clearthought bpo 6pp v4 -...

TRANSCRIPT

clearthoughtBusiness Services Insights from Clearwater International Winter 2015

Business Process OutsourcingDriven by technology, the industry is going through huge transformation

Creating valueIn its early days, the BPO industry was characterised by the ability to leverage labour arbitrage in order to reduce costs - often in an offshore call centre delivering transaction processing services. Fast forward two decades and BPO companies have moved away from commoditised low-margin service lines to focus on high value add, technology-based solutions that are delivered through collaborative working relationships between the client and service provider.

• Nearshoring continues to be a priority for offshore providers and is stimulating increasing levels of M&A activity in neighbouring regions;

• Technology is playing an ever more important role in the delivery of services. Successful BPO companies are leveraging technology to reduce costs and provide value-added services;

• Hot segments include analytics, legal process outsourcing (LPO), offshore trust administration and procurement;

• Private equity funds are driving high levels of M&A activity in the sector as portfolio companies look to acquire scale and geographic presence, as well as to build end-to-end capabilities.

CHART 1

Denmark

Finland

Germany

Netherlands

Norway

Sweden

Spain

United Kingdom

CHART 1

0% 20% 40% 60% 80% 100%

In this report, we will look at the following key themes:

Outsourcing of services per country survey

Outsourced In-houseOutsourced In-houseOutsourced In-house

SOURCE: EY

9%

19%

15%

13%

10%

9%

17%

17%

91%

81%

85%

87%

90%

91%

83%

83%

Business Services Insights from Clearwater International clearthought | Winter 2015

Market drivers

Divestment of non-core assets - Captives vs Third Party

Over the last decade, large corporates have been spinning-off their BPO assets, deeming them to be non-core divisions that do not fit the overall group strategy. The divestments reflect a growing confidence among third-party providers with specialist expertise in complex environments and which have the opportunity to focus internal resources and management bandwidth on driving core business activities. Furthermore, the sale proceeds help strengthen balance sheets or provide firepower for M&A.

Financial institutions were early adopters of low-cost offshore captives but also among the first to subsequently divest their operations. Deals included: Deutsche Bank selling its remaining 49% stake in its JV to HCL Technologies; Citigroup selling its back office unit to Tata Consultancy Services and Wipro; and UBS divesting its India Service Centre to Cognizant.

Offshoring vs Onshoring

The BPO industry’s roots are in large hubs in offshore destinations. Situated in emerging economies like China and India, leading BPO

companies have been able to draw upon comparatively cheap labour in a bid to provide cost advantages.

In addition to labour arbitrage, other factors enabling a company to service a global customer base from an overseas destination include: the lower trade barriers; better and cheaper global communications; and the increasing use of the English language.

However, faced with continued erosion of the financial advantages of labour arbitrage as well as inflation and rising property costs, certain offshore destinations are becoming increasingly expensive and therefore less attractive. Recent cost of living and salary statistics from ECA International show that wages in India are expected to grow by 10.9% during 2015 and have been growing at close to 15-20% over the last decade. This wage inflation, combined with projected real exchange rate movements, means the costs of doing business with certain offshore BPO companies is likely to rise significantly.

At the same time, global corporates are becoming increasingly dissatisfied with offshore supply chains - often led by their customer’s reaction to offshore customer support centres. That - in conjunction with reputational risks associated with communication issues, increased scrutiny on regulatory and data privacy, legal issues and the increased importance of corporate social responsibility - is resulting in BPO companies increasingly having to deliver their services domestically or from a neighbouring region, a trend that has become known as ‘reshoring’.

Over the last few years, BPO companies have been adopting multiple strategies to develop their nearshoring capabilities. For example: NASDAQ-listed Cognizant formed a partnership with Norway-based business software and services firm Visma Services to successfully win a contract with Norway Post. The deal brings together Visma’s local Norwegian accounting and regulatory expertise with Cognizant’s global delivery model and transaction processing capabilities.

• The BPO market has undergone huge transformation over the last decade and continues to demonstrate positive secular trends. Research from Gartner suggests growth is expected to continue at a modest 5-6% per annum through 2017 with some of the emerging sub-sectors growing at closer to 15%.

• However, penetration levels in the BPO industry remain very low with, on average, only 15% of services in Europe outsourced to third-party providers. Even in more mature markets with higher penetration such as the UK, Spain, Germany and Finland, BPO players are still achieving robust growth and seeing strong opportunities in existing and new service lines.

