coming into focus - compliance | cdd · coming into focus issue 28 your ......

TRANSCRIPT

Coming into focus

ISSUE 28

YOUR MAGAZINE FROM THE INTERNATIONAL COMPLIANCE ASSOCIATION

inCOMPLIANCE ®

Compliance: making a difference

Coming to the surface

Earning your wings

p.16 p.20

£4.95 where sold separately

p.32

inCOMPLIANCE®3

ICA Members’ Assembly28 March 2017, Pullman, St Pancras, London

This is a free event for all current ICA members. It will include an overview of the Association and its achievements over the past year, as well as an insight into future developments.

Paul C. Dwyer will be presenting on ‘understanding and dealing with cyber threats strategically in a financial service firm’, while Bill Howarth and David Jenkins-Handy will discuss ‘measuring culture’.

For further information and to book your place, please visit www.int-comp.org/members-assembly

Attending the Members’

Assembly will give you two CPD hours.

ICA Certificate Workshops in Anti-Corruption and Combating the Financing of TerrorismWe are offering you the chance to attend a free one-off workshop when enrolling on one of our new certificate programmes: ICA Certificate in Anti-Corruption or ICA Certificate in Combating the Financing of Terrorism.

These new certificates will only be available online, so this is a fantastic opportunity to take part in a face-to-face workshop, gain the full certificate in either Anti-Corruption or Combating the Financing of Terrorism and all with the added benefit of gaining CPD points.

The workshops for both certificates will take place on the 28th March 2017.

Further discounts are also available should you wish to attend both a certificate workshop and ICA’s 9th Annual Conference: Making a Difference the following day.

For further information on these events please visit www.int-comp.org/certificate-workshops

ICAA500

Editorial Board

Kathryn Cearns, Independent Consultant, [email protected]

Jee Meng Chen, HSBC, [email protected]

Jacob Ghanty, K&L Gates LLP, [email protected]

Tom Salmond, Ernst & Young LLP, [email protected]

Irwin Spilka, Stonehage, [email protected]

David Symes, Compliance Recruitment, [email protected]

Rachel Waldren, ANZ, [email protected]

inCOMPLIANCE®Issue 28

Publisher: International Compliance [email protected]

Editor: James [email protected]

Design: Design & Document [email protected]

Production: Dorinda Gibbons & Sophy [email protected] [email protected]

Advertising Queries: Amanda [email protected]

Chief Executive, International Compliance Association: Phil [email protected]

ICA Membership Enquiries: Dorinda Gibbons & Sophy [email protected]

ICA Qualifications: Contact our training partner, [email protected]

International Compliance Association CPD - 1 point

Advice to Readers

inCOMPLIANCE® is published six times a year by the International Compliance Association. Reproduction, copying, extraction, or redistribution by any means of the whole or part of this publication must not be undertaken without the written permission of the publishers.

inCOMPLIANCE® is distributed as a free member benefit to all members of the International Compliance Association.

Articles are published in good faith without responsibility on the part of the publishers or authors for loss occasioned to any person acting or refraining from action as a result of any views expressed therein. Opinions expressed in this publication should not be regarded as the official view of the ICA or as the personal views of the Editorial Board members of inCOMPLIANCE®.

All rights reserved in respect of all articles, drawings, photographs etc published in inCOMPLIANCE® anywhere in the world. Reproduction or imitations of these are expressly forbidden without permission of the publishers.

Printed in England

Although the current political and economic landscape appears incredibly unpredictable – with the reverberations of Brexit and the US presidential elections showing no signs of diminishing – it is perhaps worth bearing in mind that the flipside to risk and uncertainty is often opportunity. Within these challenging times, opportunities may present themselves for compliance professionals to make their presence felt through adding value to their businesses and enabling them to navigate choppy waters.

In that spirit, the ICA’s annual conference, later this month (p.16), aims to highlight the positive contribution that compliance can make to business, as well as the strides that the profession itself continues to take within a difficult climate. And you’ll find further evidence of that sentiment throughout this issue of inCOMPLIANCE®, with articles

considering the continuing evolution of the role of the compliance officer and the expanding career prospects that this presents (p.14), as well as outlining the openings available for compliance practitioners to step beyond their day jobs and “give back” to the wider compliance community (p.18).

As the challenges facing compliance become increasingly diverse and demanding, the profession must continue to raise its game, upskill and develop new tools to meet current and future needs. A positive outlook will be essential to achieving this.

.

A positive outlookJames Thomas

Editor

inCOMPLIANCE®3

ICA Certificate Workshops in Anti-Corruption and Combating the Financing of TerrorismWe are offering you the chance to attend a free one-off workshop when enrolling on one of our new certificate programmes: ICA Certificate in Anti-Corruption or ICA Certificate in Combating the Financing of Terrorism.

These new certificates will only be available online, so this is a fantastic opportunity to take part in a face-to-face workshop, gain the full certificate in either Anti-Corruption or Combating the Financing of Terrorism and all with the added benefit of gaining CPD points.

The workshops for both certificates will take place on the 28th March 2017.

Further discounts are also available should you wish to attend both a certificate workshop and ICA’s 9th Annual Conference: Making a Difference the following day.

For further information on these events please visit www.int-comp.org/certificate-workshops

ICAA500

inCOMPLIANCE®4

inCOMPLIANCE®5

Contents

3 Editor’s commentWithin challenging times, opportunities may present

themselves for compliance professionals to add value, writes James Thomas

6 Message from Phil / ICA News A roundup of the latest news

and events from the ICA

10Industry News A summary of recent developments affecting

Financial Crime Prevention, GRC, AML and CDD professionals

12Career CornerMorgan McKinley's specialist compliance team

take a look back at the hot areas of compliance recruitment the UK in 2016, whilst offering their predictions on compliance hiring in 2017

14Career CornerChris Field considers how the role of the compliance

officer has developed and how this affects the career progression of both the existing compliance community and of those interested in becoming a compliance practitioner

30Culture and ConductDavid Jackman outlines

the importance of good, independent judgement in decision-making

32Skills Salima Nanji considers the role and

responsibilities of the CF10

16Compliance: Making a difference

James Thomas previews the forthcoming ICA Annual Conference

18Community mattersThere are opportunities

for personal and professional growth through giving back to the compliance community, as James Thomas reports

20Coming to the surface One year on from their

release, Vladimir Berezansky considers the impact of the Panama Papers

REGULAR FEATURES IN THIS ISSUE

PAGE 20

PAGE 32

24 Coming into focus Matt Timmons and

Keily Blair consider the emergence and evolution of corporate disclosure requirements under the 4MLD

