digitization an engine to tide over the economic …

TRANSCRIPT

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 17 E-Mail : [email protected]

DIGITIZATION: AN ENGINE TO TIDE OVER THE ECONOMIC

FALLOUT FROM COVID-19 PANDEMIC

Dr. Sanjeev Kumar Bansal

Associate Professor,

P.G. Department of A.B.S.T.,

S.N.D.B. Govt. P.G. College,

Nohar, Rajasthan

Nidhi Arora

Research Scholar,

Department of Commerce,

MGS Univesity, Bikaner (Raj.)

ABSTRACT

The role of the banking sector in the inclusive growth of the

economy has been widely recognized by all the countries across the globe.

Several efforts have been undertaken by the RBI, Government and the service

providers i.e. the financial institutions from time to time achieve the goal of

forming a financially inclusive economy. The introduction of the Information

Technology in the banking sector has provided a new direction to all the

financial inclusion initiatives and led to the coinage of the term Digital Financial

Inclusion. Efforts have been directed to encourage the masses to adopt the digital

modes of transacting such as Internet Banking, Mobile banking etc. keeping in

mind the safety and security concerns.

The outbreak of the COVID-19 impacted all the sectors of the

economy including the banking sector. The paper money was perceived as a

carrier of the virus and hence it was avoided by the masses. The banks and the

financial institutions were also operational with limited no of staff for the limited

hours only. All these factors undoubtedly caused a lot of turbulence but also at

the same time proved to be a boon for the digitization. Various modes of the

available retail payment systems such as NEFT, UPI etc. were adopted by the

masses for performing their routine transactions. Various government schemes

such as PMJDY, AEPS, Door step Banking etc. also have contributed

significantly in the goal of forming a financially inclusive economy by using

digital means. The present paper focuses on the concept of the Digital Financial

Inclusion and its role in forming a financially inclusive economy. The impact of

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 18 E-Mail : [email protected]

the COVID-19 pandemic on the growth of retail digital transactions have also

studied in detail.

The various measures undertaken by RBI to boost the digital

transactions along with various awareness schemes during the period of the

outbreak of the COVID-19 has also been studied in detail. The latest

advancements in the direction of boosting digitization by RBI in coordination

with all the other players has also been highlighted in the paper.

Keywords: Digitization, PMJDY, AEPS, Micro ATMS, Doorstep Banking,

Digital Ombudsman.

INTRODUCTION

The banking sector has witnessed several changes since

independence. The introduction of the Information technology in the banking

sector has completely revolutionized the way the banking activities were

performed earlier. It has been realized by the RBI and the financial service

providers that the goals of forming a financially inclusive economy is not

possible to achieve without leveraging on the technology. It has led to the

coinage of the term Digital Financial Inclusion. The thrust of digital financial

inclusion is the use of cost saving digital means to reach the unbanked sections

of the population. The definition of Digital Transaction as given by Banking

Ombudsman for Digital Transactions is: “Digital Transaction’ means a payment

transaction in a seamless system affected without the need for cash at least in one

of the two legs, if not in both. This includes transactions made through digital /

electronic modes wherein both the originator and the beneficiary use digital /

electronic medium to send or receive money.”

Several efforts were undertaken by the RBI in coordination with all

the parties associated including the government of India in the said direction

such as Supporting the establishment of the required Infrastructure, setting of

National Strategy, Establishment of Digital Ombudsman, Awareness

programmes etc. The Government efforts in the form of Launch of PMJDY,

DBT, AEPS, Payment Banks etc. have also contributed significantly in bringing

the unbanked masses in the ambit of the financial inclusion.

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 19 E-Mail : [email protected]

All the above mentioned efforts of all the associated stakeholders in

the direction of the Digitisation of the banking efforts became more concentrated

with the outbreak of the COVID-19 pandemic. The demand of the digital

avenues has been increased significantly during the lockdown period as the

banks were opened for limited hours during the day. The physical currency was

also presumed as a carrier of the deadly virus therefore it was preferred by the

masses to transact digitally instead of visiting the bank branch.

The data provided by the Finance Ministry’s Department of

Financial Services (DFS) highlighted that during the last 40 days of the

lockdown the Average Daily transaction through AEPS transactions doubled to

1.13 crore. A total of 43 core transactions worth Rs 16,101 crore were made

during the lockdown period through AEPS.

OBJECTIVES OF THE STUDY

* To study the concept of Digitization in the banking sector.

