancecompanies will be relaxed gradually. For example, they can insure large-scale commercialrisks with no geographic restrictions and provide insurance for enterprises abroad, propertyinsurance, related liabilities insurance and credit insurance for foreign ®rms uponaccession.

Possible future growth may include social insurance

If the government opens the social security system to insurance companies, foreignissuers may eventually participate and play an important role in helping China to set up acomprehensive social security system. About three years ago, the government followed the

# 2000 The International Association for the Study of Insurance Economics.

CHINA'S INSURANCE MARKET: OPPORTUNITY, COMPETITION AND MARKET TRENDS 351

Singapore model and established a social insurance bureau, so now every province and cityhas its own social insurance bureau. Government, employer, and employee are all supposed topay part of the premium for pensions, medical insurance and unemployment insurance. Thegovernment recently announced that not only state-owned but also collective and privateenterprises with three or more people must join this plan. Insurance from the social insurancebureau is expected to replace the security once offered by the state-owned enterprises. Thecentral government recently decreed that a system guaranteeing welfare, unemployment,medical and pension payments will not be in place for another ®ve years. Once this marketopens up, social pension and medical bene®ts may also be considered to be among the bestmarket prospects.

More channels of investment for insurers

China's insurance regulator ismoving toallow®rmsto invest incorporatebonds insteadofonly state bonds or simple bank deposits. While accepting the need for prudence in investment,underwriterssayfallinginterest rates require themto®ndahigheryieldingalternative,since theinterest rate has been cut by the government seven times in last three years.

The governing State Council drew up rules on investments in corporate bonds issued bycentral enterprises, or companies directly under government control. They appear for now tobe ruling out purchases of bonds from other companies, which are the fastest-growing andoften most pro®table sector. The bonds that insurers can buy must have credit ratings of atleast AA-plus, among the highest gradings according to established regulatory stipulations.Insurers will be allowed to buy corporate bonds listed on the Shanghai and Shenzhen stockexchanges, said a research report by Minfa Securities.

Since October 1999, China's State Council has allowed insurance companies to raisemuch-needed funds by permitting them to invest up to 5 per cent of their total assets indirectlyin the national's stock markets via securities investment funds. The Tongsheng SecuritiesInvestment Fund was the ®rst securities investment fund to open to insurers. Four days after itsdebut, 11 insurance companies bought 900 million of the fund's 3 billion units, with ChinaLife Insurance and Ping An Insurance taking the lead at 300 million units apiece.

More recently, Chinese regulators have allowed two insurers to invest more in stocks in abid to gradually open the securities markets to more in¯ows of insurance funds, as set out inthe China Securities newspaper, citing unidenti®ed industry executives and of®cials. Infuture, Taikang Life Insurance Co. and Huatai Property Insurance Co. will be allowed toinvest up to 10 per cent of their assets in stock funds, up from a cap of 5 per cent.20 The moveshows the authorities' willingness to gradually liberalize stock investment by insurers, addingthat there is room for further raising the cap.

6. Suggestions for foreign insurers

China's approach towards foreign insurance business has historically been very cautious,and with good reason. Remember, China restricted the presence of foreign insurers in theirmarket for a long time, so the foreign insurer enters that market with an subconscious strikeagainst them. China will not automatically be willing to `̀ trust'' the foreign insurer, even afterhaving let them into their market; that trust must be earned slowly and patiently. As a

20 `China Allows Two Insurers to Invest More in Stocks' (15 March 2000) khttp://dailynews.muzi.coml

# 2000 The International Association for the Study of Insurance Economics.

352 SHEN

consequence, do not expect a rapid expansion of business in the Chinese market. By openingits market to foreigners, China has not said `̀ come and jump right in to our market''. It hasinstead said `̀ come into our country and let us see for ourselves if we can trust you enough todo business with you.'' Allowing a widespread foreign insurance presence into their market isnot something that will happen automatically. Membership of the WTO is not a magicformula; it will not automatically erase those prejudices/cautionary measures that keptChina's market closed for so long.