• The BPO market is one of the most resilient during an economic downturn, as companies place an increased focus on outsourcing as a means to drive cost efficiencies and flexibility.

• Talent shortages are a global issue and have impeded the speed of the economic recovery. A Manpower1 report found that, on average, 38% of employers are having difficulties with filling jobs. BPO companies are well positioned to benefit, particularly in relatively new markets such as content and data-related services where severe shortages are encouraging firms to outsource these roles.

• Emerging economies, often where BPO companies are headquartered to benefit from labour arbitrage, continue to demonstrate strong GDP growth with a fast-growing middle class and a growing number of major companies. In the light of this, BPO companies are starting to recalibrate their strategies and to place an increasing emphasis on growing their domestic customer base.

• An increasingly complex global regulatory environment, particularly in the financial services sector, has resulted in companies needing to invest considerable resources in order to manage their governance, risk and compliance. BPO companies have been quick to deliver technology-enabled solutions that efficiently handle risk and disclosure whilst delivering margin improvements. The wealth of opportunities in financial services is driving innovation and M&A activity.

• SMEs are outsourcing an increasing number of services, beyond payroll and accounts, as they look to keep pace with technological advances and reduce costs. BPO companies are delivering tailored propositions for smaller corporates, taking advantage of the maturity of the market and its proven success.

1 Manpower’s 2015 ‘Talent Shortage Survey’

Good examples include:

• Leading Indian outsourcer WNS Holdings, which was carved out of British Airways captive BPO unit by Warburg Pincus in 2002 and subsequently listed in 2006;

• Genpact, formed by General Atlantic Partners and Oak Hill Capital Partners’ acquisition of General Electric’s BPO arm, GE Capital International Services (GECIS), in 2005;

• Telefonica sold its Atento call centre business to US private equity firm Bain Capital for about ¤1bn in 2012, as it tried to preserve a coveted investment grade credit rating, and used the funds to help pay down its ¤57bn debt pile.

clearthought | Winter 2015 Business Services Insights from Clearwater International

Others are turning to M&A, recognising that acquisitions are often the fastest way to gain local market access: for example, Convergys’ purchase of Stream Global Services Inc for ¤741m enabled strong delivery capabilities for the group in Tunisia, El Salvador, the Dominican Republic, Costa Rica and Ireland.

While many corporates have reshored all or part of their BPO operations, there remains a strong case for companies to continue to outsource to offshore locations. There is a new wave of emerging markets - such as Vietnam, the Philippines and Romania – which are starting to signal their arrival on the scene. As a low-tax, business-friendly economy with a highly-skilled workforce, Ireland is also seen as being increasingly attractive.

Technology now key

Technology is playing an important role in the evolution of the BPO market, helping companies to target higher value services. The transition from the intensive human capital ‘lift and shift’ model towards technology BPO is fundamental if companies are to meet rising buyer expectations and achieve sustainable cost reductions. Incumbents that are slow to utilise technological advances and capabilities will be chasing more agile competitors.

BPO companies are using myriad technologies: while some - such as automation software - are being used to replace human involvement, others – like analytics – are helping to realised top line benefits.

M&A ActivityBPO providers are looking to acquire in fast-growing, technology-enabled service lines in order to fill gaps in their service matrices and win large, often international, tenders. High levels of M&A activity have been seen in the areas of analytics, legal process outsourcing (LPO) and procurement.

PO delivery capability(Scale, scope, technology & innovation, delivery footprint, and buyer satisfaction)

25th percentile

25th p

erce

ntile

75th percentile

75th p

erce

ntile

Mar

ket s

ucce

ss(R

even

ue, c

lient

s, a

nd g

row

th)

High

High

LowLow

Major ContendersLeaders

AspirantsAegis

HCL

Tech Mahindra

Proxima

HPWNS

HCMWorks

WiproAquanimaOptimum Procurement

Genpact Capgemini

TCS

Xchanging

Infosys

GEP

IBM

Accenture

Analytics

BPO companies are acquiring data analytics competencies in order to assist in the segregation and manipulation of their clients’ data sets thus helping to drive focus, efficiency and awareness of customer behaviour.

Legal Processing Outsourcing (LPO)

The LPO market is driven by the need to reduce costs and transform legal functions into leaner organisations. The sector is expanding rapidly due to a reliance on LPO specialists to provide litigation, property and compliance services.

Procurement

BPO companies have been aggressively targeting the procurement sub-sector due to the trend for companies to use external organisations to improve their supplier base, employ best practice and leverage the latest technologies.

