compaq storageworks vs. the competition kevin farley competitive response team it3 february 22, 2001...

TRANSCRIPT

Compaq StorageWorksvs.

The CompetitionKevin Farley

Competitive Response Team

IT3 February 22, 2001

February, 2001

Agenda Introduction

– Mission Statement– Delivery Methodology– Additional Resources

Vendor Overviews (Sun, HP, HDS, IBM, Dell, EMC)– Storage Strategy– Product Lines– Competitive Positioning– Strengths/Weaknesses– Attack Points– Why StorageWorks

Mission Statement

To develop and deliver best-in-class tactical competitive analysis, tools and support to Compaq’s partners and field sales organizations, ESG product marketing and ISSG in a timely manner.

Primary Coverage:

EMC - Sal Capizzi, George Lester IBM - George Lester Sun - Kevin Farley HDS - George Lester Dell - Sal Capizzi HP - Kevin Farley Xiotech - Kevin Farley

Secondary Coverage

Network Appliance - Sal Capizzi, Kevin Farley MTI - Sal Capizzi STK - Sal Capizzi Veritas, Tivoli - Competitive Team SAN market - Competitive Team Management software - Competitive Team Storage Utility – Competitive Team

Contact Information

Sal Capizzi - 508-841-2602– [email protected]

George Lester - 508-841-2064– [email protected]

Kevin Farley - 508-841-2882– [email protected]

FAX: 508-841-6183

Remember

“…Be the Ball”? – Be The Customer – Address His Concerns

Sell High Sell the Solution – not the box Document and Communicate

Compaq Storage Vs EMC

At-A-Glance

February, 2001

EMC Approach with Customers

Sells value of its storage solutions– Reality: justifying the high price

Pitches business value to CIO level– Reality: avoiding the hardware sell at the user

level Provides complete service and support as a

standard offering– Reality: does not want customers to have the

option of supporting complex Symmetrix storage systems

EMC Claims

EMC is the largest storage company Compaq as a company is not focused on

selling storage Superior SANs - Gartner Group rates EMC

highest in SAN magic quadrant EMC understands Windows/NT better than

Compaq EMC Hardware is superior to StorageWorks EMC Software is superior to SANworks

What EMC Says About Compaq Compaq is not an enterprise storage vendor due

to lack of mainframe support - Enterprise is not defined as mainframe and Compaq has relationship with ENT

Compaq is a PC Vendor - IDC shows Compaq as #1 storage vendor with 20% market share of multi-user storage

Compaq has limited experience in disaster tolerance and business critical environments; says SANWorks is immature - Although DRM, SWVR, and EVM have not shipped as long as SRDF and TimeFinder, they have been extremely successful.

Compaq doesn’t offer FC Drives - FC Drives do nothing to add performance; only CLARiiON offers FC drives, not Symmmetrix

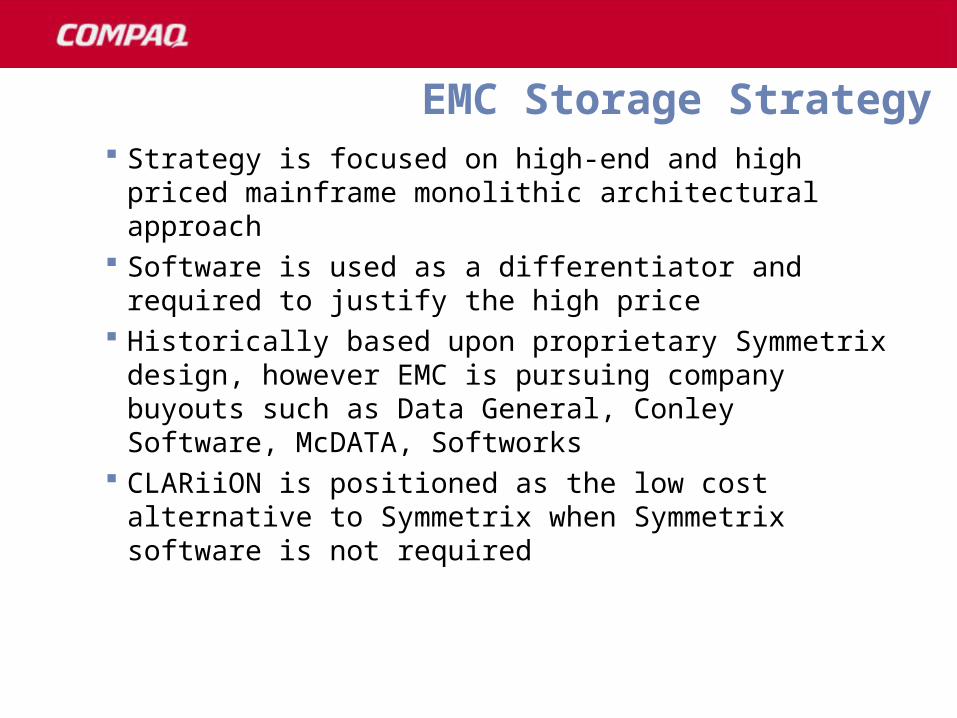

EMC Storage Strategy Strategy is focused on high-end and high priced

mainframe monolithic architectural approach Software is used as a differentiator and required to

justify the high price Historically based upon proprietary Symmetrix

design, however EMC is pursuing company buyouts such as Data General, Conley Software, McDATA, Softworks

CLARiiON is positioned as the low cost alternative to Symmetrix when Symmetrix software is not required

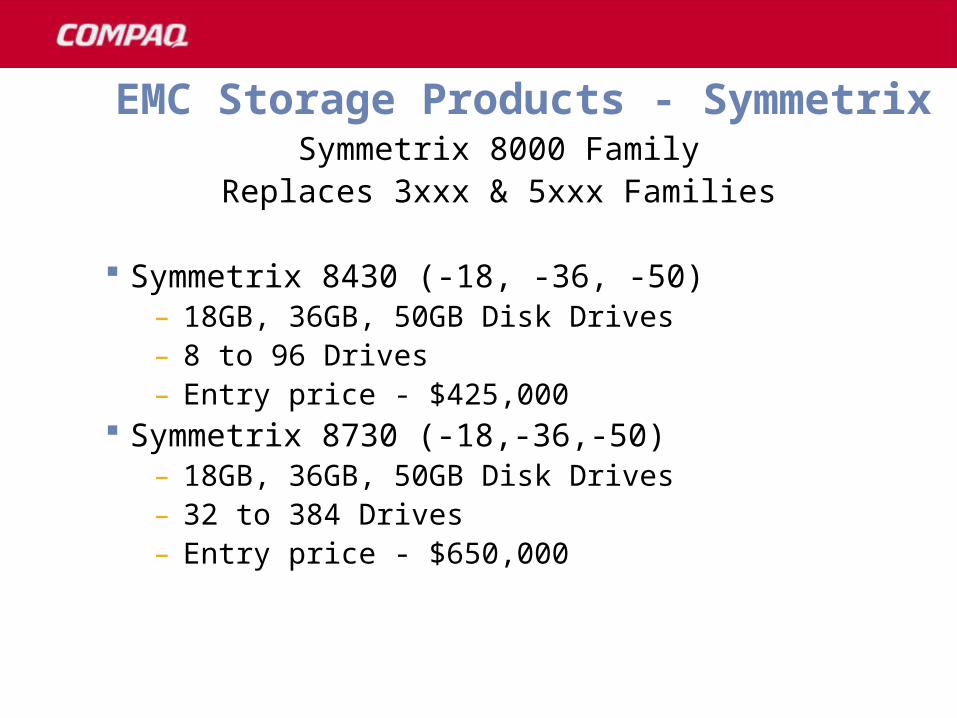

EMC Storage Products - SymmetrixSymmetrix 8000 Family

Replaces 3xxx & 5xxx Families

Symmetrix 8430 (-18, -36, -50)– 18GB, 36GB, 50GB Disk Drives– 8 to 96 Drives– Entry price - $425,000

Symmetrix 8730 (-18,-36,-50)– 18GB, 36GB, 50GB Disk Drives– 32 to 384 Drives– Entry price - $650,000

Positioning vs EMC Symmetrix

Symmetrix 8430

Symmetrix 8730

RA, MA8000

ESA, EMA 12000

ESA, EMA 12000

Compaq SAN

EMC and CLARiiON EMC product strategy focused on Symmetrix

– Symmetrix is still the strategic product for EMC All product development is targeted towards exploiting Symmetrix.

