dividend decision indiabulls financial services ltd 2011

DESCRIPTION

a project on dividend decisionsTRANSCRIPT

CHAPTER-I

- 1 -

INTRODUCTION

DIVIDEND

Dividends are payments made by a corporation to its shareholder members. It

is the portion of corporate profits paid out to stockholders. When a corporation earns

a profit or surplus, that money can be put to two uses: it can either be re-invested in

the business (called retained earnings), or it can be distributed to shareholders. There

are two ways to distribute cash to shareholders: share repurchases or dividends. Many

corporations retain a portion of their earnings and pay the remainder as a dividend.

Corporate profits (net income) are either retained by

the corporation as retained earnings or paid out to shareholders in the form of

dividends. Growing companies typically do not pay dividends, but instead prefer to

retain their earnings for growth. Older, more established companies retain a portion of

net income for growth and pay out the rest as dividends. Some companies, like

General Electric, have paid dividends to shareholders without fail every quarter for

many years.

The term Dividend refers to that part of the profits of a company which is

distributed amongst its shareholders. It may therefore be defined as the return that a

shareholder gets from the company, out of its profits, on his share holdings.

“According to the Institute of Charted Accounts of India” dividend is a

“Distribution to shareholder out of profits or reserves available for this purpose”

DIVIDEND POLICY

A dividend policy is the company's stance on how it will

dispense its earnings. It will include in its description the amount paid to shareholders

(if any) or if the company will retain the profits. It will also outline when the

dividends will be paid out, how much, and how frequent. The profit, which is any

- 2 -

positive gain, from any investment, or business venture, will be either dispersed to

investors or shareholders, or it may be re-invested back into the company.

The Dividend policy will explain exactly if the profit earnings will go the

shareholders in full, or a portion may be obtained by the company for re-investment.

The Dividend policy has the effect of dividing its net earnings into two

Parts: Retained earnings and dividends. The retained earnings provide funds two

finance the long-term growth. It is the most significant source of financing a firm’s

investment in practice. A firm, which intends to pay dividends and also needs funds to

finance its investment opportunities, will have to use external sources of finance.

Dividend policy of the firm thus has its effect on both the long-term financing and the

wealth of shareholders. The moderate view, which asserts that because of the

information value of dividends, some dividends should be paid as it may have

favorable affect on the value of the share.

The theory of empirical evidence about the dividend policy does not matter if

we assume a real world with perfect capital markets and no taxes. The second theory

of dividend policy is that there will definitely be low and high payout clients because

of the differential personal taxes. The majority of the holders of this view also show

that balance, there will be preponderous low payout clients because of low capital

gain taxes. The third view argues that there does exist an optimum dividend policy.

An optimum dividend policy is justified in terms of the information in agency costs.

- 3 -

OBJECTIVE OF THE STUDY

The basic objective of this study is as follows:

1. To understand the importance of the dividend decision and their impact on the

firm’s capital budgeting decision.

2. To know the various dividend policies followed by the firm.

3. To understand the theoretical backdrop of the various divided theories.

4. To compare the various theories of dividend with reference to their

assumptions and conclusions.

5. To know whether the dividend decisions have an impact on the market value

of the firm’s equity.

6. To see the various dividend policies of the INDIABULLS.

7. To derive the empirical evidence for the relevance theories of dividends

WALTER’S MODEL AND GORDON’S MODEL

- 4 -

IMPORTANCE OF THE STUDY

The dividend policy of a firm determines what proportion of earnings is

paid to shareholders by the way of dividends and what proportion is ploughed

back in the firm for reinvestment purposes.

If a firm‘s capital budgeting decision is independent of its dividend of its

dividend policy, a higher dividend payment will entail a greater dependence

on external financing.

On the other hand, if a firm’ s capital budgeting decision is dependent on

its dividend decision, a higher payment will cause shrinkage of its capital

budget and vice versa. In such a case the dividend policy has a bearing on the

capital budgeting decision.

Any firm, whether a profit making or non-profit organization has to take

certain capital budgeting decision.

The importance and subsequent indispensability of the capital budgeting

decision has led to the importance of the dividend decisions for the firms.

- 5 -

NEED FOR THE STUDY

The principal objective of corporate financial management is to maximize

the market value of the equity shares. Hence the key question of interest to us

in this study is, “What is the relationship between dividend policy and market

price of equity shares?”

Most of the discussion on dividend of dividend policy and firm value

assumes that the investment decision of a firm is independent of its dividend

decision.

The need for this study arise from the above raised question and the most

controversial and unresolved doubts about the relevance of irrelevance of the

dividend policy.

- 6 -

RESEARCH METHODOLOGY

Every project requires genuine research. Successes of any project and getting genuine

results from that, depends upon the research method used by the researcher.

Research Methodology is a way to systematically solve the research problems. It may

be understood as a science of studying how research is done scientifically. In this

various steps that are generally adopted by a researcher in studying the research

problem along with the logic behind them is studied.

The statically method needs the collection of data in two forms

1. Primary data

2. Secondary data

Primary Data

The primary data are those, which are collected afresh and for the first time, and thus

happen to be original in character. The data on the required information is collected

from actual persons using the product/ services. This data is more suited for the

objectives of the project.

Secondary Data

The data which have already been collected by someone else or taken from published

or unpublished sources and which have been already been passed through the

statistical process.

Mode of Data Collection

Primary source

Information gathered from interacting with employees in the organization. And the

data from the textbooks and other magazines.

Secondary source

The methodology adopted or employed in this study was mostly on Secondary data

collection i.e.

Companies Annual Reports

- 7 -

Information from Internet

Publications

Daily prices of scripts from news papers

LIMITATIONS

Every research conducted has certain limitations. These arise due to the method of

sampling used, the method of data collation used and the source of the data apart from

many other things. The limitations of this study are as follows:

The data collected is of secondary nature and hence it is difficult to ascertain the

reliability of the data.

a) The scope of the study has been limited to the impact of the dividend

on the market value of the firm’s equity. Others factors affecting the

firm’s market value have been assumed to have remained unchanged.

b) The period of the study has been limited to only five years.

c) Data collection was strictly confined to secondary source. No primary

data is associated with the project.

- 8 -

CHAPTER-II

- 9 -

IN DUSTRY PROFILE

Evolution

Indian Stock Markets are one of the oldest in Asia. Its history dates back to nearly 200

years ago. The earliest records of security dealings in India are meager and obscure.

The East India Company was the dominant institution in those days and business in its

loan securities used to be transacted towards the close of the eighteenth century.

By 1830's business on corporate stocks and shares in Bank and Cotton

presses took place in Bombay. Though the trading list was broader in 1839, there

were only half a dozen brokers recognized by banks and merchants during 1840 and

1850.

The 1850's witnessed a rapid development of commercial enterprise and

brokerage business attracted many men into the field and by 1860 the number of

brokers increased into 60.

In 1860-61 the American Civil War broke out and cotton supply from

United States of Europe was stopped; thus, the 'Share Mania' in India begun. The

number of brokers increased to about 200 to 250. However, at the end of the

American Civil War, in 1865, a disastrous slump began (for example, Bank of

Bombay Share which had touched Rs 2850 could only be sold at Rs. 87).

At the end of the American Civil War, the brokers who thrived out of Civil War

in 1874, found a place in a street (now appropriately called as Dalal Street) where

they would conveniently assemble and transact business. In 1887, they formally

established in Bombay, the "Native Share and Stock Brokers' Association" (which is

alternatively known as “The Stock Exchange "). In 1895, the Stock Exchange

- 10 -

acquired a premise in the same street and it was inaugurated in 1899. Thus, the Stock

Exchange at Bombay was consolidated.

Other leading cities in stock market operations

Ahmadabad gained importance next to Bombay with respect to cotton textile industry.

