critical appraisal of prospects of micro … appraisal of ... the light of financial sector reforms...

TRANSCRIPT

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

107

CRITICAL APPRAISAL OF PROSPECTS OF MICRO

FINANCE -A CASE STUDY OF UDAIPUR

YOGITA WAGH, DR HINA KHAN

HYDERABAD

ANDHRA PRADESH

INDIA

______________________________________________________________________________

ABSTRACT

The growth of microfinance in India has also to be seen in the light of financial sector reforms in

India starting from 1991 and the global emphasis on commercialization of the sector. The

financial sector reforms in India have focused on fostering a market based financial system by

increasing competition and improving the quality of financial services. The new approach has

been deeply influenced by the reorientation among international rural financial policy makers

centering on concepts such as self-help, self sustained growth and institutional viability. This

study is an small attempt to study the pattern of growth of Micro Finance in Udaipur for period

(2001-2010).to document the problems and prospects of Micro Finance, to explore how far MFIs

in Udaipur have been successful in strengthening the formal financial system in the process of

nurturing rural poor and to identify & evaluate the level of satisfaction of customers.

KEYWORDS: Financial inclusion, IFAD, Microfinance, MFIs, NABARD, ROSCA’s, RMK.

Introduction: The proposed Microfinance Services Regulation Bill defines microfinance eservices as

“providing financial assistance to an individual or an eligible client, either directly or through a

group mechanism for:

1) An amount, not exceeding rupees fifty thousand in aggregate per individual, for small and tiny

enterprise, agriculture, allied activities (including for consumption purposes of such individual)

or

2) An amount not exceeding rupees one lakh fifty thousand in aggregate per individual for

housing purposes, or

3) Such other amounts, for any of the purposes mentioned at items (i) and (ii) above or other

purposes, as may be prescribed.”

The poor, like the rest of society, need financial products and services to build

assets, stabilize consumption and protect themselves against risks. Microfinance serves as the

last-mile bridge to the low-income population excluded from the traditional financial services

system and seeks to fill this gap and alleviate poverty. Microfinance loans serve the low-income

population in multiple ways by: (1) providing working capital to build businesses; (2) infusing

credit to smooth cash flows and mitigate irregularity in accessing food, clothing, shelter, or

education; and (3) cushioning the economic impact of shocks such as illness, theft, or natural

disasters.

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

108

Micro Finance Institutions:

An organization or association of individuals including the following if it is established for the

purpose of carrying on the business of extending microfinance services:

1) A society registered under the Societies Registration Act, 1860,

2) A trust created under the Indian Trust Act, 1880 or public trust registered under any State

enactment governing trust or public, religious or charitable purposes,

3) A cooperative society / mutual benefit society / mutually aided society registered under any

State enactment relating to such societies or any multistate cooperative society registered under

the Multi State Cooperative Societies Act, 2002 but not including:

o A cooperative bank as defined in clause (cci) of section 5 of the Banking Regulation Act,

1949 or

o A cooperative society engaged in agricultural operations or industrial activity or purchase

or sale of any goods and services.”

Micro Finance Approaches:

1. SHG –Bank Linkage -Dominant Model

2. Financing through MFIs -Emerging Model

3. Group based government programs.

Apex Agencies Involved NABARD, SFMC - SIDBI Foundation for Microcredit, RMKFWWB Government of India –

PMRY and SJSY.

Types of MFI’s:

Microfinance itself is a credit lending model, and within this lending model exist several

subcategories, i.e. microfinance lending models, which differ in terms of where their funds are

sourced from, and how the money is governed.

Microfinance Lending Model 1: Associations

Microfinance Lending Model 2: Bank Guarantees

Microfinance Lending Model 3: Community Banking/ Grameen Bank/ Village Banking

Microfinance Lending Model 4: Cooperatives

Microfinance Lending Model 5: Credit Unions

Microfinance Lending Model 6: Non-Governmental Organizations (NGOs)

Microfinance Lending Model 7: For-profit Banks

Microfinance Lending Model 8: ROSCAs Rotating Savings and Credit Associations (ROSCAs)

Review of Available literature: Rajasthan is relatively a new entrant into micro finance, though organizations like Sewa Mandir,

an NGO operating in Udaipur had set up Self-Help Groups two decades ago for community

mobilization. The popularization of self-help groups was at the behest of NABARD when it

started facilitating bank linkage of such groups. Groups have been promoted by civil society

organizations, government and at the behest international organizations through various

programmes.

