derivatives regulatory driven changes to documentation... · 2020-05-25 · derivatives –...

TRANSCRIPT

Derivatives – regulatory driven changes to documentation

Marc Benzler, Habib Motani and Gareth Old

16/17 September 2014

Clifford Chance

Introduction

2 Derivatives – regulatory driven changes to documentation

Clifford Chance

Developments in Europe and the US

Europe – overall and specific German issues

Major heads of change – Dodd Frank/EMIR

– Resolution

– Margin

– Securities Financing Transactions

Certain Disclosure Requirements in Germany

Introduction

3 Derivatives – regulatory driven changes to documentation

Clifford Chance

EMIR/Dodd-Frank

4 Derivatives – regulatory driven changes to documentation

Clifford Chance

Timely confirmations

Reporting

Portfolio reconciliation and compression

Dispute resolution

Daily valuation

Margining

EMIR/Dodd Frank

5 Derivatives – regulatory driven changes to documentation

Clifford Chance

Bank Resolutions

6 Derivatives – regulatory driven changes to documentation

Clifford Chance

New crisis management tools for regulators to

resolve failing banks

Europe BRRD

Resolution tools – sale of business

– bridge bank

– asset separation

– bail-in

US – OLA

Bank Resolutions (1)

7 Derivatives – regulatory driven changes to documentation

Clifford Chance

BRRD includes power for resolution authority – to suspend payments and deliveries (Article 69)

– to restrict enforcement of security (Article 70)

– to suspend termination rights (Article 71)

until midnight on the business day following publication of notice

Also resolution action itself not to be event of default

(Article 68)

Regulators are looking at what could interfere with

the effective implementation of resolution actions

Section 2(a)(iii)

Resolution Default Protocol

Bank Resolutions (2)

8 Derivatives – regulatory driven changes to documentation

Clifford Chance

On occurrence of event of default or potential event

of default, non-defaulting party can suspend its own

performance

Cases regarding timely use of this right and time

limit on its use

Regulators want to see it used within a given time

period or lost

Section 2(a)(iii) Amendment Agreement

What should the time limit be? - [90] days

Section 2(a)(iii)

9 Derivatives – regulatory driven changes to documentation

Clifford Chance

Suspensions or stays intended to cover not only the

entity in resolution but also certain affiliates

Say you have: – NY Law ISDA with US sub of a European parent

– European parent is credit support provider

– European parent goes into resolution

Article 71(2) resolution authority to have power to

suspend termination rights of parties to contracts

with the subsidiary

How?

ISDA Resolution Default Protocol

10 Derivatives – regulatory driven changes to documentation

Clifford Chance

Adhering party agrees to opt-in to the resolution regime

applicable to the counterparty and each “related entity”

So your ability to terminate is subject to resolution regime of

entity in resolution

US Bankruptcy Code: expected regulations requiring giving up

cross default rights when certain entities become subject to

“ordinary” insolvency

Adhering party agrees not to exercise certain cross default

rights if related entity becomes subject to certain insolvency

regimes, including US Bankruptcy Code

Some conditions relating to credit support

ISDA Resolution Default Protocol

11 Derivatives – regulatory driven changes to documentation

Clifford Chance

Margin for Uncleared Derivatives

12 Derivatives – regulatory driven changes to documentation

Clifford Chance

Required by Dodd-Frank Act, following G20 declaration

Originally proposed May 2011

Re-proposed September 2014 following BCBS-IOSCO

recommendations

Five regulators involved: Federal Reserve, FDIC, OCC, SEC

and CFTC

Expected implementation timetable – late 2015/early 2016

Additional provisions for exchange traded derivatives

US Swap Margin Requirements

13 Derivatives – regulatory driven changes to documentation

Clifford Chance

Counterparties to a “covered swap entity”

“Covered Swap Entity” is an swap entity regulated by a US

prudential regulator

Swap entity is any entity that meets definition of SD, SBSD,

MSP or MSBSP

Financial end-users – bank, regulated financial entity,

investment company, securitization issuer, investment pool

(including REITs)

Anyone else if covered swap entity considers appropriate

US Swap Margin – who has to post?

