colorado department of revenue : how to file a sales tax

TRANSCRIPT

Colorado Department of Revenue : How to File a Sales Tax Return using form DR 0100

What you will need before you begin:

Jurisdiction/location codes for all locations where sales were taxed. • Assistance on how to look up sales and use tax rates is available on our website

Tax.Colorado.gov/how-to-look-up-sales-use-tax-rates • Location/site ID numbers corresponding to each jurisdiction/location code. Sites being filed must

be set up prior to filing returns. • Assistance on adding locations/sites to your sales tax account is available on our website

Tax.Colorado.gov/add-locations-sites-to-your-sales-tax-account • Gross sales for each location/site.

Obtain copies of paper form DR 0100.

A separate form will be needed for

each location/site being filed.

Forms are available on our website:

Tax.Colorado.gov/Sales-Use-Tax-Forms

Fill out the information section for all

returns being filed.

• Each DR 0100 should have a

separate location/site number

listed (example, 00000001-0010).

This helps the Department identify

and properly allocate local

jurisdiction taxes that are paid with

the return.

Revised February 2021

1

Form DR 0100

Colorado Department of Revenue - Education & Training - How to File a Retail Sales Tax Return by paper form DR 0100

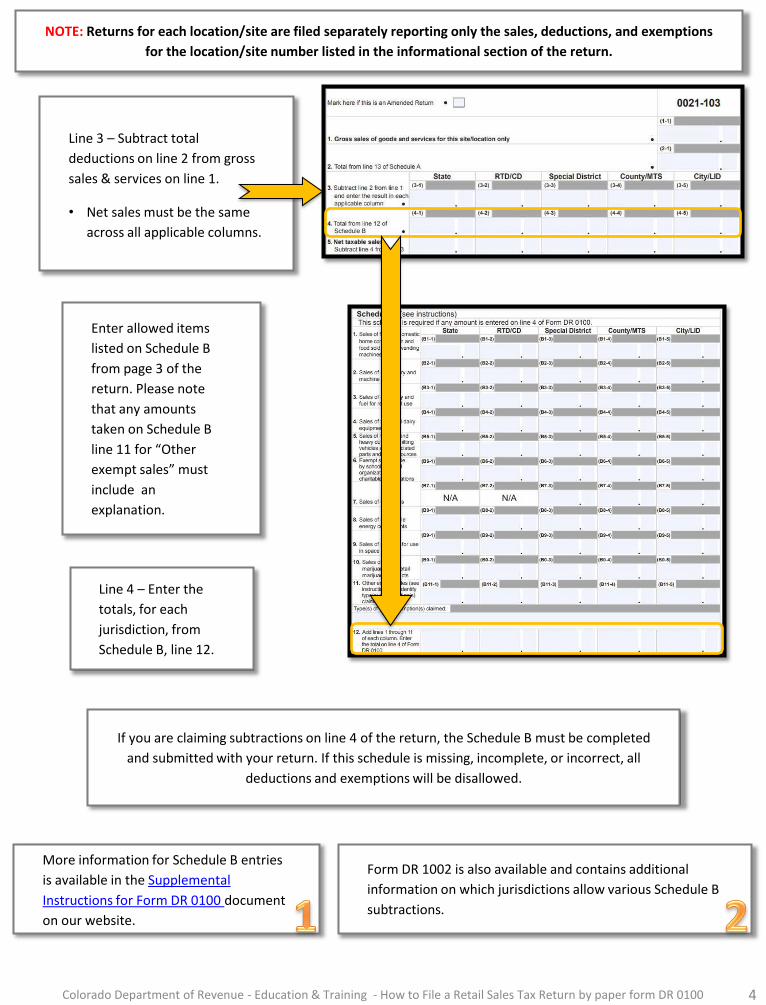

NOTE: Returns for each location/site are filed separately reporting only the sales, deductions, and exemptions

for the location/site number listed in the informational section of the return.

2

Retailers must complete all applicable lines, including lines 1, 3, 5, 7, 9, 12, 14, 17, and 18, entering 0 (zero), if

applicable. Retailers must also include Schedules A and B for each site/location, even if the schedules are

reporting 0 (zero).

More information for

Schedule A and B

entries is available in

the Supplemental

Instructions for Form DR

0100 document on our

website.

NOTE

Colorado Department of Revenue - Education & Training - How to File a Retail Sales Tax Return by paper form DR 0100

NOTE: If you are filing an

amended return, check the box

to indicate that this is an

amended return.

Form DR 0100

Form DR 1002 is

available and

contains additional

information on

which jurisdictions

allow various

Schedule B

subtractions.

DR 1002

NOTE: Returns for each location/site are filed separately reporting only the sales, deductions, and exemptions

for the location/site number listed in the informational section of the return.