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

109

Women and Child Development Department of Rajasthan has been promoting SHGs since 1997-

98 in all the 32 districts of the State. Till January 2006, there existed104861 women’s Self-Help

Groups helping 11 lakh women. The department was able to provide linkage to 43848 groups

and delivered Rs.84.31 crore credit. The savings of these groups touched Rs.38 lakh. The

information provided by NABARD reveals that by 2000, 1941 SHGs were provided credit

linkage and 1236 were refinanced and 930were women’s groups. The total bank loan was

Rs.455.70 lakh. The situation must have improved a lot since then. However, one can say that

quality and number of groups does not go hand in hand in Rajasthan.

Financial Status of Rural Poor: A Study in Udaipur District M S Sriram Smita Parhi

Aravali, again a NGO the Study of the SHGs in Rajsamand, Bikaner, and and Churu and

Bharatpur Districts (undated) .This study looks at SHGs in Rajsamand, Bikaner, Churu and

Bharatpur Districts of Rajasthan. The study deals with SHGs formed by ICDS, NGOs, and other

government departments, PRIs, SGSY. The study finds ICDS groups to be haphazardly formed

to fulfill the targets. The SHGs formed under SGSY, DPIP etc. are mainly activity groups. The

saving structure and inter-loaning structure in such groups are weak.

Ashutosh Kumar and Arun Shrimali, Feasibility Study for Initiating Income

Generating Activities with Existing Women Self Help Groups, IRMA, Anand, 1999.This

report is a feasibility study for initiating income-generating activities with women SHGs of Sewa

Mandir, Udaipur. It has studied the projects at five sites. It identifies possible sources of finance

and type of activities SHGs can undertake. It also suggests the financial gains from undertaking

the activities. It uses alternative cost benefit scenarios to arrive at type of activities a SHG can

venture into. The most important activity identified is dairying. The other activities are bamboo-

based items.

Basix, Equity for Equity

http://www.basixindia.com/micro_finance_in_india.aspBasix undertook a study funded by IFAD

to look into evolution of the MFI and its mission statement, legal status, ownership, governance

and organization structure, areas of operations, size and growth over a period, social technology,

products for savings, credit and other financial services, analysis of operating cost structure,

overall budget, sources of funding, human resources (managers and staff), accounting policies

including provisioning norms etc., system and procedures. The study looked at MFIs in

Rajasthan, UP, Bihar, Orissa, AP and Tamil Nadu.

The study observes that most of the MFIs are undercapitalized that is mainly due to their legal

form- most are Societies/ Trusts, which do not have any concept of equity. This restricts these

MFIs' ability to seek adequate debt in the long run. Moreover, there is no cushion to absorb loan

losses, though some have built reserve funds at various levels. Though the apex financial

institutions are aware of this problem, till recently they have not done much about it. In fact most

lending schemes to MFIs, such as by the RMK and FWWB, are structured to suit only NGOs

registered as Societies/Trusts. The SFMC may address this problem by insisting that larger MFIs

must move to an appropriate legal structures, such as cooperative societies or companies, which

must be well capitalised.The overall asset quality of the MFIs in the study seemed well given the

country's.

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

110

4.1 OBJECTIVES OF THE STUDY

Microfinance is not so new topic to be studied but for Udaipur, Rajasthan region it is seen that

applicability of micro financial activities is not at a good extent. So what types of initiatives are

being taken by MFIs to develop a suitable framework to spread the benefits of micro financial

activities with special reference to rural poor? It is also an examination topic to study the client’s

satisfaction from the services delivered by MFIs to them. MFIs and its activities are designed to

nourish the living standards of poor people by providing them credit and other facilities, so it

must be examined that whether the MFIs are successfully delivering their objective or not. Under

this stand point the study is a systematic effort to determine the following questions:

1. What types of channels used by MFIs to delivers the services and benefits?

2. Are there any models or theory used by MFIs for smooth delivery of services to clients?

3. Are there any geographic boundaries for delivering micro financial services?

4. Can MFIs reduce the poverty and improve living standard or rural poor?

5. What is level of satisfaction of the clients of MFIs of Udaipur, southern Rajasthan?

6. Which factors help the MFIs, to manage the client’s satisfaction effectively?

7. What type of products and services are offered by MFIs in Udaipur block.

8. Understanding the various dimensions of client satisfaction for MFIs services and

measuring its success variables also.

