creating value in mining - itmg.co.id · (usd/ton) 3q12 576 31% 133 120 $87.5 fy11 2,382 37% 707...

TRANSCRIPT

Analyst Briefing

FY12 performance results

4 March 2013

2

The views expressed here contain information derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information. Any forward looking information in this presentation has been prepared on the basis of a number of assumptions which may prove to be incorrect. This presentation should not be relied upon as a recommendation or forecast by PT. Indo Tambangraya Megah Tbk. Nothing in this release should be construed as either an offer to buy or sell or a solicitation of an offer to buy or sell shares in any jurisdiction

3

Appendices

Financial review

Commercial review

Operational review

Introduction

3

4

2

1

4

Highlights of 4Q12 and FY12 results

4Q12

658

24%

105

65

$80.6

Q-Q

+14%

-7%

-21%

-45%

-8%

Unit: US$ Mn

Coal sales 8.2 Mt

Up 1.6 Mt

+24% Q-Q

FY12

2,439

30%

558

432

$90.0

y-y

+2%

-7%

-21%

-21%

-7%

Coal sales 27.2 Mt

Up 2.5 Mt

+10% y-y

Total Revenue

Gross Profit Margin

EBIT

Net income

ASP* (USD/ton)

3Q12

576

31%

133

120

$87.5

FY11

2,382

37%

707

546

$97.1

* Includes bonus /penalty

5

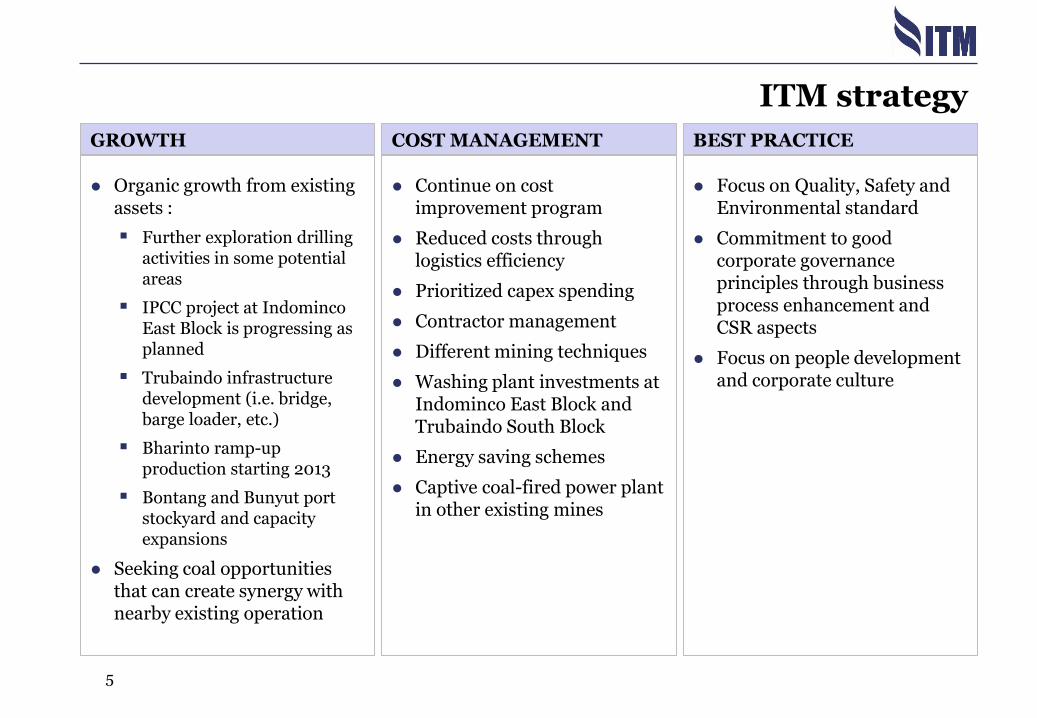

BEST PRACTICE GROWTH COST MANAGEMENT

Organic growth from existing assets :

Further exploration drilling activities in some potential areas

IPCC project at Indominco East Block is progressing as planned

Trubaindo infrastructure development (i.e. bridge, barge loader, etc.)

Bharinto ramp-up production starting 2013

Bontang and Bunyut port stockyard and capacity expansions

Seeking coal opportunities that can create synergy with nearby existing operation

Focus on Quality, Safety and Environmental standard

Commitment to good corporate governance principles through business process enhancement and CSR aspects

Focus on people development and corporate culture

Continue on cost improvement program

Reduced costs through logistics efficiency

Prioritized capex spending

Contractor management

Different mining techniques

Washing plant investments at Indominco East Block and Trubaindo South Block

Energy saving schemes

Captive coal-fired power plant in other existing mines

ITM strategy

2012 review : strengthening the core

• Indominco: Lowered SR to 12.0x from 12.6x in FY11

• Continued process on port loading capacity expansion

• Completed IPCC feasibility study as part of cost reduction program

• Capex postponement and rationalization

• Obtained gold medal award at Indonesia Fire Rescue Challenge (IFRC)

• Td. Mayang: passed TPM3 Excellence Award level 4

INDOMINCO – TD. MAYANG

• Trubaindo: ramped up production from 7.1 mt to 7.7 mt

• Shortened distance to dump area

• Capex postponement and rationalization

• Bharinto: first coal sales in 3Q12

• Completed Bharinto hauling road

TRUBAINDO - BHARINTO

• Embalut: optimized mining reserves

• Jorong: finalized mine closure master plan

EMBALUT - JORONG

• Overhead cost reduction

• Maintain dividend payout ratio

JAKARTA OFFICE

6

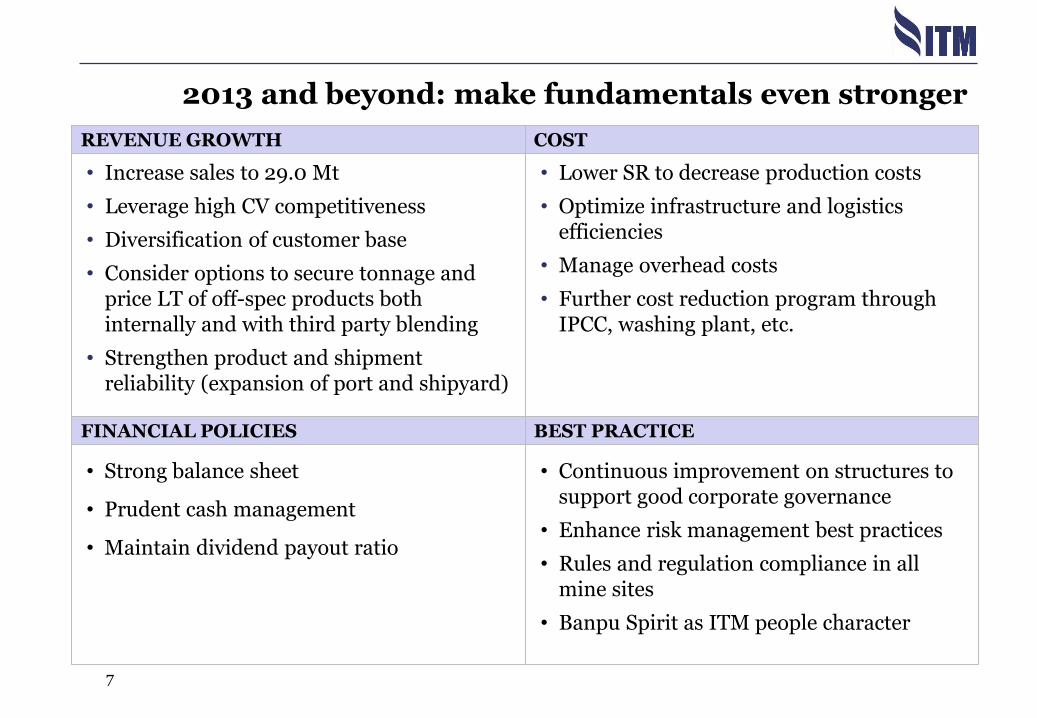

2013 and beyond: make fundamentals even stronger

• Lower SR to decrease production costs

• Optimize infrastructure and logistics efficiencies

• Manage overhead costs

• Further cost reduction program through IPCC, washing plant, etc.