Recent deal activity:

• Private equity firm Actis acquired a 30% stake in Integreon, a leading LPO and knowledge process outsourcing (KPO) firm;

• Cinven acquired CPA Global, a leading intellectual property management services provider, for a reported deal value of ¤1.34bn (£950m) - an EV/EBITDA multiple of 12.2x;

• Accenture acquired US-based Procurian, a pure-play procurement BPO company, for ¤349m ($375m). This was Accenture’s second deal in the procurement space, having previously acquired Ariba’s strategic sourcing practice.

Recent deal activity:

Procurement competitive landscape

Leaders

Major Contenders

Aspirants

Star Performers

SOURCE: Everest Group

Business Services Insights from Clearwater International clearthought | Winter 2015

Offshore trust administration

The fiduciary services market is experiencing an unprecedented level of M&A activity, led by private equity. The market remains highly fragmented but is undergoing consolidation as companies look to combat flat, home-market organic revenue growth through increasing levels of M&A.

Private equity is particularly attracted to the ‘blue chip’ heritage of many of these businesses, as well as the resilient business model with high levels of recurring revenue and strong cash conversion. Private equity funds currently holding investments in the sector include:

Investor TargetInvestment

Date Description

LDC (secondary) Equiom 2013Equiom provides a range of fiduciary, administration and management services across a variety of asset classes. The secondary buy-out facilitated the exit for Livingbridge.

CBPE Capital JTC Group 2012JTC provides corporate, fund and private client services. It has a presence in 17 locations, a global client base and over 300 employees.

Dunedin Hawksford 2008Hawksford is an independent trust company in the Channel Islands. Dunedin has supported five further bolt-ons, most recently that of Singapore-based corporate services provider Janus Corporate Solutions.

Electra PartnersElian Fiduciary Services (Jersey) Limited

2014Electra Partners acquired Elian Fiduciary Services, the fiduciary services division of the Ogier Group, for ¤253m (£180m). Elian provides trust, fund and company administration services to corporates, private clients and investment funds.

Baring Private Equity Asia (secondary)

Vistra Group 2015Baring Private Equity Asia acquired Vistra Group, a provider of company formations, trust, corporate and fund administration services, in 2015 from London-based buy-out group IK Investment Partners.

Silverfleet Capital (secondary)

IPES 2013European private equity firm Silverfleet completed the ¤70m (£50m) buy-out of IPES, a Guernsey founded international trust and corporate services provider, from RJD Partners in 2013.

BridgepointAppleby Fiduciary & Administration Business

2015Bridgepoint completed the ¤335m (£238m) acquisition of Appleby Fiduciary & Administration Business in 2015. Appleby is one of the world’s largest providers of offshore legal, fiduciary and administration services.

The Blackstone Group (secondary)

Intertrust Group Holding S.A

2012In 2012, Blackstone acquired Intertrust Group from Waterland Private Equity. Intertrust has since acquired ATC Group (ATC), a provider of fiduciary, management and administration services, from HgCapital.

Anacap PartnersFirst Names (Isle of Man) Limited

2012Formerly the International Division of IFG Group plc, First Names Group provides trust, corporate, and fund administration services.

The Carlyle GroupConifer Financial Services

2015Conifer Financial Services is a fund administrator firm which provides services for all asset classes and for hedge funds, pension funds, endowments and foundations.

Baring Private Equity (secondary)

Orangefield Group 2015Orangefield Group is a global fund administration and corporate services firm. The transaction comes a month after Orangefield Group acquired USA2Europe, a corporate services provider for technology companies.

Typically, private equity exits have either come in the form of secondary buy-outs by larger funds or trade consolidators looking to take advantage of favourable market dynamics. However, Inflexion’s recent successful IPO of Sanne Group - a global provider of fund and corporate administration services with a particular focus on alternatives - on the main market suggests a listing is a viable alternative. The group raised ¤199m (£141.6m) from the IPO - valuing the company at ¤326m (£232m), representing an EV/EBITDA multiple of around 16.0x.

Trade acquirers are also driving consolidation. One of the most high profile deals was the acquisition of listed GlobeOp Financial Services by SS&C Technologies Holdings. Other active companies include Capita, Europlan – which merged with Volaw Group - and Kleinwort Benson.

Private equity focus

Private equity groups are proving to be a credible alternative to a trade sale and are winning the race for some of the largest assets in the BPO sector.

A key factor behind this trend is the increasingly supportive nature of banks to help fund large transactions which has led to private equity groups being extremely competitive on valuation.

