demand for audit and assurance services

TRANSCRIPT

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia

Chapter 1

Demand for audit and assurance

services

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 2

Describe assurance servicesDescribe assurance services

and distinguish audit servicesand distinguish audit services

from other assurance andfrom other assurance and

non-assurance servicesnon-assurance services

provided by public accountantsprovided by public accountants

Learning objective 1

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 3

Assurance servicesAssurance services are are independent professionalindependent professional

services that improve the quality ofservices that improve the quality ofinformation for decision makersinformation for decision makers

Assurance services can beAssurance services can beperformed by public accountants performed by public accountants or a variety of other professionalsor a variety of other professionals

Assurance services

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 4

An An attestation serviceattestation service is a type of assurance is a type of assuranceservice in which the public accounting firm service in which the public accounting firm

issues a written communication that expresses issues a written communication that expresses a conclusion about the reliability of a written a conclusion about the reliability of a written

““assertion” of another partyassertion” of another party

Attestation services

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 5

The business environment often requires The business environment often requires assurance that financial information is assurance that financial information is

reliable and can be ‘trusted’reliable and can be ‘trusted’

Auditors provide attestation services Auditors provide attestation services to achieve this objectiveto achieve this objective

Reason for attestation services

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 6

Audit of historical financial statementsAudit of historical financial statements

Review of historical financial statementsReview of historical financial statements

Other attestation servicesOther attestation services

Attestation services

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 7

Most other assurance services do not meet theMost other assurance services do not meet theformal definition of attestation servicesformal definition of attestation services

The public accountant must be independentThe public accountant must be independent

TheThe public accountantpublic accountant is not required is not required to provide a written reportto provide a written report

The public accountant must provide assurance The public accountant must provide assurance about the relevance and reliability of information, about the relevance and reliability of information, but not the reliability of another party’s assertionbut not the reliability of another party’s assertion

Other assurance services

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 8

There is an increased demand for assuranceThere is an increased demand for assuranceabout computer controls surroundingabout computer controls surroundinginformation transacted electronicallyinformation transacted electronicallyand the security of the informationand the security of the information

related to the transactionsrelated to the transactions

assurance over web site controlsassurance over web site controls

assurance about information system assurance about information system (and web site) reliability(and web site) reliability

Assurance services on information technology

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 9

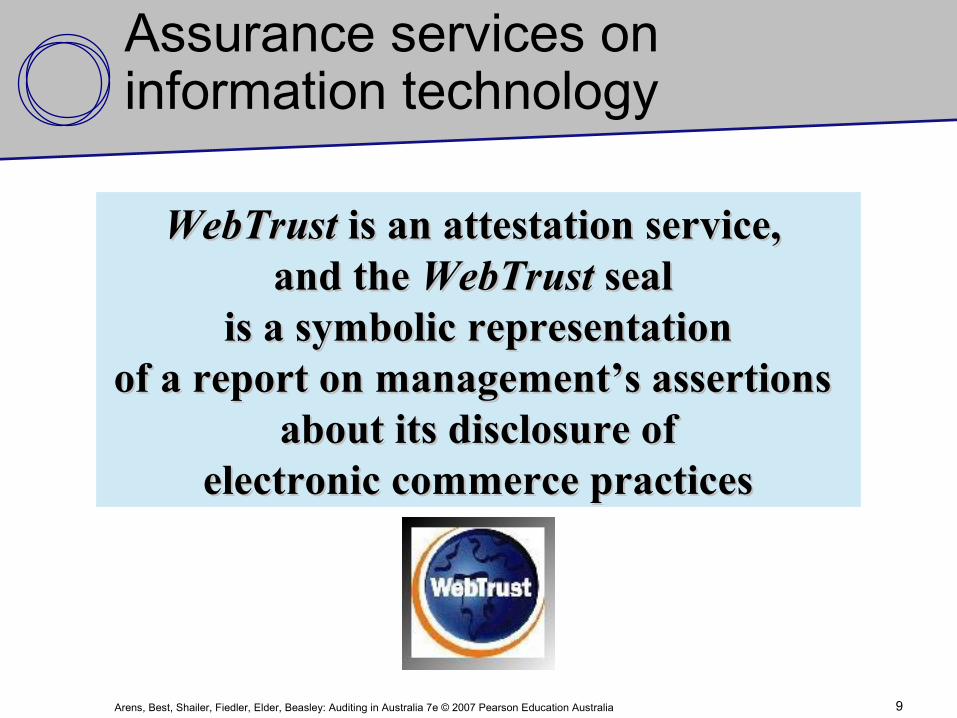

WebTrust WebTrust is an attestation service, is an attestation service, and the and the WebTrust WebTrust seal seal

is a symbolic representationis a symbolic representationof a report on management’s assertions of a report on management’s assertions

about its disclosure ofabout its disclosure ofelectronic commerce practiceselectronic commerce practices

