dnb bank dnb boligkreditt · july 2017 dnb bank dnb boligkreditt . 2 content ... 2006 2008 2010...

TRANSCRIPT

July 2017

DNB Bank

DNB Boligkreditt

2

Content

• DNB – A Brief Overview

• The Norwegian Economy

• Financial Targets, Performance and Capital

• Loan Book and Asset quality

• Funding

• Appendix: • Cover Pool Portfolio Information and LCR eligibility • Digitalization • The Norwegian Mortgage Market • Capital and Tier 1 • Additional slides – Financial Performance and Other information

3

DNB – A Brief Overview

4

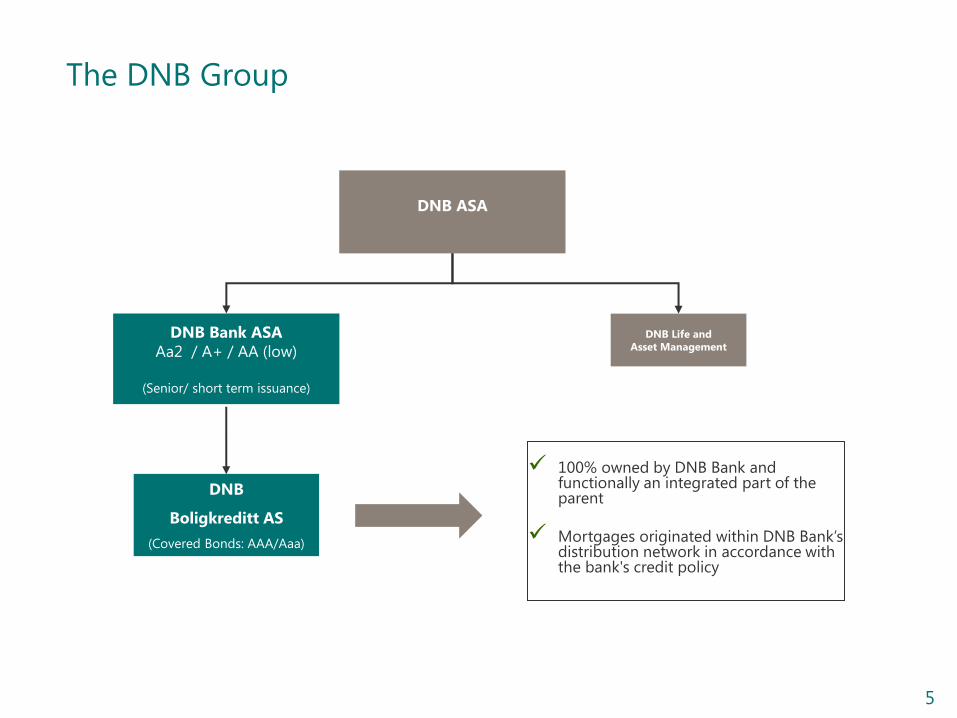

DNB - Norway’s Leading Financial Services Group

• Approximately 30 % market share in Norway

• 34 % owned by the Norwegian Government

• Credit Ratings: • Moody's: Aa2* (negative)

• S&P: A+ (stable)

• DBRS: AA (low) (stable)

* Upgraded to Aa2 with negative outlook 16 March 2016

5

The DNB Group

100% owned by DNB Bank and functionally an integrated part of the parent

Mortgages originated within DNB Bank’s distribution network in accordance with the bank's credit policy

DNB Bank ASA

Aa2 / A+ / AA (low)

(Senior/ short term issuance)

DNB Life and

Asset Management

DNB ASA

DNB

Boligkreditt AS

(Covered Bonds: AAA/Aaa)

6

The Norwegian Economy

7

Still a Solid Norwegian Economy

Source: 1) OECD Economic Outlook No. 101, June 2017

2) Ministry of Finance (National Budget 2017)

3) DNB Markets Economic Outlook April 2017

2016 2017

Budget surplus 1) 3.1 % 4.1 %

Oil fund 2) ~ EUR 826 bn ~ EUR 845 bn

Unemployment 3) 4.7 % 4.4 %

GDP growth 3) + 0.9 % + 1.6 %

Central Bank Rate 3) 0.5 % 0.5 %

8

Government Finances are Still Rock-Solid

Annual budget deficit/surplus forecast for 20171) General government net financial liabilities1)

As per cent of nominal GDP 2017

1) Source: OECD Economic Outlook No. 101, June 2017

-300

-250

-200

-150

-100

-50

0

50

100

150

200

Iceland0.9

Norway+4.1

Sweden+0.9

Finland-1.7

Poland-2.9Germany

0.7

Denmark-0.8

Ireland-0.5

Slovakia-1.2Austria

-1.0

Netherlands1.1

Belgium-1.9

United Kingdom-3.0

Luxembourg+0.7

France-3.0

Spain-3.1Portugal

-1.5

Italy-2.1

Greece-0.2

Slovenia-1.0

Hungary-2.6

Estonia-0.4

Czech R.

0.4

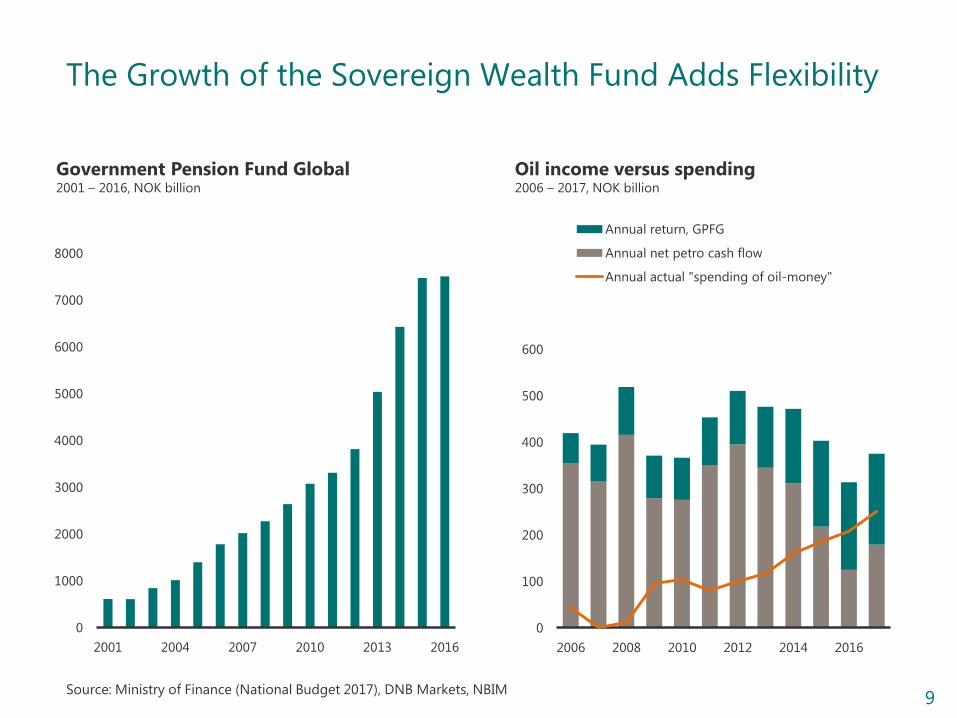

9

0

100

200

300

400

500

600

2006 2008 2010 2012 2014 2016

Annual return, GPFG

Annual net petro cash flow

Annual actual "spending of oil-money"

Government Pension Fund Global 2001 – 2016, NOK billion

Oil income versus spending 2006 – 2017, NOK billion

0

1000

2000

3000

4000

5000

6000

7000

8000

2001 2004 2007 2010 2013 2016

Source: Ministry of Finance (National Budget 2017), DNB Markets, NBIM

The Growth of the Sovereign Wealth Fund Adds Flexibility

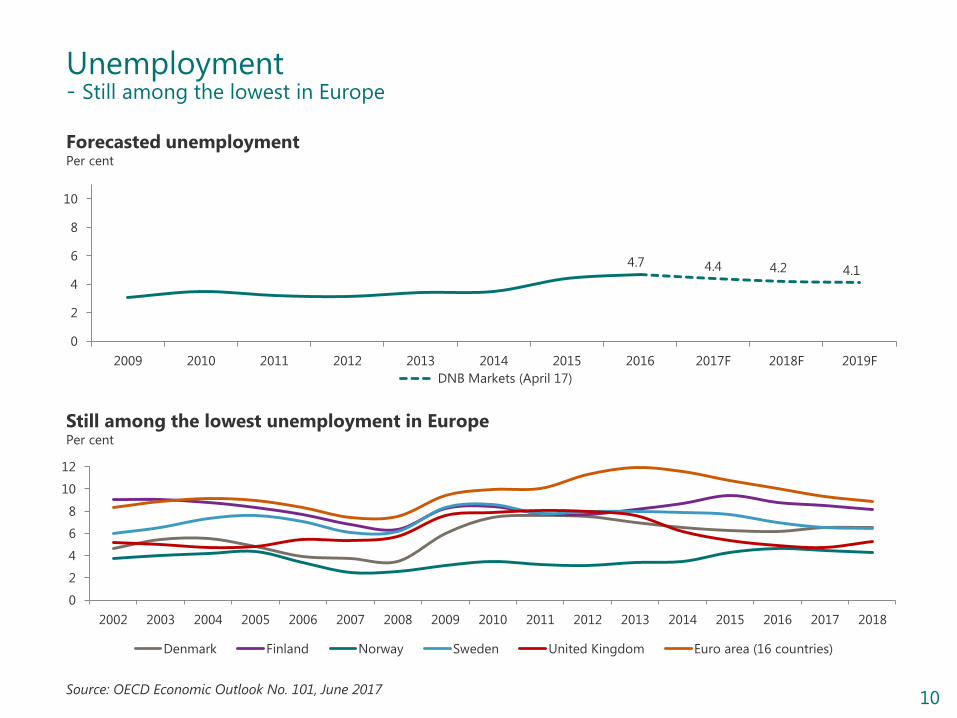

10

Forecasted unemployment Per cent

4.7 4.4 4.2 4.1

0

2

4

6

8

10

2009 2010 2011 2012 2013 2014 2015 2016 2017F 2018F 2019F

DNB Markets (April 17)

Still among the lowest unemployment in Europe Per cent

Source: OECD Economic Outlook No. 101, June 2017

Unemployment - Still among the lowest in Europe

0

2

4

6

8

10

12

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Denmark Finland Norway Sweden United Kingdom Euro area (16 countries)

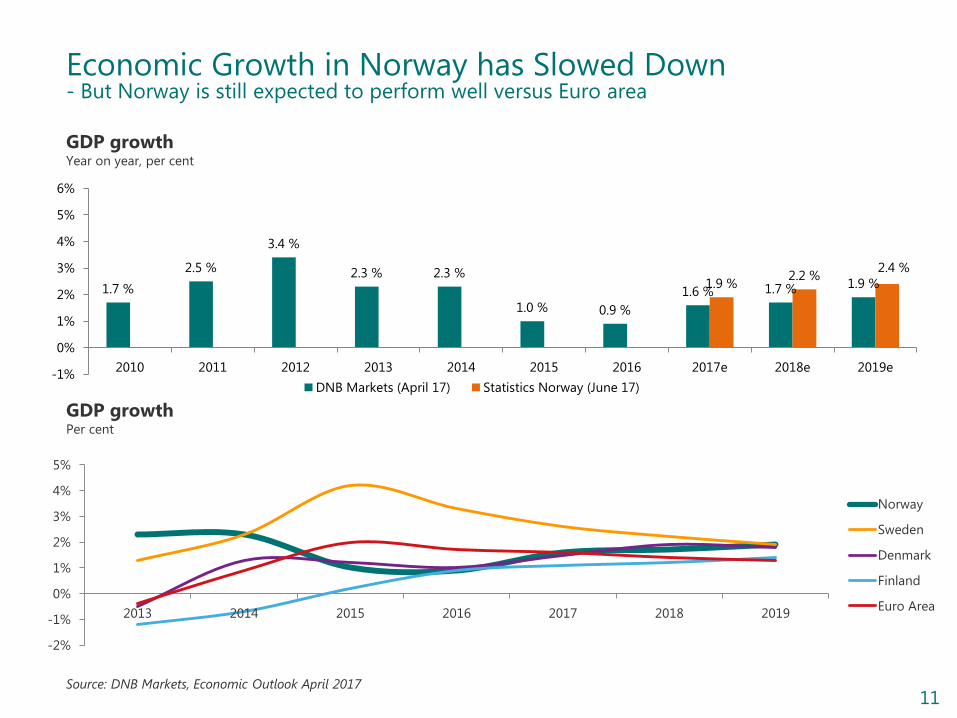

11

Economic Growth in Norway has Slowed Down - But Norway is still expected to perform well versus Euro area

1.7 %

2.5 %

3.4 %

2.3 % 2.3 %

1.0 % 0.9 %

1.6 % 1.7 % 1.9 % 1.9 % 2.2 %

2.4 %

-1%

0%

1%

2%

3%

4%

5%

6%

2010 2011 2012 2013 2014 2015 2016 2017e 2018e 2019e

DNB Markets (April 17) Statistics Norway (June 17)

GDP growth Year on year, per cent

-2%

-1%

0%

1%

2%

3%

4%

5%

2013 2014 2015 2016 2017 2018 2019

Norway

Sweden

Denmark

Finland

Euro Area

GDP growth Per cent

Source: DNB Markets, Economic Outlook April 2017

12

0

1

2

3

4

5

6

7

8

9

10

0

50

100

150

200

250

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Constant 2014 prices (lha) Share of GDP (rha)

Oil Investments are Stabilising at a High Level – Lower break-even price ensures a competitive continental shelf

Source: Thomson Datastream, DNB Markets Source: Rystad Energy, Statoil, Wall Street Journal

Break-even price: Sanctioned vs April 2017 USD per barrel, Brent Blend

Petroleum investments in Norway NOK billion, share of GDP in per cent

March 2016 September 2016 Sanctioned

Johan Sverdrup Johan Castberg

80

38

52

35

45

3035

25

April 2017

13

Financial Targets, Performance and Capital

14

Financial Ambitions for 2017 - 2019

CET1 ratio ~ 16.0 per cent 1)

Requirement including

management buffer

Cash dividend combined

with share buy-back

programme

ROE > 12 per cent

Overriding target towards

2019

C/I ratio < 40 per cent

Key performance indicator

Payout ratio > 50 per cent

1) Based on transitional rules including increased counter-cyclical buffer requirements in Singapore, Sweden and Norway.

15

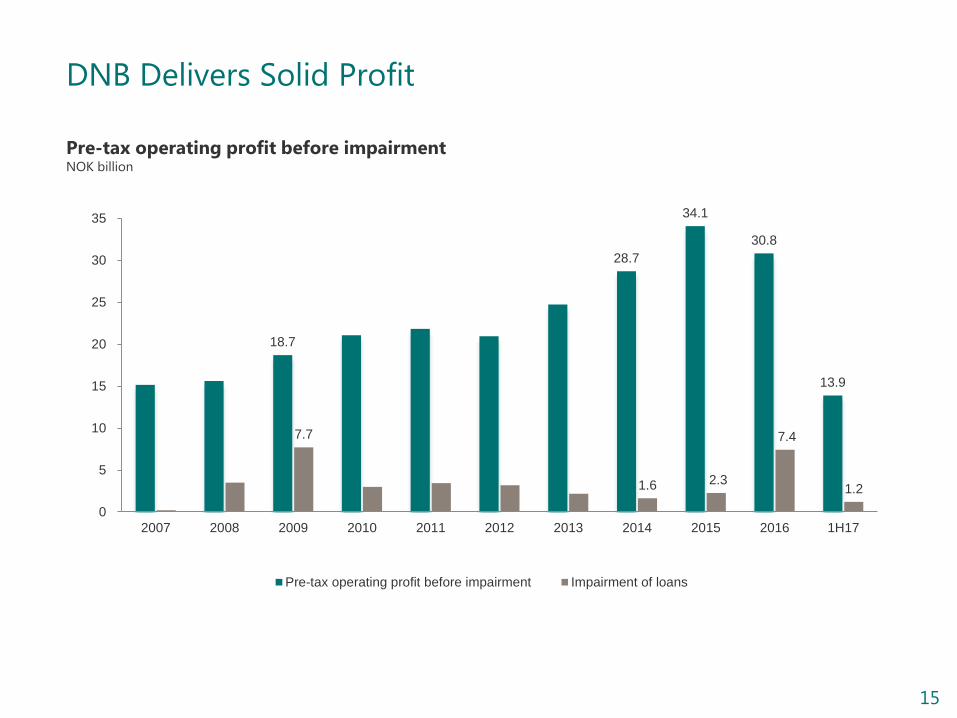

DNB Delivers Solid Profit

18.7

28.7

34.1

30.8

13.9

7.7

1.6 2.3

7.4

1.2

0

5

10

15

20

25

30

35

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 1H17

Pre-tax operating profit before impairment Impairment of loans

Pre-tax operating profit before impairment NOK billion

16

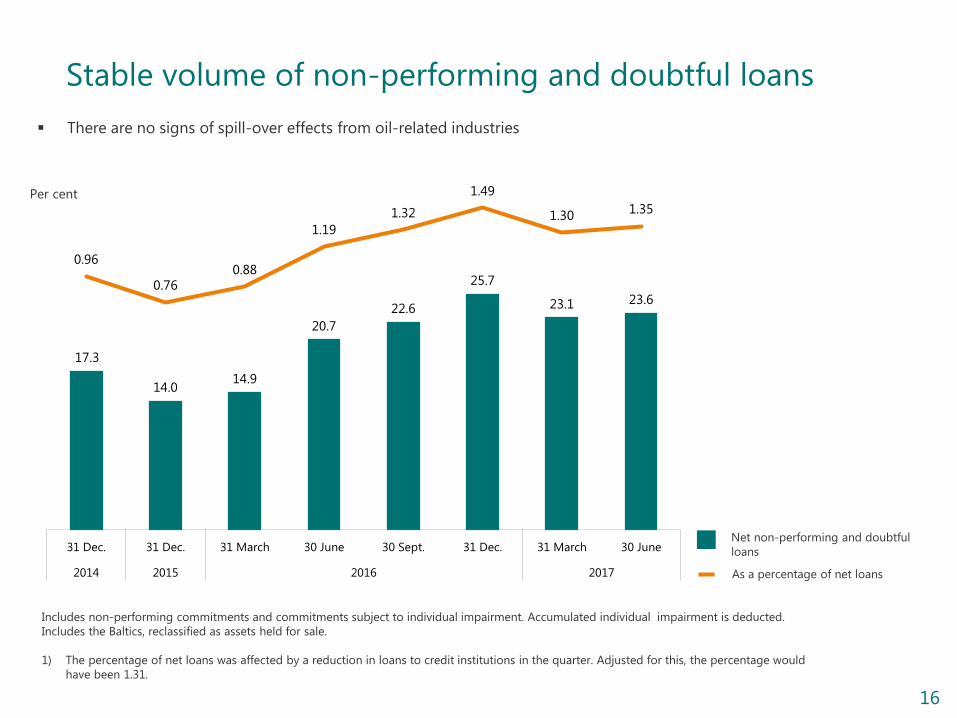

Stable volume of non-performing and doubtful loans

17.3

14.0 14.9

20.7

22.6

25.7

23.1 23.6

0.96

0.76 0.88

1.19

1.32

1.49

1.30 1.35

31 Dec. 31 Dec. 31 March 30 June 30 Sept. 31 Dec. 31 March 30 June

2014 2015 2016 2017

Includes non-performing commitments and commitments subject to individual impairment. Accumulated individual impairment is deducted.