• Increase sales to 29.0 Mt

• Leverage high CV competitiveness

• Diversification of customer base

• Consider options to secure tonnage and price LT of off-spec products both internally and with third party blending

• Strengthen product and shipment reliability (expansion of port and shipyard)

• Continuous improvement on structures to support good corporate governance

• Enhance risk management best practices

• Rules and regulation compliance in all mine sites

• Banpu Spirit as ITM people character

• Strong balance sheet

• Prudent cash management

• Maintain dividend payout ratio

7

COST REVENUE GROWTH

BEST PRACTICE FINANCIAL POLICIES

2012 vs 2013 operation summary

4Q11 1Q12 2Q12 3Q12 4Q12 1Q13

Units: Mt

7.2

5.7

Indominco

Trubaindo

Bharinto

Kitadin

Jorong

INDICATIVE OUTPUT TARGETS*

4Q11 1Q12 2Q12 3Q12 4Q12

0

5

10

15

20

25

30

35

2012 2013e 2014e 2015e 2016e

Units: Mt

Indominco

Trubaindo

Bharinto

Kitadin Jorong

* Not including inorganic growth. Note: These output targets are indicative only and are subject to change

6.8 7.0 8.0

East Kalimantan

Balikpapan

Palangkaraya

Banjarmasin

Central Kalimantan

South Kalimantan

Samarinda

Trubaindo

Bharinto

Jorong

Embalut

Indominco

Td.Mayang

1Q13e

6.7

QUARTERLY OUTPUT FY12 OUTPUT: 27.5Mt FY13 TARGET: 29.0Mt

2012 2013e

14.8 14.8

2012 2013e

7.7 7.7

2012 2013e

0.3 1.9

2012 2013e

1.2 1.2 1.2

2012 2013e

1.3 1.0

2012 2013e

2.2 2.4

8

9

Appendices

Financial review

Commercial review

Operational review

Introduction

3

4

2

1

10

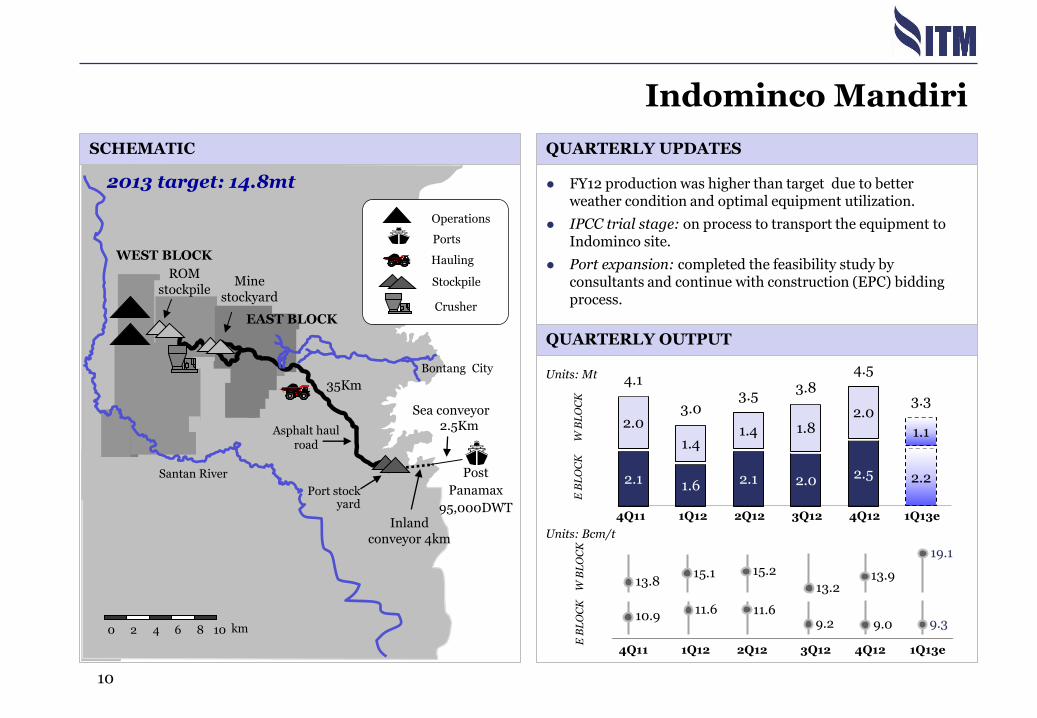

FY12 production was higher than target due to better weather condition and optimal equipment utilization.

IPCC trial stage: on process to transport the equipment to Indominco site.

Port expansion: completed the feasibility study by consultants and continue with construction (EPC) bidding process.

QUARTERLY UPDATES

Indominco Mandiri

SCHEMATIC

EAST BLOCK

Santan River Port stock

yard

Bontang City

Asphalt haul road

2.5Km

35Km

Sea conveyor

Mine stockyard

Inland conveyor 4km

0 10 6 8 2 km 4

WEST BLOCK

Operations

Stockpile

Ports

Hauling

Crusher

ROM stockpile

Post

Panamax

95,000DWT

2013 target: 14.8mt

E B

LO

CK

W

BL

OC

K

E B

LO

CK

W

BL

OC

K

2.1 1.6 2.1 2.0 2.5 2.2

2.0

1.4 1.4 1.8

2.0

1.1

4.1

3.0 3.5

3.8

4.5

3.3

Units: Mt

Units: Bcm/t

4Q11 1Q12 2Q12 3Q12 4Q12 1Q13e

10.9

13.8

11.6

15.1 15.2

11.6

13.2

9.2

4Q11 1Q12 2Q12 3Q12 4Q12 1Q13e

13.9

9.0

19.1

9.3

QUARTERLY OUTPUT

11

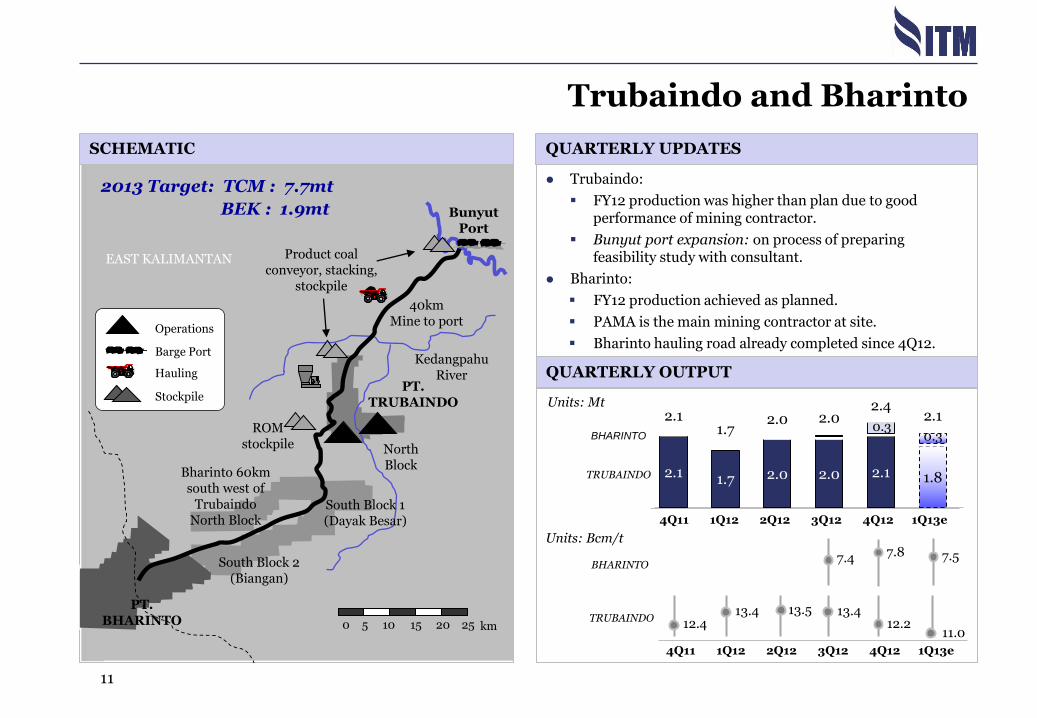

Trubaindo:

FY12 production was higher than plan due to good performance of mining contractor.

Bunyut port expansion: on process of preparing feasibility study with consultant.

Bharinto:

FY12 production achieved as planned.

PAMA is the main mining contractor at site.

Bharinto hauling road already completed since 4Q12.

