correction

DESCRIPTION

correctionTRANSCRIPT

Unit 8Unit 8

CONTROL ACCOUNTS AND ERROR

CORRECTION

1

Correction of errorsCorrection of errors

Learning objectives

◦ Introduction to the journal

◦ Types of errors

◦ Suspense account

◦ Corrected Income statement

◦ Corrected Statement of financial position

2

Books of prime entryBooks of prime entry

Recap

◦ Sales day book

◦ Purchases day book

◦ Return inwards day book

◦ Return outwards day book

◦ Cash Book/ Petty cash Book

◦ The journal

3

The journalThe journal

A book of prime entry which records

transactions which are not routine and

not recorded in any other books of prime

entry

4

Typical uses of the journalTypical uses of the journal

Year end adjustments

Acquisitions and disposal of non-current

assets

Opening entries-Entries to open a new

set of books

Correction of errors

5

Presentation of the journalPresentation of the journal

The journal shows:

◦ The date

◦ The name of the account(s) to be debited

◦ The name of the account(s) to be credited

◦ A description of the transaction – the

narrative

6

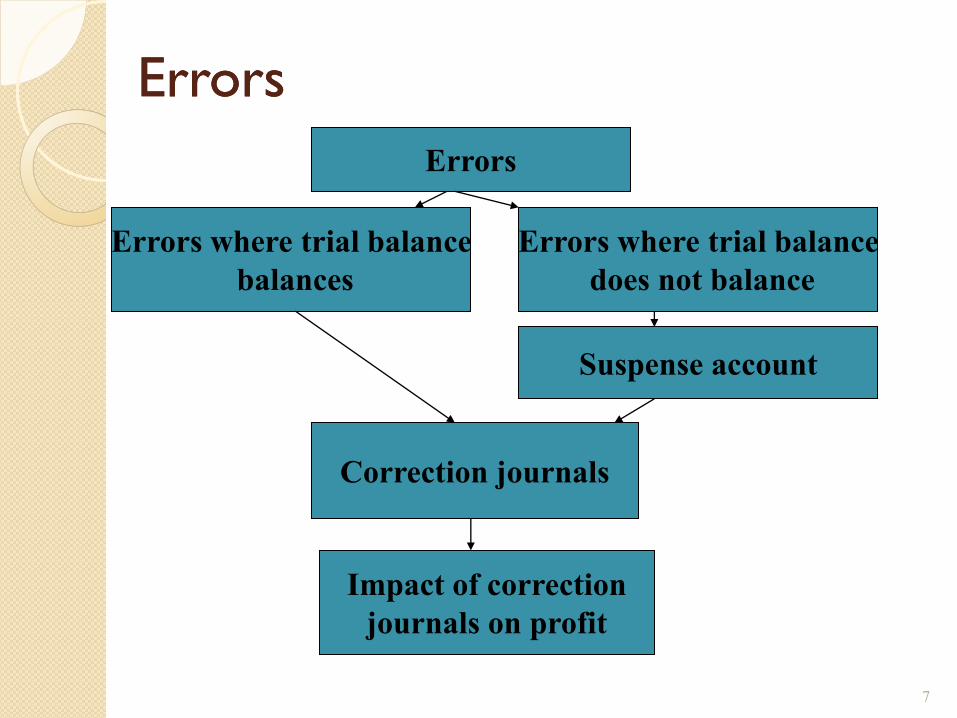

ErrorsErrors

7

Errors

Errors where trial balance

balances

Errors where trial balance

does not balance

Suspense account

Correction journals

Impact of correction

journals on profit

Errors where the trial balance still Errors where the trial balance still

balancesbalances Error of omission

Error pf commission

Error of principle

Compensating error*

Error of original entry

Reversal of entries

8

Errors where the trial balance does Errors where the trial balance does

not balancenot balance Addition errors – figures are incorrectly

added in a ledger account

Posting error –

a an entry made in one record is not posted at

all

b an entry in one record is incorrectly posted

to another

Trial balance errors – a balance is omitted,

or incorrectly extracted, in preparing the trial

balance

9

Suspense accountSuspense account

A suspense account is an account in

which the debits and credits are held

temporarily until sufficient information is

available for them to be posted to the

correct accounts

Dealt with the normal rules of double-

entry bookkeeping

10

Suspense account (Cont…)Suspense account (Cont…)

