cloud computing markets and key drivers study

TRANSCRIPT

CloudServices

MarketsandKeyDriversStudy

IqbalKhan,July2015

1

CONTENTS:• CloudlandscapeinIndia

• IndiakeydevelopmentsandTrends• IndiaCloudReadiness• IndiaLocalCloudProviders• IndiaGlobalCloudServiceProviders• IndiaKeyCoudDrivers,Barriers• IndiaManagedServicesDriversandBarriers

• KeyCustomersegmentsandsomesuccessstories• Media• Telecom• Travel/Hospitality• Manufacturing• Healthcare

• TheSMESegment• CompePtors/TheirCustomersandsize/TheirOfferingsUSP• CloudGlobalMarketLandscapeathighlevel• SoluPonandValuesellingratherthanPrice-basedselling• KeyCustomerChallengesandBenefits• CloudDecisionMakingStakeholdersandtheirroles• IntelligenPaLearningssofar• RecommendaPonsandAcPonPlan–Howtomoveforward

2

CONTENTS:• CloudlandscapeinIndia

• IndiakeydevelopmentsandTrends• IndiaCloudReadiness• IndiaLocalCloudProviders• IndiaGlobalCloudServiceProviders• IndiaKeyCoudDrivers,Barriers• IndiaManagedServicesDriversandBarriers

• KeyCustomersegmentsandsomesuccessstories• Media• Telecom• Travel/Hospitality• Manufacturing• Healthcare

• TheSMESegment• CompePtors/TheirCustomersandsize/TheirOfferingsUSP• CloudGlobalMarketLandscapeathighlevel• SoluPonandValuesellingratherthanPrice-basedselling• KeyCustomerChallengesandBenefits• CloudDecisionMakingStakeholdersandtheirroles• RecommendaPonsandAcPonPlan–Howtomoveforward

3

4

CloudLandscapeInIndia

IndiaCloudCompuPngSpending

• BMIesPmatestheoverallIndiancloudcompuPngmarketatatotalvalueofINR42.7bnandisforecasttogrowataCAGRof35.9%

• 2015-2019toreachINR194.3bninthefinalyearoftheforecast.

Source:BMI–IndiaInforma3onTechnologyReport

CloudAdopPonWillDrivetheGrowthIndia’sITMarket

• AreportpublishedbyITresearchandadvisoryfirmGartneresPmatesthatinIndiaalonethemarketforcloud-basedserviceswillrisebyathirdto$557millionthisyear,andmorethantripleby2018.

• TotalcloudmarketinIndiatogrowat45%CAGRto$14.8billion

• CloudcontribuPontoITspendtoriseto17%ofoverallmarketby2020.

• PubliccloudmarketinIndiais$700-800millionin2015andwillriseto$7.0-7.4billionin2020

• PrivatecloudmarketinIndiais$1.6-1.8billionin2015andwillriseto$7.4-7.6billionin2020.

• Government,BFSI,educaPon,healthcareandtelecomtobekeygrowthverPcals.

6~Zinnov

hhp://goo.gl/ctmc88

ImpactofServerVirtualizaPon

• ServervirtualizaPonallowsformulPpleoperaPngsystemstoberunconcurrentlyonasinglecomputerandononephysicalserver,therebyhelpingsubstanPallycutoperaPngcosts.

• InAugust2013itwasesPmatedthatservervirtualizaPoncouldhelpIndiancompaniessaveasmuchasUSD3.89bnby2020.

• Oftheprojectedsavings,USD2.37bnwouldbederivedfromlowerspendonserversthemselves,USD666mnwouldbederivedfromlowercostsforpoweringandcoolingtheserversandUSD827mnwouldbederivedfromstaffandadministraPvecostsassociatedwithrunningtheservers.

AstudybyIDCen3tledVision2020

CloudServicesandpotenPaltargets

• ISV(independentso1warevendor)isthedriverforcloudadopPon• ISVsplayaverycriPcalroleandcurrentlythereisalotofinvestmentbeingdoneindeveloping

cloudexperPse.• TheInherentadvantagesofflexibilityandriskmiPgaPon,cloudhasbecomeanessenPalpartof

ourserviceofferings.• ISVsneedtodevelopexperPseincloudtechnologyifwewanttoretainandgrowourcustomer

base.• Companiesthatareinterestedinadop8ngcloudlikeTataCommunica8ons,BajajAllianz.• TheIndiancompaniesshouldtargettheSMEsandgovernmentbasedprojectsastheyare

goingtobekeydriversofrevenueinthefuture.

~SudhirMurthy,Manager-SeniorArchitectCloudServices,WiproIndia

8

hhp://goo.gl/dLQPo4

IndiaKeyTrendsandDevelopment• April2015itwasreportedthatMicroso1andIndia-basedZohowouldsetupdatacentersinIndiatocatertothehuge

demandforcloud-basedservicesinthecountry.• ThestepwillhelpthemofferquickeraccesstodatafromlocalserversandalsomeetfutureregulaPonstohavelocal

serversfore-governanceiniPaPvesonthecloud.• Microso1intendstoestablishthreedatacentersinthecountrybyend-2015toprovideAzureandOffice365services

fromlocaldatacenters.• Zoho,ontheotherhand,isplanningtoinvestUSD1mninestablishingthedatacentreandaimstogrowitsdomesPc

andgovernmentbusinessesthroughit.• Meanwhile,inMay2015IBMwasreportedtobeconsideringopeningitsseconddatacentreinIndia.Thedatacentre

willenablethecompanytoaddressthedemandfromvarioussectorssuchasgovernmentandfinancialservices.• APACvendorsarealsotargePngIndia,forinstance,inApril2015NTTCommunica8ons(NTTCom)announcedits'India

BusinessStrategy',underwhichthecompanyplanstoconPnueitsinvestmentinandexpansionofhigh-qualitydatacentre/cloudservicesandinternaPonalnetworkservicesbasedonitsservicestrategy'GlobalCloudVision’.

• AddiPonally,NTTComannounceditsintenPontoopenanewUSD100mndatacentreintheIndiancityofMumbaiwithaninvestmentofmorethanUSD100mn.TheconstrucPonofthecentrewillbeundertakenbyNTTCom'ssubsidiaryNetmagic.Thefacility,whichisscheduledtobecomeoperaPonalfromQ315,willbeNTTCom'sninthdatacentreinIndia.

IndiaCloudReadiness

• ThesignificantchallengesoftheIndiancloudcompuPngenvironmentarecapturedintheresultsofthe2014CloudReadinessIndex,inwhichIndiaonlyscoredaheadofVietnamandwasfarbehindtheregionalleaderssuchasJapan(seeaccompanyingchartbelow).

• Indiascoredrela8velystronglyinthefreedomofinforma8onanddatasovereigntycategories,aproductofitspoliPcalandlegalsystem.Meanwhile,intermsofbusinesssophisPcaPon,thelargeoutsourcingindustry,aswellasfinancialservices,presentupsideforcloudvendors.

• However,India'sscoreisheldbackbyconcernsthatBMIhashighlightedforseveralyears,namelythepoorqualityofbroadbandinfrastructureandinsufficientinternaPonalbandwidth.

• IndiaisaregionallaggardintermsofbroadbandinfrastructureinvestmentandwedonotexpectIndiatoclosethegaptoitspeers,atleastinthemediumterm.

• Thisnetworkinfrastructuredeficitwillpushupcloudcompu8ngcostsforvendorsandend-usersandactasadragonadopPonandmarketvaluegrowth.

• Nonetheless,thesheersizeoftheIndianmarketandpoten8alforcloudadop8onwhereon-premisesdeploymentshavemuchlowerpenetraPon,hasbeensufficienttoahractvendorinterest.

CloudReadinessIndex

LocalCloudProvidersandISPsBSNL• InMay2013,telecomsoperatorBSNLandDimensionDatalaunchedjointcloudservicesinIndia.TheserviceisbasedonDimension

Data'sManagedCloudPlaqormandBSNL'senterprisecloudservicesviaitsdatacentres.Theserviceisbasedonstandardisedarchitectureandisabletosupportpublic,privateandhybridcloudmodels.Thepartnershipalreadyhas15majorclientsandistargetedatlargeenterprises,SMEsandgovernment,withBSNLstaPngthatthepublic-privatepartnershipwillbesuitableforIaaSprovisionatstateandcentralgovernmentleveltostrengthene-governmentiniPaPves.

• InlaunchingsixnewdatacentresatthesamePme,BSNLismakingaclearsteptowardsitsservices-centricstrategy.ThecompanyhasinvestedaroundINR2bninitsnewdatacentres,showingastrongcommitmenttodataservices.

• ThesixdatacentresarelocatedinMumbai,Faridabad,Ahmedabad,Jaipur,LudhianaandGhaziabad.RelianceJioInfocomm• InJune2014,RelianceJioInfocomm,asubsidiaryofIndia-basedRelianceIndustries,announcedplanstoestablish14datacentres

acrossIndia.• Themoveisinlinewiththecompany'seffortstocreateacloudcompuPnginfrastructure,whichwillenabletheoperatortoservethe

healthcare,educa8onandentertainmentsectors.• Thesedatacentreswillallowthecompanytoofferservices,includingdirect-tohometelevision,video-on-demand,mailingand

messagingservicesandvoiceoverinternettelephony.• InaddiPon,thecentreswillaidthecompanyinsynergisingtheshoppingandcontentbusinessesofNetwork18.CtrlS• DespiteincreasedcompePPonfromgloballeaders,investmentfromlocalvendorsconPnuedinH214,withIndia-baseddatacentre

providerCtrlSDataCentersannouncingplansinNovember2014toinjectINR6.26bn(USD101.23mn)intotheconstruc8onoftwonewdatacentresinChennaiandBengaluru.

Bhar8Airtel,Sify,TrimaxandNetMagicareinvesPnginbandwidthandfaciliPestosupportnewcloudserviceofferings.

