company presentation -...

TRANSCRIPT

Company Presentation

April 2017

DISCLAIMER

The information contained herein pertaining to SIBUR (the "Company") has been provided by the Company solely for use at this presentation. By attending this presentation, or by reading these presentation slides, you agree to be bound by the limitations set out below. This presentation does not constitute or form part of, and should not be construed as, an offer, solicitation or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for, any securities of the Company, nor shall any part of it nor the fact of its distribution form part of, or be relied on in connection with, any contract or investment decision relating thereto. No representation or warranty, either express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness, correctness or reliability of the information contained herein. It should not be regarded by recipients as a substitute for the exercise of their own judgment. The Company accepts no responsibility for any losses howsoever arising, directly or indirectly, from this presentation or its contents. The material contained in this presentation is presented solely for information purposes and is not to be construed as providing investment advice. As such, it has no regard to the specific investment objectives, financial situation or particular needs of any recipient. There may be material variances between estimated data set forth in this presentation and actual results, and between the data set forth in this presentation and corresponding data previously published by or on behalf of the Company. This presentation contains forward-looking statements, including (without limitation) statements containing the words "anticipates," "expects," "intends," "may," "plans," “forecasts,” "projects," "will," "would", "targets,“ “believes” and similar words. These statements are based on the current expectations and projections of the Company about future events and are subject to change without notice. All statements, other than statements of historical fact, contained herein are forward-looking statements. Forward-looking statements are subject to inherent risks and uncertainties, such that future events and actual results may differ materially from those set forth in, contemplated by or underlying such forward-looking statements. The Company may not actually achieve or realize its plans, intentions or expectations. There can be no assurance that the Company's actual results will not differ materially from the expectations set forth in such forward-looking statements. Factors that could cause actual results to differ from such expectations include, but are not limited to, the state of the global economy, the ability of the petrochemical sector to maintain levels of growth and development, risks related to petrochemical prices and regional political and security concerns. The above is not an exhaustive list of the factors that could cause actual results to differ materially from the expectations set forth in such forward-looking statements. The Company and its Affiliates are under no obligation to update the information, opinions or forward-looking statements in this presentation.