* To study the initiatives undertaken by RBI to boost the digital transaction

in the COVID period.

* Analysis of the various payment system indicators have to be done by

collecting data from RBI and NPCI.

* To analyse Efforts done by the Payment Banks with special reference to

the IPPB (India Post Payment Bank) during the outbreak of the pandemic

period.

* RBI’s latest moves during the unlocking period to promote the digital

transactions have also been analyzed.

RESEARCH METHODOLOGY

This paper is a mix of conceptual and analytical paper. The study

mainly includes literature review from secondary data. The data is collected from

national and international journals, published government reports, Newspaper,

websites. The data has been analysed from the notifications of the RBI issued

from time to time. The data provided by the Department of Financial services on

the IPPB has also been collected and analysed.

Bhartiya Shod

Volume-1, Issue-2

Website - www.shodhpatrika.com

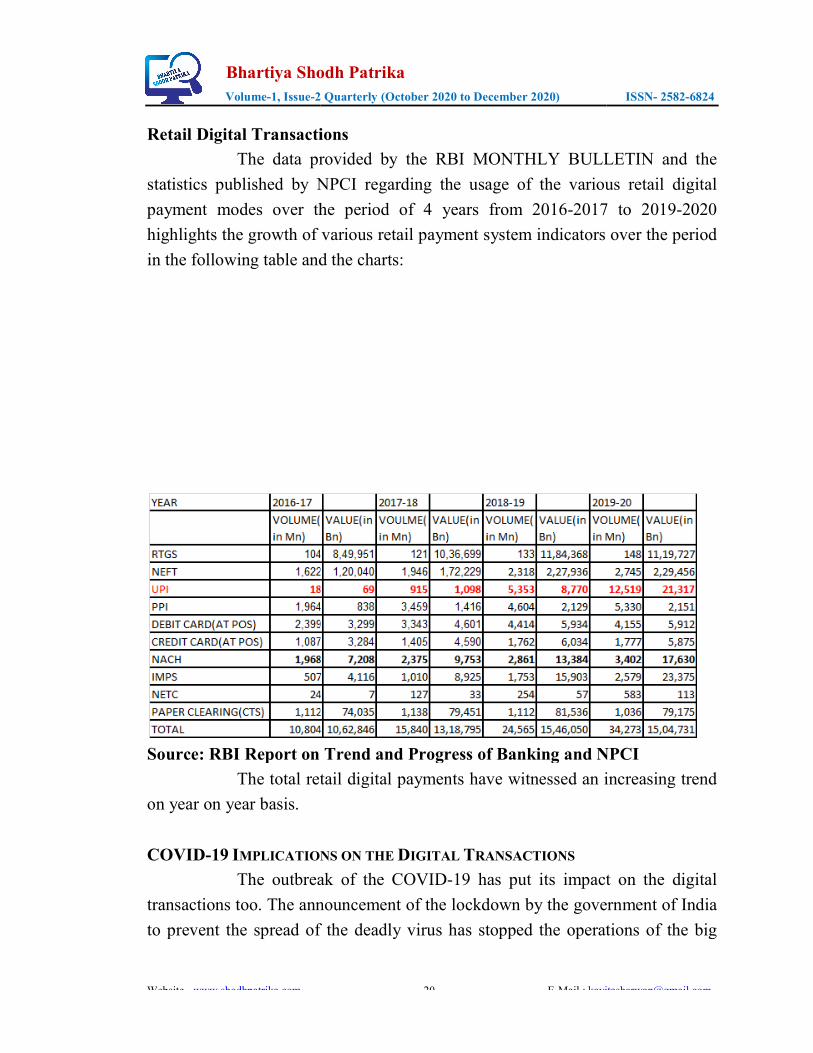

Retail Digital Transactio

The data pro

statistics published by NP

payment modes over the

highlights the growth of va

in the following table and

Source: RBI Report on T

The total reta

on year on year basis.

COVID-19 IMPLICATION

The outbreak

transactions too. The anno

to prevent the spread of t

Shodh Patrika

2 Quarterly (October 2020 to December 2020)

20 E-Mail : kavita

sactions

ta provided by the RBI MONTHLY BULLE

by NPCI regarding the usage of the various

er the period of 4 years from 2016-2017

h of various retail payment system indicators o

e and the charts:

t on Trend and Progress of Banking and NP

al retail digital payments have witnessed an in

TIONS ON THE DIGITAL TRANSACTIONS

tbreak of the COVID-19 has put its impact

e announcement of the lockdown by the govern

d of the deadly virus has stopped the operatio

ISSN- 2582-6824

ULLETIN and the

arious retail digital

2017 to 2019-2020

ators over the period

nd NPCI

an increasing trend

pact on the digital

government of India

perations of the big

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 21 E-Mail : [email protected]

business houses, industries as a result of which the volume and the value of the

high value RTGS transactions got a setback in the initial period of the lockdown.

