copyright 2002, pearson education canada1 input demand: the labour and land markets chapter 10

Post on 19-Dec-2015

215 views

TRANSCRIPT

Copyright 2002, Pearson Education Canada1

Input Demand: The Labour and Land Markets

Chapter 10

Copyright 2002, Pearson Education Canada2

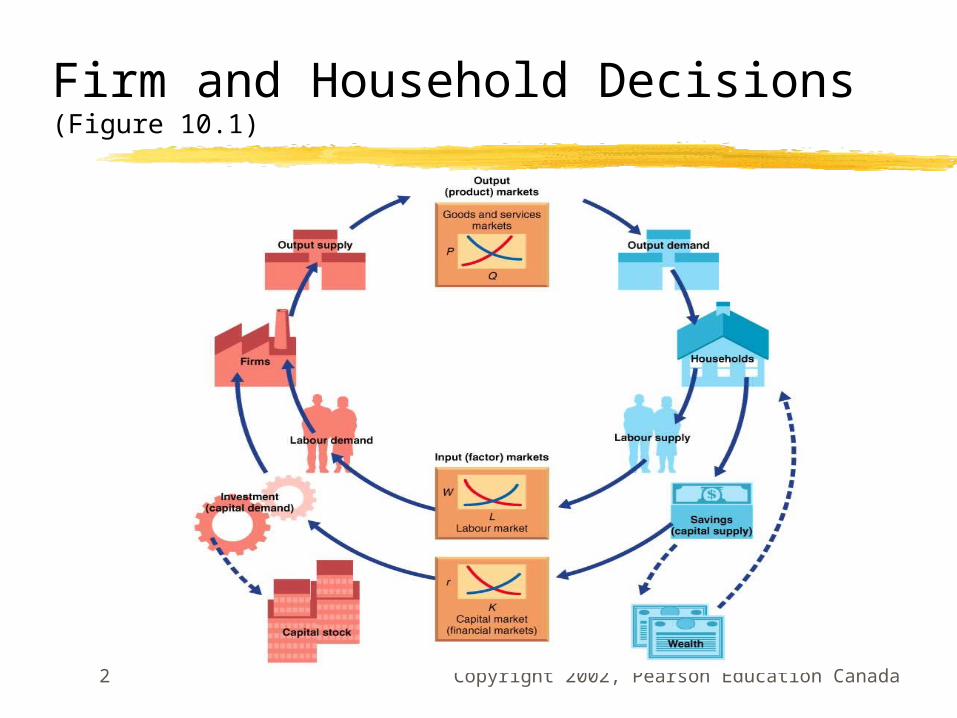

Firm and Household Decisions (Figure 10.1)

Copyright 2002, Pearson Education Canada3

Derived Demand

Derived demand is a demand for resources (inputs) that is dependent on the demand for the outputs those resources can be used to produce.

Copyright 2002, Pearson Education Canada4

Inputs

The productivity of an input is the amount of output produced per unit of that input.

Complementary inputs are factors of production that can be used together to enhance each other.

Substitutable inputs are factors of production that can be used in place of each other.

Copyright 2002, Pearson Education Canada5

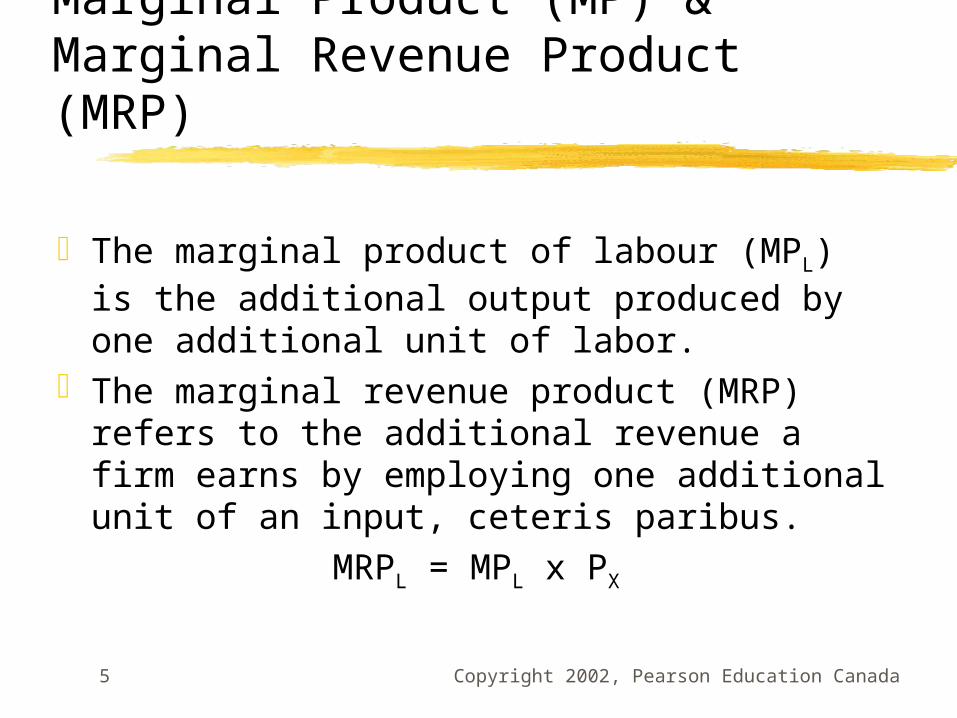

Marginal Product (MP) & Marginal Revenue Product (MRP)

The marginal product of labour (MPL) is the additional output produced by one additional unit of labor.