After 1880, many mills originated from Ahmadabad and rapidly forged ahead. As

new mills were floated, the need for a Stock Exchange at Ahmadabad was realized

and in 1894 the brokers formed "The Ahmadabad Share and Stock Brokers'

Association".

What the cotton textile industry was to Bombay and Ahmadabad, the jute industry

was to Calcutta. Also tea and coal industries were the other major industrial groups in

Calcutta. After the Share Mania in 1861-65, in the 1870's there was a sharp boom in

jute shares, which was followed by a boom in tea shares in the 1880's and 1890's; and

a coal boom between 1904 and 1908. On June 1908, some leading brokers formed

"The Calcutta Stock Exchange Association".

In the beginning of the twentieth century, the industrial revolution was

on the way in India with the Swadeshi Movement; and with the inauguration of the

Tata Iron and Steel Company Limited in 1907, an important stage in industrial

advancement under Indian enterprise was reached.

Indian cotton and jute textiles, steel, sugar, paper and flour mills and all

companies generally enjoyed phenomenal prosperity, due to the First World War.

In 1920, the then demure city of Madras had the maiden thrill of a stock exchange

functioning in its midst, under the name and style of "The Madras Stock Exchange"

with 100 members. However, when boom faded, the number of members stood

reduced from 100 to 3, by 1923, and so it went out of existence.

In 1935, the stock market activity improved, especially in South India where there

was a rapid increase in the number of textile mills and many plantation companies

- 11 -

were floated. In 1937, a stock exchange was once again organized in Madras - Madras

Stock Exchange Association (Pvt) Limited. (In 1957 the name was changed to Madras

Stock Exchange Limited).

Lahore Stock Exchange was formed in 1934 and it had a brief life. It was merged with

the Punjab Stock Exchange Limited, which was incorporated in 1936.

Indian Stock Exchanges - An Umbrella Growth

The Second World War broke out in 1939. It gave a sharp boom which was followed

by a slump. But, in 1943, the situation changed radically, when India was fully

mobilized as a supply base.

On account of the restrictive controls on cotton, bullion, seeds and other commodities,

those dealing in them found in the stock market as the only outlet for their activities.

They were anxious to join the trade and their number was swelled by numerous

others. Many new associations were constituted for the purpose and Stock Exchanges

in all parts of the country were floated.

The Uttar Pradesh Stock Exchange Limited (1940), Nagpur Stock Exchange Limited

(1940) and Hyderabad Stock Exchange Limited (1944) were incorporated.

In Delhi two stock exchanges - Delhi Stock and Share Brokers' Association Limited

and the Delhi Stocks and Shares Exchange Limited - were floated and later in June

1947, amalgamated into the Delhi Stock Exchange Association Limited.

Post-independence Scenario

Most of the exchanges suffered almost a total eclipse during depression. Lahore

Exchange was closed during partition of the country and later migrated to Delhi and

merged with Delhi Stock Exchange.

Bangalore Stock Exchange Limited was registered in 1957 and recognized in 1963.

Most of the other exchanges languished till 1957 when they applied to the Central

Government for recognition under the Securities Contracts (Regulation) Act, 1956.

- 12 -

Only Bombay, Calcutta, Madras, Ahmadabad, Delhi, Hyderabad and Indore, the well

established exchanges, were recognized under the Act. Some of the members of the

other Associations were required to be admitted by the recognized stock exchanges on

a concessional basis, but acting on the principle of unitary control, all these pseudo

stock exchanges were refused recognition by the Government of India and they

thereupon ceased to function.

Thus, during early sixties there were eight recognized stock exchanges in India

(mentioned above). The number virtually remained unchanged, for nearly two

decades. During eighties, however, many stock exchanges were established: Cochin

Stock Exchange (1980), Uttar Pradesh Stock Exchange Association Limited (at

Kanpur, 1982), and Pune Stock Exchange Limited (1982), Ludhiana Stock Exchange

Association Limited (1983), Gauhati Stock Exchange Limited (1984), Kanara Stock

Exchange Limited (at Mangalore, 1985), Magadh Stock Exchange Association (at

Patna, 1986), Jaipur Stock Exchange Limited (1989), Bhubaneswar Stock Exchange

Association Limited (1989), Saurashtra Kutch Stock Exchange Limited (at Rajkot,

1989), Vadodara Stock Exchange Limited (at Baroda, 1990) and recently established

exchanges - Coimbatore and Meerut. Thus, at present, there are totally twenty one

recognized stock exchanges in India excluding the Over The Counter Exchange of

India Limited (OTCEI) and the National Stock Exchange of India Limited (NSEIL).

The Table given below portrays the overall growth pattern of Indian stock markets

since independence. It is quite evident from the Table that Indian stock markets have

not only grown just in number of exchanges, but also in number of listed companies

and in capital of listed companies. The remarkable growth after 1985 can be clearly

seen from the Table, and this was due to the favouring government policies towards

security market industry.

Trading Pattern of the Indian Stock Market

Trading in Indian stock exchanges are limited to listed securities of public limited

companies. They are broadly divided into two categories, namely, specified securities

(forward list) and non-specified securities (cash list). Equity shares of dividend

paying, growth-oriented companies with a paid-up capital of at least Rs.50 million

- 13 -

and a market capitalization of at least Rs.100 million and having more than 20,000

shareholders are, normally, put in the specified group and the balance in non-specified

group.

Two types of transactions can be carried out on the Indian stock exchanges: (a) spot

delivery transactions "for delivery and payment within the time or on the date

stipulated when entering into the contract which shall not be more than 14 days

following the date of the contract" : and (b) forward transactions "delivery and

payment can be extended by further period of 14 days each so that the overall period

does not exceed 90 days from the date of the contract". The latter is permitted only in

the case of specified shares. The brokers who carry over the outstanding pay carry

over charges (can tango or backwardation) which are usually determined by the rates

of interest prevailing.

A member broker in an Indian stock exchange can act as an agent, buy and sell

securities for his clients on a commission basis and also can act as a trader or dealer as

a principal, buy and sell securities on his own account and risk, in contrast with the

practice prevailing on New York and London Stock Exchanges, where a member can

act as a jobber or a broker only.

The nature of trading on Indian Stock Exchanges are that of age old conventional

style of face-to-face trading with bids and offers being made by open outcry.

However, there is a great amount of effort to modernize the Indian stock exchanges in

the very recent times.

Over The Counter Exchange of India (OTCEI)

The traditional trading mechanism prevailed in the Indian stock markets gave way to

many functional inefficiencies, such as, absence of liquidity, lack of transparency,

unduly long settlement periods and benami transactions, which affected the small

investors to a great extent. To provide improved services to investors, the country's

first ring less, scrip less, electronic stock exchange - OTCEI - was created in 1992 by

country's premier financial institutions - Unit Trust of India, Industrial Credit and

Investment Corporation of India, Industrial Development Bank of India, SBI Capital

Markets, Industrial Finance Corporation of India, General Insurance Corporation and

its subsidiaries and CanBank Financial Services.

- 14 -

Trading at OTCEI is done over the centers spread across the country. Securities traded

on the OTCEI are classified into:

Listed Securities - The shares and debentures of the companies listed on the

OTC can be bought or sold at any OTC counter all over the country and they

should not be listed anywhere else

Permitted Securities - Certain shares and debentures listed on other exchanges

and units of mutual funds are allowed to be traded

Initiated debentures - Any equity holding at least one lakh debentures of a

particular scrip can offer them for trading on the OTC.

OTC has a unique feature of trading compared to other traditional exchanges. That is,

certificates of listed securities and initiated debentures are not traded at OTC. The

original certificate will be safely with the custodian. But, a counter receipt is

generated out at the counter which substitutes the share certificate and is used for all

transactions.

In the case of permitted securities, the system is similar to a traditional stock

exchange. The difference is that the delivery and payment procedure will be

completed within 14 days.