ChallengesfacedbyLocalPlayers

• However,smallerIndianproviderscouldul8matelybesqueezedouttothemarginsofthemarketasglobalgiantstargetmarketshareratherthanprofitability-atleastintheshort-to-mediumterm.

• OnestrategyforlocalcloudvendorsistotargetlessahracPveopportuniPeswherecompePPonislessintense.

• 2ndopPonisfortheseplayerstogetacquiredbyGlobalplayers

GlobalCloudServiceProvidersAWS• AWSplanstostartitsdatacenterinIndiainyear2016• GlobalIaaSmarketleaderAmazonWebServices(AWS)wasalsoreportedtobeuppingitsfocusonIndiainH214.• InOctober2014,CEOJeffBezosstatedthatAmazonmayestablishadatacentreinIndiaandthatthefirmwasevaluaPngtheviabilityofsuchastepthroughwhichit

aimstocapitaliseongrowingcloud-basedopportuniPesinIndia.• ItwasreportedAWSisconsideringthemoveinresponsetotheinvestmentbyothercloudproviderrivalssuchasGoogle,IBMandMicroso1.• AWS'strategybecameclearerinMarch2015whenitsignedadealforIndiantelecomsoperatorBhar8AirteltoprovideAWScloudcompu8ngservicesto

customersinIndia.• Undertheagreement,customerswillreceiveadedicatedconnecPonbetweentheirpremisesandAWSdatacentres.AdirectconnecPontotheAWSdatacentreswill

lowernetworkcosts,offerhigherbandwidththroughputandprovideamoreconsistentnetworkexperience,whichwillhelpbusinessesofallsizesrapidlyexpandtheirorganisaPons.

Microso1• MicrosorinNovember2014reportedplanstoinvestINR14bn(USD227mn)toestablishthreeclouddatacentresintheIndianciPesofMumbai,PuneandChennai-

withthethreecentresexpectedtobeoperaPonalbyYE15.• MicrosorintendstocapturetheIndiancloudmarket,especiallyinthebankingandtelecomindustriesthroughitsdomesPcdatacentredeploymentproject.• Thedecisionforofferingcloudservicesfromlocaldatacentrescamearerthecompanyrecordeda100%riseinitscloudbusinessinthecountryduring2013,according

toCEOSatyaNadella.MicrosorregisteredrevenuesofINR22.61bn(USD366.75mn)fromIndianoperaPonsinFY2013/14.• Microso1hasabroadcloudstrategyinIndia,butisalsotargePngspecificopportuniPeswithtailorediniPaPves.InMay2015,MicrosorintroducedEdu-Cloud,a

cloud-basedsoluPonthatcombinesadigitallearningplaqormforteachersandstudentsandsorwaresoluPonsforK-12schoolsinIndia.• ThecompanysignedadealwithSriChaitanyaSchools,achainofeducaPonalinsPtuPonswithnetworksintheIndianstatesofAndhraPradeshandTelangana,forthe

offering.Edu-Cloudwillprovideenterpriseresourceplanning,SISsolu8onsandadigitallibraryserviceoncloudfortheins8tute,inaddiPontovirtuallearningplaqormandteachertraining.Microsor'sgrowthtargetistoreach1,500insPtuPonsand6,000,000studentswithEdu-CloudinIndiabyYE16.

GlobalCloudServiceProvidersIBM• IBMreportedamorebullishoutlookforcloudservicegrowthinMarch2014.IBMseesanupwardtrendforadopPonofcloudcompuPnginIndia• EstablisheditsfirstclouddatacentreinAiroli,ontheoutskirtsofMumbai,inthestateofMaharashtra,India.Thenewfacilitywillbededicatedtowardsprivate

cloudservicescateringtoenterprisesandsmallandmediumbusinesses.Google• InApril2015,GooglesignedapartnershipdealwithUK-basedconsulPngfirmPricewaterhouseCoopers(PwC)fortheDigitalIndiainiPaPveandlarge

enterprisedealsinIndia.TheIndianpartnershipisanextensionofaglobaldealsignedinOctober2014.• Withtheagreement,Googleaimstopushitselfintolargee-governanceprojectsandimprovesalesforitscloudservicesintheAsiancountry.InaddiPonto

opportuniPesderivedfromgovernmentandpublicsectorcompanies,GoogleandPwCaretargePngindustryverPcalsincludingfinancialservices,retail,pharmaceu8calsandhealthcare.

VMWare• InMarch2015USvendorVMwareannouncedtheintroducPonofthehyper-convergedEVO:RAIL• infrastructureapplianceforIndia.TheaimoftheinfrastructureapplianceistohelpITfirmsstreamlineanddramaPcallysimplifyinstallaPonandscaling-outof

sorware-definedITinfrastructure.• VMwarejoinedhandswithFujitsu,HitachiDataSystemsandNetAppforEVO:RAIL.BT• UK-basedtelecomsoperatorBTannouncedthelaunchofitsCloudComputerserviceinIndiainFebruary2014.• TheinformaPonmanagementserviceoffersbusinessesa'payasyougo'cloudsoluPonwithhighqualityandsecuritythatpromisescostsavingsofupto40%.• BT'sCloudComputeserviceiscurrentlyavailablein17countriesacrossfourconPnents.NTTCom• APACvendorsarealsotargePngIndia,forinstance,inApril2015NTTCommunicaPons(NTTCom)announcedits'IndiaBusinessStrategy',underwhichthe

companyplanstoconPnueitsinvestmentinandexpansionofhigh-qualitydatacentre/cloudservicesandinternaPonalnetworkservicesbasedonitsservicestrategy'GlobalCloudVision'.

• AddiPonally,NTTComannounceditsintenPontoopenanewUSD100mndatacentreintheIndiancityofMumbaiwithaninvestmentofmorethanUSD100mn.TheconstrucPonofthecentrewillbeundertakenbyNTTCom'ssubsidiaryNetmagic.

• Thefacility,whichisscheduledtobecomeoperaPonalfromQ315,willbeNTTCom'sninthdatacentreinIndia.

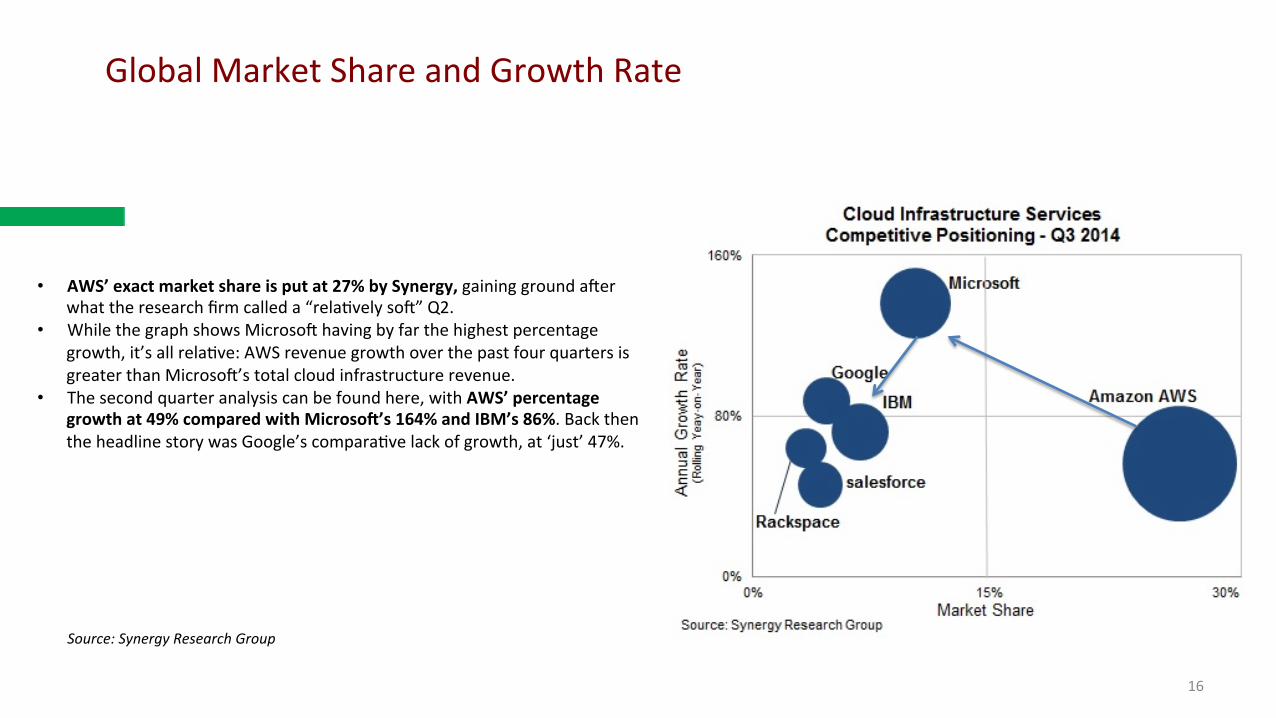

GlobalMarketShareandGrowthRate

16

• AWS’exactmarketshareisputat27%bySynergy,gaininggroundarerwhattheresearchfirmcalleda“relaPvelysor”Q2.

• WhilethegraphshowsMicrosorhavingbyfarthehighestpercentagegrowth,it’sallrelaPve:AWSrevenuegrowthoverthepastfourquartersisgreaterthanMicrosor’stotalcloudinfrastructurerevenue.

• Thesecondquarteranalysiscanbefoundhere,withAWS’percentagegrowthat49%comparedwithMicroso1’s164%andIBM’s86%.BackthentheheadlinestorywasGoogle’scomparaPvelackofgrowth,at‘just’47%.