14 Derivatives – regulatory driven changes to documentation

Clifford Chance

Initial margin (IM) or independent amounts must be posted to

and collected from a covered swap entity if the Financial End-

User is above two thresholds

USD 3 billion (US) in total notional; and

USD 65 million in required IM

Variation margin (VM), or market-to-market collateral must be

posted and collected

Minimum transfer amount $650,000

US Swap Margin – Thresholds for

Financial End-Users

15 Derivatives – regulatory driven changes to documentation

Clifford Chance

Margin is required under any swap except physically settled FX

forwards and swaps (but see Fed supervisory guidance)

No frontloading, but all outstanding swaps under a Master Netting

Agreement will be subject to margin requirements after effective date

VM:

– Must be in cash

– No haircuts apply

– Collected at least daily

IM:

– Cash, gold, Treasuries, certain securities

– Any IM collected from a covered swap entity is subject to segregation

requirements (even if IM is not required by rule)

– IM posted to a covered swap entity is not required to be segregated

– Can only be netted in broad categories (agricultural commodities, energy

commodities, metals and other commodities, credit, equity, currency and

rates)

US Swap Margin – When and what to

post

16 Derivatives – regulatory driven changes to documentation

Clifford Chance

Documentation covering requirement for IM and VM, valuation,

eligible collateral, dispute resolution

Custody/segregation requirements (especially for IM received

from covered swap entity)

