daily b - latibex.com · ¨datasul: good 2q08 results, egm expected on august 19 ... ¨ gpa: 2q08...

TRANSCRIPT

DAILY BRAZIL

August 07 2008 Settlement: August 12 2008

Banco Espírito Santo de Investimento, S.A. Equity Iberia – Brazil

MARKET OVERVIEW MACROECONOMICS STEEL/MINING

VALE: 2Q08 Slightly Lower Than Expected, but Good Nonetheless Gerdau: 2Q08 results better than expected

OIL/PETROCHEMICAL Braskem: A Little Better Than Expected Ultrapar: Good Results for Ipiranga and Ultragaz

BANKING Banco Itaú: Complementary Dividends BIC Bank: Results for 2Q08

TELECOM / IT / MEDIA Bematech: Interest on Equity Datasul: Good 2Q08 results, EGM expected on August 19 TOTVS: Good Results for 2Q08 15th Telesintese Gathering: Focus is on the new PGO

ELECTRIC UTILITIES Equatorial: 2Q08 Results Preview

RETAIL GPA: 2Q08 Operational Result in Line with Expectations

HEALTH CARE Medial Saúde: Lower, but not a cause for concern

AVIATION GOL: Air Traffic Statistics for July/08.

PULP/PAPER VCP: Consolidation on the Way

REAL ESTATE Cyrela Commercial Properties: 2Q08 Result Abyara/Brasil Brokers: Details of the Acquisition of Brasil Brokers

EDUCATION Kroton: 2Q08 Results.

CAPITAL GOODS Randon: 2Q08 Results

OTHERS ANFAVEA: Very positive Jul/08

MACRO CALENDAR CORPORATE CALENDAR SHORT INTEREST

Main Economic Figures

International Date Local Time (BZ) Indicator Reference BES Estimates Last7-Aug 8:00 AM UK BOE ANNOUNCES RATES AUG 7 - - 5.0% 5.0%7-Aug 8:45 AM EC ECB Announces Interest Rates AUG 7 - - 4.3% 4.3%7-Aug 9:30 AM US Initial Jobless Claims AUG 2 - - 420K 448K7-Aug 9:30 AM US Continuing Claims JUL 26 - - 3265K 3282K7-Aug 11:00 AM US Pending Home Sales MoM JUN - - -1.0% -4.7%7-Aug 4:00 PM US Consumer Credit JUN - - $6.8B $7.8B

Brazilian Market 6-Aug Daily Chg. YTD Chg.Ibovespa 57,542.5 1.90% -9.93%IBX-50 8,242.4 2.09% -15.51%

Fixed Income/Yield 6-Aug 5-Aug 31-DecBR40 5.47% 5.47% 5.55%30y T-Bond 4.68% 4.64% 4.51%

IBOV Most Traded Stocks R$m Quantity (k) 6M Avg.*IBOVESPA 5,436.0 - 1.00%VALE PNA 800.1 21,690 1.23%PETROBRAS PN 633.5 19,062 0.67%BRADESCO PN 210.0 6,592 1.21%ITAU HOLDING PN 201.9 6,017 1.36%CSN ON 195.2 3,375 1.14%Blue Chips Daily Chg. Monthly Last PriceBradesco PN 2.42% -5.30% 32.15Brasil Tel Part PN 2.64% -5.80% 23.30Eletrobrás PNB -1.30% 2.90% 26.65Petrobras PN 3.42% -10.30% 33.30Telemar PN 4.58% -3.20% 37.65Vale PNA 1.86% -11.80% 36.71

Ibovespa - Top Gainers Daily Chg. Monthly Last PriceVCP PN 8.98% -4.20% 39.80ROSSI ON 6.32% -1.60% 13.13BRASIL ON 5.00% -8.40% 24.15TELEMAR PN 4.58% -3.20% 37.65B2W GLOBAL ON 4.39% -3.40% 59.50

Ibovespa - Top Losers Daily Chg. Monthly Last PriceJBS ON -3.09% -15.20% 6.90GOL LINHAS AÉREAS PN -2.88% 19.70% 18.55CEMIG PN -2.41% 0.70% 36.50ELETROBRAS ON -2.40% 2.80% 30.50EMBRAER ON -1.65% 1.30% 11.90

Other Stock Markets 6-Aug Daily Chg. YTD Chg.North AmericaDow Jones US 11,656.1 0.35% -12.79%Nasdaq US 2,378.4 1.21% -11.07%S&P 500 US 1,289.2 0.34% -12.80%EuropeDax Xetra GR 6,561.4 0.65% -18.67%IBEX 35 SM 11,774.4 0.20% -22.45%CAC 40 FP 6,863.8 1.17% -32.63%FTSE 100 LN 5,486.1 0.58% -15.30%PSI 20 PL 8,185.3 -1.31% -37.22%AsiaNikkei JP 13,254.9 2.63% -13.41%Emerging MarketsTOP 40 SJ 3,368.1 1.58% -14.72%Merval AR 1,871.7 3.46% -13.02%IGPA CI 27.8 0.56% -1.80%BUX HB 141.1 -1.27% -7.11%JCI IJ 0.2 -0.18% -17.51%IPC MX 2,753.1 0.99% 1.08%RTS RU 1,814.6 0.14% -20.78%Price Index Preview May-08 Last 2007IPCA 0.65% 0.55% 4.46%IGP-M 0.72% 1.36% 7.75%Indicators 6-Aug Daily Chg. YTD Chg.Dollar (R$/US$) 1.577 0.13% -32.63%Brent (US$) 115.83 -0.69% 23.00%*Volume traded as % of average daily volume for the last 6 months

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 2 - Equity Iberia - Brazil

MARKET OVERVIEW

Equity Market

This Wednesday, US equity markets traded in negative territory in reaction to further losses announced in the mortgage market. Despite this, results reported by companies in the technology sector reversed the pessimistic mood towards the end of the day. Thus the Dow Jones and S&P 500 closed up 0.35% and 0.34%, respectively. The oil price continued the downward trend seen in the last few days, influenced by the publishing of the latest oil stock report, with Brent crude closing down 0.59% at US$117/barrel. In local markets, the Bovespa Index closed up 1.9% at 57,542 points, on volume of R$ 5.4 billion. The shares of Petrobras did not accompany the drop in the oil price, with the ordinary shares closing up 2.67%, and the preferred shares up 3.14%. VCP was the star performer on the day, up 8.98% after the announcement of the company's acquisition of part of the controlling stake of Aracruz. One of the day's highest losers was was JBS , which closed down 3.08%.

Short Position Comments

Equity rental markets saw little movement this Wednesday, with an increase in the level of donors available, and a reduction in rates. Of particular note was the shortage of donors for Aracruz PNB (ARCZ6), with a 21-day average rate of 1.55% p.a.. Other highlights were: Cyrela ON (CYRE3), trading at 3.85% p.a., compared to its 21-day average of 4.00% p.a. and Petrobras ON (PETR3), trading at 0.40% p.a., in line with its historic average.

Exchange Rate

BRL fell in the morning on USD strength but recovered in the afternoon session, closing at 1.5765 (+0.06%). Crude oil futures closed at USD 118.58 (-0.59), the Embi+ Brazil at 220 bp (-3 bp), and the yield of the 10 Yr UST at 4.03% (+1 bp).

The USD closed at R$ 1.57 up 0.06%.

Interest Rates

The lower-than-expected IGP-DI and the further drop in commodity prices led to the continued fall in domestic interest rates, especially short tenors. Jan/09 and Jan/10 rates closed at 13.72% (-2 bp) and 14.64% (-5 bp), respectively.

MACROECONOMICS No major economic indicators were released this Wednesday on international front. In Brazil, FGV institute released general price index (IGP-DI) related to July. According to monthly report, the index decelerated from 1.89% in June to 1.12% in the past month, and came below our estimates (+1.31%). As anticipated, wholesale prices have considerably eased in the end of last month, driven by both agriculture and industrial products. However, that deceleration movement was more intense than our projections had indicated. According to our estimates, IGP-M may register a positive rate of 0.14% in the first preview of August, whose result will be released on Friday, taking into account the recent trend mentioned above. Shifting to economic activity, Anfavea’s vehicle production figures rose 19.8% in July on YoY terms. Based on last data and keeping other relevant variables in their current trend, our econometric model signals a growth between 4.5% and 6.5% (YoY) in July that would represent a drop between 1% and 2% excluding seasonal factors. We will define a more accurate projection as soon as other coincident and leading indicators have been released. On Thursday, monetary policy decisions on Europe will be the highlight on international markets. Analysts expect that BoE and ECB will keep benchmark rates unchanged at 5.00% and 4.25%, respectively.

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 3 - Equity Iberia - Brazil

STEEL/MINING

VALE: 2Q08 Slightly Lower Than Expected, but Good Nonetheless Company Ticker Rating Target Price Upside Last Price R$ YTD P/E 08E EV/EBTIDA 08E DY 08EVALE ON vale3 BUY 69.4 64.5% 42.2 -29.3 8.97 5.9 2.0%

Analyst: Juliana Chu - [email protected] (11) 3074 7320 Company Ticker Rating Target Price Upside Last Price R$ YTD P/E 08E EV/EBTIDA 08E DY 08EVALE PNA vale5 BUY 64.8 76.4% 36.7 -28.4 7.8 5.2 2.3%

Analyst: Juliana Chu - [email protected] (11) 3074 7320 Vale do Rio Doce has published its results for 2Q08, reporting an operational performance slightly below our forecast, but without any major surprises. Operational performance, in general terms, was worse than we had estimated, basically due to the fact that the company did not fully recognized the impact of the iron ore price increase. On the other hand, the company benefited from a positive financial result from currency derivative trading, that we had not expected, which ended up producing higher than forecast net earnings.

Net sales in 2Q08 amounted to US$ 10.600 billion, EBITDA (not including dividends received) of US$ 5.837 billion, with EBITDA margin of 56.6% and net earnings of US$ 5.009 billion, which included a financial gain from trading in currency derivatives, metal hedging positions, etc. of US$ 724 million, US$ 681 million being from swap operations between the Brazilian Real and the US Dollar. Our estimates were for net sales of US$ 11.039 billion (bearing in mind that the company also is due to recognize the amount of US$ 553 million in the next quarter, as a consequence of the iron ore price increase in 2Q08), EBITDA cash generation EBITDA (not including dividends received) of US$ 6.393 billion, with EBITDA margin of 57.9% and net earnings of US$ 4.465 billion.

Despite this lower than expected operational performance, we consider the result to be positive. With this, we do not believe that there will be any significant impact on the company's share price, although there may be some confusion in the market in the interpretation of this result. As a consequence, we are maintaining our BUY recommendation for the preferred and ordinary shares of Vale do Rio Doce.