EMC leads with high priced Symmetrix; when too high CLARiiON comes in as last resort

CLARiiON announced snapshot and remote copy in January 2001, but still lags in comparison to SANworks

No SAN based backup and restore CLARiiON Fibre Channel disks offer no performance

advantage over UltraSCSI disks

Positioning vs EMC CLARiiON

CLARiiON 4500, 4700

CLARiiON 5200/5300*, 4700

CLARiiON 5600/5700*

RA4100, MA6000, RA/MA 8000

RA/MA 8000 plus software

RA/MA 8000 plus software

ESA/EMA 12000 plus software

* - End-of_Life

EMC Strengths/Weaknesses Reputation as mainframe storage provider Financial success Software such as TimeFinder and SRDF Aggressive sales force that sells high Multivendor connectivity including mainframe

Aging proprietary monolithic mainframe architecture Limited NT market share and mind share Two different storage architectures with Symmetrix and CLARiiON Entry price high as well as overall prices Performance just average in open systems environments Only sells storage

+

_

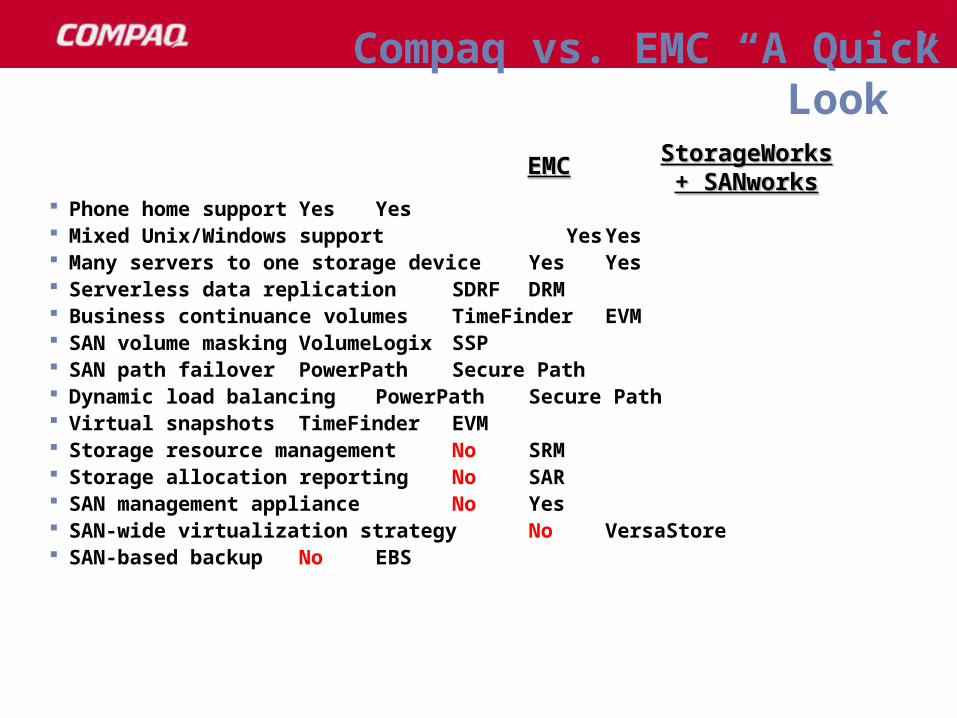

Compaq vs. EMC “A Quick Look”

Phone home support Yes Yes Mixed Unix/Windows support Yes Yes Many servers to one storage device Yes Yes Serverless data replication SDRF DRM Business continuance volumes TimeFinder EVM SAN volume masking VolumeLogix SSP SAN path failover PowerPath Secure Path Dynamic load balancing PowerPath Secure Path Virtual snapshots TimeFinder EVM Storage resource management No SRM Storage allocation reporting No SAR SAN management appliance No Yes SAN-wide virtualization strategy No VersaStore SAN-based backup No EBS

EMCEMC StorageWorksStorageWorks+ SANworks+ SANworks

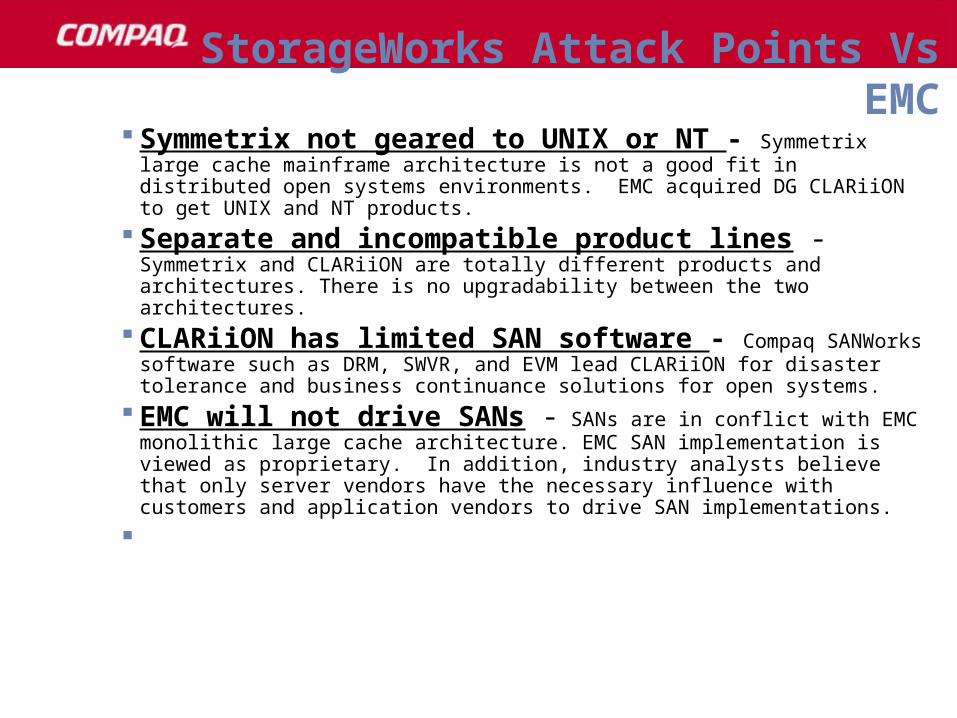

StorageWorks Attack Points Vs EMC EMC architecture is mainframe oriented -

EMC has it’s roots in the mainframe storage market and is moving the mainframe architecture of Symmetrix to open systems environments.

EMC Symmetrix offering is proprietary - EMC will not even allow customers to maintain Symmetrix storage. All changes and upgrades require EMC support personnel.

EMC product strategy focused on Symmetrix - Even with the acquisition of CLARiiON, Symmetrix is still the strategic product for EMC Most product development is targeted towards exploiting Symmetrix.

EMC is storage only company - The AViiON server group is a separate division that EMC uses as another channel to sell storage.

StorageWorks Attack Points Vs EMC Symmetrix not geared to UNIX or NT - Symmetrix

large cache mainframe architecture is not a good fit in distributed open systems environments. EMC acquired DG CLARiiON to get UNIX and NT products.

Separate and incompatible product lines - Symmetrix and CLARiiON are totally different products and architectures. There is no upgradability between the two architectures.

CLARiiON has limited SAN software - Compaq SANWorks software such as DRM, SWVR, and EVM lead CLARiiON for disaster tolerance and business continuance solutions for open systems.

EMC will not drive SANs - SANs are in conflict with EMC monolithic large cache architecture. EMC SAN implementation is viewed as proprietary. In addition, industry analysts believe that only server vendors have the necessary influence with customers and application vendors to drive SAN implementations.

Compaq offers better price - Compaq offers customers a better, more cost effective business solution. For example, a typical Symmetrix configuration has an entry price of $420,000+ and offers only average performance in Open Systems environments.

Compaq offers better performance - The mainframe centric large cache design of Symmetrix does not perform as well as StorageWorks in distributed Open Systems environments.

Compaq has stronger SAN position - Compaq has been offering SAN solutions since 1998. EMC has just recently began to formulate an open SAN strategy. A Compaq SAN provides value via a modular, scalable storage architecture versus EMC monolithic mainframe focused design.