Source:SynergyResearchGroup

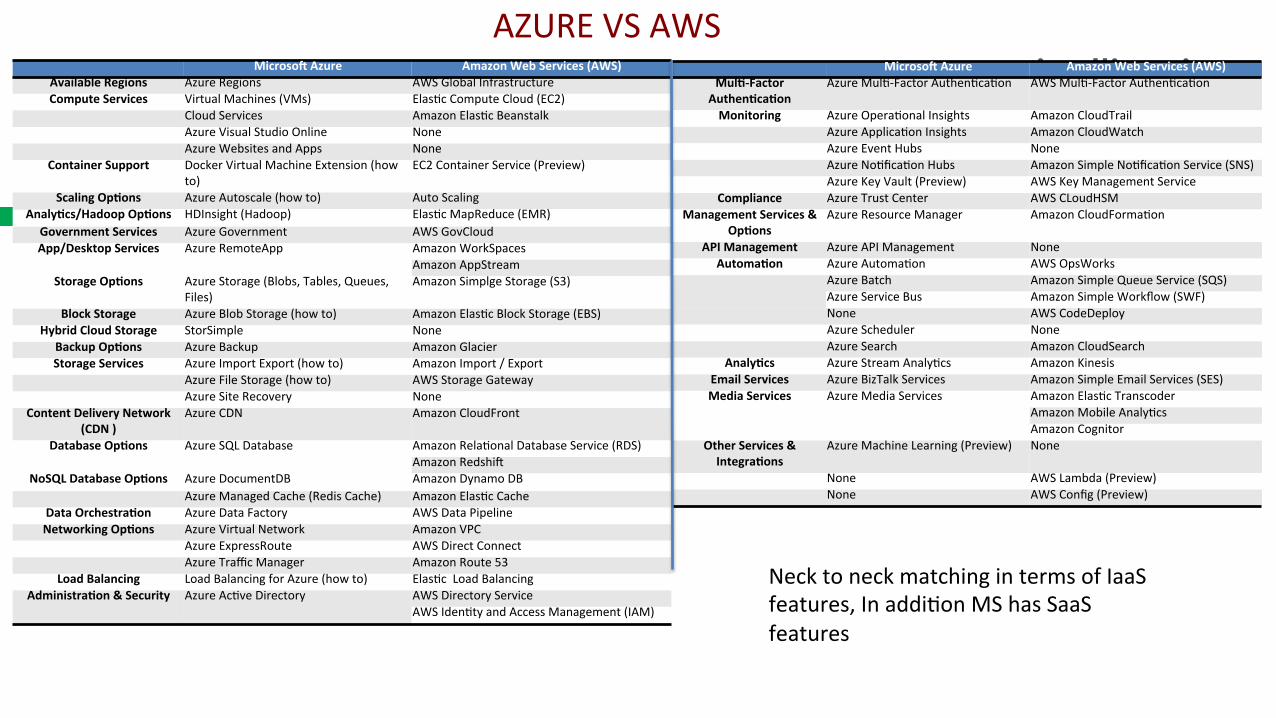

AZUREVSAWSMicroso1Azure AmazonWebServices(AWS)

AvailableRegions AzureRegions AWSGlobalInfrastructureComputeServices VirtualMachines(VMs) ElasPcComputeCloud(EC2)

CloudServices AmazonElasPcBeanstalkAzureVisualStudioOnline NoneAzureWebsitesandApps None

ContainerSupport DockerVirtualMachineExtension(howto)

EC2ContainerService(Preview)

ScalingOp8ons AzureAutoscale(howto) AutoScalingAnaly8cs/HadoopOp8ons HDInsight(Hadoop) ElasPcMapReduce(EMR)

GovernmentServices AzureGovernment AWSGovCloudApp/DesktopServices AzureRemoteApp AmazonWorkSpaces

AmazonAppStreamStorageOp8ons AzureStorage(Blobs,Tables,Queues,

Files)AmazonSimplgeStorage(S3)

BlockStorage AzureBlobStorage(howto) AmazonElasPcBlockStorage(EBS)HybridCloudStorage StorSimple None

BackupOp8ons AzureBackup AmazonGlacierStorageServices AzureImportExport(howto) AmazonImport/Export

AzureFileStorage(howto) AWSStorageGatewayAzureSiteRecovery None

ContentDeliveryNetwork(CDN)

AzureCDN AmazonCloudFront

DatabaseOp8ons AzureSQLDatabase AmazonRelaPonalDatabaseService(RDS)AmazonRedshir

NoSQLDatabaseOp8ons AzureDocumentDB AmazonDynamoDBAzureManagedCache(RedisCache) AmazonElasPcCache

DataOrchestra8on AzureDataFactory AWSDataPipelineNetworkingOp8ons AzureVirtualNetwork AmazonVPC

AzureExpressRoute AWSDirectConnectAzureTrafficManager AmazonRoute53

LoadBalancing LoadBalancingforAzure(howto) ElasPcLoadBalancingAdministra8on&Security AzureAcPveDirectory AWSDirectoryService

AWSIdenPtyandAccessManagement(IAM)

Microso1Azure AmazonWebServices(AWS)Mul8-Factor

Authen8ca8onAzureMulP-FactorAuthenPcaPon AWSMulP-FactorAuthenPcaPon

Monitoring AzureOperaPonalInsights AmazonCloudTrailAzureApplicaPonInsights AmazonCloudWatchAzureEventHubs NoneAzureNoPficaPonHubs AmazonSimpleNoPficaPonService(SNS)AzureKeyVault(Preview) AWSKeyManagementService

Compliance AzureTrustCenter AWSCLoudHSMManagementServices&

Op8onsAzureResourceManager AmazonCloudFormaPon

APIManagement AzureAPIManagement NoneAutoma8on AzureAutomaPon AWSOpsWorks

AzureBatch AmazonSimpleQueueService(SQS)AzureServiceBus AmazonSimpleWorkflow(SWF)None AWSCodeDeployAzureScheduler NoneAzureSearch AmazonCloudSearch

Analy8cs AzureStreamAnalyPcs AmazonKinesisEmailServices AzureBizTalkServices AmazonSimpleEmailServices(SES)MediaServices AzureMediaServices AmazonElasPcTranscoder

AmazonMobileAnalyPcsAmazonCognitor

OtherServices&Integra8ons

AzureMachineLearning(Preview) None

None AWSLambda(Preview)None AWSConfig(Preview)

NecktoneckmatchingintermsofIaaSfeatures,InaddiPonMShasSaaSfeatures

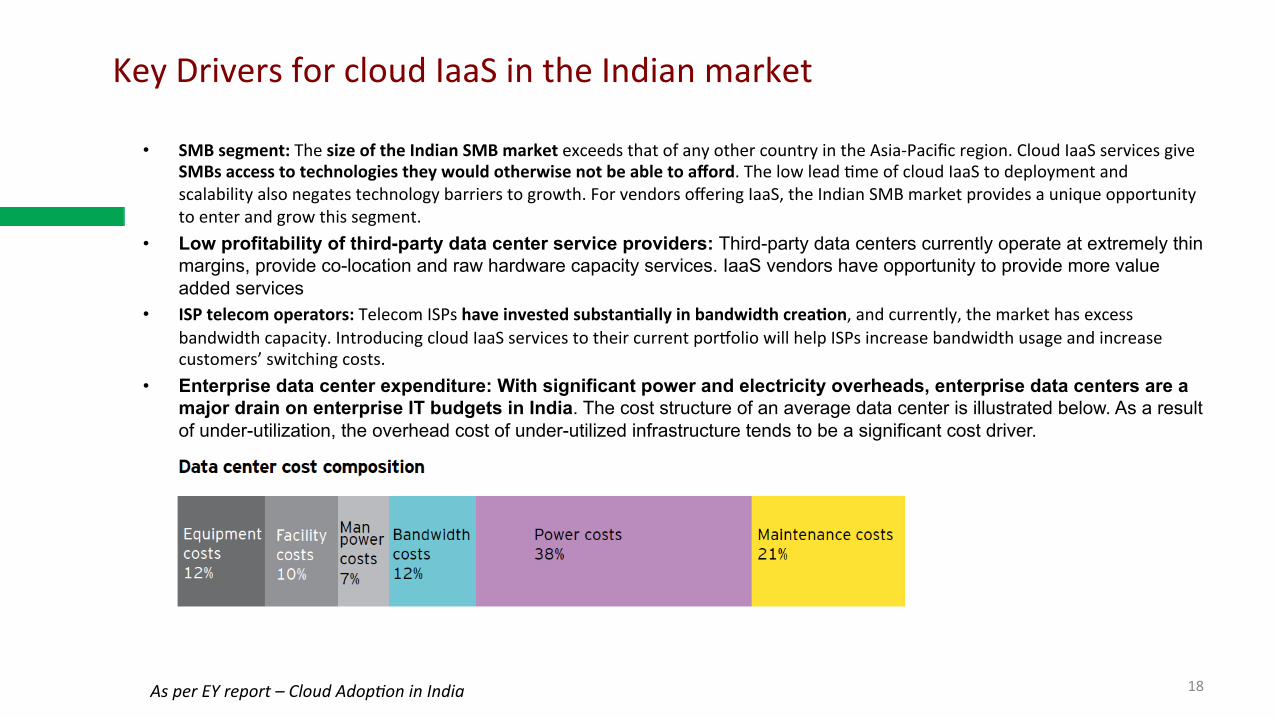

KeyDriversforcloudIaaSintheIndianmarket

• SMBsegment:ThesizeoftheIndianSMBmarketexceedsthatofanyothercountryintheAsia-Pacificregion.CloudIaaSservicesgiveSMBsaccesstotechnologiestheywouldotherwisenotbeabletoafford.ThelowleadPmeofcloudIaaStodeploymentandscalabilityalsonegatestechnologybarrierstogrowth.ForvendorsofferingIaaS,theIndianSMBmarketprovidesauniqueopportunitytoenterandgrowthissegment.

• Low profitability of third-party data center service providers: Third-party data centers currently operate at extremely thin margins, provide co-location and raw hardware capacity services. IaaS vendors have opportunity to provide more value added services

• ISPtelecomoperators:TelecomISPshaveinvestedsubstan8allyinbandwidthcrea8on,andcurrently,themarkethasexcessbandwidthcapacity.IntroducingcloudIaaSservicestotheircurrentporqoliowillhelpISPsincreasebandwidthusageandincreasecustomers’switchingcosts.