TAB. 1: RESULT SUMMARY US GAAP 2Q08 2Q08E % 1Q08 % 2Q07 %

Volume (000 ton) Iron Ore (000) 79 72 10.0% 68 15.5% 73 8.1% Nickel 69 67 2.5% 66 4.5% 67 3.0% US$ million Net Revenues 10,600 11,039 -4.0% 7,832 35.3% 8,697 21.9% Gross Profit 5,837 6,559 -11.0% 3,590 62.6% 4,913 18.8% Gross marging 55.1% 59.4% 45.8% 56.5% EBITDA* 5,995 6,393 -6.2% 3,681 62.9% 4,904 22.2% EBITDA Margin 56.6% 57.9% 47.0% 56.4% Financial Result 1,167 (241) - (711) - 501 132.9% Taxes (1,506) (809) 86.1% (358) 320.7% (1,396) 7.9% Net Profit 5,009 4,465 12.2% 2,021 147.9% 4,100 22.2%

* w/o dividends Source: Company and BES Securities Estimates

Gerdau: 2Q08 results better than expected Company Ticker Rating Target Price Upside Last Price R$ YTD P/E 08E EV/EBTIDA 08E DY 08E

GERDAU PN ggbr4 NEUTRAL 43.8 36.3% 32.1 23.3 9.5 5.7 3.1%Analyst: Juliana Chu - [email protected] (11) 3074 7320

Gerdau has published its results for 2Q08, reporting a better operational performance better than we had forecast, particularly in terms of improved operational margins. Of particular note were the operations in Brazil, which saw a significant widening in EBITDA margin, while for its Latin American operations, sales increased strongly, as did EBITDA margin - both compared to the previous quarter. It should be borne in mind that this result was also impacted by the consolidation of the operations of Macteel/Quanex, whose acquisition was completed on April 23, 2008.

The result reported in IFRS in 2Q08 amounted to net revenue of R$ 11,100 million, EBITDA generation of R$ 2,747 million, with EBITDA margin of 24.7% and net earnings of R$ 1,863 million - this latter benefiting from exchange-rate variation in the quarter. Our forecasts were for net revenue of R$ 10,348 million, EBITDA of R$ 2,384 million, EBITDA margin of 23.0% and net earnings of R$ 1,582 million.

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 4 - Equity Iberia - Brazil

Considering the good result reported and bearing in mind the favourable outlook for the company, we are maintaining our NEUTRAL recommendation for the shares of Gerdau, with a target price of R$ 43.8/share (US$ 25.8/ADR) and a BUY recommendation for Met. Gerdau, with a target price of R$ 64.7/share.

TAB.1: SUMMARY RESULTS IFRS 2Q08 2Q08E % 1Q08 % 2Q07 % Total Volume 5,495 5,460 0.6% 4,941 11.2% 4,168 31.8% Brazil + Exports 1,818 1,864 -2.5% 1,621 12.2% 1,759 3.4% USA 2,268 2,208 2.7% 2,158 5.1% 1,577 43.8% Latin America 624 610 2.3% 623 0.2% 581 7.4% Europe/Specialty 785 778 0.9% 539 45.6% 251 212.7% R$ million Net Revenues 11,100 10,348 7.3% 8,945 24.1% 7,541 47.2% Gross Profit 2,980 2,572 15.8% 2,132 39.8% 1,894 57.4% Gross Margin 26.8% 24.9% 23.8% 25.1% EBITDA 2,747 2,384 15.2% 1,985 38.4% 1,597 72.0% EBITDA Margem 24.7% 23.0% 22.2% 21.2% Financial Result 434 490 -11.5% (164) -364.2% 149 191.5% Taxes and Min. (649) (486) 33.5% (308) 110.9% (296) 119.5%

Net Profit 1,863 1,582 17.8% 874 113.1% 876 112.7% Source: Company and BES Securities

OIL/PETROCHEMICAL

Braskem: A Little Better Than Expected Company Ticker Rating Target Price Upside Last Price R$ YTD P/E 08E EV/EBTIDA 08E DY 08E

BRASKEM PNA brkm5 BUY 22.0 62.0% 13.6 -4.4 12.52 5.2 3.0%Analyst: Gilberto Pereira de Souza - [email protected] (11) 3074 7325

Braskem has published its results for 2Q08, reporting net earnings of R$383 million, up 362.8% on 1Q08, and up 36.3% on the same period a year earlier. It should be remembered that the results in 1Q08 were positively impacted by the recognition of an extraordinary item of R$ 116 million (R$ 87 million after taxes) from the sale of Petroflex, while the 2Q07 result was boosted by a R$ 111 million reversion in PIS/COFINS tax provision.

TABLE 1: BRASKEM CONSOLIDATED – RESULT HIGHLIGHTS R$ million 2Q08 (a) 2Q08e (b) (a) / (b) 1Q08 (c) (a) / (c) 2Q07 (d) (a) / (d)Net Revenues 4.405 4.510 -2,3% 4.410 -0,1% 4.969 -11,4%Gross Profit 637 542 17,5% 650 -2,0% 932 -31,7%Gross margin 14,5% 12,0% 14,7% 18,8%EBITDA 519 471 10,1% 583 -11,0% 805 -35,5%EBITDA margin 11,8% 10,5% 13,2% 16,2%Net Profit 383 354 8,1% 83 362,8% 281 36,3%

Source: Braskem / BES Securities

Margins exceed expectations - Operationally, the company reported a better margin than we had forecast, practically in line with the previous quarter, despite the impact of higher naphtha prices on production costs. This better-than-expected performance is largely due to higher-than-expected sales volume in the domestic market (as well as an improved sales mix) and a lower volume of condensate re-sales than we had estimated (we had expected this to be constant compared to the previous quarter).

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 5 - Equity Iberia - Brazil

Reaction likely to be positive - The strong sales volume in the domestic market, enabling more stock to be drawn down than we had expected, resulted in the company obtaining better margins than forecast, something which we consider to be very positive, and likely to please investors. However, we draw attention to the fact that a significant volume of sales took place in June, which may represent advance buying on the part of clients, in order to avoid the price increases announced for subsequent months. This could result in lower sales volume growth in 3Q08. The second point is with regard to the rise in sales expenses in this quarter, which we believe will have a negative impact on this result. We believe that part of this increase was due to the need to handle a higher volume of stock during the period that the plants were shut down, but it is not entirely clear exactly how much of this increase is non-recurring.

Despite these points, our view of the results and the prospects for the company continue favourable. We are maintaining our BUY recommendation for the preferred shares of Braskem, with a target price of R$ 22.00/share.

Ultrapar: Good Results for Ipiranga and Ultragaz

Company Ticker Rating Target Price Upside Last Price R$ YTD P/E 08E EV/EBTIDA 08E DY 08E

ULTRAPAR PN ugpa4 NEUTRAL Under Revision - 57.0 -8.6 - - -Analyst: Gilberto Pereira de Souza - [email protected] (11) 3074 7325

Ultrapar has published its results for 2Q08, reporting net earnings of R$ 104 million, up 15.3% on the previous quarter, and up 178.3% on 2Q07 (this quarter did not include the acquisition of the assets from Ipiranga). Of particular note was the declaration of a dividend of R$ 0.89/share (dividend yield of 1.6% on the closing share price as at August 6, 2008), which corresponds to a payout of 61% of the company's net earnings in the half-year.

TABLE 1: ULTRAPAR CONSOLIDATED – RESULT HIGHLIGHTS

R$ million 2Q08 (a) 2Q08e (b) (a) / (b) 1Q08 (c) (a) / (c) 2Q07 (d) (a) / (d)Net Revenues 6.992 6.917 1,1% 5.927 18,0% 6.181 13,1%Gross Profit 488 513 -5,0% 466 4,6% 477 2,3%Gross margin 7,0% 7,4% 7,9% 7,7%EBITDA 248 247 0,5% 222 11,5% 222 11,3%EBITDA margin 3,5% 3,6% 3,7% 3,6%Net Profit 104 102 2,3% 90 15,3% 37 178,3%

Source: Ultrapar / BES Securities Ultragaz: better volume than expected

Ultragaz ended 2Q08 with sales volume of 411,000 tons of LPG, an increase (partly seasonal) of 12.3% on 1Q08, being up 2.2% compared to the previous year, higher than we had expected, as a result of a better performance than expected in the bulk gas segment. Of particular note was the EBITDA margin per ton, up 14.8% compared to the previous quarter.

Oxiteno: Still under pressure from ethylene costs

Oxiteno ended 2Q08 with sales volume of 146,000 tons, up 6.7% compared to the previous quarter, but down 0.9% on 2Q07. The domestic market accounted for sales volume of 101,000 tons, down 9.4% on the previous year (lower sales volume in the polyester segment) but up 2.9% on 1Q08. Cost pressure, however, resulted in a further squeezing in EBITDA margin/ton - more than we had estimated.

Ipiranga: Good Operational Performance

Oil product sales volume at Ipiranga in 2Q08 amounted to 3,063,000 m³, up 11.5% on the previous year, and a seasonal increase of 13.1% on the previous quarter. Of particular note was the significant increase in ethanol sales: up 71.3% on 2Q07, well above market growth and much higher than we had forecast. The highlight here was the sharp rise in EBITDA/m³ (6.9% on the previous quarter), higher than we had estimated.

Opinion: In general, the result, both consolidated as well as for the subsidiaries, is in line with our forecasts, and likely to please investors, particularly in the case of Ipiranga and Ultragaz.

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 6 - Equity Iberia - Brazil

BANKING

Banco Itaú: Complementary Dividends

Company Ticker Rating Target Price Upside Last Price R$ YTD P/E 08E EV/EBTIDA 08E DY 08E

ITAU HOLDING PN itau4 BUY 44.3 31.0% 33.8 -6.8 12.1 - 2.9% Analyst: Mariana Moraes de Barros - [email protected] (11) 3074 7356

Banco Itaú announced the payment of complementary dividends. The gross value to be paid is one of R$ 444.8 million or R$0.15 per share which correspond to a dividend yield of 0.5% considering the closing price of August 04th. The shares will go ex-dividends on the 16th August 2008 and the payment is scheduled to take place on August 25th 2008.

BIC Bank: Results for 2Q08 BIC Bank released the results for 2Q08, with a net profit of R$ 104.7 million, representing an increase of 13.9% for the quarter and a return on equity of 25.1%, also an increase of 2.0 p.p..

It should be noted that this result, just like the result for the previous quarter, was affected by the recognition of tax credits. During this quarter, the tax credits were recognized as a result of the change in the rate of social contribution.

A table below shows the principal indicators and results for the Bank.

