ifrss and the ifrs for smes - world...

TRANSCRIPT

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter, not necessarily those of the IASC Foundation or the IASB

IASC Foundation

IFRSs and the IFRS for SMEs

Why global standards?

© 2010 IASC Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

26 May 2010

Chisinau, Moldova

Michael Wells, Director, IFRS Education Initiative, IASC Foundation

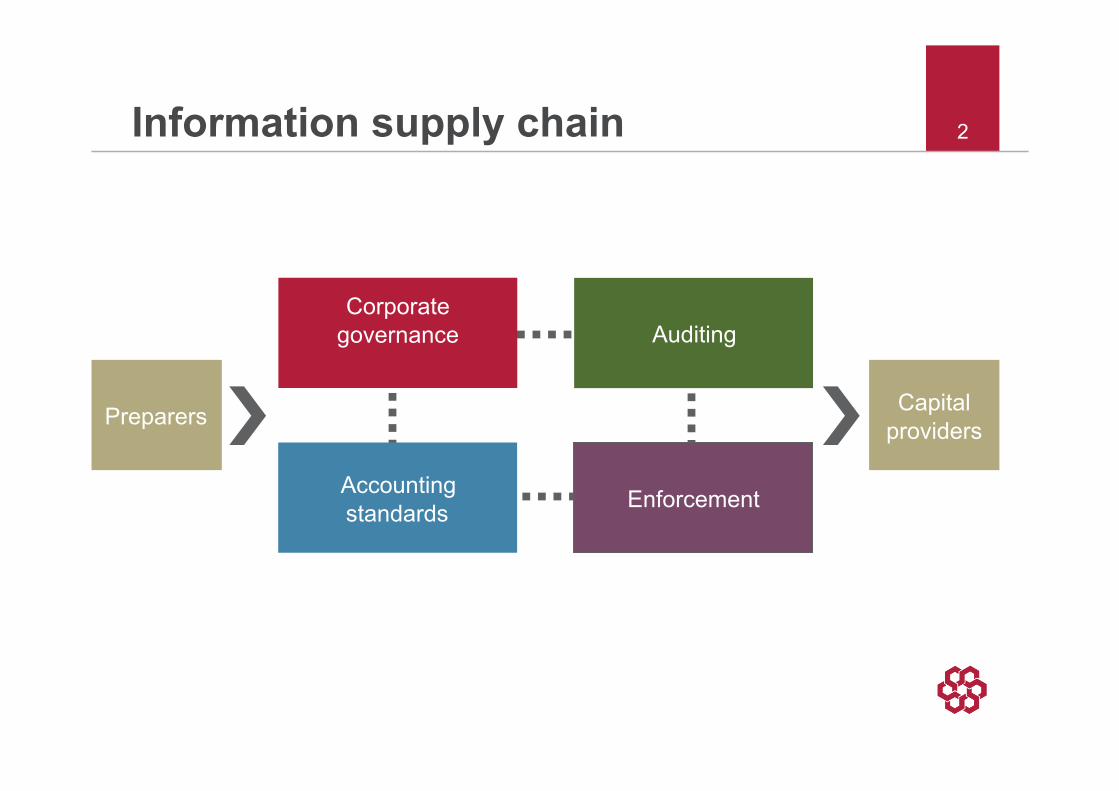

Information supply chain 2

Preparers Capital providers

Corporate governance Auditing

Accounting standards Enforcement

Benefits of global standards

• Efficient allocation of capital globally – attracting investment through transparency – reducing the cost of capital – increasing world-wide investment

• Reducing costs and increased efficiency – facilitates standardising information systems – eliminates wasteful reconciliations – audit efficiencies – education and training

3

IASB’s goal

• To provide the world’s integrating capital markets with a common language for financial reporting – in fulfilling this objective, take account of

