consolidation under ifrs - world...

TRANSCRIPT

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

Consolidation under IFRS Executive IFRS Workshop for

Regulators

3-6 June 2014, Vienna

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Darrel Scott IASB Board Member

2

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Applicable standards

IFRS 12

IFRS

10

✔

IFRS

11

✔

✗

✗

✔

IFRS

9

✗

All

IFRS

Operation

IAS

28

Venture

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

IFRS 10

4

• Single consolidation model (includes structured entities)

• Consolidation based on control – ‘power so as to benefit’

– Controller must have some exposure to risks and rewards

– Exposure is an indicator of control but not control of itself

– Power arises from rights—voting rights, potential voting

rights, other contractual arrangements, or a combination

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Definition of control

An investor controls an investee when the investor is exposed, or has rights, to variable returns from its

involvement with the investee and has the ability to affect those returns through its power over the investee.

Assessing Control

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

5

Power Exposure Link

Purpose

and design

Rights

Relevant

Activities

Decision

Making

Exposure

(or rights)

to variable

returns of

the

investee

Ability to

use power

over

investee to

affect its

own returns

6

Existing rights that give current ability to direct relevant

activities

• Power arises from rights (eg voting rights, rights from

contractual arrangements)

• Relevant activities are those that significantly affect the

investee’s returns

• An investor need not have absolute power to control an

investee

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Power

7

• Only substantive rights must be considered in assessing

power

• For a right to be substantive, the holder must have the

practical ability to exercise that right

• To be substantive, rights also need to be exercisable

when decisions about the direction of the relevant

activities need to be made

• May be voting, potential voting, contractual rights,

removal (‘kick out’), or protective rights

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Rights

8

• Investor able to make decisions at the time that those

decisions need to be taken.

– can have current ability even if it does not actively direct

– an investor is not assumed to have current ability to direct

simply because is actively directing activities

• Having the current ability is not limited to being able to

act today

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Current ability

9

• Investor holds 48% of the voting rights of an investee

• Remaining voting rights held by thousands of

shareholders, with less than 1% each

• Based on the relative size of the other shareholders,

investor concluded that a 48% interest would be sufficient

to give it control

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Rights

10

• Investor holds 35% of the voting rights of an investee.

• Three other investors each hold 5% of the voting right.

• Remaining voting rights are held by numerous other

shareholders (each holding 1% or less)

• Decisions about relevant activities require approval of a

majority of votes.

• Recent relevant meetings: 75% of voting rights have

been cast

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Rights

11

• Investor holds 45% of the voting rights of an investee.

• Eleven other investors each hold 5% of the voting right.

• No contractual agreement among shareholders to consult

any of the others or make collective decisions

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Rights

12

• Investor holds 40% of the voting rights of an investee.

• Twelve other investors each hold 5% of the voting right

• Shareholder agreement:

– Investor has the right to appoint, remove and set the

remuneration of management responsible for directing the

relevant activities

– Two-thirds majority vote of the shareholders is required to

change the agreement

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Rights

13

• Investor holds 38% of the voting rights of an investee.

• No other shareholders individually hold more than 1%

• Decisions about relevant activities require the approval of

a majority of votes

• 70% of the voting rights cast at recent relevant

shareholder meetings—except one when 78% cast

• Decisions taken at that meeting included changing the

financing arrangements that could affect future dividend

payments to shareholders

• There are no other contractual arrangements that would

affect the assessment of power

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Rights

14

• Investor holds 45% of the voting rights of an investee

• Two other investors each hold 26% of the voting right

• Remaining voting rights are held by three other

shareholders (each with 1%)

