document of the world bankdocuments.worldbank.org/curated/en/... · document of the world bank ....

TRANSCRIPT

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No. 58499-MOR

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

PROGRAM DOCUMENT

FOR A PROPOSED LOAN

IN THE AMOUNT OF EURO 150 MILLION

(US$205 MILLION EQUIVALENT)

TO

THE KINGDOM OF MOROCCO

FOR A

FIRST DEVELOPMENT POLICY LOAN IN SUPPORT OF THE

PLAN MAROC VERT

February 10, 2011

Sustainable Development Department Middle East and North Africa Region

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

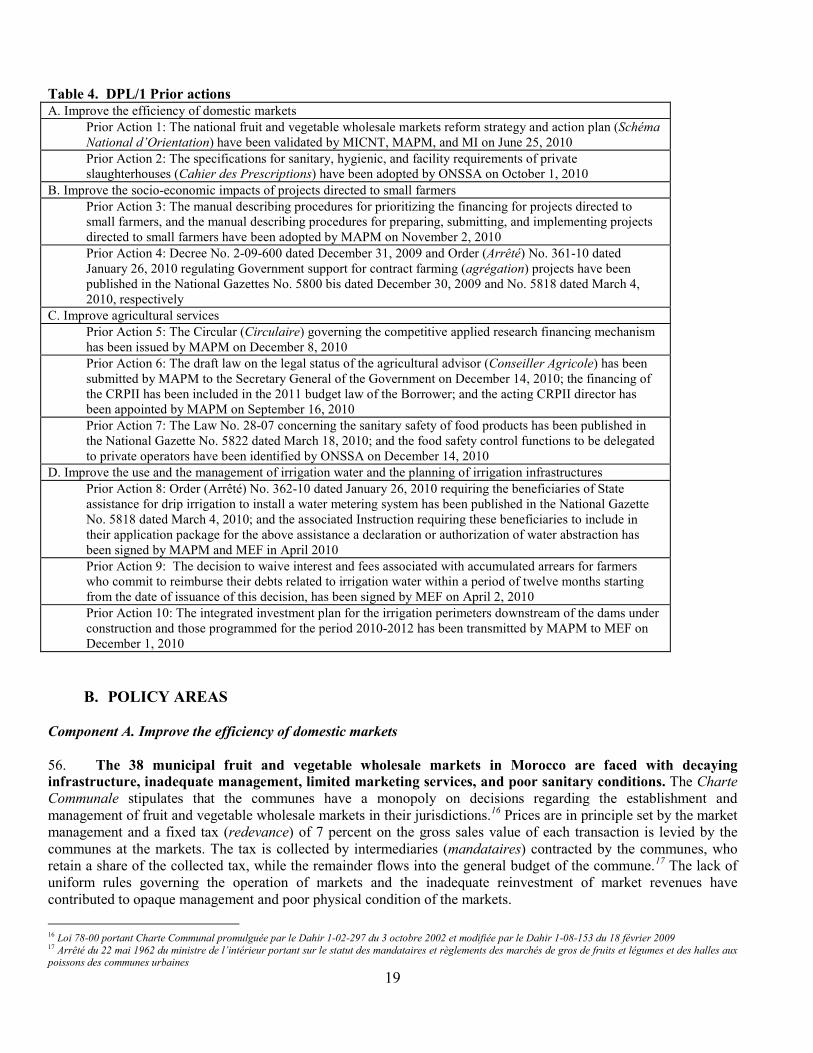

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

i

Morocco - GOVERNMENT FISCAL YEAR January 1st – December 31st

CURRENCY EQUIVALENTS (Exchange Rate Effective as of January 26th, 2011)

Currency Unit Moroccan Dirham Euro

US$1.00 MAD 8.21 €0.73

ABBREVIATION AND ACRONYMS

ADA Agricultural Development Agency (Agence pour le Développement Agricole)

AFD French Development Agency (Agence Française de Développement) AfDB African Development Bank AREF Regional Education and Training Academy (Académie Régionale

d'Education et de Formation) BAM Central Bank of Morocco (Bank Al-Maghrib) CDA Agricultural Development Center (Centre de Développement

Agricole) CFAA Country Financial Accountability Assessment CPAR Country Procurement Assessment Review CPS Country Partnership Strategy CRPII Pillar II Resources Center (Centre des Ressources Pilier II) CSM Council for Strategic Monitoring CT Centers of Works (Centres des Travaux) DPA Provincial Agricultural Directorate (Direction Provinciale de

l’Agriculture) DPL Development Policy Loan DRA Regional Agricultural Directorate (Direction Régionale de

l’Agriculture) DSS Strategy and Statistics Directorate (Direction de la Stratégie et des

Statistiques) EIA Environmental Impact Assessment EU European Union FAO Food and Agriculture Organization of the United Nations FDA Agricultural Development Fund (Fonds de Développement Agricole) FDI Foreign Direct Investment FDR Rural Development Fund (Fonds de Développement Rural) FSAP Financial Sector Assessment Program FTA Free Trade Agreement GDP Gross Domestic Product GEF Global Environment Facility GoM Government of Morocco HACCP Hazard Analysis and Critical Control Point IBRD International Bank for Reconstruction and Development IFAD International Fund for Agricultural Development IMF International Monetary Fund INDH National Initiative for Human Development (Initiative Nationale

pour le Développement Humain) INRA National Institute for Agronomic Research (Institut National de la

Recherche Agronomique) ISO International Standards Organization

ii

KfW German Development Bank LSI Large Scale Irrigation M&E Monitoring and Evaluation MAD Moroccan Dirham MAEG Ministry of Economic and General Affairs (Ministère des Affaires

Economiques et Générales) MAPM Ministry of Agriculture and Maritime Fisheries (Ministère de

l’Agriculture et de la Pêche Maritime) MCC Millenium Challenge Corporation MENA Middle East and North Africa MEF Ministry of Economy and Finance (Ministère de l’Economie et des

Finances) MET Ministry of Infrastructure and Transportation (Ministère de

l’Équipement et du Transport) MI Ministry of Interior (Ministère de l’Intérieur) MICNT Ministry of Industry, Commerce, and New Technologies (Ministère

de l’Industrie, du Commerce et des Nouvelles Technologies) MMEWE Ministry of Mines, Energy, Water and Environment (Ministère des

Mines, de l’Energie, de l’Eau et de l’Environnement) MTEF Medium-Term Expenditure Framework (Cadre de Dépenses à

Moyen Terme) ONSSA National Food Safety Agency (Office National de Sécurité Sanitaire

des Produits Alimentaires) OPA Professional Agriculture Organization (Organisation Professionnelle

Agricole) ORMVA Public Agricultural Development Agency (Office Régional de Mise

en Valeur Agricole) PAR Regional Agricultural Plan (Plan Agricole Régional) PARL Public Administration Reform Loan PEFA Public Expenditure and Financial Accountability PFM Public Financial Management System PMV Green Morocco Plan (Plan Maroc Vert) PNEEI National Program of Irrigation Water Conservation (Programme

National d'Economie d'Eau en Irrigation) PPPs Public Private Partnerships PSIA Poverty and Social Impact Analysis SCCF Special Climate Change Fund SEAT State Secretariat for Territorial Planning (Secrétariat d'Etat chargé

de l'Aménagement du Territoire) SEEE State Secretariat for Water and Environment (Secrétariat d’Etat

chargé de l’Eau et de l’Environnement) SEP Social and Economic Program SOE State-Owned Enterprise TA Technical Assistance UCS Use of Country System USAID United States Agency for International Development VAT WMSs

Value-Added Tax Wholesale Market and Slaughterhouses

Vice President:

Country Director: Sector Director:

Task Team Leader:

Shamshad Akhtar Simon Gray Laszlo Lovei Julian A. Lampietti

iii

MOROCCO

SUPPORT PLAN MAROC VERT DPL

TABLE OF CONTENTS LOAN AND PROGRAM SUMMARY....................................................................................................................... i I. INTRODUCTION ................................................................................................................................................ 1 II. COUNTRY CONTEXT ....................................................................................................................................... 1

A. RECENT ECONOMIC DEVELOPMENTS IN MOROCCO ................................................ 5 B. MACROECONOMIC OUTLOOK AND DEBT SUSTAINABILITY .................................. 8