the needs of – small and medium-sized entities – emerging economies

4

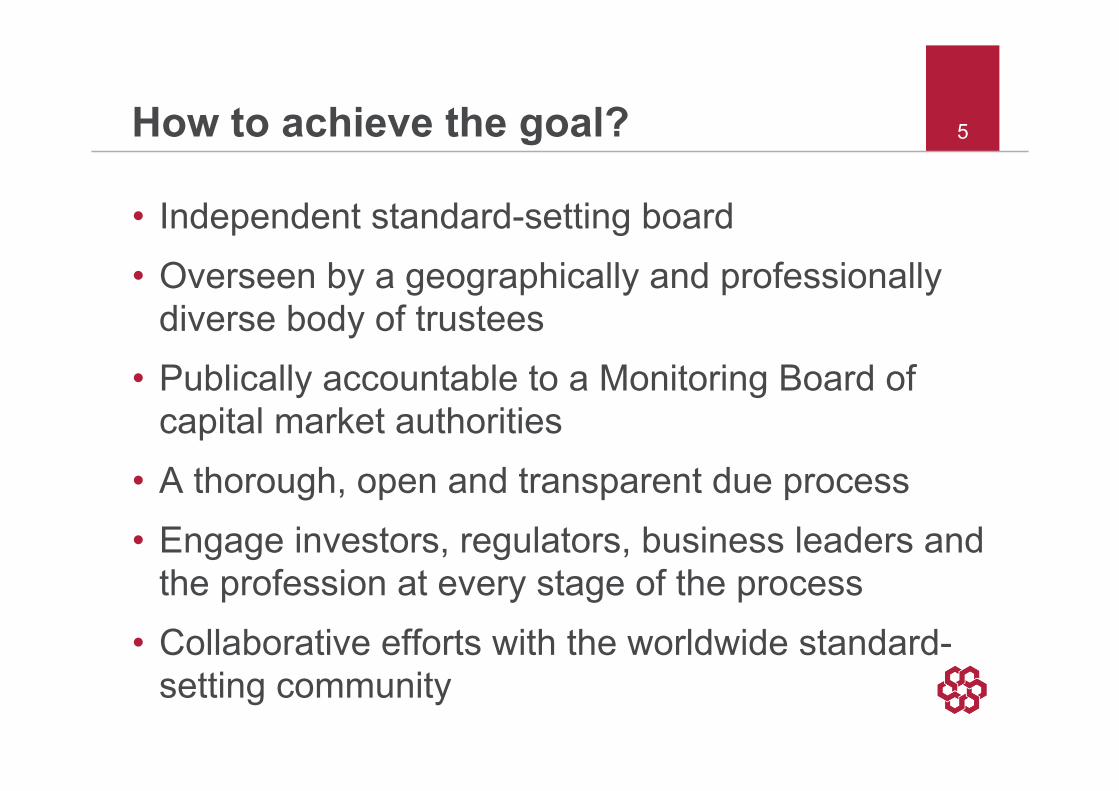

How to achieve the goal?

• Independent standard-setting board • Overseen by a geographically and professionally

diverse body of trustees • Publically accountable to a Monitoring Board of

capital market authorities • A thorough, open and transparent due process • Engage investors, regulators, business leaders and

the profession at every stage of the process • Collaborative efforts with the worldwide standard-