StorageWorks Attack Points Vs EMC

Why StorageWorks Vs EMC? SANs are an inflection point in the storage market Modular architecture more conducive to take

advantage of SANs Hardware product feature/functions have moved to

parity And who better connects to your business than

Compaq Provides business value for the customer Today's SAN market is an integration and test market

and that’s what Compaq does best

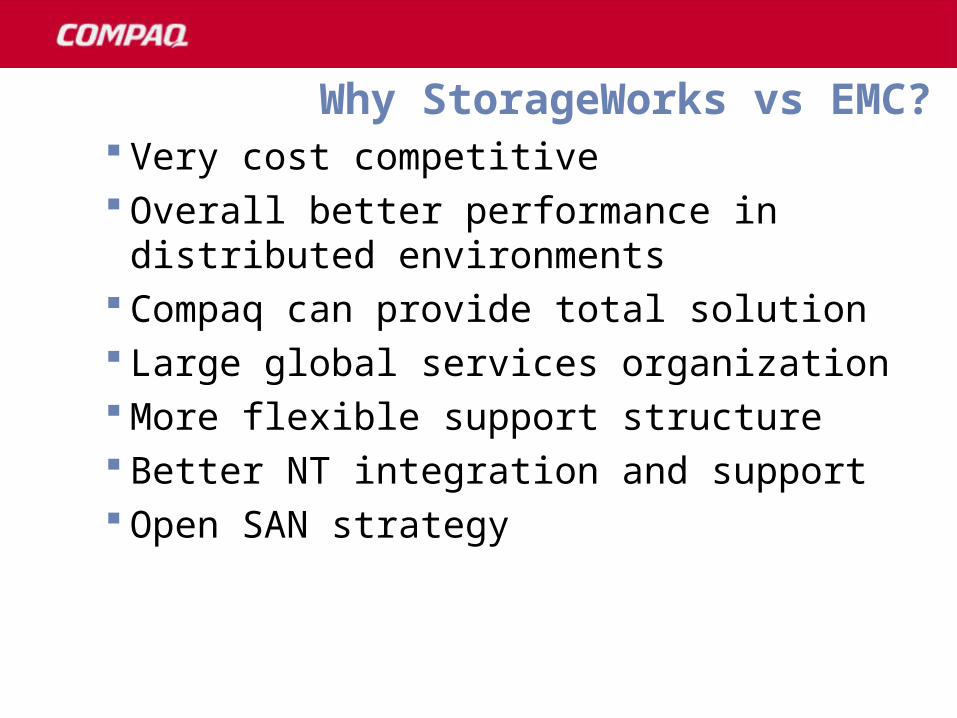

Why StorageWorks vs EMC? Very cost competitive Overall better performance in distributed

environments Compaq can provide total solution Large global services organization More flexible support structure Better NT integration and support Open SAN strategy

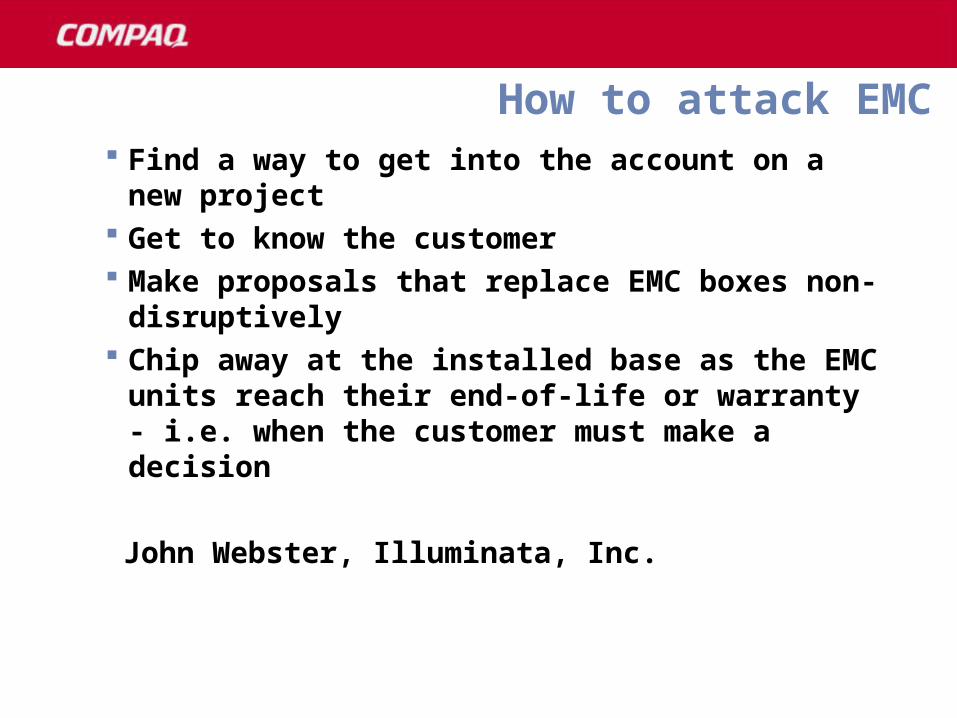

How to attack EMC Find a way to get into the account on a new

project Get to know the customer Make proposals that replace EMC boxes non-

disruptively Chip away at the installed base as the EMC units

reach their end-of-life or warranty - i.e. when the customer must make a decision

John Webster, Illuminata, Inc.

Compaq Storage Vs Sun Microsystems

At-A-Glance

February, 2001

Sun Storage Strategy

Sun’s CEO Scott McNealy - “We will win on storage, storage is not an industry, it’s a feature of the server.”

Sun’s Enterprise Storage Strategy is clearly a very aggressive capitalization of Sun’s server strategy

– Resulted in a fragmented set of storage products

– Inferior products = Dissatisfied Customers Fundamental component is Solaris and servers for

host-based functionality Storage is an afterthought

Sun Storage Products StorEdge A1000/D1000

– Entry level UltraSCSI (host and disk) storage– A1000 supports single storage RAID controller– D1000 - JBOD with host-based SW RAID– Based on 3 generation old LSI/Symbios

technology StorEdge A3500 and A3500FC

– UltraSCSI or FC host interface– Supports 56 UltraSCSI drives in single cabinet– Supports Solaris and NT– Based on old 486DX4 controller technology

CANNOT BE UPGRADED!

Sun Storage Products

StorEdge A5100/5200– Host-based software RAID with FC host and disk

interface– A5100 supports 14x18.2 GB 7.2K rpm drives – A5200 supports 22x9.1GB 10k rpm drives– Support Solaris and NT– Based on Sun Proprietary Technology

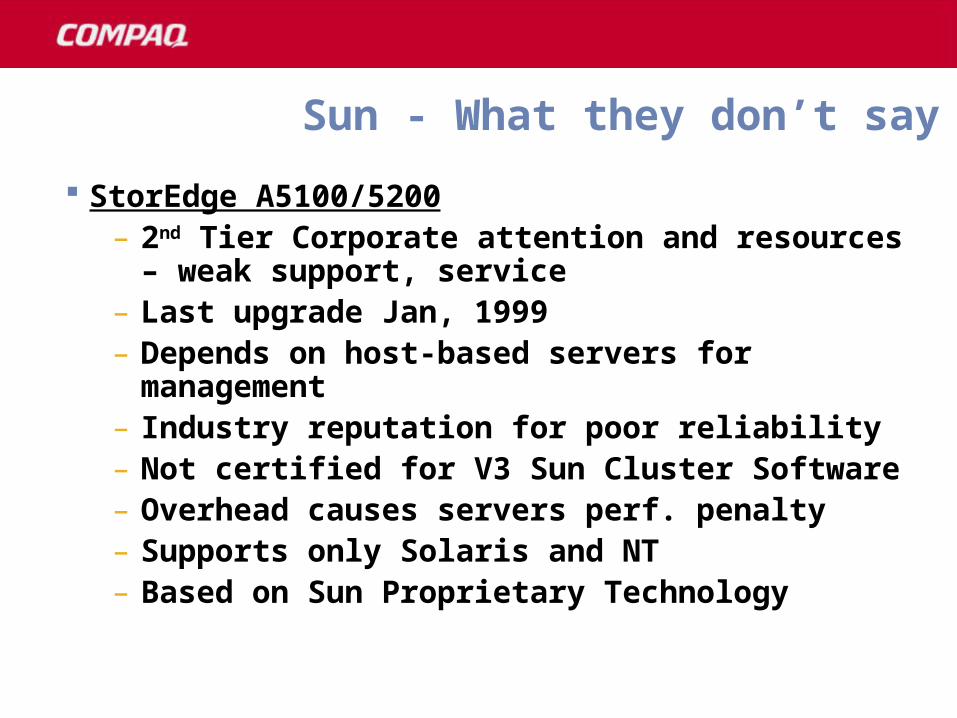

Sun - What they don’t say

StorEdge A5100/5200– 2nd Tier Corporate attention and resources – weak

support, service– Last upgrade Jan, 1999– Depends on host-based servers for management – Industry reputation for poor reliability– Not certified for V3 Sun Cluster Software– Overhead causes servers perf. penalty– Supports only Solaris and NT– Based on Sun Proprietary Technology

