cia. hering - marketscreener.com · 6 hering stores chain performancehering stores chain...

TRANSCRIPT

Cia. Hering

Interim Financial Information for the Quarter ended September 30, 2017 and Independent Auditor's Review Report

(Free Translation into English from the Original Previously Issued in Portuguese for the Convenience of Readers Outside Brazil)

Cia. Hering (Publicly-held company)

Quarterly financial information September 30, 2017

Table of contents Performance report 3 - 9

Independent auditor’s report on the review 10 - 11

Balance sheets 12

Statements of income 13

Statements of comprehensive income 14

Statements of changes in equity 15 - 16

Statements of cash flows 17

Statements of added value 18 Notes to the financial statements 19 - 88

3

Consolidated HighlightsConsolidated HighlightsConsolidated HighlightsConsolidated Highlights

Gross Revenue of R$ 433.7 million in 3Q17

Net Income of R$ 51.9 million

� Gross Revenue of R$ 433.7 million, 5.1% higher than 3Q16,

influenced by own stores, webstores and foreign market

performance;

� R$ 63.8 million EBITDA (+30.9%), 310 bp of margin expansion

due to sales growth and gross margin increase, partially offset

by higher operating expenses;

� Net Income of R$ 51.9 million (-9.8%), explained by a reduction

in financial income as a result of a lawsuit gain in 3Q16,

impacting comparison basis, and higher Income Tax and Social

Contribution effective rate;

� ROIC of 16.7% (+130 bp vs. 3Q16), due to a recovery in the

Company’s operating income.

ChangeChangeChangeChange ChangeChangeChangeChange

3Q17 / 3Q163Q17 / 3Q163Q17 / 3Q163Q17 / 3Q16 9M17 / 9M169M17 / 9M169M17 / 9M169M17 / 9M16

Gross RevenueGross RevenueGross RevenueGross Revenue 433,689433,689433,689433,689 412,758412,758412,758412,758 5.1%5.1%5.1%5.1% 1,304,0461,304,0461,304,0461,304,046 1 ,233,2671,233,2671,233,2671,233,267 5.7%5.7%5.7%5.7%

Domestic Market 420,917 403,743 4.3% 1,268,324 1,201,383 5.6%

Foreign Market 12,772 9,015 41.7% 35,722 31,884 12.0%

Net RevenueNet RevenueNet RevenueNet Revenue 375,103375,103375,103375,103 350,567350,567350,567350,567 7.0%7.0%7.0%7.0% 1,109,9531,109,9531,109,9531,109,953 1,043,0121,043,0121,043,0121,043,012 6.4%6.4%6.4%6.4%

Gross ProfitGross ProfitGross ProfitGross Profit 172,830172,830172,830172,830 140,845140,845140,845140,845 22.7%22.7%22.7%22.7% 490,350490,350490,350490,350 406,988406,988406,988406,988 20.5%20.5%20.5%20.5%

Gross Margin 46.1% 40.2% 590 bp 44.2% 39.0% 520 bp

Cash Gross Profit Cash Gross Profit Cash Gross Profit Cash Gross Profit ( a )( a )( a )( a )

179,900179,900179,900179,900 147,964147,964147,964147,964 21.6%21.6%21.6%21.6% 511,158511,158511,158511,158 427,885427,885427,885427,885 19.5%19.5%19.5%19.5%

Cash Gross Margin (a)

48.0% 42.2% 580 bp 46.1% 41.0% 510 bp

Net IncomeNet IncomeNet IncomeNet Income 51,91751,91751,91751,917 57,53557,53557,53557,535 -9.8%-9.8%-9.8%-9.8% 177,764177,764177,764177,764 148,468148,468148,468148,468 19.7%19.7%19.7%19.7%

Net Margin 13.8% 16.4% -260 bp 16.0% 14.2% 180 bp

EBITDA EBITDA EBITDA EBITDA (b) (b) (b) (b) 63,81763,81763,81763,817 48,75148,75148,75148,751 30.9%30.9%30.9%30.9% 179,434179,434179,434179,434 146,618146,618146,618146,618 22.4%22.4%22.4%22.4%

EBITDA Margin (b) 17.0% 13.9% 310 bp 16.2% 14.1% 210 bp

ROIC ROIC ROIC ROIC (c)(c)(c)(c) 16.7%16.7%16.7%16.7% 15.4%15.4%15.4%15.4% 130 bp130 bp130 bp130 bp 16.7%16.7%16.7%16.7% 15.4%15.4%15.4%15.4% 130 bp130 bp130 bp130 bp

(a) Gross Profit and Gross Margin without Depreciation allocated to cost

(b) Earnings before interest, taxes, depreciation, amortization and participations

(c) Last 12 months

3Q163Q163Q163Q16 9M179M179M179M17 9M169M169M169M16R$ ThousandR$ ThousandR$ ThousandR$ Thousand 3Q173Q173Q173Q17

4

SALES PERFORMANCESALES PERFORMANCESALES PERFORMANCESALES PERFORMANCE

The channel breakdown does not consider “Others”.

Company's gross sales totaled R$ 433.7 million in 3Q17, 5.1% higher than 3Q16, influenced by own stores and

webstores performance. In addition, the greater penetration of the company's products in several Latin American

markets stands out, contributing to sales growth in the foreign market (+41.7%).

The multibrand channel posted 1.2% growth in 3Q17 sales, totaling R$ 181.5 million. The increase, lower than the first

quarters of the year, is attributed mainly to higher orders concentration for the largest collections of the year (Winter

and High Summer), leading to purchases postponement for 4Q17. The channel, more exposed to the country’s

economic cycles, showed stability in the number of active customers and higher average purchase of existing

customers.

Sales to franchises reached R$ 152.4 million, 3.9% lower than 3Q16, influenced by (i) reduction of 26 stores, among

transfers and closings, in the last 12 months, (ii) higher orders’ concentration for the High Summer collection (mostly

invoiced in 4Q17) and (iii) anticipation, in 3Q16, of part of the invoiced volume of the Higher Summer collection as part

of the preparation of the network for the period of high sales, impacting comparison basis.

Stores operated by the Company registered a 35.4% increase in sales, reaching R$ 66.3 million, mainly influenced by the

net addition of 11 stores in the last 12 months and an improvement in same-store sales in all brands, also favored by

the greater concentration of points of sale in the Southeast, best regional performance in the quarter.

Webstores maintained its double-digit growth trend (+25.0%), with emphasis on the implementation of a new Hering

store layout, launch of exclusive collections for the channel, such as partnership with renowned stylists and good

performance of the online outlet (Espaço Hering).

Regarding brands’ performance, Hering and Hering Kids stood out with an increase of 3.8% and 9.1%, respectively,

supported by good product offering, store experience and communication, in line with previous quarters. DZARM.

registered a 5.4% increase, with better sales performance in flagship stores and PUC decreased 3.9%, with signs of

stabilization and sequential improvement in same-store sales.

In the 9M17, the Company's gross sales totaled R$ 1.3 billion, a 5.7% increase over the same period in 2016, influenced

by the good performance of all brands, notably Hering Kids (+17.3%). Regarding the distribution channels, the

multibrand sales growth stands out, with a 7.4% increase in the 9 month period, own stores growth (+22.6%), as a

result of better supply management and store opening, as well as the double-digit increase in the webstores (+24.1%).

ChangeChangeChangeChange ChangeChangeChangeChange

3 Q1 7 / 3 Q1 63 Q1 7 / 3 Q1 63 Q1 7 / 3 Q1 63 Q1 7 / 3 Q1 6 9 M1 7 / 9 M1 69 M1 7 / 9 M1 69 M1 7 / 9 M1 69 M1 7 / 9 M1 6

Gross RevenueGross RevenueGross RevenueGross Revenue 4 33 ,6 894 33 ,6 894 33 ,6 894 33 ,6 89 4 12 ,7 584 12 ,7 584 12 ,7 584 12 ,7 58 5 .1 %5 .1 %5 .1 %5 .1 % 1 ,3 04 ,0 461 ,3 04 ,0 461 ,3 04 ,0 461 ,3 04 ,0 46 1 ,23 3,26 71,23 3,26 71,23 3,26 71,23 3,26 7 5.7%5.7%5.7%5.7%

Domestic Market 420,917 403,743 4.3% 1,268,324 1,201,383 5.6%

Foreign Market 12,772 9,015 41.7% 35,722 31,884 12.0%

Domestic Market Gross RevenueDomestic Market Gross RevenueDomestic Market Gross RevenueDomestic Market Gross Revenue 4 20 ,9 174 20 ,9 174 20 ,9 174 20 ,9 17 4 03 ,7 434 03 ,7 434 03 ,7 434 03 ,7 43 4 .3 %4 .3 %4 .3 %4 .3 % 1 ,2 68 ,3 241 ,2 68 ,3 241 ,2 68 ,3 241 ,2 68 ,3 24 1 ,20 1,38 31,20 1,38 31,20 1,38 31,20 1,38 3 5.6%5.6%5.6%5.6%

Hering 305,224 294,183 3.8% 923,085 885,793 4.2%

Hering Kids 59,392 54,440 9.1% 180,387 153,797 17.3%

PUC 30,434 31,680 -3.9% 88,027 86,920 1.3%

DZARM. 17,161 16,279 5.4% 52,394 48,974 7.0%

Other 8,706 7,161 21.6% 24,431 25,899 -5.7%

ChangeChangeChangeChange ChangeChangeChangeChange

3 Q1 7 / 3 Q1 63 Q1 7 / 3 Q1 63 Q1 7 / 3 Q1 63 Q1 7 / 3 Q1 6 9 M1 7 / 9 M1 69 M1 7 / 9 M1 69 M1 7 / 9 M1 69 M1 7 / 9 M1 6

Multibrand 181,473 179,367 1.2% 573,469 533,984 7.4%

Franchise 152,383 158,608 -3.9% 434,905 449,737 -3.3%

Owned Stores 66,347 49,001 35.4% 202,053 164,805 22.6%

Webstore 12,008 9,606 25.0% 33,466 26,958 24.1%

TotalTotalTotalTotal 4 12 ,2 114 12 ,2 114 12 ,2 114 12 ,2 11 3 96 ,5 823 96 ,5 823 96 ,5 823 96 ,5 82 3 .9 %3 .9 %3 .9 %3 .9 % 1 ,2 43 ,8 931 ,2 43 ,8 931 ,2 43 ,8 931 ,2 43 ,8 93 1 ,17 5,48 41,17 5,48 41,17 5,48 41,17 5,48 4 5.8%5.8%5.8%5.8%

Multibrand 44.0% 45.2% -120 bp 46.1% 45.4% 70 bp

Franchise 37.0% 40.0% -300 bp 35.0% 38.3% -330 bp

Owned Stores 16.1% 12.4% 370 bp 16.2% 14.0% 220 bp

Webstore 2.9% 2.4% 50 bp 2.7% 2.3% 40 bp

TotalTotalTotalTotal 10 0 .0%10 0 .0%10 0 .0%10 0 .0% 1 0 0.0%1 0 0.0%1 0 0.0%1 0 0.0% - 1 0 0.0%1 0 0.0%1 0 0.0%1 0 0.0% 1 00 .0 %1 00 .0 %1 00 .0 %1 00 .0 % -

Domestic Market ShareDomestic Market ShareDomestic Market ShareDomestic Market Share

Gross Revenues - R$ thous.Gross Revenues - R$ thous.Gross Revenues - R$ thous.Gross Revenues - R$ thous.