Compared to the traditional Exchanges, OTC Exchange network has the following

advantages:

OTCEI has widely dispersed trading mechanism across the country which

provides greater liquidity and lesser risk of intermediary charges.

Greater transparency and accuracy of prices is obtained due to the screen-

based scrip less trading.

Since the exact price of the transaction is shown on the computer screen, the

investor gets to know the exact price at which s/he is trading.

Faster settlement and transfer process compared to other exchanges.

- 15 -

In the case of an OTC issue (new issue), the allotment procedure is completed

in a month and trading commences after a month of the issue closure, whereas

it takes a longer period for the same with respect to other exchanges.

Thus, with the superior trading mechanism coupled with information transparency

investors are gradually becoming aware of the manifold advantages of the OTCEI.

National Stock Exchange (NSE)

With the liberalization of the Indian economy, it was found inevitable to lift the

Indian stock market trading system on par with the international standards. On the

basis of the recommendations of high powered Pherwani Committee, the National

Stock Exchange was incorporated in 1992 by Industrial Development Bank of India,

Industrial Credit and Investment Corporation of India, Industrial Finance Corporation

of India, all Insurance Corporations, selected commercial banks and others.

Trading at NSE can be classified under two broad categories:

(a) Wholesale debt market and

(b) Capital market.

Wholesale debt market operations are similar to money market operations -

institutions and corporate bodies enter into high value transactions in financial

instruments such as government securities, treasury bills, public sector unit bonds,

commercial paper, certificate of deposit, etc.

There are two kinds of players in NSE:

(a) Trading members and

(b) Participants.

- 16 -

Recognized members of NSE are called trading members who trade on behalf of

themselves and their clients. Participants include trading members and large players

like banks who take direct settlement responsibility.

Trading at NSE takes place through a fully automated screen-based trading

mechanism which adopts the principle of an order-driven market. Trading members

can stay at their offices and execute the trading, since they are linked through a

communication network. The prices at which the buyer and seller are willing to

transact will appear on the screen. When the prices match the transaction will be

completed and a confirmation slip will be printed at the office of the trading member.

NSE has several advantages over the traditional trading exchanges. They are as

follows:

NSE brings an integrated stock market trading network across the nation.

Investors can trade at the same price from anywhere in the country since inter-

market operations are streamlined coupled with the countrywide access to the

securities.

Delays in communication, late payments and the malpractice’s prevailing in

the traditional trading mechanism can be done away with greater operational

efficiency and informational transparency in the stock market operations, with

the support of total computerized network.

Unless stock markets provide professionalized service, small investors and foreign

investors will not be interested in capital market operations. And capital market being

one of the major source of long-term finance for industrial projects, India cannot

afford to damage the capital market path. In this regard NSE gains vital importance in

the Indian capital market system.

Preamble

Often, in the economic literature we find the terms ‘development’ and ‘growth’ are

used interchangeably. However, there is a difference. Economic growth refers to the

sustained increase in per capita or total income, while the term economic development

implies sustained structural change, including all the complex effects of economic

growth. In other words, growth is associated with free enterprise, where as

- 17 -

development requires some sort of control and regulation of the forces affecting

development. Thus, economic development is a process and growth is a phenomenon.

Economic planning is very critical for a nation, especially a developing country like

India to take the country in the path of economic development to attain economic

growth.

Why Economic Planning for India?

One of the major objective of planning in India is to increase the rate of economic

development, implying that increasing the rate of capital formation by raising the

levels of income, saving and investment. However, increasing the rate of capital

formation in India is beset with a number of difficulties. People are poverty ridden.

Their capacity to save is extremely low due to low levels of income and high

propensity to consume. Therefore, the rate of investment is low which leads to capital

deficiency and low productivity. Low productivity means low income and the vicious

circle continues. Thus, to break this vicious economic circle, planning is inevitable for

India.

The market mechanism works imperfectly in developing nations due to the ignorance

and unfamiliarity with it. Therefore, to improve and strengthen market mechanism

planning is very vital. In India, a large portion of the economy is non-monetized; the

product, factors of production, money and capital markets is not organized properly.

Thus the prevailing price mechanism fails to bring about adjustments between

aggregate demand and supply of goods and services. Thus, to improve the economy,

market imperfections has to be removed; available resources has to be mobilized and

utilized efficiently; and structural rigidities has to be overcome. These can be attained

only through planning.

In India, capital is scarce; and unemployment and disguised unemployment is

prevalent. Thus, where capital was being scarce and labour being abundant, providing

useful employment opportunities to an increasing labour force is a difficult exercise.

Only a centralized planning model can solve this macro problem of India.

Further, in a country like India where agricultural dependence is very high, one

cannot ignore this segment in the process of economic development. Therefore, an

economic development model has to consider a balanced approach to link both

- 18 -

agriculture and industry and lead for a paralleled growth. Not to mention, both

agriculture and industry cannot develop without adequate infrastructural facilities

which only the state can provide and this is possible only through a well carved out

planning strategy. The government’s role in providing infrastructure is unavoidable

due to the fact that the role of private sector in infrastructural development of India is

very minimal since these infrastructure projects are considered as unprofitable by the

private sector.

Further, India is a clear case of income disparity. Thus, it is the duty of the state to

reduce the prevailing income inequalities. This is possible only through planning.

Planning History of India

The development of planning in India began prior to the first Five Year Plan of

independent India, long before independence even. The idea of central directions of

resources to overcome persistent poverty gradually, because one of the main policies

advocated by nationalists early in the century. The Congress Party worked out a

program for economic advancement during the 1920’s, and 1930’s and by the 1938

they formed a National Planning Committee under the chairmanship of future Prime

Minister Nehru. The Committee had little time to do anything but prepare programs

and reports before the Second World War which put an end to it. But it was already

more than an academic exercise remote from administration. Provisional government

had been elected in 1938, and the Congress Party leaders held positions of

responsibility. After the war, the Interim government of the pre-independence years

appointed an Advisory Planning Board. The Board produced a number of somewhat

disconnected Plans itself. But, more important in the long run, it recommended the

appointment of a Planning Commission.

The Planning Commission did not start work properly until 1950. During the first

three years of independent India, the state and economy scarcely had a stable structure

at all, while millions of refugees crossed the newly established borders of India and

Pakistan, and while ex-princely states (over 500 of them) were being merged into

- 19 -

India or Pakistan. The Planning Commission as it now exists was not set up until the

new India had adopted its Constitution in January 1950.

Objectives of Indian Planning

The Planning Commission was set up the following Directive principles :

To make an assessment of the material, capital and human resources of the

country, including technical personnel, and investigate the possibilities of

augmenting such of these resources as are found to be deficient in relation to

the nation’s requirement.

To formulate a plan for the most effective and balanced use of the country’s

resources.

Having determined the priorities, to define the stages in which the plan should

be carried out, and propose the allocation of resources for the completion of

each stage.

To indicate the factors which are tending to retard economic development, and

determine the conditions which, in view of the current social and political

situation, should be established for the successful execution of the Plan.

To determine the nature of the machinery this will be necessary for securing

the successful implementation of each stage of Plan in all its aspects.

To appraise from time to time the progress achieved in the execution of each

stage of the Plan and recommend the adjustments of policy and measures that

such appraisals may show to be necessary.

To make such interim or auxiliary recommendations as appear to it to be

appropriate either for facilitating the discharge of the duties assigned to it or

on a consideration of the prevailing economic conditions, current policies,

measures and development programs; or on an examination of such specific

problems as may be referred to it for advice by Central or State Governments.

The long-term general objectives of Indian Planning are as follows:

Increasing National Income

- 20 -

Reducing inequalities in the distribution of income and wealth

Elimination of poverty

Providing additional employment; and

Alleviating bottlenecks in the areas of : agricultural production, manufacturing

capacity for producer’s goods and balance of payments.