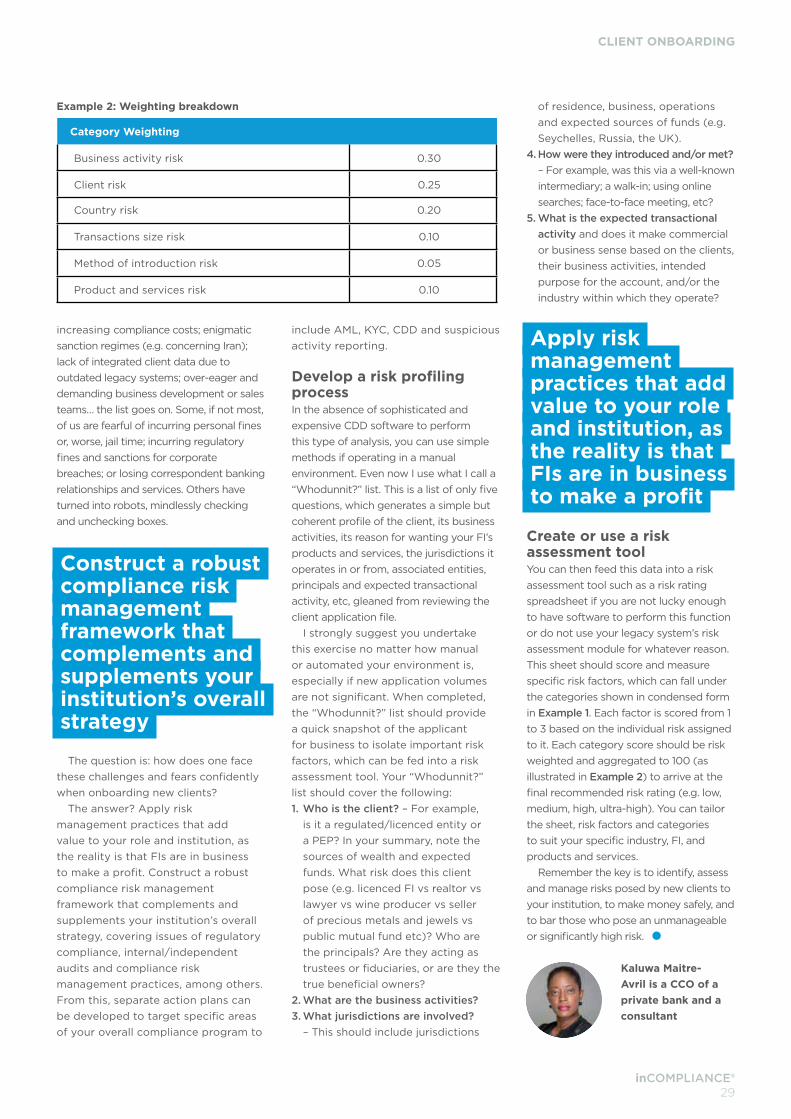

27In my honest opinionKaluwa Maitre-

Avril takes a frank look at client onboarding procedures

34 A basic means of survivalIn the midst of

the ongoing refugee crisis, Deepa Chandrasekhar considers the imperative to facilitate remittance frameworks in fragile states

36An ongoing struggleWith perceived levels of

bribery and corruption on the increase, Ruth Hutchinson reports from the launch of Transparency International’s 2016 Global Corruption Perceptions Index

38 Dirty money seeping through banks

Banks have largely ignored IP theft. However, they may be facilitating their clients’ insidious commercial transactions, opening up a dragnet for themselves, warns Rohan Bedi

41 Rotten to the core?In the wake of the Wells

Fargo fake accounts scandal numerous questions remain to be answered about the role of governance, risk management and compliance at the bank, writes Richard Griffith

inCOMPLIANCE®4

inCOMPLIANCE®5

Have you thought about writing an article for inCOMPLIANCE®?Writing an article is a great opportunity to raise your profile within ICA and present a topic of relevance to your fellow members. Writing an article on anti-money laundering, compliance, financial crime or associated disciplines will also earn you valuable CPD!

Visit tinyurl.com/jvbu58r and download our document on Article writing tips and Blogging Best Practice to enhance your skills in this area and learn about structure, themes and writing style.

Please note: you don’t have to be an ICA Member to register your interest in submitting.

If you are interested in writing an article for inCOMPLIANCE®, email us at: [email protected] and remember to include your full name and your topic of interest.

PAGE 24

PAGE 41

inCOMPLIANCE®7

Since the last issue of inCOMPLIANCE® we have had an exciting time at ICA as we launched our 2017 roadshow of member events, running a total of 11 hot topic briefing sessions, each attended by 30 – 70 members (plus a handful of guests).

As a professional membership body there is nothing more rewarding than meeting, exchanging views with, and inspiring and educating our members. If you didn’t manage to attend at least one of those events then please keep an eye on the website for an announcement of our next set of dates. The feedback we received – particularly for our keynote speakers – was overwhelmingly positive.

We also took the opportunity to show members a “hands-on” demonstration of the new CPD centre and member benefits, which was well-received.

However, the biggest events in the ICA calendar are still to come!

Elsewhere in this edition you will find information about our all-important Annual Members’ Assembly, 9th Annual Conference and our first ever Fellows’ dinner; all staged at the end of March. Each of these events gives you the opportunity to understand and shape the future of your association, so do please come along and have your say.

I look forward to saying hello to you at one of the many upcoming events.

inCOMPLIANCE®6

A Note from PhilPhil Ryan ICA CEO

Malaysia briefing session reviewOn 12 January 2017 ICA held a briefing session hosted by our partners in Malaysia, the Asian Institute of Chartered Bankers. The event started with a presentation from the Chairman of Malaysia's Compliance Officers Networking Group (CONG), Mr V. Maslamani (who also sits on the ICA International Board), entitled “Compliance 2.0”. The presentation looked at the new compliance regime in Malaysia following the implementation of Bank Negara's (BNM) Compliance Paper, which became effective 1 January 2017.

ICA's Regional Director, Andrew Glover, then looked at the current state of regulation across the globe, specifically in Malaysia, noting in particular the new BNM requirements on firms to provide "accredited training" to all appropriate staff. Andrew also took the opportunity to run through the current programmes offered in Malaysia, as well as to introduce some new "short courses" including the various ICA Specialist Certificates.

Best wishes

Phil

inCOMPLIANCE®7

NEWS FROM THE ICA

ICA annual events in MarchDon’t forget to register for the ICA events taking place on the 28-29 March 2017. More information about all of the events is available on the ICA website where you can register online.

Cumplen ConferencePhil Ryan, ICA CEO, was a keynote speaker at the Annual CUMPLEN conference in Madrid and spoke about the evolution of the compliance professional in the Anglo-Saxon world. Feedback was very positive and a lot of questions centred on ICA’s global overview of how compliance is changing, in different jurisdictions, from a legally-dominated discipline with a rules-based focus into a principles-based, forward-looking practice, which is now establishing itself as a first career in its own right.

Singapore briefing event reviewICA held a briefing event on 17 January 2017 in front of a packed auditorium of 306 attendees. The event started with a presentation from the Director of Workforce Singapore, Mr Kenneth Wong, to launch the Professional Conversion Programme, a new initiative aimed at building skilled workers in the financial services industry. ICTA is proud to have signed the Letter of Appointment and is the only provider of structured training for compliance professionals in Singapore.

Andrew Glover, ICA Regional Director, then took to the stage and discussed the current programmes that are offered in Singapore, as well as introducing our new “Ethics, Rules and Regulations CPD courses for Financial Advisor Representatives”.

inCOMPLIANCE®

8inCOMPLIANCE®

9

NEWS FROM THE ICA

February was a very busy month for the ICA team as we took to the road around the UK crown dependencies and Bahrain to meet our members and prospective students.

The Hot Topic Networking events are free of charge and allow you, our members, to come along and listen to a relevant topic and network with your fellow members. We were very grateful to our colleagues Jonathan Bowdler, Andy Clarke and Pekka Dare from ICT who delivered the sessions. These included:

• Illicit enrichment – the UK response

• How do you build a compliance culture?

• Practical challenges in implementing sanctions controls

ICA Chief Executive, Phil Ryan, and Senior Membership Manager, Tom Perry, attended the events to talk about ICA member benefits, including a demonstration of the CPD Centre. The sessions encouraged member participation and the ICA team were certainly kept busy with interesting questions and ideas for future events.

Our first event in Bahrain was particularly well-attended, with lots of member engagement increasing the planned session time to over two hours, keeping Jonathan Bowdler on his toes!

For those of you who were unable to attend the sessions, all of the topics were recorded and will be available in the CPD Centre. The slides from the event will also be available through the ICA News area on the ICA Website.

The next events will be taking place in September and we hope to see you there. Keep checking the ICA website for details.

Following the Hot Topic events, we held our Open Day events for prospective students who wish to embark on an ICA Qualification. Tutors were again on hand to discuss the qualifications, and ICA staff were there to explain the new membership requirements and the benefits associated with joining our Professional Community.

We hope you enjoy looking at the photos and please let us have your feedback on these events or ideas for future ones at [email protected].