QUARTERLY UPDATES

Trubaindo and Bharinto

SCHEMATIC

QUARTERLY OUTPUT

Mahakam River

South Block 1 (Dayak Besar)

North Block

40km Mine to port

Kedangpahu River

ROM stockpile

Bunyut Port

0 10 25 15 20 5 km

Product coal conveyor, stacking,

stockpile

EAST KALIMANTAN

Bharinto 60km south west of

Trubaindo North Block

South Block 2 (Biangan)

PT. BHARINTO

PT. TRUBAINDO

Operations

Stockpile

Hauling

Barge Port

2013 Target: TCM : 7.7mt

BEK : 1.9mt

2.1 1.7 2.0 2.0 2.1 1.8

2.1 1.7

2.0 2.0 2.4

2.1

TRUBAINDO 12.4 13.4 13.5

TRUBAINDO

BHARINTO

13.4

Units: Mt

Units: Bcm/t

12.2

BHARINTO 7.4 7.8

4Q11 1Q12 2Q12 3Q12 4Q12 1Q13e

0.3

4Q11 1Q12 2Q12 3Q12 4Q12 1Q13e

11.0

7.5

0.3

12

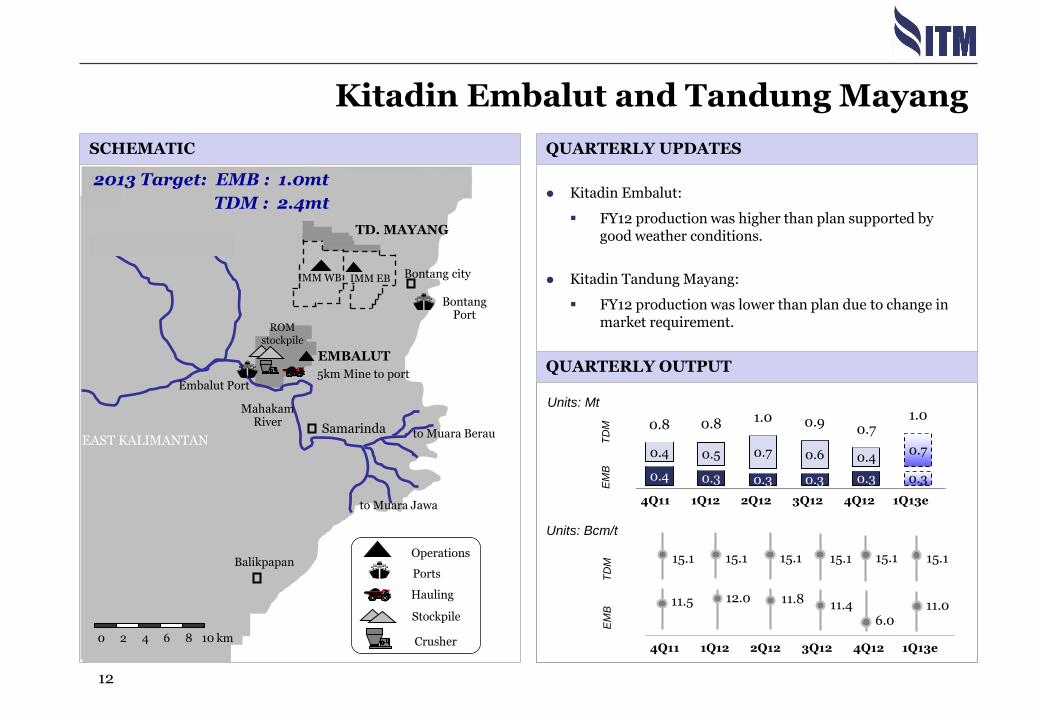

Kitadin Embalut:

FY12 production was higher than plan supported by good weather conditions.

Kitadin Tandung Mayang:

FY12 production was lower than plan due to change in market requirement.

QUARTERLY UPDATES

Kitadin Embalut and Tandung Mayang

SCHEMATIC

QUARTERLY OUTPUT

0.4 0.3 0.3 0.3 0.3 0.3

0.4 0.5 0.7 0.6 0.4 0.7

0.8 0.8 1.0 0.9 0.7

1.0

Balikpapan

Mahakam River

Samarinda to Muara Berau

Bontang city

EMBALUT

Embalut Port

to Muara Jawa

ROM stockpile

Operations

Stockpile

Ports

Hauling

Crusher 0 10 6 8 2 km 4

5km Mine to port

TD. MAYANG

EAST KALIMANTAN

IMM EB IMM WB

Bontang Port

TDM : 2.4mt

11.5 12.0 11.8 T

DM

E

MB

E

MB

T

DM

15.1 15.1 15.1

11.4

15.1

Units: Mt

Units: Bcm/t

6.0

15.1

4Q11 1Q12 2Q12 3Q12 4Q12 1Q13e

4Q11 1Q12 2Q12 3Q12 4Q12 1Q13e

11.0

15.1

2013 Target: EMB : 1.0mt

Coal terminal

Jorong

Pelaihari

Pacific Ocean

Haul road

0 10 25 15 20 5 km

20km

Operations

Stockpile

Hauling

Barge Port

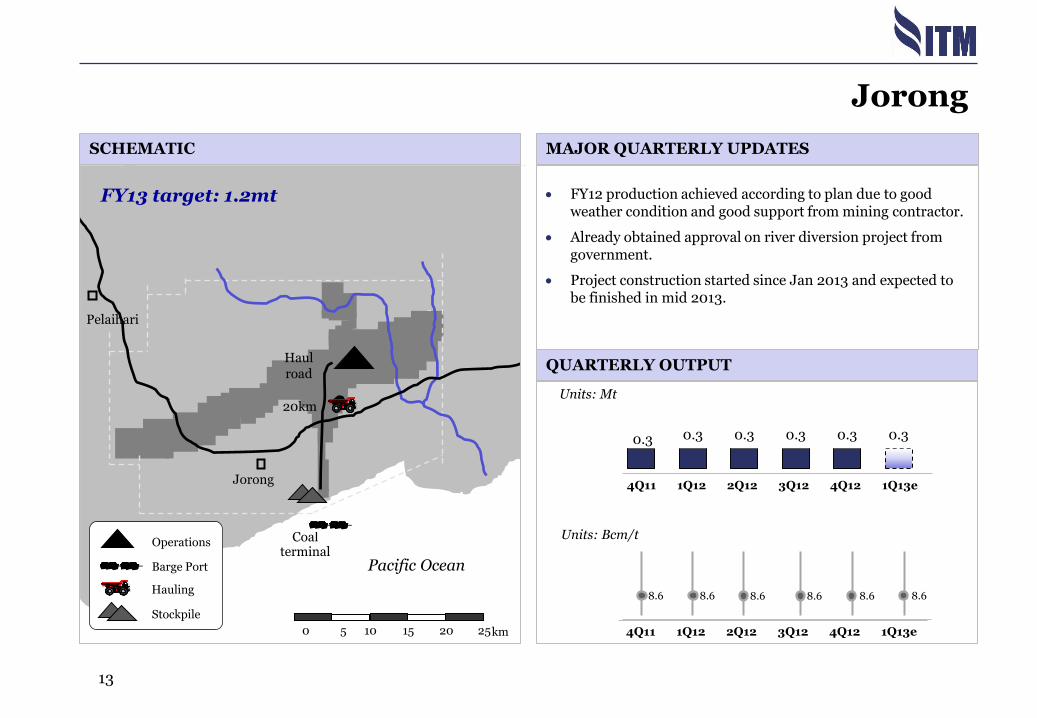

FY13 target: 1.2mt

MAJOR QUARTERLY UPDATES

13

Jorong

FY12 production achieved according to plan due to good weather condition and good support from mining contractor.

Already obtained approval on river diversion project from government.

Project construction started since Jan 2013 and expected to be finished in mid 2013.