Includes the Baltics, reclassified as assets held for sale.

1) The percentage of net loans was affected by a reduction in loans to credit institutions in the quarter. Adjusted for this, the percentage would

have been 1.31.

Per cent

Net non-performing and doubtful

loans

As a percentage of net loans

There are no signs of spill-over effects from oil-related industries

17

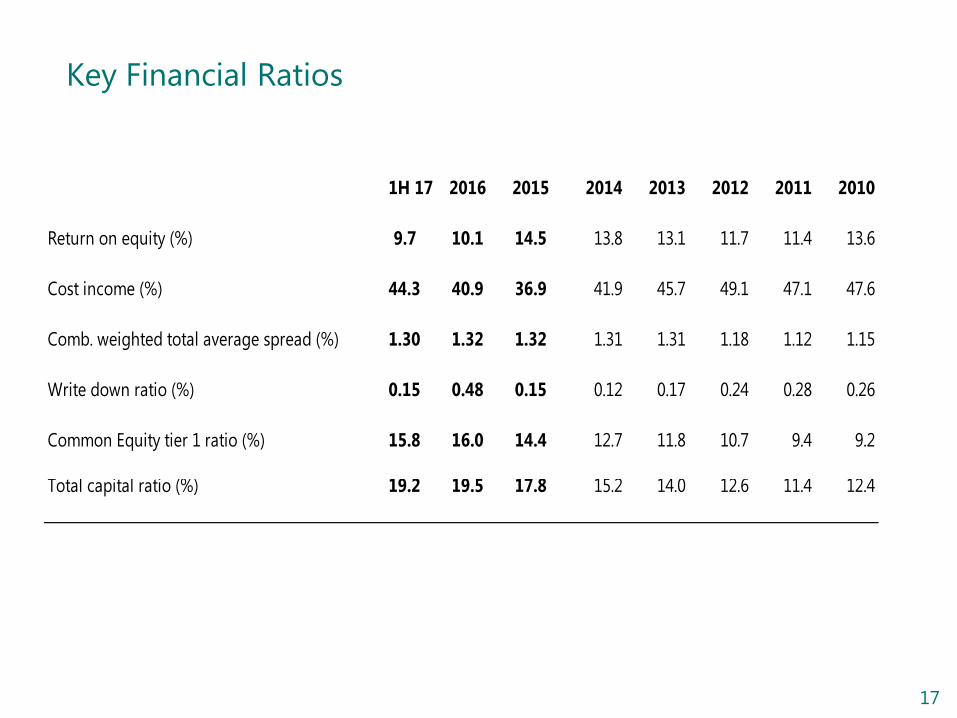

Key Financial Ratios

1H 17 2016 2015 2014 2013 2012 2011 2010

Return on equity (%) 9.7 10.1 14.5 13.8 13.1 11.7 11.4 13.6

Cost income (%) 44.3 40.9 36.9 41.9 45.7 49.1 47.1 47.6

Comb. weighted total average spread (%) 1.30 1.32 1.32 1.31 1.31 1.18 1.12 1.15

Write down ratio (%) 0.15 0.48 0.15 0.12 0.17 0.24 0.28 0.26

Common Equity tier 1 ratio (%) 15.8 16.0 14.4 12.7 11.8 10.7 9.4 9.2

Total capital ratio (%) 19.2 19.5 17.8 15.2 14.0 12.6 11.4 12.4

18

DNB CET1 Capital Generation

CET1 build up and dividend Basis points (bps) – transitional rules

138

101 92

175

160 32

40 55

65 89

2012 2013 2014 2015 2016

CET1 build up Dividends

CET1 capital ratio – transitional rules Per cent

8.5 9.2 9.4

10.7

11.8

12.7

14.4

16.0 15.8

2009 10 11 12 13 14 15 16 1H17

Equity development NOK bn

118 127

142

159

190

206 207

2011 2012 2013 2014 2015 2016 1H17

19

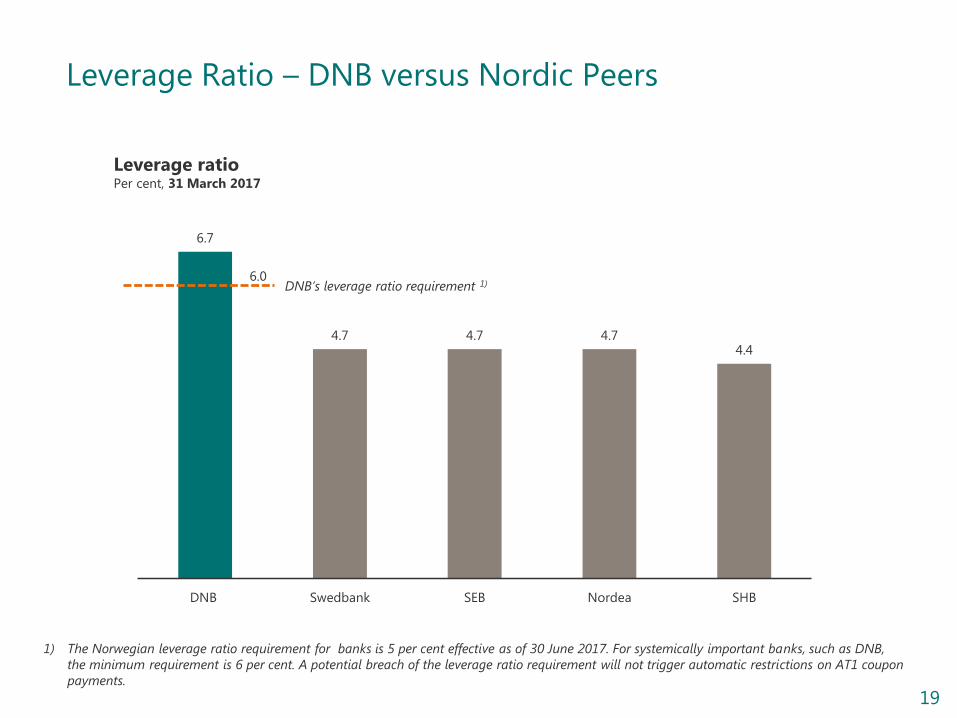

6.7

4.7 4.7 4.7 4.4

DNB Swedbank SEB Nordea SHB

Leverage Ratio – DNB versus Nordic Peers

Leverage ratio Per cent, 31 March 2017

DNB’s leverage ratio requirement 1)

1) The Norwegian leverage ratio requirement for banks is 5 per cent effective as of 30 June 2017. For systemically important banks, such as DNB,

the minimum requirement is 6 per cent. A potential breach of the leverage ratio requirement will not trigger automatic restrictions on AT1 coupon

payments.

6.0

20

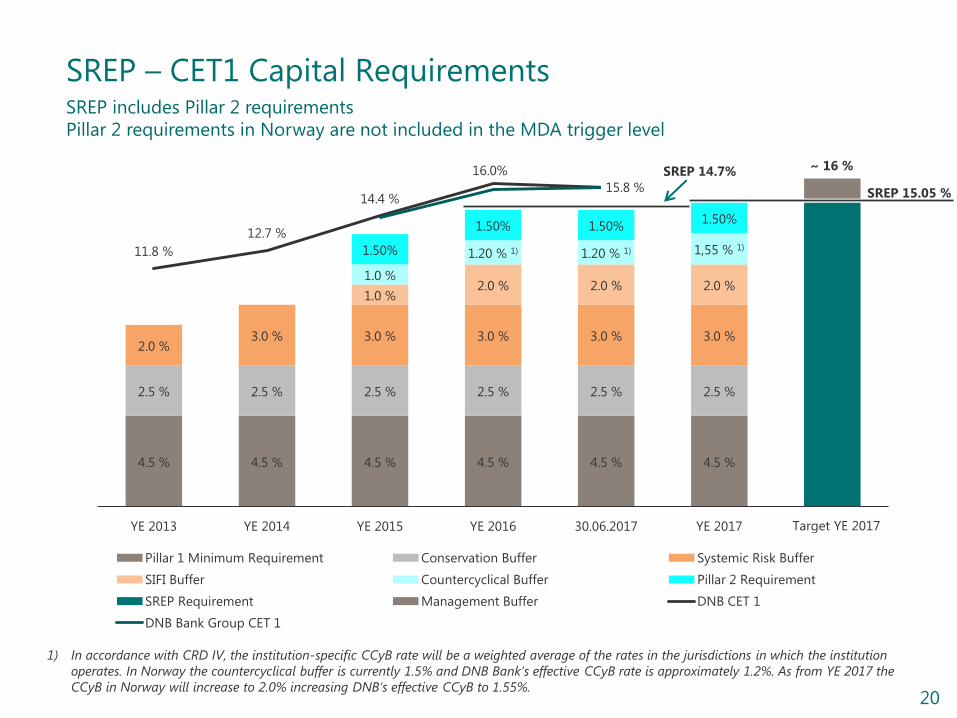

4.5 % 4.5 % 4.5 % 4.5 % 4.5 % 4.5 %

2.5 % 2.5 % 2.5 % 2.5 % 2.5 % 2.5 %

2.0 % 3.0 % 3.0 % 3.0 % 3.0 % 3.0 %

1.0 % 2.0 % 2.0 % 2.0 %

1.0 %

1.20 % 1) 1.20 % 1) 1,55 % 1) 1.50%

1.50% 1.50% 1.50%

11.8 %

12.7 %

14.4 %

16.0%

YE 2013 YE 2014 YE 2015 YE 2016 30.06.2017 YE 2017

Pillar 1 Minimum Requirement Conservation Buffer Systemic Risk Buffer

SIFI Buffer Countercyclical Buffer Pillar 2 Requirement

SREP Requirement Management Buffer DNB CET 1

DNB Bank Group CET 1

15.8 %

Target YE 2017

SREP – CET1 Capital Requirements

1) In accordance with CRD IV, the institution-specific CCyB rate will be a weighted average of the rates in the jurisdictions in which the institution

operates. In Norway the countercyclical buffer is currently 1.5% and DNB Bank’s effective CCyB rate is approximately 1.2%. As from YE 2017 the

CCyB in Norway will increase to 2.0% increasing DNB’s effective CCyB to 1.55%.

SREP 15.05 %

~ 16 %

SREP includes Pillar 2 requirements

Pillar 2 requirements in Norway are not included in the MDA trigger level

SREP 14.7%

21

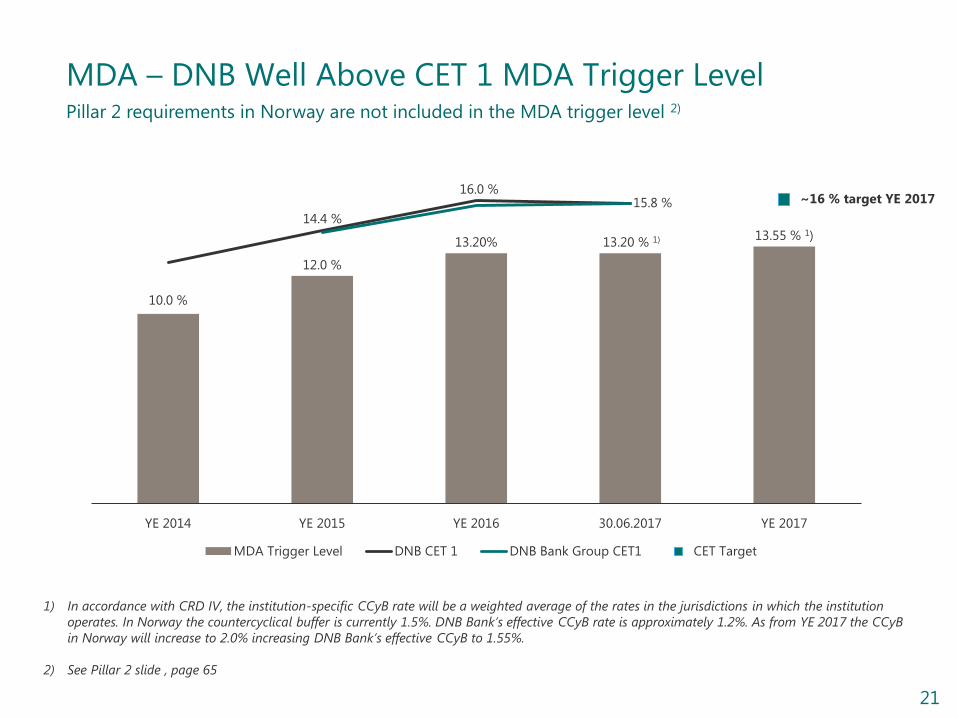

MDA – DNB Well Above CET 1 MDA Trigger Level Pillar 2 requirements in Norway are not included in the MDA trigger level 2)

1) In accordance with CRD IV, the institution-specific CCyB rate will be a weighted average of the rates in the jurisdictions in which the institution

operates. In Norway the countercyclical buffer is currently 1.5%. DNB Bank’s effective CCyB rate is approximately 1.2%. As from YE 2017 the CCyB

in Norway will increase to 2.0% increasing DNB Bank’s effective CCyB to 1.55%.

2) See Pillar 2 slide , page 65

~16 % target YE 2017

10.0 %

12.0 %

13.20% 13.20 % 1) 13.55 % 1)

16.0 % 15.8 %

14.4 %

YE 2014 YE 2015 YE 2016 30.06.2017 YE 2017

MDA Trigger Level DNB CET 1 DNB Bank Group CET1 CET Target

22

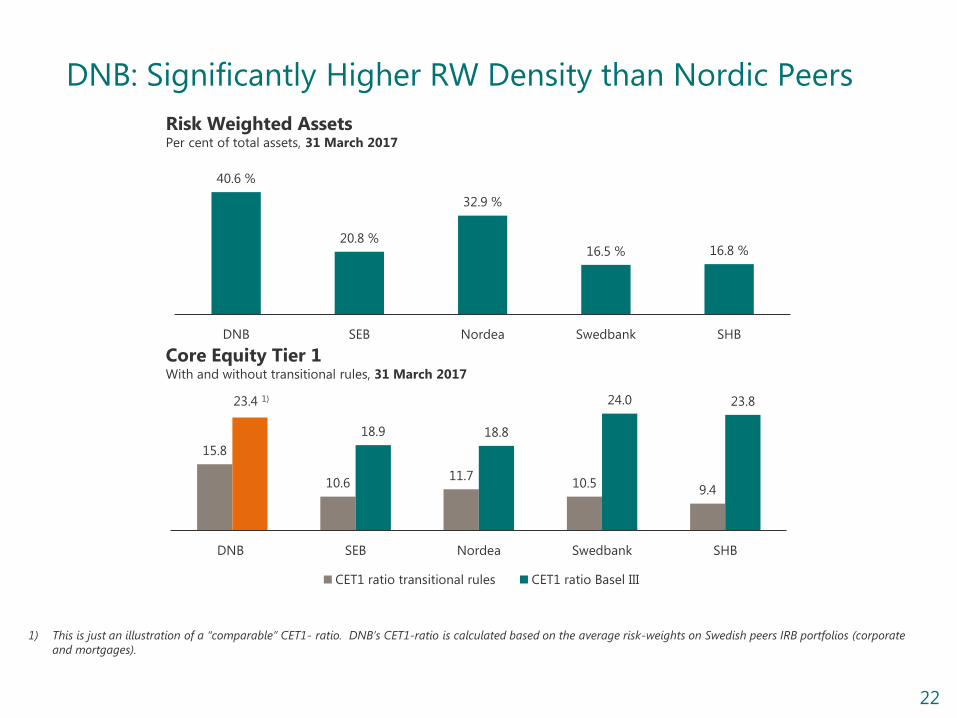

DNB: Significantly Higher RW Density than Nordic Peers

Risk Weighted Assets Per cent of total assets, 31 March 2017

Core Equity Tier 1 With and without transitional rules, 31 March 2017

15.8

10.6 11.7

10.5 9.4

23.4 1)

18.9 18.8

24.0 23.8

DNB SEB Nordea Swedbank SHB

CET1 ratio transitional rules CET1 ratio Basel III

1) This is just an illustration of a “comparable” CET1- ratio. DNB’s CET1-ratio is calculated based on the average risk-weights on Swedish peers IRB portfolios (corporate

and mortgages).