Assurance services on information technology

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 10

SysTrustSysTrust is an attest-type engagement is an attest-type engagement to evaluate and test system reliability into evaluate and test system reliability inareas such as security and data integrityareas such as security and data integrity

Assurance services on information technology

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 11

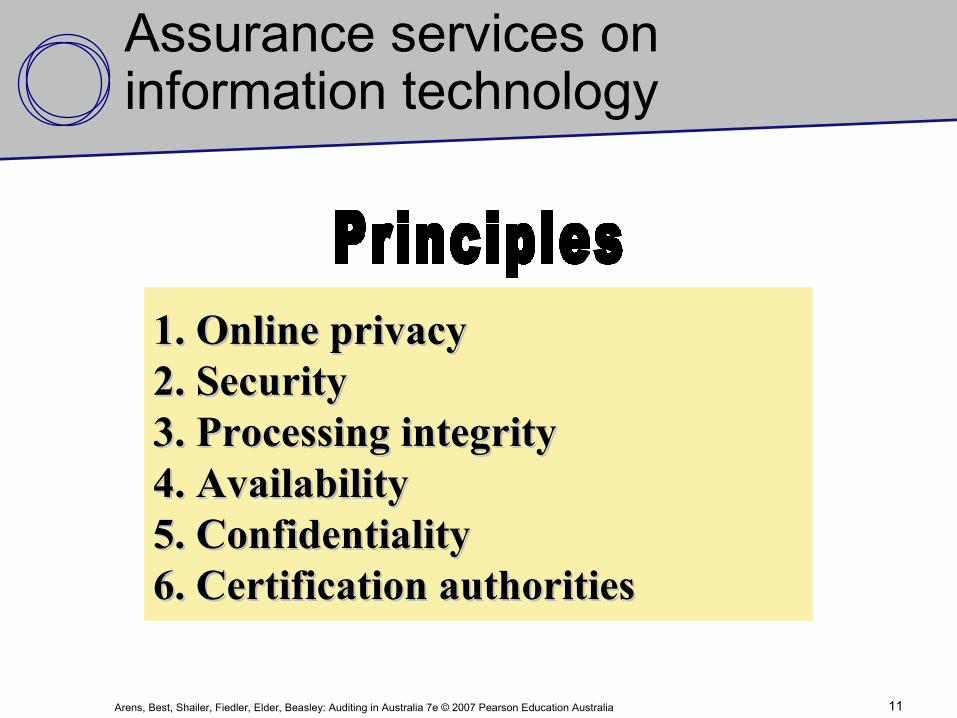

1. Online privacy1. Online privacy2. Security2. Security3. Processing integrity3. Processing integrity4. Availability4. Availability5. Confidentiality5. Confidentiality6. Certification authorities6. Certification authorities