III. THE GOVERNMENT’S PROGRAM AND PARTICIPATORY PROCESSES ......................................... 11 IV. BANK SUPPORT TO THE GOVERNMENT’S PROGRAM ....................................................................... 14

A. LINKS TO THE CPS ............................................................................................................ 14 B. COLLABORATION WITH THE IMF AND OTHER DONORS ........................................ 14 C. RELATIONSHIP TO OTHER BANK OPERATIONS ........................................................ 15 D. LESSONS LEARNED .......................................................................................................... 15 E. ANALYTICAL UNDERPINNINGS .................................................................................... 17

V. FIRST DEVELOPMENT POLICY LOAN IN SUPPORT OF THE PLAN MAROC VERT .................... 18 A. OPERATION DESCRIPTION ............................................................................................. 18 B. POLICY AREAS .................................................................................................................. 19 Component A. Improve the efficiency of domestic markets .......................................................... 19 Component B. Improve the socio-economic impacts of projects directed to small farmers ........... 22 Component C. Improve agricultural services ................................................................................. 24 Component D. Improve the use and the management of irrigation water and the planning of irrigation infrastructure ................................................................................................................... 28

VI. OPERATION IMPLEMENTATION ............................................................................................................... 31 A. POVERTY AND SOCIAL IMPACT ................................................................................... 31 B. ENVIRONMENTAL ASPECTS .......................................................................................... 32 C. IMPLEMENTATION, MONITORING AND EVALUATION ........................................... 33 D. FIDUCIARY ASPECTS ....................................................................................................... 34 E. RISKS AND RISK MITIGATION ....................................................................................... 35

VII. ANNEXES ........................................................................................................................................................... 37 A. ANALYTICAL AND ADVISORY WORK ......................................................................... 37 A. Domestic Markets .................................................................................................................. 37 B. Agricultural Investment Support ........................................................................................... 37 C. Agricultural Services ............................................................................................................. 38 D. Irrigation Water .................................................................................................................... 38 B. LETTER OF DEVELOPMENT POLICY ............................................................................ 39 C. PROPOSED POLICY MATRIX .......................................................................................... 59 D. PROPOSED RESULTS MONITORING AND EVALUATION FRAMEWORK ................................ 62 E. MOROCCO FISCAL SUSTAINABILITY ANALYSIS ...................................................... 64

This Loan was prepared by an IBRD team consisting of: Julian Lampietti (Task Team Leader), Mohammed Medouar (Rural Development Specialist), Hassan Lamrani (Irrigation Specialist), Gabriella Izzi (Agriculture and Climate Change Specialist), Andrea Liverani (Social Development Specialist), Stefano Paternostro (Country Economist), Khalid El Massnaoui (Senior Economist), Gael Gregoire (Environment Specialist), Jean-Charles De Daruvar (Lawyer), Anas Abou El Mikias (Financial Management Specialist), Abdoulaye Keita (Procurement Specialist), Anwar Soulami (Communications Specialist), Nabil Chaherli (Agricultural Economist), Emmanuel Hidier (Markets Specialist, FAO), Fabio Maria Santucci (Agricultural Services Consultant, FAO), Philip Van der Celen (Agricultural Policy and Operations Consultant, FAO), Eavan O’Halloran (Senior Country Officer), Françoise Clottes (Country Director), Hocine Chalal (Regional Safeguards Advisor), and Hassine Hedda (Finance Officer). The team worked under the guidance of Simon Gray (Country Director), Laszlo Lovei (Sector Director), and Luis Constantino (Sector Manager).

i

LOAN AND PROGRAM SUMMARY

MOROCCO

FIRST DEVELOPMENT POLICY LOAN IN SUPPORT OF THE PLAN MAROC VERT

Borrower Kingdom of Morocco

Implementing Agency

Ministry of Economy and Finance (MEF) and Ministry of Agriculture and Maritime Fisheries (MAPM)

Financing Data EURO150 million Operation Type

The proposed operation is the first DPL in a programmatic series of 2 single-tranche DPLs

Main Policy Areas

• Domestic Markets • Agricultural Investment Support • Agricultural Services • Irrigation Water

Key Outcome Indicators

The key outcome indicators for the programmatic series of DPLs are detailed in Annexes C and D, and summarized below: A. Improve the efficiency of domestic markets: (i) Number of fruit and vegetable wholesale markets under new management model launched; (ii) Number of private slaughterhouses launched; and (iii) Number of slaughterhouse concessions under new management model launched B. Improve the socio-economic impacts of projects directed to small farmers: (i) Share of new Pillar II projects submitted by Professional Agriculture Organizations (OPA); and (ii) Share of small farmers benefitting from Pillar II projects C. Improve agricultural services: (i) Share of research and extension projects funded through the competitive financing mechanism; (ii) Number of public-private partnerships for agricultural extension created; (iii) Number of training days per category of actor; (iv) Number of Hazard Analysis and Critical Control Point (HACCP)-certified agri-food processing establishments; and (v) Number of sanitary alerts notified by commercial partners (third countries) / number of shipment of products (number of certificates produced) D. Improve the use and the management of irrigation water and the planning of irrigation infrastructures: (i) Percentage increase of the number of declarations and authorization of water abstraction received / delivered; (ii) Cumulated number of farmers participating in projects of collection reconversion to drip irrigation; (iii) Share of Operation and Maintenance costs covered by irrigation water tariffs in seven Public Agricultural Development Agencies (ORMVAs); and (iv) Number of irrigation schemes located downstream of dams under construction or programmed with allocated resources / number of dams with agricultural scope under construction or programmed with allocated resources

Program Development Objectives and Contribution to CPS

The proposed loan is the first in a programmatic series of 2 single-tranche loans designed to support the implementation of the Government’s Plan Maroc Vert (PMV) program. The objectives of

ii

the series are to: (i) Improve the efficiency of domestic markets; (ii) Improve the socio-economic impacts of investments directed to

small farmers; (iii) Improve agricultural services; and (iv) Improve the use and the management of irrigation water and the

planning of irrigation infrastructures. The proposed DPL series is a key component of the new Country Partnership Strategy (CPS) (FY10-FY13). It addresses three long term development challenges facing Morocco identified in the CPS: (i) Enhancing growth and employment; (ii) Reducing social disparities; and (iii) Ensuring sustainability. It contributes directly to the three pillars around which the Bank’s program is structured: (i) Growth, competitiveness, and employment; (ii) Service delivery to citizens; and (iii) Sustainable development in a changing climate. Furthermore, it is linked to the two cross-cutting themes of governance and territoriality.

Risks and Risk Mitigation

Government commitment to agriculture sector reform may weaken. There is a risk that DPL/2 does not materialize due to a weakening of Government commitment to sector reform. This is unlikely given the strong commitment to the implementation of the PMV by His Majesty the King and by the Government. Morocco’s Advanced Association Status with the EU and bilateral agricultural trade liberalization will help maintain momentum of sector reforms. MAEG has set up an inter-ministerial committee to coordinate the actions of all stakeholders of the project. Some of the proposed reforms may be opposed by vested interests and marginalized stakeholders. This is most likely to occur in relation to reforms associated with domestic markets, and tariff adjustments for irrigation water. Specific measures to mitigate these risks are identified in the PSIA and incorporated in the program design. In the short term, Morocco is confronted with uncertainties on the timing, speed and shape of the recovery process from the global crisis. Spill-overs from the global credit turmoil have so far remained limited as external debt is relatively low and long-term, and macroeconomic policies have been strengthened. In addition, the Moroccan banking sector is generally stable, adequately capitalized, profitable, and resilient to shocks. However, it is too early to predict how the global economy will emerge from the recession particularly in the EU. Consequently, it is not yet clear to what extent Morocco’s economy will continue to be confronted with the impact of the economic slowdown on its exports, remittances, ability to attract FDI and sustainability of its public stimulus program. The associated economic risks can be partly mitigated through continued strong macroeconomic management and Morocco’s track record suggests that it is well placed to face the uncertainties of the current situation. This risk will be mitigated through continued monitoring and dialogue with the authorities on

iii

the overall macroeconomic context, as well as analysis of options for remedial measures as requested. In the medium term, Morocco’s overall outlook is positive but predicated on the effectiveness of the set of reforms currently under way in several sectors. Should the current reform efforts take longer than anticipated, it is uncertain if the current economic structure can sustain the pre-crisis economic growth performance in the medium term. This potential risk is mitigated by Government’s strong commitment to proceed with the envisaged reforms as well as the Bank engagement in multiple related sectors including financial sector, energy sector, business environment, and the water sector. Morocco remains susceptible to chronic drought. The dependence of Morocco agriculture on rainfed yields, particularly for poor and vulnerable farmers, coupled with increased water scarcity and climate change poses long run concerns for the agriculture sector. The Government is aware of the situation and is developing an integrated strategy to address climate change issues. The Bank is supporting this effort with programmatic work on climate change as well as a Special Climate Change Fund (SCCF) / Global Environment Facility (GEF) grant integrating climate change adaptation into the PMV.