• No other arrangements that affect decision-making

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Rights

15

• Investor A holds 70% of the voting rights of an investee

• Investor B has 30% of the voting rights of the investee as

well as an option to acquire half of investor A’s voting

rights

• Option can be exercised anytime in next two years, fixed

price, deeply out of the money and expected to remain so

• Investor A exercises its votes and actively directs

relevant activities of the investee

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Rights

16

• Investor A and two other investors each hold a third of

the voting rights of an investee

• Investor A also holds debt instruments convertible into

ordinary shares at a fixed price, out of the money but not

deeply

• If converted, investor A would hold 60% of the voting

rights

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Rights

17

• Investor holds 40% of the voting rights of Investee as well

as option to acquire another 20%

• Option is exercisable during 51 weeks in each calendar

year; however, it is not exercisable during the last week

of every year

• The option is exercisable for a nominal amount

• Decisions about the relevant activities require the

approval of a majority at relevant shareholders’ meetings,

which are generally held during the first or second quarter

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Rights

18

Fact pattern:

• Next scheduled shareholders’ meeting is in eight months

• Shareholders with at least 5% of the voting rights can call

a special meeting to change the existing policies

• Policies over the relevant activities changed only at

special or scheduled shareholders’ meetings.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Rights

19

• A: An investor holds a majority of the voting rights.

• B: An investor is party to a forward contract to acquire the

majority of shares

• C: An investor holds a substantive option to acquire the

majority of shares (In the money).

• D: An investor is party to a forward contract to acquire the

majority of shares (forward contract’s settlement date in

six months)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Rights

20

• For many investees, a range of operating and financing

activities significantly affect their returns

• Examples of relevant activities:

– selling and purchasing of goods or services;

– managing financial assets during their life (including upon

default);

– selecting, acquiring or disposing of assets;

– researching and developing new products or processes;

and

– determining a funding structure or obtaining funding.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Relevant Activities

21

• Examples of decisions about relevant activities include

but are not limited to:

– establishing operating and capital decisions of the

investee, including budgets; and

– appointing and remunerating an investee’s key

management personnel or service providers and

terminating their services or employment.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Relevant Activities

22

• Two investors (A and B) form an investee to develop and

market a medical product

• Investor A will develop and obtain patent

• Investor B will manufacture and market

• Obtaining patent for the product requires significant

uncertainty and effort

• Patent results in 10 year exclusivity

• The 10 year exclusivity corresponds to 95% of the fair

value of the patent

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Relevant activity

23

• Investee purchases receivables and services them on a

day-to-day basis for its investors

• Upon default of a receivable the investee automatically

puts the receivable to Investor A

• Managing the receivables upon default is relevant

because it is the only activity that can significantly affect

the investee’s returns

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Relevant activity

24

• Bank A enters into a credit default swap with Investee B

• Under the credit default swap, Bank A pays a fee for

credit risk passed to Investee B

• Investee B issues notes linked to the credit risk to

multiple unrelated investors

• There are very few, if any, decisions to be made after

initially setting up Investee B

• Neither Bank A nor the investors have any voting or other

rights that give them the ability to direct activities that

significantly affect Investee B’s returns

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Relevant activity

25

• Investee’s only business: purchase receivables and

service them on a day-to-day basis for its investors.

• Upon default of a receivable the investee automatically

puts the receivable to Investor A (put agreement between

the investor and the investee).

• Managing the receivables upon default is relevant

because it is the only activity that can significantly affect

the investee’s returns.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Relevant activity

Assessing Control

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

26

Power Exposure Link

Purpose

and design

Rights

Relevant

Activities

Decision

Making

Exposure

(or rights)

to variable

returns of

the

investee

Ability to

use power

over

investee to

affect its

own returns

27

• Broad definition of returns:

– dividends

– remuneration from services to an investee, fees and

exposure to losses

– residual interests on liquidation

– tax benefits

– access to future liquidity

– returns not available to other investors (eg synergies)

• Returns that have the potential to vary as a result of the

performance of the investee.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Exposure to variable returns

28

• An investor is exposed to variable returns when the

investor’s returns have the potential to vary as a result of

the investee’s performance

• The investor’s returns can be only positive, only negative

or both positive and negative

• Although only one investor can control an investee, more

than one party can share in the returns of an investee

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Exposure to variable returns