• Enterprise data center expenditure: With significant power and electricity overheads, enterprise data centers are a major drain on enterprise IT budgets in India. The cost structure of an average data center is illustrated below. As a result of under-utilization, the overhead cost of under-utilized infrastructure tends to be a significant cost driver.

18AsperEYreport–CloudAdop3oninIndia

KeyBarriersforCloudAdopPon

CloudAdapPoninIndiahasbeenontherisespeciallyinthenewageeconomyandStart-ups,CustomersarewakinguptoquesPonsaroundScalability,Infracost,TCOetc.Majorhindranceandroadblocks• DataSecurityandPrivacy,IntegraPonwithexisPngOnPremiseSystemsandSecurity• LackofverPcal/sectorExperPse• Legalandregulatorycompliance• DataCenters(AWS)residingoutofthecountry,whichlimitsadopPoninBFSI,ResistanceinFinancialSector• EcosystemMaturityTheIndiaIaaSecosystemissPllinnascentstages–Thisisanopportunityaswell,wehaveblue

oceans• Customerawareness-CustomersNotawareofitsoverallimpactandthereturnoninvestment(ROI)thatadopPng

suchtechnologiescanyield.AlsoNotawareofthespecificservicesthatvendorsinthisspaceoffer.• ConnecPvity:PoorconnecPvitymayprovetobeasignificantbarriertoadopPon.LowinternetandPCpenetraPon

(lessthan1%inurbanareas,31PCsper1,000,accordingtoNASSCOM’sreport,PerspecPve2020)arediscouraging

19

KeyDriversforManagedServicesProviders

• Needtocontrolcosts.CostpressuresaredrivingtheadopPonofmanagedanddatacenterservices.Thedemandwillgrowatahigherrateassmallandmedium-sizedfirmsalsorealizethebenefitofuPlizingITsystemsonanopexmodel.

• Focusoncorebusiness.DuetotheincreasedcompePPonandwithITinfrastructurebecomingmorecomplexanddemanding,manyorganizaPonsarefindingitdifficulttomanagetheirinfrastructurethemselves,andarethusoutsourcingthetasktovariousmanagedserviceproviders(MSPs),helpingthemfocusontheircorebusinessinsteadofworryingaboutIT.

• Growthofhos8ngproviders.DuetoastrongfocusofnewtelecomserviceprovidersonthedeliveryofhosPngservices,parPcularlyforthehosPngofapplicaPonssuchasenterpriseresourceplanning(ERP),customerrelaPonshipmanagement(CRM),andothers,therewouldbeopportuniPesforITservicesvendorsintheareasofprovidingwhite-labeledservicestothetelecomserviceproviders.

• Riskmi8ga8ons.Managedservicesprovidersdonotprovidesupportonlyintheeventofanemergencyorrecoverybutalsoprovidemonitoring,whichcanbeinvaluableinpreven8ngproblemsbeforetheycanhaveanimpactonthebusiness.ProacPveandremotemonitoringleadstotheearlyidenPficaPonofanyissuesandcanfixthemorenbeforeweevenknowthereisaproblem.AutomaPctriggersthatrangefromlowtonercartridgestodwindlingdiskspacetoapotenPalserverfailurearesetuptoidenPfyanyproblembeforeitaffectsourbusiness.

20IDC:IndiaManagedServices2013MarketAnalysisand2014–2018Forecast

KeyInhibitorsforManagedServicesProviders

• InternalResistancebytheITmanagers• Lossofcontrol.ITmanagershaveclearconcernsabouthandingovertheirsystemsandapplicaPonstoathirdparty,whichmaynot

necessarilyhaveadeepunderstandingoftheirsystems.AcommonbeliefamongorganizaPonsisthatoncetheirsystemsareoutsourced,theydonothavecontroloverthem.

• Lackofver8cal/sectorexper8se.IndiaorganizaPons—specificallyinsectorsthatdealwithintensivedatavolumeandhavecomplexbusinessprocesses(suchastransportaPon,uPliPes,andothers)—believethatserviceproviderslackver8calexper8seandfailtounderstandthecomplicatedbusinessprocessesandapplica8onsrunningtheseprocesses,whichisessenPal.Thepartners'lackofunderstandingofsuchapplicaPonslimitstheengagementscope.OrganizaPonshavestartedadopPngan80:20modelwhenitcomestooutsourcingthemanagementofapplicaPons,whichessenPallymeans80%ofthenoncriPcalapplicaPonsareoutsourcedand20%ofthebusiness-criPcalapplicaPonsaremanagedin-house.

• Datasecurity.Thelackoftrustthatanorganiza8onwilllosecontroloveritsdataandsystemishinderingthegrowthofmanagedservices.FearaboutlosingconfidenPaldataisamajorconcernamongorganizaPonscontemplaPngtoadoptmanagedservices.

• Cloudservicesadop8on.ThoughtheimpactofthisinhibitoristhusfarlimitedinIndia,itisexpectedtobecomemorepronouncedinthenextfewyears.Asorganiza8onsbecomecomfortablewithandmoreeducatedaboutcloudtechnology,adop8onwillincrease.Insomecases,organizaPonsare"leapfrogging"managedservicesdirectlytoacloudengagement.ThisisespeciallyevidentintheSMBsegment,wheretherearemanyeconomicalcloudtoolssuchasGmailandDropboxbeingused.IDCexpectsthatsuchtoolswillgaintracPoninthelargeenterprisesegmentaswell.SaaSwill,forexample,takemarketsharefromhostedapplicaPonmanagementservices

21IDC:IndiaManagedServices2013MarketAnalysisand2014–2018Forecast

KeyTakeawaysfromMarketOverview

• HugeopportunityintheIndiamarket,goodpotenPalintheSMBSegment• ShoulduPlizetheKeyDriversandOvercometheBarriersinOurValue

ProposiPoni.eEducatethecustomerson– Cloud,itsbenefits,CapextoOpexetc– UsecaseswithROI– DataPrivacyandSecurity– TransparencyofInfrausage– Hybridinfrastructuremodels– Legalcompliances

• DevelopverPcalexperPsee.ginMediaorHealthcare• TargettosupportCloudservicesprovidersinthisorder

1. AWS2. MSAzure3. IBMCloud4. GoogleCloud

22

23

CloudMajorCustomerSegments

CloudManagedServicesMarketSegmentsCloudManagedServicesmarketissegmentedby:

• Type:• BusinessServices• DataCentreServices• NetworkServices• MobilityServices• SecurityServices

• Ver8cals:Banking• FinancialServicesandInsurance(BFSI)• Telecom&IT• Retail• Government&PublicSector• Healthcare• Manufacturing• Energy&uPliPes• Others(EducaPon,Media&Entertainment,Travel&

Hospitality,TransportaPonandLogisPcs)

24hhp://goo.gl/rRRr8C(GartneridenPfiesadopPonofcloudcompuPnginIndia)

• BasedonSize• SME• Enterprise

• BasedonRegions:• NorthAmerica• APAC• Europe• LaPnAmerica• MEA

25

IndustryVerPcals

26

MediaIndustry

FeaturesofMediaCompanies

• AsmediacompanieslookatwaystoreducetheirITexpenditureandmaximizetheirreturnsoninvestmentsrela8ngtoIT,cloudcompuPngadopPonisgainingtracPonascompaniesrecognizethemulPtudeofbenefitsthatitcanpotenPallyoffer.

• Inordertosource,deliver,andmanagegrowingvolumesofinformaPonandreducetheirinfrastructureandsorwarelicensecosts,mediacompaniessuchascableandbroadcastfirms,andproducPoncompaniesareconPnuouslylookingtoadopttheon-demandcloudservicesmodel.Asaresult,52%,48%,and48%ofmediacompaniesareplanningtoinvestinSaaS,IaaS,andPaaSrespec8vely,throughtotheendof2015

• Hybridcloudisincreasinglypreferredinmediacompanies,asitfacilitatesthebestofbothpublicandprivatecloud,therebygivingcompaniesmuchneededflexibilityinhosPngtheirhugeandvariedcontentandworkloads.

27

CloudcompuPng–vendormindshareamongmediacompanies

28

• Googlehasthehighestvendormindshareof39%,closelyfollowedbyMicrosor,as32%ofrespondentsareselecPngthiscompanyasoneoftheleadingplayersinthecloudcompuPngdomain.

• MediacompaniescanbenefitfromGoogleCloudDataflow,whichanalyzeslivedata,poten8allygivinguserstheabilitytoviewtrendsandkeepthemalertedtoeventsastheyhappen,therebyprovidingreal-8mebusinessanalysis.

• MicrosorofferingsincludeWindowsServerwithHyper-V,SystemCenter,WindowsAzure,andOffice365.

• WindowsAzureMediaServices,acloud-basedPaaSsoluPonthatenablesmediacompaniestobuildanddelivermediasoluPonstocustomersefficiently.

• Microsorhasbuiltvarietyofcustom-buildservicesthatenablesthespeedieradop8on,encoding,format-conversion,storage,contentprotec8on,andstreamingofbothliveandon-demandvideo.Thecompanyhasacquiredthecloud-compuPngcompanyGreenBuhon,whichallowsmediafirmsthatrequirehugeamountsofcompuPngpowertouseexisPngintegraPonswithcloudandrunperformance-intensiveworkloads.

29

Travel/Hospitality

CaseStudy:redBus

• redBusisanIndiantravelagencythatspecializesinbustravelthroughoutIndiabysellingbusPcketsthroughoutthecountry.Ticketsarepurchasedthroughthecompany’sWebsiteorthroughtheWebservicesofitsagentsandpartners.

• Thecompanyalsooffersso1ware,onaSo1wareasaService(SaaS)basis,whichgivesbusoperatorstheopPonofhandlingtheirownPckePngandmanagingtheirowninventories.