The BPO market has all the hallmarks of an attractive industry, namely: long term contracts, strong visibility of earnings, an asset light model, strong cash conversion and positive secular trends. Investors also see strong opportunities to scale businesses through targeted acquisitions that leverage technology. Subsequently, deals are often signed with the agreement that additional capital is available to fund future acquisitions and this is one of the key drivers of M&A activity in the sector.

Deal volume by buyer type - last 3 years

TradePE-backed TradePrivate Equity

SOURCE: CWI Analysis, Mergermarket

clearthought | Winter 2015 Business Services Insights from Clearwater International

• Bain Capital acquired a 30% equity stake in Genpact from General Atlantic and Oak Hill Capital for ¤908m (£645m), valuing the business at an EV/EBITDA multiple of 10.5x. As part of the deal, Bain promised to introduce Genpact to its portfolio companies in order to help generate new business wins. Bain has since acquired call centre businesses Atento and VXI Global Solutions.

• CVC Capital Partners acquired an 80% stake in SPi Global Holdings Inc, a provider of voice and non-voice services in the areas of knowledge process outsourcing and customer relationship management, from Philippine Long Distance Telephone Company

for approximately ¤298m ($320m). CVC has since provided additional capital to help fund the purchase of China-based Bachieve International Inc, a move that expands SPi’s delivery capabilities in the region.

• Charterhouse Capital Partners acquired a 60% stake in Webhelp from Astorg Partners and Barclays PE for approximately ¤340m. Since that deal, the company has acquired HEROtsc - the largest call-centre company in Scotland - and also made acquisitions in Germany, Italy and the Netherlands.

• Expert Global Solutions completed the ¤422m (£300m) acquisition of APAC Customer Services, a provider of customer care outsourcing solutions, for an EV/EBITDA multiple of 9.4x.

Other funds with investments in the sector include Baird Capital, which owns Accume Partners; TPG Capital, which holds a 34.5% stake in Sutherland Global Services; Cinven, which counts both Northgate Information Solutions and CPA Global as portfolio companies; and Advent International, which owns Equiniti.

Transaction multiples in the BPO sector are highly dependent on the scale of the business, niche focus and the degree of technology enablement.

Typically, for sub-¤200m deals involving customer contact management centres, we are seeing EBITDA multiples ranging from 5.5-7.5x. However, for businesses with scale, tech-enabled solutions, market-leading positions and broad geographic profiles that stretch across continents, EBITDA multiples often exceed 10x.

Companies providing vertical specific solutions or operating in emerging sub-sectors of the BPO market are attractive targets to incumbents looking to deliver end-to-end vertical solutions and

move up the value chain. These companies are often being acquired at close to double-digit multiples, as a scarcity of available assets, an overhang of private equity funds and strong trade balance sheets drive up valuations.

When it comes to assessing the valuations of technology-based businesses, like data, analytics or CRM, multiples are often quoted on a revenue rather than EBITDA basis. This is because targets often report very low or even loss making financials at the point of transacting due to the business being in its early stages of development and as such are yet to achieve the scale to cover relatively large product development and marketing costs. Typically, we are seeing revenue multiples range between 3-5x and EBITDA multiples of 12-14x.

We fully expect to see a sustained high level of M&A activity through the rest of 2015 and into 2016. The sector dynamics are positive with both trade and private equity acquirers showing a strong appetite for domestic and cross-border transactions.

M&A activity will continue to be underpinned by BPO companies and private equity backed platforms looking to extend their reach in emerging markets, build nearshore hubs, and make the transition to technology-enabled, high value-added services.

In a market experiencing rapid change, the winners will be those who have the ability and confidence to grow with their clients’ demands.

Conclusion

Acquirer Contax Capita plc ConvergysOne Equity

PartnersBain Capital Bain Capital Serco Group plc

TargetAllus BPO

CenterAvocis AG

Stream Global Services Inc

APAC Customer Services

30% Genpact Atento S.A. Intelenet

Country

Enterprise Value (¤m)

182 210 682 416 2,875 1,051 569

Year 2011 2015 2014 2011 2012 2012 2011

6.7x 6.8x 8.4x 9.4x 10.5x 10.7x 10.8x

LTM EV/EBITDA multiples

Recent deal activity:

Attractive multiples

Business Services Insights from Clearwater International clearthought | Winter 2015