Table 1: Results

2Q08(a) 1Q08(b) (a)/(b) 2Q07 (c) (a)/(c) Net Income 104.7 91.9 13.9% 33.0 217.3% Net Income1 44.9 69.2 -35.1% 21.4 109.8% Stockholders' Equity1 1,670.6 1,596.9 4.6% 796.5 109.8% Average Assets 11,909 10,937 8.9% 8,858 34.4% Return on avarage equity 25.1% 23.0% 2.0 p.p. 16.6% 8.5 p.p. Adjusted Return on avarage equity1 10.8% 17.3% -6.6 p.p. 10.7% 0.0 p.p. Return on avarage assets 3.9% 3.6% 0.3 p.p. 1.7% 2.2 p.p.

Source: Company 1 Exclude fiscal credit

The Credit Portfolio recorded strong growth during the quarter of 18.1%, with the highlight being the

operations in the middle market (+20.5%). In the Financial System, the expansion during the quarter was 3.9% for the individual portfolio and 9.5% for the corporate portfolio, taking into account only the operations referenced for the rate of interest.

Table 2: Credit portfolio

2Q08(a) 1Q08(b) (a)/(b) 2Q07 (c) (a)/(c) Individuals 984 972 1.2% 995 -1.1% - Payroll Loans 425.0 443.3 -4.1% 497 -14.4% - Personal Loans 115.6 136.6 -15.4% 125.2 -7.7% - Others 443.5 392.1 13.1% 373.2 18.8% Middle 8,187 6,794 20.5% 4,850 68.8% Total 9,172 7,766 18.1% 5,845 56.9%

Source: Company, not included loans assignment with recourse

This strong growth led the provision for loan losses to increase by 10.7% with this, the allowance for loan losses over the total loans reach 1.9%, stable in comparison with the previous quarter. The coverage for credit due reached 260.7%, a significant improvement over 1Q08 (137.6%).

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 7 - Equity Iberia - Brazil

With regard to the D-H portfolio coverage reached 68.5% showing a deteriorating position compared with 1Q08 (78.8%).

The strong growth in the credit portfolio wound up benefiting the financial margin of the bank, which reached 9.6%, representing a growth of 0.6 p.p. compared to 1Q08. The table below displays the behavior of the financial margin.

Table 3: Financial Margin

(R$ million)

2Q08(a) 1Q08(b) (a)/(b) 2Q07 (c) (a)/(c) Financial margin (A) 242.6 220.5 10.0% 143.1 69.5% Provision for loan losses 39.2 35.4 10.7% 36.2 8.3%

Financial margin after provision for loan losses (B) 203.4 185.1 9.9% 106.9 90.3% Average Assets (C) 10,102 9,745 3.7% 7,769 30.0% Net interest margin before provision (A/C) 9.6% 9.1% 0.6 p.p. 7.4% 2.2 p.p. Net interest margin after provision (B/C) 8.1% 7.6% 0.5 p.p. 5.5% 2.5 p.p.

Source: Company

Expenditures increased by 4.6% during the quarter, with highlights for the administrative expenditures that increased by 18.4%. Despite this increase, the index of efficiency continue to present a declining trend line during 2Q08 and reached 34.8% (-2.1 p.p.).

The Basle index was 14.9%, a reduction of 4.3 p.p. against 1Q08 and was impacted by the new methodology for calculating exchange-rate exposure, according to the bank.

Opinion: We like the growth in the credit portfolio and the improvement in financial margins. On the other hand, the results for operations reached R$ 109.6 million, finishing 3.2% lower than in 1Q08 because of higher administrative expenses and a growth in the lineup other operating expenses (as a function of fiscal and tax contingencies) that were R$ 37.8 million, against R$ 14.8 million in 1Q08.

TELECOM / IT / MEDIA

Bematech: Interest on Equity News: Bematech (BEMA3) announced the payment of Interest on Equity in the gross amount of R$ 0.05/share, equivalent to a dividend yield of 0.69% per share, based on the stock quote of August 5, R$ 7.28. The payment will be made up to August 31. Company’s stocks will be traded “ex-interest on equity” as of August 6.

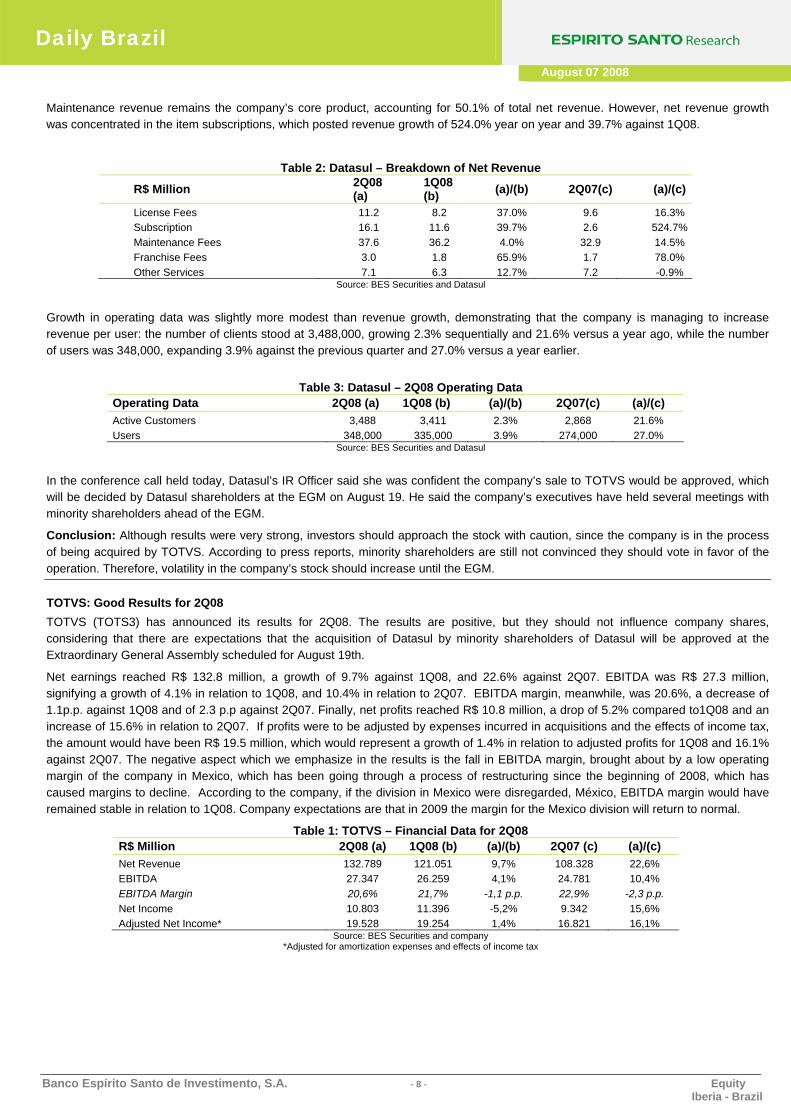

Datasul: Good 2Q08 results, EGM expected on August 19 Datasul (DSUL3) reported its 2Q08 results. The numbers were very positive, but should not be a catalyst for the stock, given the expectation ahead of the Extraordinary General Meeting (EGM) on August 19, which will decide on the sale of the company to TOTVS (TOTS3). Net revenue was R$75.0 million, growing 17.3% sequentially and 39.2% year on year. EBITDA was R$17.2 million, up 37.0% sequentially and 50.0% year on year, while EBITDA margin was 23.0%, expanding 3.3 p.p. against 1Q08 and 1.7 p.p. versus 2Q07. Lastly, net income was R$11.2 million, growing 33.4% on 1Q08 and 47.9% from a year earlier.

Table 1: Datasul – 2Q08 Financial Results

R$ Million 2Q08 (a) 1Q08 (b) (a)/(b) 2Q07 (c) (a)/(c) Net Revenue 75.0 64.0 17.3% 53.9 39.2% EBITDA 17.2 12.6 37.0% 11.5 50.0% EBITDA Margin 23.0% 19.6% 3.3 p.p. 21.3% 1.7 p.p. Net Income 11.2 8.4 33.4% 7.6 47.9%

Source: BES Securities and Datasul

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 8 - Equity Iberia - Brazil

Maintenance revenue remains the company’s core product, accounting for 50.1% of total net revenue. However, net revenue growth was concentrated in the item subscriptions, which posted revenue growth of 524.0% year on year and 39.7% against 1Q08.

Table 2: Datasul – Breakdown of Net Revenue

R$ Million 2Q08 (a)

1Q08 (b) (a)/(b) 2Q07(c) (a)/(c)

License Fees 11.2 8.2 37.0% 9.6 16.3% Subscription 16.1 11.6 39.7% 2.6 524.7%Maintenance Fees 37.6 36.2 4.0% 32.9 14.5% Franchise Fees 3.0 1.8 65.9% 1.7 78.0% Other Services 7.1 6.3 12.7% 7.2 -0.9%

Source: BES Securities and Datasul

Growth in operating data was slightly more modest than revenue growth, demonstrating that the company is managing to increase revenue per user: the number of clients stood at 3,488,000, growing 2.3% sequentially and 21.6% versus a year ago, while the number of users was 348,000, expanding 3.9% against the previous quarter and 27.0% versus a year earlier.

Table 3: Datasul – 2Q08 Operating Data

Operating Data 2Q08 (a) 1Q08 (b) (a)/(b) 2Q07(c) (a)/(c) Active Customers 3,488 3,411 2.3% 2,868 21.6% Users 348,000 335,000 3.9% 274,000 27.0%

Source: BES Securities and Datasul

In the conference call held today, Datasul’s IR Officer said she was confident the company’s sale to TOTVS would be approved, which will be decided by Datasul shareholders at the EGM on August 19. He said the company’s executives have held several meetings with minority shareholders ahead of the EGM.

Conclusion: Although results were very strong, investors should approach the stock with caution, since the company is in the process of being acquired by TOTVS. According to press reports, minority shareholders are still not convinced they should vote in favor of the operation. Therefore, volatility in the company’s stock should increase until the EGM.

TOTVS: Good Results for 2Q08 TOTVS (TOTS3) has announced its results for 2Q08. The results are positive, but they should not influence company shares, considering that there are expectations that the acquisition of Datasul by minority shareholders of Datasul will be approved at the Extraordinary General Assembly scheduled for August 19th.