• Thebiggestproblemwasthattheinfrastructurecouldnoteffec8velyhandleprocessingfluctua8ons,whichhadanegaPveimpactonproducPvity.AddiPonally,theprocurementofserversorupgradingtheserverconfiguraPonwasanextremelyPme-consumingendeavor.

• A1ertes8ngtheAWSsolu8ononasmallapplica8onforseveralmonths,thetravelagencydeterminedthatitwasveryworkableandconvenient.

Benefits• WithfeatureslikeElas8cLoadBalancingandmul8pleavailabilityzones,AWSprovidestherequiredinfrastructuretobuildforredundancy

andauto-failover.Whenyouincorporatetheseinyoursystem/applicaPondesign,youcanachievehighreliabilityandscale.• Byscalingupanddowndynamicallybasedontheload,wemaintainperformanceaswellasminimizecost.WiththePmesavingsthatthe

ITanddevelopmentstaffsobtainfromtheAWSsoluPon,AWSgivesusanoverallcostbenefitofabout30-40%• Abilitytoinstantlyreplicatethewholesetupondemandfortes8ngbycrea8nganddestroyinginstancesondemandfor

experimenta8on,therebyreducingthe8metomarket• SincejoiningforceswithAWS,redBushasgainedthefreedomtoexperimentonnewsolu8onsandapplica8onsatminimalcost,increased

theefficiencyofitsoperaPons,andimproveditsprofitability.

30

31

HealthcareVerPcal

HealthcareSectorPrimaryCloudUsage• Tradi8onallyskep8calaboutadopPngcloudcompuPngbecauseofstrictprivacyandsecurityrules(HIPAAcompliance)• Costpressuresandadvancementinprivacyandsecuritystandardsleadingtocloudadop8on• CloudadopPonmainlyinthestoragesegment• Majorusageofcloudfor

– medicalimagearchiving.– email– medicalrecordsystems– personalhealthrecords– HIEs(HealthInformaPonExchange)– Portals– Enterprisecontentmanagement(ECM)– ClinicalcollaboraPon– Mobilityofdevicesandremotepa8entcare

• HealthcarepayersorganizaPons,whilelesscauPousaroundcloud-basedsoluPons,arefindinganeedto– managetheamountofcontentacrosslargeorganizaPons.– ECMsystemsareanimperaPveneedfororganizaPonsuchasUnitedHealthcarewiththeamountofcontentalongwithneedto

managedataacrossaconsolidatedhealthcarepayerorganizaPon.

32

33

ManufacturingIndustry

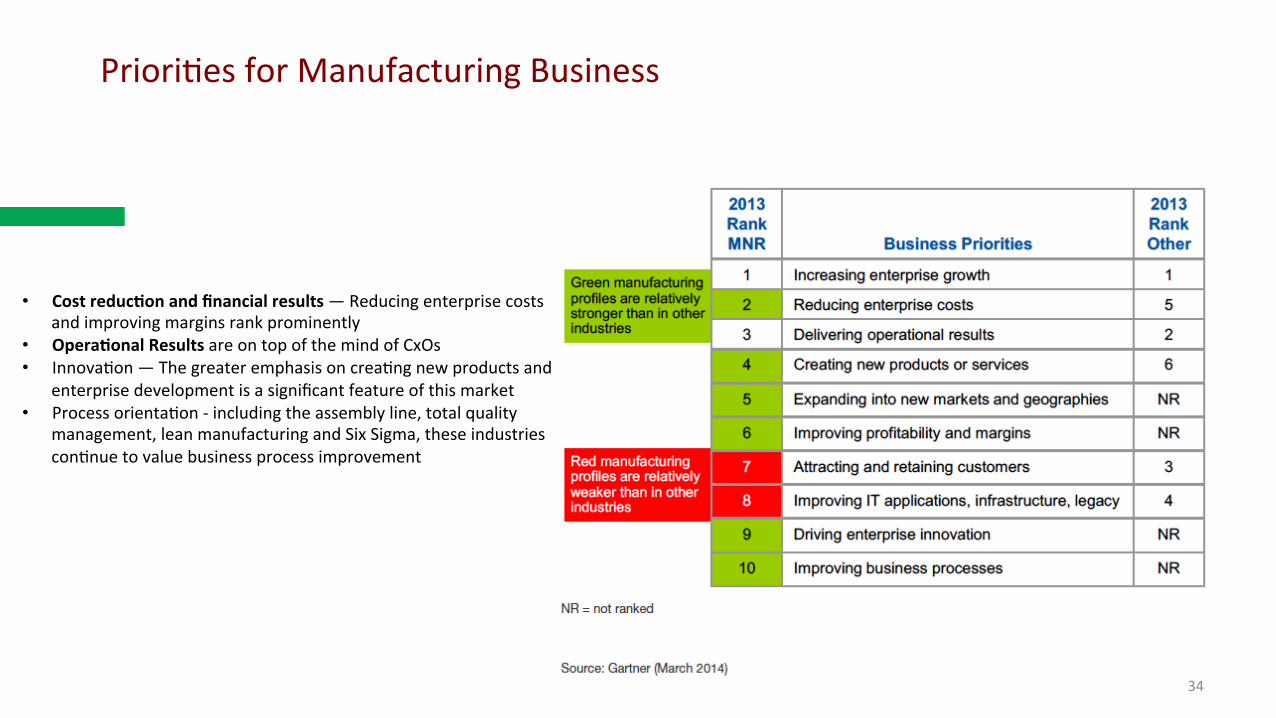

PrioriPesforManufacturingBusiness

34

• Costreduc8onandfinancialresults—Reducingenterprisecostsandimprovingmarginsrankprominently

• Opera8onalResultsareontopofthemindofCxOs• InnovaPon—ThegreateremphasisoncreaPngnewproductsand

enterprisedevelopmentisasignificantfeatureofthismarket• ProcessorientaPon-includingtheassemblyline,totalquality

management,leanmanufacturingandSixSigma,theseindustriesconPnuetovaluebusinessprocessimprovement

WhyCloudMakesSenseforManufacturingCompanies?

• Higheremphasisoncost– BecauseofrelaPvelyhighercostsforenergy,plant,andequipmentandmaintenance.Thisspending"crowdsout"

discrePonaryITspending– Furthermore,andperhapsbecauseofthisuniquecoststructure,arelaPvelyhighpercentageofCIOsinMNRreportto

CFOs.ThisresultsincostmanagementpracPceshavingastrongerinfluenceand/orgreaterhurdlestojus8fyingROI.

• RealizingvaluefromTradi8onalITtakeslongerthanbusinessescanafford–Thelengthynatureofsystemdesign,development,deploymentandvaluecapturedfromtradiPonalinhouseITisorenseenasdetrimentaltothelargerbusinessobjecPves–Cloudcanhelphere

• Revisingprocess-orientedITsystemsisdifficult–TradiPonalITsystemsdonotmatchconPnuousimprovementandprocessopPmizaPon,soITisorenviewedasaninhibitortoprocesschange.

• LargenumberofLegacySolu8ons-ManufacturingfirmshavelonglegaciesoflocalITsystemsdeveloped.Thislegacycanpreventcompaniesfrommakinglargeinvestmentstostandardizeand/ortransformtheirbusiness.Asaresult,companieso1enpursuemanysmallchanges,ratherthanambi8ousandlarge-scaleITprograms.

35

ITSoluPonsMapforManufacturingIndustry

36

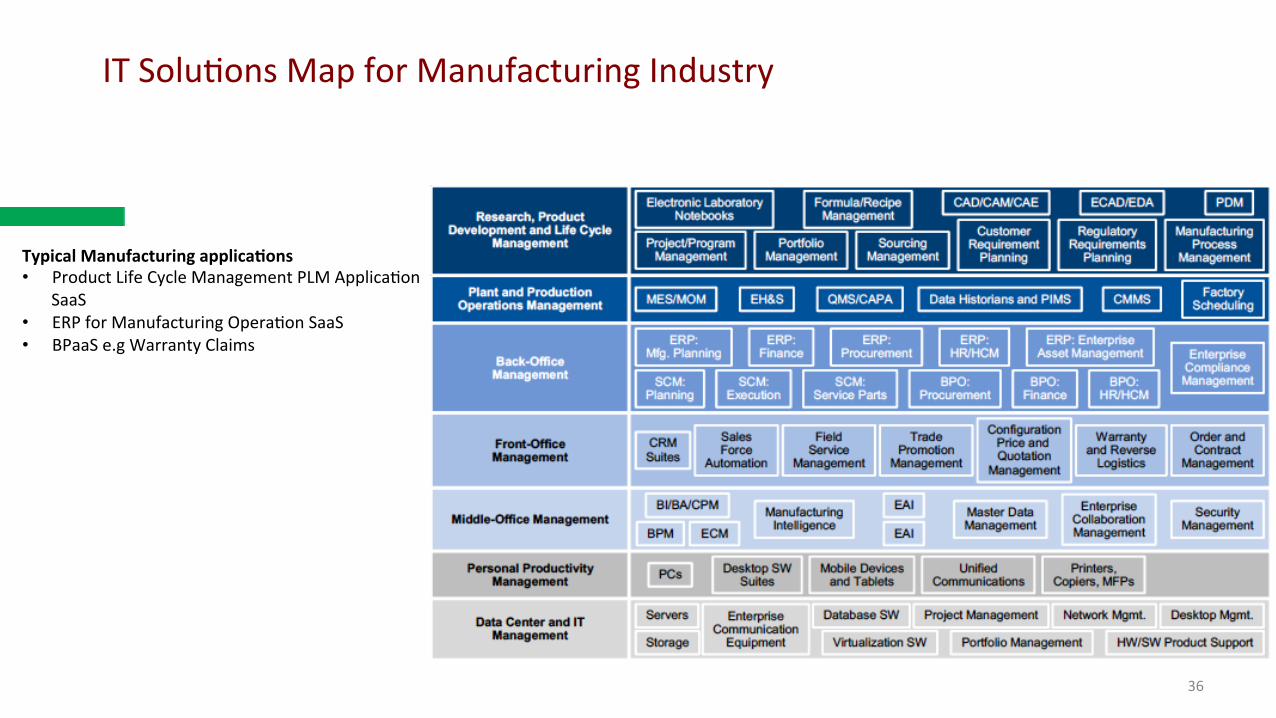

TypicalManufacturingapplica8ons• ProductLifeCycleManagementPLMApplicaPon

SaaS• ERPforManufacturingOperaPonSaaS• BPaaSe.gWarrantyClaims

TakeawaysfromIndustryVerPcals

• Thereareuniqueneedsofeveryindustry– Storage,mediaconversions,streaming,hybridcloudforMediaindustry– EHR,Storage,MobilitysoluPonsforHealthcare– DRandbackupforManufacturing

