director networks, information environment, and corporate … · 2020-03-18 · 1 1. introduction...

TRANSCRIPT

Director Networks, Information Environment, and Corporate Investment

Rebecca N. Hann

Robert H. Smith School of Business

University of Maryland

Musa Subasi

Robert H. Smith School of Business

University of Maryland

Yue Zheng

School of Business and Management

The Hong Kong University of Science and Technology

Marcy 2019

Abstract

We explore whether director connections improve the efficiency of a firm’s investment decisions

by enhancing its external information environment. We find that board connectedness is

negatively associated with the extent of under- and overinvestment. The effect of board

connectedness on underinvestment is stronger for firms characterized by greater financial

constraints, higher demand for external capital, lower financial reporting quality, and less analyst

following, while the effect of board connectedness on overinvestment is stronger for firms

subject to greater monitoring by external stakeholders and higher agency costs. These findings

suggest that director networks serve as an information intermediary that provides important

information to external capital providers and monitors, thereby mitigating underinvestment

arising from capital constraints and overinvestment arising from agency problems.

Keywords: Director networks; information environment; investment efficiency; information

asymmetry; agency costs.

JEL Classifications: G3, G14, L14, G31

We would like to thank Ferhat Akbas, David Erkens, Gilles Hilary, Fikret Polat, and workshop participants at the

University of Maryland, the 2017 Washington Area Accounting Conference, and the 2018 Carnegie Mellon

University Summer Slam Conference for their valuable comments.

1

1. Introduction

Director networks serve as a conduit of information exchange and knowledge sharing

among corporate board members. Prior studies suggest that director networks can affect

corporate decisions by influencing the firm’s internal information set (e.g., Haunschild and

Beckman, 1998; Beckman and Haunschild, 2002). However, the flow of information in the

network is not unidirectional—important information about the firm can also be transmitted from

the firm’s corporate directors to external market participants such as short sellers, mutual fund

managers, and sell-side analysts (e.g., Cohen et al., 2008, 2010; Akbas et al., 2016;). A natural

question that arises is: Does this outflow of information affect the quality of managers’ corporate

decisions by influencing the firm’s external information environment? In this paper, we shed

light on this question by examining the effect of boardroom connections on corporate investment

efficiency.

Ex-ante, whether boardroom connections have a significant effect on a firm’s external

information environment, or how such an effect should influence the firm’s investment

efficiency, is unclear. On the one hand, ample empirical evidence suggests that both public and

private information travels through director networks. To the extent that boardroom connections

enhance a firm’s external information environment, these connections may improve investment

efficiency through two channels. First, by facilitating the transmission of private information to

outside stakeholders, board connections can reduce information asymmetry between the firm and

its external capital providers and thereby mitigate the underinvestment problem arising from

capital constraints. Second, by improving the information sets of external monitors such as

institutional investors and analysts, board connections can improve these monitors’ ability to

2

assess the firm’s investment opportunities and oversee managerial investment decisions, and

thereby, curb the overinvestment problem caused by managerial entrenchment.

On the other hand, corporate directors have a duty of confidentiality and may suffer

potential legal and reputational consequences for revealing sensitive firm information to

outsiders, which implies that the extent to which value-relevant information is transmitted to

outsiders may be limited. Moreover, sensitive firm information may be revealed to only certain

groups of outsiders through the boardroom network, which could result in increased information

asymmetry among investors. For example, Akbas et al. (2016) show that for firms with more

connected directors, the trades of sophisticated investors such as short sellers, option traders, and

financial institutions reveal a higher degree of informedness. To the extent that only a subset of

investors are privy to the private information transmitted in the network, boardroom connections

may lead to greater adverse selection, which can exacerbate underinvestment for capital-

constrained firms. In addition, information transmitted through director networks may be

miscommunicated, misleading, or incorrect, in which case such information may not always be

useful to external investors and monitors. Thus, whether director connections can increase

investment efficiency by improving a firm’s external information environment is a priori unclear.

In this paper, we address this question by exploring the separate effects of director

connections on under- and overinvestment. Identifying the different effects of boardroom

connections on under- and overinvestment is important because the factors that drive

underinvestment are quite different from those that drive overinvestment. In particular, firms

tend to underinvest for reasons related to financial constraints, while they tend to overinvest for

reasons related to agency problems (e.g., Jensen 1986, 2005; Stulz, 1990; Harford, 1999; Biddle

et al., 2009). These different determinants of under- and overinvestment allow us to study the

3

information and monitoring roles of director networks and formulate two sets of hypotheses.

First, we predict that if board connections reduce information asymmetry by facilitating

information flow to external capital providers, then the extent of underinvestment should be

lower for more connected firms, with this effect stronger for firms that are more financially

constrained and for firms with a weaker external information environment. Second, we predict

that if board connections mitigate agency problems by enhancing monitoring from external

monitors (e.g., institutional investors), then the extent of overinvestment should be lower for

more connected firms, with this effect stronger for firms with higher agency costs and for firms

with a greater presence of external monitors.

We test these hypotheses using a panel of U.S. firms over the period 2000-2015. To

capture board connectedness, we use the total number of first-degree links to outside boards, a

measure that is widely used in the social network literature (e.g., Salk and Brannen, 2000;

Larcker et al., 2013; Chuluun et al., 2014).1 Investment inefficiency is defined as the extent to

which firm investment deviates from the level predicted given the firm’s investment

opportunities (Brennan, 2003). Accordingly, we follow prior studies (e.g., Biddle et al., 2009;

Chen et al., 2011) and measure investment inefficiency as the absolute value of the difference

between actual investment and the expected level of investment given the firm’s investment

opportunities, with a positive (negative) difference reflecting overinvestment (underinvestment).

We begin our analysis by exploring the effect of board connectedness on investment

efficiency for the “underinvestment” sample. We find that investment is significantly more

1 We use first-degree director connections as our primary measure of board connectedness in part because it allows

us to retain a larger number of observations in our sample. Also, for information flowing from the firm to external

market participants, higher-degree connections may result in the transmission of more noisy information about the

firm, and hence may play less of a role in enhancing a firm’s external information environment. Nevertheless, we

employ three alternative measures of connectedness used in the social network literature, namely, CLOSENESS,

BETWEENESS, and EIGENVECTOR, in our main tests. See Section 3.2.2 for a more detailed discussion.

4

efficient for firms with more connected boards, controlling for various factors previously shown

to affect investment efficiency (e.g., financial reporting quality, institutional ownership, and

financial slack). In particular, investment efficiency is 13% higher when we move from the firms

in the highest connectedness decile to those in the lowest decile, ceteris paribus, which points to

an economically significant effect of board connectedness on the efficiency of capital outlays.

While the negative association between board connectedness and the degree of

underinvestment is consistent with boardroom connections improving investment efficiency, the

exact mechanism is unclear. This result could be driven by board connectedness enhancing a

firm’s external information environment, which improves access to external capital due to

reduced information asymmetry between the firm and external capital providers, or by

boardroom connections enhancing a firm’s internal information environment (e.g., through the

board’s advising role), which allows managers to make more informed decisions.2 We conjecture

that if the reduction in underinvestment for more connected firms is driven at least in part by the

first channel (i.e., the “external information channel”), the effect should be stronger for more

financially constrained firms. Consistent with this conjecture, we find that the effect of

connectedness on underinvestment is stronger for financially constrained firms (as captured by

the Whited-Wu index, the Hadlock-Pierce size and age index, and the absence of an S&P debt

rating). We further examine whether the effect of board connectedness on underinvestment

varies with firms’ need for external capital. We find that the effect of connectedness on

underinvestment is stronger for firms with greater demand for external equity financing (as

captured by Rajan and Zingales’ (1998) measures of external capital needs).

2 Although we control for measures of managers’ information quality in our multivariate analysis, our results may be

driven in part by board connectedness improving managers’ information set.

5

To shed additional light on the external information channel, we examine how the effect

of board connectedness on underinvestment varies with the strength of other information sources

that affect the firm’s external information environment. Prior research finds that high-quality

financial reporting and analyst coverage reduce information asymmetry and facilitate efficient

investment. If director connections serve as an alternative source of information, their effect on

underinvestment should be weaker to the extent that capital providers benefit from other

information mechanisms in place. Consistent with this conjecture, we find that the effect of

connectedness on underinvestment is less pronounced for firms with higher financial reporting

quality and more analyst following, which suggests that director networks serve as a substitute

for other external information mechanisms.

We also explore whether the information transmitted to external capital providers comes

primarily from directors’ connections to banks. To do so, we construct a measure of

connectedness that focuses on connections to financial institutions. We find that, directors’

connections to banks have no incremental effect on the extent to which firms underinvest after

controlling for the total number of interlocks, suggesting that the effect of board connectedness

on underinvestment is not an artifact of directors’ connections to financial institutions. Taken

together, our findings are consistent with director networks serving as an important information

intermediary that enhances a firm’s external information environment, which mitigates

underinvestment arising from information asymmetry.

Next, we explore the effect of board connectedness on investment efficiency for the

“overinvestment” sample. In univariate analyses, we find a negative and statistically significant

association between board connectedness and the degree of overinvestment. In multivariate

analyses, however, the negative association becomes statistically insignificant. The absence of a

6

significant effect could be driven by board connectedness having offsetting effects on investment

efficiency for firms with different characteristics. Specifically, as we discuss above, while board

connectedness may improve a firm’s external information environment, which should increase

the monitoring effectiveness of other external stakeholders, boardroom connections may

negatively affect the board’s own monitoring. Indeed, prior research shows that boards with

social ties to their CEOs have greater advisory ability but lower monitoring efficiency (e.g.,

Schmidt, 2015; Hwang and Kim, 2009). Barnea and Guedj (2009) further argue that when

directors are not connected, they work to build their reputation by providing superior monitoring,

whereas when they are highly connected, they provide softer monitoring as they feel that their

status in the network is secure. To shed light on whether the information transmission role of

boardroom connections enables external stakeholders to become better monitors of managerial

actions, we conduct two sets of cross-sectional tests.

First, we examine whether the effect of board connectedness on overinvestment varies

with the degree of external monitoring. If director networks transmit information that is

incrementally useful to external monitors, board connectedness should have a more pronounced

effect on overinvestment for firms with greater external monitoring. In contrast, if board

connectedness is a substitute for other forms of external monitoring, then its effect on

overinvestment should be weaker for firms with greater external monitoring. We find that well-

connected firms with higher institutional ownership and analyst coverage are less likely to

overinvest. This result suggests that the external information effect of director networks

improves the monitoring effectiveness of external stakeholders and thereby curbs overinvestment

from entrenched managers.

7

Second, we examine whether the effect of board connectedness on overinvestment is

stronger for firms that have higher agency costs. Following prior theory and evidence on the

agency costs of free cash flow and overvalued equity (Jensen, 1986, 2005; Moeller,

Schlingemann, and Stulz, 2005; Fu, Lin, and Officer, 2013), we capture agency costs using two

measures, namely, excess cash holdings and stock overvaluation.3 We find that well-connected

firms with higher excess cash holdings or overvalued equity are less likely to overinvest

compared to their less-connected counterparts. Taken together, our results suggest that

boardroom connections provide value-relevant information to external monitors, which helps

mitigate overinvestment arising from agency problems.

