digital asia – asean in ascendence. team finland future watch report, may 2016

TRANSCRIPT

DIGITAL ASIA:

ASEAN IN ASCENDENCE

Contact information

dfasdf

Ross O’Brien, Principal ITC analyst and Managing Director

Intercedent Asia

9a Hilltop Plaza 49 Hollywood Road

Central, Hong Kong

[email protected] @obrienross

Founded in 1992, Intercedent Asia provides research based consulting for market

entry and market development strategy in the Asia Pacific region, including demand management,

strategic market assessment, competitive intelligence, partner selection, site selection, and strategic

planning assistance. Intercedent Asia has offices in Singapore, Beijing, Hong Kong and Sydney.

Tekes – the Finnish Funding Agency for Innovation

Tekes is the main public funding organisation for research, development and innovation in Finland.

Tekes funds wide-ranging innovation activities in research communities, industry and service sectors

and especially promotes cooperative and risk-intensive projects. Tekes’ current strategy puts strong

emphasis on growth seeking SMEs.

2

Executive

summary

Digital communications, Internet applications and technologies have long been

essential to economic and social development across Asia, and have been fostered

by their governments in two unique ways:

By tightly coordination activity between regulators, telecom network operators

and technology manufacturers.

By benchmarking the progress of other leading digital economies. Singapore seeks to stay ahead of the digital economic curve, by investing in leading-edge technologies and applications to increase their national competitiveness in global industries. Singapore is definitely ASEAN’s digital leader. The Philippines and Vietnam are digital leapfroggers. Both suffer from infrastructure deficits, so digital technology deployment is focused mobile commerce, data analytics or ‘shared economy’ applications to sidestep infrastructure hurdles. Financial technologies—particularly around new lending models, mobile payments and blockchain—generates significant attention and investment in the three South-east Asian countries surveyed in this report. Beyond fintech, each of these countries has other distinct sectors from which digital industries are being built:

Singapore’s government’s well-managed and comprehensive civil bureacracy has been a catalyst for smart city and transportation technologies and applications,

The Philippines has an incredibly vibrant IT-enabled Business Process and Knowledge Process Outsourcing (BPO & KPO) industry, which dovetails with a healthcare competency, in turn generating innovation around telemedicine and ehealth device development.

Vietnam’s digital economy is centered around manufacturing, but there is an increasing amount of innovation and entrepreunerialism around communications and security applications development.

The ASEAN Economic Community (AEC) will likely create some digital infrastructure

initiatives at a cross-governmental level, but progress will be slow. More important for

regional digital development will be two other factors: rapid expansion of South-east

Asia’s venture capital industry (largely headquartered in Singapore) and the

digital knock-on effects of China’s “Belt and Road” transportation infrastructure

investments in the region.

There is strong commitment to build digital capabilities in each of the three ASEAN

countries surveyed in this report. Moreover, each has fast-growing technology

entreprenuer sectors, particularly around Fintech. Those seeking to invest in the

region, or use it as a platform for international expansion, however, should also be

aware of potential limitations in each market:

Singapore’s government support, in terms of planning, regulation and direct

investment, is strong—perhaps too strong. There is a danger that too much

incubation may smother innovation.

Vietnam has successfully transformed its export manufacturing sector

through an industrial zone development strategy. Relying on this model is not

as useful for software and applications development. Vietnam’s government

has also created ASEAN’s most restrictive Internet content environment.

The Philippines, due to its touchy relations with China, will probably not

enjoy much of a “Belt and Road” boost. Its IT development policies are

heavily weighted towards job creation, and this may stunt digital

innovation in an ecosystem which seeks efficiency and process automation.

3

Digital industry

development has

always been a

priority for South-

east Asian

governments

1. Leaders and leapfroggers

Singapore, Vietnam and the Philippines, and their

paths to digital transformation

1.1. National Information Infrastructure Initiatives

Digital communications, Internet applications and technologies have long been seen as essential to economic and social development across Asia. (This report will commonly refer to the sector collectively as ITC—Information Technology and Communications.) Perhaps more so than in any other emerging market economies, nearly all governments in Asia have been conscious of the need to invest in telecommunications infrastructure (particularly, but not exclusively, mobile cellular networks) in a coordinated fashion since the late 1980s. Moreover Asia (somewhat late to global liberalisation trends) has steadily deregulated communications markets over the last 25 years, to allow competitive services to spur more industry development, and lessen the state’s direct role in voice and data service provision. This was done to speed up the pace of development, and increase penetration of communications services in consumer and enterprise markets.

Policy frameworks and precise goal-setting around ITC—commonly referred to as National Information Infrastructure Initiatives, or NIII—guide these efforts. The results have been tremendous in South-east Asia. In its 2015 report on ASEAN infrastructure development, the ASEAN Sectretariat and UNCTAD report that mobile penetration of the region’s population has grown from 26% in 2005 to over 115% today (Figure 1). 43% of ASEAN’s population has access to mobile broadband Internet connectivity, and South-east Asia’s Internet bandwidth capacity has grown over 165% in the last 10 years. UNCTAD reckons that in the Philippines, the communications sector contributed nearly 5% of value-add to its GDP (Figure 2).

There are two unique aspects of the ways emerging Asian economies leverage ITC to sustain and promote growth:

The first is that, despite attempts to liberalise and deregulate, Asian government bodies have always closely managed digital industry development through tight coordination between regulators, telecom network operators and technology manufacturers. In other words, Asian governments have never let ITC industries grow through market forces alone. For decades, governments actively channel state funds to strategic digital industries, support R&D facilities and direct their state-owned telcos to purchase from domestic manufacturing facilities.