Operation ID P116557

1

IBRD PROGRAM DOCUMENT FOR A

FIRST DEVELOPMENT POLICY LOAN IN SUPPORT OF THE PLAN MAROC VERT TO THE KINGDOM OF MOROCCO

I. INTRODUCTION 1. This Program Document proposes a first Development Policy Loan (DPL) in support of the Plan Maroc Vert to the Kingdom of Morocco. The proposed operation is the first of a programmatic series of two single-tranche DPLs. It follows a request by the Government of Morocco (GoM) in February 2009 and confirmed in January 2010. The loan supports the implementation of four components of the agri-food sector investments and reforms outlined in the Plan Maroc Vert (PMV), the GoM’s agricultural development strategy for the period 2008-2020. These components include: (i) domestic markets; (ii) agricultural investment support; (iii) agricultural services; and (iv) irrigation water. The objectives of the operation structured around these four components are to: (i) improve the efficiency of domestic markets; (ii) improve the socio-economic impacts of projects directed to small farmers; (iii) improve agricultural services; and (iv) improve the management of irrigation water and the planning of irrigation infrastructures. 2. The program supports an ambitious government initiative in the agriculture sector and builds on extensive dialogue between the World Bank and the GoM and is underpinned by a large body of analytical work and sector operations. The proposed program has benefited from a broad range of analytical work recently completed by the World Bank and others. Key analytical activities completed by the World Bank include economic and sector work, policy notes, and topical research and analysis covering strategic themes such as agri-food trade, wholesale markets and food security, agricultural subsidy schemes, contract-farming, land markets, rural poverty, climate change adaptation, and territorial development. The program also builds on the outcomes and experience from past and ongoing Bank operations in water and irrigation, integrated rural development, human development, and public sector administration reform. Additional value added of the World Bank includes bringing global best practice lessons to the implementation of the PMV as well as encouraging inter-ministerial dialogue.

3. The policy framework supported by this program is helping the Ministère de l’Agriculture et de la Pêche Maritime (MAPM) inform, focus, and leverage the support of other donors and the private sector. A large number of multilateral and bilateral donors are mobilizing around the investment agenda set out by the PMV. Key players include the Millennium Challenge Corporation (MCC), European Union (EU), African Development Bank (AfDB), French Development Agency (AFD), International Fund for Agricultural Development (IFAD), Belgian Cooperation (BC), the German Development Bank (KfW), and the Food and Agriculture Organization (FAO). Most of the programs under development will support the implementation of Pillar II investment projects in specific agri-food chains (filières) in certain Regions or focus on capacity-building activities related to the Pillar II investment program and sustainable natural resource management.

II. COUNTRY CONTEXT1

4. Over the last decade, Morocco carried out sound macroeconomic policies and continued to sustain momentum of structural reforms. As a result, the growth pattern shifted to a higher level averaging 5.1 percent over 2001-09, almost double of the average rate of the 1990s (2.8 percent). The good growth performance allowed the Gross Domestic Product (GDP) per capita to almost double over the last decade to reach US$2,890 in 2009. Furthermore, sound fiscal policies led to the consolidation of public finances, allowing the budget to run surpluses in 2007 and 2008 (averaging 0.3 percent of GDP) and to withstand well in 2009 the impact of the global crisis, with a

1 Unless otherwise indicated, all estimations and projections of economic indicators are those of the World Bank. All historical data are those of the government.

2

manageable budget deficit of 2.2 percent of GDP. The Government adopted a prudent debt strategy and debt of the Treasury steadily declined to 46.9 percent of GDP in 2009 from 62 percent in 2005. In addition, the monetary authorities pursued appropriate monetary policy geared toward maintaining low and stable inflation (an average 2.2 percent since 2005) and enhanced financial sector supervision. Furthermore, the country sought to deepen its integration into the world economy through the signing of many Free Trade Agreements (FTAs) culminating with the recent “Advanced Status” awarded by the EU. Overall, these efforts have led to a stable macroeconomic stance, stronger public finances, and a sound financial sector. On the basis of these achievements, Morocco gained “investment grade” rating in 2007 from Fitch, which was confirmed again in 2009 and 2011. In March 2010, it received the “Investment grade” again from Standard & Poor (BBB- with stable outlook) which further reinforced the confidence of investors, both domestic and foreign. 5. With the involvement of the private sector Morocco designed and is implementing specific sector strategies to increase investment and employment in sectors of the economy with high growth potential. Thus, investment in these sectors has increased, strengthening the fundamentals of the economy. While gross investment hovered around 25 percent of GDP on average in the 1990s, it increased rapidly in the 2000s, to reach an outstanding rate of 36 percent of GDP in 2009 with strong participation of the private sector and State-Owned Enterprises (a share of 64 percent of the total) (Figure 1). High Foreign Direct Investments (FDI) inflows (an average 4.5 percent of GDP over the last five years) also contributed to reinforce gross investment. These higher investment rates geared to dynamic sectors led to improved diversification and growth potential of the Moroccan economy, and reduced volatility.2

Higher investment also improved the employment situation with the number of jobless shrinking to 9.1 percent in 2009, although efforts are necessary to further reduce unemployment among young people, especially those with a degree.

6. Reforms triggered positive changes in the Moroccan economic structure but manufacturing is losing momentum. The structure of production changed in favor of services and this to the disadvantage of both primary and secondary sectors’ shares in GDP declining over time. The shrinking of the secondary sector’s share is mainly due to falling manufacturing which has steadily declined over the last two decades, denoting some weaknesses at the level of the productive tissue that reduces its productive capacity and hinders its long term growth and development. This weakness stems from the slow structural transformation in the manufacturing sector, which also explains the modest results of Moroccan exports. The latter continue to be concentrated around relatively undiversified, low knowledge, low value-added, traditional products. As a consequence, exports do not fully benefit from trade dynamics of Morocco’s trade partners and thus have been unable to fulfill their potential for contributing to growth and job creation.

7. The agri-food sector is an important pillar of the Moroccan economy. Representing 15 percent of Morocco’s GDP and 23 percent of the country’s exports, and employing close to half of the labor force, the agri-food sector (together with the forestry and fishing) is a pillar of the Moroccan economy. In the rural areas it is the primary source of employment and income for about 80 percent of the labor force. Although rural poverty decreased from 25 percent in 2001 to 14 percent in 2007 largely due to the combined effect of increases in the value of agricultural production, diversification of the rural economy, and increases in remittances, the contribution to overall inequality of the gap between rural and urban living standards in Morocco is the highest of any Middle East and North Africa

2 The standard deviation of growth rates in the 2000s is three and half times less than in the 1990s.

Figure 1. Rising investment, in percent of GDP

Source: Moroccan Government and Staff estimates.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2004 2005 2006 2007 2008 2009

Private & SOEs Households Public Administration

Changes in stock FDI (right axis)

