creating a leading african copper & cobalt...

TRANSCRIPT

Annual Report 2007

Creating a Leading African Copper & Cobalt Company

Company Overview

Katanga Mining Limited is creating an industry leader in copper and cobalt. Its joint venture operations in the Democratic Republic of Congo are in production, and the company has the potential to become Africa’s largest copper producer and the world’s largest cobalt producer by 2011.

In January 2008, Katanga merged with Nikanor PLC, which has an adjacent copper-cobalt complex, to create a company with a US$3.8 billion market capitalization. A four-year phased ramp-up will see the company targeting production of over 300,000 tonnes of refined copper and over 30,000 tonnes of refined cobalt a year by 2011 from a major single-site operation.

01 Company Overview01 2007 Highlights02 President’s Letter06 Board of Directors

08 Progress Review08 Project Review12 Operations Review16 Social Responsibility Review19 Financial Review

21 MD&A21 Management’s Discussion and Analysis

34 Financial Statements34 Management’s Responsibility for

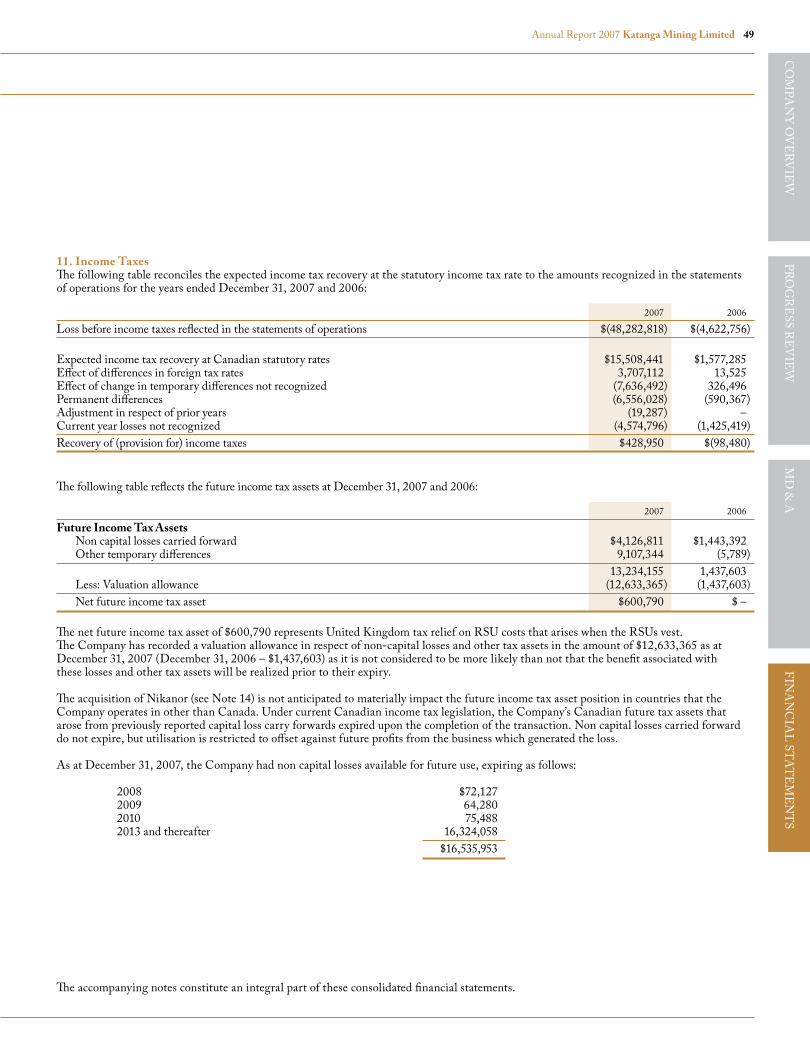

Financial Reporting35 Auditors’ Report36 Consolidated Financial Statements39 Notes to Consolidated Financial Statements

57 Shareholder Information

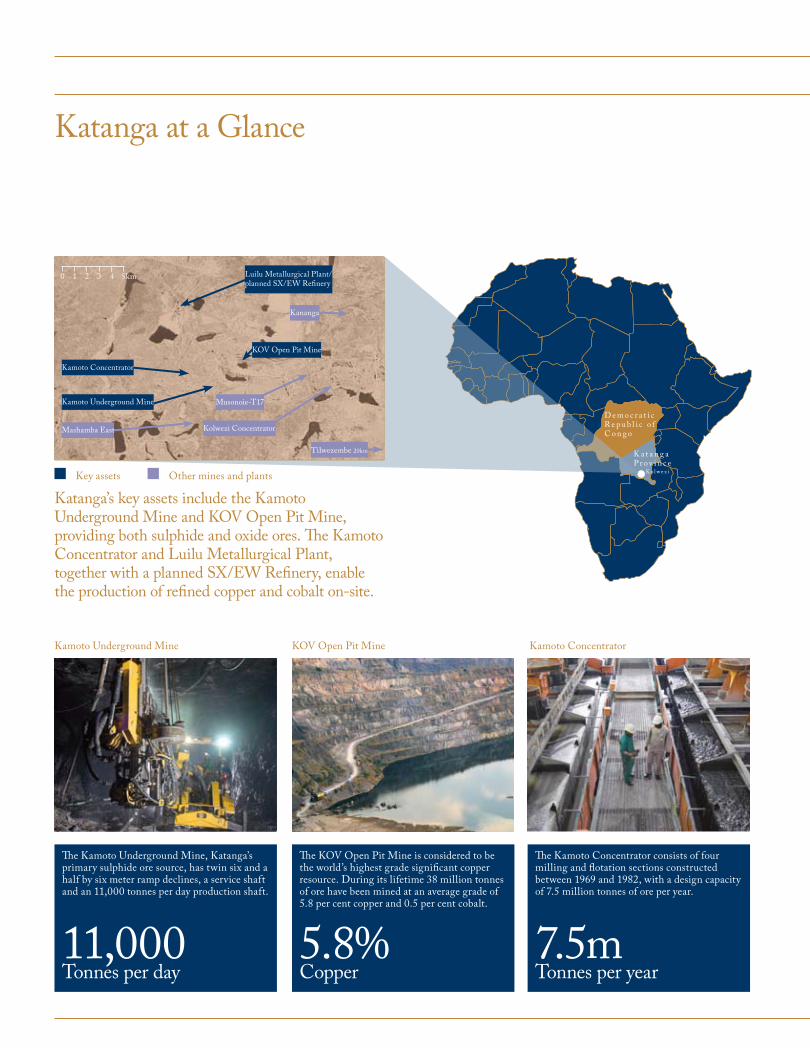

Katanga at a Glance

Luilu Metallurgical Plant/planned SX/EW Refinery

Musonoie-T17

Kolwezi Concentrator

KOV Open Pit Mine

Mashamba East

D e m o c r a t i cR e p u b l i c o f C o n g o

K a t a n g aP r o v i n c e

K o l w e z i

Katanga’s key assets include the Kamoto Underground Mine and KOV Open Pit Mine, providing both sulphide and oxide ores. The Kamoto Concentrator and Luilu Metallurgical Plant, together with a planned SX/EW Refinery, enable the production of refined copper and cobalt on-site.

Kamoto Underground Mine KOV Open Pit Mine Kamoto Concentrator

The Kamoto Underground Mine, Katanga’s primary sulphide ore source, has twin six and a half by six meter ramp declines, a service shaft and an 11,000 tonnes per day production shaft.

The KOV Open Pit Mine is considered to be the world’s highest grade significant copper resource. During its lifetime 38 million tonnes of ore have been mined at an average grade of 5.8 per cent copper and 0.5 per cent cobalt.

The Kamoto Concentrator consists of four milling and flotation sections constructed between 1969 and 1982, with a design capacity of 7.5 million tonnes of ore per year.

11,000Tonnes per day

5.8%Copper

7.5mTonnes per year

0 1 3 4 5km2

Key assets Other mines and plants

Tilwezembe 20km

Kamoto Underground Mine

Kamoto Concentrator

Kananga

Large-scale, low-cost and long-life producerKatanga’s mine complex is currently in production, with a phased ramp-up targeting over 300,000 tonnes of refined copper and over 30,000 tonnes of refined cobalt a year by 2011, giving the company the potential to be Africa’s largest copper producer and the world’s largest cobalt producer. Substantial high-grade resources indicate a potential mine life of 40+ years, with one of the world’s lowest production costs.

Proven management team and track recordKatanga’s Board and management team are comprised of industry veterans with a track record of successful project execution, proven local operating expertise and a history of running large-scale operations. The team brought the Kamoto site into production at the end of 2007 on schedule and on budget, and is continuing its phased approach for the development of the enlarged mine complex.

Globally significant integrated single-site operationKatanga’s integrated mine complex is considered to be the largest single-site project in the world producing both copper and cobalt. It contains both underground and open pit mines, providing both sulphide and oxide ores. A concentrator and metallurgical plant enable the production of refined copper and cobalt metal on-site. The complex is a mix of existing assets being progressively refurbished and a new state-of-the-art refinery which is under construction.

Genuine commitment to sustainable developmentA company of Katanga’s scale has the opportunity to make a significant impact in the Democratic Republic of Congo. Along with financial benefits in the form of royalties and taxes, a coordinated community investment program will produce positive change for communities surrounding the operations. Katanga’s aim is to help ensure that the social and economic benefits stemming from its project will last well beyond the life of the mine.

Luilu Metallurgical Plant Planned SX/EW Refinery Other mines and plants

The Luilu Metallurgical Plant has roasters, leaching circuits and electro-winning cells for copper and cobalt production. It has a potential capacity of 175,000 tonnes of copper and 8,000 tonnes of cobalt a year.

The planned greenfield SX/EW Refinery more than doubles Katanga’s capacity, with increased recoveries and higher grade metal production. Its design has two modules, each producing 80,000 tpy copper and 10,000 tpy cobalt.

In addition to its key assets, Katanga also has the Kolwezi Concentrator, the previously-mined Mashamba East open pit, and the cobalt-rich Musonoie-T17, Kananga and Tilwezembe deposits, with grades up to 0.87 per cent cobalt.

175,000Tonnes per year

80,000Tonnes per year

0.87%Cobalt

Our Strengths

-50

0

50

100

150

200

250

300

Katanga Relative TSX Diversified Metals & Mining Index Relative

Jan

07

Feb

07

Mar

07

Ap

r 07

May

07

Jun

e 07

July

07

Aug

07

Sep

07

Oct

07

Nov

07

Dec

07

%

01Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

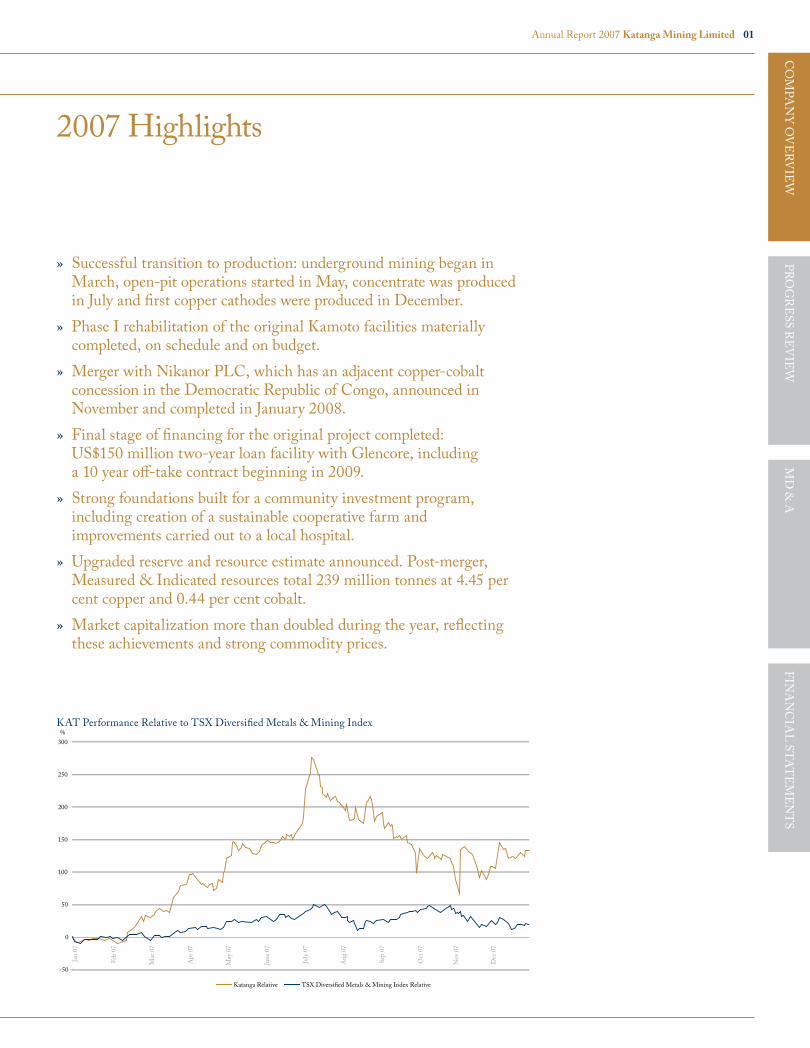

2007 Highlights

Successful transition to production: underground mining began in March, open-pit operations started in May, concentrate was produced in July and first copper cathodes were produced in December.

