corporaterestructuring 130301214603-phpapp02

TRANSCRIPT

Corporate Restructuring

Meaning

Corporate restructuring refers to the changes in ownership,

business mix, assets mix and alliances with a view to enhance the

shareholder value.

Hence, corporate restructuring may involve ownership

restructuring, business restructuring and assets restructuring.

Forms of Corporate Restructuring

1) Merger or Amalgamation

Merger or amalgamation may take two forms:

• Absorption

• Consolidation

In merger, there is complete amalgamation of the assets and liabilities as

well as shareholders’ interests and businesses of the merging companies.

There is yet another mode of merger. Here one company may purchase

another company without giving proportionate ownership to the

shareholders’ of the acquired company or without continuing the business

of the acquired company.

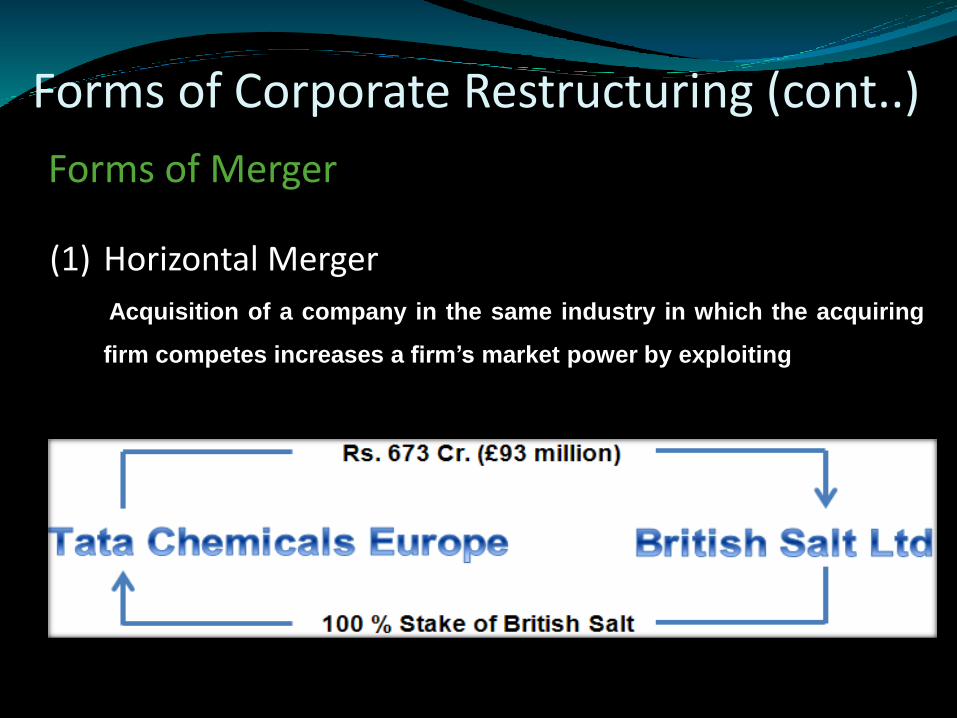

Forms of Merger

Forms of Corporate Restructuring (cont..)