Our causal inference based on the relationship between board connectedness and

investment efficiency may suffer from the endogenous nature of board connectedness. First, it is

possible that an omitted or unobservable firm characteristic that drives both investment

efficiency and board connectedness results in a spurious correlation between these two variables.

For example, more prestigious firms or firms with higher-quality managers may make more

efficient capital outlay decisions, and at the same time attract more connected directors to serve

on the board.4 Second, it is possible that our results suffer from reverse-causality, whereby firms

that make more efficient investment decisions recruit more connected directors to benefit from

these directors’ access to information and resources. We conduct four sets of tests to address

these endogeneity concerns. First, we control for various measures of managerial quality such as

management forecast accuracy and the ratio of insider stock transactions to total transactions. We

3 Consistent with Jensen’s (2005) theory on the agency costs of overvalued equity, Fu et al. (2013) find that

overvalued acquirers significantly overpay for their targets. Similarly, Moeller, Schlingemann, and Stulz (2005) find

that bidders in large loss deals have significantly larger market-to-book ratios. These findings suggest that

overvalued acquirers engage in value-destroying acquisitions. 4 Consistent with this idea, Masulis and Mobbs (2014) find that directors who serve on multiple boards allocate their

time and effort to each firm based on the firm’s relative prestige.

8

continue to find similar results. Second, as in Larcker et al. (2013) and Schabus (2018), we

restrict our sample to firms whose board composition remains unchanged from the prior year to

the current year, which ensures that any change in board connectedness stems from exogenous

changes in a given board member’s outside directorships. When we rerun our main analyses with

this restricted sample, we continue to obtain similar results. Third, we include firm fixed effects

to control for time-invariant firm-specific unobservable or omitted factors. We again obtain

similar results. Finally, as in Larcker et al. (2013), we examine the relationship between board

connectedness in a given year and lagged changes in investment efficiency. We find no evidence

of an association between prior investment efficiency and current board connectedness. These

tests help corroborate our causal inference that board connectedness results in more efficient

investment decisions.

Our paper makes several contributions to the literature. First, our study adds to the

growing literature on the effect of director networks on corporate decisions and firm value (e.g.,

Larcker et al., 2013; Akbas et al., 2016; Schabus, 2018) by uncovering a new channel through

which director networks can have real effects and enhance firm value. Specifically, our results

suggest that director connections, by enhancing a firm’s external information environment, can

lead to more efficient investment decisions. Second, prior studies that explore the role of

boardroom connections as a source of information focus primarily on the flow of information

from the network to the firm (e.g., Haunschild and Beckman, 1998; Beckman and Haunschild,

2002). Our paper extends this work by establishing that the flow of information in the director

network is not unidirectional. In particular, we show that real benefits derive from the flow of

information from the firm to external market participants. Third, our paper complements the

growing literature on the effect of the information environment on investment efficiency (e.g.,

9

Biddle et al., 2009; Chen et al., 2011, Shroff et al., 2014). Our findings suggest that director

networks have a significant effect on the firm’s external information environment, and in turn

investment efficiency, that is incremental to the effect of analyst coverage and financial reporting

quality. Moreover, our cross-sectional results indicate that director networks represent an

important channel of information exchange that serves as a substitute for other information

intermediaries such as analysts, and that choosing a well-connected board may be an effective

way to improve a firm’s external information environment.

The rest of the paper is organized as follows. Section 2 provides a brief discussion of the

prior literature and motivates our analyses. Section 3 describes our sample, variables, and

research design. Sections 4 and 5 present our main empirical results. In section 6 we discuss

additional analyses and robustness tests. Finally, section 7 concludes.

2. Related Literature and Motivation

Corporate directors build valuable experience and knowledge over the years serving as

board members and possess a wealth of firm-, industry-, and market-related information.

Connections with corporate officers serving on various boards provide channels through which

directors could exchange information and resources, form new relationships, and leverage

existing ones (Larcker et al. 2013). Several studies examine the effect of director networks on

firms’ internal information environment and the quality of various corporate decisions. For

example, Beckman and Haunschild (2002) show that firms pay lower premiums and engage in

better performing acquisitions when they are connected to other firms that have heterogeneous

prior acquisition experience. Larcker et al. (2013) highlight the role of director networks as a

channel through which firms share information and resources and show that firms with well-

connected boards earn superior stock returns. Similarly, Schabus (2018) argues that better access

10

to information and resources enables well-connected firms to make higher quality planning and

forecasting. Collectively, the results in these studies highlight the role of director networks as a

channel through which managers become informed about other firms’ practices and use that

information in their strategic decisions.

The effect of director networks on firms’ internal information environment

notwithstanding, the findings in nascent research point to the possibility that the information in

director networks could flow to external market participants, which in turn could have an impact

on the firm’s external information environment. For example, Cohen, Frazzini, and Malloy

(2010) show that sell-side analysts gain comparative information advantages through their

educational ties with senior officers and board members of firms that they cover. In a similar

vein, Akbas et al. (2016) show that sophisticated traders such as short sellers, option traders, and

institutional investors execute more profitable trades in the stocks of firms whose boards have

more connected directors. The results in these studies highlight the role of director networks as a

mechanism that could alter a firm’s external information environment. However, it is unclear ex-

ante whether the impact of director networks on firm’s external information environment is

beneficial or detrimental to the wealth of existing stakeholders. We shed light on this question by

examining the effect of director networks on investment efficiency.

A large body of prior work has examined the impact of various economic and

institutional forces on the efficiency of corporate investment (e.g., Love 2003; Chen et al. 2011;

Bae et al. 2017). Most related to our study is the stream of literature on the effects of the firm’s

external information environment on the quality of firms’ investment decisions. Using various

measures of accounting quality, Biddle and Hilary (2006) show that higher-quality accounting

enhances the efficiency of investment decisions. Further refining the notion of investment

11

efficiency, Biddle et al. (2009) show that higher-quality financial reporting reduces both over-

and underinvestment. Chen et al. (2011) use a sample of private firms from emerging markets

and document a significant effect of financial reporting quality on investment efficiency.

Goodman et al. (2014) show that the quality of manager’s earnings forecasts, an externally

available measure of managers’ forecasting ability is associated with better performing

acquisitions and more efficient fixed capital investments. Further, aspects of financial reporting

behavior such as accounting conservatism (Lara, Osma, and Penalva, 2016), financial

misreporting (McNichols and Stubben 2008), and the disclosure of material internal control

weaknesses (Cheng, Dhaliwal, and Zhang 2013) affect the quality of corporate investment

decisions. Finally, a battery of studies investigates how information quality affects capital

allocation efficiency and economic growth in the international setting. For example, Shroff et al.

(2014) find that the investment decisions of foreign subsidiaries in country-industries with more

transparent information environments are more responsive to local growth opportunities.5

A priori the predictions on how board connectedness affects a firm’s external

information environment and, in turn, its investment efficiency are mixed. On the one hand, if

director networks enhance a firm’s external information environment and facilitate better access

to relevant firm-specific information for capital providers, then they should have a positive

impact on investment efficiency by reducing the extent of both under- and overinvestment. With

respect to underinvestment, the effect of board connectedness on investment efficiency likely

stems from director networks reducing the information asymmetry between the firm and its

capital providers. Hence, the information risk perceived by capital providers should be lower for

firms with well-connected boards compared to otherwise similar firms and, therefore, board

connectedness should mitigate the underinvestment problem arising from financial constraints.

5 Other related studies include Francis, Huang, Khurana, and Pereira (2009), and Li and Shroff (2010).

12

Similarly, for firms that otherwise would overinvest, connected boards could facilitate

information transmission to external monitors (e.g., institutional investors and analysts) and

enable them to become more effective monitors of corporate investment, which in turn should

mitigate the overinvestment that arises due to agency problems.

On the other hand, the information spread through director networks may be

miscommunicated, incorrect, or misleading (Larcker et al. 2013) and may not possess the two

fundamental qualitative characteristics of decision useful information—relevance and faithful

representation—to enhance the information environment of the firm and affect capital providers’

decisions.6 Moreover, boardroom connections have been instrumental in the diffusion of various

negative corporate practices such as option backdating (Bizjak et al., 2009), poison pill adoptions

(Davis 1991), and earnings management (Chiu et al., 2013), all of which could have a

detrimental effect on the firm’s external information environment upon revelation.7

For privately disseminated information, such as that transmitted through director

networks, there is the added issue of how widely disseminated the information is (i.e., are less

connected investors at an information disadvantage relative to those who can tap on the director

networks). The results in Cohen et al (2010) and Akbas et al. (2016) suggest that firm-specific

information is transmitted to select groups of investors or information intermediaries. If frictions

in financial markets prevent these agents from signaling their private information to other

stakeholders, then boardroom connections may lead to adverse selection, which can exacerbate

underinvestment for capital-constrained firms. Given these opposing arguments, whether director

6 Statement of Financial Accounting Concepts No. 8 (September 2010). 7 Other studies on interfirm mimetic behavior have shown that firms with shared directors have more similar

governance structures (Bouwman, 2011), similar effective tax rates (Brown and Drake, 2014), and are more likely to

follow tied firms’ when switching stock exchanges (Rao, Davis, and Ward 2000).

13

networks improve firms’ external information environment and, in turn, the efficiency of

investment decisions is ultimately an empirical question.

3. Sample Selection, Variable Construction, and Research Design

3.1. Sample

Our sample begins with all firms covered in the BoardEx database over the period from

2000 to 2015. We exclude firms in the financial industries (SIC code 6000 – 6999) and utility

industries (SIC code 4900 – 4999) and drop firm-year observations with less than $1 million

book value of assets. Financial information is from Compustat, analyst forecast data are from

I/B/E/S, and institutional ownership data are from Thomson Reuters 13f filings. We require a

minimum of 20 observations in each industry-year to construct our investment efficiency

variables. After conducting these screening procedures and merging with various datasets, our

final sample includes 29,432 firm-year observations covering 3,830 unique firms operating in 39

industries based on the Fama and French 48 industry portfolios.

3.2. Variable Construction

3.2.1. Investment (in)efficiency

We follow prior studies (Biddle et al. 2009; Chen et al. 2011; Chen et al. 2013) and

measure investment (in)efficiency by estimating a parsimonious model of investment that

captures the extent to which a firm deviates from the expected investment level. Specifically,

using sales growth in a given year as a proxy for a firm’s growth opportunities, we estimate the

following model:

𝐼𝑁𝑉𝐸𝑆𝑇𝑀𝐸𝑁𝑇𝑖,𝑡+1 = 𝛼0 + 𝛼1𝑆𝐴𝐿𝐸𝑆_𝐺𝑅𝑖,𝑡 + 𝜀𝑖,𝑡+1, (1)

where 𝐼𝑁𝑉𝐸𝑆𝑇𝑀𝐸𝑁𝑇𝑖,𝑡+1 is firm i’s total investment in year t+1, calculated as the sum of

capital expenditures, research and development expenditures, and acquisition expenditures less

14

cash receipts from the sale of property, plant, and equipment and divided by lagged total assets.

For easier presentation, we follow Biddle et al. (2009) and multiply 𝐼𝑁𝑉𝐸𝑆𝑇𝑀𝐸𝑁𝑇𝑖,𝑡+1 by 100.