Choose your market and local partner carefully

The key to opening the Chinese market is not acquiring a licence ± it is understanding theChinese: their way of doing business, their way of behaving, the place that honour,compromise, conciliation and long-term thinking have in their relationships (business andpersonal). Foreign insurers that recognize this will also recognize the need to establishthemselves in a manner that allows China and the Chinese to view them as more than foreignentities. By adopting a business format that Chinese insurance regulatory authorities seem tohave already given preference to (with a Chinese partner, and in the format of a Joint Venture),the foreign insurance company should not consider that they are making a necessarycompromise to satisfy regulators. They are making a very important investment in acquiring ateacher who will help them learn about the market that they wish to enter. In Chinaacquisitions are not possible because comparable enterprises do not usually exist. This almostinevitably means that a business must be started from scratch. When it comes to partnering, itis critical that your partners share your goals and that what each brings to the table does notoverlap with but complements the other. Several years ago, China's central bank wouldusually suggest which partner a licensed foreign insurer should consider. According to theWTO agreement, foreign insurers will have the freedom to choose their own joint venturepartner. This is a positive development because a foreign insurer now can resist the Chineseregulatory authority's `̀ arranged marriage'' if it is inconsistent with the entrant's approach.

Long-term commitment requires patience

It is no secret today that the key factor in winning a licence in China is to demonstrate thatthe company can provide supports and assistance in developing China's insurance market. Forexample, in 1995 Chubb group founded the Chubb School of Insurance at the ShanghaiUniversity of Finance and Economics, the ®rst foreign invested training centre in China.China may scrap geographical restrictions on foreign insurance ®rms within ®ve years, in itslatest effort to show that it is ready to join the World Trade Organization. Still, some foreigninsurers said they do not expect any quick gains in China, where they are also limited to sellingeither non-life or life insurance, not both. Nor should they. Cultivation of such huge anduntapped market requires and deserves that foreign insurers invest effort in buildingrelationships that will help their presence in China to be understood as one of mutual bene®tand not as sudden occupation by opportunistic corporate raiders.

`̀ The easy part is to say the market will be opened. It is the implementation that isdif®cult,'' said Russ Miller, managing director and chief representative of Principal LifeInsurance Co. in Beijing. `̀ There's still no de®nitive answer as to how they are going to do it.''

That has not prevented foreign insurers from trying to enter the $15 billion China market,potentially the world's most lucrative. The CIRC predicts premium income will more thandouble by 2004, to 260 billion yuan ($31 billion). Miller said it takes at least 17 months after a

# 2000 The International Association for the Study of Insurance Economics.

CHINA'S INSURANCE MARKET: OPPORTUNITY, COMPETITION AND MARKET TRENDS 353

foreign ®rm gets a licence to set up a joint venture with a Chinese insurer to sell the ®rstinsurance policy. Part of the time lag could stem from the fact that there are many foreigninsurers, but only 13 Chinese insurance companies.

It is essential to approach international markets as investments, not as expenditures. Thisrequires patience. As Mr Dominic D'Alessandro, CEO of Manulife Financial said, `̀ I havefrequently said that I will probably be retired from Manulife before our Chinese joint venturepays its ®rst dividend.'' Such a remark has had two effects: it has dampened Boardexpectations and it has spurred people in Hong Kong and Shanghai to a frenzy of activity.

The establishment of mutual trust is the key to success

Manulife set up the ®rst China±foreign joint venture life insurance company in 1996.One of Manulife's competitors approached a Chinese government of®cial after its openingceremony. They told her they too, were a big North American insurer and why did they not getthe licence? Here is how she responded: `̀ It is not important to be big or the biggest. It isimportant to be ®rst. And Manulife was ®rst.'' She went on to say: `̀ You have to set up thefriendship ®rst. You have to have good relationships ®rst for mutual trust.'' This is the ®rst andforemost factor of success in the international arena ± in fact, in any business venture. It is sosimple that it is sometimes overlooked. The establishment of mutual trust. Manulife hasworked hard to establish this trust with the Chinese in different ways over the past severalyears. They opened representative of®ces in various cities in the country and diligently set outto cultivate relationships and make themselves known to key decision-makers. For example,in 1992, Manulife established a comprehensive training programme for the People'sInsurance Company of China. A year later, Manulife began sponsoring an actuarial examcentre ± the ®rst and only such centre in the entire country. A year after that, Manulifelaunched a training programme in Canada for of®cials from the People's Bank of China. Eachyear, four promising PBOC employees are brought to Toronto for a year during which they areexposed to various facets of the life insurance business.21