3

(MENA) country. In fact, poverty rates in rural areas are almost 3 times as high as in urban areas and 70 percent of poverty in Morocco remains rural. With a Gini coefficient of 0.6, land remains inequitably distributed: a majority of low-productivity smallholders owns only 26 percent of cultivated land, while a minority of less than one percent of mostly commercial and export-oriented farms owns about 14 percent. 8. Despite some successes in selected commodities, the agri-food sector’s growth potential is constrained by the dualistic nature of farming in Morocco. The vast majority of the 1.5 million agricultural holdings are semi-subsistence farms that have low productivity and product quality levels and limited market integration. These farms are small (70 percent are less than 5 hectares) and largely rainfed and vulnerable to recurrent droughts. They often have aging household heads with a low education level (more than 45 percent of the heads of farming families are over 55 years old, and 81 percent are illiterate), make limited use of modern technologies, and lack technical know-how. In order to meet their food consumption and animal feed needs and partially in response to the incentives provided by Government subsidy schemes and market protection, smallholders typically engage in the production of low-value agricultural commodities such as wheat and barley. This large group of smallholder farmers co-exists with a small but very efficient group of commercial farmers producing crops (such as citrus, tomatoes, strawberries, grapes, melons, and peppers) for high-value export markets and milk for domestic markets. This sub-sector of mainly irrigated production accounts for 7 percent of GDP, 50 percent of Morocco’s agricultural value added, generates over 75 percent of Morocco’s agricultural exports, and provides jobs to 50 percent of the rural labor force. 9. This duality was partly a result of policies that have limited the opportunities of traditional agriculture and smaller farmers. First, an antiquated legislative system of commercialization of certain agricultural products designed to raise municipal revenues raises the cost and lowers the quality of fruits, vegetables and meat. The results are lower producer and higher consumer prices and reduced incentives for quality and value-addition. Second, the effectiveness of the traditional support (extension, credit, technology), particularly for small farmers, has eroded due to the absence of an integrated approach that the takes account of the links between production and marketing, availability of adequate technical support and attention to quality of the products. Third, the participation of the farmers and communities in the design and implementation of support policies has been limited, with a centralized approach dominating.

10. Morocco launched a transformative agricultural development strategy - the Plan Maroc Vert (PMV) for the period 2008-2020. The PMV is an ambitious strategy that aims to transform the agri-food sector into a stable source of growth, competitiveness, and broad-based economic development in rural areas through a combination of agricultural investments and systemic public sector reforms. The PMV addresses important constraints in the sector and embodies a paradigm shift from a highly protected to a more open market oriented agriculture and away from concerns with only farm-level production and towards integrated value-addition all along the agri-food chain that will bring better opportunities to small and large farmers alike. Institutionally, it represents a major shift from state intervention that replaces private sector to one that focuses on delivering public goods and services and developing Public Private Partnerships (PPPs) to support the sector. In the period 2009-2020, an estimated 140 billion MAD of combined public and private sector investments are envisaged in around 1,500 commercial (Pillar I) and smallholder (Pillar II) agriculture investment projects. The latter would focus mainly on marginalized rural areas. In combination with the GoM’s ongoing Programme National d'Economie d'Eau en Irrigation (PNEEI) and the systemic public sector reforms undertaken by the PMV, these investments are to realize the agri-food sector’s domestic and export growth potential, particularly in fresh and processed high-value fruits and vegetables, stemming from Morocco’s geographic position and privileged access to the EU and US markets, rising domestic demand for quality food driven by growing incomes, favorable climate, and abundant and relatively low cost labor.

4

A. Macroeconomic achievements over the last decade

Source: Moroccan Government and Staff estimates.

Figure 2. Growth shifted to higher path and is less volatile and less dependent on agriculture (in percent)

Figure 3. Unemployment declined (in percent)

Figure 4. External position is solid with vulnerability in trade (in percent of GDP)

Figure 5. Public Finances have improved before the global crisis (in percent of GDP)

Figure 6. Inflation remains subdued (in percent)

Figure 7. Central Government debt is declining and sustainable (in percent of GDP)

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

-7.0

-4.0

-1.0

2.0

5.0

8.0

11.0

14.0

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

GDP Agriculture output (right axis) Poly. (GDP)

0%

8%

16%

24%

32%

40%

0%

5%

10%

15%

20%

25%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

National (Left axis) Urban (Left axis)Urban Youth (right axis) Urban Women (right axis)

-28

-18

-8

2

12

22

32

-6

-4

-2

0

2

4

6

8

10

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Current account balance Net reserves in months of GNFSForeign direct investments, Gross Trade Balance (right axis)

0%

5%

10%

15%

20%

25%

30%

35%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%19

95

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Budget deficit Wages & salaries

Consumer subsidies Total revenues (Right Axis)

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

CPI Food Non-Food

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Foreign Domestic Total

5

Table 1. Selected Macroeconomic Indicators (in percent of GDP) 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 Est. I. National Accounts

Gross Investment 26.1 25.9 27.4 29.1 28.8 29.4 32.5 38.1 36.0 35.7 Gross National Savings 30.4 29.6 30.5 30.8 30.7 31.6 32.4 32.9 31.0 31.7 Government Investment (Nat. Acc.) 2.6 2.2 2.1 2.1 1.9 2.1 2.3 2.7 3.1 2.6 Private Investment (incl. SOEs) 23.6 23.7 25.3 27.0 26.9 27.4 30.2 35.4 32.8 33.1

Of which SOEs 4.4 4.8 4.9 5.6 6.1 7.1 8.0 9.6 11.5 14.3 II. Central Government Finances

Total revenues 22.4 22.1 21.6 22.2 23.8 25.1 27.4 29.7 25.9 23.8 Tax revenue 20.4 20.4 19.8 20.0 21.7 22.2 24.9 27.4 23.4 22.1 Current Expenditure. Of which 21.9 20.6 20.6 20.8 24.1 21.5 21.7 22.8 20.7 21.1

Wages 11.3 10.9 11.2 11.2 11.7 10.9 10.7 10.2 10.2 10.3 Capital Expenditure 5.1 4.5 4.1 4.2 3.9 4.1 4.6 5.5 6.3 5.1 Global Balance -5.7 -4.1 -4.4 -4.0 -5.2 -2.0 0.2 0.4 -2.2 -4.2

III. Balance of Payments Imports GNFS 32.6 32.9 32.0 34.8 38.2 39.8 46.0 52.1 40.7 42.8

Exports GNFS 29.6 30.2 28.6 29.2 31.6 33.1 36.2 37.6 28.8 32.6 Trade Balance -10.3 -9.9 -10.9 -13.9 -17.0 -18.3 -22.3 -24.7 -20.8 -21.0 Tourism receipts 6.8 6.5 6.5 6.9 7.8 9.1 9.5 8.1 7.2 7.5 Workers' remittances 8.6 7.1 7.2 7.4 7.7 8.3 8.9 7.7 6.8 7.1 Current Account Balance 4.3 3.7 3.2 1.7 1.9 2.2 -0.1 -5.2 -5.0 -4.0 Foreign Direct Investment, net 7.6 1.4 4.9 1.9 5.0 4.6 6.2 4.1 2.8 2.0 Reserves, net (months of GNFS imp.) 8.8 9.1 10.0 9.9 9.9 10.0 8.8 6.6 7.6 7.6

IV. Indicators of Credit Capacity of CG Public Debt of CG 67.1 63.7 60.8 58.2 62.1 57.3 53.5 47.3 46.9 48.2

Total interest payments/Tax revenues 21.6 19.1 18.4 17.4 15.2 14.5 12.6 9.7 10.1 10.3 Memo:

Country’s external debt stock/GDP 49.8 44.5 36.5 29.6 27.2 27.1 27.3 23.4 24.7 25.8 Consumer price (%, yearly average) 0.6 2.8 1.2 1.5 1.0 3.3 2.0 3.7 1.2 0.9 GDP Growth (%) 7.6 3.3 6.3 4.8 3.0 7.8 2.7 5.6 4.9 3.5 Non Agriculture GDP growth (%) 5.7 3.2 3.6 4.7 5.6 5.4 6.5 4.2 1.4 6.1 Unemployment (%) 12.5 11.6 11.6 11.0 11.2 9.7 9.8 9.6 9.1 9.0

Source: Moroccan Government and staff estimates.