Net earnings reached R$ 132.8 million, a growth of 9.7% against 1Q08, and 22.6% against 2Q07. EBITDA was R$ 27.3 million, signifying a growth of 4.1% in relation to 1Q08, and 10.4% in relation to 2Q07. EBITDA margin, meanwhile, was 20.6%, a decrease of 1.1p.p. against 1Q08 and of 2.3 p.p against 2Q07. Finally, net profits reached R$ 10.8 million, a drop of 5.2% compared to1Q08 and an increase of 15.6% in relation to 2Q07. If profits were to be adjusted by expenses incurred in acquisitions and the effects of income tax, the amount would have been R$ 19.5 million, which would represent a growth of 1.4% in relation to adjusted profits for 1Q08 and 16.1% against 2Q07. The negative aspect which we emphasize in the results is the fall in EBITDA margin, brought about by a low operating margin of the company in Mexico, which has been going through a process of restructuring since the beginning of 2008, which has caused margins to decline. According to the company, if the division in Mexico were disregarded, México, EBITDA margin would have remained stable in relation to 1Q08. Company expectations are that in 2009 the margin for the Mexico division will return to normal.

Table 1: TOTVS – Financial Data for 2Q08 R$ Million 2Q08 (a) 1Q08 (b) (a)/(b) 2Q07 (c) (a)/(c) Net Revenue 132.789 121.051 9,7% 108.328 22,6% EBITDA 27.347 26.259 4,1% 24.781 10,4% EBITDA Margin 20,6% 21,7% -1,1 p.p. 22,9% -2,3 p.p. Net Income 10.803 11.396 -5,2% 9.342 15,6% Adjusted Net Income* 19.528 19.254 1,4% 16.821 16,1%

Source: BES Securities and company *Adjusted for amortization expenses and effects of income tax

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 9 - Equity Iberia - Brazil

All components of the company’s gross earnings display a good development, both in comparison with 1Q08 as well with 2Q07. The key highlight in its growth was service revenues, which showed a growth of 13.1% in 2Q08 against 1Q08, and user licenses which grew by 35.1% in relation to 2Q08.

Table 2: TOTVS – Opening of Gross Earnings for 2Q08

Million 2Q08 (a) 1Q08 (b) (a)/(b) 2Q07 (c) (a)/(c) License Fees 37,697 34,522 9.2% 27,908 35.1% Services 51,976 45,938 13.1% 42,359 22.7% Maintenance 59,660 57,099 4.5% 49,481 20.6%

Source: BES Securities and company

With regard to operating data, the key highlight involved sales of new Vitrine software licenses for customers who were already part of the company’s customer base, which exhibited growth of 67.1% against 1Q08. The negative aspect to be noticed is with relation to sales of software licenses (other than Vitrine and BCS) to clients of the customer base which fell by 32.7% in relation to 1Q08.

Table 3: TOTVS – Operating data for 2Q08

Operating Data 2Q08 (a) 1Q08 (b) (a)/(b) 2Q07 (c) (a)/(c) New clients 353 293 20,5% 336 5,1% Software (other than Vitrine and BCS) Base clients 996 1.481 -32,7% 882 12,9% New clients 160 142 12,7% - - Vitrine Base clients 132 79 67,1% - - New clients 7 - - - - BCS Sisjuri

Base clients 358 - - - - Source: BES Securities and company

Conclusion: The results are positive, but they should not cause an impact on company shares, inasmuch as there are market expectations concerning the approval of the acquisition of Datasul by Datasul’s own minority shareholders. According to the press, the minority shareholders of Datasul are not yet convinced to vote in favor of the operation. Therefore, it is necessary to be cautious as well with the shares of TOTVS.

15th Telesintese Gathering: Focus is on the new PGO At an event held yesterday in Brasília by Momento Editorial, entitled the 15th Telesintese Gathering, executives of various operators and institutions of the telecommunications industry presented their visions on the change of the regulatory framework which is under way through the new PGO (General Licensing Plan) and the PGR (General Plan for the updating of Regulations). The theme of the gathering was: The new telecommunications policy and regulatory changes: where does Brazil want to be?

As was to be expected, the small operators defended aspects of the new regulatory framework that promote competition, while incumbents focused on two obligations imposed on them by Anatel in the new PGO: (i) the need for separation of companies between public telephony and broad band, and (ii) the need for a transfer of license in the event of the sale of any of the company’s assets (broad band, public telephony, mobile telephony, etc.).

We underscore the following most significant aspects of the event:

Anatel: we believe that the most important news announced by the president of Anatel, Ronaldo Sardenberg, was that the Agency has hired a consultant to evaluate the impact of the separation between fixed telephony and broad band. The study should be ready in 60 days and should help Anatel in deciding whether or not to maintain this requirement of the licensees. In this light, it is our understanding that the approval of the new PGO must be contingent upon this study.

GVT (GVTT3): GVT's Vice President for Regulatory Affairs, Carlos Alberto Nunes, referring to NET (NETC4), said that there cannot continue to be a regulatory environment in which one single player can provide video service. In the current situation, neither the incumbents nor the entrants can offer service directly. In order for them to be able to offer triple-play, for example, they have to do what the incumbents did: (i) purchase a company with a TVA license (Pay-TV), for example, the purchase of TVA company by Telefônica; (ii) or purchase a Cable TV company (CATV), for example, the purchase of Way-TV by Oi. Finally, he also said that GVT, in moving to expand its telephony network, has suffered from the high costs of municipal taxes, which in some cases reach up to 22% of the rate.

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 10 - Equity Iberia - Brazil

Telefônica (TLPP3 and TLPP4): Telefônica’s Vice President for Strategic and Regulatory Planning, Mauricio Giusti, believes that the company separation generates inefficiency and increases costs for licensees. He also said that this requirement would give rise to something that doesn’t make sense: if the Telefônica concession were sold, for example, the mobile telephony part would also have to be sold.

Oi (TNLP3, TNLP4): with regard to the company separation in the new PGO, Oi president Luiz Eduardo Falco emphasized that the measure, in addition to being illegal, infringing the LGT (General Law of Telecommunications), will increase the price of broad band for Oi by around 10%. This cost, according to him, will be passed along in prices. Furthermore, he estimated, by the end of the concession in 2025, the additional taxes generated by the separation would be on the order of R$3.5 billion. In closing, he defended once again the merger with BrT on the basis of three arguments: (a) the creation of a Brazilian multinational; (b) the generation of a new R&D cycle encouraged by the new business, and (c) the possibility of facing up to the foreign multinationals operating in Brazil, Telmex and Telefônica, with a large group.

ELECTRIC UTILITIES

Equatorial: 2Q08 Results Preview

Company Ticker Rating Target Price Upside Last Price R$ YTD P/E 08E EV/EBTIDA 08E DY 08EEQUATORIAL ON eqtl3 BUY 24.0 57.9% 15.2 - 7.24 3.6 12.8%

Analyst: Gilberto Pereira de Souza - [email protected] (11) 3074 7325Analyst: Alexandre Kogake Claudio - [email protected] (11) 3074 7327

Equatorial will report its results on August 12, 2008 after market close. This is the second quarter in which the company will report consolidated results that include its 25.0% share in Light. To facilitate comparison between the periods, we made a pro forma consolidation of the previous quarters. Energy supply considers 100% of Cemar and 25% of Light.

Table: Result estimates – 2Q08 PREVIEW 2Q08E (a) 1Q08 (b) (a) / (b) 2Q07 (c) (a) / (c) Energy supplied (GWh) 2,033 1,975 2.9% 1,951 4.2%Residential 847 848 -0.1% 801 5.7%Industrial 247 217 14.1% 240 3.1%Commercial 544 534 1.9% 521 4.4%Other segments 395 377 4.8% 389 1.6%

Result (R$ milhões)Net Revenues 543 560 -3.1% 561 -3.3%Part A margin 274 272 0.5% 307 -10.7%gross margin 50.4% 48.6% 1.8 p.p. 54.6% -4.2 p.p.EBIT 132 126 5.3% 169 -21.5%EBITDA 174 165 5.6% 207 -15.9%EBITDA margin 32.1% 29.5% 2.7 p.p. 36.9% -4.8 p.p.Net profit 47 72 -34.3% 117 -59.6%

Source: Equatorial and Espirito Santo Research

We are updating our projections based on Equatorial's 1Q08 results, the latest valuation of Light, and macroeconomic premises. The main reason for raising Equatorial's price target was the change in Light’s price target from R$ 29.20 to R$ 31.10 per share. In the current valuation, Cemar and Equatorial holding represent R$ 16.20 per share and their stake in Light R$ 7.80 per share.

Valuation. Considering the closing price on August 6, 2008, Equatorial (Cemar asset) is currently trading at a net EV/BRR multiple of 1.36x, which is in line with the 1.34x for the energy distributors in our coverage universe (Eletropaulo, Light and Coelce). We believe that Equatorial should trade in higher multiples due to its lower manageable costs in comparison with the reference company (60% of ER) and better growth prospects for the market in its area of concession. Hence, we reiterate our BUY recommendation for Equatorial's shares with the price target of R$24.0 per share and upside potential of 57.9% for the end of 2008.

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 11 - Equity Iberia - Brazil

RETAIL

GPA: 2Q08 Operational Result in Line with Expectations

Company Ticker Rating Target Price Upside Last Price R$ YTD P/E 08E EV/EBTIDA 08E DY 08EPÃO AÇUCAR PN pcar4 NEUTRAL 45.4 22.7% 37.0 8.3 20.4 8.6 1.2%

Analyst: Luiz Carlos Cesta - [email protected] (11) 3074 7322 The Pão de Açúcar Group (GPA) has published its results for 2Q08, reporting EBITDA of R$ 303.7 million (2.3% less than we had estimated) and net earnings of R$ 60 million (23.7% less than we had forecast).

Gross margin 40 bps lower than estimated

The company's gross margin was 40 bps less than we had estimated and 200 bps less than reported in 2Q07. We had already expected some narrowing in margins on an annual comparison given the absorption of the Assai store chain into the main company, as well as the increased participation of non-food sales as a percentage of the total, which have relatively tighter margins (although a higher average ticket). Despite this, the company announced that: (i) maintaining its strategy of competitive prices, (ii) the selling of non-food products at a relatively low price as a consequence of promotions and, (iii) the change in ICMS taxation in the state of São Paulo (which no longer allows deductions from gross revenue to be included in the company's costs), were all responsible for this drop.

Expenses (before tax) lower than estimated

Despite the fact that the incorporation of the Assai chain has reduced the company's gross margins, operational expenses in relation to net revenues have also come down due to the fact that this format operates on a lower expense budget. Thus, operational expenses (before tax) represented 18.4% of net revenues, being in line with our expectations. Compared to 2Q07,operational expenses as a proportion of net sales dropped by 260 bps.

Conclusion

The result for 2Q08 can be considered positive, given that they show a trend of improving margins for the next few quarters. Despite this, we believe that this improvement had to a certain extent been built in to the company's share price. We are therefore maintaining our NEUTRAL recommendation for the shares.