The second aspect is the way Asian governments plan for the future of their digital industries. Most Asian governments devote considerable effort in understanding ITC trends and industry direction, taking particular heed to benchmark the progress of other leading digital economies, in North America, Europe, and across Asia. This,in turn, informs decisions around how foreign investment is channelled into their economies.

4

Singapore seeks to

be a globally

competitive digital

leader, while The

Philippines and

Vietnam use

digital tools and

processes to

leapfrog

infrastructure

hurdles

Singapore invests in

Fintech to maintain

its position as a

global finance

center

The Philippines and

Vietnam see

Fintech as a tool to

boost financial

inclusion

Singapore’s vision

embraces Smart

This manifests itself in South-east Asian countries in different ways, depending on their level of economic development. Advanced economies—primarily Singapore and Malaysia—seek to stay ahead of the digital economic curve, by investing in leading-edge technologies and applications that allow them to increase their national competitiveness in global industries. Singapore is definitely ASEAN’s digital leader. Most of the rest of South-east Asia is poorer, and suffers from critical infrastructure deficits, despite well-coordinated NIIIs. For such countries, digital technology deployment is focused on such solutions as mobile commerce, data analytics or ‘shared economy’ applications to sidestep infrastructure hurdles, or speed the pace of economic development. The Philippines and

Vietnam fall into this second category: digital leapfroggers. 1.2. Digital leverage: transforming economies, stepping up competitiveness—and

stepping over hurdles

Financial technologies—particularly around new lending models, mobile payments and blockchain—are a digital sector that generates significant attention and investment in the three South-east Asian countries surveyed in this report. Singapore has the region’s most developed financial infrasture, and the government intends to use digital technology to maintain its position as a globally competitive finance hub. Ensuring Singapore’s Fintech sector is also world class is regarded as a key part of maintaining that competitiveness. But Philippines and Vietnam have very large unbanked populations, and their big Fintech opportunities to expand credit and lending to these sectors, particularly among women and the poor, according to a 2015 report by the Finance and Private Sector Development Team of the World Banks’ Development Research Group. Singapore is a major centre for foreign exchange trading, and algorithmic (machine-to-machine) trading is expanding as well. Crowdfunding (peer-to-peer) lending is also developing. The government’s central bank, the Monetary Authority of Singapore (MAS) has indicated that it will only formaly regulate its Fintech sector when it matures, and participating companies are large enough to impact outcomesin the wider financial system. Government funding supports a start-up ecosystem, although there is a fear that government support stifles real risk-taking entrepreunerialism. Vietnam and the Phillipines each have populations over 90m, and both have extremely fast-growing middle classes. Yet both countries are horribly underbanked (only 30% of adults have a bank account and 26.5% a debit card in Vietnam; see Figure 3). Mobile payments and peer-to-peer transfers have become a vast industry, as they give underbanked poorer populations tools to borrow and lend that they desperately need (Figure 4). Remittance businesses are another driver of Fintech development in both markets: more than 10m Filipino overseas workers who send more than US$2bn home monthly, largely via smartphones.

5

Domestic

competencies in IT

BPO and healthcare

could turn the

Philippines into an

e-health

innovation hub

Beyond Fintech, the three countries surveyed in this report each has other distinct sectors from which digital industries are being built:

Singapore again is the bright spot here, in terms of infrastructure and organisation. The government’s well-managed and comprehensive civil bureacracy has been a catalyst for smart city and transportation technologies and applications, largely defined around the country’s forward-looking attempt to manage the challenges of its increasing urbanisation.

The Philippines has an incredibly vibrant IT-enabled Business Process and Knowledge Process Outsourcing (BPO & KPO) industry, which generated over US$25bn in annual service exports last year. This industry dovetails with two other service industry competencies: legal services and healthcare, the latter in particular has begun to foment innovation and start-ups around telemedicine and ehealth device development.

Vietnam’s digital economy has largely been centered around its growth as a manufacturing center for consumer electronics, microprocessors and other digital infrastructure. There are an estimated 14,000 ITC-oriented manufacturing ventures in the country, employing in excess of 200,000 professionals. While many of these ventures are large multinationals or their subcontractors, there is an increasing amount of innovation and entrepreunerialism around communications and security applications development and mobile applications.

6

China’s ‘Belt and

Road’ investments

in ASEAN will play a

significant role in

defining the region’s

digital direction

The AEC will not do

much for South-east

Asia’s digital

agenda

1.3. Regionalization as a digital driver: within ASEAN, and without December 31 2015 saw the formal launch of the ASEAN Economic Community, an agreement between the 10 ASEAN member states to create a unified, competitive production base which is optimally integrated into the global economy. The AEC’s higher order goals are to promote a single market with equitable economic development across South-east Asia. The AEC will likely create some momemtum behind digital infrastructure initiatives at a cross-governmental level, particularly around security and biometric technologies used to facilitate faster, safer movement of people and goods within South-east Asia. However, coordination and implementation to date has been slow, for while most ASEAN states are broadly aligned with AEC objectives, certain key initiatives, such as efforts to increase mobility of skilled labour, are still contentious issues amongst member states. There will be more effective digital cross-polination in ASEAN at an M&A level. Singapore’s venture capital community is already quite active in investments in e-commerce ventures in the region: NSI, a technology-focused division of the Singapore-based Northstar private equity firm, has nearly a dozen investments in South-east Asian B2B and B2C ventures, including Singaporean online grocer Redmart, inventory management software firm Tradegekko and the fast-expanding Indonesian ride and delivery booking service Go-Jek. Singapore’s government-linked companies, such as SingTel and Singapore Technologies Telemedia (STT), have had decades of experience investing in neighboring mobile communications markets. Earlier this year saw Vietnam’s largest mobile company, the military-owned Viettel, acquire a license to operate Myanmar’s fourth mobile network, adding to nine other markets and over 250m customers on its networks globally (including Myanmar, Viettel has stakes in carriers in Cambodia, Laos and Timor Leste in the region, as well as Africa, Latin America and the Caribbean). China’s influence on digital technology industries and innovation in South-east Asia can be understood through three interconnected trade and investment trends unfolding:

China continues to pivot the growth drivers of its economy away from lower-value export manufacturing and towards domestic consumption. As a result, China’s fast-growing wages and increasingly serving oriented economy has seen some of its manufacturing industry migrate to South-east Asia—and particularly Vietnam.

China’s “Belt and Road” initative, which is a massive global program of (primarily) transport infrastructure development, has resulted in more than US$20bn in high-speed rail and port projects throughout South-east Asia.

Outbound investment of Chinese digital technology and Internet firms into ASEAN’s communications and e-commerce markets.

China will, as a result, play a significant role in defining the digital direction of South-east Asia. High-speed rail infrastructure will likely link to Singapore’s smart city initiatives, and Chinese investment in e-commerce and Internet businesses will increasingly leverage Singapore’s role as South-east Asia’s finance hub. Vietnam’s growing role as an extension of China’s supply chain will see investment from China, both in terms of port and land transport infrastructure investment, and potentially in supply chain management and logistics technologies and solutions. The Philippines, however, will be less of a beneficiary of China’s regional investment, in part due to geopolitical tensions between the two countries.

7

Government

support of

technology start-ups

in Singapore is

huge—but does it

coddle more than

it encourages?

2. Singapore: the smart nation

Singapore’s nationalist-interventionist approach to

digital innovation will ensure its position as the pivot

point for tech start-ups in ASEAN

2.1. Technology development policy: government priorities Singapore’s government arguably has Asia’s clearest and most comprehensive vision for leveraging digital technologies for economic development and regional (if not global) competitive advantage. The Infocomm Development Authority of Singapore (iDA) is a unique ITC regulator, in that it also serves as trade and industry promotion agency as well. As will be discussed, the Monetary Authority of Singapore (MAS) is also actively promoting development in the Fintech space. There are two over-arching national initiatives that largely inform the government’s digital development objectives:

iN2015, an initiative launched a decade ago to increase the density of infocomm infrastructure across Singapore,and promote the development of digital-intensive industries in the country, and

Smart Nation, a coordinated effort to use digital solutions to manage five upcoming challenges for the country: increasing urbanisation, its aging population, healthcare, sustainable power generation, and transport/mobility management. The initiative has its own programme office, reporting to the Prime Minister’s office.

The iN2015 programme largely met its goals. A comprehensive ‘next generation’ broadband infrastructure, with an emphasis on cloud computing, has been developed. Singapore stresses government-sponsored experimentation with new digital applications and solutions. In December 2015 and January 2016, trials of driverless transportation were initiated with 6km of public road, reportedly outfitted with some 1,000 sensors, under the Smart Nation initiative. The Singapore government boasts some 55,000 (largely technology-oriented) start-ups created over the decade to 2014, some specifically funded by the iDA’s own venture capital subsidiary, Infocomm Investments Pte Ltd (IIPL). Last February, IIPL started an incubator facility called Build Amazing Startups Here (BASH), which has turned into an ‘accelerator of accelerators’, with an emphasis on hosting initiatives from other digitally-forward countries. Tenants include the Danish-founded Fintech/IoT accelerator Startupbootcamp, Amsterdam-based Rockstart (specialising in mobile app development) and Dubai Silicon Oasis Authority. BASH reports that some 65 ventures assisted in its first year, with a 50% success rate. Singapore’s government is highly conscious of the need to give technology start-ups room to breathe, in both a regulatory sense and in its role as a facilitator. MAS, for instance, has indicated that it will not strictly regulate the Fintech sector until solutions and applications start to gain critical mass in the country. Yet the government is also often perceived as micromanaging the sector. The government’s copious promotional activities, funding and facilities are seen by some in the investment community as coddling start-ups, rather than accelerating their progress. Moreover, Singapore is also not always keen to allow digitially-enabled business models to unleash their full potential: in late 2014, the Land Transport Authority issued regulations significantly restricting car-booking apps such as Uber and GrabTaxi to use only licensed taxi and not offer discounts to regulated flag-fall rates. (Local restrictions has perhaps been a boon to local efforts: Singapore-based GrabTaxi is now South-east Asia’s largest car-booking service, with over 200,000

8

Singapore puts its

money—billions in

government and

private venture

capital—where its

digital vision is

drivers across the region, a valuation in excess of $1bn and a potential IPO in the works). 2.2. Technology-intensive industrial sectors and ecosystem

The iDA estimates that the value of Singapore’s infocomm industry rose from S$45bn in 2006 to S$167bn in 2014. Exports still take up nearly 70% of that total however, underscoring the country’s decades-long dependency on hardware exports, largely in computer equipment and peripherials. In fact, Hardware as a percentage of Singapore’s industry has shown a marked increase over the years; iDA survey data shows that in 2006, some 46% of industry value was in software and services, but by 2014 that had dropped to 31%