𝑆𝐴𝐿𝐸𝑆_𝐺𝑅𝑖,𝑡 is the percentage change in firm i’s sales between year t-1 and t. The model is

estimated within each Fama and French 48 industry portfolio with at least 20 observations in a

given year.

The residuals from Equation (1) capture the deviation from the predicted investment level

and are used to measure firm investment (in)efficiency. We classify firms with negative

(positive) residuals in a given year as underinvesting (overinvesting) firms. INVEST_INEFF is

defined as the absolute value of the residuals from Equation (1), and higher values of that

variable reflect a larger degree of under- or overinvestment.

3.2.2. Board Connectedness

To measure director connectedness, we follow prior research (e.g., Larcker et al., 2013;

Chuluun et al. 2014; Bajo et al. 2016) and examine four dimensions of well-connectedness

established in the social networks literature.8 Our primary measure, DEGREE, captures the total

number of first-degree links to outside boards. Intuitively, a board is better connected if its

directors have more direct links with individuals in outside boards. The second measure,

CLOSENESS, captures how easily or quickly a board can reach an outside board through

interlocking directorates. It is measured as the inverse of the average distance between a board

and an outside board. The third measure, BETWEENESS, captures how well-situated a board is

in terms of the network paths it lies on. It is defined as the average proportion of paths between

two other outside boards on which a board lies. The fourth measure, EIGENVECTOR, captures

how connected a board is based on its direct contacts. It is measured by the eigenvector of the

8 We only provide a brief description of the four measures of connectedness in this section. For a more detailed

discussion on the constructions of these measures please refer to Larcker et al. (2013).

15

matrix formed by assigning 1(0) to its elements if a board is (not) directly connected to another

board.

3.3. Research Design

To test our main hypotheses, we estimate the following equations separately for the

underinvestment and overinvestment subsamples. This research design allows us to separately

examine whether connectedness affects both and is consistent with the prior literature (Chen et

al. 2011; Chen et al. 2013; Biddle et al. 2009).9

𝐼𝑁𝑉𝐸𝑆𝑇_𝐼𝑁𝐸𝐹𝐹𝑖,𝑡+1 = 𝛽0 + 𝛽1𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 + 𝛽2𝐶𝑂𝑁𝑇𝑅𝑂𝐿𝑖,𝑡 + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝑗 + 𝑌𝑒𝑎𝑟𝑡 + 𝜀𝑖,𝑡, (2)

where 𝐼𝑁𝑉𝐸𝑆𝑇_𝐼𝑁𝐸𝐹𝐹𝑖,𝑡+1 captures investment (in)efficiency, which is the absolute value of the

residuals from estimating the investment model as described in Section 3.2.1. 𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 is

director connectedness and is defined as one of the four measures – DEGREE, CLOSENESS,

BETWEENNESS, and EIGENVECTOR. We use either the continuous or decile ranking of the

connectedness measures.

𝐶𝑂𝑁𝑇𝑅𝑂𝐿𝑖,𝑡 represents a matrix of control variables which include various firm

characteristics that might confound the effect of director connectedness on investment efficiency.

Our control variables are largely consistent with those used in the prior literature (Biddle and

Hilary 2006; Biddle et al. 2009; Chen et al. 2013). To isolate the effect of director networks, we

control for other dimensions of firms’ information environment, including financial reporting

quality (FRQ) estimated based on the modified Dechow and Dichev (2002) model, the natural

logarithm of the number of financial analysts following the firm (ANALYST_FOL), and

managers’ private information (PRIVATE_INFO) as captured by absolute abnormal returns

around earnings announcements. We also include two firm characteristics, firm size (SIZE),

9 Biddle et al. (2009) adopt a multinomial logit regression design, where they classify firm-years into three groups –

underinvestment, efficient investment, and over investment based on the residuals from regressing investment on

sales growth. Our results hold if we take such approach.

16

measured as the natural logarithm of total assets, and market-to-book ratio (M/B), calculated as

the market value of total assets divided by the book value of total assets. Further, we control for

several corporate governance mechanisms, namely, the natural logarithm of institutional

ownership (IO), the size of the board (BOARD_SIZE), board independence (BOARD_IND), and

the average age of directors (BOARD_AGE). To capture the idea that firms in different stages of

their business cycles may have different board compositions and investment policies, we control

for firm age (AGE) measured as the natural logarithm of the number of years that a firm has been

covered by CRSP, the length of the operating cycle (OPCYCLE) calculated as the natural

logarithm of (receivables to sales plus inventory to cost of goods sold multiplied by 360), and the

incidence of loss (LOSS) which equals one if income before extraordinary items is negative and

zero otherwise.

As the long-term solvency of the firm affects investment choices, we control for firm

capital structure (KSTRUCTURE) defined as the long-term debt divided by the sum of long-term

debt and the market value of equity; financial slack (SLACK) measured as the ratio of cash and

cash equivalents to PP&E. To control for the effect of the uncertainty in firms’ operating

environment on investment decisions, we include cash flow volatility (CFOVOL), sales volatility

(SALESVOL), and investment volatility (INVESTVOL). Lastly, we follow prior studies and

control for asset tangibility (TANGIBILITY) measured as the ratio of PP&E and total assets,

dividend payout (DIVIDEND), which equals one if the firm paid a dividend and zero otherwise,

bankruptcy risk (Z_SCORE), cash flow from operations divided by sales (CFOSALE), industry

leverage (IND_K, the average KSTRUCTURE of firms in the same industry).

The Appendix provides a detailed description of the variables. All continuous variables

are winsorized each year at the bottom and top 1% level. We include industry fixed effects and

17

year fixed effects to control for unobserved industry factors and market-wide performance shifts

over the sample period, respectively. Standard errors are clustered by firm.10 We predict that 𝛽1

is negative for the underinvestment and the overinvestment group, respectively.

4. Empirical Results: Board Connections and Investment Efficiency

4.1. Descriptive Statistics

Table 1, Panel A reports the descriptive statistics on our main variables. In our final

sample of 29,383 firm-year observations, 19,632 firm-years are classified as the underinvestment

group and 9,751 firm-years fall into the overinvestment group. As can be seen in Table 1, while

there is a larger number of firms that underinvest, the average deviation from expected

investment level is higher for overinvesting firms (13.057) than underinvesting firms (7.865).

This pattern is consistent with what has been reported in prior studies (e.g., Biddle et al. 2009;

Chen et al. 2011). In terms of connectedness measures, the mean (median) DEGREE is 5.6 (4),

which suggests that on average our sample firms have five direct links with outside boards. 11

Turning to the control variables, the mean and median total assets are $667 and $615

million, respectively. Approximately 27% of firms experience losses during our sample period.

On average, our sample firms are followed by three analysts and have institutional ownership of

50%. In addition, the average firm holds 24.78% of tangible assets relative to total assets and has

a market leverage of 14%.

Table 1, Panel B reports correlations among our main variables separately for

underinvestment and overinvestment firm-years. For both groups, INVEST_INEFF is negatively

and significantly correlated with measures of board connectedness, lending support to our

conjecture that well-connected firms are less likely to engage in inefficient investment.

10 Our inferences remain qualitatively the same when we cluster standard errors by firm and year. 11 These figures are comparable to the mean (5.1) and median (3) DEGREE reported by Larcker et al (2013).

18

Moreover, within each group of firm-years, DEGREE, BETWEENNES, and CLOSENESS are

highly positively correlated with each other. The correlations of EIGENVECTOR with the other

three measures are all significantly positive albeit at smaller magnitudes.

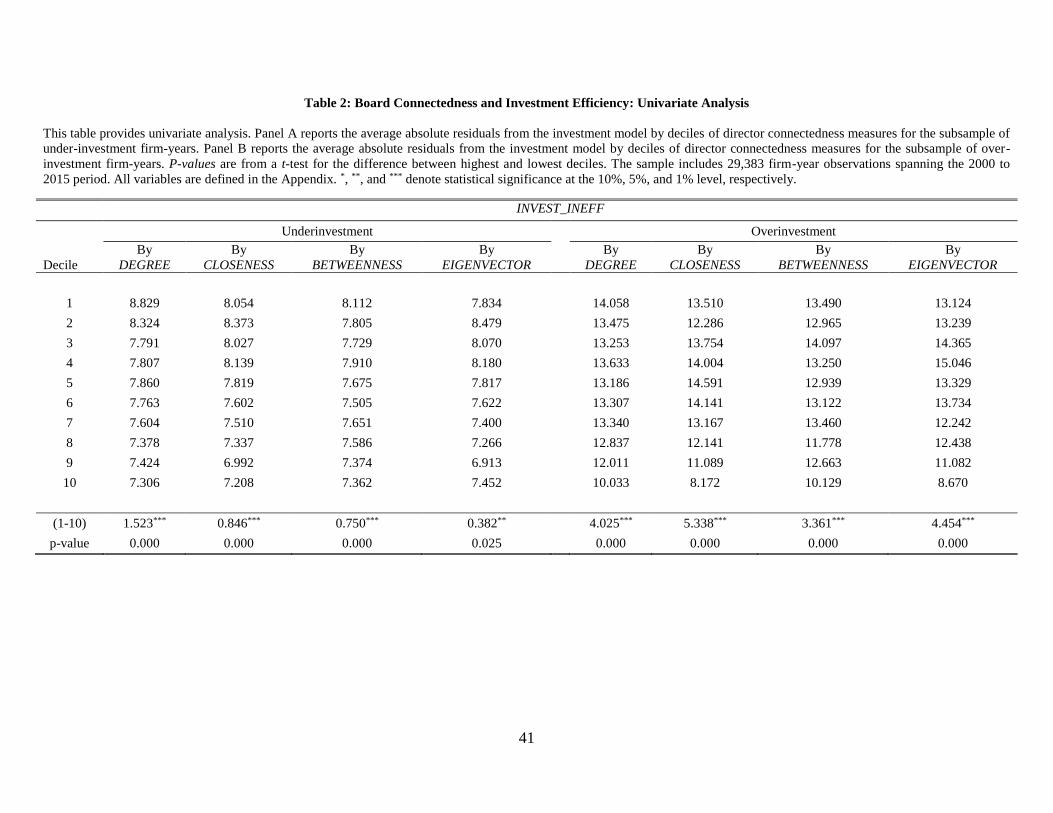

4.2. Univariate Results

We begin our analysis of the effect of board connectedness on firm investment efficiency

by conducting univariate analyses. We sort the four measures of board connectedness into

deciles by year and then calculate the average INVEST_INEFF for each decile of connectedness

measure. In order to understand whether board connectedness reduces investment inefficiency

due to both underinvestment and overinvestment, we perform this analysis separately within the

underinvestment and overinvestment subsamples.

Table 2 reports the results for the univariate tests. For the underinvestment group, we

observe a decline in INVEST_INEFF as board connectedness increases across all four

connectedness measures. For example, as DEGREE moves from the first to the tenth decile of its

distribution, INVEST_INEFF decreases from 8.829 to 7.306, reflecting a difference of 1.523,

which is significant at the 1% level. A similar pattern is present for the overinvestment group

(e.g., INVEST_INEFF declines from 14.058 to 10.033 as DEGREE changes from the first to the

tenth decile); however, the monotonic relation between investment efficiency and connectedness

measures is less clear. Taken together, the univariate results are consistent with board

connectedness mitigating both underinvestment and overinvestment, with the effect being

stronger for the underinvestment subsample.