Phase I rehabilitation of the original Kamoto facilities materially completed, on schedule and on budget.

Merger with Nikanor PLC, which has an adjacent copper-cobalt concession in the Democratic Republic of Congo, announced in November and completed in January 2008.

Final stage of financing for the original project completed: US$150 million two-year loan facility with Glencore, including a 10 year off-take contract beginning in 2009.

Strong foundations built for a community investment program, including creation of a sustainable cooperative farm and improvements carried out to a local hospital.

Upgraded reserve and resource estimate announced. Post-merger, Measured & Indicated resources total 239 million tonnes at 4.45 per cent copper and 0.44 per cent cobalt.

Market capitalization more than doubled during the year, reflecting these achievements and strong commodity prices.

»

»

»

»

»

»

»

KAT Performance Relative to TSX Diversified Metals & Mining Index

02 Katanga Mining Limited Annual Report 2007

President’s Letter

Copper production from our joint venture’s Luilu refinery began in December after 18 months of challenging work. This accomplishment met our primary goal for 2007. Furthermore, it was achieved within our US$175 million budget, another key objective.

Katanga’s market capitalization more than doubled during 2007, reflecting onsite accomplishments and strong commodity prices. The transition from developer to producer during the year encompassed several milestones. Production began at the Kamoto Underground Mine in March. Open-pit operations started in May, although production was limited until September when the heavy equipment required could be transported across the Lualaba River. In July, concentrate production from the Kamoto Concentrator began, while cold commissioning of the Luilu Metallurgical Plant started in November, and first copper cathode was produced mid-December.

Achieving production as scheduled within the Phase I budget of US$175 million was an important team accomplishment considering the condition of the site when the joint venture started managing it on July 3, 2006. The stage is now set for Phase II, which began in early 2008 as planned.

Merger with NikanorOn November 6, 2007, we announced an offer to acquire Nikanor PLC. The transaction, which closed January 11, consolidates mining operations in the Kolwezi district and will yield important synergies. These include reduced capital and operating costs as we remove duplication and collectively enhance metallurgical recoveries. The greater scale of our operations will also improve our capability to address external matters such as government relations and infrastructure.

Financing completedSecuring the third and final stage of financing for the Kamoto project was a key objective in 2007, but uncertainty created by a government-mandated review of joint ventures with State companies, as well as a hostile takeover attempt, meant we were unable to close a syndicated credit facility. However, by year-end we successfully secured a US$150 million convertible loan from Glencore. The facility includes copper and cobalt off-take rights beginning in 2009 that will provide superior marketing strength for our business.

“Katanga’s market capitalization more than doubled during 2007, reflecting onsite accomplishments and strong commodity prices.”

03Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

Healthy resourcesAn upgraded reserve and resource estimate was announced early in the year. Proven and probable ore grades for both the Kamoto Underground Mine and the Musonoie-T17 open-pit mine increased materially as a result of additional information and refined plans. The merger brings an additional 126 million tonnes of high grade resources in the KOV deposit that will drive expansion over the next three years.

After year-end, we announced a transaction transferring the Mashamba West and Dikuluwe deposits to our joint venture partner Gécamines in return for either replacing the resource or paying US$825 million from its share of joint venture production. These two deposits were scheduled to be mined starting in 2023 and 2020 respectively, and more value may be created in the joint venture by replacing these resources with ores that can be mined earlier. Post-transaction, the joint ventures have a nominal 239 million tonnes of reserves and resources at average grades of 4.45 per cent copper and 0.44 per cent cobalt.

Operational progressBy year-end, refurbished facilities were operating satisfactorily, although below capacity as mining rates increase. Open pit and underground operations, while improving, are lagging behind the plan. The principal limitation is workforce productivity, and we see the development of employee skills and capabilities as a long-term challenge. However, ongoing initiatives to improve performance helped mining rates in the T17 open pit to exceed plan by year-end, and the required quantities of oxide ores are available. Costs in 2007 were capitalized, as mine and plant operations during the year were in their start-up phase.

Ongoing transformation of the DRCTransformation of the DRC into a country with representative government continued in 2007. Services are still minimal, and power and transportation infrastructure must improve dramatically to meet the needs of a large-scale mining project. Working closely with government agencies, we are steadily improving outcomes to meet our

needs; for example, we received authorization to clear customs and immigration in Kolwezi, thereby avoiding border crossing congestion at Kasumbalesa.

Having travelled to Lubumbashi and Kolwezi for 10 years, I see a clear difference today. Katanga now employs more than 4,000 Congolese nationals with a local payroll exceeding US$2.8 million per month. Resurgence of the mining industry has revived the regional economy, and more goods and services are available, including better air services and the opening of hotels and restaurants. Above all, I see growing confidence and more self-initiative among the Congolese people.

Community projects begunWe started several initiatives during 2007 to help improve services in Kolwezi. Working with community groups and non-governmental organizations, we delivered a number of projects for the benefit of our employees and the wider community in areas such as agriculture, sanitation and medical services. These included establishing a self-sustaining farm cooperative, clearing

Employees by a cascade mill in the Kamoto Concentrator

Lifting starter sheets in the Luilu Metallurgical Plant

Underground operations

04 Katanga Mining Limited Annual Report 2007

thousands of meters of local drains and ditches, and making infrastructure improvements at the Mwangeji Hospital, all highlighted later in this report.

In 2008 we expect to accelerate progress in this area. The priorities are to restart the Mutoshi Institute, a training school for mineworkers, in conjunction with other mining companies and Gécamines; rehabilitate roads in Kolwezi; and continue to upgrade the Mwangeji Hospital.

President’s Letter continued

Progress against 2007’s goalsIn reviewing the goals set in last year’s Annual Report, I see achievement in most respects. Phase I of our capital program was materially completed on budget. We raised $150 million for project needs, though it took a different form than originally intended. About 700 people were added to the site organization during the year, and operational performance is improving.

A further goal was to improve the quality of life for our employees and the community. As you will read in this report, progress was made and we have plans for 2008 that should enhance conditions. The final goal I set was to increase Katanga’s market value. The market capitalization of the company at the end of December 2007 was 132 per cent greater than at the end of December 2006; an indication, I believe, of progress made onsite and the market’s appetite for natural resource companies.

In-d

epth About the DRC

At 2.34 million square kilometers, the Democratic Republic of Congo (DRC) is the third largest country in Africa. It has a population of 65.7 million people.

The DRC’s vast mineral wealth includes copper, cobalt, diamonds, gold, coltan and zinc. The country is estimated to contain 10 per cent of the world’s copper resources and 50 per cent of its cobalt resources, centered on the Katanga Province in the south east of the country.

Since independence from Belgium in 1960, the DRC has had a turbulent history. Following a five-year civil war, a transitional government was formed in July 2003 and elections in 2006 confirmed Joseph Kabila as President. The world’s largest UN peacekeeping force is in the country overseeing the shift to democracy.

Confidence in the DRC is growing among Western companies. The introduction of a new mining code in 2002 was an important element in attracting private sector investment, with over US$2.1 billion in capital raised for DRC mining projects in 2006/07. The country’s economy saw growth of 6.1 per cent in 2007.

“Our new enlarged Board will continue to serve all Katanga shareholders, guiding the company as we embark on the exciting road ahead.”

05Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

Opportunities and challenges aheadIn 2008 we face new challenges, such as managing extensive greenfield construction in a country with limited infrastructure, while continuing to strengthen operating performance and increase current production. There are opportunities as well, such as beginning to mine at KOV earlier than planned and compressing the timeline for the Kamoto rehabilitation.

Your Board of Directors contended with many challenges this past year, from a creeping takeover attempt to a range of matters associated with the Nikanor bid, and I thank them for their dedication and guidance. Our new enlarged Board will continue to serve all Katanga shareholders, guiding the company as we embark on the exciting road ahead.

Goals for 2008As production grows and the capital program increases capacity during the year, we set the following goals for 2008:

Completing the greenfield feasibility study for the combined project by the third quarter.

Completing Phase II rehabilitation and expansion, thereby increasing capacity of the Kamoto Concentrator and Luilu Metallurgical Plant to 100,000 tonnes of copper cathode per year.

In parallel with this, developing the KOV pit for production and beginning construction of the associated greenfield whole-ore leaching and SX/EW facility.

Integrating provisions of the DCP joint venture agreement into the KCC joint venture agreement and having the mining/exploitation concessions issued directly to KCC by the government.

Ensuring that the effectiveness and capability of the on-site management team continues to grow and develop.

Continuing to increase Katanga’s enterprise value as a result of profitable production and efficient use of capital.

»

»

»

»

»

»

Ore stockpile A farm cooperative was established Examining the mine plan

I also wish to extend my appreciation to our employees, whose efforts and performance enabled us to achieve our objectives in 2007. We welcome Nikanor’s employees to the Katanga family as well, and look forward to working together as one team on the ambitious program ahead.

We will stay focused on our operating objectives and expansion program during 2008 to deliver intended results as we have in the past.

Arthur H. DittoPresident, Chief Executive Officer and Director

06 Katanga Mining Limited Annual Report 2007

Board of Directors

Chairman Hugh Stoyell (left) on a site tour

Katanga Mining Limited’s 10-person Board of Directors has broad experience in the mining sector and strong connections in the Democratic Republic of Congo. The Board is committed to corporate governance standards consistent with best practices in the natural resources sector.

Hugh StoyellIndependent Non-Executive ChairmanHugh Stoyell has more than 40 years of experience in the South African mining industry. His career includes 30 years in gold and chrome mining with Rand Mines Limited and 10 years with Duiker Mining Limited, retiring as the company’s Chairman and Managing Director in 2002. Most recently Mr Stoyell has acted as a consultant to various Black Economic Empowerment mining companies. He is currently a Non-Executive Director of Sentula Mining Limited as well as caretaker Chief Operating Officer of Siyanda Coal Limited.

Rafael BerberNon-Executive DirectorRafael Berber is Managing Partner of RP Capital Group, a London-based investment firm which he co-founded in July 2004. Mr. Berber formerly served as Vice Chairman of Global Capital Markets & Financing and Global Head of the Equity-Linked Products Group at Merrill Lynch, where he spent 16 years spearheading the development of the firm’s equity derivatives and emerging markets franchise.

Arthur H. DittoPresident, Chief Executive Officer and DirectorArthur Ditto has over 40 years of experience in the mining industry and has held the position of President, CEO and Director of Katanga Mining Limited since November 2005. Between 1993 and 2005, he served Kinross Gold Corporation in a variety of capacities, including President, Chief Operating Officer, Vice Chairman and Director. Prior to that, Mr Ditto was President and CEO of Plexus Resources and held various senior management and engineering positions in large copper producing operations with Anaconda/Arco.

George A. ForrestNon-Executive DirectorGeorge Forrest has been President of the Forrest Group, a private conglomerate of industrial enterprises, for over 20 years. The company was founded in 1922 in what is now the Democratic Republic of Congo and is one of the country’s largest industrial enterprises. Today the Forrest Group has operations located in Africa, Europe and the Middle East with businesses spanning civil engineering, mining, manufacturing and construction.

Malta D. Forrest Non-Executive DirectorMalta Forrest is the third generation of the Forrest family to be associated with the Forrest Group conglomerate of industrial enterprises. With extensive experience of operations in the Democratic Republic of Congo, his executive positions include Construction Manager and Deputy Managing Director of Enterprise Générale Malta Forrest SPRL.