40.6 %

20.8 %

32.9 %

16.5 % 16.8 %

DNB SEB Nordea Swedbank SHB

23

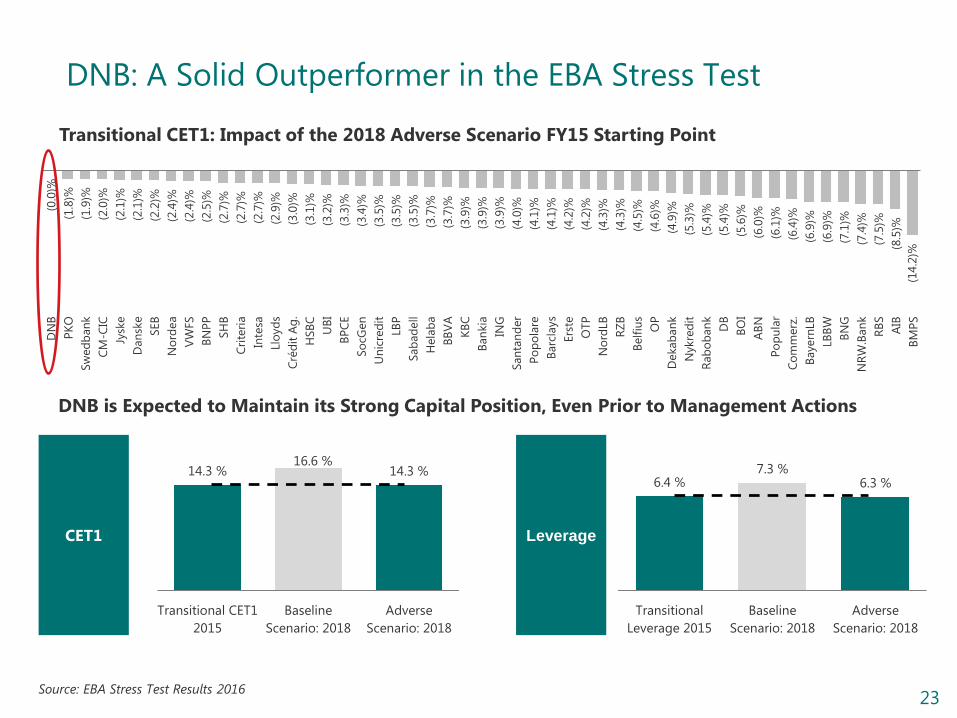

DNB: A Solid Outperformer in the EBA Stress Test (0

.0)%

(1.8

)%

(1.9

)%

(2.0

)%

(2.1

)%

(2.1

)%

(2.2

)%

(2.4

)%

(2.4

)%

(2.5

)%

(2.7

)%

(2.7

)%

(2.7

)%

(2.9

)%

(3.0

)%

(3.1

)%

(3.2

)%

(3.3

)%

(3.4

)%

(3.5

)%

(3.5

)%

(3.5

)%

(3.7

)%

(3.7

)%

(3.9

)%

(3.9

)%

(3.9

)%

(4.0

)%

(4.1

)%

(4.1

)%

(4.2

)%

(4.2

)%

(4.3

)%

(4.3

)%

(4.5

)%

(4.6

)%

(4.9

)%

(5.3

)%

(5.4

)%

(5.4

)%

(5.6

)%

(6.0

)%

(6.1

)%

(6.4

)%

(6.9

)%

(6.9

)%

(7.1

)%

(7.4

)%

(7.5

)%

(8.5

)%

(14.2

)%

DN

B

PK

O

Sw

ed

ban

k

CM

-CIC

Jysk

e

Dan

ske

SEB

No

rdea

VW

FS

BN

PP

SH

B

Cri

teri

a

Inte

sa

Llo

yd

s

Cré

dit

Ag

.

HSB

C

UB

I

BP

CE

So

cGen

Un

icre

dit

LBP

Sab

ad

ell

Hela

ba

BB

VA

KB

C

Ban

kia

ING

San

tan

der

Po

po

lare

Barc

lays

Ers

te

OTP

No

rdLB

RZ

B

Belf

ius

OP

Dekab

an

k

Nykre

dit

Rab

ob

an

k

DB

BO

I

AB

N

Po

pu

lar

Co

mm

erz

.

Bayern

LB

LBB

W

BN

G

NR

W.B

an

k

RB

S

AIB

BM

PS

Transitional CET1: Impact of the 2018 Adverse Scenario FY15 Starting Point

14.3 % 16.6 %

14.3 %

Transitional CET1

2015

Baseline

Scenario: 2018

Adverse

Scenario: 2018

CET1 Leverage

6.4 % 7.3 %

6.3 %

Transitional

Leverage 2015

Baseline

Scenario: 2018

Adverse

Scenario: 2018

DNB is Expected to Maintain its Strong Capital Position, Even Prior to Management Actions

Source: EBA Stress Test Results 2016

24

Loan Book and Asset Quality

25

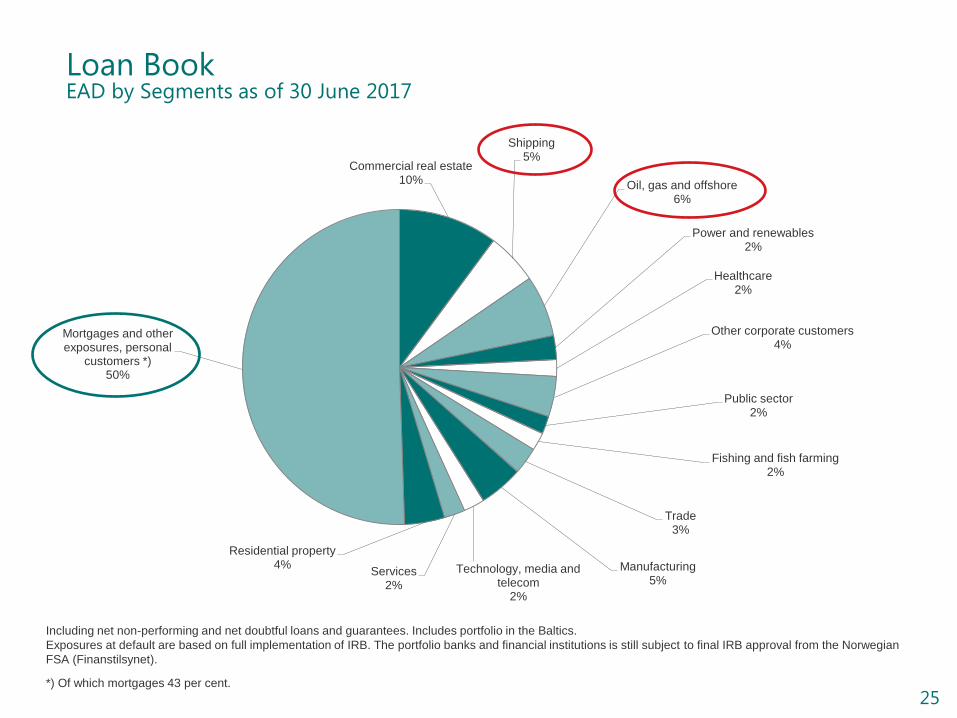

Commercial real estate 10%

Shipping 5%

Oil, gas and offshore 6%

Power and renewables 2%

Healthcare 2%

Other corporate customers 4%

Public sector 2%

Fishing and fish farming 2%

Trade 3%

Manufacturing 5%

Technology, media and telecom

2%

Services 2%

Residential property 4%

Mortgages and other exposures, personal

customers *) 50%

Loan Book EAD by Segments as of 30 June 2017

Including net non-performing and net doubtful loans and guarantees. Includes portfolio in the Baltics.

Exposures at default are based on full implementation of IRB. The portfolio banks and financial institutions is still subject to final IRB approval from the Norwegian

FSA (Finanstilsynet).

*) Of which mortgages 43 per cent.

26

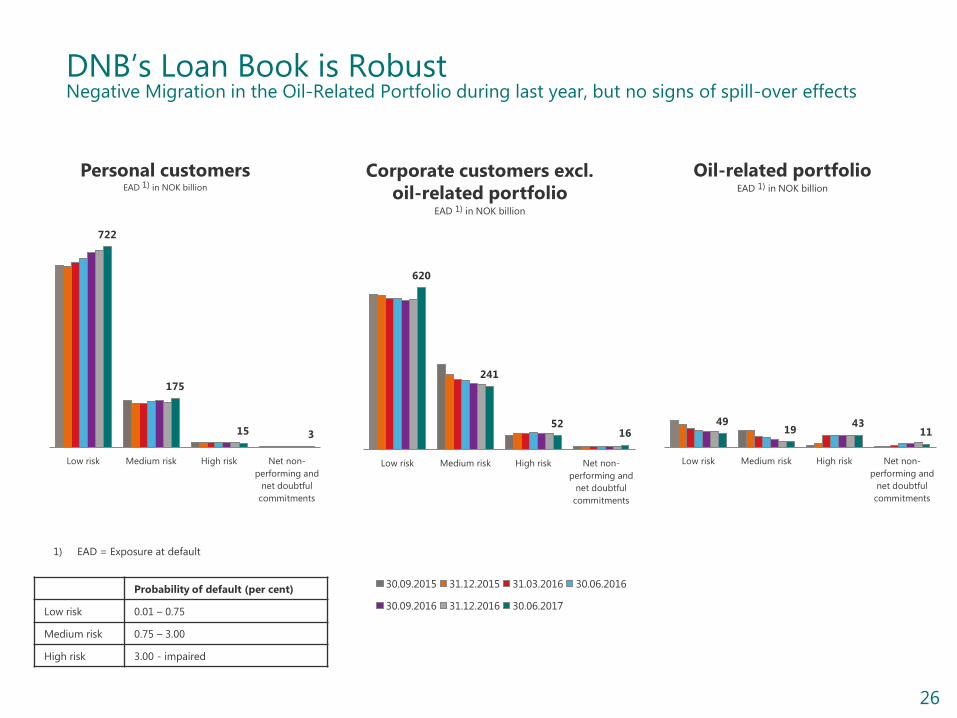

DNB’s Loan Book is Robust Negative Migration in the Oil-Related Portfolio during last year, but no signs of spill-over effects

Personal customers EAD 1) in NOK billion

Corporate customers excl.

oil-related portfolio EAD 1) in NOK billion

Oil-related portfolio

EAD 1) in NOK billion

1) EAD = Exposure at default

722

175

15 3

Low risk Medium risk High risk Net non-

performing and

net doubtful

commitments

620

241

52 16

Low risk Medium risk High risk Net non-

performing and

net doubtful

commitments

30.09.2015 31.12.2015 31.03.2016 30.06.2016

30.09.2016 31.12.2016 30.06.2017

49 19

43 11

Low risk Medium risk High risk Net non-

performing and

net doubtful

commitments

Probability of default (per cent)

Low risk 0.01 – 0.75

Medium risk 0.75 – 3.00

High risk 3.00 - impaired

27

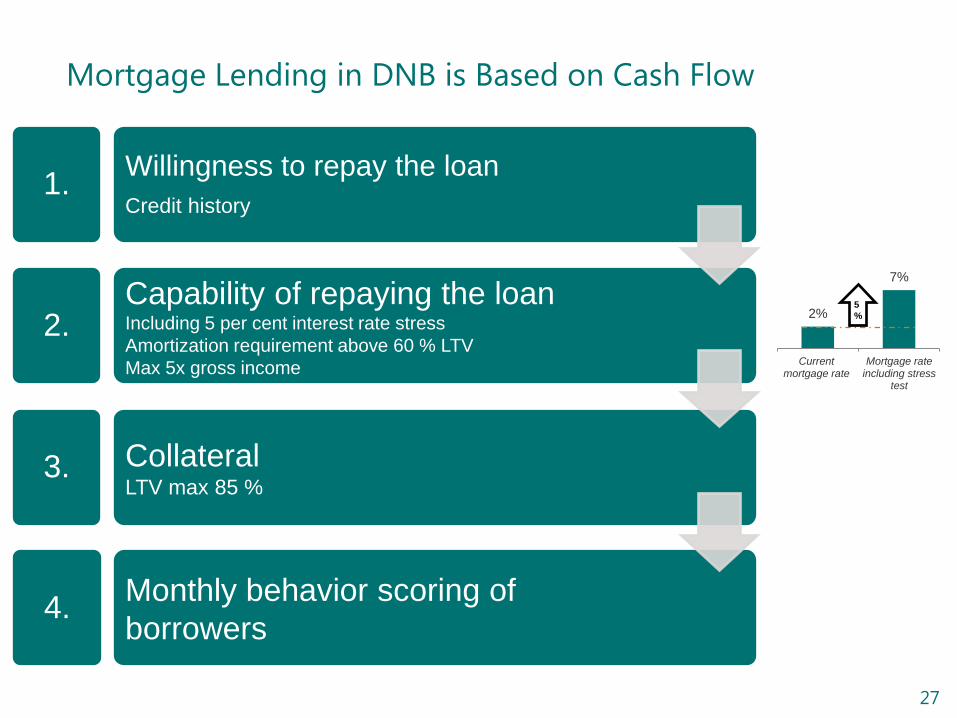

2%

7%

Currentmortgage rate

Mortgage rateincluding stress

test

Mortgage Lending in DNB is Based on Cash Flow

5

%

Willingness to repay the loan

Credit history

Capability of repaying the loan Including 5 per cent interest rate stress

Amortization requirement above 60 % LTV

Max 5x gross income

Collateral LTV max 85 %

Monthly behavior scoring of

borrowers

1.

2.

3.

4.

28

House Price Growth Can be Explained by Fundamentals

Norwegian House Prices

Source: Real Estate Norway, Statistics Norway

Completed housings less

growth in households

Source: Statistics Norway/ DNB Markets

Nominal House Prices 2000-2017

Source: Eiendomsverdi AS

(member of the European AVM Alliance)

0

100

200

300

400

500

600

700

800

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

2015

Nominal prices

CPI-deflated prices

Income per capita-deflated prices

0

50

100

150

200

250

300

350

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Norway UK

Sweden Denmark

USA

-20,000

-15,000

-10,000

-5,000

0

5,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

29

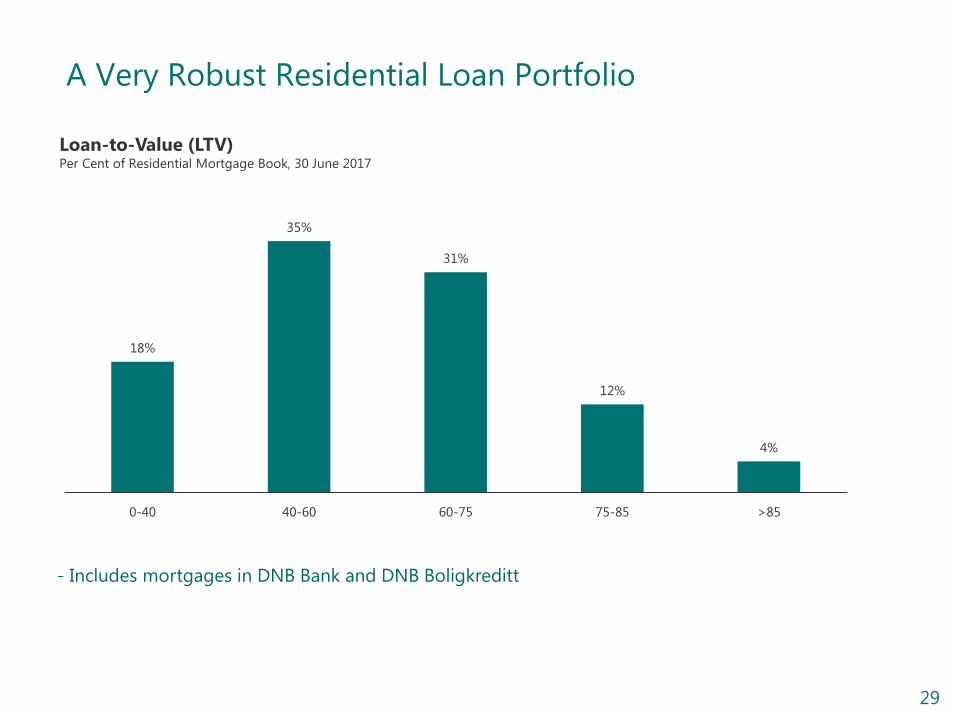

A Very Robust Residential Loan Portfolio

18%

35%

31%

12%

4%

0-40 40-60 60-75 75-85 >85

Loan-to-Value (LTV) Per Cent of Residential Mortgage Book, 30 June 2017

- Includes mortgages in DNB Bank and DNB Boligkreditt

30

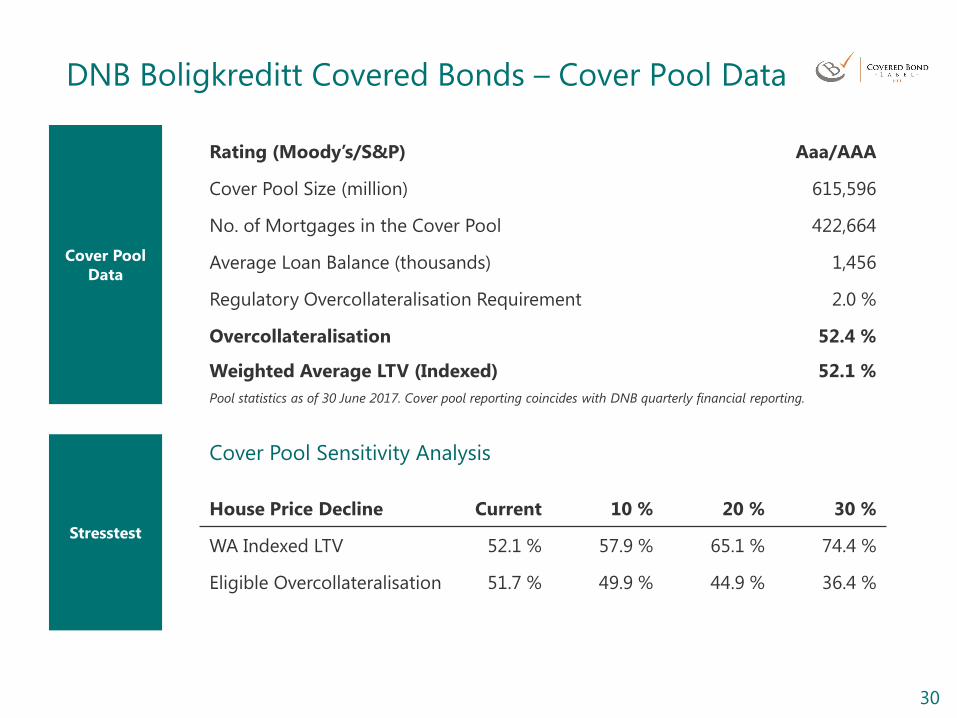

Cover Pool

Data

DNB Boligkreditt Covered Bonds – Cover Pool Data

Rating (Moody’s/S&P) Aaa/AAA

Cover Pool Size (million) 615,596

No. of Mortgages in the Cover Pool 422,664

Average Loan Balance (thousands) 1,456

Regulatory Overcollateralisation Requirement 2.0 %

Overcollateralisation 52.4 %

Weighted Average LTV (Indexed) 52.1 %

Pool statistics as of 30 June 2017. Cover pool reporting coincides with DNB quarterly financial reporting.