3Q 173Q 173Q 173Q 17 3Q1 63Q1 63Q1 63Q1 6 9M1 79M1 79M1 79M1 7 9 M169 M169 M169 M16

3Q 173Q 173Q 173Q 17 3Q1 63Q1 63Q1 63Q1 6 9M1 79M1 79M1 79M1 7 9 M169 M169 M169 M16

5

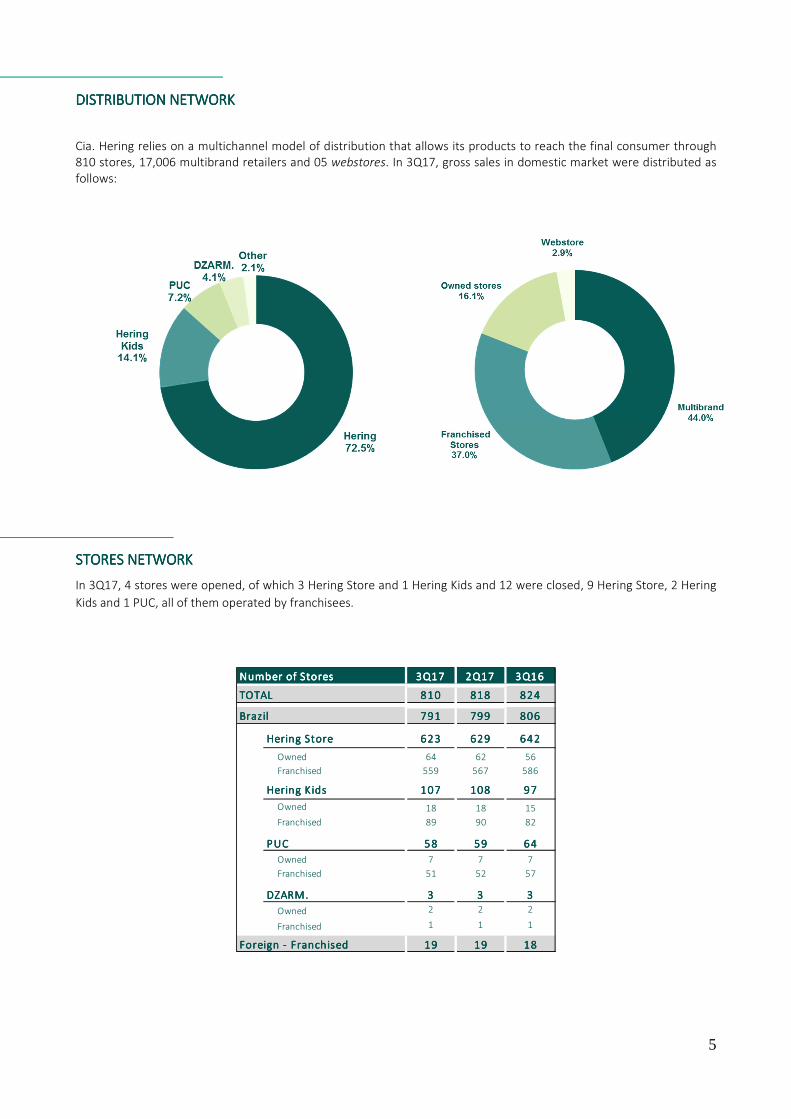

DISTRIBUTION NETWORKDISTRIBUTION NETWORKDISTRIBUTION NETWORKDISTRIBUTION NETWORK

Cia. Hering relies on a multichannel model of distribution that allows its products to reach the final consumer through

810 stores, 17,006 multibrand retailers and 05 webstores. In 3Q17, gross sales in domestic market were distributed as

follows:

STORES NETWORKSTORES NETWORKSTORES NETWORKSTORES NETWORK

In 3Q17, 4 stores were opened, of which 3 Hering Store and 1 Hering Kids and 12 were closed, 9 Hering Store, 2 Hering

Kids and 1 PUC, all of them operated by franchisees.

Number of StoresNumber of StoresNumber of StoresNumber of Stores 3Q173Q173Q173Q17 2Q172Q172Q172Q17 3Q163Q163Q163Q16

TOTALTOTALTOTALTOTAL 810810810810 818818818818 824824824824

BrazilBrazilBrazilBrazil 791791791791 799799799799 806806806806

Hering StoreHering StoreHering StoreHering Store 623623623623 629629629629 642642642642

Owned 64 62 56

Franchised 559 567 586

Hering K idsHering K idsHering K idsHering K ids 107107107107 108108108108 97979797

Owned 18 18 15

Franchised 89 90 82

PUCPUCPUCPUC 58585858 59595959 64646464

Owned 7 7 7

Franchised 51 52 57

DZARM.DZARM.DZARM.DZARM. 3333 3333 3333

Owned 2 2 2

Franchised 1 1 1

Foreign - FranchisedForeign - FranchisedForeign - FranchisedForeign - Franchised 19191919 19191919 18181818

6

HERING STORES CHAIN PERFORMANCEHERING STORES CHAIN PERFORMANCEHERING STORES CHAIN PERFORMANCEHERING STORES CHAIN PERFORMANCE

Sales of Hering Store network (owned and franchised) to final consumers (sell-out) increased by 3.6%, totaling R$ 299.4

million in the quarter, influenced by same-store sales (+3.5%), better operational execution and gradual improvement

of both consumer environment and macroeconomic indicators. Lower consumers’ flow in the stores, resulting in check-

outs decrease, was more than offset by an increase in the average ticket.

Initial performance analysis of the stores renovated last year suggests that those points of sale coupled with best

practices (inventory management, product exposure, visual merchandising, among others) has favored its performance.

The company continues to concentrate efforts to move forward in the initiatives’ adoption, by the network, that favor

inventory turnover and minimize the negative effects caused by stockout and leftovers.

Sales of own stores grew 36.4%, favored by the net addition of 8 stores in the last 12 months. This result was influenced

by an increase in the average price, which can partly be explained by better inventory management, reducing sales of

discounted items, in addition to the combination of price increase and better sale’s performance of the new basics line.

In the first nine months of 2017, net sales fell 1.0%, impacted by sales area reduction, partially offset by better

execution in own stores.

Hering Store Chain Performanc eHering Store Chain Performanc eHering Store Chain Performanc eHering Store Chain Performanc e 3Q173Q173Q173Q17 3Q163Q163Q163Q16Chg.Chg.Chg.Chg.

3Q17 / Q163Q17 / Q163Q17 / Q163Q17 / Q169M179M179M179M17 9M169M169M169M16

Chg.Chg.Chg.Chg.

9M17 / 9M169M17 / 9M169M17 / 9M169M17 / 9M16

Number of StoresNumber of StoresNumber of StoresNumber of Stores 623623623623 642642642642 -3 .0%-3 .0%-3 .0%-3 .0% 623623623623 642642642642 -3 .0%-3 .0%-3 .0%-3 .0%

Franchise 559 586 -4.6% 559 586 -4.6%

Owned 64 56 14.3% 64 56 14.3%

Sales (R$ thousand) Sales (R$ thousand) Sales (R$ thousand) Sales (R$ thousand) ( 1 )( 1 )( 1 )( 1 ) 299,444299,444299,444299,444 289 ,089289,089289,089289,089 3 .6%3.6%3.6%3.6% 920,355920,355920,355920,355 929 ,658929,658929,658929,658 -1 .0%-1 .0%-1 .0%-1 .0%

Franchise 239,094 244,830 -2.3% 737,883 782,111 -5.7%

Owned 60,350 44,259 36.4% 182,472 147,547 23.7%

Same Store Sales growthSame Store Sales growthSame Store Sales growthSame Store Sales growth ( 2 ) ( 2 ) ( 2 ) ( 2 ) 3.5% 3 .5% 3 .5% 3 .5% -10 .9% -10 .9% -10 .9% -10 .9% 1440 bp1440 bp1440 bp1440 bp -0 .5% -0 .5% -0 .5% -0 .5% -7 .9% -7 .9% -7 .9% -7 .9% 740 bp740 bp740 bp740 bp

Sales Area (m²) 87,563 90,961 -3.7% 87,563 90,961 -3.7%

Sales (R$ per m²) 3,420 3,178 7.6% 10,511 10,220 2.8%

Check-Outs 2,266,348 2,464,683 -8.0% 6,961,959 7,775,332 -10.5%

Units 4,932,711 5,200,707 -5.2% 14,615,065 15,960,675 -8.4%

Units per Check-Out 2.18 2.11 3.3% 2.10 2.05 2.4%

Average Sales Price (R$) 60.71 55.59 9.2% 62.97 58.25 8.1%

Average Sales Ticket (R$) 132.13 117.29 12.7% 132.20 119.57 10.6%

(1) The amounts referred to the sales to final costumers ('sell out')

(2) Compared to the same period of the previous year

7

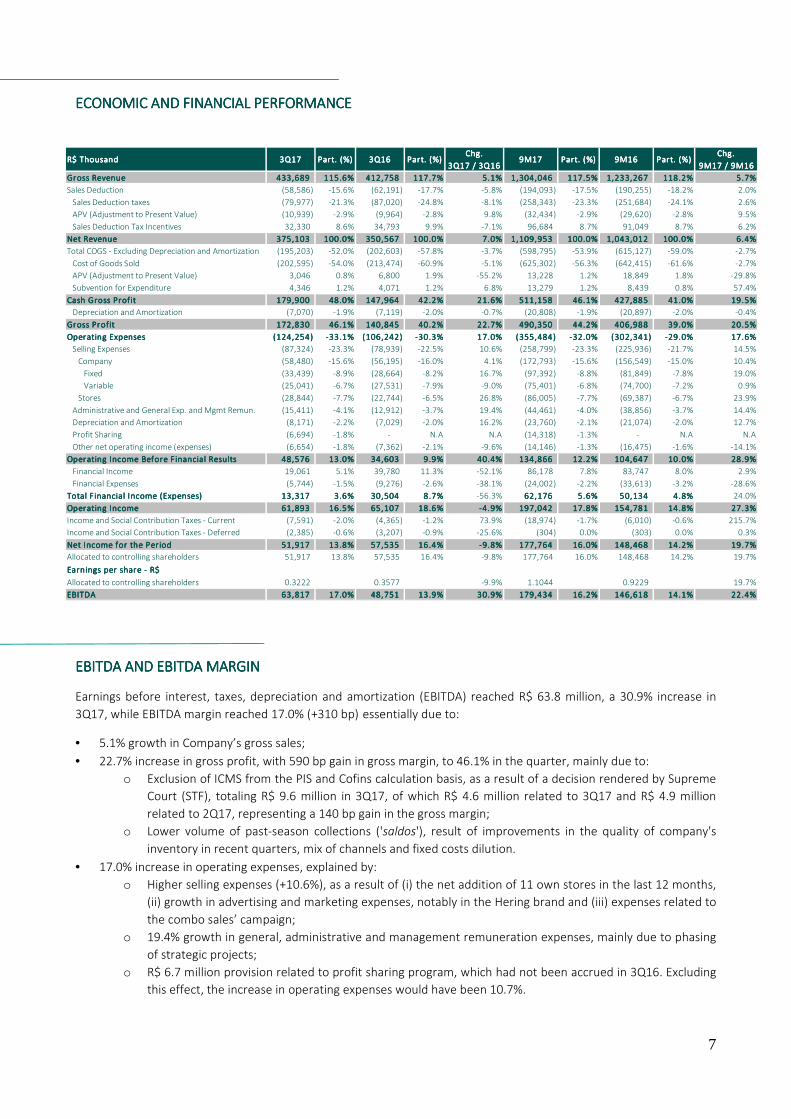

ECONOMIC AND FINANCIAL PERFORMANCEECONOMIC AND FINANCIAL PERFORMANCEECONOMIC AND FINANCIAL PERFORMANCEECONOMIC AND FINANCIAL PERFORMANCE

EBITDA AND EBITDA MARGINEBITDA AND EBITDA MARGINEBITDA AND EBITDA MARGINEBITDA AND EBITDA MARGIN

Earnings before interest, taxes, depreciation and amortization (EBITDA) reached R$ 63.8 million, a 30.9% increase in

3Q17, while EBITDA margin reached 17.0% (+310 bp) essentially due to:

• 5.1% growth in Company’s gross sales;

• 22.7% increase in gross profit, with 590 bp gain in gross margin, to 46.1% in the quarter, mainly due to:

o Exclusion of ICMS from the PIS and Cofins calculation basis, as a result of a decision rendered by Supreme

Court (STF), totaling R$ 9.6 million in 3Q17, of which R$ 4.6 million related to 3Q17 and R$ 4.9 million

related to 2Q17, representing a 140 bp gain in the gross margin;

o Lower volume of past-season collections ('saldos'), result of improvements in the quality of company's

inventory in recent quarters, mix of channels and fixed costs dilution.

• 17.0% increase in operating expenses, explained by:

o Higher selling expenses (+10.6%), as a result of (i) the net addition of 11 own stores in the last 12 months,

(ii) growth in advertising and marketing expenses, notably in the Hering brand and (iii) expenses related to

the combo sales’ campaign;

o 19.4% growth in general, administrative and management remuneration expenses, mainly due to phasing

of strategic projects;

o R$ 6.7 million provision related to profit sharing program, which had not been accrued in 3Q16. Excluding

this effect, the increase in operating expenses would have been 10.7%.

