dnb bank asa analyst contacts 09... · banking, notably through the 2015 launch of the successful...

TRANSCRIPT

FINANCIAL INSTITUTIONS

ISSUER IN-DEPTH12 September 2019

RATINGSDomicile Norway

Leng Term CRR Aa2

Type LT Counterparty RiskRating - Fgn Curr

Outlook Not Assigned

Long Term Debt Aa2

Type Senior Unsecured -Fgn Curr

Type LTBank Deposits -Fgn Curr

Outlook StableBaseline CreditAssessment

A3

Source: Moody's Investors Service

Analyst Contacts

Roland Auquier [email protected]

Malika Takhtayeva +44.20.7772.8662Associate [email protected]

Simon Ainsworth +44 207 772 5347Associate Managing [email protected]

Sean Marion +44.20.7772.1056MD-Financial [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

DNB Bank ASADNB on track to meet profitability targets as it shifts itsbusiness model and extends its lead in digital innovation

We expect Norwegian lender DNB Bank ASA to achieve its profitability targets over theoutlook period, helped by its strong domestic franchise, as well as a strategic transformationdesigned to diversify its income sources and extend its lead in the digitalization of bankingservices. We regard the bank's reorganization, which includes increased emphasis on feegenerating businesses such as investment banking and asset management, as credit positive.

DNB extends digital innovation beyond retail market. As part of its strategic overhaul,DBN is extending its digital expertise to corporate banking, having launched DBN Puls, anapp for small business managers, in November 2018. The bank has also partnered withtreasury management software firm TreasuryXpress to enhance its treasury and cashmanagement services for international corporate clients. DNB, Norway's biggest bank witha 28% share of the retail lending market, is already a leader in the digitalization of retailbanking, notably through the 2015 launch of the successful mobile payment app, Vipps.

New emphasis on capital-light, fee-based business. DNB is also building up itsinvestment banking and asset management divisions as part of its reorganization. Theseactivities are less capital-intensive than traditional lending, and also generate fee revenue,reducing DNB's dependence on lending income. At the same time, DNB is taking a moreselective approach to international corporate lending, while continuing to cut its exposure tothe oil and offshore sector, a source of material loan losses in recent years.

Strong underlying profitability, despite high IT and compliance-related costs.We expect DNB to achieve its targeted 12% return on equity (ROE) and cost-to-incomeratio of 40% over the outlook period. Our view reflects profitable lending growth at thebank's domestic franchise, enhanced by controlled cost increases and more optimal use ofcapital, thanks in part to the transformation programme. While DNB's 12% ROE target isbelow some of its Nordic peers, this reflects higher local capital requirements. DNB's CET1requirement is set to increase further following the implementation of the European Union'sCRR/CRD IV capital regulation in the second half of the year.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

DNB extends digital innovation beyond retail marketDNB, Norway's largest lender, has been a front-runner in the European banking industry's digital journey. This is partly becauseNorwegians have a strong affinity for technology, and were early adopters of online banking services. Norway ranked second in Europefor online banking usage as of 2018 (see Exhibit 1). Less than 5% of the country's payment transactions were done using cash in 2018.

Exhibit 1

Norway had the second highest rate of online banking use among 16-74 year olds in Europe in 2018Online banking usage

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

% o

f In

div

iduals

Source: European Commission's Digital Scoreboard

DNB's tech-savvy approach is illustrated by its pre-emptive launch of the Vipps mobile payment app in May 2015, three years beforetech rivals Apple Pay and Google Pay became available to Norwegian consumers. To ensure large-scale adoption, DNB made Vippsavailable to the customers of all Norwegian banks from launch. In early 2017, it sold stakes in the platform to over 100 Norwegianlenders, retaining a 52% holding. The sale convinced some participating banks to shelve their own mobile payment offerings in favourof Vipps, which is now used by two-thirds of the Norwegian population.

DNB's early and large-scale adoption of digital banking channels, including Vipps, allowed it to close 70% of its branch networkin 2015-18, despite its continued expansion in the mortgage market. While branches are no longer present in numerous urbancommunities, including relatively large cities such as Kirkenes, Hammerfest, Fauske and Narvik, DNB has managed to retain itscustomer base given the shift in consumer behaviour.