(Figure 5). Singapore’s accelerator ecosystem, for all the concerns about government over-intervention, leads Asia by a wide margin in terms of invested capital. The industry observers Tech in Asia estimate that Singapore’s accelerators have invested close to US$7.5bn in some 55 deals (Figure 6), far above the next largest source India (which has generated US$5bn invested in 174 deals). In addition to private equity funds like NSI and large government-linked venture capital organisations like IIPL, the government’s own sovereign wealth funds GIC and Temasek are both incredibly active in the digital investment space. The Asian Venture Capital Journal reported in 2013 that Singapore had some US$24bn in available funding for digitally-oriented early stage firms. There are also many grants and subsidy programmes for new ventures, such as reimbursement programmes implemented by International Enterprise Singapore, the country’s external market promotion agency. Local firms seeking to expand internationally can receive up to 70% of development expenses (if they working through ‘approved’ incubators) through the Market Access Incubation and Market Readiness Assistance Programmes. 2.3. Financial technology initiatives and firms Both the iDA and MAS have made Fintech a particular industry promotion priority. As mentioned, MAS has been very open about its ‘sandbox’ approach, allowing Fintech firms to experiment without fear of getting hemmed in by regulatory activity. That said, neither does MAS want to fall behind in its policy development: in August 2015, MAS started a FinTech & Innovation Group (FTIG) to ensure financial regulation kept

9

Singapore’s smart

city agenda is

preparing for an

aging, crowded

future

pace with industry development. The FTIG has three pillars which will track developments in payment technologies, infrastructure-related solutions (such as big data), and new innovations. MAS also has a correlary Smart Nation programme to track Fintech industry developments known as ‘Smart Financial Centre’. There is a groundswell of industry-sponsored activity around Fintech: Singapore’s largest bank, DBS, recently conducted a bitcoin-centric ‘hackathon’ with Startupbootcamp; one solution produced focused on virtual ledger solutions for unbanked consumers in the Philippines. The iDA, which has sponsored a “code::XtremeApps” hackathon for nearly a decade, is also using its annual event this year to promote Fintech solutions. However, these events have also come under criticism in Singapore’s development community, as they often attract more media attention than coders, and because sponsors have on occasion claimed IPR rights for solutions developed during the event. Multiple Fintech start-ups, many with regional (if not global) aspirations, have been gaining traction in Singapore:

Mobile commerce and Mobile POS firms: SoftPay Mobile is a Singapore-based MPOS firm with operations in in Vietnam, Indonesia and Malaysia, and claims a 300% increase in processing volume since it launched in early 2015, thanks to strong demand among merchants in rural communities. GoSwiff is another Singapore-based MPOS firm operating across South-east Asia (particularly in the Philippines), looking into developing tokenisation technology and payment platforms for mobile operators. Fastacash and Kashmi blend social media, mobile apps and MPOS capabilities to facilitate mobile cash transfers. CreateApp is an SME-oriented mobile app development firm in Singapore which is also developing mobile commerce capabilities; the company is rapidly expanding its distribution network in India, Indonesia and other South-east Asian markets.

Crowdfunding platforms with focus on specific Singaporean market segments. This include Ethis (Ethical Investments Southeast Asia), a real estate investment platform, currently focused on Sharia (Islamic financing)-compliant developments in Indonesia and Malaysia, and Funding Societies, a “Peer-to-SME” lending platform which allows individual lenders to contribute to small businesss loans using an escrow account.

Algorithmic trading and forex trading technology are also areas attracting entrepreunerial attention. London-based emerging market currency trading technology firm R5 was given MAS authority to launch in Singapore earlier this year.

2.4. Smart Cities, Security and IoT Smart city definition and development in Singapore is coordinated under the aforementioned Smart Nation initiative. In these efforts, however, the country relies heavily on its robust urban planning civil infrastructure, particularly the incredibly successful Housing Development Board (HBD), the nearly 50-year-old public housing authority in which over three-quarters of Singapore’s population live. The HBD kicked off a Smart HDB Town Framework in 2014, aimed at leveraging several technologies, but primarily Big Data Analytics and sensors, to incorporate intelligence into four ‘dimensions’ of Singapore’s public housing environment:

Planning, incorporating housing and traffic data into programmes to manage HDB development and incorporate sustainable design and management elements into construction of housing and related facilities (such as car parks);

Environment, including sensor technology to build responsive systems for climate management;

Estate, which aims at doing the same for facilities maintenance and public utility consumption, and

10

Surprisingly,

Singapore’s e-

health priorities

are somewhat

basic, focused on

IT infrastructure

developed and

training

Cyber security is

increasing priority

as Singapore has a

lot of ‘digitally

dependent’

industries at stake

Living, which is focused on ‘smart home’ for individual resident applications such as appliance and energy management, and healthcare connectivity

The Singaporean government is making inroads into Internet of Things (IoT) technology development—and, naturally, invesment—as a key component in its Smart Nation objectives. In January of this year Irvine, California-based Greenwaves Systems, which develops mobile connection and management solutions for machine-to-machine (M2M) communications, received a combined US$60m in Series C and mezzanine financing from Singapore’s Economic Development Board and STT. Greenwaves promptly announced the opening of an IoT R&D facility in Singapore’s Science Park II. The iDA has also been anticipating the operational challenges that IoT brings to existing digital infrastructure: this January, it announced a programme to develop an Over-the-Air Subscription Management standard that will allow for M2M communications which switch between mobile network environments without the need to switch or add additional SIM cards to IoT devices. The iDA is supremely concerned about cybersecurity, as it is at the heart of several key industry sectors. Not only does it affect the country’s strategically important financial services industry, security impacts its role as a logistics and distribution hub as well as a thriving data centre colocation industry with around 50 providers operating over 40 facilities, which will generate an estimated US$1.2bn in revenues in 2016 by industry analysts Structure Research. There is a small but specialised business ecosystem around security solutions in Singapore. Many have military or identity management applications, such as Biometronic, an Indian biometric identification technology firm managed out of Singapore. One Singapore-based firm, i-Sprint, which specialises in identity management solutions, was ranked number 50 in ‘Cybersecurity Ventures’ first quarter 2016 list of 500 global security firms. Like many other core segments in Singapore’s digital economy, its Cyber Security Agency (CSA), established in 2015, reports directly to the Prime Minister’s office. Deputy Prime Minister Teo Chan also serves as the Coordinating Minister for National Security. In March this year, it opened a Cyber Forensics Laboratory during a cross-agency cybersecurity incident exercise, which coordinated and analysed responses to a cybersecurity event affecting finance, government, power and communications infrastructure. 2.5. Healthcare

