corporate headquarters petron megaplaza makati city

TRANSCRIPT

Pag-IBIG FundCorporate Headquarters

Petron MegaPlaza358 Sen. Gil Puyat Ave.,

Makati City

Circular No. 371

TO: ALL CONCERNED

SUBJECT: REVISED GUIDELINES ON THE Pag-IBIG GROUP HOUSINGLOAN PROGRAM

Pursuant to the approval of Senior Management Committee, the RevisedGuidelines on the Pag-IBIG Group Housing Loan Program are hereby issued:

A. OBJECTIVES

The Pag-IBIG Group Housing Loan Program aims to:

1. Engage the participation and involvement of project proponents in housingprovision, through land development and house construction on land ownedand provided by the project proponent;

2. Encourage project proponents to share in the development of housingpackages by providing subsidy programs and other forms of assistance forthe intended beneficiaries.

3. Promote homeownership among the beneficiaries making it moreaffordable for them.

B. COVERAGE

The Pag-IBIG Group Housing Loan Program shall be open to the followingproject proponents with juridical personality:

1. Local Government Units2. Employers3. Employees' Associations4. Cooperatives

C. FINANCING SCHEME

The project proponent shall be given access to the Pag-IBIG Group HousingLoan for site development and house construction, where the units from theproject to be financed shall be offered for sale to the project beneficiaries.

1. Under the scheme, the project proponent shall provide land to serve asproject site. He may, likewise, provide subsidy to project beneficiaries inthe form of infrastructure support, preparation of plans, titling, extension offacilities and other resource.

1

2. The housing project subject of the loan shall benefit at least thirty (30)potential buyers per phase or building.

D. ELIGIBILITY REQUIREMENTS

1. The proponent must have juridical personality.

2. The proponent owns and provides the land for the housing project.

3. The proponent is Financially capable of fulfilling its commitment to the Fundrelative to the Pag-IBIG Group Housing Program.

4. The proponent have a good credit standing among banks, financialinstitutions and other government housing agencies.

5. The proponent is not engaged in the business of development andconstruction of low-cost and socialized housing.

6. The key officers shall also be subject to credit and background investigation.

7. There must be at least thirty (30) potential buyers who are Pag-IBIGmembers. They must have committed to acquire the property generatedfrom the project and have been pre-qualified by the Fund prior to applicationfor Pag-IBIG Group Housing Loan. The number of potential buyers must be15% more than the number of units.

8. The sales package of the housing units to generated by the projectshould not exceed the maximum loanable amount under the prevailingretail housing programs.

E. TERMS AND CONDITIONS

1. Loan Purpose

The proceeds of the Pag-IBIG Group Housing Loan shall be used for anyof the following purposes:

1.1 Development of residential subdivision, provided that all of the lotsbeing developed will have a housing component;

1.2 Construction of units eligible for mortgage financing under theexisting guidelines of the Pag-IBIG Housing Loan Program.

1.3 Development of Medium-Rise Building in highly urbanized areas.

No part of the loan, however, shall be used to purchase or redeem land.

2. Loan Amount

The amount of loan to be granted shall be based on whichever is lowerof the following:

2.1. Actual project need as supported by cash flow projections; and,

2

2.2. Prudent production cost as defined in the Fund's AppraisalManual.

Provided, the loan amount and any other outstanding wholesale loan,if any, shall not exceed the project proponent's debt capacity andSingle Borrower's Limit.

3. Interest Rate

The loan shall bear interest at the rate based on the prevailing rates ofthe Fund's Full Risk-Based Financing Framework for wholesale loanprograms.

4. Loan Term

The loan shall be repaid based on the project's cash flow projections orthree (3) years, whichever is lower.

5. Criteria for Developmental Financing

5.1 Technical

5.1.1 Site I Location

The site must be approved for development into ahousing project by the appropriate authorities, and shallmeet the following criteria:

a. With legitimate title/s or other instruments provinga secured tenure on the properties subject of theloan, free from liens and encumbrances.

b. Physical suitability and accessibility as defined inthe rules and standards established by theHLURB,

c. Must be within a distance of five (5) kilometerradius from community infrastructures such asschools, commercial centers, churches, etc.