2

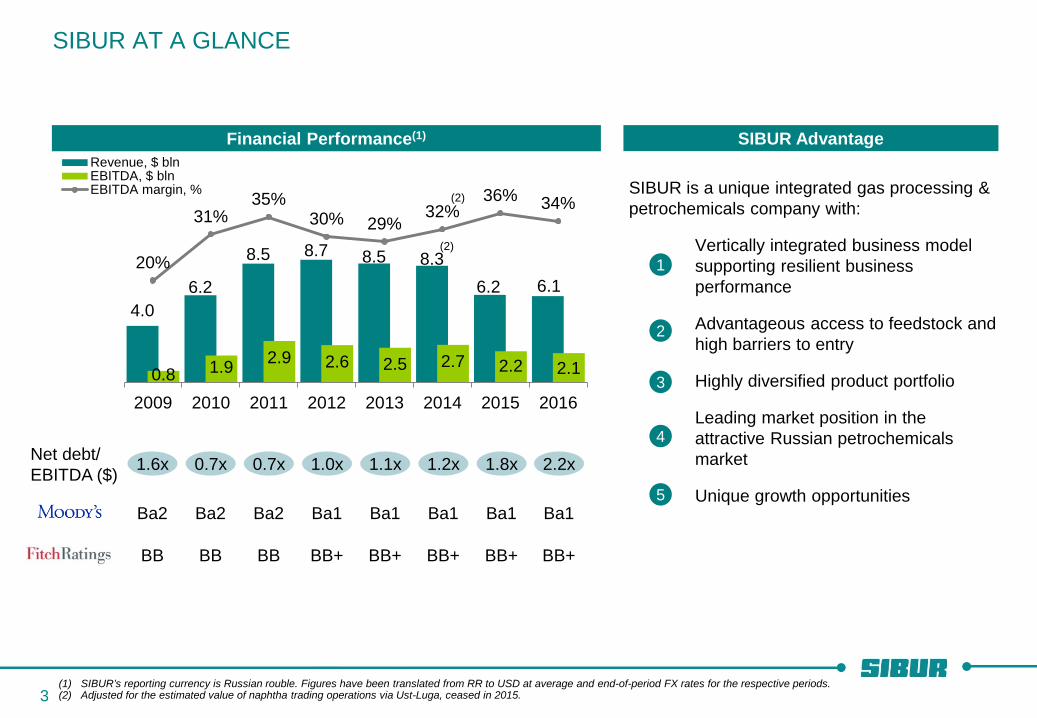

4.0 6.2

8.5 8.7 8.5 8.3 6.2 6.1

0.8 1.9 2.9 2.6 2.5 2.7 2.2 2.1

20%

31% 35%

30% 29% 32%

36% 34%

2009 2010 2011 2012 2013 2014 2015 2016

Revenue, $ blnEBITDA, $ blnEBITDA margin, % (2)

(2)

SIBUR AT A GLANCE

(1) SIBUR’s reporting currency is Russian rouble. Figures have been translated from RR to USD at average and end-of-period FX rates for the respective periods. (2) Adjusted for the estimated value of naphtha trading operations via Ust-Luga, ceased in 2015.

Financial Performance(1)

Net debt/ EBITDA ($)

SIBUR is a unique integrated gas processing & petrochemicals company with:

Vertically integrated business model supporting resilient business performance

Advantageous access to feedstock and high barriers to entry

Highly diversified product portfolio

Leading market position in the attractive Russian petrochemicals market

Unique growth opportunities

SIBUR Advantage

1

2

3

4

5

1.6x

Ba2

BB

0.7x

Ba2

BB

0.7x

Ba2

BB

1.0x

Ba1

BB+

1.1x

Ba1

BB+

1.2x

Ba1

BB+

1.8x

Ba1

BB+

3

2.2x

Ba1

BB+

4 (1) Numbers based on 2016 FY. (2) Associated petroleum gas is oil-based feedstock. (3) Natural gas liquids include raw NGL, LPG (liquefied petroleum gas), naphtha are gas-based feedstock.

LOGISTICS CLIENTS SUPPLIERS

NGLs(3) (6.2 mtpa) Natural gas (18.2 bcmpa)

Feedstock (3.4 mtpa)

Feedstock &

Energy

Gross sales: ₽ 196 bln

EBITDA margin:

30.9%

EXTERNAL SOURCING OF

HYDROCARBON FEEDSTOCK

APG(2)

(21.9 bcmpa)

NGLs(3)

(3.4 mtpa)

Olefins & Polyolefins Gross sales:

₽ 107 bln EBITDA margin:

45.5%

Plastics, Elastomers & Intermediates Gross sales:

₽ 132 bln EBITDA margin:

23.8%

PETROCHEMICALS

1. Vertically integrated business model supporting resilient business performance

SIBUR OPERATES A UNIQUE VALUE CHAIN(1)

(1.1 mtpa)

(2.3 mtpa)

YAMAL-NENETS AUTONOMOUS AREA

KHANTY-MANSI AUTONOMOUS AREA

Purovsky GCP (NOVATEK)

Gubkinskiy GPP

Muravlenkovskiy GPP

Vyngapurovskiy GPP

Nyagan GPP

Nizhnevartovskiy GPP

Belozerniy GPP

Yuzhno-Priobskiy GPP

Tobolsk production site

PYT-YAKH

TOBOLSK

PUROVSK

NOYABRSK

TYUMEN REGION

Yuzhno-Balykskiy GPP

UNIQUE LARGE-SCALE TRANSPORTATION AND FEEDSTOCK PROCESSING INFRASTRUCTURE IN WESTERN SIBERIA

2. Advantageous access to feedstock and high barriers to entry

SIBUR / third-party gas processing plant (GPP)

SIBUR / third-party compressor station

third-party gas condensate plant

SIBUR gas fractionation unit (GFU)

SIBUR propane dehydrogenation facility (PDH)

SIBUR polymers production SIBUR / third-party loading rack

SIBUR owns and operates the largest and most extensive infrastructure for processing and transportation of feedstock in Western Siberia:

8(1) out of 10 gas processing plants (GPP)

APG processing capacity of 25.4(1) bcm p.a.