A. RECENT ECONOMIC DEVELOPMENTS IN MOROCCO 11. In the context of the global economic crisis, growth performance in Morocco has been good. Economic growth in 2009 reached 4.9 percent following a growth rate of 5.6 percent in 2008. This performance is mainly due to an exceptionally good agricultural output, which gained 30.6 percent benefiting from a favorable climate. This shows that agricultural variations due to weather conditions still affect GDP growth, albeit with less intensity than in the past. Growth of the non-agricultural GDP slowed down to a much lower rate than projected due to the negative impact of the global crisis. It edged down to 1.4 percent over 2009 compared to 4.2 percent registered the previous year and it is mostly explained by a slow-down or decline of most of the activities, especially manufacturing and tourism. 12. Data from the first three quarters of 2010 show that the economy is recovering from the effects of the global economic slowdown that started in late 2008. Non-agricultural GDP gained 5.4 percent in the first quarter of 2010 and stabilized at around 4.8 percent in the second and third quarters. It is expected that growth momentum of the non-agricultural activities would continue through the end of the year. However, total GDP growth is estimated to be around 3-3.5 percent for the whole year owing to a lower, although good harvest this year compared to the exceptional one of last year, translating into an estimated negative growth of the agricultural output (down 8 percent). Furthermore, there are no apparent signs that the recent sovereign debt crisis of Greece and Ireland and the subsequent restrictive policies of some European countries have had any major impact on exports or capital inflows.

6

13. The Government has implemented a stimulus package to support the income of the population and help the most affected sectors (Box 1). The income support package is mostly benefiting the low income employees. It includes an increase of 10 percent in the wages of civil servants at the lower end of the salary scale and the Minimum Wage for private sector employees. The wage increase was implemented in two steps, the first increase of 5 percent in July 2008 and the second one in July 2009. In addition, effective January 2009, the marginal income tax rate was cut from 42 percent to 40 percent and further to 38 percent in January 2010. At the same time the upper end of the exempt income bracket was extended. In addition to the measures aiming to preserve employment, direct support measures for firms affected by the crisis included financial relief (guarantees on loans; rescheduling of debt; help with export insurance) as well as subsidies for training and marketing. Economic stimulus was also provided through some monetary easing. The total budgetary gross cost of the stimulus package has been estimated by the government at MAD21 billion3

(over the 2008-2010 period) or 2.7 percent of 2010 GDP, and as such does not pose a risk to the medium term sustainability of public finances.

3 Because of their structural nature, the extra subsidies for food and petroleum products (MAD 7 billion) generated by higher world prices of cereals and fuels are not included in the stimulus package.

Box 1. Fiscal Stimulus packages and Outcomes

The Government has implemented several measures to help affected firms cope with the decline of external demand. Early in 2009, the Government set up a high level Council for Strategic Monitoring (CSM), comprising concerned ministers as well as representatives of the private and banking sectors, to follow developments related to the ongoing global crisis. The CSM targeted the export sectors hit by the effects of the global crisis for support through the following measures that would expire at the end of 2010:

• Social component: budgetary support to help firms in the payment of their contribution to employees’ social benefits

• Financial component: public guarantees for financing roll-over funds of firms and for rescheduling of their debt service

• Commercial component: budgetary support for the prospection and marketing costs abroad, and preferential conditions for export insurance

• Training component: Budgetary support for training and logistics Subsequently specific support programs have been designed for tourism and remittances and investment of Moroccan workers residing abroad.

Data as of June 2010 show that 70 percent of the demand for support concerned social benefits relief and was requested by 443 firms, of which 398 firms operating in the textiles sector and the remaining firms in automotive equipment and electronics. At the same time, 129 firms benefited from loan guarantees (of which most are operating in the textiles sector), and 134 firms benefited from training, of which 111 firms from the textiles sector and 20 from automotive equipment.

Measures to help low income households were already started in 2008 and included in the 2009 and 2010 Budget Laws. For the most part, they consisted of tax relief and wage increases for selected groups as well as an increase in social expenditures by relevant government departments. These measures, along with a much higher public investment program in place for 2009 and confirmed for 2010, kept domestic demand high as reflected in the rising credit to consumption, equipment and real estate (see below). Specific measures included the following:

• The marginal income tax was cut from 42 percent to 38 percent, and the upper limit of the tax-exempt bracket was increased by 25 percent;

• Salaries of civil servants at the lower end of the pay scale were increased by 10 percent (5 percent in July 2008 and 5 percent in July 2009);

• For private sector employees, the minimum wage was raised by 10 percent (5 percent in July 2008 and 5 percent in July 2009); and

• Minimum pension payments were increased by 20 percent and family allowances by 33 percent.

Economic stimulus was also provided through monetary easing. Reserve requirements for banks were cut in steps from 15 to 8 percent over 2009, and further to 6 percent effective April 1st, 2010. The Central Bank also cut its policy rate by 25 basis-points in March 2009 translating into a policy rate of 3.25 percent.

7

14. Public finances continue to be well managed despite the impact of the global crisis on the budget. The steady reform efforts of expenditure and tax management and sound active debt management over the last few years have been critical in maintaining public finances on a sustainable path. These reforms translated into better control of the Government’s consumption, enhanced tax collection, and declining public debt. In this context, the budget deficit was limited to 2.2 percent of GDP in 2009 despite decreasing revenues impacted by the reduction of corporate and personal tax rates, the slow-down of economic activities ensuing the global crisis and the introduction of the stimulus package. This manageable deficit follows a good performance of public finances that were in slight surplus in 2007 (0.2 percent of GDP) and in 2008 (0.4 percent of GDP), which is remarkable given the impact on the budget of high subsidies following the food and fuel crisis. 15. Recent data on budget execution over the first 10 months of 2010 show that the annualized budget deficit would be contained to less than 4 percent of GDP. The budget deficit is mainly explained by soaring food and fuel subsidies (up 135.6 percent) caused by increasing world prices. The deficit, however, may have been even larger without efforts to improve revenue collection that helped fiscal revenues to gain 2.3 percent despite the impact of the global crisis and the effects of the stimulus package. It is clear that subsidies still represent a heavy burden on the budget and thus constitute a potential risk factor for sustainability in case of serious exogenous shocks such as very high world prices of fuels and food items or severe drought. Nevertheless, public finance stance remains sustainable due to the sound macroeconomic policies and accompanying sectoral measures the Government is undertaking to mitigate the effect of such shocks. Indeed, the Government continued to improve tax administration and collection and contain recurrent expenditures (up only 2.3 percent), of which the wage bill. It launched a medium term plan to reform the subsidy system along an ambitious program aiming at enhancing the productivity of the agricultural sector and insulating it from the uncertainties of the climate conditions. In addition, the Government is implementing better targeted social programs such as conditional cash transfer program and a scaled up non-contributory health insurance scheme for the poor (RAMED). The stable macroeconomic stance and the continued reform momentum have allowed Morocco to successfully issue Euro 1 billion of bonds in the international market end September 2010, at relatively low interest rate (4.5 percent), with a risk premium of 200 basis points, showing the confidence of international investors for the positive economic prospects of Morocco. 16. Sound fiscal management helped further reduce the Treasury’s debt. Reflecting the good performance of public finances and sound active debt management, the debt stock of the central Government declined to 46.9 percent of GDP in 2009, down by almost a half percentage point compared to the previous year (and by more than 6.5 percentage points relative to 2007). The decline is explained by a decrease in that of domestic debt, which fell by 1.2 percentage points to reach 36.2 percent of GDP, while foreign debt slightly increased by 0.8 percentage point of GDP (representing 10.7 percent of GDP) reflecting the Government’s debt strategy to improve the share of external debt in total public debt, contributing in this way to the reinforcement of the external reserves of the country. 17. The Government and the central bank showed continued commitment to fighting inflation. Helped by prudent monetary policies, protected domestic markets from increasing world food and fuel prices and ample domestic food supply inflation was low over the first 11 months of 2010 (0.9 percent). This inflation rate is less than that of 2009 (1.2 percent) the same period and much less than that of 2008 (3.7 percent). Both food and non-food inflation have been low (1 and 0.9 percent respectively). 18. The external position remains solid with signs of improvements of the current account. For the first time since the 1980s, the current account ran large deficits in 2008 (5.2 percent of GDP) and 2009 (5 percent of GDP). The latest data show that current account deficit improved to an estimated 4 percent of GDP over the first 11 months of 2010. Current account deficits followed comfortable surpluses over the period 2001-06 (average surplus of 2.8 percent of GDP) and a quasi-balance in 2007 (a deficit of 0.1 percent of GDP). The improvement of the current account is principally explained by buoyant exports and the recovery in workers’ remittances and tourism receipts are following the on-going recovery of world economy that is having a positive impact on exports over the first 11 months of 2010, exports of goods increased by 26.7 percent (while imports gained only 12.9 percent), remittances by 7.8 percent and tourism receipts by 7.3 percent. Consequently, after declining by US$ 5.3 billion (or down 21.4 percent) at end June 2010 (y/y), net foreign reserves started to steadily improve over the last months reducing the loss to US$ 2.3 billion by end November 2010, reaching US$ 22.4 billion, which represent 6.9 months