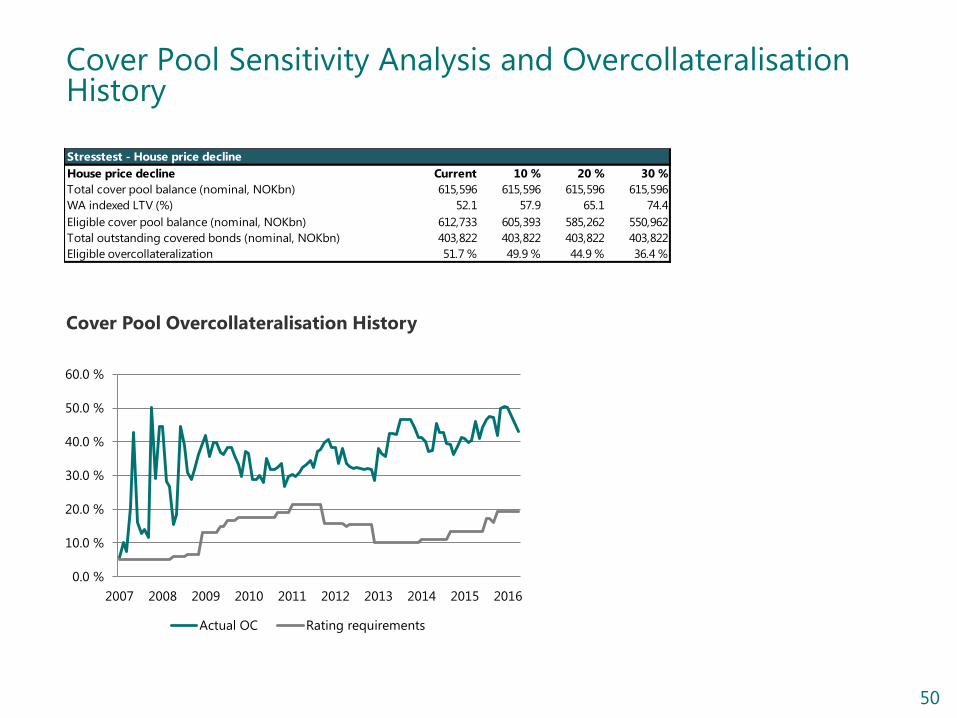

Stresstest

House Price Decline Current 10 % 20 % 30 %

WA Indexed LTV 52.1 % 57.9 % 65.1 % 74.4 %

Eligible Overcollateralisation 51.7 % 49.9 % 44.9 % 36.4 %

Cover Pool Sensitivity Analysis

31

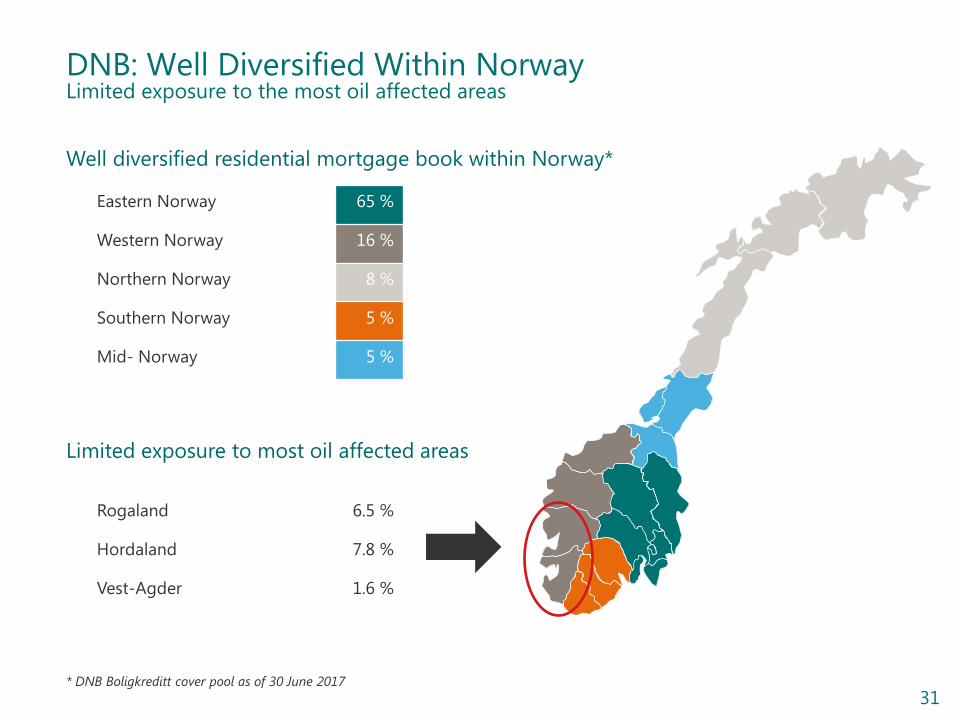

DNB: Well Diversified Within Norway Limited exposure to the most oil affected areas

Well diversified residential mortgage book within Norway*

* DNB Boligkreditt cover pool as of 30 June 2017

Eastern Norway 65 %

Western Norway 16 %

Northern Norway 8 %

Southern Norway 5 %

Mid- Norway 5 %

Limited exposure to most oil affected areas

Rogaland 6.5 %

Hordaland 7.8 %

Vest-Agder 1.6 %

32

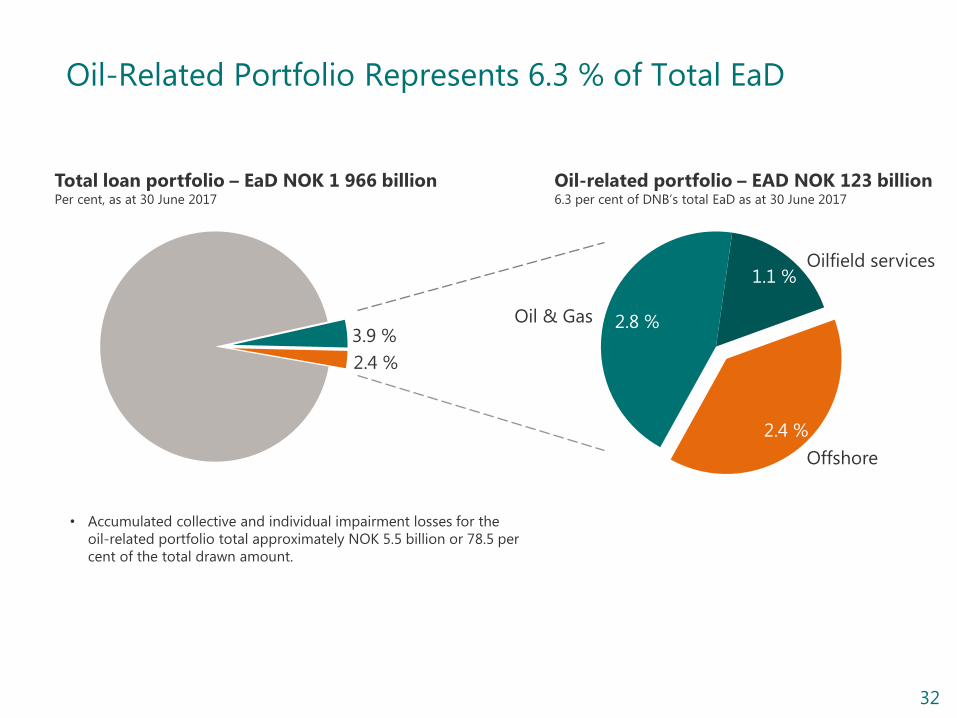

Oil-Related Portfolio Represents 6.3 % of Total EaD

6 %

8 %

7 %

11 %

Total loan portfolio – EaD NOK 1 966 billion Per cent, as at 30 June 2017

Oil-related portfolio – EAD NOK 123 billion 6.3 per cent of DNB’s total EaD as at 30 June 2017

3.9 %

2.4 %

2.8 %

1.1 %

2.4 %

• Accumulated collective and individual impairment losses for the

oil-related portfolio total approximately NOK 5.5 billion or 78.5 per

cent of the total drawn amount.

Oil & Gas

Oilfield services

Offshore

33

49

19

43

11

Low risk Medium risk High risk Net non-performingand net doubtful

commitments

2 5

32

9

Low risk Medium risk High risk Net non-performingand net doubtful

commitments

Oil-Related Portfolio Major Challenges Within the Offshore Portfolio

DNB’s oil-related portfolio split by sub-segment in terms of exposure (EaD) and by risk grade

EaD: Exposure at Default, PD: Probability of default. Figures from Fact book as at 31 March 2017.

Based on DNB's risk classification system, where 1 represents the lowest risk and 10 the highest risk.

Total Oil related segments EaD in NOK billion

Offshore EaD in NOK billion

Oil and Gas EaD in NOK billion

Oilfield Service EaD in NOK billion

37

9 7 1

Low risk Medium risk High risk Net non-performingand net doubtful

commitments

10 5 4

1

Low risk Medium risk High risk Net non-performingand net doubtful

commitments

30.09.2015 31.12.2015 31.03.2016 30.06.2016

30.09.2016 31.12.2016 31.03.2017 30.06.2017

34

Offshore Exposure is 2.4 % of DNB’s Total Loan Portfolio

Total loan portfolio – EaD NOK 1 966 billion Per cent, as at 30 June 2017

2.4 %

1.1 %

0.7 % 0.6 %

Offshore exposure – EaD NOK 48 billion Per cent of DNB’s portfolio, as at 30 June 2017

Offshore Supply Vessels (OSV)

Other offshore

Rig

35

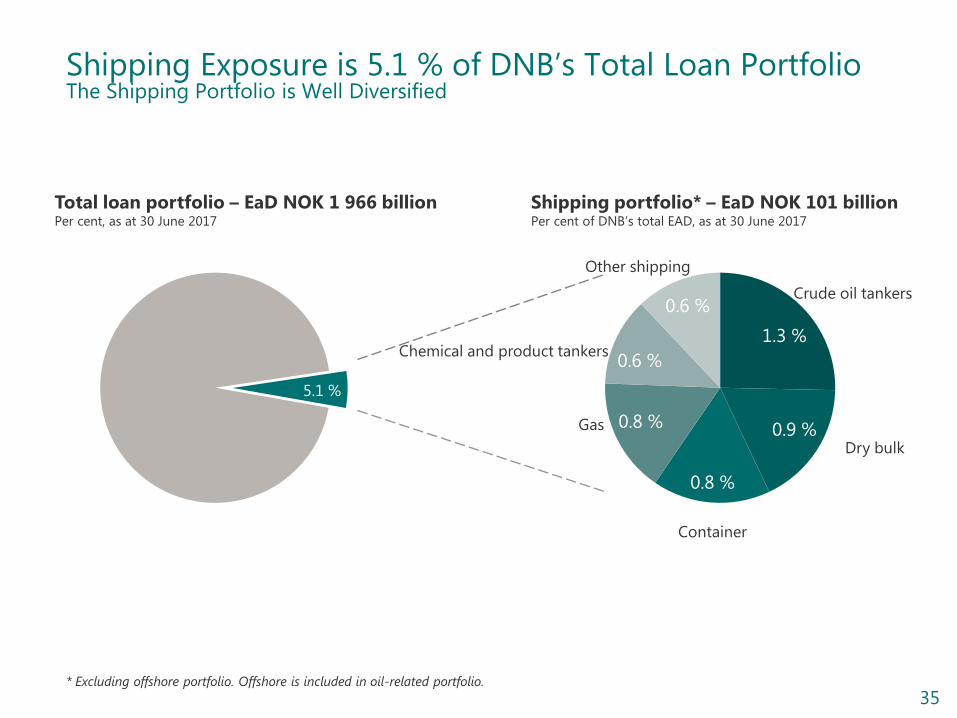

Shipping Exposure is 5.1 % of DNB’s Total Loan Portfolio The Shipping Portfolio is Well Diversified

6 %

8 %

7 %

11 %

Total loan portfolio – EaD NOK 1 966 billion Per cent, as at 30 June 2017

Shipping portfolio* – EaD NOK 101 billion Per cent of DNB’s total EAD, as at 30 June 2017

5.1 %

1.3 %

0.9 %

0.8 %

0.8 %

0.6 %

0.6 % Crude oil tankers

Dry bulk

Gas

Container

Other shipping

Chemical and product tankers

* Excluding offshore portfolio. Offshore is included in oil-related portfolio.

36

Risk Classification and Migration DNB’s Shipping Book - Excluding Offshore

Shipping* – EaD distribution by PD bracket NOK billion

29

67

16

5

Low risk Medium risk High risk Net non-performing and net doubtful

commitments

30.09.2015 31.12.2015 31.03.2016 30.06.2016 30.09.2016 31.12.2016 31.03.2017 30.06.2017

* Numbers for the Shipping Offshore and Logistics Division excluding offshore

portfolio. Offshore is included in oil-related portfolio.

37

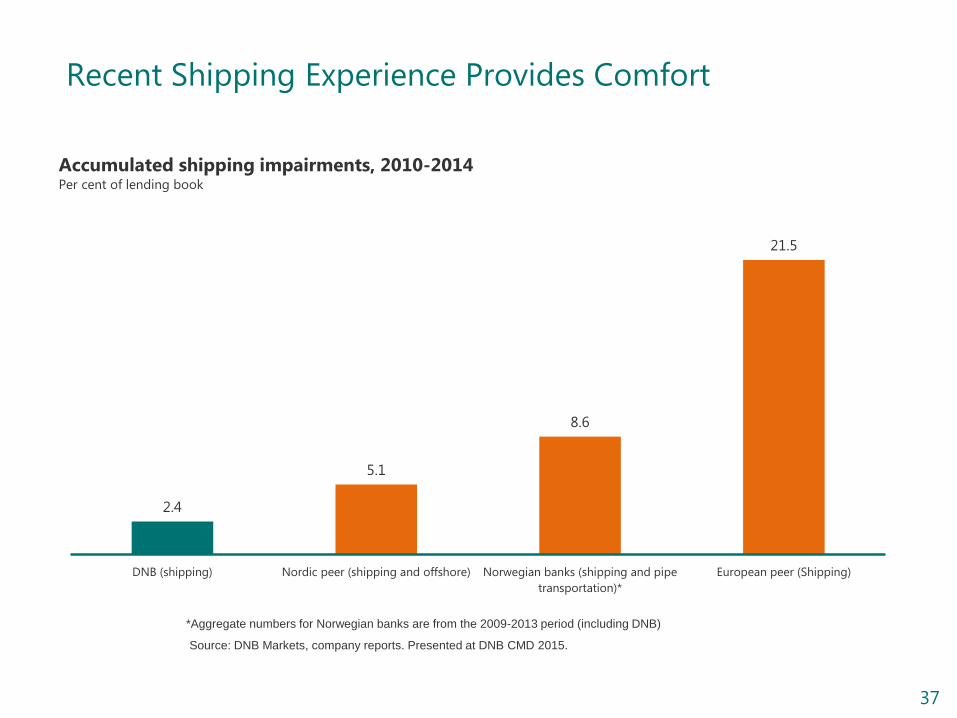

Recent Shipping Experience Provides Comfort

Accumulated shipping impairments, 2010-2014 Per cent of lending book

2.4

5.1

8.6

21.5

DNB (shipping) Nordic peer (shipping and offshore) Norwegian banks (shipping and pipe

transportation)*

European peer (Shipping)

*Aggregate numbers for Norwegian banks are from the 2009-2013 period (including DNB)

Source: DNB Markets, company reports. Presented at DNB CMD 2015.