• Whenweapproachanycompanyfromthesetargetedindustries,weneedto– Checkthecompaniesbackground– CheckthepotenPalneedofthecompany– UseaCloudCaseStudyandprepareacasebasedonCustomer’sLatentneed– ShowthebenefitsofCloudasperthecustomersneed– Createtheneed,ratherthanaskingfortheneed

• DevelopverPcalexperPseinsegmentslikeMediaandHealthcare.AWShasaseparatehealthcarecompetency

37

38

TheSMESegment

India’sSMESegment

• HugeSMEsector-Studiessuggestthatthereareatleast7.5mnSMEsinIndia.• Sector’scontribuPontothecountry’sGDPisexpectedtoincreaseto22%in2020from17%in2011.• Small&MediumEnterprises(SMEs)accountfor45%ofIndia’stotalmanufacturingoutputandemployaround40%ofitsworkforce• IndianSMEsareexpectedtoincreasecloudadopPonatCAGRof20%between2012and2016• SMEcloudopportunitywasworthINR16.9bn,ofwhichINR9.2bnwasaccountedforbySaaSandINR7.7bnbyIaaS.• SomesmallerIndiancompaniessuchasIndiagames,Rediff.com,HungamaDigitalMediaand8KMileshavestartedtouPlisecloud

compuPngtechnologytoboostservicedelivery.• Theearliestdemandcamefromsuppliersinindustriessuchasautopartsandancillaries,wheresmallerfirmswereobligedtoimplement

e-commercesystemstosynchronizewiththeirlargercustomers.• ThedemandforcloudservicesbySMEsisparPcularlyhighintheareasof

– DisasterRecovery– RemotedatabasemanagementandStorage– e-mailhosPng.

Source:EY

India’sSMESegmentKeyCharacterisPcs

• PriceisanimportantconsideraPoninthesector• SlowTechAdopPonbecauseof

– Lackofunderstandingofbusinessbenefitstechnology.ItisesPmatedthataround60%ofIndianSMEssPllusepaper-basedsystems,butanincreasingnumberarenowtryingtoconverttodigital

– LackofguidanceontheinherentabiliPesoftechnologiesandhowthesecanbeintegratedandinsPtuPonalizedintheirbusinesses

– Resistancetoincurringupfrontinvestment-relatedcoststoimplementtechnology– Lackofskilledmanpowertomanagetechnologysetups

• Firmsinsectorssuchastransportnowhaveagreaterawarenessaboutthepoten8albenefitsoftechnologyuPlizaPon.

• So1wareapplica8onvendorswhoprovidepackagedbusinesssuites,suchasCustomerRela8onshipManagement(CRM),payroll,HR,enterpriseresourceplanning(ERP)andcollabora8veapplica8onsareexpectedtooutpacetradi8onalso1warelicensingvendorsbynearly800%inIndia

CloudusageinIndiaissPlllimitedtoadhocpilotprojects,withsmallbusinesseshavingahigherpercentage.

SourceIDC 41

Findings§ Whileallrespondentssaidthattheyusecloudservices,prominentusage(43%respondents)ofcloudisattheadhoclevelandfocusedprimarilyonpilotprojects.§ Smallbusinesseshaveahigherpercentageofadhocprojects(51%)whencomparedwithmedium-sizedandlargeenterprises(41–43%);“op8mized"usageofcloudishigherinlarge

andmedium-sizedenterprises(15%)whencomparedwithsmallbusinesses(6%).

Insights/Recommenda8ons

§ Usersshouldunderstandthetechnology,itsbenefits,andserviceproviders;andtransiPonpilotstoproducPonforservicesthatmaximizeefficiency.§ TheyshouldevaluatevendorandtechnologyopPonsforcloudandbeginpilotsforspecificusecases.

0 5 10 15 20 25 30 35 40 45 50

Optimized — Have broadly implemented a cloud-first strategy that is proactively managed

Managed — Currently widespread use of cloud supported by proactive business and IT leadership

Repeatable — Currently using cloud computing which is consistent effort made to reuse best practices and resources

Opportunistic — Currently using cloud computing which are driven by the business needs of individual workgroups and departments

Ad hoc — Focuses primarily on pilot projects

(%)

KeyTakeawaysfromtheSMESegment

• SME’shaveahugepotenPal• MicroandSmallcompaniesaresPllinad-hocphase• ShouldtargetMediumsizecompanies500-1000employees,10Cr+revenue• NeedtoeducatethesecompanieswiththeUseCasesandpotenPalbenefitsoftheCloud

42

43

CloudLandscapeAndMajorMarketsGlobal

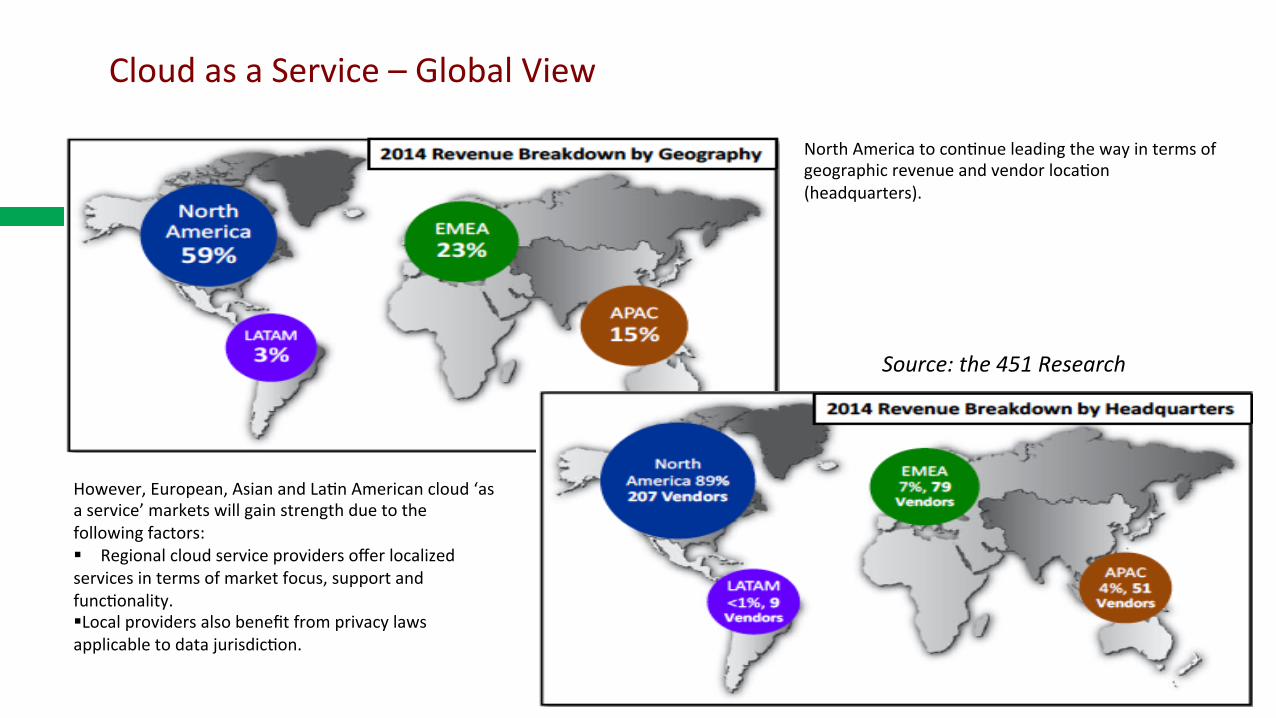

CloudasaService–GlobalView

However,European,AsianandLaPnAmericancloud‘asaservice’marketswillgainstrengthduetothefollowingfactors:§ Regionalcloudserviceprovidersofferlocalizedservicesintermsofmarketfocus,supportandfuncPonality.§LocalprovidersalsobenefitfromprivacylawsapplicabletodatajurisdicPon.

NorthAmericatoconPnueleadingthewayintermsofgeographicrevenueandvendorlocaPon(headquarters).

Source:the451Research

CloudCompuPngAsaService:VerPcalRevenue

45

• ServiceproviderswithverPcal-specific/segment-specificexperPseandacustomer-centric

approachtoservicedeliverywillwintheheartsandmindsofcustomers.• Expectincreaseswithintheretail,e-commerceandhealthcareindustries.