Assurance services on information technology

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 12

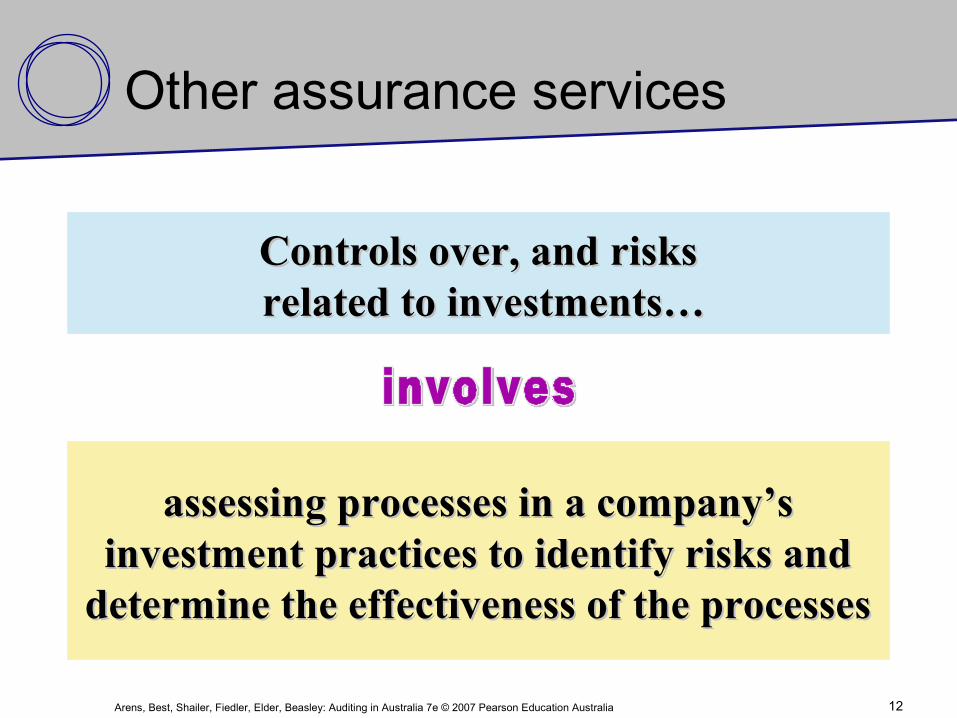

Controls over, and risksControls over, and risks related to investments…related to investments…

assessing processes in a company’sassessing processes in a company’sinvestment practices to identify risks andinvestment practices to identify risks and

determine the effectiveness of the processesdetermine the effectiveness of the processes

Other assurance services

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 13

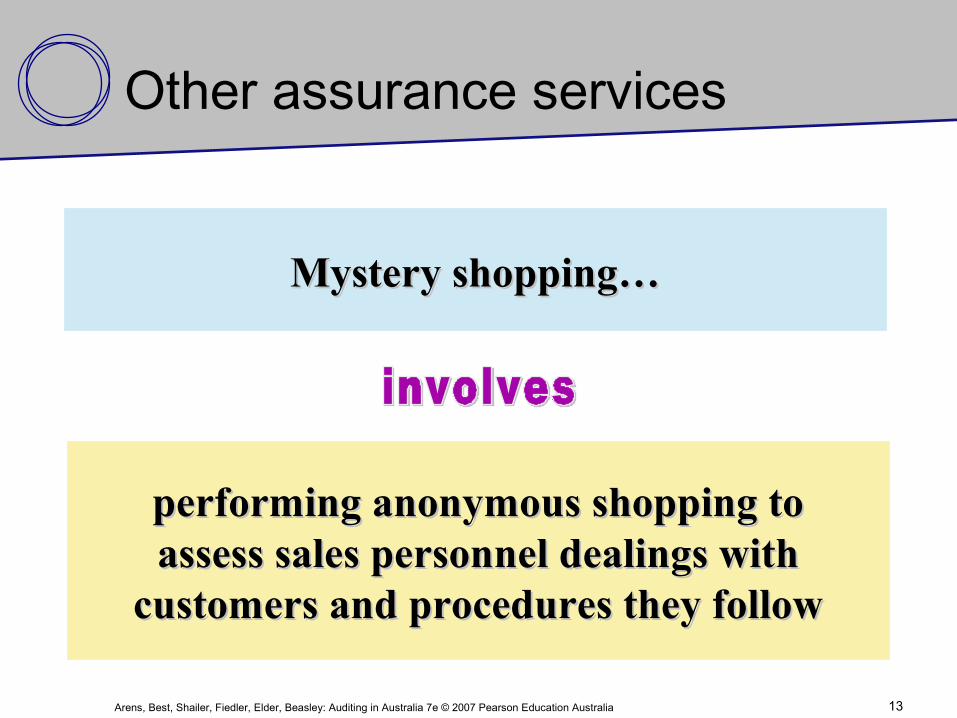

Mystery shopping…Mystery shopping…

performing anonymous shopping toperforming anonymous shopping toassess sales personnel dealings withassess sales personnel dealings with