29

• A fund manager manages a mutual fund

• The fund manager determines the investment policy and

strategy of the fund

• An investor owns 55% of the shares in the fund

• No investor can unilaterally change the investment policy

and strategy of the fund

• No investor can remove the fund manager without cause

• Investors can redeem their interests at any time

• The fund manager receives a market-based management

fee of 2% of the net asset value

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Exposure to variable returns

Assessing Control

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

30

Power Exposure Link

Purpose

and design

Rights

Relevant

Activities

Decision

Making

Exposure

(or rights)

to variable

returns of

the

investee

Ability to

use power

over

investee to

affect its

own returns

31

• Power and exposure to variable returns from its

involvement with the investee are necessary conditions

for control (but still not enough)

• To control an investee, an investor must also have the

ability to use its power to affect investor’s returns from its

involvement with the investee

• Control occurs when the power can be used to benefit

the investor

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Link between power and returns

32

• An example of power without control is an agency

relationship

• Agency relationship has a principal and an agent

• The agent is a party contracted by a principal to perform

some service on behalf of the principal which involves

delegating some authority to the agent

• Delegated power does not mean control

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Link between power and returns

33

• Investee purchases financial assets funded by debt and

equity instruments issued to a number of investors

• Equity tranche absorbs first losses and receives residual

return

• Investor holds 35% of the equity tranche

• Investor also manages asset portfolio within guidelines

• Guidelines include decisions about the selection,

acquisition and disposal of the assets

• Investor receives market-based fixed and and

performance-related fees

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Link between power and returns

34

• A fund manager establishes, markets and manages a

fund according to narrowly defined parameters

• Fund manager:

– has discretion about the assets in which to invest

(Investors do not hold any substantive rights)

– holds a 10% investment in the fund

– does not have any obligation to fund losses beyond its

10% investment

– receives a market-based fee for its services equal to 1%

of the net asset value of the fund (fees are commensurate

with the services provided)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Agency

35

Fact pattern:

• A fund manager establishes, markets and manages a

fund and must make decisions in the best interests of all

investors

• Can be removed by simple majority but only for breach of

contract

• Fund manager has wide decision-making discretion

• The fund manager receives a market-based fee for its

services (fixed and performance-related). The fees are

commensurate with the services provided.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Agency

36

• A: fund manager also has 2% in the fund. No obligation

to fund losses beyond investment

• B: fund manager also has a more substantial investment

in the fund. No obligation to fund losses beyond

investment.

• C: fund manager has 20% investment. However, in this

example the fund manager can be removed by the board

of directors who are all independent of the fund manager

and are appointed by the other investors.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Agency

37

Rights to remove the manager (protective vs other)

Aggregate returns—magnitude and variability

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Agency: main judgements

38

• Entity can control with less than 50% of voting rights.

• Factors to consider include:

– Size of the holding relative to the size and dispersion of

other vote holders

– Potential voting rights

– Other contractual rights

• If the above not conclusive consider additional facts and

circumstances that provide evidence of power (eg voting

patterns at previous board meeting, etc)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

De facto Control

39

Substantive potential voting rights (PVR) can give the

holder power

• Consider the terms and conditions, including:

– Whether there are any barriers that prevent the holder

from exercising

– Whether exercise of the rights would be beneficial to the

holder

– Whether the rights are exercisable when decisions need

to be made

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Potential Voting Rights

40

General principles apply

• Consider purpose and design

• Identify which investee activities significantly affect its’

returns (‘relevant activities’)