There are two main reasons why suspense accounts may be created:-

◦ On the extraction of a trial balance the debits are not equal to the credits and the difference is put to a suspense account.

◦ When a bookkeeper performing double entry is not sure where to post one side of an entry he may debit or credit a suspense account and leave the entry there until its ultimate destination is clarified.

11

Control accounts

12

CONTROL ACCOUNTS

13

What is a control account (Total What is a control account (Total

accounts)accounts)

Is an account in the nominal ledger which

summarizes the transactions in a number of other

accounts

Examples of control accounts could include:-

◦ The sales ledger control account, which

summarizes the individual customer accounts

◦ The purchases ledger control account, which

summarizes the individual supplier accounts

14

Reasons/Advantages Of Having Total Reasons/Advantages Of Having Total

/Control Accounts:/Control Accounts:

The Control accounts serve as an independent check/internal check on the accuracy of the Ledgers.

Control Accounts can assist Management to safeguard against fraudulent entries if there is a proper segregation of duties by making sure the person taking charge of the Ledgers do not prepare the Control Accounts.

To prepare the Trial Balance, it is quicker to extract the total/control accounts of the trade debtors and trade creditors account instead of extracting the details of the individual balances of the individual trade debtors and trade creditors accounts.

15

Reasons/Advantages Of Having Total Reasons/Advantages Of Having Total

/Control Accounts:/Control Accounts:

Control Accounts facilitate the location of

errors. For example, at any time the closing

balance of the Trade Debtors Control Account

must equal to the sum of the individual trade

debtors accounts balances. Hence, if the two

totals do not agree, we can quickly know that

there must errors in either the Sales Ledger or

the Control Account.

16

Control accounts are part of the double Control accounts are part of the double

entry systementry system

Usually, control accounts i.e. the debtors total

account and the creditors total account are an

integral part of the double entry system.

If this is so, then the sales ledger and the

purchases ledger will only be memorandum

accounts i.e. accounts which are not part of the

double entry system and which are kept only for

reference and control purposes.

17

Control accounts are NOT part of the Control accounts are NOT part of the

double entry systemdouble entry system

In the rare cases where control accounts are

memorandum only, the sales ledger and the

purchases ledger would then be part of the

double entry system.

The debtors total account and the purchases

total accounts would be kept for

memorandum purposes only

18

Sales ledger control account Sales ledger control account

(Debtors control account)(Debtors control account)

Is used to control the ledger

The entries in the sales ledger control account comes from the books of prime entry, not from the individual accounts in the sales ledger

This provides a checking facility because, if information in the books of prime entry is posted directly to the individual accounts and also in the control account, a cross check can be made

The balance on the control account should be the same as the total balances on the individual sales account.

If they are not, then an error has occurred

19

Sales ledger control accountSales ledger control accountBalance b/d(should tally with

sum of sales ledger debit balances

at end of previous period

X Balance B/f (total of sales

ledger credit balances b/f

from previous period)

X

Credit sales (total in sales day

book) X Return inwards (total of

Return inwards book) X

Dishonored cheques (Bank

statement and cash book) X Bad debts (journal) X

Cash received from debtors

(Cash column on received

side)

X

Cash discounts allowed

(total of discount column of

cash book)

X

Balance c/d (should tally

with sum of debit balance on

the individual debtor

accounts in the sales ledger)

X

20

Example 1Example 1--Sales ledger control accountSales ledger control account1 Sept Money owed by customers Rs 5,700