customers and procedures they followcustomers and procedures they follow

Other assurance services

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 14

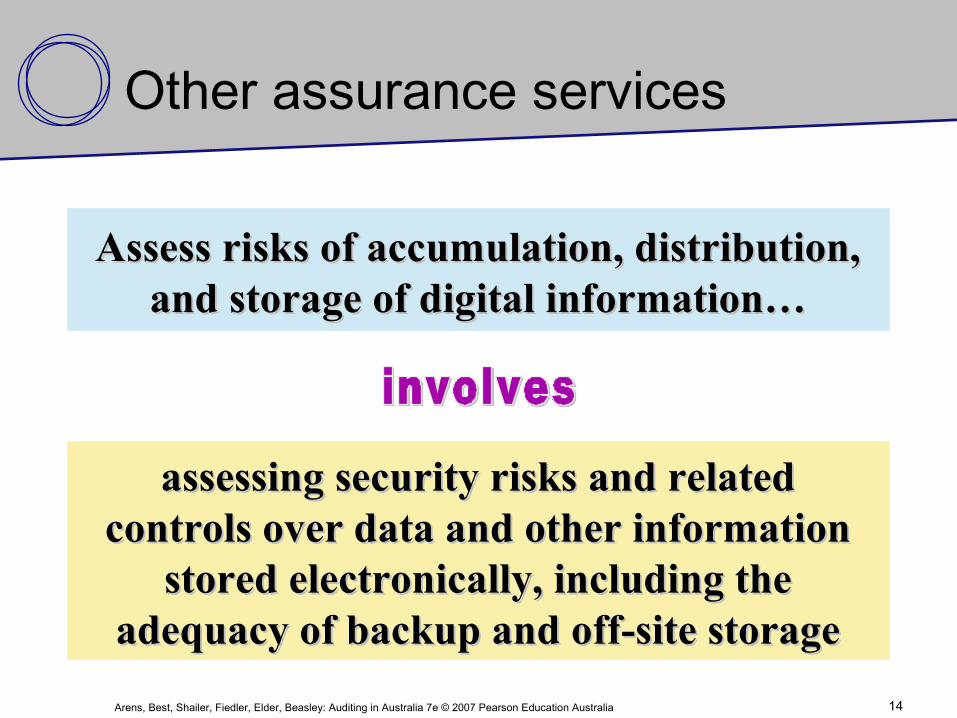

Assess risks of accumulation, distribution,Assess risks of accumulation, distribution,and storage of digital information…and storage of digital information…

assessing security risks and relatedassessing security risks and relatedcontrols over data and other informationcontrols over data and other information

stored electronically, including thestored electronically, including theadequacy of backup and off-site storageadequacy of backup and off-site storage

Other assurance services

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 15

Fraud and illegal acts risk assessment…Fraud and illegal acts risk assessment…

developing fraud risk profiles and assessing developing fraud risk profiles and assessing the adequacy of systems and policies inthe adequacy of systems and policies in

preventing and detecting fraud and illegal actspreventing and detecting fraud and illegal acts

Other assurance services

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 16

Other assurance services

Annual environmental audit…Annual environmental audit…

assessing whether company policies ensure assessing whether company policies ensure compliance with environmental compliance with environmental

standards and laws standards and laws

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 17

ASSURANCE SERVICESASSURANCE SERVICES

Other Attestation Services(e.g., WebTrust, SysTrust)

Other Assurance Services(e.g., ElderCare Plus)