• Identify how decisions about relevant activities are made

• Determine if investor has ability to make those decisions

• Determine if investor is exposed to variability associated

with returns of the investee

• Determine whether investor has ability to use its power to

affect its own returns

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Structured entities

41

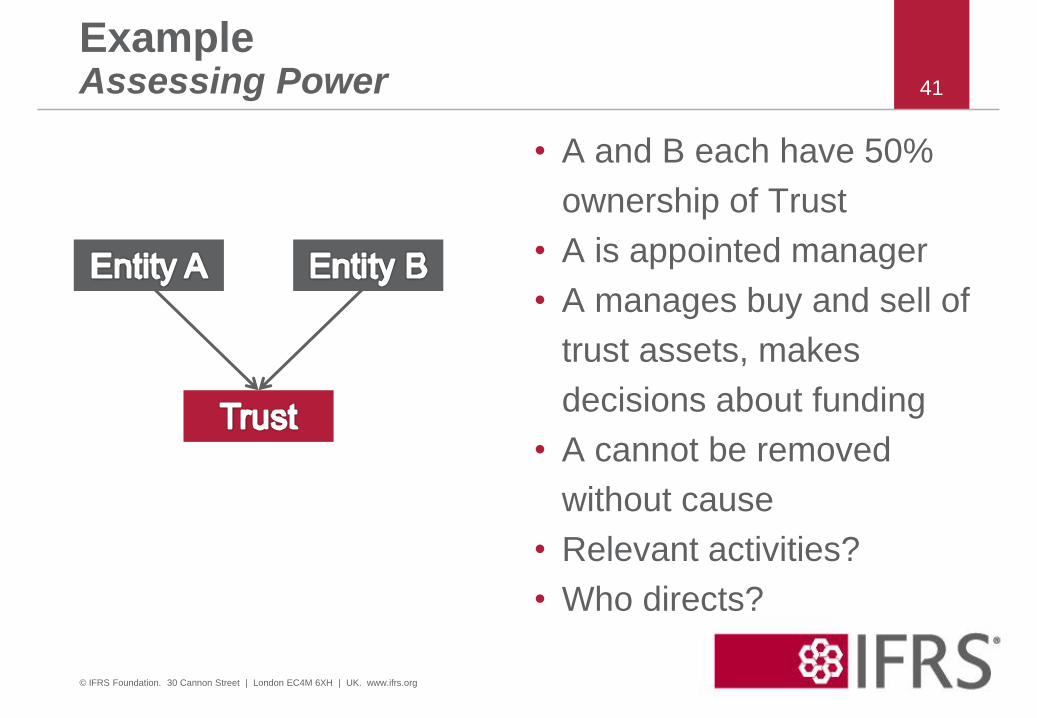

• A and B each have 50%

ownership of Trust

• A is appointed manager

• A manages buy and sell of

trust assets, makes

decisions about funding

• A cannot be removed

without cause

• Relevant activities?

• Who directs?

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Assessing Power

42

Consider all of the following:

• scope of the decision-making authority

• rights held by other parties (ie kick-out rights)

• remuneration of the decision-maker

• other interests that the decision maker holds in the

investee

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Agency relationships

43

Responsible Entity:

• Broad decision making

powers

• Removal by simple majority

• Remuneration market-

based (1% of assets under

management + 20% of

profits above a hurdle)

• Equity interest of 20%

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example Delegated rights

44

An investment entity:

• Only invests for returns earned from investment income

and/or capital appreciation

• Manages and evaluates investment performance on fair

value basis

Accounting

• Measure subsidiaries, JVs and associates at fair value

• Non investment entity parent consolidates subsidiaries,

but can still measure JVs and associates of its

investment entity subsidiary at fair value

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Investment entities

45

• Determining control requires an assessment of all

relevant facts and circumstances, including:

– purpose and design of the investee;

– activities of the investee;

– how decisions about those activities are made; and

– rights held by the party involved with the investee

• Particularly challenging for some structured entities:

– relevant activities in those entities are not usually directed

by voting or similar rights.;

– benefits or returns expected from such investments can

be more difficult to assess.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Judgements and estimates