451ResearchMarketMonitor

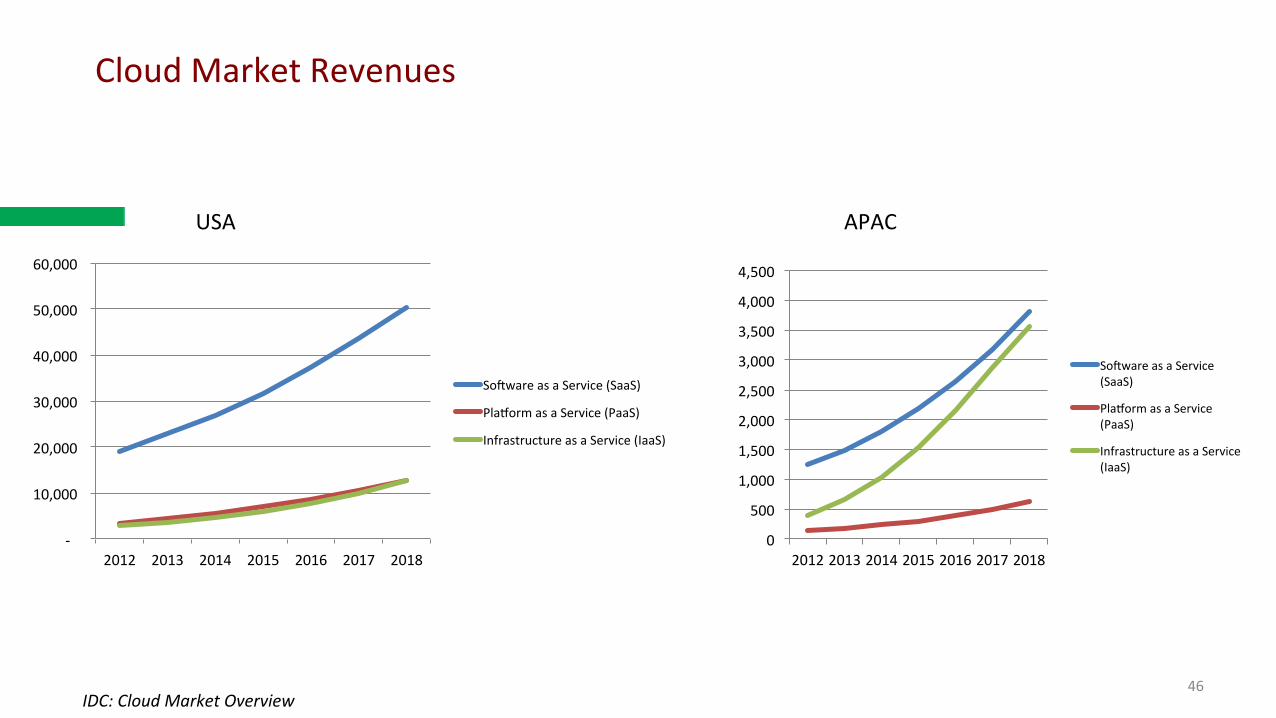

CloudMarketRevenues

46

-

10,000

20,000

30,000

40,000

50,000

60,000

2012 2013 2014 2015 2016 2017 2018

SorwareasaService(SaaS)

PlaqormasaService(PaaS)

InfrastructureasaService(IaaS)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2012201320142015201620172018

SorwareasaService(SaaS)

PlaqormasaService(PaaS)

InfrastructureasaService(IaaS)

USA APAC

IDC:CloudMarketOverview

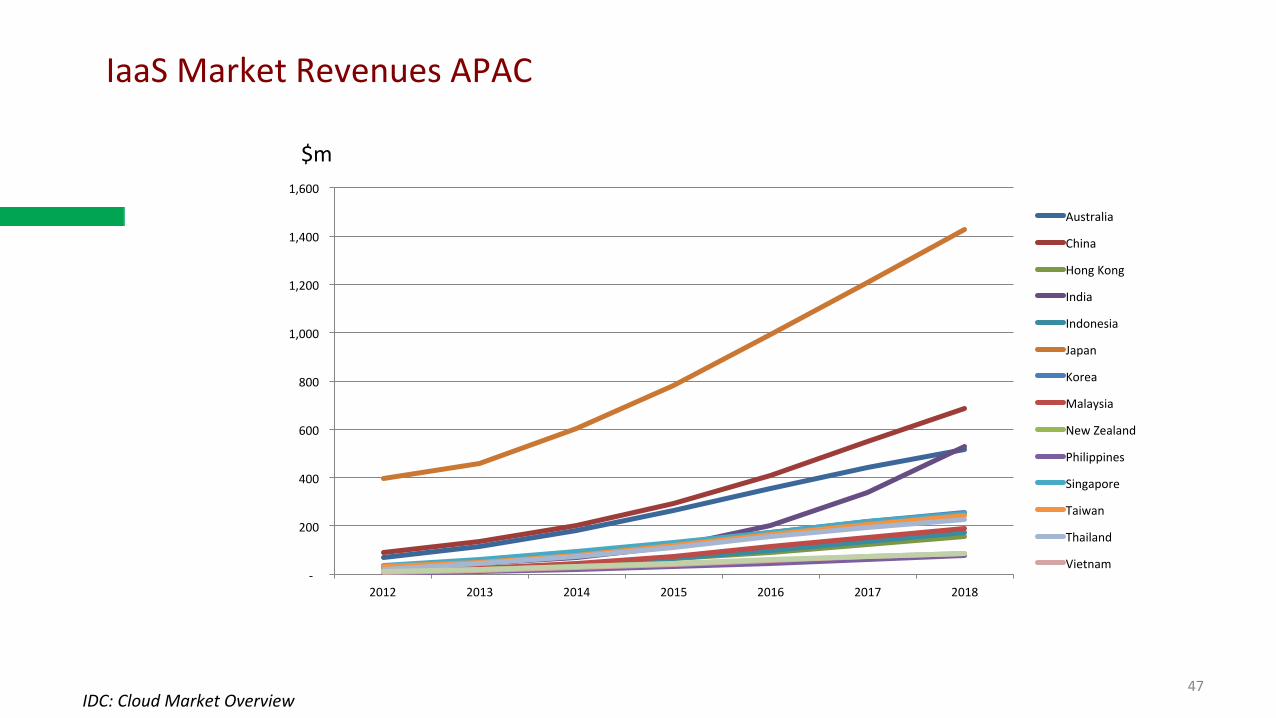

IaaSMarketRevenuesAPAC

47

-

200

400

600

800

1,000

1,200

1,400

1,600

2012 2013 2014 2015 2016 2017 2018

Australia

China

HongKong

India

Indonesia

Japan

Korea

Malaysia

NewZealand

Philippines

Singapore

Taiwan

Thailand

Vietnam

$m

IDC:CloudMarketOverview

GlobalCloudManagedServicesMarket

• TheglobalCloudManagedServicesmarketisexpectedtogrowfrom$52.23Billionin2015to

$118.43Billionby2020,ataCAGRof15.5%from2015to2020.• MajorplayersintheCloudManagedServicesmarket:

-AccenturePLC-Alcatel-Lucent-AtosSE-CiscoSystems,Inc.

-ComputerSciencesCorporaPon-Ericsson

-Fujitsu-Hewleh-PackardCompany-IBMCorporaPon

-NTTDataCorporaPon

48hhp://goo.gl/rRRr8C

KeyTakeawaysfromGlobalMarket

• NorthAmericatoconPnueleadingthewayintermsofgeographicrevenueandvendorlocaPon

• Emergingmarketsareexpectedtosignificantlyincreasetheircloudspendingoverthenextthreeyearsascomparedwithmorematuremarkets.In2015,India,BrazilandMexicowillbedrivingthisdemand

• USAandAustraliaarequiteagoodbetforinternaPonalexpansion

49

50

KeyCustomerChallengesandBenefits

Customer Technical Challenges for Cloud Adoption

51AsperEYreport–CloudAdop3oninIndia

• DatasecurityandprivacyisamajorconcernforenterprisesconsideringimplemenPngcloudIaaSservices.CloudIaaSisadistributedcompuPngmodelwithinherentambiguityaroundwherethedataresides.ThisdistributedmodelleadstoapercepPonofhigherriskandsecuritychallenges.

• AcloudserviceprovidercanmiPgatetheserisksbyestablishinganeffecPvesecurityandcontrolsframeworkinthefollowingareas:

• IdenPtyandriskmanagement• Complianceandaudit• ApplicaPonlevelsecurity• Databackupandrecovery• LegalCompliance

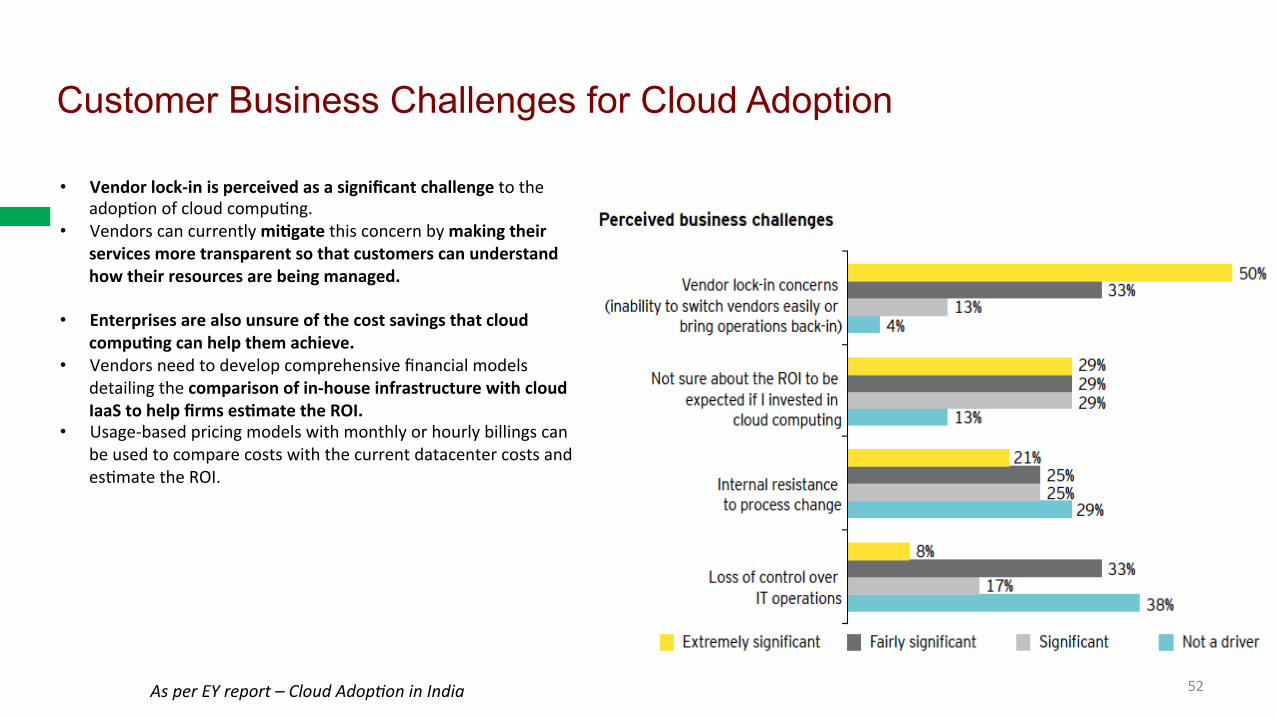

Customer Business Challenges for Cloud Adoption

52AsperEYreport–CloudAdop3oninIndia

• Vendorlock-inisperceivedasasignificantchallengetotheadopPonofcloudcompuPng.