The Smart Nation initiatve has identified healthcare, particularly as it relates to the

needs of Singapore’s aging population. Currently more than 11% of the population is

over 65 years old, and the government forecasts that this will grow to over 25% of the

population—some 900,000 citizens—by 2030. Digital innovation initiatives in

healthcare are also connected to Singapore’s biomedical sciences industry cluster,

which the government has been promoting for well over a decade.

Suprisingly, however, much of the iDA’s digital healthcare efforts are centered on

fairly basic IT training and ‘informationalisation’ of healthcare providers and facilities.

These include a GP IT Enablement Programme, and a Health IT Professional

Development initiative. While basic, Singapore feels this is a necessary remedial

effort to raise the usage of digital solutions in the sector in order to then take

advantage of longer-term innovations. Such forward-looking areas include:

Integrated Clinic Management System (CMS) Programme, an ongoing

effort to create a single repository for medial records, established in 2006,

11

and managed by the Singapore-based e-government solutions provider

CrimsonLogic;

Healthcare Innovation Program, an iDA-sponsored incubation effort

established in collaboration with Motorola Solutions (acquired by US-based

Zebra in 2014), largely focused on mobile devices and applications in patient

care and facilities management

12

Vietnam is

redeploying a

successful

manufacturing

industry park

strategy to boost IT

solutions and

software

development—but

will it work?

3. Vietnam: China +1…and then some

Vietnam’s fast-growing manufacturing export sector

has created wealth and opportunity, and with it

investment in digital innovations

3 3.1. Technology development policy: government priorities As discussed in Chapter 1, much of Vietnam’s digital economy development policy has focused on its rapidly-expanding export manufacturing sector, rather than services and applications. Vietnam is, in a sense, the most ‘China-like’ of ASEAN countries—a centrally-planned economy guided by a communist government which uses global trade to accelerate its industrialisation. The country has the world’s fastest export growth after China itself. Vietnam exported US$2.5bn a month in 2004, and over US$14bn monthly in 2015. And, similar to China, Vietnam’s role as a manufacturing giant has quickly evolved. No longer just a producer of labour-intensive clothing and accessories, Vietnam is a major supply node for global digital components and consumer electronics firms. China provides not only a template for Vietnam’s manufacturing aspirations, it drives them. China’s manufacturing is its shedding lower-value, labour-intensive production, and Vietnam (among others) has thus become an extension of China’s supply chain, taking components from China and assembling finished products with cheaper labour. Chinese exports to Vietnam are now 35% of Vietnam’s exports. In other words, China is not handing over production to Vietnam so much as the supply chain of these two countries have become intertwined. Much of Vietnam’s increasingly electronics-oriented manufacturing is produced in clusters of industrial parks, where producers enjoy tax breaks, investment incentives and preferred access to logistics facilities. As of mid-2015, there were 212 such parks across the country, which generated over US$110bn in revenue last year, according to the Ministry of Planning and Investment. Vietnam’s Ministry of Information and Communications (MIC) is looking to emulating this success: a decree in November 2013 (No. 154/2013/ND-CP) established provisions for the development of IT and software parks with a similarly attractive set of tax breaks (capped at 10% over 30 years of operations).

Yet few have emerged. Quang Trung Software City (QTSC) in Ho Chi Minh City, is reasonably successful, and last year the Hanoi People’s Committee has earmarked over US$43bn for a software park with local software developer Hanel as an anchor tenant. However, colocating multiple software firms does not produce the same synergies as it does for manufacturing firms. The MIC may need to update its development and promotional strategies. Vietnam consumers enjoy extremely high mobile Internet penetration, and are voracious consumers of social media and online content (see 3.2, below). This broadly is in line with the objectives of the government’s digital master plan. That said, Vietnam’s government has a complicated and contradictory relationship with the Internet. The government routinely cracks down on bloggers (a 2014 decree criminalising online content critical of the government), and politically motivated cyberattacks are frequent. The advocacy organisation Freedom House gives Vietnam an Internet freedom score of 76 (100 being the worst score), lowest in South-east Asia and second-worst in Asia after China. The government also seeks to restrict non-political Internet activity: this January decree 124/2015/ND-CP imposes stiff fines

13

High Internet and

smartphone

penetration coupled

with low banking

rates creates a

perfect Fintech

storm in Vietnam

for e-commerce and mobile commerce retailers who fail to register with the Ministry of Industry and Trade, in an attempt to clamp down on Vietnam’s informal digital retail sector. 3.2. Technology-intensive industrial sectors

Vietnam is ranked 12

th globally for electronics manufacturing. Two of the world’s

leading smartphone manufacturers, Korea’s Samsung and LG, each have a collection of factories in Vietnam; their estimated investments in these facilities is more than US$5bn and US$1bn respectively. Intel has also invested over US$1bn, in its largest semiconductor testing centre outside of the US. Each of these giants has pulled an increasing number of sub-contractors and parellel process manufacturers into their Vietnamese orbit. The software and IT outsourcing industry is a slightly different story. The numbers are impressive: there are an estimated 3,000 companies employing over 200,000 people (Figure 7), and the Vietnam Software Association (VINASA) estimates the sector’s revenue have grown 10% annually over the last decade, to US$3bn in 2015, While is is decent, it is not on par with Vietnam’s manufacturing industry successs. The government has recently been encouraging software sector participants to expand faster.

