dof asa q2 2016 presentation

TRANSCRIPT

Q2 Financial Presentation 2016

DOF ASA

Highlights

- Q2 Presentation 2016DOF ASA

Main Highlights

General good operational performance in the period Increased activity from subsea projects Average utilisation total fleet of 88% Backlog 79% for the remainder of 2016 Refinancing completed in August Skandi Acu (PLSV) delivered and on-hire in August

3

All numbers based on management reporting

EBITDA Q2 MNOK 760 (EBITDA excl hedge MNOK 814)

- Q2 Presentation 2016DOF ASA

Highlights

Subsea

• Average utilisation project fleet 92% and TC (time charter) fleet 82%Project fleet:• Increased utilisation in Atlantic (North Sea) and US-gulf regions• Asia Pacific – Good utilisation and performance• Brazil – Low utilisationTC fleet:• Reduced utilisation – class dockings, vessels idle between contracts

AHTS/PSV

• North Sea & Med – Good utilisation, reduced earnings, one vessel in lay-up

• Brazil – Good utilisation and performance Brazil flagged fleet

• Asia Pacific – Variable utilisation and earnings

Operational

4

- Q2 Presentation 2016DOF ASA

Highlights

5

Skandi Gamma awarded extension with Maersk UK until end of 2016 Skandi Caledonia awarded extension with Apache until mid-January 2017 DOF Subsea awarded 5+2+2 year IMR contract to the Shell Prelude FLNG

facility Skandi Niteroi awarded 8 months firm and 8 months options with Petrobras Skandi Achiever secured ROV and diving contracts until end-October 2016 Skandi Vitoria awarded a new contract with Petrobras for the remainder of 2016 Skandi Emerald and Skandi Giant awarded 120 days + 1 x 5 weeks option each

with Schlumberger Asia Services, India Geograph awarded an 18 months extension with Petrobras Various subsea project contracts securing back log in Q2 Skandi Marstein awarded an 18 months contract with Nexen Petroleum UK, start

up May

Contracts

- Q2 Presentation 2016DOF ASA

Highlights

Fleet

6

Financing

Skandi Acu (PLSV) delivered in April and on-hire on 8 yrs contract with Petrobras

Skandi Paraty (AHTS) delivered in April and on-hire on a 4 yrs contract with Petrobras

Normand Reach redelivered

DOFSUB05 repaid in April

New Subordinated Convertible bond and a right issue in placed in August

A new facility of NOK 3 800 mill agreed

Overview Group

- Q2 Presentation 2016DOF ASA

DOF ASA in brief

Vessels

Fleet 67 vessels (wholly and partly owned) (19 PSV, 20 AHTS, 28 Subsea)

• 62 owned vessels in operation• 2 owned less than 50% • 3 Subsea newbuilds

1 subsea vessel chartered in from external owner

63 ROVs, 4 ROVs on order

NOK 31.9 billion in fair market value owned vessel in operation* (100% basis)

Average age 9.3 years, value adjusted fleet age of 6.7 years

Back log* Total NOK 63.5 bn

• Firm contracts : NOK 29.8 bn• Options: NOK 33.3 bn

Global organisation Head office in Norway Regional offices in Australia,

Singapore, UK, USA, Canada, Angola, Argentina and Brazil

Total of 4 601 employees* Subsea employees: 1 590 Marine personnel: 2 715

(*As per 30.06.2016)

8

28

20

19

1

Subsea

AHTS

PSV

Chartered SubseaVessels

- Q2 Presentation 2016DOF ASA

Fleet overview and contract coverage

* Including Newbuilds** Excl. vessels with minority share

9

No. of vessels

PSV AHTS Subsea Total fleet

DOF ASA/DOF REDERI AS 17 4 2 23

NORSKAN OFFSHORE 1 10 2 13

DOF SUBSEA AS 0 0 22* 22

DOF INSTALLER ASA 0 0 2 2

DOF DEEPWATER AS 0 5 0 5

Total fleet 18 19 28 65**

Contract coverage

Remaining 2016 Firm 87 % 71 % 78 % 79 %

Remaining 2016 Including options 94 % 71 % 82 % 82 %

2017 Firm 53 % 52 % 48 % 50 %

2017 Including options 79 % 56 % 58 % 63 %

Expectations for 2016:

