city of sebastian, floridapublic.cityofsebastian.org/pdfs/02finstmts.pdf · the city of sebastian...

TRANSCRIPT

i

CITY OF SEBASTIAN, FLORIDA

Comprehensive Annual Financial Report For the Year Ended September 30, 2002

CITY COUNCIL

Walter W. Barnes ...............................Mayor James A. Hill .......................................Vice-Mayor Joe Barczyk .........................................Councilmember Edward J. Majcher, Jr. ......................Councilmember Ray Coniglio ........................................Councilmember

Prepared By: Mark C. Mason, CPA Director of Finance

THIS PAGE INTENTIONALLY LEFT BLANK

ii

iii

INTRODUCTORY SECTION

This section contains the following subsections:

Table of Contents

Letter of Transmittal

Certificate of Achievement for Excellence in Financial Reporting for the Fiscal Year Ended September 30, 2001

Organizational Chart

List of Officials

iv

CITY OF SEBASTIAN, FLORIDA

COMPREHENSIVE ANNUAL FINANCIAL REPORT SEPTEMBER 30, 2002

TABLE OF CONTENTS

INTRODUCTORY SECTION Page

Title Page....................................................................................................................................................... i Table of Contents........................................................................................................................................... iv Letter of Transmittal ...................................................................................................................................... vii Certificate of Achievement for Excellence in Financial Reporting ............................................................... x Organizational Chart...................................................................................................................................... xi List of Officials.............................................................................................................................................. xii

FINANCIAL SECTION Independent Auditor’s Report ....................................................................................................................... 3

Management’s Discussion and Analysis ....................................................................................................... 5

Basic Financial Statements – Overview

Government-wide Financial Statements:

Statement of Net Assets.......................................................................................................................... 13

Statement of Activities ........................................................................................................................... 14

Fund Financial Statements:

Balance Sheet – Governmental Funds.................................................................................................... 15

Statement of Revenues, Expenditures, and Changes in Fund Balances – Governmental Funds........................................................................................................................... 16

Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities ....................................................................... 17

Statement of Net Assets – Proprietary Funds ......................................................................................... 18

Statement of Revenues, Expenses, and Changes in Fund Net Assets – Proprietary Funds .................... 19

Statement of Cash Flows – Proprietary Funds ...................................................................................... 20

Statement of Fiduciary Net Assets – Fiduciary Funds............................................................................ 22

Statement of Changes in Fiduciary Net Assets – Fiduciary Fund – Pension Trust ................................ 23

Notes to Financial Statements................................................................................................................... 24

Required Supplementary Information:

Schedule of Revenues, Expenditures, and Changes in Fund Balances – Budget and Actual – General Fund............................................................................................................................ 39

Schedule of Revenues, Expenditures, and Changes in Fund Balances – Budget and Actual – Discretionary Sales Tax Special Revenue Fund ...................................................................... 40

Notes to the Required Supplementary Information – Budget Comparisons .............................................. 41

Police Officers’ Pension Plan – Schedule of Contributions from the Employer and other Contributing Entities .............................................................................................................................. 42

Combining and Individual Nonmajor Financial Fund Statements and Budget to Actual Schedules

Combining Balance Sheet – Nonmajor Governmental Funds ....................................................................... 46

Combining Statement of Revenues, Expenditures, and Changes in Fund Balances – Nonmajor Governmental Funds .................................................................................................................................. 48

Schedule of Revenues, Expenditures, and Changes in Fund Balances – Budget and Actual – Local Option Gas Tax Special Revenue Fund............................................................................. 50

Schedule of Revenues, Expenditures, and Changes in Fund Balances – Budget and Actual – Riverfront Redevelopment Special Revenue Fund...................................................................... 51

Schedule of Revenues, Expenditures, and Changes in Fund Balances – Budget and Actual – Recreation Impact Fee Special Revenue Fund ............................................................................ 52

v

PageSchedule of Revenues, Expenditures, and Changes in Fund Balances – Budget and Actual – Stormwater Utility Special Revenue Fund .................................................................................. 52

Schedule of Revenues, Expenditures, and Changes in Fund Balances – Budget and Actual – Law Enforcement Forfeiture Special Revenue Fund................................................................... 53

Schedule of Revenues, Expenditures, and Changes in Fund Balances – Budget and Actual – G.R.E.A.T. Program Special Revenue Fund ............................................................................... 53

Schedule of Revenues, Expenditures, and Changes in Fund Balances – Budget and Actual – Debt Service Fund ....................................................................................................................... 54

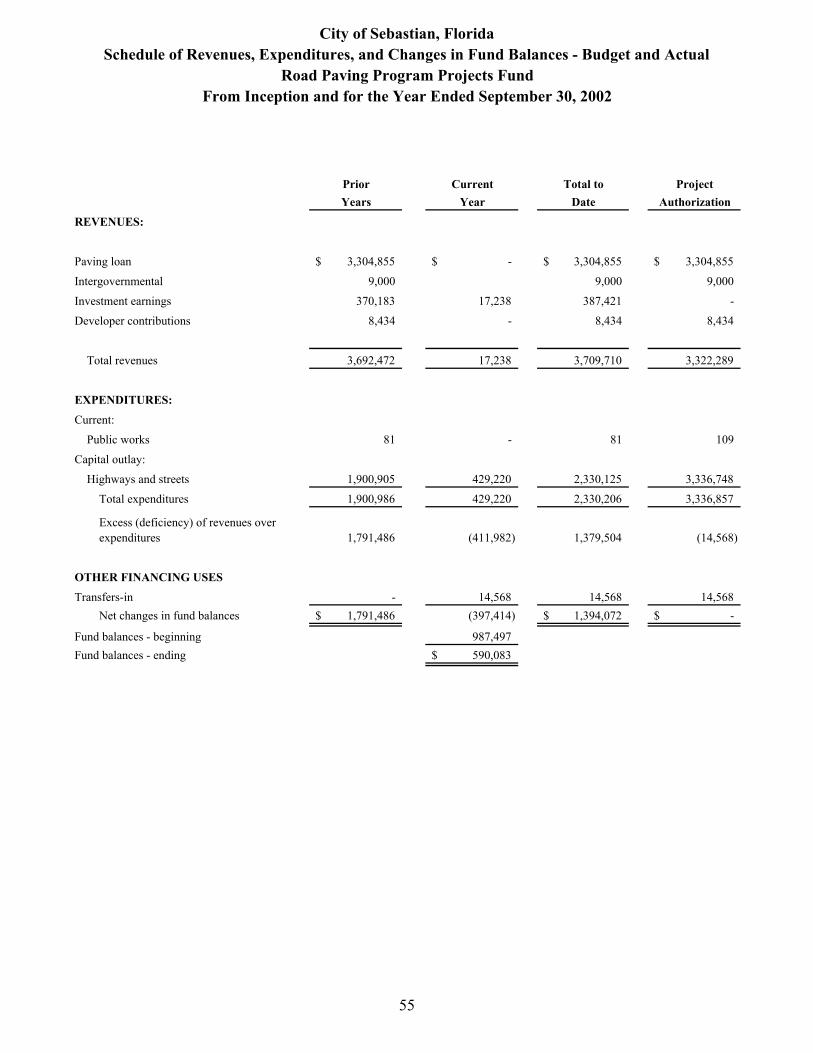

Schedule of Revenues, Expenditures, and Changes in Fund Balances – Budget and Actual – Road Paving Program Projects Fund........................................................................................... 55

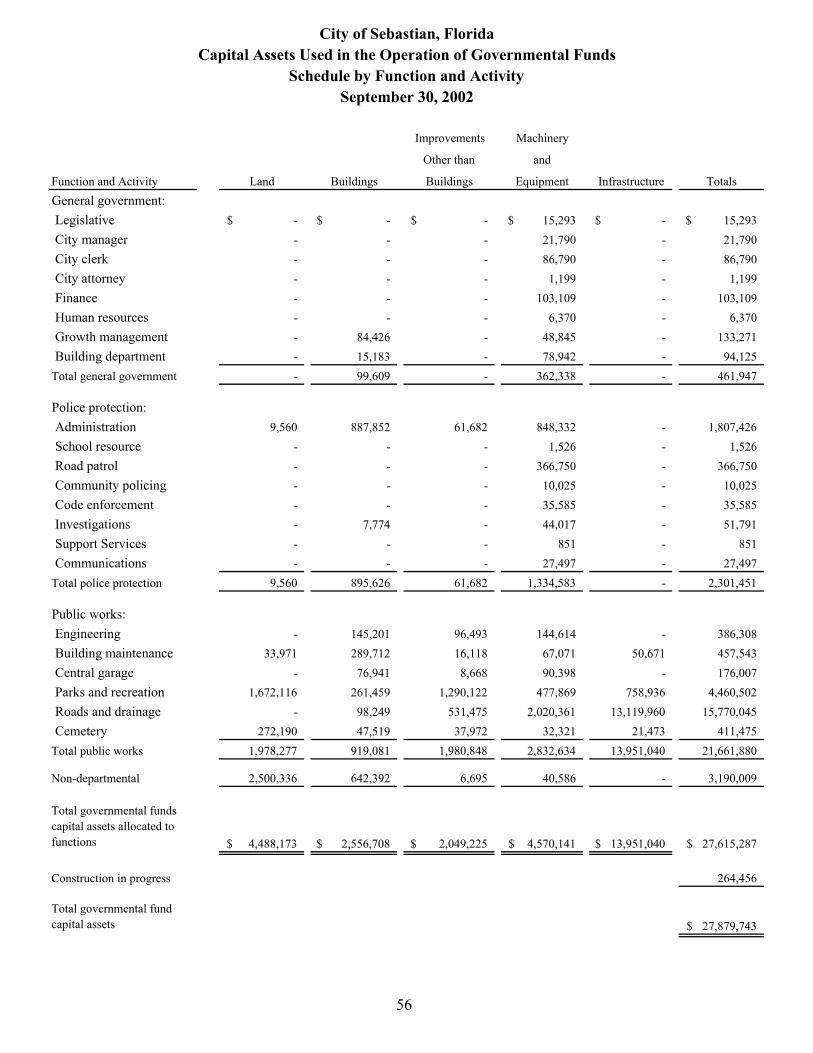

Capital Assets Used in the Operations of Governmental Funds – Schedule by Function and Activity......... 56