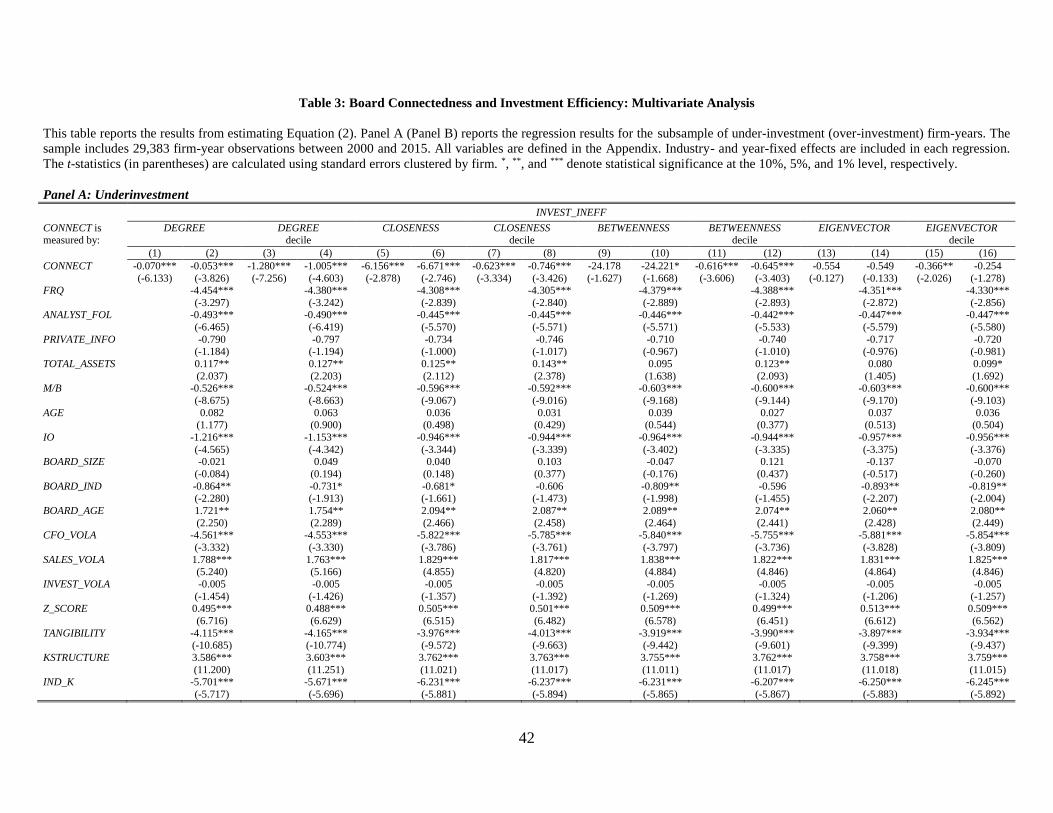

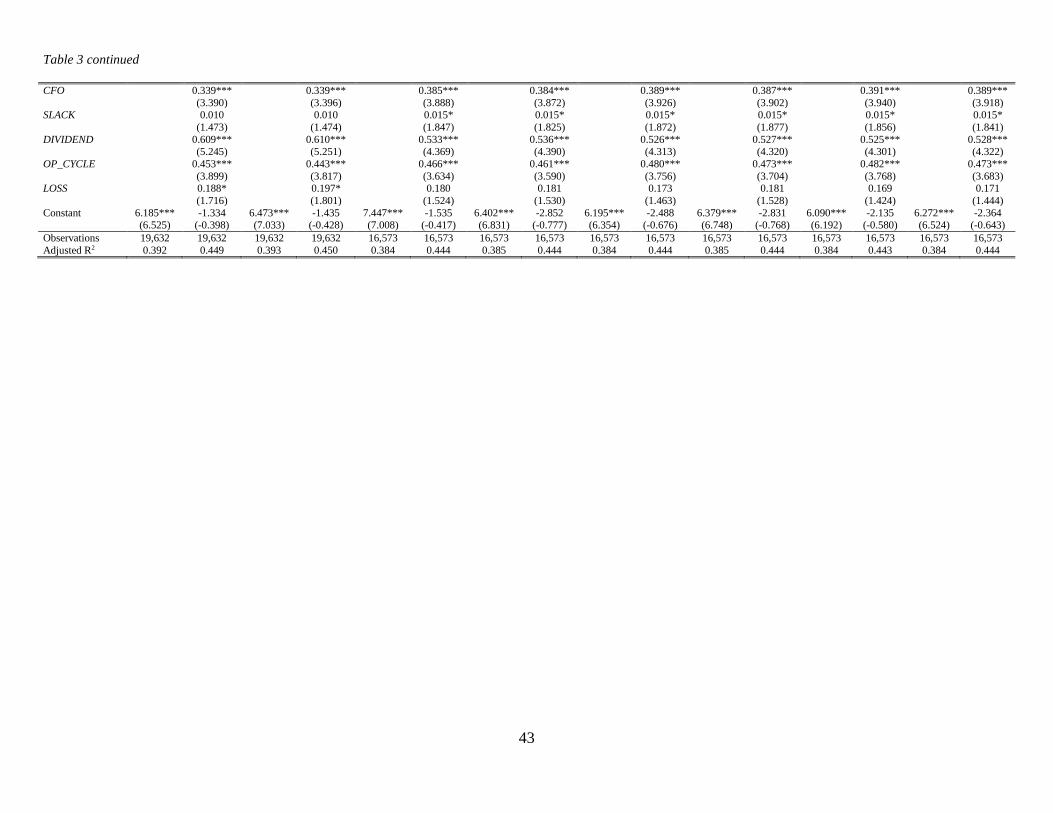

4.3 Multivariate Results

In this section, we employ a regression approach to test our main hypothesis that board

connectedness improves investment efficiency. Table 3 reports the results from estimating

19

Equation (2) using both continuous and decile-ranked connectedness measures. As shown in

Table 3, Panel A, in the majority of specifications, the coefficient estimates on the connectedness

measures are negative and statistically significant. For example, in Column (1), which includes

industry- and year-fixed effects but no other controls, the coefficient estimate on DEGREE is -

0.070 (p-value <0.01). When we add the vector of control variables in Column (2), the

coefficient estimate on DEGREE is -0.053 and significant at the 1% level. Results are consistent

when we use the decile ranked DEGREE. While we continue to find significant results for

CLOSENESS and BETWEENNESS, the results based on EIGENVECTOR are relatively weaker

as in the univariate results. These findings suggest that director connectedness mitigates

underinvestment, with the effect being stronger for more direct connections. Further, the results

are economically meaningful as well. For example, in Column (2), a one standard deviation

increase in DEGREE reduces INVEST_INEFF by 0.26, which represents a 3.3% decrease in

investment efficiency relative to the sample average of INVEST_INEFF. In Column (4), as

DEGREE moves from the bottom to the top decile, INVEST_INEFF decreases by 1.005, which

represents a 11.4% (1.005/8.829) reduction in underinvestment. Taken together, the results in

Panel A, Table 3 suggest that director connectedness is associated with more efficient investment

among firms that are in the underinvestment subsample.

Table 3, Panel B provides the results from estimating Equation (2) for observations in the

overinvestment subsample. Across the specifications in which only industry- and year-fixed

effects are included, the coefficient estimates on the four proxies of director connectedness are

negative and statistically significant. However, the effect becomes insignificant once the full set

of control variables are included. These results again mimic the findings from our univariate

analyses – the impact of director connectedness on investment efficiency is more pronounced on

20

the underinvestment side. However, in additional analyses we provide evidence on situations

where connectedness might play a more important role in reducing overinvestment.

5. Board Connectedness and Investment Efficiency: Cross-sectional Tests

Prior research shows that firms tend to underinvest mainly due to financial constraints

and overinvest due to mainly agency problems. In this section, we explore whether board

connectedness mitigates these inefficiencies by improving firms’ external information

environment. In 5.1, we focus on the underinvestment sample and examine how the effect of

board connectedness on investment efficiency varies with financial constraints, dependence on

external capital, and the availability/strength of other external sources of information that could

substitute for director networks. In 5.2, we consider firms in the overinvestment sample and

examine whether board connectedness mitigates investment inefficiencies emanating from

agency problems by increasing external monitors’ informedness and thereby enabling them to

become more effective monitors of managerial actions.

5.1. Underinvestment

5.1.1 The role of board connections in mitigating the effect of financial constraints on

underinvestment

Boardroom networks are important channels through which information is exchanged and

diffused (Schoorman et al. 1981; Haunschild and Beckman 1998; Larcker et al. 2013; Chuluun et

al. 2014). Well-connected directors who can leverage social relationships and increase the

visibility of firms’ positive NPV projects, could help bridge the information gap between the

firm and its capital providers. Hence, for otherwise similar firms, the information risk perceived

by lenders should be lower for well-connected firms. Accordingly, we expect financially

constrained firms and firms that are more dependent on external financing (as opposed to

21

internally generated cash) to benefit the most from a well-connected board in terms of accessing

capital and therefore the effect of board connectedness in reducing underinvestment should be

more pronounced among these firms.

To test these predictions, we modify Equation (2) by interacting our connectedness

measures with proxies of financial constraints and external capital needs and estimate the

following regressions using firm-years in the underinvestment subsample:

𝐼𝑁𝑉𝐸𝑆𝑇_𝐼𝑁𝐸𝐹𝐹𝑖,𝑡+1 = 𝛽0 + 𝛽1𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 + 𝛽2𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 ∗ 𝐹𝐼𝑁𝐶𝑂𝑁𝑆𝑇𝑅𝐴𝐼𝑁𝑇𝑆𝑖,𝑡

+𝛽3𝐹𝐼𝑁𝐶𝑂𝑁𝑆𝑇𝑅𝐴𝐼𝑁𝑇𝑆𝑖,𝑡 + 𝛽4𝐶𝑂𝑁𝑇𝑅𝑂𝐿𝑖,𝑡 + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝑗 + 𝑌𝑒𝑎𝑟𝑡 + 𝜀𝑖,𝑡, (3)

𝐼𝑁𝑉𝐸𝑆𝑇_𝐼𝑁𝐸𝐹𝐹𝑖,𝑡+1 = 𝛾0 + 𝛾1𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 + 𝛾2𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 ∗ 𝐹𝐼𝑁𝑁𝐸𝐸𝐷𝑖,𝑡

+𝛾3𝐹𝐼𝑁𝑁𝐸𝐸𝐷𝑖,𝑡 + 𝛾4𝐶𝑂𝑁𝑇𝑅𝑂𝐿𝑖,𝑡 + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝑗 + 𝑌𝑒𝑎𝑟𝑡 + 𝜀𝑖,𝑡, (4)

where 𝐹𝐼𝑁𝐶𝑂𝑁𝑆𝑇𝑅𝐴𝐼𝑁𝑇𝑆 measures the degree to which a firm is financially constrained and is

based on one of the following three measures: the Whited-Wu (WW) index (Whited and Wu,

2006), the size and age (SA) index (Hadlock and Pierce, 2010), and the absence of an S&P credit

rating (CRATING). The WW index and the SA index are robust predictors of the degree to which

a firm is financially constrained (Hadlock and Pierce, 2010), with larger values of both indices

indicating that the firm is more financially constrained. Extant literature offers motivations for

treating firms without a credit rating as financially constrained. Firms without a credit rating tend

to have difficulty accessing public debt markets (Faulkender and Petersen, 2006) and thus have

to rely on intermediaries such as banks with less competitive terms. Whited (1992) argues that

unrated firms are more opaque than rated firms, and hence more likely to be rationed by lenders

because the rating process helps reduce information asymmetries. Therefore, we create a dummy

variable, CRATING, which equals one if the firm does not have a credit rating (and is therefore

more financially constrained), and zero otherwise.