SCHEMATIC

QUARTERLY OUTPUT

8.6 8.6 8.6 8.6 8.6 8.6

Units: Mt

Units: Bcm/t

4Q11 1Q12 2Q12 3Q12 4Q12 1Q13e

4Q11 1Q12 2Q12 3Q12 4Q12 1Q13e

0.3 0.3 0.3 0.3 0.3 0.3

14

Appendices

Financial review

Commercial review

Operational review

Introduction

3

4

2

1

15

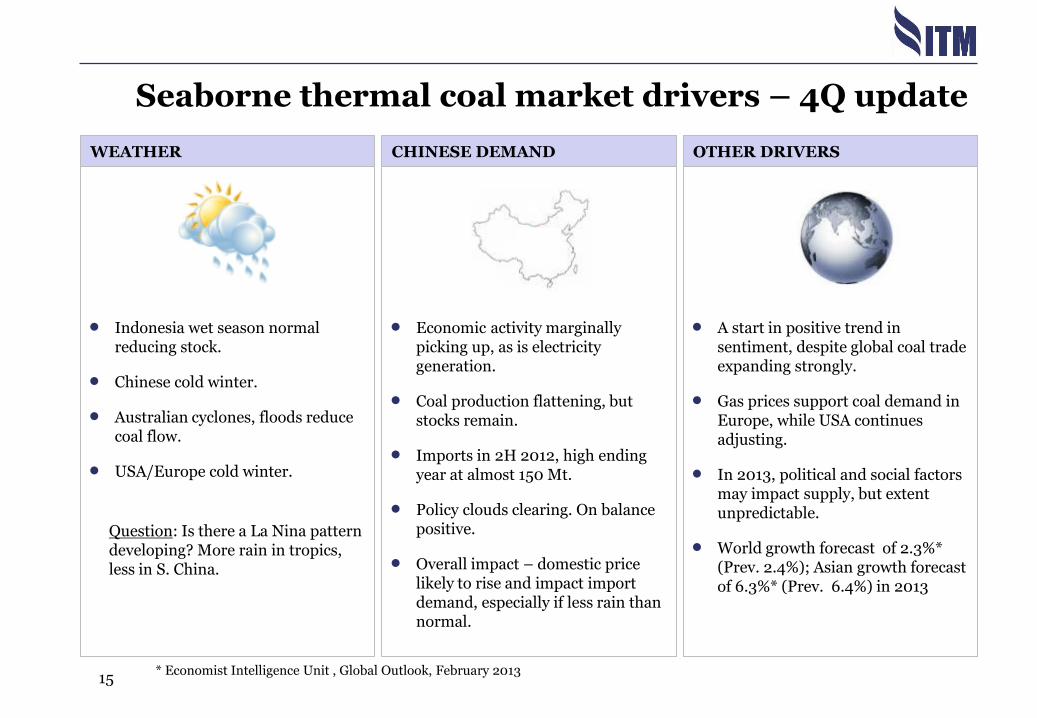

OTHER DRIVERS WEATHER CHINESE DEMAND

Indonesia wet season normal reducing stock.

Chinese cold winter.

Australian cyclones, floods reduce coal flow.

USA/Europe cold winter.

Question: Is there a La Nina pattern developing? More rain in tropics, less in S. China.

A start in positive trend in sentiment, despite global coal trade expanding strongly.

Gas prices support coal demand in Europe, while USA continues adjusting.

In 2013, political and social factors may impact supply, but extent unpredictable.

World growth forecast of 2.3%* (Prev. 2.4%); Asian growth forecast of 6.3%* (Prev. 6.4%) in 2013

Economic activity marginally picking up, as is electricity generation.

Coal production flattening, but stocks remain.

Imports in 2H 2012, high ending year at almost 150 Mt.

Policy clouds clearing. On balance positive.

Overall impact – domestic price likely to rise and impact import demand, especially if less rain than normal.

Seaborne thermal coal market drivers – 4Q update

* Economist Intelligence Unit , Global Outlook, February 2013

16

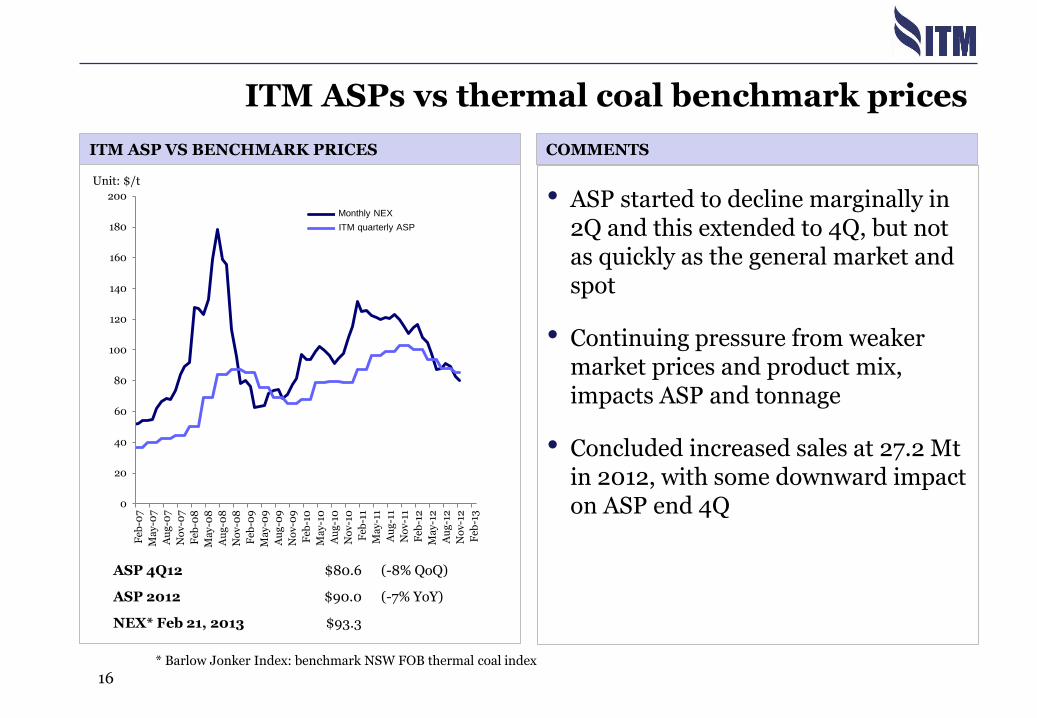

ITM ASPs vs thermal coal benchmark prices

ITM ASP VS BENCHMARK PRICES

* Barlow Jonker Index: benchmark NSW FOB thermal coal index

ASP 4Q12 $80.6 (-8% QoQ)

ASP 2012 $90.0 (-7% YoY)

NEX* Feb 21, 2013 $93.3

Unit: $/t

COMMENTS

0

20

40

60

80

100

120

140

160

180

200

Feb

-07

Ma

y-0

7

Au

g-0

7

No

v-0

7

Feb

-08

Ma

y-0

8

Au

g-0

8

No

v-0

8

Feb

-09

Ma

y-0

9

Au

g-0

9

No

v-0

9

Feb

-10

Ma

y-1

0

Au

g-1

0

No

v-1

0

Feb

-11

Ma

y-1

1

Au

g-1

1

No

v-1

1

Feb

-12

Ma

y-1

2

Au

g-1

2

No

v-1

2

Feb

-13

Monthly BJI

Quarterly Banpu Indonesia ASP

• ASP started to decline marginally in 2Q and this extended to 4Q, but not as quickly as the general market and spot

• Continuing pressure from weaker market prices and product mix, impacts ASP and tonnage

• Concluded increased sales at 27.2 Mt in 2012, with some downward impact on ASP end 4Q