3

Line 1 – Enter the gross sales

for the location/site

indicated by the account

number.

• Do not put the same

amount in Line 1 for each

location.

Line 2 – Enter the total

from Schedule A, Line 13.

More information

for Schedule A

entries is available

in the Supplemental

Instructions for

Form DR 0100

document on our

website.

If you are claiming subtractions on line 2 of the return, the

Schedule A must be completed and submitted with your

return. If this schedule is missing, incomplete, or incorrect, all

deductions and exemptions will be disallowed.

Enter allowed items listed on Schedule A

from pages 2 and 3 of the return. Please

note that any deductions taken on Schedule

A line 12 for “Other exempt sales” must

include an explanation.

Colorado Department of Revenue - Education & Training - How to File a Retail Sales Tax Return by paper form DR 0100

4

Line 3 – Subtract total

deductions on line 2 from gross

sales & services on line 1.

• Net sales must be the same

across all applicable columns.

NOTE: Returns for each location/site are filed separately reporting only the sales, deductions, and exemptions

for the location/site number listed in the informational section of the return.

Colorado Department of Revenue - Education & Training - How to File a Retail Sales Tax Return by paper form DR 0100

If you are claiming subtractions on line 4 of the return, the Schedule B must be completed

and submitted with your return. If this schedule is missing, incomplete, or incorrect, all

deductions and exemptions will be disallowed.

Line 4 – Enter the

totals, for each

jurisdiction, from

Schedule B, line 12.

Enter allowed items

listed on Schedule B

from page 3 of the

return. Please note

that any amounts

taken on Schedule B

line 11 for “Other

exempt sales” must

include an

explanation.

Form DR 1002 is also available and contains additional

information on which jurisdictions allow various Schedule B

subtractions.

More information for Schedule B entries

is available in the Supplemental

Instructions for Form DR 0100 document

on our website.

5

Line 5 – Subtract line 4

from line 3 for each

column.

Line 8 – Enter any tax collected in excess of the tax due as computed on line 7.

Example - $50 is collected in county sales tax, but only $45 is calculated in the county column of the return, the

excess $5 must be reported in the county column in line 8. This may occur when there are sales tax rate

decreases. If tax is collected using the old rate on items purchased after the decrease goes into effect, then the

excess that was collected should be reported on this line.

NOTE: Returns for each location/site are filed separately reporting only the sales, deductions, and exemptions

for the location/site number listed in the informational section of the return.

Colorado Department of Revenue - Education & Training - How to File a Retail Sales Tax Return by paper form DR 0100

Line 7 – Multiply the net

taxable sales on line 5 by

the tax rate on line 6 for

each column.

Line 6 – Form DR 1002

contains up-to-date tax rate

information for all Colorado

state-collected tax

jurisdictions.

Line 9 – Add lines 7

and 8 for each column

Line 10 – Service Fee Rates for all

applicable Colorado state-collected

jurisdictions are available in the DR 1002.

Line 11 – Multiple the

value on line 9 by the

rate on line 10 for

each column.

6

NOTE: Returns for each location/site are filed separately reporting only the sales, deductions, and exemptions

for the location/site number listed in the informational section of the return.

Colorado Department of Revenue - Education & Training - How to File a Retail Sales Tax Return by paper form DR 0100

Service Fee Cap: The total combined Colorado state

service fee allowed to a retailer for any given filing

period is limited to $1,000. This limit applies to the

company as a whole, regardless of the number of

locations. Additionally, retailers with multiple locations

will be required to consolidate all locations into one

account.

If the combined Colorado state service fee calculated on

all of the retailer’s sales tax returns for all sites/locations

for the filing period exceeds $1,000, the retailer must

complete the State Service Fee Worksheet DR 0103. The

worksheet is used to determine what amount, if any,

the retailers must add to the total balance due

calculated on the retailer’s returns.

Different jurisdictions may have different service fee

caps. Service fees and limit caps are listed in the DR

1002

Service Fee: A service fee (also known as a vendor fee) is a percentage of the sales tax collected that a retailer

is allowed to retain in order to cover the expenses incurred by collecting and remitting sales tax. Not all

jurisdictions allow a service fee. Please see the DR 1002 for service fee rates for all Colorado state-collected

jurisdictions.