Economic growth, as the primary objective has remained in focus in all Five Year

Plans. Approximately, economic growth has been targeted at a rate of five per cent

per annum. High priority to economic growth in Indian Plans looks very much

justified in view of long period of stagnation during the British rule

COMPANY PROFILE

- 21 -

Introduction to Indiabulls

Indiabulls is India’s leading Financial and Real Estate Company with a wide

presence throughout India. They ensure convenience and reliability in all their

products and services. Indiabulls has over 640 branches all over India. The customers

of Indiabulls are more than 4,50,000 which covers from a wide range of financial

services and products from securities, derivatives trading, depositary services,

research & advisory services, consumer secured & unsecured credit, loan against

shares and mortgage & housing finance. The company employs around 4000

Relationship managers who help the clients to satisfy their customized financial goals.

Indiabulls entered the Real Estate business in the year 2005 with its group of

companies. Large scale projects worth several hundred million dollars are evaluated

by them.

Indiabulls Financial Services Ltd is listed on the National Stock Exchange

(NSE), Bombay Stock Exchange (BSE) and Luxembourg Stock Exchange. The

market capitalization of Indiabulls is around USD 2500 million (29thDecember,

2006). Consolidated net worth of the group is around USD 700 million. Indiabulls

and its group companies have attracted USD 500 million of equity capital in Foreign

Direct Investment (FDI) since March 2000. Some of the large shareholders of

- 22 -

Indiabulls are the largest financial institutions of the world such as Fidelity Funds,

Goldman Sachs, Merrill Lynch, Morgan Stanley and Farallon Capital.

In middle of 1999, when e-commerce was just about starting in India,

Sameer Gehlaut and his close IIT Delhi friend Rajiv Rattan got together and bought a

defunct securities company with a NSE membership and started offering brokerage

services. A Few months later, their friend Saurabh Mittal also joined them. By

December 1999, the company embarked on its journey to build one of the first online

platforms in India for offering internet brokerage services. In January 2000, the 3

founders incorporated Indiabulls Financial Services and made it as the flagship

company.

In mid 2000, Indiabulls Financial Services received venture capital funding from Mr

L.N. Mittal & Mr Harish Fabiani. In late 2000, Indiabulls Securities, a subsidiary of

Indiabulls Financial Services started offering online brokerage services and

simultaneously opened physical offices across India. By 2003, Indiabulls securities

had established a strong pan India presence and client base through its offices and on

the internet.

In September 2004, Indiabulls Financial Services went public with an IPO at Rs 19 a

share. In late 2004, Indiabulls Financial Services started its financing business with

consumer loans. In March 2005, Indiabulls Properties Private Ltd, a subsidiary of

Indiabulls Financial Services, participated in government auction of Jupiter Mills, a

defunct 11 acre textile mill owned by NTC in Lower Parel, Mumbai. Indiabulls

Properties private Ltd won the mill in auction and that purchase started Indiabulls real

estate business. A few months later, Indiabulls Real Estate company pvt ltd bought

Elphinstone mill in Lower Parel, another textile mill auctioned by NTC.

With real estate business gaining size, Indiabulls Financial Services demerged the real

estate business under Indiabulls Real Estate and each shareholder of Indiabulls

Financial Services received additional share of Indiabulls Real Estate through the

demerger. Subsequently, Indiabulls Financial Services also demerged Indiabulls

- 23 -

Securities and each shareholder of Indiabulls Financial Services also received a share

of Indiabulls Securities.

In year 2007, Indiabulls Real Estate incorporated a 100% subsidiary, Indiabulls

Power, to build power plants and started work on building Nashik & Amrawati

thermal power plants. Indiabulls Power went public in September 2009.

Today, Indiabulls Group has a networth of Rs 16,796 Crore & has a strong presence

in important sectors like financial services, power & real estate through independently

listed companies and Indiabulls Group continues its journey of building businesses

with strong cash flows.

MANAGEMENT TEAM

Indiabulls Group

Mr Rajiv Rattan - Vice Chairman

Mr Saurabh Mittal - Vice Chairman

Mr Gagan Banga - Group Spokesperson

Mr Ashok Kacker - Group President

Mr Saket Bahuguna - Group CLO

Mr Ashok Sharma - Group CFO

Mr Ajit Mittal - Group Director

Mr Gurbans Singh - Group Director

Mr Tejinderpal Singh Miglani - Group CIO

Indiabulls Financial Services Limited

Mr Gagan Banga - CEO

- 24 -

Mr Ashwini Kumar Hooda - DMD

Indiabulls Real Estate Limited

Mr Vipul Bansal - CEO

Mr Narendra Gehlaut - Joint MD

Indiabulls Power Limited

Mr Ranjit Gupta - CEO

Mr Murali Subramanian - COO

Indiabulls Securities Limited

Mr Divyesh Shah - CEO

Mr Vijay Babbar – DMD

Indiabulls supports Money life Foundation in Empowering Investors

“Moneylife Foundation” in collaboration with Indiabulls, recently organized an

‘Investor, Empower Yourself’ seminar, which was held at the lush Town & Country

Club at New Gurgaon, in the National Capital Region (NCR), on Saturday, 7th May

2011. This was the first occasion for Moneylife Foundation to venture into other

territories outside Maharashtra. Indiabulls played a major role in helping this event

happen successfully.

The event witnessed over 300 attendees not only from Gurgaon but also from other

parts of National Capital Region (NCR), Delhi, Allahabad, Ludhiana, Chandigarh &

other cities from northern region of India. The venue was fully packed with eager &

curious investors. “Moneylife Foundation” expressed its gratitude towards helpful

- 25 -

team of Indiabulls led by Mr. Gagan Banga, CEO - Indiabulls Financial Services Ltd,

for making this event such a huge success.

The event started with introductory remarks & guidance by Mr. Gagan Banga, CEO -

Indiabulls Financial Services Ltd. Mr. Veeresh Malik, Consulting Editor, Moneylife,

Delhi gave a brief introduction about Moneylife Foundation.Then audience was

guided by Sucheta Dalal, Trustee - Moneylife Foundation and Managing Editor-

Moneylife, on How to be Safe with your money & Debashis Basu, Trustee -

Moneylife Foundation and Editor- Moneylife about How to be smart with your

investments. Mr. Sachin Choudhary, Director & Business Head - Indiabulls Housing

Finance Ltd, talked about Do's and Don’ts of Housing Mortgages. Ms. Sucheta Dalal

also explained the importance & procedure of Wills & Nominations.

This event helped people in understanding how to become an aware and empowered

investor. The attendees included both finically literate & new investors. They posted

number of intelligent questions which were adequately answered by all the speakers.

Empowering today’s investors by creating awareness and guiding them in taking wise

decisions when it comes to money or investments was the main objective of ‘Investor,

Empower Yourself’ seminar. During the Panel Discussion with the panel members

Sucheta Dalal, Debashis Basu & Sachin Choudhary, quite a few interesting &

informative issues regarding Investments were discussed. Mr. Monu Ratra, National

Sales Manager - Indiabulls housing Finance Ltd gave Vote of Thanks.

This event received many request and suggestions from audience about continuing

with such events all over India so that citizens of India will be more empowered

investors & ultimately nation will benefit from it. There were some requests from

audience to telecast further events live on television & internet so that those who are

unable to attend the event will also get the guidance. The knowledge shared about the

investments during the event was well appreciated by all.

Moneylife Foundation has been instrumental in promoting financial literacy & pro-

customer advocacy in India. Moneylife Foundation has been organizing such events

at the Moneylife Knowledge Centre in Mumbai, and also in various cities across

- 26 -

Maharashtra. The Foundation has completed 15 months of spreading financial literacy

& has hosted around 49 speakers and 61 events. Currently, more than 5,000 people

are members of the Foundation.

After the seminar, Indiabulls received feedbacks from some attendees congratulating

Indiabulls’ team about the success of seminar. Many of the attendees mentioned that

they are looking forward to such seminars in future.