Telecom services in Vietnam are a particular success story. UNCTAD estimates that, Vietnam has 1.5 subscriptions for every citizen, the highest mobile service penetration in ASEAN. Vietnam also has South-east Asia’s highest broadband penetration levels after ‘rich ASEAN’ (Singapore, Malaysia and Brunei), and the highest smartphones penetration in emerging ASEAN. 16% of the country is between the ages of 15 and 25—and, according to consultancy Moore Corporation, over 95% of them are online.

91% of Vietnamese access video content over the Internet, the highest in ASEAN. Use of international Internet and social media sites is also intense; over 70% of Internet advertising revenue in Vietnam is generated by Google and FaceBook. Vietnam’s mobile operators companies have not only been domestically successful, one in particular—Vietnam military-owned Viettel—now earns over 15% of its US$10bn in 2015 service revenue from its shares in 10 mobile licenses in 10 different countries. 3.3. Financial technology initiatives Vietnam’s indigenous Fintech ecosystem is growing rapidly, driven by a confluence of two factors: its high Internet and smartphone penetration,and its low bank account percentage of its population with formal bank account penetration. Remittances from overseas Vietnamese into the country exceeded US$12.5bn in 2015, and, similar to the Philippines much of that money was transmitted through mobile payment and social media apps. Singapore-based Fintech News estimates that there are over 30

14

The government’s

conflicted

relationship with

Internet content

ironically is creating

a cyber security

industry

local Fintech start-ups in Vietnam—more than half of them focused on mobile payment applications. Apart from a few payment solutions firms which sprung up over the course of the remittance boom, most Vietnamese Fintech start-ups were created in the last three years. In recent months Vietnam’s Fintech sector has attracted significant international investor attention. Momo, an e-wallet, peer-to-peer transfer and mobile payments app firm started in 2014 claims 2.5m unique users. In March, Momo took in US$28m in series B funding from Standard Chartered Private Equity and one of Momo’s original backers Goldman Sachs. A US-based early-stage venture capital firm, 500 Startups, also launched a US$10m ‘micro-fund’ in March, aimed at Vietnamese Fintech and e-commerce firms. In April, Singapore’s SoftPay Mobile, acquired another mobile payment provider, MPOS Technology JSC, which works with one of Vietnam’s largest taxi groups, as well as leading South-east Asian e-commerce platform (and now Alibaba subsidiary) Lazada. Vietnam’s remittance economy and growing IT outsourcing space is also creating traction in the cryptocurrency space. Three firms—Cash2vn, VBTC and Bitcoin Vietnam—have started up over recently, all aimed at facilitating remittances and peer-to-peer transfers for unbanked and/or overseas communities.

3.4. Smart Cities, Security and IoT

Vietnam’s government, as been discussed, manages its technology industry development centrally, although the central government does rely on municipal and provincial People’s Committees to implement its (primarily infrastructure-based) vision. The central government, as also discussed, is keen to build up digitally-oriented manufacturing parks and economic zones, which local governments use to compete for FDI. This has both positive and negative connotations for smart city technology development in Vietnam. Negative, in that the central government lacks overarching smart city vision, and without top-down guidance, smart city application development will be sporadic and slow. Positive, in that smart city applications are considered a value-add to municipalities and provinces building technology parks, and the residential zones adjacent to them. Binh Duong New City, an urban development to the north of Ho Chi Minh City, recently held a Smart City Summit to solicit discussions around integrated facility management and design. The local government is collaborating with the Dutch technology region Brainport Eindhoven. This is largely seen as a competitive bid to attract invement away from neighboring schemes. The Saigon Hi-Tech Park Incubator Center is also attempting to build up competency around IoT applications and is organising competitions (in a ‘hackathon’ vein) to attract IoT start-ups. Vietnam’s cybersecurity solution industry is gaining international prominence, ironically thanks to the severity with which its government cracks down on the Internet. Government restrictions have created a cyberwar with digital political dissidents, many of whom developed their skills in Vietnam’s thriving IT industry. Vietnam Computer Emergency Response Team reported attacks on over 18,000 websites in the country in the first nine months of 2015—among them government sites, including some 2.5m attacks on the Ho Chi Minh City portal along last year. Much like Russia, another emerging market cyber-conflict, Vietnam has developed an IT security service firms in parallel to its politically-motivated hacker ecosystem. Vietnam lacks a central cybersecurity agency, but the government has passed extensive Internet security regulations, which will come into effect this July.

15

3.5. Healthcare

Like Singapore, Vietnam’s healthcare IT priorities are centered on basic IT infrastructure development, and training for healthcare officials. Vietnam’s Department of Science and Training has been tasked with increasing technology literacy skills in hospitals and clinics. Vietnam’s Ministry of Health has a number of ongoing initiatives in conjunction with the Asian eHealth Information Network, largely around standardised healthcare data and unique patient IDs. Rural telemedicine initiatives are also in development.

16

Will the Philippines

be the first country

to completely

digitalise money?