setting community

5

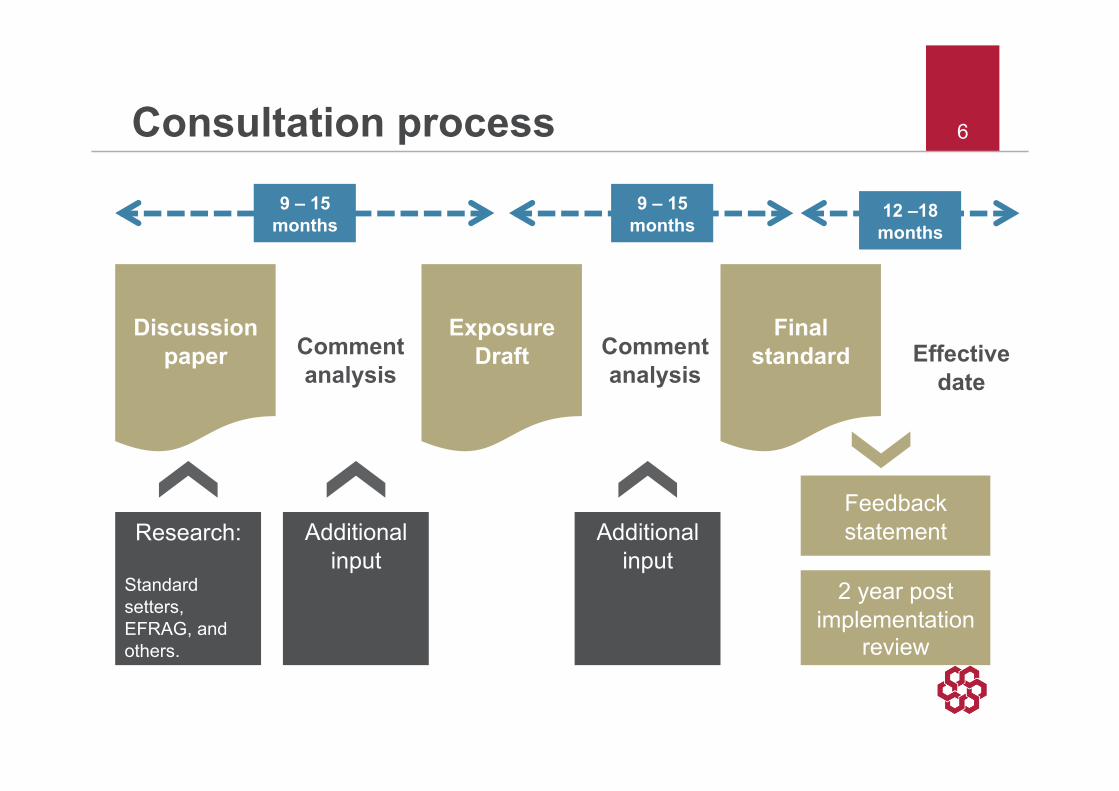

Consultation process 6

Discussion paper

Exposure Draft

Final standard Comment

analysis Comment analysis

Research:

Standard setters, EFRAG, and others.

Effective date

9 – 15 months

9 – 15 months

12 –18 months

Additional input

Additional input

Feedback statement

2 year post implementation

review

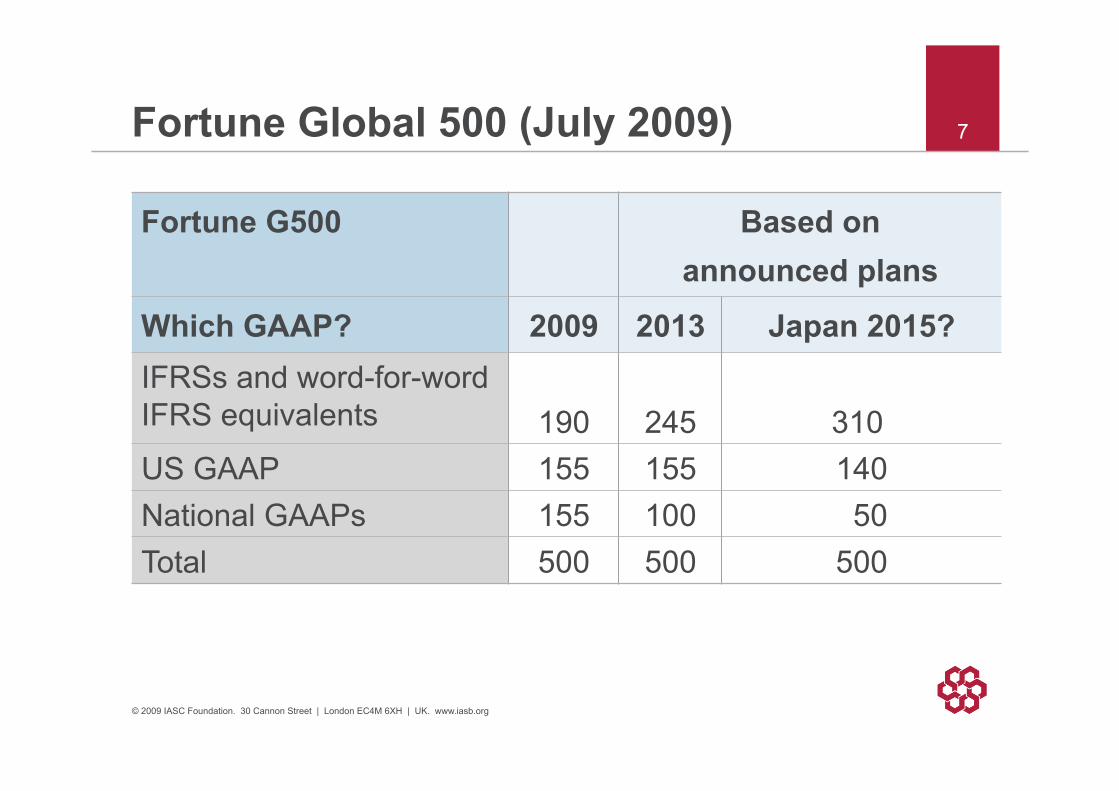

Fortune Global 500 (July 2009)