CertainManagementConsulting

ATTESTATION SERVICES

Audits Reviews

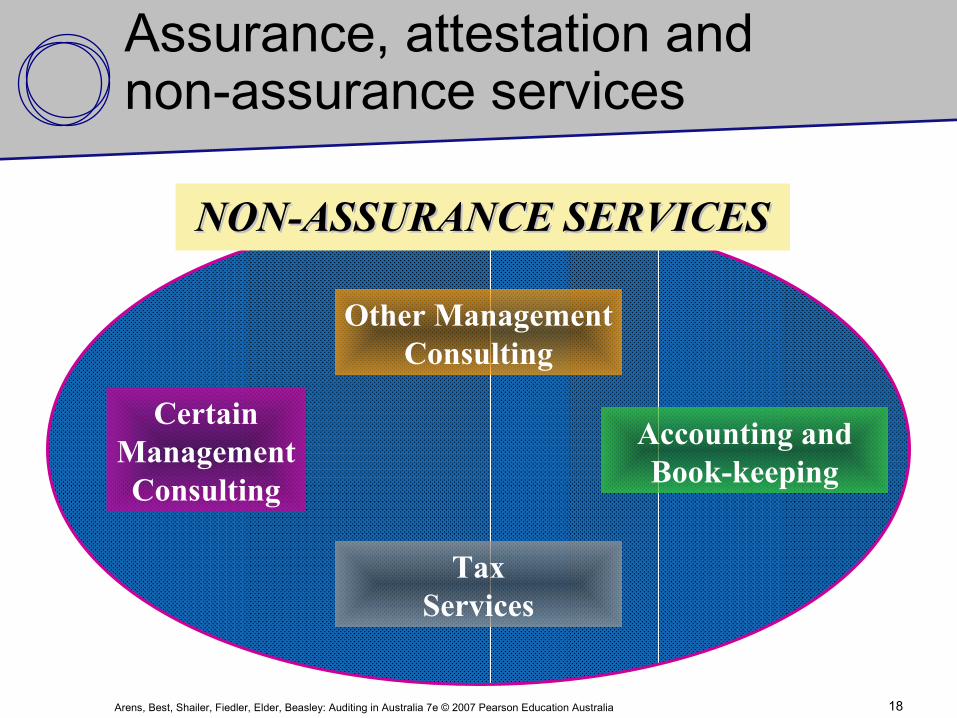

Assurance, attestation and non-assurance services

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 18

NON-ASSURANCE SERVICESNON-ASSURANCE SERVICES

Other ManagementConsulting

TaxServices

CertainManagementConsulting

Accounting andBook-keeping

Assurance, attestation and non-assurance services

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 19

Explain the importanceExplain the importance

of auditing in reducingof auditing in reducing

information riskinformation risk

Learning objective 2

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 20

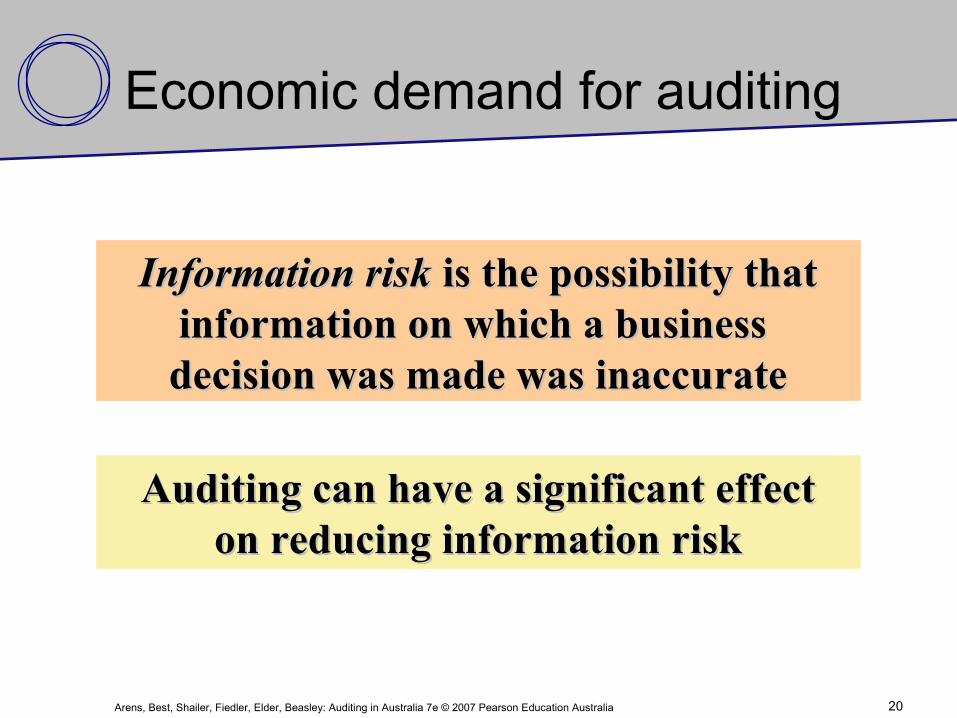

Information riskInformation risk is the possibility that is the possibility thatinformation on which a business information on which a business decision was made was inaccuratedecision was made was inaccurate

