data import for successful 2017 reporting slide decks and recordings from past aca user group...

TRANSCRIPT

Data Import for Successful 2017 ReportingUsing Integrity Data’s ACA Compliance Solution

For Importing DataOctober 24, 2017

Agenda`

• Resources:• Knowledge Base• ACA User Group• Support• Webinars

• DEMO’s• KB Articles• Data Import

• Microsoft Dynamics GP Cloud Connector• Q&A• ACA Service Hours Scenarios

2© Integrity Data 2016. All rights reserved.

Resources

3

4

Affordable Care Act reporting FAQs on Integrity Data’s site:• Go to http://www.integrity-data.com/knowledge-base/• Then click on ‘Support >> Knowledge Base’

5

Affordable Care Act reporting FAQs on Integrity Data’s site (cont):

6

Find slide decks and recordings from past ACA User Group lessons on this page:http://www.integrity-data.com/aca-user-group-content-library

Password: ACAUG

7

A different type of ACA tracking to keep in mind

© Integrity Data 2016. All rights reserved.

Always email this address

[email protected] that we can track

your concern – and see that everyone who must weigh in on the answer can do so.

* Recommended way to get Support questions answered promptly and fully.

Next lessonsin our ACA User Group series

• 2:30 p.m. Eastern• 1:30 p.m. Central• 12:30 p.m. Mountain• 11:30 a.m. Pacific• 9:30 a.m. Alaskan• 8:30 a.m. Hawaiian-Aleutian

November 211095-C Palooza!

DEMO’sIntegrity Data Knowledge Base

Integrity Data ACA Compliance Solution Import

9

Questions from the Demo?

10

Integrity Cloud Connector for Microsoft Dynamics GP

11

Integrity Cloud Connector for Microsoft Dynamics GP

12

Integrity Cloud Connector for Microsoft Dynamics GP

Employee Export

13

Integrity Cloud Connector for Microsoft Dynamics GP

Dependent Export

14

Integrity Cloud Connector for Microsoft Dynamics GP

Transactions Export

15

ACA Service Hours

16

“HOURS” means “hours of service”

In addition to paid hours that are clocked on the job, this includes situations that are not paid but during which the employee is available to the employer.

“FULL-TIME” means

130 hours of service in a month – the monthly equivalent of at least 30 hours of service a week

“Hours” and “Full-time employee”ACA REDEFINITIONS

17

Hours of service – the ACA standard for calculating full-time status

TIME TO INCLUDE:

• Jury duty

• Military deployment

• FMLA absence

• Leave of absence

• Vacation

• Holiday

• Illness

• Incapacity

• Layoff

18 © Integrity Data 2016. All rights reserved.

Required for: Exempt employeesNon-exempt employees

Account for:Hours that an employee is

available to the employer In addition to paid hours on

the job

ACA Service Hours• IRS regulations for ACA enforcement require an employer to find a

“reasonable” method for converting an employee’s time to an hours-of-service equivalent, so that all their time can be accounted for.

19

ACA Service Hours• By the Class – if you are in higher education and have adjunct faculty

members• On-Call Workers• Piecework

• By the Catch – if you are in the fishing industry• By the Haul – if you are in the trucking industry• By the Bin – if you are in the fruit-picking industry• By the Visit – Home Healthcare Worker

