continued earnings improvement text despite...

TRANSCRIPT

TextText

Continued earnings improvement despite temporary headwinds in operationsPresentation of the Q1/2018 resultsMartin Lindqvist, President & CEOHåkan Folin, CFOApril 20, 2018

Agenda

2

Q1/2018 – In summary

Q1/2018 – Performance by divisionFinancials

Outlook

Q&A

Q1/2018 – In summary

3

Generally good demand

Good growth in strategic areasPositive outlook – volume and price

Improved earnings despite operational headwinds

HYBRIT takes the next step AGM approved dividend of SEK 1.00 per share

Q1 negatively impacted by operational issues in Sweden

4

Lack of rail car capacity of slabs between Luleåand Borlänge

Alternative sea transport via Oxelösund usedResulting in delays, higher shipment costs, and output and shipment losses

Production disruption in Oxelösund in the blast furnace

Resulted in 2 weeks of lost steel making production, and also impacting rolling

Luleå

OxelösundBorlänge

55

Spot price development: Hot Rolled Coil (HRC) in Northern Europe, Plate in US, HRC in China

Indexed (Jan 2013 =100)

Q1

Northern Europe/HRC

US/Plate

HRC, Northern Europe

Plate, US

HRC, China

0

20

40

60

80

100

120

140

160

Jan13

Mar13

May13

Jul13

Sep13

Nov13

Jan14

Mar14

May14

Jul14

Sep14

Nov14

Jan15

Mar15

May15

Jul15

Sep15

Nov15

Jan16

Mar16

May16

Jul16

Sep16

Nov16

Jan17

Mar17

May17

Jul17

Sep17

Nov17

Jan18

Mar18

Northern Europe US China

Strong demand both in Europe and North America

Good demand continued, low imports,inventories in balance, spot prices

increasedStrong demand fromboth end-users and

distributors, low inventories, plate spot

prices increased sharply

Q1/2018 -Performance by division

6

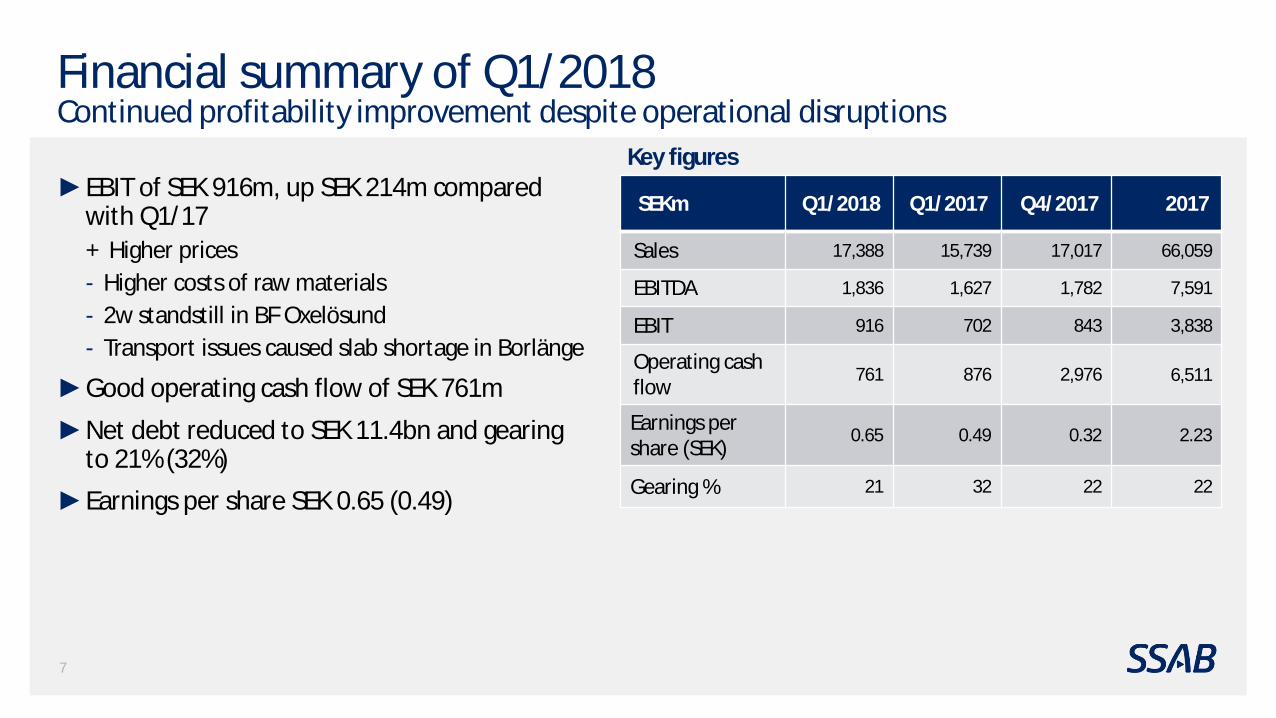

Financial summary of Q1/2018Continued profitability improvement despite operational disruptions