Raw NGL processing capacity of 8.0 mmtpa at flagship gas fractionation unit (GFU) in Tobolsk (out of 9.5 mmtpa of the Company’s total capacity)

Pipeline network of 2,708 km

4 railway loading racks (out of 6 operated by Feedstock & Energy segment)

ECONOMIES OF SCALE

INTEGRATED INFRASTRUCTURE HIGH BARRIERS TO ENTRY

SIBUR / third-party power plant

SIBUR / third-party APG pipeline Gazprom condensate pipeline SIBUR / Gazprom natural gas pipeline SIBUR raw NGL pipeline truck transportation

5 (1) Including Yuzhno-Priobskiy GPP operated under JV.

Hyd

roca

rbon

Fee

dsto

ck

Purc

hasi

ng E

xpen

ses

SECURED ACCESS TO FEEDSTOCK

Notes: (1) Billion cubic metres. (2) 49% of APG supplied by Rosneft to the GPPs of its JV with SIBUR. In March 2014, SIBUR gained full control over the JV via acquisition of a 49% stake from Rosneft. (3) 49% of raw NGL produced at the GPPs of the JV between SIBUR and Rosneft. These volumes were obtained by Rosneft and sold to SIBUR. In March 2014, SIBUR gained full control over

the JV via acquisition of a 49% stake from Rosneft. (4) IHS CERA. (5) CDU TEK.

13.0 13.9 19.4

21.2 21.9 18.7 19.6

20.8

2012 2013 2014 2015 2016

0

10

20

30

40

50

60

2005 2010 2015 2020 2025 20300

20

40

60

80

100

2005 2010 2015 2020 2025 2030

1.9 2.1 2.2

3.4 3.6 2.6 2.8

3.4

2012 2013 2014 2015 2016

24.7 25.6 25.8 27.9 26.3

7.3 9.4 20.5 22.4 22.4 32.0 35.0 46.4 50.3 48.7

2012 2013 2014 2015 2016

Outlook for Feedstock-Rich Gas Production in Russia(4)

90% of APG supplies for 2017 guaranteed under multi-year contracts WA maturity of supply

contracts – 15.1 years

NOVATEK Gazprom Rosneft Gazprom Neft

RussNeft

Key Supply Contracts as of 31 December 2016

APG NGLs

93% of NGLs supplies for 2017 guaranteed under multi-year contracts WA maturity of supply

contracts – 16.9 years

SIBUR’s Feedstock Purchases

Associated Petroleum Gas Unstable Gas Condensate mln tonnes 2016 APG flaring –

c.13%(5) of produced volumes

bcm(1)

mln tonnes

bcm(1)

SIBUR’s purchases Purchases from Rosneft in JV(3)

SIBUR’s purchases Rosneft’s share in APG purchases(2)

₽ bln

APG NGLs

APG

N

GLs

2. Advantageous access to feedstock and high barriers to entry

6

(1) Based on 2016FY. (2) External sales. (3) LPG, naphtha and raw NGL.

F&E (Feedstock & Energy) O&P (Olefins & Polyolefins) PE&I (Plastics, Elastomers & Intermediates)

7

3. Highly diversified product portfolio

DIVERSE DRIVERS AND END-MARKETS(1)

Key end-markets

Petrochemicals, fractionation FMCG, construction, packaging

Residential applications

Power, utilities

FMCG, construction, automotive, fuels, chemicals, petrochemicals

Key drivers

Commodity cycle, global oil prices Transportation costs

and export duties

Indexation of regulated natural gas prices

Import substitution Demand/supply in multiple end-customer

markets

Demand/supply in multiple end-customer markets Natural rubber prices for synthetic rubbers