© 2009 IASC Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

7

Fortune G500 Based on announced plans

Which GAAP? 2009 2013 Japan 2015? IFRSs and word-for-word IFRS equivalents 190 245 310 US GAAP 155 155 140 National GAAPs 155 100 50 Total 500 500 500

8 Ideal use of IFRSs

Adopt IFRSs as issued by the IASB – audit report & basis of presentation note

refer to conformity with IFRSs – without local ‘endorsement’

9 The IFRS for SMEs

Good financial reporting made simple • 230 pages (vs +2,800 in full IFRSs) • Simplified international standard

– built on an IFRS foundation • Designed for the general purpose

financial statements of SMEs • Internationally recognised

10 Why an IFRS for SMEs?

• Improve access to credit – bank lending decisions and monitoring

outstanding loans – supports lending based on the borrower’s

financial performance and cash flows – vendors evaluate finances of buyers (and

vice versa) – foreign loans and suppliers – credit rating

11 Why an IFRS for SMEs continued

• Improve access to equity capital – non-management investors – foreign venture capital

• Education and training • Auditing efficiencies • Ease burden where full IFRSs is now

required

12 Why would an SME want to adopt it?

• “Transparency, Ownership, and Financing Constraints in Private Firms” (Hope, Thomas, and Vyas), November 2009

• Study: Around 31,000 small companies in 68 developing countries and emerging markets

• Abstract: We find that private firms with greater financial transparency experience significantly lower problems with gaining access to external finance (and obtain those funds at a lower cost) than do other private firms.

13 Why would an SME want to adopt it?

• “Financial Reporting Quality and Investment Efficiency of Private Firms in Emerging Markets” (Chen, Hope, and Li, November 2009)

• Study: Around 7,000 small companies in 20 emerging markets

• Abstract: We find strong evidence that accounting quality positively affects investment efficiency (i.e., is negatively related to both underinvestment and overinvestment) for our sample of relatively small private firms in lower-income countries.