The marginal revenue product (MRP) refers to the additional revenue a firm earns by employing one additional unit of an input, ceteris paribus.

MRPL = MPL x PX

Copyright 2002, Pearson Education Canada6

Marginal Revenue Product per Hour of Labour in Sandwich Production (Table 10.1)

Copyright 2002, Pearson Education Canada7

Deriving a Marginal Revenue Product Curve from Marginal Product (Figure 10.2)

The marginal revenue product of labour is the price of output, Px, times the marginal product of labour, MPL.

In competition, MRPL is the market value of labour’s marginal product.

As long as output price is constant, the MRPL curve has the same downward slope as the MPL curve.

Copyright 2002, Pearson Education Canada8

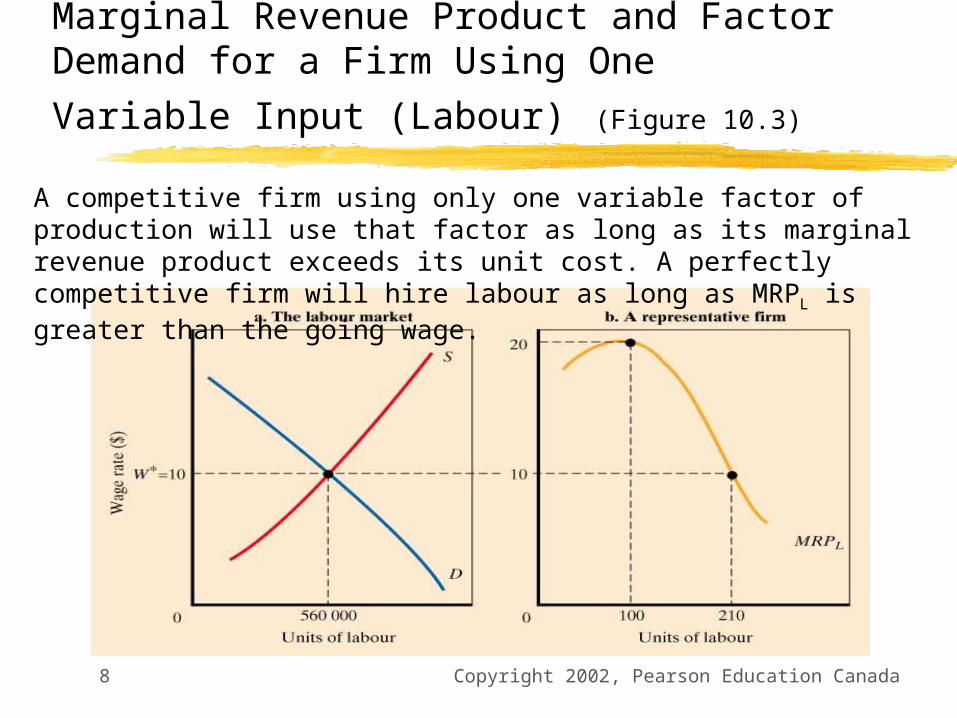

Marginal Revenue Product and Factor Demand for a Firm Using One Variable

Input (Labour) (Figure 10.3)

A competitive firm using only one variable factor of production will use that factor as long as its marginal revenue product exceeds its unit cost. A perfectly competitive firm will hire labour as long as MRPL is greater than the going wage.

Copyright 2002, Pearson Education Canada9

The Two Profit-Maximizing Conditions Are Simply Two Views of the Same Choice Process (Figure 10.4)

Copyright 2002, Pearson Education Canada10

A Firm Employing Two Variable Factors of Production

Suppose that the firm can vary its employment of both labour and capital.

How can the firm’s demand for labour and capital be characterized?

When more than one factor vary, we must consider the impact of a change in one factor price on the demand for other factors.

Copyright 2002, Pearson Education Canada11

Two Effects When the Price of an Input Changes

The factor substitution effect is the tendency of firms to substitute away from a factor whose relative price has risen and toward a factor whose relative price has fallen.

The output effect is the tendency of a firm to increase output when the price of an input falls; which in turn increases the demand for all inputs.

These effects explain the downward sloping input demand curve.

Copyright 2002, Pearson Education Canada12

Land Markets

Land has perfectly inelastic supply; the supply is strictly fixed.

Demand-determined price refers to the price of a good that is fixed in supply; it is determined exclusively by what firms and households are willing to pay for the good.

Pure rent is the return to any factor of production that is fixed in supply.

The firm will use land up to the point where MRPH = PH where H is land (hectares).

Copyright 2002, Pearson Education Canada13

The Firm’s Profit-Maximizing Condition in Input Markets

PL = MRPL = (MPL x PX) Labour Market

PK = MRPK = (MPK x PX) Capital Market

PH = MRPH = (MPH x PX) Land Market

MPL = MPK = MPH

PL PK PH

Copyright 2002, Pearson Education Canada14

Input Demand Curves

Several factors contribute to shifts in input demand curves: demand for outputs complementary and substitutable inputs prices of other inputs technological change

Copyright 2002, Pearson Education Canada15

Marginal Productivity Theory of Income Distribution

At equilibrium, all factors of production end up receiving rewards determined by their productivity as measured by marginal revenue product.

Copyright 2002, Pearson Education Canada16

Review Terms & Concepts

complementary inputs demand determined

price derived demand factor substitution effect marginal product of

labour (MPL) marginal productivity

theory of income distribution

marginal revenue product (MRP)

output effect of a factor price change

productivity of an input

pure rent substitutable inputs technological change