• All Unpaid Leaves – FMLA, Jury Duty, Military

20

21

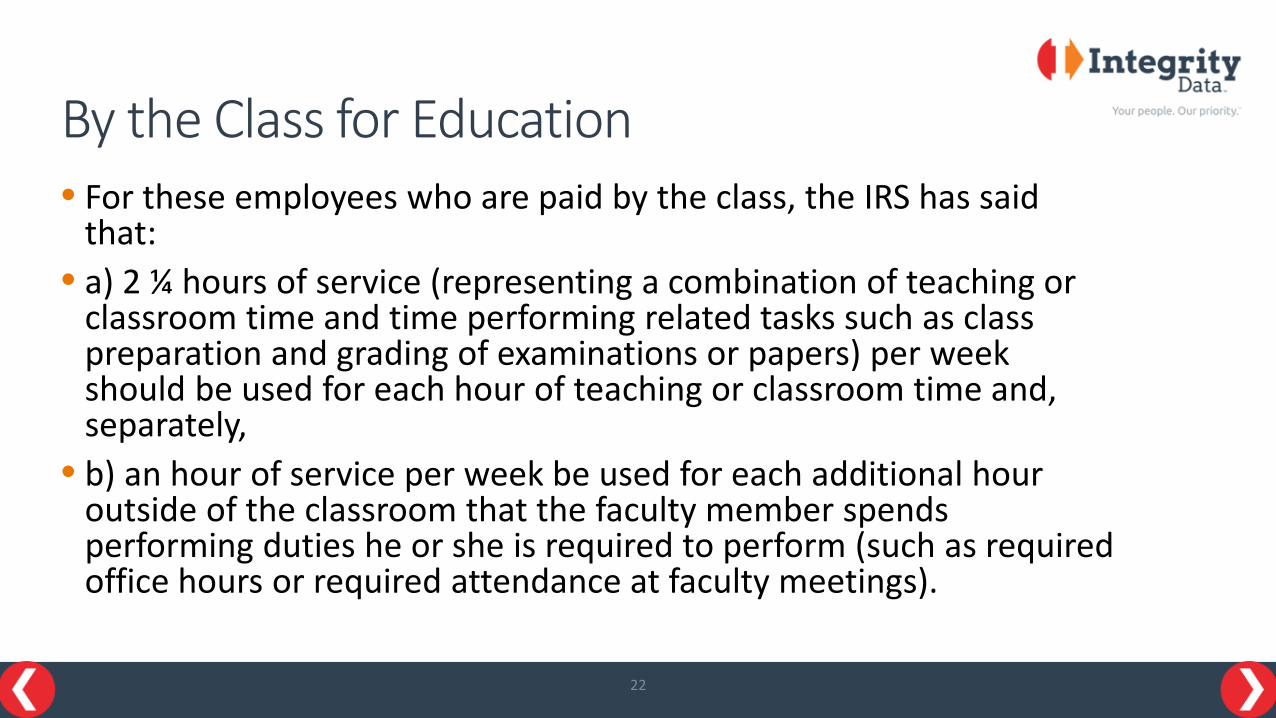

By the Class for Education• For these employees who are paid by the class, the IRS has said

that:• a) 2 ¼ hours of service (representing a combination of teaching or

classroom time and time performing related tasks such as class preparation and grading of examinations or papers) per week should be used for each hour of teaching or classroom time and, separately,

• b) an hour of service per week be used for each additional hour outside of the classroom that the faculty member spends performing duties he or she is required to perform (such as required office hours or required attendance at faculty meetings).