5.1.2 Project Development

a. Project DeSign - The project design, i.e. the typeof land development and the type of housingunits, must conform to HLURB standards andmust address an identified market.

All lots in the project site must have a housingcomponent.

b. Necessary Support Facilities - The project shallinclude provision for necessary support facilitiesin accordance with the standards of HLURB.

c. The proponent shall obtain the services of adeveloper accredited by the Fund in thedevelopment of the housing project.

3

5.2 Market

5.2.1 The prospective member-buyers must be Pag-IBIGmembers and must qualify to avail of a loan under theprevailing Pag-IBIG end-user housing loan guidelines.

5.2.2 All prospective member-buyers must have committed tobuy a property in the housing project. The number ofprospective member-buyers must be 15% more than thenumber of units.

6. Loan Releases

Loan releases to project proponents shall be based on project need andsubmission of the documentary requirements necessary for loan releaseper type of project proponent. The amount to be released shall be subjectfurther to the following conditions:

6.1 Loan shall be released in tranches based on construction schedule.The initial loan release shall be based on the cash flow projectionof the project proponent, not to exceed 50% of the approved loanamount, as provided in Item E Section 2 hereof.

6.2 Succeeding loan releases shall be made only after at least ninetypercent (90%) of the previous release has been infused in thehousing project as assessed in its latest appraisal.

6.3 The outstanding obligation at any given time shall not exceed amaximum of seventy percent (70%) of the collateral value (land andimprovements ).

7. Loan Payment

7.1 Payments shall be applied in accordance with the following order ofpriorities:

a. Penaltyb. Interestc. Principal

7.2 Interest - the first interest payment on the loan shall be due at theend of the 13th month from initial loan release and shall be paidmonthly thereafter.

7.3 Principal - The principal payment on the loan shall be paid not laterthan the end of the 18th month from initial loan release and shall bepaid monthly thereafter.

7.4 If there are sales or Pag-IBIG housing loans generated from theproject at any time after the initial release, part of the takeoutproceeds shall be assigned to the Fund based on the projectproponent's cash flow projection in payment of the loan obligationfor the period. Application of the takeout proceeds to the loanobligation shall be in accordance with the above order of priorities.

4

The assignment of sales proceeds, however, does not relinquishthe project proponent's obligation to collect the proceeds frombuyers and to remit the same to HDMF.

8. Collateral

8.1 The Pag-IBIG Group Housing Loan shall be secured by first realestate mortgage on the real estate property subject of the loan. Itmust be covered by a Transfer Certificate of Title (TCT) issuedby the Register of Deeds, free from all liens and encumbrances;and must be registered in the name of the project proponent.

8.2 Additional Collateral

8.2.1. In case the value of the on-site collateral is insufficient, thePag-IBIG Group Housing Loan may be secured byadditional or substitute collateral acceptable to the Fund,the value of which must be in accordance with the loan-to-collateral ratio provided for in Item E Section 6.3 hereof.This may come in the form of undeveloped, partiallydeveloped or developed residential lands, either adjacentor contiguous to the project site or located in other area.The loan-to-value ratio of the additional collateral shall belimited to 50% of the appraised value.

8.2.2. Assignment of Rental Payments from CommercialConcessions

The LGU shall assign twenty percent (20%) of the rentalpayments from its commercial concessions, such as stallsin the public market and/or passenger terminals.

8.3 HDMF shall allow partial releases of collateral provided that theLoan to Collateral Value on the real estate property after therelease of collateral shall not exceed seventy percent (70%).

