classifying corporate mefa applications: development and empirical test of a conceptual model

TRANSCRIPT

Eco-Management and AuditingEco-Mgmt. Aud. 8, 25–35 (2001)DOI: 10.1002/ema.145

CLASSIFYING CORPORATEMEFA APPLICATIONS:DEVELOPMENT ANDEMPIRICAL TEST OF ACONCEPTUAL MODEL

Stefan A. Seuring*

Carl-von-Ossietzky Universitat Oldenburg, Germany

Based on the conceptual framework ofLCA, this research aims to provide aframework for the classification andcompilation of corporate material andenergy flow analysis (MEFA), whichallows small and medium sizedenterprises to use MEFA as a tool incorporate decision making.

This resulted in a framework formaterial and energy flow analysis(MEFA), where corporate applicationsare classified according to thedimensions user, temporal type andmanagerial focus. This concept wasapplied to seven corporate MEFA casestudies, by interviewing the keyemployees involved in compiling thecase studies.

The model was checked to determinewhether it portrays the case studyapplications. The three dimensions usedproved to be suitable, as the MEFAapplications observed for the individualcases studies were in agreement with theones suggested by the model. Copyright

© 2001 John Wiley & Sons, Ltd and ERPEnvironment.

Received 11 September 2000Accepted 7 November 2000

LIMITS OF LCA APPLICATIONS

Some remarks on the development of LCA

Life-cycle assessment (LCA) is definedas a methodology that ‘studies the en-vironmental aspects and potential im-

pacts throughout a product’s life-cycle (i.e.cradle to grave) from raw material acquisi-tion through production, use and disposal.’(ISO 14040, 1997, p 2). Comprehensive casestudies have been presented, which cover thecomplete life-cycle of complex products.

While much is to be learned from suchLCAs, only large companies seem to use thetool to its full extent, as case study sum-maries suggest (Stolting and Rubik, 1992; Ru-bik et al., 1996; Bultmann, 1997). Frequently,smaller companies find this approach diffi-cult to handle. The effort and expenditurenecessary to conduct an LCA seem not to bejustified by the outcomes (Schaltegger, 1997).Furthermore, enterprises are often not able tounderstand the complete life cycles of all oftheir products, especially if the company ispart of several supply or value chains. Still,the analytical instruments that companieshave on hand to assess their products or

* Correspondence to: Stefan Seuring, Department of Productionand the Environment, Institute of Business Administration,Carl von Ossietzky University of Oldenburg, Birkenweg 5,26111 Oldenburg, Germany.

Copyright © 2001 John Wiley & Sons, Ltd and ERP Environment.

S. A. SEURING

production process often lack an environ-mental focus, which an LCA would be ableto deliver.

Further reasons are the lack of staffknowledge on environmental issues in smalland medium sized enterprises (SME), as wellas time and money constraints, which fur-ther limit their ability to conduct LCAs. Of-ten these companies have difficultiescompiling an input–output analysis for oneof their products and/or their (correspond-ing) processes, even though material and en-ergy flows form the physical basis of everyindustrial activity.

The reasons mentioned have led to a lackof knowledge about LCA in wide parts ofindustry. Still, the need to improve the envi-ronmental quality of products and produc-tion processes arises for different aspects,which range from public or political pres-sure, including legal acts, to strategic com-petitive advantages (Porter and van derLinde, 1995).

To overcome this ignorance of LCA con-cepts, SMEs can benefit from a methodologi-cal framework that offers the most importantbenefits of LCA, without its complexmethodology. In particular, the scope in theassessment of products or production pro-cesses has to be limited. To separate the ap-proach taken here from comprehensiveLCAs, the term corporate material and en-ergy flow analysis (MEFA) is used.

Material and energy flow analysis (MEFA)

A classification of MEFA applications helpscompanies to oversee what they can use thetool for in corporate practice. Therefore, thefollowing research questions are addressed.

1. How can the conceptual framework ofLCA be used to fit corporate applica-tions? Which LCA concepts can be usedto characterize corporate MEFA?

2. Which classes of MEFA can be distin-guished and how do they fit with appli-cations observed by selected case studies?

There are various opinions concerning theusage of the term LCA. Specially, SETAC

argues that LCA case studies have to coverthe entire life cycle.

Hence, another term is helpful that distin-guishes approaches taken in corporate casestudies from the claim of LCA, as a methodthat, based on the LCA perspective, yieldssimilar results without having the methodo-logical complexity of a full LCA. This in-evitably involves a trade-off between cost,scientific accuracy of the results and appli-cability of the method as well as its conse-quences in a company.

As an environmental assessment tool, amaterial and energy flow analysis (MEFA) isa reduction in the scope of an LCA to justone stage of the product life cycle, along thephases goal and scope definition, inventoryand interpretation of results. It should benoted that for simplicity, the acronym willbe used both for the process of conductingthe MEFA as well as for its result, which isequivalent to an inventory in the ISO termi-nology.

The definition provided for MEFA is inaccordance to a note in the ISO 14040: ‘IfLCA is to be successful in supporting envi-ronmental understanding of products, it isessential that LCA maintains its technicalcredibility while providing flexibility, practi-cality and cost effectiveness of application.This is particularly true if LCA is to be ap-plied within small and medium sized enter-prises,’ (ISO 14040, 1997, p 3) as proposedhere.

Enterprises have to take care of cost effec-tiveness in applying tools such as LCA orMEFA. We emphasize again, ‘the reasons fortaking shortcuts [such as MEFA] are that afull LCA is costly, time consuming and oftenlimited in applications where quick, effec-tive, and yet accurate, decisions must bemade’ (Weitz et al., 1996, p 79). Using MEFAinside companies yields applicable andmeaningful results because concentrating oncompanies’ production processes allows adetailed assessment that is not possible out-side their gates. As these processes form thephysical basis of the companies’ activities adetailed knowledge about them is beneficialfor corporate decision making.