Auditing can have a significant effectAuditing can have a significant effecton reducing information riskon reducing information risk

Economic demand for auditing

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 21

List the causes of informationList the causes of information

risk, and explain how thisrisk, and explain how this

risk may be reducedrisk may be reduced

Learning objective 3

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 22

1. Remoteness of information1. Remoteness of information

2. Biases and motives of the provider2. Biases and motives of the provider

3. Voluminous data3. Voluminous data

4. Complex exchange transactions4. Complex exchange transactions

Causes of information risk

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 23

1. User verifies information1. User verifies information

2. User shares information risk with management2. User shares information risk with management

3. Audited financial statements are provided3. Audited financial statements are provided

Reducing information risk

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 24

Describe auditingDescribe auditing

Learning objective 4

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 25

AuditingAuditing is the accumulation and evaluation is the accumulation and evaluation of evidence about information of evidence about information

to determine and report on to determine and report on the degree of correspondence between the degree of correspondence between the information and established criteriathe information and established criteria

Auditing should be done by a competent, Auditing should be done by a competent, independent personindependent person

Nature of auditing

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 26

EvidenceEvidence is any information used is any information used by the auditor to determine whether the by the auditor to determine whether the

information being audited is stated in information being audited is stated in accordance with established criteriaaccordance with established criteria

Accumulating &evaluating evidence

It is important to obtain a sufficient quality It is important to obtain a sufficient quality and volume of evidence and volume of evidence

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 27

The auditor must be:The auditor must be:• qualified to understand the criteria usedqualified to understand the criteria used• competent to know the competent to know the typestypes and and amountamount

of evidence needed to reach proper of evidence needed to reach proper conclusionsconclusions

Competence of the individuals performing the Competence of the individuals performing the audit is of little value if they are audit is of little value if they are biasedbiased in the in the

accumulation and evaluation of evidenceaccumulation and evaluation of evidence

Competent independent person

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 28

The final stage in the auditing processThe final stage in the auditing processis preparing the is preparing the Audit Report,Audit Report, which which

is the communication of theis the communication of theauditor’s findings to usersauditor’s findings to users

Reporting

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 29

Distinguish betweenDistinguish between

auditing and accountingauditing and accounting

Learning objective 5

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 30

Accounting:Accounting: the recording, classifying and summary of the recording, classifying and summary of economic events for the purpose of providing economic events for the purpose of providing financial information used in decision makingfinancial information used in decision making

Auditing: Auditing: determining whether recorded information determining whether recorded information properly reflects the economic events that properly reflects the economic events that occurred during the accounting periodoccurred during the accounting period

Distinction betweenauditing and accounting

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 31

Differentiate the threeDifferentiate the three

main types of auditsmain types of audits

Learning objective 6

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 32

Financial Statement AuditFinancial Statement AuditFinancial Statement AuditFinancial Statement Audit

Performance AuditPerformance AuditPerformance AuditPerformance Audit

EfficiencyEfficiencyEfficiencyEfficiency EffectivenessEffectivenessEffectivenessEffectiveness

Compliance AuditCompliance AuditCompliance AuditCompliance Audit

Types of audits

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 33

ExampleExample

InformationInformation

CriteriaCriteria

EvidenceEvidence

Annual audit of WoolworthsAnnual audit of Woolworthsfinancial statementsfinancial statements

Woolworths financialWoolworths financialstatementsstatements

Accounting StandardsAccounting Standards

Documents, records, and outsideDocuments, records, and outsidesources of evidencesources of evidence

Financial statement audit

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 34

ExampleExample

InformationInformation

CriteriaCriteria

EvidenceEvidence

Evaluate computerised payroll systemEvaluate computerised payroll systemfor efficiency and effectivenessfor efficiency and effectiveness

Number of records processed, costs ofNumber of records processed, costs ofthe department, and number of errorsthe department, and number of errors

Company standards for efficiency andCompany standards for efficiency andeffectiveness in payroll departmenteffectiveness in payroll department

Error reports, payroll records, andError reports, payroll records, andpayroll processing costspayroll processing costs

Performance audit

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 35

ExampleExample

InformationInformation

CriteriaCriteria

EvidenceEvidence

Determine that bank requirementsDetermine that bank requirementsfor loan continuation have been metfor loan continuation have been met