9. Warranties

The project proponent shall provide the following warranties:

9.1 Documentation - The project proponent warrants that alldocuments submitted to HDMF relative to the program, are valid,binding and enforceable in all other respects that they purport tobe;

9.2 Title/Ownership of Property - The project proponent warrantsthat he is the lawful owner of the property. Likewise, the projectproponent warrants that the property is free from all liens,encumbrances and adverse claims, that the title/ownershippapers have no vitiating defects, which could have been found ordiscovered with the exercise of proper diligence and technicalskills.

9.3 Project Development - The project proponent warrants that theproject shall be developed and completed in accordance with thedevelopmental plans approved by the government agencies andother regulatory bodies concerned;

5

9.4 House Construction - The project proponent warrants that theresidential units have been constructed in accordance with theplans and specifications approved by the concerned regulatoryagencies, as well as with the local ordinances, and that there areno hidden defects whatsoever in the construction of the saidunits;

9.5 Misrepresentation - The project proponent warrants that any ofits employees or agent allowed to transact or do business in itsbehalf, has not committed any act of misrepresentation;

9.6 Compliance with Laws, Rules and Regulations - The projectproponent warrants that all pertinent laws, rules and regulationshave been complied with.

9.7 Delivery of Accounts and Occupancy of Units - Accountsdelivered by the project proponent to HDMF shall be free fromlien and encumbrances. The project proponent shall turn overthe properties to the beneficiaries upon release of the takeoutproceeds, and the beneficiaries can occupy these propertiesimmediately.

F. OTHER PROVISIONS

1. Project Appraisal

HDMF shall conduct the appraisal on the property subject of landdevelopment and house construction.

2. Project Timetable

The construction of the project must commence within six (6) months fromthe receipt of the Notice of Approval (NOA) and, within a period of twelvemonths from initial loan release, must have units ready for occupancy.Moreover, the project must be fully completed within a maximum period ofthree (3) years.

3. Monitoring

The housing project shall be subject to routine financial and technicalmonitoring throughout the period of the Pag-IBIG Group Housing Loan.

The project proponent may employ a third party project manager as deemednecessary by the Fund.

4. Loan Processing Fees

The project proponent shall be charged with a processing fee of P100 perunit to be generated for the housing project or P10,OOO.OO, whichever ishigher.

6

-----~--

5. Penalties

The project proponent shall be charged with a penalty of 1/20 of 1% of anyunpaid amount for each day of delay for failure to pay loan obligations whendue.

6. Default

The project proponent shall be considered in default under the followingcircumstances:

6.1 Failure to pay three (3) consecutive amortizations and otherobligations on the loan.

6.2 Failure to comply within the specified timeframe for landdevelopment and house construction.

6.3 Failure to comply with any of the terms and conditions of the loan.

7. Effects of default

Upon occurrence of default, such default shall have the following effects,alternate, concurrent and cumulative with each other, which the Fund mayexercise singly or collectively:

7.1 Declare the outstanding obligation, together with accrued interest,penalties, fees and other obligations immediately due anddemandable:

7.1.1 Subject to penalty equivalent to one-twentieth of onepercent (1/20 of 1% ) for every day of delay;

7.1.2 Continue to bear interest at the stipulated rate from thetime the unpaid Notels or other amounts due or otherobligations become due and payable

7.2 Call on the Assignment of Contract Receivables from commercialconcessions

7.3 Foreclose the mortgage securing the loan

7.4 In case the bid price is not sufficient to cover the outstandingobligation, attorney's fee, foreclosure and other expenses, or incase of partial dacion, file an action for deficiency judgment.

7.5 To apply, at its option, at any time, the borrower's monies, which forany reason and under any contract, are presently or hereafter comeinto the possession or control of the Fund in full or partial paymentof the borrower's obligation in the loan agreement and in thepromissory note

7.6 Enforce any and all rights, actions and remedies provided for underthe loan agreement and promissory note evidencing the loan

7

7.7 Avail of any other remedies provided for under existing laws,including but not limited to the filing of an action for sum of moneyor damages against the borrower. As an auxiliary to the civil actionfor sum of money or damages, the Fund may pray for the provisionalremedy of attachment, when the proper statutory grounds forattachment exist.