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

IFRS 11

47

Joint Arrangement

• IFRS 11 Joint Arrangements establishes principles for

financial reporting by parties to a joint arrangement

• Joint control exists where the parties, or a group of the

parties, have joint control of the arrangement

• Parties to a joint arrangement recognise their

rights and obligations arising from the arrangement,

regardless of its structure or legal form

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Joint Control

48

• Parties that have rights to the assets and obligations for

the liabilities relating to the arrangement are parties to a

joint operation

– A joint operator accounts for assets, liabilities and

corresponding revenues and expenses arising from the

arrangement

• Parties that have rights to the net assets of the

arrangement are parties to a joint venture

– A joint venturer accounts for an investment in the

arrangement using the equity method.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Classification

49

Structured through separate vehicle

• Assess the parties’ rights and obligations arising from the

arrangement by considering:

– the legal form of the separate vehicle

– the terms of the contractual arrangement, and, if relevant,

– other facts and circumstances

• Determine whether parties have rights to assets and

obligation for liabilities, or to net assets

Not structured through separate vehicle

• Parties have rights to assets and obligation for liabilities,

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Separate vehicle

50 Separate vehicle

Joint Venture

Jo

int O

pe

ratio

n

Legal form Do the parties have rights to the assets

and obligations for the liabilities?

Contractual

terms

Do parties have contractual rights to the

assets, and obligations for the liabilities?

Other

Is the arrangement designed so:

• Its activities primarily aim to provide

parties with an output, and

• b) It depends on the parties for settling

liabilities?

✔

✗

✗

✗

✔

✔

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

51

• Separate vehicle is jointly controlled by two parties

• Purpose of the vehicle is to construct and sell residential

units

• Neither legal form nor the contractual terms give the

parties rights to the assets or obligations for the liabilities

• Equity contributed is sufficient to buy the land and raise

debt finance for the construction

• Sales proceeds will be used to repay external debt and

remaining profit is distributed to parties

• Parties provide guarantee to financier

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example

52

• Two parties jointly establish an entity over which they

have joint control to process the ore from a mine

• Parties have agreed:

– Parties purchase all the output produced by the entity in a

ratio of 60:40 (in proportion to ownership interest)

– Entity cannot sell the output to third parties

– Price of the output is set by the parties at a level to cover

production and admin costs (i.e. Entity breaks even)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Example

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

IFRS 12

54

Combined disclosure standard for:

• Subsidiaries

• Joint arrangements

• Associates

• Unconsolidated structured entities

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Scope

55

To disclose information that helps users of financial

statements evaluate:

• the nature of, and risks associated with, an entity’s

interests in other entities, and

• the financial effects of those interests on the entity’s

financial position, financial performance and cash flows

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Disclosure objective

56

Disclosure

• significant judgements and assumptions made

• information about interests in:

– subsidiaries

– joint arrangements and associates

– unconsolidated structured entities

• any additional information that is necessary to meet the

disclosure objective

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Meeting the objective

57

• The composition of the group (including any changes)

• Involvement of NCI in the group’s activities (including

profit and loss allocation and summarised financial

information for subsidiaries with large NCI)

• The effect of significant or unusual restrictions on assets

and liabilities

• The nature of, and changes in, the risks associated with

structured entities

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Subsidiaries

58

• Nature, extent and financial effects of interests eg:

– nature, purpose, size, activities and financing

– For sponsors not providing other risk disclosures

– Type of income earned

– The carrying amount of all assets transferred

• Nature of and changes in risks associated with interests

– Carrying amount of the assets and liabilities recognised

– Maximum exposure to loss and comparison to carrying

amounts

– Non-contractual support provided

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Unconsolidated structured entities

59

• Nature, extent and financial effects of interests eg:

– Name and nature where individually-material

– Summarised financial information for each individually-

material JV and associate, and in total for all others

– Fair value where individually material if quoted

– Unrecognised share of losses of JVs and associates

– Nature and extent of restrictions on transfer of funds

• Nature of and changes in risks associated with interests

– Commitments and contingent liabilities

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Joint arrangements and associates

60

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Questions