Aristotelis Mistakidis Non-Executive DirectorAristotelis Mistakidis has been with Glencore International AG, a leading privately held, diversified natural resources company, since 1993. Mr Mistakidis is also currently Chairman of Mopani Copper Mines PLC and a director of Recyclex SA (formerly Metaleurop SA).

Jean-Claude Masangu Mulongo*Independent Non-Executive DirectorJean-Claude Masangu Mulongo is the Governor of the Central Bank of the Democratic Republic of Congo. Mr Masangu Mulongo has also represented the DRC in various roles including Governor for the DRC and second Vice President of the G24 at

07Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

Members of the Board and executive team on a site tour in the Luilu Metallurgical Plant (left) and Kamoto Underground Mine (right)

the International Monetary Fund, and Deputy Governor for the DRC at the World Bank. Prior to the Central Bank, he spent the majority of his career with the Citibank Group in Kinshasa.

Stephen Oke*Independent Non-Executive DirectorStephen Oke has over 30 years of experience in the mining and metals industry. He is currently a non-executive director of International Ferro Metals Ltd. Mr Oke spent 12 years in various operational management positions for the UK’s National Coal Board, Anglovaal Ltd, BP Coal and Johannesburg Consolidated Investment Co Ltd. Subsequently he has held senior positions in the investment banking industry, specializing in the metals and mining sector. Mr Oke was a Director of Nikanor PLC from June 2007 until its merger with Katanga Mining Limited.

Terry Robinson*Independent Non-Executive DirectorTerry Robinson has 35 years of international business experience.

Board committeesThe Board currently has three committees – audit, compensation and corporate governance – the mandates of which are consistent with best practices.

The role of the Audit Committee is to monitor the quality, integrity, and legal and regulatory compliance, of the company’s financial statements and other financial information. It also oversees the qualifications and independence of the independent external auditor and the internal audit procedures.

The role of the Compensation Committee is to review and approve the remuneration packages of the executive and senior management team, review the compensation of the Board on at least an annual basis, and administer the company’s compensation plans.

The role of the Corporate Governance Committee is to review the company’s corporate governance practices and assess the functioning and effectiveness of the Board, its committees and individual Board members.

Joint venture representationIn addition to the Board of Directors of Katanga Mining Limited, the Boards of Katanga’s two joint ventures, Kamoto Copper Company (KCC) and DRC Copper and Cobalt Project (DCP) meet a number of times a year. These Boards include representatives from Katanga’s joint venture partner Gécamines, a DRC state-owned mining company.

He is an independent non-executive director of EVRAZ Group SA, the largest Russian vertically integrated steel producer. Mr Robinson’s career includes serving as Deputy Chairman of Chapada Diamonds plc, Chief Executive and then Chairman of The Albert Fisher Group Plc and Chief Executive of Halstead Services Ltd. He was a Director of Nikanor PLC from July 2006 until its merger with Katanga Mining Limited.

Robert Wardell*Independent Non-Executive DirectorRobert Wardell is Vice-President, Finance & Chief Financial Officer of Victory Nickel Inc. Prior to that he was an audit partner with Deloitte & Touche, LLP. He has over 37 years of public accounting experience including nine years with the accounting and auditing technical group of Deloitte & Touche and 11 years as an audit partner based in Toronto.

* Member of Audit Committee Member of Compensation Committee Member of Corporate Governance Committee

08 Katanga Mining Limited Annual Report 2007

Project Review

Katanga completed the first phase of a complex brownfield project against a tight deadline, in a country with extremely limited infrastructure and services.

The Project team succeeded in handing over the assets to the Operations team on schedule and on budget, ensuring the joint venture could produce its first copper cathode by the end of 2007.

Much of the work in 2007 was characteristic of a major maintenance shutdown and refurbishment. In total, 34 kms of old electrical cable were removed and 81 kms of new cable installed; 71 new motor control centers were designed and installed; 383 new control and monitoring instruments were installed; over 950 tonnes of structural steel and plate work was completed; and 75 kms of new pipe was installed.

Skilled Project teamTo achieve the complex task at hand, a Project team was assembled and led by a team of 26 from Katanga who provided overall construction management. Engineering and procurement services were provided by Hatch, while construction was accomplished by Congolese and South African contractors. Civil and support work on site was carried out by Congolese contractors. The project team peaked at approximately 1,300

people, and a total of 2,229,000 work hours were spent in the reconstruction effort during the year. Approximately 60 per cent of the project manpower was provided by local labor.

Kamoto Underground MineThe rehabilitation needed to achieve Phase I production capacity at the Kamoto Underground Mine was fairly limited and much of the work was completed by site personnel. Primary pumping capacity was restored through a combination of new and rebuilt pumps and motors. Secondary pumping refurbishment continued throughout the year. Other work included restoring basic services such as dewatering and ventilation.

The new production fleet for Kamoto was ordered late in 2006. Equipment began arriving on site in the first quarter of 2007 and by mid-year the entire production fleet was operational.

“Much of the work in 2007 was characteristic of a major maintenance shutdown and refurbishment.”

09Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

Kamoto ConcentratorThe Phase I program called for restoration of the Kamoto Concentrator sufficient to process a minimum of 50,000 tonnes of sulphide ore and 20,000 tonnes of oxide ore per month. A component of this year’s plan was to restore much of the piping and electrical infrastructure needed for Phase I operations and beyond. Nearly all water and air delivery pipes were replaced during the year, as were all required motor control centers.

The surface crusher, conveyor systems and stockpile reclaim areas were either rebuilt or replaced. Two of the Kamoto mills were thoroughly serviced and relined, and new lubrication systems were installed. Essentially all of the process piping and pumps were replaced. Tanks were rebuilt and rubber lined to ensure their long-term service.

In the flotation cells, underlying structural support required only minimal clean up and repainting, but the cells themselves all required substantial rebuilding. A total of 88 of the original flotation cells and

related infrastructure were removed and rebuilt, and all were rubber lined and new flotation mechanisms were installed.

To transfer concentrate and water from the Kamoto Concentrator to the Luilu Metallurgical Plant, the existing pipelines between the sites were removed and four new pipelines, totaling 28 kms, were installed. New tailings pumps and delivery pipelines were installed.

Luilu Metallurgical PlantThe Luilu Metallurgical Plant was in a very poor condition and required extensive refurbishment to restore it to a reliable operating state. Substantial repair or replacement of the infrastructure took place throughout the year, including the replacement of approximately 32,000 square meters of roofing, installation of all new sump pumps, replacement of lighting and upgrading of safety installations.

The concentrate receiving and storage areas were restored to near full capacity. The thickeners and other tanks, vacuum pumps and two of the four drum filters were rebuilt, and

essentially all of the piping was replaced. All of the conveyor components were removed and replaced as required.

Because of the lead time required to design and build new roasters, the decision was made to restore the existing roaster section to reliable short-term operating condition. Substantial effort went into stabilizing the building structure. New pumps were installed, the regrind mill was rebuilt, and the roaster shell was serviced and a new refractory lining was installed.

In the leaching area, three new oxide receiving tanks were built and other leach tanks and CCD tanks were repaired as required. The cobalt area required extensive replacement of pumps and piping and four new tanks were installed. One belt filter and two filter presses were installed, to replace existing drum filters. The remaining original tanks were repaired as required and returned to service.

A new control system was installed at the Kamoto Concentrator

Workers fiberglassing electro-winning tanks (far left) and flotation cells in operation following extensive refurbishment (above)

Lifting cathodes at the Luilu Metallurgical Plant

10 Katanga Mining Limited Annual Report 2007

Work in the electro-winning section started with the cleanup, repair and relining of 54 cells. An additional 28 starter sheet cells were repaired and relined. New busbar fittings were designed and installed, and three new tanks were built and the distribution piping replaced. The existing lead anodes were cleaned and returned to service and new stainless steel cathodes were purchased for starter sheet production.

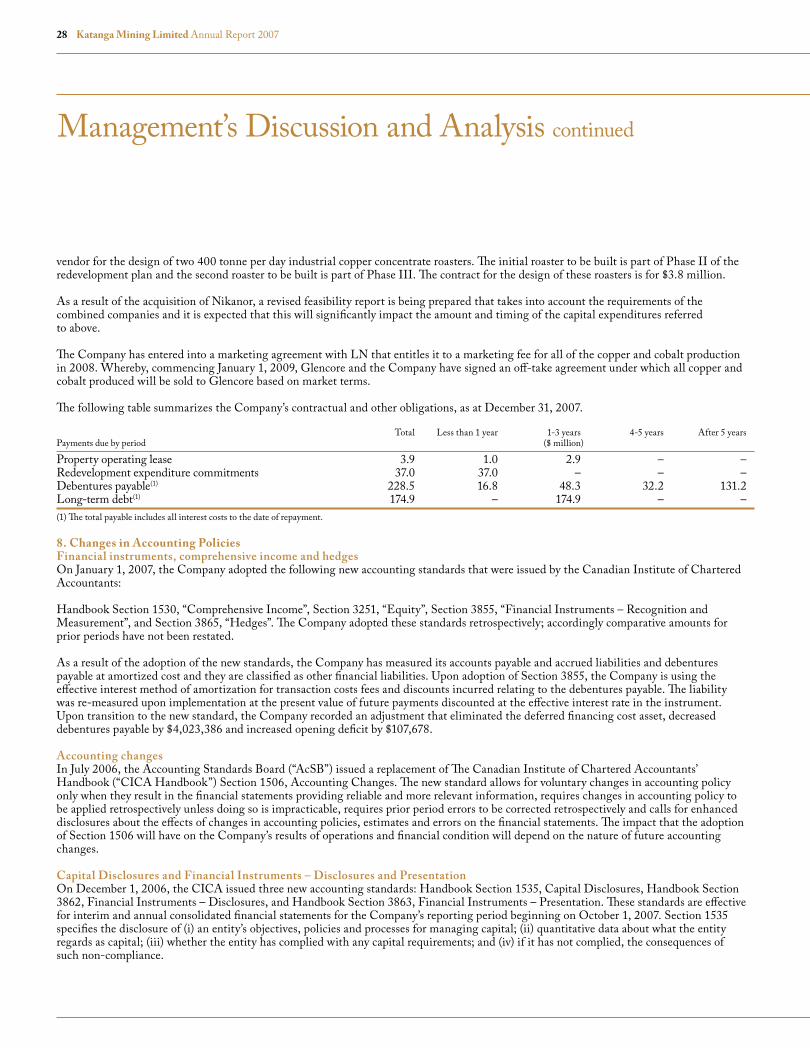

Kamoto Phase IIPhase II of the rehabilitation of the original Kamoto assets will be completed in 2008. A further mill and additional 58 flotation cells will be refurbished in the Kamoto Concentrator. In the Luilu Metallurgical Plant, leaching and electro-winning capacity will be doubled and a new roaster will be constructed. Preliminary engineering for Phase II began in October 2007, with site civil works for the new roaster beginning in November. Fabrication of the roaster unit began in the last quarter of the year.

Production capacity for the Kamoto assets will reach a nominal 150,000 tonnes of copper and 8,000 tonnes of cobalt in 2010 following completion of the four-phase rehabilitation. There is a progressive reduction in year to year capital spending for the added capacity, with the budget for 2008 set at US$136 million. Options for accelerating the later phases will be examined as part of the feasibility study due in Q3 2008.

Logistics expertiseDuring the course of the 18-month rehabilitation project, over 600 separate loads were shipped to site. The Project team substantially reduced the time taken to transport materials from Johannesburg: a journey that took over four weeks at the beginning of the year was reduced to as low as seven days, with an average of 12 days achieved.

Four full-time expeditors made frequent visits to manufacturers, ensuring scheduled deliveries were maintained for the smooth supply of materials. Through negotiation with the government, the joint venture was able to obtain authorization to clear customs in Kolwezi, thereby avoiding the severe border crossing congestion at Kasambala.

A weak bridge over the Lualaba River presented problems, as loads over 60 tonnes had to be broken down. The joint venture worked with other local mining companies and Gécamines to refurbish the Lualaba barge, an alternative that sped up the transit of large loads. While the majority of materials arrived by road, some larger items came via rail, demonstrating the availability of the rail network.

In-d

epth

Project Review continued

The waste stacker at KOV

11Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

Combined projectIn parallel with the Phase II rehabilitation, Katanga will develop the KOV open pit and build a whole-ore leach and SX/EW facility. A phased approach will be taken to the construction of the plant, with two 80,000 tonne per year copper production modules planned.

