decision rights and corporate control 5th set of transparencies for tocf

Post on 22-Dec-2015

213 views

TRANSCRIPT

DECISION RIGHTS AND CORPORATE

CONTROL

5th set of transparencies for ToCF

2

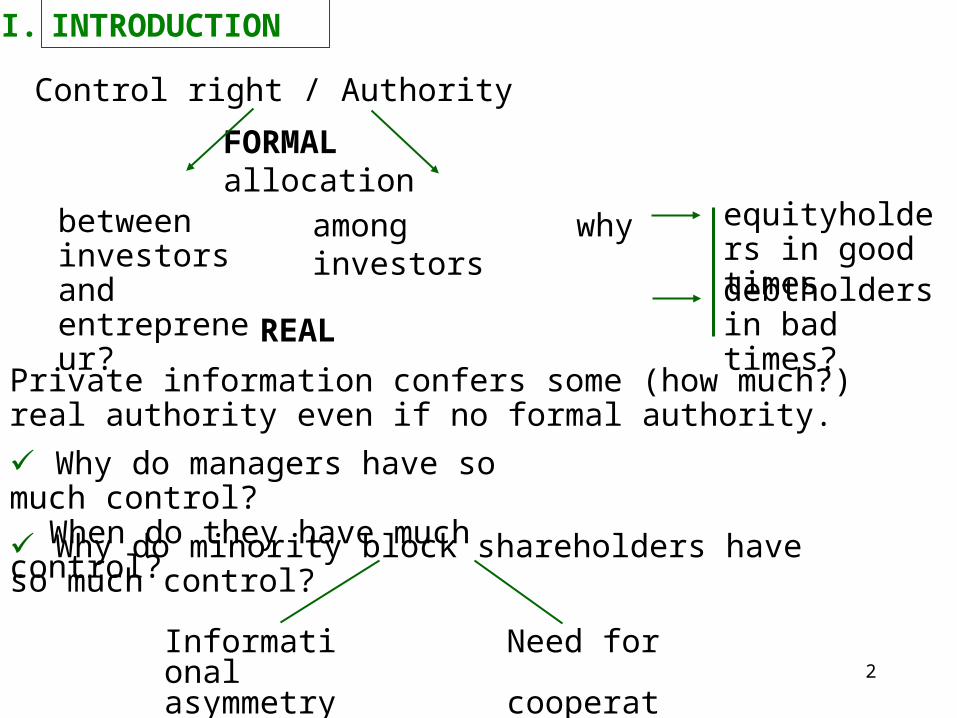

I. INTRODUCTION

Control right / Authority

FORMAL allocation

between investors and entrepreneur?

among investors why equityholders in good timesdebtholders in bad times?REAL

Private information confers some (how much?) real authority even if no formal authority.

Informational asymmetry

Need for cooperation

Why do minority block shareholders have so much control?

Why do managers have so much control?When do they have much control?

3

Action non describable, can’t be contracted upon; but can allocate control right

II. ALLOCATION OF FORMAL AUTHORITY

(Reinterpretation of) Aghion-Bolton 1992

RELINQUISHING CONTROL RIGHTS TO INVESTORS INCREASES PLEDGEABLE INCOME AND THUS BOOSTS DEBT CAPACITY.

investors decide

entrepreneur decides

Example: Fixed investment model

4

Suppose action is first-best inefficient:

Entrepreneur control: bears all of receives only part of R does not take painful (profit-enhancing) action.

Investors control: bear none of select profit-enhancing action.

Or A not sufficient to attract financing, then (if not too large) investor control second-best optimal.

Either A large and then entrepreneur

retains control

5

Reminiscent of costly collateral pledging!

[First-best efficient action two reasons for investor control].

ONE ARGUMENT IN FAVOR OF "SHAREHOLDER VALUE"

6

STRENGTH OF BORROWER’ S BALANCE SHEET

ST decisions collaborators LT investment managerial compensationetc.

MULTIPLE CONTROL RIGHTS:

no funding entrepreneurrelinquishescontrol

entrepreneurretains control

A

K control rights

7

Parameters

8

(maximizes pledgeable income)

relinquish only efficient ones.

Entrepreneur keeps control rights for which

Case #2 (capital constraint)

Case #1 (uninteresting)