I was pleased to see a verygood turnout. Great topical information and fantastic opportunity to meetothers in the community

LARA BULLOCK

This was a very topical and useful event timed to fit in with a busy work schedule. I would not hesitate to recommend attending a similar event

MICHELE DOREY

inCOMPLIANCE®9

NEWS FROM THE ICA

I've been in the compliance role for 18 months and the compliance culture has always been the one thing that almost seemed fictional. It was great to listen to my fellow members and the presenter about creating a good compliance culture and I came away with lots of useful information, which I will be looking to implement in my workplace

The ICA qualifications and events add real value to my working life, challenging my views and enforcing critical thinking that can be employed in my day to day role

CHRIS MORTON

Jonathan always delivers a very lively, engaging and enthusiastic lecture

This was an excellent presentation. Please could we have more of this?

inCOMPLIANCE®10

INDUSTRY NEWS

Mossack Fonseca partners arrested in connection with Odebrecht scandalThe founders of Mossack Fonseca – the law firm at the centre of the Panama Papers leak (see further, p.20) – have been arrested on charges of money laundering, following a raid by Panamanian prosecutors. Jürgen Mossack and Ramón Fonseca stand accused of establishing offshore accounts that allowed Brazilian engineering company Odebrecht to funnel bribes to various countries.

According to Panama’s Attorney General, Kenia Porcell, the raid yielded information that "allegedly identifies the Panamanian firm as a criminal organisation that is dedicated to hiding assets or money from suspicious origins."

Odebrecht sits at the centre of a corruption scandal that has implicated political leaders from across the region and last year the company signed the largest anticorruption settlement in history after admitting to bribing officials in more than a dozen countries to the tune of $800m in order to obtain government contracts. The settlement has sparked a wave of further investigations across the region.

Industry News

Big banks face prosecution for RAND manipulation Seventeen international banks – including JPMorgan, Bank of America Merrill Lynch, HSBC, Credit Suisse and Barclays – are facing prosecution in connection with RAND manipulation, after South Africa’s Competition Commission referred a collusion case to the coutntry's Competition Tribunal. The referral is the culmination of an investigation that began in April 2015.

The Commission found that, from at least 2007, the banks used chatrooms to "collude on prices for bids, offers and bid-offer spreads for spot trades in relation to currency trading" and "manipulated the price of bids and offers through agreements to refrain from trading and creating fictitious bids and offers at particular times".

The Commission is calling for the imposition of penalties of up to 10% of annual turnover.

inCOMPLIANCE®11

INDUSTRY NEWS

US: AML framework “of limited benefit”“Many if not most of the resources devoted to AML/CFT by the financial sector have limited law enforcement or national security benefit, and in some cases cause collateral damage to other vital US interests,” according to a report published by The Clearing House. The report summarised the findings of around 60 experts, including senior former and current law enforcement, national security, bank regulatory and domestic policy officials; leaders of prominent think tanks; consultants and lawyers practicing in the field; FinTech CEOs; and the heads of AML/CFT at multiple major financial institutions.

Amongst the key strategic problems identified, the report cites the absence of prioritisation, the absence of an overarching purpose, and the outdated SARs regime. Operational problems include: counterproductive examination standards and processes, significant barriers to information sharing, and inefficiencies, such as multiple firms conducting due diligence on the same customers. Proposals for reform include:

• Better co-ordination of AML/CFT policy across the government, with the Department of Treasury taking a more prominent role

• FinCEN should reclaim sole supervisory responsibility for large, multinational financial institutions

• FinCEN should propose a safe harbour rule allowing FIs to innovate in a Financial Intelligence Unit (FIU) “sandbox”

• Policymakers should further facilitate the flow of raw data from financial institutions to law enforcement to assist with the modernisation of the current AML/CFT technological paradigm.

Wells Fargo cuts bonuses as more customers are implicated in scandalWells Fargo has announced that it will withhold bonuses from its senior executives, following the fallout from the fake accounts scandal. Eight senior executives – including President and Chief Executive Officer, Tim Sloan, Chief Financial Officer, John Shrewsberry, and Chief Risk Officer, Michael Loughlin – will lose their 2016 bonuses, while the bank will also reduce their long-term performance share payouts by up to 50%. In total, the cuts amount to $32m.

In a statement from the bank, Chairman Stephen Sanger said that the measures did not relate to findings of improper behaviour but “are part of the board’s ongoing efforts to promote accountability and ensure Wells Fargo puts customer interests first”.

Meanwhile, the bank revealed in its annual 10-K regulatory filing that more customers than previously believed may have been affected by the accounts scandal. According to CNBC, the bank reported that there could be "an increase in the identified number of potentially impacted customers".

inCOMPLIANCE®11

JPMorgan urges regulatory cutbacksThe CFO of JPMorgan, Marianne Lake, is urging the Trump administration to move ahead with the removal of regulations imposed on big banks in the wake of the financial crisis. During a presentation to investors, she suggested that: “A lot has been done to improve safety and soundness and confidence in financial markets and financial institutions, a lot of which was necessary. However, it is perfectly reasonable and rational — and also normal — after many years, and many new rules and requirements, to pause and step back and take a look at the entirety of them, individually and together." She added that: “The industry has come an extremely long way, and the time does feel right to provide more consistency and flexibility.” President Trump has pledged to cut back significantly on regulation, with the Dodd Frank Act under particular scrutiny.

inCOMPLIANCE®

12

CAREER CORNER

KYCThe KYC market across 2016 was very inconsistent compared with previous years. The year started off with a flourish with one of the world’s most established financial services firms hiring in excess of 40 contractors. This was to be the biggest mass hire of the last 12 months. Interestingly, challenger banks within the City and regionally hired around 10-30 contractors throughout the year. The market also took a slight downturn due to firms near or off-shoring their KYC functions to cheaper locations, such as Bournemouth, Belfast, Moscow, Poland and India.

Control roomHiring within the control room remained steady throughout 2016. On the permanent side, hiring focused on candidates at both the AVP and VP level. At the AVP level, candidates with good experience within control room surveillance topics were in demand. Hiring at the VP level focussed on candidates with previous experience of managing members within a team and previous experience within the private side has proved beneficial. At the AVP/VP level the control room market has been candidate short and as such multiple roles can be presented to candidates with typical salary increases of 15-20% being on offer.

RegulatoryConsistent with the pattern of recent years, regulation and regulatory change was top of the agenda for compliance recruitment in 2016. In the permanent market, the focus was on hiring individuals at the senior VP level who have expert knowledge of policies. In particular, candidates with good knowledge of MiFID II were in demand due to the need to ensure that the necessary resources are in place in time for its implementation in January 2018.

Similar trends were witnessed across the contracting market. The first half of the year saw increased hiring across MiFID II, the Market Abuse Regulation (MAR) and Senior Managers Regime (SMR) due to their upcoming implementation. Hiring slowed towards the second half of the year as firms were looking to transition these people from temporary to permanent positions

in order to cut costs. Typical rates within this area ranged from £700 - £1,000 per day.

SurveillanceWith the MAR coming into effect across the EU in July 2016, the world of surveillance was very busy, particularly in H1 2016. Most banking clients were looking for individuals with excellent product knowledge, especially in the equities, fixed income, money markets and FX businesses. Not only did we see a big uptake in core product surveillance roles, we also experienced more demand for those individuals with lexicon and voice surveillance experience. A number of larger banks were seeking to improve systems and develop bespoke lexicons to ensure that they were reporting accurately on all instances of market abuse and impropriety. This led to more demand for quantitative and technically-minded individuals who were able to bridge the gap between IT and compliance.

MonitoringCandidates with thematic monitoring experience remain highly sought after. Individuals with audit backgrounds who have moved into a first or second line role have found the market increasingly productive with a range of opportunities available.

Financial crime complianceThe need for financial crime professionals was a consistent requirement for companies in 2016. This demand is the result of a variety of factors, including regulatory pressure and changes in legislation, as well as many firms diversifying portfolios in order to generate profits in what was a difficult year for markets.

AMLGeneral AML vacancies were the focus of mid-sized firms, as larger firms continue to split responsibilities into more specialist positions. These vacancies have largely been at the AVP/VP level and encompass sanctions, transaction monitoring and enhanced due diligence (EDD) responsibilities. Smaller companies, including challenger banks, also increased the size of their AML teams as

Looking back, looking forward

Morgan McKinley’s specialist compliance team take a look back at the hot areas of compliance recruitment in the UK in 2016, whilst

offering their predictions on compliance hiring in 2017

CAREER CORNER

they continue to gain traction and generate business from more household names. For permanent opportunities salaries range from £50,000 - £75,000 for AVP Level and £75,000 - £120,000 for VP Level. The equivalent contract roles will pay £250 - £350 per day (AVP) and £350 - £500 per day (VP).