Chg.Chg.Chg.Chg. Chg.Chg.Chg.Chg.

3Q17 / 3Q163Q17 / 3Q163Q17 / 3Q163Q17 / 3Q16 9M17 / 9M169M17 / 9M169M17 / 9M169M17 / 9M16

Gross RevenueGross RevenueGross RevenueGross Revenue 433,689433,689433,689433,689 115.6%115.6%115.6%115.6% 412,758412,758412,758412,758 117.7%117.7%117.7%117.7% 5.1%5.1%5.1%5.1% 1,304,0461,304,0461,304,0461,304,046 117.5%117.5%117.5%117.5% 1,233,2671,233,2671,233,2671,233,267 118.2%118.2%118.2%118.2% 5.7%5.7%5.7%5.7%

Sales Deduction (58,586) -15.6% (62,191) -17.7% -5.8% (194,093) -17.5% (190,255) -18.2% 2.0%

Sales Deduction taxes (79,977) -21.3% (87,020) -24.8% -8.1% (258,343) -23.3% (251,684) -24.1% 2.6%

APV (Adjustment to Present Value) (10,939) -2.9% (9,964) -2.8% 9.8% (32,434) -2.9% (29,620) -2.8% 9.5%

Sales Deduction Tax Incentives 32,330 8.6% 34,793 9.9% -7.1% 96,684 8.7% 91,049 8.7% 6.2%

Net RevenueNet RevenueNet RevenueNet Revenue 375,103375,103375,103375,103 100.0%100.0%100.0%100.0% 350,567350,567350,567350,567 100.0%100.0%100.0%100.0% 7.0%7.0%7.0%7.0% 1,109,9531,109,9531,109,9531,109,953 100.0%100.0%100.0%100.0% 1,043,0121,043,0121,043,0121,043,012 100.0%100.0%100.0%100.0% 6.4%6.4%6.4%6.4%

Total COGS - Excluding Depreciation and Amortization (195,203) -52.0% (202,603) -57.8% -3.7% (598,795) -53.9% (615,127) -59.0% -2.7%

Cost of Goods Sold (202,595) -54.0% (213,474) -60.9% -5.1% (625,302) -56.3% (642,415) -61.6% -2.7%

APV (Adjustment to Present Value) 3,046 0.8% 6,800 1.9% -55.2% 13,228 1.2% 18,849 1.8% -29.8%

Subvention for Expenditure 4,346 1.2% 4,071 1.2% 6.8% 13,279 1.2% 8,439 0.8% 57.4%

Cash Gross Profit Cash Gross Profit Cash Gross Profit Cash Gross Profit 179,900179,900179,900179,900 48.0%48.0%48.0%48.0% 147,964147,964147,964147,964 42.2%42.2%42.2%42.2% 21.6%21.6%21.6%21.6% 511,158511,158511,158511,158 46.1%46.1%46.1%46.1% 427,885427,885427,885427,885 41.0%41.0%41.0%41.0% 19.5%19.5%19.5%19.5%

Depreciation and Amortization (7,070) -1.9% (7,119) -2.0% -0.7% (20,808) -1.9% (20,897) -2.0% -0.4%

Gross ProfitGross ProfitGross ProfitGross Profit 172,830172,830172,830172,830 46.1%46.1%46.1%46.1% 140,845140,845140,845140,845 40.2%40.2%40.2%40.2% 22.7%22.7%22.7%22.7% 490,350490,350490,350490,350 44.2%44.2%44.2%44.2% 406,988406,988406,988406,988 39.0%39.0%39.0%39.0% 20.5%20.5%20.5%20.5%

Operating ExpensesOperating ExpensesOperating ExpensesOperating Expenses (124,254)(124,254)(124,254)(124,254) -33.1%-33.1%-33.1%-33.1% (106,242)(106,242)(106,242)(106,242) -30.3%-30.3%-30.3%-30.3% 17.0%17.0%17.0%17.0% (355,484)(355,484)(355,484)(355,484) -32.0%-32.0%-32.0%-32.0% (302,341)(302,341)(302,341)(302,341) -29.0%-29.0%-29.0%-29.0% 17.6%17.6%17.6%17.6%

Selling Expenses (87,324) -23.3% (78,939) -22.5% 10.6% (258,799) -23.3% (225,936) -21.7% 14.5%

Company (58,480) -15.6% (56,195) -16.0% 4.1% (172,793) -15.6% (156,549) -15.0% 10.4%

Fixed (33,439) -8.9% (28,664) -8.2% 16.7% (97,392) -8.8% (81,849) -7.8% 19.0%

Variable (25,041) -6.7% (27,531) -7.9% -9.0% (75,401) -6.8% (74,700) -7.2% 0.9%

Stores (28,844) -7.7% (22,744) -6.5% 26.8% (86,005) -7.7% (69,387) -6.7% 23.9%

Administrative and General Exp. and Mgmt Remun. (15,411) -4.1% (12,912) -3.7% 19.4% (44,461) -4.0% (38,856) -3.7% 14.4%

Depreciation and Amortization (8,171) -2.2% (7,029) -2.0% 16.2% (23,760) -2.1% (21,074) -2.0% 12.7%

Profit Sharing (6,694) -1.8% - N.A N.A (14,318) -1.3% - N.A N.A

Other net operating income (expenses) (6,654) -1.8% (7,362) -2.1% -9.6% (14,146) -1.3% (16,475) -1.6% -14.1%

Operating Income Before Financial ResultsOperating Income Before Financial ResultsOperating Income Before Financial ResultsOperating Income Before Financial Results 48,57648,57648,57648,576 13.0%13.0%13.0%13.0% 34,60334,60334,60334,603 9.9%9.9%9.9%9.9% 40.4%40.4%40.4%40.4% 134,866134,866134,866134,866 12.2%12.2%12.2%12.2% 104,647104,647104,647104,647 10.0%10.0%10.0%10.0% 28.9%28.9%28.9%28.9%

Financial Income 19,061 5.1% 39,780 11.3% -52.1% 86,178 7.8% 83,747 8.0% 2.9%

Financial Expenses (5,744) -1.5% (9,276) -2.6% -38.1% (24,002) -2.2% (33,613) -3.2% -28.6%

Total Financial Income (Expenses)Total Financial Income (Expenses)Total Financial Income (Expenses)Total Financial Income (Expenses) 13,31713,31713,31713,317 3.6%3.6%3.6%3.6% 30,50430,50430,50430,504 8.7%8.7%8.7%8.7% -56.3% 62,17662,17662,17662,176 5.6%5.6%5.6%5.6% 50,13450,13450,13450,134 4.8%4.8%4.8%4.8% 24.0%

Operating IncomeOperating IncomeOperating IncomeOperating Income 61,89361,89361,89361,893 16.5%16.5%16.5%16.5% 65,10765,10765,10765,107 18.6%18.6%18.6%18.6% -4.9%-4.9%-4.9%-4.9% 197,042197,042197,042197,042 17.8%17.8%17.8%17.8% 154,781154,781154,781154,781 14.8%14.8%14.8%14.8% 27.3%27.3%27.3%27.3%

Income and Social Contribution Taxes - Current (7,591) -2.0% (4,365) -1.2% 73.9% (18,974) -1.7% (6,010) -0.6% 215.7%

Income and Social Contribution Taxes - Deferred (2,385) -0.6% (3,207) -0.9% -25.6% (304) 0.0% (303) 0.0% 0.3%

Net Income for the PeriodNet Income for the PeriodNet Income for the PeriodNet Income for the Period 51,91751,91751,91751,917 13.8%13.8%13.8%13.8% 57,53557,53557,53557,535 16.4%16.4%16.4%16.4% -9.8%-9.8%-9.8%-9.8% 177,764177,764177,764177,764 16.0%16.0%16.0%16.0% 148,468148,468148,468148,468 14.2%14.2%14.2%14.2% 19.7%19.7%19.7%19.7%

Allocated to controlling shareholders 51,917 13.8% 57,535 16.4% -9.8% 177,764 16.0% 148,468 14.2% 19.7%

Earnings per share - R$Earnings per share - R$Earnings per share - R$Earnings per share - R$

Allocated to controlling shareholders 0.3222 0.3577 -9.9% 1.1044 0.9229 19.7%

EBITDA EBITDA EBITDA EBITDA 63,81763,81763,81763,817 17.0%17.0%17.0%17.0% 48,75148,75148,75148,751 13.9%13.9%13.9%13.9% 30.9%30.9%30.9%30.9% 179,434179,434179,434179,434 16.2%16.2%16.2%16.2% 146,618146,618146,618146,618 14.1%14.1%14.1%14.1% 22.4%22.4%22.4%22.4%

Part. (%)Part. (%)Part. (%)Part. (%)R$ ThousandR$ ThousandR$ ThousandR$ Thousand 3Q173Q173Q173Q17 Part. (%)Part. (%)Part. (%)Part. (%) 3Q163Q163Q163Q16 Part. (%)Part. (%)Part. (%)Part. (%) 9M179M179M179M17 Part. (%)Part. (%)Part. (%)Part. (%) 9M169M169M169M16

8

NET INCOME AND NET MARGIN NET INCOME AND NET MARGIN NET INCOME AND NET MARGIN NET INCOME AND NET MARGIN

The company’s net income totaled R$ 51.9 million in the quarter, a 9.8% decrease compared to 3Q16. In addition to the

points discussed in the previous section, the result is also explained by:

• Net financial revenue of R$ 13.3 million, a 56.3% decrease compared to 3Q16 due to (i) the recognition of R$

16.7 million in financial income in that quarter, from a lawsuit related to Compulsory Loan to Eletrobrás in the

80’s and 90’s and (ii) lower net financial income, resulting from lower interest rate from investments, related

to a decrease in DI and Selic rates and lower average cash position.

• Higher effective income tax rate than observed in 3Q16, as a result of (i) extemporaneous credit recognized in

3Q16 and (ii) higher volume of imported items invoiced in the quarter.

CAPITAL EXPENDITURE CAPITAL EXPENDITURE CAPITAL EXPENDITURE CAPITAL EXPENDITURE

Investments totaled R$ 13.5 million in the quarter and its allocation prioritized:

• Higher amount to industrial plants, with emphasis on the new wave of implementation of the automated

boxing and distribution system (Sorter) in the Anápolis/GO Distribution Center;

• Investments in technology directed to omnichannel initiatives and sales systems’ integration.

The increase compared to 3Q16 is explained by the different phasing of investments, which in 2016 were concentrated

in the fourth quarter. For 2017, the Company expects to invest up to R$ 67.9 million, in line with the capital budget

approved at the Ordinary General Meeting.

Reconciliation of EBITDA - R$ thousandReconciliation of EBITDA - R$ thousandReconciliation of EBITDA - R$ thousandReconciliation of EBITDA - R$ thousand 3Q173Q173Q173Q17 3Q163Q163Q163Q16Chg.Chg.Chg.Chg.

3Q17 / 3Q163Q17 / 3Q163Q17 / 3Q163Q17 / 3Q169M179M179M179M17 9M169M169M169M16

Chg.Chg.Chg.Chg.

9M17 / 9M169M17 / 9M169M17 / 9M169M17 / 9M16

Net IncomeNet IncomeNet IncomeNet Income 51,91751,91751,91751,917 57,53557,53557,53557,535 -9.8%-9.8%-9.8%-9.8% 177,764177,764177,764177,764 148,468148,468148,468148,468 19.7%19.7%19.7%19.7%

(+) Income and Social Contribution Tax 9,976 7,572 N.A 19,278 6,313 N.A

(-) Net Financial Income (13,317) (30,504) -56.3% (62,176) (50,134) 24.0%

(+) Depreciation and Amortization 15,241 14,148 7.7% 44,568 41,971 6.2%

= EBITDA= EBITDA= EBITDA= EBITDA 63,81763,81763,81763,817 48,75148,75148,75148,751 30.9%30.9%30.9%30.9% 179,434179,434179,434179,434 146,618146,618146,618146,618 22.4%22.4%22.4%22.4%

EBITDA MarginEBITDA MarginEBITDA MarginEBITDA Margin 17.0%17.0%17.0%17.0% 13.9%13.9%13.9%13.9% 310 bp310 bp310 bp310 bp 16.2%16.2%16.2%16.2% 14.1%14.1%14.1%14.1% 210 bp210 bp210 bp210 bp

9

CASH CASH CASH CASH FLOWSFLOWSFLOWSFLOWS

In 3Q17, Cia. Hering generated R$ 27.9 million of free cash, similar to 3Q16. Company’s higher profitability (EBITDA)

was offset by greater need of working capital, notably in inventories, explained by manufacture anticipation of the High

Summer collection aiming at optimizing the Company’s manufacturing process.