Monthly NEX

ITM quarterly ASP

17

655

620

530

400

500

600

700

800

900

1,000

Feb

-11

Ma

y-1

1

Au

g-1

1

No

v-1

1

Feb

-12

Ma

y-1

2

Au

g-1

2

No

v-1

2

Feb

-13

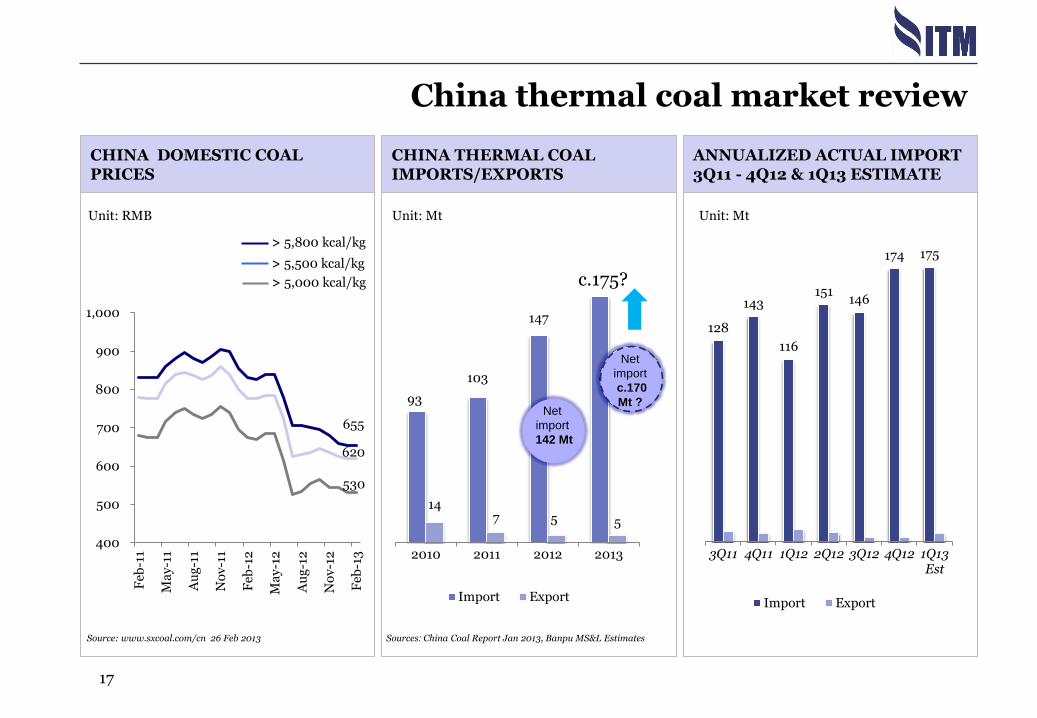

ANNUALIZED ACTUAL IMPORT 3Q11 - 4Q12 & 1Q13 ESTIMATE

CHINA DOMESTIC COAL PRICES

CHINA THERMAL COAL IMPORTS/EXPORTS

China thermal coal market review

Source: www.sxcoal.com/cn 26 Feb 2013

Unit: RMB

> 5,800 kcal/kg

> 5,500 kcal/kg

> 5,000 kcal/kg

Sources: China Coal Report Jan 2013, Banpu MS&L Estimates

Unit: Mt Unit: Mt

93

103

147

14 7 5 5

2010 2011 2012 2013

Import Export

Net

import

142 Mt

Net

import

c.170

Mt ?

c.175?

128

143

116

151 146

174 175

3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13Est

Import Export

COAL SALES 2012

18

ITM coal sales 2012

COAL SALES BREAKDOWN BY DESTINATION

JAPAN 4.5 Mt

PHILIPPINES 1.6 Mt

THAILAND 1.8 Mt

INDIA 3.3 Mt

HK 0.6 Mt

S KOREA 1.5 Mt CHINA

7.1 Mt

TAIWAN 2.3 Mt

ITALY 1.4 Mt

1.5

INDONESIA 2.5 Mt

MALAYSIA 0.4 Mt

OTHERS 0.1 Mt

26%

16%

12%

9%

8%

7%

6%

6%

5% 2% 2%

Total Coal Sales: 27.2 Mt

Japan

China

Taiwan

S Korea

Italy

Thailand

Philippines

Hong Kong

India

Indonesia

Malaysia Others 1%

44%

24%

9%

23%

19

Indicative coal sales 2013

COAL SALES CONTRACT AND PRICING STAUTS

Contract Status Price Status

Fixed

Index

Unpriced

Unsold

TARGET SALES 2013: 29.0 Mt

77%

23%

Contracted

Uncontracted

20

Appendices

Financial review

Commercial review

Operational review

Introduction

3

4

2

1

21

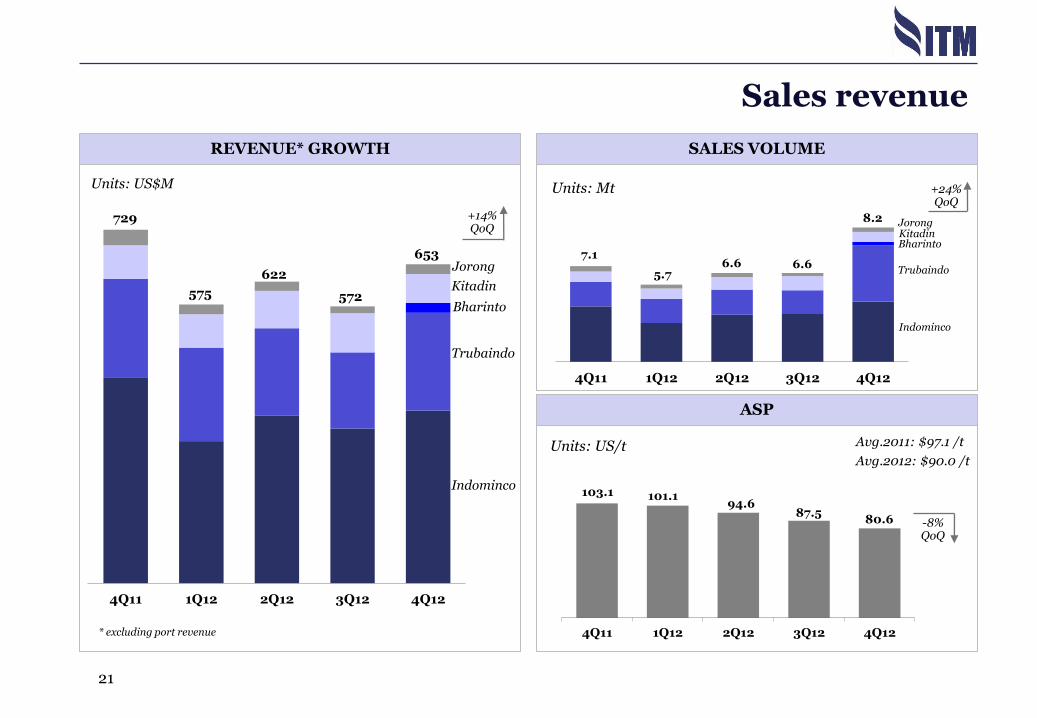

SALES VOLUME

Sales revenue

REVENUE* GROWTH

ASP

4Q11 1Q12 2Q12 3Q12 4Q12

Units: US$M

+14% QoQ

Indominco

Trubaindo

Jorong

Kitadin

Bharinto

4Q11 1Q12 2Q12 3Q12 4Q12

Units: Mt

Indominco

Trubaindo

Jorong Kitadin Bharinto

+24% QoQ

Units: US/t

4Q11 1Q12 2Q12 3Q12 4Q12

-8% QoQ

* excluding port revenue

729

575

622

572

653

103.1 101.1 94.6

87.5 80.6

7.1

5.7 6.6 6.6

8.2

Avg.2011: $97.1 /t

Avg.2012: $90.0 /t

22

Average gross margin

Revenue

GPM* (%)