Indiabulls has been participating in such Corporate Social Activities with many other

socially aware groups and trusts & Indiabulls is committed to continue in doing so in

future.

THE HUB

The Hub at One Indiabulls Centre at Lower Parel is an intelligently designed business

centre in Mumbai

In the past few years serviced office industry has been maturing in India and today is

a mainstream occupancy option for businesses of all sizes. Whether a start-up, SME

or a multi-national, companies are now opting for viable alternative to leasing or the

outright purchase of commercial workspace.

Thus managed business centers have emerged as an innovative solution to these

workspace requirements. The Hub at One Indiabulls Centre at Lower Parel is one

such intelligently designed business centre in Mumbai that offers 25,000sqft of fully

equipped, serviced workspace not only suitable for large corporations but also for

small businesses and lean team set ups due to the option of small customized spaces.

The real advantage of The Hub is not just that it is more cost effective but also it

offers best possible working environment by offering conveniences such as advanced

security, pantry and maintenance services including IT and utility bills for electricity,

water & HVAC.

- 27 -

What’s more, those moving into The Hub serviced offices enjoy the added benefit of

cutting edge IT and telecom infrastructure, reception and secretarial support, hi-tech

meeting rooms and video conferencing suites as well as business lounge, food courts

and state of the art fitness centre.

Not to forget among various factors that can affect a business and its success and

growth, is the address or the location of the office especially those of newly

established enterprises. The Hub within a world class contemporary business complex

located between Nariman Point and Bandra Kurla Complex and in close proximity to

Bandra Worli Sea Link is undeniably in the finest commercial location in Mumbai’s

upcoming central business district- Lower Parel.

Undeniably, The Hub is a new age business centre that provides a very attractive

proposition to businesses of all sizes to help their own business grow and prosper.

Indiabulls CSR Initiative - Drug Access Program for cancer patients

in partnership with Novartis

As part of our deep commitment to social causes, Indiabulls has taken up this noble

project named “Novartis Oncology Access” in partnership with Novartis

(manufacturer of drugs) & Max foundation (NGO). We as the financial partner are

helping them assess actual income of patient & family & based on assessed income;

recommend the drugs donation slab as per approved guidelines & SOP.

Novartis are the developers & makers of Glivec (Imatinib) - a medication for the

treatment of Ph+ chronic myeloid leukemia (CML) in chronic phase, accelerated

phase and blast crisis for both pediatric and adult patients. This drug is also indicated

for adult patients with adjuvant, unresectable and/or metastatic c-kit / cd-117

gastrointestinal stromal tumors (GIST). Tasigna (nilotinib) a drug recently launched

by Novartis is used as medication for the treatment of Ph+ chronic myeloid leukemia

(CML) in chronic phase, accelerated phase and blast crisis for only adult patients.

NOA program:

The NOA program is a drug access program for to help patients who have been

prescribed Glivec and Tasigna but cannot afford to pay for the entire treatment cost.

- 28 -

This program is run by Novartis along with its partner Physicians- enrolls patient

under this program after diagnosis, The MAX Foundation- independent NGO –

Assist patient throughout the program in completing formalities & procurement of

medicines, Indiabulls Financial Services - independent body for financial evaluation

of patient, collection & safekeeping the submitted documents with confidentiality and

C&F outlets – Independent pharmacist, dispenses drugs to patients & manage drug

inventory.

Indiabulls Financial Services: As a NOA partner we are performing task of the local

credit evaluation agency which works as an independent and unbiased body for the

financial analysis and assessment of the patient and family members’ earning capacity

to afford medical expenses on critical disease. The analysis bases on income levels

assessment by way of financial evaluation ,field verification, living standard, personal

discussion with patient/ care taker & guidelines as per standard operating procedure

(SOP) which is prepared by Novartis based on the WHO guidelines for drug donation

programs using Business for Social Responsibility’s (BSR) cost of living index, a

well-established international guide often used as eligibility criteria for determining

access to drug assistance programs. Based on the family composite Income a suitable

donation decision is given.

Contractibility

Indiabulls has designated a dedicated Help-Line Number: 022 30491720 that will

receive patient calls during office hours (9:00 a.m. to 6.00 p.m.) so it may handle in-

bound calls in response only to queries regarding the submission of requirements for

the NOA. For any medical or clinical queries, Indiabulls Financial Services refer

patients to their treating physician.

Businesses

Indiabulls Group is one of the country's leading business houses with business

interests in Power, Financial Services, Real Estate and Infrastructure . Indiabulls

Group companies are listed in Indian and overseas financial markets. The Net worth

of the Group is Rs 16,796 Crore and the total planned capital expenditure of the

Group by 2013-14 is Rs 35,000 Crore.

- 29 -

Indiabulls Power is currently developing Thermal Power Projects with an aggregate

capacity of 5400 MW. The first unit is expected to go on stream in May 2012. The net

worth of Indiabulls Power is Rs 3,917 Crore. The company has a total capital

expenditure of Rs 27,500 Crore. The company has been assigned 'BBB' rating.

Indiabulls Financial Services is one of India’s leading non-banking finance

companies providing Home Loans, Commercial Vehicle Loans and Secured SME

Loans. The company has a net worth of Rs 4,680 crore with an asset book of over Rs

18,500 Crore. The company has disbursed loans over Rs 45,000 Crore to over

3,00,000 customers till date. Amongst its financial services and banking peers,

Indiabulls Financial Services ranks amongst the top few companies both in terms of

net worth and capital adequacy. Indiabulls Financial Services has been assigned

‘AA+’ rating and has presence in over 90 cities and towns with a total branch network

of 140 branches.

Indiabulls Real Estate is among India's top Real Estate companies with development

projects spread across residential complexes, integrated townships, commercial office

complexes, hotels, malls, Special Economic Zones (SEZs) and infrastructure

development. Indiabulls Real Estate partnered with Farallon Capital Management

LLC of USA to bring the first FDI into real estate in the country. The company has a

networth of Rs 7,953 Crore and has purchased prime land, mostly in the metros and

other Tier 1 cities worth Rs 4,000 Crore in government auctions alone. Indiabulls

Real Estate is currently developing 57 million sqft into premium quality, high-end

commercial, residential and retail spaces. The company has been assigned 'A+' rating.

Indiabulls Securities is one of India's leading capital markets companies providing

securities broking and advisory services. Indiabulls Securities also provides

depository services, equity research services and IPO distribution to its clients and

offers commodities trading through a separate company. These services are provided

both through on-line and off-line distribution channels. Indiabulls Securities is a

pioneer of on-line securities trading in India. Indiabulls Securities’ in-house trading

platform is one of the fastest and most efficient trading platforms in the country.

Indiabulls Securities has been assigned the highest rating BQ-1 by CRISIL.

- 30 -

Indiabulls foundation

India has witnessed an economic transformation over the past two decades, translating

into higher incomes, better educational opportunities, improved infrastructure, a

dynamic private sector, and leadership in the global community. We have much to be

proud of.

But we also recognize that we have a long way to go. Over 700 million people live

under $2 a day. Learning levels in schools remain abysmally low; most of our rural

population do not have access to basic health care, regular electricity, clean water, and

sanitation. India has some of the world’s worst statistics on basic development

indicators such as malnutrition, infant mortality, and gender discrimination.

As a society, we are at the confluence of accelerated economic progress and extreme

deprivation, all in the same country, at the same time.

As corporate citizens, we at Indiabulls are conscious of the opportunities and the

responsibility that this confluence presents.

Investments to increase income levels of our poorest people will expand business

opportunities manifold. Investments to improve education, health and skills training

will improve the efficiency of the economy. Protecting our environment will actually

lower our costs of doing business. Providing our youth with gainful employment and

a chance to improve their lives will ensure societal and political stability- setting a

strong foundation for economic sustainability. All of these investments will help

create an inclusive society, ensuring a sustainable return to our shareholders.