22

We use two measures to capture firms’ needs of external capital financing, FINNEED,

following Rajan and Zingales (1998). The first measure, EXTFIN, is based on the notion that the

amount of targeted investment that cannot be financed through internal cash flows will be

supported by external financing. EXTFIN is defined as the difference between the firm’s capital

expenditures and cash flow from operations scaled by capital expenditures. The second measure,

EQUITY, is equal to the difference between total sales and purchases of common and preferred

stock scaled by capital expenditures. Larger values of EQUITY imply higher demand for external

capital from the equity market. All other variables used in Equations (3) and (4) are defined in

the Appendix.

If board connectedness mitigates underinvestment by enhancing the board’s information

intermediary role and facilitating the firm’s access to external capital, then we expect negative

coefficients on CONNECT * FINCONSTRAINTS and CONNECT * FINNEED (i.e., 𝛽2 < 0 and

𝛾2 < 0). Table 4 presents the regression results. From Panel A, the coefficient on the interactions

of DEGREE and the three measures of financial constraints (WW, SA, and CRATING) are all

significantly negative. Similarly, in Panel B, the coefficients on the interactions of DEGREE

with both EXTFIN and EQUITY are negative and significant.12 These results provide strong

support to our conjecture that director networks enable firms to access external capital and

prevent underinvestment by helping bridge the information gap between the firm and external

capital providers and thus enhancing the board’s information intermediary role.

5.1.2 Board connections and the moderating effect of alternative external sources of information

To the extent that director connections represent alternative information sources to other

information channels, we expect firms to benefit more from director connections when other

12 Results are similar when we use BETWEENNESS, CLOSENESS, and EIGENVECTOR and are not tabulated for

brevity.

23

sources of information are less available or of lower quality. To test this conjecture, we conduct

cross-sectional analyses based on analyst coverage and financial information quality, which are

two alternative channels that can help reduce information asymmetry. In particular, analysts

convey valuable information that can help resolve information asymmetry between the firm and

its external providers of capital as well as among outsiders (Hong, Lim, and Stein 2000; Baker,

Nofsinger, and Weaver 2002; Frankel and Li 2004; Bowen, Chen, and Cheng 2008). Previous

studies document that financial reporting quality serves an important role in mitigating

information frictions that hamper investment efficiency (Biddle and Hilary 2006; Biddle et al.

2009; Chen et al. 2011). For firms with lower analyst coverage and lower quality of financial

reporting, information diffusion through directors would matter more in reducing information

asymmetry and increasing investment efficiency. We estimate the following equations using the

underinvestment firm-years:

𝐼𝑁𝑉𝐸𝑆𝑇_𝐼𝑁𝐸𝐹𝐹𝑖,𝑡+1 = 𝛽0 + 𝛽1𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 + 𝛽2𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 ∗ 𝐴𝑁𝐴𝐿𝑌𝑆𝑇_𝐹𝑂𝐿𝑖,𝑡

+𝛽3𝐴𝑁𝐴𝐿𝑌𝑆𝑇_𝐹𝑂𝐿𝑖,𝑡 + 𝛽4𝐶𝑂𝑁𝑇𝑅𝑂𝐿𝑖,𝑡 + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝑗 + 𝑌𝑒𝑎𝑟𝑡 + 𝜀𝑖,𝑡, (5)

𝐼𝑁𝑉𝐸𝑆𝑇_𝐼𝑁𝐸𝐹𝐹𝑖,𝑡+1 = 𝛾0 + 𝛾1𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 + 𝛾2𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 ∗ 𝐹𝑅𝑄𝑖,𝑡

+𝛾3𝐹𝑅𝑄𝑖,𝑡 + 𝛾4𝐶𝑂𝑁𝑇𝑅𝑂𝐿𝑖,𝑡 + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝑗 + 𝑌𝑒𝑎𝑟𝑡 + 𝜀𝑖,𝑡, (6)

where ANALYST_FOL is the natural logarithm of the number of analysts following the firm. We

follow the existing literature and measure FRQ by accruals quality as estimated via a modified

Dechow and Dichev (2002) model wherein working capital accruals is regressed on lagged,

current, and future cash flows plus the change in revenue and PP&E. All other variables are

defined previously. Appendix provides detailed variable definitions. We expect both 𝛽2 and 𝛾2 to

be negative if board network affects the tendency of under-investment through the information

channel.

24

Table 5 reports the results from estimating Equations (5) and (6). For both cross-sectional

tests conditional on analyst coverage and financial reporting quality, the coefficient estimates on

the interaction terms are negative and statistically significant, suggesting a greater influence of

connectedness on underinvestment when information asymmetry is high. Such findings provide

evidence that director networks allow boards to more effectively perform their information

intermediary roles, which reduces information asymmetries between firms and capital providers

and therefore mitigates underinvestment.

5.2 Overinvestment

The empirical evidence we have reported thus far provides strong support for the

hypothesis that board connectedness improves a firm’s external information environment. An

implication of this hypothesis is that for firms with well-connected boards, external stakeholders

should become more effective monitors of managerial actions as they become endowed with

higher quality information about the firm. In order to examine whether this is the case, in this

section we conduct two sets of cross-sectional tests using the overinvestment subsample.

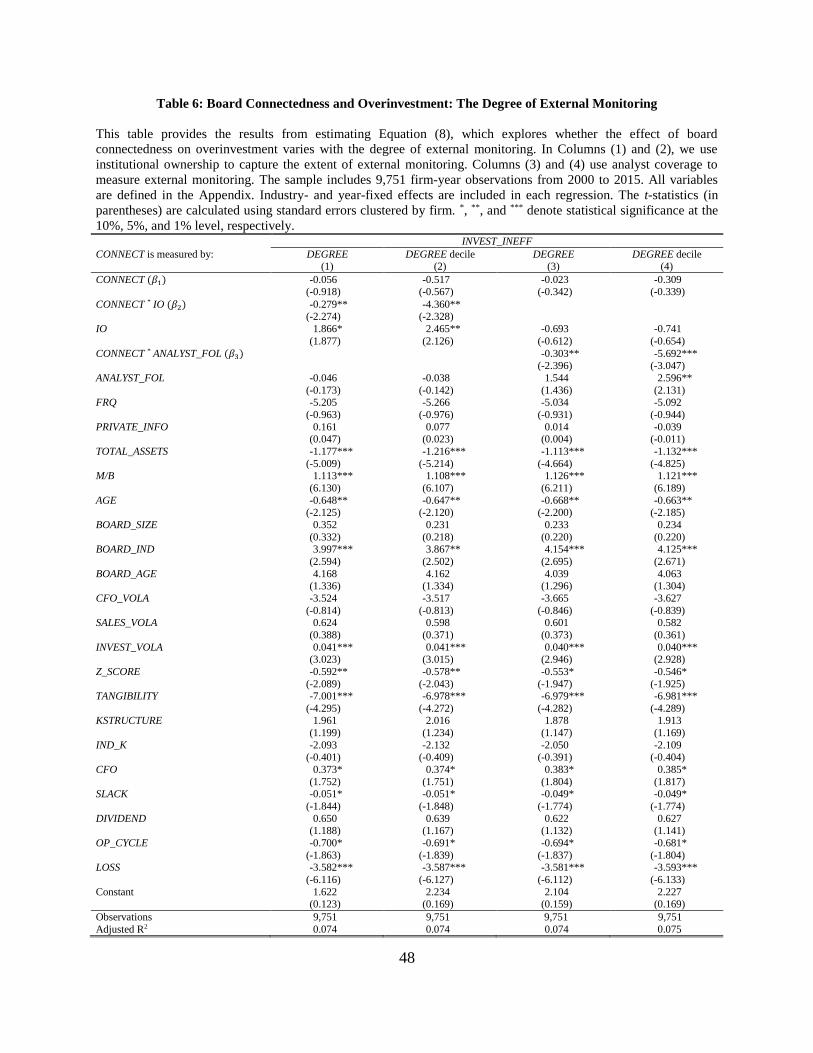

5.2.1 Board connections and the effectiveness of external monitors in mitigating overinvestment

In this subsection, we examine how the effect of board connectedness on the extent of

overinvestment varies with the monitoring pressure from external monitors via the following

panel regression:

𝐼𝑁𝑉𝐸𝑆𝑇_𝐼𝑁𝐸𝐹𝐹𝑖,𝑡+1 = 𝛽0 + 𝛽1𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 + 𝛽2𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 ∗ 𝐸𝑋𝑇𝑀𝑂𝑁𝐼𝑇𝑂𝑅𝑖,𝑡

+𝛽3𝐸𝑋𝑇𝑀𝑂𝑁𝐼𝑇𝑂𝑅𝑖,𝑡 + 𝛽4𝐶𝑂𝑁𝑇𝑅𝑂𝐿𝑖,𝑡 + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝑗 + 𝑌𝑒𝑎𝑟𝑡 + 𝜀𝑖,𝑡, (7)

where EXTMONITOR represents the degree of external monitoring. We use two proxies for the

strength of the external monitoring pressure: institutional ownership and the number of analysts

following the firm. Definitions for all other variables are provided in Appendix. If director

networks transmit information that is incrementally useful to institutional investors and analysts,

25

then board connectedness should have a more pronounced effect in reducing the extent of

overinvestment for firms with greater institutional ownership and analyst coverage. Put

differently, the relationship between INVEST_INEFF and CONNECT should become more

negative for larger values of EXTMONITOR (i.e., 𝛽2 < 0). In contrast, if board connectedness is

a substitute for other forms of external monitoring, then its effect in reducing overinvestment

should be muted for firms with greater external monitoring (i.e. 𝛽2 > 0).

Table 6 presents the results from estimating equation (7). The coefficient estimates on the

interaction of DEGREE and both measures of external monitoring are significantly negative in

all specifications, suggesting that well-connected firms with higher institutional ownership and

analyst coverage are less likely to overinvest. This result implies that the external information

effect of director networks improves the monitoring effectiveness of external stakeholders and

thereby curbs overinvestment from entrenched managers. It also indicates that the monitoring

from institutional shareholders and analysts complements the role of board connectedness.