There will be a steep growth curve for both copper and cobalt production through to 2011, with a target of over 300,000 tonnes of refined copper per annum and over 30,000 tonnes of refined cobalt per annum. A feasibility study will be prepared by Q3 2008 for the integration of the combined assets following the merger with Nikanor.

An outline plan for the combined mine complex has the Kamoto Concentrator and Luilu Metallurgical Plant processing sulphide ore only. Oxide ore and all cobalt production will be processed through the new SX/EW facility, which will produce higher grade refined metal with better recoveries. Initial synergies that can be realized during 2008 will be explored, such as processing ore from Tilwezembe through the Kamoto Concentrator.

Goals for 2008The goals for 2008 relate to continuing the Kamoto rehabilitation while planning and beginning work on the combined operation, with both brownfield and greenfield construction under way:

Completing the feasibility study on the combined project by the end of Q3.

Reviewing the enlarged operations to ensure early synergies are realized ahead of the feasibility study completion.

Beginning mining at KOV by the end of the year, ahead of the dewatering program completion.

Continuing Kamoto Phase II construction as planned, reviewing the possibility of accelerating later phases.

Beginning construction of the acid plant and the first module of the greenfield whole-ore leaching and SX/EW facility.

»

»

»

»

»

“There will be a steep growth curve for both copper and cobalt production through to 2011.”

12 Katanga Mining Limited Annual Report 2007

Operations Review

Katanga made the transition from rehabilitation to production in 2007, with the Operations team working with the Project team to ensure a smooth handover and commissioning of the joint venture’s assets. The focus then shifted to ensuring a successful ramp-up and ongoing operations across the site.

Kamoto Underground MineThe first round was blasted in March. In total, 175,000 tonnes of ore were mined during the year. There was a progressive ramp-up towards the end of the year, with 45,000 tonnes mined in December.

While all equipment was in place, the management team was not staffed as quickly as planned. By year-end, however, leadership was in place to direct the underground

workforce and establish discipline and planning. The team will be supported by a small group of experienced contract miners in 2008.

The target is to exceed 60,000 tonnes per month of ore by April and thereafter increasing to 90,000 tonnes by year end.

Musonoie-T17 Open Pit Mine Pre-stripping began on schedule in May at Musonoie-T17, which is mined under contract. The ore body was not as close to the surface as the available information had indicated, and significantly more pre-stripping was required. Once mining began, over 30,000 tonnes of ore was mined. In addition, stockpiles of oxide ore were treated.

The transition from clean-up and rehabilitation to production has been challenging, with a steep learning curve to establish the management team, infrastructure and procedures for successful operation of a complex site.

“The overall reliability and performance of the plant has exceeded expectations.”

13Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

Kamoto ConcentratorThe total tonnage of sulphide concentrate produced was just under 12,000 tonnes. As a consequence of the late arrival of oxide ore from Musonoie-T17, oxide production did not begin until December. However, the overall reliability and performance of the plant has exceeded expectations.

Luilu Metallurgical PlantThe Luilu facility had limited operations in 2007, with cold commissioning beginning in late November and the first starter sheets stripped on December 17. The first commercial copper cathodes were produced on December 22. The physical quality of initial cathodes was variable as expected, but with good chemical quality overall. The

Luilu team will work over the early part of 2008 to ensure the consistency of the process, aiming to produce LME “A” grade copper, a higher quality than was historically produced at the facility. To achieve this, a change of system is planned from March onwards whereby copper will be plated directly onto a stainless steel cathode, rather than on copper starter sheets as originally conceived.

Operations team in placeFor a variety of reasons, both specific to candidates and as a result of the attempted hostile takeover in the summer, it took longer to fill management positions than anticipated. The team is now in place: Stuart Allen joined in September as Secretary General, responsible for HR and business improvement.

Adrian de Freitas, who has extensive experience in underground operations, joined just before the end of the year as Operations Director.

The merger with Nikanor also gave the opportunity to draw on an enlarged skills base to fill some remaining positions. Eamonn Browne is in charge of the open pits and Michael Watters leads the procurement function in Johannesburg to ensure spare parts and consumables are in place for reliable operation.

Accommodation needsTo accommodate the expatriate workforce, houses have been progressively refurbished, and 39 are now available. A construction camp

Flotation cells in the Kamoto Concentrator (far left) and employees in the Luilu Metallurgical Plant examine copper cathodes (above)

Blasting at the T17 open pit

14 Katanga Mining Limited Annual Report 2007

Operations Review continued

of semi-permanent accommodation for the Project team workforce was expanded in phases during the course of the year. By the end of the year, up to 590 people could be accommodated with full catering facilities.

An accommodation block is under construction near the former Kolwezi golf club, which will provide 40 single units, including rooms for visitors and a restaurant. Progress on the new block has been delayed but

should be completed in early 2008. The addition of a 100-person “village” from Nikanor means that sufficient accommodation will be available for the envisaged expatriate workforce by the end of the first quarter in 2008, and the use of hotel and boarding-house style accommodations will be phased out.

Workforce developmentWhen the joint venture took over the site in July 2006 it inherited a workforce of approximately 1,500 individuals, mainly ex-Gécamines workers. New hires during 2007 have taken this to over 2,400, with an additional 1,600 joining as a result of the Nikanor merger. There is a “lost generation” of workers who as a result of the decline of the mining industry in the DRC did not benefit from either formal education or on-the-job training. Substantial training investment is required to improve their skill base.

Safety cultureWhen the joint venture took over the Kamoto site there was little focus on safety, thus it was imperative to establish a safety culture. A dedicated safety team was formed and regular inspections carried out. A particular focus was placed on ensuring employees wear Personal Protective Equipment (PPE) at all times.

There were, unfortunately, two deaths during the year: one of an experienced employee seconded to a contractor, and the other a sub-contractor. The causes of both were fully investigated and there is confidence that improvements have been made, with greater training and supervision in key areas. There were no lost time accidents recorded in December.

An external audit was recently completed to evaluate progress and assess continuing risks, liabilities and compliance gaps. The site is implementing a company-wide safety system that will comply with ISO standards. A number of employees have received offsite training at NOHSA in South Africa, and the system will be rolled out onsite during 2008.

In-d

epth

“The Katanga Operations team has worked with its counterparts at Nikanor to ensure the smooth implementation of the merger.”

The construction camp built to house workers Underground operations began in March Copper production began in December

Goals for 2008The overriding goal for 2008 is to establish the benchmark for successful operations in the DRC. This includes:

Further developing a culture of safety and respect for the environment throughout the operations.

Making a strong focus on production and cost goals a way of life for the entire workforce, including a clear link between performance and recognition.

Demonstrating the capability of the mining operations to dependably meet expected production and cost performance.

Rapidly improving the systems and support functions assisting the management team, and selectively recruiting in order to ensure a critical mass of management.

Reinforcing an image of upstanding behavior to drive the continued consolidation of a business environment meeting international standards.

Strengthening cooperation with the DRC at a local, provincial, and national level.

»

»

»

»

»

»

15Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

Nearly 200,000 hours of training were conducted in 2007. The proposed restart of the Mutoshi Institute, a former training school for mine workers, by a group of local mining companies in conjunction with Gécamines will play an important role in meeting future training needs. There is also a plan to identify Congolese workers for a management development program to eventually replace much of the expatriate workforce.

EnvironmentEnvironmental emissions were at a low level in 2007 due to the transition to production. No significant environmental infraction or incident was reported during the year. Environmental baseline data continues to be collected and progress was made with water (surface and ground), soil, noise and air studies.

These will inform the Environmental and Social Impact Assessment and will be compiled in 2008 into long-term management plans.

Integration with NikanorSince the merger was announced in November, the Katanga Operations team has worked with its counterparts at Nikanor to ensure the smooth implementation of the merger on the ground. A management team was swiftly put in place after the merger was completed, and then toured each of the Katanga and Nikanor sites to enable employees to ask questions.

16 Katanga Mining Limited Annual Report 2007

Social Responsibility Review

Social responsibility has a very clear meaning to Katanga: supporting the social infrastructure to create a platform that ensures long-term, sustainable improvements in the day-to-day lives of those surrounding the company’s operations.

Clear progress was made in all areas of Katanga’s social responsibility strategy and activities during 2007. This is particularly noteworthy in the context of an environment still suffering from high unemployment, artisanal mining activity and weak general infrastructure. The following is a progress report on initiatives undertaken during the year.

Governance improvedIn 2007, Katanga improved the governance structure used to guide decisions and ensure compliance with corporate standards. Three important measures were completed:

A Sustainable Development Policy was approved by the Board of

»

Directors, from which a broad range of policies and procedures was developed.Performance criteria became a standard provision in all social development projects. In addition, it became mandatory to direct all payments into recognized bank accounts, and cash payment of contracts was eliminated.International codes and standards became standard reference for Katanga’s policies and procedures including, by way of example, the Voluntary Principles for Security and Human Rights in all security training and management plans.

Ongoing consultationIn April 2007, consultation with a far-reaching audience including government authorities, traditional chiefs, non-governmental organizations (NGOs), community groups and other mining companies was undertaken through a number of community-based engagement sessions. Katanga’s meetings were conducted in both French and Swahili to ensure full comprehension of the discussions.

»

»

Feedback from local stakeholders attending these meetings was consistent regardless of location: “We want our children to be educated”, “We want you to hire locally” and “We need better healthcare”. This feedback, which aligned closely with Katanga’s own thinking, formed the basis for a number of initiatives during the year, as outlined below.

To ensure that communication channels remain open with local stakeholders, an ongoing consultation and grievance process was established and is managed by a dedicated management team. Katanga believes that continual communication with local stakeholders will help ensure that issues and concerns are addressed before they become problems.

Community investmentKatanga’s level of commitment to the community can be measured by progress made in four areas of social development:

HealthcareInfrastructure improvements at the Mwangeji Hospital were completed during 2007, including repairs to the

“To ensure that communication channels remain open with local stakeholders, an ongoing consultation and grievance process was established.”

17Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

Goals for 2008In addition to expanding efforts in governance and transparency, priorities include:

In collaboration with other mining companies in the area, rehabilitating the Mutoshi Training Institute and upgrading instructional capacity.

Further upgrading the delivery of community medical services through both the Mwangeji Hospital and the community clinic network.

Initiating a malaria vector control program in the general Kolwezi area.

Sponsoring the start of the GAVI Alliance community inoculation program.

Completing improvements to roads in the town of Kolwezi.

Expanding support to upgrading local educational capacity.

Producing a public progress report summarizing activities for the year.

»

»

»

»

»

»

»

perimeter security wall and the construction of two new sanitation blocks that restored toilet and shower capacity to the hospital. The facility was also the benefactor of a collaborative effort between Katanga and Project CURE, a US-based non-profit group, for a shipment of donated medical supplies and equipment due to arrive in early 2008. The value of these two projects exceeded US$650,000.

Work also began with Crusader Health, an independent medical services provider, to rehabilitate and manage a new hospital and three clinic facilities in local communities surrounding the mine. In addition to contributing to the capital costs for facility rehabilitation, medical expenses for employees and their dependents are paid for by the company, totalling approximately US$3 million per year. InfrastructureA broad range of projects was completed in 2007, yielding improvements to local roads and sanitation. Initiatives included the restoration of the national road between Kanina and Kapata, which

Harvesting the first crop at the Mukweji Farm and (far left) refurbishing the farmhouse

employed 100 artisanal miners; rebuilding of a section of road between Kolwezi and Nguba; and the clearing of approximately 3,000 metres of drains and ditches in Manika, reducing health and sanitation issues associated with standing water.

To assist with needed upgrades to local power distribution capacity, the company donated a large transformer to the Congolese power authority. Expenditure for infrastructure improvement initiatives throughout 2007 totalled approximately US$2.75 million.