Copyright © 2001 John Wiley & Sons, Ltd and ERP Environment Eco-Mgmt. Aud. 8, 25–35 (2001)

26

CLASSIFYING CORPORATE MEFA APPLICATIONS

A CONCEPTUAL FRAMEWORK OFCORPORATE MEFA

Dimensions of corporate MEFA applications

After clarifying the term MEFA, the functionsof MEFA in corporate practice remain to bestudied. Knowing the possible applicationsof MEFA will help companies to classifyintended case studies before they areconducted.

However, the specific functions depend onthe situation. A review of the literature re-veals that they can be classified according tovarious dimensions.

� Use in public policy versus industrial envi-ronmental management (ISO 14040, 1997, p3; Neitzel, 1997; Goidel and McKiel, 1996, p8.1; Allen, 1996, p 5.1; Fava and Consoli,1996, p 11.1).

� One-off approach versus continuous appli-cation (Kytzia, 1995, pp 92, 147).

� Use for internal or external purposes (Jasch,1992, p 13; Braunschweig and Muller-Wenk, 1993, p 21; Consoli et al., 1993, p 33;Gray et al., 1993, p 174; Gensch, 1993, pp65–74; Grotz and Scholl, 1996, pp 226–230).

� Use for retrospective, affirmative orprospective purposes (Rubik et al., 1996, p107).

� Use for technical, organizational or strategicapplications (as often done in managementliterature).

Subsequently, these categories are assessedregarding their suitability within the corporatecontext.

Public policy versus corporateenvironmental managementVarious references including the ISO 14040norm address the distinction of whether LCAis used for public policy making or industrialenvironmental management. LCA applica-tions in public policy usually aim to preparepolitical decisions, which may result in legis-lation (Fava et al., 1994, p 5, UBA, 1992, p 7).Therefore, it has different actors and interestscompared with corporate applications. Theseaspects are not reflected here any further, butas a company may use LCA to influence

public policy, the borders are ill defined be-tween the different functional uses.

One-off approachesCorporate decisions can be categorized intothose that have to be taken once or repeat-edly. Management information systems try toutilize information for structured problemsthat occur continually, such as the concept ofeco-controlling that utilizes eco-balances forcontinuous decision making (Schaltegger,1997, p 3).

In contrast, enterprises review their activi-ties as done in policy analysis (Wildavsky,1978) or strategic control (Bungay and Goold,1991). This is best carried out in one-off ap-proaches, which are tailored to specific pur-poses and aspects of the organization(Wehrmeyer, 1995, p 22). MEFA best fits thiscategory and accordingly the use of MEFA forrepeated decision making is not consideredhere.

Internal/external useAnother variable presented is whether theintended user is inside or outside the com-pany. This is a categorization that reflects thefact that every company has internal and ex-ternal activities and stakeholders. Still, it is auseful distinction, as corporate action andcommunication are different on these twolevels.

Temporal typeRegarding temporal aspects, three types ofLCA can be distinguished, which are retro-spective, affirmative or prospective (Rubik etal., 1996, p 107).Retrospective. This mode is used for the confir-mation, assessment or falsification of earlierdecisions, e.g. when the changes to a productof material and energy consumption are com-pared with a previous product after the pro-duction of the new design already started.Affirmative. Here, the structure of an existingproduct or production line is analysed. It as-sists in learning about the system studied andidentifying vague optimization potentials.Prospective. This is the ‘ideal type’, where thecase study is used to optimize a product orprocess system by identifying ecological weak

Copyright © 2001 John Wiley & Sons, Ltd and ERP Environment Eco-Mgmt. Aud. 8, 25–35 (2001)

27

S. A. SEURING

spots and/or providing information for re-design and innovation.

This dimension is applicable as it helps toassess why the case study is conducted.

Managerial focusFinally, MEFAs can be distinguished accord-ing to their managerial focus (short focus) intothose for technical/operational, managerial/or-ganizational or strategic levels. The technical/operational level describes direct operations(e.g. production) of a company, while themanagerial/organizational level sets theframework for the operations, e.g. by definingthe organizational structure of a company.Strategic management determines the princi-pal or long term goals of a company. MEFAcase studies can be directed to all three levels.Furthermore, revision and corporate planningaffects these levels, too.