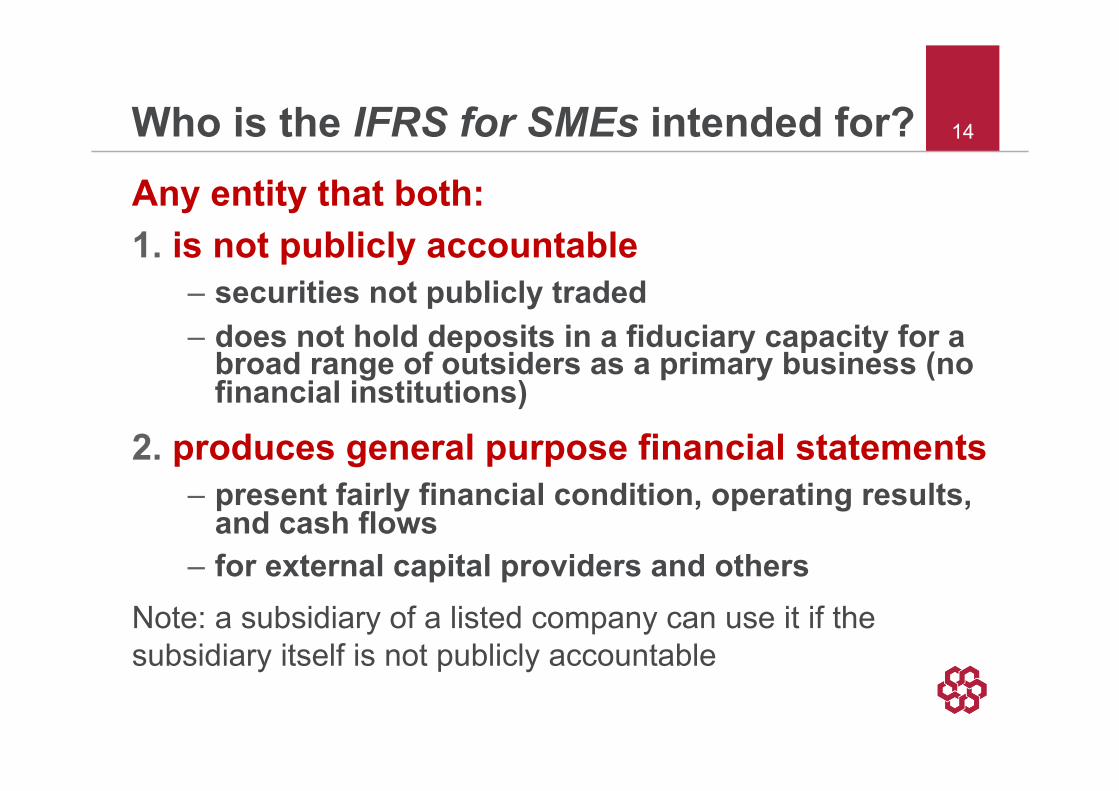

14 Who is the IFRS for SMEs intended for? Any entity that both: 1. is not publicly accountable

– securities not publicly traded – does not hold deposits in a fiduciary capacity for a

broad range of outsiders as a primary business (no financial institutions)

2. produces general purpose financial statements – present fairly financial condition, operating results,

and cash flows – for external capital providers and others

Note: a subsidiary of a listed company can use it if the subsidiary itself is not publicly accountable

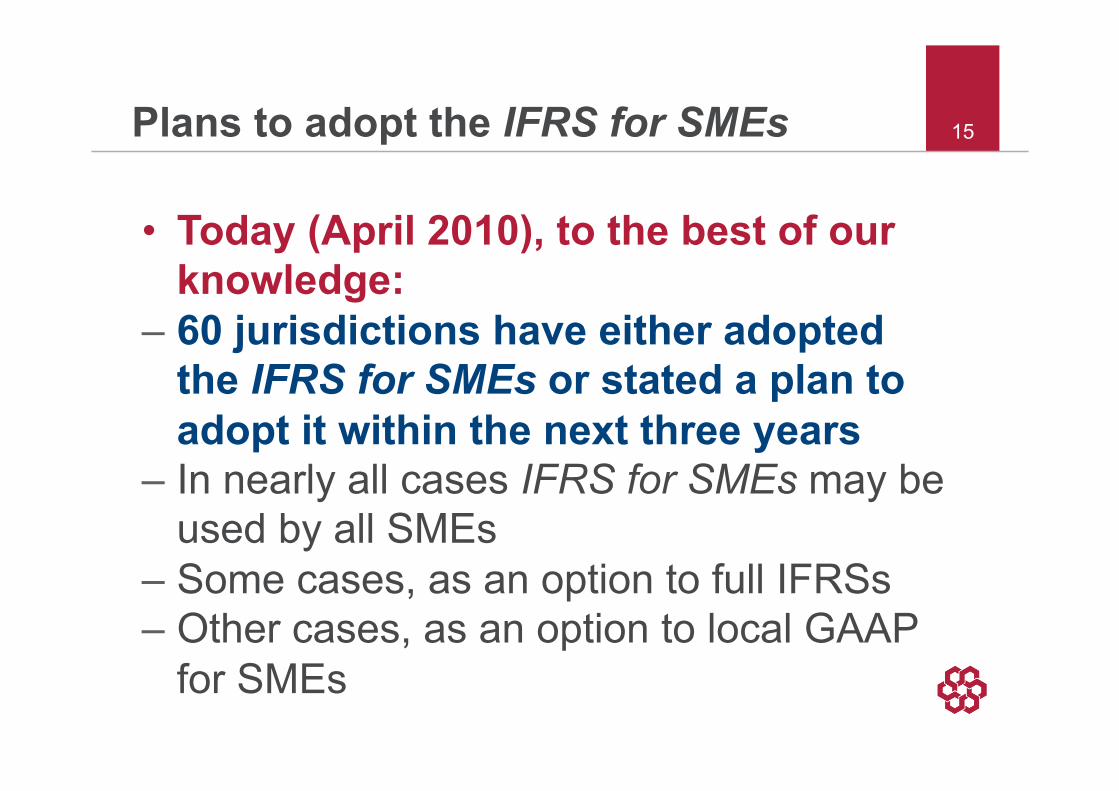

15 Plans to adopt the IFRS for SMEs

• Today (April 2010), to the best of our knowledge:

– 60 jurisdictions have either adopted the IFRS for SMEs or stated a plan to adopt it within the next three years