SanctionsSanctions-related roles, including screening and advisory, were heavily recruited for in 2016, with the majority of vacancies coming from global investment banks. As these firms have a global footprint and large volumes of “high risk” clients who may do some business or may be associated with SDN’s or specific jurisdictions, the need for screening SWIFT payments for potential hits has become essential in order to reduce the susceptibility to large regulatory fines. Because of this, risk assessment skills are essential to these roles as judgment calls need to be made on each transaction

EDDMuch like generalist AML positions, EDD roles have remained consistent. However, in 2016 the skillset required has changed. There is now a heavy emphasis on investigative ability such as those from a governmental

agency (i.e. SOCA or the NCA). Performing in depth risk assessments on PEPs, sanctions, ABC or CTF issues requires more than just a KYC analyst. A financial Intelligence and even journalistic background with financial services is advantageous.

As a team, we see 2017 continuing in the same way that 2016 left off, with a continuous hiring stream in the AML/financial crime space and also a steep increase in regulatory hiring, particularly within GDPR & MiFID II projects.

If you wish to see more market updates, salary surveys, regulatory blogs or have any recruitment-related questions or needs, please contact the compliance team at Morgan McKinley.

Morgan McKinley is a global recruitment firm which was established in 1988. The Group employs more than 800 people across Australia, China, France, Hong Kong, Ireland, Japan, Singapore, the United Arab Emirates, and the United Kingdom. The core business recruits professionals in the following specialist disciplines: Tax, Projects and Change, IT PMO, IT Data & Applications, IT Development, Core Finance, Senior Finance, Specialist Finance, Risk, Compliance, Sales & Marketing and Office Support (and Engineering in Ireland).

inCOMPLIANCE®

14inCOMPLIANCE®

15

I have been recruiting within compliance for over five years and have witnessed significant changes in the industry

in that time alone. One thing is for certain: the demand for good regulatory professionals continues to grow.

Whether you are interested in getting into your first compliance position, are an experienced compliance practitioner looking to further your career, or are taking on an ICA qualification, this article should provide some insight into what employers are looking for and how you may want to target opportunities.

Choosing complianceI have spoken with a wide range of compliance professionals, from both a candidate and client perspective. All have different personalities and approaches to regulatory and business standards, usually dependent on their sector. However, they all have broadly similar goals in mind, namely, “the customer”, and keeping the company they work for trading compliantly.

We have all heard the out-dated term “business prevention unit”. I met recently with a CFO who used this term, and suggested that compliance is "a bit like drawing the short straw and having added responsibilities, plus it’s an expensive resource for something we can do ourselves”. This got me thinking: although the term may have been used light-heartedly, does the profession still have this stigma?

I have first hand experience of the fact that compliance used to be a back-office function. I am sure most of you have also experienced this for yourselves. Some of you may also have colleagues

who were moved into compliance from other business areas rather than being made redundant. On the one hand, it is great that companies aren’t making redundancies! On the other, such practices raise the question of whether regulatory requirements are truly being understood and met by everyone in the team.

From a recruitment perspective (and I am aiming this at the junior to mid-level) it is important for us as recruiters to find professionals who choose to be in compliance, rather than those who may have had their hand forced. Likewise it is important for companies to ensure that the right people are in these areas. After all, the FCA expects suitable and robust policies and procedures to be embedded into businesses, which includes advising the business and boards on emerging regulation, identifying operational training needs, and shaping the right culture. Unless you truly understand and buy into compliance from the start, getting the right message across, whilst building and maintaining trust within the business, is easier said than done.

However, I have seen a positive change. I do believe that employers are taking regulatory requirements more seriously. For example, I have noticed a growth in companies hiring to increase team sizes and, broadly speaking, compliance teams are not getting smaller. Moreover, these days we have chief compliance officers / compliance directors sitting on boards and reporting to the chief exec. Indeed, recruiting a credible compliance leader is high on the agenda for start-ups or companies expanding into other markets.

Going back to my meeting with the

CFO, although their remark about the “business prevention unit” may have been a passing comment, they did eventually point out that managing and adhering to FCA requirements is a full time job in itself and, actually, if they are to trade with customers, retail or institutional, they need to show that they value regulations enough to have a dedicated compliance officer on site.

We’ve come a long waySomeone once said to me that: “a good compliance department will always be there. They’ll have good systems and controls in place no matter what regulatory changes occur”. But I do wonder if this was the case 15 years ago.

I took the liberty of speaking to a number of experienced professionals who were around before the FSA/FCA was formed. Back then compliance didn’t necessarily have a voice. Instead, it was down to a responsible “compliance officer” trying to convince their colleagues that they ought to conduct business in a certain way because it was the right thing to do.

Thankfully things are very different now. The FCA has positively impacted our industry by introducing the likes of TCF, which led to conduct risk, which got some companies thinking about the associated reputational risks to their business, all of which have influenced companies to roll these focus areas out internally, in turn driving recruitment needs for industry specialists.

For example the industry currently needs specialists in financial promotions, data protection and records/information management, and financial crime. In fact, apart

CAREER CORNERCAREER CORNER

EvolutionChris Fields considers how the role of the compliance officer has developed and how this affects the career progression of both

current and future compliance practitioners

ICA Fellows’ Dinner

28 March 2017 | Pullman | St Pancras | London

We are delighted to invite all ICA Fellows to our inaugural Fellow’s Dinner. We would like to hear the views of our longest serving members as to how we, as a professional body, can support our members more successfully.

We'd love to get your views on the future development and strategies of the Association, as well as provide you with a great opportunity to network with other Fellows.

As senior practitioners within the industry, we truly value your contribution and we hope you can join us.

There is no charge to attend this event and places are allocated on a first come, first served basis.

inCOMPLIANCE®15

from that the latter, some of these have been flying under the radar until now, but with the General Data Protection Regulation (GDPR) coming into force, the need for these professionals is coming ever more into focus, which we expect will drive salaries up.

Most recently, the senior managers regime (SMR) and the senior insurance managers regime (SIMR) have been in the spotlight. A number of compliance leaders I have spoken with believe that mentalities are changing, which is making their job easier, and truly making the compliance profession a “business partnering role” (I am generalising somewhat as this does already exist in some companies).

The value of qualificationsSo how does all of this link recruitment? We’ve already touched on certain directives shaping key areas that you may want to pursue: GDPR, the Fourth Money Laundering Directive, marketing, and SMR (for the more experienced readers). But ultimately it comes down to looking where you’ll be most needed and actually doing what you enjoy,

which will play to your strengths and skills. I have seen candidates shape very successful careers out of a single compliance discipline, such as financial promotions. I appreciate that everyone will have different paths, but the fundamentals remain the same.

It doesn’t matter how experienced you are, recruiters and employers still look for relevant professional qualifications, as well as how consistent your experience is. And as far as the ICA’s position and recognition within the industry is concerned, most compliance professionals I speak to know, have heard, or – better still – have an ICA qualification. This supports my earlier comment on having true compliance professionals in your team.

One of the topics that often comes up when I’m talking to a hiring manager is exactly this: “It’s not essential, but if they have a professional qualification then even better”. Subconsciously, seeing those three letters next to your name makes a difference.

Remain current and sharpMy advice to you is to attend regulatory

events and meetings, to remain current and sharp with industry topics. Understand what your peers are doing and what their thoughts are. Make sure that you can evidence that you are looking at regulatory developments and news outside of work. An ICA qualification is the best way to do this.

The most respected compliance leaders I know do this and have openly said that this is what they look for when they are hiring.

As a final thought, what you do doesn’t need to be “business as usual” all of the time. Be innovative. Stand out for doing the simple things well. That, with the right approach to educating the company you work for about compliance, will make you stand out and will ultimately progress your career.

Chris Fields manages senior compliance appointments for Broadgate Search. contact him on

CAREER CORNERCAREER CORNER

ICA Fellows’ Dinner

28 March 2017 | Pullman | St Pancras | London

We are delighted to invite all ICA Fellows to our inaugural Fellow’s Dinner. We would like to hear the views of our longest serving members as to how we, as a professional body, can support our members more successfully.