The Indiabulls Group is keen to help in building an inclusive and prosperous society

and we are beginning our efforts in this direction through Indiabulls Foundation.

One of the first initiatives of the Foundation is to support the development of rural

districts. Our aim is to support development across multiple domains in a district

based approach. Some of the areas where we want to help are in economic

development and skills training, access to drinking water, school education, public

health, agriculture and support to the local government.

- 31 -

Commercial Vehicle Loans

Indiabulls Commercial Vehicle Loans offers commercial auto loans to a variety of

business owners. We are a preferred financer with first time buyers as well as fleet

operators providing commercial vehicle loans with simple documentation and quick

results.

The Commercial Vehicle Finance provided by us helps the small and medium

operators to acquire vehicles with minimum hassle and documentation. We provide

customized financing options to suit your needs.

Our strength lies in the quick completion of transactions, long association with

transporters and the intimate knowledge of the market and its nuances.

Our finance schemes are easy to understand with no hidden costs.

We assure you a quick, transparent and hassle-free deal.

1. Product Offering

Finance for new commercial vehicles

Finance for used vehicles

Tractor Loans

2. Proposed Finance

Tyre Funding

Accidental Funding

Engine Funding

Take over loans

Top up loan on existing loan with us

- 32 -

3. Features of Loan Offering

Loan for up to 15 years old vehicles.

The best loan offering in the market – up to 95% for used vehicles & 100%

for new commercial vehicle chassis

Max tenure of up to 48 months for used vehicles 60 months for new

commercial vehicle chassis

Max tenure of up to 48 months for used vehicles 60 months for new

commercial vehicle chassis

Customized loan to suit your needs

Door Step Services

Easy Documentation

Quick & Hassle free services

Attractive Rate of Interest

No intermediary or Direct Marketing Agent for loan processing

- 33 -

Senior Vice President

Regional Manager

Branch ManagerSenior Sales Manager

Support System Sales Function

RM/SRM

ARM

Local ComplianceOfficer

Back OfficeExecutive

Dealer

Organization Structure- Board of Directors:

- 34 -

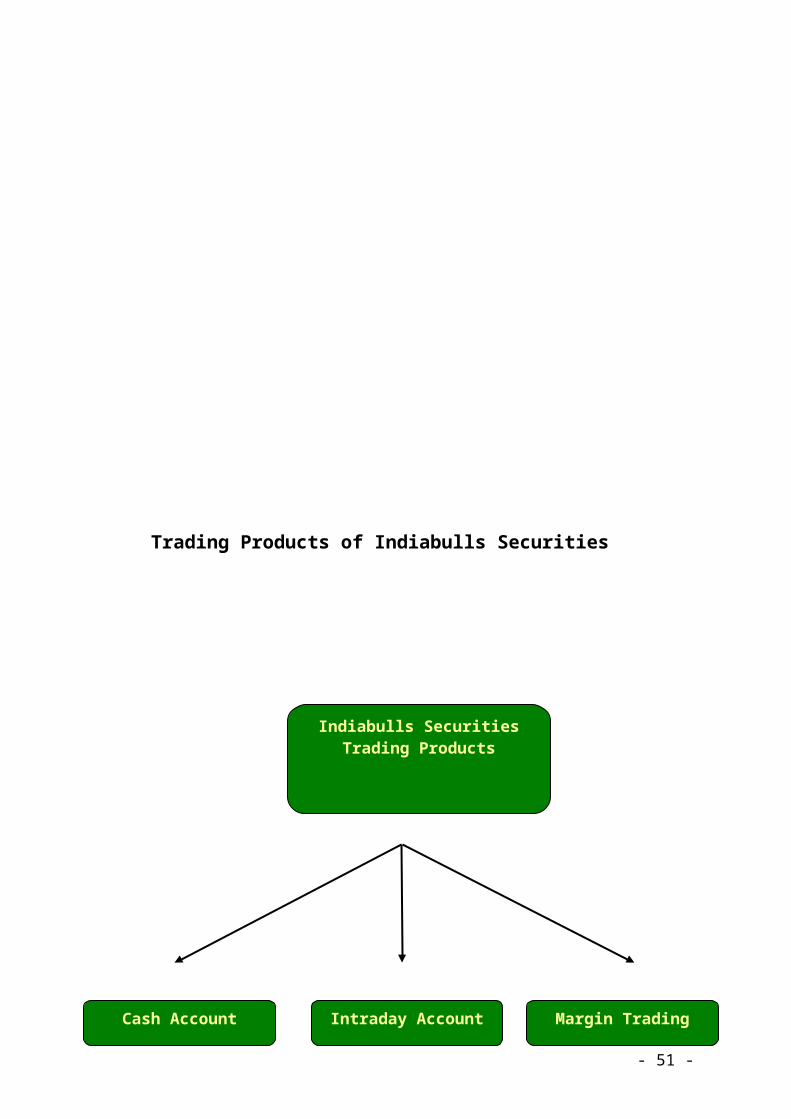

Indiabulls SecuritiesTrading Products

Cash Account Intraday Account Margin Trading

Trading Products of Indiabulls Securities

Indiabulls Securities provide three products for trading. They are

Cash Account

Intraday Account

Margin Trading (Mantra)

- 35 -

Cash Account: It provides the client to buy 4 times of cash balance in his trading

account.

Intraday Product: It provides the client to buy 8 times of his cash balance in the

trading account.

Mantra Account: Also called as margin trading, is a special account to buy on

leverage for a longer duration

Indiabulls Financial Services Ltd

Indiabulls Financial Services Ltd. was incorporated in the year 2005.The Auditors of

Indiabulls Financial Services Ltd. are Deloitte, Haskins & Sells. The main activity of

this company is in relation to securities and stock brokerage. It was also responsible

for setting up one of India’s first trading platforms.

The subsidiaries of Indiabulls Financial Services Ltd. include:

Indiabulls Capital Services Ltd.

Indiabulls Commodities Pvt. Ltd.

Indiabulls Credit Services Ltd.

Indiabulls Finance Co. Pvt. Ltd

Indiabulls Housing Finance Ltd.

Indiabulls Insurance Advisors Pvt. Ltd.

Indiabulls Resources Ltd.

Indiabulls Securities Ltd.

The Bankers of Indiabulls Financial Services Ltd. are as follows:

ABN-Amro Bank

Andhra Bank

- 36 -

Bank of Maharashtra

Bank of Rajasthan Ltd.

Canara Bank

Centurion Bank of Punjab Ltd.

Citibank

Corporation Bank

Dena Bank

HDFC Bank Ltd

HSBC Ltd.

ICICI Bank Ltd.

IDBI Ltd

Industrial Bank Ltd.

ING Vysya Bank Ltd

Karnataka Bank

Punjab National Bank

State Bank Of India

Syndicate Bank

Union Bank Of India

UTI Bank Ltd.

Yes Bank Ltd.

- 37 -

CHAPTER-III

REVIEW OF LITERATURE

- 38 -

DIVIDEND DECISIONS- THEORITICAL FRAME WORKS

Introduction and Meaning:

The term dividend refers to that part of profits of a company which is

distributed by the company among its shareholders. It is the reward of the

shareholders for investments made by them in the shares of the company.

A dividend is a payment made by a company to its shareholders. A

company can retain its profit for the purpose of reinvestment in the business

operations (known as retained earnings), or it can distribute the profit among its

shareholders in the form of dividends.

A dividend is not regarded as expenditure; rather, it is considered a

distribution of assets among shareholders. The majority of companies keeps a

component of their profits as retained earnings and distributes the rest as dividend.