In addition, the amount allocated to investments increased in comparison to the same period last year, as detailed in

the respective section.

There was a positive flow of R$ 3.1 million in the quarter from franchisees’ financing program who joined the Store

Refurbishment Plan in 2016.

INDEBTEDNESSINDEBTEDNESSINDEBTEDNESSINDEBTEDNESS

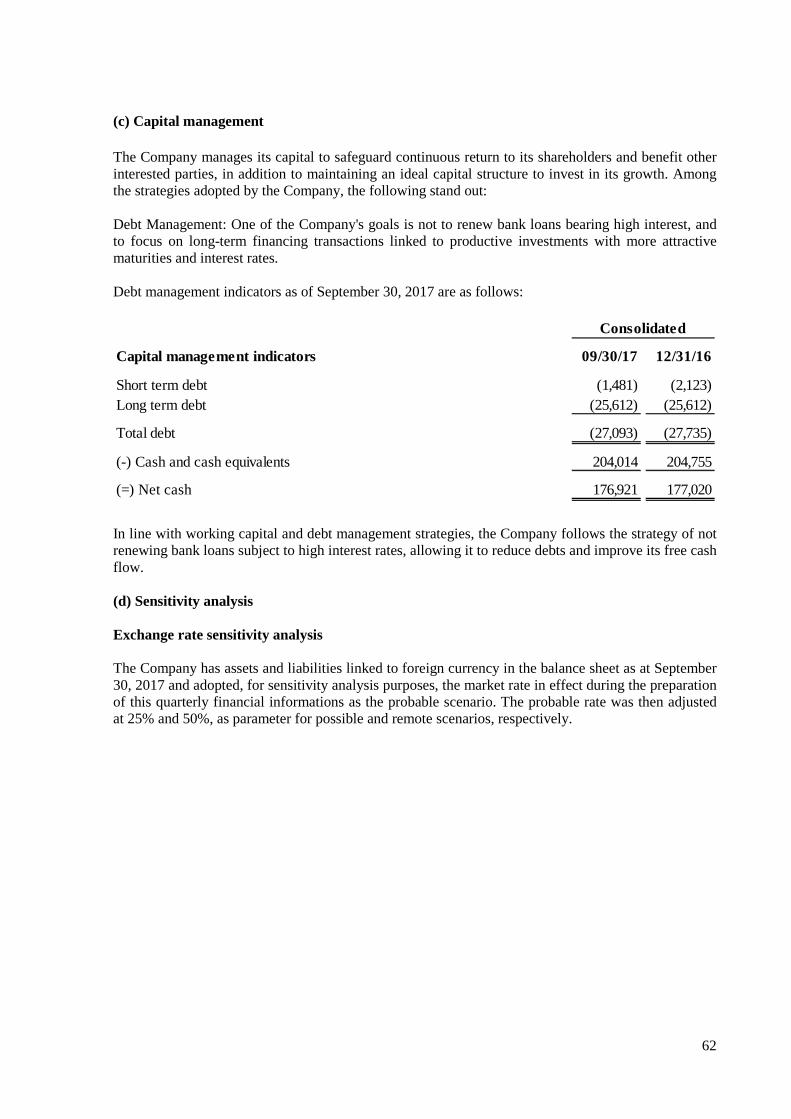

Cia. Hering ended 3Q17 with a net cash of R$ 176.9 million, as detailed below.

Cash Flow - Consol idated (R$ thousand)Cash Flow - Consol idated (R$ thousand)Cash Flow - Consol idated (R$ thousand)Cash Flow - Consol idated (R$ thousand) 3Q173Q173Q173Q17 3Q163Q163Q163Q16 Chg.Chg.Chg.Chg. 9M179M179M179M17 9M169M169M169M16 Chg.Chg.Chg.Chg.

EBITDAEBITDAEBITDAEBITDA 63,8 1763,8 1763,8 1763,8 17 48 ,75 148,75 148,75 148,75 1 15 ,06615 ,06615 ,06615 ,066 179,434179,434179,434179,434 146,6 18146,6 18146,6 18146,6 18 3 2 ,81 63 2,81 63 2,81 63 2,81 6

Non cash items 3,871 (5,475) 9,346 15,553 (3,409) 18,962

APV (Adjustment to Present Value) - Clients and Suppliers 6,821 3,858 2,963 17,585 14,715 2,870

Current Income tax and Social Contribution (7,591) (4,365) (3,226) (18,974) (6,010) (12,964)

Working Capital CapexWorking Capital CapexWorking Capital CapexWorking Capital Capex (25,5 87)(25,5 87)(25,5 87)(25,5 87) (10 ,63 6)(10,63 6)(10,63 6)(10,63 6) (14 ,951)(14 ,951)(14 ,951)(14 ,951) (49 ,448)(49,448)(49,448)(49,448) 74 ,1 4274,1 4274,1 4274,1 42 (12 3,59 0)(12 3,59 0)(12 3,59 0)(12 3,59 0)

(Increase) decrease in trade accounts receivable 19,989 7,102 12,887 54,829 99,824 (44,995)

(Increase) decrease in inventories (50,075) (32,013) (18,062) (108,060) (19,443) (88,617)

Increase (decrease) in accounts payable to suppliers (8,814) 25,329 (34,143) (25,810) 12,581 (38,391)

(Decrease) in taxes payable 1,672 (4,418) 6,090 (8,104) (21,043) 12,939

Refurbishment Project - Franchisee Financing 3,144 (6,117) 9,261 9,146 (8,612) 17,758

Others 8,497 (519) 9,016 28,551 10,835 17,716

CapExCapExCapExCapEx (13,3 86)(13,3 86)(13,3 86)(13,3 86) (4 ,30 3)(4 ,30 3)(4 ,30 3)(4 ,30 3) (9 ,083)(9 ,083)(9 ,083)(9 ,083) (34 ,682)(34,682)(34,682)(34,682) (14 ,2 58)(14,2 58)(14,2 58)(14,2 58) (2 0 ,42 4)(2 0,42 4)(2 0,42 4)(2 0,42 4)

Free Cash FlowFree Cash FlowFree Cash FlowFree Cash Flow 27,9 4527,9 4527,9 4527,9 45 27 ,83 027,83 027,83 027,83 0 115115115115 109,468109,468109,468109,468 211,7 98211,7 98211,7 98211,7 98 (10 2,33 0)(10 2,33 0)(10 2,33 0)(10 2,33 0)

Management and Ac counting Cash Flow Conc i l iation (R$ thousand)Management and Ac counting Cash Flow Conc i l iation (R$ thousand)Management and Ac counting Cash Flow Conc i l iation (R$ thousand)Management and Ac counting Cash Flow Conc i l iation (R$ thousand) 3Q173Q173Q173Q17 3Q163Q163Q163Q16 Chg.Chg.Chg.Chg. 9M179M179M179M17 9M169M169M169M16 Chg.Chg.Chg.Chg.

DFC - Cash prov ided by operating ac tiv ities DFC - Cash prov ided by operating ac tiv ities DFC - Cash prov ided by operating ac tiv ities DFC - Cash prov ided by operating ac tiv ities 48,0 7048,0 7048,0 7048,0 70 58 ,77 958,77 958,77 958,77 9 (10 ,709)(10 ,709)(10 ,709)(10 ,709) 189,512189,512189,512189,512 261,4 75261,4 75261,4 75261,4 75 (7 1 ,96 3)(7 1,96 3)(7 1,96 3)(7 1,96 3)

Adjustment – Financ ial i tems al loc ated to operating c ashAdjustment – Financ ial i tems al loc ated to operating c ashAdjustment – Financ ial i tems al loc ated to operating c ashAdjustment – Financ ial i tems al loc ated to operating c ash (6 ,7 39)(6 ,7 39)(6 ,7 39)(6 ,7 39) (26 ,64 6)(26,64 6)(26,64 6)(26,64 6) 19 ,90719 ,90719 ,90719 ,907 (45 ,362)(45,362)(45,362)(45,362) (35 ,4 19)(35,4 19)(35,4 19)(35,4 19) (9 ,94 3)(9 ,94 3)(9 ,94 3)(9 ,94 3)

Unrealized exchange and monetary variation (742) - (742) (2,291) - (2,291)

Financial Result (13,317) (30,504) 17,187 (62,176) (50,134) (12,042)

APV (Adjustment to Present Value) - Clients and Suppliers 6,821 3,858 2,963 17,585 14,715 2,870

Interest paid on loans 499 - 499 1,520 - 1,520

DFC - Cash f lows from investing activ itiesDFC - Cash f lows from investing activ itiesDFC - Cash f lows from investing activ itiesDFC - Cash f lows from investing activ ities (13,3 86)(13,3 86)(13,3 86)(13,3 86) (4 ,30 3)(4 ,30 3)(4 ,30 3)(4 ,30 3) (9 ,083)(9 ,083)(9 ,083)(9 ,083) (34 ,682)(34,682)(34,682)(34,682) (14 ,2 58)(14,2 58)(14,2 58)(14,2 58) (2 0 ,42 4)(2 0,42 4)(2 0,42 4)(2 0,42 4)

Free Cash Flow GenerationFree Cash Flow GenerationFree Cash Flow GenerationFree Cash Flow Generation 27,9 4527,9 4527,9 4527,9 45 27 ,83 027,83 027,83 027,83 0 115115115115 109,468109,468109,468109,468 211,7 98211,7 98211,7 98211,7 98 (10 2,33 0)(10 2,33 0)(10 2,33 0)(10 2,33 0)

* The adjusted cash flow as presented above is not a Brazilian Generally Accepted Accounting Practice and IFRS financial performance measurement. The

information on this table was calculated for the management of the Company and has not been audited by independent auditors.

** Working Capital provisions in this Cash Flow Statement were reported as Non-cash items, which explains the difference between the reported figures in the

balance sheet.

Indebtedness - R$ thousandIndebtedness - R$ thousandIndebtedness - R$ thousandIndebtedness - R$ thousand 3Q173Q173Q173Q17% of % of % of % of

total debttotal debttotal debttotal debt2Q172Q172Q172Q17

% of % of % of % of

total debttotal debttotal debttotal debt3Q163Q163Q163Q16

% of % of % of % of

total debttotal debttotal debttotal debt

Short Term (1,481) 5% (2,651) 9% - 0%

Long Term (25,612) 95% (25,612) 91% - 0%

TotalTotalTotalTotal (27,093)(27,093)(27,093)(27,093) 100%100%100%100% (28,263)(28,263)(28,263)(28,263) 100%100%100%100% ---- 0%0%0%0%

(-) Cash and Cash Equivalents 204,014 212,666 270,599

(=) Net Cash(=) Net Cash(=) Net Cash(=) Net Cash 176,921176,921176,921176,921 184,403184,403184,403184,403 270,599270,599270,599270,599

KPMG Auditores Independentes, uma sociedade simples brasileira e firma-membro da rede KPMG de firmas-membro independentes e afiliadas à KPMG International Cooperative (“KPMG International”), uma entidade suíça.

KPMG Auditores Independentes, a Brazilian entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

KPMG Auditores Independentes

R. São Paulo, 31 - 1º andar - Sala 11 - Bairro Bucarein

89202-200 - Joinville/SC - Brasil

Caixa Postal 2077 - CEP 89201-970 - Joinville/SC - Brasil

Telefone +55 (47) 3205-7800, Fax +55 (47) 3205-7815

www.kpmg.com.br

Quarterly Information Review Report (A free translation of the original report in Portuguese)

To the Shareholders and Board of Directors Cia Hering Blumenau - SC Introduction We have reviewed the interim financial statements, individual and consolidated, of Cia Hering (“Company”) contained within the Quarterly Information for the quarter ended September 30, 2017, which comprise the balance sheet as of September 30, 2017 and the related statements of income and comprehensive income, for the three and nine months period then ended and the changes in shareholders’ equity and cash flows for the nine months period then ended, including the notes to the financial statements. Management is responsible for the preparation of the interim financial statements in accordance with the technical pronouncement CPC 21(R1) and IAS 34 - Interim Financial Reporting, issued by the International Accounting Standards Board - IASB, as well as for the presentation of these information in accordance with the standards issued by the Brazilian Securities and Exchange Commission (CVM) applicable to the Quarterly Information. Our responsibility is to express a conclusion on the interim financial statements based on our review. Scope of the review We conducted our review in accordance with Brazilian and international standards for reviewing interim financial information (NBC TR 2410 and ISRE 2410 - Review of Interim Financial Information Performed by the Independent Auditor of the Entity, respectively). An interim review consists principally of making enquiries and having discussions with persons responsible for financial and accounting matters, and applying analytical and other review procedures. An interim review is substantially less in scope than an audit conducted in accordance with auditing standards and, consequently, does not provide assurance that we would become aware of any or all significant matters that might be identified in an audit. Accordingly, we do not express such an audit opinion.