Capacity-buildingLocal economic expansion in Kolwezi requires diversification. To support this process, Katanga initiated the revitalization of a 30-hectare farm with the goal of creating a self-sustaining and independent cooperative. The farm is now producing a commercial crop of vegetables being sold throughout Kolwezi. Farm produce is also being purchased by the catering companies providing services to Katanga’s construction camp. Katanga provided the initial capital required by this

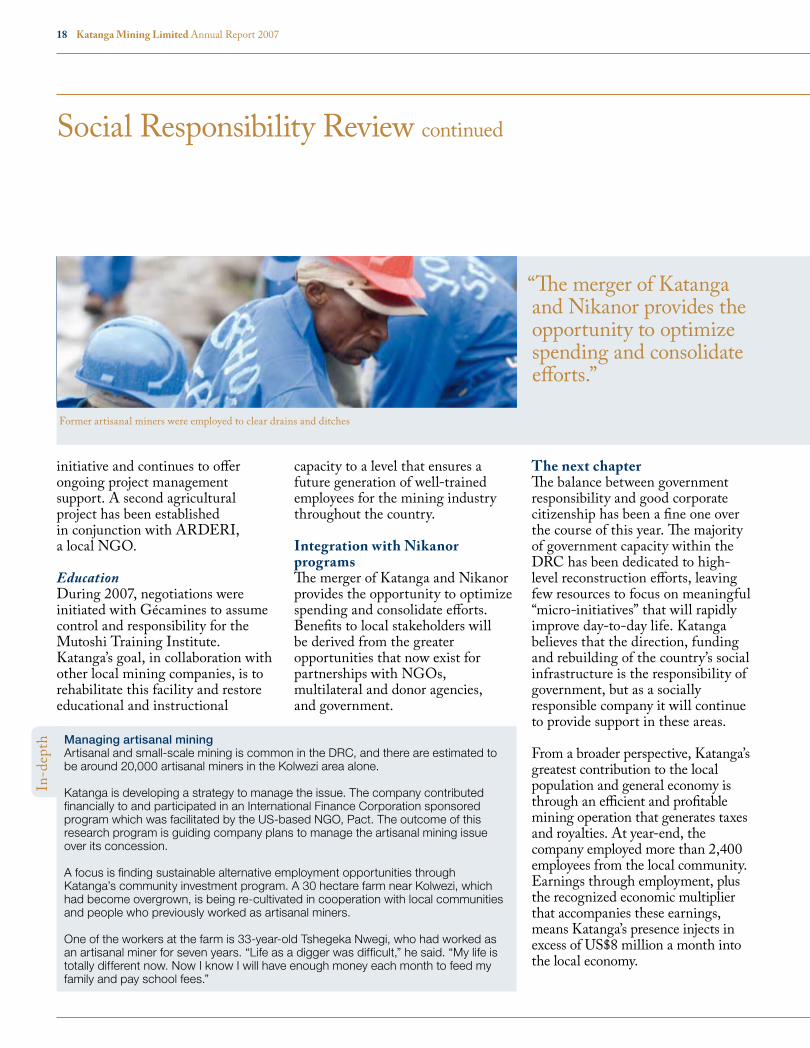

Former artisanal miners were employed to clear drains and ditches

18 Katanga Mining Limited Annual Report 2007

initiative and continues to offer ongoing project management support. A second agricultural project has been established in conjunction with ARDERI, a local NGO.

EducationDuring 2007, negotiations were initiated with Gécamines to assume control and responsibility for the Mutoshi Training Institute. Katanga’s goal, in collaboration with other local mining companies, is to rehabilitate this facility and restore educational and instructional

capacity to a level that ensures a future generation of well-trained employees for the mining industry throughout the country.

Integration with Nikanor programsThe merger of Katanga and Nikanor provides the opportunity to optimize spending and consolidate efforts. Benefits to local stakeholders will be derived from the greater opportunities that now exist for partnerships with NGOs, multilateral and donor agencies, and government.

Managing artisanal miningArtisanal and small-scale mining is common in the DRC, and there are estimated to be around 20,000 artisanal miners in the Kolwezi area alone.

Katanga is developing a strategy to manage the issue. The company contributed financially to and participated in an International Finance Corporation sponsored program which was facilitated by the US-based NGO, Pact. The outcome of this research program is guiding company plans to manage the artisanal mining issue over its concession.

A focus is finding sustainable alternative employment opportunities through Katanga’s community investment program. A 30 hectare farm near Kolwezi, which had become overgrown, is being re-cultivated in cooperation with local communities and people who previously worked as artisanal miners.

One of the workers at the farm is 33-year-old Tshegeka Nwegi, who had worked as an artisanal miner for seven years. “Life as a digger was difficult,” he said. “My life is totally different now. Now I know I will have enough money each month to feed my family and pay school fees.”

In-d

epth

Social Responsibility Review continued

“The merger of Katanga and Nikanor provides the opportunity to optimize spending and consolidate efforts.”

The next chapterThe balance between government responsibility and good corporate citizenship has been a fine one over the course of this year. The majority of government capacity within the DRC has been dedicated to high-level reconstruction efforts, leaving few resources to focus on meaningful “micro-initiatives” that will rapidly improve day-to-day life. Katanga believes that the direction, funding and rebuilding of the country’s social infrastructure is the responsibility of government, but as a socially responsible company it will continue to provide support in these areas.

From a broader perspective, Katanga’s greatest contribution to the local population and general economy is through an efficient and profitable mining operation that generates taxes and royalties. At year-end, the company employed more than 2,400 employees from the local community. Earnings through employment, plus the recognized economic multiplier that accompanies these earnings, means Katanga’s presence injects in excess of US$8 million a month into the local economy.

19Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

Financial Review

Katanga began 2008 with a healthy balance sheet and is now generating operational cash flow. The US$175 million Phase I refurbishment program was delivered on budget and copper production began on schedule in December 2007, with the first sales recorded early in the new year.

Following the completion of the merger with Nikanor in January 2008, Katanga had approximately US$500 million in cash. The company has a low debt level, with US$125 million in corporate debentures and a US$150 million convertible loan.

Marketing agent appointedIn May 2007 Katanga appointed LN Metals International Ltd as sole agent for 2008 for the marketing of copper and cobalt from its Kamoto operations. LN Metals is assisting the company in establishing a worldwide customer base for its initial copper cathode and cobalt metal production to enable it to maximize the profitability of its 2008 production. Production during 2008 is expected to be 30,500 tonnes of copper cathode and 1,600 tonnes of cobalt metal.

Financing in placeDuring 2007 Katanga had planned to arrange the final stage of its three-stage financing. Three lead arrangers were mandated in March. However, ongoing uncertainty generated by the mining license review in the Democratic Republic of Congo and the hostile takeover attempt over the summer meant that alternative arrangements were required.

In November, Katanga entered into a US$150 million two-year loan facility with Glencore Finance (Bermuda) Limited. The loan bears interest at LIBOR plus four per cent per annum payable upon maturity. It is convertible in whole or in part at the option of Glencore into up to 9,157,509 common shares at any time during the first year and only on repayment of the Facility during the second year.

Additionally, Katanga and Glencore agreed to a 10 year off-take contract starting in 2009 under which Glencore will buy 100 per cent of Katanga’s annual copper and cobalt production at market terms. The agreement provides for payment by Glencore of 90 per cent of the expected sales value upon loading at

In Katanga’s final pre-production year, the company secured the last stage of its financing for the original Kamoto project and entered into off-take agreements for 2008 and for 2009 onwards.

“Katanga began 2008 with a healthy balance sheet and is now generating operational cash flow.”

20 Katanga Mining Limited Annual Report 2007

the mine gate, with the balance payable upon delivery of the metal at the discharge port. This significantly reduces working capital requirements. Following the merger with Nikanor, Glencore’s off-take agreement was extended for the life of all Katanga’s mines on the same terms.

Future financing requirementsFollowing the merger with Nikanor, the company plans to develop a combined mine complex using a phased expansion approach, which will allow a greater portion of capital expenditure to be funded from internally produced cash flows.

Financing requirements are anticipated to be up to US$500 million, to be funded by a loan facility for drawdown in the second half of 2009. The requirements will be reduced by early cash flow from production, which will be more significant if copper and cobalt prices remain at their current levels. The final amount of financing required will be determined by a feasibility study on the expanded mine complex to be published in the third quarter of 2008.

Goals for 2008Capital expenditure for 2008 will be funded from existing cash reserves, with additional financing not anticipated before mid-2009. Goals for the year relate to marketing the first commercial production and establishing future funding requirements:

Generating operational cash flow through successful marketing of metal.

Refining additional funding requirements as part of the feasibility study.

Agreeing terms with a group of lenders for a debt facility for drawdown in the second half of 2009.

Integrating Katanga and Nikanor finance teams and systems.

Implementing the Management Information System business platform.

»

»

»

»

»

Financial Review continued

Underground mining at Kamoto

21Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

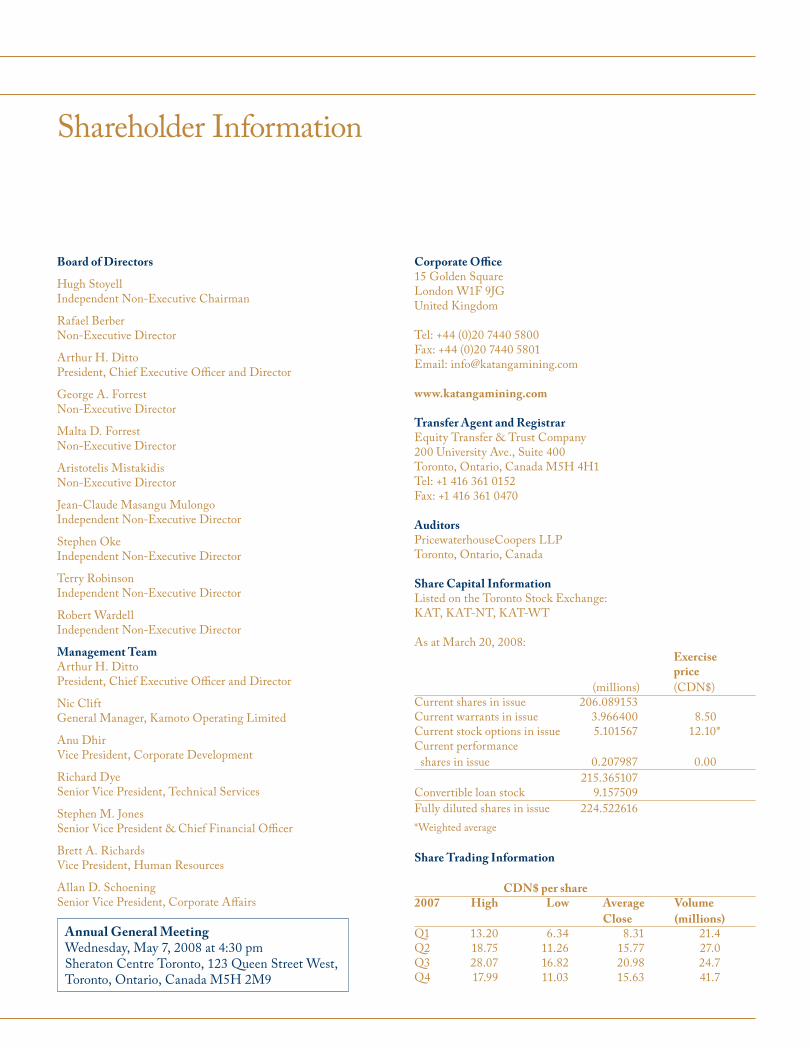

The following discussion and analysis is management’s assessment of the results of operations and financial condition of Katanga Mining Limited (“Katanga” or the “Company”) and should be read in conjunction with its 2007 audited consolidated financial statements. The consolidated financial statements have been prepared in accordance with Canadian generally accepted accounting principles. All dollar amounts unless otherwise indicated are in United States dollars. This information has been prepared as of March 20, 2008. Katanga’s common shares, warrants and notes trade on the TSX Exchange under the symbols “KAT” “KAT.WT” and “KAT.NT” respectively. Its most recent filings are available on the System for Electronic Document Analysis and Retrieval (“SEDAR”) and can be accessed through the internet at www.sedar.com.