Modelling MEFA applications

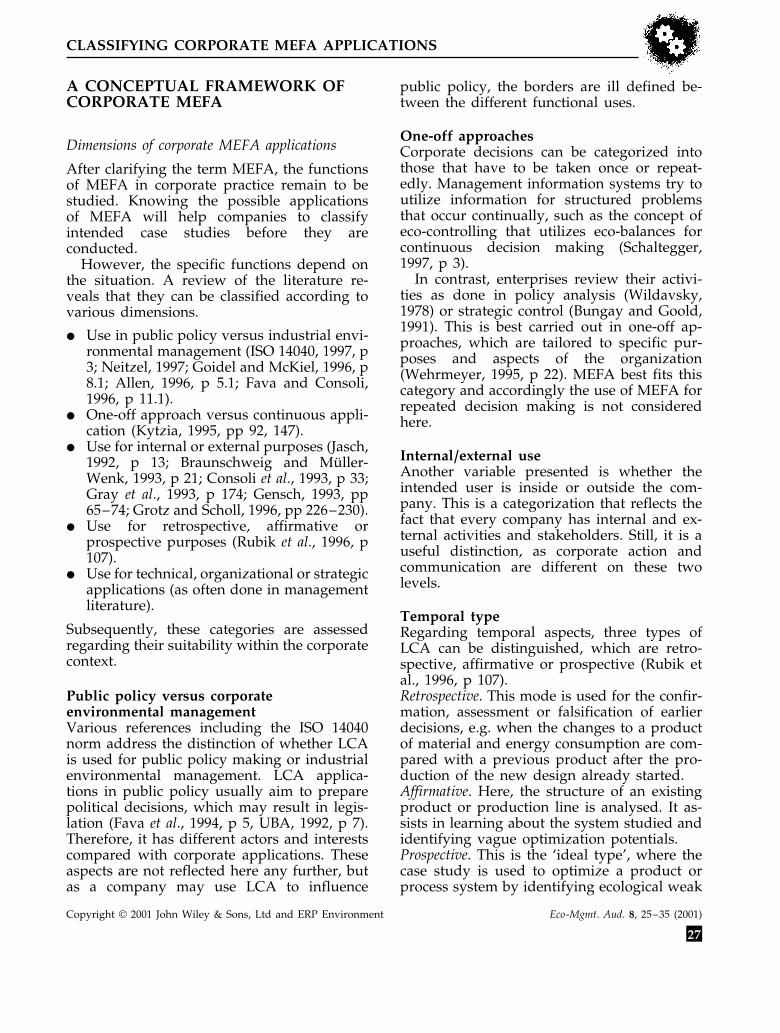

Summarizing the arguments provided, the ap-plications addresses will exclude public policyuses. Within the corporate context, only one-off approaches are taken into account. Hence,these two dimensions will not be consideredfurther. The remaining categorization can begraphed into the dimensions user, type andfocus, which are now combined. The resultingmodel allows one to analyse which specificapplications result. The categorization ofMEFA applications according to the three di-mensions fits well with the applications men-tioned in various publications, but offers amodel to systemize them.

Taking all three variables, user, type andfocus, together, a matrix with a total of 18fields is formed as displayed in Figure 1. Thissection outlines the resulting fields of the ma-trix and their applications with reference toliterature given above. It has to be noted thatthe distinctions made are ideal types. Hence,the borders between neighbouring fields ofthe tables are often blurred.

The two following sections describe themodel further. For better presentation, theyare divided into internal and external applica-tions as summarized in Tables 1 and 2.

Internal applicationsThe retrospective application offers thechance to review past decisions on all threelevels as well as to assess technical or organi-zational effects. On the strategic level, LCA orMEFA can be used for issues of policy analy-sis or strategic control. The affirmative use isclosely linked to this. A MEFA assists in infor-mation gathering, which enables operative ormanagerial control by compiling and structur-ing data. Recording data year by year, thefirst step towards management informationsystems is performed.

The prospective use covers aspects of ‘weakspot analysis’, process and product optimiza-tion at the technical level as well as stafftraining and organizational learning. Finally,LCA is applied as a strategic planning instru-ment. This topic is raised in various publica-tions (Heijungs et al., 1996, p 29), even basedon empirical studies (Grotz and Scholl, 1996,p 227; Bultmann, 1997, pp 46–60), but noexplanations or samples are given.

External applicationsExternal applications of LCA fit within thecontext of the external relations and especiallythe communication of an enterprise. Hence, itranges from providing technical informationfor customers and suppliers to public policylobbying.

The retrospective use centres on the infor-mation of various stakeholder groups, draw-ing a wider line from the operational to thestrategic level. The external and affirmative

Figure 1. Classification of MEFA applications.

Copyright © 2001 John Wiley & Sons, Ltd and ERP Environment Eco-Mgmt. Aud. 8, 25–35 (2001)

28

CLASSIFYING CORPORATE MEFA APPLICATIONS

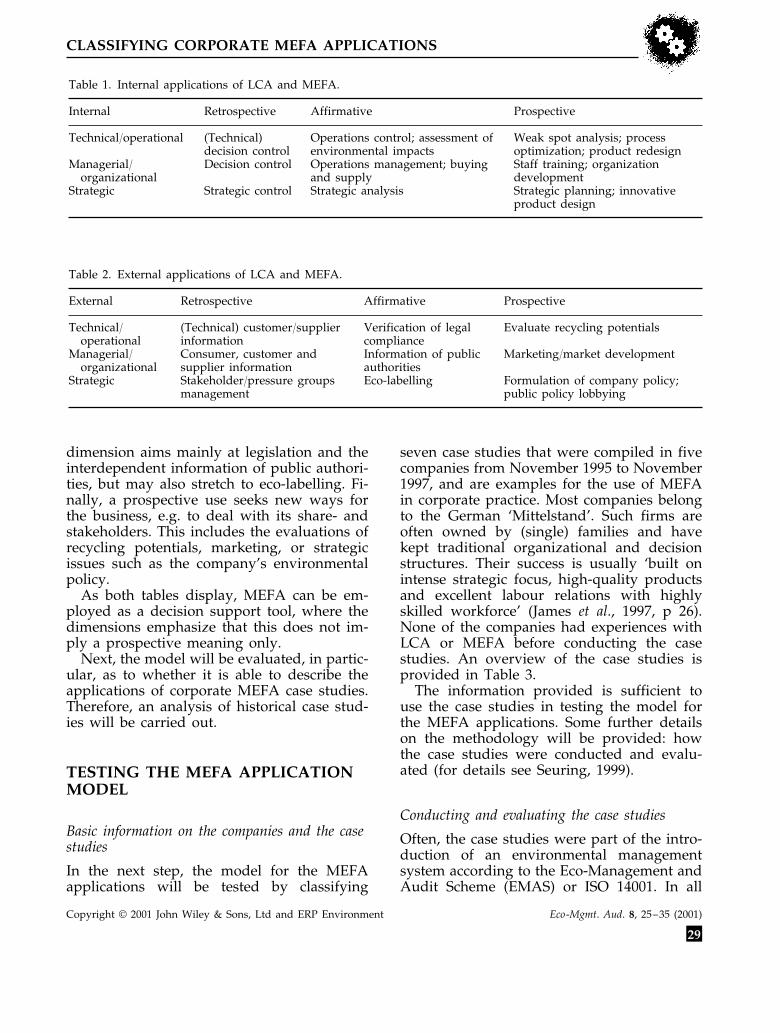

Table 1. Internal applications of LCA and MEFA.