7

EBIT of SEK 916m, up SEK 214m comparedwith Q1/17+ Higher prices- Higher costs of raw materials- 2w standstill in BF Oxelösund- Transport issues caused slab shortage in Borlänge

Good operating cash flow of SEK 761m

Net debt reduced to SEK 11.4bn and gearing to 21% (32%)Earnings per share SEK 0.65 (0.49)

SEKm Q1/2018 Q1/2017 Q4/2017 2017

Sales 17,388 15,739 17,017 66,059

EBITDA 1,836 1,627 1,782 7,591

EBIT 916 702 843 3,838

Operating cash flow

761 876 2,976 6,511

Earnings per share (SEK)

0.65 0.49 0.32 2.23

Gearing % 21 32 22 22

Key figures

Sales and EBITDA marginSEKm

8

SSAB Special SteelsGood demand continued in all segments, especially Construction Machinery and Material Handling

EBIT of SEK 434m, up SEK 191m comparedwith Q1/17+ Higher prices+ Higher volumes- Higher costs of raw materials- Standstill in BF Oxelösund

Shipments +9% vs. Q4/17 and +25% vs. Q1/17

SEKm Q1/2018 Q1/2017 Q4/2017 2017

Sales 4,674 3,925 4,368 16,053

EBITDA 569 377 777 2,002

EBIT 434 243 641 1,465

Shipments,ktonnes 346 277 318 1,192

-5%

0%

5%

10%

15%

20%

25%

-500

500

1,500

2,500

3,500

4,500

5,500

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

Sales EBITDA %

9

SSAB Special SteelsShipments

(thousand tonnes)

277318

346

0

50

100

150

200

250

300

350

400

Q1 2017 Q4 2017 Q1 2018

243

641

434

0

100

200

300

400

500

600

700

Q1 2017 Q4 2017 Q1 2018

Operating profit(SEK millions)

KtonSEKm

Lost sales and underabsorption

+ SEK 265 m. compensation for breakdown

Negative impactfrom standstill

Standstill in Q1 did not impactshipmentsImpacted by

breakdown in rolling mill

SEKm

10

SSAB Europe

10

Good demand continued in all segments

EBIT in Q1/18 was SEK 657m, down SEK 169m vs. Q1/17+ Higher prices

Higher raw material costsTransportation problems causing slab shortage in BorlängeLower volume

Shipments +4% vs. Q4/17, but -4% vs. Q1/17+ Automotive premium continued at good level,

+11% vs. Q1/17

Sales and EBITDA margin

SEKm Q1/2018 Q1/2017 Q4/2017 2017

Sales 8,051 7,657 7,768 31,048

EBITDA 998 1,182 811 4,405

EBIT 1) 657 826 460 2,988

Shipments,ktonnes 939 982 901 3,745

1) Excluding depreciation/amortization on surplus values on intangible and tangible fixed assets related to the acquisition of Rautaruukki.

0%2%4%6%8%10%12%14%16%18%20%

01,0002,0003,0004,0005,0006,0007,0008,0009,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

Sales EBITDA %

SSAB Americas

11

Demand improved and plate prices continued to increase

EBIT in Q1/18 was SEK 129m, up SEK 286m from Q1/17+ Higher prices+ Higher volumes+ No maintenance outage (Q1-Q2/17 in Mobile)- Higher raw material costs

Shipments +8% vs. Q1/17, but slightly lower than in Q4/17

SEKm Sales and EBITDA margin

SEKm Q1/2018 Q1/2017 Q4/2017 2017

Sales 3,363 3,019 3,230 12,727

EBITDA 283 8 141 818

EBIT 1) 129 -157 -15 183

Shipments,ktonnes 523 486 525 1,971

1) Excluding depreciation/amortization on surplus values on intangible and tangible fixed assets related to the acquisition of IPSCO.