4.2 RESEARCH DESIGN

According to Zikmund, W. G. (2006), “The research design contributes the blue print for the

collection, measurement and analysis of data”. The research design is the plan and structure of

investigation so conceived as to obtain an answer to the research problem.

Cooper (2006) suggests essentials of research design:

An activity- and time-based plan

A plan always based on the research question

A guide for selecting sources and types of information

A framework for specifying the relationships among the study’s variables

A procedural outline for every research activity

This study accentuate on identifying the critical success of MFIs in boosting the living standard

of rural poor, means research focuses on a set of issues of a single type of organization unit in

this research it is MFIs (Micro Financial Institutions) locate in Udaipur district of southern

Rajasthan.

There are usually two approaches used in conducting a scientific research. One is deductive

approach and another is inductive approach. All scientific theories involve both induction and

deduction and they sometimes differ in the degree to which they emphasize one over another

(Graziano, 2004). A researcher examines and then authentically records what is observed,

without any prejudice. Some of these statements of inspections are established as true and serve

as the basis for theories and laws. In order to establish what is true or false, and to draw

conclusions, two ways are applied: induction and deduction. The basis of induction is empirical

evidence, while that of deduction is logic (Ghauri, Gronhaug, 2002).

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

111

If the deductive approach is used, the researchers generate hypothesis from theory. After that,

they use empirical research and data collection to test the hypothesis. In a deductive approach,

conclusions come from the evidences. In an inductive approach, researchers start working with

empirical observations. Based on these, the researchers make hypotheses that are used to develop

new theories and later these new theories are added to the established ones (Bryman, Bell,

2003). Inductive approach emphasizes on induction and stays very close to the empirical data

(Graziano et al., 2004). So an inductive approach focuses on developing new theories, which

are then used to elaborate general statements, coming from empirical observations.

According to Creswell (1994) there are number of practical criteria to make a distinction

between the deductive and the inductive approach. Perhaps the most significant of these criteria,

is the nature of topic of research. That is, a topic on which there is a wealth of literature from

which one can define a theoretical framework, and a hypothesis lends itself more readily to

deduction. When the topic of research is new, there exists much debate, and on which there is

little literature available, it may be more appropriate to work inductively by producing data,

analyzing and reflecting on what theoretical themes, the data points to.

The purpose of this research / study is not to construct a fresh theory, but to investigate the

research questions based on empirical research and primary data. Furthermore, in this thesis, we

will generate hypotheses from theories and then, we will use empirical research and primary data

to test the hypotheses. When we will draw our conclusions, we will also apply our logic.

Therefore, based on research question and scientific ideal, we chose to follow the deductive

approach.

4.3 SAMPLING PROCEDURE

According to Duckworth, W.E., (1962), sampling techniques are approaches used in selecting

samples from a study population. Given the large scale and complexity of various micro-

financial institutions, the judgmental sampling procedure, a random sampling technique was

used to select the MFIs for analyzing the critical success factors. For selecting the client’s

random sampling was used in this study.

4.3.1 SAMPLING PROCEDURE FOR MICRO FINANCIAL INSTITUTIONS

The nature of research design is such that the micro financial institutions were identified through

judgmental and random sampling procedure. The researcher has used his judgment at the level of

selection of MFI among various MFIs located in district to examine their critical success factor

and their contribution in poverty alleviation of rural poor. The judgment for selection of MFIs

has been pertained to: the size and scale of MFI, locality of MFI, and availability of various

types of financial services, public awareness, and cost applied in service.

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

112

A list of participating MFIs is given in Table 4.1.

Table 4.1: Participating MFIs in Research

S. No. NAME OF PARTICIPATING INSTITUTIONs

BANKS

1. Allahabad Bank

2. Bank Of Baroda

3. Dena Bank

4. Vijaya Bank

5. Canara Bank

6. Oriental bank of Commerce

COOPEATIVE BANKS & CREDIT UNIONS

7. Rajasmand Urban Cooperative Bank

8. Udaipur Mahila Samriddhi

9. Urban Cooperative Bank

10. Kamakshi Credit Cooperative Society

NGO’s

11. SEWA Mandir

12. Rural India Development Institute

13. SAHAYATA

RRB’s

14. Rajasthan Gramin Bank

15. Mewar Anchlik Gramin Bank

16. Baroda Rajasthan Gramin bank

Source: - Survey

Total 100 questionnaires were administered to capture the relevant information of MFIs and their

activities for rural poor.