Exhibit 2

Usage of DNB's digital platforms has risen rapidly...Annual visits to DNB's digital platform, in millions

Exhibit 3

...leading to a contraction of its branch networkNumber of DNB branches

73 83 85 86 83 92 83 80 76

12

949

113156

200244

281

0

50

100

150

200

250

300

350

400

2010 2011 2012 2013 2014 2015 2016 2017 2018

Desktop Mobile

Source: Company reports

198187

156141

116

57 57 56

0

50

100

150

200

250

2011 2012 2013 2014 2015 2016 2017 2018

Source: Company reports

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 12 September 2019 DNB Bank ASA: DNB on track to meet profitability targets as it shifts its business model and extends its lead in digital innovation

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

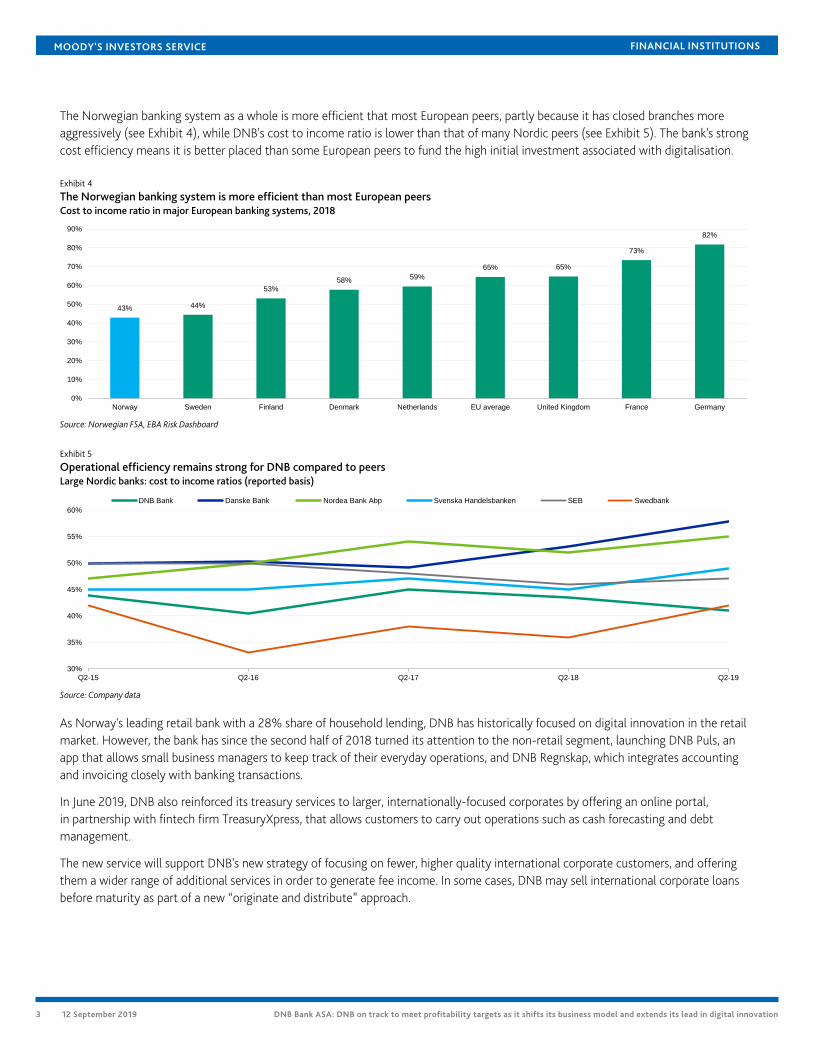

The Norwegian banking system as a whole is more efficient that most European peers, partly because it has closed branches moreaggressively (see Exhibit 4), while DNB's cost to income ratio is lower than that of many Nordic peers (see Exhibit 5). The bank's strongcost efficiency means it is better placed than some European peers to fund the high initial investment associated with digitalisation.

Exhibit 4

The Norwegian banking system is more efficient than most European peersCost to income ratio in major European banking systems, 2018

43% 44%

53%58% 59%

65% 65%

73%

82%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Norway Sweden Finland Denmark Netherlands EU average United Kingdom France Germany

Source: Norwegian FSA, EBA Risk Dashboard

Exhibit 5

Operational efficiency remains strong for DNB compared to peersLarge Nordic banks: cost to income ratios (reported basis)

30%

35%

40%

45%

50%

55%

60%

Q2-15 Q2-16 Q2-17 Q2-18 Q2-19

DNB Bank Danske Bank Nordea Bank Abp Svenska Handelsbanken SEB Swedbank

Source: Company data

As Norway's leading retail bank with a 28% share of household lending, DNB has historically focused on digital innovation in the retailmarket. However, the bank has since the second half of 2018 turned its attention to the non-retail segment, launching DNB Puls, anapp that allows small business managers to keep track of their everyday operations, and DNB Regnskap, which integrates accountingand invoicing closely with banking transactions.

In June 2019, DNB also reinforced its treasury services to larger, internationally-focused corporates by offering an online portal,in partnership with fintech firm TreasuryXpress, that allows customers to carry out operations such as cash forecasting and debtmanagement.

The new service will support DNB's new strategy of focusing on fewer, higher quality international corporate customers, and offeringthem a wider range of additional services in order to generate fee income. In some cases, DNB may sell international corporate loansbefore maturity as part of a new “originate and distribute” approach.