Correlation with oil prices S

Currency nature

$ ₽ Domestic sales Export sales

EBITDA (₽ bln) and

margin

61 49

32

Liquids(2) Natural Gas

Revenue(2) structure 100%

30%

70% 24%

76% 36%

64%

30.9% 45.5% 23.8%

51 49

LDPE

65

35

Ole

fins

&

Poly

olef

ins

Plas

tics,

ela

stom

ers

and

inte

rmed

iate

s

LEADING PLAYER IN THE HIGH-GROWTH DOMESTIC MARKET

2015

2015

2015

%

%

MEG

Others SIBUR’s share

Growth Fundamentals

Kg per Capita Consumption of Polyolefins

Polypropylene Polyethylene (LDPE)

Source: IHS, Market Report, IISPR.

SIBUR’s Share in Russia’s Production Capacity

4

4

6

8

Russia

China

Eastern Europe

Western Europe

7

14

13

18

Russia

China

Central Europe

Western Europe

72

28

BR

47 53

SBR SBS

% % %

100

%

4. Leading market position in the attractive Russian petrochemicals market

44 56

Polypropylene

%

17

83 55

45 %

PET

%

Expandable polystyrene

8

Russia Consumption Growth Outlook

CAGR, 2016-2022

5.0%

3.3%

3.3%

2.5%

2.4%

2.0%

2.0%

1.9%

LLDPE

PP

MEG

PVC

HDPE

PET

EPS

LDPE

Western Europe

PETROCHEMICALS

FEEDSTOCK

PETROCHEMICALS AND END-PRODUCTS

FEEDSTOCK

>6,000 km

>4,000 km

Long distances with infrastructural constraints

Significant export duties for naphtha and LPG in Russia Ample feedstock

base

Significant export duties for naphtha and LPG in Russia

SIBUR’s production assets China and Northeast Asia

EFFICIENT MONETISATION OF STRANDED FEEDSTOCK

5. Unique growth opportunities

SIBUR’s petrochemical hub

in Tobolsk

Naphtha price(1)

Notes: (1) USD per tonne. (2) USD per tonne of polyethylene, assuming naphtha consumption ratio of 2.2x, and net of by-product credits. (3) USD per tonne of polyethylene. (4) USD per tonne of LPG-mix (propane and butane). (5) USD per tonne of olefins, assuming LPG-mix consumption ratio of 1.35x.

Transportation to W.Europe(3)

PE

pric

e in

Wes

tern

Eur

ope

Illustrative HDPE price build-up

LPG price in Europe(4)

Transport & export duties(4)

LPG price in Tobolsk(4)

LPG feedstock cost in Tobolsk(5)

HDPE production cost net of by-product credits(3)

Wes

tern

Eur

ope

Tobo

lsk

Naphtha feedstock cost(2)

Total cost for producers(3)

HDPE production cost (3)

Total cost for producers(3)

9

(1) Source: IHS 2015, SIBUR estimates.

ZAPSIBNEFTEKHIM (ZAPSIB-2): EXPANSION OF POLYOLEFINS PRODUCTION IN TOBOLSK

5. Unique growth opportunities

10

Strong Position on the Global Cost Curve (2019)(1) HDPE and LLDPE Spreads to Feedstock

0

500

1,000

1,500

2,000

2,500PE CFR China - LPG spread LPG, West Europe, CIF NWE

PE HDPE Blow Moulding CFR China PE LLDPE Film CFR China

$ per tonne

Project Overview

Propane

Ethylene 1,500 Ethylene

cracking unit (ECU)

’000 tonnes

Ethane

N-Butane

HDPE - 350

HDPE - 350

LLDPE / HDPE - 400

LLDPE / HDPE - 400

PP - 500 Propylene

525

ECU

CONFIGURATION

PE Units

PP Unit

LICENSOR EP C

1.5 mtpa of ethylene 525 ktpa of propylene 100 ktpa of crude C4

1.5 mtpa of PE

0.5 mtpa

ME Avg NA Avg

NEA Avg WE Avg

0

500

1,000

1,500

2,000

2,500

0.0 50.0 100.0 150.0 200.0

1. Zapsibneftekhim 2. Tobolsk-Polymer 3. Sibur-Kstovo 4. Tomskneftekhim

ME – Middle East, NA – North America, NEA – Northeast Asia, WE – Western Europe

$ per tonne

Cumulative capacity (‘000 000 tonnes)