Sun Storage Products StorEdge T3 “Purple” - Announced 6-14-2000

– Modular design, SBus/FC-AL host connectivity– 9 disks per drawer, 8 drawers per rack (72 disk

total per cabinet)– Single Controller per drawer– 18GB, 36GB 73GB FC drives– 5.2TB capacity per rack - Max 168TB– Only Solaris support; NT in Q1’01– Based on MaxStrat Technology

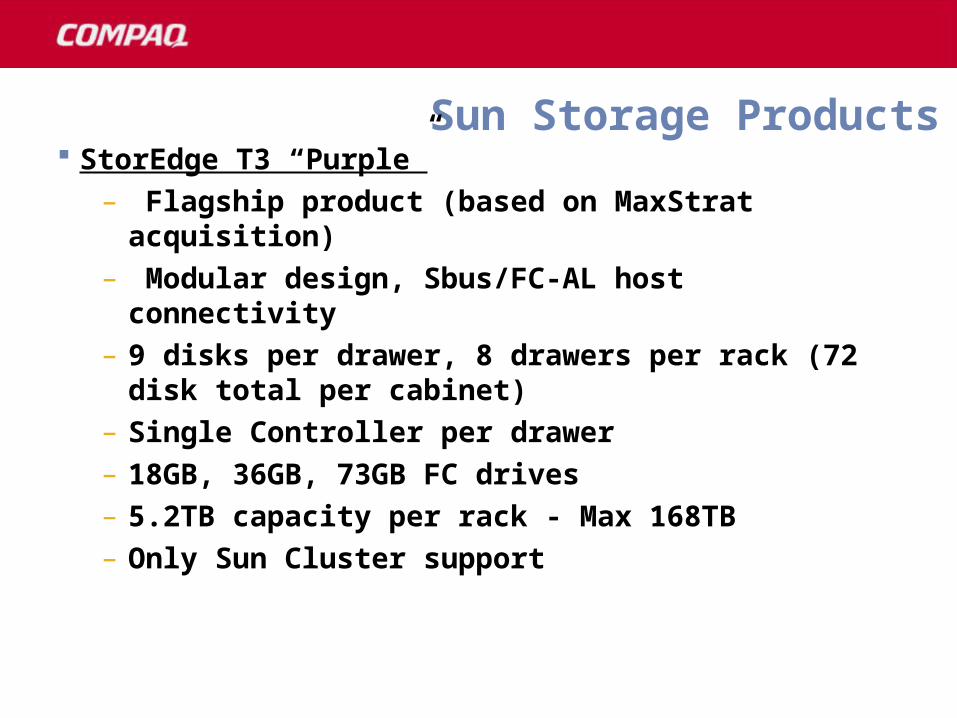

Sun Storage Products StorEdge T3 “Purple”

– Flagship product (based on MaxStrat acquisition)– Modular design, Sbus/FC-AL host connectivity– 9 disks per drawer, 8 drawers per rack (72 disk

total per cabinet)– Single Controller per drawer– 18GB, 36GB, 73GB FC drives– 5.2TB capacity per rack - Max 168TB– Only Sun Cluster support

Sun - What they don’t say StorEdge T3 “Purple”

– Redundant controllers aren’t ready - don’t work– Limited clustering support (only V2.2 from Sun)– LUNS/RAID limited to single shelf– Every 9 disks needs an additional controller!– Every shelf needs individual LUN management– Field Service will learn “on your nickle”– Dependent on server availability to access data -

U10K has technical flaws– Not certified by Sun for new V3 Sun Cluster Software– Installation/wiring nightmare

Compaq vs. Sun “A Quick Look”

Phone home support No Yes Mixed Unix/Windows support No Yes Many servers to one storage device Yes Yes Serverless data replication No DRM Business continuance volumes Instant Image EVM SAN volume masking Limited SSP SAN path failover No Secure Path Dynamic load balancing Limited Secure Path Virtual snapshots Instant Image EVM Storage resource management No SRM Storage allocation reporting No SAR Host-independent SAN management No Yes Open SAN initiatives/commitment No Yes SAN-based backup No EBS

SUNSUN StorageWorksStorageWorks+ SANworks+ SANworks

Positioning vs Sun

StorEdge A1000/D1000

StorEdge A3500/A3500FC, T3 “Purple”

StorEdge A5100/5200, T3 “Purple”

StorEdge T3 “Purple”

RA3000/RA4200 MA8000

MA6000, MA8000 ESA12000

MA6000, MA8000

RA4200, MA6000, MA8000, EMA12000

Sun Strengths/Weaknesses

UNIX server success Storage capture rate on Sun servers at initial sale Message as standards leader, Jiro and Java

Limited multivendor platform support Multiple storage architectures, i.e., MAXSTRAT,

LSI/Symbios as well as SUN proprietary Limited knowledge for support of NT, no other UNIX Lack of penetration into large IT shops Current products going EOL soon

+

_

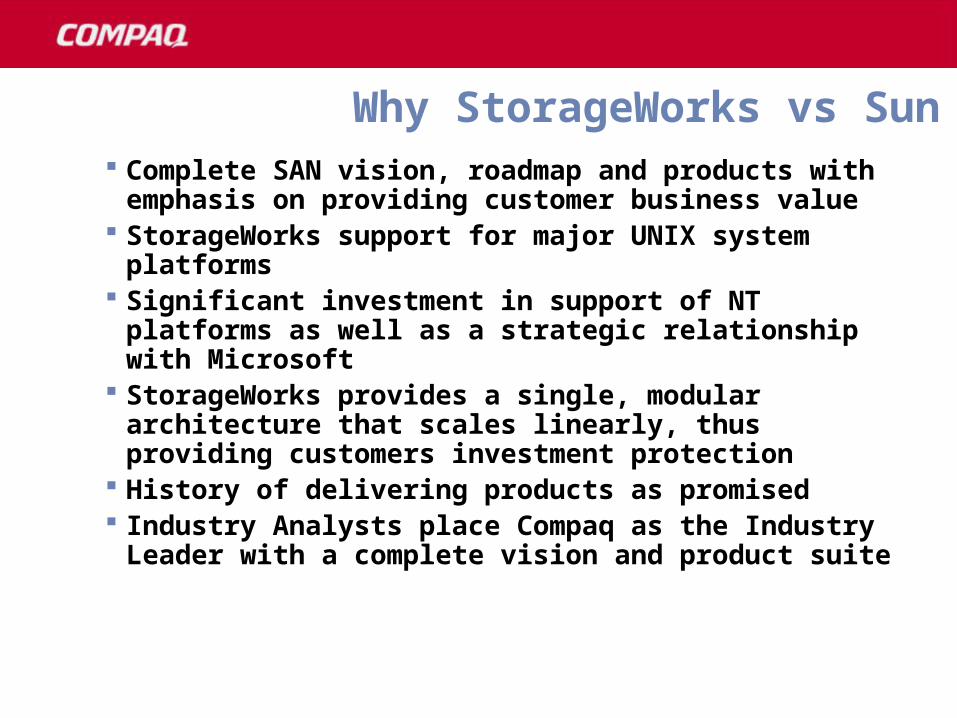

Why StorageWorks vs Sun Complete SAN vision, roadmap and products with

emphasis on providing customer business value StorageWorks support for major UNIX system

platforms Significant investment in support of NT platforms

as well as a strategic relationship with Microsoft StorageWorks provides a single, modular

architecture that scales linearly, thus providing customers investment protection

History of delivering products as promised Industry Analysts place Compaq as the Industry

Leader with a complete vision and product suite

Business Concerns with Sun Investment Protection? - Sun effectively EOL’d their

existing products when T3 “Purple” was announced. (Sun offers 3 different architectures.)