Marisa: 2Q08 Results

Marisa disclosed its earnings for 2Q08, with net revenues of R$ 355.9 million, EBITDA of R$ 71.8 million and net income totaling R$ 29.6 million, numbers slightly higher than average market expectation. The increase in sales through the same stores concept was 5.8% higher than 2Q07, growth under that foreseen by the company for the current year (8-10%), although justifiable by the strong comparison base (SSS in 2Q07 was 22.7%). The negative results in the Northeast region (mainly due to greater selectivity of the Marisa Card in this region due to higher payment default rates), where sales were under the average of the other regions, also contributed to numbers below the guidance. However, according to the company, in the month of July it was possible to observe a two-digit increase in same store sales.

The retail operation posted a net profit of R$ 27.4 million in the period, which represented a slight increase over the R$ 27.2 million recorded in 2Q07. For its part, the Marisa Card operation (financial services) obtained a R$ 2.2 million net profit in 2Q08, compared to a R$ 5.4 million for the same period last year. This improvement was mainly a result of the increase in interest-bearing installment sales and a greater control of Marisa Card losses, which wound up helping the company’s consolidated income, different from 2Q07 and also 1Q08 when the financial services negatively impacted earnings.

R$ Million 2Q08 (a) 1Q08 (c) (a) / (b) 2Q07 (b) (a) / (c)

Net Revenue 355,9 255,8 39,1% 300,1 18,6% Gross Profit 182,0 114,0 59,6% 155,1 17,3% Gross Margin 51,1% 44,6% 6,6 p.p. 51,7% -0,5 p.p. EBITDA 71,8 -8,4 - 54,6 31,5% EBITDA Margin 20,2% -3,3% 23,5 p.p. 18,2% 2,0 p.p. Net Income 29,6 -12,4 - 21,9 35,2% Source: Marisa and BES Securities

The retail operation’s gross margin for the period was 52.3%, a decline of 1.7 p.p. compared to 2Q07’s gross margin. The reduction, according to the company, is justified by Winter product promotions resulting from higher temperatures in 2Q08.

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 12 - Equity Iberia - Brazil

General and administrative expenses of the retail operation went from 5.7% in 2Q07 to 5.0% in the period, as a percentage of net income. Sales expenses in 2Q08 totaled R$ 106.8 million, compared to R$ 86.3 million in 2Q07, an increase of 1.0 p.p., analyzed as a percentage of net revenues.

The Marisa Card was responsible for 60.8% of the Company’s total sales in 2Q08 and, thus, represented a smaller share than registered in 2Q07, when it was 68.0%. This decline was due to the fact that 24% of the total sales area (213,000 m3) of the stores is newer than one year and sales through the Marisa Card have a lower penetration in new stores. It is important to note that the measures taken by the company to correct an aggressive policy of credit acceptance in the past few years are now being perceived in the results of this quarter, where there was better control of payment defaults.

Opinion: Positive. A good result, somewhat above the market consensus, positively impacted by better controls in the financial services division and the availability of credit, although without big surprises in the retail operations.

HEALTH CARE

Medial Saúde: Lower, but not a cause for concern Company Ticker Rating Target Price Upside Last Price R$ YTD P/E 08E EV/EBTIDA 08E DY 08E

MEDIAL ON medi3 BUY 37.7 121.7% 17.0 -26.9 9.1 6.0 1.0%Analyst: Juliana Chu - [email protected] (11) 3074 7320

Medial Saúde published its results for the 2Q08 revealing a poorer operational performance than we had been expecting, but one which did not produce much in the way of concern or surprises. The weaker result was caused for the most part by a higher medical loss ratio than we had been forecasting, and this attributed by the company to a spill over effect from the 1Q08.

The company’s net premiums for the 2Q08 came to a figure of R$ 459 million, with an adjusted medical loss ratio of 76.5% (utilizing the methodology adopted in the 1Q08), an adjusted EBITDA of R$ 7 million (an EBITDA margin of 1.6%) and an adjusted net profit of R$ 11 million. We had been estimating net premiums of R$ 463 million, a medical loss ratio of 74.4%, an EBITDA figure of R$ 12 million (an EBITDA margin of 2.7%) and an adjusted net profit of R$ 16 million.

It should also be borne in mind that in the 2Q08 for the very first time Medial Saúde gave a breakdown of the results by business units, posting a revenue of R$ 105.5 million and an operating profit of R$ 4.6 million for the hospital division, and a revenue of R$ 14.3 million and an operating profit of R$ 0.7 million for the diagnostics division.

The 2Q08’s results mean that the company maintains its original expectations regarding its medical loss ratio this year in between 70% and 72% using the former methodology and a level of between 68% and 70% on the basis of the new methodology that began to be used from 1Q08 onwards. We also stress that Medial recently implemented a new line of products, concentrated on 2 special lines, and that the impact of this new strategy should be seen over the next few quarters.

Taking into account this performance and the future outlook for the company, we are maintaining our BUY recommendation for Medial Saúde’s shares with a target price of R$ 37.7/share.

TAB. 1: RESULT SUMMARY 2Q08 2Q08E % 1Q08 % 2Q07 %

Plan Members ‘000s 1,403 1,409 -0.4% 1,386 1.3% 1,408 -0.3% R$ million Net Plan Premium 459 463 -0.8% 441 4.1% 394 16.5% Medical Loss Ratio 76.5% 74.4% 63.4% 77.2% Gross Profit 94 109 -13.1% 151 -37.6% 83 14.2% EBITDA adj 7 12 -39.8% 56 -86.9% 2 236.4% EBITDA Margin adj 1.6% 2.7% 12.8% 2.2% Net Profit (8) (4) 93.7% 24 -131.3% (6) 18.8%

Adjusted Net Profit 11 16 -30.5% 44 -75.6% 6 92.9% Source: Company and BES Securities

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 13 - Equity Iberia - Brazil

AVIATION

GOL: Air Traffic Statistics for July/08. Gol Linhas Aéreas Inteligentes published its Air Traffic statistics for July/08 which revealed a 16.9% drop in the supply of seats (ASK) by comparison with June/08, coming out at a figure of 3,591 million. It is our assessment that this decrease is a result of the restructuring of the company’s flight network (that began on March/08) which has led to a reduction in the number of seats offered (ASK) both on the domestic market as well as on the international one. The number of passengers transported per kilometer flown (RPK) also showed a decrease in both markets by comparison with June/08. However, the smaller drop exhibited in the RPK, meant that in July/08 the company’s total occupation rate came out a figure of 64.7% which is 0.5 p.p. higher than the comparable figure observed for June/08.

Table 1. Air Traffic Statistics in July/08. Operational Data (Consolidated) Jul/08 (a) Jun/08 (b) (a)/(b) Jul/07 (c) (a)/(c) Total System ASK (mm) (1) 3.591 4.320 -16,9% 3.013 19,2% RPK (mm) (2) 2.323 2.774 -16,3% 2.063 12,6% Load Factor 64,7% 64,2% 0,5 p.p. 68,4% -3,8 p.p. Domestic Market ASK (mm) (1) 2.838 3.217 -11,8% 2.267 25,2% RPK (mm) (2) 1.769 2.133 -17,1% 1.565 13,0% Load Factor 62,3% 66,3% -4,0 p.p. 69,1% -6,7 p.p. International Market ASK (mm) (1) 753 1.103 -31,7% 747 0,9% RPK (mm) (2) 554 641 -13,6% 497 11,4% Load Factor 73,6% 58,1% 15,4 p.p. 66,6% 7,0 p.p.

1 Seat-Kilometer Offered

2 Passenger-Kilometer Transported

Source: the Company

Table 2. Air Traffic Statistics, by company, July/08. GTA Jul-08 Jun-08 % ASK (mm) 2.664 3.419 -22,1% RPK (mm) 1.713 2.234 -23,3% Load Factor 64,3% 65,4% -1,1 p.p. VRG Jul-08 Jun-08 ASK (mm) 927 901 2,9% RPK (mm) 610 540 13,0% Load Factor 65,8% 59,9% 5,9 p.p.

Source: the Company

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 14 - Equity Iberia - Brazil

Graph 1. Change in the 12-month Occupation Rate.

-500

1.0001.5002.0002.5003.0003.5004.0004.5005.000

jul/07

ago/0

7se

t/07

out/0

7

nov/0

7

dez/0

7jan

/08fev

/08

mar/08

abr/0

8

mai/08

jun/08

jul/08

50%52%54%56%58%60%62%64%66%68%70%

ASK (million) RPK (million) Load Factor (Right Axes)

Opinion: This is negative for the company’s shares. Despite the lower growth in the number of seats offered (ASK) the company’s occupation rate posted a mere 0.5 p.p. growth vis-à-vis June/08. We draw attention to the fact that July is a vacation month and that the company’s occupation rate should have registered a greater growth under this comparison basis. Proof of this can be seen by comparing the figures from July/08 with those for July/07 which reveals a 3.8 p.p. drop in the occupation rate.

PULP/PAPER

VCP: Consolidation on the Way Company Ticker Rating Target Price Upside Last Price R$ YTD P/E 08E EV/EBTIDA 08E DY 08EVCP PN vcpa4 BUY 67.8 70.5% 39.8 -32.6 39.5 12.3 1.0%

Analyst: Juliana Chu - [email protected] (11) 3074 7320

VCP has announced the acquisition of the shares of Aracruz held by Arapar (Lorentzen), which can lead to a major step towards the consolidation of Brazil's paper and pulp industry. Assuming that the corporate restructuring that is being proposed is carried out, VCP would be on the way to becoming the world’s largest eucalyptus market pulp company.

ACQUISITION: The announcement involves the acquisition of 127,506,500 ordinary shares held by Arapar (Lorentzen), the equivalent to 28% of the ON shares of Aracruz and 12.4% of the company's total shares, by VCP and Votorantim Industrial (VDI).

PRICE: The amount involved in the operation is R$ 2.710 billion, or R$ 21.25/ ON share. VCP has indicated that it has received a commitment from 3 banks (Caylon, Santander and HSBC) for the funding of this operation.

REORGANISATION: VCP is also proposing corporate restructuring, with the aim of merging VCP and Aracruz, which is conditional on Arainvest (Safra) waiving its right of preference and joint sale. Arainvest has 90 days to announce its decision.

It should be borne in mind that the Arainvest group (Safra) holds 127,506,500 ON shares and 27,737,000 PN shares. For the reorganization, VCP has indicated that the swap ratio (taking a DCF valuation) could vary between 0.22 and 0.24 share of VCP for 1.00 share of Aracruz, including both the ON and PN.

SYNERGIES SAVINGS: Synergies savings of around R$ 4.5 billion have been indicated, which according to VCP should be mainly obtained through restructuring, in other words 80% of these savings is dependent on the merging of the two companies. This figure was calculated, considering aspects involving procurement, logistics, capital expenditure, etc.