5.2.2 The role of board connections in mitigating the effect of agency costs on overinvestment

In this section, we examine whether the effect of board connectedness on overinvestment

is stronger for firms that have higher agency costs. We consider firms’ agency costs arising from

cash holdings and overvalued equity. Our use of cash holdings is motivated by Jensen (1986),

who suggests that free cash flow exacerbates agency problems by providing managers with the

capital to undertake inefficient investments. Hence, firms with relatively large amounts of cash

and liquid securities tend to have higher agency costs. 13 In addition to cash holdings, we also

consider agency costs of overvalued equity, which is grounded on the idea that overvalued firms

13 Consistent with this theory, Blanchard, Lopez-di-Silanes, and Vishny (1994) document excessive investment and

acquisition activity for eleven firms that experience a large cash windfall following a legal settlement. Harford

(1999) finds that cash-rich firms are more likely to make acquisitions that later experience abnormal deterioration in

operating performance. Bates (2005) finds that firms who retain cash from subsidiary sales tend to invest more

relative to industry peers.

26

are associated with more severe agency problems and have higher likelihood of overinvesting.

Jensen (2005) argues that when a firm’s equity becomes substantially overvalued it sets in

motion a set of organizational forces that might lead to value-destroying investments. 14

We estimate the following regression within the overinvestment subsample:

𝐼𝑁𝑉𝐸𝑆𝑇_𝐼𝑁𝐸𝐹𝐹𝑖,𝑡+1 = 𝛽0 + 𝛽1𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 + 𝛽2𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 ∗ 𝐴𝐺𝐸𝑁𝐶𝑌𝐶𝑂𝑆𝑇𝑖,𝑡

+𝛽3𝐴𝐺𝐸𝑁𝐶𝑌𝐶𝑂𝑆𝑇𝑖,𝑡 + 𝛽4𝐶𝑂𝑁𝑇𝑅𝑂𝐿𝑖,𝑡 + 𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝑗 + 𝑌𝑒𝑎𝑟𝑡 + 𝜀𝑖,𝑡, (8)

where AGENCYCOST is measured as either cash holdings (CASHHOLD) or the degree of stock

overvaluation (OVERVALUATION). CASHHOLD is calculated as the ratio of cash and cash

equivalents to sales and OVERVALUATION is the natural logarithm of the ratio of the observed

market value of equity to the intrinsic value of equity constructed as in Fu et al. (2013).15

Because industry is a significant factor in determining firm-level cash holdings, we adjust cash

holdings by industry median. Both CASHHOLD and OVERRVALUATION are decile ranked and

normalized to the range of [0,1]. Definitions for all other variables are provided in the Appendix.

Table 7 presents the regression results. In all specifications, the coefficient estimates on

the interaction of DEGREE and measures of agency costs are negative and significant, indicating

that director connectedness is associated with less overinvestment for firms with higher agency

costs. More importantly, the sum of the coefficient on DEGREE and that on DEGREE *

AGENCYCOST is negative and statistically significant in all regressions, which suggests that

board networks effectively help mitigate overinvestment for firms that experience relatively

serious agency problems. Such results are consistent with boardroom connections enhancing

14 Consistent with this argument, Moeller, Schlingemann, and Stulz (2005) find that acquiring firms in large loss

deals have significantly higher market-to-book ratios than acquirers in other deals. Moreover, Fu, Lin, and Officer

(2013) show that overvalued acquirers overpay for their targets and such acquisitions are concentrated among

acquirers with governance problems. 15 Please refer to Appendix of Fu et al. (2013) for details on how this measure is constructed.

27

boards’ monitoring role, thereby curbing overinvestment arising from management

entrenchment.

6. Additional Analyses and Robustness Tests

In this section, we conduct several additional analyses to provide more insights into the

effects of director connectedness on investment efficiency and assess the robustness of our

results to alternative explanations, specifications, and variable measurements.

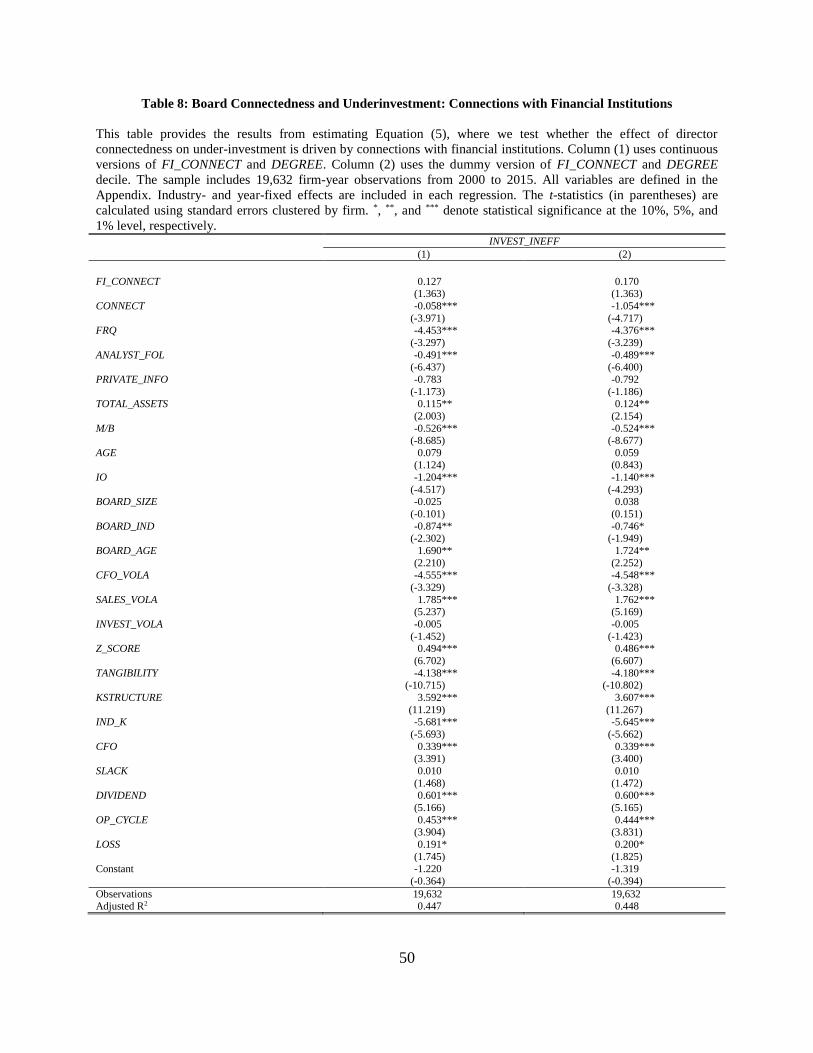

6.1. Director Connections with Financial Institutions and Underinvestment

To the extent that firms’ directors have connections with board members at financial

institutions such as banks, such links might enable firms to have easier access to capital and, in

turn, have lower likelihood of underinvestment. To test this conjecture, we estimate the

following regression:

𝐼𝑁𝑉𝐸𝑆𝑇_𝐼𝑁𝐸𝐹𝐹𝑖,𝑡+1 = 𝛽0 + 𝛽1𝐹𝐼_𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 + 𝛽2𝐶𝑂𝑁𝑁𝐸𝐶𝑇𝑖,𝑡 + 𝛽3𝐶𝑂𝑁𝑇𝑅𝑂𝐿𝑖,𝑡

+𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦𝑗 + 𝑌𝑒𝑎𝑟𝑡 + 𝜀𝑖,𝑡, (9)

where 𝐹𝐼_𝐶𝑂𝑁𝑁𝐸𝐶𝑇 is either the number of first-degree links to boards of financial institutions

(SIC code 6000-6999) or a dummy variable that equals one if the firm has at least one link to

boards of financial institutions and zero otherwise. All other variables are as previously defined.

We predict 𝛽1 < 0 if connections to financial institutions play a role in reducing

underinvestment.

Table 8 reports the results from estimating Equation (9). For brevity, we only report

results based on DEGREE. For both the continuous and decile ranked DEGREE, the coefficient

on FI_CONNECT is insignificant, while that on DEGREE remains negative and significant.

Thus, we fail to find any evidence that suggests that the effect of connectedness on

underinvestment is due to director connections with board members at financial institutions.

28

6.2. Robustness Tests

6.2.1 Endogeneity

Our finding of a positive relationship between board connectedness and firm investment

efficiency may suffer from potential endogeneity issues that could make our causal inferences

based on that relationship problematic. First, it is possible that the relationship between board

connectedness and investment efficiency is spurious as it might arise due to an omitted or

unobservable firm characteristic that drives both investment efficiency and board connectedness.

For example, more prestigious firms or firms with higher-quality managers may make more

efficient investment decisions, and at the same time attract more connected directors to serve on

their boards. Second, it is possible that our results suffer from a reverse-causality (i.e., firms that

make more efficient investment decisions recruit more connected directors to benefit from these

directors’ access to information and resources). While it is not clear in what direction the

correlated omitted variables problem will bias the effect we document, the reverse-causality

likely results in the same relationship between board connectedness and investment efficiency

upon which we base our causal inferences. We employ various approaches to gauge the

robustness of our causal inference to these two sources of endogeneity.

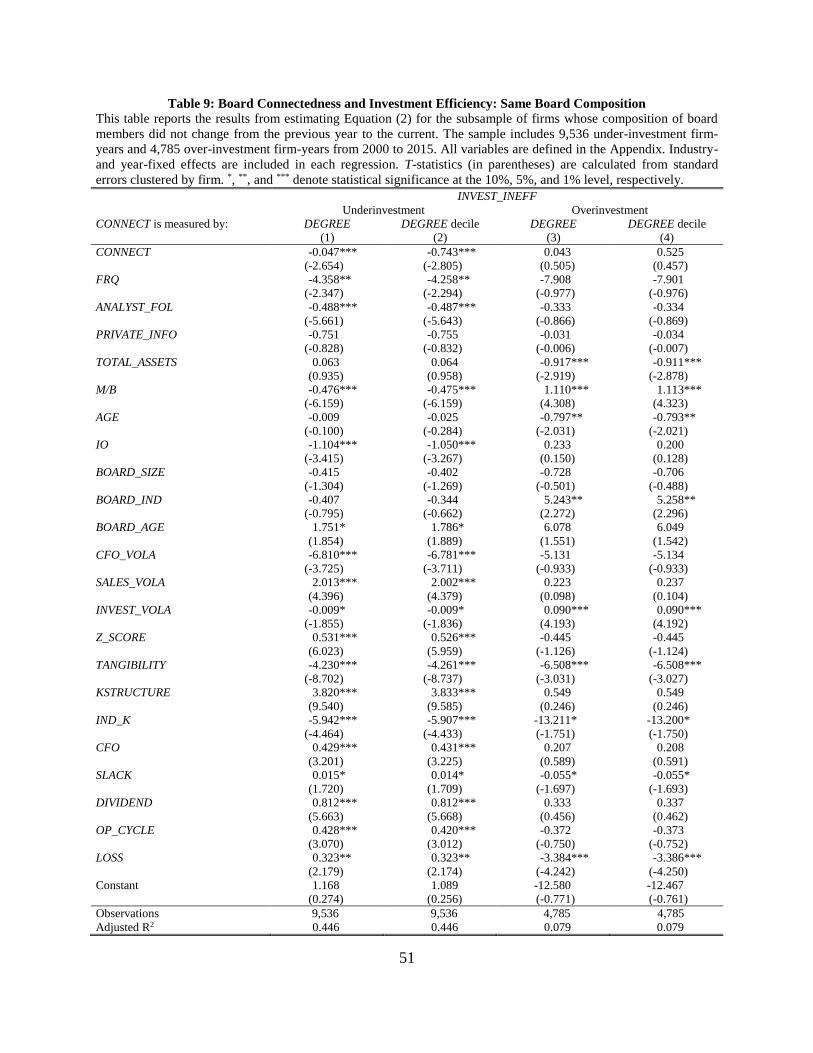

First, we restrict our sample to firms whose board compositions remain unchanged from

the prior year to the current year. That is, the board is composed of the same group of directors in

years t-1 and t.16 This exercise is based on the idea that changes in board centrality for such firms

must be due to changes in the boards of other companies in the network or from their board

members taking additional directorships at other firms. Hence, for this subset of firms, board-

16 This approach has been used by Larcker et al. (2013) in assessing the strength of their causal inference based on

the positive relation between board connectedness and future firm performance. It has also been used by Schabus

(2018) who examines the relationship between board connectedness and the accuracy of managers’ forecasts of

earnings, sales, and expenditures.