8. Development Loan for Another Project

The project proponent may apply for additional development loan, providedat least fifty percent (50%) of the previous loan has already been paid, andproject development is completed.

G. APPROVING AUTHORITY

All applications shall be subject to the approval of the appropriate levelof approving/signing authorities.

H. REPEALING CLAUSE

Pag-IBIG Fund Circular Nos. 293 and 354, as well as all memoranda, rules,regulations and other issuances inconsistent herewith are hereby repealed,amended or modified accordingly.

I. EFFECTIVITY

These guidelines take effect after one month from issuance of these guidelines.

~~~ATTY. DARLENE MARIE B. BERBERABE

Chief Executive Officer

Makati City,

December 27, 2016

8

ANNEXA

SPECIFIC POLICIES FOR LOCAL GOVERNMENT UNITS

A. TARGET MARKET

Interested and eligible LGUs may apply for GHLP. However, as a specialfocus, the Fund will be proactive in marketing the GHLP to LGUs to caterto the housing needs of the unserved/underserved Pag-IBIG Fundmembers in their area.

B. INTEREST RATES FOR PROJECT BENEFICIARIES

The interest rate shall be based on the rates under the applicable retailhousing loan programs.

C. PRELIMINARY REQUIREMENTS FOR LOAN APPLICATION

The following documents shall be submitted to the Fund:

1. Letter of Application

2. Resolution of Sanguniang Bayan / Panlungsod / Panlalawigan approving,certifying and ratifying:

a. The project site

b. Authorizing the Local Chief Executive to secure a Pag-IBIG GroupHousing Loan from and enter into a mortgage with HDMF to financethe housing project.

c. Authorizing the Provincial/Municipal/City Treasurer to certify theavailability of funds for the housing project upon receipt of the Noticeof Approval (NOA) from HDMF.

3. Preliminary development plan, specifications, estimates and house plansindicating the selling price of housing units, lot sizes, floor areas andbreakdown of total number of production.

4. Three (3) year audited financial statements certified by the LGUAccountantor by COA

5. Certification on Debt Service Capacity issued by the Bureau of LocalGovernment Finance

6. List of elected officials and key officers, and their resumes

7. List of potential buyers and income profile

9

8. Certified True Copy of TCT (Mother Title) free from liens and encumbrances

D. REQUIREMENTS FOR LOAN RELEASE

The following documents shall be submitted to the Fund prior to loan release:

1. Approved Subdivision Plan, house plans, specifications, estimates, HLURBpermits and LGU Development Permit.

2. Ordinance passed by the Sangguniang Panlalawigan / Panlungsod / Bayanon the following:

a. Inclusion of the housing project in the LGU's approved localdevelopment plan;

b. Annual budget of the LGU, which shall reflect allocation for debtservicing of the Pag-IBIG Group Housing Loan, for the calendar yearfollowing date of initial loan release. This particular ordinance mustbe submitted to the Fund after it has been enacted by the localSanggunian.