Internal Retrospective Affirmative Prospective

Technical/operational (Technical) Weak spot analysis; processOperations control; assessment ofdecision control optimization; product redesignenvironmental impacts

Managerial/ Staff training; organizationDecision control Operations management; buyingand supply developmentorganizational

Strategic Strategic control Strategic analysis Strategic planning; innovativeproduct design

Table 2. External applications of LCA and MEFA.

Affirmative ProspectiveRetrospectiveExternal

(Technical) customer/supplierTechnical/ Evaluate recycling potentialsVerification of legalcomplianceinformationoperational

Managerial/ Consumer, customer and Information of public Marketing/market developmentauthoritiessupplier informationorganizational

Formulation of company policy;Eco-labellingStakeholder/pressure groupsStrategicmanagement public policy lobbying

dimension aims mainly at legislation and theinterdependent information of public authori-ties, but may also stretch to eco-labelling. Fi-nally, a prospective use seeks new ways forthe business, e.g. to deal with its share- andstakeholders. This includes the evaluations ofrecycling potentials, marketing, or strategicissues such as the company’s environmentalpolicy.

As both tables display, MEFA can be em-ployed as a decision support tool, where thedimensions emphasize that this does not im-ply a prospective meaning only.

Next, the model will be evaluated, in partic-ular, as to whether it is able to describe theapplications of corporate MEFA case studies.Therefore, an analysis of historical case stud-ies will be carried out.

TESTING THE MEFA APPLICATIONMODEL

Basic information on the companies and the casestudies

In the next step, the model for the MEFAapplications will be tested by classifying

seven case studies that were compiled in fivecompanies from November 1995 to November1997, and are examples for the use of MEFAin corporate practice. Most companies belongto the German ‘Mittelstand’. Such firms areoften owned by (single) families and havekept traditional organizational and decisionstructures. Their success is usually ‘built onintense strategic focus, high-quality productsand excellent labour relations with highlyskilled workforce’ (James et al., 1997, p 26).None of the companies had experiences withLCA or MEFA before conducting the casestudies. An overview of the case studies isprovided in Table 3.

The information provided is sufficient touse the case studies in testing the model forthe MEFA applications. Some further detailson the methodology will be provided: howthe case studies were conducted and evalu-ated (for details see Seuring, 1999).

Conducting and evaluating the case studies

Often, the case studies were part of the intro-duction of an environmental managementsystem according to the Eco-Management andAudit Scheme (EMAS) or ISO 14001. In all

Copyright © 2001 John Wiley & Sons, Ltd and ERP Environment Eco-Mgmt. Aud. 8, 25–35 (2001)

29

S. A. SEURING

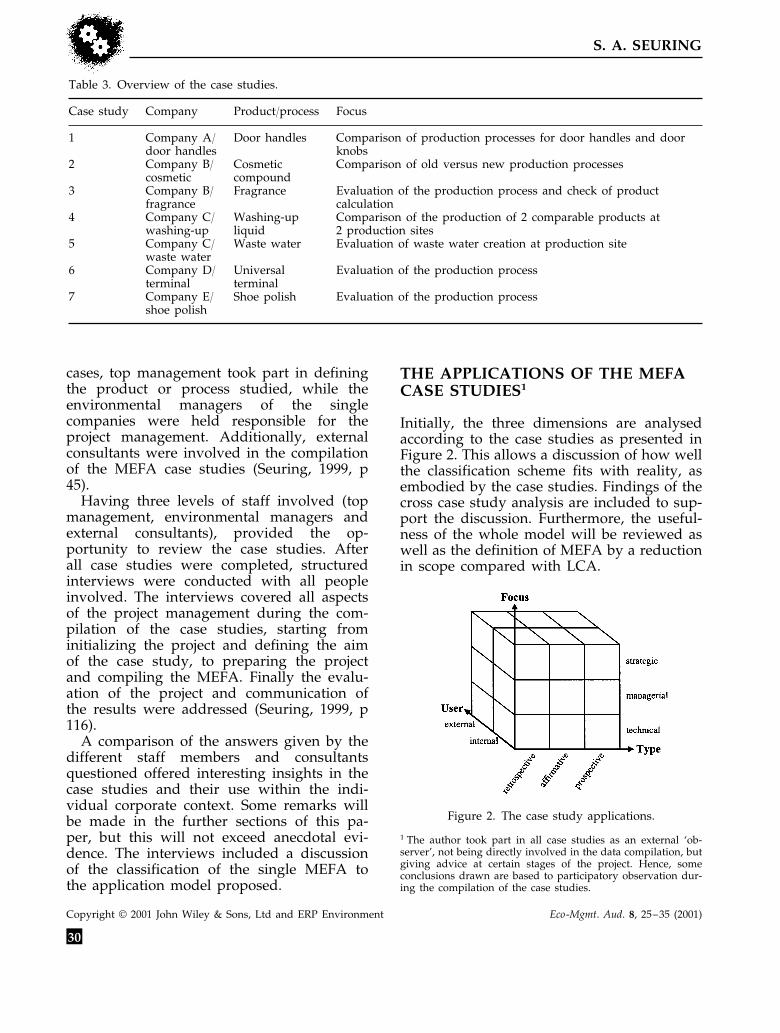

Table 3. Overview of the case studies.

CompanyCase study FocusProduct/process

1 Company A/ Door handles Comparison of production processes for door handles and doorknobsdoor handles

Company B/ Cosmetic Comparison of old versus new production processes2compoundcosmetic

3 Company B/ Evaluation of the production process and check of productFragrancecalculationfragrance

4 Company C/ Comparison of the production of 2 comparable products atWashing-up2 production siteswashing-up liquid

5 Company C/ Evaluation of waste water creation at production siteWaste waterwaste water

Evaluation of the production processUniversalCompany D/6terminalterminal

Evaluation of the production process7 Shoe polishCompany E/shoe polish

cases, top management took part in definingthe product or process studied, while theenvironmental managers of the singlecompanies were held responsible for theproject management. Additionally, externalconsultants were involved in the compilationof the MEFA case studies (Seuring, 1999, p45).