Master netting agreement

– only means of netting VM

– covered swap entity must have well-founded basis that agreement is

enforceable in bankruptcy

US Swap Margin – Documentation

17 Derivatives – regulatory driven changes to documentation

Clifford Chance

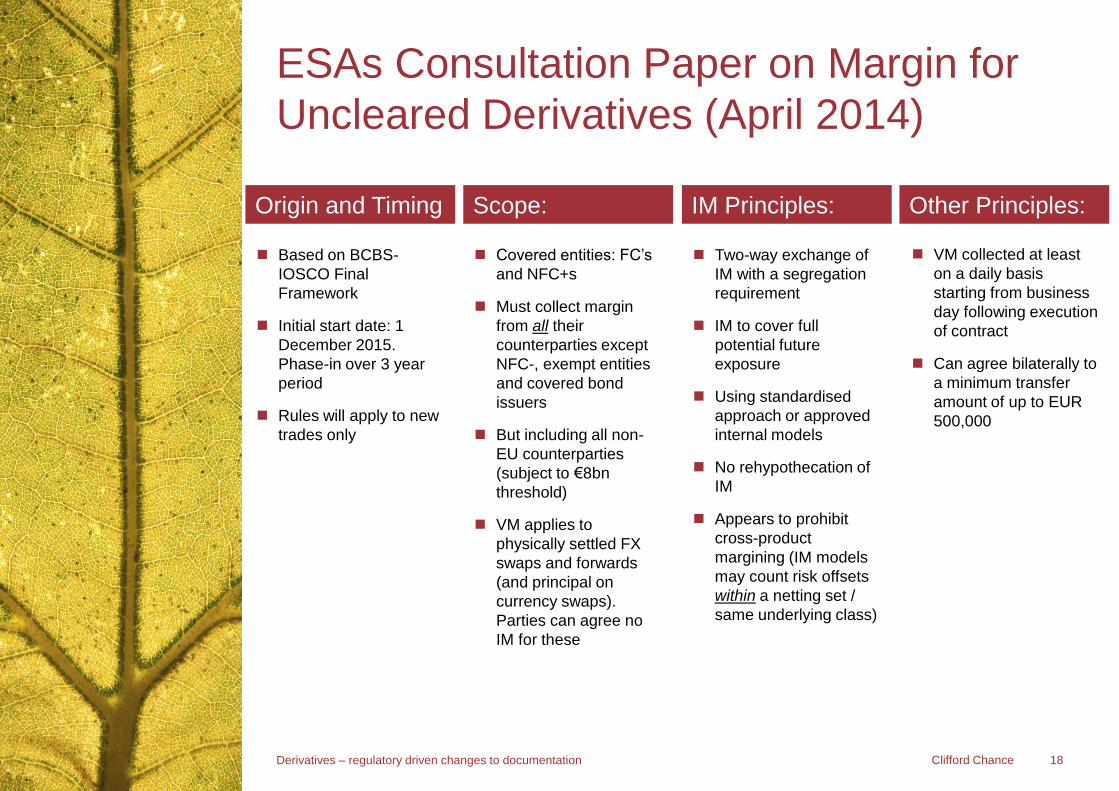

ESAs Consultation Paper on Margin for

Uncleared Derivatives (April 2014)

18 Derivatives – regulatory driven changes to documentation

Scope: IM Principles: Other Principles: Origin and Timing

Based on BCBS-

IOSCO Final

Framework

Initial start date: 1

December 2015.

Phase-in over 3 year

period

Rules will apply to new

trades only

Covered entities: FC’s

and NFC+s

Must collect margin

from all their

counterparties except

NFC-, exempt entities

and covered bond

issuers

But including all non-

EU counterparties

(subject to €8bn

threshold)

VM applies to

physically settled FX

swaps and forwards

(and principal on

currency swaps).

Parties can agree no

IM for these

Two-way exchange of

IM with a segregation

requirement

IM to cover full

potential future

exposure

Using standardised

approach or approved

internal models

No rehypothecation of

IM

Appears to prohibit

cross-product

margining (IM models

may count risk offsets

within a netting set /

same underlying class)