KPMG Auditores Independentes, uma sociedade simples brasileira e firma-membro da rede KPMG de firmas-membro independentes e afiliadas à KPMG International Cooperative (“KPMG International”), uma entidade suíça.

KPMG Auditores Independentes, a Brazilian entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

Conclusion about the interim financial statements Based on our review, we are not aware of any fact that leads us to believe that the individual and consolidated interim financial statements included in the quarterly information referred to above have not been prepared, in all material respects, in accordance with CPC 21(R1) and IAS 34 issued by the IASB applicable to the Quarterly Information and presented in accordance with the standards issued by the Brazilian Securities and Exchange Commission.

Other issues

Statements of value added The individual and consolidated interim financial statements, in relation to the statements of value added for the nine months period ended in September 30, 2017, prepared under the responsibility of the Company’s Management and presented as supplementary information regarding IAS 34, were submitted to review procedures performed jointly with the review of the interim quarterly information of the Company. In order to form our conclusion, we assessed if the statements are reconciled with the interim accounting information and records, as applicable, and if their form and content are in accordance with the criteria defined in CPC 09 - Statements of Value Added. Based on our review, we are not aware of any fact that would lead us to believe that the statements of value added aforementioned have not been fairly stated, in all material aspects, in relation to the interim financial statements, individual and consolidated, taken as a whole. Comparative interim financial information The amounts reported in the individual and consolidated balance sheets as of December 31, 2016 were previously audited by other independent auditors who issued an unqualified report on February 13, 2017. The amounts reported in the individual and consolidated statements of income and comprehensive income for the three and nine months period ended September 30, 2016 and changes in equity and cash flows for the three and nine months period ended September 30, 2016, were previously reviewed by other independent auditors who issued an unqualified report on October 21, 2016. The individual company and consolidated statements of value added for the nine month period ended September 30, 2016 were submitted to the same review procedures by those independent auditors and based on their review, those auditors issued an opinion reporting that nothing had come to their attention that caused them to believe that the accompanying statements of value added had not been prepared, in all material respects, in accordance with the individual and consolidated interim financial information taken as a whole. Joinville October 20, 2017 KPMG Auditores Independentes CRC SC-000071/F-8 Original report in Portuguese signed by Marcelo Lima Tonini Accountant CRC PR-045569/O-4 T - SC

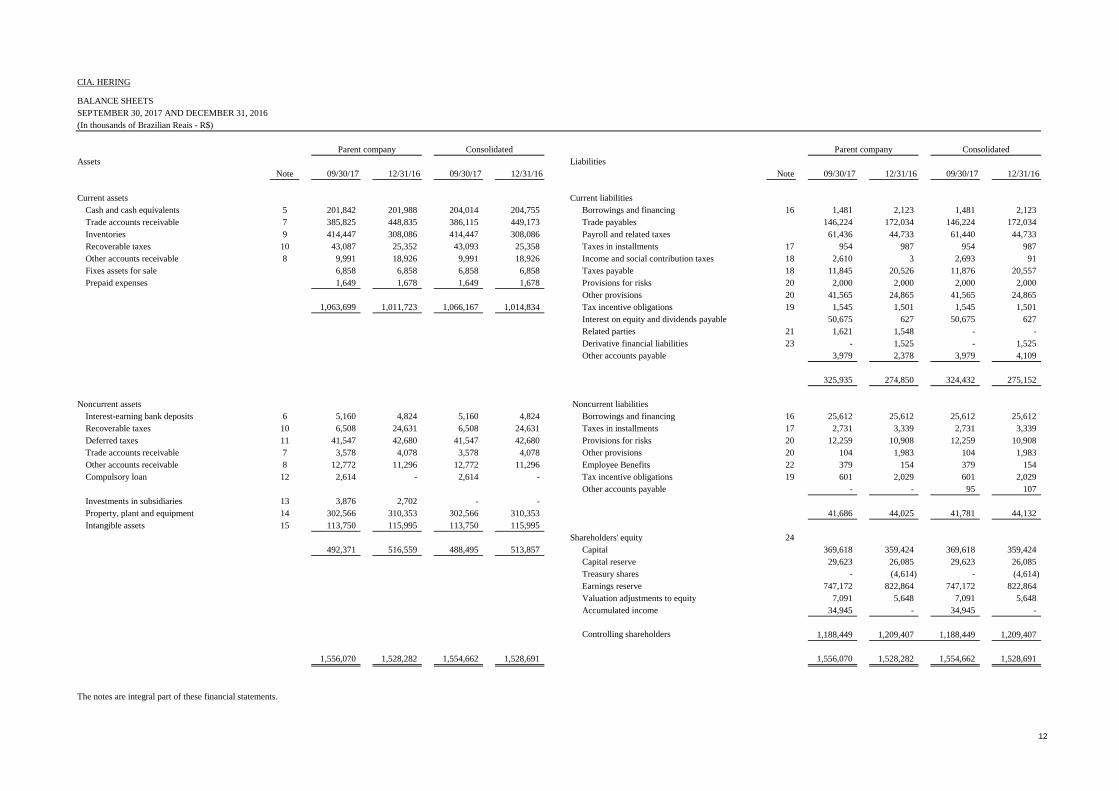

CIA. HERING

BALANCE SHEETSSEPTEMBER 30, 2017 AND DECEMBER 31, 2016(In thousands of Brazilian Reais - R$)

Assets LiabilitiesNote 09/30/17 12/31/16 09/30/17 12/31/16 Note 09/30/17 12/31/16 09/30/17 12/31/16

Current assets Current liabilitiesCash and cash equivalents 5 201,842 201,988 204,014 204,755 Borrowings and financing 16 1,481 2,123 1,481 2,123 Trade accounts receivable 7 385,825 448,835 386,115 449,173 Trade payables 146,224 172,034 146,224 172,034 Inventories 9 414,447 308,086 414,447 308,086 Payroll and related taxes 61,436 44,733 61,440 44,733 Recoverable taxes 10 43,087 25,352 43,093 25,358 Taxes in installments 17 954 987 954 987 Other accounts receivable 8 9,991 18,926 9,991 18,926 Income and social contribution taxes 18 2,610 3 2,693 91 Fixes assets for sale 6,858 6,858 6,858 6,858 Taxes payable 18 11,845 20,526 11,876 20,557 Prepaid expenses 1,649 1,678 1,649 1,678 Provisions for risks 20 2,000 2,000 2,000 2,000

Other provisions 20 41,565 24,865 41,565 24,865 1,063,699 1,011,723 1,066,167 1,014,834 Tax incentive obligations 19 1,545 1,501 1,545 1,501

Interest on equity and dividends payable 50,675 627 50,675 627 Related parties 21 1,621 1,548 - - Derivative financial liabilities 23 - 1,525 - 1,525 Other accounts payable 3,979 2,378 3,979 4,109

325,935 274,850 324,432 275,152

Noncurrent assets Noncurrent liabilitiesInterest-earning bank deposits 6 5,160 4,824 5,160 4,824 Borrowings and financing 16 25,612 25,612 25,612 25,612 Recoverable taxes 10 6,508 24,631 6,508 24,631 Taxes in installments 17 2,731 3,339 2,731 3,339 Deferred taxes 11 41,547 42,680 41,547 42,680 Provisions for risks 20 12,259 10,908 12,259 10,908 Trade accounts receivable 7 3,578 4,078 3,578 4,078 Other provisions 20 104 1,983 104 1,983 Other accounts receivable 8 12,772 11,296 12,772 11,296 Employee Benefits 22 379 154 379 154 Compulsory loan 12 2,614 - 2,614 - Tax incentive obligations 19 601 2,029 601 2,029

Other accounts payable - - 95 107 Investments in subsidiaries 13 3,876 2,702 - - Property, plant and equipment 14 302,566 310,353 302,566 310,353 41,686 44,025 41,781 44,132 Intangible assets 15 113,750 115,995 113,750 115,995

Shareholders' equity 24492,371 516,559 488,495 513,857 Capital 369,618 359,424 369,618 359,424

Capital reserve 29,623 26,085 29,623 26,085 Treasury shares - (4,614) - (4,614) Earnings reserve 747,172 822,864 747,172 822,864 Valuation adjustments to equity 7,091 5,648 7,091 5,648 Accumulated income 34,945 - 34,945 -

Controlling shareholders 1,188,449 1,209,407 1,188,449 1,209,407

1,556,070 1,528,282 1,554,662 1,528,691 1,556,070 1,528,282 1,554,662 1,528,691

The notes are integral part of these financial statements.

Parent company ConsolidatedConsolidatedParent company

12

CIA. HERING

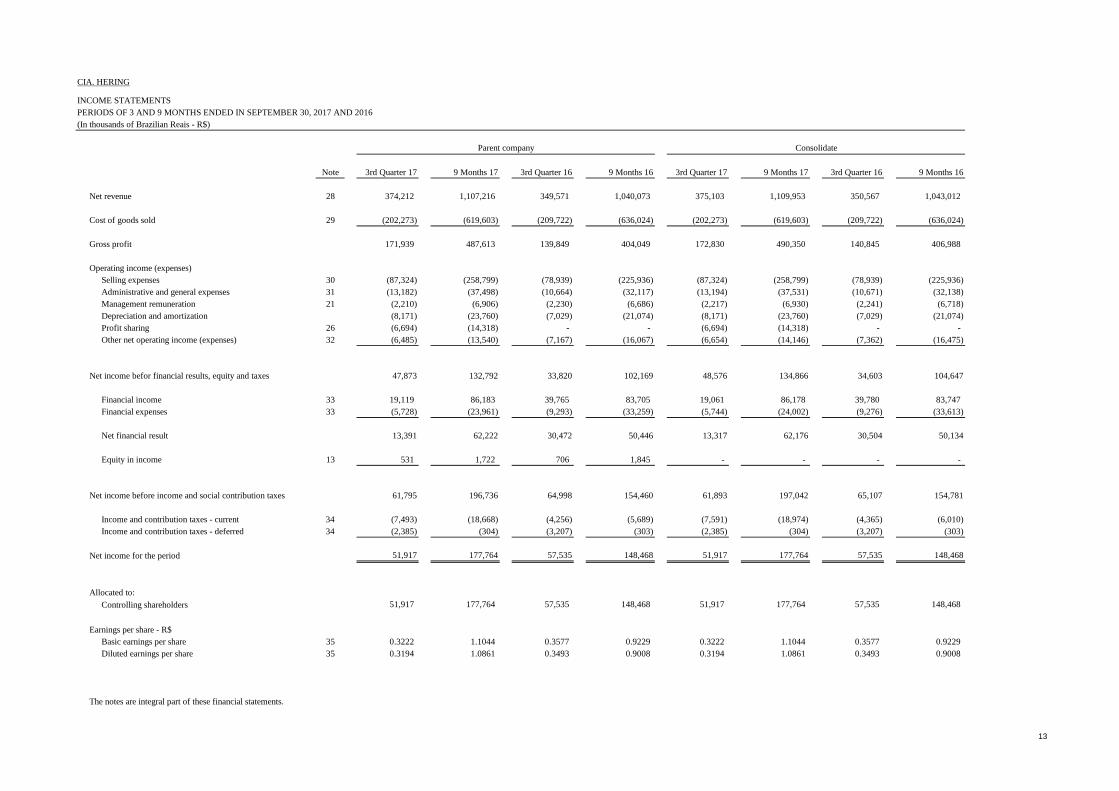

INCOME STATEMENTSPERIODS OF 3 AND 9 MONTHS ENDED IN SEPTEMBER 30, 2017 AND 2016(In thousands of Brazilian Reais - R$)

Note 3rd Quarter 17 9 Months 17 3rd Quarter 16 9 Months 16 3rd Quarter 17 9 Months 17 3rd Quarter 16 9 Months 16