And, micro financial activities are determining the success of these MFIs in poverty alleviation

program at rural level of study area block of Udaipur district.

4.3.2 SAMPLING PROCEDURE FOR CLIENTS

For collecting the responses of clients’ convenience sampling procedure is followed. Under this

procedure it is taken care of that responses are collected from only those clients who are able to

understand the necessity of the research, and can interpret that any of the fruitful outcome will

definitely benefited them in future into services offered by MFIs. Another issue was under

consideration while selecting the clients that the respondent should know about the MFIs and

their activities and must be a microfinance participant.

Total of 400 questionnaires were distributed to clients or microfinance participants. Fist unit of

formal structured questionnaire was administered to capture, group participation, new loans,

uses, and loan repayment as well as household incomes and also helps to determine their

satisfaction with the help of second unit of questionnaire.

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

113

4.4 PROCEDURE FOR DATA COLLECTION

To attain the objectives of the study required data were collected through both primary and

secondary data source.

4.4.1 PRIMARY DATA

Primary data is unpublished data and generally collected through the respondents. In this study

primary data was collected under following categories:

1. Raw and Unpublished facts and figures from MFIs database, Files and Records.

2. By observing clients opinion about the services by investigating them through a

structured questionnaire.

3. Enquiring clients from different blocks of the study area to capture comprehensive

information to identify the contribution of MFIs in nourishing their standard of living.

4. Structured questionnaire used to obtain data on factors which affects efficiency of micro-

financing activities.

5. Study of study area blocks families’ households before and after micro financing

activities.

Two different set of questionnaire were prepared for data collection, under following

classification:

1. Questionnaire to determine success of MFI in nurturing the rural poor.

2. Questionnaire to determine satisfaction level of clients of Micro Finance institutions.

This method is considered significant to corroborate the log data and highlight the other factors

affecting the success of MFIs in service delivery and client satisfaction. The closed ended

questionnaire was designed to obtain the opinions of clients and MFIs about the success of MFI

in nourishing the rural poor living standard and client’s satisfaction.

4.4.2 SECONDARY DATA

The data which is procured through already published sources like reports, websites, research

papers, books etc is known as secondary data. Main sources of such kind of data were databases

of MFIs that are their log files which were computerized. Also, important data such as the

turnover of clients, their educational profiles with the cost applied on services, infrastructure

facilities detail were collected and subsequently validated by interviewing the employees of

MFIs. The client’s flow was quantified using this data. Existing data were also obtained from the

records and office reports.

4.5 ANALYSIS AND PRESENTATION

The data obtained through both sets of questionnaire were analyzed by using appropriate

statistical tools. The filled up questionnaires were coded and master data sheet was prepared. The

data was then tabulated and classified on the basis of independent and dependent variables.

Detail analysis, interpretation and discussion of the data are presented in chapter-5.

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

114

The summary statistics of the collected data have been presented in a systematic manner. The

statistical tests: descriptive statistical analysis (Mean, Standard Deviation, and Percentage), t-test,

principal component factor analysis and ANOVA were used for analysis.

5.2.1 HYPOTHESES FRAMED FOR THE STUDY

H0A : There is no significant relationship between employees and MFIs success.

H1A : There is significant relationship between employees and MFIs success.

H0B : There is no significant relationship between client base and MFIs success.

H1B : There is significant relationship between client base and MFIs success.

H0C : There is no significant relationship between Infrastructure Facilities and MFIs success.

H0C : There is significant relationship between Infrastructure Facilities and MFIs success.

H0D : There is no significant relationship between cost of service and MFIs success.

H1D : There is significant relationship between cost of service and MFIs success.

H0E : There is no significant relationship between External environmental factors and MFIs

success.

H1E : There is significant relationship between External environmental factors and MFIs

success.

H0F : There is no significant relationship between improvement in economic status and Rural

Poor Nurturing.

H1F : There is significant relationship between improvement in economic status and Rural

Poor Nurturing.

H0G : There is no significant relationship between improvement in social status and Rural

Poor Nurturing.