OUR OPINION: We consider the acquisiton, as well as corporate restructuring, as being positive for the companies, particularly VCP. As a consequence, we are reiterating our BUY recommendation for the shares of VCP and Aracruz. However, we point out that Aracruz's share performance is likely to be linked to the swap ratio indicated by VCP, which leads us to recommend a BUY recommendation for the shares of Aracruz only if the price of the share is less than 0.24x to 0.22x of the price of VCP.

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 15 - Equity Iberia - Brazil

REAL ESTATE

Cyrela Commercial Properties: 2Q08 Result

highlights 2Q08(a) 1Q08(b) (a)/(b) 1H08 (c) 1H07 (d) (c)/(d) Net Revenue 24.9 23.6 5.5% 48.5 37.1 30.7% Gross Profit 22.3 21.4 4.2% 43.7 27.0 61.9% Gross Margin 89.6% 90.7% -1.1 b.p. 90.1% 72.8% +17.3 b.p. EBITDA 20.3 19.0 6.8% 39.3 25.2 56.0% EBITDA Margin 81.5% 80.5% +1.0 b.p. 81.0% 67.9% +13.1 b.p. Net Income 8.3 7.5 10.7% 15.7 2.1 647.6% Net Margin 33.3% 31.8% +1.6 b.p. 32.4% 5.7% +26.7 p.p.

Source: Company.

* The company held its IPO in the first half of 2007, so there are no comparative figures relative to the 1Q07

The main 2Q08 highlights were: (1) the increased weight of the office buildings segment, whose share of gross revenue climbed from 54.2%, in the 1Q08, to 55.8%, with the addition of two new properties to the portfolio; and (2) the reduced vacancy rate, which fell from 8.3%. in the 1H07, to just 0.4% in the 2T08, reflecting greater sector demand for such developments.

The narrowing of the gross margin was chiefly due to the 127.7% quarter-over-quarter upturn in mall leasing costs to R$ 1.2 million, while the healthier EBITDA margin was due to the reduction in administrative expenses, which fell by 21.7% in the same period, closing the 2Q08 at R$ 1.8 million.

The company’s greatest risk lies in the concentration of leasing contract renewals in any given period. Currently, maturities are concentrated in 2011 (22%) and 2013 (39%), with 2008, 2009 and 2010 accounting for 3%, 12% and 15%, respectively.

In addition to its results, CCP announced an agreement with AMB Property Corporation to develop projects in Brazil’s industrial segment. The two companies will retain 50% each of the new venture, but no further details are available as yet. The industrial leasing segment accounts for around 6.7% of CCP’s total revenue.

Abyara/Brasil Brokers: Details of the Acquisition of Brasil Brokers News: Brasil Brokers has reached a deal to acquire a controlling interest (51%) in Abyara Intermediação Imobiliária (Abyara’s property brokerage, consulting and advisory assets), with an option to acquire the remaining 49% over the next three years (14.5% in the first and second years and 20% in the third year). The total value of the acquisition is R$ 250 million, with a down payment of R$ 150 million and the payment of R$ 50 million within 120 days and R$ 50 million within 180 days. The transaction will be made in two phases: in the first, BR Brokers will subscribe R$ 176 million in stock issued by Abyara Brokers (the new company to be constituted following the acquisition – see Chart 1). In the second, Brasil Brokers will buy the stock that Abyara Planejamento Imobiliário holds in Abyara Brokers over a period of three years if it exercises the put and call options guaranteed to each other under the agreement. Another important aspect of the transaction is the need for the new company, Abyara Brokers, to pay out 100% of its net income as dividends after one year of operations.

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 16 - Equity Iberia - Brazil

Bear in mind that the earn-out process presented for 2009 and 2010 will be based on the net income of Abyara Brokers in the previous four quarters and the P/E multiple of Brasil Brokers in the previous 60 trading sessions, with the application of a 35% discount on both figures. The potential acquisition in 2011 will follow the same methodology for the two previous years, except that it will use the average net income and average P/E multiple of the periods to calculate the exercise price.

Therefore, if we consider that the new company may be fully acquired by Brasil Brokers after the last earn-out phase, we estimate the 2007 results of the company together with the operations of Brasil Brokers as follows:

*At end of earn-out process.

Comment: Our opinion is that the news is positive for Brasil Brokers, but negative for Abyara.

For Brasil Brokers, the synergy gains will be captured by the addition to its operations of R$12.0 billion in potential sales and 1,158 brokers. For Abyara, the sale of part of its brokerage operations could adversely impact its results going forward, given that at the close of 2007 the brokerage segment accounted for approximately 27.7% of gross revenue, 91.3% of EBITDA and practically 100% of net income.

Chart 1: Creation of Abyara Broker Chart 2: Potential Acquisition – Sep. 2009

BRASILBROKERS

ABYARA

ABYARABROKERS

R$ 176,0 milionR$ 169.9 milion in financial liabilities

49% 51%

BRASILBROKERS

ABYARA

ABYARABROKERS

Dividends Dividends

34.5% 65.5%

Chart 3: Potential Acquisition – Sep. 2010 Chart 4: Potential Acquisition – Sep. 2011

BRASILBROKERS

ABYARA

ABYARABROKERS

Dividends20% 80%

Dividends

BRASILBROKERS

ABYARA

ABYARABROKERS

Dividends100%

Dividends

Source: Brasil Brokers. Source: Brasil Brokers.

Table 1: Operating Indicators

Indicators 2007 Brasil Brokers Abyara *Abyara Brokers Net Revenue 27,9 64,2 92,1 EBITDA 10,3 32,8 43,1 EBITDA margin 36,9% 51,1% 46,8% Net Income 9,2 27,0 36,2 Net Margin 33,0% 42,1% 39,3%

Backlog to 2009 (R$ Bi) 32,0 12,3 44,3 Launches (R$ MM) 3.199 600 3.799 Sold units (R$ MM) 11.360 2.184 13.544 Contracted Sales (R$ MM) 2.404 598 3.002 Brokers 7.076 1.115 8.191

Source: Companies.

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 17 - Equity Iberia - Brazil

The price paid by Brasil Brokers for Abyara Brokers suggests a value of approximately R$656.8 million for this operation, which indicates an EV/EBITDA ’07 multiple of 20.0x. Lopes is currently trading at roughly 15.7x actual EBITDA in 2007.

We believe that with this operation Abyara is moving forward in its strategy of focusing operations on its property development operations, which the company launched approximately one year ago. Note that Abyara closed 1Q08 with net debt of R$363.5 million.

EDUCATION

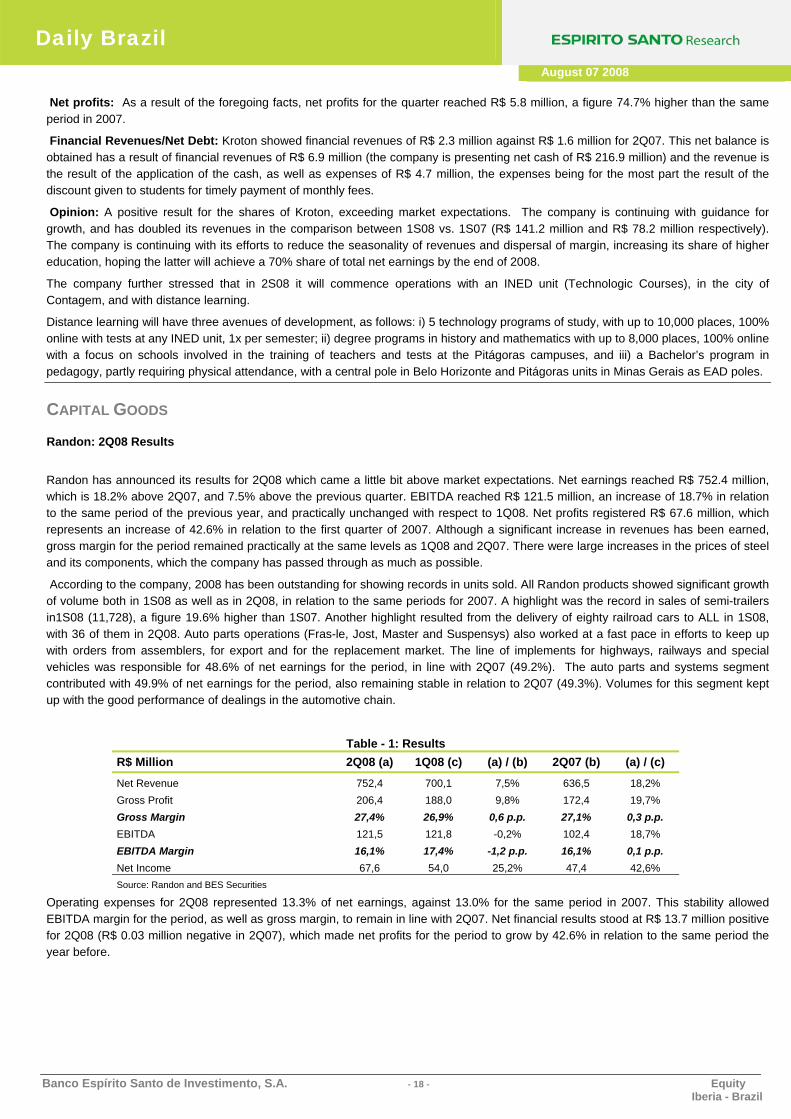

Kroton: 2Q08 Results. Kroton Educacional has announced its results for 2Q08, presenting net revenues of R$ 70.2 million, EBITDA of R$ 8.0 million and net profits of R$ 5.8 million.

Table 1. 2Q08 Results

R$ 000' 2Q08(a) 1Q08(b) (a/b) 2Q07*(c) (a/c) Net Revenue 70.218 70.985 -1,1% 33.085 112,2% K - 12 24.127 37.831 -36,2% 16.356 47,5% Post Secondary 46.091 33.114 39,2% 16.317 182,5% Others 0 40 - 412 - Gross Profit 21.768 39.947 -45,5% 15.341 41,9% Gross Margin 31,0% 56,3% -25,3 p.p. 46,4% -15,4 p.p. EBITDA Adj. 8.011 25.947 -69,1% 5.703 40,5% EBITDA Margin 11,4% 36,6% -25,1 p.p. 17,2% -5,8 p.p. Net Profit 5.815 25.627 -77,3% 3.329 74,7% 0 0 0 0 0

Net Debt (216.910) (287.100)

Avg. Students - Post Secundary 35.442 23.560 50,4% 10.803 228,1% *2T07 Adjusted for IPO expenses (R$ 0,9 milhões)

Source: Company.

As a result of seasonality shown in operations of basic instruction, which concentrates a large part of its revenues in the first quarter of each year, the comparison with 1Q08 is rendered problematic.