Business Risk? - “Purple” has technical and reliability issues. Does the customer want to “field de-bug” a new, unproven product while maintaining their critical business operations?

Performance? - Sun servers handle storage functions and consume CPU cycles (est. 20%+ perf. penalty) instead of offloading mundane tasks to intelligent controllers. Customers pay more and get less.

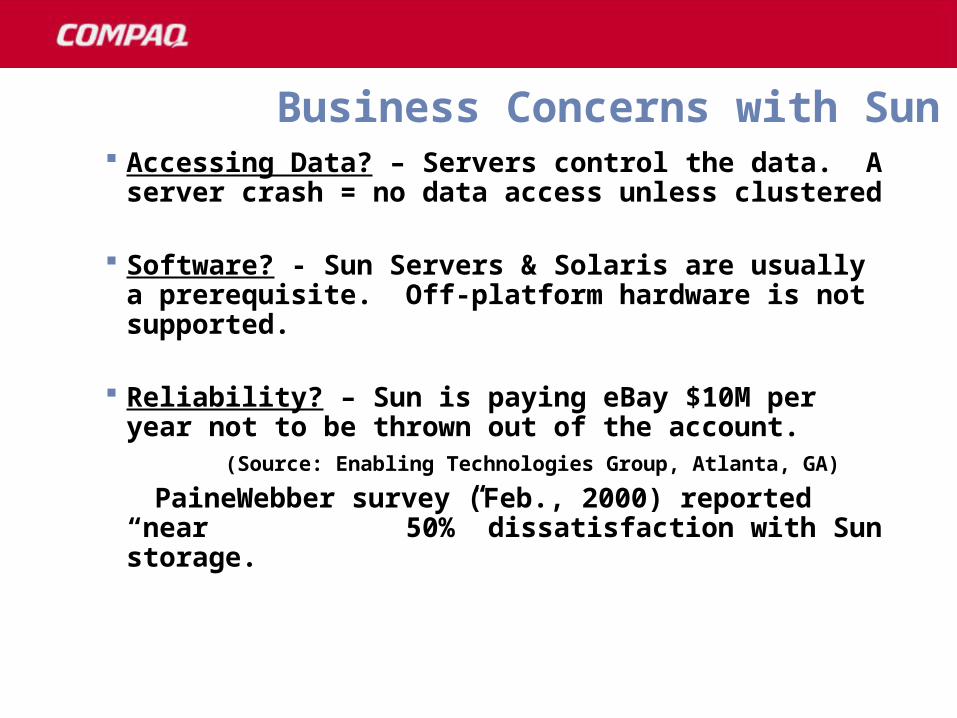

Business Concerns with Sun Accessing Data? – Servers control the data. A

server crash = no data access unless clustered

Software? - Sun Servers & Solaris are usually a prerequisite. Off-platform hardware is not supported.

Reliability? – Sun is paying eBay $10M per year not to be thrown out of the account.

(Source: Enabling Technologies Group, Atlanta, GA)

PaineWebber survey (Feb., 2000) reported “near 50%” dissatisfaction with Sun storage.

Attack Points Against Sun

Sun will stress Sun-on-Sun, direct attach with Solaris control, preventing Customers from operating in an Open, mixed platform environment. Compaq offers vendor-neutral, universal connectivity.

Through the VersaStor alliance, IBM and Compaq are driving open management standards. Sun is Solaris centric.

Compaq offers global support through one (1) organization. Sun depends on 250+ independent organizations.

Compaq Storage Vs Hewlett-Packard

At-A-Glance

October, 2000

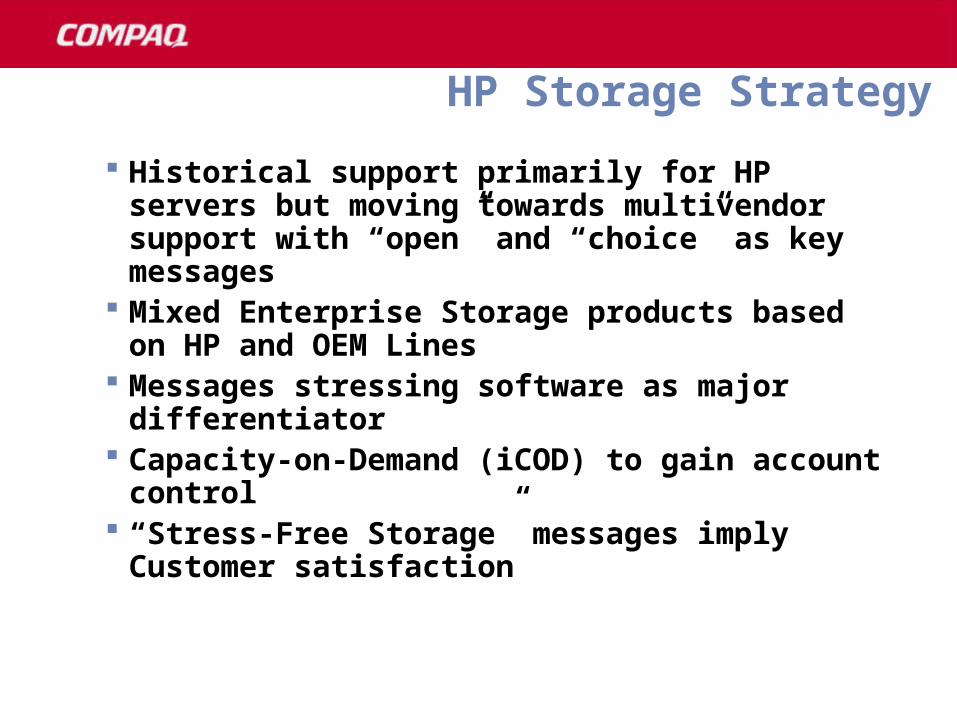

HP Storage Strategy

Historical support primarily for HP servers but moving towards multivendor support with “open” and “choice” as key messages

Mixed Enterprise Storage products based on HP and OEM Lines

Messages stressing software as major differentiator

Capacity-on-Demand (iCOD) to gain account control

“Stress-Free Storage” messages imply Customer satisfaction

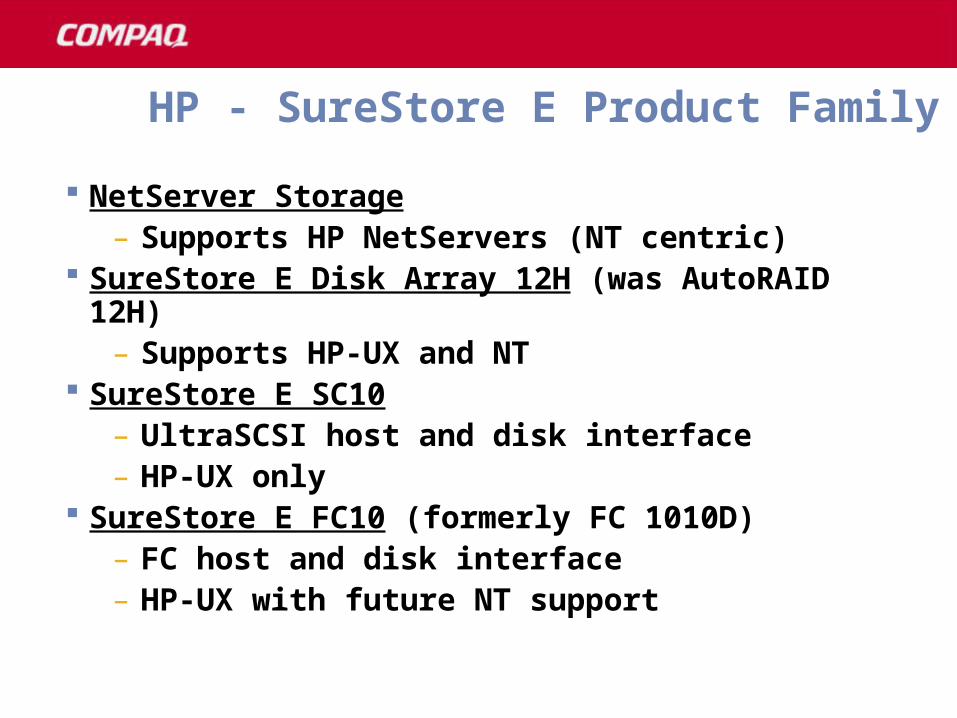

HP - SureStore E Product Family

NetServer Storage– Supports HP NetServers (NT centric)

