debt, deflation, and debacle

DESCRIPTION

by Richard Vague, managing partner of Gabriel Investments, and Robert Hockett, professor of law at Cornell University Law SchoolTRANSCRIPT

Debt, Deflation, and Debacle

Presentation to the GIC Richmond, Virginia

April 9, 2013

0

50

100

150

200

250

300

1945 2011

Debt to GDP

The Raging Debate Between Stimulus and Austerity

on Public Debt

Blue — Federal Debt

Red — Private Debt

Debate tends to omit discussion of private debt

0

10

20

30

40

50

60

70

80

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

U.S. Home Mortgages as a percent of GDP

(in percent)

Mortgage Loans/GDP

Mortgage Loans if Continued 16% Trend

3

Average 16% growth in previous four decades

RUNAWAY LENDING! 68% growth in ten years and 46% growth in six years

$2.5 trillion in excess mortgages vs trend line

Inevitable spate of non-payment after a period of binge lending brought the Great Recession

Higher asset values not a mitigant, true constraint is income

Rapid Increase in Private Debt Caused the Great Recession

Why Does High Debt to GDP Matter?

• If a home or business owner has high levels of debt, reduced capacity for additional spending and investment

• In aggregate, a country’s capacity for growth is constrained if its citizens and businesses collectively are operating at high leverage

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

GDP Non-FinancialPrivate Debt

Total Public Debt Money Supply Trade Tax Receipts

2011 Comparison of Economic Categories (in billions)

5

$9 trillion growth in the last ten years

GDP growth correlates more to private debt growth than government debt growth

-10%

-5%

0%

5%

10%

15%

20%

25%

19

70

19

73

19

76

19

79

19

82

19

85

19

88

19

91

19

94

19

97

20

00

20

03

20

06

20

09

U.S. Growth in GDP, Private Debt, and Public Debt

1970-2011

Growth in GDP

Growth in Private

Growth in Public

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

Japan Growth in GDP, Public Debt, and Private Debt

1990-2010

Growth GDP

Growth Public Debt

Growth PrivateDebt

Also correlates more than consumer or business separately, M2, trade imbalance levels

If runaway private lending caused the Great Recession, did it also lead to the Great

Depression?

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

19

19

19

20

19

21

19

22

19

23

19

24

19

25

19

26

19

27

19

28

19

29

19

30

19

31

19

32

19

33

19

34

19

35

Nominal Private Debt Totals 1919-1935 (in billions)

66% growth 1919-1929

8

80

100

120

140

160

180

200

1 2 3 4 5 6 7 8 9 10 11

Private Debt to GDP Trends prior to the Great Depression and Great Recession

(in percent)

Private Debt/GDP 1920-1930

Private Debt/GDP 1997-2007

Runaway Lending: 40% Private Debt to GDP Growth

If the 1920s and 2000s had 40% private debt growth, how many

OTHER times in the last century has private debt growth been 40% in a

single decade?

0

50

100

150

200

250

19

16

19

19

19

22

19

25

19

28

19

31

19

34

19

37

19

40

19

43

19

46

19

49

19

52

19

55

19

58

19

61

19

64

19

67

19

70

19

73

19

76

19

79

19

82

19

85

19

88

19

91

19

94

19

97

20

00

20

03

20

06

20

09

KEY GRAPH: Private Debt and Public Debt to GDP 1916-2011

(in percent)