The data provided by the various payment system operators and the service

providers and RBI in this context is as follows:

* During Jan- May 2020 the cumulative value of the digital transactions

declined by 25.5 percent year on year basis.

* The retail digital transaction value declined by 10.6% as compared to

increase of 31.3% last year.

* Both the parameters (Total digital Transactions and the Retail Digital

Transactions) although start recovering in the unlocking period from May

2020.

* RBI move of waiving RTGS charges gave a push to the RTGS

transactions since July 2019. The volume of the RTGS transactions

although registered growth on year on year basis till February 2020 but

due to the Covid declined in March by 12.3%, April 52.5%, May 27.5%.

* The volume of the RTGS transactions regained in May 2020 as the

business were again set up on the track.

* The transactions through UPI has also got a setback in the lockdown

period. IMPS Transactions have started declining in Feb 2020 and the

trend continued since May 2020 with the sharpest decline in April 2020.

* UPI transactions Volume declined by 5.9% in March 2020 reaching to

less than 1 billion transactions since May 2020.

* The usage of the Rupay Cards at the E commerce portal has increased

manifold as compared to the usage at PoS due to social distancing.

All the above mentioned points highlights the Integration of the

Digital Economy with the Real Economy of the country which is a positive

indicator for future growth and prosperity of the country in the coming period.

DIGITISATION IN BANKING SECTOR

The definition of Digital Transaction as given by Banking

Ombudsman for Digital Transactions is: “Digital Transaction’ means a payment

transaction in a seamless system affected without the need for cash at least in

one of the two legs, if not in both. This includes transactions made through

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 22 E-Mail : [email protected]

digital / electronic modes wherein both the originator and the beneficiary use

digital / electronic medium to send or receive money.”

The introduction of the Digital technologies in the banking sector

has contributed significantly in the growth and development of this sector in

general and the economy as a whole in particular. It has been recognised

worldwide that the usage of the low cost digital technologies can contribute

significantly in bridging the gap between the banked and the unbanked and

underbanked sections of the society.

Therefore, the RBI and the government of the India has always

endeavoured to boost the digital transactions in the country with the ultimate

goal of forming a financially inclusive and prosperous economy.

Various efforts undertaken by the RBI and the Government of India

in the said direction are:

* PMJDY and Rupay Cards * Demonetisation

* Digital India Campaign

* On tap licensing of the Payment Banks and Small Finance Banks

* Digital Ombudsman * Deepening Digital Financial

Literacy

* Launch of UPI * Aadhar and India Stack

* JAM (Jan Dhan Aadhar Mobile Trinity) * Regulatory Sandbox.

* DBT (Direct Benefit Transfer) * GST

The ultimate goal of all the above mentioned efforts has been on

reducing the dependence of the paper currency and changing the mindset of the

masses towards the digital technologies. The efforts have been not only

concentrated to provide the support to strengthen the digital infrastructure but

extend till creating awareness and educating the masses to adopt digital modes of

payments.

RBI INITIATIVES TO BOOST THE DIGITAL TRANSACTIONS IN THE COVID

PERIOD.

The outbreak of the COVID-19 has put its impact on the economies

of the various countries with India has no escape. All the business activities

became standstill during the initial days. The imposition of the lockdown has

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 23 E-Mail : [email protected]

worsened the situation. The RBI and the government has to come up with the

plans of the revival of the economy with the twin goals of the development and

the safety of the masses.

The imposition of the Social Distancing norms, reduced operating

hours of the banks, assumption of the paper money as a carrier of the deadly

virus has encouraged masses to transact digitally during the Pandemic period.

RBI as a regulator bank of the banking sector has played a very significant role

in the said direction by encouraging the masses to transact digitally. Support of

the various modes of communication such as Advertisements by the Governor

Media on Television, Radio and Print Media was solicited to encourage the

masses.