STATISTICAL SECTION (Unaudited) Table

General Governmental Expenditures & Other Financing Uses by Function – Last Ten Fiscal Years............................................................................................................ 1 58

General Governmental Revenues & Other Financing Sources – Last Ten Fiscal Years........................................................................................................................... 2 60

Property Tax Levies and Collections – Last Ten Fiscal Years ................................................. 3 62

Assessed and Estimated Actual Value of Property – Last Ten Fiscal Years ............................ 4 64

Principal Taxpayers .................................................................................................................. 5 66

Property Tax Rates – Direct and Overlapping Governments – Last Ten Fiscal Years............. 6 67

Special Assessments Billing and Collections – Last Ten Fiscal Years..................................... 7 68

Computation of Legal Debt Margin.......................................................................................... 8 69

Ratio of Net General Obligation Bonded Debt to Assessed Value and Net General Obligation Bonded Debt Per Capita ........................................................................ 9 70

Ratio of Annual Debt Service Expenditures for General Obligation Bonded Debt To Total General Government Expenditures ........................................................................ 10 70

Computation of Direct and Overlapping Bonded Debt – General Obligation Bonds............... 11 71

Revenue Bond Coverage – Golf Course Bond – Last Ten Fiscal Years................................... 12 72

Demographic Statistics – Last Ten Fiscal Years ...................................................................... 13 73

Property Value, Construction and Bank Deposits – Last Ten Fiscal Years.............................. 14 74

Miscellaneous Statistics............................................................................................................ 15 76

SINGLE AUDIT SECTION

Independent Auditor’s Report on Compliance and on Internal Control Over Financial Reporting Based on an Audit of Financial Statements Performed in Accordance with Governmental Auditing Standards............................................................................................................. 79

Independent Auditor’s Report on Compliance and Internal Control over Compliance Applicable to Each Major State Project ..................................................................................................... 81

Schedule of Findings and Questioned Costs – State Projects ........................................................................ 83

Schedule of Expenditures of State Financial Assistance ............................................................................... 86

Independent Auditor’s Management Letter ................................................................................................... 87

THIS PAGE INTENTIONALLY LEFT BLANK

vi

viii

REPORTING ENTITY

The City of Sebastian is located on the central east coast of Florida, “the Treasure Coast”, in Indian River County. The City is a Florida municipal corporation with a five-member City Council comprised of five council members with a Mayor selected from the five members. The City operates under a Council-City Manager form of government. The Director of Finance reports to the City Manager and they are responsible for the administration of City finances. The City provides a wide range of services including general government administration, police protection, public works, a golf course, and a general aviation airport.

This report includes all funds of the City. In evaluating the City as a reporting entity, we have included all component units for which the City Council is financially accountable.

The component units have been blended with the financial statements presented for the Primary Government because the component unit’s governing body is the same as the City Council or because the component unit exclusively serves the City. The blended component units are the Riverfront Redevelopment Agency and the Sebastian Police Officer’s Pension Trust Fund.

FACTORS AFFECTING FINANCIAL CONDITIONS

The information presented in the financial statements is perhaps best understood when it is considered from the broader perspective of the specific environment within which the City of Sebastian operates.

Local Economy

The City of Sebastian currently enjoys a favorable economic environment and local indicators (building permits, both commercial and residential) suggest continued stability. The region, though agricultural in nature, also enjoys light industrial as well as a strong retail base which draws numerous visitors from around the area.

The region (which includes the City of Sebastian and the surrounding unincorporated area with the same county) has a fluctuating labor force depending on agricultural demand and a strong retirement community. Although the labor force fluctuates, unemployment in the region has been between 6.8% and 9.8% over the past several years.

Long-term Financial Planning

The voters of Indian River County in November 2003, extended the Infrastructure Sales Surtax in the amount of $.01 per $1.00 sale for an additional fifteen years and seven months beginning in January 2004. This Infrastructure Sales Surtax is estimated to provide the City in excess of $40 million dollars over the life of the extension.

U.S. Highway 1, which includes a substantial portion of the business district of the City of Sebastian, underwent major renovations over the past year. This should have a considerable impact on tourism and commercial opportunities. In addition, over the past year, three new commercial centers and doctor’s offices have been built along this major artery in the City.

FINANCIAL INFORMATION

Internal Accounting Controls

In developing and evaluating the City’s accounting system, consideration is given to the adequacy of internal accounting controls. Internal accounting controls are designed to provide reasonable, but not absolute, assurances regarding: (1) the safeguarding of assets against loss from unauthorized use or disposition; and (2) the reliability of financial records for preparing financial statements and maintaining accountability for assets. The concept of reasonable assurance recognizes that: (1) the cost of a control should not exceed the benefits likely to be derived, and (2) the evaluation of costs and benefits requires estimates and judgements of management.

All internal control evaluations occur within this framework. We believe that the City’s internal accounting controls adequately safeguard assets and provide reasonable assurance of proper recording of financial transactions.

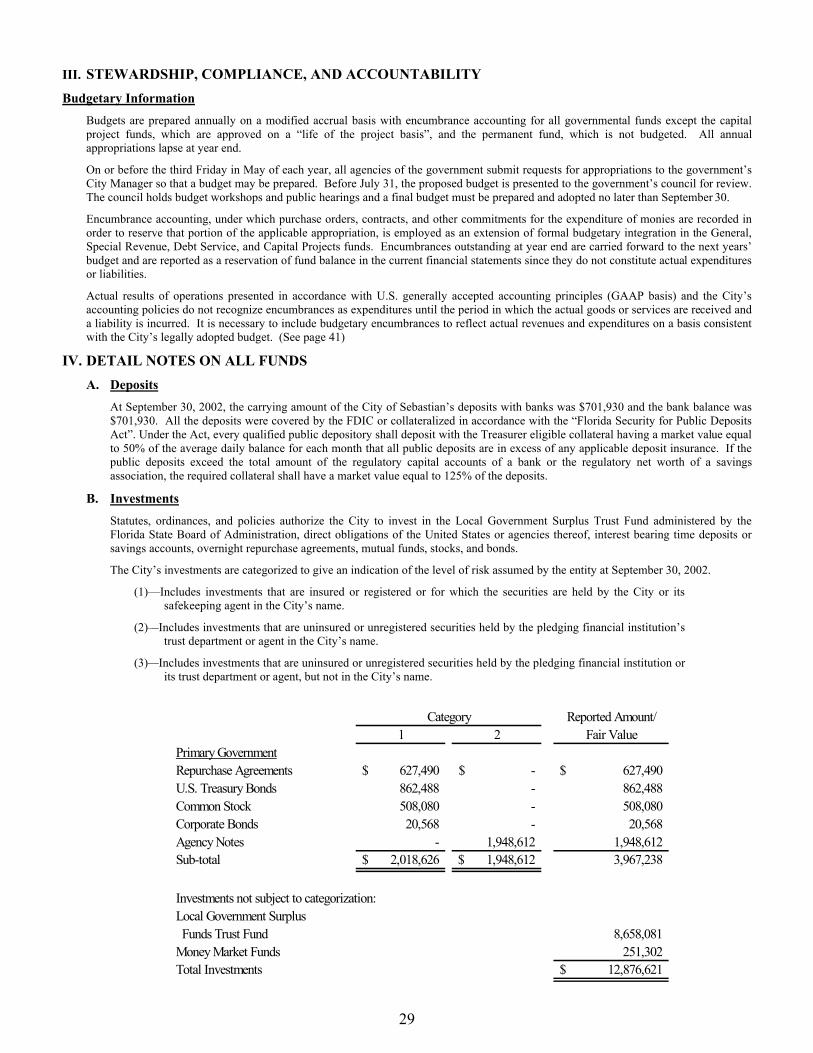

Budgetary Control

Budgetary control is maintained at the budget account level by the encumbrance of estimated purchase amounts prior to the release of purchase orders to vendors. Open encumbrances are reported as reservations of fund balances as of September 30, 2002. Appropriations are approved on an annual basis and are subject to regular

ix

review by City Management and a quarterly review by the City Council. Monthly budget reports are submitted to senior administrative officials and are available to the City Council.

Cash Management

Cash temporarily idle during the year was invested in repurchase agreements and other obligations with maturities less than one year. Funds were invested with the State Board of Administration which pools funds from local governmental units and with local banks which are considered Qualified Public Depositories as described in the Florida Security for Public Deposits Act. In addition, the City maintains a zero balance disbursement account system whereby excess funds are cleared from the account at the end of each banking day and automatically invested in an overnight repurchase agreement.