Ethylene Propylene

1 1

2 3 3 4 4

NA Avg

NEA Avg

ME Avg

WE Avg

11

ZAPSIB-2 PROGRESS UPDATE

Progress Update as of 28 February 2017, %

21

58

87

100

Construction

Procurement

Detail Engineering

FEED

Project Residual Budget for 2017-2020(1)

$ 5.8 bln

$ 30%

€ 30%

₽ 40%

Funding Sources Project Budget

65%

10%

25%

SIBUR own funds

NWF and RDIF(2)

ECA(3)

(1) Data as of 31 December 2016. Numbers and respective percentages calculated based on exchange rates as of 31 December 2016; RR/USD at 60.7, RR/EUR at 63.8. (2) Cash balances as of 31 December 2016. NWF stands for National Wealth Fund. RDIF stands for Russian Direct Investment Fund. (3) Undrawn amount of ECA (Export Credit Agency).

Overall progress as of 28 February 2017: 41%

Overall progress by major units as of 28 February 2017:

Steam cracker – 44%

PE unit – 30%

PP unit – 33%

RR 193 bln invested by 2016EY

More than 11,000 construction workers at the site as of 28 February 2017

Please follow the link to see the video of the construction site: https://www.sibur.ru/en/press-center/video/

5. Unique growth opportunities

1. Business Description: Additional Details

2. Key Recent Financials

3. Market Prices

12

EXTENSIVE ASSET BASE THROUGHOUT RUSSIA

Salekhard ●

Kemerovo ●

Tyumen ●

Omsk ●

Samara ● ● Ufa

Voronezh ●

● Saint-Petersburg

Tver●

Tula●

● Nizhniy Novgorod

Kursk●

● Tomsk Krasnoyarsk ●

● Purovsk Moscow●

Tobolsk ●

WESTERN SIBERIA

WESTERN SIBERIA Largest oil & gas

reserves region in Russia

22 tcm

48 bln bbl Proven oil reserves

Proven gas reserves

Joint Ventures

facilities operated under JVs

Energy Products

gas processing & fractionation, MTBE & other fuel additives

Petrochemicals

basic polymers synthetic rubbers plastics & organic synthesis

intermediates other chemicals

Logistics

raw NGL pipeline transshipment facility in Ust-Luga operated by SIBUR

Khanty-Mansiysk ● ● Perm

13

● Svobodny

ENERGY PRODUCTS

C1 C2

Methane (gas) Ethane (gas)

C3-4 C5-6 C7+

Propane (gas / liquid) Butane (gas / liquid)

Isobutane (gas / liquid)

Pentane (liquid) Isopentane (liquid)

Hexane (liquid)

Heavy fractions

Liquefied Petroleum Gas (LPG) Naphtha

Raw Natural Gas Liquids (Raw NGL)

Oil

Natural Gas

Associated Petroleum Gas (APG)

fractions can be used as petrochemical feedstock

14

MULTIPLE PRODUCTS, GEOGRAPHIES AND CUSTOMER GROUPS

Over 1,400 large customers…

…from more than 80 countries

…representing diverse range of end-customer industries

…with low customer concentration

…and balanced contract / spot sales structure

5%

6%

16%

25%

20%

58%

Plastics, Elastomers& Intermediates

Olefins & Polyolefins

Feedstock & Energy

Top-10 Largest customer

Customer Concentration Contract / Spot Structure of Sales 2016 2016

62% 54% 39%

38% 46% 61%

Feedstock &Energy

Olefins &Polyolefins

Plastics,Elastomers &Intermediates

Spot Contract

58 29

7 5 1

22

11

7 15 4

11

10

6 5

9

Total Group Sales Breakdown

Other

Asia CIS

Europe Russia

Other

LPG

Naphtha

Natural gas

MTBE and fuel additives

BOPP films

PP, PE

2016

%

By products By region

15

%

Plastics and organic synthesis products

Elastomers

Intermediates and other chemicals

24

Skovorodino

Chayandinskoye

Kovyktinskoye

Blagoveshchensk Irkutsk

Amur GPP (Gazprom)