• Our global footprint, track record and project capacity will be vital to secure utilisation

• Blocking rights in Brazil vital to secure contracts in this region

- Q2 Presentation 2016DOF ASA

DOF backlog overview 2016 -2020

• Total value backlog from 2020 and onwards is MNOK 34,927

26,813

2016 2017 2018 2019 2020 ThereafterOption 180 857 1 380 1 721 1 899 27 499Firm 3 646 5 588 4 813 4 190 3 172 8 577

8 577

27 499

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

10 000

NO

K m

illio

n

Contract coverage at 30.06.2016

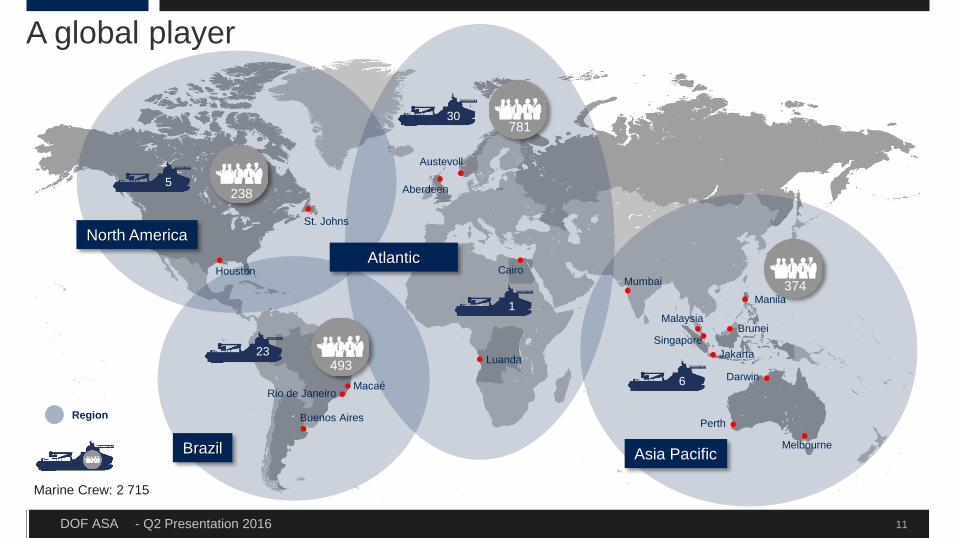

- Q2 Presentation 2016DOF ASA 11

RegionPerth

Rio de Janeiro

Buenos Aires

Singapore

Houston

St. Johns

Aberdeen

Cairo

Brunei

Macaé

Jakarta

Manila

Luanda

Austevoll

Malaysia

30

5

23

6

1

Melbourne

Darwin

781

493

374

North America

Asia PacificBrazil

Atlantic

238

Marine Crew: 2 715

Mumbai

A global player

- Q2 Presentation 2016DOF ASA

374

Region

Perth

Rio de Janeiro

Buenos Aires

Singapore

Houston

St. Johns

Aberdeen

Cairo

Brunei

Macaé

Jakarta

Manila

Luanda

Austevoll

Malaysia

30

5

23

61

Melbourne

Darwin

781

493

238

Mumbai

Access to market - selected awards ytd 2016North Sea:Aug 2016: Skandi Gamma extension until end of 2016 with MaerskAug 2016: Skandi Caledonia extension until mid-January 2017 with Apache Apr 2016: Subsea frame agreement – 5 years with Maersk Apr 2016: Large PSV Skandi Gamma 3 months to MaerskApr 2016: PSV Skandi Marstein 18 months to NexenFeb 2016: Large AHTS Skandi Vega 1 year to Statoil

SE Asia / Australia:Jul 2016: MPSV and fulltime underwater services (IMR) to Shell Australia,