Risk Management

All risk management activities are recorded in each particular fund, including general property liability insurance premiums and related costs and workers compensation. The City administers both policies under the direction of the Finance and Human Resources departments, respectively. In addition, the City has a Safety Committee that reviews all worker compensation accidents and provides recommendations for corrective action.

Retirement Commitments

Police Officers’ Pension Plan – There were 34 active and retired members in the Police Officers’ Pension Plan as of September 30, 2002. This pension plan is a single employer, defined benefit plan and is administered by a Board of Trustees. The actuarially determined funding requirements are based upon the market value of the pension plan’s investment portfolios. The City’s policy of funding to meet the actuarially determined requirements was met for 2002. Contributions to the pension plan totaled $153,211, which includes $8,620 from the City, $61,714 from employees, and $82,877 from the State of Florida.

REPORTING ACHIEVEMENT

The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to the City of Sebastian for its comprehensive annual financial report for the fiscal year ended September 30, 2001. The Certificate of Achievement is a prestigious national award recognizing conformance with the highest standards for preparation of state and local government financial reports. In order to be awarded a Certificate of Achievement, a government must publish an easily readable and efficiently organized comprehensive annual financial report. This report must satisfy both U.S. generally accepted accounting principles and applicable legal requirements.

A Certificate of Achievement is valid for a period of one year only. We believe that our current comprehensive annual financial report continues to meet the Certificate of Achievement Program’s requirements and we are submitting it to the GFOA to determine its eligibility for another certificate.

ACKNOWLEDGEMENTS

The preparation of this report would not be possible without the dedicated service of the Finance department staff. Their efforts toward improving the accounting and financial reporting systems has led to the improved quality of information reported to the City Council, State and federal agencies and the citizens of the City of Sebastian. We sincerely appreciate their contributions.

Respectfully submitted,

Mark C. Mason, CPA Director of Finance

Terrence R. Moore City Manager

x

CITY OF SEBASTIANORGANIZATIONAL CHART

xi

CITY

MANAGER

GROWTH MANAGEMENT

BUILDING DEPARTMENT

POLICE FINANCE

HUMAN RESOURCES

GOLF COURSE

AIRPORT

BOARDS &

COMMISSIONS

ADMINISTRATION

UNIFORM

DETECTIVE

DISPATCH

PUBLIC WORKS

CITIZENS OF SEBASTIAN

CITY COUNCIL

CITY

ATTORNEYCITY

CLERK

ENGINEERING

CODE

ENFORCEMENT

SUPPORT

SERVICES

COMMUNITY

POLICING

SCHOOL RESOURCEBUILDING

MAINTENANCE

PARKS &

RECREATION

CEMETERY

ROADS & DRAINAGE

GENERAL SERVICES

ADMINISTRATION

CENTRAL GARAGE

xii

CITY OF SEBASTIAN, FLORIDA

CITY OFFICIALS

City Manager TERRENCE R. MOORE

City Clerk SALLY A. MAIO, CMC

City Attorney RICH STRINGER

DEPARTMENT HEADS:

Director of Finance MARK C. MASON, CPA

City Engineer DAVID FISHER, P.E.

Police Chief JAMES DAVIS

Public Works Director TERRY HILL

Growth Management Director TRACY HASS

Building Director GEORGE BONACCI

Human Resources Director JAMES SEXTON

Golf Course Manager GREG GARDNER

Airport Manager JASON MILEWSKI

1

FINANCIAL SECTION

This section contains the following subsections:

Independent Auditor’s Report

Management’s Discussion and Analysis

Government-wide Financial Statements

Fund Financial Statements

Notes to Financial Statements

Required Supplementary Information

Combined and Individual Fund Statements and Schedules

THIS PAGE INTENTIONALLY LEFT BLANK

2

5

MANAGEMENT’S DISCUSSION AND ANALYSIS

The City of Sebastian’s (the “City”) discussion and analysis is designed to (a) assist the reader in focusing on significant financial issues, (b) provide an overview of the City’s financial activity, (c) identify changes in the City’s financial position, (d) identify any material deviations from the financial plan, and (e) identify individual fund issues or concerns.

Since the Management’s Discussion and Analysis (MD&A) is designed to focus on the current years activities, resulting changes and currently known facts, please read it in conjunction with the Transmittal Letter (beginning on page vii) and the City’s financial statements (beginning on page 13).

HIGHLIGHTS

Financial Highlights

The City’s Net Assets increased by $3,096,106 primarily as a result of completing and capitalizing $2,210,367 in capital improvement projects, purchases of capital equipment of $400,199 and the implementation of the Recreation Impact Fee and Stormwater Utility Fee which contributed $1,044,138 in additional revenue for capital improvements. The total cost of all the City’s programs was $10,673,279, an increase of $1,561,842 or 17.1%. During the year, the City’s governmental-type activities revenues increased $1,756,001 or 17.3% and expenses increased 1,539,443 or 20.6%, over the previous year. The City’s business-type activities revenue increased by $37,503 or 2.1% and expenses increased by $22,399 or 1.4%. The City completed $556,015 in land purchases, representing 11.5 acres, for recreation. The City completed $704,306 in road reconstruction and repaving.

USING THIS ANNUAL REPORT

The annual report consists of a series of financial statements. The Statement of Net Assets and the Statement of Activities (on pages 13 and 14) provide information about the activities of the City as a whole and present a longer-term view of the City’s finances. Fund financial statements begin on page 15. For governmental activities, these statements tell how these services were financed in the short term as well as what remains for future spending. Fund financial statements also report the City’s operations in more detail by providing information about the City’s most significant funds. The remaining statements provide financial information about activities for which the City acts solely as a trustee or agent for the benefit of those outside of the government.

Reporting the City as a Whole

Our analysis of the City as a whole begins on page 13. One of the most important questions asked about the City’s finances is, “Is the City as a whole better off or worse off as a result of the year’s activities?” The Statement of Net Assets and the Statement of Activities report information about the City as a whole and about its activities in a way that helps answer this question. These statements include all assets and liabilities using the accrual basis of accounting, which is similar to the accounting used in most private-sector companies. All of the current year’s revenues and expenses are taken into account regardless of when cash is received or paid.

These two statements report the City’s net assets and changes in them. You can think of the City’s net assets – the difference between assets and liabilities – as one way to measure the City’s financial health, or financial position. Over time, increases or decreases in the City’s net assets, is one indicator of whether its financial

6

health is improving or deteriorating. You will need to consider other nonfinancial factors, however, such as changes in the City’s property tax base and the condition of the City’s roads, to assess the overall health of the City.

In the Statement of Net Assets and the Statement of Activities, we divide the City into two kinds of activities: Governmental activities – Most of the City’s basic services are reported here, including the police, public works and parks departments, and general administration. Property taxes, franchise fees, and state shared revenue finance most of these activities.

Business-type activities – The City charges a fee to customers to help it cover all or most of the cost of certain services it provides. The City’s Golf Course and Airport are reported here.

Reporting the City’s Most Significant Funds

Our analysis of the City’s major funds begins on page 15. The fund financial statements provide detailed information about the most significant funds – not the City as a whole. Some funds are required to be established by State law and by bond covenants. However, the City Council establishes many other funds to help it control and manage money for particular purposes (like the road paving program) or to show that it is meeting legal responsibilities for using certain taxes, grants, and other money (like the local option gas tax and infrastructure sales surtax (a.k.a. Discretionary Sales Tax)). The City’s two kinds of funds – governmental and proprietary – use different accounting approaches.

Governmental funds – Most of the City’s basic services are reported in governmental funds, which focus on how money flows into and out of those funds and the balances left at year-end that are available for spending. These funds are reported using an accounting method called modified accrual accounting, which measures cash and all other financial assets that can readily be converted to cash. The governmental fund statements provide a detailed short-term view of the City’s general government operations and the basic services it provides. Governmental fund information helps you determine whether there are more or fewer financial resources that can be spent in the near future to finance the City’s programs. We describe the relationship (or differences) between governmental activities (reported in the Statement of Net Assets and the Statement of Activities) and governmental funds in reconciliations at the bottom of the fund financial statements.

Proprietary funds – When the City charges customers for the services it provides – whether to outside customers or to other units of the City – these services are generally reported in proprietary funds. Proprietary funds are reported in the same way that all activities are reported in the Statement of Net Assets and the Statement of Activities. In fact, the City’s enterprise funds (a component of proprietary funds) are the same as the business-type activities we report in the government-wide statements but provide more detail and additional information, such as cash flows, for proprietary funds.

The City as Trustee

The City is the trustee, or fiduciary, for the Police Officers’ Pension Plan. The City’s fiduciary activities are reported in separate Statements of Fiduciary Net Assets and Changes in Fiduciary Net Assets on page 22 and 23. We exclude these activities from the City’s other financial statements because the City cannot use these assets to finance its operations. The City is responsible for ensuring that the assets reported in these funds are used for their intended purposes.

The City holds deposits for various individuals and businesses for contract performance that are then returned when the contract has been completed. These deposits are accounted for in an Agency fund, where assets equal liabilities.