Form DR 0103

7

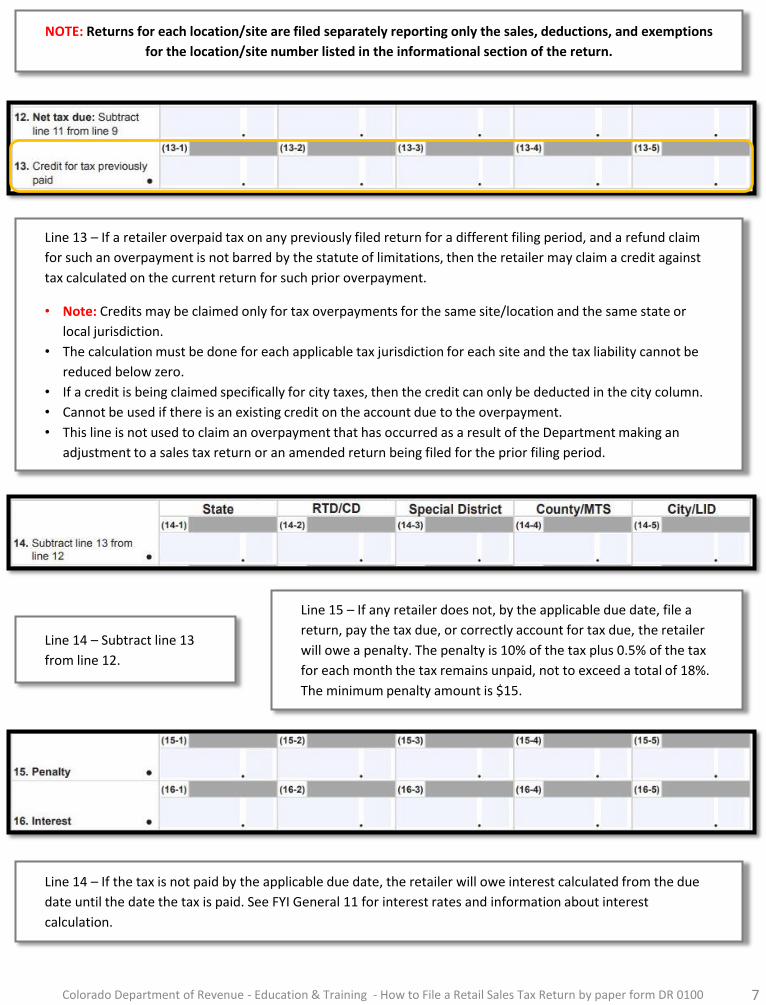

Line 15 – If any retailer does not, by the applicable due date, file a

return, pay the tax due, or correctly account for tax due, the retailer

will owe a penalty. The penalty is 10% of the tax plus 0.5% of the tax

for each month the tax remains unpaid, not to exceed a total of 18%.

The minimum penalty amount is $15.

Line 14 – Subtract line 13

from line 12.

Line 13 – If a retailer overpaid tax on any previously filed return for a different filing period, and a refund claim

for such an overpayment is not barred by the statute of limitations, then the retailer may claim a credit against

tax calculated on the current return for such prior overpayment.

• Note: Credits may be claimed only for tax overpayments for the same site/location and the same state or

local jurisdiction.

• The calculation must be done for each applicable tax jurisdiction for each site and the tax liability cannot be

reduced below zero.

• If a credit is being claimed specifically for city taxes, then the credit can only be deducted in the city column.

• Cannot be used if there is an existing credit on the account due to the overpayment.

• This line is not used to claim an overpayment that has occurred as a result of the Department making an

adjustment to a sales tax return or an amended return being filed for the prior filing period.

NOTE: Returns for each location/site are filed separately reporting only the sales, deductions, and exemptions

for the location/site number listed in the informational section of the return.

Colorado Department of Revenue - Education & Training - How to File a Retail Sales Tax Return by paper form DR 0100

Line 14 – If the tax is not paid by the applicable due date, the retailer will owe interest calculated from the due

date until the date the tax is paid. See FYI General 11 for interest rates and information about interest

calculation.

8

If you need assistance making a payment, refer to our payments webpage: Tax.Colorado.gov/Payment-FAQ

Additional How To Resources can be found at:

Tax.Colorado.gov/Sales-Tax-Filing-Information YouTube Channel: corevenueonline

NOTE: Returns for each location/site are filed separately reporting only the sales, deductions, and exemptions

for the location/site number listed in the informational section of the return.

Colorado Department of Revenue - Education & Training - How to File a Retail Sales Tax Return by paper form DR 0100

• Correct version of form DR 0100 is used

• The account number and site number are entered

correctly on the return

• The correct tax rates are used – See DR 1002

• All pages of the return are complete and included in

mailing

• All required lines are complete for all columns

• Form DR 0103 is included if filing multiple locations

The amount on line 18 is the total tax due for the location filed on the return. If you are filing

multiple locations use form DR 0103 to calculate the full amount due for all sites taking the

service/ vendor fee cap into consideration. The amount calculated on line 5 of the DR 0103 is the

total tax amount due for all sites being filed.

Line 17 – Add lines 14, 15,

and 16 for each column.

Line 18 – Add amounts from

line 17 for all columns.

Verify the following before mailing your return:

Revised February 2021