– In nearly all cases IFRS for SMEs may be used by all SMEs

– Some cases, as an option to full IFRSs – Other cases, as an option to local GAAP

for SMEs

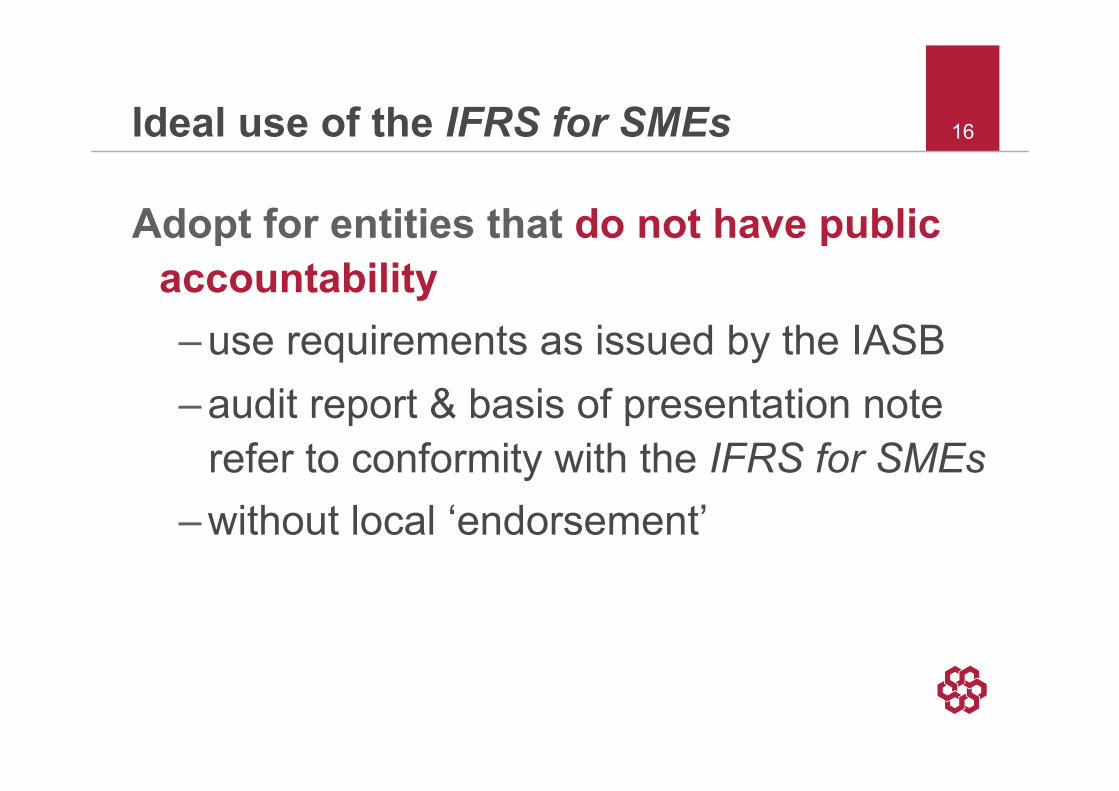

16 Ideal use of the IFRS for SMEs

Adopt for entities that do not have public accountability – use requirements as issued by the IASB – audit report & basis of presentation note

refer to conformity with the IFRS for SMEs – without local ‘endorsement’