3. Resolution/s passed by the Sangguniang Panlalawigan / Panlungsod /8ayan approving, confirming and ratifying the following:

a. All the terms and conditions of the loan

b. The authority for the Local Chief Executive to execute a real estatemortgage and all documents pertaining to the loan.

c. Directive for the LGU's Treasurer and Accountant to enter the loanin the LGU's books

d. The authority for the Provincial/City/Municipal Treasurer to certify theallocation of budget for debt servicing for the Pag-IBIG GroupHousing Loan in the Annual Budget.

e. In case additional or substitute collateral is used to secure the loan,authority for LGU to Mortgage real property other than the onesubject of the loan and for the Local Chief Executive to execute theReal Estate Mortgage in favor of HDMF

4. Execution of Loan and Mortgage Agreement (LMA) between LGU andHDMF and annotation of First Real Estate Mortgage on the title/s of thehousing project subject of the loan.

5. Cash flow projection

6. Authority to Debit from the LGU's regular savings account with its depositorybank to settle any unpaid amount in the event of default.

10

7. If necessary, Deed of Assignment of Rental Payments from CommercialConcessions

E. LOAN RELEASE

The loan proceeds shall be directly released to a special fund, which shouldbe used exclusively for the purpose of the housing project subject of the loan.

F. LOCAL HOUSING BOARD

A Local Housing Board/Office or its equivalent will facilitate the implementationof policies, plans and programs of the LGU for all housing related activities. Itmust be established prior to application for Pag-IBIG Group HousingProgram.

11

ANNEXB

SPECIFIC POLICIES FOR EMPLOYERS, COOPERATIVES,EMPLOYEES' ASSOCIATION AND OTHER GROUPS

A. PRELIMINARY REQUIREMENTS FOR LOAN APPLICATION

The following documents shall be submitted to the Fund:

1. Letter of Application

2. Registration with proper agency that would vest the project proponent withlegal personality (e.g. Securities and Exchange Commission, CooperativeDevelopment Authority, Housing and Land Use Regulatory Board)

3. Articles of Incorporation and By-laws

4. Secretary's Certificate containing the Resolutions passed and approved bythe project proponent's Board of DirectorslTrustees on the following:

a. Grant of authority to the project proponent to avail of a Pag-IBIGGroup Housing Loan from the HDMF and to mortgage the propertysubject of the loan in favor of HDMF

b. Designate the project proponent's representatives who areauthorized to secure a Pag-IBIG Group Housing Loan and to executeand sign loan documents relative thereto

c. Designate the project proponent's representatives who areauthorized to execute a real estate mortgage

5. Preliminary development plan, specifications, estimates and house plansindicating the selling price of housing units, lot sizes, floor areas andbreakdown of total number of production.