29

related endogenous choices made by a firm are less likely to affect its board centrality; rather, it

is the decisions of other firms that are exogenous in nature that drive the change in the focal

firm’s board centrality. The results from this analysis are reported in Table 9. The sample size

drops significantly as a result of holding the board composition constant from the prior year to

the current year; however, in our baseline regressions we continue to find a significantly negative

association between investment inefficiency and degree centrality. This negative association

continues to hold when we control for other firm characteristics for the underinvestment

subsample and remain insignificant on average in the overinvestment subsample. Second, we

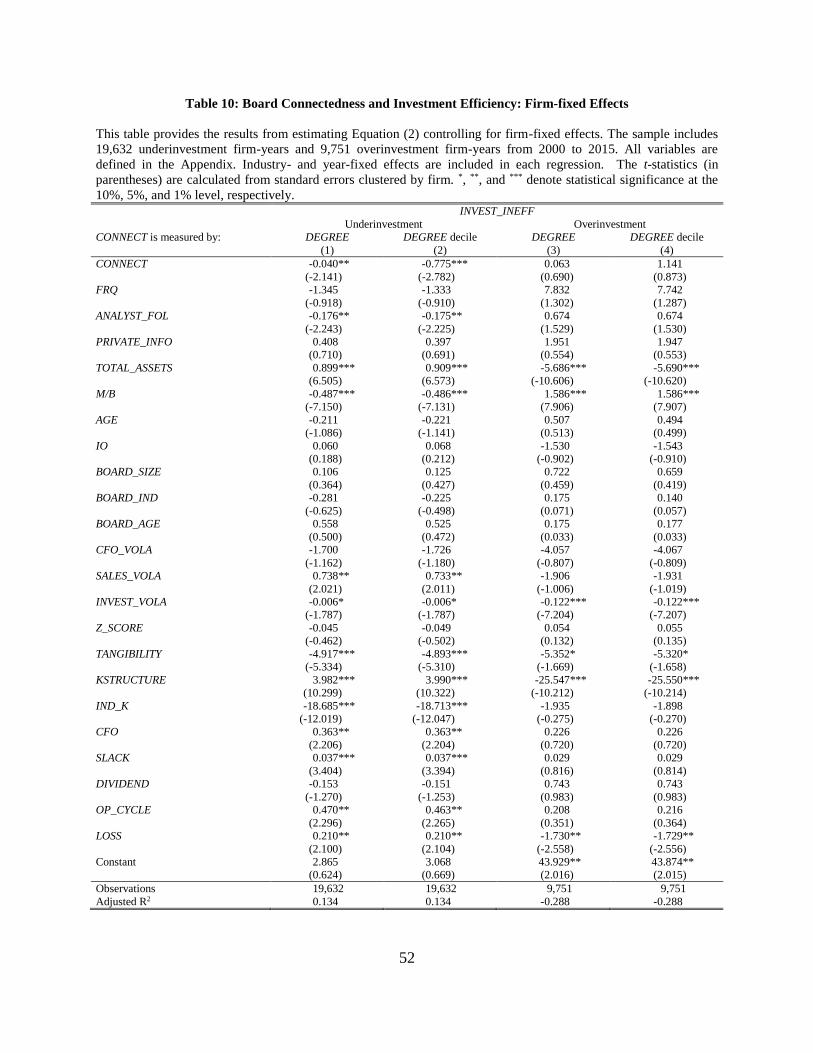

include firm fixed effects to control for time-invariant firm-specific unobservable or omitted

factors. The results, reported in Table 10, are similar to those in Table 2 and our inference

remains the same. Third, in untabulated analyses we control for various measures of managerial

quality such as management forecast accuracy and the ratio of insider stock transactions to total

transactions. Our inferences remain qualitatively the same. Finally, as in Larcker et al. (2013), in

untabulated tests, we examine the relationship between board connectedness in a given year and

lagged changes in investment efficiency and find no evidence in support of the argument that

firms with higher prior investment efficiency attract more connected directors to their boards.

Collectively, the results in this section help mitigate endogeneity concerns and corroborate our

causal inference based on the relationship between board connectedness and investment

efficiency.

6.2.2 Other Robustness Tests

We perform a battery of additional analyses (untabulated) to test the robustness of our

results. First, we measure investment as capital expenditure scaled by total assets, capital

expenditure scaled by plant, property, and equipment (PP&E) or capital expenditure plus R&D

30

expenditure scaled by total assets. Our results hold using these alternative measures of

investment. Second, we employ modified versions of the investment model. Specifically, we

follow Chen et al. (2011) and allow differential effects of positive and negative sales growth on

investment by adding a negative sales growth dummy and its interaction with sales growth. In

addition, following Chen et al. (2013), we include Tobin’s Q in the investment model. Our

inferences remain unaffected if we use the above two specifications. Third, we follow Biddle et

al. (2009) and adopt a multinomial logit regression design, where we classify firm-years into

three groups – under-investment, efficient investment, and over-investment based on the

residuals from regressing investment on sales growth. Our results hold if we take such approach.

7. Conclusion

Corporate directors possess valuable firm-, industry-, and market-related information that

they share with other corporate officers via social networks. A large stream of literature has

examined whether the information that flows through director networks impacts a firm’s

corporate decisions by affecting its internal information environment. However, recent studies

show that firm-specific information is likely to leak to outsiders such as short sellers, option

traders, and securities analysts when the firm’s board is more connected (Cohen et al., 2010;

Akbas et al., 2016). In this paper, we examine whether this outflow of information affects a

firm’s external information environment, and, consequently, the quality of its corporate decisions

by focusing on the effect of boardroom connections on corporate investment efficiency.

Using a panel of U.S. firms over the period 2000-2015, we separately analyze the

mechanisms through which board connectedness affects investment efficiency for firms that

under- and overinvest. For the underinvestment sample, we find the extent of underinvestment is

significantly lower when the board is more connected, controlling for various factors previously

31

shown to affect investment efficiency, including a firm’s information environment (e.g.,

financial reporting quality, analyst coverage, and manager’s information quality). This effect is

stronger for financially constrained firms and for firms with greater demand for external equity

financing, consistent with boardroom connections improving a firm’s external information

environment. We further find that the effect of board connectedness on underinvestment is less

pronounced for firms with higher financial reporting quality and more analyst following, which

suggests that director networks serve as a substitute for other external information mechanisms.

For the overinvestment subsample, we find that well-connected firms with higher

institutional ownership and analyst coverage are less likely to overinvest, suggesting that the

external information effect of director networks facilitates the monitoring effectiveness of

external stakeholders in curbing overinvestment from entrenched managers. Moreover, well-

connected firms with higher excess cash holdings or overvalued equity are less likely to

overinvest compared to their less-connected counterparts, consistent with boardroom connections

facilitating the flow of information to external monitors, which helps mitigate overinvestment

arising from agency problems.

Taken together, our results suggest that boardroom networks formed by shared board

directors can have a significant effect on firms’ external information environment and, in turn, on

the quality of managerial decisions by enabling external stakeholders to become better-informed

and more effective monitors. Our findings thus uncover a new channel through which director

networks can have real effects and increase firm value.

32

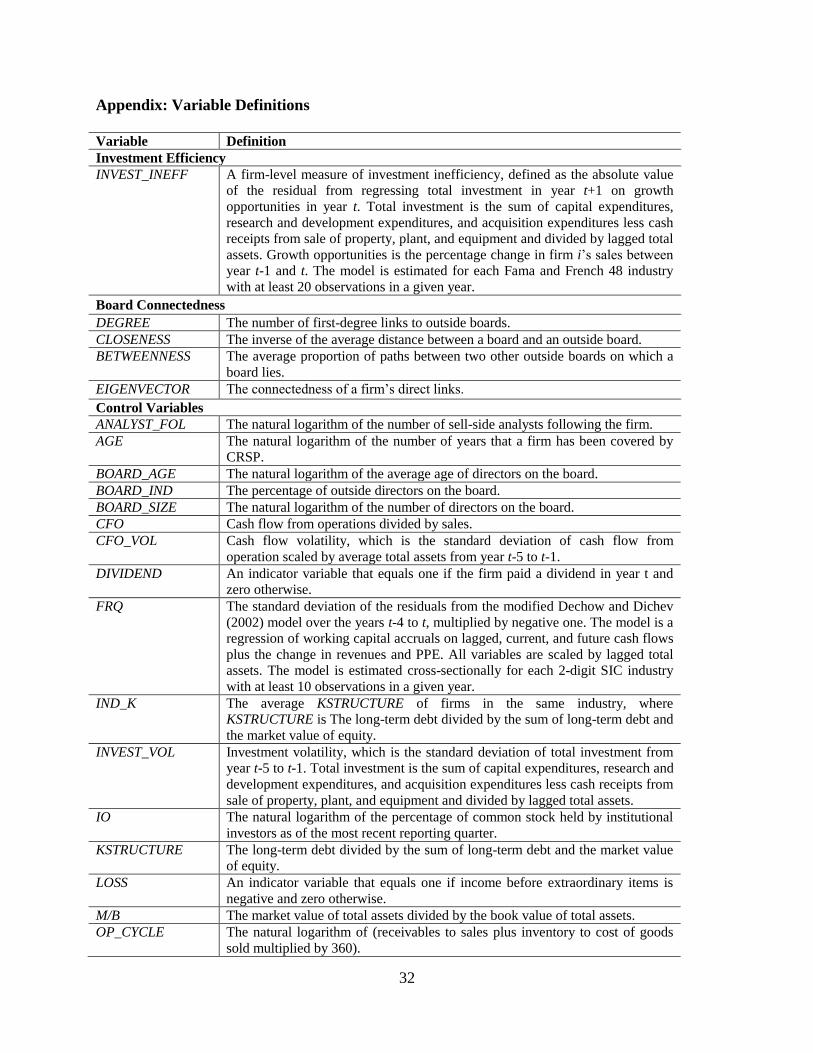

Appendix: Variable Definitions

Variable Definition

Investment Efficiency

INVEST_INEFF A firm-level measure of investment inefficiency, defined as the absolute value

of the residual from regressing total investment in year t+1 on growth

opportunities in year t. Total investment is the sum of capital expenditures,

research and development expenditures, and acquisition expenditures less cash

receipts from sale of property, plant, and equipment and divided by lagged total

assets. Growth opportunities is the percentage change in firm i’s sales between

year t-1 and t. The model is estimated for each Fama and French 48 industry

with at least 20 observations in a given year.