Amur Chemical Plant (SIBUR)

WESTERN SIBERIA

EASTERN SIBERIA

Svobodny

Power of Siberia Gas Pipeline

GAZPROM AND SIBUR – JOINT INVESTMENT PROJECT ON CONSTRUCTION OF GAS PROCESSING AND CHEMICAL HUB IN AMUR REGION

(1) Billion cubic metres. (2) Million cubic metres.

60 mcm(2)

42 bcm(1) Gas processing capacity

Helium production capacity

Products: methane, ethane, propane, butane, pentane-

hexane fraction

16

1. Business Description: Additional Details

2. Key Recent Financials

3. Market Prices

17

6.2 6.1

2015 2016

(1.4%)

379.9 411.8

2015 2016

18

SIBUR FINANCIAL SUMMARY(1)

Operating Cash Flow Revenue Investing Cash Flow(3)

Rus

sian

Rou

bles

, bln

(1) Values in USD estimated based on average RR/USD rate of 67.0349 and 60.9579 in 2016 and 2015, respectively . (2) Adjusted EBITDA, including share of the Group’s portion in joint ventures and associates EBITDA (3) Includes CapEx and M&A.

+8.4%

289.2 308.7

2015 2016

Operating Expenses

+6.7%

4.5 4.6

2015 2016

+1.6%

Adj. EBITDA Operating Cash Flow Operating Expenses Investing Cash Flow(3)

USD

Equ

ival

ents

, bln

(il

lust

rativ

e)

Revenue

119.1 137.7

2015 2016

+15.6% 123.4 142.2

2015 2016

2.0 2.1

2015 2016

+5.1%

+15.3%

2.0 2.1

2015 2016

+4.8%

141.7 149.2

2015 2016

EBITDA(2)

+5.3%

2.3 2.2

2015 2016

(4.3%)

EBITDA(2)

Share of JVs and associates EBITDA

19

119.1 (84.4)

(40.4)

186.0

(18.1) (14.9)

(2.9)

144.4

Net OCF CapEx(1) M&A Net borrowings

Dividends paid

Interest paid

Other Net CF

(145.7) 137.7

(64.0)

(16.2) (21.9) (1.4)

(111.4)

Net OCF CapEx(1) Net debt repayment/settlement

Dividends paid

Interest paid

Other Net CF

CASH FLOW STATEMENT HIGHLIGHTS

FY 2015 Cash Flow Reconciliation

RR bln

FY 2016 Cash Flow Reconciliation

Net cash from operating activities increased by 17.3% y-o-y on higher EBITDA, adjusted for the changes in certain provisions, primarily related to Tyumenenergo lawsuit (closed in July 2015) positive impact from WC changes on higher trade and other payables …partially offset by higher income tax paid

Net cash used in investing activities increased by 15.3% y-o-y on substantial increase in CapEx due to expansive ZapSib-2 financing …partially compensated by M&A activities in 2015

Net cash used in financing activities attributable to substantial debt repayment as opposed to new borrowings for ZapSib-2 financing and Yugragazpererabotka acquisition in 2015

Key Factors

RR bln

(1) Includes purchase of property, plant and equipment, intangible assets and other non-current assets.