Having three levels of staff involved (topmanagement, environmental managers andexternal consultants), provided the op-portunity to review the case studies. Afterall case studies were completed, structuredinterviews were conducted with all peopleinvolved. The interviews covered all aspectsof the project management during the com-pilation of the case studies, starting frominitializing the project and defining the aimof the case study, to preparing the projectand compiling the MEFA. Finally the evalu-ation of the project and communication ofthe results were addressed (Seuring, 1999, p116).

A comparison of the answers given by thedifferent staff members and consultantsquestioned offered interesting insights in thecase studies and their use within the indi-vidual corporate context. Some remarks willbe made in the further sections of this pa-per, but this will not exceed anecdotal evi-dence. The interviews included a discussionof the classification of the single MEFA tothe application model proposed.

THE APPLICATIONS OF THE MEFACASE STUDIES1

Initially, the three dimensions are analysedaccording to the case studies as presented inFigure 2. This allows a discussion of how wellthe classification scheme fits with reality, asembodied by the case studies. Findings of thecross case study analysis are included to sup-port the discussion. Furthermore, the useful-ness of the whole model will be reviewed aswell as the definition of MEFA by a reductionin scope compared with LCA.

Figure 2. The case study applications.

1 The author took part in all case studies as an external ‘ob-server’, not being directly involved in the data compilation, butgiving advice at certain stages of the project. Hence, someconclusions drawn are based to participatory observation dur-ing the compilation of the case studies.

Copyright © 2001 John Wiley & Sons, Ltd and ERP Environment Eco-Mgmt. Aud. 8, 25–35 (2001)

30

CLASSIFYING CORPORATE MEFA APPLICATIONS

As Figure 2 summarizes, most of the casestudies belong to the internal category. This isin accordance with the fact that none of thecompanies had previous experience with theinstrument of MEFA or LCA.

The MEFA case studies were applied tocompare the findings to other instruments incorporate decision support or to learn moreabout an established process or technology aswell as MEFA as management tool. Furthersupport for this issue is provided by the factthat five of the case studies are classified astechnical and only one each belongs to themanagerial or strategic level.

The third dimension ‘temporal type’ con-cludes this, too, as five of the studies areretrospective or affirmative and not compiledwith a prospective aim, e.g. to cause changesat the product design or production process.Still, all managers reported that they hadgained additional knowledge from the MEFAand saw the case studies as valuable for theircompany.

The single variables user, type and focusare subject to further assessment, testing theirappropriateness within the model. This leadsto a review of the total model.

Internal and external user

As only one case study was conducted forexternal purposes, the insights into the userdimension are limited. External applicationsare expected to be applied, when the compa-nies feel confident about the use of MEFA.

Still, the categories are suitable for classify-ing MEFA applications, as details provided tointernal practitioners do not have to take thecompanies’ secrecy interest into account. Thisenables an open discussion of findings. Out-side communication usually centres onspecific aims, depending on the stakeholdergroup addressed. Therefore, it will be re-stricted in scope.

The problem of this classification is thatinternal users may decide at some point afterthe MEFA took place to publish the findings.This happened in the door handle and thecosmetic case studies. Nevertheless, it is justi-fied to distinguish the two categories, as thecontent of the report had been modified,

particularly to preserve the companies’secrecy interests. The user dimension and itsinternal and external categories are suitablefor the classification of the MEFA case studiespresented.

Type of case study

The case studies are assigned to all threecategories of the dimension type, which isclosely connected to the objectives of the sin-gle case study. Retrospective studies such ascompany B (cosmetic) and company E (shoepolish) were carried out to confirm decisionstaken. This aim was met in both cases. Due toa lack of historic data, the old processes inparticular were studied, so that improvementsmade by the introduction of the new produc-tion process were emphasized. However, theimpacts of the case studies were limited tothis benefit and learning about MEFA as acorporate management tool.

The case studies in the affirmative categorywere even more among the focus of learningabout MEFA methodology. As neither a retro-spective decision was questioned nor aprospective one prepared, the case studieswere conducted to review a process orproduct. However, the conclusions drawn bythe management were comparable to those ofother case studies, as each case study revealedsome optimization potentials (Seuring, 1999,pp 52–70).

Two case studies had prospective aims,which are said to be the ideal type (Rubik etal., 1996, p 107). However, even though bothstudies were set up with a prospective aim,this carries the danger of having wrong pre-conceptions. As an example this can be por-trayed in the wastewater case study. Often,large amounts of waste or wastewater createdcan be attributed to a few major sources. Ifthese sources were identified, they would of-fer a chance for optimization. While this wasexpected to be the case, the findings showedthat only a single source yielding more than10% of the wastewater could be identified,while other sources contributed 5–10% each.Hence, optimization was possible and carriedout, but the resulting effects were restricted.

Copyright © 2001 John Wiley & Sons, Ltd and ERP Environment Eco-Mgmt. Aud. 8, 25–35 (2001)

31

S. A. SEURING

One major improvement was the introductionof the measurements themselves.

The variable type with its three categories(retrospective, affirmative and prospective)distinguishes the case studies in a suitablemanner. The process of compiling the casestudy, evaluating its findings and puttingthem into the corporate context might trans-form a retrospective one into a prospectiveone. But the opposite can also happen, as it isnot possible to oversee such a project com-pletely at its start.

Furthermore, it would be important to ad-dress which kind of optimization is sufficientas a result of the MEFA case study. It mightrange from a modification of one parameter ina single process of a whole process chain tothe complete redesign of a product. This leadsto the conclusion that a case study intended tobe retrospective might cause greater effectsthan a prospective one.