Board Connectedness

DEGREE The number of first-degree links to outside boards.

CLOSENESS The inverse of the average distance between a board and an outside board.

BETWEENNESS The average proportion of paths between two other outside boards on which a

board lies.

EIGENVECTOR The connectedness of a firm’s direct links.

Control Variables

ANALYST_FOL The natural logarithm of the number of sell-side analysts following the firm.

AGE The natural logarithm of the number of years that a firm has been covered by

CRSP.

BOARD_AGE The natural logarithm of the average age of directors on the board.

BOARD_IND The percentage of outside directors on the board.

BOARD_SIZE The natural logarithm of the number of directors on the board.

CFO Cash flow from operations divided by sales.

CFO_VOL Cash flow volatility, which is the standard deviation of cash flow from

operation scaled by average total assets from year t-5 to t-1.

DIVIDEND An indicator variable that equals one if the firm paid a dividend in year t and

zero otherwise.

FRQ The standard deviation of the residuals from the modified Dechow and Dichev

(2002) model over the years t-4 to t, multiplied by negative one. The model is a

regression of working capital accruals on lagged, current, and future cash flows

plus the change in revenues and PPE. All variables are scaled by lagged total

assets. The model is estimated cross-sectionally for each 2-digit SIC industry

with at least 10 observations in a given year.

IND_K The average KSTRUCTURE of firms in the same industry, where

KSTRUCTURE is The long-term debt divided by the sum of long-term debt and

the market value of equity.

INVEST_VOL Investment volatility, which is the standard deviation of total investment from

year t-5 to t-1. Total investment is the sum of capital expenditures, research and

development expenditures, and acquisition expenditures less cash receipts from

sale of property, plant, and equipment and divided by lagged total assets.

IO The natural logarithm of the percentage of common stock held by institutional

investors as of the most recent reporting quarter.

KSTRUCTURE The long-term debt divided by the sum of long-term debt and the market value

of equity.

LOSS An indicator variable that equals one if income before extraordinary items is

negative and zero otherwise.

M/B The market value of total assets divided by the book value of total assets.

OP_CYCLE The natural logarithm of (receivables to sales plus inventory to cost of goods

sold multiplied by 360).

33

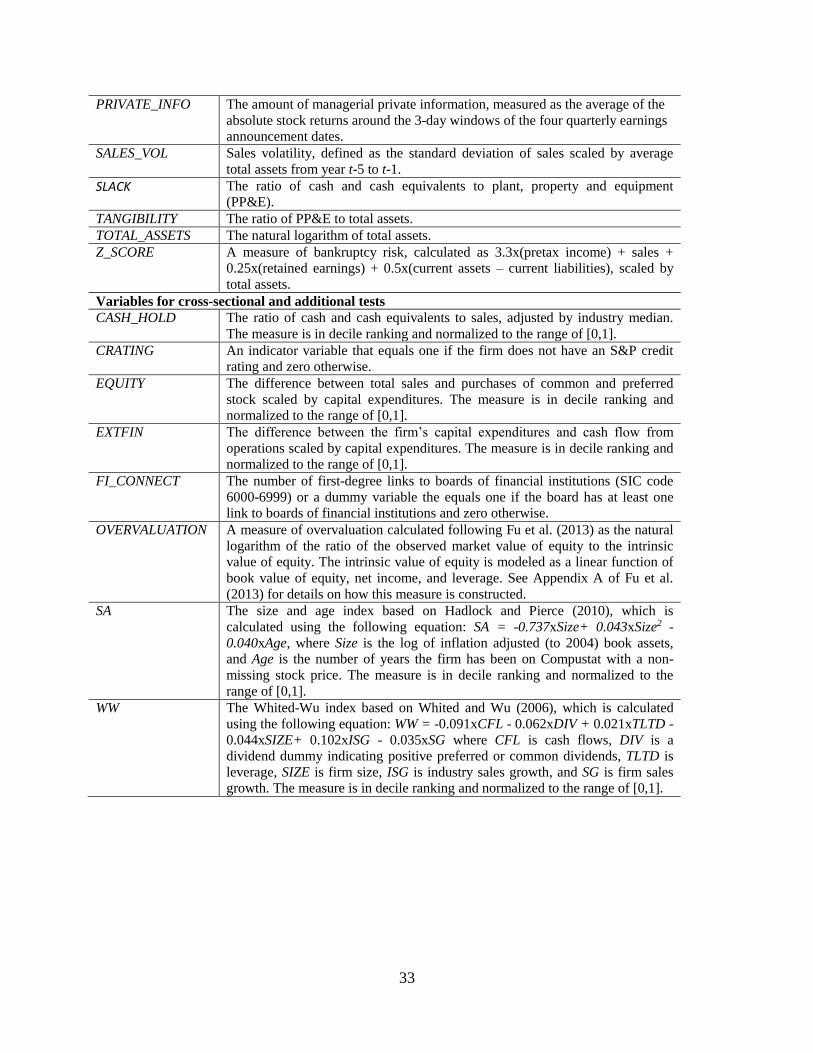

PRIVATE_INFO The amount of managerial private information, measured as the average of the

absolute stock returns around the 3-day windows of the four quarterly earnings

announcement dates.

SALES_VOL Sales volatility, defined as the standard deviation of sales scaled by average

total assets from year t-5 to t-1.

SLACK The ratio of cash and cash equivalents to plant, property and equipment

(PP&E). TANGIBILITY The ratio of PP&E to total assets.

TOTAL_ASSETS The natural logarithm of total assets.

Z_SCORE A measure of bankruptcy risk, calculated as 3.3x(pretax income) + sales +

0.25x(retained earnings) + 0.5x(current assets – current liabilities), scaled by

total assets.

Variables for cross-sectional and additional tests

CASH_HOLD The ratio of cash and cash equivalents to sales, adjusted by industry median.

The measure is in decile ranking and normalized to the range of [0,1].

CRATING An indicator variable that equals one if the firm does not have an S&P credit

rating and zero otherwise.

EQUITY The difference between total sales and purchases of common and preferred

stock scaled by capital expenditures. The measure is in decile ranking and

normalized to the range of [0,1].

EXTFIN The difference between the firm’s capital expenditures and cash flow from

operations scaled by capital expenditures. The measure is in decile ranking and

normalized to the range of [0,1].

FI_CONNECT The number of first-degree links to boards of financial institutions (SIC code

6000-6999) or a dummy variable the equals one if the board has at least one

link to boards of financial institutions and zero otherwise.

OVERVALUATION A measure of overvaluation calculated following Fu et al. (2013) as the natural

logarithm of the ratio of the observed market value of equity to the intrinsic

value of equity. The intrinsic value of equity is modeled as a linear function of

book value of equity, net income, and leverage. See Appendix A of Fu et al.

(2013) for details on how this measure is constructed.

SA The size and age index based on Hadlock and Pierce (2010), which is

calculated using the following equation: SA = -0.737xSize+ 0.043xSize2 -

0.040xAge, where Size is the log of inflation adjusted (to 2004) book assets,

and Age is the number of years the firm has been on Compustat with a non-

missing stock price. The measure is in decile ranking and normalized to the

range of [0,1].

WW The Whited-Wu index based on Whited and Wu (2006), which is calculated

using the following equation: WW = -0.091xCFL - 0.062xDIV + 0.021xTLTD -

0.044xSIZE+ 0.102xISG - 0.035xSG where CFL is cash flows, DIV is a

dividend dummy indicating positive preferred or common dividends, TLTD is

leverage, SIZE is firm size, ISG is industry sales growth, and SG is firm sales

growth. The measure is in decile ranking and normalized to the range of [0,1].

34

References

Akbas, Ferhat, Felix Meschke, and M. Babajide Wintoki. 2016. “Director Networks and

Informed Traders.” Journal of Accounting and Economics 62:1–23.

Armstrong, Christopher S. and David F. Larcker. 2009. “Discussion of ‘“The Impact of the

Options Backdating Scandal on Shareholders”’ and “Taxes and the Backdating of Stock

Option Exercise Dates.” Journal of Accounting and Economics 47:50–58.

Bae, Gil Soo, Dan S. Dhaliwal, and Phillip T. Lamoreaux. 2017. “Auditors and Client

Investment Efficiency.” The Accounting Review 92(2):19–40.

Bajo, Emanuele, Thomas J. Chemmanur, Karen Simonyan, and Hassan Tehranian. 2016.

“Underwriter Networks, Investor Attention, and Initial Public Offerings.” Journal of

Financial Economics 000:1–33.

Baker, H. Kent, John R. Nofsinger, and Daniel G. Weaver. 2002. “International Cross-Listing

and Visibility.” The Journal of Financial and Quantitative Analysis 37(3):495–521.

Barnea, Amir and Ilan Guedj. 2009. “Director Networks.” Working Paper.

Barzuza, Michal and Quinn Curtis. 2015. “Board Interlocks and Corporate Governance.”

Delaware Journal of Corporate Law 39:669–702.

Bates, Thomas W. 2005. “Asset Sales, Investment Opportunities, and the Use of Proceeds.” The

Journal of Finance 60(1):105–35.

Beckman, Christine M., and Pamela R. Haunschild. 2002. "Network Learning: The Effects of

Partners' Heterogeneity of Experience on Corporate Acquisitions." Administrative Science

Quarterly 47(1): 92-124.

Benson, Bradley W., Subramanian Rama Iyer, Kristopher J. Kemper, and Jing Zhao. 2016.

“Director Networks and Credit Ratings.” Working Paper.

Biddle, Gary C. and Gilles Hilary. 2006. “Accounting Quality and Firm-Level Capital

Investment.” The Accounting Review 81(5):963–82.

Biddle, Gary C., Gilles Hilary, and Rodrigo S. Verdi. 2009. “How Does Financial Reporting

Quality Relate to Investment Efficiency?” Journal of Accounting and Economics 48:112–

31.

Bizjak, J., M. Lemmon, and R. Whitby. 2009. “Option Backdating and Board Interlocks.”

Review of Financial Studies 22(11):4821–47.

Black, F., 1976. "Studies of stock price volatility changes." Proceedings of the 1976 Meetings of

the American Statistical Association, Business and Economic Statistics Section.

35

Blanchard, Olivier Jean, Florencio Lopez-de-Silanes, and Andrei Shleifer. 1994. “What Do

Firms Do with Cash Windfalls?” Journal of Financial Economics 36:337–60.

Bouwman, C. H. S. 2011. “Corporate Governance Propagation through Overlapping Directors.”

Review of Financial Studies 24(7):2358–94.

Bowen, Robert M., Xia Chen, and Qiang Cheng. 2008. “Analyst Coverage and the Cost of

Raising Equity Capital: Evidence from Underpricing of Seasoned Equity Offerings.”

Contemporary Accounting Research 25(3):657–99.

Brennan, Michael J. 2003. "Corporate Investment Policy." In Handbook of the Economics of

Finance, vol. 1: 167-214. Elsevier.

Brown, Jennifer L. and Katharine D. Drake. 2013. “Network Ties Among Low-Tax Firms.” The

Accounting Review 89(2):483–510.

Cai, Ye and Merih Sevilir. 2012. “Board Connections and M&A Transactions.” Journal of

Financial Economics 103(2):327–49.