VM collected at least

on a daily basis

starting from business

day following execution

of contract

Can agree bilaterally to

a minimum transfer

amount of up to EUR

500,000

Clifford Chance

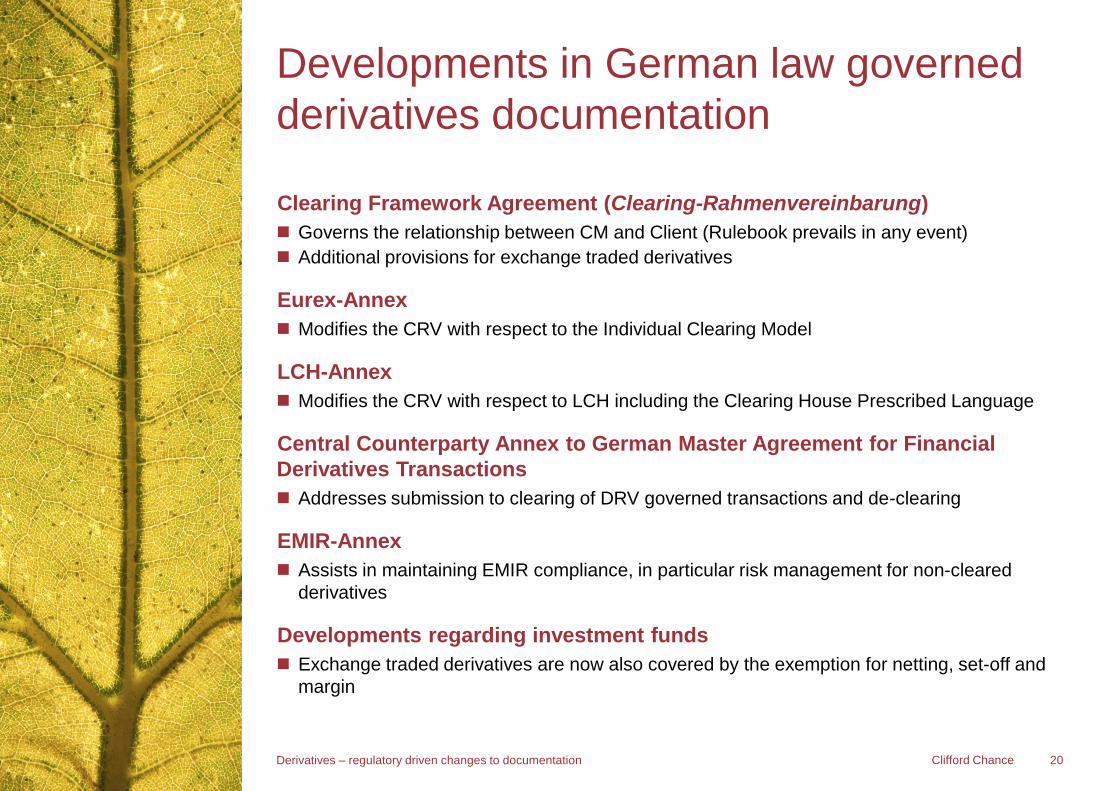

Germany

19 Derivatives – regulatory driven changes to documentation

Clifford Chance

Clearing Framework Agreement (Clearing-Rahmenvereinbarung)

Governs the relationship between CM and Client (Rulebook prevails in any event)

Additional provisions for exchange traded derivatives

Eurex-Annex

Modifies the CRV with respect to the Individual Clearing Model

LCH-Annex

Modifies the CRV with respect to LCH including the Clearing House Prescribed Language

Central Counterparty Annex to German Master Agreement for Financial

Derivatives Transactions

Addresses submission to clearing of DRV governed transactions and de-clearing

EMIR-Annex

Assists in maintaining EMIR compliance, in particular risk management for non-cleared

derivatives

Developments regarding investment funds

Exchange traded derivatives are now also covered by the exemption for netting, set-off and

margin

Developments in German law governed

derivatives documentation

20 Derivatives – regulatory driven changes to documentation

Clifford Chance

Summary

According to Germany's Federal Supreme Court (Bundesgerichtshof, "BGH"), early

termination provisions which exclude the ʺcherry-pickingʺ right of a German insolvency

representative in respect of mutual contracts under section 103 of the German Insolvency

Code (Insolvenzordnung, ʺInsOʺ) are void under section 119 InsO

While the judgment concerned a contract for the supply of energy, the BGH's decision has

wider implications which generally affect early termination provisions and in particular close-

out netting

The BGH dismissed the payment claim in its judgment of 15 November 2012

Insolvency-related termination clauses restricting the insolvency representative's cherry-

picking right (section 103 InsO) are invalid (section 119 InsO)

Insolvency-related termination clauses are termination rights based on: (1) a stoppage of payments (Zahlungseinstellung),

(2) the filing of an application for the opening of insolvency proceedings or

(3) the opening of insolvency proceedings

According to the BGH, this would not apply if the contractual termination clause

corresponds to a statutory exemption which provides for an early termination upon a party's

insolvency

The judgment does not apply to termination clauses which are based on defaults in general

such as a failure to deliver or perform or breach of contract

BGH judgment of 15 November 2012 on

insolvency-related termination rights (1)

21 Derivatives – regulatory driven changes to documentation

Clifford Chance

Impact of the statutory close-out netting provision under section 104 InsO

Section 104 InsO is mandatory law and prevails over contractual arrangements

While the BGH did not mention section 104 InsO, we understand that section 104 InsO as a

statutory netting provision qualifies as a statutory exemption and any contractual early

termination and netting agreements which include transactions covered by section 104 InsO

should not be void under section 119 InsO

As a consequence, not only the timing of the early termination right is decisive but also

whether or not the relevant transactions subject to the contractual netting agreement qualify

either as fixed date transactions (Fixgeschäft) or financial transactions (Finanzleistungen),

both terms as referred to in section 104 para. 1 or para. 2 InsO respectively

If based on the application of section 104 InsO, contractual netting agreements are

enforceable in an insolvency, the valuation of the terminated transactions should also be

determined as agreed between the parties

If not, section 104 para. 3 InsO applies which provides for generic principles for valuation

and calculation at the relevant market or exchange price on any date within 5 working days

upon the opening of insolvency proceedings determined by the parties. Where parties fail to

reach an agreement on the date, the prices applicable on the second working day following

the opening of insolvency proceedings prevail

To summarise, no changes to documentation required (but legal assessment whether in or

out of scope of section 104 InsO is essential)