(1) Horizontal Merger

Acquisition of a company in the same industry in which the acquiring

firm competes increases a firm’s market power by exploiting

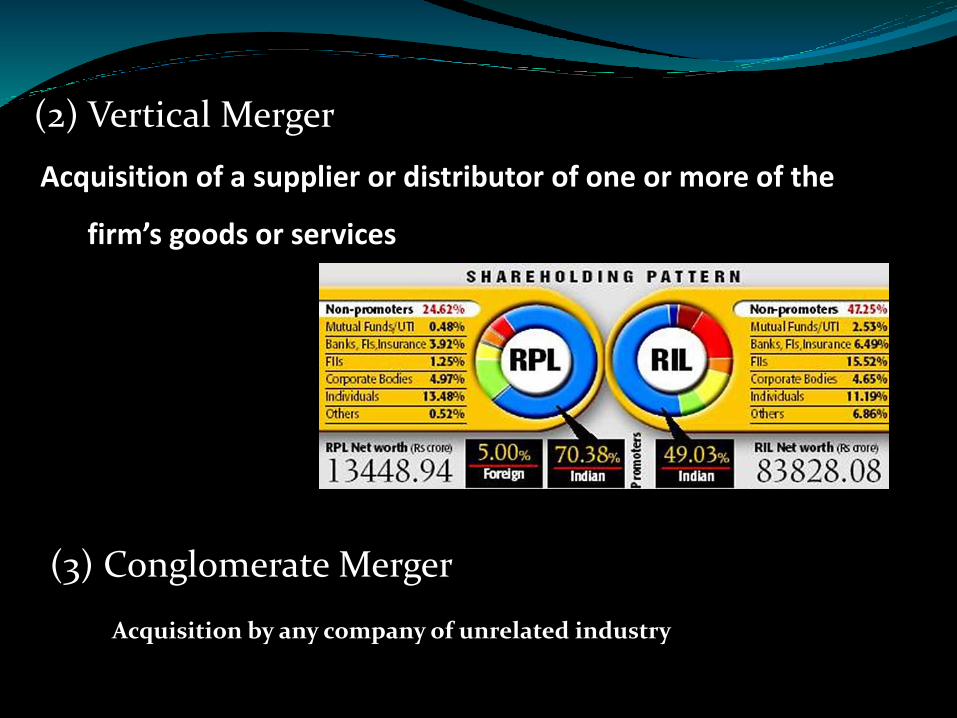

(2) Vertical Merger

Acquisition of a supplier or distributor of one or more of the

firm’s goods or services

(3) Conglomerate Merger

Acquisition by any company of unrelated industry

Forms of Corporate Restructuring (cont..)

Acquisition may be defined as an act of acquiring effective

control over assets or management of a company by another

company without any combination of businesses or

companies.

A substantial acquisition occurs when an acquiring firm

acquires substantial quantity of shares or voting rights of the

target company.

Takeover – The term takeover is understood to connote hostility. When

an acquisition is a ‘forced’ or ‘unwilling’ acquisition, it is called a

takeover.

A holding company is a company that holds more than half of the

nominal value of the equity capital of another company, called a

subsidiary company, or controls the composition of its Board of

Directors. Both holding and subsidiary companies retain their separate

legal entities and maintain their separate books of accounts.

Forms of Corporate Restructuring (cont..)

Limit competition.

Utilise under-utilised market power.

Overcome the problem of slow growth and profitability

in one’s own industry.

Achieve diversification.

Gain economies of scale and increase income with

proportionately less investment.

Establish a transnational bridgehead without excessive

start-up costs to gain access to a foreign market

Motives of Corporate Restructuring

Utilise under-utilised resources–human and physical

and managerial skills.

Displace existing management.

Circumvent government regulations.

Reap speculative gains attendant upon new security

issue or change in P/E ratio.

Create an image of aggressiveness and strategic

opportunism, empire building and to amass vast economic

powers of the company.

Motives of Corporate Restructuring (Cont..)

Legal Procedures for merger and acquisition

Payment by cash or securities

Transfer of assets and liabilities

Filing of the Court order

Sanction by the High Court

Shareholders’ and creditors’ meetings

Application in the High Court

Approval of board of directors

Information to the stock exchange

Permission for merger

10

Legal Process of Merger & Acquisition

Process (Cont…)

Approval of Merger Information to stock Exchange

Approval of Board of Directors

Application in High Court Shareholders & Creditors meeting

Sanction by High Court

Process (Cont…)Filing of Court Order Transfer of Assets &

LiabilitiesPayment By cash or

Securities

Methods of Valuation

In order to apply DCF technique, the followinginformation is required:

• Estimating Free Cash Flows

Revenues and expenses

Cor.tax and depreciation:

Working capital changes

• Estimating the Cost of Capital

• Terminal Value

Discounted Cash flow Method

Calculation of financial synergy(1) Pooling of Interests Method:

In the pooling of interests method of accounting,

the balance sheet items and the profit and loss items

of the merged firms are combined without

recording the effects of merger. This implies that

asset, liabilities and other items of the acquiring and

the acquired firms are simply added at the book

values without making any adjustments.