The three categories utilized for the variable‘temporal type’ are difficult to distinguish inreality. The categorization would be beneficialduring the goal and scope definition phases,as it would help to check the intended aimsand their appropriateness. Therefore, it mightbe valuable to analyse this dimension in theproject initiation and evaluation stage andcompare the findings, to obtain full access tothe kind of information offered by the dimen-sion type.

Managerial focus

Technical/operational levelFinally, the dimension managerial focus (forshort, focus) is assessed. Five case studies areassigned to the technical level (see Figure 2),as most case studies provided a list of possi-ble improvements to the process operation orproduct itself. As these suggestions were seenas beneficial for the company, it is surprisingthat in most cases the findings did not lead todirect action. This might be caused by the factthat the reports were prepared by the externalconsultants, who left the companies immedi-ately after completing the study. Therefore,they were not able to support the implemen-tation of the findings.

In some cases staff that would have beenable to transfer these findings into action didnot know about the project report. Therefore,it is surprising, that both environmental man-agers and top management saw positive ef-fects, concerning environmental and economicaspects. However, it fits with the picture ofinsufficient transfer to action that often theywere not able to state specific ones. Already,these issues lead to the managerial/organiza-tional level.

Managerial/organizational levelOnly the fragrance case study at company Bfalls into this category (Figure 2), but manage-rial or organizational issues were addressedin various reports and formed part of thediscussions within the interviews. Most im-portant are data documentation, reportingand storage, of both technical and accountingdata. Depending on the companies’ computersystems, the amount of information that wasused in the MEFA had a high degree of vari-ability. In some cases, almost no useful infor-mation was offered. On the other hand,up-to-date computer systems with integratedproduction management did reveal a lot ofuseful information that formed part of theinventory.

The integration of all data processing sys-tems inside the company would improve theability to compile a MEFA case study time-and cost-efficiently. Major parts of the datacollection necessary can be simplified, if theyare taken from available data, e.g. the enter-prise resource planning system.

Several case studies emphasized the impor-tance of staff action for the physical inventory,but even more important is the methodologi-cal learning of staff. The interviews showed awide range of different consequences. Somemanagers did know e.g. about LCA softwareand current developments in LCA, and sawthe case study as valuable for the companies’learning on environmental management tools.They plan to broaden their knowledge infuture.

In contrast, in some case studies the reportsdid not even reach some of the people directlyinvolved. This prevents learning beyond thedirect action taken in compiling the data.

Copyright © 2001 John Wiley & Sons, Ltd and ERP Environment Eco-Mgmt. Aud. 8, 25–35 (2001)

32

CLASSIFYING CORPORATE MEFA APPLICATIONS

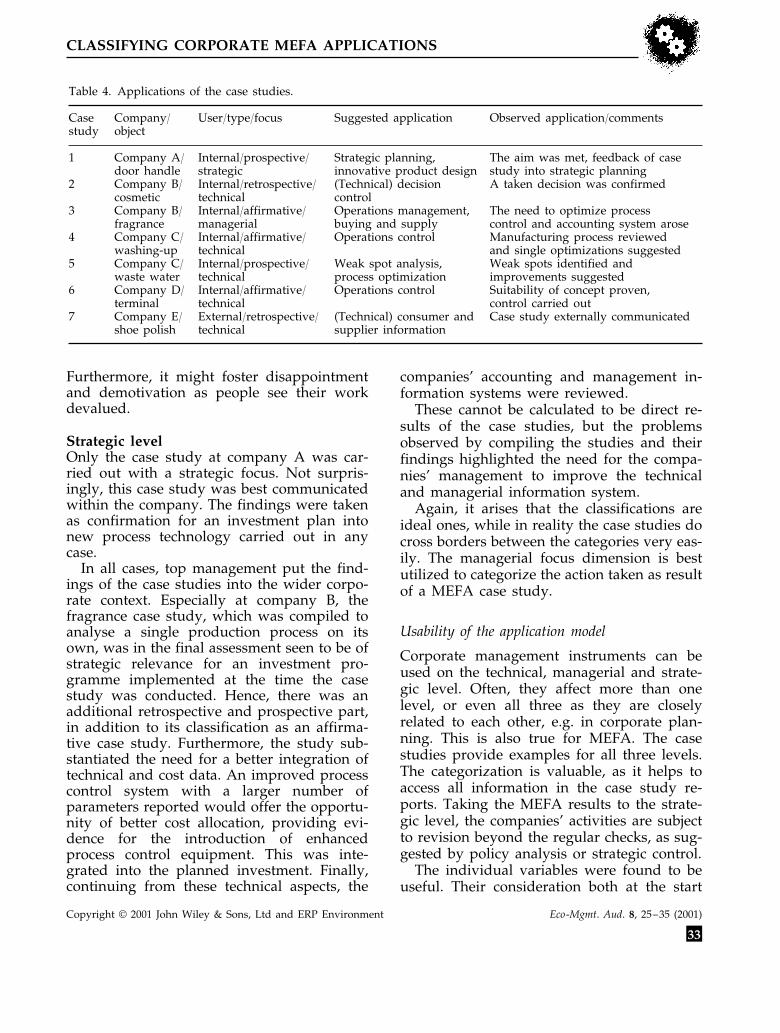

Table 4. Applications of the case studies.