Net revenues: Kroton presented net revenues of R$ 70.2 million, which constitutes a growth of 112.2% compared to 2Q07. This growth is the consequence of the increase in the average number of enrolled students, chiefly in the higher education segment, which grew by 228.1% in the same period of comparison. Such growth occurred as a result of the acquisitions made and the opening of new campuses. For the first time, Kroton registered (65.6%) of revenues coming from post secondary in the company’s total net revenues.

Table 2. Composition of net earnings.

Sales Mix 2Q08(a) 1Q08(b) (a/b) 2Q07(c) (a/c) Post

Secundary 65,6% 46,6% 19,0

p.p. 49,3% 16,3

p.p.

K - 12 34,4% 53,3% -

18,9 p.p. 49,4% -

15,1 p.p.

Others 0,0% 0,1% -0,1

p.p. 1,2% -1,2

p.p. Source: Company.

Gross Profits/Gross Margin: The company reported gross profits of R$ 21.8 million, exhibiting growth of 41.9% compared to 2Q07. Gross margin of 31.0% remained 15.4 percentage points below the margin presented in 2Q07 of 46.4%. This decline is related to the process of maturation of the existing campuses, the change in the company’s mix of revenues and the transition of units acquired to Kroton’s operational model.

EBITDA/EBITDA Margin: EBITDA of R$ 8.0 million represented a growth of 40.5% compared to the same period in 2007. In spite of this gain in EBITDA, as a result of the increase in the size of the company, EBITDA margin of 11.4% went down by 5.8 p.p. compared to 2Q07, chiefly represented by greater expenses on sales and personnel, beyond those noted above, as a result of the absorption and inauguration of new units.

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 18 - Equity Iberia - Brazil

Net profits: As a result of the foregoing facts, net profits for the quarter reached R$ 5.8 million, a figure 74.7% higher than the same period in 2007.

Financial Revenues/Net Debt: Kroton showed financial revenues of R$ 2.3 million against R$ 1.6 million for 2Q07. This net balance is obtained has a result of financial revenues of R$ 6.9 million (the company is presenting net cash of R$ 216.9 million) and the revenue is the result of the application of the cash, as well as expenses of R$ 4.7 million, the expenses being for the most part the result of the discount given to students for timely payment of monthly fees.

Opinion: A positive result for the shares of Kroton, exceeding market expectations. The company is continuing with guidance for growth, and has doubled its revenues in the comparison between 1S08 vs. 1S07 (R$ 141.2 million and R$ 78.2 million respectively). The company is continuing with its efforts to reduce the seasonality of revenues and dispersal of margin, increasing its share of higher education, hoping the latter will achieve a 70% share of total net earnings by the end of 2008.

The company further stressed that in 2S08 it will commence operations with an INED unit (Technologic Courses), in the city of Contagem, and with distance learning.

Distance learning will have three avenues of development, as follows: i) 5 technology programs of study, with up to 10,000 places, 100% online with tests at any INED unit, 1x per semester; ii) degree programs in history and mathematics with up to 8,000 places, 100% online with a focus on schools involved in the training of teachers and tests at the Pitágoras campuses, and iii) a Bachelor’s program in pedagogy, partly requiring physical attendance, with a central pole in Belo Horizonte and Pitágoras units in Minas Gerais as EAD poles.

CAPITAL GOODS

Randon: 2Q08 Results

Randon has announced its results for 2Q08 which came a little bit above market expectations. Net earnings reached R$ 752.4 million, which is 18.2% above 2Q07, and 7.5% above the previous quarter. EBITDA reached R$ 121.5 million, an increase of 18.7% in relation to the same period of the previous year, and practically unchanged with respect to 1Q08. Net profits registered R$ 67.6 million, which represents an increase of 42.6% in relation to the first quarter of 2007. Although a significant increase in revenues has been earned, gross margin for the period remained practically at the same levels as 1Q08 and 2Q07. There were large increases in the prices of steel and its components, which the company has passed through as much as possible.

According to the company, 2008 has been outstanding for showing records in units sold. All Randon products showed significant growth of volume both in 1S08 as well as in 2Q08, in relation to the same periods for 2007. A highlight was the record in sales of semi-trailers in1S08 (11,728), a figure 19.6% higher than 1S07. Another highlight resulted from the delivery of eighty railroad cars to ALL in 1S08, with 36 of them in 2Q08. Auto parts operations (Fras-le, Jost, Master and Suspensys) also worked at a fast pace in efforts to keep up with orders from assemblers, for export and for the replacement market. The line of implements for highways, railways and special vehicles was responsible for 48.6% of net earnings for the period, in line with 2Q07 (49.2%). The auto parts and systems segment contributed with 49.9% of net earnings for the period, also remaining stable in relation to 2Q07 (49.3%). Volumes for this segment kept up with the good performance of dealings in the automotive chain.

Table - 1: Results R$ Million 2Q08 (a) 1Q08 (c) (a) / (b) 2Q07 (b) (a) / (c)

Net Revenue 752,4 700,1 7,5% 636,5 18,2% Gross Profit 206,4 188,0 9,8% 172,4 19,7% Gross Margin 27,4% 26,9% 0,6 p.p. 27,1% 0,3 p.p. EBITDA 121,5 121,8 -0,2% 102,4 18,7% EBITDA Margin 16,1% 17,4% -1,2 p.p. 16,1% 0,1 p.p. Net Income 67,6 54,0 25,2% 47,4 42,6% Source: Randon and BES Securities

Operating expenses for 2Q08 represented 13.3% of net earnings, against 13.0% for the same period in 2007. This stability allowed EBITDA margin for the period, as well as gross margin, to remain in line with 2Q07. Net financial results stood at R$ 13.7 million positive for 2Q08 (R$ 0.03 million negative in 2Q07), which made net profits for the period to grow by 42.6% in relation to the same period the year before.

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 19 - Equity Iberia - Brazil

For 2008, the company intends to invest R$ 250.0 million, a large part of it in increasing production capacity, a level 27% greater than that invested in 2007 (R$ 196.5 million), thus demonstrating confidence in the expansion of its business. Let us recall that in 1S08 R$ 98.5 million were entered as investment, against R$ 76.3 million in 1S07.

Opinion: Positive. Strong results. The automotive chain continues to harvest the fruits of the expansion of the economy. Randon's expectations for 2S08 point towards a promising semester, which is at the same time challenging, in view of the waiting list for implements and trucks caused by the increase in orders, in addition to the new forecast of a record agricultural harvest. Among these challenges, the company has listed inflationary pressure in the supply chain and inversion of the curve of the interest rate.

OTHERS

ANFAVEA: Very positive Jul/08 News: The National Association of Vehicle Manufacturers (ANFAVEA) released the results regarding the performance of the automotive industry for Jul/08. According to ANFAVEA, the commercialization of new vehicles achieved 288.1 thousand units, which represents a 12.5% increase comparing to previous month and 32.5% increase comparing to Jul/07. From Jan/08 to Jul/08, the automotive industry has achieved 1.7 million units commercialized, which represents an impressive 30.4% growth against the same period of previous year (1.3 million). The flex-fuel vehicles, which can run either with gasoline or ethanol (or any proportion of both) represented 87.6% of the total vehicles sold during 2008.

Opinion. Positive. The numbers for Jul/08 disclosed by ANFAVEA confirm an excellent moment that the whole automotive industry has been experiencing. We remember that such 30.8% growth until Jul/08 is well above the official guidance provided by ANFAVEA, which comprises growth around 24.0% for the industry in 2008. We believe such performance reported in Jul/08 may be received as positive not only for the automotive industry, but for companies from different sectors such as: Steel (Usiminas e CSN), Transports (Tegma) and Sugar & Ethanol (Cosan, Sao Martinho and Guarani).

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 20 - Equity Iberia - Brazil

MACRO CALENDAR

Brazil

Date Local Time (BZ) Indicator Reference BES Estimates Consensus Last08-Aug 08:00 AM FGV CPI IPC-S AUG 7 0.53% - - 0.53%08-Aug 08:00 AM FGV Preview Inflation IGP-M AUG 7 0.14% - - 1.76%08-Aug 09:00 AM IBGE Inflation IPCA (MoM) JUL 0.55% 0.60% 0.74%08-Aug 09:00 AM IBGE Inflation IPCA (YoY) JUL 6.39% - - 6.06%08-Aug 09:00 AM IBGE Inflation INPC (MoM) JUL 0.60% - - 0.91%

International

Date Local Time (BZ) Indicator Reference BES Estimates Consensus Last07-Aug 08:00 AM UK BOE ANNOUNCES RATES AUG 7 - - 5.00% 5.00%07-Aug 08:45 AM EC ECB Announces Interest Rates AUG 7 - - 4.25% 4.25%07-Aug 09:30 AM US Initial Jobless Claims AUG 2 - - 420K 448K07-Aug 09:30 AM US Continuing Claims JUL 26 - - 3265K 3282K07-Aug 11:00 AM US Pending Home Sales MoM JUN - - -1.0% -4.7%07-Aug 04:00 PM US Consumer Credit JUN - - $6.8B $7.8B08-Aug 09:30 AM US Nonfarm Productivity 2Q P - - 2.5% 2.6%08-Aug 09:30 AM US Unit Labor Costs 2Q P - - 1.4% 2.2%08-Aug 11:00 AM US Wholesale Inventories JUN - - 0.6% 0.8%

Source: Bloomberg, BES Investimento.