The various endeavors of the RBI during the locking and unlocking

period in the direction of the Digitisation of the banking operations are as

follows:

� March 16, 2020: Availability of Digital Payment Options

The RBI has brought to the notice of the general public that the

various modes of transacting digitally like NEFT, IMPS, UPI are available round

the clock to facilitate fund transfer, making payments and payment of the bills.

RBI urged the masses to use these modes of transacting and avoid

visiting the crowded places to support the prevention of the spread of the deadly

virus.

The RBI has urged the members of the general public to change their mindset

and adopt the digital modes of transaction using the mobile phone and the

internet by sitting at their home itself. This will provide a boost to the digital

transactions in line with the RBI vision 2020-21 and safety of masses too.

* March 31, 2020: Doorstep banking services for Senior Citizens and

Differently Abled Persons.

RBI has advised banks to make concentrated efforts to offer certain

basic banking services to the senior citizens of more than 70 years of age and

differently abled persons at the doorstep.

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 24 E-Mail : [email protected]

* The doorstep services should be offered on Pan India basis. Banks should

prepare a Board approved framework for determining the branches where

such services will be provided.

* The Banks should create awareness among the masses about the

availability of such services by proper display arrangements in the

branches as well as on their websites.

* Various charges associated with the services should also be displayed for

the information of the masses.

� June 22, 2020: RBI Sensitises members of Public on safe use of Digital

Transactions.

Safety and Security of the Digital transactions are of paramount

importance to the users of the digital transactions. The RBI has always

concentrated its efforts on spreading the awareness among the masses regarding

the safe usage of the digital modes. The RBI’s flagship programme in the said

direction i.e. RBI KEHTA HAI has been actively implemented through print

and Audio visual media.

The programme focuses on spreading awareness on the following

basic parameters:

(i) Prohibited sharing of their ATM / Card (Debit / Credit / Prepaid) details

with anyone

(ii) not sharing their Password, PIN, OTP, CVV, UPI-PIN, etc.

(iii) avoid undertaking banking or other financial transactions through public,

open or free wifi-networks;

(iv) not storing important banking data on the mobile, e-mail, electronic wallet

or purse.

It has been reiterated that the bank never asks for such information from

their customers over the mobile phone.

DBT through APBS in Covid Pandemic

DBT stands for Direct Benefit Transfer. It is a scheme launched by

the government of India to transfer the benefits of various social security

schemes such as Pension, scholarship, LPG Subsidies etc. directly in the Aadhar

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 25 E-Mail : [email protected]

linked bank account of the beneficiaries. This has been used to prevent the

corruption and mismanagement of the government funds.

For facilitating the DBT transactions, a unique payment system was

operated by NPCI which uses Aadhar number as a basis for crediting the

government subsidiaries and benefits directly in the Aadhar enabled bank

account of the beneficiary.

During the COVID-19 pandemic this system was used by

government to provide financial assistance to the women Jan Dhan Account

Holders under PMJDY Scheme. A total 204 million Women Jan Dhan Account

holders received Rs 500 per month for 3 months in their bank accounts.

AEPS and COVID-19 Pandemic

AEPS stands for Aadhar Enabled Payment Systems. To facilitate

the disbursement of the government entitlements in the form of subsidiaries,

pension, scholarship etc. an interoperable payment system was developed by

NPCI. Under this system the beneficiary can withdraw money from his Aadhar

linked account of any bank with the help of micro ATMs held by the business

correspondents. The entire transaction can be completed with the following 3

inputs only:

(a) Bank Name (b) Aadhar number

(c) Fingerprint captured during enrollment.

Banking Services Offered by AePS are:

* Cash deposit * Cash Withdrawal

* Balance Enquiry * Mini statement

* Fund transfer through Aadhar

The AePS transactions using the micro ATMs has increased

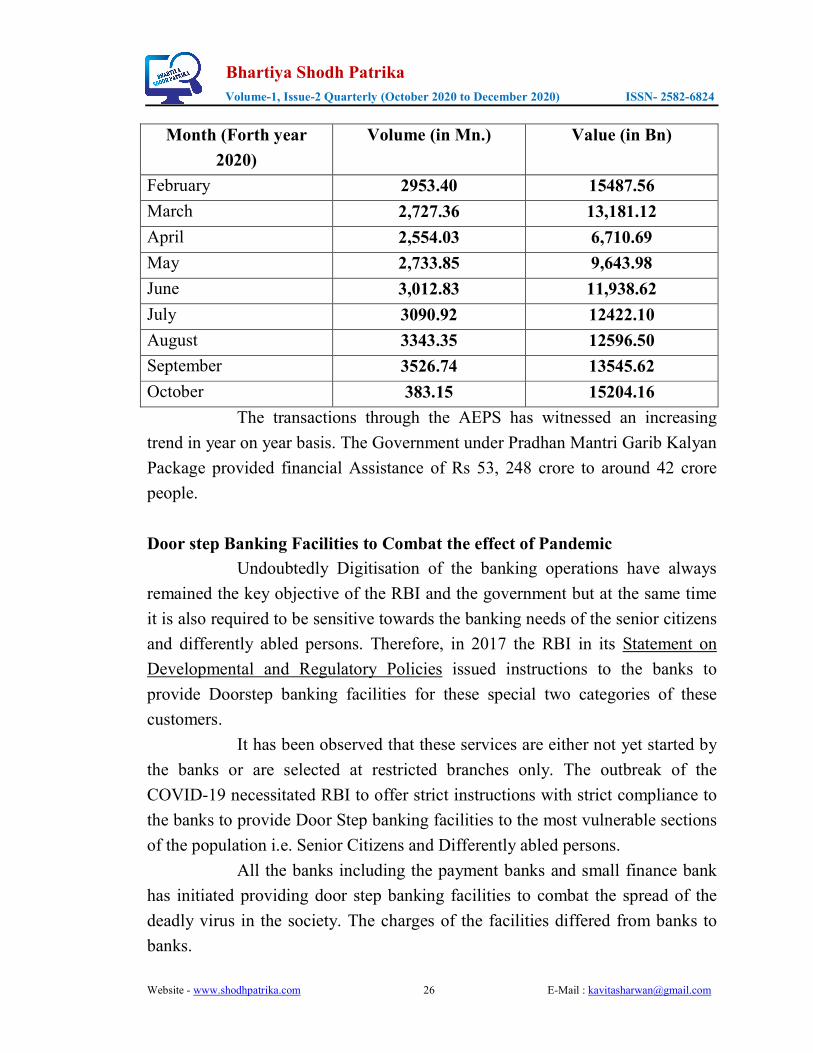

manifold during the pandemic period. The following table highlights the trend in

the usage of AEPS (Both financial and Non-Financial Transactions) during the

outbreak of COVID-19.

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 26 E-Mail : [email protected]

Month (Forth year

2020)

Volume (in Mn.) Value (in Bn)

February 2953.40 15487.56

March 2,727.36 13,181.12

April 2,554.03 6,710.69

May 2,733.85 9,643.98

June 3,012.83 11,938.62

July 3090.92 12422.10

August 3343.35 12596.50

September 3526.74 13545.62

October 383.15 15204.16

The transactions through the AEPS has witnessed an increasing

trend in year on year basis. The Government under Pradhan Mantri Garib Kalyan

Package provided financial Assistance of Rs 53, 248 crore to around 42 crore

people.

Door step Banking Facilities to Combat the effect of Pandemic

Undoubtedly Digitisation of the banking operations have always

remained the key objective of the RBI and the government but at the same time

it is also required to be sensitive towards the banking needs of the senior citizens

and differently abled persons. Therefore, in 2017 the RBI in its Statement on

Developmental and Regulatory Policies issued instructions to the banks to

provide Doorstep banking facilities for these special two categories of these

customers.

It has been observed that these services are either not yet started by

the banks or are selected at restricted branches only. The outbreak of the

COVID-19 necessitated RBI to offer strict instructions with strict compliance to

the banks to provide Door Step banking facilities to the most vulnerable sections

of the population i.e. Senior Citizens and Differently abled persons.

All the banks including the payment banks and small finance bank

has initiated providing door step banking facilities to combat the spread of the

deadly virus in the society. The charges of the facilities differed from banks to

banks.

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 27 E-Mail : [email protected]