Private/GDP

Public Debt/GDP

1916 2011

0

50

100

150

200

2501

91

6

19

19

19

22

19

25

19

28

19

31

19

34

19

37

19

40

19

43

19

46

19

49

19

52

19

55

19

58

19

61

19

64

19

67

19

70

19

73

19

76

19

79

19

82

19

85

19

88

19

91

19

94

19

97

20

00

20

03

20

06

20

09

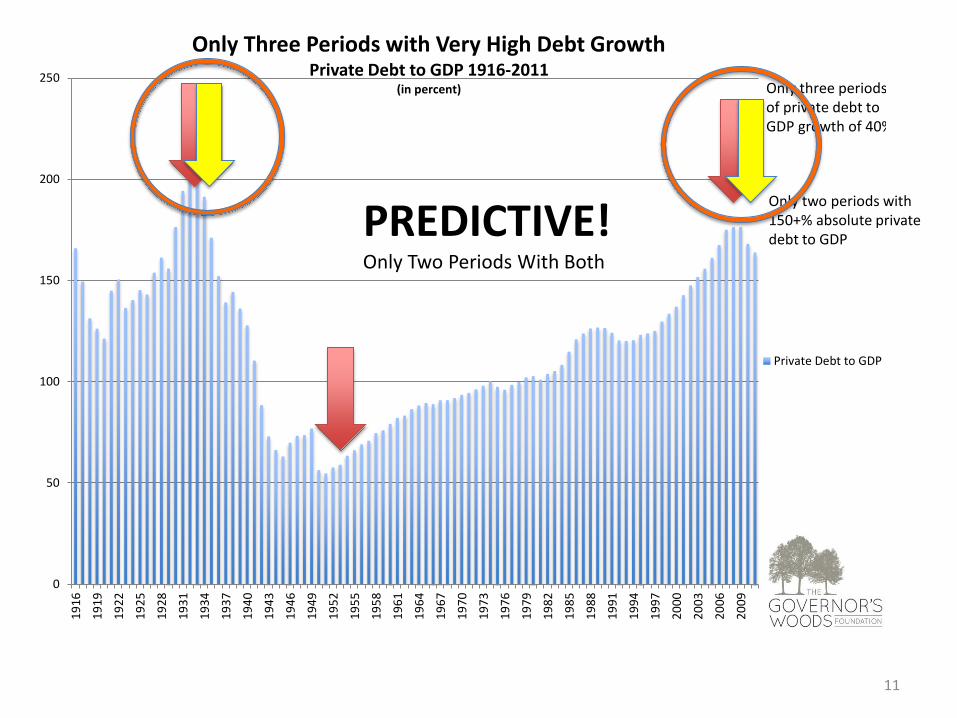

Only Three Periods with Very High Debt Growth Private Debt to GDP 1916-2011

(in percent)

Private Debt to GDP

Only three periods of private debt to GDP growth of 40%

11

Only two periods with 150+% absolute private debt to GDP

PREDICTIVE! Only Two Periods With Both

• GOOD NEWS: we now have a tool for predicting — and preventing — the next major crisis of this magnitude

• But how did we miss something so obvious?

• Because many prevailing economic theories and forecasting models ignore debt as “net zero”

• False comfort from low interest rates

• In addition, we missed it because it is widely held that loan growth is always bullish

• WE ARE STILL WELL ABOVE 150% PRIVATE DEBT TO GDP — and growth is harder when you have high debt

• SO HOW WOULD YOU ADVISE DECREASING OUR HIGH RATIO OF DEBT?

– Paying down debt?

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

1920 1921 1922 1923 1924 1925 1926 1927 1928 1929 1930 1931 1932 1933 1934 1935 1936 1937 1938 1939

Nominal U.S. GDP, Private Debt, and Public Debt 1920-1939 (in billions)

Private Debt

GDP

Public Debt

• Bank runs precipitated loan liquidation

• Attitude of times: Treasury Secretary Mellon said “liquidate labor, liquidate stocks, liquidate farmers, liquidate real estate … it will purge the rottenness out of the system. … Enterprising people will pick up from less competent people.”

• Mellon advocated weeding out “weak” banks

• The single biggest lesson of the Great Depression for economists was to AVOID major debt pay down — a “liquidity crunch”

• Thus, in the 2000s, we again had runaway lending, but no massive debt pay down after the crisis point, so instead of private debt contraction of 25% and unemployment of 25%, it was 3% and 9%

0

5000

10000

15000

20000

25000

30000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Nominal U.S. GDP, Private Debt, and Public Debt Trends 1998 to 2011

(in billions)

Private Debt

GDP

Public Debt

Private Debt/GDP has declined 10% from crisis peak, but is 15% above 2000 and 53% above 1980

• We avoided Depression, but we have a NEW DILEMMA,

– deleveraging contracts GDP, while

– re-leveraging promotes growth, but increases the structural precariousness of the economy and dampens future growth

• EUROZONE CRISIS is also about runaway private debt

• Runaway lending happened in Japan in 1991 — almost 40% private debt growth in ten years then a stock and real estate crash. But no private debt or GDP contraction for 5 years and private debt still at 150% of GDP over 20 years later.