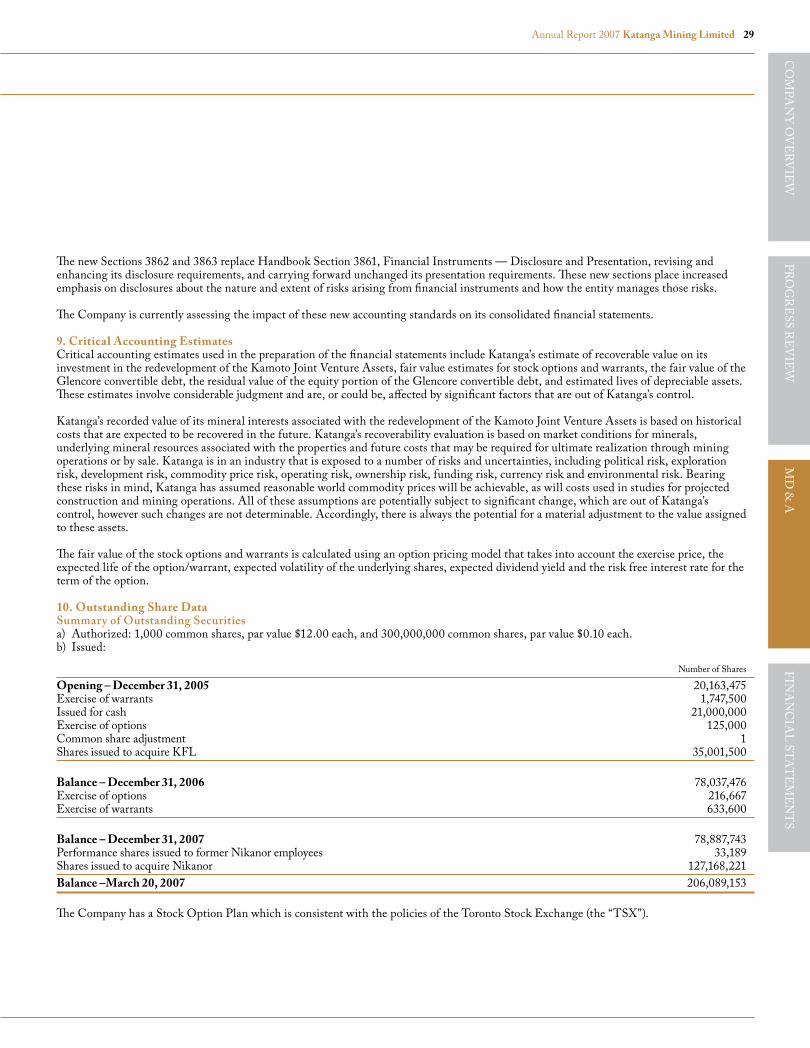

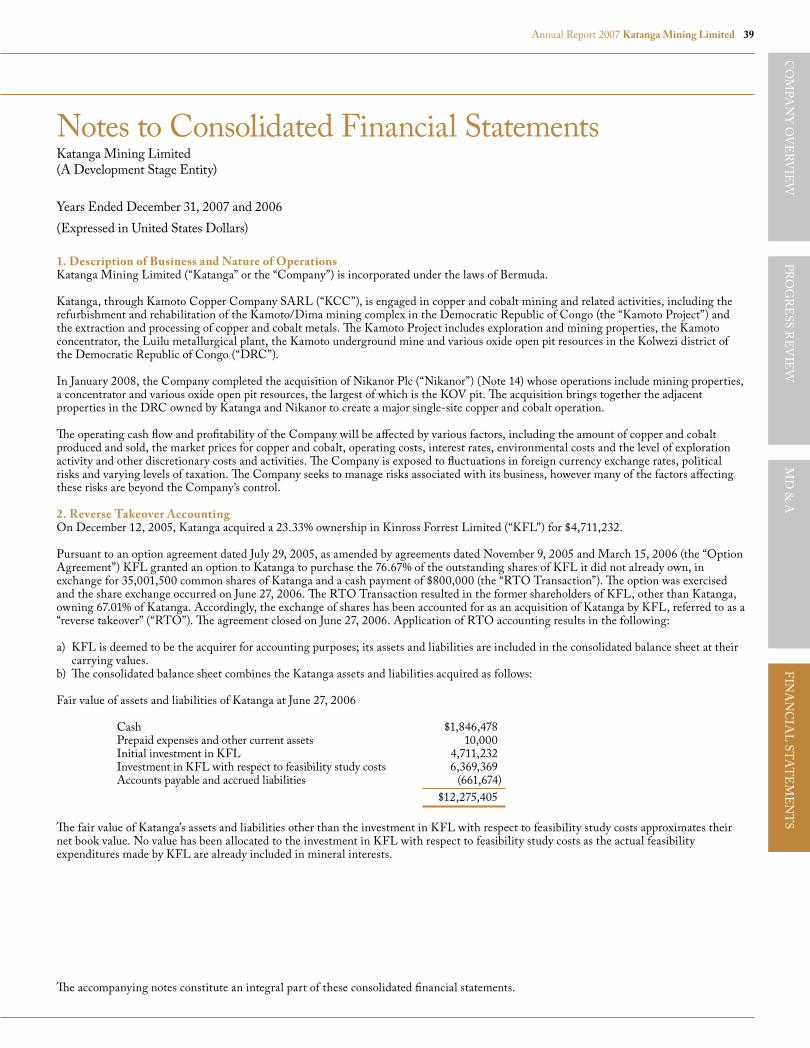

1. Company OverviewKatanga is incorporated under the laws of Bermuda and is engaged in the acquisition and development of mineral properties.

In 2004 Kinross Forrest Limited (“KFL”) (which later became a subsidiary of the Company) entered into a joint venture with La Generale des Carrieres et des Mines (“Gécamines”) and set up a project company called Kamoto Copper Company SARL (“KCC”) (75% KFL and 25% Gécamines). Katanga, through KCC, is engaged in copper and cobalt mining and related activities, including the refurbishment and rehabilitation of the Kamoto/Dima mining complex in the Democratic Republic of Congo (the “Kamoto Project”) and the extraction and processing of copper and cobalt metals. The Kamoto Project includes exploration and mining properties, the Kamoto concentrator, the Luilu metallurgical plant, the Kamoto underground mine and various oxide open pit resources in the Kolwezi district of the Democratic Republic of Congo.

In January 2008, the Company completed the acquisition of Nikanor Plc (“Nikanor”). Nikanor has 75% ownership of a project company called DRC Copper and Cobalt Project S.A.R.L (“DCP”) with the other 25% held by Gécamines. DCP’s operations include mining properties, a concentrator and various oxide open pit resources, the largest of which is the KOV pit. The acquisition brings together the adjacent properties in the Democratic Republic of Congo, owned by Katanga and Nikanor, which were previously part of the same complex, to create a major single-site copper and cobalt operation.

2. Highlights and Outlook Highlights for 2007 and the start of 2008

Construction team build up began onsite in January 2007 and the last of the major infrastructure contracts were awarded.

An updated reserves and resources statement was released in February 2007. Proven and probable ore grades for the Kamoto underground mine increased significantly. Total reserves and resources are 161.9 million tonnes of ore with an average copper grade of 3.50% and an average cobalt grade of 0.38%.

The underground mine became operational and blasting began on March 21, 2007.

Concentrator commissioning began on schedule in mid-July. In total, one sulphide and one oxide mill and 88 flotation cells were operational in phase one.

The seven kilometer concentrate delivery pipeline to the metallurgical plant was completed in July.

The Company has entered into a marketing agreement with LN Metals International Ltd (“LN”) that entitles it to a marketing fee for all copper and cobalt production in 2008.

Glencore International AG (“Glencore”) and the Company have signed an off-take agreement whereby, commencing January 1, 2009, all copper and cobalt produced will be sold to Glencore based on market terms.

Extensive improvements were implemented to health and safety standards and operating procedures.

Community Development activities that commenced in the year for the local area include agriculture, enterprise creation, health, sanitation and infrastructure programs.

Arthur Ditto was appointed as Chairman of the Company’s Board of Directors on July 3, 2007 following the resignation of Robert Buchan as the Company’s Non-executive Chairman.

Blasting began at the end of September at the Musonoie-T17 open pit mine and the first ore was extracted.

»

»

»

»

»

»

»

»

»

»

»

Management’s Discussion and Analysis

22 Katanga Mining Limited Annual Report 2007

Management’s Discussion and Analysis continued

In July 2007, Central African Mining & Exploration Company plc (“CAMEC”) advised Katanga that it intended to make a takeover offer for the Company. In response, Katanga established an Independent Committee of the Board of Directors to review all strategic alternatives available to the Company to achieve maximum value for shareholders. CAMEC’s offer was made formally on August 29 and withdrawn on September 6.

A US$150 million two-year convertible debt facility was arranged with Glencore on November 5, 2007.

A special meeting of shareholders held on November 2 approved an increase in Katanga’s share capital to provide the Company with the flexibility for future equity financings or acquisitions.

On November 6, 2007 Katanga announced the acquisition of Nikanor, which has an adjacent copper-cobalt concession in the DRC. The acquisition was completed on January 11, 2008 and the consideration for the Nikanor shares comprised of 0.613 new common shares of the Company and $2.16 in the form of a cash return to each Nikanor shareholder from Nikanor’s existing cash resources.

Cold commissioning at the Luilu Metallurgical Plant began in late November and the first starter sheets were stripped on December 17. The first commercial copper cathodes were produced on December 22, 2007 and shipped in January 2008.

On February 8, 2008, the Company announced that Gécamines and Kamoto Copper Company signed an agreement that sets out compensation, security and payment in exchange for the release to Gécamines of the portion of the KCC concession that represents the Mashamba West and Dikuluwe deposits. The agreement provides that the deposits either be replaced or that the Company is fairly compensated for their economic value. These deposits were not scheduled to start producing oxide ores until 2020 and 2023, respectively.

OutlookProduction for 2008 is forecast to be 30,500 tonnes of copper cathode and 1,600 tonnes of cobalt metal, generating Katanga’s first operational cash flow.

Kamoto’s Phase II rehabilitation is commencing as planned and the Company is reviewing the possibility of accelerating later phases. A further mill and additional 58 flotation cells will be refurbished in the Kamoto Concentrator. In the Luilu Metallurgical Plant, leaching and electro-winning capacity will be doubled and a new roaster will be constructed.

In parallel with the Phase II rehabilitation, Katanga will develop the KOV open pit and build a whole-ore leach and SX/EW facility. Construction of the acid plant and the first of two 80 thousand tonne per year modules of the SX/EW facility will begin during 2008.

Completion of the feasibility study on the enlarged project due to the acquisition of Nikanor is expected by the end of September 2008.

A full integration of the Nikanor assets is expected to be completed during 2008. A four year phased ramp-up is planned with a forecast production of over 300,000 tonnes of refined copper and over 30,000 tonnes of refined cobalt by 2011.

The acquisition will bring together the adjacent properties in the DRC owned by Katanga and Nikanor, which were previously part of the same Mine Complex, to create a major single-site copper and cobalt operation.

Additional funding requirements as part of the feasibility study will be calculated and terms agreed with a group of lenders for a debt facility for drawdown in the first half of 2009.

We will continue to evolve a culture of safety and respect for the environment throughout the Company’s operations to ensure consistent performance at the level expected of world-class operators.

Continued expansion of the skills and operational knowledge of the work force is seen as a major challenge going forward. Nearly 200,000 hours of training were carried out in 2007. The proposed restart in 2008 of the Mutoshi Institute, a former training school for mine workers, will play an important role in meeting future training needs.