Net revenue 28 374,212 1,107,216 349,571 1,040,073 375,103 1,109,953 350,567 1,043,012

3.04Cost of goods sold 29 (202,273) (619,603) (209,722) (636,024) (202,273) (619,603) (209,722) (636,024)

Gross profit 171,939 487,613 139,849 404,049 172,830 490,350 140,845 406,988

Operating income (expenses)3.06.01Selling expenses 30 (87,324) (258,799) (78,939) (225,936) (87,324) (258,799) (78,939) (225,936) 3.06.02.02Administrative and general expenses 31 (13,182) (37,498) (10,664) (32,117) (13,194) (37,531) (10,671) (32,138) 3.06.02.01Management remuneration 21 (2,210) (6,906) (2,230) (6,686) (2,217) (6,930) (2,241) (6,718) 3.06.02.03Depreciation and amortization (8,171) (23,760) (7,029) (21,074) (8,171) (23,760) (7,029) (21,074) 3.06.05.01Profit sharing 26 (6,694) (14,318) - - (6,694) (14,318) - - 3.06.05.02Other net operating income (expenses) 32 (6,485) (13,540) (7,167) (16,067) (6,654) (14,146) (7,362) (16,475)

3.06.03Net income befor financial results, equity and taxes 47,873 132,792 33,820 102,169 48,576 134,866 34,603 104,647

Financial income 33 19,119 86,183 39,765 83,705 19,061 86,178 39,780 83,747 Financial expenses 33 (5,728) (23,961) (9,293) (33,259) (5,744) (24,002) (9,276) (33,613)

3.06.03.02.023.06.06.02Net financial result 13,391 62,222 30,472 50,446 13,317 62,176 30,504 50,1343.06.06.01

Equity in income 13 531 1,722 706 1,845 - - - -

3.10Net income before income and social contribution taxes 61,795 196,736 64,998 154,460 61,893 197,042 65,107 154,7813.11

Income and contribution taxes - current 34 (7,493) (18,668) (4,256) (5,689) (7,591) (18,974) (4,365) (6,010) Income and contribution taxes - deferred 34 (2,385) (304) (3,207) (303) (2,385) (304) (3,207) (303)

Net income for the period 51,917 177,764 57,535 148,468 51,917 177,764 57,535 148,468

Allocated to:

Controlling shareholders 51,917 177,764 57,535 148,468 51,917 177,764 57,535 148,468

Earnings per share - R$Basic earnings per share 35 0.3222 1.1044 0.3577 0.9229 0.3222 1.1044 0.3577 0.9229 Diluted earnings per share 35 0.3194 1.0861 0.3493 0.9008 0.3194 1.0861 0.3493 0.9008

The notes are integral part of these financial statements.

Parent company Consolidate

13

CIA. HERING

STATEMENT OF COMPREHENSIVE INCOMEPERIODS OF 3 AND 9 MONTHS ENDED IN SEPTEMBER 30, 2017 AND 2016(In thousands of Brazilian Reais - R$)

Note 3rd Quarter 17 9 Months 17 3rd Quarter 16 9 Months 16 3rd Quarter 17 9 Months 17 3rd Quarter 16 9 Months 16

Net income 51,917 177,764 57,535 148,468 51,917 177,764 57,535 148,468

Items that can be subsequently reclassified to profit:Fair value of financial instruments of cash flow hedge - - 1,228 (8,363) - - 1,228 (8,363)

- - 1,228 (8,363) - - 1,228 (8,363)

Comprehensive income 51,917 177,764 58,763 140,105 51,917 177,764 58,763 140,1053

Profit allocated to: Controlling shareholders 51,917 177,764 58,763 140,105 51,917 177,764 58,763 140,105

4The notes are integral part of these financial statements.

Parent company Consolidated

14

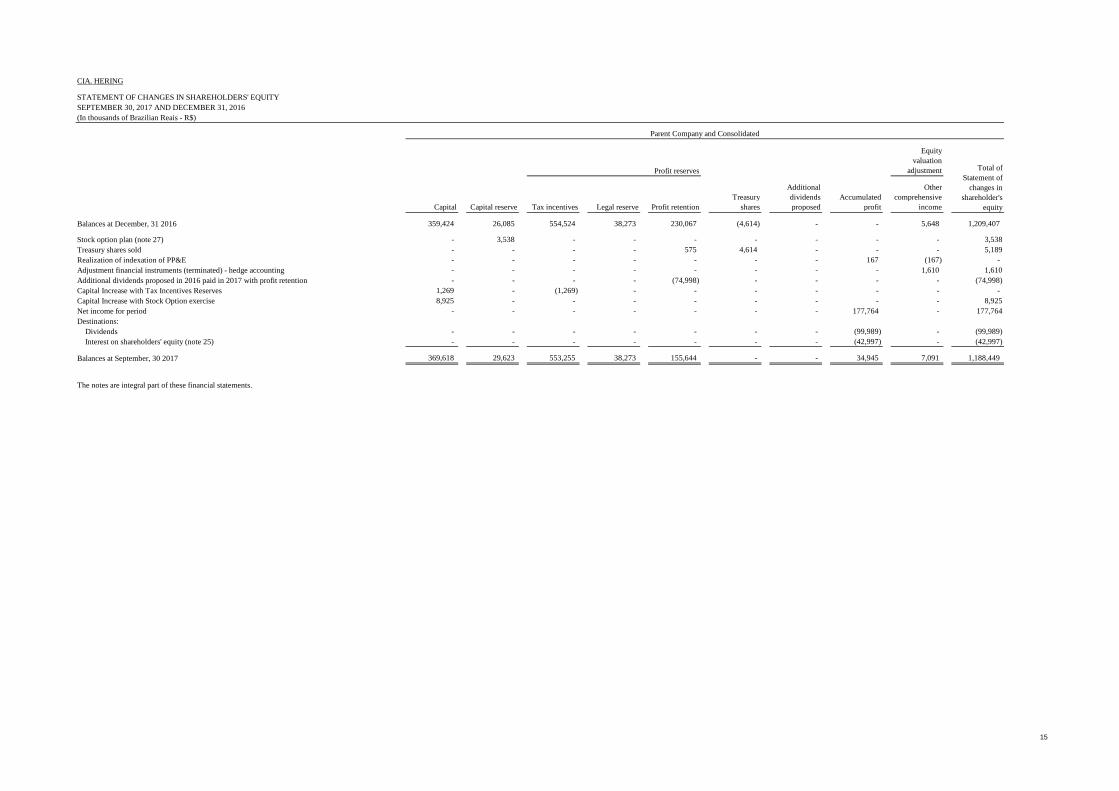

CIA. HERING

STATEMENT OF CHANGES IN SHAREHOLDERS' EQUITYSEPTEMBER 30, 2017 AND DECEMBER 31, 2016(In thousands of Brazilian Reais - R$)

Equity valuation

adjustment

Capital Capital reserve Tax incentives Legal reserve Profit retention Treasury

shares

Additional dividends proposed

Accumulated profit

Other comprehensive

income

Balances at December, 31 2016 359,424 26,085 554,524 38,273 230,067 (4,614) - - 5,648 1,209,407

Stock option plan (note 27) - 3,538 - - - - - - - 3,538Treasury shares sold - - - - 575 4,614 - - - 5,189Realization of indexation of PP&E - - - - - - - 167 (167) - Adjustment financial instruments (terminated) - hedge accounting - - - - - - - - 1,610 1,610Additional dividends proposed in 2016 paid in 2017 with profit retention - - - - (74,998) - - - - (74,998) Capital Increase with Tax Incentives Reserves 1,269 - (1,269) - - - - - - - Capital Increase with Stock Option exercise 8,925 - - - - - - - - 8,925Net income for period - - - - - - - 177,764 - 177,764Destinations:

Dividends - - - - - - - (99,989) - (99,989) Interest on shareholders' equity (note 25) - - - - - - - (42,997) - (42,997)

Balances at September, 30 2017 369,618 29,623 553,255 38,273 155,644 - - 34,945 7,091 1,188,449

The notes are integral part of these financial statements.

Parent Company and Consolidated

Profit reserves Total of Statement of

changes in shareholder's

equity

15

CIA. HERING

STATEMENT OF CHANGES IN SHAREHOLDERS' EQUITYSEPTEMBER 30, 2016 AND DECEMBER 31, 2015(In thousands of Brazilian Reais - R$)

Equity valuation

adjustment

Capital Capital reserve Tax incentives Legal reserve Profit retention Treasury

shares

Additional dividends proposed

Accumulated profit

Other comprehensive

income

Balances at December, 31 2015 346,368 20,569 424,298 28,302 344,179 (41,323) 39,994 - 11,577 1,173,964

Stock option plan (note 27) - 4,157 - - - - - - - 4,157Treasury shares cancel - - - - (36,323) 36,323 - - - - Treasury shares sold - - - - (10) 386 - - - 376Realization of indexation of PP&E - - - - - - - 170 (170) - Adjustment financial instruments (terminated) - hedge accounting - - - - - - - - (4,093) (4,093) Adjustment financial instruments (outstanding) - hedge accounting - - - - - - - - (4,270) (4,270) Additional dividends proposed in 2015 paid in 2016 - - - - - - (39,994) - - (39,994) Transfer of profit retention reserve 13,056 - - - (13,056) - - - - - Net income for period - - - - - - - 148,468 - 148,468Destinations:

Dividends and Interest on shareholders' equity (note 24.e and 25) - - - - - - - (42,086) - (42,086)

Balances at September, 30 2016 359,424 24,726 424,298 28,302 294,790 (4,614) - 106,552 3,044 1,236,522

The notes are integral part of these financial statements.

Parent Company and Consolidated

Profit reserves Total of Statement of

changes in shareholder's

equity

16

CIA. HERING

STATEMENT OF CASH FLOWS

PERIODS OF 9 MONTHS ENDED IN SEPTEMBER 30, 2017 AND 2016

(In thousands of Brazilian Reais - R$)

09/30/17 09/30/16 09/30/17 09/30/16

Cash flows from operating activities4.01.01.01

Net income of the period 177,764 148,468 177,764 148,468 Adjustments to reconcile net income to net cash generated by

4.01.01.02 operating activities:4.01.01.03 Deferred taxes 304 303 304 303 4.01.01.04 Unrealized exchange and monetary variation 2,365 (259) 2,291 - 4.01.01.05 Depreciation and amortization 44,568 41,971 44,568 41,971 4.01.01.06 Provision for doubtful accounts 8,729 6,173 8,729 6,173 4.01.01.07 Write-off of fixed assets 146 235 146 235

Stock option plan 3,538 4,157 3,538 4,157 Provision for adjustment to realizable value 1,699 5,774 1,699 5,774 Provisions for contingencies 3,830 3,070 3,830 3,070 Employee Benefits 225 1,584 225 1,584 Compulsory loan (2,614) (24,402) (2,614) (24,402) Equity in (loss) income of subsidiaries (1,722) (1,845) - -

4.01.02.01Changes in assets and liabilities4.01.02.02 Decrease in trade accounts receivable 54,781 99,467 54,829 99,824 4.01.02.03 (Increase) in inventories (108,060) (19,443) (108,060) (19,443) 4.01.02.04 Decrease in recoverable taxes 388 7,292 388 7,290 4.01.02.05 Decrease (increase) in other accounts receivable 7,488 (584) 7,488 (584) 4.01.02.06 (Decrease) increase in accounts payable to suppliers (25,810) 12,581 (25,810) 12,581 4.01.02.06 Increase (decrease) in accounts payable and provisions 31,559 (4,101) 29,821 (4,483)

Increase in IRPJ and CSLL 13,778 3,539 14,038 3,813 4.01.02.07 Income tax and social contribution paid (11,171) (3,460) (11,436) (3,722) 4.03.05 (Decrease) in taxes payable (10,706) (21,133) (10,706) (21,134)

Interest paid on loans (1,520) - (1,520) -

Cash provided by operating activities 189,559 259,387 189,512 261,475

Cash flows from investing activitiesDividends received 548 1,128 - -

4.02.01 Purchase of property, plant and equipment (22,620) (6,004) (22,620) (6,004) Purchase of intangible assets (12,062) (8,254) (12,062) (8,254)

Cash used in investing activities (34,134) (13,130) (34,682) (14,258)

4.03.01Cash flows from financing activities4.03.02Capital increase 8,925 - 8,925 - 4.03.07Interest earning bank deposits (336) (1,701) (336) (1,701) 4.03.03Interest on equity and dividends (167,936) (82,078) (167,936) (82,078)

Repayments of loans (1,413) (1,308) (1,413) (1,308) 4.03.06Disposal of treasury shares for the stock option plan 5,189 376 5,189 376

Cash used in financing activities (155,571) (84,711) (155,571) (84,711)

(Decrease) Increase in cash and cash equivalents (146) 161,546 (741) 162,506

4.05.01(Decrease) Increase in cash and cash equivalents4.05.02At the beginning of the period 201,988 104,325 204,755 108,093

At the end of the period 201,842 265,871 204,014 270,599

(146) 161,546 (741) 162,506

The notes are integral part of these financial statements.