7

THE CITY AS A WHOLE

Financial Analysis of the City as a Whole

The City’s combined net assets increased $3.1 million from $22.2 million to $25.3 million or 13.9%. Looking at the net assets and net revenues of the governmental and business-type activities, the largest increase occurred in the governmental-type activities. Our analysis focuses on net assets (Table 1) and changes in net assets (Table 2) of the City’s governmental and business-type activities.

GOVERNMENT-WIDE STATEMENTS

Statement of Net Assets

The following table reflects the condensed Statements of Net Assets:

For more detail information see the Statement of Net Assets on page 13.

Net assets of the governmental-type activities increased $2.9 million or 14.3%. Unrestricted net assets-the part of net assets that can be used to finance day-to-day operations without constraints established by debt covenants, enabling legislation, or legal requirements-increased from $5.4 million to $5.9 million or $500,000, while restricted net assets increased $1.0 million from $2.3 million to $3.3 million. Investment in capital assets, net of related debt increased from $12.8 to $14.2 million or $1.6 million.

Unrestricted net assets increased as a result of communication services taxes exceeding anticipated amounts and an increase in building permit fees exceeding anticipated amounts due to an increase in building activity resulting from a decrease in interest rates. Restricted net assets increased from the implementation and receipt of net revenue in excess of expenditures from the Stormwater Utility Fee ($720,814) and the Recreation Impact Fee ($258,455).

Net assets of the City’s business-type activities increased by 9.3% ($1.942 million compared to $1.778 million) in fiscal year 2002. The increase results from capital contributions from the Florida Department of Transportation-Aviation Section for capital improvements at the City’s general aviation airport of $264,772, however, net assets at the golf course decreased $7,127.

2002 2001 2002 2001 2002 2001

Current and other assets 10,157$ 8,400$ 1,827$ 2,152$ 11,984$ 10,552$

Capital assets 17,743 16,620 2,527 2,393 20,270 19,013

Total assets 27,900$ 25,020$ 4,354$ 4,545$ 32,254$ 29,565$

Non-current liabilities 4,043$ 4,251$ 2,278$ 2,371$ 6,321$ 6,622$

Other liabilities 459 303 134 396 593 699

Total liabilities 4,502$ 4,554$ 2,412$ 2,767$ 6,914$ 7,321$

Net assets:

Invested in capital assets,

net of related debt 14,243$ 12,778$ 364$ 151$ 14,607$ 12,929$

Restricted 3,290 2,270 458 641 3,748 2,911

Unrestricted 5,865 5,418 1,120 986 6,985 6,404

Total net assets 23,398$ 20,466$ 1,942$ 1,778$ 25,340$ 22,244$

Governmental Activities Business-type Activities Total Primary Government

Table 1

Statements of Net Assets

as of September 30, 2002 and 2001

(in thousands)

8

The following chart shows the revenue and expenses of the total primary government.

The City’s total revenues increased by 15.0% ($1.794 million). The total cost of all programs increased by 17.1% ($1.562 million) with two new programs added this year. Even with this increase in expenses, the City was still able to cover its costs. Our analysis below separately considers the operations of governmental and business-type activities.

Governmental Activities

The cost of all governmental activities this year was $9.0 million compared to $7.5 million last year. However, as shown in the Statement of Activities on page 14, the amount the City’s taxpayers ultimately financed for these activities through City taxes was only $4.4 million because some of the cost was paid by those who directly benefited from the programs ($1.7 million) or by other governments and organizations that subsidized certain programs with grants and contributions ($3.7 million). Overall the City’s governmental program revenues increased in fiscal year 2002 from $4.1 million to $5.4 million, principally based upon the implementation of the Recreation Impact and Stormwater Utility Fees, which amounted to $258,455 and $785,683, respectively. The City paid for the remaining “public benefit” portion of governmental activities with $4.4 million in taxes and with other revenues, such as interest and general entitlements.

2002 2001 2002 2001 2002 2001

REVENUES

Program revenues:

Charges for services 1,682$ 792$ 1,545$ 1,282$ 3,227$ 2,074$

Operating grants and contributions 958 902 51 124 1,009 1,026

Capital grants and contributions 2,734 2,444 214 299 2,948 2,743

General revenues:

Property taxes 2,616 2,557 - - 2,616 2,557

Other taxes 1,750 1,905 - - 1,750 1,905

Intergovernmental 2,069 1,336 - - 2,069 1,336

Other 119 236 32 99 151 335

Total revenues 11,928 10,172 1,842 1,804 13,770 11,976

EXPENSES

General government 2,010 1,676 - - 2,010 1,676

Public safety 2,946 2,527 - - 2,946 2,527

Public works 2,767 2,082 - - 2,767 2,082

Housing and community development 223 242 - - 223 242

Culture and recreation 777 674 - - 777 674

Cemetery 104 95 - - 104 95

Golf Course - - 1,393 1,341 1,393 1,341

Airport - - 284 314 284 314

Interest on long-term debt 169 161 - - 169 161

Total expenses 8,996 7,457 1,677 1,655 10,673 9,112Change in net assets 2,932$ 2,715$ 165$ 149$ 3,097$ 2,864$

Ending net assets 23,398$ 20,466$ 1,942$ 1,778$ 25,340$ 22,244$

Activities Activities Government

Governmental Business-type Total Primary

Table 2

Changes in Net Assets

For the Fiscal Years Ended September 30, 2002 and 2001

(in thousands)

9

On the next page is a graphic illustration of the comparison for governmental activities revenue and expenses.

Business-type Activities

Revenues of the City’s business-type activities (see Table 2) increased by 2.1% ($1.842 million in fiscal year 2002 compared to $1.804 million in fiscal year 2001) and expenses rose 1.3%. The factors driving the results are:

The City golf course, benefiting from a full year’s operation (course was closed for four months in fiscal year 2001 for renovations) increased its revenues by 19% and expenses rose 12.3%, to $1.4 million. Higher costs due to an increase in debt service interest and personal services costs drove the increase. The City general aviation airport enjoys a continued interest by the Florida Department of Transportation-Aviation Section to upgrade the airport facilities as evidenced by repeated support via grant funding. Although revenues decreased by 11.8%, expenses decreased a corresponding amount, 9.6%, both decreases due to the completion and adoption of the Airport Master Plan, resulting in a net increase in assets.

Following is a graphic comparison of the City’s business-type activities.

Governmental Activities for 2002 and 2001

-

500

1,000

1,500

2,000

2,500

3,000

3,500

Charges for services

Operating grants

Captital grants

Propertytaxes

Other taxes

Intergovernmental

Other revenue

General government

Publicsafety

Publicworks

Housing and community

development

Culture

and recreation

Cemetery

Interest on long-term

debt

Revenue/Expense types

Am

ou

nt

2002 2001

Business-Type Activities Comparison

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Charges for services

Operating gran

ts

Captital grants

Otherrevenue

Golf Course expenses

Airport e

xpenses

Revenue/Expense types

Am

ou

nt

2002 2001

10

THE CITY’S FUNDS

As the City completed the year, its governmental funds (as presented in the balance sheet on page 15) reported a combined fund balance of $9.6 million, which is an increase of $1.6 million over the prior year of $8.0 million. The primary reason for the overall increase is the addition of two new programs, the Recreation Impact Fee and the Stormwater Utility Fee. In addition, the general fund received $446,237 in excess of anticipated revenue primarily due to the Communications Services Tax implemented by the State of Florida in the current fiscal year.

General Fund Budgetary Highlights

Over the course of the year, the City Council revised the City budget three times. These budget amendments fall into three categories. The first category includes amendments and supplemental appropriations that were approved shortly after the beginning of the year and reflect the actual beginning balances (versus the amounts originally estimated in July 2001). The second category includes the changes that the Council made during the year to take into account the City’s staff restructuring efforts. The principal amendment was to provide for a larger distribution from the Communications Services Tax than originally calculated of $197,106. The Communications Services Tax was implemented by the State of Florida in an effort to combine several disparate communications franchise and utility tax rates throughout the State into one common rate for all. As a result, the revenue received from the State exceeded original estimates based upon rates used for the various fees in the prior year.

Even with these adjustments, the actual charges to appropriations (expenditures) were $224,109 below the final budgeted amount.

The City’s General fund balance of $3,922,747 reported on page 15 differs from the General fund’s budgetary balance of $3,055,620 reported in the budgetary comparison schedule on page 39. This is principally due to the fact that the budgetary fund balance excludes $197,131 of encumbrances reported as expenditures for budgetary purposes, as well as $669,996 of excess revenues over expenses exceeding the amended budget.

CAPITAL ASSET AND DEBT ADMINISTRATION

Capital Assets

At the end of 2002 the City had $32,001,428 invested in a broad range of capital assets, including land, police and public works equipment, buildings, park facilities, roads, bridges, and stormwater drainage structures. This amount represents a net increase (including additions and deductions) of $1,745,555, or 5.8%, over last year. The following table illustrates the changes in capital assets. See page 30 in the notes to the financial statements for detailed changes in capital assets.