Calculation of financial synergy (cont..)

Particulars

Share Capital

Fixed Assets

Liabilities

Current Assets

Company X

200

150

250

250

Company y

240

170

200

120

After Merger

= 440

= 320

= 450

= 370

After merger both balance sheet will be combined is called

pooling of interest method

(2) Purchase Method

Under the purchase method, the assets and

liabilities of the acquiring firm after the

acquisition of the target firm may be stated at their

exiting carrying amounts or at the amounts

adjusted for the purchase price paid to the target

company.

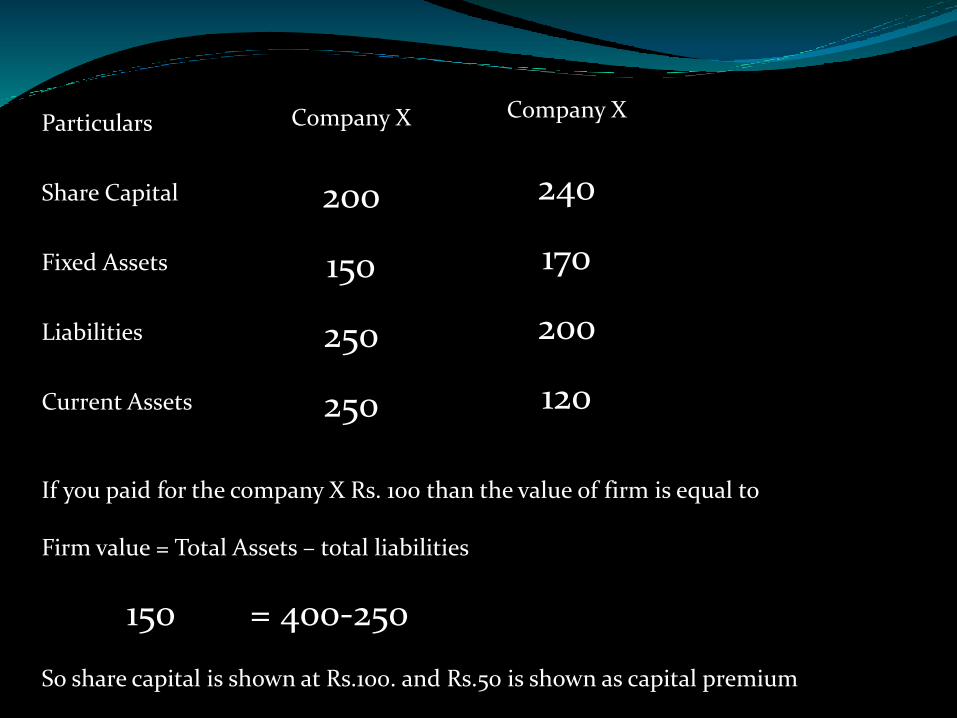

Calculation of financial synergy (cont..)

Particulars

Share Capital

Fixed Assets

Liabilities

Current Assets

Company X

200

150

250

250

Company X

240

170

200

120

If you paid for the company X Rs. 100 than the value of firm is equal to

Firm value = Total Assets – total liabilities

150 = 400-250

So share capital is shown at Rs.100. and Rs.50 is shown as capital premium

A divestment involves the sale of a company’s assets, orproduct lines, or divisions or brand to the outsiders.

It is reverse of acquisition.

Motives:

Strategic change

Selling cash cows

Disposal of unprofitable businesses

Consolidation

Unlocking value

Divestiture

Strategic Alliance“A strategic alliance is a voluntary, formal arrangement

between two or more parties to pool resources to achieve a

common set of objectives that meet critical needs while

remaining independent entities.”