Observed application/commentsCompany/ Suggested applicationUser/type/focusCaseobjectstudy

Company A/ The aim was met, feedback of caseInternal/prospective/ Strategic planning,1study into strategic planningdoor handle strategic innovative product design

2 A taken decision was confirmedCompany B/ Internal/retrospective/ (Technical) decisioncosmetic controltechnical

3 Company B/ The need to optimize processInternal/affirmative/ Operations management,managerial buying and supply control and accounting system arosefragrance

4 Company C/ Internal/affirmative/ Operations control Manufacturing process reviewedand single optimizations suggestedwashing-up technical

5 Company C/ Internal/prospective/ Weak spots identified andWeak spot analysis,technical process optimizationwaste water improvements suggested

6 Company D/ Suitability of concept proven,Internal/affirmative/ Operations controlterminal technical control carried outCompany E/ Case study externally communicatedExternal/retrospective/ (Technical) consumer and7

technical supplier informationshoe polish

Furthermore, it might foster disappointmentand demotivation as people see their workdevalued.

Strategic levelOnly the case study at company A was car-ried out with a strategic focus. Not surpris-ingly, this case study was best communicatedwithin the company. The findings were takenas confirmation for an investment plan intonew process technology carried out in anycase.

In all cases, top management put the find-ings of the case studies into the wider corpo-rate context. Especially at company B, thefragrance case study, which was compiled toanalyse a single production process on itsown, was in the final assessment seen to be ofstrategic relevance for an investment pro-gramme implemented at the time the casestudy was conducted. Hence, there was anadditional retrospective and prospective part,in addition to its classification as an affirma-tive case study. Furthermore, the study sub-stantiated the need for a better integration oftechnical and cost data. An improved processcontrol system with a larger number ofparameters reported would offer the opportu-nity of better cost allocation, providing evi-dence for the introduction of enhancedprocess control equipment. This was inte-grated into the planned investment. Finally,continuing from these technical aspects, the

companies’ accounting and management in-formation systems were reviewed.

These cannot be calculated to be direct re-sults of the case studies, but the problemsobserved by compiling the studies and theirfindings highlighted the need for the compa-nies’ management to improve the technicaland managerial information system.

Again, it arises that the classifications areideal ones, while in reality the case studies docross borders between the categories very eas-ily. The managerial focus dimension is bestutilized to categorize the action taken as resultof a MEFA case study.

Usability of the application model

Corporate management instruments can beused on the technical, managerial and strate-gic level. Often, they affect more than onelevel, or even all three as they are closelyrelated to each other, e.g. in corporate plan-ning. This is also true for MEFA. The casestudies provide examples for all three levels.The categorization is valuable, as it helps toaccess all information in the case study re-ports. Taking the MEFA results to the strate-gic level, the companies’ activities are subjectto revision beyond the regular checks, as sug-gested by policy analysis or strategic control.

The individual variables were found to beuseful. Their consideration both at the start

Copyright © 2001 John Wiley & Sons, Ltd and ERP Environment Eco-Mgmt. Aud. 8, 25–35 (2001)

33

S. A. SEURING

and the end of the case study would provideuseful insights and ensure that all aspects aretaken into account. After the three dimensionsuser, type and focus have been subject to anassessment separately, the whole model’ssuitability, i.e. the combination of the threevariables, has to be reviewed.

To provide a useful classification, the di-mensions used in a model have to be inde-pendent from each other, so that differentaspects are analysed by each of them. This isgiven for the dimensions user, type and focus.They allow the classification of the case stud-ies. A comparison of the applications de-scribed for the single fields of the modelmatrix, as displayed in Tables 1 and 2, fitswith the actual use presented for the studies.The independence of the dimensions is sup-ported by the fact that no categories of twodifferent dimensions are only observedjointly.

Table 4 compares the modes of applicationobserved with the applications proposed bythe model. A close fit is given for all casestudies, which provides evidence for theusability of the model.

If the model is used during the initiationand preparation of the project, it will help tocheck and classify the aims to be addressed.This reassures the importance of the projectinitiation and aim definition step for the pro-ject management. Using the model to classifya case study before it is compiled would helpto avoid most of the problems reported. Inthis respect, the MEFA case studies portrayedare in line with problems reported in othercases (Newton and Harte, 1997).

The issues of decision support have beenaddressed implicitly within the previous sec-tions. MEFA does provide a chance to gainaccess to technical data that supports corpo-rate decisions. In this respect, MEFA is similarto other instruments of decision making, butis particularly suitable for technical and envi-ronmental aspects.

Concluding remarks

Like all activities of a company, MEFA cannotbe seen isolated from its context. Withoutknowing its own processes and their related

material and energy flows, a company mightfind it increasingly difficult to operate in acompetitive environment. MEFA is able tocontribute to this knowledge and close someof the gaps.

MEFA is close to other corporate instru-ments. On the technical level, MEFA providesdata for technical optimization like mechani-cal or process engineering do traditionally.Improvements or innovations in process tech-nologies often lead to better use of resources,complemented by a reduction of the amountof waste produced. This addresses a chancefor both MEFA and environmental manage-ment itself, as its use would transfer fromcompliance-orientated instruments to instru-ments that help to create business opportuni-ties and long term competitiveness ofcompanies.

Having gained experience in MEFA, somemanagers might decide to move beyond theirown factory gates. Being able to handleMEFA, they might want to move on andexplore the potential of LCA by assessing thecomplete product life cycle (Consoli et al.,1993, p 7; Boustead, 1996, p 147).

MEFA can be seen as a corporate applica-tion of LCA concepts. Therefore, it can beextended to reach LCA. This has to be doneobserving the limited ability in time andmoney of companies to conduct LCA studies.The recent and further development ofscreening and streamlining techniques (Chris-tiansen, 1997; Curran and Young, 1996, p 57)will expand the use of LCA in companies.

ACKNOWLEDGEMENTS

This research was sponsored by the German FederalMinistry of Education and Research under the grantnumber F 107396.

REFERENCES

Allen D. 1996. Applications of life-cycle assessment. InEnvironmental Life Cycle Assessment, Curran MA (ed.).McGraw-Hill: New York; 5.1–5.18.

Boustead I. 1996. LCA – how it came about: the begin-ning in the U.K. International Journal of LCA 1(3):147–150.