8

of imports, down from 7.6 months in 2009. In parallel to the improvement of the international commerce, operations which have allowed an increase in the level of foreign reserves by about Euro 1 billion by the Government on the international market end September 2010 include the recent selling of 40 percent of Medi-Telecom for Euro 640 million, and increasing share of foreign financing of the budget. 19. The recent economic events revealed once again the weaknesses inherent in the Moroccan trade structure. The trade deficit deteriorated to 24.7 percent of GDP in 2008, up from 22.3 percent of GDP in 2007 (and only 11 percent in 2000). It improved in 2009 as imports declined by more than exports in nominal terms (20.8 percent of GDP). The latest data show the trade deficit further improved to 19.4 percent of GDP by end November 2010. The high trade deficit is mainly a volume effect rather than a price effect because Morocco actually benefited from positive terms of trade movement: while the price of oil and food imports increased, so did the price of key Moroccan exports such as phosphate products and agri-food. The poor performance of exports reflects their low diversification and lack of competitiveness. This explains largely why Moroccan exports were not able to benefit fully from the many FTAs it signed over the last decade such as those with the EU, the USA, and Turkey. The PMV is aimed at addressing those weaknesses by promoting private sector-led investments, in particular in higher quality and value agri-food products.

20. Monetary and exchange rate policies remained appropriate. In 2008, the central bank (BAM) resorted to raising the cost of money (plus 25 basis points in September 2008) to contain soaring credit and inflation, while it relaxed its policy to enhance liquidity in the face of the global crisis. As liquidity tightened and inflationary pressures started to ease over the second half of 2008 through 2009, BAM relaxed gradually the money reserve rate reducing it from 15 to 12 percent January 2009, and then to 10 percent July 2009. BAM decided to further cut the money reserve rate to 8 percent in October 2009 and to 6 percent starting April 2010 to ease the pressure on liquidity and thereby allowing Banks to be able to cope with the new money demands while contributing to keeping interest rates close to the BAM’s policy rate. It has also cut its policy rate by 25 basis points in March 2009 to reach 3.25 percent. Despite these relaxed policies, money supply slowed to 5.5 percent (y/y) by end November 2010, compared to an average 14.5 percent over 2005-2008. Although credit for equipment soared at 18 percent, total credit to the private sector slowed down (up 11 percent) driven by reduced growth in credit for consumption (up 7.7 percent), construction (up 9.6 percent), and for working capital (up 5.7 percent). At the same time, the stock of non-performing loans increased by 8.2 percent (y/y) , but their share in total credit to the economy has been on a downward trend over time (from 4.9 percent in November 2009 to 4.8 percent November 2010). In recent years the exchange rate remained in line with macroeconomic fundamentals with no signs of misalignment.

B. MACROECONOMIC OUTLOOK AND DEBT SUSTAINABILITY 21. Sound macroeconomic and fiscal policies, as well as efforts to improve sector productivity and competitiveness, put Morocco in a position to maneuver with less damage through the moderate effects of the global crisis, while being in a position to benefit from the recovery of the world economy (Table 2). The decision of the Government to continue its reform efforts and revamp its sector strategies along the targeted and short term sector fiscal stimulus should allow the Moroccan economy to expect good prospects over the medium term. Meanwhile, economic growth is estimated to be between 3-3.5 percent in 2010 mostly owing to the recovery of the non-agricultural sector benefiting from dynamic activities such as construction, finance services, telecommunication, and tourism.

9

Table 2. Base-line Medium Term Macroeconomic Indicators

Est. Projections

2008 2009 2010 2011 2012 2013 Growth Rates in percent

Real GDP 5.6 4.9 3.5 4.4 5.1 5.2 Real private consumption 6.0 4.0 3.8 3.6 5.0 4.2 Real Gross Domestic Investment 12.8 4.4 4.2 4.9 5.3 5.5 Export Volume (GNFS) 7.2 1.9 7.4 6.0 7.0 7.7 Import Volume (GNFS) 12.2 12.2 4.7 4.9 6.5 6.2 GDP deflator 5.9 1.8 2.0 2.0 2.0 1.9

Ratios to GDP Gross Domestic Investment 38.1 36.0 35.7 35.8 35.9 36.0

Fiscal Balance 0.4 -2.2 -4.2 -3.6 -3.4 -3.2 Central Government Debt 47.3 46.9 48.2 47.9 47.2 46.4

of which foreign 9.9 10.7 12.1 13.1 13.2 13.2 Current Account balance -5.2 -5.0 -4.0 -3.2 -2.7 -2.1 FDI, gross 2.3 0.9 2.0 3.1 3.4 4.6 External Debt (public and private) 23.4 24.7 25.8 26.6 26.0 24.4

Source: Moroccan Government and Staff estimates. 22. Growth prospects in the medium term are positive.4 It is assumed that the Government will sustain the reform momentum of the last few years, achieve the ambitious public investment programs it devised, and continue to implement the main sector strategies it launched, thus consolidating further economic diversification, growth potential, and domestic demand, and it is also assumed that the world economy will slowly recover from the current crisis to allow the on-going export promotion strategies to achieve their targets and contribute to growth. Under these conditions, growth rates will improve from the low 3.5 percent estimated for 20105

to around 5.2 percent in 2013. Should the underlying sources of growth assumed above be slow to materialize, growth prospects would have to be adjusted downward. Moreover, there is a potential risk that even pre-crisis growth levels might not be sustainable over the medium term if internal demand remains the key driver of growth.

23. Sound macroeconomic policies will help contain inflation at low levels. Inflation edged down to 1 percent only in 2009, mainly driven by ample food supply and to a lesser extent by declining prices of imported food items, and should remain subdued at around 2 percent thereafter. As the Moroccan agriculture sector meets domestic demand for most of basic food commodities and even allows to export many food items, its inflation rate is only slightly affected by international food price fluctuations. In addition, subsidies for staple food and energy prices – while clearly having an impact on the budget – contribute to a stable inflation rate. 24. After a temporary higher estimated deficit in 2010, the fiscal stance should remain sound over the medium term, with fiscal deficits around the targeted threshold of 3 percent of GDP, benefiting from the ongoing fiscal reform and more targeted social programs, as well as a better-controlled wage bill. The budget deficit is expected to edge up to 4.2 percent of GDP in 2010 before gradually dropping to 3.2 percent by 2013. Reaching this outcome implies maintaining momentum of the ongoing tax reform to broaden the tax base, improve the efficiency of the VAT, strengthen tax administration, and remove unproductive tax exemptions in order to reduce the high tax expenditures. These measures would offset the negative impact of the reduced top rates on corporate and personal income taxes. Under these assumptions, revenues are projected to stabilize at around 25 percent of GDP. On the expenditure side, the consolidation of public finances relies on four critical measures: deepening of fiscal reform, achievement of oil and food consumption subsidies reform, continued tight control of the wage bill evolution, and an active debt management. Under these conditions, public debt will slightly increase in 2010 48.2 percent of GDP before following a downward trend to decline to less than 46.5 percent of GDP in 2013.

4 IMF (2010), Morocco: 2009 Article IV Consultation—Staff Report; Public Information Notice on the Executive Board Discussion; and Statement by the Executive Director for Morocco 5 The low growth in 2010 is mainly explained by normal agricultural output translating into a negative growth rate for agriculture after an outstanding growth in 2009.