6. Three (3) year audited financial statements certified by a Certified PublicAccountant

7. List of key officers, and their resumes

8. List of potential buyers and income profile.

9. Certified True Copy of TCT (Mother Title) free from liens andencumbrances.

B. REQUIREMENTS FOR LOAN RELEASE

The following documents shall be submitted to the Fund prior to loan release:

12

1. Approved Subdivision Plan, house plans, specifications, estimates, HLURBpermits and LGU Development Permit.

2. Execution of Loan and Mortgage Agreement (LMA) between the projectproponent and HDMF and annotation of First Real Estate Mortgage on thetitlets of the housing project subject of the loan.

3. If applicable, presentation of a Joint Venture Agreement I Memorandum ofAgreement with a developer t contractor who will undertake thedevelopment and completion of the project.

4. Cash flow projection

13

ANNEXC

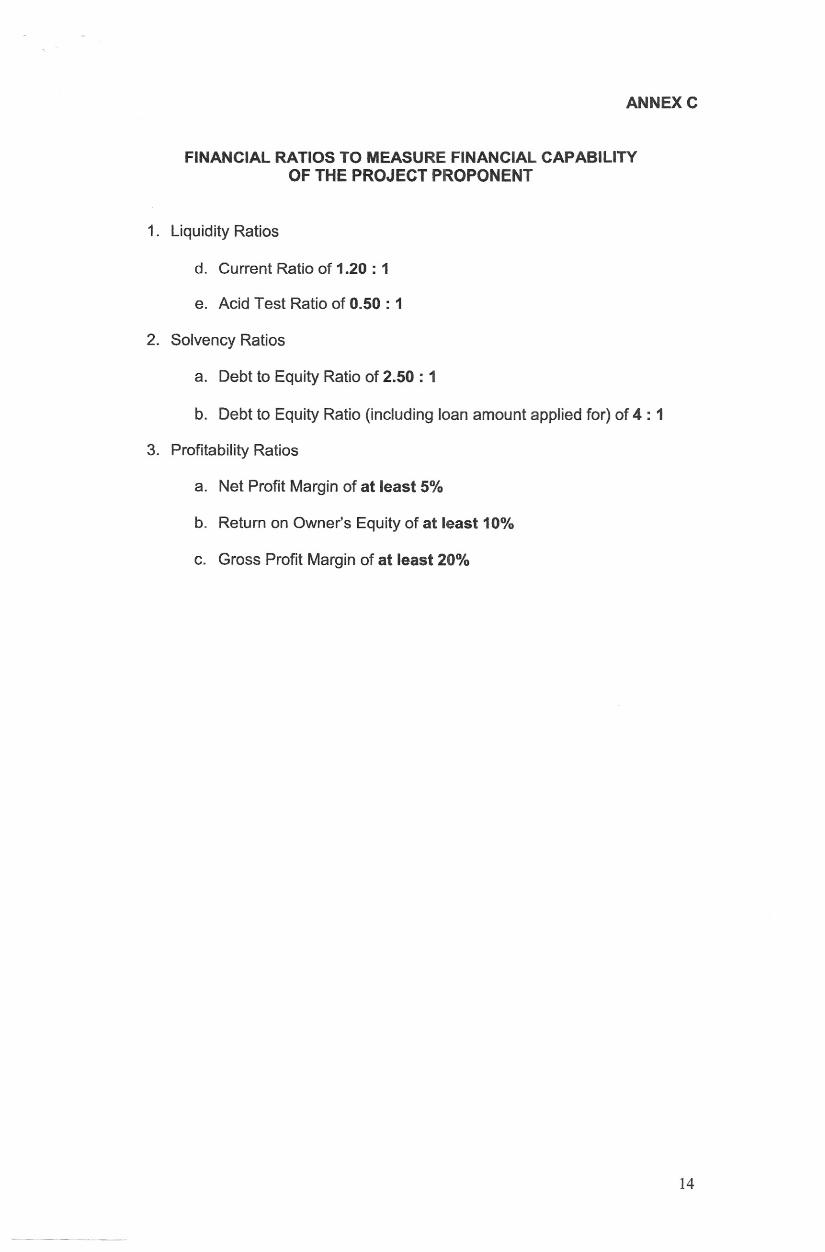

FINANCIAL RATIOS TO MEASURE FINANCIAL CAPABILITYOF THE PROJECT PROPONENT

1. Liquidity Ratios

d. Current Ratio of 1.20 : 1

e. Acid Test Ratio of 0.50 : 1

2. Solvency Ratios

a. Debt to Equity Ratio of 2.50 : 1

b. Debt to Equity Ratio (including loan amount applied for) of 4 : 1

3. Profitability Ratios

a. Net Profit Margin of at least 5%

b. Return on Owner's Equity of at least 10%

c. Gross Profit Margin of at least 20%

14

ANNEXO

ALTERNATIVE APPROACHES AVAILABLE TO LGUs/PROJECTPROPONENTS TO FAST TRACK LOAN TAKEOUTS UNDER THE PROGRAM

The LGUs/Project Proponents may consider the following alternative approachesto enable the target beneficiaries to still avail of Pag-IBIG Housing Loan:

1. It can enter into a joint venture with the landowner and a developer. In thisoption, the land is owned by an individual or company, the developer will be incharge of land development and house construction, and the project proponentwill pre-qualify the beneficiaries who will be availing of Pag-IBIG housing loan.

2. The project proponent can enter into a joint venture with a developer. While theproject proponent provides the land, the developer can provide the cost for landdevelopment and house construction. The Fund can then process the housingloan applications of the eligible beneficiaries of project proponent pre-qualifiedand takeout the approved loans.

3. For the LGU, it can apply for a developmental loan from the Landbank of thePhilippines and have the housing loan applications of the target beneficiariesprocessed and taken out with the Fund.

4. A home-matching program can be established to assist the project proponent'starget beneficiaries. The Fund may recommend accredited developers andhousing projects that will tailor-fit the needs of the beneficiaries based on theirpreferred property location, house models, and price ranges of property. Assoon as the beneficiaries had chosen their dream house/property, the Fundshall process and approve the housing loan applications of qualified borrowers.

15