Prelude FLNG facility for 5 years + 2 x 2 year optionsMay 2016: 2x AHTS for 120 days with Schlumberger in IndiaApr 2016: LOI for EPCI project in 2017

12

Canada:Apr 2016: Subsea IMR / construction contracts

Brazil:Aug 2016: Skandi Acu on-hire 8 yrs to PetrobrasJun 2016: 7 months on PLSV Skandi Vitória to PetrobrasJun 2016: 8+8 months on PLSV Skandi Niterói to PetrobrasMay 2016: Subsea RSV Geograph 18 months to PetrobrasMay 2016: Skandi Paraty on-hire 4 yrs to Petrobras

West Africa:Apr 2016: FPSO installation YinsonJan 2016: PLSV 4 months

Argentina:Mar 2016: 2x AHTS 8-month extension contracts

US GoM:Jun 2016: ROV and dive contracts for Skandi Achiever

- Q2 Presentation 2016DOF ASA

Vessel Yard Delivery Type Contract Financing

Skandi Buzios 50% owned Vard Norway 2016 PLSV 8 yrs Petrobras

Skandi Recife 50% owned Vard Brazil 2017 PLSV 8 yrs Petrobras Loan agreement signed with BNDES

Skandi Olinda 50% owned Vard Brazil 2017 PLSV 8 yrs Petrobras Loan agreement signed with BNDES

Remaining newbuilding program

13

- Q2 Presentation 2016DOF ASA

2001-2006 2009 2010 2011 2012 2013 2016

Establishing a strategic position in Brazil

Skandi Copacabana First Brazilian built AHTS

vessel by DOF

Skandi Vitória and NiteróiFirst Brazilian built PLSVs

Skandi Amazonas and Skandi IguaçuBiggest AHTS vessels built in Brazil by DOF

4 new PLSV´s 2 built in Brazil

2006: DOF Subsea Brasil

established

Skandi Salvador First Brazilian built CSV

Skandi SantosFirst CSV installing x-mas tree

2001: First step in Brazil

Strategy: Brazilian flag, local content, local employees New contracts in H1 2016 confirms the Groups strategy

Skandi Açu on-hire for 8 yrs contractSkandi Paraty on-hire 4 yrs contract

GeographPetrobras extended

contract by 18 months

- Q2 Presentation 2016DOF ASA

10

12

72

0

20

40

60

80

100

# vesselsBrazil AHTS fleet per April 2016

Brazil flag - DOFBrazil flag - OtherForeign

In DOF’s main segments, PLSV and AHTS, DOF vessels are protected by the CAA certificate system favoring local flagged & built vessels – no DOF vessels have been cancelled in Brazil

Petrobras has reduced the number of non-Brazilian vessels through two waves of vessel reduction, and the current fleet of AHTS vessels is estimated to be equal to the long-term demand for such vessels

Based on the percentage of foreign flagged vessels, and assuming continuation of the policy preferring Brazilian flagged vessels, DOF’s Brazilian AHTS vessels should be employed as long as total demand does not drop by more than 50-70%

The Brazilian legislation with CAA certificate is instrumental in keeping Brazilian flagged vessels on contract

Through the subsidiary DOF Subsea, the DOF Group is similarly well positioned in the PLSV segment:

DOF Group has 6 PLSVs including newbuilds, of which 4 are Brazilian built and 2 can be imported with Brazilian rights. There are no other known Brazilian built PLSVs

DOF Group has high local content in Brazil protected by flag regulations

Source: Managers based on data from IHS Petrodata

15

Refinancing DOF ASA

- Q2 Presentation 2016DOF ASA

Transaction summary

DOF ASA (excl 100% owned Norskan and 51% owned DOF Subsea) has restructured its capital structure through the following transactions:

A right issue of NOK 1 060 million completed in August A new Subordinated Convertible Bond established and replaced DOF 09,10 and 11, at 50% par value, NOK 1 032,5

million. Repurchase of NOK 209 million in the Subordinated Convertible Bond A new facility of NOK 3 800 million has been agreed with 13 banks to refinance 27 vessels with softer terms ( 75%

reduction in installments and and new financial covenants Net debt reduced by NOK 2 900 million Liquidity position improved by NOK 4 500 million over the next four years

Conclusion: DOF is in positioned to withstand a prolonged downturn

17

- Q2 Presentation 2016DOF ASA

DOF ASA position after refinancing

DOF have sufficient liquidity to sustain a downturn until 2020DOF is well positioned for healthy earnings when the market recovers

Positioned for market recovery

Access to market

through global presence

Strong back-log/long-term

contracts

Major oil & gas

customers

Offering vessel + subsea services

Leading subsea IMR

provider Modern, high-end fleet

Unique position in

Brazil

Improved financial position

18

- Q2 Presentation 2016DOF ASA

DOF Group has 3 business areas

DOF ASA

Norskan “DOF Rederi” DOF Subsea

Wholly-owned Brazilian entity

Fleet of 13 vessels whereof 10 Brazilian built or flagged, with local flag privileges

1 PSV, 10 AHTS vessels and 2 subsea vessels

Specialised in Brazil built tonnage to take advantage of local-flag benefits, effectively giving “local vessels” first-right-of-refusal over non-local vessels, including the possibility to “block” international vessels while on contracts

The non-Brazilian offshore vessel activities

18 PSVs, 9 AHTS* vessels, and 2 subsea vessels

• Including 5 owned 50% via DOF Deepwater

Subsea contractor owning 24 subsea vessels and 2 chartered-in

Owned 51/49% with First Reserve Corporation

Has built a global presence over the last 10 years

Developed the project business gradually; increasing complexity step-by-step and building a larger project back-log

Mix between owned and chartered in vessels

19

Installment in the restructured DOF Rederi

to be reduced by 75 % over the next 3 years

- Q2 Presentation 2016DOF ASA

DOF Group actual 2015 EBITDA was NOK 3.3 billion, excluding sales gains

Newbuilds for delivery after 2015* will generate NOK ~1.0 billion annual EBITDA on already firm contracts

DOF should generate in excess of NOK 4 billion in EBITDA in a normal market

Compared to an estimated 2020 net debt of NOK ~18 billion

Above implies NOK ~8-900 million net profit to DOF ASA shareholders

*Adding EBITDA of NOK ~1.2 billion gross on consolidated level: 4 PLSVs co-owned with Technip on 8-year contracts to Petrobras from delivery 2016/17 + Skandi Africa delivered 2015 with 5-year contract to Technip (9 months EBITDA included in figure as 3 months were reflected in 2015 EBITDA) + AHTS Paraty delivered mid-2016. Net of sold vessels: 5 vessels sold in Brazil in April 2015, Skandi Arctic sold June 2015, 3 PSVs sold 2H 2015, and Skandi Protector in 1Q16

Improving DOF’s financial position

-

1 000

2 000

3 000

4 000

5 000

NOK million

20

- Q2 Presentation 2016DOF ASA

DOF Group has 3 business areas

DOF ASA

Norskan “DOF Rederi” DOF Subsea

- 500

1 000 1 500 2 000 2 500 3 000 3 500 4 000

2012 2013 2014 2015 2016E

EBITDA

DOF Subsea Norskan "DOF Rederi"

21

Break-even EBITDA post-restructureAdjusted instalment NOK 1 600 million

Interest NOK 900 million

Maintenance CAPEX (est) NOK 250 - 400 million

Break-even EBITDA* NOK 2 750 – 2 900 million

* Compared to 2016, additional EBITDA of NOK 800 million from newbuilds

NIBD* NOK 20 400 millionper August

According to management reporting

- Q2 Presentation 2016DOF ASA

Adjust the Group’s capacity to the challenging market

Several cost cutting measures have been implemented during the last 12 months

The organisation has been reduced (onshore and offshore) with above10%

Salary cuts of 5-15% for the onshore employees in most of the regions has been implemented