22

23

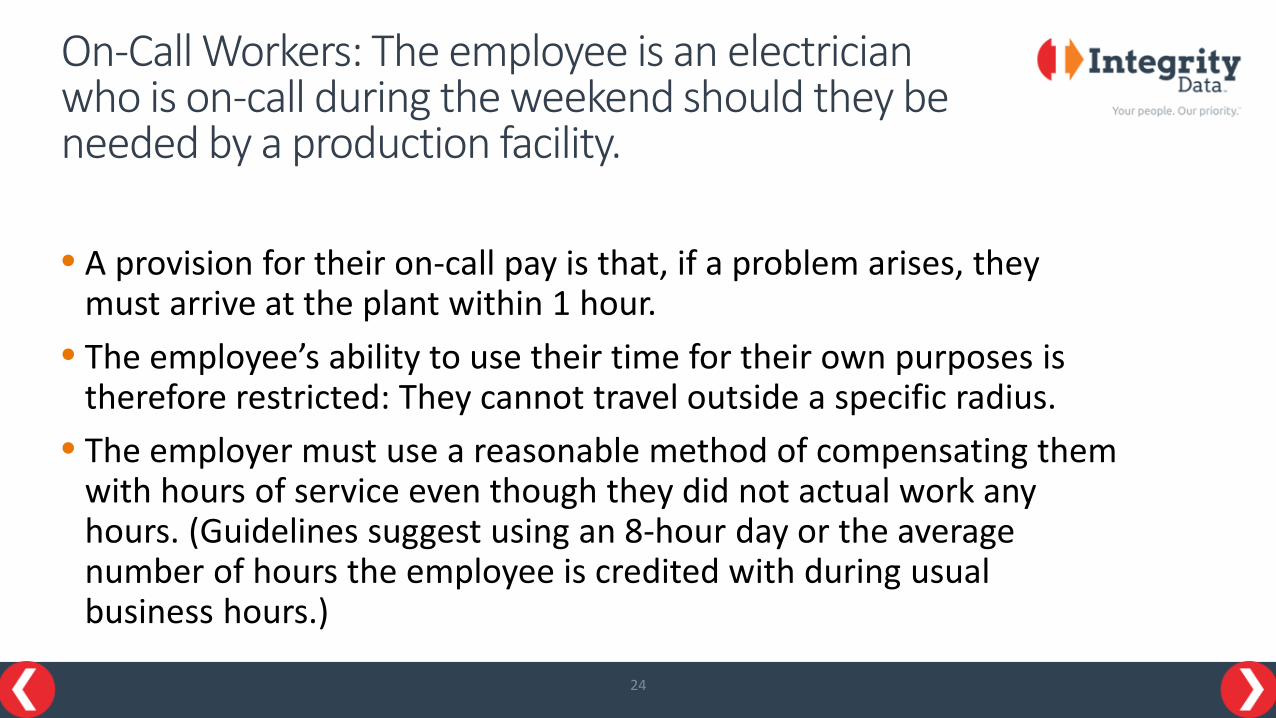

On-Call Workers: The employee is an electrician who is on-call during the weekend should they be needed by a production facility.

• A provision for their on-call pay is that, if a problem arises, they must arrive at the plant within 1 hour.

• The employee’s ability to use their time for their own purposes is therefore restricted: They cannot travel outside a specific radius.

• The employer must use a reasonable method of compensating them with hours of service even though they did not actual work any hours. (Guidelines suggest using an 8-hour day or the average number of hours the employee is credited with during usual business hours.)

24

On-Call Workers: The employee is a software technician who has a laptop and communications access.

• If called up to perform technical support services during the off hours, this employee is required to log into the customer’s site and provide those services.

• During the weekend, this employee is not called upon.• They had no restrictions on their movements and ability to use their

time as they wanted.• No hours of service need to be credited to them.

25

Piecework – By the Catch• On average, boats are out 12 hours a day.• Therefore, a worker is credited 12 hours

times the number of days he or she is out on a boat.

• So the crew of a fishing boat out for four days would each be credited with 48 hours.

26

Piecework – By the Haul

• Ex: 50 miles = 1 hour of service• A trucker who traveled 400 miles in one day would be credited with

8 hours of service • The 50-miles-to-1-hour-of-service conversion is based on such

factors as speed limits and break times.

27

Piecework – By the Bin

• In the case of compensation of apple pickers being compensated by the bin, one company we work with pays $13 a bin and estimates that a bin takes 1 hour to pick.

• So an employee compensated $107.25 in a day would be credited with 8.25 hours. That is, 107.25 divided by 13.

28

Piecework – by the Visit• Paid a Flat Amount for each visit• Determine the average number of hours for the Visit Amount

• A Home Healthcare Worker is paid a flat amount of $75.00 per visit. The average time of a visit is 3 hours of service.

29

All Unpaid Leaves – FMLA, Jury Duty, Military

• Use the average work hours per day from an employees normal working time times the number of days off in a month.

30

All Unpaid Leaves – FMLA, Jury Duty, Military

• Use the average work hours per day from an employees normal working time times the number of days off in a month.