50%

100%

150%

200%

250%

300%

350%

400%

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

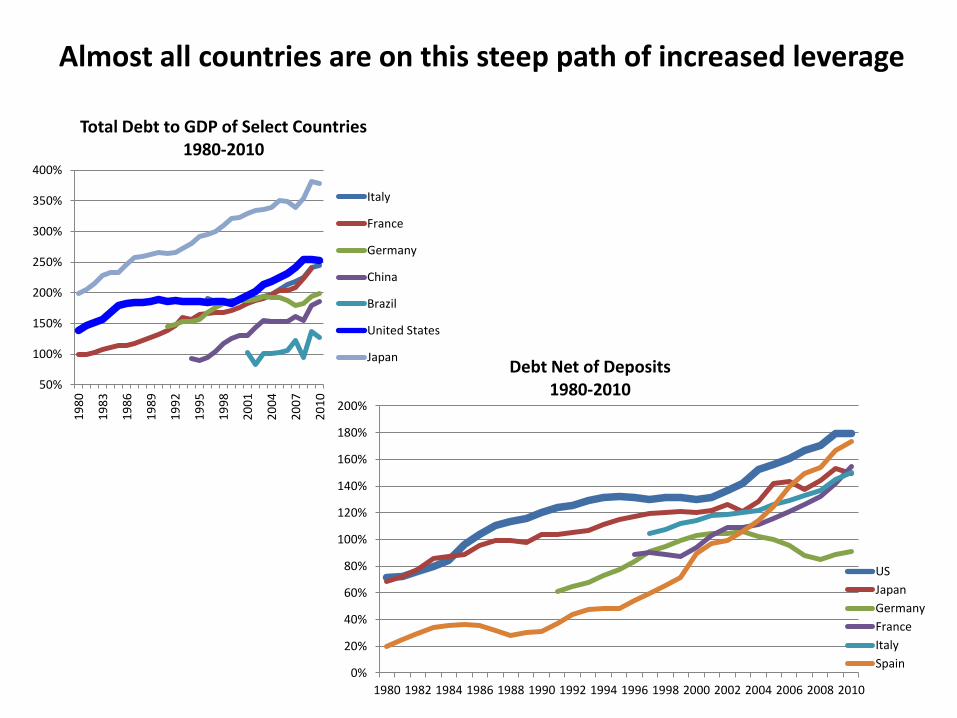

Total Debt to GDP of Select Countries 1980-2010

Italy

France

Germany

China

Brazil

United States

Japan

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Debt Net of Deposits 1980-2010

US

Japan

Germany

France

Italy

Spain

Almost all countries are on this steep path of increased leverage

• SO HOW WOULD YOU ADVISE DECREASING OUR HIGH LEVELS OF DEBT? – Paydown — causes economic contraction

– Getting government debt under control — a must at some point, but does create short-term GDP pressure and does not address private debt levels

– Growth or Inflation – takes 15 to 20 years or more — and bumps up against the dampening effect of debt on growth

– Debt restructuring — obstacle of moral hazard and objections regarding wealth transfer — but a trillion in restructuring is better than a trillion in new stimulus

– Live with it — don’t we always?

Dr. Robert C. Hockett

125.00

135.00

145.00

155.00

165.00

175.00

185.00

195.00

205.00

215.00

225.00

-3.00%

-2.50%

-2.00%

-1.50%

-1.00%

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

Jul-06 Dec-06 May-07 Oct-07 Mar-08 Aug-08 Jan-09 Jun-09 Nov-09 Apr-10 Sep-10 Feb-11 Jul-11 Dec-11 May-12

20

-Cit

y C

om

po

site

Ca

se S

hill

er

Ho

me

Pri

ce I

nd

ex

3-M

on

th M

ov

ing

Av

era

ge

Ch

an

ge

In 2

0-C

ity

Co

mp

osi

te C

ase

Sh

ille

r H

om

e P

rice

In

de

x

20-City Composite Case Shiller Home Price IndexJuly 2006 to May 2012

3 Month Moving Average Change in HPI 20-City Composite HPI

August 2009

June2010

July2011

Post-Bust Home Price Cyclicality

Regional Concentration of High LTV Underwater Mortgages CoreLogic Negative Equity