0%2%4%6%8%10%12%14%16%18%20%

0

1,000

2,000

3,000

4,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

Sales EBITDA %

Tibnor

Sales increased by 2% both vs. Q1/17 and Q4/17

EBIT in Q1/18 was SEK 67m, down SEK 32m from Q1/17

Lower volumes and margins

12

SEKm Sales and EBITDA margin

SEKm Q1/2018 Q1/2017 Q4/2017 2017

Sales 2,058 2,019 2,012 7,821

EBITDA 87 118 63 334

EBIT 1) 67 99 42 252

Shipments (kton) 176 190 180 7161) Excluding depreciation/amortization on surplus values on intangible and tangible fixed assets related to the acquisition of Rautaruukki.

0%

1%

2%

3%

4%

5%

6%

7%

0

500

1,000

1,500

2,000

2,500

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

Sales EBITDA %

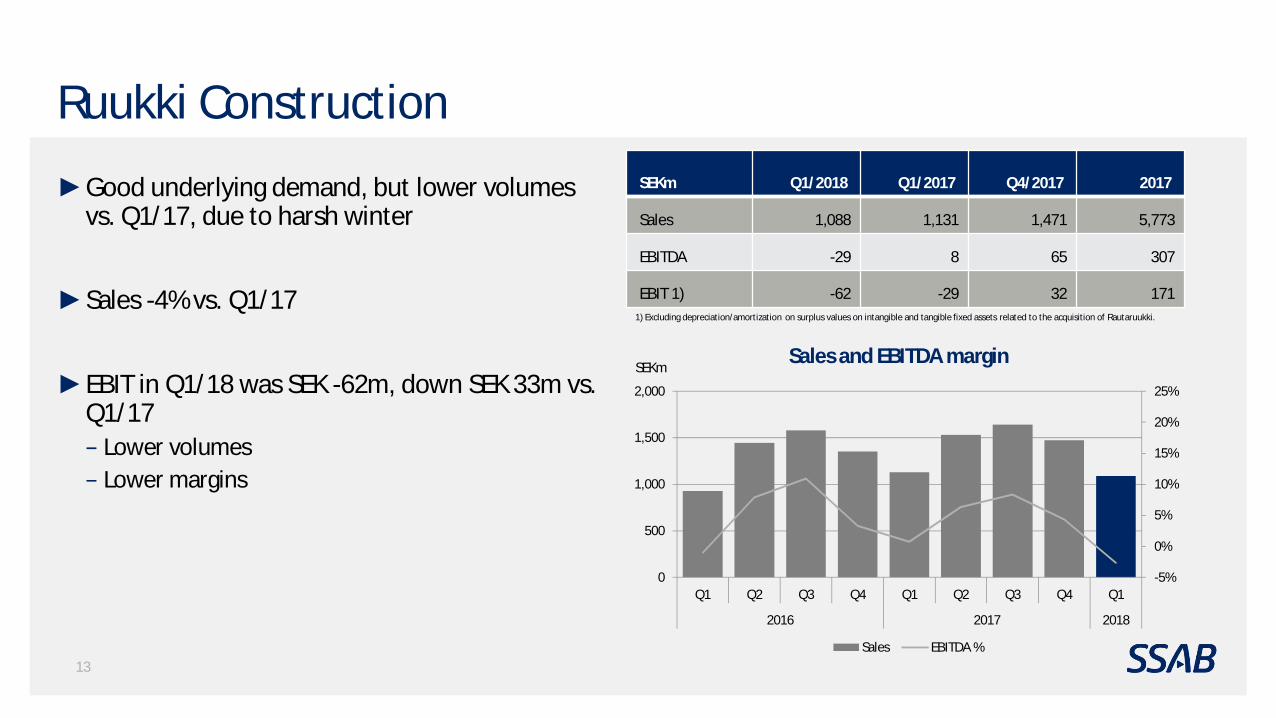

Ruukki Construction

Good underlying demand, but lower volumes vs. Q1/17, due to harsh winter

Sales -4% vs. Q1/17

EBIT in Q1/18 was SEK -62m, down SEK 33m vs. Q1/17

Lower volumesLower margins

13

SEKmSales and EBITDA margin

SEKm Q1/2018 Q1/2017 Q4/2017 2017

Sales 1,088 1,131 1,471 5,773

EBITDA -29 8 65 307

EBIT 1) -62 -29 32 1711) Excluding depreciation/amortization on surplus values on intangible and tangible fixed assets related to the acquisition of Rautaruukki.