7. Concluding remarks

Today, more and more companies are facing the reality of a global economy and anenvironment characterized by international operation. For some companies, this new realitymeans the opportunity to vastly expand their market. For others, it means being faced withmore and more competition at home. For most, both possibilities are demanding attention andcausing a re-evaluation of traditional approaches to the insurance market. If your companywishes to win over the world's insurance market, you had better put China into your strategy.Today most international players are convinced that several trends seem to be encouragingtheir expanding efforts into China. These factors include greater political stability in China,opening of its market, growing privatization of the insurance industry and greater uniformityin solvency regulation. China's relatively low penetration and density indicate that the 1.2billion population may be using their dollars to provide for more basic needs, such as food andhousing. But things have been changing in the past few years and will eventually reach a stagewhere Chinese citizens generally understand, value and purchase insurance. The premiumgrowth rate of China is another measure of its market's attractiveness. There are, however,

21 Dominic D'Alessandro, `Competing in Asia: The Manulife Story' (22 January 1997).

# 2000 The International Association for the Study of Insurance Economics.

354 SHEN

some challenges for a company's entry into such a high-growth market. Entering a quicklygrowing market may require a considerable investment of money, time and effort since thismarket lacks the technology, regulatory system and skilled work force needed to sustain aviable insurance industry. Because of the large start-up expenses a company incurs, theearnings from this market may be negligible, or even non-existent, for many years. The Chinamarket, however, offers greater potential for insurers willing to commit themselves to agrowing country for a long term.

Many foreign insurers who have queued for years to enter China's coveted insurancemarket would not be ready to do business if they were allowed in too soon. A lack of trainedstaff, inadequate market knowledge, an embryonic regulatory environment and a relativelysmall market to aim at in the beginning could take their toll on many prospective entrants. Ifthings do move ahead quickly and China does accede to the WTO, how many of the companieswaiting to enter the market would be ready for trading in a fully open market within six years?That prospect poses some very signi®cant challenges to management: the process ofliberalization has been set in motion and companies should already have devised actionplans identifying the cities they should target or the products they should offer.

Foreign insurers have set up some 200 representative of®ces in China, eagerly waitingfor the market of 1.2 billion people to open up to full foreign competition. Only a handful of®rms have been granted licences so far and are restricted to underwriting in Guangzhou andShanghai. If China does gain membership of the WTO by the end of this year, its of®cial offeron insurance liberalization would see about a dozen cities opened by 2002 and more thandouble that by 2003 ± a market of about 96 million compared to about 33 million now. Foreignlife insurers would have access to health insurance by 2004 and group life business by 2005,non-life insurers would have no geographic restrictions, though they would be excluded fromthird-party motor insurance, one of the most attractive classes of business.

The movement of China towards open competition with foreign insurers is inevitable. Itis best understood as being driven (and ultimately sustained by) a combination of rapidlycontinuing market reforms and unprecendented demand; internal factors that shall endure asthe hallmarks of the new economy in this, the world's largest insurance market.

China's desire to remove its barriers and at last become a participant in the market of ourglobal village is thus the driving force behind its insurance reforms. Its membership in theWTO, while signi®cant, will only serve to accelerate a process that is already and inexorablyunderway. Dammed water, whether it is released gradually or suddenly, ¯ows in but onedirection.

It is thus essential for foreign insurers to understand that China, as the initiator of thisprocess will seek (irrespective of the pace at which its market opens) to maintain control overits implementation. Such control is most likely to manifest itself in scrupulous monitoring andregulation of the day to day business affairs of foreign insurers in China.

The foreign insurer poised to enter the Chinese market would thus be well advised tomake thorough its preparations. Only by securing a comprehensive understanding of themarketplace and cultivating strong relationships and goodwill with Chinese insurers andregulators, can the foreign insurer hope to survive and thrive in this vast and untapped marketamid the vagaries of a regulatory environment that is yet in its infancy.

# 2000 The International Association for the Study of Insurance Economics.

CHINA'S INSURANCE MARKET: OPPORTUNITY, COMPETITION AND MARKET TRENDS 355