We'd love to get your views on the future development and strategies of the Association, as well as provide you with a great opportunity to network with other Fellows.

As senior practitioners within the industry, we truly value your contribution and we hope you can join us.

There is no charge to attend this event and places are allocated on a first come, first served basis.

inCOMPLIANCE®

16

ICA ANNUAL CONFERENCE

Compliance: Making a difference

James Thomas previews the forthcoming ICA Annual Conference

In the face of a relentless stream of “bad news” stories it is important to remember the essential contribution that compliance professionals make towards their firms’

success, to emphasise the value of this contribution within today’s challenging business climate, and to acknowledge the benefits of compliance to wider society. Compliance is as significant as it has ever been, not only for the avoidance of regulatory and reputational penalties but, increasingly, for leveraging positive business opportunities.

Today, compliance professionals don’t simply manage regulatory risk; they contribute to the wider strategic goals of a firm. With that in mind, the theme of the ICA’s 9th annual conference is “Making a Difference”. The conference will focus on the truly positive aspects of compliance: the ongoing opportunities for the compliance function to influence key stakeholders and outcomes in order to drive businesses forward.

Moreover, the event will not only highlight the contribution of senior compliance practitioners towards strategic decision-making in firms; it will also emphasise the potential for practitioners at all levels to have a positive impact on both business cultures and outcomes.

In the morning session, delegates will hear the perspectives of compliance thought leaders (see Conference highlights), while the afternoon will feature a series of optional practical workshops focused on the development of useful soft skills, including guidance on running teams and on building your professional profile.

The conference offers an excellent opportunity to learn, share experience with colleagues, celebrate how far the profession has come, and uncover new ideas for its continuing development. We hope to see you there!

The conference will take place on Wednesday 29 March 2017, Pullman, St Pancras, London, 09:00 - 13:00. Additional afternoon workshops will take place until 15:30.

Attending the ICA Annual Conference is worth 6 CPD points.

For further details, and to reserve your place, go to: http://www.int-comp.org/events/ica-events/ica-annual-conference/

Conference highlights• In his keynote address, Richard Bistrong CEO, Front-

line Anti-Bribery LLC and Former FCPA Violator & FBI/UK Cooperator, will outline the importance of, and approaches to, Demonstrating the real value of effective compliance.

• Kyril Farbman, European Compliance Director, McDonald's, Rowland Jack, Founder, I Trust Sport, and Tim Glasby, Compliance Manager and MLRO, Europe at Travelers, will provide diverse multi-sector perspectives on Making a difference through compliance.

• Former Olympus CEO turned whistleblower, Michael Woodford, will offer key insights into corporate governance, fraud and whistleblowing, drawn from his experience in bringing to light the £1bn Olympus scandal.

• Talent, targets and reducing corruption: a discussion about how the people make the difference (speaker TBC)

Join the conversation on Twitter #ICAconf

How do we as regulatory and financial crime compliance professionals make a dierence?

At this year’s ICA Annual Conference we will be focusing on the truly positive aspects of compliance: the ongoing opportunities for the compliance function to influence key stakeholders and outcomes in order to drive businesses forward.

Today, compliance professionals don't simply manage regulatory risk: they also contribute to the wider strategic goals of a firm.

For further information on speakers and topics of discussion, and to book your place, please visit www.int-comp.org/annual-conference

How do we as regulatory and financial crime compliance professionals make a dierence?

At this year’s ICA Annual Conference we will be focusing on the truly positive aspects of compliance: the ongoing opportunities for the compliance function to influence key stakeholders and outcomes in order to drive businesses forward.

Today, compliance professionals don't simply manage regulatory risk: they also contribute to the wider strategic goals of a firm.

For further information on speakers and topics of discussion, and to book your place, please visit www.int-comp.org/annual-conference

inCOMPLIANCE®

18inCOMPLIANCE®

19

GIVING BACK

Compliance has grown considerably as a profession in recent years, both in terms of numbers employed and in profile. This owes much to advances in standards

and competences. However, a further factor has been the development and expansion of a community of compliance professionals. Generating and sustaining such a community relies upon individuals “giving back” in one way or another.

I spoke with four ICA Fellows to discover how they have given back and what this has brought them in terms of personal and professional benefits. I also asked them how individuals can support the continuing growth of the profession, and why this remains as important as ever.

Personal and professional developmentGiving back may take several forms (see Box) and, similarly, the underlying motivations (and the resulting rewards) can be diverse. Fereda Sands explains how she first got involved in activities outside of her “day job”. “One of my former bosses encouraged me to start giving back and I’ve been doing so ever since,” she recalls. “It’s important for me as a compliance professional to try to gain some exposure for the profession as a whole. I also want to highlight that the Caribbean region has done so much to ensure that its financial services industry is up to par. But on a purely personal level, when you give back the professional networking and exposure that you get is invaluable. You can’t put a dollar figure on it.”

Barbara Neiger describes the motivation behind her work as “intrinsic”. “Ever since I started my university studies after high school I wanted to write a book and to teach from that textbook,” she explains. “What keeps me motivated now is the reward you get back from the students. I currently supervise three masters students and the ideas they have, and their passion and enthusiasm, untainted by experience, is extremely rewarding. Moreover, the questions that you get asked are completely different: they challenge me, and force me to think in a generic and systemic way.”

As well fulfilling this long-held personal ambition, her contribution towards the growth of the profession through writing, teaching, speaking at conferences and developing international standards has, naturally, also resulted in business opportunities. “I work as an independent consultant, so reputation is important to me. Speaking at conferences

and developing international standards not only gives back to the community but has also helped to reaffirm my reputation, and from that strong reputation further opportunities arise through meeting new people and networking,” she adds.

For Dean Rowan, the motivation is a similar mix of the professional and the personal. “Dealing with the multifaceted and often unrelated issues I encounter in my various capacities has helped to broaden my thinking and allowed me to solve problems in quite unique and new ways,” he explains. “More particularly it has helped me to build relationships at the most senior levels, and gets me in a position to have a voice that actually gets heard.”

Pro bono work also offers him a great sense of personal satisfaction. An example of this is the voluntary work he has undertaken in Ethiopia, working with various government ministries towards elevating the skills and competences within the Ethiopian financial services market and bringing these in line with international best practice standards. “I wrote a 22-page road map which was presented in Parliament,” he explains, “and I’m now working with the Vice Governor of the central bank and the State Minister to pull together a detailed plan. Fundamentally I am trying to assist the country, and that’s very rewarding. My suggestion to all professionals is that stepping beyond your day-to-day responsibilities and moving into a capacity where you can share your skill and experience is not only personally gratifying, it brings value to the next generation of professionals. My goal is to make a genuine difference.”

Supporting future generationsFundamentally, “giving back” in this way is key to the current and future health of the compliance profession as a whole.

In 2016, Marios Skandalis became the first ever compliance professional to be named Banker of the Year – Cyprus, by Acquisition International (UK). “It is actually a pleasant breakthrough for a compliance professional to have won this award,” he explains, “as it rightly positions the compliance function where it stands today and that is within the top category of business functions and sectors of the professional community.”

The award came as the culmination of a three-year programme aimed at transforming the culture at Bank of Cyprus, and within the financial sector in Cyprus more generally, towards a culture of values. Independent recognition

Community matters There are many opportunities for personal and professional growth through giving back to the compliance community,

as James Thomas reports

inCOMPLIANCE®19

of his efforts provides not only a standard for others in the community to aspire to, but also a legacy for future generations of compliance professionals to pick up and build upon. Indeed, as Mr Skandalis says: “Cultural transformation itself doesn’t have an end. It’s an open-ended objective. You must always make sure you take steps forward, but there is no final destination, because in order to maintain this level of culture and values embedded in staff members you need to constantly keep awareness levels high and remind people that the institutional governance is not based merely on rigid policy frameworks or procedural frameworks but rather on values.”