Dividend policy of a firm, thus affects both the long-term financing and the

wealth of shareholders. As a result, the firm’s decision to pay dividends must be

reached in such a manner so as to equitably assign the distributed profits and retained

earnings. Since divided is a right of shareholders to participate in the profits and

surplus of the company for their investment in the share capital of the company, they

should receive fair amount of the profits. The company should, therefore, distribute a

reasonable amount as dividends to its members and retain the rest for its growth and

survival.

Dividend refers to that portion of a firm’s net earnings, which are paid out

to the shareholders. A major decision of financial management is the dividend

decision in the sense that the firm has to choose between distributing the profits to the

- 39 -

shareholders and plugging them back into the business. The choice would obviously

hinge on the effect of the decision on the maximizations of shareholders wealth.

There are however, conflicting opinions regarding the impact of dividends on

the valuation of a firm. According to one school of thought, dividends are irrelevant

so that the amount of dividends paid has no effect on the, valuation of a firm. On the

other hand, certain theories consider the dividend decision as relevant to the value of

the firm measured in terms of the market price of the shares.

The purpose of this report is, therefore, to present a critical analysis of some

important theories representing these two schools of thought with a view to

illustrating the relationship between dividend policy and the valuation of a firm. The

theories, which support the relevance hypothesis, are examined in the report.

Definition of Dividend:

1. A sum of money to be divided and distributed; the share of a sum divided that

falls to each individual; a distribute sum, share, or percentage; -- applied to the

profits as appropriated among shareholders, and to assets as apportioned

among creditors; as, the dividend of a bank, a railway corporation, or a

bankrupt estate.

2. A number or quantity which is to be divided.

Overview of Dividend Decision Dividend decision

Refers to the policy that the management formulates in regard to earnings for

distribution as dividends among shareholders. Dividend decision determines the

division of earnings between payments to shareholders and retained earnings The

Dividend Decision, in corporate finance, is a decision made by the directors of a

company about the amount and timing of any cash payments made to the company's

stockholders. The Dividend Decision is an important part of the present day

corporate world. The Dividend decision is an important one for the firm as it may

influence its capital structure and stock price. In addition, the Dividend decision may

determine the amount of taxation that stockholders pay.

- 40 -

Factors influencing Dividend Decisions

There are certain issues that are taken into account by the directors while making the

dividend decisions:

Free Cash Flow

Signaling of Information

Clients of Dividends

Free Cash Flow Theory

The free cash flow theory is one of the prime factors of consideration when a

dividend decision is taken. As per this theory the companies provide the shareholders

with the money that is left after investing in all the projects that have a positive net

present value.

Signaling of Information

It has been observed that the increase of the worth of stocks in the share market is

directly proportional to the dividend information that is available in the market about

the company. Whenever a company announces that it would provide more dividends

to its shareholders, the price of the shares increases.

Clients of Dividends

While taking dividend decisions the directors have to be aware of the needs of the

various types of shareholders as a particular type of distribution of shares may not be

suitable for a certain group of shareholders.

It has been seen that the companies have been making decent profits and also reduced

their expenditure by providing dividends to only a particular group of shareholders.

For more information please refer to the following links:

Forms of Dividend

Scrip Dividend- An unusual type of dividend involving the distribution of promissory notes that calls for some type of payment at a future date.

Bond Dividend- A type of liability dividend paid in the dividend payer's bonds.

- 41 -

Property Dividend- A stockholder dividend paid in a form other than cash, scrip, or the firm's own stock.

Cash Dividend- A dividend paid in cash to a company's shareholders , normally out of the its current earnings or accumulated profits

Debenture Dividend

Optional Dividend- Dividend which the shareholder can choose to take as either cash or stock.

Factors affecting stability of dividend policy

There are a number of factors which effect stability of dividend policy. They are as

follows:

1. Stability of Earnings: The nature of business has an important bearing on

the dividend policy. Industrial units having stability of earings may formulate

a more consistent dividend policy than those having an uneven flow of

incomes because they can predict easily their savings and earnings.

2. Liquidity of Funds: Availability of cash and sound financial position is also

an important factor in dividend decisions. A dividend represents a cash

outflow, the greater the funds and the liquidity of the firm the better the ability

to pay dividend.

3. Extent of Share Distribution: Nature of ownership also affects the

dividend decisions. A closely held company is likely to get the assent of the

shareholders for the suspension of dividend or for following a conservative

dividend policy.

4. Government Policy: The earnings capacity of the enterprise is widely

affected by the change is fiscal, industrial, labour, control and other

government policies.

5. Age of Corporation: Age of the corporation is one of the important factor.

A newly established company many require much of its earnings for

expansion and plant improvement and may adopt a rigid dividend policy

- 42 -

while, an older company can formulate a clear cut and more consistent policy

regarding dividend.

6. Need for Additional Capital: Companies retain a part of their profits for

strengthening their financial position. The income may be conserved for

meeting the increased requirements of working capital or of future expansion.

7. Past Dividend Rates: While formulating the Dividend Policy, the directors

must keep in mind the dividend paid in past years. The current rate should be

around the average past rate. In a new concern, the company should consider

the dividend policy of the rival organization.

8. Taxation Policy: High taxation reduces the earnings of the companies and

consequently the rate of dividend is lowered down.

Residual dividend policy

Is used by companies, which finance new projects through equity that is internally

generated. In this policy, the dividend payments are made from the equity that

remains after all the project capital needs are met. This equity is also known as

residual equity. It is advisable that those companies, which follow the policy of

residual dividend, should maintain a balanced debt/equity ratio. If a certain amount

of money is left after all forms of business expenses then the corporate houses

distribute that money among its shareholders as dividends.

The companies that follow a residual dividend policy pay dividends only if other

satisfactory opportunities and sources of investment of funds are not available. The

main advantage of a residual dividend policy is that it reduces to the issues of new

stocks and flotation costs. The drawback of this policy mainly lies in the facts that

such a policy does not have any specific target clients. Moreover, it involves the risk

of variable dividends. This policy helps to set a target payout.

Before opting for the policy of residual dividend, the earnings that need to be

retained to back up the capital budget have to be calculated. Then, the earnings that

are left can be paid out in the form of dividends to the shareholders. Thus, the issue of

- 43 -

new equities gets considerably reduced and this in turn leads to reduction in signaling

and flotation costs. The amount payable as dividend fluctuates heavily if this policy is

practiced. When the total value of productive investments is in excess of the total

value of retained earnings and sustainable debt, the companies feel the urge to exploit

the opportunities thus created to postpone a few investment schemes.

Calculation of Residual dividend policy:

Let's suppose that a company named CBC has recently earned $1,000 and has a strict

policy to maintain a debt/equity ratio of 0.5 (one part debt to every two parts of

equity). Now, suppose this company has a project with a capital requirement of $900.

In order to maintain the debt/equity ratio of 0.5, CBC would have to pay for one-third

of this project by using debt ($300) and two-thirds ($600) by using equity. In other

words, the company would have to borrow $300 and use $600 of its equity to

maintain the 0.5 ratio, leaving a residual amount of $400 ($1,000 - $600) for

dividends. On the other hand, if the project had a capital requirement of $1,500, the

debt requirement would be $500 and the equity requirement would be $1,000, leaving

zero ($1,000 - $1,000) for dividends. If any project required an equity portion that

was greater than the company's available levels, the company would issue new stock

Arguments against Dividends

First, some financial analysts feel that the consideration of a dividend policy is

irrelevant because investors have the ability to create "homemade" dividends. These

analysts claim that this income is achieved by individuals adjusting their personal

portfolios to reflect their own preferences. For example, investors looking for a steady

stream of income are more likely to invest in bonds (in which interest payments don't

change), rather than a dividend-paying stock (in which value can fluctuate). Because

their interest payments won't change, those who own bonds don't care about a

particular company's dividend policy.