»

»

»

»

»

»

»

»

»

»

»

»

»

»

»

23Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

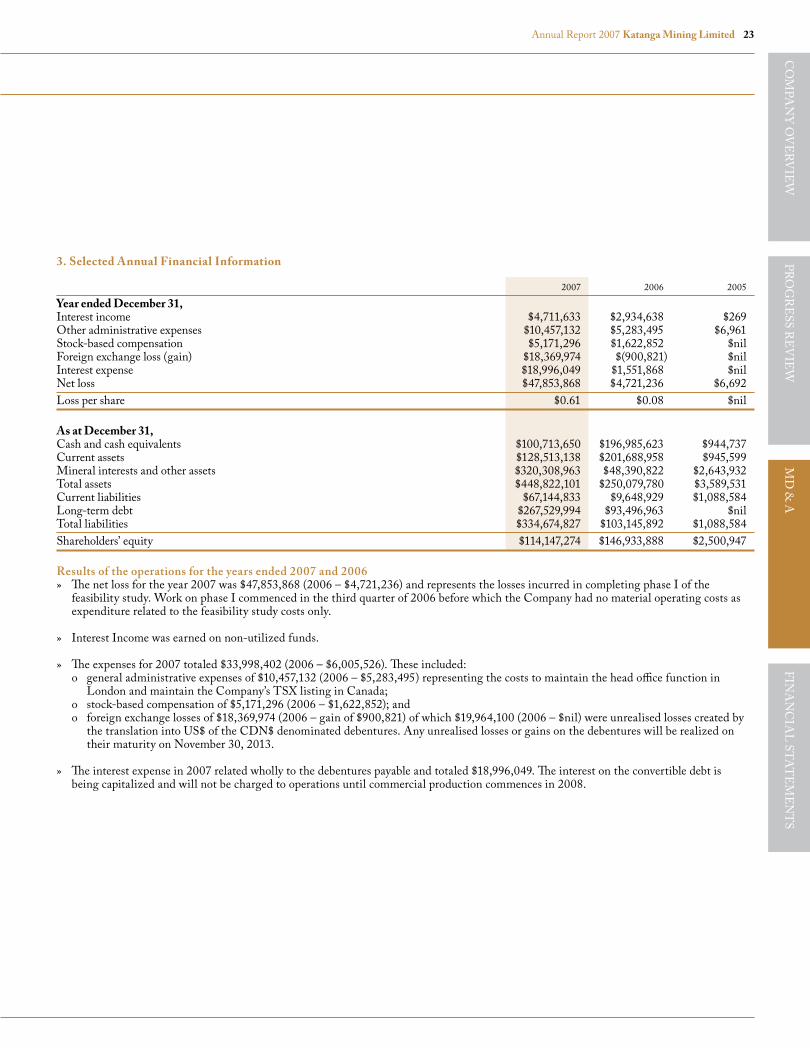

3. Selected Annual Financial Information

2007 2006 2005

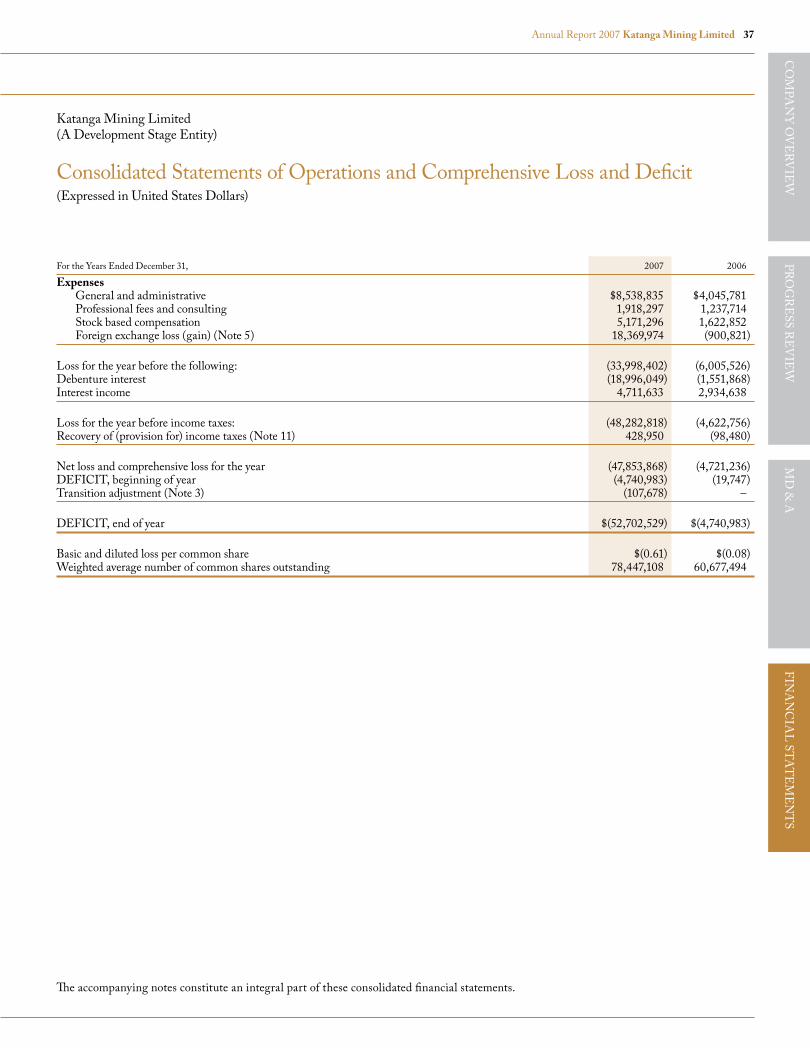

Year ended December 31, Interest income $4,711,633 $2,934,638 $269Other administrative expenses $10,457,132 $5,283,495 $6,961Stock-based compensation $5,171,296 $1,622,852 $nilForeign exchange loss (gain) $18,369,974 $(900,821) $nilInterest expense $18,996,049 $1,551,868 $nilNet loss $47,853,868 $4,721,236 $6,692

Loss per share $0.61 $0.08 $nil

As at December 31, Cash and cash equivalents $100,713,650 $196,985,623 $944,737Current assets $128,513,138 $201,688,958 $945,599Mineral interests and other assets $320,308,963 $48,390,822 $2,643,932Total assets $448,822,101 $250,079,780 $3,589,531Current liabilities $67,144,833 $9,648,929 $1,088,584Long-term debt $267,529,994 $93,496,963 $nilTotal liabilities $334,674,827 $103,145,892 $1,088,584

Shareholders’ equity $114,147,274 $146,933,888 $2,500,947

Results of the operations for the years ended 2007 and 2006The net loss for the year 2007 was $47,853,868 (2006 – $4,721,236) and represents the losses incurred in completing phase I of the feasibility study. Work on phase I commenced in the third quarter of 2006 before which the Company had no material operating costs as expenditure related to the feasibility study costs only.

Interest Income was earned on non-utilized funds.

The expenses for 2007 totaled $33,998,402 (2006 – $6,005,526). These included: o general administrative expenses of $10,457,132 (2006 – $5,283,495) representing the costs to maintain the head office function in

London and maintain the Company’s TSX listing in Canada; o stock-based compensation of $5,171,296 (2006 – $1,622,852); and o foreign exchange losses of $18,369,974 (2006 – gain of $900,821) of which $19,964,100 (2006 – $nil) were unrealised losses created by

the translation into US$ of the CDN$ denominated debentures. Any unrealised losses or gains on the debentures will be realized on their maturity on November 30, 2013.

The interest expense in 2007 related wholly to the debentures payable and totaled $18,996,049. The interest on the convertible debt is being capitalized and will not be charged to operations until commercial production commences in 2008.

»

»

»

»

24 Katanga Mining Limited Annual Report 2007

Management’s Discussion and Analysis continued

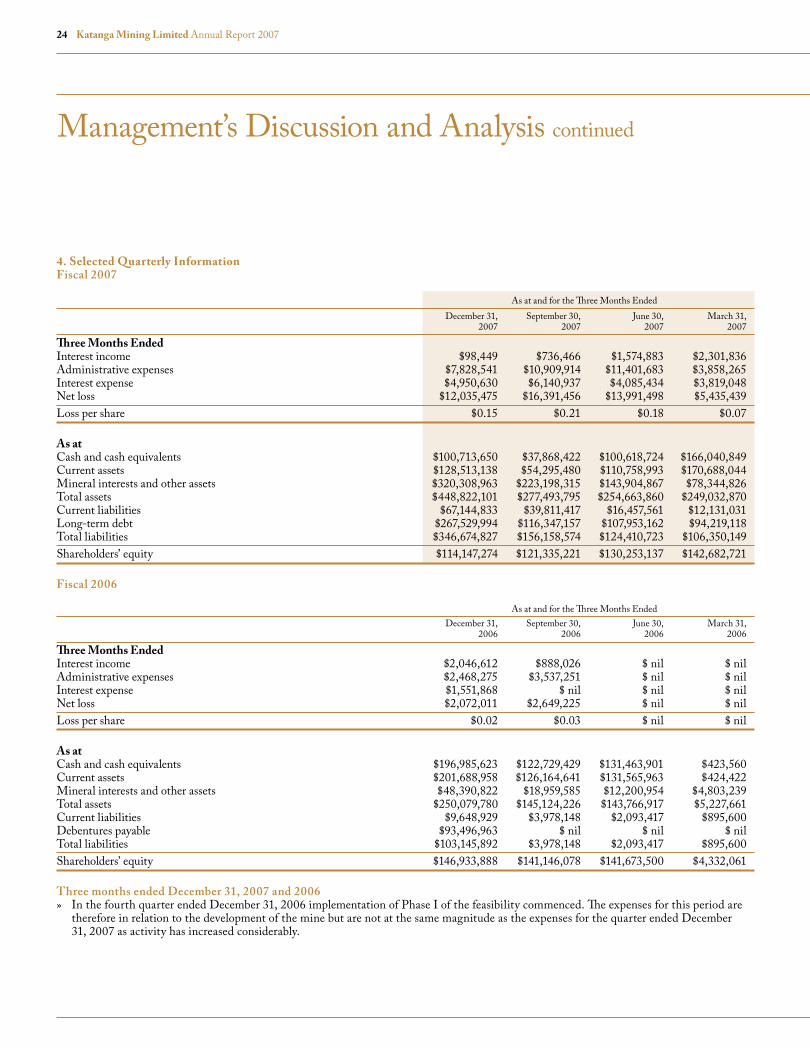

4. Selected Quarterly InformationFiscal 2007

As at and for the Three Months Ended

December 31, September 30, June 30, March 31, 2007 2007 2007 2007

Three Months EndedInterest income $98,449 $736,466 $1,574,883 $2,301,836Administrative expenses $7,828,541 $10,909,914 $11,401,683 $3,858,265Interest expense $4,950,630 $6,140,937 $4,085,434 $3,819,048Net loss $12,035,475 $16,391,456 $13,991,498 $5,435,439

Loss per share $0.15 $0.21 $0.18 $0.07

As atCash and cash equivalents $100,713,650 $37,868,422 $100,618,724 $166,040,849Current assets $128,513,138 $54,295,480 $110,758,993 $170,688,044Mineral interests and other assets $320,308,963 $223,198,315 $143,904,867 $78,344,826Total assets $448,822,101 $277,493,795 $254,663,860 $249,032,870Current liabilities $67,144,833 $39,811,417 $16,457,561 $12,131,031Long-term debt $267,529,994 $116,347,157 $107,953,162 $94,219,118Total liabilities $346,674,827 $156,158,574 $124,410,723 $106,350,149

Shareholders’ equity $114,147,274 $121,335,221 $130,253,137 $142,682,721

Fiscal 2006

As at and for the Three Months Ended

December 31, September 30, June 30, March 31, 2006 2006 2006 2006

Three Months Ended Interest income $2,046,612 $888,026 $ nil $ nilAdministrative expenses $2,468,275 $3,537,251 $ nil $ nilInterest expense $1,551,868 $ nil $ nil $ nilNet loss $2,072,011 $2,649,225 $ nil $ nil

Loss per share $0.02 $0.03 $ nil $ nil

As atCash and cash equivalents $196,985,623 $122,729,429 $131,463,901 $423,560Current assets $201,688,958 $126,164,641 $131,565,963 $424,422Mineral interests and other assets $48,390,822 $18,959,585 $12,200,954 $4,803,239Total assets $250,079,780 $145,124,226 $143,766,917 $5,227,661Current liabilities $9,648,929 $3,978,148 $2,093,417 $895,600Debentures payable $93,496,963 $ nil $ nil $ nilTotal liabilities $103,145,892 $3,978,148 $2,093,417 $895,600

Shareholders’ equity $146,933,888 $141,146,078 $141,673,500 $4,332,061

Three months ended December 31, 2007 and 2006In the fourth quarter ended December 31, 2006 implementation of Phase I of the feasibility commenced. The expenses for this period are therefore in relation to the development of the mine but are not at the same magnitude as the expenses for the quarter ended December 31, 2007 as activity has increased considerably.