38

Funding

39

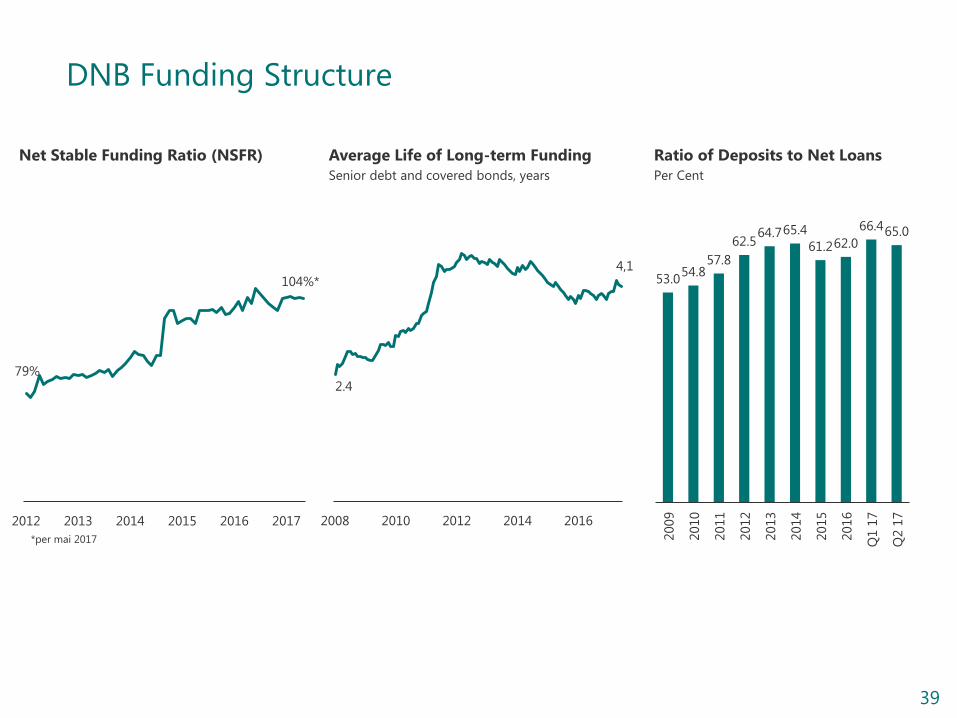

DNB Funding Structure

79%

104%*

2012 2013 2014 2015 2016 2017

Net Stable Funding Ratio (NSFR)

2.4

4,1

2008 2010 2012 2014 2016

Average Life of Long-term Funding

Senior debt and covered bonds, years

Ratio of Deposits to Net Loans

Per Cent

53.0 54.8

57.8

62.5 64.7 65.4

61.2 62.0

66.4 65.0

2009

2010

2011

2012

2013

2014

2015

2016

Q1 1

7

Q2 1

7

*per mai 2017

40

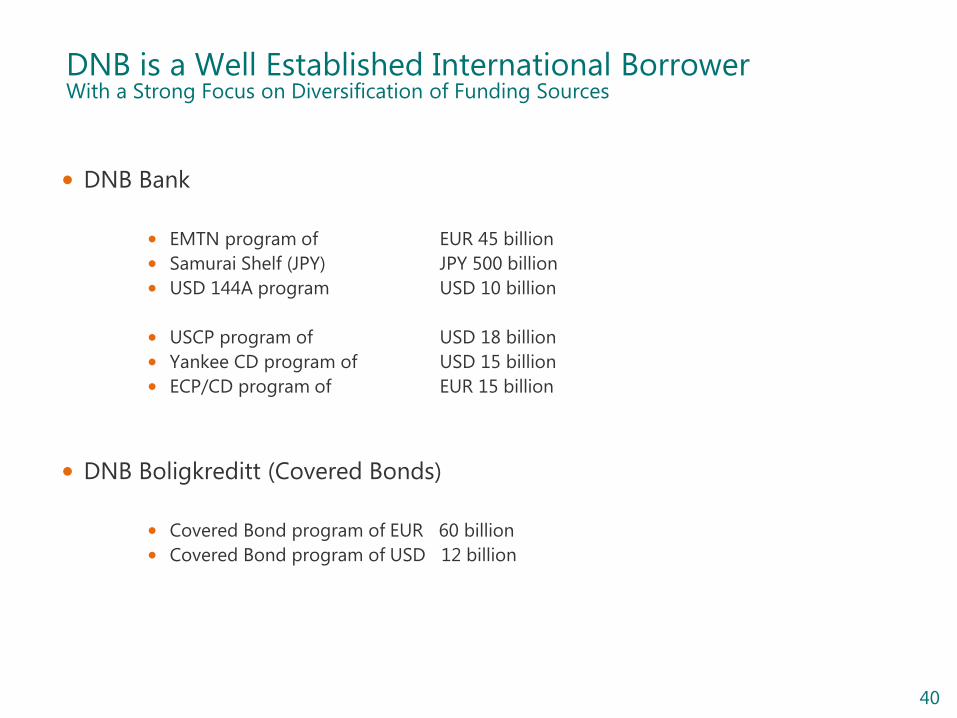

DNB is a Well Established International Borrower With a Strong Focus on Diversification of Funding Sources

• DNB Bank

• EMTN program of EUR 45 billion

• Samurai Shelf (JPY) JPY 500 billion

• USD 144A program USD 10 billion

• USCP program of USD 18 billion

• Yankee CD program of USD 15 billion

• ECP/CD program of EUR 15 billion

• DNB Boligkreditt (Covered Bonds)

• Covered Bond program of EUR 60 billion

• Covered Bond program of USD 12 billion

41

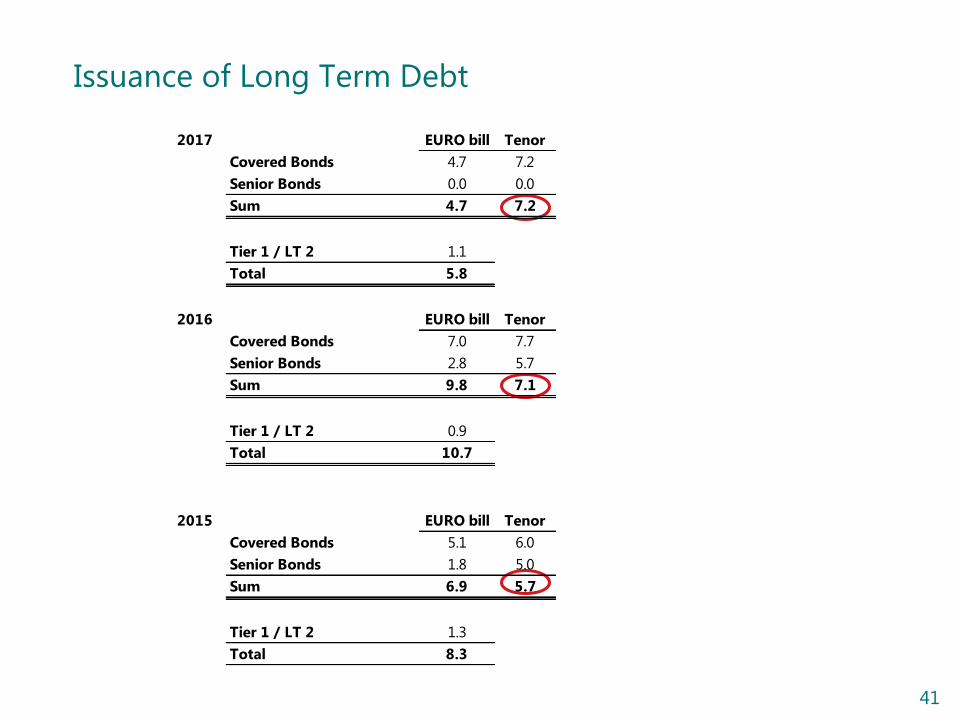

Issuance of Long Term Debt

2017 EURO bill Tenor

Covered Bonds 4.7 7.2

Senior Bonds 0.0 0.0

Sum 4.7 7.2

Tier 1 / LT 2 1.1

Total 5.8

2016 EURO bill Tenor

Covered Bonds 7.0 7.7

Senior Bonds 2.8 5.7

Sum 9.8 7.1

Tier 1 / LT 2 0.9

Total 10.7

2015 EURO bill Tenor

Covered Bonds 5.1 6.0

Senior Bonds 1.8 5.0

Sum 6.9 5.7

Tier 1 / LT 2 1.3

Total 8.3

42

A Well Established International Covered Bond Issuer

Volume

Tenor

Maturity

EUR 1,500 mn 7 years 2017 – Aug

EUR 1,500 mn 5 years 2018 – Jan

EUR 1,500 mn 5 years 2018 – Nov

EUR 1,500 mn 7 years 2019 – Jun

EUR 1,250 mn 5 years 2019 – Oct

EUR 1,250 mn 5 years 2020 – Oct

EUR 1,500 mn 5 years 2021 – Jan

EUR 1,500 mn 10 years 2021 – Jun

EUR 2,000 mn 5 years 2022 – Jan

EUR 2,000 mn 10 years 2022 – Mar

EUR 1,000 mn 10 years 2022 – Nov

EUR 1,500 mn 7 years 2023 – Apr

EUR 1,500 mn 10 years 2026 – Sep

EUR 1,000 mn (FRN) 5 years 2019 – Jan

EUR 1,000 mn (FRN) 7 years 2021 – Nov

USD 2,000 mn 5 years 2018 - Mar

USD 1,250 mn 5 years 2020 - May

USD 1,500 mn 5 years 2022 - Mar

GBP 500 mn (FRN) 5 years 2020 - Feb

43

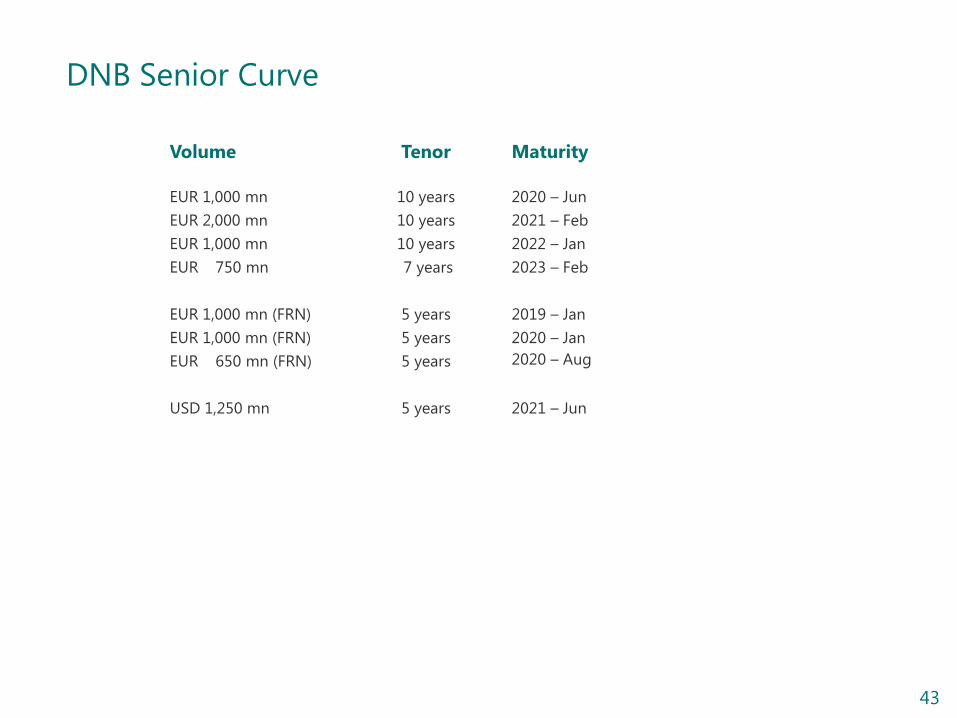

DNB Senior Curve

Volume

Tenor

Maturity

EUR 1,000 mn 10 years 2020 – Jun

EUR 2,000 mn 10 years 2021 – Feb

EUR 1,000 mn 10 years 2022 – Jan

EUR 750 mn 7 years 2023 – Feb

EUR 1,000 mn (FRN) 5 years 2019 – Jan

EUR 1,000 mn (FRN) 5 years 2020 – Jan

EUR 650 mn (FRN) 5 years 2020 – Aug

USD 1,250 mn 5 years 2021 – Jun

44

Funding Contacts

Long Term Funding: Short Term Funding:

• Thor Tellefsen

Senior Vice President, Head of Long Term Funding

Phone direct: + 47 24 16 91 22

Mobile: + 47 915 44 385

E-mail: [email protected]

• Håkon Røsand

Senior Vice President, Long Term Funding

Phone direct: + 47 24 16 91 27

Mobile: + 47 906 16 892

E-mail [email protected]

• Kristine Øvrebø

Senior Vice President, Long Term Funding

Phone direct: + 47 24 16 91 25

Mobile: + 47 916 08 005

E-mail: [email protected]

• Åsmund Midttun

Senior Dealer, Rates, FICC

Phone direct: +47 24 16 90 28

Mobile: +47 901 13 559

E-mail: [email protected] / [email protected]

• Erik Brække

Senior Vice President, Rates, FICC

Phone direct: +47 24 16 90 31

Mobil: +47 930 47 504

E-mail: [email protected] / [email protected]

• Stephen Danna

First Vice President, FX/Rates/Commodities, New York

Phone direct: +1 212 681 2550

Mobil: +1 646 824 0072

E-mail: [email protected] / [email protected]

https://www.dnb.no/en/about-us/investor-relations/funding.html

45

Appendix

Appendix A:

Cover Pool Portfolio Information and LCR

Eligibility

46

Future Updates On Cover Pool Developments

DNB has implemented the common Harmonised Transparency Template of

the European Covered Bond Council which is available on the DNB website.

Information about the cover pool of DNB Boligkreditt may be accessed via

DNB Boligkreditt’s web page:

https://www.dnb.no/en/about-us/investor-relations/funding.html

Contacts DNB Boligkreditt AS:

- Per Sagbakken, CEO: [email protected] +47 906 61 159

Portfolio information is updated when DNB quarterly results are released

47

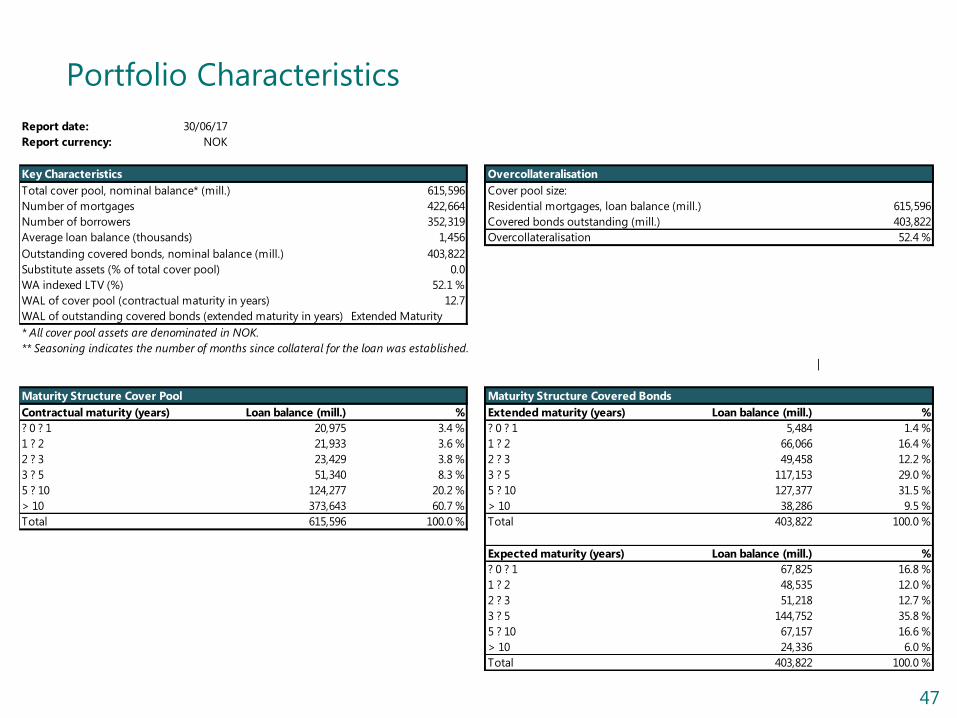

Portfolio Characteristics

Report date: 30/06/17

Report currency: NOK

Key Characteristics Overcollateralisation

Total cover pool, nominal balance* (mill.) 615,596 Cover pool size:

Number of mortgages 422,664 Residential mortgages, loan balance (mill.) 615,596

Number of borrowers 352,319 Covered bonds outstanding (mill.) 403,822

Average loan balance (thousands) 1,456 Overcollateralisation 52.4 %

Outstanding covered bonds, nominal balance (mill.) 403,822

Substitute assets (% of total cover pool) 0.0

WA indexed LTV (%) 52.1 %

WAL of cover pool (contractual maturity in years) 12.7

WAL of outstanding covered bonds (extended maturity in years) Extended Maturity

* All cover pool assets are denominated in NOK.

** Seasoning indicates the number of months since collateral for the loan was established.

|

Maturity Structure Cover Pool Maturity Structure Covered Bonds

Contractual maturity (years) Loan balance (mill.) % Extended maturity (years) Loan balance (mill.) %

? 0 ? 1 20,975 3.4 % ? 0 ? 1 5,484 1.4 %

1 ? 2 21,933 3.6 % 1 ? 2 66,066 16.4 %

2 ? 3 23,429 3.8 % 2 ? 3 49,458 12.2 %

3 ? 5 51,340 8.3 % 3 ? 5 117,153 29.0 %

5 ? 10 124,277 20.2 % 5 ? 10 127,377 31.5 %

> 10 373,643 60.7 % > 10 38,286 9.5 %

Total 615,596 100.0 % Total 403,822 100.0 %

Expected maturity (years) Loan balance (mill.) %

? 0 ? 1 67,825 16.8 %

1 ? 2 48,535 12.0 %

2 ? 3 51,218 12.7 %

3 ? 5 144,752 35.8 %

5 ? 10 67,157 16.6 %

> 10 24,336 6.0 %

Total 403,822 100.0 %

48

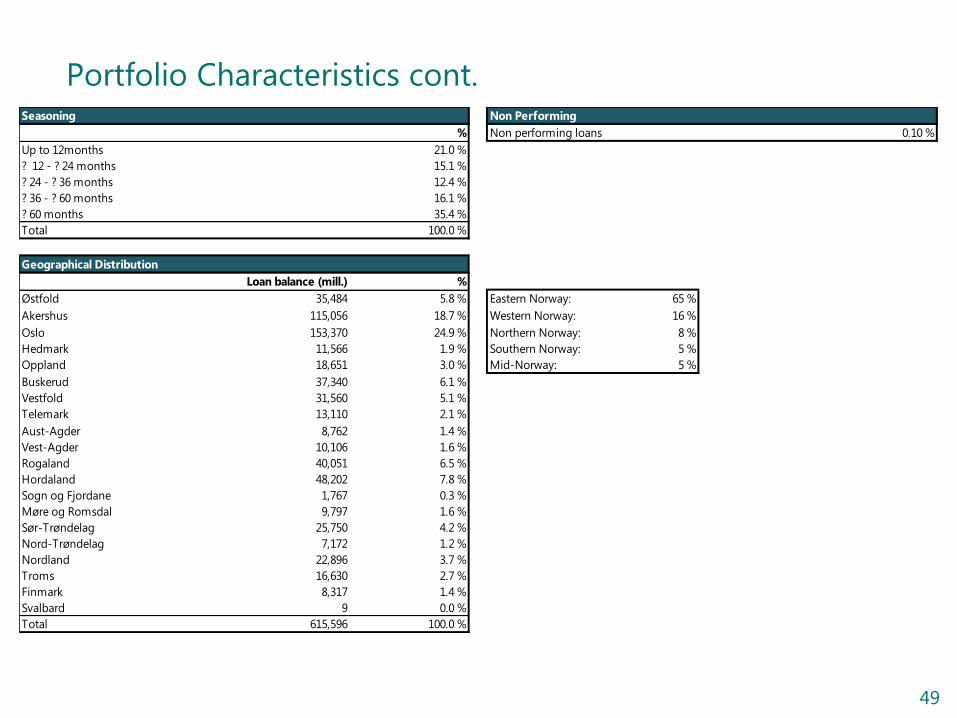

Portfolio Characteristics cont.