H1G : There is significant relationship between improvement in social status and Rural Poor

Nurturing.

H0H : There is no significant relationship between improvement in political status and Rural

Poor Nurturing.

H1H : There is significant relationship between improvement in political status and Rural Poor

Nurturing.

5.2.2 Testing of Hypotheses

The study concentrates on examining the critical success factors of MFIs and focuses on the

factors which ensure the nourishment of rural poor. So established hypotheses determines the

significant relationship between the identified dimensions and MFIs success and nurturing of

rural poor.

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

115

Table 5.6: Effect of dimensions on MFIs success as a critical success factors

Dimensions Variables Mean S.D F Sig Accepted /

Rejected

Employees

Clients are Aware about

MFA 3.15 1.451 1.646 .004* Rejected

Loan Defaults are there 3.33 1.346 2.587 .001* Rejected

MFI is achieving the

objective of financial

inclusion

3.02 1.411 2.312 .003* Rejected

Training program for

clients to aware about the

MFIs

3.84 1.247 1.788 .001* Rejected

Micro Financial activities

nourish the living state of

poor

4.04 1.157 1.797 .006* Rejected

Client Base

Client Turnover is Good 2.87 1.225 1.812 .004* Rejected

Loan Defaults are there 3.01 1.331 2.014 .002* Rejected

Education Level of Clients

is Low 3.21 1.587 1.810 .001* Rejected

Clients are uneducated for

financial service 3.09 1.322 1.682 .002* Rejected

Clients Complain about

services 3.60 1.479 2.226 .021* Rejected

Infrastructure

Facilities

Transportation facilities

are there to reach

customers

2.31 1.308 1.658 .011* Rejected

Telecommunication

facilities are good 2.92 1.392 1.556 .008* Rejected

Communication due to

geographic dispersion is

difficult

3.09 1.277 1.313 .009* Rejected

Costs

High operational cost 4.01 1.012 1.771 .006* Rejected

Lack of Access of funding 3.64 1.222 1.801 .001* Rejected

Loan collection method

leads to delayed payment 3.55 1.045 2.426 .010* Rejected

Fraud is a problem for

business

3.12 1.113 1.826 .015* Rejected

External

Environment

Political 4.11 0.985 2.445 .004* Rejected

Economical 3.44 1.169 2.621 .001* Rejected

Social 3.09 1.223 1.952 .009* Rejected

Technological 3.16 1.362 2.059 .001* Rejected

Legal 2.54 1.319 1.847 .001* Rejected

* Significant at .05 level.