1 Sept Money owed to customers Rs 350

30 Sept Sales Rs

35,680

30 Sept Return inwards Rs 1,350

30 Sept Cheque payment by credit

customers

Rs

32,360

30 Sept Cash payments by credit

customers

Rs 4,300

30 Sept Money owed by customers Rs 3,190

30 Sept Money owed to customers Rs 170

21

Credit balances on the sales Credit balances on the sales

ledger control accountledger control account

Such balances arise when

◦ The customer has overpaid

◦ Credit notes have been issued for fully

paid for goods

◦ Payment is received in advance of

raising invoices

The Purchases ledger control account

may show a debit balance for similar

reasons

22

Purchase ledger control account Purchase ledger control account

or creditors total accountor creditors total account Sometimes known as creditors control

account

Is used to control the purchases ledger

which contains the accounts of

individual suppliers who supply goods

on credit

Information needed to prepare the

purchases ledger control account

comes from books of prime entry

23

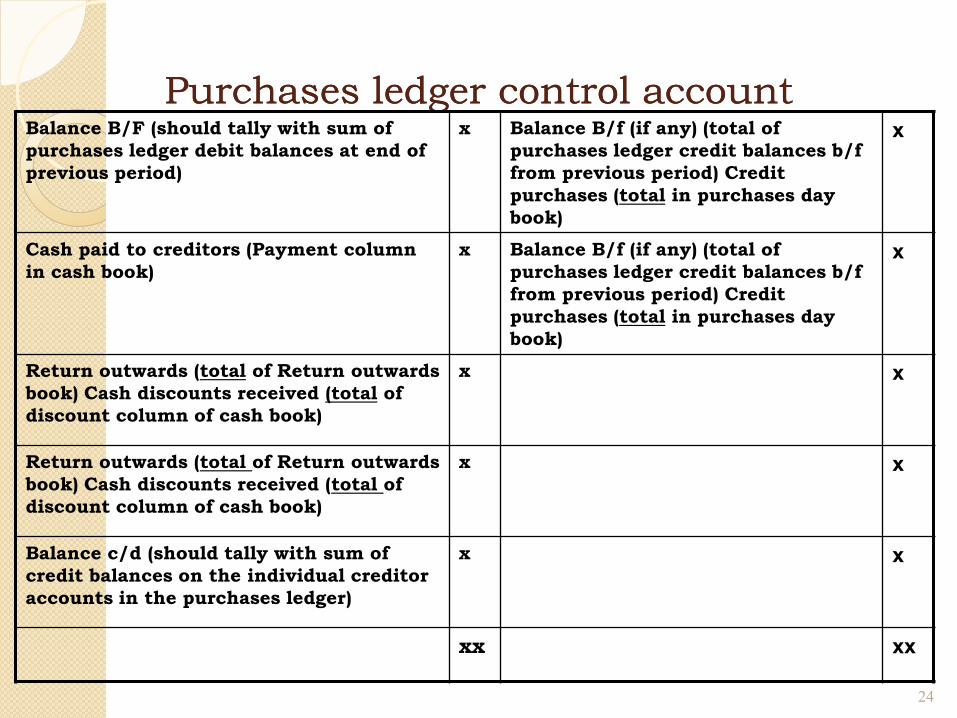

Purchases ledger control accountPurchases ledger control accountBalance B/F (should tally with sum of

purchases ledger debit balances at end of

previous period)

x Balance B/f (if any) (total of

purchases ledger credit balances b/f

from previous period) Credit

purchases (total in purchases day

book)

x

Cash paid to creditors (Payment column

in cash book)

x Balance B/f (if any) (total of

purchases ledger credit balances b/f

from previous period) Credit

purchases (total in purchases day

book)

x

Return outwards (total of Return outwards

book) Cash discounts received (total of

discount column of cash book)