3 12 September 2019 DNB Bank ASA: DNB on track to meet profitability targets as it shifts its business model and extends its lead in digital innovation

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

We view DNB's continued focus on digital innovation as warranted, given the increasing competition from technology companies: inthe digital era incumbent traditional banks must deliver innovation in product design to thrive, while ceding ground to competitors inselect markets where necessary.

New emphasis on capital-light, fee-based businessNorway's strong operating environment - given the oil-rich country's economic resilience and household sector's strong abilityto service debt - and DNB's sizeable domestic franchise - with Norwegian borrowers accounting for 70% of the bank's loans as ofDecember 2018 - are key positive credit drivers. As of 31 December 2018, DNB had 2.1 million retail customers, 221,000 corporatecustomers, 1.3 million internet bank users, and 227,000 non-life policyholders across Norway. The bank's robust pricing power and highdomestic brand recognition are further strengths. Taken together, these factors support DBN's profitability.

However, while DNB's core earnings are resilient, the bank's revenues are more heavily tilted towards lending income than those ofits main competitors (see Exhibit 6). The bank is therefore refocusing on fee-generating activities that are less capital-intensive thantraditional lending, such as investment banking and asset management. DNB is also Norway's largest asset management company withapproximately 475,000 mutual fund customers in Norway, and 168 institutional clients in Norway and Sweden. The bank also ownsDNB Markets, Norway's leading investment firm.

Exhibit 6

DNB is more dependent on lending income than large Nordic peersLarge Nordic banks' revenue mix, Q2 2019

0%

20%

40%

60%

80%

100%

120%

DNB Bank Danske Bank Nordea Bank Abp Svenska Handelsbanken SEB Swedbank

Net interest income Fee and Commission income Net gains on financial instruments Other income

Source: Company reports

DNB's new, more selective approach to international corporate lending will also moderate its dependence on lending income. Theinternational portfolio had average loans of NOK441.8 billion at the end of June 2019, down 10% from year-end 2017. The declinelargely reflects DNB's efforts to cut its exposure to the oil and offshore sectors, which generated material loan losses following a sharpfall in oil prices in mid-2014. The bank set up a new non-core division in January 2018 to accelerate the rebalancing of shipping and oilrelated exposures, enabling the rest of the group to focus on profitable new business.

We view DNB's total loan portfolio as well diversified. Retail lending (mainly residential mortgages) accounted for 54% of exposuresat default (EAD) at end-June 2019, with the remainder spread across industries. Shipping and commercial real estate (CRE), whichwe typically view as relatively volatile, accounted for 3.2% and 9% of EAD respectively. While exposure to the riskier oil, gas, oilfieldservices and offshore sectors has fallen, it still accounted for 5.1% of EAD at end-June 2019.

4 12 September 2019 DNB Bank ASA: DNB on track to meet profitability targets as it shifts its business model and extends its lead in digital innovation

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Exhibit 7

Oil - Related (Oil & Gas and Offshore) and Shipping Portfoliorepresents 8.3% of Total Customer EaD as of June 2019...

Exhibit 8

...down from 15.3% in September 2015

Oil & Gas3.2%

Offshore1.9%

Shipping portfolio3.2%

Other Customer EaD91.7%

Source: Company reports

Oil-related portfolio8.4%

Shipping portfolio6.9%

Other Customer EaD84.7%

Source: Company reports

DNB's problem loans accounted for 1.6% of gross loans at end-June 2019, down from 1.8% at year-end 2018, and from 2.6% two yearsearlier. The improvement largely reflects a better performance from the bank's oil and offshore portfolio. DNB's asset risk compares wellwith that of most European peers (see Exhibit 9).

Exhibit 9

DNB has strong asset risk metrics compared to most European systemsDNB's problem loan raio (%) vs. Norwegian and Euro area average

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

2011 2012 2013 2014 2015 2016 2017 2018

DNB Norway Euro Area

Asset weighted average for rated banks in Eurozone and NorwaySource: Moody's Banking Financial Metrics

DNB remains on track to meet its profitability targetsWe expect DNB to achieve its targeted 12% return on equity (ROE) and cost-to-income ratio of 40% over the outlook period. Ourview reflects profitable lending growth generated by the bank's domestic franchise, enhanced by controlled cost increase and moreoptimal use of capital.

We expect that volumes in the personal customer and small business segments will continue to rise, which, together with marginexpansion, will increase DNB's net interest income by more than 4% CAGR over the next 12-18 months. We nonetheless caution thatincreased competition on the lending side will limit the benefits from expected rate hikes, as the bank will need to pass more on to thedepositors than in recent months.

At the same time, tight cost controls should limit operating expense growth to 2% CAGR, despite an anticipated increase in technologyand compliance-related spending. We also expect a moderate pick up of impairments, even as credit conditions remain benign duringthe period.