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

116

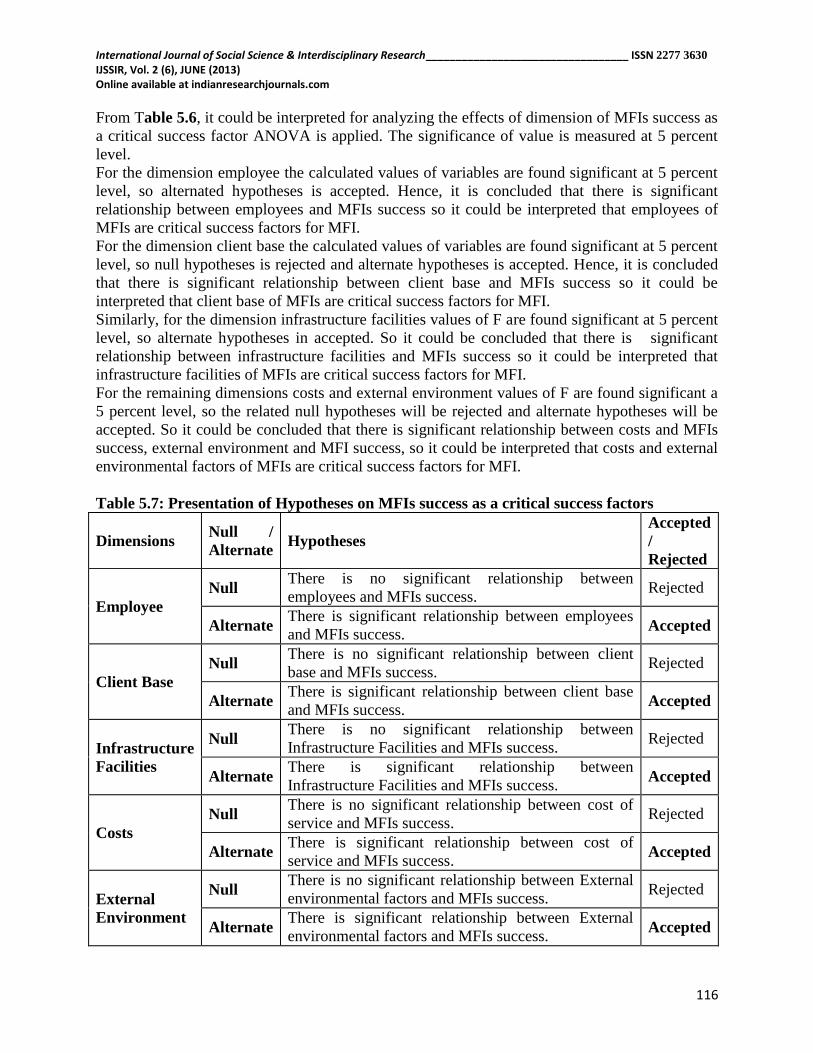

From Table 5.6, it could be interpreted for analyzing the effects of dimension of MFIs success as

a critical success factor ANOVA is applied. The significance of value is measured at 5 percent

level.

For the dimension employee the calculated values of variables are found significant at 5 percent

level, so alternated hypotheses is accepted. Hence, it is concluded that there is significant

relationship between employees and MFIs success so it could be interpreted that employees of

MFIs are critical success factors for MFI.

For the dimension client base the calculated values of variables are found significant at 5 percent

level, so null hypotheses is rejected and alternate hypotheses is accepted. Hence, it is concluded

that there is significant relationship between client base and MFIs success so it could be

interpreted that client base of MFIs are critical success factors for MFI.

Similarly, for the dimension infrastructure facilities values of F are found significant at 5 percent

level, so alternate hypotheses in accepted. So it could be concluded that there is significant

relationship between infrastructure facilities and MFIs success so it could be interpreted that

infrastructure facilities of MFIs are critical success factors for MFI.

For the remaining dimensions costs and external environment values of F are found significant a

5 percent level, so the related null hypotheses will be rejected and alternate hypotheses will be

accepted. So it could be concluded that there is significant relationship between costs and MFIs

success, external environment and MFI success, so it could be interpreted that costs and external

environmental factors of MFIs are critical success factors for MFI.

Table 5.7: Presentation of Hypotheses on MFIs success as a critical success factors

Dimensions Null /

Alternate Hypotheses

Accepted

/

Rejected

Employee

Null There is no significant relationship between

employees and MFIs success. Rejected

Alternate There is significant relationship between employees

and MFIs success. Accepted

Client Base

Null There is no significant relationship between client

base and MFIs success. Rejected

Alternate There is significant relationship between client base

and MFIs success. Accepted

Infrastructure

Facilities

Null There is no significant relationship between

Infrastructure Facilities and MFIs success. Rejected

Alternate There is significant relationship between

Infrastructure Facilities and MFIs success. Accepted

Costs

Null There is no significant relationship between cost of

service and MFIs success. Rejected

Alternate There is significant relationship between cost of

service and MFIs success. Accepted

External

Environment

Null There is no significant relationship between External

environmental factors and MFIs success. Rejected

Alternate There is significant relationship between External

environmental factors and MFIs success. Accepted

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

117

So from Table 5.7, it could examined that all the alternate hypotheses were accepted, these

hypotheses confirms that all dimension employee, client base, infrastructure facilities, costs and

external environment are critical success factor for MFI success.

Table 5.8: Analyzing the dimensions confirms nurturing of the rural poor by Micro

financial activities

Dimensions Variables Mean S.D F Sig Accepted /

Rejected

Economic

Increase in Income 2.81 .965 1.542 .001* Rejected

Increase in Saving 3.15 1.114 1.941 .009* Rejected

Increase in Income

generating activities 2.87 1.122 2.011 .002* Rejected

Reduction of Poverty 2.42 1.019 1.649 .006* Rejected

Improved decision power 2.50 1.246 1.797 .006* Rejected

Social

Communication with

financial institution

employees

2.79 1.331 1.742 .005* Rejected

Participation in social

development activities 2.00 .987 2.119 .001* Rejected

Social structure

improvement 2.16 .995 1.827 .001* Rejected

Political

Participation in Village

Meetings 2.89 1.458 1.658 .009* Rejected

Voting independently

without money pressure 2.23 1.136 1.782 .010* Rejected

* Significant at .05 level.