DEBT PROFILE

20

Key Figures

RR bln, except as stated 31 Dec 2016 31 Dec 2015 Change, % Total debt 341.8 457.1 (25.2%)

Conventional debt 182.1 299.0 (39.1%) ZapSibNeftekhim related debt 159.7 158.1 1.0%

Cash & cash equivalents 60.6 172.1 (64.8%) Net debt 281.2 285.1 (1.4%)

Conventional net debt 163.4 247.2 (33.9%)

ZapSibNeftekhim related net debt 117.8 37.9 210.8%

WA loan tenor (years) 6.8 6.3 WA Conventional debt 2.7 2.7 WA ZSN related debt 11.4 13.0

Available credit lines, incl. 184.5 287.7 (35.9%) Committed 112.5 169.9 (33.8%)

31 Dec 2016 31 Dec 2015

Debt / EBITDA 2.4x 3.4x

Net debt / EBITDA 2.0x 2.1x

Conventional net debt 1.2x 1.8x ZSN related net debt 0.8x 0.3x

Leverage Ratios

100%

47%

94%

58%

53%

6%

29% 13%

Unsecured/Secured

Fixed/Floating

Long-term/Short-term

USD/RUB/EUR

Overview

Loan portfolio structure as of 31 Dec’16

Total debt decreased by 25.2% mainly due to: repayment and refinancing of debt denominated

primarily in foreign currencies RR appreciation 31 Dect’16 vs. 31 Dec’15 Net debt moderately decreased mainly on substantial

debt repayments, while financing of ZapSibNeftekhim CapEx from the funds provided by the NWF Net leverage marginally decreased to 2.0x from 2.1x conventional net leverage decreased to 1.2x from 1.8x

on recent debt repayments ZapSibNeftekhim net leverage increased to 0.8x from

0.3x on on-going project financing As of 31 Dec’16, all of the debt was unsecured

LIQUIDITY AND DEBT MATURITY PROFILE(1)

21 (1) Items denominated in USD and EUR are converted into RR at RR/USD and RR/EUR FX rates as of 31 December 2016.

61

112

72

245

22 42 48 51 56

20 13 13 13

157

Liquidity 2017 2018 2019 2020 2021 2022 2023 2024 2025 After 2025

As of 31 December 2016, RR bln

cash & cash equiv.

committed credit lines

uncommitted credit lines

eurobond undrawn EUR ECA loans RR bonds ECA NWF

62 62 62 62

109 109

137 137

193 193

67 Fe

edst

ock

proc

essi

ngca

paci

ty, T

rans

porta

tion

infra

stru

ctur

e

Pet

roch

emic

als

Oth

er

TOTA

L

INVESTMENT PROGRAMME

RR bln (excl. VAT)

2009 – 2016(1)

567 in 8yrs

Transportation infrastructure

Feedstock processing

capacity

Petrochemicals Maintenance, R&D, IT,

and other

TOTAL

(1) CapEx includes purchase of property, plant and equipment, as well as purchase of intangible assets and other non-current assets. (2) The Board of Directors will review the budget later in the year and the number may be revised subject to macroeconomic and market environment.

RR 200 bln(2) (excl. VAT) investment programme approved by SIBUR BoD for 2017

22

ZapSibNeftekhim CapEx

170

330

1. Business Description: Additional Details

2. Key Recent Financials

3. Market Prices

23

Feedstock and Energy

MARKET UPDATE

Rebased to 100

Plastics, Elastomers and Intermediates Rebased to 100

Plastics, Elastomers and Intermediates Rebased to 100

Olefins and Polyolefins Rebased to 100

Source: Argus, Platts, Bloomberg, ICIS, Malaysian Rubber Board, Chemease, Federal Antimonopoly Service of Russian Federation 24

0%20%40%60%80%

100%120%140%160%180%200%220%240%

Natural Rubber Butadiene StyreneBrent ₽/$

0%

20%

40%

60%

80%

100%

120%

140%

160%

Polystyrene MEG MTBEPET Brent ₽/$

0%

20%

40%

60%

80%

100%

120%

140%

160%

Brent NaphthaLPG CIF ARA (large) Natural gasLPG DAF Brest ₽/$

0%

20%

40%

60%

80%

100%

120%

140%

LDPE PP raffia China Main PortPP MRC CPT Moscow Brent₽/$

INVESTOR RELATIONS CONTACTS

[email protected] Phone: +7 (495) 777-55-00 (*39-47) www.investors.sibur.com

25