Copyright © 2001 John Wiley & Sons, Ltd and ERP Environment Eco-Mgmt. Aud. 8, 25–35 (2001)

34

CLASSIFYING CORPORATE MEFA APPLICATIONS

Braunschweig A, Muller-Wenk R. 1993. O8 kobilanzen furUnternehmungen. Oldenbourg: Vienna.

Bultmann A. 1997. Produktokobilanzen und ihre An-wendung in deutschen Unternehmen, Schriftenreihe desIO8 W 112/97. Berlin.

Bungay S, Goold M. 1991. Creating a strategic controlsystem. Long Range Planning 24(3): 32–39.

Christiansen K (ed). 1997. Simplifying LCA: Just a Cut?,final report from the SETAC-Europe LCA Screeningand Streamlining Working Group. Brussels.

Consoli F, Allen D, Boustead I, Fava J, Franklin W,Jensen A, de Oude N, Parrish R, Perriman R, Postleth-waite D, Quay B, Seguin J, Vigon B (eds). 1993.Guidelines for Life-Cycle Assessment: a ‘Code of Practice’.From the SETAC Workshop held at Sesimbra, 1993.Brussels.

Curran MA, Young S. 1996. Report from the EPA confer-ence on streamlining LCA. International Journal of LCA1(1): 57–60.

Fava JA, Consoli FJ. 1996. Application of life-cycle as-sessment to business performance. In EnvironmentalLife Cycle Assessment, Curran MA (ed.). McGraw-Hill:New York; 11.1–11.12.

Fava JA, Denison R, Jones B, Curran MA, Vigon B, SelkeS, Barnum J (eds). 1994. A Technical Framework forLife-Cycle Assessment, workshop report, 1991, SecondPrinting. Smugglers Notch: Vermont.

Gensch C-O. 1993. Erfahrungen bei der Erstellung vonProdukt-O8 kobilanzen und Produktlinienanalysen inZusammenarbeit mit der Industrie. In Produktlinien-analyse und O8 kobilanzen, Grießhammer R, Pfeiffer R(eds). 2. Freiburger Kongreß: Freiburg; 65–74.

Goidel E-S, McKiel M. 1996. Public policy applicationsof life-cycle assessment. In Environmental Life CycleAssessment, Curran MA (ed.). McGraw-Hill: NewYork; 8.1–8.11.

Gray R, Bebbington J, Walters D. 1993. Accounting for theEnvironment. London: Chapman.

Grotz S, Scholl G. 1996. Application of LCA in Germanindustry. International Journal of LCA 1(4): 226–230.

Heijungs R, Huppes G, Udo de Haes H, van den BergNW, Dutilh CE. 1996. Life Cycle Assessment: What It Isand How To Do It: the Uses of Life Cycle Assessment.UNEP: Paris.

ISO 14040. 1997. Life Cycle Assessment – Principles andFramework. Berlin.

James P, Prehn M, Steger U. 1997. Corporate Environmen-tal Management in Britain and Germany. Anglo-GermanFoundation: London.

Jasch C. 1992. Was ist und kann eine O8 kobilanz? O8 kobi-lanz, Umweltcontrolling und Environmental Auditing,Schriftenreihe des IO8 W 8/92. Wien.

Kytzia S. 1995. Die O8 kobilanz als Bestandteil des be-trieblichen Informationssystems, PhD Thesis, St. Gallen.

Neitzel H. 1997. Bilanz und Perspektiven der Nutzung vonO8 kobilanzen in Politikbewertung und Umweltkennzeich-nungen, Vortrag O8 kobilanzen – Trends und Perspek-tiven, Workshop der GDCh-Fachgruppe Umwelt-chemie und O8 kotoxikologie, 1997, Frankfurt amMain.

Newton T, Harte G. 1997. Green business: technicistskitsch? Journal of Management Studies 34(1): 75–98.

Porter ME, van der Linde C. 1995. Green and competi-tive: ending the stalemate. Harvard Business Review73(5): 120–134.

Rubik F, Grotz S, Scholl G. 1996. O8 kologische Entlas-tungseffekte durch Produktokobilanzen. Landesanstalt furUmweltschutz Baden-Wurttemberg: Karlsruhe.

Schaltegger S. 1997. Economics of life cycle assessment:inefficiency of the present approach. Business Strategyand the Environment 6: 1–8.

Seuring S. 1999. Corporate Material and Energy Flow Anal-ysis – Framework, Compilation, Evaluation. SAS: Olden-burg.

Stolting P, Rubik F. 1992. U8 bersicht uber okologischeProduktbilanzen. Heidelberg.

UBA (Umweltbundesamt) (ed.). 1992. O8 kobilanzen furProdukte: Bedeutung – Sachstand – Perspektiven, UBATexte 38/92. Berlin.

Wehrmeyer W. 1995. Measuring Environmental BusinessPerformance: a Compre-hensive Guide (Business and theEnvironment Practitioner Series). Cheltenham.

Weitz KA, Todd JA, Curran MA, Malkin MJ. 1996.Streamlining life cycle assessment: considerations anda report on the state of practice. International Journal ofLCA 1(2): 79–85.

Wildavsky A. 1978. Policy analysis is what informationsystems are not. Accounting Organizations and Society3(1): 77–88.

BIOGRAPHY

Stefan A. Seuring, Dipl.-Betriebswirt, M.Sc.Chem., M.Sc. Env.M., Department of Produc-tion and the Environment, Institute for Busi-ness Administration, Faculty of Business,Economics and Law Carl-von-Ossietzky Uni-versitat Oldenburg, Birkenweg 5, 26111 Old-enburg, Germany. Tel.: +49 441 798 8310.Fax: +49 441 798 8341. Email: [email protected]

Copyright © 2001 John Wiley & Sons, Ltd and ERP Environment Eco-Mgmt. Aud. 8, 25–35 (2001)

35