From Table 5.8, it could be interpreted for analyzing the dimensions confirms nurturing of the

rural poor by Micro financial activities ANOVA is applied. The significance of value is

measured at 5 percent level.

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

118

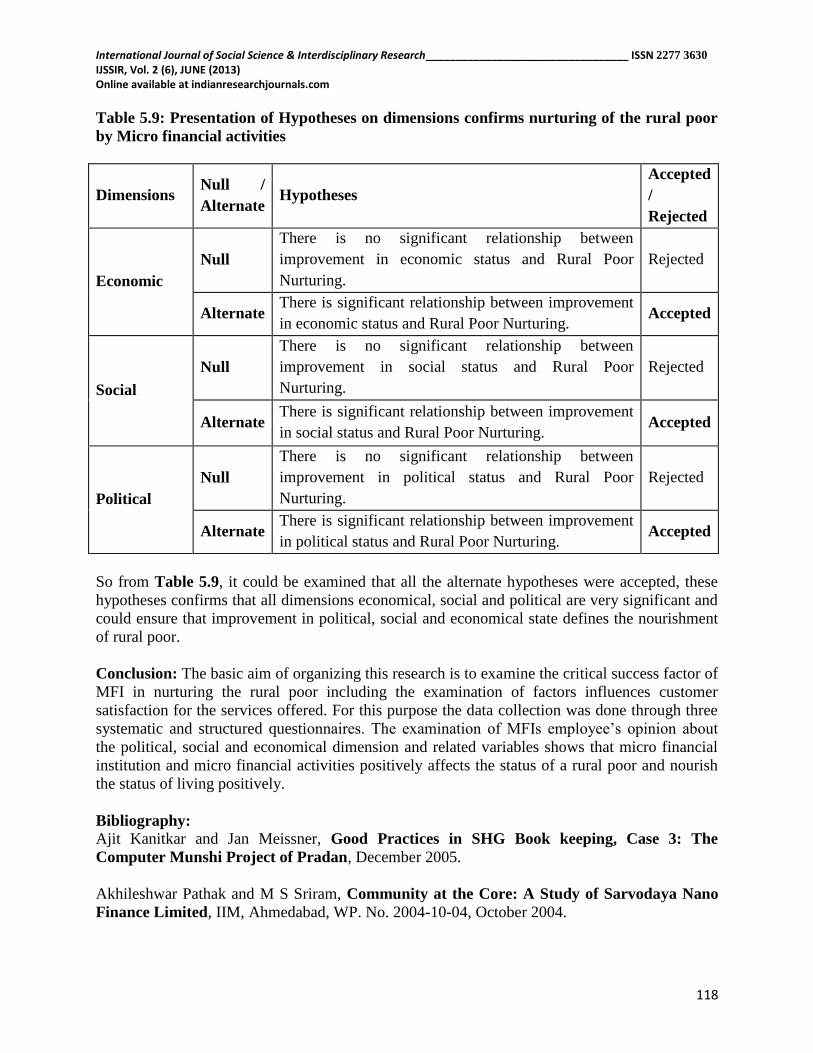

Table 5.9: Presentation of Hypotheses on dimensions confirms nurturing of the rural poor

by Micro financial activities

Dimensions Null /

Alternate Hypotheses

Accepted

/

Rejected

Economic

Null

There is no significant relationship between

improvement in economic status and Rural Poor

Nurturing.

Rejected

Alternate There is significant relationship between improvement

in economic status and Rural Poor Nurturing. Accepted

Social

Null

There is no significant relationship between

improvement in social status and Rural Poor

Nurturing.

Rejected

Alternate There is significant relationship between improvement

in social status and Rural Poor Nurturing. Accepted

Political

Null

There is no significant relationship between

improvement in political status and Rural Poor

Nurturing.

Rejected

Alternate There is significant relationship between improvement

in political status and Rural Poor Nurturing. Accepted

So from Table 5.9, it could be examined that all the alternate hypotheses were accepted, these

hypotheses confirms that all dimensions economical, social and political are very significant and

could ensure that improvement in political, social and economical state defines the nourishment

of rural poor.