SureStore E Disk Array 12H (was AutoRAID 12H)– Supports HP-UX and NT

SureStore E SC10– UltraSCSI host and disk interface– HP-UX only

SureStore E FC10 (formerly FC 1010D)– FC host and disk interface– HP-UX with future NT support

SureStore E FC60– Based on LSI/Symbios - FC host interface– HP-UX and NT

SureStore E XP48– Mid range version of XP 512 (48 disk capacity)

SureStore E XP256 (formerly MC256)– Based on HDS 7700E– 9TB capacity - uses non-standard HDS drives– Replaces EMC Symmetrix

SureStore E XP 512– Based on HDS 9900E– Supports 512 disks - 24TB capacity– New crossbar bus technology

HP - SureStore E Product Family

Positioning vs HP NetServer System/6

NetServer Rack Storage/12 NetServer Rack/12FC

SureStore E Disk Array 12H

SureStore E SC10 SureStore E FC60 SureStore E XP48

SureStore E XP256, XP512

RA3000, RA4x00, MA6000, MA8000

RA3000, RA4x00,MA6000, MA8000

MA6000, MA8000

MA8000 EMA 12000 Compaq SAN

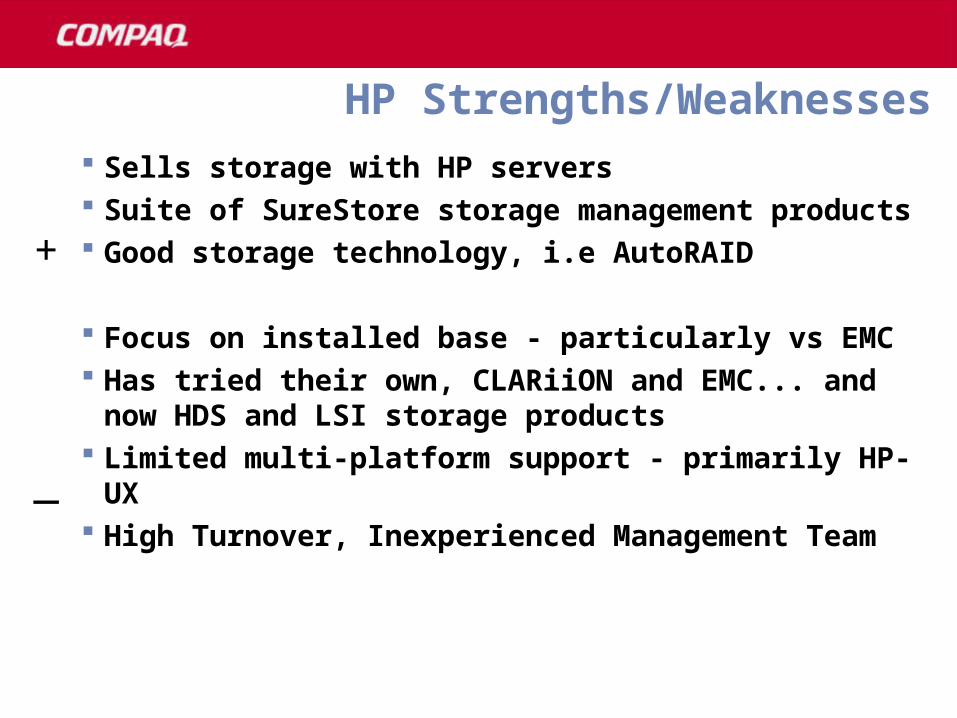

HP Strengths/Weaknesses

Sells storage with HP servers Suite of SureStore storage management products Good storage technology, i.e AutoRAID

Focus on installed base - particularly vs EMC Has tried their own, CLARiiON and EMC... and now

HDS and LSI storage products Limited multi-platform support - primarily HP-UX High Turnover, Inexperienced Management Team

+

_

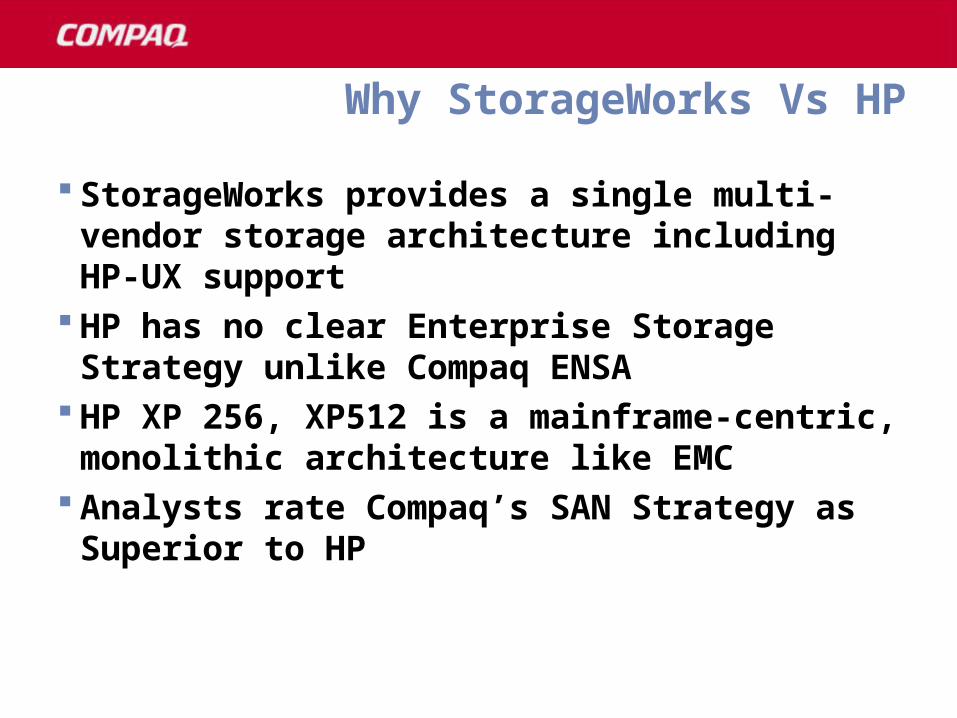

Why StorageWorks Vs HP

StorageWorks provides a single multi-vendor storage architecture including HP-UX support

HP has no clear Enterprise Storage Strategy unlike Compaq ENSA

HP XP 256, XP512 is a mainframe-centric, monolithic architecture like EMC

Analysts rate Compaq’s SAN Strategy as Superior to HP

Attack Points against HP

Too Many Different Architectures - Which is best? HP’s technology? LSI/Symbios? Hitachi? What about installed CLARiiON? How many rooms of spare parts does the Customer need?

Limited Multi-Platform Knowledge/Experience - HP sells primary to HP-UX accounts with some NT. What if the customer has Solaris or AIX or Tru64 or OpenVMS?

Risk of HP (again) Switching to Another Company - in early’99, HP re-signed with EMC for 3yrs, terminated in June, signed with HDS for 3yrs.

Significantly More Expensive - Across product groups, in similar configurations HP is generally 30% - 80% more expensive than Compaq.

Compaq Storage Vs Hitachi Data Systems (HDS)

At-A-Glance

February, 2001

HDS Storage Strategy

Combine hardware, software and services for total solutions

Build alliances and relationships to provide “one-stop-shopping”

Stress continuous uptime and fault-tolerant solutions

Provide an “Open” SAN Architecture allowing customers to select any storage product from any vendor.