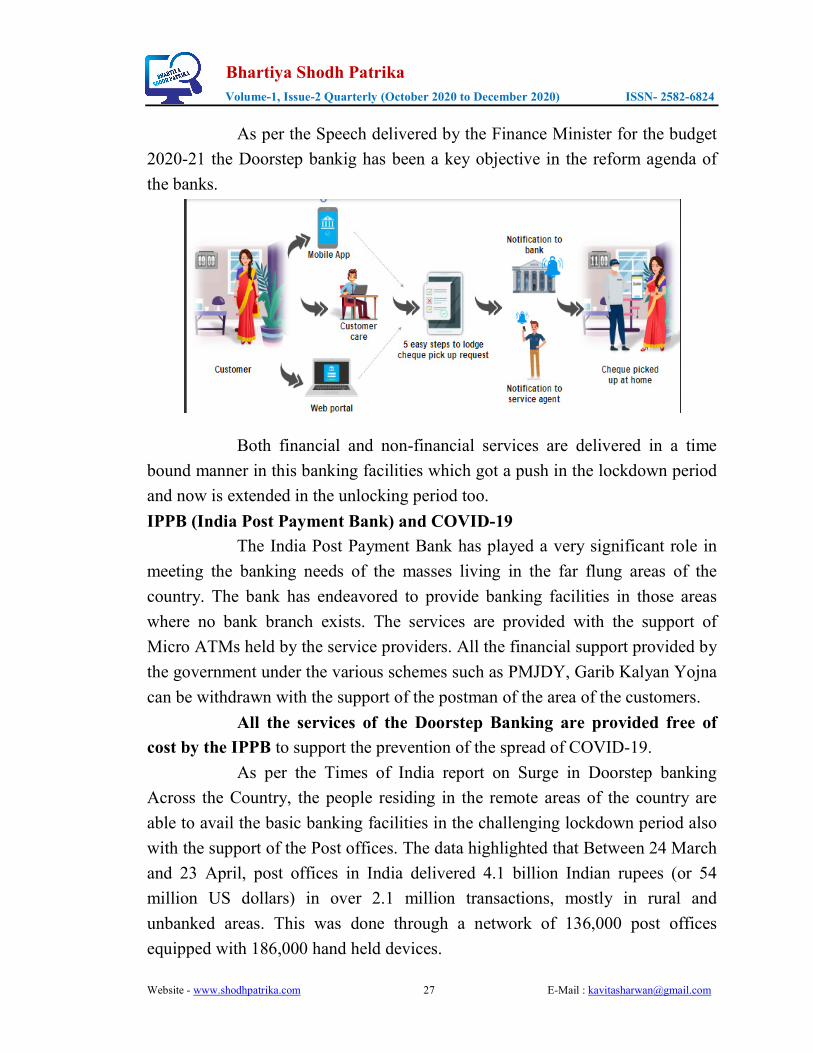

As per the Speech delivered by the Finance Minister for the budget

2020-21 the Doorstep bankig has been a key objective in the reform agenda of

the banks.

Both financial and non-financial services are delivered in a time

bound manner in this banking facilities which got a push in the lockdown period

and now is extended in the unlocking period too.

IPPB (India Post Payment Bank) and COVID-19

The India Post Payment Bank has played a very significant role in

meeting the banking needs of the masses living in the far flung areas of the

country. The bank has endeavored to provide banking facilities in those areas

where no bank branch exists. The services are provided with the support of

Micro ATMs held by the service providers. All the financial support provided by

the government under the various schemes such as PMJDY, Garib Kalyan Yojna

can be withdrawn with the support of the postman of the area of the customers.

All the services of the Doorstep Banking are provided free of

cost by the IPPB to support the prevention of the spread of COVID-19.

As per the Times of India report on Surge in Doorstep banking

Across the Country, the people residing in the remote areas of the country are

able to avail the basic banking facilities in the challenging lockdown period also

with the support of the Post offices. The data highlighted that Between 24 March

and 23 April, post offices in India delivered 4.1 billion Indian rupees (or 54

million US dollars) in over 2.1 million transactions, mostly in rural and

unbanked areas. This was done through a network of 136,000 post offices

equipped with 186,000 hand held devices.

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 28 E-Mail : [email protected]

The numbers more than doubled in the next three weeks and 50

days of the lockdown marked 10 billion Indian rupees (133 million US dollars)

in cash being delivered by postmen to account holders at their doorstep.