AARHUS • BARCELONA • BEIJING • BIRMINGHAM • COPENHAGEN • DUBLINLISBON • LONDON • MADRID • MANCHESTER • NOTTINGHAM • PORTO • SHANGHAI

www.clearwaterinternational.com

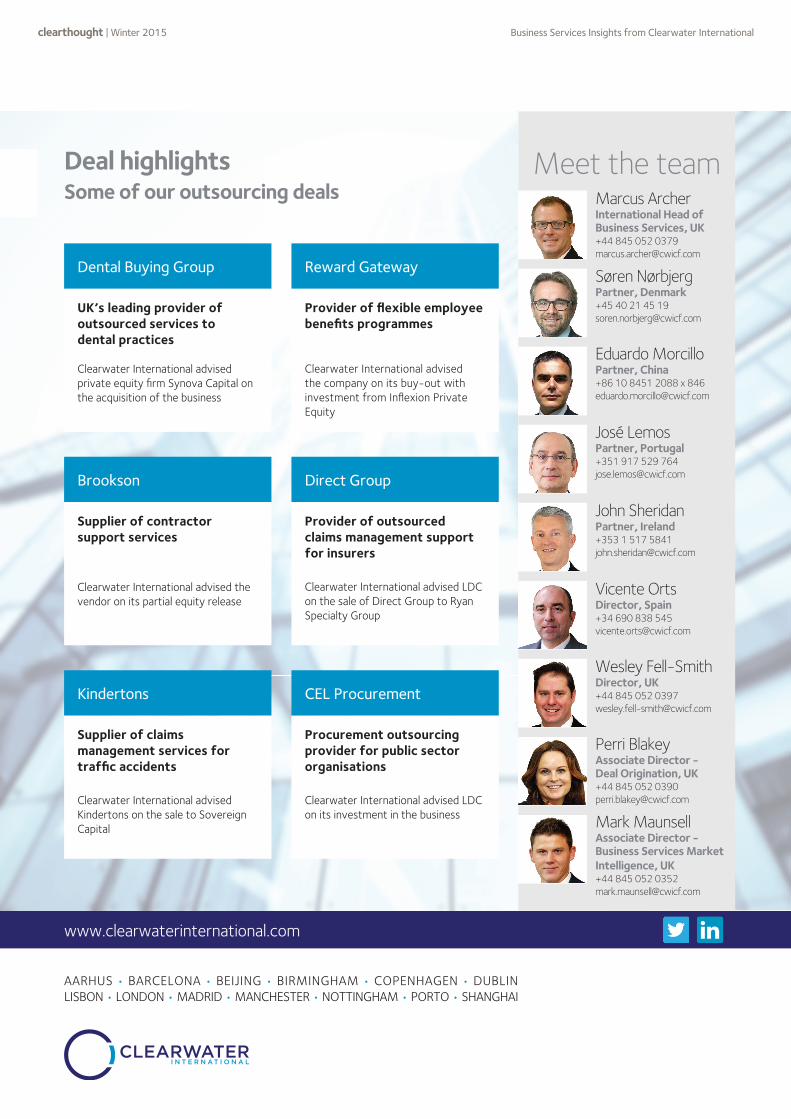

Deal highlightsSome of our outsourcing deals Marcus Archer

International Head of Business Services, UK+44 845 052 [email protected]

Søren NørbjergPartner, Denmark+45 40 21 45 [email protected]

Eduardo MorcilloPartner, China+86 10 8451 2088 x [email protected]

José LemosPartner, Portugal+351 917 529 [email protected]

John SheridanPartner, Ireland+353 1 517 [email protected]

Vicente OrtsDirector, Spain+34 690 838 [email protected]

Wesley Fell-SmithDirector, UK+44 845 052 [email protected]

Perri BlakeyAssociate Director - Deal Origination, UK+44 845 052 [email protected]

Mark MaunsellAssociate Director - Business Services Market Intelligence, UK+44 845 052 [email protected]

Meet the team

UK’s leading provider of outsourced services to dental practices

Clearwater International advised private equity fi rm Synova Capital on the acquisition of the business

Dental Buying Group

Provider of fl exible employee benefi ts programmes

Clearwater International advised the company on its buy-out with investment from Infl exion Private Equity

Reward Gateway

Supplier of claims management services for traffi c accidents

Clearwater International advised Kindertons on the sale to Sovereign Capital

Kindertons

Procurement outsourcing provider for public sector organisations

Clearwater International advised LDC on its investment in the business

CEL Procurement

Supplier of contractor support services

Clearwater International advised the vendor on its partial equity release

Brookson

Provider of outsourced claims management support for insurers

Clearwater International advised LDC on the sale of Direct Group to Ryan Specialty Group

Direct Group