Conclusion: The basic aim of organizing this research is to examine the critical success factor of

MFI in nurturing the rural poor including the examination of factors influences customer

satisfaction for the services offered. For this purpose the data collection was done through three

systematic and structured questionnaires. The examination of MFIs employee’s opinion about

the political, social and economical dimension and related variables shows that micro financial

institution and micro financial activities positively affects the status of a rural poor and nourish

the status of living positively.

Bibliography:

Ajit Kanitkar and Jan Meissner, Good Practices in SHG Book keeping, Case 3: The

Computer Munshi Project of Pradan, December 2005.

Akhileshwar Pathak and M S Sriram, Community at the Core: A Study of Sarvodaya Nano

Finance Limited, IIM, Ahmedabad, WP. No. 2004-10-04, October 2004.

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

119

Aravali, The Study of the SHGs in Rajsamand, Bikaner, Churu and Bharatpur Districts

(undated).

Aravali, Situational Analysis of SHG-Bank Linkage in Rajasthan, April 2002.

Ashutosh Kumar and Arun Shrimali, Feasibility Study for Initiating Income Generating

Activities with Existing Women Self Help Groups, IRMA, Anand, 1999. Basix, Equity for

Equity, http://www.basixindia.com/micro_finance_in_india.asp

C.P. Mohan and Simanchal Sahu, Information Bureau for Micro Finance (undated). EDA

Rural Systems, The Maturing of Indian Microfinance,http://www.edaruarl.com/imar.html.

Gaurav Ranjan Sinha, Different Aspects Related to Self Help Groups and Need Assessment

of the Members: A Study of Jhadol Block, Udaipur during the Auditing of Self- Help

Groups, 2003.

HDRC and Aravali, Aajeevika - Livelihoods in Rajasthan: Status, Constraints and

Strategies for Sustainable Change, discussion paper series- 6 (undated). Info change micro-

credit, http://www.infochangeindia.org/micro-creditIbp.jsp

L.B. Prakash et al.,Financial Analysis of SHGs in India: Value for Money? (Sakhi Samiti: A

Federation of Women SHGs promoted by Pradan) (undated).

Malika Singh, Rajiv Khandelwal and Snigdha Chakraborty, Collaboration for Improving

Institutional Credit for Self- Help Groups of Rural Poor: A Review of NABARD, NGOs,

Banks and SHGs linkages in Rajasthan State, August 1997

M.S. Sriram and Radha Kumar, Conditions in Which Micro finance has Emerged in Certain

Regions and Consequent Policy Implications, IIM, Ahmedabad, May 2005.

M.S. Sriram and Smita Parhi, Financial Status of Rural Poor: A Study in Udaipur District,

IIM, Ahmedabad (undated).

NABARD and GTZ, Towards a Refined and Improved Management Information System

for Linkage Banking: Results of the Study on MIS at SHG Level, July2005 (draft).

Nutan Kanerai, Impact Assessment of SHGs, Sewa Mandir, 2003.

Piyush Tiwari and S.M. Fahad, Concept Paper: Micro finance Institutions in India, available

at http://www.gdrc.org/icm/conceptpaper-india.html.

Price Water House Coopers, Rural Finance Sector Restructuring and Development, draft

interim report, Rajasthan, component 1A, August 2004.Stuart Rutherford, The Poor and Their

Money, OUP, New Delhi, 2000 (second impression).

International Journal of Social Science & Interdisciplinary Research__________________________________ ISSN 2277 3630 IJSSIR, Vol. 2 (6), JUNE (2013) Online available at indianresearchjournals.com

120

Surjit Singh, Micro Finance for Poor in Rajasthan: The Importance of Self-Help Groups,

IDS Jaipur WP No.118, 2000. Also Surjit Singh, Micro Credit in Rajasthan:The Role of Self-

Help Groups, IDS, Jaipur (a research report), 2000.

Surjit Singh, Self-Help Groups: The Concerns, paper for a seminar on Self- Help Groups:

Vision, Role and Ideology organised by IDSJ, CASA, New Delhi and Suskham Vikas Sansthan,

HCM-RIPA, Jaipur, June 28-29, 2002.

Surjit Singh and V. Sagar (2004) Agriculture Credit in India, Academic Foundation, New

Delhi.

Wolfgang Hannover, Impact of Micro Finance Linkage banking in India on the Millennium

Development Goals (MDG), NABARD and GTZ, 2005.