2002 2001 2002 2001 2002 2001

Land 4,488,173$ 3,748,585$ 9,060$ 9,060$ 4,497,233$ 3,757,645$

Buildings 2,556,708 2,310,816 333,189 344,114 2,889,897 2,654,930

Improvements 2,049,225 2,367,192 574,109 540,990 2,623,334 2,908,182

Equipment 4,570,141 4,384,245 486,016 450,633 5,056,157 4,834,878

Infrastructure 13,951,040 13,288,248 2,371,821 2,372,976 16,322,861 15,661,224

Construction-in

Process 264,456 356,079 347,490 82,935 611,946 439,014

Totals 27,879,743$ 26,455,165$ 4,121,685$ 3,800,708$ 32,001,428$ 30,255,873$

Table 3

Totals

G overnmental

Activities

B usiness-type

Activities

11

The City’s fiscal year 2003 capital budget calls for another $4,841,868 in capital projects, principally for the completion of airport improvements of $2,855,000, funded primarily by State and Federal Grants, and road improvements of $762,000 funded by discretionary sales tax and local option gas tax revenue sources.

Debt

At September 30, 2002, the City had $5,791,998 in bonds, notes and capital leases outstanding versus $6,229,027 at September 30, 2001 – a decrease of 7.0% – as shown in the following table:

The decrease in debt is solely attributable to principal payments. The City did not issue any new debt in fiscal year 2002. See note IV.H. on pages 34 and 35 for further information.

The City’s revenue refunding bond carries an AAA rating from Standard & Poor’s, a rating it has held since 1992. All of the City’s other debt, primarily notes and a capital lease, are not rated.

Other obligations of the City include accrued vacation pay and sick leave.

ECONOMIC FACTORS AND NEXT YEAR’S BUDGETS AND RATES

The City’s elected and appointed officials considered many factors when setting the fiscal year 2003 budget, tax rates, and fees that will be charged for the business-type activities. One of those factors is the economy.

Sebastian’s local economy consists largely of retail and service industries. Less than one percent is devoted to industrial activities. Construction of new homes is the largest single business in the area. Some of the largest retail stores include Wal-Mart Stores, Inc. and Winn Dixie Stores, Inc. The Indian River County unemployment rate in 2002 was 9.8% up from 6.8% in the previous year and down from a high of 11.9% in 1992. This indicates that although business growth in the area has improved as evidenced by the construction of several new commercial establishments in the area, the unemployment of farm workers continues to burden the unemployment rate. Continued stability and the increase of annual residential building permits issued provides a trend for steady economic development in the area.

These indicators were taken into account when adopting the General Fund budget for fiscal year 2003. Amounts available for appropriation in the General Fund budget are $9,403,970, an increase of 11.2% over the final fiscal year 2002 budget of $8,130,544. Property taxes (benefiting from a 2002 increase in assessed valuations of 8.63%), public services taxes, and State shared revenue are expected to lead this increase. The City will use these increases in revenues to finance programs we currently offer, implement an active recreation program, as well as, the effect that we expect inflation to have on program costs. Budgeted expenditures, not including transfers out, are expected to rise 9.1%, to $8,759,970 from $8,030,544 in fiscal year 2002. Increased wage and cost-of-living adjustments and health insurance based on agreements reached with the police and general employee’s unions in fiscal year 2002 of roughly $981,320, including an increase of $125,358 in worker’s compensation insurance are the largest increments.

2002 2001 2002 2001 2002 2001

134,299$ 187,901$ -$ -$ 134,299$ 187,901$

2,593,939 2,773,847 - - 2,593,939 2,773,847

788,957 900,000 - - 788,957 900,000

- - 2,274,803 2,367,279 2,274,803 2,367,279

Totals 3,517,195$ 3,861,748$ 2,274,803$ 2,367,279$ 5,791,998$ 6,229,027$

Table 4

Governmental Business-type

Activities Activities Totals

Revenue Note (backed by

local option gas tax)

Capital lease obligation

(backed by City)

Revenue bond (backed by

golf course revenue)

Special assessment debt

12

If these estimates are realized, the City’s budgetary fund balance is expected to increase moderately by the close of fiscal year 2003.

As for the City’s business-type activities, we expect the fiscal year 2003 results will also be moderate based upon current and future initiatives:

The Golf Course results are anticipated to increase slightly as a result of rate increases for play.

The Airport is undergoing a reconstruction and economic development revitalization, as a result of master planning initiatives, primarily funded with Federal Aviation Administration and Florida State grants. In addition, the airport has entered into a lease agreement for T-hangers that is anticipated to increase revenues by 35.2% upon completion of construction. The results of operations, however, are expected to be modest for several years.

CONTACTING THE CITY’S FINANCIAL MANAGEMENT

This financial report is designed to provide our citizens, taxpayers, customers, and investors and creditors with a general overview of the City’s finances and to show the City’s accountability for the money it receives. If you have questions about this report or need additional information, contact the City Finance Department at City of Sebastian, 1225 Main Street, Sebastian, Florida 32958.

Governmental Business-type

Activities Activities Total

ASSETS

Cash and cash equivalents:

Cash in banks 500,680$ 1,250$ 501,930$

Equity in pooled investments 6,720,303 820,500 7,540,803

Receivables 699,272 58,751 758,023

Special assessment receivable 66,048 - 66,048

Inventory 19,220 13,203 32,423

Prepaid expenses 8,927 2,465 11,392

Investments 1,003,750 - 1,003,750

Restricted assets:

Temporarily restricted:

Equity in pooled investments 722,054 819,308 1,541,362

Permanently restricted:

Cash in banks 200,000 - 200,000

Equity in pooled investments 199,225 - 199,225

Deferred charges 17,264 111,175 128,439

Capital assets (net of accumulated depreciation):

Land 4,488,173 9,060 4,497,233

Buildings 1,490,070 82,636 1,572,706

Improvements other than buildings 1,372,607 457,738 1,830,345

Machinery and equipment 2,029,584 175,756 2,205,340

Infrastructure 8,097,873 1,454,775 9,552,648

Construction in progress 264,456 347,490 611,946

Total assets 27,899,506 4,354,107 32,253,613

LIABILITIES

Accounts payable and accrued liabilities 334,328 59,359 393,687

Retainage payable 25,820 - 25,820

Accrued interest payable 34,149 3,549 37,698

Deferred revenues 57,952 71,308 129,260

Deposits 6,340 - 6,340

Noncurrent liabilities:

Due within one year 391,251 223,023 614,274

Due in more than one year 3,651,776 2,054,803 5,706,579

Total liabilities 4,501,616 2,412,042 6,913,658

NET ASSETS

Invested in capital assets, net of related debt 14,242,832 363,827 14,606,659

Restricted for:

Capital projects - 21,919 21,919

Highways and streets 1,654,288 - 1,654,288

Redevelopment 25,540 - 25,540

Recreation 258,455 - 258,455

Stormwater 720,814 - 720,814

Law enforcement 20,764 - 20,764

Debt service 163,870 436,095 599,965

Perpetual care:

Expendable 46,714 - 46,714

Nonexpendable 399,225 - 399,225

Unrestricted 5,865,388 1,120,224 6,985,612

Total net assets 23,397,890$ 1,942,065$ 25,339,955$

The accompanying notes to financial statements are an integral part of this financial statement.

13

City of Sebastian, Florida

Statement of Net Assets

September 30, 2002

Op

erat

ing

Cap

ital

Ch

arge

s fo

rG

ran

ts a

nd

Gra

nts

an

dG

over

nm

enta

lB

usi

nes

s-ty

pe

Fu

nct

ion

/Pro

gram

Exp

ense

sS

ervi

ces

Con

trib

uti

ons

Con

trib

uti

on

sA

ctiv

itie

sA

ctiv

itie

sT

otal

Gov

ernm

enta

l ac

tivi

ties

:

Gen

eral

gov

ernm

ent

2,01

0,28

8$

65

1,69

8$

-$

-$

(1,3

58,5

90)

$

-$

(1,3

58,5

90)

$

Pub

lic

safe

ty2,

945,

701

146,

361

12

3,66

7

35,7

82

(2

,639

,891

)

-

(2

,639

,891

)

Pub

lic

wor

ks2,

766,

797

785,

683

83

4,56

2

2,20

4,35

1

1,

057,

799

-

1,05

7,79

9

Hou

sing

and

com

mun

ity

deve

lopm

ent

223,

207

24

,869

-

-

(198

,338

)

-

(198

,338

)

Cul

ture

and

rec

reat

ion

777,

019

24

,563

-

493,

946

(2

58,5

10)

-

(2

58,5

10)

Cem

eter

y10

4,24

1

48,4

50

-

-

(5

5,79

1)

-

(5

5,79

1)

Inte

rest

on

long

-ter

m d

ebt

168,

749

-

-

-

(1

68,7

49)

-

(1

68,7

49)

Tot

al g

over

nmen

tal

acti

viti

es8,

996,

002

1,68

1,62

4

95

8,22

9

2,73

4,07

9

(3

,622

,070

)

-

(3

,622

,070

)

Bus

ines

s-ty

pe a

ctiv

itie

s:

Gol

f C

ours

e1,

393,

551

1,36

5,02

7

49

0

-

-

(2

8,03

4)

(2

8,03

4)

Air

port

283,

726

17

9,37

3

50,5

97

21

4,1

75

-

160,

419

16

0,41

9

Tot

al b

usin

ess-

type

act

ivit

ies

1,677

,277

1,54

4,40

0

51

,087

214,

175

-

13

2,38

5

132,

385

Tot

al g

over

nmen

t10

,673

,279

$

3,22

6,02

4$

1,

009,

316

$

2,94

8,25

4$

(3

,622

,070

)13

2,38

5(3

,489

,685

)

Gen

eral

Rev

enue

s:

Pro

pert

y ta

xes

2,61

5,93

9

-

2,

615,

939

Pub

lic

util

ity

taxe

s98

3,23

6

-

983,

236

Fra

nchi

se f

ees

766,

901

-

76

6,90

1

Int

ergo

vern

men

tal

2,06

8,75

3

-

2,

068,

753

Unr

estr

icte

d in

vest

men

t ea

rnin

gs11

8,84

0

32,1

22

15

0,96

2

Tot

al g

ener

al r

even

ues

6,55

3,66

9

32

,122

6,58

5,79

1

Cha

nge

in n

et a

sset

s2,

931,

599

164,

507

3,

096,

106

Net

ass

ets

- be

ginn

ing

20,4

66,2

91

1,

777,

558

22,2

43,8

49

Net

ass

ets

- en

ding

23,3

97,8

90$

1,

942,

065

$

25,3

39,9

55$

The

acc

om

pan

yin

g n

otes

to

fina

nci

al s

tate

men

ts a

re a

n in

tegr

al p

art

of t

his

fina

ncia

l st

atem

ent.