Loan Size Concentration Risk

Private individuals Loan balance (mill.) Number of loans %

? 1,000,000 81,234 187,772 10 largest exposures 0.2 %

> 1,000,000 ? 2,000,000 190,152 128,378 10 largest exposures excl. housing cooperatives 0.1 %

> 2,000,000 ? 3,000,000 154,235 63,297

> 3,000,000 ? 4,000,000 82,739 24,074 Property Types

> 4,000,000 ? 5,000,000 41,094 9,245 Loan balance (mill.) %

> 5,000,000 47,924 7,298 Residential 615,596 100.0 %

Total 597,377 420,064 Commercial 0 0.0 %

Other 0 0.0 %

Housing Cooperatives Loan balance (mill.) Number of loans Total 615,596 100.0 %

? 5,000,000 2,954 1,673

> 5,000,000 ? 10,000,000 3,076 428 o/w Housing Cooperatives / Multi-family assets 18,219 3.0 %

> 10,000,000 ? 20,000,000 4,393 310 o/w Forest & Agriculture 0 0.0 %

> 20,000,000 ? 50,000,000 4,943 155

> 50,000,000 ? 100,000,000 1,956 28 Occupancy Type

> 100,000,000 897 6 %

Total 18,219 2,600 Owner occupied 87.5%

Second homes / Holiday houses 0.4%

LTV buckets Buy to let / Non owner occupied houses 0.1%

Indexed LTV Loan balance (mill.) % Other 12.0%

? 0 ? 40 142,141 23.1 % Total 100.0%

40 ? 50 100,223 16.3 %

50 ? 60 143,644 23.3 % Repayment Type

60 ? 70 150,190 24.4 % %

70 ? 80 70,050 11.4 % Amortization 72.6 %

80 ? 90 6,051 1.0 % Interest only* 27.4 %

90 ? 100 1,806 0.3 % Total 100.0 %

>100 1,493 0.2 % *No principal payments for a limited period of time.

Total 615,596 100.0 %

49

Portfolio Characteristics cont. Seasoning Non Performing

% Non performing loans 0.10 %

Up to 12months 21.0 %

? 12 - ? 24 months 15.1 %

? 24 - ? 36 months 12.4 %

? 36 - ? 60 months 16.1 %

? 60 months 35.4 %

Total 100.0 %

Geographical Distribution

Loan balance (mill.) %

Østfold 35,484 5.8 % Eastern Norway: 65 %

Akershus 115,056 18.7 % Western Norway: 16 %

Oslo 153,370 24.9 % Northern Norway: 8 %

Hedmark 11,566 1.9 % Southern Norway: 5 %

Oppland 18,651 3.0 % Mid-Norway: 5 %

Buskerud 37,340 6.1 %

Vestfold 31,560 5.1 %

Telemark 13,110 2.1 %

Aust-Agder 8,762 1.4 %

Vest-Agder 10,106 1.6 %

Rogaland 40,051 6.5 %

Hordaland 48,202 7.8 %

Sogn og Fjordane 1,767 0.3 %

Møre og Romsdal 9,797 1.6 %

Sør-Trøndelag 25,750 4.2 %

Nord-Trøndelag 7,172 1.2 %

Nordland 22,896 3.7 %

Troms 16,630 2.7 %

Finmark 8,317 1.4 %

Svalbard 9 0.0 %

Total 615,596 100.0 %

50

Cover Pool Sensitivity Analysis and Overcollateralisation History

Cover Pool Overcollateralisation History

0.0 %

10.0 %

20.0 %

30.0 %

40.0 %

50.0 %

60.0 %

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Actual OC Rating requirements

Stresstest - House price decline

House price decline Current 10 % 20 % 30 %

Total cover pool balance (nominal, NOKbn) 615,596 615,596 615,596 615,596

WA indexed LTV (%) 52.1 57.9 65.1 74.4

Eligible cover pool balance (nominal, NOKbn) 612,733 605,393 585,262 550,962

Total outstanding covered bonds (nominal, NOKbn) 403,822 403,822 403,822 403,822

Eligible overcollateralization 51.7 % 49.9 % 44.9 % 36.4 %

51

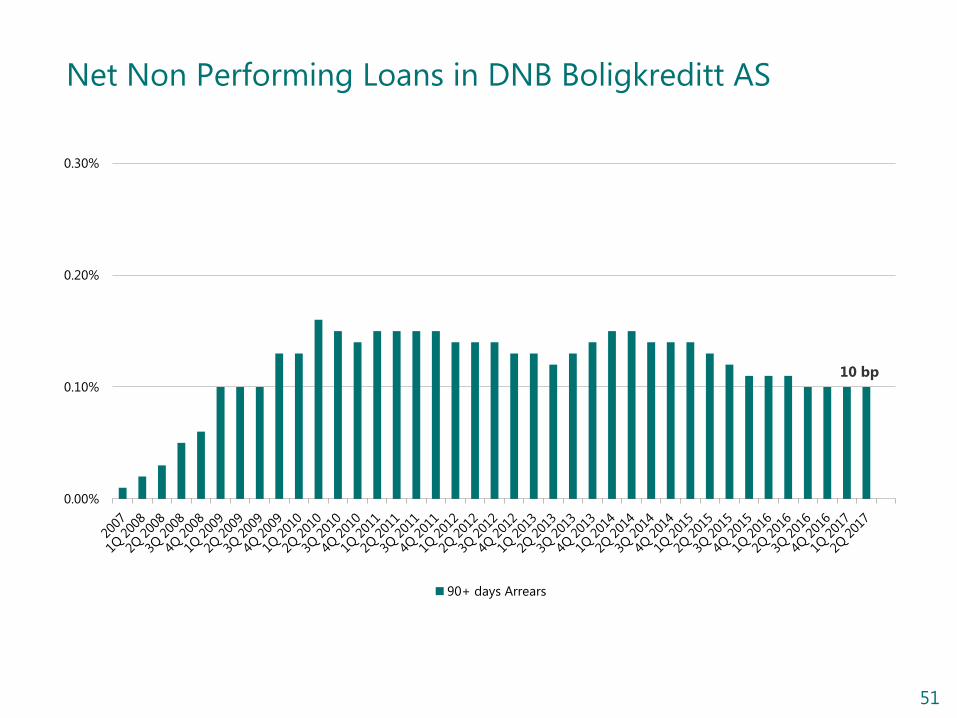

Net Non Performing Loans in DNB Boligkreditt AS

0.00%

0.10%

0.20%

0.30%

90+ days Arrears

10 bp

52

Covered Bonds Issued by DNB Boligkreditt AS Qualifies for Level 1-Assets Pursuant to LCR-regulation (Slide 1 of 2)

Covered bonds issued by DNB Boligkreditt AS fulfil the requirements to qualify as

Level 1-assets pursuant to Commission Delegated Regulation (EU) 2015/61

regarding liquidity coverage requirement for credit institutions (“LCR-regulation”).

With reference to Article 10(1)(f) of the LCR-regulation, DNB Boligkreditt AS

confirms the following:

• Covered bonds issued by DNB Boligkreditt AS meet the requirements to be

eligible for the treatment set out in Article 129(4) of Regulation (EU) No

575/2013 (“CRR”) and the requirements referred to in Article 52(4) of Directive

2009/65/EC, cf. the European Commission’s website:

http://ec.europa.eu/finance/investment/legal_texts/index_en.htm

• The exposures to institutions in the cover pool meet the conditions laid down

in Article 129(1)(c) and in Article 129(1) last subparagraph of CRR

53

Covered Bonds Issued by DNB Boligkreditt AS Qualifies as Level 1-Assets Pursuant to LCR-regulation (Slide 2 of 2)

With reference to Article 10(1)(f) of the LCR-regulation, DNB Boligkreditt AS

confirms the following (cont.):

• DNB Boligkreditt AS gives the information required in Article 129(7) of CRR

to its investors

• Covered bonds issued by DNB Boligkreditt AS are assigned a credit

assessment by a nominated ECAI which is at least credit quality step 1 in

accordance with Article 129(4) of CRR, and the equivalent credit quality step

in the event of short term credit assessment

• The cover pool does at all times meet an asset coverage requirement of at

least 2 % in excess of the amount required to meet the claims attaching to

the covered bonds issued by DNB Boligkreditt AS

54

ECB Eligibility and CRD-Compliance of Covered Bonds Issued by DNB Boligkreditt AS

• All covered bonds issued by DNB Boligkreditt AS fulfil the eligibility criteria for

marketable assets set by the Eurosystem and are thus eligible for Eurosystem monetary

policy operations.

• The Eurosystem set additional criteria for own use of eligible instruments in the

Eurosystem monetary policy operations. In the case of covered bonds, the instruments

must be issued in accordance with the criteria set out in Part 1, points 68 to 70 of Annex

VI to Directive 2006/48/EC. The covered bonds issued by DNB Boligkreditt AS fulfil these

criteria, but the Eurosystem has not checked the fulfilment of these conditions for

Norway, since Norway is not part of the EU. Therefore, covered bonds issued by DNB

Boligkreditt AS are marked with a "N/A" what regards ‘own-use covered bonds’ in ECB's

eligible asset database.

• DNB Boligkreditt AS confirms that the covered bonds it issues are compliant with

the CRD-requirement set forth in the Eurosystem guidelines. In addition, DNB

Boligkreditt AS confirms that it gives the information required in Regulation (EU) No

575/2013 ("CRR") article 129 (7) to its investors, so that the covered bonds issued by DNB

Boligkreditt AS are eligible for the preferential treatment set out in CRR article 129 (4).

55

Appendix

Appendix B:

Digitalization

56

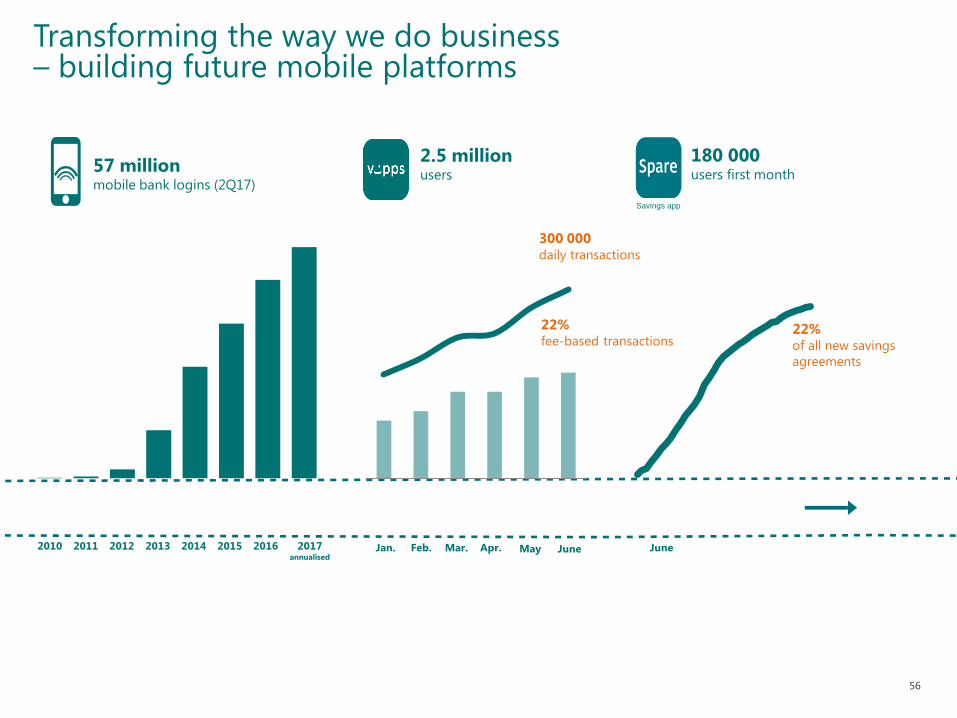

22% of all new savings

agreements

300 000 daily transactions

2.5 million users

June May June Jan. Feb. Mar. Apr.

22% fee-based transactions

180 000 users first month

Savings app

57 million mobile bank logins (2Q17)

2010 2015 2016 2017 annualised

2011 2012 2013

Transforming the way we do business – building future mobile platforms

2014

57

Transforming the way we do business – smarter use of capital

Investment in capital-light products Defined contribution: #1 market position

Capital reallocation Loans reduced by NOK 9.5 billion in

cyclical industries in 2Q17

IBD Ranked #1 among debt capital markets, investment

grade and high-yield issuers in Norway 1)

Ranked #2 in Nordic countries research 2)

1) Source: Prospera customer satisfaction survey 2017

2) Source: Extel 2017 research

58

Appendix

Appendix C:

The Norwegian Mortgage Market

59

The Norwegian Residential Mortgage Market

• Nearly 80% of Norwegians own their home: • Few mortgages are buy-to-let.

• Norway is primarily a floating interest rate market: • The large majority of mortgages originated by DNB are floating rate.

• Rates on floating rate mortgages can be reset at any time and at the bank’s own

discretion, by giving debtors six weeks’ notice.

• Loans are normally underwritten with a term of 15-25 years: • Average size for new mortgages originated by DNB is approximately NOK 1,000,000

(EUR 110,000).

• In Norway, all borrowing costs are deductible from taxable income at

the current rate of 24 %: • Households are therefore better able to withstand an increase in interest rates.

Source: Finance Norway - FNO

60

Appendix

Appendix D:

Capital and Tier 1

61

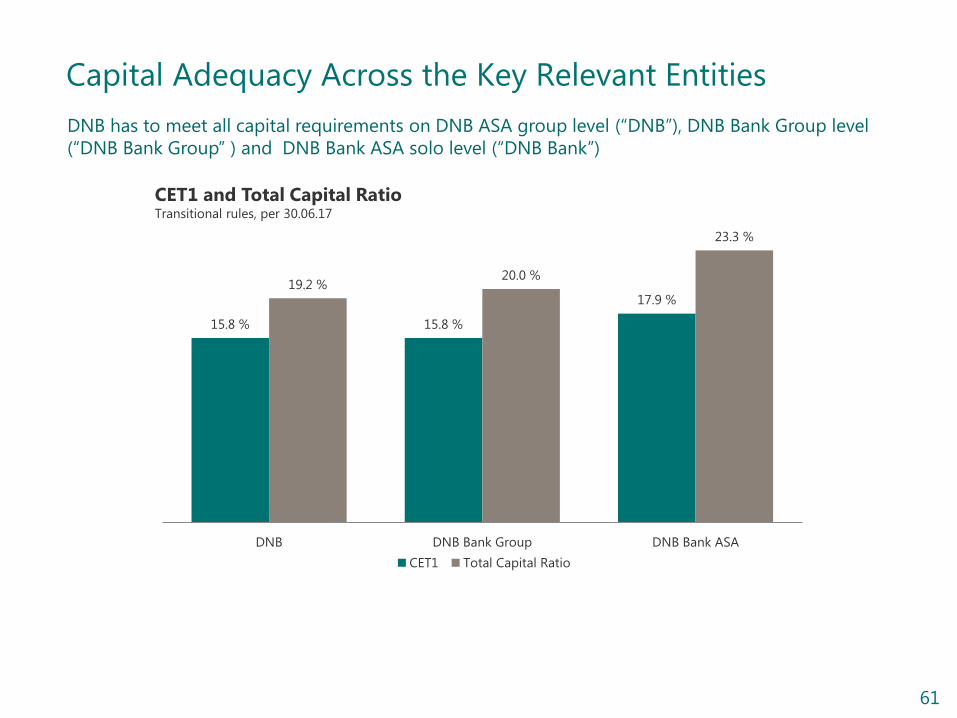

Capital Adequacy Across the Key Relevant Entities

DNB has to meet all capital requirements on DNB ASA group level (“DNB”), DNB Bank Group level

(“DNB Bank Group” ) and DNB Bank ASA solo level (“DNB Bank”)

15.8 % 15.8 %

17.9 % 19.2 %

20.0 %

23.3 %

DNB DNB Bank Group DNB Bank ASA

CET1 Total Capital Ratio

CET1 and Total Capital Ratio Transitional rules, per 30.06.17

62

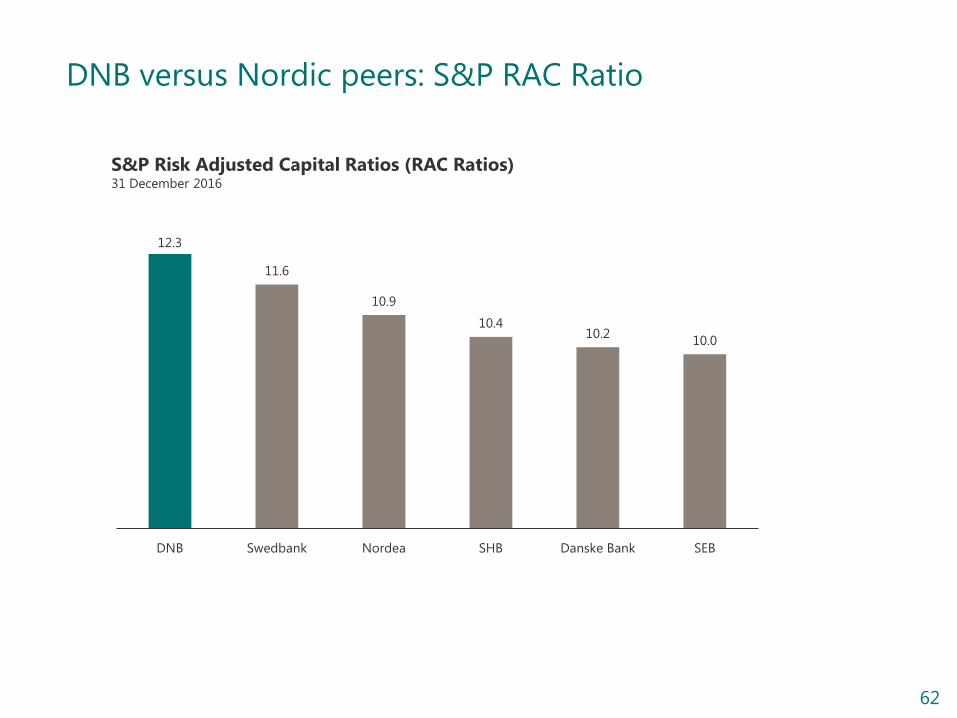

DNB versus Nordic peers: S&P RAC Ratio

12.3

11.6

10.9

10.4 10.2

10.0

DNB Swedbank Nordea SHB Danske Bank SEB

S&P Risk Adjusted Capital Ratios (RAC Ratios) 31 December 2016

63

Overall Capital Requirements under SREP

• Pillar 1 capital requirements in Norway consist of minimum requirements and

combined buffer requirements

• As a result of the SREP, the supervisors may decide on additional capital add-on (pillar

2), which together with the pillar 1 requirements form the Overall capital

requirement

• If there is a breach of the combined buffer requirements under Pillar 1, there will be

automatic restrictions on dividends etc. (ref. CRD IV article 141)

• However a breach of the Overall capital requirement under SREP will not cause

automatic restrictions:

• The Bank will have to present a plan to the NFSA how to restore the capital ratios

• If the plan is not sufficient, the NFSA will consider other measures.