Vessels have been re-allocated among regions in order to secure utilisation

Chartered-in vessels reduced from 5 vessels to 1 vessel

10 vessels sold

Re-negotiated terms with all major suppliers

Cost focus going forward Continuously focus on adjusting the Group’s capacity, cost level and risk exposure to the market

going forward

22

FinancialsManagement Reporting

- Q2 Presentation 2016DOF ASA

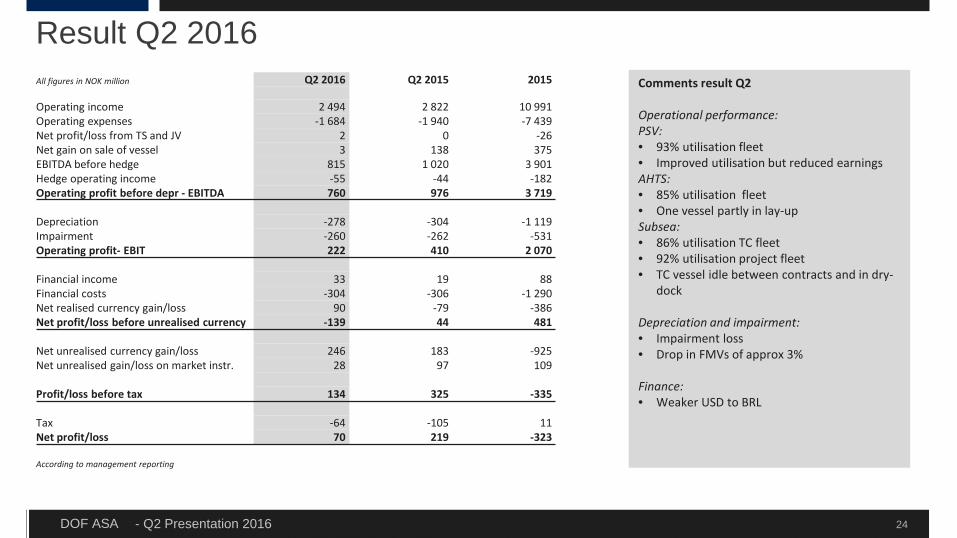

Result Q2 2016Comments result Q2

Operational performance:PSV:• 93% utilisation fleet• Improved utilisation but reduced earningsAHTS:• 85% utilisation fleet• One vessel partly in lay-upSubsea:• 86% utilisation TC fleet• 92% utilisation project fleet • TC vessel idle between contracts and in dry-

dock

Depreciation and impairment:• Impairment loss • Drop in FMVs of approx 3%

Finance:• Weaker USD to BRL

24

All figures in NOK million Q2 2016 Q2 2015 2015

Operating income 2 494 2 822 10 991 Operating expenses -1 684 -1 940 -7 439 Net profit/loss from TS and JV 2 0 -26 Net gain on sale of vessel 3 138 375 EBITDA before hedge 815 1 020 3 901 Hedge operating income -55 -44 -182 Operating profit before depr - EBITDA 760 976 3 719

Depreciation -278 -304 -1 119 Impairment -260 -262 -531 Operating profit- EBIT 222 410 2 070

Financial income 33 19 88 Financial costs -304 -306 -1 290 Net realised currency gain/loss 90 -79 -386 Net profit/loss before unrealised currency -139 44 481

Net unrealised currency gain/loss 246 183 -925 Net unrealised gain/loss on market instr. 28 97 109

Profit/loss before tax 134 325 -335

Tax -64 -105 11 Net profit/loss 70 219 -323

According to management reporting

- Q2 Presentation 2016DOF ASA

11 %20 %

69 %

EBITDA Q2 2016

PSV AHTS CSV

10 %

30 %60 %

EBITDA Q2 2015

PSV AHTS CSV

25

Segment reporting Q2 2016PSV AHTS CSV Total

Amounts in NOK mill Q2 2016 Q2 2015 Q2 2016 Q2 2015 Q2 2016 Q2 2015 Q2 2016 Q2 2015Operating income 247 301 416 400 1 777 2 076 2 439 2 778 Gain on sale of tangible assets - - - 96 3 42 3 138 Operating result before depreciation and impairment (EBITDA) 84 102 155 288 522 587 760 976 Depreciation 59 49 66 75 153 180 278 304 Impairment 55 12 78 140 127 110 260 262 Operating result (EBIT) -31 40 11 72 242 297 222 410