Double 10%:

Philippines’ IT-BPO

industry is

10% of its

GDP

10% of global

BPO revenues

4. The Philippines: a nation of global citizens

The Philippines has seen its exports of labour and

skills both fuel an economic boom, and drive digital

technology innovation

4 4.1. Technology development policy: government priorities

The digital development policies of the Philippines’ Department of Transportation and Communications (DOTC) and the Commission on Information and Communication Technology (CICT) are closely tied to strategically important national industries. In 2011, the CICT outlined its Philippines Digital Strategy (PDS), a five-year programme with four pillars—Transformational Leadership, Education, Jobs Creation and Economic Growth and, somewhat incongruently, Environment Protection—much of which is centered on fostering and expanding the country’s IT-enabled service sector.

Increasing Internet connectivity is also a government priority: there is currently a plan

under way to provide effectively ubiquitous WiFi connectivity in public facilities

nationwide by the end of 2016, with estimated operational costs of US$32m.

The government has seized upon the country’s mobile payment affinity to launch a programme called e-peso, partially funded and developed in cooperation with USAID, through its Microenterprise Access to Banking (MABS) initiative, and in collaboration with the poverty reduction aid organisation Chemonics.

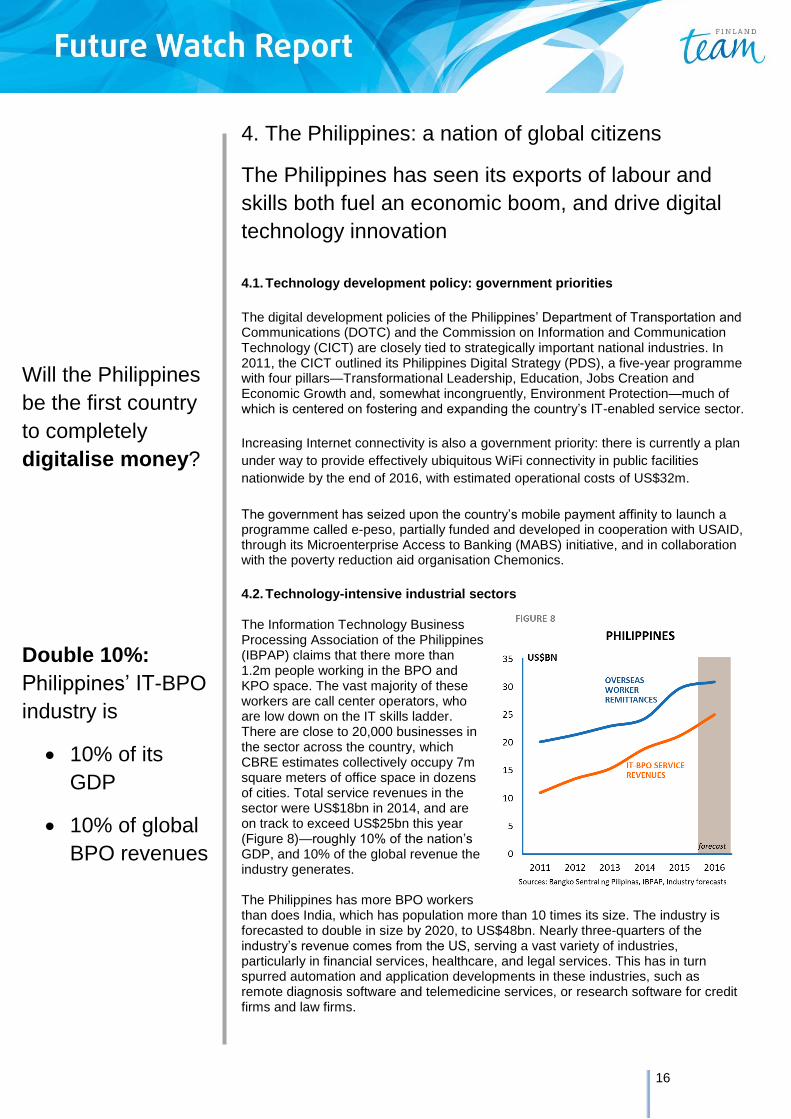

4.2. Technology-intensive industrial sectors The Information Technology Business Processing Association of the Philippines (IBPAP) claims that there more than 1.2m people working in the BPO and KPO space. The vast majority of these workers are call center operators, who are low down on the IT skills ladder. There are close to 20,000 businesses in the sector across the country, which CBRE estimates collectively occupy 7m square meters of office space in dozens of cities. Total service revenues in the sector were US$18bn in 2014, and are on track to exceed US$25bn this year (Figure 8)—roughly 10% of the nation’s GDP, and 10% of the global revenue the industry generates. The Philippines has more BPO workers than does India, which has population more than 10 times its size. The industry is forecasted to double in size by 2020, to US$48bn. Nearly three-quarters of the industry’s revenue comes from the US, serving a vast variety of industries, particularly in financial services, healthcare, and legal services. This has in turn spurred automation and application developments in these industries, such as remote diagnosis software and telemedicine services, or research software for credit firms and law firms.

17

The Philippines

leveraged its huge

remittance

industry to become

an early mobile

money innovator.

Will local Fintech

players help the

Philippines leapfrog

into the smartphone

era?