• The measures will depend on the reasons behind the breach

64

Pillar 2 not Included in the MDA Trigger Level in Norway

MDA restrictions will only apply if there is a breach of the

Pillar 1 requirements

(Minimum capital requirements + Combined buffer requirements)

Pillar 2 requirements in Norway do not influence the MDA

trigger level

• Stated in a letter from the Ministry of Finance dated 15 January 2016

• Confirmed by the NFSA in a response letter dated 15 February 2016, and stated in a

circular from the NFSA dated 27 June 2016

65

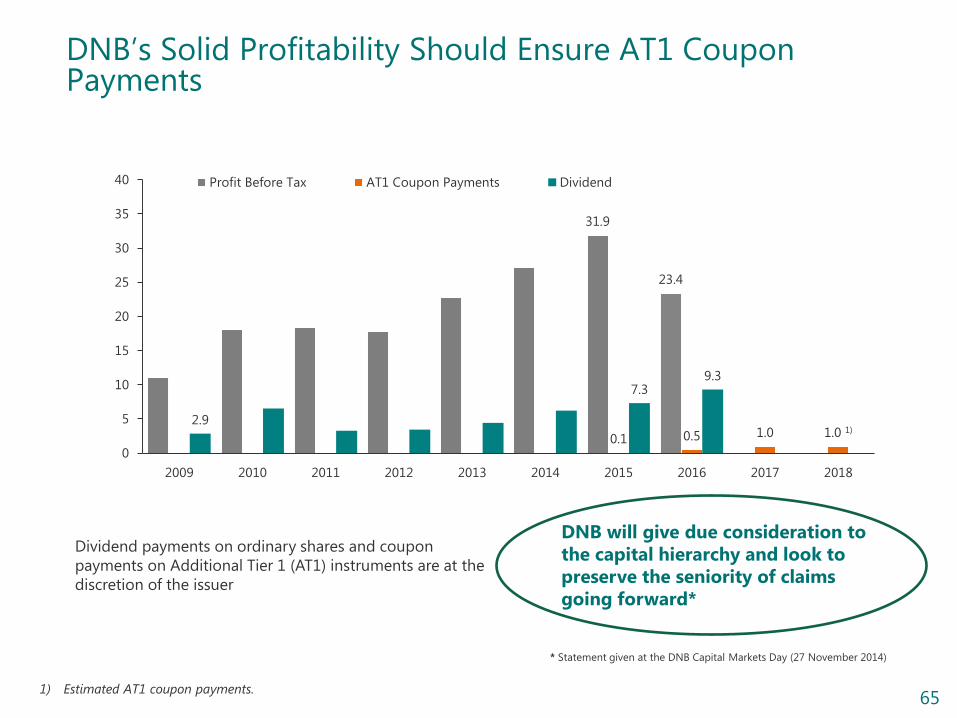

DNB’s Solid Profitability Should Ensure AT1 Coupon Payments

Dividend payments on ordinary shares and coupon

payments on Additional Tier 1 (AT1) instruments are at the

discretion of the issuer

* Statement given at the DNB Capital Markets Day (27 November 2014)

31.9

23.4

0.1 0.5 1.0 1.0 1) 2.9

7.3 9.3

0

5

10

15

20

25

30

35

40

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Profit Before Tax AT1 Coupon Payments Dividend

DNB will give due consideration to

the capital hierarchy and look to

preserve the seniority of claims

going forward*

1) Estimated AT1 coupon payments.

66

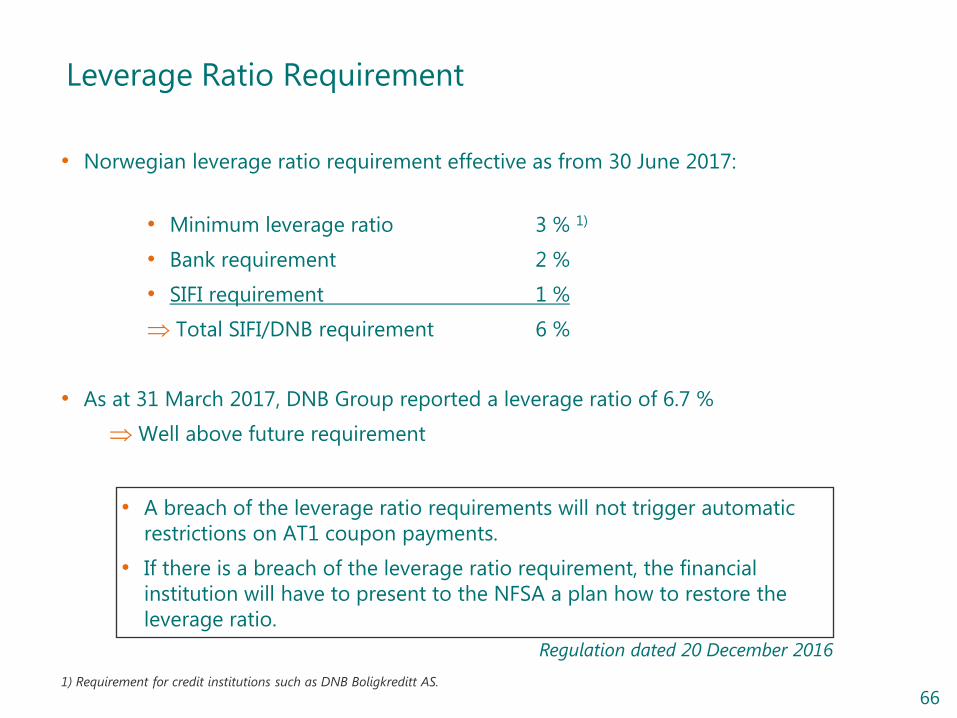

Leverage Ratio Requirement

• Norwegian leverage ratio requirement effective as from 30 June 2017:

• Minimum leverage ratio 3 % 1)

• Bank requirement 2 %

• SIFI requirement 1 %

Total SIFI/DNB requirement 6 %

• As at 31 March 2017, DNB Group reported a leverage ratio of 6.7 %

Well above future requirement

• A breach of the leverage ratio requirements will not trigger automatic

restrictions on AT1 coupon payments.

• If there is a breach of the leverage ratio requirement, the financial

institution will have to present to the NFSA a plan how to restore the

leverage ratio.

Regulation dated 20 December 2016

1) Requirement for credit institutions such as DNB Boligkreditt AS.

67

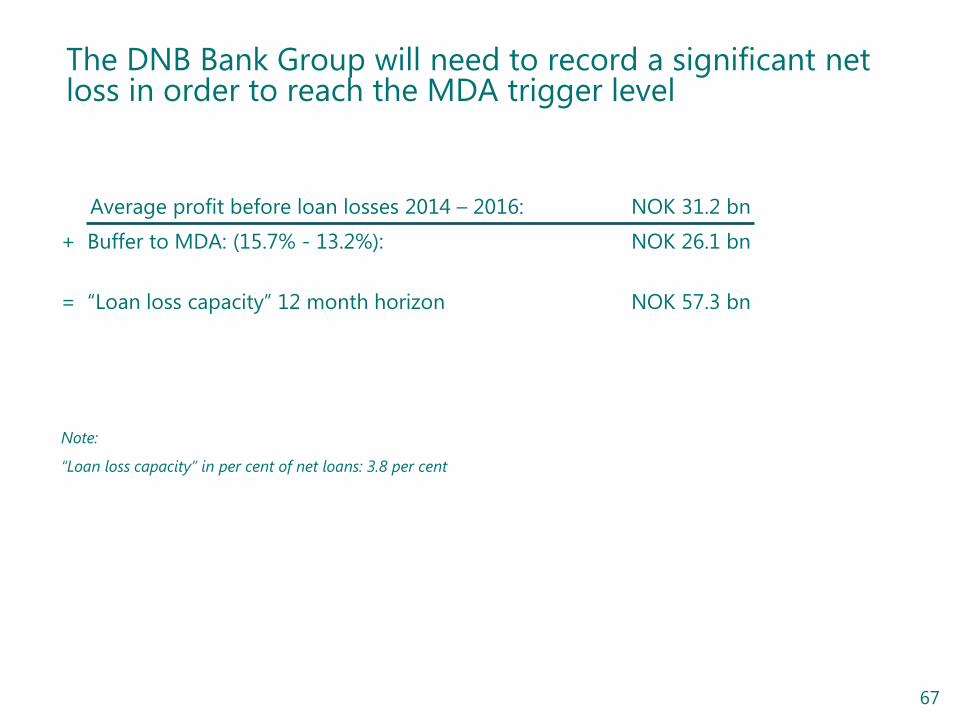

The DNB Bank Group will need to record a significant net loss in order to reach the MDA trigger level

Average profit before loan losses 2014 – 2016: NOK 31.2 bn

+ Buffer to MDA: (15.7% - 13.2%): NOK 26.1 bn

= “Loan loss capacity” 12 month horizon NOK 57.3 bn

Note:

“Loan loss capacity” in per cent of net loans: 3.8 per cent

68

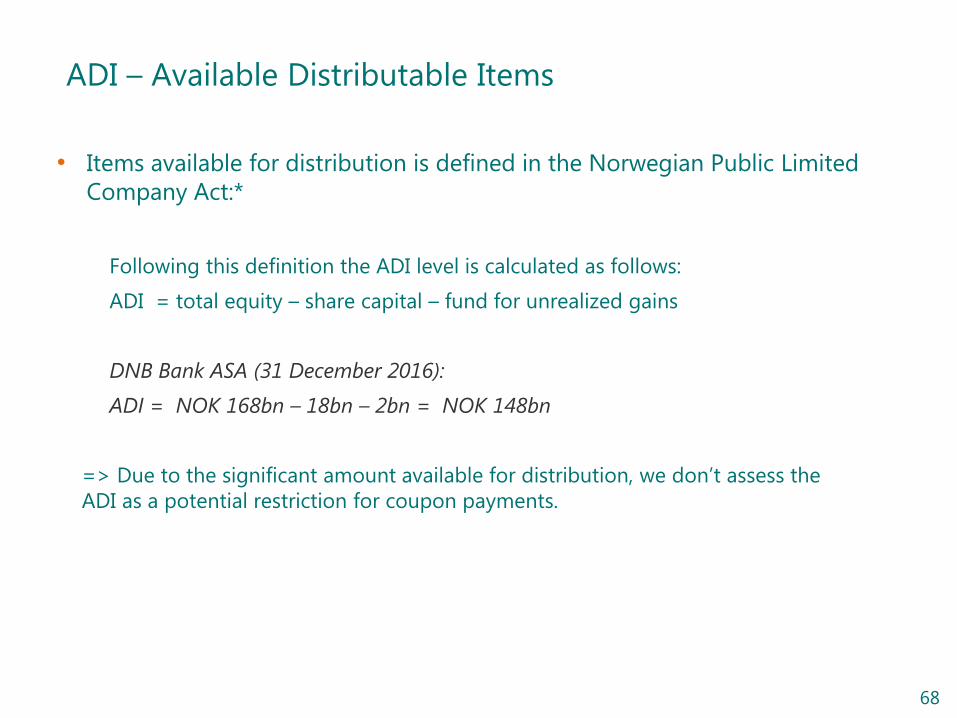

ADI – Available Distributable Items

• Items available for distribution is defined in the Norwegian Public Limited

Company Act:*

Following this definition the ADI level is calculated as follows:

ADI = total equity – share capital – fund for unrealized gains

DNB Bank ASA (31 December 2016):

ADI = NOK 168bn – 18bn – 2bn = NOK 148bn

=> Due to the significant amount available for distribution, we don’t assess the

ADI as a potential restriction for coupon payments.

69

Appendix

Appendix E:

Additional Slides

- Financial performance and Other information

70

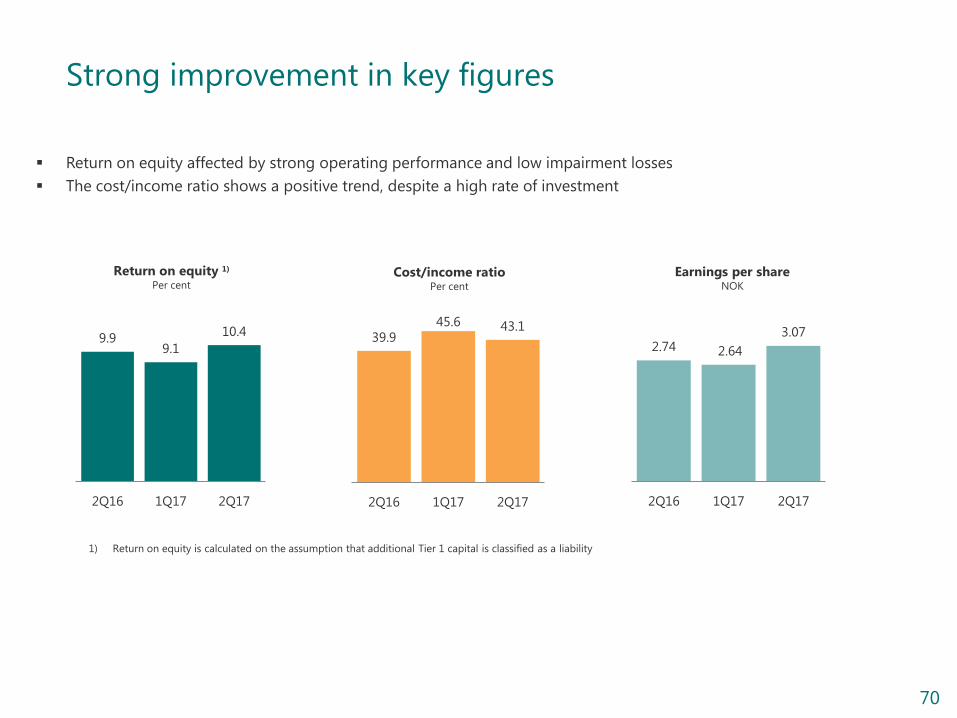

Strong improvement in key figures

39.9

45.6 43.1

2Q16 1Q17 2Q17

Cost/income ratio Per cent

Return on equity 1)

Per cent

9.9 9.1

10.4

2Q16 1Q17 2Q17

1) Return on equity is calculated on the assumption that additional Tier 1 capital is classified as a liability

2.74 2.64

3.07

2Q16 1Q17 2Q17

Earnings per share NOK

Return on equity affected by strong operating performance and low impairment losses

The cost/income ratio shows a positive trend, despite a high rate of investment

71

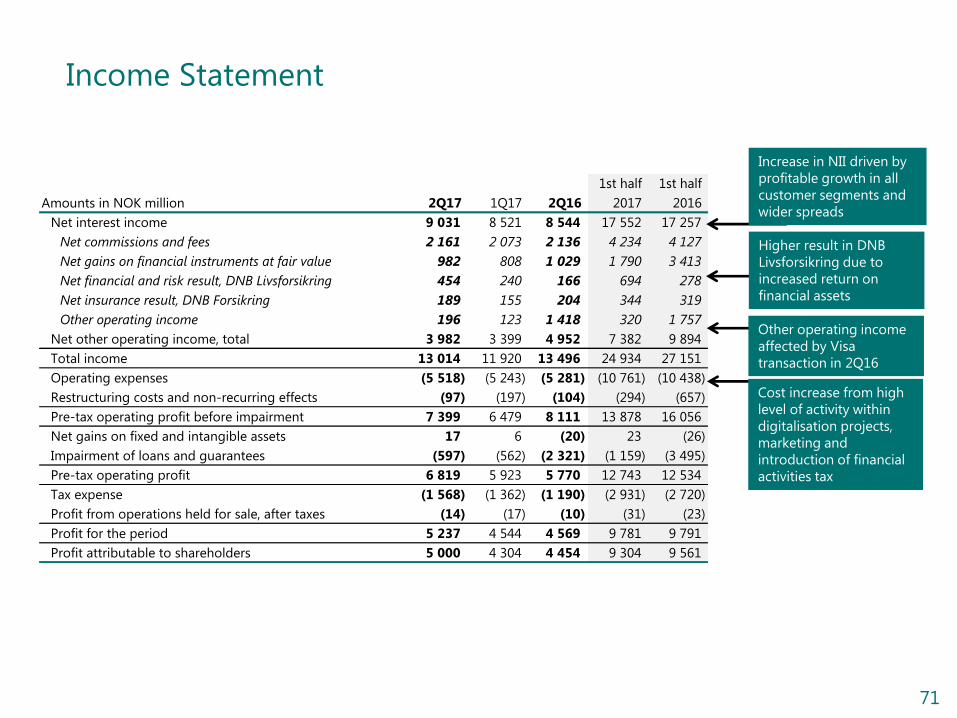

Income Statement

1st half 1st half

Amounts in NOK million 2Q17 1Q17 2Q16 2017 2016

Net interest income 9 031 8 521 8 544 17 552 17 257

Net commissions and fees 2 161 2 073 2 136 4 234 4 127

Net gains on financial instruments at fair value 982 808 1 029 1 790 3 413

Net financial and risk result, DNB Livsforsikring 454 240 166 694 278

Net insurance result, DNB Forsikring 189 155 204 344 319

Other operating income 196 123 1 418 320 1 757

Net other operating income, total 3 982 3 399 4 952 7 382 9 894

Total income 13 014 11 920 13 496 24 934 27 151

Operating expenses (5 518) (5 243) (5 281) (10 761) (10 438)