»

25Annual Report 2007 Katanga Mining LimitedC

OM

PA

NY

OV

ER

VIE

WP

RO

GR

ES

S R

EV

IEW

MD

& A

FIN

AN

CIA

L S

TA

TE

ME

NT

S

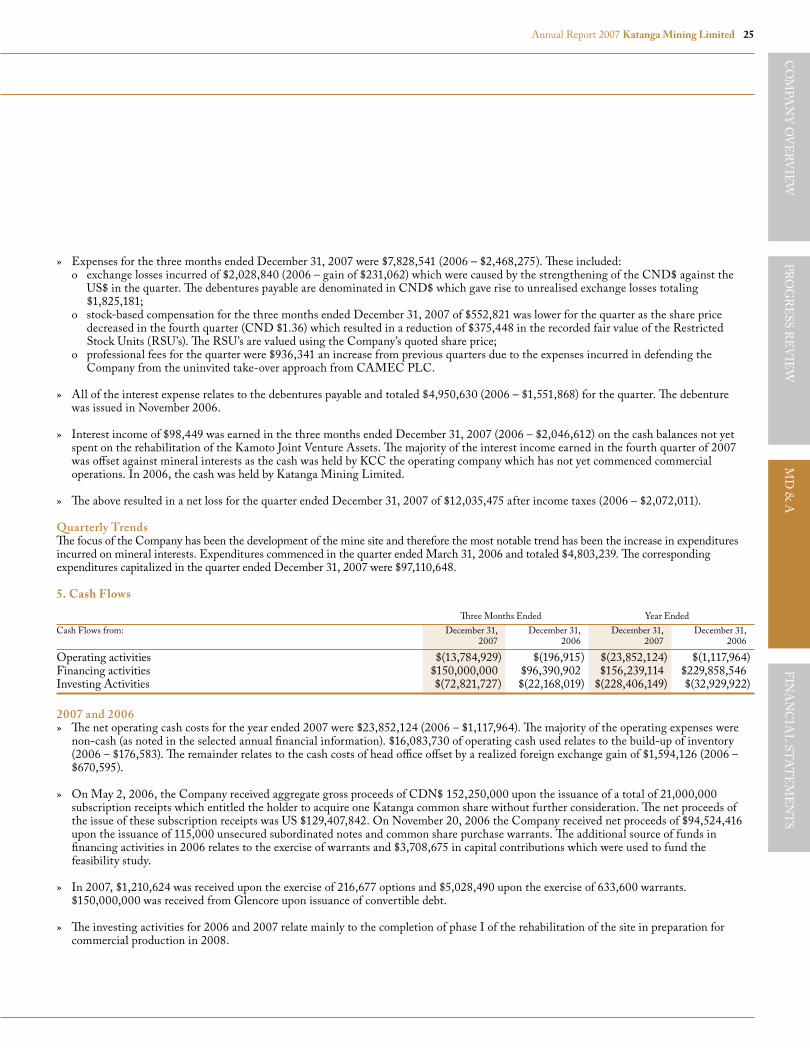

Expenses for the three months ended December 31, 2007 were $7,828,541 (2006 – $2,468,275). These included: o exchange losses incurred of $2,028,840 (2006 – gain of $231,062) which were caused by the strengthening of the CND$ against the

US$ in the quarter. The debentures payable are denominated in CND$ which gave rise to unrealised exchange losses totaling $1,825,181;

o stock-based compensation for the three months ended December 31, 2007 of $552,821 was lower for the quarter as the share price decreased in the fourth quarter (CND $1.36) which resulted in a reduction of $375,448 in the recorded fair value of the Restricted Stock Units (RSU’s). The RSU’s are valued using the Company’s quoted share price;

o professional fees for the quarter were $936,341 an increase from previous quarters due to the expenses incurred in defending the Company from the uninvited take-over approach from CAMEC PLC.

All of the interest expense relates to the debentures payable and totaled $4,950,630 (2006 – $1,551,868) for the quarter. The debenture was issued in November 2006.

Interest income of $98,449 was earned in the three months ended December 31, 2007 (2006 – $2,046,612) on the cash balances not yet spent on the rehabilitation of the Kamoto Joint Venture Assets. The majority of the interest income earned in the fourth quarter of 2007 was offset against mineral interests as the cash was held by KCC the operating company which has not yet commenced commercial operations. In 2006, the cash was held by Katanga Mining Limited.

The above resulted in a net loss for the quarter ended December 31, 2007 of $12,035,475 after income taxes (2006 – $2,072,011).

Quarterly TrendsThe focus of the Company has been the development of the mine site and therefore the most notable trend has been the increase in expenditures incurred on mineral interests. Expenditures commenced in the quarter ended March 31, 2006 and totaled $4,803,239. The corresponding expenditures capitalized in the quarter ended December 31, 2007 were $97,110,648.

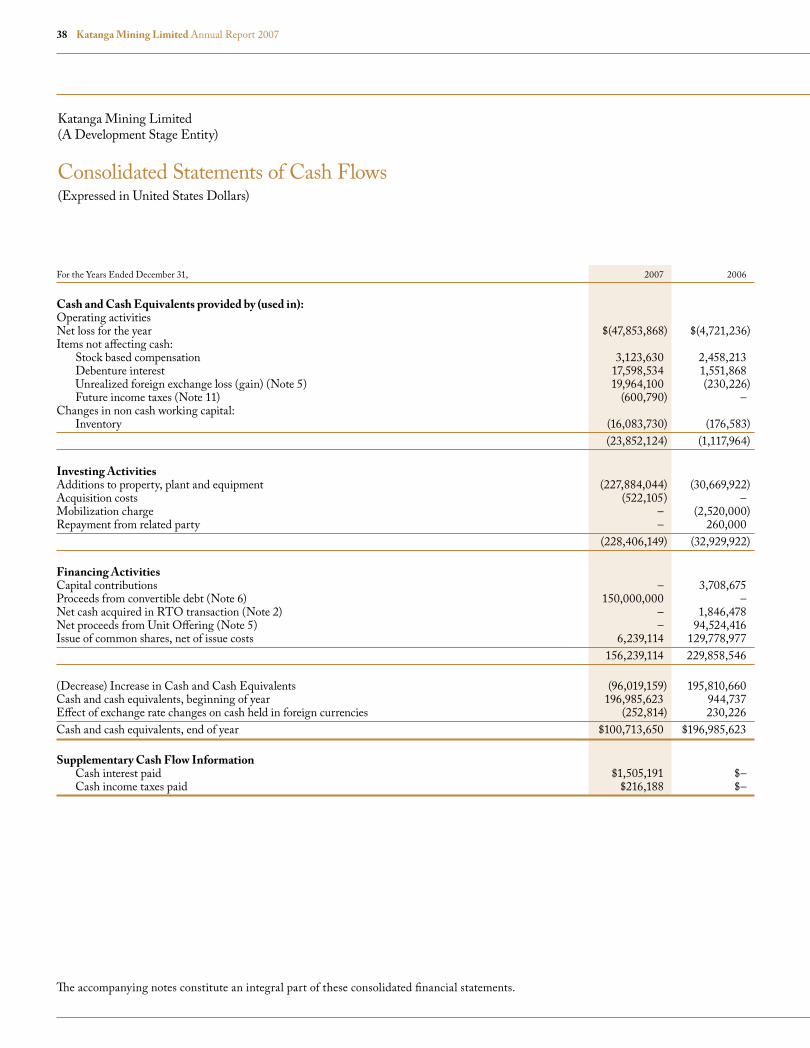

5. Cash Flows Three Months Ended Year Ended

Cash Flows from: December 31, December 31, December 31, December 31, 2007 2006 2007 2006

Operating activities $(13,784,929) $(196,915) $(23,852,124) $(1,117,964)Financing activities $150,000,000 $96,390,902 $156,239,114 $229,858,546Investing Activities $(72,821,727) $(22,168,019) $(228,406,149) $(32,929,922)

2007 and 2006The net operating cash costs for the year ended 2007 were $23,852,124 (2006 – $1,117,964). The majority of the operating expenses were non-cash (as noted in the selected annual financial information). $16,083,730 of operating cash used relates to the build-up of inventory (2006 – $176,583). The remainder relates to the cash costs of head office offset by a realized foreign exchange gain of $1,594,126 (2006 – $670,595).

On May 2, 2006, the Company received aggregate gross proceeds of CDN$ 152,250,000 upon the issuance of a total of 21,000,000 subscription receipts which entitled the holder to acquire one Katanga common share without further consideration. The net proceeds of the issue of these subscription receipts was US $129,407,842. On November 20, 2006 the Company received net proceeds of $94,524,416 upon the issuance of 115,000 unsecured subordinated notes and common share purchase warrants. The additional source of funds in financing activities in 2006 relates to the exercise of warrants and $3,708,675 in capital contributions which were used to fund the feasibility study.

In 2007, $1,210,624 was received upon the exercise of 216,677 options and $5,028,490 upon the exercise of 633,600 warrants. $150,000,000 was received from Glencore upon issuance of convertible debt.

The investing activities for 2006 and 2007 relate mainly to the completion of phase I of the rehabilitation of the site in preparation for commercial production in 2008.

»

»

»

»

»

»

»

»

26 Katanga Mining Limited Annual Report 2007

Management’s Discussion and Analysis continued

Three months ended December 31, 2007 and 2006For the three months ended December 31, 2007, non-cash items in operating expenses included unrealized foreign exchange losses on the debentures of $1,825,181 (2006 – $nil) and $3,772,208 (2006 – $1,551,868) for debenture interest which was paid in January 2008.

For the three months ended December 31, 2007, inventory (in operating activities) increased by $5,883,566 (2006 – $176,583) as a result of the build-up of spares in preparation for commercial production in 2008.

The remainder of the cash expenditures in operating activities relates to head office expenditures.

The financing activities in the three months ended December 31, 2007 relate to the issuance of convertible debt to Glencore. The amount for the three months ended December 31, 2006 relates to the issuance of the unsecured subordinated notes and associated warrants.

Investing activities in the three months ended December 31, 2006 relate to costs incurred on the start of Phase I of the rehabilitation project. For 2007, investing activities relate to similar costs incurred but at a much higher level due to the increase in activity as the Company neared production.

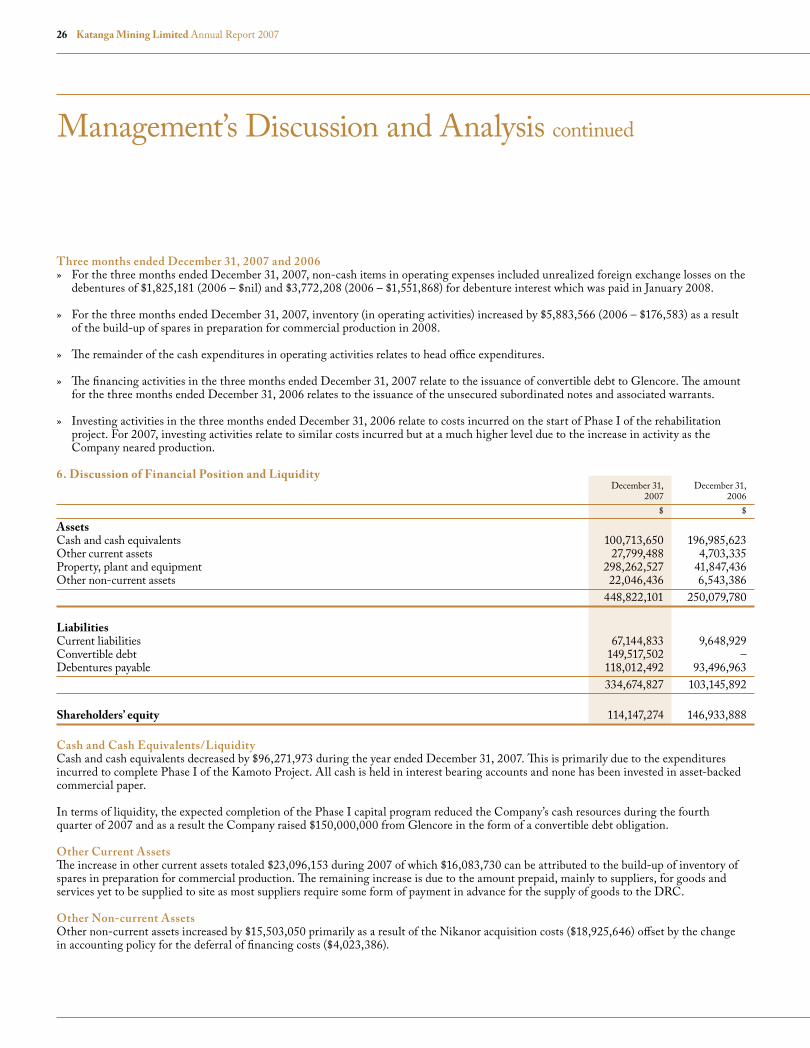

6. Discussion of Financial Position and Liquidity December 31, December 31, 2007 2006

$ $

AssetsCash and cash equivalents 100,713,650 196,985,623Other current assets 27,799,488 4,703,335Property, plant and equipment 298,262,527 41,847,436Other non-current assets 22,046,436 6,543,386

448,822,101 250,079,780

LiabilitiesCurrent liabilities 67,144,833 9,648,929Convertible debt 149,517,502 –Debentures payable 118,012,492 93,496,963

334,674,827 103,145,892

Shareholders’ equity 114,147,274 146,933,888