-5%

0%

5%

10%

15%

20%

25%

0

500

1,000

1,500

2,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

Sales EBITDA %

Financials

Improvement year-on-year continued

15

Sales

EBITDA and EBITDA margin

Shipments1

EBITDA per tonne delivered steel

1) Including the steel operations: Special Steels, Europe and Americas

02,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

SEK

mill

ion

0200400600800

1,0001,2001,4001,6001,8002,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

kton

s

0.0 %

2.0 %

4.0 %

6.0 %

8.0 %

10.0 %

12.0 %

14.0 %

0

500

1,000

1,500

2,000

2,500

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

SEK

mill

ion

EBITDA EBITDA %

0200400600800

100012001400

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

SEK/

tonn

e

Change in operating profit Q1/2018 vs. Q1/2017

SEKm

16

916

280702

Q1/2018Other

74

FXFixed cost

-210

Var COGS

-1 130

Volume

0

Price

1 200

Q1/2017

Change in operating profit Q1/2018 vs. Q4/2017

SEKm

17

*Includes the compensation of SEK 265m for the breakdown in Oxelösund

520

100

175

110916

Q1/2018Other*

-197

FXFixed costVar COGS

-635

VolumePriceQ4/2017*

843

Continued positive cash flow in Q1SEKm Q1/2018 Q1/2017 Q4/2017 2017

Operating profit before depreciation/amortization 1,836 1,627 1 782 7 591

Change in working capital -799 -526 1 736 303

Maintenance expenditure -285 -215 -563 -1 366

Other 9 -10 21 -17

Operating cash flow 761 876 2 976 6 511

Financial items -141 -222 -197 -943

Taxes -236 -21 -94 -249

Cash flow from current operations 384 633 2 685 5 319

Strategic capital expenditure in plant and machinery-63 -44 -85 -237

Acquisitions of shares and operations -10 0 0 -11

Divestments of shares and operations 0 0 1 1

Cash flow before dividend 311 589 2 601 5 072

18

Cash flow trend

Potential to further improve profitability

Well-investedReduction of working capital/sales

Lower interest cost

Tax rate ~20%

19

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17 Q3/17 Q4/17 Q1/18

Operating cash flow (Rolling 12 months)

SEKmOperating cash flow

Maturity profile and net debt

20

Loans maturing in 2018-2020 amounts to around SEK 9.2bn

Duration of the loan portfolio was 5.5 years (5.5 at the end of 2017)

Net gearing ratio decreased from 22% at the end of 2017 to below 21%

Net debt decreased by SEK 183m during Q1/18 and amounted to SEK 11.4bn

SEKm

Maturity profile Q1/2018

9.2bn

Back-up facilities

Cash

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Cash andback-upfacilities

2018 2019 2020 2021 2022 2023+

Iron ore and coking coal – Purchase prices increased

21

Average coking coal purchase price in Q1/18 was 23% higher in terms of SEK (+27% in USD) vs. Q4/17

Coking coal

Iron ore

Average pellet purchase price in Q1/18 was 18% higher in terms of SEK (+21% in USD) vs. Q4/17

SSAB’s purchase price, coking coal and iron ore

Indexed

50

100

150

200

250

300

Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018

Coal ( SSAB purchase price, index) Iron ore (SSAB purchase price, index)

0

50

100

150

200

250

300

350

400

Jan-

15Fe

b-15

Mar

-15

Apr-

15M

ay-1

5Ju

n-15

Jul-1

5Au

g-15

Sep-

15O

ct-1

5N

ov-1

5De

c-15

Jan-

16Fe

b-16

Mar

-16

Apr-

16M

ay-1

6Ju

n-16

Jul-1

6Au

g-16

Sep-

16O

ct-1

6N

ov-1

6De

c-16

Jan-

17Fe

b-17

Mar

-17

Apr-

17M

ay-1

7Ju

n-17

Jul-1

7Au

g-17

Sep-

17O

ct-1

7N

ov-1

7De

c-17

Jan-

18Fe

b-18

Mar

-18

Apr-

18

Chicago #1HM Scrap (AMM) [USD/gross ton]

Scrap – Upwards price trend continued

22

SSAB’s average purchase price for scrap was 23% higher in Q1/18 vs. Q4/17 (USD)

Spot prices have increased also in April

Scrap spot priceUSD/gross ton

Q1/2018

Source: AMM

Outlook

SSAB’s outlook for Q2/2018

24

Segment Volume trend Q2 vs. Q1 Comment

SSAB Special Steels High level in Q1

SSAB Europe Transport problem resolved

SSAB Americas Strong demand

In North America, demand for heavy plate is expected to remain strong

In Europe, demand for strip and heavy plate is expected to remain good

The underlying demand for high-strength steels is anticipated to be good in most markets