BGH judgment of 15 November 2012 on

insolvency-related termination rights (2)

22 Derivatives – regulatory driven changes to documentation

Clifford Chance

High disclosure standards to discharge duty of care under an investment advisory

agreement

Existing knowledge or experience does not permit a conclusion in relation to the customer’s

willingness to take risks

Information on unlimited risks (not to be designated that this is of a “theoretical” nature but

rather that this depends on developments of the spread which may become “real and

ruinous”)

Bank needs to ensure customer’s knowledge and information of the risk profile of the

relevant product is substantially at the same level as the bank’s own knowledge and

information

Specific disclosure of initial negative market value of swap (also based on a (potential)

conflict of interest caused by the bank’s hedging activities)

No information that the bank entered into the transaction with the intention to make profits

need to be provided

To summarise, increased requirements for documentation and client related disclosure

BGH judgment of 22 March 2011 on

CMS Spread Ladder Swaps

23 Derivatives – regulatory driven changes to documentation

Clifford Chance

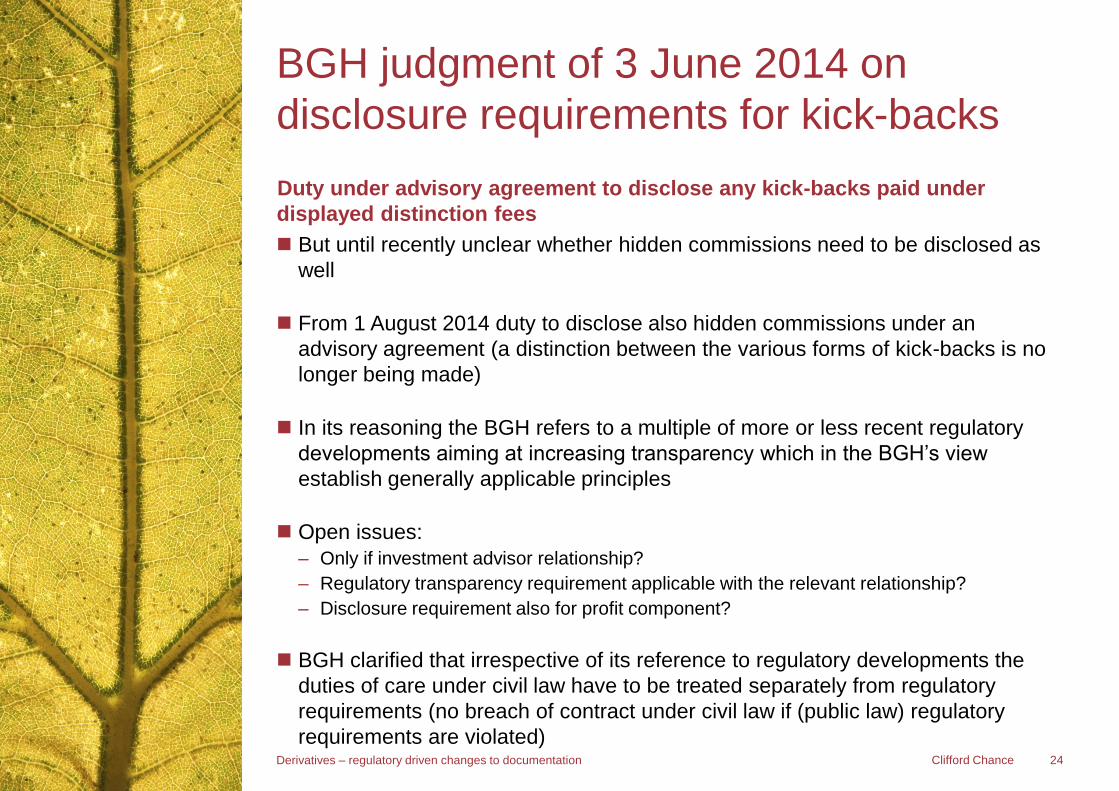

Duty under advisory agreement to disclose any kick-backs paid under

displayed distinction fees

But until recently unclear whether hidden commissions need to be disclosed as

well

From 1 August 2014 duty to disclose also hidden commissions under an

advisory agreement (a distinction between the various forms of kick-backs is no

longer being made)

In its reasoning the BGH refers to a multiple of more or less recent regulatory

developments aiming at increasing transparency which in the BGH’s view

establish generally applicable principles

Open issues:

– Only if investment advisor relationship?