10

Table 3. Morocco: Financing Requirements of the Treasury (in percent of GDP) Est. Projections

2008 2009 2010 2011 2012 2013 Financing required 9.3 10.8 11.8 10.9 10.8 10.5 Budget deficit (+) -0.4 2.2 4.2 3.6 3.4 3.2 Amortization 9.7 8.6 7.6 7.4 7.4 7.3

Domestic 8.3 7.8 6.8 6.5 6.4 6.3 External 1.4 0.8 0.8 0.9 1.1 1.0

Total Financing available 9.3 10.8 11.8 10.9 10.8 10.5 Domestic financing 6.6 7.1 7.0 7.8 8.3 8.3 External disbursement 1.7 2.1 3.6 1.6 1.4 1.1 Others (Privatization, capital grants, CST*) 1.0 1.6 1.2 1.5 1.2 1.1 Source: Moroccan Government and staff estimates. (*) CST: Comptes Spéciaux du Trésor 25. The financing needs stemming from the higher budget deficit in 2010 and declining deficits over the medium term are easily financed through domestic market as well as from increased drawings on external loans (Table 3). In this context, domestic financing would remain the main source, although external financing would improve its contribution. Indeed, since 2006, net external financing reversed its long negative trend and became positive, reflecting the Government’s strategy to slightly change the debt composition in favor of external borrowing. This financing strategy would ease the pressure on domestic financial markets and prevent any crowding out of the private sector’s investment now that the money market is less liquid than in previous years. At the same time it is consistent with the intention to maintain a comfortable level of foreign reserves. 26. The Government’s debt strategy is to diversify financing sources and take on a greater proportion of external financing. Three main factors underpin the decision of the Government to reinforce its external sources, especially multilateral and concessional. The first is linked to Morocco’s public debt maturity structure. The maturity of public debt has fallen in recent years and will fall further given that the Government mostly financed its needs through issuing T-bills of up to 1 year in the domestic market. The main reason behind this choice is to avoid affecting long-term floating rates for Banks’ domestic lending to the private sector, especially housing credit, as they are indexed to primary market rates on long-term securities (10 and 15 year bonds).6

The second relates to the higher balance of payments needs although the level of foreign reserves remains relatively comfortable. The third is due to the current higher borrowing requirements of the Budget, in a context of tightening liquidity of the domestic financial markets after a long period of an over-liquid money market. Consequently, additional external lending is consistent with prudent debt management which fosters improved terms of debt, while maintaining a comfortable level of foreign reserves and at the same time avoids pressure on domestic financial markets. In September 2010 Morocco successfully completed a ten year bond issue for one Billion Euros against a total demand of over 2.2 Billion, further attesting international markets confidence in Morocco’s sound macroeconomic stability.

27. A comprehensive public debt sustainability analysis shows that the fiscal framework is robust to downside risk in the medium term (see Annex E.3). Public debt under the two main shocks proved sustainable over the medium term.7 Under alternative scenarios, six other shocks to the baseline scenario are simulated,8

and public debt sustainability is preserved in all of them. Under these shocks, public debt would slightly increase in 2010 and, for a few simulations in 2011 as well, before steadily declining over the medium term.

28. The external position is expected to remain sustainable over the medium term. The current account deficit is estimated to have improved in 2010 (4 percent of GDP) and would continue its slight downward trend over the medium term to edge down to 2.1 percent of GDP in 2013, as the impact of reforms and sector strategies take hold. Indeed, the balance of payments is expected to progressively improve, with lower trade and current account deficits, which would benefit from improved export potentials and a recovery of tourism activities and workers’ 6 However, since early this year, credit with variable interest rates is no longer linked to the rate of long-term treasury bonds. 7 The two main shocks are A1: Key variables are at their historical averages; and A2: No policy change (constant primary balance). 8 See Annex E.3 for their description.

11

remittances. This scenario assumes that Morocco would reap the fruits of its continued reform efforts, its sound macroeconomic and fiscal policies, and targeted sector strategies that entail higher public investments, which would translate into higher private investments, including FDI, and progressive gains in competitiveness of its exports, including tourism. In this context, external debt is expected to follow an inverted U path reaching a maximum at 26.6 percent of GDP in 2011 from 24.7 percent of GDP in 2009 before steadily dropping to 24.4 percent by 2013 while net foreign reserves will stay at an average of 6.5 months of imports. 29. Balance of payments financing requirements do not constitute a serious concern given the sound economic fundamentals, the country’s low external debt stock, and the ample foreign reserves. As the current account deficits are projected to steadily improve in the medium term, there are no constraints on financing them through multilateral and bilateral credit lines along other private capital flows, including FDI. The latter is expected to gradually improve, attracted by an improved business environment and the opportunities offered by important structural projects and the devised privatization program of the country. 30. In sum, Morocco’s macroeconomic framework remains adequate and sustainable in the medium term. The moderate effects of the global crisis on the Moroccan economy have been mitigated by the good economic fundamentals resulting from sound macroeconomic policies carried out over the last years and by the response of the Government through the stimulus package to mitigate these effects on the population and businesses alike. The stimulus package has allowed supporting investors’ confidence and domestic demand while reducing risks. The Government’s commitment to maintain momentum of reform effort supports robust prospects of investment, growth, and employment.

III. THE GOVERNMENT’S PROGRAM AND PARTICIPATORY PROCESSES 31. The Government installed in October 2007 seeks to strengthen Morocco’s economic growth and competitiveness while improving social indicators. The GoM’s Social and Economic Program (SEP) for the period 2008-2012 aims to increase the country’s growth and export potential by promoting investment in key infrastructure (energy, transport, water) and productive sectors such as industry and agriculture. In order to ensure that the ensuing growth dynamic results in improved social outcomes, these investment programs are combined with increased efforts to improve access to quality health, education, and housing as well as better targeted social protection programs. The GoM’s commitment to these objectives has been reflected in increased budget resources under a multiannual framework for six priority sectors: health, education, justice, water, energy, and agriculture. To further facilitate attainment of these sector goals and priorities, the Government is pursuing a series of crosscutting reforms in the areas of governance, public sector management, and decentralization. 32. The GoM has an ambitious agricultural development strategy, the Plan Maroc Vert (PMV), for the period 2008-2020. The PMV, launched in April 2008, constitutes an ambitious investment program in the agri-food sector and provides a road map for implementing a series of systemic public sector reforms. The ongoing Programme National d'Economie d'Eau en Irrigation (PNEEI) is an integral part of the GoM’s strategy. The PMV’s development was motivated by several factors, including: (i) the desire of the Government to confront problems of falling productivity and low incomes in the agri-food sector; (ii) the mounting uncertainty in international commodity markets in the period 2007-2008; and (iii) the domestic pressure to address the challenges in a sector that was perceived as a drag on the rest of the economy. The Plan aims to transform the agri-food sector into a key source of economic growth that contributes to employment creation and poverty reduction in rural areas. At the same time, policy reforms and investments in a productive, dynamic and market-oriented agri-food sector are designed to improve food security in Morocco, promote the country’s integration in the global economy, and help the sector adapt to climate change. The vision laid down in the PMV constitutes a paradigm shift from the strategies of the past which have emphasized food self-sufficiency through inward-looking, import substitution policies. The PMV recognizes the opportunities and threats that come with an increasingly competitive global economy and sets out to integrate the agri-food sector in this global framework.