The prices realized by the three steel divisions are expected to be somewhat higher during the second quarter, particularly for SSAB Americas

25

Initiative for fossil-free steel – HYBRITJoint venture with Vattenfall and LKAB

Successful pre-feasibility study closed in Q1 2018

Planning and designing of pilot plants in Luleå and the iron ore field in Norrbotten

First ground to be broken during the summer

Summary

26

Generally good demand

Good growth in strategic areasPositive outlook - volume and price

Improved earnings despite operational headwinds

Questions & Answers

Appendix

Major planned maintenance outages in 2018

29

No major planned maintenance outages in Q2/18

Costs in 2018 are estimated to be SEK 885m (1,010) Lower cost in SSAB Americas compared to 2017

SEKm Q1/18 Q2/18 Q3/18 Q4/18 2018 2017

SSAB Special Steels

- - - 230 230 230

SSAB Europe - 40 210 125 375 390

SSAB Americas - - - 280 280 390

Total - 40 210 635 885 1,010

Note: The estimates shown in table includes direct maintenance cost and cost of lower capacity utilization (under absorption), but excludes lost margins.

SSAB’s key customer segments – outlook Segment Outlook for Q2

vs. Q1 Comments on outlook

Heavy TransportSolid demand expected in Europe, especially heavy truck segment

Slight improvement expected for Railcar production in US (dry goods)

Automotive Automotive is expected to remain at high level in Europe, increase in Asia and slow down in US

Construction MachineryDemand in the main European markets is expected to continue at good level

Continued recovery in US expected

Material HandlingHigh activity in the Mining sector

Pick-up also in investments of new machinery

EnergyContinued solid demand in wind energy expected

Oil-related segments has improved, higher activity in line pipe

Construction Demand expected to be seasonally improving

Service Centers (US) Demand in general expected to remain good

30

Anti-dumping measures are in placeand under preparation in EU and the US

Cold-rolled carbon steels (China, Russia)Hot-Rolled flat carbon steels (China) • Final AD duties for strip 18%-36% in April 2017 and 65%-74% for

plate in Feb 2017

Hot-Rolled flat carbon steels (Brazil, Russia, Iran, Serbia and Ukraine)

Definitive AD duties on imports of hot rolled coil from Brazil, Iran, Russia and Ukraine in Oct 2017

Under preparationIn place

Europe

US

Hot-rolled sheet and coils (China, Russia, India, Ukraine, Indonesia, Taiwan, Thailand)Hot-rolled sheet and coils (Australia, Brazil, Japan, Korea, Netherlands, Turkey)Heavy plate (China, India, Indonesia, Russia, Ukraine)Heavy plate (China, Austria, Belgium, Taiwan, France, Germany, Italy, Japan, South Korea)• Final AD decision for the 8 countries in March 2017 – increased

duties vs. preliminary duties

• Final AD and CVD decision on Chinese plate AD margin of 68% and a subsidy (CVD) margin of 251%

As a result of the Section 232 steel investigation a duty of 25% was imposed on imports from all countries (exceptions for a number of countries, including a temporary exception for the EU-28)

Corrosion Resistant Steel (China) Provisional anti-dumping duties of 17.2%-28.5% in Aug 2017

Cold-rolled sheet and coils (Brazil, India, Korea, Russia, United Kingdom)Heavy plate (Turkey, Brazil, South Africa)

Preliminary AD decision in place for Turkey, Brazil, South Africa

31

Net debt and gearing continued to decrease

32

Net gearing ratio decreased from 22% at the end of 2017 to below 21%

Net debt decreased by SEK 183m during Q1/18 and amounted to SEK 11.4bn

%SEKm

Net debt and net debt/equity ratio

0

10

20

30

40

50

60

2012 2013 2014 2015 2016 2017 Q1/20180

5,000

10,000

15,000

20,000

25,000

30,000

Net interest bearing debt, SEKm Net gearing ratio, %

Debt cost and duration%

Duration on debt portfolio and interest rate

33

Duration of the loan portfolio was 5.5 years (5.5 at the end of 2017)

Averaged fixed interest term was 1.0 years (1.1 in Q4/17) Average interest rate was 3.60% (3.42 % in Q4/17)

Years

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Avg. duration (rhs) Avg. interest rate