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 21 - Equity Iberia - Brazil

CORPORATE CALENDAR Company Date Events Detail

TIM 7-Aug 2Q08 Release Before Market Opening

TIM 7-Aug Conference Call 2Q08 13h00 Portuguese / 11h00 English

CVRD 7-Aug Conference Call 2Q08 11h00

Totvs 7-Aug Conference Call 2Q08 15h00 Portuguese / 13h00 English

Randon 7-Aug Conference Call 2Q08 -

Cteep 7-Aug 2Q08 Release -

DASA 7-Aug 2Q08 Release After Market Closing

Grupo Pão de Acúcar 7-Aug Conference Call 2Q08 14h00 Portuguese / English

B2W 7-Aug 2Q08 Release -

Kroton 7-Aug 2Q08 Release -

Brasil Ecodiesel 7-Aug 2Q08 Release -

Rodobens 7-Aug Conference Call 2Q08 10h00 Portuguese / 12h00 English

Camargo Corrêa 7-Aug Conference Call 2Q08 14h00 Portuguese / 13h00 English

Unibanco 7-Aug 2Q08 Release SP

BRMALLS 7-Aug Conference Call 2Q08 15h00 Portuguese / 16h00 English

Braskem 8-Aug Conference Call 2Q08 -

Ultrapar 8-Aug Conference Call 2Q08 -

B2W 8-Aug Conference Call 2Q08 -

Cesp 8-Aug 2Q08 Release After Market Closing

Kroton 8-Aug Conference Call 2Q08 -

Alpargatas 8-Aug 2Q08 Release -

Brasil Ecodiesel 8-Aug Conference Call 2Q08 -

Bovespa 8-Aug 2Q08 Release SP

Light 8-Aug 2Q08 Release After Market Closing

Iguatemi 11-Aug 2Q08 Release After Market Closing

Petrobras 11-Aug 2Q08 Release After Market Closing

Suzano Petroquímica 11-Aug 1Q08 Release -

Agrenco 11-Aug 2Q08 Release -

CCR 11-Aug 2Q08 Release -

Cemig 11-Aug 2Q08 Release After Market Closing

Globex 11-Aug 2Q08 Release After Market Closing

Pine 11-Aug 2Q08 Release SP

Banco ABC 11-Aug 2Q08 Release SP

Banco Paraná 11-Aug 2Q08 Release SP

Positivo 12-Aug 2Q08 Release -

Amil 12-Aug 2Q08 Release -

Eletrobras 12-Aug 2Q08 Release -

Embraer 12-Aug Analysts Meeting -

Brascan Residential 12-Aug 2Q08 Release After Market Closing

Braskem 12-Aug Analysts Meeting SP

CPFL 12-Aug 2Q08 Release After Market Closing

Duratex 12-Aug 2Q08 Release -

Amil 12-Aug Conference Call 2Q08 15h00

Agrenco 12-Aug Conference Call 2Q08 -

GOL 12-Aug 2Q08 Release Before Market Opening

GOL 12-Aug Conference Call 2Q08 12h00 English / 13h30 Portuguese

Cemig 12-Aug Conference Call 2Q08 9h00

Globex 12-Aug Conference Call 2Q08 -

Banrisul 12-Aug 2Q08 Release SP

Sofisa 12-Aug 2Q08 Release SP

Light 12-Aug Conference Call 2Q08 16h00

Marfrig 12-Aug 2Q08 Release -

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 22 - Equity Iberia - Brazil

Equatorial 12-Aug 2Q08 Release After Market Closing

Cesp 13-Aug Conference Call 2Q08 10h00 Portuguese / 11h00 English

Eletropaulo 13-Aug 2Q08 Release After Market Closing

CPFL 13-Aug Conference Call 2Q08 11h00

AES Tietê 13-Aug 2Q08 Release After Market Closing

Renner 13-Aug 2Q08 Release After Market Closing

Providência 13-Aug 2Q08 Release -

Petrobras 13-Aug Conference Call 2Q08 -

Multiplan 13-Aug 2Q08 Release After Market Closing

Eletrobras 13-Aug Conference Call 2Q08 -

Copel 13-Aug 2Q08 Release -

Fertilizantes Heringer 13-Aug 2Q08 Release -

ALL 13-Aug Conference Call 2Q08 -

CSU 13-Aug Conference Call 2Q08 11hs Portuguese / 12hs English

Wilson Sons 13-Aug 2Q08 Release -

Positivo 13-Aug Conference Call 2Q08 -

Tractebel 13-Aug 2Q08 Release After Market Closing

Gafisa 14-Aug 2Q08 Release After Market Closing

PDG Realty 14-Aug 2Q08 Release After Market Closing

Company 14-Aug 2Q08 Release After Market Closing

Abyara 14-Aug 2Q08 Release After Market Closing

Unipar 14-Aug 2Q08 Release -

Brasil Brokers 14-Aug 2Q08 Release After Market Closing

Anhanguera 14-Aug 2Q08 Release -

Tempo 14-Aug 2Q08 Release -

Even 14-Aug 2Q08 Release After Market Closing

General Shopping 14-Aug 2Q08 Release After Market Closing

OHL 14-Aug 2Q08 Release After Market Closing

Klabin Segall 14-Aug 2Q08 Release After Market Closing

MRV 14-Aug 2Q08 Release After Market Closing

CCP 14-Aug 2Q08 Release -

Inpar 14-Aug 2Q08 Release After Market Closing

Brasil Brokers 14-Aug 2Q08 Release After Market Closing

Grupo Pão de Acúcar 14-Aug Same-Store-Sales -

Copasa 14-Aug 2Q08 Release -

Equatorial 14-Aug Conference Call 2Q08 14h00 Portuguese / 12h00 English

Ambev 14-Aug 2Q08 Release -

Celesc 14-Aug 2Q08 Release -

Providência 14-Aug Conference Call 2Q08 -

Minerva 14-Aug 2Q08 Release -

Estacio 14-Aug 2Q08 Release -

SEB 14-Aug 2Q08 Release -

Lupatech 14-Aug 2Q08 Release After Market Closing

Grendene 14-Aug 2Q08 Release After Market Closing

Cia Hering 14-Aug 2Q08 Release -

Fertilizantes Heringer 14-Aug Conference Call 2Q08 11h00 Portuguese / 11h00 English

Tegma 14-Aug 2Q08 Release -

Coelce 14-Aug 2Q08 Release -

Wilson Sons 14-Aug Conference Call 2Q08 -

TAM 14-Aug 2Q08 Release Before Market Opening

Cyrela Brazil Realty 14-Aug 2Q08 Release After Market Closing

Rossi Residencial 14-Aug 2Q08 Release After Market Closing

Panamericano 14-Aug 2Q08 Release SP

Cruzeiro do Sul 14-Aug 2Q08 Release SP

Multiplan 14-Aug Conference Call 2Q08 11h45 Portuguese / 10h30 English

Daily Brazil

August 07 2008

Banco Espírito Santo de Investimento, S.A. - 23 - Equity Iberia - Brazil

Usiminas 14-Aug 2Q08 Release Before Market Opening

Renner 14-Aug Conference Call 2Q08 11h00

Marfrig 14-Aug Conference Call 2Q08 -

Eletropaulo 15-Aug Conference Call 2Q08 14h30

AES Tietê 15-Aug Conference Call 2Q08 13h30

Copel 15-Aug Conference Call 2Q08 15h00

Tractebel 15-Aug Conference Call 2Q08 10h00

PDG Realty 15-Aug Conference Call 2Q08 9h00 Portuguese / 11h00 English

Company 15-Aug Conference Call 2Q08 -

Cyrela Brazil Realty 15-Aug Conference Call 2Q08 10h00 Portuguese / 12h00 English

Lopes 15-Aug Conference Call 2Q08 -

Abyara 15-Aug Conference Call 2Q08 -

Brasil Brokers 15-Aug Conference Call 2Q08 -

Anhanguera 15-Aug Conference Call 2Q08 -

MRV 15-Aug Conference Call 2Q08 -

CCP 15-Aug Conference Call 2Q08 -

Inpar 15-Aug Conference Call 2Q08 11h00 Portuguese / 13h00 English

Brasil Brokers 15-Aug Conference Call 2Q08 -

OHL 15-Aug Conference Call 2Q08 11h00 Portuguese / 13h00 English

Grendene 15-Aug Conference Call 2Q08 10h30

Grendene 15-Aug Conference Call 2Q08 10h30

Tegma 15-Aug Conference Call 2Q08 09h00 Portuguese / 10h00 English

TAM 15-Aug Conference Call 2Q08 10h00 Portuguese / 11h30 English

Rossi Residencial 15-Aug Conference Call 2Q08 10h00 Portuguese / 12h00 English

Klabin Segall 15-Aug Conference Call 2Q08 10h00 Portuguese / 12h00 English

Gafisa 15-Aug Conference Call 2Q08 9h00 Portuguese / 11h00 English

General Shopping 15-Aug Conference Call 2Q08 14h00 Portuguese / 15h30 English

Even 17-Aug Conference Call 2Q08 -

SEB 18-Aug Conference Call 2Q08 -

Lupatech 18-Aug Conference Call 2Q08 -

Log-In 18-Aug Conference Call 2Q08 10h00 Portuguese / 11h30 English

Unipar 19-Aug Analysts Meeting SP

ALL 19-Aug Analysts Meeting 11h00

Eletrobras 20-Aug Analysts Meeting -

WEG 20-Aug Analysts Meeting -

Randon 26-Aug Analysts Meeting 18h00

Eletropaulo 27-Aug Analysts Meeting -

Alpargatas 28-Aug Analysts Meeting -

Cia Hering 28-Aug Analysts Meeting -

Even 1-Sep Analysts Meeting SP

Daily Brazil

August 07 2008

EquityIberia - Brazil

SHORT INTEREST

Period: 08/05/08Company Ticker Days Open Average Volume Fluctuation

21 days R$ VolumeKlabin KLBN4 22 24 174.840.128 -0,39%Telesp TLPP4 19 25 79.109.335 1,09%Eletrobras ELET6 18 22 634.593.646 2,12%CPFL Energia CPFE3 17 15 292.700.224 0,11%Celesc CLSC6 11 15 52.962.655 -2,64%Cemig CMIG4 11 12 736.953.895 2,32%Gafisa GFSA3 10 11 288.513.760 -1,38%Telemar-Tele NL Par TNLP4 10 9 276.405.751 4,97%Sabesp SBSP3 10 11 122.055.813 -0,79%Perdigao PRGA3 9 8 286.550.611 4,22%

10 LARGEST OPEN POSITIONS

Source: Espirito Santo Research e CBLC

Period: 08/05/08Company Ticker Volume Fluctuation

R$ VolumeSAO MARTINHO SMTO3 14.636.562 -59,08%Porto Seguro PSSA3 25.091.582 -13,12%B2W Global BTOW3 123.497.239 -8,59%Natura NATU3 101.052.167 -7,49%Comgas CGAS5 35.582.041 -7,46%

OPEN POSITIONS - 5 HIGHEST DECREASES*

Source: Espirito Santo Research, CBLC and Economática. *Variations in companies with a minimum of 3 days open

Days Open

45367

Period: 08/05/08Company Ticker Volume Fluctuation

R$ VolumeUniverso Online UOLL4 6.878.323 16,84%Copasa MG CSMG3 24.184.198 5,64%Telemar-Tele NL Par TNLP4 276.405.751 4,97%Positivo POSI3 10.918.417 4,71%AES Tiete GETI4 30.428.723 4,62%

Source: Espirito Santo Research, CBLC and Economática. *Variations in companies with a minimum of 3 days open

OPEN POSITIONS - 5 HIGHEST INCREASES*

Days Open

4

36

103

EquityIberia - Brazil

DAILY BRAZIL Espírito Santo Research

August 07 2008

SHORT INTEREST

OPEN POSITION - IBRX 100 Period: 08/05/08Ticker Name Open Volume Average Ticker Name Open Volume Average Ticker Name Open Volume Average