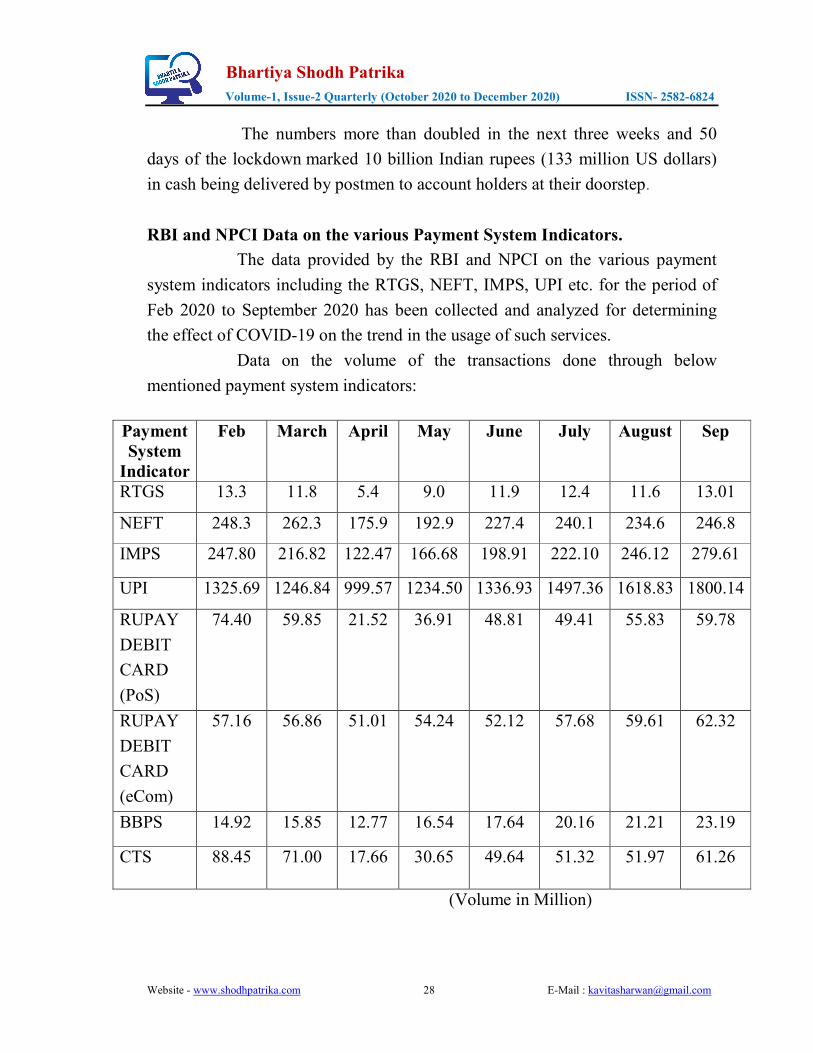

RBI and NPCI Data on the various Payment System Indicators.

The data provided by the RBI and NPCI on the various payment

system indicators including the RTGS, NEFT, IMPS, UPI etc. for the period of

Feb 2020 to September 2020 has been collected and analyzed for determining

the effect of COVID-19 on the trend in the usage of such services.

Data on the volume of the transactions done through below

mentioned payment system indicators:

(Volume in Million)

Payment

System

Indicator

Feb March April May June July August Sep

RTGS 13.3 11.8 5.4 9.0 11.9 12.4 11.6 13.01

NEFT 248.3 262.3 175.9 192.9 227.4 240.1 234.6 246.8

IMPS 247.80 216.82 122.47 166.68 198.91 222.10 246.12 279.61

UPI 1325.69 1246.84 999.57 1234.50 1336.93 1497.36 1618.83 1800.14

RUPAY

DEBIT

CARD

(PoS)

74.40 59.85 21.52 36.91 48.81 49.41 55.83 59.78

RUPAY

DEBIT

CARD

(eCom)

57.16 56.86 51.01 54.24 52.12 57.68 59.61 62.32

BBPS 14.92 15.85 12.77 16.54 17.64 20.16 21.21 23.19

CTS 88.45 71.00 17.66 30.65 49.64 51.32 51.97 61.26

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 29 E-Mail : [email protected]

Interpretation:

� As the business activities were slowed down due to the lockdown imposed

by the government the RTGS transactions got a big hit in the month of

April and later the transactions improved slowly and slowly.

� The NEFT transactions have also got a setback in the initial days of the

lockdown in the month of April and started recovering in the later months.

� The IMPS transactions although slowed in month of April but regained

very fast in the coming months. As the IMPS transactions are preferred for

small value transactions the declining trend recovered very fast.

� The UPI transactions have also witnessed the same trend as IMPS. The

transactions through UPI has become even more in the post lockdown

period as compared to the pre lockdown period.

� The impact of the social distancing can be witnessed in the Rupay Debit

Card transactions as people preferred to use Debit Card at online

transactions instead of using it at PoS Terminals.

� The BBPS transactions have increased on month on month basis

highlighting the acceptance of digital means of transacting over making

the bill payments over the counter.