31

Exclusions• Volunteer employees – Hours of bona fide volunteer service for a government

entity or tax-exempt organization do not count as hours of service.• Students performing work-study – Hours of service do not include hours

performed by students as part of the federal work study program or a substantially similar program of a state or political subdivision.

• Members of religious orders – a religious order is permitted to not count as an hour of service work performed by an individual who is subject to a vow of poverty. For this exclusion to apply, the employee must be a member of the religious order and must be performing tasks that are usually required of active members of that order.

• Compensation that is not U.S. source income – Hours of service do not include hours for which an employee receives compensation that is taxed as income from sources outside the United States (generally meaning certain work overseas).

32

COBRA and Continued Coverage

33

COBRA and Continued Coverage • For Self Insured Companies ONLY• For the purpose of 1095-C generation, you have the option of

clicking Continued Coverage for an employee. Continued Coverage includes COBRA benefits or insurance for retired employees.

• For companies that are Fully Insured (BCBS, UnitedHealthcare, etc.) the insurance company issues a 1095-B.

34

COBRA and Continued Coverage

35

Government Entities andIndian Tribal Governments

36

Government Entities and Indian Tribal Governments

• There is no exclusion from the Employer Shared Responsibility provisions for the following entities. • Federal• State• Local• Indian tribal government

37

Government Entities, Indian Tribal Governments – 1094-C Filing• If you are part of a larger government unit and are reporting on your

entity you will need to associate yourself with the larger designated government entity.

• In doing so you will only be required to submit your information and the designated government entity will be required to include your totals in Part III of their submission.

38

Government Entities, Indian Tribal Governments – 1094-C Filing• An example of this scenario is a State agency, the State of Illinois for

example, who processes and reports their payroll separately. The State of Illinois will be required to include the employee total count information in their 1094-C.

• In this scenario, you check the Government Entity box in the ACA Company Setup. Then, you will fill in the State of Illinois information in the Government Entity window. On the 1094-C, Part I, line 1-8, will be your company information taken from the Company Setup window. Line 9-16 will be the State of Illinois information taken from the Government Entity Setup window.

39

Government Entities, Indian Tribal Governments – 1094-C Filing• An example of this scenario is a State agency, the State of Illinois for

example, who processes and reports their payroll separately. The State of Illinois will be required to include the employee total count information in their 1094-C.

• In this scenario, you check the Government Entity box in the ACA Company Setup.

40

Government Entities, Indian Tribal Governments –1094-C Filing

• Then, you will fill in the State of Illinois information in the Government Entity window. On the 1094-C, Part I, line 1-8, will be your company information taken from the Company Setup window. Line 9-16 will be the State of Illinois information taken from the Government Entity Setup window.

41

Employer shared responsibility provisions as they apply to Indian Tribal Governments

42

Addressed in an IRS group call on Friday, May 15, 2015

© Integrity Data 2015. All rights reserved.

“Employer shared responsibility provisions apply to employers that are ALEs, even if employees are exempt from the individual shared responsibility provision – which would include members of a federally recognized Indian tribe.

For purposes of determining whether the employer is an applicable large employer, all employees are counted, subject to the seasonal work exception we talked about, and that's regardless of whether they are exempt from the individual shared responsibility provision. So all applicable large employers with full-time employees who are exempt from the individual shared responsibility provision will be subject to the employer shared responsibility provisions – if they are an ALE.

Employees who are exempt from the individual shared responsibility provision may be eligible for a premium tax credit. And if no full-time employees receive the premium tax credit, the employer won't be subject to the employer shared responsibility payment.

However, if an applicable large employer does not offer coverage to its full-time employees and their dependents, and a full-time employee receives the premium tax credit, they will be liable for the employer shared responsibility payment – categorically based on the number of full-time employees.

So the bottom line is the employer shared responsibility provisions still apply – regardless of whether an employee may be exempt from the individual shared responsibility provision.”