x x

Return outwards (total of Return outwards

book) Cash discounts received (total of

discount column of cash book)

x x

Balance c/d (should tally with sum of

credit balances on the individual creditor

accounts in the purchases ledger)

x x

xx xx

24

Example 2Example 2-- Purchases ledger Purchases ledger

control accountcontrol account

1 July Money owed to suppliers Rs 37,450

31 July Credit purchases Rs 231,600

31 July Return outwards Rs 12,900

31 July Total payments Rs 222,000

31 July Discount received Rs 6,770

31 July Money owed by suppliers Rs 560

31 July Money owed to suppliers Rs 27,940

25

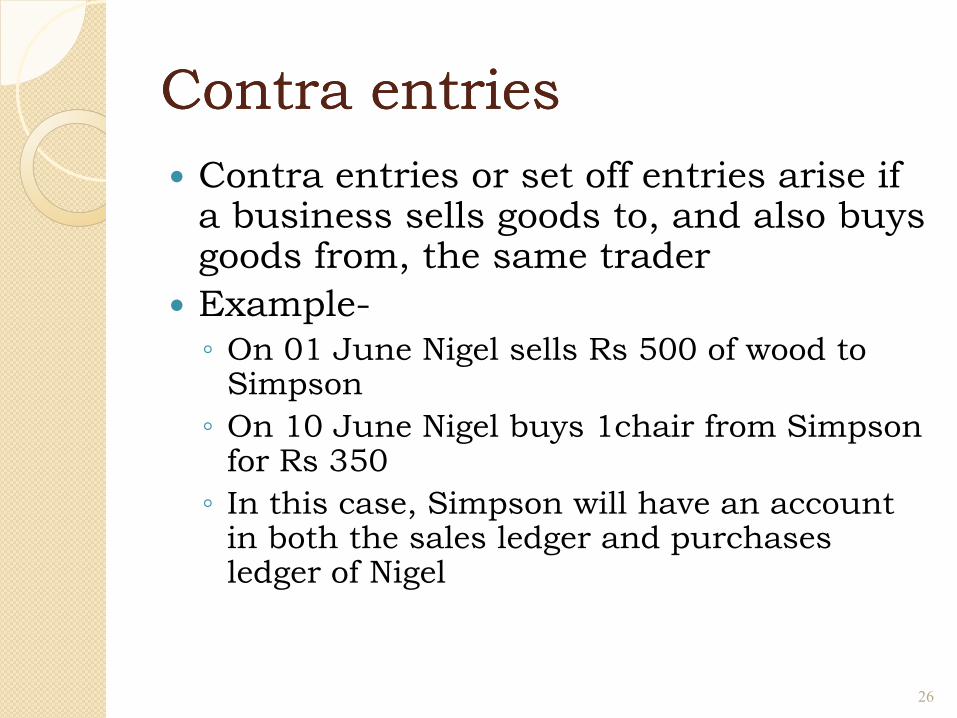

Contra entriesContra entries

Contra entries or set off entries arise if a business sells goods to, and also buys goods from, the same trader

Example-

◦ On 01 June Nigel sells Rs 500 of wood to Simpson

◦ On 10 June Nigel buys 1chair from Simpson for Rs 350

◦ In this case, Simpson will have an account in both the sales ledger and purchases ledger of Nigel

26

Accounts of SimpsonAccounts of Simpson

01/06 Credit sales Rs 500

10/06 Credit purchases Rs350

27

Purchases ledger

Simpson

Sales ledger

Simpson

Treatment of a contra entryTreatment of a contra entry

01/06 Credit sales Rs 500 30/06 Contra Purchases Ledger Rs 350

30/06 Bank Rs 150

30/06 Contra Sales ledgerRs

350

10/06 Credit purchases Rs 350

28

Purchases ledger

Simpson

Sales ledger

Simpson

Activity 1Activity 1

Sales ledger control account and

purchases ledger control account

29