Sampling of High LTV Zip Code Areas

ZIP Code City State % Underwater % Price Decline

92301 Adelanto CA 64% -70%

93501 Mojave CA 65% -71%

93505 California City CA 72% -71%

33035 Homestead FL 68% -69%

33127 Miami FL 57% -70%

33142 Miami FL 62% -66%

30274 Riverdale GA 85% -71%

30296 Riverdale GA 84% -66%

30297 Forest Park GA 81% -72%

89030 North Las Vegas NV 77% -76%

89101 Las Vegas NV 75% -76%

89106 Las Vegas NV 72% -71%

89115 Las Vegas NV 77% -72%

Employment-to-Population Ratio Trendline

50%

52%

54%

56%

58%

60%

62%

64%

66%

35%

40%

45%

50%

55%

60%

65%

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Employment-to-Population Ratio, 1960-2012

Women's Labor Force Participation (left)

Full-time Employment to Population Ratio (right)

Full-time and Part-time Employment-to-Population Ratio (right)

Source: Bureau of Labor Statistics

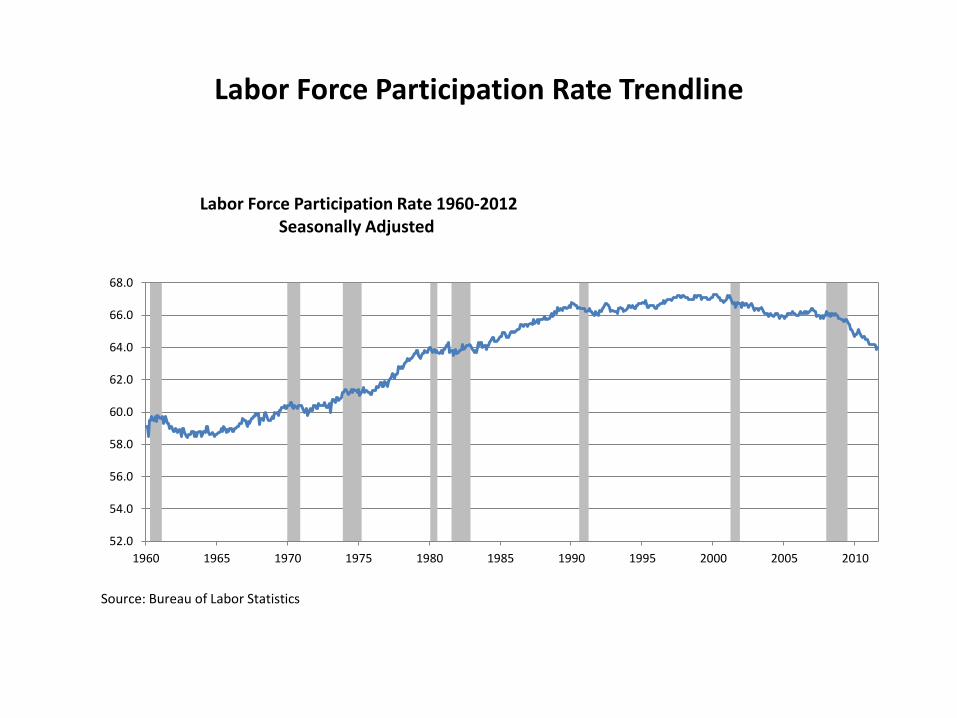

Labor Force Participation Rate Trendline

52.0

54.0

56.0

58.0

60.0

62.0

64.0

66.0

68.0

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Labor Force Participation Rate 1960-2012 Seasonally Adjusted

Source: Bureau of Labor Statistics

Lease Swap

A Resides

B Resides

A Resides

A Resides

B Resides

B Resides

Date 1

Date 2

Date 3

A Owns B Owns

A/B Negative Equity

A/B Bankruptcy

A/B Positive Equity

Structure of Modification Transaction via Eminent Domain

• Investors:

Private &/or Federal

Current MBS

Holders

Eminent

Domain

Trusts

States/

Subunits

PLS Trusts

Overlapping Membership

Good Loans Bad Loans

$

$

$ $

$

New Obligation New Lending

Home-

Owners

Note: The double-headed arrow represents class overlap rather than a flow. The two vertical arrows crossing the dotted line represent a

detour between the “bad loan” and “good loan” arrows.