HDS Storage Products Freedom 9200 Series

– Announced January, 2001– 7.2TB capacity– All Fibre Architecture

Freedom 7700E– 11TB Max. Capacity– HP reselling as HP XP256

Freedom Lighting 9900– Model 9960 - 24TB Max. Capacity– HP reselling as HP XP512

Compaq vs. HDS “A Quick Look”

Phone home support Yes Yes Mixed UNIX/Windows support Yes Yes Many servers to one storage device Yes Yes Serverless data replication Remote Copy DRM Business continuance volumes ShadowImage EVM SAN LUN masking LUN Manager SSP SAN path failover Path Manager Secure Path Dynamic load balancing Path Manager Secure Path Virtual snapshots ShadowImage EVM SAN Storage resource management No SRM Storage allocation reporting No SAR SAN management appliance No Yes SAN-wide virtualization strategy No VersaStore SAN-based backup No EBS

HDSHDS StorageWorksStorageWorks+ SANworks+ SANworks

Positioning vs HDS

HDS 9200

HDS 7700E

HDS 9960

MA6000 & MA8000, EMA12000

MA8000 &

EMA12000

EMA12000

Compaq SAN

HDS Strengths/Weaknesses Recognition in large IT shops IBM mainframe connectivity Reputation for highly available, high performance

array products

Mainframe niche is primary market Limited resources due to company size Dependent upon parent Hitachi to fund

development Lacks a large global services organization. Total

employee population approximately 2,300

+

_

StorageWorks Attack Points Vs HDS

HDS has limited resources - HDS has less than 2,300 total employees and is rumored to be under pressure from Hitachi Ltd. to either get healthy and profitable or get lost. They are seriously lacking in engineering, sales and service resources.

HDS leads technology versus solutions - In order to claim performance leadership HDS has introduced a switch architecture controller that is totally new and unproven. They claim high performance based upon I/O specifications, but have not provided any real world benchmark or performance data.

HDS employs proprietary technology - For example, they use proprietary Hitachi disk drives and PowerPC CPUs in their HDS 7700 and HDS 9900 subsystems

Compaq has stronger SAN position - Compaq has been offering SAN solutions since 1998. HDS lacks SAN management capability. According to Evaluator Group they have not delivered a common storage management capability and they lack a real plan, roadmap or timeline for achieving their SAN management goals.

Compaq offers better performance - The mainframe centric large cache designs of the HDS 7700E and HDS 9900 may not perform as well as StorageWorks in distributed Open Systems environments.

Compaq offers better price - Compaq offers customers a better, more cost effective business solution. For example, an HDS 9900 configuration of 3TB has a list price of $1.5 million versus $700,000 for a 3TB EMA 12000.

StorageWorks Attack Points Vs HDS

Why StorageWorks vs HDS Compaq delivers the Enterprise

Information Utility through ENSA, StorageWorks and value added software and services

SANs are an inflection point in the storage market and Compaq is better positioned to take advantage than HDS

Compaq SANs can provide the business value customers are looking for at significantly less cost

Compaq Storage Vs IBM

At-A-Glance

February, 2001

IBM Storage Strategy

IBM’s primary approach to storage has consistently been based on its proprietary architectures, i.e. S/390, AS/400, RS/6000 and Netfinity servers.

Seascape strategy attempts to unite different architectural components, including:

– Storage arrays and tape solutions– ADSM and Tivoli management– SAN components

Goal to be an OEM storage technology provider as well as market share leader

Compaq/IBM Alliance Strategic partnership between two industry

leaders– Cooperate to improve interoperability for customers– Work together to help define and promote open

standards for networked storage– Create a common open architecture to support storage

virtualization, data sharing and policy based storage management

Compaq VersaStor technology and Tivoli System-managed Storage technology will interoperate in support of open storage network environments

– Strengthen each company’s portfolios Storage solutions and services

– Endorse Tivoli enterprise management solutions

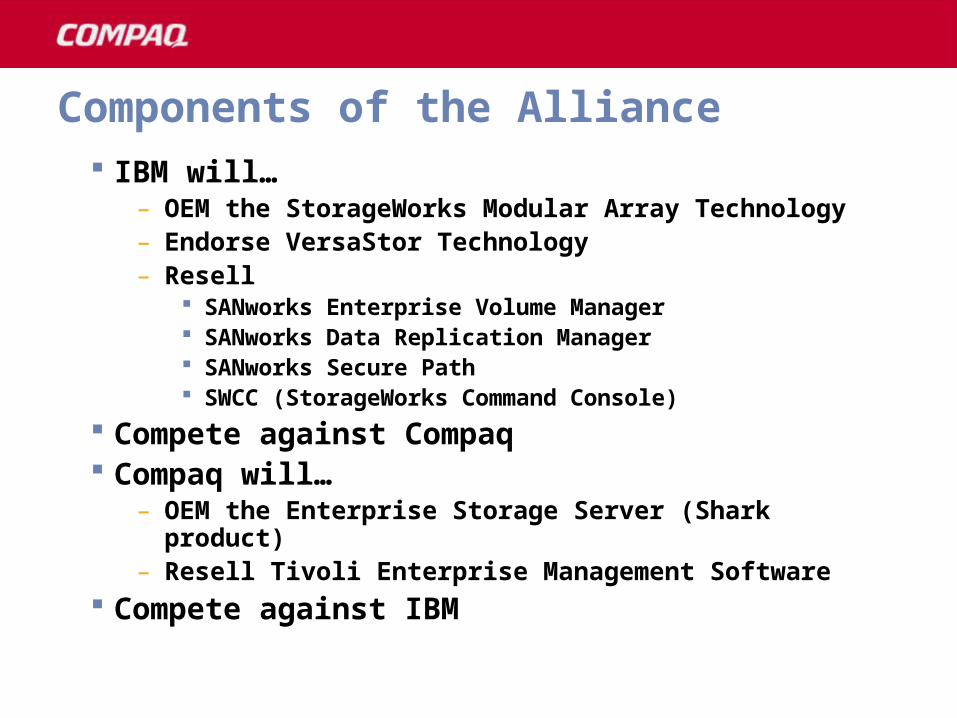

Components of the Alliance IBM will…

– OEM the StorageWorks Modular Array Technology– Endorse VersaStor Technology– Resell

SANworks Enterprise Volume Manager SANworks Data Replication Manager SANworks Secure Path SWCC (StorageWorks Command Console)

Compete against Compaq Compaq will…

– OEM the Enterprise Storage Server (Shark product)– Resell Tivoli Enterprise Management Software

Compete against IBM

IBM Storage Products

Netfinity Storage for IBM Intel-based Netfinity Servers

– EXP15, EXP200/300 SCSI arrays, EXP500 FC-AL arrays

7133 Serial Disk System– Midrange SSA solution scalable from 36GB to over 3.5TB– Supports NT, AIX, HP-UX, Solaris

Fibre Channel Array 2102– Storage for HP, Sun, IBM UNIX and Intel servers– Scalable from 36GB to over 2 TB

IBM Storage Products

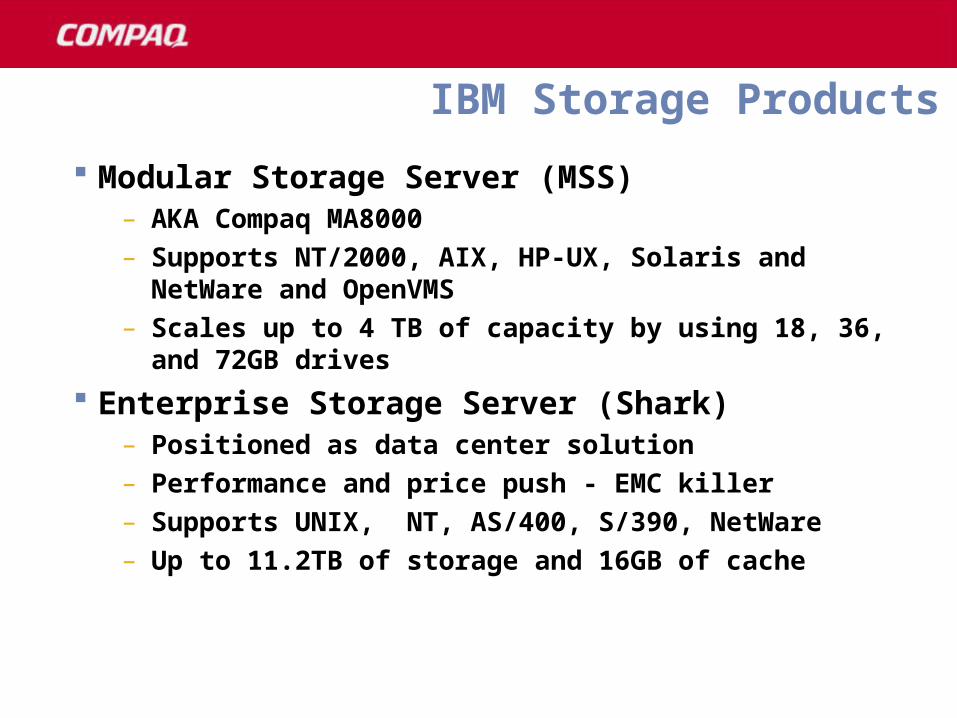

Modular Storage Server (MSS) – AKA Compaq MA8000– Supports NT/2000, AIX, HP-UX, Solaris and NetWare and