The second argument claims that little to no dividend payout is more favorable for

- 44 -

investors. Supporters of this policy point out that taxation on a dividend are higher

than on a capital gain. The argument against dividends is based on the belief that a

firm that reinvests funds (rather than paying them out as dividends) will increase the

value of the firm as a whole and consequently increase the market value of the stock.

According to the proponents of the no dividend policy, a company's alternatives to

paying out excess cash as dividends are the following: undertaking more projects,

repurchasing the company's own shares, acquiring new companies and profitable

assets, and reinvesting in financial assets

Arguments for Dividends

In opposition to these two arguments is the idea that a high dividend payout is

important for investors because dividends provide certainty about the company's

financial well-being; dividends are also attractive for investors looking to secure

current income. In addition, there are many examples of how the decrease and

increase of a dividend distribution can affect the price of a security. Companies that

have a long-standing history of stable dividend payouts would be negatively affected

by lowering or omitting dividend distributions; these companies would be positively

affected by increasing dividend payouts or making additional payouts of the same

dividends. Furthermore, companies without a dividend history are generally viewed

favorably when they declare new dividends.

The residual dividend policy is more suitable for the government concerns because

they mainly aim for creation of value and maximization of wealth and therefore they

have to make use of every value added investment opportunity that comes on their

way. A little change in the basic postulates of the policy usually occurs when it is

applied to the government sector because it takes into its purview the government's

liking for dividends rather than capital gains.

The dividend discount model is used for the purpose of equity valuation. There are

different types of dividend discount model and all these models are very useful. The

usefulness of the DDM (dividend discount model) depends on the application of the

same.

- 45 -

A sensitivity analysis of the dividend discount model is very necessary because the

model itself is highly sensitive towards the presumptions regarding the growth and

discount rates.

The investor can be benefited by the sensitivity analysis because this particular

analysis can provide an idea about how various presumptions can create different

values. The dividend discount model compels the investor to think about different

situations regarding the market price of the stock.

The dividend discount model is used by huge number of professionals because the

model is able to illustrate the difference between reality and theories through different

examples. But at the same time it should also be remembered that there are some

important factors like the realistic transition phases and some others, which are

missing from the DDM.

The DDM needs various data to bring out the value of an equity. DPS(1), which

represents the amount of expected dividend, is very important for DDM. The growth

rate in dividend is also an important factor in the use of dividend discount model.

Another important data is 'Ks'. 'Ks' represents the expected rate of return and this can

be estimated through the following formula:

Risk-free rate + (market risk premium)* Beta

There are several types of dividend discount model. Following are the two most

preferred types of DDM:

Stable Model: According to this model, value of stock is equal to DPS(1) / Ks

- g. This model is appropriate for the firms with long term steady growth.

These types of firms pretend to grow simultaneously with the long term

nominal development rate of the economy.

Two-Stage Model: This particular model tries to bring out the difference

between the theory and the reality. It simply pretends that the company would

- 46 -

go through several good and bad periods. According to this model, the

company that is going through a high-growth period is bound to face a decline

in the growth rate. After that downfall the company is expected to experience

a stable growth phase.

IRRELEVANCE OF DIVIDEDS:

MODIGLIANI AND MILLER MODEL:

The crux of the argument supporting the irrelevance of dividends to Valuation is that

the dividend policy of a firm is a part of its financing decision. As a part of the

financing decision, the dividend policy of the firm is a residual decision and dividends

are passive residuals

Crux of the Argument:

The crux of the MM position on the irrelevance of dividend is the arbitrage

argument. The arbitrage process, involves a swathing and balancing operation. In

other words, arbitrage refers to entering simultaneously y into two transactions here

are the acts of paying out dividends and raising external funds either through the sale

of new shares or raising additional loans-to finance investment programmes. Assume

that a firm has some investment opportunity.

Given its investment decision, the firm has two alternatives: (i) it can passiceretain is

earnings to finance the investment programmed; (ii) or distribute the earnings to he

shareholders as dividend and raise an equal amount externally through the sale of new

shares/bonds for the purpose. If the firm selects the second alternative, arbitrage

process is involved, in that payment of dividends is associated with raising funds

through other means of financing, the effect of dividend payment on

Shareholders’ wealth will be exactly offset by the effect of raising additional

share capital.

- 47 -

When dividends are paid to the shareholders, the market price of the shares

will decrease. What the investors as a result of increased dividends gain will be

neutralized completely vie the reduction in the terminal value of the shares. The

market price before and after the payment of dividend would be identical. The

investors according to Modigliani and Miller, would, therefore, be indifferent between

dividend and retention of earnings. Since the shareholders are indifferent, the wealth

would not be affect by current and future dividend decisions of the firm. It would

depend entirely upon the expected future earnings of the firm.

There would be no difference to the validity of the mm premise, if external funds

were raised in the form of debt instead of equity capital. This is because of their

indifference between debt and equity witty retest to leverage. The cost of capital is

independent of leverage and the cost of debt is the same as the real cost of equity.

Those investors are indifferent between dividend and retained earnings imply that

the dividend decision is irrelevant. The arbitrage process also implies that the total

market value plus current dividends of two firms, which are alike in all respects

except D/P ratio, will be identical. The individual shareholder can retain and invest

his own earnings as we;; as the firm would. With dividends being irrelevant, a firm’s

cost of capital would be independent of its D/P ratio.

Finally, the arbitrage process will ensure that-under conditions of uncertainty also the

dividend policy would be irrelevant. When two firms are similar in respect of

business risk, prospective future earnings and investment policies, the market price of

their shares must be the same. This, mm argues, is wealth to less wealth. Differences

in current and future dividend policies cannot affect the market value of the two firms

as the present value of prospective dividends plus terminal value is the same.

A Critique:

Modigliani and Miller argue that the dividend decision of the firm is irrelevant

in the sense that the vale the firm is independent of it. The crux of their argument is

- 48 -

that the investors are indifferent between dividend and retention of earnings. This is

mainly because of the balancing natures internal financing (retained earnings) and

external financing (rising of funds externally) consequent upon distribution earnings

to finance investment program’s. Whether the mm hypotheses provides a satisfactory

framework for the theoretical relationship between dividend decision and valuation

will depend, in the ultimate analysis on whether external and internal financing really

balance each other. This in turn, depends upon the critical assumptions stipulated by

them. Their conclusions, it may be noted, under the restrictive assumptions, a

logically consistent and intuitively appealing. But these assumptions are unrealistic

and untenable in practice As a result, the conclusion that dividend payment and other

methods of financing exactly offset each other and, hence, the irrelevance of

dividends is not a practical proposition’ it is merely of theoretical relevance.

The validity of the MM Approach is open to question on two Coutts:(i)

Imperfection of capital market, and (ii) Resolution of uncertainty

Market Imperfection: Modigliani and Miller assume that capital markets

Are perfect. This implies that there are no taxes; flotation costs do not exist and there

is absence of transaction costs. These assumptions ate untenable in actual situations.

A. Tax Effect:

An assumption of the mm hypothesis is that there are no taxes. It implies that

retention of earnings (internal financing) and payment of dividends (external

financing) are, from the viewpoint of law treatment, on an equal footing the investors

would find both forms of financing equally desirable. The tax liability of the

investors, broadly speaking, is of two types: (i) tax on dividend income, and (ii0

capital gains. While the first type of tax is payable by the investors when the firm

pays dividends, the capital gains tax is related to retention of earnings. From an

operational viewpoint, capital gains tax is (i) lower thebe the tax or dividend income

and (ii) it becomes payable only sheen shares are actually sold, than is, it is a differed

till the actual sale of the shares. The types of taxes, MM position would imply

otherwise. The different tax treatment of div dined and capital gains means that with

- 49 -

the retention of earnings the shareholders. For example, a firm pays dividends to the

shareholders out of the retained earnings; to finance its investment program’s it issues

rights shares. The shareholders would have to pay tax on the dividend income at rates

appropriate to their income bracket. Subsequently, they would purchase the shares of