Restructuring costs and non-recurring effects (97) (197) (104) (294) (657)

Pre-tax operating profit before impairment 7 399 6 479 8 111 13 878 16 056

Net gains on fixed and intangible assets 17 6 (20) 23 (26)

Impairment of loans and guarantees (597) (562) (2 321) (1 159) (3 495)

Pre-tax operating profit 6 819 5 923 5 770 12 743 12 534

Tax expense (1 568) (1 362) (1 190) (2 931) (2 720)

Profit from operations held for sale, after taxes (14) (17) (10) (31) (23)

Profit for the period 5 237 4 544 4 569 9 781 9 791

Profit attributable to shareholders 5 000 4 304 4 454 9 304 9 561

Increase in NII driven by

profitable growth in all

customer segments and

wider spreads

Cost increase from high

level of activity within

digitalisation projects,

marketing and

introduction of financial

activities tax

Other operating income

affected by Visa

transaction in 2Q16

Higher result in DNB

Livsforsikring due to

increased return on

financial assets

72

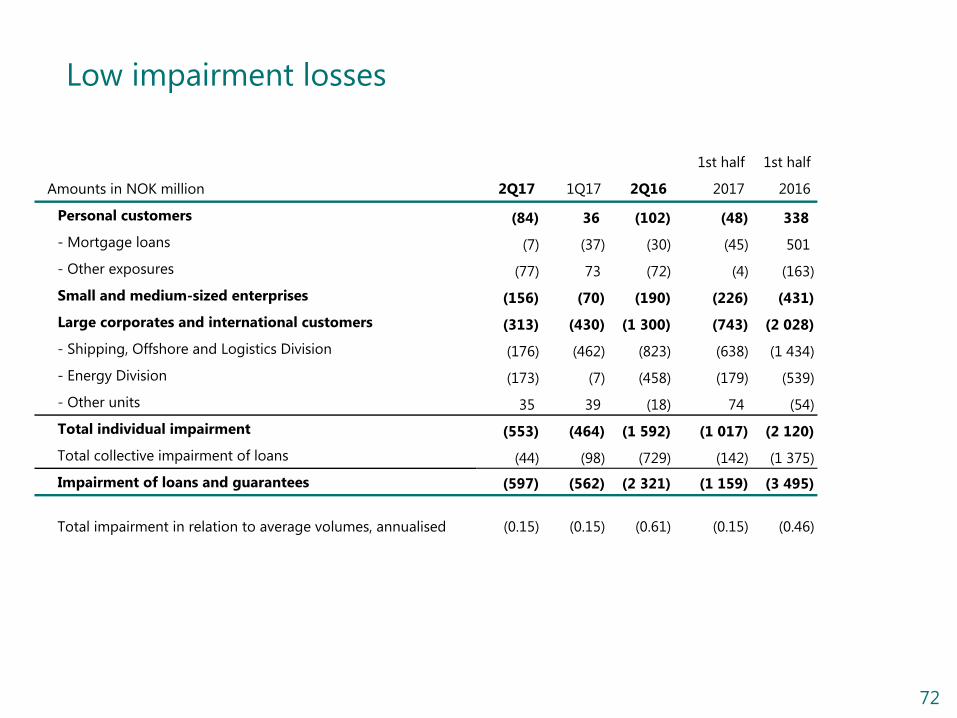

Low impairment losses

1st half 1st half

Amounts in NOK million 2Q17 1Q17 2Q16 2017 2016

Personal customers (84) 36 (102) (48) 338

- Mortgage loans (7) (37) (30) (45) 501

- Other exposures (77) 73 (72) (4) (163)

Small and medium-sized enterprises (156) (70) (190) (226) (431)

Large corporates and international customers (313) (430) (1 300) (743) (2 028)

- Shipping, Offshore and Logistics Division (176) (462) (823) (638) (1 434)

- Energy Division (173) (7) (458) (179) (539)

- Other units 35 39 (18) 74 (54)

Total individual impairment (553) (464) (1 592) (1 017) (2 120)

Total collective impairment of loans (44) (98) (729) (142) (1 375)

Impairment of loans and guarantees (597) (562) (2 321) (1 159) (3 495)

Total impairment in relation to average volumes, annualised (0.15) (0.15) (0.61) (0.15) (0.46)

73

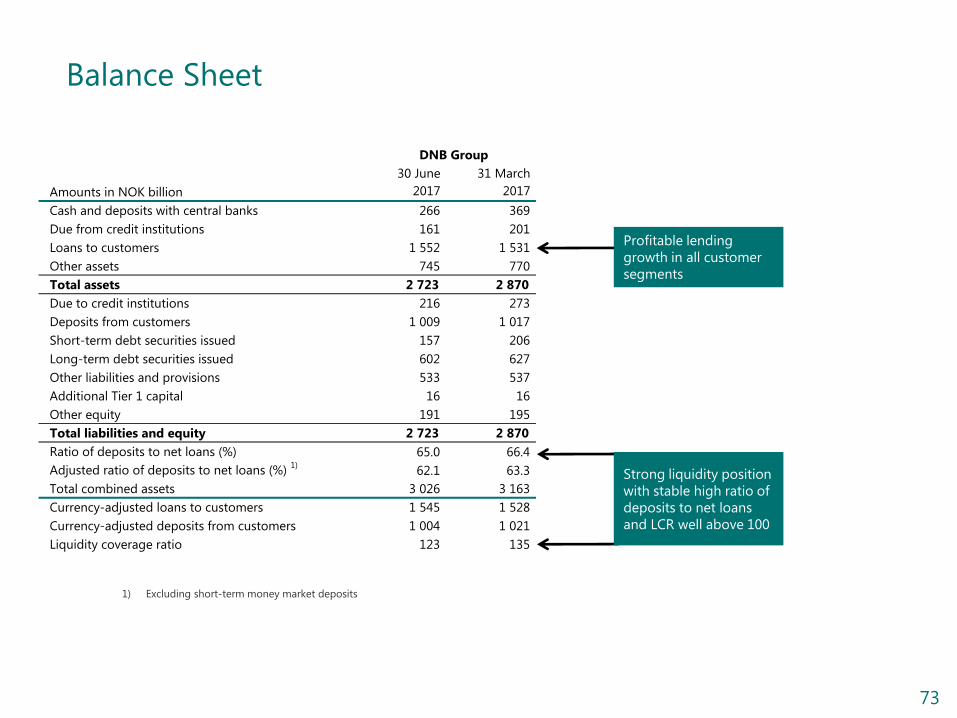

Balance Sheet

30 June 31 March

Amounts in NOK billion 2017 2017

Cash and deposits with central banks 266 369

Due from credit institutions 161 201

Loans to customers 1 552 1 531

Other assets 745 770

Total assets 2 723 2 870

Due to credit institutions 216 273

Deposits from customers 1 009 1 017

Short-term debt securities issued 157 206

Long-term debt securities issued 602 627

Other liabilities and provisions 533 537

Additional Tier 1 capital 16 16

Other equity 191 195

Total liabilities and equity 2 723 2 870

Ratio of deposits to net loans (%) 65.0 66.4

Adjusted ratio of deposits to net loans (%) 1)

62.1 63.3

Total combined assets 3 026 3 163

Currency-adjusted loans to customers 1 545 1 528

Currency-adjusted deposits from customers 1 004 1 021

Liquidity coverage ratio 123 135

DNB Group

1) Excluding short-term money market deposits

Profitable lending

growth in all customer

segments

Strong liquidity position

with stable high ratio of

deposits to net loans

and LCR well above 100

74

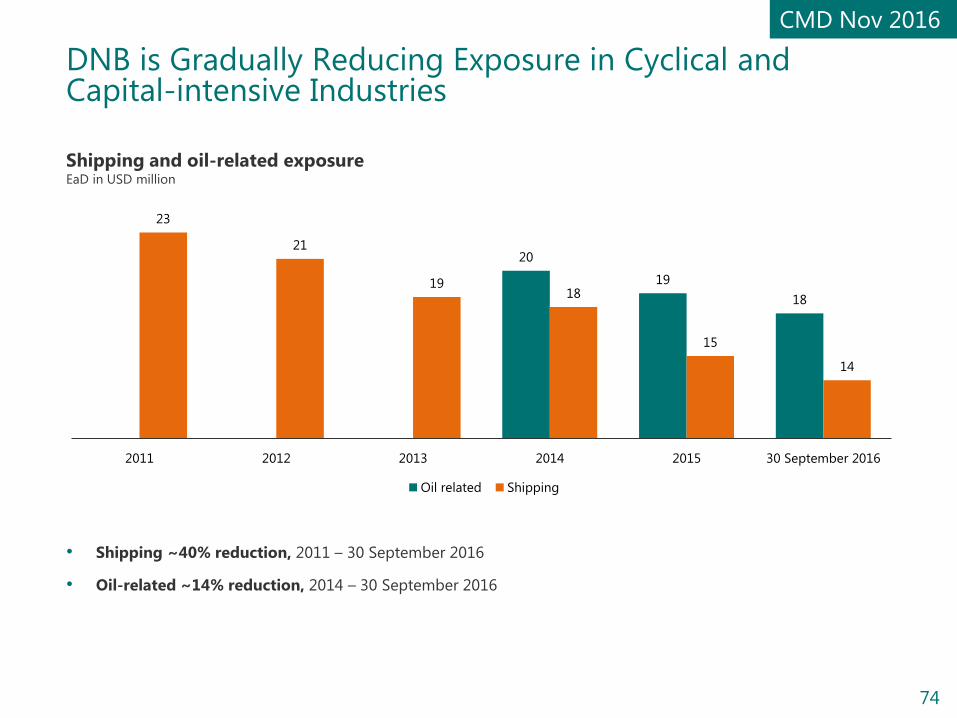

DNB is Gradually Reducing Exposure in Cyclical and Capital-intensive Industries

Shipping and oil-related exposure EaD in USD million

20

19

18

23

21

19 18

15

14

2011 2012 2013 2014 2015 30 September 2016

Oil related Shipping

• Shipping ~40% reduction, 2011 – 30 September 2016

• Oil-related ~14% reduction, 2014 – 30 September 2016

CMD Nov 2016

75

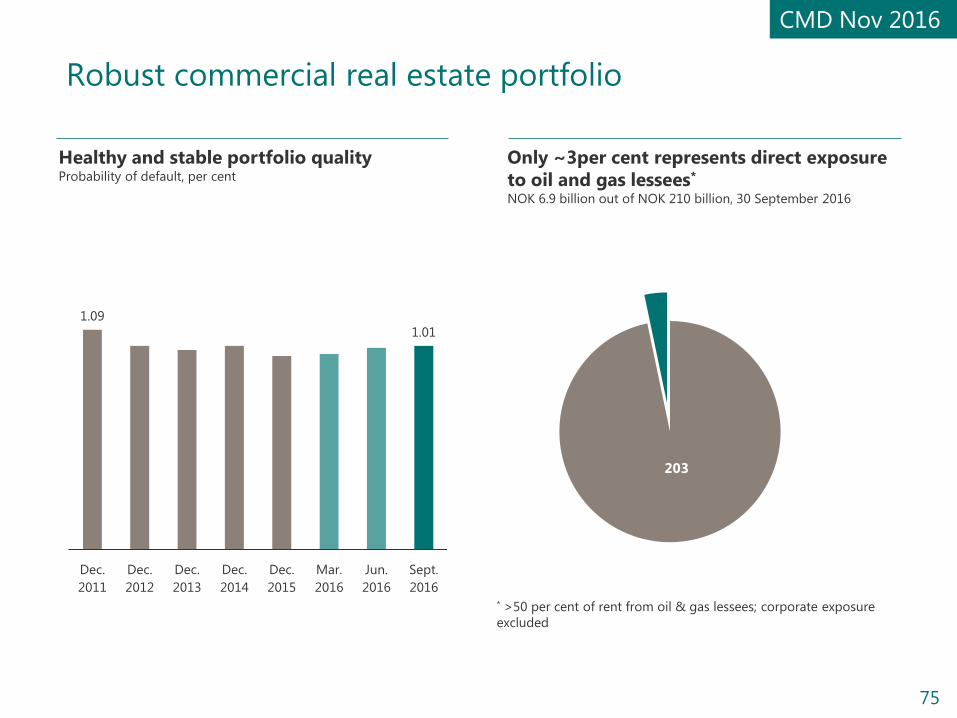

Robust commercial real estate portfolio

* >50 per cent of rent from oil & gas lessees; corporate exposure

excluded

Healthy and stable portfolio quality Probability of default, per cent

203

Only ~3per cent represents direct exposure

to oil and gas lessees*

NOK 6.9 billion out of NOK 210 billion, 30 September 2016

1.09

1.01

Dec.

2011

Dec.

2012

Dec.

2013

Dec.

2014

Dec.

2015

Mar.

2016

Jun.

2016

Sept.

2016

CMD Nov 2016

76

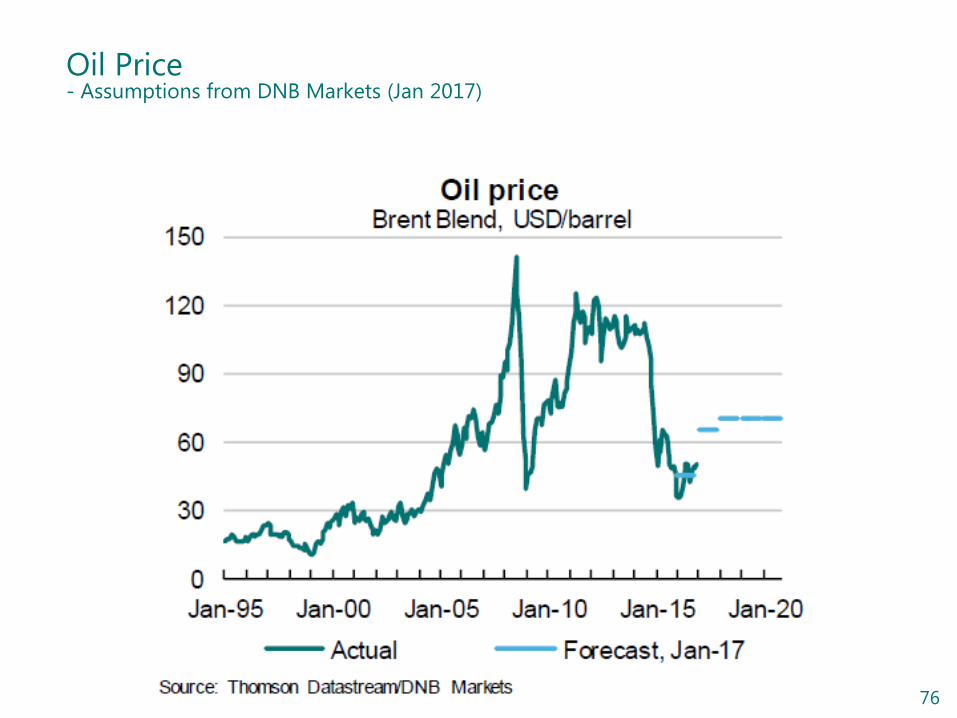

Oil Price - Assumptions from DNB Markets (Jan 2017)

77

Disclaimer

• This material has been prepared on the basis of the information provided by DNB Bank ASA (referred to as "DNB Bank") and public available sources. DNB ASA – the holding company of the DNB group is referred to as "DNB " in this presentation.

• This material is presented solely for information purposes and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments and should not be treated as giving investment advice. It has no regard to the specific investment objectives, financial situation or particular needs of any recipient. No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein. It should not be regarded by recipients as a substitute for the exercise of their own judgment. Any opinions expressed in this material are subject to change without notice and DNB Bank is not under any obligation to update or keep current the information contained herein. In addition, institutions mentioned in this material, their affiliates, agents, directors, partners and employees may make purchases and/or sales of the Notes as principal or agent or may act as market maker or provide investment banking or other services in respect of the Program or the Notes which may be issued from time to time thereunder. DNB, the Arranger and the Dealers and their respective affiliates, agents, directors, partners and employees accept no liability whatsoever for any loss or damage of any kind arising out of the use of all or any part of this material.

• The Notes are not to be offered or sold in any jurisdiction in circumstances in which the distribution of this document or the Notes would be prohibited in such jurisdiction. This document must not be acted on or relied on by persons who are not eligible to invest in the Notes. Any investment or investment activity to which this communication relates is available only to persons eligible to invest in the Notes and will be engaged in only with such persons.

• Furthermore, you should consult with your own legal, regulatory, tax, business, investment, financial and accounting advisers to the extent that you deem it necessary, and make your own investment, hedging and trading decisions (including decisions regarding the suitability of an investment in the Notes which may be offered from time to time) based upon your own judgment and advice from such advisers as you deem necessary and not upon any view expressed in this presentation.