Company recordsCompany records

Loan agreement provisionsLoan agreement provisions

Financial statements andFinancial statements andcalculations by the auditorcalculations by the auditor

Compliance audit

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 36

Identify the primaryIdentify the primary

types of auditorstypes of auditors

Learning objective 7

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 37

Internal AuditorsInternal Auditors

Public Accounting FirmsPublic Accounting Firms

Tax AuditorsTax Auditors

Officers serving Auditor-GeneralOfficers serving Auditor-General

Types of auditors

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 38

Describe the nature Describe the nature

of public accounting firms, of public accounting firms,

what they do, what they do,

and their structureand their structure

Learning objective 8

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 39

International firmsInternational firms

National firmsNational firms

Large local & regional firmsLarge local & regional firms

Small local firmsSmall local firms

Public accounting firms

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 40

Accounting & book-keepingAccounting & book-keeping

Tax servicesTax services

Management consulting/Corporate RecoveryManagement consulting/Corporate Recovery

Audit proceduresAudit procedures

Activities of public accounting firms

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 41

� Sole proprietorship

� Partnership

� Incorporated company

Form of public accounting firms

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 42

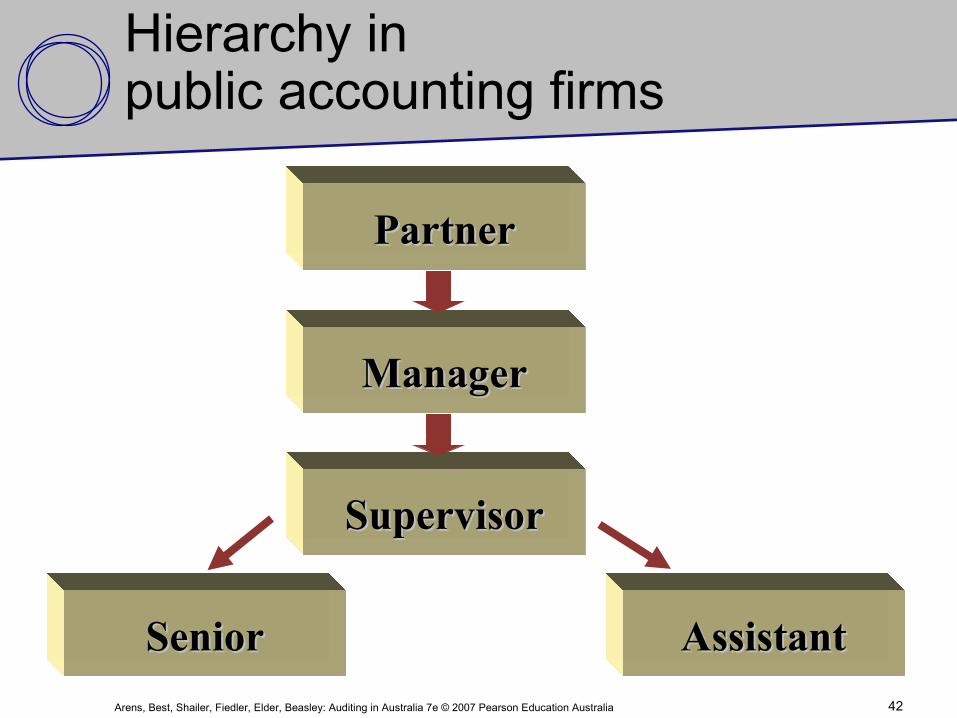

PartnerPartner

ManagerManager

SupervisorSupervisor

SeniorSenior AssistantAssistant

Hierarchy in public accounting firms

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 43

Describe the key functions Describe the key functions

performed by theperformed by the

professional accounting bodiesprofessional accounting bodies

Learning objective 9

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 44

The Institute of Chartered The Institute of Chartered

Accountants Accountants

in Australiain Australia

CPA AustraliaCPA Australia

Professional accounting bodies

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 45

Establishing professional requirementsEstablishing professional requirements

Research & publicationsResearch & publications

Continuing educationContinuing education

Activities of professional accounting bodies

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 46

Use auditing standards Use auditing standards

as a basis for further studyas a basis for further study

Learning objective 10

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 47

Auditing standards

CLERP 9 led to amendments to the CLERP 9 led to amendments to the Corporations Act 2001Corporations Act 2001, which gave , which gave

auditing standards the ‘force of law’auditing standards the ‘force of law’