12

33. The PNEEI is an integral part of the PMV’s reform and investment agenda. The PNEEI aims to improve agricultural revenues by supporting the conversion of the current irrigation technologies by using more efficient irrigation technologies and practices, as well as a better valorization of water at both the production and marketing level. These strategic objectives were confirmed by the National Water Strategy developed by the State Secretariat for Water and Environment (SEEE) in 2009. The PNEEI is a 15 year development program supporting the conversion of an estimated 550,000 hectares of surface irrigation to drip irrigation, of which 395,000 hectares situated within Large Scale Irrigation (LSI) systems. It is structured around 5 components: (i) modernization of collective irrigation systems; (ii) modernization of individual irrigation systems; (iii) improved agricultural water management; (iv) enhanced technical assistance for drip irrigation and productivity improvements; and (v) targeted support measures. 34. The PMV’s investment program is structured around two pillars. An estimated 140 billion MAD of combined public and private investments are expected to be directed to a total of 955 commercial (Pillar I) and 545 smallholder (Pillar II) agricultural development projects in the period 2008-2020. Pillar I investments aim to integrate commercially-oriented producers in agri-food chains with high value added and high productivity. Pillar II investments aim to increase incomes of smallholder farms through crop switching, diversification, and intensification, as well as strengthening farmer organizations and supporting their integration in suitable agri-food chains. The overall philosophy is that Pillar I projects will rely largely on significant private sector financing with some public support. Pillar II projects will mainly be financed by public resources. In the period 2008-2020, total public investment resources for Pillar I and II projects (including cross-cutting reforms, see following paragraph) are expected to amount to 66.6 billion MAD (approximately one-third of the total cost of the PMV) and would serve primarily to leverage the private investment (approximately two thirds of the cost of the PMV) resources required to realize the program. Under both pillars, the process of value creation is to be driven by a voluntary aggregation of farmers and farm organizations (agrégés) around private investors, traders, and/or entrepreneurs (agrégateurs). One of the most innovative features of the PMV is that it conditions Government support on the conclusion of tri-lateral contractual arrangements between agrégateurs, agrégés, and the GoM. The aggregation model is designed to help overcome existing land constraints, promote farmer organization, and enable producers’ access to finance, knowledge, and technologies, support risk-sharing, and improve marketing. Of the 1,500 projects9

envisaged under the PMV, 168 are currently being implemented. They include 62 Pillar I projects totaling MAD18.9 billion and 106 Pillar II projects totaling MAD5.6 billion.

35. To achieve the successful implementation of the two pillar strategy, the PMV’s investment program focuses on a series of cross-cutting actions. The key strategic axes of this cross-cutting systemic public sector reform program include:

(i) Reorienting the role of the MAPM towards its regulatory functions and delegating other agricultural services functions to private actors through Public Private Partnerships (PPPs), to specialized agencies for agricultural development and food safety, and to professional organizations;

(ii) Improving the agricultural business environment through improved access to investment financing as well as a realignment and improved targeting of agricultural subsidy schemes;

(iii) Pursuing new agricultural Free Trade Agreements (FTAs) and reorienting existing ones to improve access to high value export markets and gradually liberalize protected sub-sectors;

(iv) Reducing domestic market distortions through increased investment and improved management of marketing infrastructure and liberalizing distribution systems for fruit, vegetables, and meat;

(v) Strengthening irrigation water policies by delegating management of LSI systems to private operators, increasing water tariffs in large irrigation perimeters, extending existing irrigation perimeters, promoting on-farm drip irrigation, and ensuring inter-agency coordination of investment programs;

(vi) Mobilizing agricultural land by accelerating the process of private sector participation in the management of state-owned and collective lands and promoting aggregation.

9 These projects were identified through a participatory planning and consultation process at the regional level and each year specific projects are/will be further developed into bankable projects by the regional directorates. The design of these investments is based around a supply chain concept. Priority supply chains have been defined for each region based on their economic and agro-climatic conditions.

13

36. Since the launch of the PMV the GoM has undertaken important institutional reforms and arranged for program financing. With respect to the PMV’s agricultural policy and institutional reform agenda, the MAPM has established 16 Regional Agricultural Directorates (DRAs) contributing to more de-concentrated service delivery in each region and restructured the Chambers of Agriculture, (reducing their number from 37 to 16). In another nod to de-concentration, MAPM’s Regional Agricultural Directorate (DRAs) and Provincial Agricultural Directorate (DPAs) prepared in consultation with sector stakeholders 16 Regional Agricultural Plans (PARs) including territorial-based agricultural investment proposals (Pillar I and II), which have been adopted by the Regional Councils, the Chambers of Agriculture, and the local authorities in April 2009. It also signed results-oriented contract programs with 10 priority agri-food chains (filières) on the basis of the PARs. Professional associations (Inter-professions) have been established for these priority agri-food chains. Furthermore, specialized agencies such as ADA10 and ONSSA11 have been created and tasked with implementing the PMV’s investment program (Pillar I and II) and the recently adopted Food Safety Law respectively. In December 2009, the GoM concluded its agricultural trade negotiations with the European Commission. If approved by the European Parliament, the agricultural Free Trade Agreement (FTA) will immediately provide full market access for most Moroccan agri-food exports, while gradually opening the Moroccan market for agri-food imports from the EU over a period of 10 years (except for a number of sensitive products such as wheat, red and white meat, and olive oil).12 With regards to program financing, the MAPM signed a Medium Term Expenditure Framework (MTEF) 2009-2015 with the Ministry of Economy and Finance (MEF) in April 2009.13

Importantly, the Finance Law for 2010 includes an agricultural budget in line with the MTEF. In addition, the MAPM and MEF have signed an agreement with respect to the revision of 6 Decrees and 25 Arrêtés related to the Agricultural Development Fund (FDA) with a view to simplify procedures and aligning support measures with the strategic directions of the PMV.

37. The PMV includes a consultative process. Consultations have taken place in the context of the annual review of the 16 PARs and the monitoring of the implementation progress of the contract-programs signed with the 10 priority agri-food chains. In addition, consultations with universities and professional organizations were organized by the World Bank in relation to the preparation of the CPS, while consultations with producer organizations and associations were organized by the MAPM at the national and provincial level during the preparation of the proposed DPL. Furthermore, consultations have been organized with dedicated stakeholder focus groups in the context of the Poverty and Social Impact Analysis (PSIA) and the Environmental Due Diligence Review as part of the preparation of the proposed DPL (see sections VI.A and VI.B). The outcome of these consultations highlighted the following concerns: (i) large number of intermediaries and lack of transparency in fruit, vegetable, and red meat value chains contributing to relatively high consumer prices and low producer revenues; (ii) weak human and technical capacity of producers and producer organizations constraining technology transfers and access to finance; (iii) insecure land rights and land fragmentation limiting agricultural investments; and (iv) unsustainable use of water resources. Suggestions included: (i) improving financial support mechanisms for producers and producer organizations; (ii) developing strong support structures for producers and producer organizations; (iii) strengthening the dialogue between Government and professional organizations; and (iv) promoting efficient water use and agricultural land management. The consultations confirmed the importance of the PMV and relevance of the specific actions in the proposed DPL, including modernizing domestic marketing and distributions systems, improving the effectiveness of available public investment support under Pillar II through increased transparency and accountability, strengthening agricultural services to producers and producer organizations, and improving the sustainability of irrigation water resources.

10 Loi 42-08 portant création de l’Agence pour le Développement Agricole promulguée par le dahir n° 1-09-16 du 22 safar 1430 (18 février 2009) 11 Loi 25-08 portant création de l’Office National de Sécurité Sanitaire des Produits Alimentaires publiée au Bulletin Officiel Nr 5714 du 5 mars 2009 12 The FTA would allow for the immediate liberalization for 67 percent of fresh agricultural products, 98 percent of agro-industrial products, and 100 percent of fishery products. A limited list of products including tomatoes, garlic, clementines, strawberries, cucumbers, zucchinis and sugar would continue to be subjected to a differentiated treatment, while enjoying improved access to the European market through increased quotas or reduced entry prices. EU products will benefit from a progressive liberalization of the Moroccan market over 10 years, with the exception of 19 product categories that will be subjected to a differentiated treatment, including common wheat, meats, and olive oil. 13 The agreement defines the total (public and private) financial needs associated with the implementation of the PMV during the period 2008-2020, which are estimated at 17 billion USD. The public financing share of this amount (including donor resources) is estimated at 8 billion USD.

14

IV. BANK SUPPORT TO THE GOVERNMENT’S PROGRAM

A. LINKS TO THE CPS

38. The proposed DPL is aligned with the objectives and priorities defined in the Country Partnership Strategy (CPS) 2010-2013. It addresses the three long term development challenges facing Morocco identified in the CPS: (i) enhancing growth and employment; (ii) reducing social disparities; and (iii) ensuring sustainability. By supporting the GoM’s pursuit of institutional and policy reforms in relation to domestic markets, agricultural investments and services, and irrigation water resources, it contributes directly to the three thematic pillars around which the Bank’s program is structured: (i) growth, competitiveness, and employment; (ii) service delivery to citizens; and (iii) sustainable development in a changing climate. Furthermore, it is linked to the two cross-cutting themes of governance and territoriality. Though most pronounced in the proposed Pillar II component, both themes are mainstreamed across the four components of the proposed DPL.