OpenVMS– Scales up to 4 TB of capacity by using 18, 36, and 72GB

drives

Enterprise Storage Server (Shark)– Positioned as data center solution– Performance and price push - EMC killer– Supports UNIX, NT, AS/400, S/390, NetWare– Up to 11.2TB of storage and 16GB of cache

Positioning vs IBM

Netfinity Storage

7133 Serial Disk System Modular Storage Server Fibre Channel Array

2102

ESS (Shark)

RA4X00

MA6000 MA8000

EMA12000

Compaq SAN

IBM Strengths/Weaknesses Well entrenched in large IT shops IBM mainframe connectivity Storage management framework with Seascape

architecture and Tivoli software

Major focus in now on winning back market share from EMC - becomes distraction

Slow to adopt FC; Limited multivendor connectivity ESS lacks support for native Fibre channel,

Flashcopy and Peer-to-Peer Remote Copy Mainframe is still a priority

+

_

Why StorageWorks vs IBM

Compaq delivers the Enterprise Information Utility through ENSA, StorageWorks and value added software and services

SANs are an inflection point in the storage market and Compaq is better positioned to take advantage than IBM

Compaq SANs can provide the business value customers are looking for at significantly less cost

StorageWorks Attack Points Vs IBM

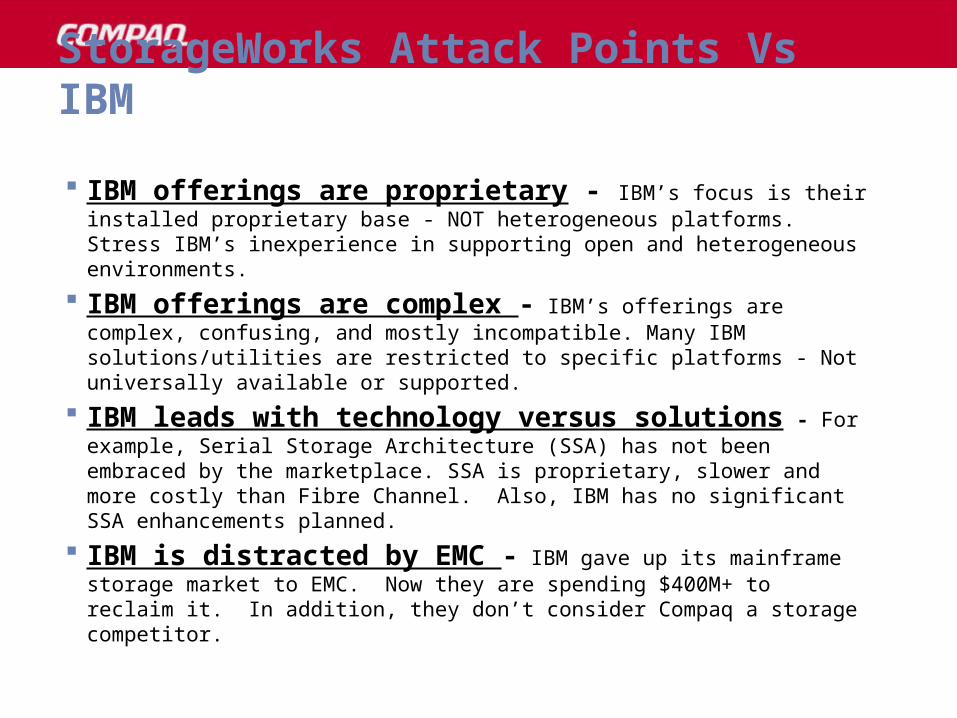

IBM offerings are proprietary - IBM’s focus is their installed proprietary base - NOT heterogeneous platforms. Stress IBM’s inexperience in supporting open and heterogeneous environments.

IBM offerings are complex - IBM’s offerings are complex, confusing, and mostly incompatible. Many IBM solutions/utilities are restricted to specific platforms - Not universally available or supported.

IBM leads with technology versus solutions - For example, Serial Storage Architecture (SSA) has not been embraced by the marketplace. SSA is proprietary, slower and more costly than Fibre Channel. Also, IBM has no significant SSA enhancements planned.

IBM is distracted by EMC - IBM gave up its mainframe storage market to EMC. Now they are spending $400M+ to reclaim it. In addition, they don’t consider Compaq a storage competitor.

Compaq has stronger SAN position - Compaq has been offering SAN solutions since 1998. IBM just recently began to formulate a SAN strategy. A Compaq SAN provides value via a modular, scalable storage architecture versus IBM’s monolithic mainframe focused design.

Compaq delivers on its promises - IBM is known for pre-announcing products/features and failing to deliver. IBM has failed to deliver key ESS capabilities such as Flashcopy and Peer-to-Peer Remote Copy.

Compaq offers better performance - The mainframe centric large cache design of ESS does not perform as well as StorageWorks in distributed Open Systems environments.

Compaq offers better price - Compaq offers customers a better, more cost effective business solution. For example, a minimum ESS (Shark) configuration of 420GB has an entry price of $310,000+ and offers average performance in Open Systems environments.

StorageWorks Attack Points Vs IBM

Compaq Storage Vs Dell Computer Corp.

At-A-Glance

February, 2001

Dell Storage Strategy Dell implements a direct sales model for storage -

Sells on price Dell is not an enterprise storage vendor

– Supports Dell Intel platforms only (added ProLiant)

– Does not support non-Intel based UNIX– Acquires technology through partners

Dell is new to the external storage market– Historically sold storage internal to Dell server– Did not begin selling external RAID storage

until 1998 with the introduction of PowerVault

Dell Storage Products PowerVault 701N, 705N – Low-end NAS PowerVault 735N – Mid-range NAS PowerVault 224F - JBOD Disk Enclosure PowerVault 660F - FC Storage Array

Dell’s low end NAS products are OEM’d from Quantum. Network Appliance relationship dissolved.

Dell’s PowerVault 735N is a Dell design CLARiiON OEM agreement effectively cancelled

Positioning vs. PowerVault

PowerVault 701N, 705N, 735N

PowerVault 224F, 660F

TaskSmart 2400

MA8000 EMA 12000 Switched SAN and

software RA4000 for ProLiant

only storage

Dell Strengths/Weaknesses Price Direct Sales Model

New to enterprise storage market Focus limited to NT (Some NetWare and UNIX) Limited to Dell and ProLiant servers today No technology expertise in storage Layoffs, reduced R&D investment, refocus towards

existing PC products

+

_

Why StorageWorks Vs Dell Clear vision and product roadmap for SANs Support for heterogeneous platforms today

–Convergenet provides an added middle layer of complexity and management

Large global services organization Experience in the enterprise storage market -

Dell’s direct model not the best fit for enterprise sales

Attack Points Against Dell

Investment Protection? Dell dropped Network Appliance, replaced CLARiiON. Where’s the stability and compatibility? Upgrades typically require replacing existing products.

Enterprise Experience? Dell’s focus has been on NT with no evidence of supporting of UNIX from Sun, HP, IBM or Compaq.

Product Selection? Dell has limited storage offerings. Compaq has a complete suite to select from to best match customer requirements

Attack Points Against Dell

SAN Experience? Gartner ranks Dell as average with limited vision while Compaq is rated as the clear leader.

Product Consistency? Dell frequently changes suppliers. There is very little uniformity in components. How many types of spare parts will the customer need to stock?

Service & Support? Dell depends upon 3rd parties to provide service for Dell products. What about multi-vendor environments?