14

Ch

ange

s in

Net

Ass

ets

Net

(E

xpen

se)

Rev

enu

e an

d

Cit

y of

Seb

asti

an, F

lori

da

Sta

tem

ent

of A

ctiv

itie

s

For

th

e ye

ar e

nd

ed S

epte

mb

er 3

0, 2

002

Pro

gram

Rev

enu

es

Road Other Total

Discretionary Capital Paving Governmental Governmental

General Sales Tax Improvements Program Funds Funds

ASSETS

Cash and cash equivalents:

Cash in banks 500,680$ -$ -$ -$ -$ 500,680$

Equity in pooled investments 2,315,917 429,770 1,534,787 - 2,439,829 6,720,303

Receivables 224,296 6 11,912 - 333 236,547

Due from other funds 2,294 - - - - 2,294

Due from other governments 186,700 160,903 49,751 - 65,371 462,725

Special assessments receivable - - - - 66,048 66,048

Inventory 19,220 - - - - 19,220

Prepaid items 8,927 - - - - 8,927

Investments 1,003,750 - - - - 1,003,750

Restricted assets:

Cash in banks - - - - 200,000 200,000

Equity in pooled investments - - - 590,083 331,196 921,279

Total assets 4,261,784$ 590,679$ 1,596,450$ 590,083$ 3,102,777$ 10,141,773$

LIABILITIES AND FUND BALANCES

Liabilities:

Accounts payable 274,745$ 92$ 45,967$ -$ 43,751$ 364,555$

Retainage payable - - 4,973 - 20,847 25,820

Due to other funds - - - - 2,294 2,294

Deposits 6,340 - - - - 6,340

Deferred revenues 57,952 - - - 66,048 124,000

Total liabilities 339,037 92 50,940 - 132,940 523,009

Fund balances:

Reserved for:

Encumbrances 197,131 - 289,674 425,518 191,600 1,103,923

Inventory 19,220 - - - - 19,220

Prepaid items 8,927 - - - - 8,927

Donations 6,810 - - - - 6,810

Debt service - - - - 131,971 131,971

Law enforcement - - - - 18,470 18,470

Cemetery care - - - - 445,939 445,939

Unreserved:

Designated for emergencies 350,000 - - - - 350,000

Designated for employee events 8,221 - - - - 8,221

Unreserved, reported in:

General fund 3,332,438 - - - - 3,332,438

Special revenue funds - 590,587 - - 1,217,701 1,808,288

Capital projects funds - - 1,255,836 164,565 964,156 2,384,557

Total fund balances 3,922,747 590,587 1,545,510 590,083 2,969,837 9,618,764

Total liabilities and fund balances 4,261,784$ 590,679$ 1,596,450$ 590,083$ 3,102,777$

17,742,763

(3,963,637)

Net assets of governmental activities 23,397,890$

The accompanying notes to financial statements are an integral part of this financial statement.

City of Sebastian, Florida

Balance Sheet

Governmental Funds

September 30, 2002

15

Capital assets used in governmental funds are not financial resources and therefore are not reported in the funds.

Some liabilities, including compensated absences and notes and capital leases, are not due and payable in the current

period and therefore are not reported in the funds (Note II.A. page 28).

Amounts reported for governmental activities in the statement of net assets (page 13) are different because:

Road Other Total

Discretionary Capital Paving Governmental Governmental

General Sales Tax Improvements Program Funds Funds

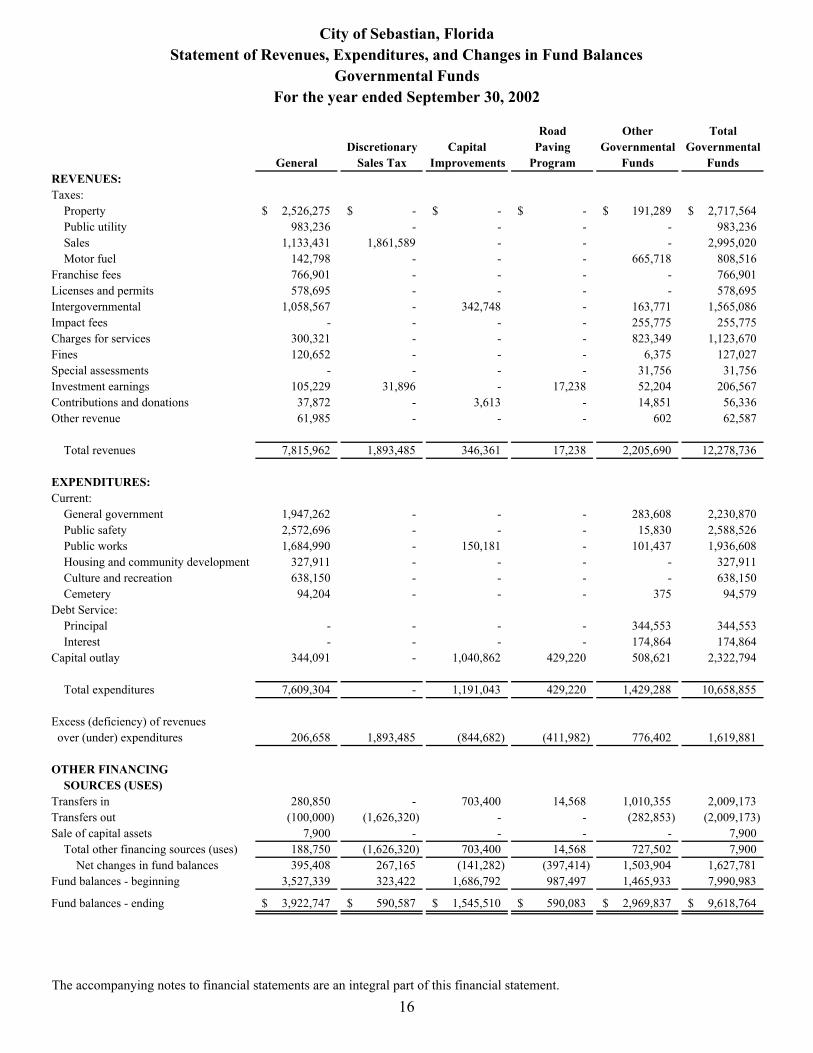

REVENUES:

Taxes:

Property 2,526,275$ -$ -$ -$ 191,289$ 2,717,564$

Public utility 983,236 - - - - 983,236

Sales 1,133,431 1,861,589 - - - 2,995,020

Motor fuel 142,798 - - - 665,718 808,516

Franchise fees 766,901 - - - - 766,901

Licenses and permits 578,695 - - - - 578,695

Intergovernmental 1,058,567 - 342,748 - 163,771 1,565,086

Impact fees - - - - 255,775 255,775

Charges for services 300,321 - - - 823,349 1,123,670

Fines 120,652 - - - 6,375 127,027

Special assessments - - - - 31,756 31,756

Investment earnings 105,229 31,896 - 17,238 52,204 206,567

Contributions and donations 37,872 - 3,613 - 14,851 56,336

Other revenue 61,985 - - - 602 62,587

Total revenues 7,815,962 1,893,485 346,361 17,238 2,205,690 12,278,736

EXPENDITURES:

Current:

General government 1,947,262 - - - 283,608 2,230,870

Public safety 2,572,696 - - - 15,830 2,588,526

Public works 1,684,990 - 150,181 - 101,437 1,936,608

Housing and community development 327,911 - - - - 327,911

Culture and recreation 638,150 - - - - 638,150

Cemetery 94,204 - - - 375 94,579

Debt Service:

Principal - - - - 344,553 344,553

Interest - - - - 174,864 174,864

Capital outlay 344,091 - 1,040,862 429,220 508,621 2,322,794

Total expenditures 7,609,304 - 1,191,043 429,220 1,429,288 10,658,855

Excess (deficiency) of revenues

over (under) expenditures 206,658 1,893,485 (844,682) (411,982) 776,402 1,619,881

OTHER FINANCING

SOURCES (USES)

Transfers in 280,850 - 703,400 14,568 1,010,355 2,009,173

Transfers out (100,000) (1,626,320) - - (282,853) (2,009,173)

Sale of capital assets 7,900 - - - - 7,900

Total other financing sources (uses) 188,750 (1,626,320) 703,400 14,568 727,502 7,900

Net changes in fund balances 395,408 267,165 (141,282) (397,414) 1,503,904 1,627,781

Fund balances - beginning 3,527,339 323,422 1,686,792 987,497 1,465,933 7,990,983

Fund balances - ending 3,922,747$ 590,587$ 1,545,510$ 590,083$ 2,969,837$ 9,618,764$

The accompanying notes to financial statements are an integral part of this financial statement.