Similarly, Ms Neiger’s contribution is strongly focused on supporting the next generation of professionals, and imparting upon them the skills and knowledge to carry compliance forward. She teaches two Masters-level classes at Lauder Business School. “Teaching is perhaps not what one might immediately think of as ‘giving back’ to the community,” she suggests, “but it is one of the most effective ways in which you can shape awareness, instead of always doing so through scandals and media reports. For this part of my career I want to assist the next generation of managers to perform and to lead legally-compliant teams for the benefit of all stakeholders.”

A further way in which giving back can safeguard the future of the profession is through the creation of support structures that allow professionals to share experience and knowledge on an ongoing basis without fear of negative consequences. As Ms Sands explains: “I got involved with the CRCA because I think as a region we need to stay together, not least because we get so much more done when working together as colleagues, as opposed to competing against each other.” Mr Rowan agrees that associations and voluntary organisations can offer valuable “safe spaces” for knowledge exchange and collaborative work. “The Bahrain Compliance and Anti-Money Laundering group provides a good forum for networking as well as a very safe environment for talking with your colleagues in a non-competitive manner to share how you’re doing with common issues,” he says.

How can I get involved?So what steps should you take if you want to get involved in giving back? “First of all, join your local association,” says Ms Sands. “Then you can volunteer on one of the committees, to participate, or to speak at an event. There are many options and, depending on how many hours you have to commit to it, we can find a place for you.”

At a time when compliance professionals are busier than ever, some may be discouraged from taking on extracurricular responsibilities. The message, however, is that while giving back may not work for everyone, with an organised approach such activities can be a positive complement to your day-to-day work. “It depends on your own capacity to take on challenges, and yes there is a risk that you can spread yourself too thin,” says Mr Rowan. “However, I have a group of like-minded professionals who care about doing something important. They sit around me and support me and provide assistance.”

For Ms Neiger, “it’s really a question of what you’re passionate about”. As a self-employed individual, the key for her has been to stay organised and to maximise the use of her time by outsourcing any functions that are not within her core competence. “I know

exactly what I do not want and I will say ‘no’ to certain things if I’m asked to them. It’s a question of time consumption,” she says. “And remain focused by doing one thing after the other – multitasking is time consuming.” She also suggests that individuals concerned about the time commitment should “start at a small scale” for example through giving external guest lectures on your core experience. “Start small,” she says, “but start.”

If you have been involved in "giving back" and would like to share your experience, contact: [email protected]

GIVING BACK

BOX: Different approaches

Barbara Neiger is a Consultant and founder of neiger.C adisory e.U. She is a Lecturer in Corporate Governance and Corporate Compliance Practice at the Lauder Business School and Managing Partner and Co-Founder of IACRG Services GmbH. She is

Co-author of ISO 37001 Anti-bribery management systems and ISO 19600 Compliance management systems. She is a regular speaker at international conferences and is a member of the Austrian Compliance Association.

Dean Rowan is Chief Risk and Compliance Officer for an Investment Bank and Chairman of the Bahrain Compliance and AML Officers. He is Regional Director of The Professional Risk Managers International Association (PRMIA), which is the ICA equivalent in the

risk world, and an Advisory Board Member for the ICA. He is also an Advisory Board Member for two Bahrain Universities (Ahlia University and PolyTechnic University). He is a frequent professional speaker, market commentator and author, and undertakes pro bono work in Central East Africa.

Fareda Sands is Vice President, Compliance Department at Credit Suisse, and is currently President of the Bahamas Association of Compliance Officers (BACO) and a Director of the Caribbean Regional Compliance Association (CRCA). At a domestic level,

BACO supports the compliance community in the Bahamas through organising lunches, seminars and workshops, which provide both an opportunity to learn and to network. At a regional level, the CRCA’s annual conference covers compliance issues geared specifically to the Caribbean.

Marios Skandalis is Director of Group Compliance at Bank of Cyprus. He founded, and chairs, the annual International Compliance Forum, which takes place in Cyprus with participants from all over the world. He is also the Executive Vice Chairman

of the Board of Transparency International (Cyprus), through which he co-ordinates a number of transparency and anti-corruption events and activities. He has been a keynote speaker at major European anti-financial crime forums and conferences. As Vice President of the Institute of Certified Public Accountants of Cyprus, he has founded a compliance technical committee composed of the chief compliance officers of the major corporations in Cyprus to support the compliance obligations of qualified accountants in Cyprus. He also writes for the local and international press.

THE PANAMA PAPERS

inCOMPLIANCE®

20inCOMPLIANCE®

21

“Offshore tax haven”… what a supremely evocative designation! It conjures up scenes from

1950s-era films of pre-revolutionary Cuba... delightfully rakish raconteurs flaunting opaquely-generated wealth, which they’ve stashed away in SPVs bearing innocuous names... hot jazz (“bah-bah loo!”) and chilled cocktails laced with rum and Angostura bitters... “Taxes? What taxes? All my taxes are away on holiday – ha, ha, ha!”

Recent leaks – typified by the Panama Papers of last year – have largely dispelled this romanticised view of offshore tax havens as being “intriguingly dodgy yet exclusive”. Instead, the popular attitude towards the “offshore-osphere” is currently better described as “righteously indignant and offended”. In the words of Juan Carlos Varela, President of Panama: “It is clear that the affair shined a light into the dark corners of global finance and sparked a worldwide reform agenda. Despite the unfortunate name, the Panama Papers has been good for Panama as well as for the world.”1

PrecedentsThe Panama Papers was by no means an unprecedented event. Quite the contrary; it was only the most recent in a series of similar instances in which pilfered – hacked or otherwise illicitly-removed – proprietary information with compromising and/or sensational implications was divulged to the general public and/or to interested governmental (primarily tax) authorities (see Figure 1).

In this respect, if the definition

articulated by Nassim Nicholas Taleb in “The Black Swan” (2007)2 is to be applied, the Panama Papers scandal was by no means a “black swan” event. Rather, this was an enormous grey or perhaps even white swan. Previous similar events include:• “Cablegate” (2010) – In late

November 2010, WikiLeaks began releasing classified cables that had been sent to the US State Department by 274 of its consulates, embassies, and diplomatic missions from around the world. Dating from December 1966 to February 2010, these cables contained diplomatic analyses from world leaders, and assessments by American diplomats of their host countries and officials.3

• Offshore Leaks (2013) – This disclosure could be described as a full dress rehearsal for the Panama Papers. In April 2013, an International Consortium of Investigative Journalists (ICIJ) report was released, disclosing details of 130,000 offshore accounts. It detailed the results of an ICIJ investigation based on a cache of 2.5m secret records obtained by ICIJ Director, Gerard Ryle. In producing this document, the ICIJ collaborated with journalists from around the world to produce a series of reports published in connection with the ICIJ’s “The Global Muckraker.”4

• Luxembourg Leaks or “LuxLeaks” (2014) – In November 2014, the ICIJ brought to light a financial scandal based on its investigations into confidential information on tax rulings in Luxembourg, which were organised by PricewaterhouseCoopers from

2002 to 2010 to benefit the firm’s clients. This investigation resulted in the disclosure of tax rulings for over three hundred multinational companies based in Luxembourg. The scandal attracted international attention to tax avoidance schemes in Luxembourg and elsewhere, and contributed to the implementation of measures to regulate tax avoidance schemes beneficial to multinational companies.5

• Swiss Leaks (2015) – In February 2015, the ICIJ website released “Swiss Leaks: Murky Cash Sheltered by Bank Secrecy”, detailing the results of an investigation conducted by over 130 journalists in Paris, Washington, Geneva, and in 46 other countries. The report alleged that, between November 2006 and March 2007, €180.6bn passed through HSBC accounts held in Geneva by over 100,000 clients and 20,000 offshore companies. The data for this period came from files surreptitiously removed from HSBC Private Bank in late 2008 by Hervé Falciani, a former employee, which he subsequently handed over to French authorities. The ICIJ’s “Swiss Leaks” report concluded that the bank profited from its clients’ tax evasion practices.6

Two equally vital questionsA favourite didactic question of lawyers and financial forensics professionals in explaining their methodologies is: cui bono? (i.e. to whose benefit?). But when judging the overall utility of offshore tax havens to the global economy, a second

Coming to the surface

One year on from their release, Vladimir Berezansky considers the impact of the Panama Papers

THE PANAMA PAPERS

inCOMPLIANCE®21

(sadly often ignored) question must also be considered: cui detrimento? (i.e. to whose detriment?). Neither of these questions is rhetorical, and they are equally vital to an adequate assessment of the broader significance of offshore tax havens.