5 12 September 2019 DNB Bank ASA: DNB on track to meet profitability targets as it shifts its business model and extends its lead in digital innovation

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

The anticipated improvements partly reflect the impact of the strategic overhaul, which will encourage more optimal use of capitalthanks to the switch towards less capital intensive activity, as well as an increased flow of net fee and commission income.

DNB's 12.0% return on equity (ROE) target is well below some of its Nordic peers (e.g. 15% ROE target for Swedbank). This reflectshigher local capital requirements, which have forced Norwegian banks to bolster their capital bases earlier than scheduled underinternational rules. DNB's leverage ratio of 7.1% as of 30 June 2019 compares well against international peers and is the highest amongthe largest Nordic banks (see Exhibit 10).

Exhibit 10

DNB reported the highest leverage ratio among major Nordic peers in Q2 2019Large Nordic banks: Leverage ratios (reported basis)

7.1%

4.4%

5.0%

4.5% 4.6%4.8%

3.50%3.75%4.00%4.25%4.50%4.75%5.00%5.25%5.50%5.75%6.00%6.25%6.50%6.75%7.00%7.25%7.50%

Q2-19 Q2-19 Q2-19 Q2-19 Q2-19 Q2-19

DNB Bank Danske Bank Nordea Bank Abp Svenska Handelsbanken SEB Swedbank

Source: Company reports, Moody's calculations

Norway's Ministry of Finance said in June 2019 that DNB's CET1 requirement will increase from 15.8% to 16.6%, once the EuropeanUnion's CRR/CRD IV capital regulation takes effect in the second half of the year. The bank will also have to comply with a highercountercyclical buffer of around 40 basis points.

We remain comfortable with the bank's current capital levels, and estimate that its current capital generation of 40 basis points perquarter will leave some room for growth. DNB reported a second-quarter CET1 ratio, excluding transitional effects, of 17.3% at end-June 2019.

Strong sustained capital generation and an anticipated CET1 ratio above 18% throughout our outlook period should support the bank'spolicy of maintaining a minimum 50% dividend payout ratio.

Exhibit 11

DNB's regulatory capitalisation remains one of the strongest in the Nordic regionLarge Nordic banks: Common Equity Tier 1 ratios

15.5%

1.0%

16.5%

13.7%

2.9%

16.6%

13.3%15.1%

1.5%

2.0%14.8%

17.1%

14.7% 14.6%

1.9% 1.5%

16.6%16.1%

10.0%

12.5%

15.0%

17.5%

20.0%

22.5%

25.0%

27.5%

Q2-19 Q2-19 Q2-19 Q2 -19 Q2 -19 Q2 -19

DNB Bank Danske Bank Nordea Bank Abp Svenska Handelsbanken SEB Swedbank

Minimum CET1 requirement Buffer Reported CET1 Series13

Following Nordea's move to Finland, and due to the uncertainty regarding its future capital requirements, the bank has voluntarily committed to comply with nominal capital requirementsfrom the 2018 SREP as 13.3% until the ECB has issued its SREP decision in 2019.Source: Company Data

6 12 September 2019 DNB Bank ASA: DNB on track to meet profitability targets as it shifts its business model and extends its lead in digital innovation

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Moody’s related publications

» Banking System Outlook - Norway: High capital buffers balanced by margin pressure underpin our stable outlook, 5 September2019

» Credit Opinion: DNB Bank ASA - Update to credit analysis following rating outlook change to stable from negative, 11 June 2019

» Cross-Sector – Norway: Norway’s proposed systemic risk buffer and risk weight floors are credit positive for banks and coveredbonds, 1 July 2019

» Annual credit analysis: Government of Norway – Aaa stable, 28 June 2019

» Banks – Norway: Loss-absorbing debt issuance to benefit large banks' senior creditors, 4 June 2019

To access any of these reports, click on the entry above. Note that these references are current as of the date of publication of thisreport and that more recent reports may be available. All research may not be available to all clients.

7 12 September 2019 DNB Bank ASA: DNB on track to meet profitability targets as it shifts its business model and extends its lead in digital innovation

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

© 2019 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEEMOODY’S RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’SRATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDITRATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAYALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDITRATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONSARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONSCOMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONSWITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDERCONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSESAND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDITRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for ratings opinions and services rendered by it fees ranging from $1,000 to approximately $2,700,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as tothe creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for ratings opinions and services rendered by it feesranging from JPY125,000 to approximately JPY250,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1174658

8 12 September 2019 DNB Bank ASA: DNB on track to meet profitability targets as it shifts its business model and extends its lead in digital innovation

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

9 12 September 2019 DNB Bank ASA: DNB on track to meet profitability targets as it shifts its business model and extends its lead in digital innovation