EBITDA margin 34 % 34 % 37 % 72 % 29 % 28 % 31 % 35 %EBIT margin -12 % 13 % 3 % 18 % 14 % 14 % 9 % 15 %

According to management reporting

- Q2 Presentation 2016DOF ASA

Historical Performance Group (excl gain from sale of assets)

26

According to management reporting

Q2 2013 Q2 2014 Q2 2015 Q2 2016Operating revenue 2 493 2 791 2 778 2 439EBITDA 770 866 838 757EBITDA margin 31 % 31 % 30 % 31 %

Non-current assets 28 347 28 757 28 610 30 682Current assets 4 727 4 861 4 976 4 495Total Assets 33 074 33 617 33 586 35 177

Equity 6 408 7 365 6 592 6 380Non-current debt 22 228 19 812 19 491 23 080Current debt 4 438 6 441 7 503 5 717Total Equity and Debts 33 074 33 617 33 586 35 177

0%

5%

10%

15%

20%

25%

30%

35%

40%

-

500

1 000

1 500

2 000

2 500

3 000

3 500

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016

EBIT

DA M

argi

n %

MN

OK

Operating revenue EBITDA EBITDA margin

- Q2 Presentation 2016DOF ASA

Balance Q2 2016Comments to balance

Assets:• One vessel sold and two vessels delivered

since year end• Intangible assets include deferred tax assets

MNOK 1 003 and goodwill MNOK 409

Financial assets:• Financial assets include minority share and

long term funding of JVs (ship owning companies)

Equity:• Positive (unrealised) currency impact since

year end

Non Current Liabilities:• Secured debt MNOK 20 348• Unsecured debt (bonds) MNOK 2 652

Current liabilities:• Current part interest term debt includes

bond, MNOK 700, balloons MNOK 280, normal amortisation , interest & credit facilities

27

Amounts in NOK million 30.06.2016 30.06.2015 31.12.2015

ASSETSIntangible assets 1 413 1 404 1 941Vessel and other tangible assets 26 305 24 006 24 967Newbuilds 2 315 2 834 943Financial assets 649 366 530Non-current assets 30 682 28 610 28 381

Receivables 2 828 3 026 2 772Cash and cash equivalents 1 667 1 951 2 220Asset held for sale 0 0 477Current assets incl asset held for sale 4 495 4 976 5 469Total assets 35 177 33 586 33 850

EQUITY AND LIABILITIESSubscribed equity 1 452 1 452 1 452Retained equity 1 339 1 542 439Non-controlling equity 3 590 3 599 3 281Equity 6 380 6 592 5 172

Provisions for commitments 79 130 121Other non-current liabilities 23 000 19 361 22 946Non-current liabilities 23 080 19 491 23 067

Current part of interest bearing debt 3 806 5 604 3 198Other current liabilities 1 911 1 899 2 152Liabilities held for sale 0 0 260Current liabilities 5 717 7 503 5 611Total equity and liabilities 35 177 33 586 33 850

According to management reporting

- Q2 Presentation 2016DOF ASA

Key Figures

28

-

1,00

2,00

3,00

4,00

5,00

6,00

7,00

8,00

9,00

-

5 000

10 000

15 000

20 000

25 000

2011 2012 2013 2014 2015 H2 2016*

Mill

ion

NO

K

NIBD historical development

Net interest bearing debt ex unemployed capital

EBITDA ex gain on sale of assets and hedge accounting

NIBD/EBITDA

* EBITDA for current quarter plus 3 previous quarters.