Parent company Consolidated

17

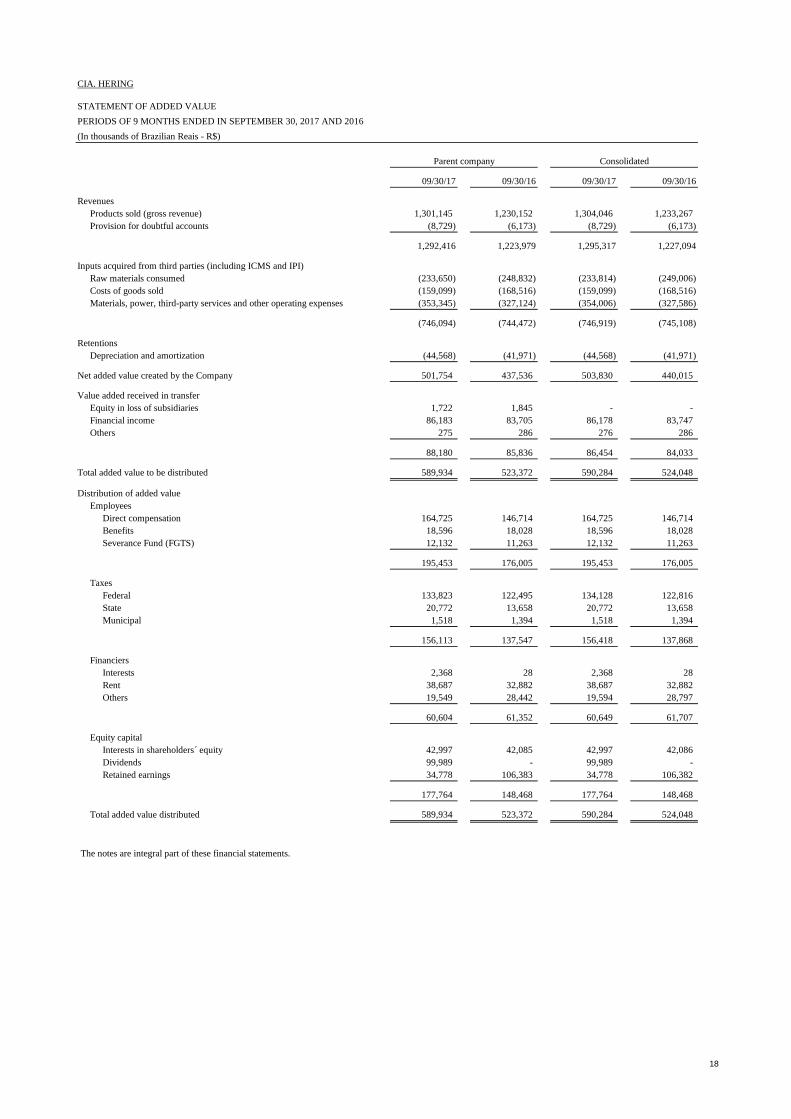

CIA. HERING

STATEMENT OF ADDED VALUE

PERIODS OF 9 MONTHS ENDED IN SEPTEMBER 30, 2017 AND 2016

(In thousands of Brazilian Reais - R$)

09/30/17 09/30/16 09/30/17 09/30/16

RevenuesProducts sold (gross revenue) 1,301,145 1,230,152 1,304,046 1,233,267 Provision for doubtful accounts (8,729) (6,173) (8,729) (6,173)

1,292,416 1,223,979 1,295,317 1,227,094

Inputs acquired from third parties (including ICMS and IPI)Raw materials consumed (233,650) (248,832) (233,814) (249,006) Costs of goods sold (159,099) (168,516) (159,099) (168,516) Materials, power, third-party services and other operating expenses (353,345) (327,124) (354,006) (327,586)

(746,094) (744,472) (746,919) (745,108)

RetentionsDepreciation and amortization (44,568) (41,971) (44,568) (41,971)

Net added value created by the Company 501,754 437,536 503,830 440,015

Value added received in transferEquity in loss of subsidiaries 1,722 1,845 - - Financial income 86,183 83,705 86,178 83,747 Others 275 286 276 286

88,180 85,836 86,454 84,033

Total added value to be distributed 589,934 523,372 590,284 524,048

Distribution of added valueEmployees

Direct compensation 164,725 146,714 164,725 146,714 Benefits 18,596 18,028 18,596 18,028 Severance Fund (FGTS) 12,132 11,263 12,132 11,263

195,453 176,005 195,453 176,005

TaxesFederal 133,823 122,495 134,128 122,816 State 20,772 13,658 20,772 13,658 Municipal 1,518 1,394 1,518 1,394

156,113 137,547 156,418 137,868

FinanciersInterests 2,368 28 2,368 28 Rent 38,687 32,882 38,687 32,882 Others 19,549 28,442 19,594 28,797

60,604 61,352 60,649 61,707

Equity capitalInterests in shareholders´ equity 42,997 42,085 42,997 42,086 Dividends 99,989 - 99,989 - Retained earnings 34,778 106,383 34,778 106,382

177,764 148,468 177,764 148,468

Total added value distributed 589,934 523,372 590,284 524,048

The notes are integral part of these financial statements.

Parent company Consolidated

18

19

CIA. HERING NOTES TO THE QUARTERLY FINANCIAL INFORMATION FOR THE PERIOD ENDED SEPTEMBER 30, 2017 AND 2016 (Amounts in thousands of Brazilian reais - R$, unless otherwise stated)

1 General information Cia. Hering, with main offices in Blumenau, Santa Catarina, and manufacturing units in the States of Santa Catarina, Goiás, and Rio Grande do Norte, was founded in 1880 and its key activity is the production and marketing of threads, fabrics, and knitwear, textiles and knitwear, and clothing in general. The Company's shares are traded on the New Market segment of São Paulo Stock Exchange (Bovespa), under the ticker symbol HGTX3.

2 Preparation basis (a) Statement of compliance with IFRS and CPCs (Accounting Pronouncements issued by the Accounting Pronouncements Committee) The company’s interim financial statements, contained in the Quarterly Financial Statements report as of September 30, 2017, comprise the individual and consolidated interim financial statements elaborated according to CPC 21 – Interim Financial Statements and IAS 34 – Interim Financial Reporting, issued by the IASB – International Accounting Standard Board and presented in accordance with the Brazilian Securities and Exchange Comission (“CVM”) laws related to Interim Financial Statements. The Company’s Administrators declare that all relevant information specific to the individual and consolidated quarterly information, and only such information, is being evidenced, and corresponds to the information used in management. The individual and consolidated interim financial information for the period ended September 30, 2017 was authorized for conclusion by Management on October 20, 2017. (b) Measurement basis The individual and consolidated quarterly financial information were prepared based on the historical cost, except for the defined benefit actuarial assets or liabilities that are recognized as the total net of plan assets, plus the unrecognized cost of prior service and unrecognized actuarial losses, net of unrecognized actuarial gains and the present value of the defined benefit obligation, the share based plan and derivative financial instruments, which are recognized at their fair values. (c) Functional currency and reporting currency This individual and consolidated quarterly financial information is presented in Brazilian Reais, which is the Company’s functional currency. All financial information presented in Brazilian Reais has been rounded to the nearest value, unless otherwise indicated.

20

(d) Use of estimates and judgments The preparation of individual and consolidated quarterly financial information according to IFRS and BR GAAP standards requires Management to make judgments, estimates and assumptions that affect the application of accounting principles and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. Estimates and assumptions are reviewed in a continuous manner. Revisions related to accounting estimates are recognized in the period when the estimates are revised and in any future period affected. Information about critical judgment referring to the accounting policies adopted which impact the amounts recognized in the individual and consolidated quarterly financial information, which may occasionally differ from realizable values, are included in the following notes: Note 11 - Realization of deferred income tax Note 20 – Provision for risk and other provisions Note 22 – Employee benefits Note 23 – Risk management and financial instruments Note 27 – Stock options plan measurement Note 36 - Classification and recording of lease agreements (e) Going Concern The quarterly financial information were prepared based on the assumption of continuity. Management has assessed the Company's ability to continue operating normally and is convinced that it has the resources to continue its business in the future. Management is not aware of any material uncertainties that could generate significant doubt as to its ability to continue operating.

3 Significant accounting policies The accounting policies summarized below have been consistently applied to all the periods presented in this individual and consolidated quarterly financial informations. (a) Consolidation base The consolidated quarterly financial information includes the quarterly financial information of Cia. Hering and its subsidiaries, as listed below:

País 09/30/17 12/31/16

Hering Internacional SAFI Uruguai 100.00 100.00

Participação (%)

HRG Comércio do Vestuário e IntermediaçãoBrasil 99.99 99.99

de Serviços Financeiros Ltda.

The quarterly financial information of the subsidiaries is included in the consolidated quarterly financial information as from the date they start to be controlled by the Company until the date such control ceases. The accounting policies of the subsidiaries are aligned with the policies adopted by the Company.

21

The quarterly financial information of subsidiaries is recognized under the equity method in the subsidiary’s individual quarterly financial information. Main procedures of consolidation: •••• Elimination of intercompany asset and liability account balances; •••• Elimination of investments in the equity of the subsidiaries; •••• Elimination of intercompany income and expense balances and unearned income arising from

intercompany transactions. Unrealized losses are eliminated in the same way as unrealized gains, but only to the extent that there is no evidence of impairment; and

•••• Identification of non-controlling interests in the consolidated quarterly financial information. (b) Foreign currency The Company’s Management has defined that its functional currency is the Real in accordance with the rules established in CPC 02 (R2) (IAS 21) - Effects of the Changes in Exchange Rates and Translation of Financial Statement, approved by CVM Resolution 640/10. Transactions in foreign currency, i.e. all transactions that are not carried out in the functional currency, are translated at the exchange rate on the dates of each transaction. Monetary assets and liabilities in foreign currency are translated into the functional currency at the exchange rate on the closing date. The gains and losses from the fluctuations in the exchange rates on monetary assets and liabilities are recognized in the statement of income. Non-monetary assets and liabilities acquired or contracted in foreign currency are translated based on the exchange rates on the dates of the transactions or on the dates of valuation at fair value when applicable. (c) Financial instruments (i) Non-derivative financial assets The Company initially recognizes the loans, receivables and deposits on the date that they are originated. All other financial assets (including assets designated at fair value through profit or loss) are initially recognized on the date of the negotiation under which the Company becomes a party to the contractual provisions of the instrument. The Company writes off a financial asset when the contractual rights to the cash flows from the financial asset expire, or when the Company transfers the contractual rights to receive the cash flows from a financial asset in a transaction that substantially transferred all the risks and rewards related to the ownership of the asset. Any interest in transferred financial assets that is created or retained by the Company is recognized as a separate asset or liability.

22

The Company has the following non-derivative assets: Investments held to maturity If the Company has the intent and capacity of holding to maturity the debt securities, these financial assets are classified as held to maturity. The investments held up to maturity are initially recognized at fair value plus any transaction costs directly assignable. After their initial recognition, investments held to maturity are measured at amortized cost using the effective interest rate method, reduced by any impairment losses. Any sale or reclassification of a significant amount of held-to-maturity investments not close to their maturity date would result in the reclassification of all held to-maturity investments as available-for-sale, preventing the Company from classifying investments as held-to-maturity for the current and the following two financial years.