Units: US$M

Indominco Trubaindo Kitadin Jorong

28% 19%

4Q11

512

28%

242

39%

93

46%

38

390

22%

3Q12

188

28%

103

35% 17

16%

Bharinto

19%

427

19%

4Q12

242

19%

72

31%

24

19%

24

0 2

ITM Consolidated

4Q11 3Q12

733

39%

4Q12

576

31%

658

24%

4Q11 3Q12 4Q12 4Q11 3Q12 4Q12 4Q11 3Q12 4Q12 4Q11 3Q12 4Q12

17% 23%

23

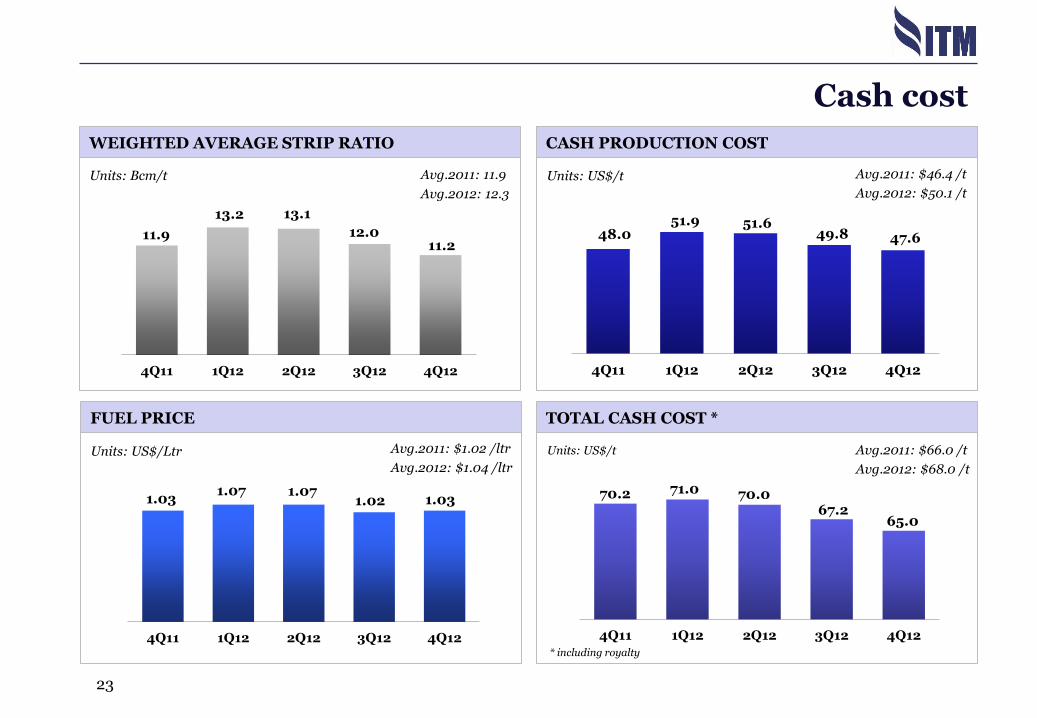

Cash cost

4Q11 1Q12 2Q12 3Q12 4Q12

Units: US$/t

* including royalty

4Q11 1Q12 2Q12 3Q12 4Q12

Units: US$/Ltr

4Q11 1Q12 2Q12 3Q12 4Q12

Units: Bcm/t

4Q11 1Q12 2Q12 3Q12 4Q12

Units: US$/t

WEIGHTED AVERAGE STRIP RATIO CASH PRODUCTION COST

TOTAL CASH COST *

FUEL PRICE

48.0 51.9

11.9

13.2

1.03 1.07 70.2 71.0

13.1

1.07

51.6

70.0 1.02

12.0 49.8

67.2

11.2

1.03

47.6

65.0

Avg.2011: 11.9

Avg.2012: 12.3

Avg.2011: $1.02 /ltr

Avg.2012: $1.04 /ltr

Avg.2011: $46.4 /t

Avg.2012: $50.1 /t

Avg.2011: $66.0 /t

Avg.2012: $68.0 /t

24

EBITDA CONSOLIDATED

*COGS = Prod cost + Transport cost + Inv. movement

Units: US$M

Revenue 3Q12 4Q11 4Q12

148.5

COGS Selling Royalty Admin

120.6 (16.3)

+82.1

-19% QoQ

(10.5)

Higher Volume by 24% Lower ASP by 8%

(83.6)

234.6

+0.4

MINE BY MINE

Units: US$M

125.6

65.5

44.3

75.8

36.6 37.3

71.6

23.1 27.9

0.8 (0.2) 0.5

Indominco Trubaindo 4Q11

Kitadin Jorong 3Q12 4Q12

Bharinto

3.7 2.0 3.5

4Q11 3Q12 4Q12 4Q11 3Q12 4Q12 4Q11 3Q12 4Q12 4Q11 3Q12 4Q12

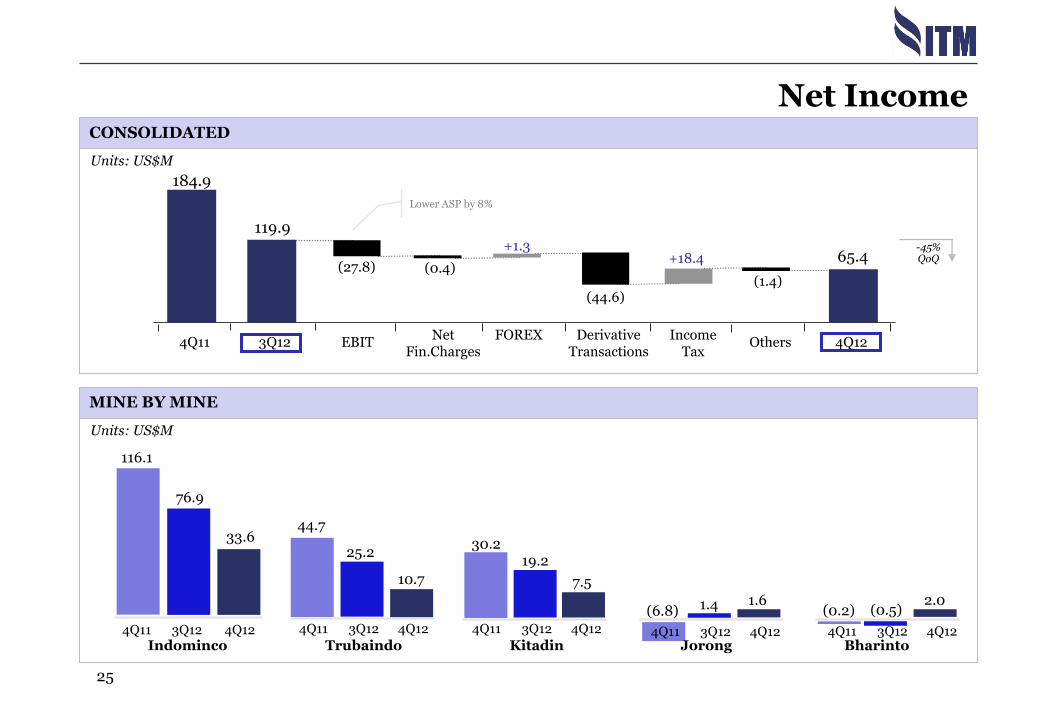

116.1

30.2

44.7

25.2 19.2

1.4

33.6

10.7 7.5

1.6

76.9

(6.8) (0.5) 2.0

(0.2)

25

Net Income CONSOLIDATED

184.9

65.4 -45% QoQ

119.9

(27.8) (1.4)

Lower ASP by 8%

Units: US$M

MINE BY MINE

Units: US$M

3Q12 4Q12 Others EBIT Income

Tax Derivative

Transactions FOREX Net

Fin.Charges 4Q11

Indominco Trubaindo Kitadin Jorong Bharinto

(0.4)

+1.3

(44.6)

+18.4

4Q11 3Q12 4Q12 4Q11 3Q12 4Q12 4Q11 3Q12 4Q12 4Q11 3Q12 4Q12 4Q11 3Q12 4Q12

26

CASH POSITION

Net Market Gearing (%)

Net D/E (times)

(0.34)

(34%)

(0.47)

(44%)

(0.57)

(57%)

(0.41)

(41%)

2008 2009 2011 2010 2012

(0.46)

(46%)