Q2 2016 Q2 2015 2015

FINANCIAL RESULTEBITDA margin (ex. net gain on sale of vessel and hedge accounting) 1 33 % 31 % 32 %EBIT margin (ex. net gain on sale of vessels and hedge accounting) 2 11 % 11 % 17 %

Profit per share ex. non-controlling interest -0,07 0,60 0,73

Profit per share ex. unrealised loss/gain and taxes -0,12 -0,96 5,00

BALANCEReturn on net capital 5 % 3 % -6 %Equity ratio 18 % 20 % 15 %Value adjusted equity 30 % 32 % 33 %Net interest bearing debt 24 723 22 560 23 731 Net interest bearing debt ex. unemployed capital 22 408 19 727 22 788 NIBD/EBITDA 3 14,51 10,67 6,46 NIBD/EBIT 4 47,02 22,12 12,14

1 EBITDA excluded net gain on sale of assets and hedge accounting / Operating Income

2 EBIT excluded net gain on sale of assets and hedge accounting / Operating Income3 Net interest bearing debt excluded unemployed capital / 4 quarters rolling EBITDA excluded net gain on sale of assets and hedge accounting4 Net interest bearing debt excluded unemployed capital / 4 quarters rolling EBIT excluded net gain on sale of assets and hedge accounting

According to management reporting

- Q2 Presentation 2016DOF ASA

Net interest bearing debt 30.06.2016

29

Comments current interest bearing debt:

Non-current debt:• DOF9, DOF10 and DOF11 MNOK 1 365

deleted in August and replaced with a Subordinated Convertible Bond

Current debt:• DOF09 MNOK 700 (deleted in August)• Debt to credit institutions:

• Two balloons MNOK 280• Amortisation MNOK 2 253

Cash and derivatives:• MNOK 457 represent cash deposit

Amounts in NOK million 30.06.2016 30.06.2015 31.12.2015

Bond loan 2 652 3 378 3 347 Debt to credit institutions 20 115 15 725 19 328 Total non-current interest bearing liabilities 22 766 19 102 22 674

Bond loan 700 700 422 Debt to credit institutions 2 533 4 218 2 422 Utilised credit facilities 391 491 172 Liabilities held for sale - - 260 Total current interest bearing liabilities 3 624 5 409 3 276

Total interest bearing liabilities 26 390 24 511 25 951

Cash and cash equivalents 1 667 1 951 2 220 Total net interest bearing liabilities 24 723 22 560 23 731

Newbuilds 2 315 2 834 943

Net interest bearing liabilities, excluding unemployed capital 22 408 19 727 22 788

According to management reporting

- Q2 Presentation 2016DOF ASA

Cash Flow Statement

30

Comments Cash flow Statement

Operating activities• High volatility in working capital in Q2 2016

Investing activities• Delivery of two new-builds

Financing activitites:Proceeds: Funding new builds

Refinancing one facilityPrepayments: Balloons and amortisation

Amounts in NOK million Q2 2016 Q2 2015 YTD Q2 2016 YTD Q2 2015

Cash from operating activities 781 1 236 1 432 1 797 Net interest paid -277 -276 -551 -635 Taxes paid -14 -46 -39 -137 Net cash from operating activities 490 913 842 1 026

Sale of tangible assets 3 659 551 1 919 Purchase of tangible assets -1 611 -1 183 -2 838 -3 244 Sale of shares -0 417 3 417 Purchase of shares - - - -Other changes in investing activities -17 -167 -149 -190 Net cash from investing activities -1 625 -274 -2 433 -1 097

Proceeds from borrowings 1 629 1 757 3 292 3 510 Prepayment of borrowings -609 -1 954 -2 203 -4 272 Payment from/to non-controlling interests -26 -18 -26 -18 Net cash from financing activities 993 -216 1 063 -780

Net changes in cash and cash equivalents -142 423 -528 -851

Cash and cash equivalents at the start of the period 1 799 1 522 2 220 2 695 Exchange gain/loss on cash and cash equivalents 10 5 -25 107 Cash and cash equivalents at the end of the period 1 667 1 951 1 667 1 951