Tim Berger | Tax Law Specialist, Internal Revenue ServiceExempt Organizations Office, Tax Exempt and Government Entities Division | Washington, DC

Would the employer have to ever offer coverage when they may know that their employees have exemption status?

© Integrity Data 2015. All rights reserved.

Seasonal Workers

44

When an employer counts employees to determine ALE status, how do you handle seasonalworkers?• Employee hours are tracked as anyone else• The ONLY time seasonal workers come into play is in calculating an

employer’s• The seasonal worker exception applies so that the employer will

not be treated as an applicable large employer if it reasonably expects: • (1) its workforce to exceed 50 full-time employees (including FTEs) for 120

days or fewer during the current calendar year, and • (2)the employees in excess of 50 employed during such 120-day period to be

seasonal workers.

45

Rehire or New Employee or Returning Employee??

46

Rehire? New Employee? Returning Employee ??• Referred to as breaks in service rule• All employees:

• 13 consecutive weeks• 26 consecutive weeks for educational organization

• Rule of party for short term employees• Returning Employee:

• If a employee who was terminated returns to service and they had previously enrolled in health coverage and their return to service was within a stability period they were eligible for, the employer must honor the remainder of the stability period and offer them continued coverage.

47

Special Rules around Employment Status changes

48

Employee moves from full-time to part-time• Companies cannot automatically drop coverage when employee

classification changes• Employees that go from full-time to part-time will be tested as if they

were a variable-hour employee from the beginning

Employees move from part-time to full-time• Company must offer them coverage no later that the first day of the

month after their first three full months at the new full-time position

Rehire – break-in-service rules• The break-in-service rule applies to both the look-back and the monthly

measurement methods.• Returning employee can be classified a new hire provided they:

1. Had a break in service for 13 consecutive weeks, if the employer is not an educational institution

2. Had a break in service for 26 consecutive weeks, if the employer is an educational institution

3. Had previously been employed for at least 4 weeks and their absence of service was greater than their previous service – Rule of Parity

• Classifying employee as a rehire (new employee) or continuing them as an ongoing employee is at sole discretion of employer.

• The ACA rehire rules do not affect other areas of a company’s benefits. They are limited to health benefits.

Returning employees that would have been in a stability period

• If a returning employee had tested eligible for health coverage and they returned to service within the stability period they would have been entitled to, the company must honor that stability period.

• Company would have until the first day after the employee’s first three full months after return.

Resources

53

Next lessonsin our ACA User Group series

• 2:30 p.m. Eastern• 1:30 p.m. Central• 12:30 p.m. Mountain• 11:30 a.m. Pacific• 9:30 a.m. Alaskan• 8:30 a.m. Hawaiian-Aleutian

November 211095-C Palooza!

55

Find slide decks and recordings from past ACA User Group lessons on this page:http://www.integrity-data.com/aca-user-group-content-library

Password: ACAUG

56

Affordable Care Act reporting FAQs on Integrity Data’s site:• Go to http://www.integrity-data.com/knowledge-base/• Then click on ‘ACA Reporting Requirements’ or ‘ACA Compliance Solution’

57

A different type of ACA tracking to keep in mind

© Integrity Data 2016. All rights reserved.

Always email this address

[email protected] that we can track

your concern – and see that everyone who must weigh in on the answer can do so.

* Recommended way to get Support questions answered promptly and fully.

Questions?

58

Thank you for joining us

To add team members to our notification list for ACA User Group calls:

Email Lindy Belley

www.integrity-data.com888.786.6162

For clarifications on details presented and to suggest topics for future ACA User Group calls:

Email Keith Schmidt

60

Integrity Data’s publications and presentations are designed to make employers aware of IRS reporting requirements under the Affordable Care Act, best practices for compliance with those requirements, and the consequences of noncompliance.

This material is intended to provide accurate information as of the date posted. It is provided with the understanding that neither Integrity Data, nor the authors and presenters, are rendering legal or accounting advice.

With respect to your organization’s decision making for Affordable Care Act compliance, review the information presented with legal counsel specializing in employee benefits law.