16

City of Sebastian, Florida

Statement of Revenues, Expenditures, and Changes in Fund Balances

Governmental Funds

For the year ended September 30, 2002

Net change in fund balances - total government funds 1,627,781$

1,122,610

344,553

(163,345)

Change in net assets of governmental activities 2,931,599$

The accompanying notes to financial statements are an integral part of this financial statement.

Reconciliation of the Statement of Revenues, Expenditures,

To the Statement of Activities

For the year ended September 30, 2002

and Changes in Fund Balances of Governmental Funds

17

Some expenses and revenues reported in the statement of activities do not add to or require the use of current financial

resources and therefore are not reported as revenues or expenditures in governmental funds (Note II.B. page 28).

Governmental funds report capital outlays as expenditures. However, in the statement of activities the cost of those assets is

allocated over their estimated useful lives and reported as depreciation expense. This is the amount by which capital outlay

($2,322,794) exceeded depreciation ($1,240,899, net of loss on disposal of assets of $87,894) in the current period. In the

governmental funds, the proceeds from the sale ($7,900) increased financial resources.

Repayment of debt principal is an expenditure in governmental funds, but the repayment reduces long-term liabilities in the

statement of net assets. This is the amount by which repayments reduced long-term liabilities (Note II.B. page 28).

City of Sebastian, Florida

Totals

ASSETS

Current assets:

Cash and cash equivalents:Cash in banks 1,250$ -$ 1,250$Equity in pooled investments 592,954 227,546 820,500

Accounts receivable 76 4,930 5,006Due from other governments - 53,745 53,745Inventory 13,203 - 13,203Prepaid expenses 1,725 740 2,465

Total current assets 609,208 286,961 896,169

Noncurrent assets:Restricted asset - cash and cash equivalents:

Equity in pooled investments 458,014 361,294 819,308Unamortized bond issue costs 111,175 - 111,175Capital assets:

Land - 9,060 9,060Buildings 333,189 - 333,189Improvements other than buildings 226,537 347,572 574,109Machinery and equipment 337,709 148,307 486,016Infrastructure 1,615,848 755,973 2,371,821Construction in process - 347,490 347,490

Less accumulated depreciation (1,265,580) (328,650) (1,594,230)

Total noncurrent assets 1,816,892 1,641,046 3,457,938

Total assets 2,426,100 1,928,007 4,354,107

LIABILITIESCurrent liabilities:

Accounts payable and accrued liabilities 22,979 36,380 59,359Accrued interest payable 3,549 - 3,549Current portion of long-term debt 222,718 305 223,023Deferred revenue 70,989 319 71,308

Total current liabilities 320,235 37,004 357,239

Noncurrent liabilities:Long-term debt 2,054,803 - 2,054,803

Total liabilities 2,375,038 37,004 2,412,042

NET ASSETSInvested in capital assets,

net of related debt (915,925) 1,279,752 363,827Restricted for:

Capital projects 21,919 - 21,919Debt service 436,095 - 436,095

Unrestricted 508,973 611,251 1,120,224

Total net assets 51,062$ 1,891,003$ 1,942,065$

The accompanying notes to financial statements are an integral part of this financial statement.

18

Golf Course Airport

Enterprise Funds

City of Sebastian, Florida

Proprietary Funds

September 30, 2002

Statement of Net Assets

Totals

Operating revenues:

Charges for fees and rents:

Golf course fees 1,309,498$ -$ 1,309,498$

Rents 29,798 167,061 196,859

Other revenue 26,221 12,312 38,533

Total operating revenues 1,365,517 179,373 1,544,890

Operating expenses:

Salaries, wages and employee benefits 279,735 67,829 347,564

Contractual services, materials and supplies 860,905 132,232 993,137

Depreciation 126,776 83,665 210,441

Amortization 13,099 - 13,099

Total operating expenses 1,280,515 283,726 1,564,241

Operating income (loss) 85,002 (104,353) (19,351)

Nonoperating revenues (expenses):

Investment earnings 20,907 11,215 32,122

Interest expense (112,803) - (112,803)

Loss on sale of fixed assets (233) - (233)

Total nonoperating revenues (expenses) (92,129) 11,215 (80,914)

Loss before capital contributions (7,127) (93,138) (100,265)

Capital contributions - 264,772 264,772

Change in net assets (7,127) 171,634 164,507

Total net assets - beginning 58,189 1,719,369 1,777,558

Total net assets - ending 51,062$ 1,891,003$ 1,942,065$

The accompanying notes to financial statements are an integral part of this financial statement.

19

Golf Course Airport

Enterprise Funds

City of Sebastian, Florida

Proprietary Funds

Statement of Revenues, Expenses and Changes in Fund Net Assets

For the year ended September 30, 2002

Totals

ACTIVITIES:

Cash received from customers and users 1,296,401$ 159,784$ 1,456,185$

Cash payments to suppliers (969,628) (179,697) (1,149,325)

Cash payments for employee services (277,474) (67,972) (345,446)

Other operating receipts 56,019 12,312 68,331

Payments for interfund services used (38,088) (32,114) (70,202)

activities 67,230 (107,687) (40,457)

CASH FLOWS FROM CAPITAL AND

RELATED FINANCING ACTIVITIES:

Acquisition and construction of capital assets (45,337) (299,863) (345,200)

Receipts from capital grants - 307,573 307,573

Principal paid on revenue bond maturities (100,000) - (100,000)

Interest paid on revenue bonds (104,481) - (104,481)

Net cash provided (used) by capital and

related financing activities (249,818) 7,710 (242,108)

CASH FLOWS FROM INVESTING

ACTIVITIES:

Interest on investments 20,972 11,251 32,223

Net cash provided by investing activities 20,972 11,251 32,223

Net decrease in cash and cash equivalents (161,616) (88,726) (250,342)

1,213,834 677,566 1,891,400

1,052,218$ 588,840$ 1,641,058$

The accompanying notes to financial statements are an integral part of this financial statement.

Net cash provided (used) by operating

20

City of Sebastian, Florida

Statement of Cash Flows

Proprietary Funds

For the year ended September 30, 2002

Enterprise Funds

Golf Course Airport

CASH FLOWS FROM OPERATING

Cash and cash equivalents, October 1

Cash and cash equivalents, September 30

Totals

Reconciliation of operating income (loss) to

net cash provided (used) by operating activities:

Operating income (loss) 85,002$ (104,353)$ (19,351)$

Adjustments not affecting cash:

Depreciation expense 126,776 83,665 210,441

Amortization 13,099 - 13,099

Changes in assets and liabilities:

Decrease (increase) in accounts receivable 7,294 (4,696) 2,598

Decrease in prepaid expenses 113 2,295 2,408

Decrease in inventories 12,577 - 12,577

Decrease in accounts payable (159,501) (81,874) (241,375)

Increase (decrease) in compensated absences 4 (685) (681)

Increase in accrued wages and taxes 2,257 542 2,799

Decrease in deferred revenues (20,391) (2,581) (22,972)

Total adjustments (17,772) (3,334) (21,106)

Net cash provided (used) by operating activities 67,230$ (107,687)$ (40,457)$

Cash and cash equivalents reconciliation:

Cash and cash equivalents :

Cash in banks 1,250$ -$ 1,250$

Equity in pooled investments 592,954 227,546 820,500

Restricted asset - cash and cash equivalents:

Equity in pooled investments 458,014 361,294 819,308

Cash and cash equivalents at September 30 1,052,218$ 588,840$ 1,641,058$

The accompanying notes to financial statements are an integral part of this financial statement.

21

Enterprise Funds

(Continued)

City of Sebastian, Florida

AirportGolf Course

Statement of Cash Flows

Proprietary Funds

For the year ended September 30, 2002

Pension

Trust Agency

Police

Officers' Performance

Pension Deposits

ASSETS

Cash and cash equivalents:

Cash in banks 251,301$ -$

Equity in pooled investments - 4,182

Receivables:

Employee contributions 2,265 -

Interest and dividends 26,737 -

Total receivables 29,002 -

Investments, at fair value:

U.S. government obligations 862,488 -

Federal agency notes 944,862 -

Corporate bonds 20,568 -

Common stock 508,080 -

Total investments 2,335,998 -

Total assets 2,616,301 4,182$

LIABILITIES

Refunds payable - 4,182$

Total liabilities - 4,182$

NET ASSETS

Held in trust for pension benefits 2,616,301$

The accompanying notes to financial statements are an integral part of this financial statement.

22

City of Sebastian, Florida

Fiduciary Funds

Statement of Fiduciary Net Assets

September 30, 2002

Police

Officers'

Pension

ADDITIONS

Contributions:

Employer 8,620$

Plan members 61,714

State 82,877

Total contributions 153,211

Investment earnings:

Net decrease in fair value of investments (48,448)

Interest and dividends 112,906

Total investment earnings 64,458

Less investment expenses (19,732)

Net investment earnings 44,726

Total additions 197,937

DEDUCTIONS

Benefits 24,283

Refunded contributions 18,053

Other expenses 7,253

Total deductions 49,589

Change in net assets 148,348

Net assets - beginning of year 2,467,953

Net assets - end of year 2,616,301$

The accompanying notes to financial statements are an integral part of this financial statement.