The Philippines’ IT-BPO industry is well-managed and well-supported, yet it owes its origins and fast growth to a happy, and somewhat contradictory, coincidence. Roughly 10% of the country works overseas, and has been doing so for decades. Mobile phone companies, in turn facilitates remittances and phone calls from overseas workers and have seen their revenues grow—and as will be discussed in section 4.3, become major Fintech players in the process. These carriers in turn have invested in international telecommunications capacity to continue serving the overseas worker community and the growing social media and Internet appetites of Filipinos at home. All that extra connectivity, and the high skills of the country’s workers, have served as the core ingredients of the BPO sector. In other words, the Philippines’ labour drain created the conditions for the country’s fastest growing job creation sector. BPO revenue is expected to surpass remittances in the next year. 4.3. Financial technology initiatives

The Philippines remittance industry is globally recognised for having produced sophisticated mobile peer-to-peer transfer and payment solutions. This has created regional global interest in developing payment and mobile money applications. Traditional banks have been looking into the space, as a way of extending their reach: it is estimated that over 37% of the country’s 1,637 municipalities do not have a single bank branch. The most established domestic players in Philippines Fintech are, perhaps unsurprisingly, the country’s celcos, led by the country’s leading carrier SMART, largely owned by the incumbent national operator PLD. SMART launched a mobile money transfer service, SMART Money in 2001; the country’s second-largest carrier, Global Telecom, launched a similar offering, GCash, in 2004. This has been transformational for unbanked consumers, and is an important lever for financial inclusion: USAID reckones that between 2006 and 2012, some 3m mobile banking transactions with collective value of US$400m were registered. Mobile money is also commonly used as an e-commerce currency, and is widely accepted as for payments over such portals as Lazada.

The mobile operators have given way to a host of other Fintech app developers in the Philippines—in fact, as mobile money swiftly evolves from text messaging-based services and prepaid top-ups to the smartphone app world, these traditional players are in danger of being disintermediated. So too are pawn shops, which control significant amounts of the ‘last mile’ of the remittance dispursement supply chain. Government attention in this space, particularly the e-peso programme which is aimed at creating a ‘carrier neutral’ digital currency, could also accelerate these efforts. Significant Fintech players on the rise include:

Rebit and Coins.ph are Bitcoin-based remitters (colloquially known as ‘rebittance’ providers) for Filipino communities domestically and globally. Coins.ph has a direct deposit relationship with the convienience store chain 7-eleven, which has 1,600 stores in the Philippines, and boasts a total of 10,000 ‘cash-in, cash-out’ retailer relationships nationwide.

Ayannah, a Philippines-based Fintech start-up funded by multiple Silicon Valley firms (including 500 Startups) which has developed peer-to-peer remittance Software as a Service platforms for peer-to-peer transfers and top-ups.

LoanSolutions, a crowdfuning lender.

Online pawnshop and micro-lender PawnHero.ph.

The Philippines’ growing regional leadership in Fintech solutions is having knock-on effects for Big Data Analytics. Big Data is seen as a platform for increasing financial inclusion, and dovetails well with the country’s thriving IT outsourcing industry. Ayannah is seeking to leverage the half a billion transaction records and social media information has generated in its digital payment services to develop credit

18

The Philippines

knows IT

outsourcing and

healthcare. It is

leveraging these

assets to drive e-

health applications

and device

development

Jump-starting

smart city efforts:

GrabTaxi provides

the Phillippines’

Transport

Department traffic

congestion analysis

scoring services. Indian e-commerce start-up LendingKart is looking to do something similar with Philippines’ digital lender Lenddo. PLDT is looking to invest over US$100m in big data service development, again off the back of its extensive payment and mobile service transaction records and existing data centre infrastructure.

4.4. Smart Cities, Security and IoT

Start-ups in adjacent technology sectors are beginning to jump-start the Philippines’ smart city efforts. Recently, the Singapore-based GrabTaxi ride-booking service announced a partnership with the World Bank to assist the DOTC in managing traffic congestion, by gathering and analysing traffic data generated by GrabTaxi’s participating drivers in Manila and Cebu. Much like Vietnam, the Philippines lacks a nation-wide initiative on smart city development. Various municipalities leverage their cornerstone digital industries to jump-start their intelligent infrastructure plans—or, in many cases, leverage smart city investments as a selling point to attract investors. Davao City, which credits the BPO industry with creating some 34,000 jobs in 2015, in 2013 earmarked US$3m to commission IBM to build an intelligent city programme largely focused on public safety monitoring and management. There are a handful of firms focused on smart city-centric access management technologies with an IoT spin—the aptly-named IoT Philippines, Inc. being one of them.

4.5. Healthcare As discussed in Chapter 1, digital healthcare solutions are a particular competency in the Philippines. Again, this is due to a convergence of factors: high Internet penetration, a long-term focus on training healthcare professionals (there are half a million licensed nurses in the Philippines, a penetration five times higher than the ASEAN average), and its considerable depth as a BPO provider to the global health and insurance sector. Against this backdrop, it is understandable that the Philippines’ Department of Health (DoH) has arguably South-east Asia’s most comprehensive strategies for the implementation of eHealth. A rolling five-year eHealth Strategic Framework details objectives for standardising IT infrastructure and practices, and (similar to the other South-east Asian countries surveyed) enhancing human resource capabilities. Many of these targets focus on ‘electrifying’ patient records and services. At the end of 2014, all 70 DoH hospitals were running an e-claim system under the country’s national healthcare system Philhealth, and the government plans to have 85m citizens—effectively the entire country—registered under the Philhealth e-claim scheme. Unifying data centres and record management is another goal, as is the development and distribution of digital devices for remote medical services. The DoH e-Health framework targeted the provision of 1,000 telemedicine devices known as RxBoxes in Rural Health Units across the country by the end of 2015. RxBox is a multi-purpose medical sensor developed by the National Telemedicine Center, which allows remote professionals to measure and diagnose medical issues, and store and manage data.