Example -

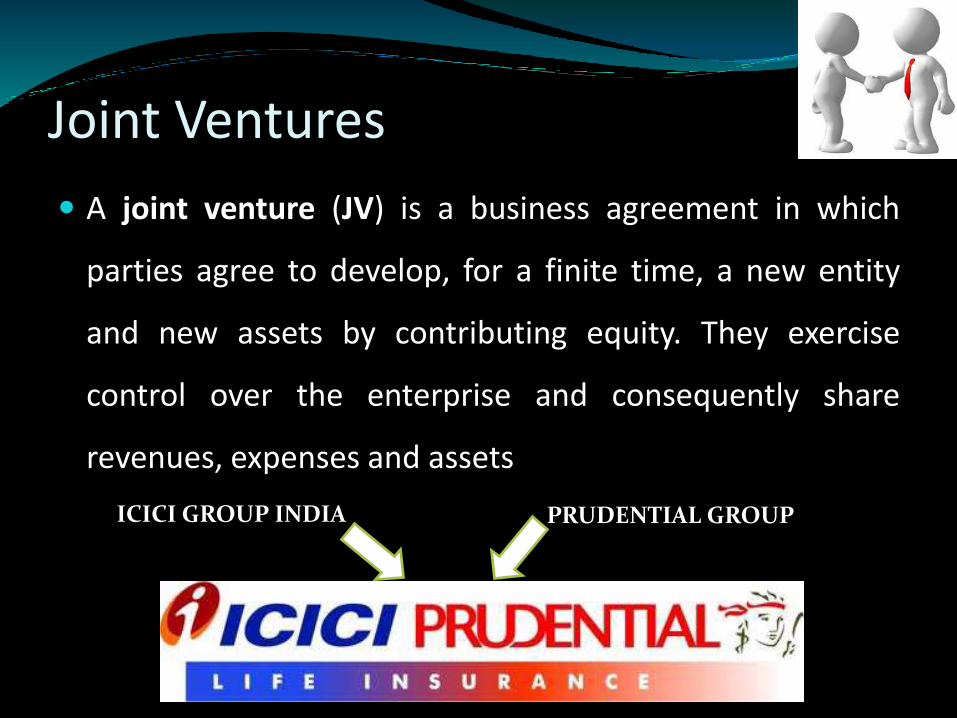

Joint Ventures

A joint venture (JV) is a business agreement in which

parties agree to develop, for a finite time, a new entity

and new assets by contributing equity. They exercise

control over the enterprise and consequently share

revenues, expenses and assets

ICICI GROUP INDIA PRUDENTIAL GROUP

Sell-off When a company sells a part of its business to a third party, it is

called sell-off.

It is a usual practice of a large number of companies to sell-off

to divest unprofitable or less profitable businesses to avoid

further drain on its resources.

Sometimes the company might sell its profitable but non-core

businesses to ease its liquidity problems.

Spin-off When a company creates a new company from the

existing single entity, it is called a spin-off.

The spin-off company would usually be created as asubsidiary.

Hence, there is no change in ownership.

After the spin-off, shareholders hold shares in twodifferent companies.

An employee stock ownership plan (ESOP) is an employee-

owner scheme that provides a company's workforce with an

ownership interest in the company. In an ESOP, companies

provide their employees with stock ownership, often at no cost

to the employees. Shares are given to employees and may be

held in an ESOP trust until the employee retires or leaves the

company. The shares are then sold.

E.g. First company introduce ESOP is Inforsys.

Employee Stock Ownership

Leverage Buy-out (LBO) A leveraged buy-out (LBO) is an acquisition of a company in which

the acquisition is substantially financed through debt. When the

managers buy their company from its owners employing debt, the

leveraged buy-out is called management buy-out (MBO).

The following firms are generally the targets for LBOs:

High growth, high market share firms

High profit potential firms

High liquidity and high debt capacity firms

Low operating risk firms

The evaluation of LBO transactions involves the same analysis as for

mergers and acquisitions. The DCF approach is used to value an LBO.