One reason why offshore tax havens are ignored and/or discreetly accessed by so many “upstanding” citizens of so many Western democracies is a collective failure of logic regarding their tangible and measurable detriment to the global economy. Indeed, invoking a concept as arguably insubstantial as “detriment to the global economy” – beyond the ranks of those professionally sensitised – can be a tough slog even today, much less a decade or two ago when the problems engendered by offshore tax havens first began to fester and multiply. A major inhibiting factor in assessing the relative benefits and detriments of offshore tax havens to the global economy is the continuing absence of reliable statistics regarding the total amount of funds and/or in-kind assets that correspond to this category. Putatively sound estimates range between $21tn and $32tn7, but the implied margin of error in such estimates renders them essentially useless for any purpose other than shock value.

To be clear, offshore tax havens have entirely legitimate and beneficial business purposes. But these circumstances are often forgotten, usually as a result of collective emotional whiplash caused by careening from the “intriguingly dodgy yet exclusive”

perceptions (as parodied above) to the “righteously indignant and offended” mindset that takes hold after yet another scandal or exposé – especially on the scale of the Panama Papers – erupts via the world’s media outlets.

Low- or no-tax havens and relative national advantageTo revert briefly to basic principles: every sovereign nation has essentially complete discretion over its domestic revenue-generating infrastructure (i.e. articulating the type and rates of taxes, customs duties, administrative fees, etc that shall apply within its territorial borders and to its citizens). One of the many legitimate policy goals of a nation’s revenue-generating infrastructure is enhanced competitiveness designed to attract foreign investment.

Not surprisingly, national governments tend to shape their revenue-generating infrastructures to encourage foreign investment that is most consistent with the contours of their domestic economies. Territorially large nations with big populations tend to use their tax codes to encourage so-called foreign direct investment (FDI) in large-scale infrastructure projects, often on a jointly-managed basis in which issues such as project cost allocations, technology transfers (if relevant), and profit sharing arrangements are carefully detailed.

A geographically smaller, more remote and/or less populated country usually needs to compete for foreign investment (often as a major supplement

to its domestic revenue base) in “niche” sectors of the global economy, i.e. by emphasising its specific history, culture and geography as a tourist destination and by heavily promoting natural resources and products that might be either unique or of high value-added net worth (such as rare gems, cutting edge electronics, Swiss watches, etc).

From Watergate to 9/11During the three decades beginning approximately with the Watergate Scandal and ending quite abruptly with 9/11, Western governmental investigators, law enforcement authorities and regulators – primarily those focused on enforcing tax, banking and securities markets regulations – became increasingly aware of the trend towards “anonymising” the seed funds and the proceeds of criminal activity within the legitimate funds flows of entirely legal business and commercial activity.

During this period, the realisation that profits generated from longstanding and well-known international criminal structures – those engaged primarily in narcotrafficking, the “white slave” trade (as it was then known) and other illicit commercial activity such as smuggling – were viewed largely as a nuisance that required appropriately aggressive intervention by law enforcement and the prosecutorial power of all affected nations. The policy construct that drove Western and other national governments to take measures deemed necessary at this time could be described as not dissimilar to a

inCOMPLIANCE®

22inCOMPLIANCE®

23

farmer’s approach to weed control or a homeowner’s struggle with rodents and insects.

Compliance to the rescue!With 9/11 and related terrorist-instigated tragedies such as the 07/07 bombings in London, Western governments rapidly recalibrated their national security and law enforcement strategies. The ease with which international terrorist groups such as al-Qaeda were able to “anonymise” their funds was suddenly identified as a global security threat, and sweeping measures were demanded for addressing this threat immediately and definitively. Hence, the innocuous-sounding Watergate-era mantra “Follow the money” morphed into the increasingly invasive and sweeping (i.e. extraterritorial) policy imperatives now known as Anti-Money Laundering (AML), Know Your Client (KYC) and, most especially, Countering (or Combating) the Financing of Terrorism (CFT).

On so many different levels 9/11 was a watershed moment in world history. This includes, of course, the virtual conscription and militarisation of the middle and back offices of licensed and regulated financial institutions, and the emergence of compliance as a conceptually-distinct function and area of expertise. Indeed, it would not be a distortion to assert that compliance, in macroeconomic terms, was a demand-driven function for which there was initially no supply. Specifically, the unprecedented and fundamentally innovative regulatory obligations created by the post-9/11 esprit de guerre and imposed on major

global banks – eventually, on the entire financial services sector – created (or perhaps identified) a vacuum that needed to be filled; and it was filled by the compliance function.

Following the 9/11 call to arms, another decade was needed to achieve full articulation and deployment of financial regulatory compliance as a comprehensive array of robust internal policies and procedures designed to mitigate assessed degrees of exposure to specifically identified regulatory (and, over time, reputational and other) risks. By the time of the 2008-2009 global financial crisis, most banks, investment firms, insurance companies and other licensed financial institutions at least understood what “global best practices” required of them in their respective markets, even if meeting such exacting standards was not a fully achieved goal in specific instances.

Concentric circles of influenceLed primarily by the US and UK investigative and financial regulatory authorities, North American, Western European and mature Asian global banks, securities exchanges and capital markets undertook and fulfilled a comprehensive programme aimed at ensuring the continuity and interconnectedness of domestic financial regulatory regimes for individual nations.

Back when fundamental principles and metrics for robust compliance enforcement mechanisms were being promulgated by national legislative initiatives, international efforts such

as the Wolfsberg Group, the Financial Action Task Force (FATF / GAFI) and the Basel Accords were fostering cross-border consensus on relevant financial regulatory standards to facilitate maximum uniformity and efficiency of multinational banking and securities market activities.

It is important to understand that this process began first between and among financial services regulators and licensed financial institutions in the US, the UK, Western Europe and several mature Asian markets. The first concentric circle beyond this “inner core” consisted of the mainly contiguous large emerging market players in Latin America, Eastern Europe / Eurasia, the Middle East and Asia. Only after the gradual integration of this second concentric circle was well underway did the influence of global best practices finally reach the more far-flung jurisdictions, including many – but not all – of the offshore tax havens.

Progress towards harmonising most of the world’s major, second-tier and outlying banking and financial services markets was anything but linear or uniformly successful. To the present day, for example, FATF / GAFI continues to identify (“name and shame”) so-called “high risk and non-cooperative jurisdictions”8 and builds consensus towards full implementation of global best practices within a tolerable bandwidth of local diversity.

Not surprisingly, offshore tax havens have been among the most reluctant – even recalcitrant, at times – jurisdictions to import and implement robust financial regulatory compliance. Over time, the “pincers” of bottom-

THE PANAMA PAPERS

Figure 1: Volume of data compared to previous leaks

©Süddeutsche Zeitung, SZ.de, April 2016, reproduced with permission

inCOMPLIANCE®23

up momentum – most especially, the aggressive extraterritoriality of certain national players (primarily the US and the UK) – in combination with top-down pressures exerted by a growing array of international and continental / regional organisations – including, quite recently, the Multilateral Convention on Mutual Administrative Assistance in Tax Matters9 and its implementing mechanism, the Common Reporting Standard (CRS) – have borne tangible results throughout much of the offshore world of tax havens.

The foregoing notwithstanding, one cannot afford the luxuries of naïveté or rudimentary linear thinking. The processes of multilateral (institutional) and cross-border (bilateral national) brow-beating of a steadily diminishing number of recalcitrant offshore jurisdictions into compliance with a gradually increasing minimum threshold for qualifying as having adopted global best practices are meeting with increasingly stiff resistance. This should surprise no one. As discussed previously, there are no truly reliable – much less proven – estimates of the amount of offshore wealth that exists. Certainly this “dark matter” of our global financial universe includes enough funds to coerce key persons and institutions to forbear from cutting off the Hydra’s last head.