• Vendorscancurrentlymi8gatethisconcernbymakingtheirservicesmoretransparentsothatcustomerscanunderstandhowtheirresourcesarebeingmanaged.

• Enterprisesarealsounsureofthecostsavingsthatcloudcompu8ngcanhelpthemachieve.

• Vendorsneedtodevelopcomprehensivefinancialmodelsdetailingthecomparisonofin-houseinfrastructurewithcloudIaaStohelpfirmses8matetheROI.

• Usage-basedpricingmodelswithmonthlyorhourlybillingscanbeusedtocomparecostswiththecurrentdatacentercostsandesPmatetheROI.

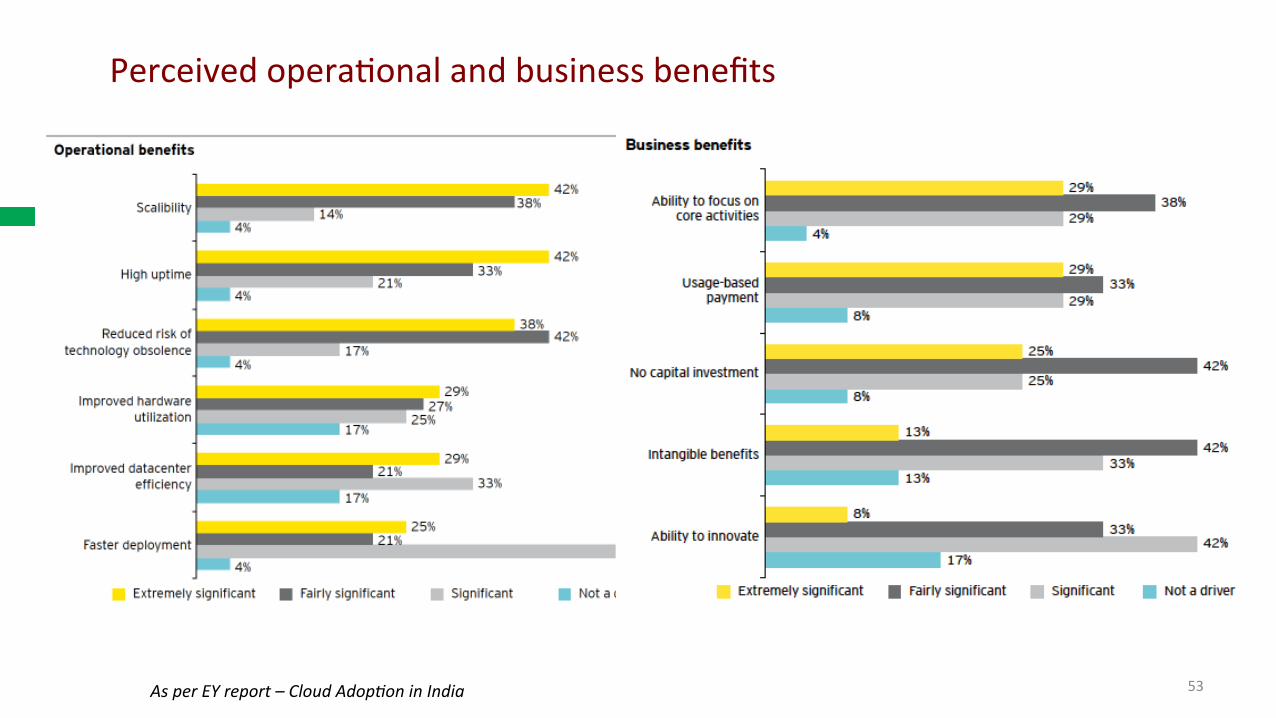

PerceivedoperaPonalandbusinessbenefits

53AsperEYreport–CloudAdop3oninIndia

Vendorassessmentcriteria

54

• DatasecurityandprivacyagainshinesthroughasthetopdifferenPaPngfactorfortheenterprise.

• SLACompliance,CostCompePvenessandPortability-Interoperabilityto

avoidvendorlock-inarethekeyassessmentcrietrias

• WithcloudIaaSservicesbeinganewbusinessandoperaPonalmodel,ahighdegreeofcustomerinterac8onduringthesalescycleandastrongsupportframeworkwillassistcustomersinadop8ngthetechnologyseamlessly

AsperEYreport–CloudAdop3oninIndia

PreferredPricingModels

55

• Atruepay-as-you-usemodelbasedontheuseofresourcessuchasperhourusageorCPUcyclesconsumedwillbeaqrac8vetotheSMBsegment.

• MoreflexiblemodelsintegraPngthefeaturesofusage-andcontract-basedpricingcanbedeveloped,whereserverinstancescanbechargedonadailyormonthlybasisinsteadofhourly.

• Reservedinstanceswithdiscountsonhourlyratescanbemorecost-effec8veforlargerenterpriseswithvisibilityondemand.ReservedinstancesarelikelytohelplargeenterprisesbeheresPmateandplantheircloudIaaSneeds.

AsperEYreport–CloudAdop3oninIndia

KeyTakeawaysfromCustomerChallenges

• Communicatewithbuyersonthepercep8onofcloudbenefitsandchallenges:ThepercepPonofthesebenefitsandchallengesneedtobefactoredintocommunicaPonstrategies,serviceofferingsandSLAstructures.

– DatasecurityandprivacyisthetopmostconcernforcloudadopPon,followedbylatencyandresourceupPme– Vendorlock-inandnotsureabouttheROIaremainbusinesschallenges– Scalability,highupPmeandreducedriskoftechnologyobsolencearethemaintechnicalperceivedbenefits– FocusoncoreacPviPes,payforusageandnocapitalexpenditurearethemainbusinessperceivedbenefits

• DataSecurity,SLAcomplianceandCostcompe88venessarethemainparametersforvendorselecPon–AddressalloftheseconcernsinthecommunicaPon

• DeveloppricingmodelsandROIexpecta8ons:Enterprisesareexpectedtobenefitfromdetailedfinancialmodelsbenchmarkingin-housedatacentercostswiththeinvestmentandrunningcostsassociatedwiththecloudIaaSmodel,usingdifferentpricingmodelstohelpesPmatetheROI.

• Setuptestlabs:Shouldsetuptestareas,whichcustomerscanaccessonanexperimentalbasis.ThiswillallowenterprisestoexperiencethetechnologybeforefullscaleadopPon.

56AsperEYreport–CloudAdop3oninIndia

57

CloudDecisionMaking

KeyRolesandPosiPonsinCloudServicesPurchasing

• Influencers—BusinessexecuPvesandmanagers,seniorITleaders(excludingtheCIO)andnon-CIOITfuncPonalroleshavethebiggestinfluenceovercloud-relatedbudgets.

• Decisionmakers—However,theprimarycloudbudgetdecisionmakertendstobetheC-levelexecuPves,includingCEOs,CIOsandtoalesserextent,otherC-levelexecuPvesandseniorITleaders.

• Budgetcontrollers—Controlofcloud-relatedbudgetsistypicallyheldbytheCFO,butinsomecasesdelegatedtothefuncPonalroles.

DecisionMakersbyRoles,AcrossRegions

• CEOsandCIOss8llretainthelargestcontrolovercloudbudgetdecisionsfornow.Acrossgeographies

• CEOsinAsia/PacificandCIOsinNorthAmericahavethebiggestroleindecidingcloudspending.

• CFOsdidnothavethebiggestsayinclouddecisionmaking,theyhadthemostcontrolinbudgetcontrol.

• Asinfluencersofcloudspending,seniorITleaderswhoreportintotheCIOshavethemostimpact.

KeyTakeawaysfromCloudDecisionMaking

• NeedtohaveGoodcontactwithCEOandCIOsofthecompanieswearetargePng.

• MaintainmindshareintheITdepartment,andalsoincreaseyoursphereofinfluenceandaccesstotheC-level.HelporganizaPonsconnectinternally(ITandbusinessunits)withyoursoluPonsandseeallsidesofthebenefitstocloudsoluPons.

60

ConsultaPveSelling

BothenterprisesandserviceprovidersarelikelytobenefitfromaconsultaPveapproachandin-depthdiscussionswithcloudIaaSserviceprovidersinthefollowingareas:• Thedifferen8a8ngbenefitsofcloudIaaSservices• UseCases,Pricingstructures,financialmodelsandreturnoninvestment(ROI)thatacloud

adoptercanexpectfrommovingtothecloud• Guidelinesandbenchmarkstohelpenterprisesselectapplica8onsthataremostsuitablefor

adopPngeithertheprivateorthepubliccloudmodels• AddressingsecurityanddataprivacyissuessaPsfactorily•Extendingcustomersupporttoadoptersofthetechnology

61AsperEYreport–CloudAdop3oninIndia

62

AcPonPlan,HowtoMoveForwards

RecommendaPonsandAcPonPlan

• TargettheRightSegment,SizeoftheFirm,SectoroftheFirm• PrepareDetailedusecasesrelevantfortheTargetCustomers• PrepareTestLabsofthecommonusecases• InterfacewithRightStakeholders

63

ThankYou

64