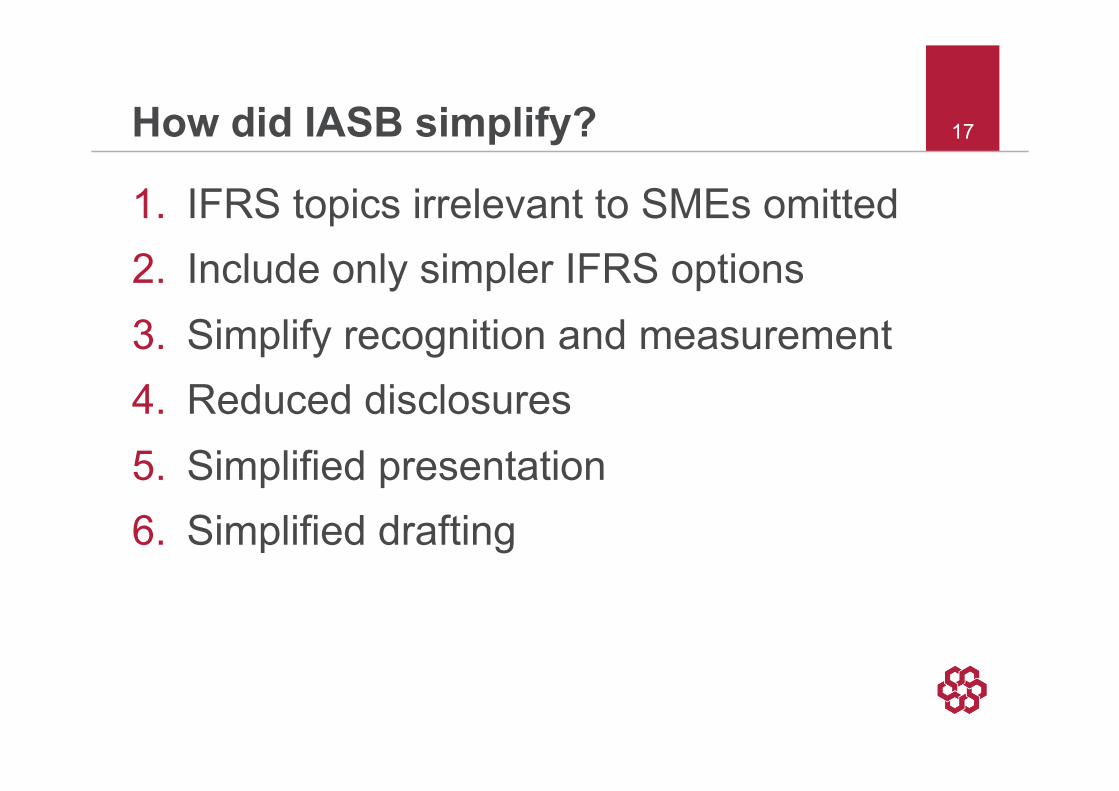

17 How did IASB simplify?

1. IFRS topics irrelevant to SMEs omitted 2. Include only simpler IFRS options 3. Simplify recognition and measurement 4. Reduced disclosures 5. Simplified presentation 6. Simplified drafting

18 Plan for maintenance

• Initial comprehensive review after 2 years implementation experience

– fix errors and omissions, lack of clarity – consider need for improvements based on

recent IFRSs and amendments to IASs • Thereafter once every three years

(approximately) omnibus exposure draft of updates

19

Implementation support for the IFRS for SMEs

• Released with the IFRS for SMEs – illustrative financial statements – presentation and disclosure checklist

• SME Implementation Group to address questions

– guidance in the form of Q&As • IASCF training material • Facilitate regional ‘train the trainers’

workshops organised by others

IASCF IFRS for SMEs training material

• IASCF does not certify accountants • Training material developed for use by

others – developed by IASCF education staff – multi-level peer review – not IASB approved

• 35 standalone modules (1 for each section of the IFRS for SMEs)

• Training material = +2,000 A4 pages

20

Access to IASCF training material • Free to download (PDF files of modules)

http://www.iasb.org/IFRS+for+SMEs/Training+modules.htm

• Self study • You can incorporate the modules (PDF

files) into your IFRS for SMEs education and training programmes

21

• Each module includes – introductory material – explanation of the requirements

– full text of the requirements – ‘how to’ examples – other explanations

– discussion of important judgements – comparison with full IFRSs – test your knowledge—multiple choice – apply your knowledge—case studies

Content of IASCF training material 22

Propose to development agencies & others

• Fund the official translation of the training material?

• Organise regional ‘train the trainers’ workshops?

– IASCF staff willing to lead regional workshops • Assist developing nations build

sustainable IFRS for SMEs application capacity? Regional ‘train the trainers’ workshops are already planned in 2010 for Africa, Asia and Latin America & the Caribbean

23

24 Translations of the IFRS for SMEs

• Complete or nearly complete: – Chinese, Spanish, Italian, Romanian • In process: – Arabic, Czech, French, Japanese, Serbian,

Turkish • Proposed or in discussion: – Armenian, Khmer, Macedonian, Polish,

Portuguese, Russian, Ukrainian

25 Translations of the IASCF training material

• Proposed or in discussion: – Russian (USAID funding) – Spanish (World Bank funding)

© 2010 IASC Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

26 Questions or comments?

Expressions of individual views by members of the IASB and its staff are encouraged.

The views expressed in this presentation are those of the presenter.

Official positions of the IASB on accounting matters are determined only after extensive due process and deliberation.