Eruption and aftermathThe timing of the Panama Papers scandal was quite fortuitous and possibly instrumental in focussing global public attention on the heretofore little-noticed world of offshore tax havens. Given the interplay of disparate forces eventually coalescing on the “offshore-osphere” as an object of collective concern, the overall impact of the Panama Papers might have been blunted had this scandal erupted any earlier. As considered previously, there was nothing conceptually novel or distinctive about the Panama Papers (except for the volume of data divulged).

Approaching the one-year mark of this scandal’s spectacular explosion, it seemed at first as though most of the immediate fallout would be surprisingly meagre. After the initial eruption of the offshore island’s dreaded “righteously

indignant and offended” volcano, the native population, fearing the worst, took to their boats and relocated for an indefinite period to several neighbouring inhabited islands of the “intriguingly dodgy yet exclusive” archipelago... and waited.

A few of the braver souls among the displaced population undertook occasional exploratory forays to their home island, where they found clear evidence of the volcano’s damage. Government investigators and an evidently large contingent of law firms and auditors had left unmistakeable traces of their ravages: the Prime Minister of Iceland had abruptly resigned from office; and the Presidents of Argentina and Russia as well as the Prime Ministers of Pakistan and (at the time) the UK all felt themselves compelled to issue blanket denials of illegal relationships with the devastated offshore island. In the aggregate, a ponderous amount of structural damage had occurred, to be sure; but with each succeeding visit, the recon teams were bringing gradually more encouraging reports back to the displaced population.

But just a day or two before their offshore island was to be declared once again safe to inhabit, the natives were horror-struck to learn that an even more powerful earthquake on the Brazilian mainland had wrought far more devastation than the volcano which had originally forced them from their homes.

At the time of writing, Panamanian prosecutors have arrested the founding partners of Mossack Fonseca, the firm at the centre of the Panama Papers leak. According to Kenia Porcell, Panama’s

Attorney General, the decision to arrest Ramón Fonseca Mora and Jürgen Mossack was related to the Panamanian bank regulator’s seizure of FPB Bank in connection with its alleged involvement in Latin America’s largest ever corruption investigation, Lava Jato, or “Operation Car Wash”. Lava Jato is a Brazilian bribery probe involving prosecutors in numerous jurisdictions who are investigating allegations of systematic bribery of public officials by Petrobras (Petróleo Brasileiro SA), Brazil’s state-run oil company, and Odebrecht, a Brazilian-listed engineering company (the largest of its kind in Latin America).

Regardless of where these investigations may ultimately lead, there seems little room for doubt that the Golden Age of the “offshore-osphere” has waned, and those who continue to make use of their “tax optimisation” features now have the burden of proving that their decisions are at least legal, if not perhaps entirely ethical.

Vladimir Berezansky was one of the first foreign professionals to bring Western (US, UK, EU) regulatory compliance

leadership to the Russian/CIS/CEE financial services market. He has experience in Russia/CIS and Eastern Europe, as well as Cyprus, Switzerland and in London’s financial markets. Among his specialisations, he is a recognised expert in structured offshore Russian wealth.

THE PANAMA PAPERS

1. The Miami Herald, 2 January 20172. See inCOMPLIANCE issue 27, p.193. https://en.wikipedia.org/wiki/United_States_diplomatic_cables_leak 4. https://en.wikipedia.org/wiki/Offshore_Leaks 5. https://en.wikipedia.org/wiki/Luxembourg_Leaks 6. https://en.wikipedia.org/wiki/Swiss_Leaks 7. See, e.g., https://trofire.com/2015/07/31/the-worlds-wealthy-are-hiding-

up-to-32-trillion-in-offshore-accounts- 3/8. http://www.fatf-gafi.org/publications/high-riskandnon-

cooperativejurisdictions/?hf=10&b=0&s=desc(fatf_releasedate)9. http://www.oecd.org/tax/automatic-exchange/international-framework-

for-the-crs/10. http://www.bbc.com/news/world-latin-america-38947440 and http://

www.comp-matters.com/article.php?id=173252#.WKdDO4VOK7U

inCOMPLIANCE®

24inCOMPLIANCE®

25

4MLD

Coming into focusMatt Timmons and Keily Blair consider the emergence and

evolution of corporate disclosure requirements under the 4MLD

inCOMPLIANCE®25

4MLD

As part of a sweeping tide in global regulatory and legislative reform concerning corporate transparency, the Fourth Money Laundering

Directive (4MLD) seeks to bolster corporates’ defences against tax evasion, money laundering and terrorism. By June 2017, all European Economic Area (EEA) member states must have implemented their obligations under the Directive. Although the EU advocates taking a “risk-based approach” to compliance with 4MLD, the reality is that the implementation of the Directive has far-reaching implications for financial institutions and other businesses operating across the EEA, in particular in relation to tax transparency.

4MLD applies to a wide range of entities that are deemed to be at risk of being involved in money laundering or terrorist financing (“obliged entities”). The list of obliged entities includes credit and financial institutions, auditors, external accountants and tax advisers, estate agents, certain legal professionals (when they participate in any financial or real estate transaction), trust or company service providers, providers of gambling services, and persons trading in goods to the extent that payments are made or received in cash in an amount of €10,000 or more (often referred to as “high value dealers”).

At the same time as considering country-by-country reporting (CbCr), legislative changes as a result of base erosion and profit shifting (BEPS), and the requirement to disclose tax strategy, in-house teams now face a new compliance demand, designed to complement the broader trend of disclosure regarding the way UK and global businesses are structured and governed.

UBO registers 4MLD increases both the scope and the depth of the existing anti-money laundering regime. One of its more onerous provisions is the requirement that member states implement a new Ultimate Beneficial Ownership (UBO) register to apply to all companies and LLPs (in some cases LPs and Trusts). As 4MLD is a Directive, as opposed to a Regulation, member states must enact their own domestic legislation to implement it. This will create local divergences complicating compliance for corporations with a footprint across the EEA. These businesses must now comply with up to 31 UBO registers, each with differing requirements and local nuances, such as filing and public disclosures.

To date not all member states have released legislative proposals, which will further complicate the job of in-house teams charged with compliance. For example, Luxembourg

has yet to provide concrete proposals; Spain has a newly-elected government and although legislation is promised it has not been forthcoming; and the Swedish government has promised a consultation paper to be released early in 2017. In those jurisdictions where draft or proposed legislation has been published it is clear that there are already differences emerging.

United KingdomSince April 2016, UK businesses have been required to comply with the people with significant control (PSC) regime. This required all UK companies/LLPs (whether UK- or foreign-parented) to disclose who ultimately controls and owns the business. Despite this existing requirement, a review of public filings to date would indicate that the PSC regime has not been properly understood and there is still some way to go before companies are compliant with 4MLD. A consultation on the implementation of the Directive along with proposed amendments to the PSC regime concluded on 10 November 2016.

Germany Expected implementation of 4MLD into national law will occur during the first half of 2017. The published consultation proposes that:• A 25% threshold is applied for holding of shares or voting

rights in respect of being identified as a beneficial owner• Information on beneficial ownership will be maintained on

the transparency register• Information to be provided on the register will include:

first name, surname, full date of birth, residence of the beneficial owner and the extent of interest in the entity in question

• Where information on the beneficial owner is not available from any other existing public register, the legal representative of a corporate entity is obliged to obtain information in respect of the identified beneficial owner. They are also required to update the register and confirm annually that the information on the register is correct and up to date.

The Netherlands The current proposed positions are: • There will be a public register and the information

disclosable on that register in respect of identified beneficial owners will be similar to the UK requirements

• Users will have to register online, will be charged a fee to inspect the records, and users other than specifically-designated authorities will only have access to limited beneficial owner information

• Similar to the UK, in exceptional circumstances the details of identified beneficial owners will not be disclosable Circumstances will be assessed on a case-by-case basis

• The submission of beneficial ownership information will rest with the company and beneficial owners are obliged to cooperate

• Failure to submit, late-submission or incorrect / incomplete submission of data is likely to give rise to a financial penalty and/or criminal penalties.

The implementation of the Directive has far reaching implications for financial institutions and other businesses operating across the EEA

inCOMPLIANCE®