9

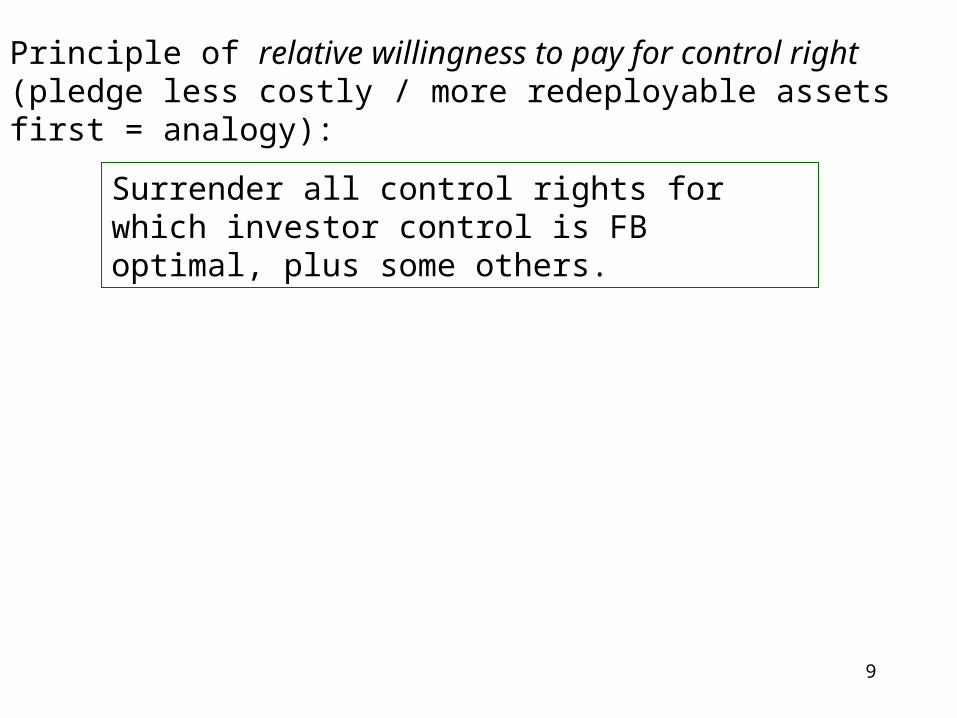

Principle of relative willingness to pay for control right (pledge less costly / more redeployable assets first = analogy):

Surrender all control rights for which investor control is FB optimal, plus some others.

10

ApplicationSTART UP

"BORROWSAGAINST ASSETS"

"BORROWSAGAINST INCOME"

Firm withstrong balancesheet

Firm withweak balancesheet

cash (A) collateralsome safe income stream low private benefit

no cash no collateral no safe income stream

relinquishesrelatively fewcontrol rights (borrows frommarket, bank,...)

relinquishes mostcontrol rights(borrows from venturecapitalist,...)

11

CONTINGENT CONTROL RIGHTS RAISE BORROWING CAPACITY

B

Combined with signal (e.g., ST profit):

In the absence of action (or with a noncontingent action):

(if signal sufficient statistic).

• With a contingent action: entrepreneur control and reward if high signal

12

entrepreneur control and reward if high signal

• With a contingent action: investor control and no reward if low signal

13

Pledgeable income:

Pledgeable income under noncontingent investor control:

is smaller if (interesting case)

14

III. REAL AUTHORITY

Theory often assumes that management has formal right to choose:

investment

dividends / retained earnings

debt / financial structure

next manager when departing CEO

takeover defenses

etc.

inaccurate unintuitive

Yet, management has substantial say in these decisions.Reconciliation: formal and real authority.

15

which rights,

when real authority?

Issue with approach of directly assuming management has formal rights:

[ depends on CORPORATE GOVERNANCE!]

16

INTUITIVE APPROACH

n ex ante identical actions, plus status quo (0,0) only 1 action is "relevant" (others bad)

Suppose entrepreneur

(a) learns

relevant action

(b) proposes the action.Uninformed investors rubberstamp iff

(say, stronger balance sheet) more likely to rubberstamp.

Otherwise deadlock.

identity not known ex ante

furthermore and

17

Ownership concentration and (active) monitoring:

18

STRENGTH OF BALANCE SHEET AND CORPORATE GOVERNANCE

Arm’s lengh relationship (no active monitor)

rubberstampingA STRONGER BALANCE SHEET LEADS TO A LESS

CONFLICTUAL RELATIONSHIP

if investors rubberstamp.(extra term 0 by definition: )

19

Relationship lending

Suppose cost c > 0: active monitor has same information as entrepreneur

criterion:

independent of A.

(second reason for why) relationship lending covaries positively with weakness of balance sheet.

20

MULTIPLE SECURITIES AND OUTSIDE EQUITY

COSTS WELL UNDERSTOOD: Externalities among investors(Jensen-Meckling 1976).

SHAREHOLDERS(OUTSIDE EQUITY) CREDITORS

INSIDERS

D

Debtholders’ payoff

D profit

21

MULTIPLE SECURITIES AS A DISCIPLINING DEVICE

(Dewatripont-Tirole 1994)

LIQUIDATION,

DOWNSIZINGL

FINAL OUTCOME

SECOND EFFORT (CHOICE OF p)

FIRST EFFORT

INTERMEDIATE PROFIT

IR p

0 1-p

POOR INTERMEDIATE PERFORMANCE DEBT CONTROL

LIQUIDATION, INTERFERENCE

FAIR INTERMEDIATE PERFORMANCE EQUITY CONTROL

CONTINUATION

22

Dewatripont’s puzzle :

Tension between

Design of multiple securities in the first place

Facilitating renegotiation among investors

Bondholder trustee and exchange offer institutions.Literature on bankruptcy.