� The CTS Transactions through dipped in April but regained in later

months.

All the above points highlight the integration of digital modes of the payment

with the mindset and acceptance by the masses.

Recent Initiatives undertaken by RBI in the post lockdown period to boost

Digitisation.

Recognizing the integration of the digital modes of the payment

systems with the society the RBI has undertaken several latest initiatives in the

said direction to boost the economic growth and prosperity of the nation. Few

latest initiatives include:

* Setting up of Innovation Hub for Financial Inclusion and Efficient

Banking.

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 30 E-Mail : [email protected]

The RBI in its endeavors to set up a financially inclusive economy

has planned to set up an Innovation Hub to incubate the new ideas and

capabilities that can be leveraged to boost the growth of the economy.

The Regulatory Sandbox is one of the initiative in the said direction

wherein the new ideas are tested and implemented in a closed environment. But

due to the outbreak of COVID-19 various testing activities were delayed.

* Offline Retail Payment System using Mobile, Card, wallets- Pilot

The RBI in its Statement on Developmental and Regulatory

Package dated 6 Aug 2020 instructed banks and the service providers to provide

offline retail payment system using mobile, cards and Wallets for remote

payments. The testing will be conducted in a closed environment to test the

viability of the project. The scheme shall be implemented till March 2021.

* Online Dispute Resolution System for Digital Payments.

To boost the retail digital payments in the country it is required that

the masses of the country should be ready to accept these services. For this the

retail payment system should be efficiently monitored and the dispute resolution

system should be put in place that can handle the grievances in an effective and

efficient manner.

It will support the growth as well as the stability of the entire

financial system in the country.

Conclusion

The banking sector has witnessed several changes since

nationalization. The introduction of the information technology in the banking

sector has gradually revolutionized the entire banking sector. From online banks

branches to internet banking, the banking services are extended to provide

Doorstep banking services to the customers. Reserve Bank of India and the

government has always endeavored to use low cost technology to reach the goals

of the Financial Inclusion by providing the access of baking services to the

masses residing in far flung areas of the country.

The outbreak of the COVID-19 disturbed all the activities of the

masses. Banking Services are of paramount importance which are required to be

delivered to the masses in a safe and secure manner. The Digitisation of the

operations of the banks was the important tool in the hand of the government and

Bhartiya Shodh Patrika

Volume-1, Issue-2 Quarterly (October 2020 to December 2020) ISSN- 2582-6824

Website - www.shodhpatrika.com 31 E-Mail : [email protected]

RBI to reach the goals of providing financial assistance to the peoples living in

rural areas.

Various efforts were undertaken by RBI to encourage masses to

adopt digital modes of payment to perform their routine activities. The RBI in its

attempt to push the digital growth also promoted safe use of these modes and

educating masses to not to share their personal details such as OTP, ATM pin

etc. over the mobile phone.

Introduction of the Doorstep banking facilities and the role played

by the Postman of IPPB played a significant role in helping the masses to combat

the effects of COVID-19. The analysis of the data of various digital modes of

payment pre and post lockdown period highlights the acceptance and integration

of the digital modes of payment in the society as the volume of the digital

transactions slowed down in the initial days of lockdown.

Thus it can be concluded that Digitisation is the need of the hour.

Digital transactions can play an important role if conducted in a safe and secured

manner.

References

1. Raghavendra Nayak “A Conceptual Study on Digitalization of Banking - Issues and

Challenges in Rural India”, International Journal of management, IT and Engineering,

2018.

2. K. Suma Vally and K. HemaDivya “A Study on Digital Payments in India with

Perspective of Consumer’s Adoption”, International Journal of Pure and Applied

Mathematics, 2018.

3. MathangiR. ,Latasri O.T. and Isaiah OnsarigoMiencha “Improving Service Quality

through Digital Banking - Issues and Challenges”, International Journal of Recent

Scientific Research, 2017.

4. IpsitaParia and Dr. ArunangshuGiri “A Literature Review on Impact of Digitalization

on Indian Rural Banking System and Rural Economy”, Research Review International

Journal of Multidisciplinary, 2018.

5. Anthony Rahul Golden S. “An Overview of Digitalization in Indian Banking Sector”,

Indo - Iranian Journal of Scientific Research (IIJSR), October -December, 2017.

6. Santiago Carbo -Valverde “The Impact on Digitalization on Banking and Financial

Stability”, Journal of Financial Management, Markets and Institutions, 2017.