23

City of Sebastian, Florida

Statement of Changes in Fiduciary Net Assets

Fiduciary Fund - Pension Trust

For the year ended September 30, 2002

24

CITY OF SEBASTIAN, FLORIDA Notes to the Financial Statements

September 30, 2002

I. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The City of Sebastian (the “City”), a Florida Municipal Corporation, was incorporated in 1924 under Sections 1826-1832 of the Revised Florida Statutes. The City has a population of approximately 17,200 living in an area of approximately 13.5 square miles. The governing body is a five member elected City Council with a mayor elected from the five members. The City Council appoints the City Managerwho is responsible for the administration of all City services.

The financial statements of the City have been prepared in conformity with U.S. generally accepted accounting principles as applied to governmental units. The more significant of the City’s accounting policies are described below:

A. Reporting Entity

In evaluating the City as a reporting entity, management has included all component units in accordance with Governmental Accounting Standards Board (GASB) Statement No. 14, “Defining the Financial Reporting Entity”. The Financial Reporting Entity consists of the City of Sebastian (the primary government) and its blended component units. Blended component units are legallyseparate organizations for which the City Council is financially accountable. The component units discussed below are included in the City’s reporting entity.

Blended Component Units

The following component units are blended with the primary government for financial statement purposes because the component unit’s governing body is substantially the same as the City Council or because the component unit exclusively serves the City. The financial statements of these component units may be obtained from the City Clerk of the City of Sebastian.

Community Redevelopment Agency (CRA) – The governing body of the CRA is the Sebastian City Council. The CRA is accounted for in a special revenue fund entitled “Riverfront Redevelopment”.

City of Sebastian Police Officers’ Pension Plan – The City Council only appoints two of the five members of the governing board,but it is financially responsible for funding the police officers’ pension benefits. The City of Sebastian Police Officers’ Pension Trust Fund only exists to provide pension benefits to City of Sebastian police officers. It is accounted for as a Pension Trust fund entitled “Police Officers’ Pension”.

B. Basic Financial Statements

The government-wide financial statements (i.e., the statement of net assets and the statement of changes in net assets) report information on all of the nonfiduciary activities of the primary government and its blended component units. For the most part, the effect of interfund activity has been removed from these statements. Governmental activities, which normally are supported by taxes and intergovernmental revenues, are reported separately from business-type activities, which rely to a significant extent on fees and charges for support.

Separate fund financial statements are provided for governmental funds, proprietary funds, and fiduciary funds, even though the latter are excluded from the government-wide financial statements. Major individual governmental funds and major individual enterprisefunds are reported as separate columns in the fund financial statements.

GASB Statement No. 34 Basic Financial Statements and Management Discussion and Analysis for State and Local Governments sets forth minimum criteria (percentage of the assets, liabilities, revenues or expenditures/expenses of either fund category or thegovernmental and enterprise funds combined) for the determination of major funds. The nonmajor funds are combined in a column in the fund financial statements and detailed in the combining section.

C. Measurement Focus, Basis of Accounting, and Financial Statement Presentation

1. Economic Resources Measurement Focus and Accrual Basis of Accounting

The government-wide financial statements are reported using the economic resources measurement focus and the accrual basis of accounting, as are the proprietary fund and fiduciary fund financial statements. This means that revenues are recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of the related cash flows. Property taxes are recognized as revenues in the year for which they are levied. Grants and similar items are recognized as revenue as soon asall eligibility requirements imposed by the provider have been met.

25

In applying the “susceptible to accrual” concept to intergovernmental revenues pursuant to GASB Statement No. 33, Accounting and Financial Reporting for Nonexchange Transactions as amended by GASB Statement No. 36, Recipient Reporting of Certain Shared Nonexchange Revenues (the City may act as either provider or recipient), the provider should recognize liabilities and expenses and the recipient should recognize receivables and revenue when the applicable eligibility requirements including timerequirements, are met. Resources transmitted before the eligibility requirements are met should, under most circumstances, be reported as advances by the provider and deferred revenue by the recipient.

Private-sector standards of accounting and financial reporting issued prior to December 1, 1989, generally are followed in boththe government-wide and proprietary fund financial statements to the extent that those standards do not conflict with or contradict guidance of the Governmental Accounting Standards Board. Governments also have the option of following subsequent private-sector guidance for their business-type activities and enterprise funds, subject to this same limitation. Thegovernment has elected not to follow subsequent private-sector guidance.

As a general rule the effect of interfund activity has been eliminated from the government-wide financial statements.

The statement of activities demonstrates the degree to which the direct expenses of a given function or segment are offset by program revenues. Direct expenses are those that are clearly identifiable with a specific function or segment. Programrevenues include 1) charges to customers or applicants who purchase, use, or directly benefit from goods, services, or privileges provided by a given function or segment and 2) grants and contributions that are restricted to meeting the operational or capital requirements of a particular function or segment. Taxes and other items not properly included among program revenues are reported instead as general revenues.

Proprietary funds distinguish operating revenues and expenses from nonoperating items. Operating revenues and expenses generally result from providing services and producing and delivering goods in connection with a proprietary fund’s principal ongoing operations. The principal operating revenues of the golf course fund are charges to customers for sales and services and for the airport fund lease revenue. Operating expenses for enterprise funds include cost of sales and services, administrativeexpenses, and depreciation on capital assets. All revenues and expenses not meeting this definition are reported as nonoperating revenues and expenses.

2. Modified Accrual

Governmental fund financial statements are reported using the current financial resources measurement focus and the modifiedaccrual basis of accounting. Revenues are recognized as soon as they are both measurable and available. “Available” means collectible within the current period or soon enough thereafter to be used to pay liabilities of the current period. For this purpose, the City considers revenues to be available if they are collected within sixty (60) days of the end of the current fiscal period. All material revenues, except for occupational licenses and property taxes, are considered measurable and available andare thus susceptible to accrual. Occupational licenses are not considered available since neither a legally enforceable claim exists nor were the related services provided before October 1, 2002. Expenditures are generally recognized under the modifiedaccrual basis of accounting when the related fund liability is incurred, if measurable. An exception to this general rule is principal and interest on general long-term obligations, which are recognized when due.

Property taxes, public utility taxes, franchise fees, sales and fuel taxes, licenses, and interest associated with the current fiscalperiod are all considered to be susceptible to accrual and so have been recognized as revenues in the current fiscal period. Only the portion of special assessments receivable due within the current fiscal period is considered to be susceptible to accrual asrevenue of the current period. All other revenue items are considered to be measurable and available only when cash is receivedby the government.

The government reports the following major governmental funds:

The general fund is the government’s primary operating fund. It accounts for all financial resources of the general government, except those required to be accounted for in another fund.

The discretionary sales tax fund accounts for the financial resources used for infrastructure improvements and equipment purchases.

The capital improvements fund accounts for the accumulated resources associated with infrastructure improvements such as drainage, parks and buildings.

The road paving program fund accounts for the resources associated with debt for the purposes of reconstructing and paving roads.

The government reports the following major proprietary funds:

The golf course fund accounts for the activities of the municipal golf course.

The airport fund accounts for the activities of the municipality’s general aviation airport.

26

Additionally, the government reports the following fund types:

The pension trust fund accounts for the activities of the Police Officer’s Retirement System, which accumulates resources for pension benefit payments to qualified police officers.

The performance deposits fund accounts for deposits placed by bidders and developers to guarantee performance pursuant to bid or contract and for deposits for use of City owned buildings and parks to guarantee performance pursuant to contract. These funds are held by the City as agent for individuals and businesses.

When both restricted and unrestricted resources are available for use, it is the government’s policy to use restricted resources first, and then unrestricted resources as needed.

D. Assets, Liabilities and Fund Equity

1. Cash and cash equivalents

Cash and cash equivalents represents all investments that are short term, highly liquid, and readily convertible to a specifiedcash value. These investments generally have original maturities of three months or less. Cash equivalents consist of cash inbanks and on hand.

2. Equity in pooled investments

Equity in pooled investments consists of investments in the Local Government Surplus Funds Trust Fund administered by the Florida State Board of Administration. The State Board of Administration is not a registrant with the Securities and Exchange Commission. However, the Board has adopted operating procedures consistent with the requirements for a 2a-7 fund. In accordance with the regulations of 2a-7 like pools, the City’s share of investments held at the State Board of Administration arereported at amortized cost, which approximates fair value. This pool is regulated by the State and the fair value of the position in the pool is the same as the value of the pool share. Investment earnings of the pool are allocated to the participating funds at the end of each month based upon the ratio of each participant’s investment to the total pooled investments.

Pursuant to Florida Statutes, interest income earned on Local Option Gas Tax funds is required to be earmarked for transportation infrastructure improvements. Local Option Gas Tax funds held as investments in the Transportation Projects fund, which are part of an internal investment pool, are assigned and recorded in the Local Option Gas Tax Special Revenue Fund in accordance with these legal restrictions.

As of September 30, 2002, all funds participated in pooled cash investments except the Pension Trust and the Road Paving Program.

3. Investments

Investments, including the Police Officers’ Pension Fund, are stated at fair value, (quoted market price or the best available information).

4. Interfund Receivables and Payables