Loans and receivables Loans and receivables are financial assets with fixed or determinable payments, but not quoted on any active market. Such assets are initially recognized at fair value plus any transaction costs directly assignable. After their initial recognition, loans and receivables are measured at amortized cost using the effective interest rate method, reduced by any impairment losses. Loans and receivables comprise trade accounts receivable and other credits. Cash and cash equivalents include balances of cash and interest earning bank deposits. (ii) Non-derivative financial liabilities The Company recognizes debt securities issued and subordinated liabilities on the date that they are originated. All other financial liabilities (including liabilities designated at fair value through profit or loss) are recognized initially on the negotiation date on which the Company becomes a party to the contractual provisions of the instrument. The Company writes off a financial liability when its contractual obligations are discharged, cancelled or settled. The Company has the following non-derivative financial liabilities: borrowings and financing, suppliers and other accounts payable. Such financial liabilities are initially recognized at fair value plus any transaction costs directly assignable. After their initial recognition, these financial liabilities are measured at amortized cost using the effective interest rate method. Financial assets and liabilities are offset and the net amount reported in the balance sheet only when there is a legally enforceable right to set off and there is intention to settle on a net basis, or to realize the asset and settle the liability simultaneously. (iii) Derivative financial liabilities The Company has derivative financial instruments to manage its exposure to currency risks, including forward foreign exchange contracts. Derivatives are initially recognized at fair value on contracting date and subsequently re-measured at fair value on period. Possible gains or losses are immediately recognized in income, unless derivative is assigned and effective as a hedge instrument, in this case, time of recognition in income depends on hedging relationship nature.

23

The Company assigns certain hedging instruments for risk in foreign exchange rates variation in firm commitments, as cash flow hedge. At the beginning of hedging relationship, for the adoption of the “ Hedge Accounting” the Company documents the relation between the hedge instrument and the hedged item with its objectives in risk management and its strategy to assume several hedging transactions. In addition, in the beginning of the hedge operation and continuously, the Company documents if the hedging instrument used in a hedging relationship is highly effective to offset in the hedged item's fair value or cash flow, attributable to the hedged risk. The effective portion of changes in derivatives’ fair value that is assigned and qualified as cash flow hedge is recognized in other comprehensive income. Gains or losses related to the ineffective portion are immediately recognized under “financial income”. Amounts previously recognized in other comprehensive income and accumulated in shareholders' equity are reclassified into income for the period in which the hedged item affects income, under the same statement of income caption in which such item is recognized. However, when a foreseen hedged transaction results in the recognition of a non-financial asset or liability, gains and losses previously recognized in other comprehensive income and accumulated in equity are transferred to the initial measurement of this asset or liability cost. “Hedge accounting” is interrupted when the Company cancels the hedging relationship, hedge instrument matures or is sold, rescinded or executed, or no longer qualifies as hedge accounting. Any gains or losses recognized in other comprehensive income and accumulated in equity on that date remain in equity and are recognized when foreseen transaction is finally recognized in income. When the foreseen transaction is no longer expected to occur, accumulated gains or losses that are deferred in shareholders' equity are immediately recognized in income. Derivatives that are not assigned as hedging instruments are classified as current assets or liabilities. Note 23 includes more detailed information on derivative financial instruments. (d) Cash and cash equivalents Includes cash balances, current accounts (demand bank deposits), short term investments (interest earning bank deposits) considered immediately marketable or convertible into a known sum of cash and subject to an insignificant risk of change of value. Interest earning bank deposits are presented at cost plus income calculated up to the balance sheet date and do not exceed the market value. (e) Trade accounts receivable Trade accounts receivable are recorded at the amount invoiced, adjusted to present value (note 7). The amount recorded as provision for doubtful accounts is considered sufficient by management to cover any losses on the realization of the receivables. (f) Inventories Inventories are measured at the lower value between the cost and net realizable value. The cost of inventories is based on the weighted cost of acquisition or production and includes expenditures for acquiring, production and conversing costs, as well as other costs incurred in bringing them to their existing location and condition. In the case of manufactured inventories and work in progress, cost includes an appropriate share of overheads based on normal operating capacity.

24

The net realizable value is the estimated price at which inventories can be realized in the normal course of business, deducted from the estimated completion costs and selling expenses. (g) Property, plant and equipment (PP&E) (i) Recognition and measurement PP&E items are stated at historical acquisition or construction cost, net of accumulated depreciation and impairment losses, when applicable. Purchased software that is integral to the functionality of a piece of equipment is capitalized as part of that equipment. When parts of a PP&E item have different useful lives, they are accounted for as separate items (major components) of PP&E. Gains and losses on disposal of a PP&E item are determined by comparing the proceeds from disposal with the carrying amount of PP&E and are recognized net within "Other income" in the income statement. (ii) Depreciation Depreciation is calculated over the depreciable amount, which is the cost of an asset, or other amount substituted for cost. The residual value of the assets written off is not material, and, accordingly, is not considered in the determination of the depreciable amount. Depreciation is recognized in the income statement using the straight-line method over the estimated useful life of each part of an item of property, plant and equipment, since this is the method that best reflects the consumption pattern of the future economic benefits embodied in the asset. Land is not depreciated. The estimated useful lives for the current period were calculated using the weighted average useful life of the assets of each group, are presented below:

Average useful life (years)

Buildings and improvements 31.48 Facilities and production equipament 9.44 Furniture and fixtures 6.28 Computer and peripherals 4.78 Vehicles 4.52 Leasehold improvements 7.58

Description

The depreciation methods, useful lives and residual values will be reviewed at each reporting date and potential adjustments will be recognized as a change in accounting estimates prospectively.

25

(iii) Subsequent costs The replacement cost of a component of PP&E is recognized in the carrying value of the item when it is probable that the future economic benefits embodied in the component will flow to the Company and its cost can be reliably measured. The carrying amount of the component that is replaced is written off. Costs of normal maintenance on property, plant and equipment are charged to the income statement as incurred. (h) Intangible assets (i) Recognition and measurement The Company's intangible assets are trademarks and patents, right to use properties and software. The value of patents and trademarks refers to the registration of the Company's brands at the competent national and international entities that are amortized according to the validity of the records. Right to use properties refers to the registration of commercial sites of the own stores that are amortized according to term defined in the contract. The software value refers to third parties software acquired and internally generated that are amortized over the useful life defined. All of them have defined useful lives and are measured at cost, net of accumulated amortization and impairment losses. (ii) Amortization Amortization is calculated over the cost of the asset, or other amount substituted for cost. Amortization is recognized in profit or loss on a straight-line basis over the estimated useful lives of the intangible assets from the date they are available for use, since this is the method that best reflects the consumption pattern of the future economic benefits embodied in the asset. The useful estimated lives are as follows:

Trademarks and patents 10.00 Right to use properties 4.99 Software licenses 8.64

Description

(iii) Subsequent expenditures Subsequent expenditures are capitalized only when they increase the future economic benefits embodied in the specific asset to which they relate. All other expenditures, are recognized in profit or loss as incurred.

26

(i) Impairment (i) Financial assets (including receivables) A financial asset measured at fair value through profit or loss is assessed at each reporting date for objective evidence of impairment. An asset is impaired when there is objective evidence that a loss event has occurred after the initial recognition of the asset, and that such loss event had a negative effect on the estimated future cash flows of that asset that can be reliably estimated. The objective evidence that financial assets are impaired may include default or late payment by a debtor, restructuring of the amount owed to the Company under conditions that would not be considered in other transactions or indications that a debtor or issuer will declare bankruptcy. The company considers evidence of loss of value for loans and receivables. All significant loans and receivables are assessed for impairment. A decrease in the recoverable value of a financial asset measured at amortized cost is calculated as the difference between the asset's carrying amount and the present value of estimated future cash flows discounted at the financial asset's original effective interest rate. The losses are recognized in a provision in the income statement against receivables. Interest on the impaired asset continues to be recognized through the reversion of the discount. When a subsequent event causes the amount of the impairment loss to decrease, the decrease in impairment loss is reversed through profit or loss. (ii) Non-financial assets The carrying values of non-financial assets of the Company are reviewed each period to determine whether there is sign of loss in the recovery value (impairment). If such indication exists, the asset's recoverable amount is determined. The Administration has not identified any information that showed loss of recoverable value of nonfinancial assets. (j) Leasing The Company is the lessor under store lease agreements. The Company reviewed these agreements and classified them as operating lease, since it does not substantially transfer the risks and rewards of the ownership of the leased property to the lessee. Payments are recorded in the income statement linearly over the period of the leasing.

27

(k) Employee benefits (i) Defined benefit plans A defined benefit plan is a post-employment benefit plan other than the defined contribution plan. The Company possess medical aid and private pension plan for its employees (defined benefit plans). For both cases, the actuarial calculations are performed annually by a qualified and independent actuary hired by the Company. The Company's net obligation in respect of defined benefit pension plans is calculated separately for each plan by estimating the amount of the future benefit that employees have earned in return for their service in the current and prior periods; that benefit is discounted to their present value. Any unrecognized prior service costs and the fair values of any plan assets are deducted. The discount rate is the yield of prime debt securities at the reporting date, whose maturity dates approximate the terms and conditions of the Company's obligations and are denominated in the same currency in which the benefits are expected to be settled. In the case of the pension plan, when the calculation results in a benefit for the Company, the asset to be recognized is limited to the total of any unrecognized prior service costs and the present value of the economic benefits available as future plan refunds or reduction in the future payments. In order to calculate the present value of the economic benefits, consideration is given to any minimum funding requirements that apply to any Company plan. An economic benefit is available to the Company when it is realizable over the plan life, or upon settlement of the plan's liabilities. When the benefits of a plan are increased, the portion of the increased benefit relating to past service by employees is recognized as an expense in the income statement on a straight-line basis over the average period until the benefits become vested. To the extent that the benefits vest immediately, the expense is recognized immediately in the income statement. Remeasurements, composed of gains and losses, the effect of the limit of assets (assets ceiling) and the return on plan assets, both excluding net interest, are recognized in the statement of comprehensive income, if at all, in the period in which they occur. Remeasurements are not reclassified to profit or loss in subsequent periods. The Company recognizes all actuarial gains and losses resulting from defined benefit plans in other comprehensive income. (ii) Other long-term benefits to employees The Company’s net obligation in relation to employee benefits other than pension plans and health plans is the amount of the future benefit that employees have earned in return for their service in the current and prior years. That benefit is discounted to calculate its present value, and the fair value of any related assets is deducted. The calculation is performed on the projected unit credit method. Any actuarial gains and losses are recognized in the income (loss) in the period they occur. (iii) Short-term benefits to employees Obligations for short-term employee benefits are measured on a non-discounted basis and incurred as expenses as the related service is rendered. The liability is recognized at the amount expected to be paid under the cash bonus plans or short-term profit sharing if the Company has a legal or constructive obligation to pay this amount as a result of prior service rendered by the employee, and the obligation can be reliably estimated.

28

(iv) Share-based transactions The effects of the share based plan are calculated based on the fair value and recognized in the balance sheet and statement of income at the extent the contractual conditions are met. (l) Provisions A provision is recorded when the Company has a legal or constructive obligation as a result of a past event, which can be reliably estimated, and it is probable that an outflow of funds will be required to settle the obligation. If the effect of the amount over time is significant, provisions are calculated by discounting the expected future cash flows at a pre-tax rate which reflects the current market evaluations as to the value of the cash over time and the specific risks of the liability. (m) Adjustment to present value Fixed purchase and sale transactions in installments were brought to present value on transactions date, based on deadlines and at the rate of 0.66% p.m. and 0.85% p.m., respectively. These rates represent SELIC rate for the period in purchase transactions and discount rate in early payment of sale transactions. No assumptions were made that took into account credit risk factors or other risks, because the Company uses a simplified model and because of the operations’ characteristics. The average days sales outstanding is 77 days and the average days payable outstanding is 46 days. The “Prodec III” tax incentive, subject to annual interest of 4%, was adjusted to present value at the Company’s average borrowing rate. The adjustment to present value of purchases is recorded to trade payables and charged to financial income/loss, over the duration of the term in the case of trade payables. The adjustment to present value of credit sales is charged to trade receivables and the realization thereof is recorded under financial income/loss over the duration of the term. The adjustment to present value of tax incentive obligations and non-current taxes payable and the contra entry thereof are recorded under financial income/loss. (n) Capital Common shares are classified as shareholders' equity. Additional costs directly attributable to the issue of shares and share options are recognized as a deduction from shareholders' equity, net of any tax effects. The minimum mandatory dividends, as established in the by-laws, are recognized as liabilities when approved by the General Assembly. (i) Treasury Shares The Company's own equity instruments that are repurchased (treasury shares) are recorded at cost, as a reduction of equity. No gain or loss is recognized in the statement of income on the purchase, sale, issue or cancellation of the Company's own equity instruments.

29