– Regulatory transparency requirement applicable with the relevant relationship?

– Disclosure requirement also for profit component?

BGH clarified that irrespective of its reference to regulatory developments the

duties of care under civil law have to be treated separately from regulatory

requirements (no breach of contract under civil law if (public law) regulatory

requirements are violated)

BGH judgment of 3 June 2014 on

disclosure requirements for kick-backs

24 Derivatives – regulatory driven changes to documentation

Clifford Chance

MiFID requirements

Fully implemented but likely not giving rise to investors’ claims (regulatory provisions serve

generally public interests only but see BGH decision of 3 June 2014)

Additional requirements (for retail clients)

Requirement to keep detailed written records of advice (Beratungsprotokoll) – § 34 (2a)

WpHG

Product Information Sheet – § 31 (3a) WpHG

Recommendation of suitable instruments only – § 31 (4a) WpHG

Eligibility requirements for sales persons – § 34d WpHG

Comprehensive disclosure obligation with respect to inducement for third parties if non-fee

based investment advisory relationship

Fee-based Investment Advice Act

– No kick-backs etc. from third parties

– Diversified portfolio of offered instruments

– Organisational separation from any other activities if also non-fee based investment advisory services

are affected

Assets Investment Act

– Information Sheet / Prospectus Requirements

– Extension of definition “financial instruments”

Enforcement action by BaFin

Regulatory Background

25 Derivatives – regulatory driven changes to documentation

Clifford Chance

Investment advisory agreement / relationship

May be entered by implicit conduct

E.g. bank publishes (or makes statements which are construed as or deemed to

be) individual recommendations

Applies irrespective of client categorisation under MiFID

Duty of care

Investor-related advice

– “Know your customer” (financial situation, investment profits, personal knowledge and

experience)

Object-related advice

– Specific risks and characteristics of the investment

Examples:

Verification of sales material

Monitoring of financial news

Information duty regarding legal requirements / limitations

General duties under civil law

26 Derivatives – regulatory driven changes to documentation

Clifford Chance

Securities Financing Transactions

27 Derivatives – regulatory driven changes to documentation

Clifford Chance

FSB Policy Framework for addressing shadow banking risks in

securities lending and repos (August 2013)

European Commission Proposed Regulation on reporting and

transparency of securities financing transactions (January 2014)

What are SFTs? – securities lending and borrowing transactions

– repos and reverse repos

– buy sell backs and sell buy backs

– transactions having an equivalent economic effect

Reporting to trade repositories

Disclosure to fund investors – in fund manager reports

– prospectuses: policies, criteria, limits etc

Securities Financing Transactions (1)

28 Derivatives – regulatory driven changes to documentation

Clifford Chance

Rehypothecation – written agreement

– prior consent

– risk disclosure

– collateral to be transferred to an account in the name of the receiving

counterparty

Securities Financing Transactions (2)

29 Derivatives – regulatory driven changes to documentation

Clifford Chance

Contacts

30 Derivatives – regulatory driven changes to documentation

Marc Benzler Partner, Frankfurt

T: +49 697 199 3304

E: marc.benzler

@cliffordchance.com

Gareth Old Partner, New York

T: +1 212 878 8539

E: gareth.old

@cliffordchance.com

Habib Motani Partner, London

T: +44 20 7006 1718

E: habib.motani

@cliffordchance.com

Clifford Chance, 10 Upper Bank Street, London, E14 5JJ

© Clifford Chance 2014

Clifford Chance LLP is a limited liability partnership registered in England and Wales under number OC323571

Registered office: 10 Upper Bank Street, London, E14 5JJ

We use the word 'partner' to refer to a member of Clifford Chance LLP, or an employee or consultant with equivalent standing and qualifications