Balance sheet

KEY RATIOS

DEBT POSITION

Units: US$M

2008

222

2009

429

2011

612

295

2010 2012

461

Units: US$M

2008

11 55

2009

0

2011

0

2010

0

2012

27

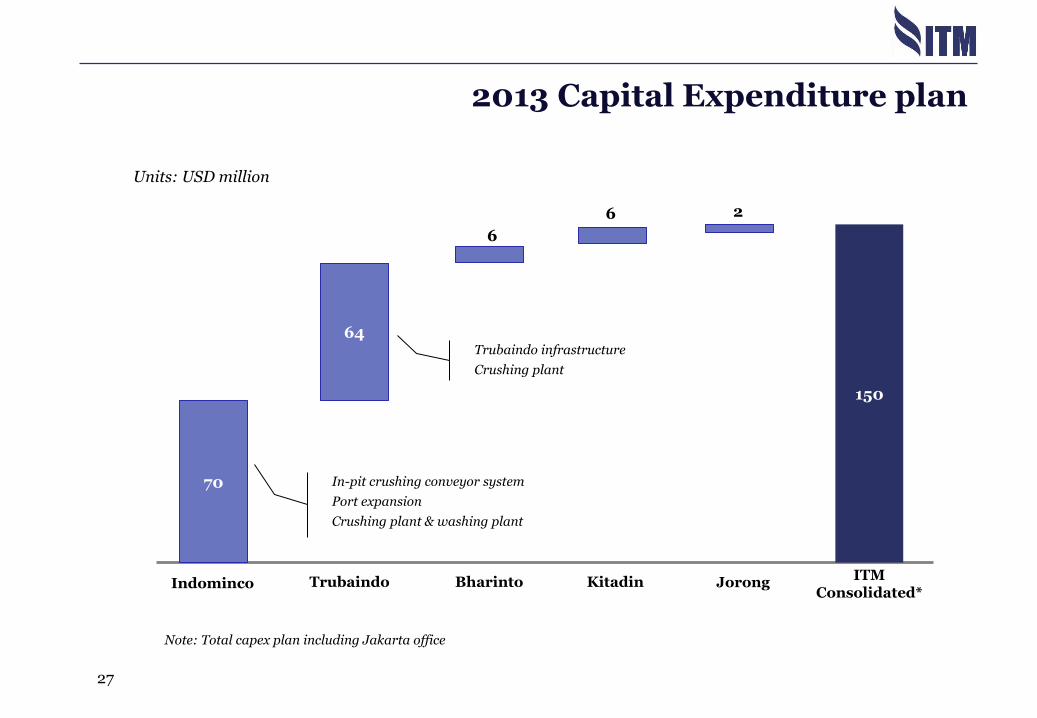

2013 Capital Expenditure plan

Note: Total capex plan including Jakarta office

Units: USD million

Indominco Trubaindo Bharinto Kitadin Jorong ITM

Consolidated*

150

64

70

2

In-pit crushing conveyor system

Port expansion

Crushing plant & washing plant

Trubaindo infrastructure

Crushing plant

6

6

28

Appendices

29

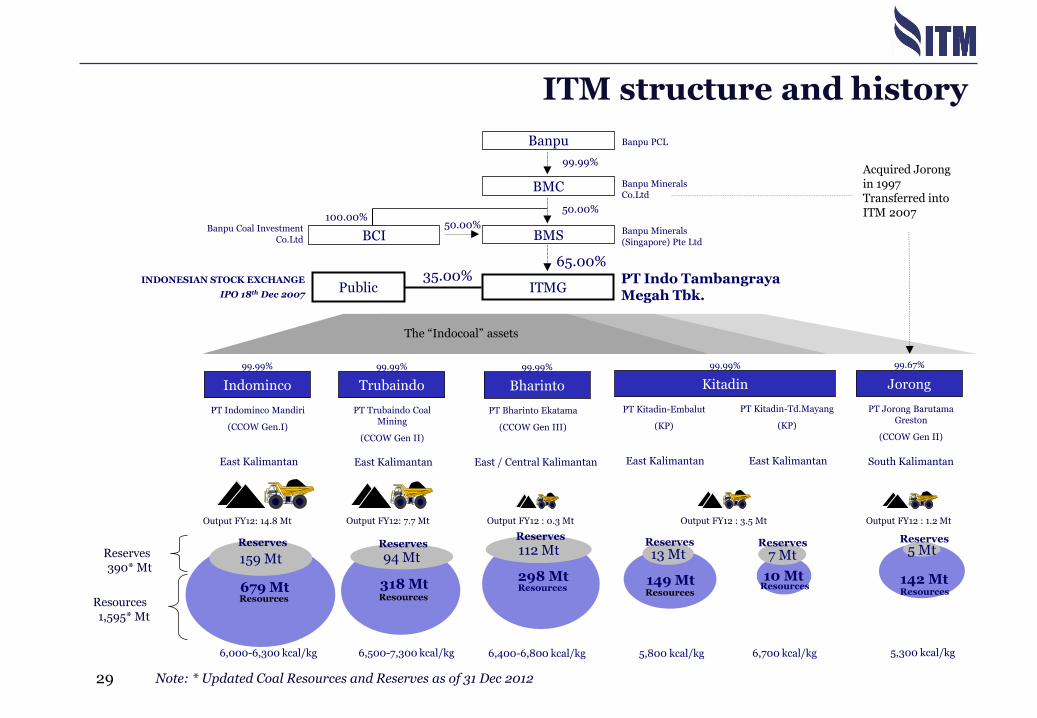

ITM structure and history

Note: * Updated Coal Resources and Reserves as of 31 Dec 2012

ITMG

65.00%

Indominco Trubaindo Jorong

PT Indominco Mandiri

(CCOW Gen.I)

PT Trubaindo Coal Mining

(CCOW Gen II)

PT Kitadin-Embalut

(KP)

PT Jorong Barutama Greston

(CCOW Gen II)

50.00%

PT Indo Tambangraya Megah Tbk.

Banpu Minerals (Singapore) Pte Ltd

99.99% 99.99% 99.99% 99.67%

Banpu Minerals Co.Ltd

Reserves 390* Mt

Resources 1,595* Mt

BMS

99.99%

BMC

Banpu PCL Banpu

Public 35.00%

Kitadin

PT Kitadin-Td.Mayang

(KP)

BCI 50.00%

100.00% Banpu Coal Investment

Co.Ltd

East Kalimantan East Kalimantan South Kalimantan East Kalimantan

INDONESIAN STOCK EXCHANGE

IPO 18th Dec 2007

6,500-7,300 kcal/kg 6,000-6,300 kcal/kg 5,800 kcal/kg 6,700 kcal/kg 5,300 kcal/kg

Acquired Jorong in 1997 Transferred into ITM 2007

Output FY12: 14.8 Mt Output FY12: 7.7 Mt Output FY12 : 3.5 Mt Output FY12 : 1.2 Mt

Bharinto

PT Bharinto Ekatama

(CCOW Gen III)

99.99%

East / Central Kalimantan

6,400-6,800 kcal/kg

Output FY12 : 0.3 Mt

The “Indocoal” assets

East Kalimantan

159 Mt

679 Mt Resources

Reserves

94 Mt

318 Mt Resources

Reserves 13 Mt

149 Mt Resources

Reserves 112 Mt

298 Mt Resources

Reserves

5 Mt

142 Mt Resources

Reserves

7 Mt

10 Mt Resources

Reserves

30

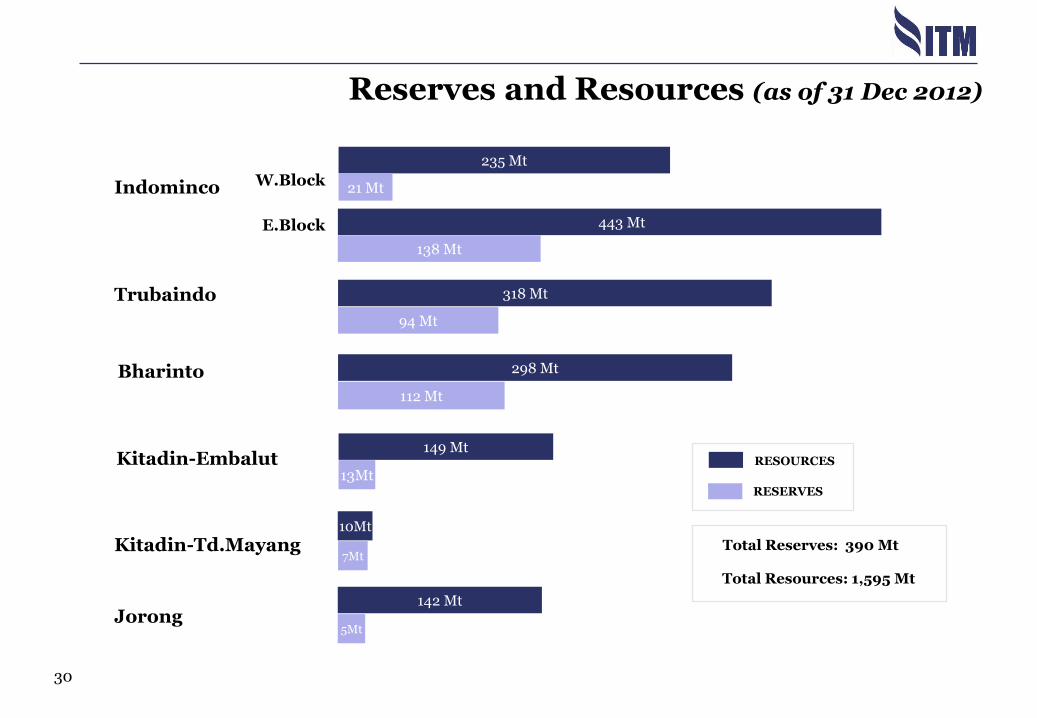

Reserves and Resources (as of 31 Dec 2012)