ASAs represent MINIMUM standards ASAs represent MINIMUM standards of performance for auditorsof performance for auditors

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 48

Standards are divided into:Standards are divided into:

Introductory matters

Principles & responsibilities

Risk assessment & response

Audit Evidence

Conclusions/reporting

Using the work of others

Specialised areas

Auditing standards

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 49

Identify quality control standards Identify quality control standards

and practices withinand practices within

the accounting professionthe accounting profession

Learning objective 11

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 50

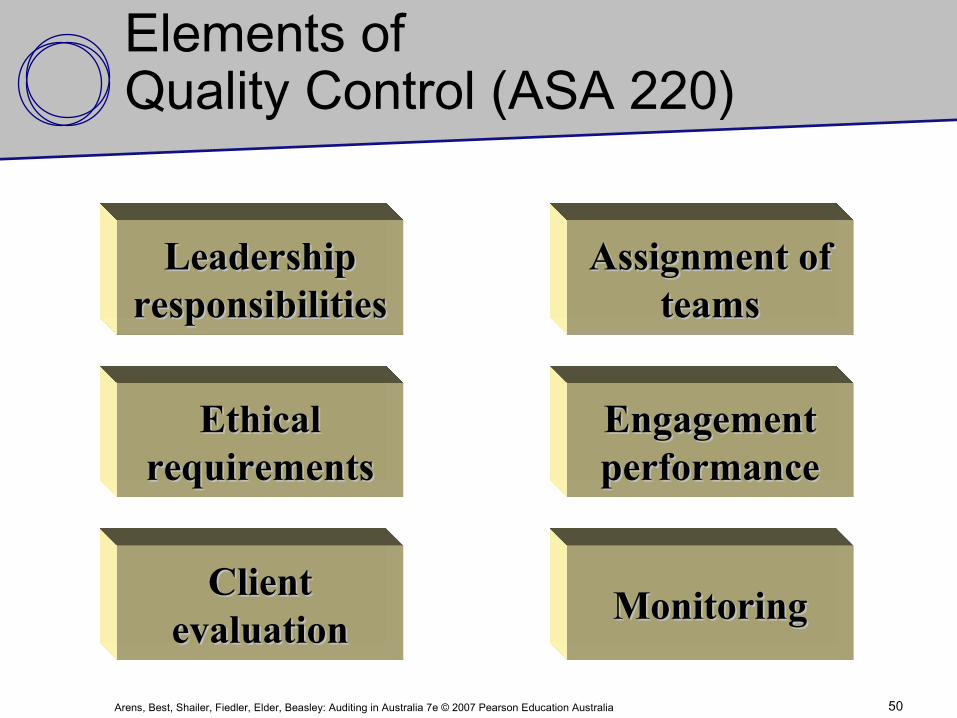

Leadership Leadership responsibilitiesresponsibilities

Ethical Ethical requirementsrequirements

Assignment of Assignment of teamsteams

Client Client evaluationevaluation

Engagement Engagement performanceperformance

MonitoringMonitoring

Elements of Quality Control (ASA 220)

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 51

ICAA/CPAICAA/CPA AustraliaAustraliaICAA/CPAICAA/CPA AustraliaAustralia

Commitment to excellence through self regulated

quality control

Peer review program

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 52

Summarise the role of theSummarise the role of the

Corporations ActCorporations Act in in

accounting and auditingaccounting and auditing

Learning objective 12

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 53

Audit ProvisionsAudit Provisions

QualificationsAppointmentRemovalPowers and dutiesReporting

Accounting Accounting ProvisionsProvisions

Accounting Standards

Reliable financial reports

Director Responsibilities

Corporations act

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 54

Describe the impact of Describe the impact of

e-commerce on e-commerce on

public accountantspublic accountants

Learning objective 13

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia 55

1. Information security2. Assurance and compliance applications3. Disaster and business continuity planning4. IT governance5. Privacy management6. Digital identity and authentication technologies7. Wireless technologies8. Application and data integration9. Paperless digital technologies10. Spyware detection and removal

AICPA top technologies

Arens, Best, Shailer, Fiedler, Elder, Beasley: Auditing in Australia 7e © 2007 Pearson Education Australia

End of Chapter 1