Indominco

Trubaindo

Kitadin-Td.Mayang

Jorong

W.Block

E.Block

235 Mt

21 Mt

443 Mt

149 Mt

13Mt

142 Mt

5Mt

318 Mt

94 Mt

298 Mt

112 Mt

10Mt

RESOURCES

RESERVES

Kitadin-Embalut

Total Reserves: 390 Mt

Total Resources: 1,595 Mt

138 Mt

7Mt

Bharinto

31

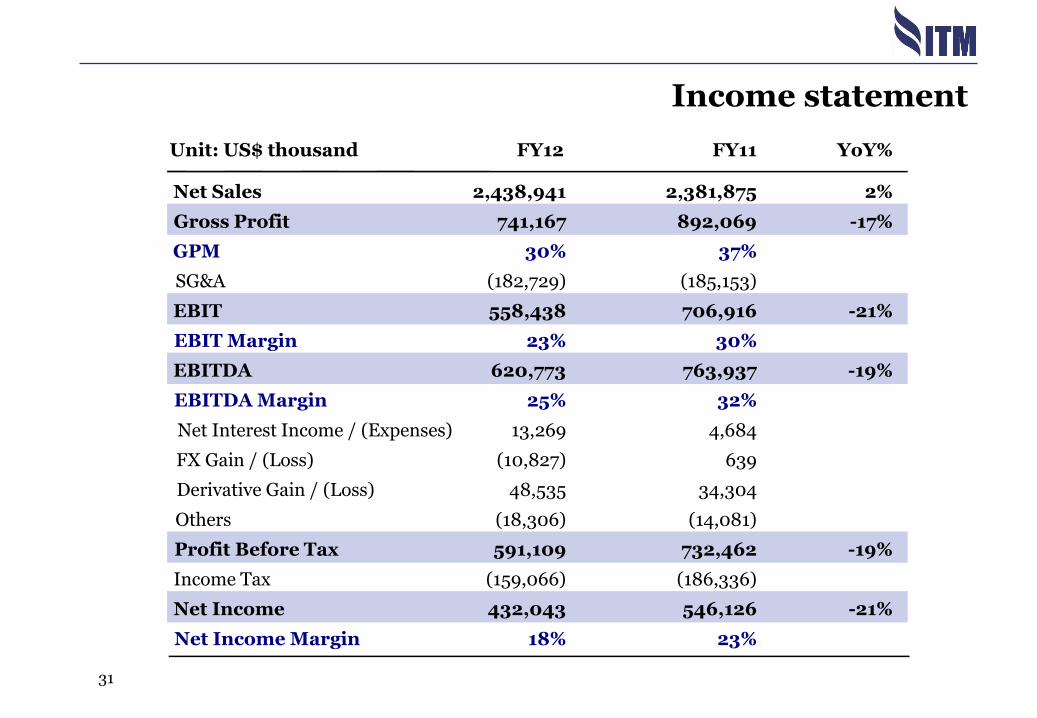

Income statement

Unit: US$ thousand FY12 FY11 YoY%

Net Sales 2,438,941 2,381,875 2%

Gross Profit 741,167 892,069 -17%

GPM 30% 37%

SG&A (182,729) (185,153)

EBIT 558,438 706,916 -21%

EBIT Margin 23% 30%

EBITDA 620,773 763,937 -19%

EBITDA Margin 25% 32%

Net Interest Income / (Expenses) 13,269 4,684

FX Gain / (Loss) (10,827) 639

Derivative Gain / (Loss) 48,535 34,304

Others (18,306) (14,081)

Profit Before Tax 591,109 732,462 -19%

Income Tax (159,066) (186,336)

Net Income 432,043 546,126 -21%

Net Income Margin 18% 23%

32

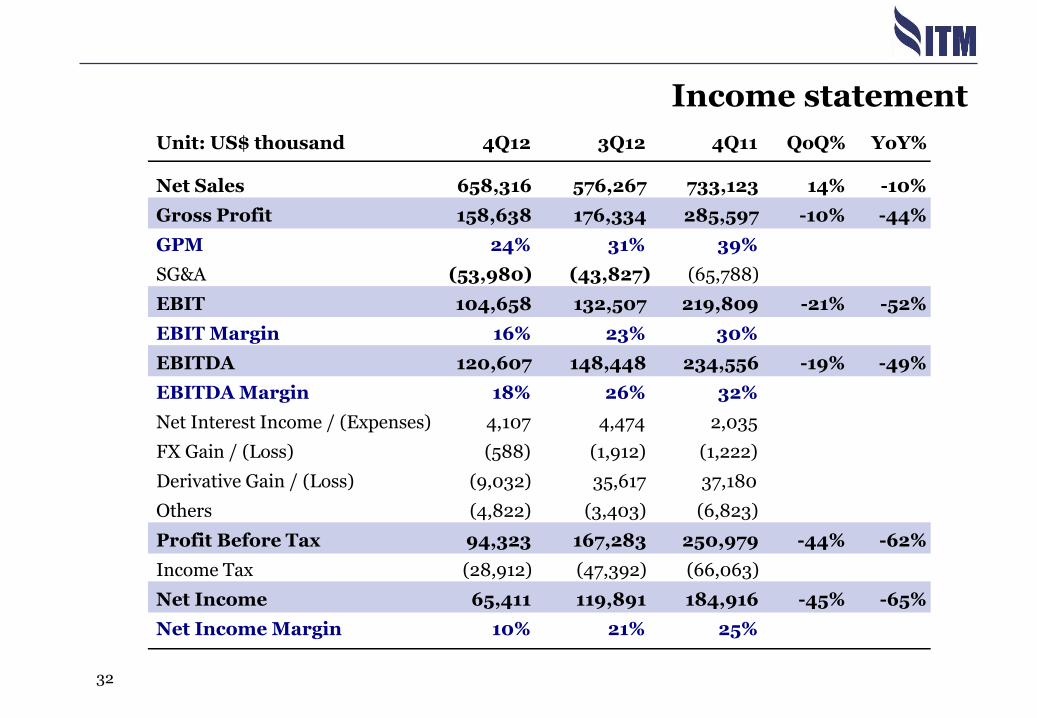

Unit: US$ thousand 4Q12 3Q12 4Q11 QoQ% YoY%

Net Sales 658,316 576,267 733,123 14% -10%

Gross Profit 158,638 176,334 285,597 -10% -44%

GPM 24% 31% 39%

SG&A (53,980) (43,827) (65,788)

EBIT 104,658 132,507 219,809 -21% -52%

EBIT Margin 16% 23% 30%

EBITDA 120,607 148,448 234,556 -19% -49%

EBITDA Margin 18% 26% 32%

Net Interest Income / (Expenses) 4,107 4,474 2,035

FX Gain / (Loss) (588) (1,912) (1,222)

Derivative Gain / (Loss) (9,032) 35,617 37,180

Others (4,822) (3,403) (6,823)

Profit Before Tax 94,323 167,283 250,979 -44% -62%

Income Tax (28,912) (47,392) (66,063)

Net Income 65,411 119,891 184,916 -45% -65%

Net Income Margin 10% 21% 25%

Income statement

33

2012 operating cost

2012 AVERAGE OPERATING COSTS

0

10

20

30

40

50

60

70

80

1Q12 2Q12 3Q12 4Q12 FULL YEAR

Mining and contractor cost

* Coal transportations, repair and maintenance, salaries and allowance, etc.

$74 $72

$69 $70

$/t

$67

Other production costs*

Depreciation & Amortization

SG&A expenses

Royalty

34

SALES VOLUME

Sales revenue

REVENUE* GROWTH

ASP

2008 2009 2010 2011 20122008 2009 2010

Units: US$M

2011

* excluding port revenue

2012

1,291

1,494

1,635

+2% YoY

2,370 2,422

Indominco

Trubaindo

Jorong

Kitadin

Bharinto

2008 2009 2010 2011 2012

Units: Mt

Indominco

Trubaindo

Jorong

Kitadin Bharinto

17.7

21.0 22.2

24.7

27.2 +10% YoY

2008 2009 2010 2011 2012

Units: US/t

2008 2009 2010 2011 2012

73.9

-7% YoY

71.5 74.9

97.1 90.0

2008 2009 2010 2011 2012