According to management reporting

- Q2 Presentation 2016DOF ASA 31

Management reporting vs Financial reportingRESULT Q2 2016 Q2 2015

Amounts in NOK mill

Management reporting

Reconciliation to equity method

Financial reporting

Management reporting

Reconciliation to equity method

Financial reporting

Operating income 2 439 -75 2 364 2 778 -129 2 648 Operating expenses -1 684 29 -1 655 -1 940 20 -1 920 Net profit from associated and joint ventures 2 -29 -28 0 104 104 Net gain on sale of tangible assets 3 - 3 138 -43 95

Operating profit before depreciation EBITDA 760 -75 685 976 -48 928 Depreciation -278 12 -266 -304 23 -282 Impairment -260 28 -232 -262 - -262 Operating profit - EBIT 222 -35 187 410 -25 384

Financial income 33 6 39 19 4 23 Financial costs -304 10 -294 -306 13 -293 Net realised gain/loss on currencies -90 15 -74 -79 13 -67 Net unrealised gain/loss on currencies 246 -1 244 183 -27 156 Net changes in fair value of financial instruments 28 -0 27 97 -2 96 Net financial costs -88 30 -58 -85 - -85 Profit (loss) before taxes 134 -5 129 325 -25 300 Taxes -64 5 -59 -105 25 -81 Profit (loss) 70 -0 70 219 0 219

- Q2 Presentation 2016DOF ASA 32

Management reporting vs Financial reportingBALANCE 30.06.2016 30.06.2015

Amounts in NOK mill

Management reporting

Reconciliation to equity method

Financial reporting

Management reporting

Reconciliation to equity method

Financial reporting

ASSETSIntangible assets 1 413 -68 1 345 1 404 -91 1 313 Tangible assets 28 620 -4 294 24 327 26 840 -2 796 24 044 Non-current financial assets 649 1 290 1 939 366 1 011 1 377

Total non-current assets 30 682 -3 071 27 611 28 610 -1 877 26 733

Receivables 2 828 -124 2 703 3 026 -73 2 953 Cash and cash equivalents 1 667 -225 1 442 1 951 -76 1 874

Total current assets 4 495 -349 4 145 4 976 -149 4 827 Asset held for sale - - - - - -

Total current assets incl. Asset held for sale 4 495 -349 4 145 4 976 -149 4 827 Total assets 35 177 -3 421 31 756 33 586 -2 026 31 560

EQUITY AND LIABILITIESEquity 6 380 - 6 380 6 592 - 6 592 Non-current provisions and commitments 79 -35 45 130 -30 101 Non-current liabilities 23 000 -3 047 19 953 19 361 -1 767 17 594 Current liabilities 5 717 -339 5 378 7 503 -229 7 274

Total liabilities 28 797 -3 421 25 376 26 994 -2 026 24 968 Liabilities held for sale - - - - - -Total liabilities incl. Liabilities held for sale 28 797 -3 421 25 376 26 994 -2 026 24 968 Total equity and liabilities 35 177 -3 421 31 756 33 586 -2 026 31 560

Net interest bearing liabilities 24 723 -3 034 21 689 22 560 -1 856 20 705

- Q2 Presentation 2016DOF ASA

DO

F ex

Sub

sea

DO

F S

ubse

a

Bonds:• DOF09, 10 and 11 deleted and replaced by a Subordinated

Convertible bond

Bank Balloons:• Reduced amortisation DOF after refinancing

DOF GROUP COUNTERPARTY EXPOSURE Q2 2016

33

ECA mainly represent exposure with Norwegian and Brazilian ECAs

Debt maturity profile after restructuring debt

-

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2016 2017 2018 2019 2020 After

Bank Debt

Balloons

Bond

-

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

2016 2017 2018 2019 2020 After

Bank Debt

Balloons

Bond

44 % 50 %

6 %

ECA

Banks

Bonds

DOF Subsea

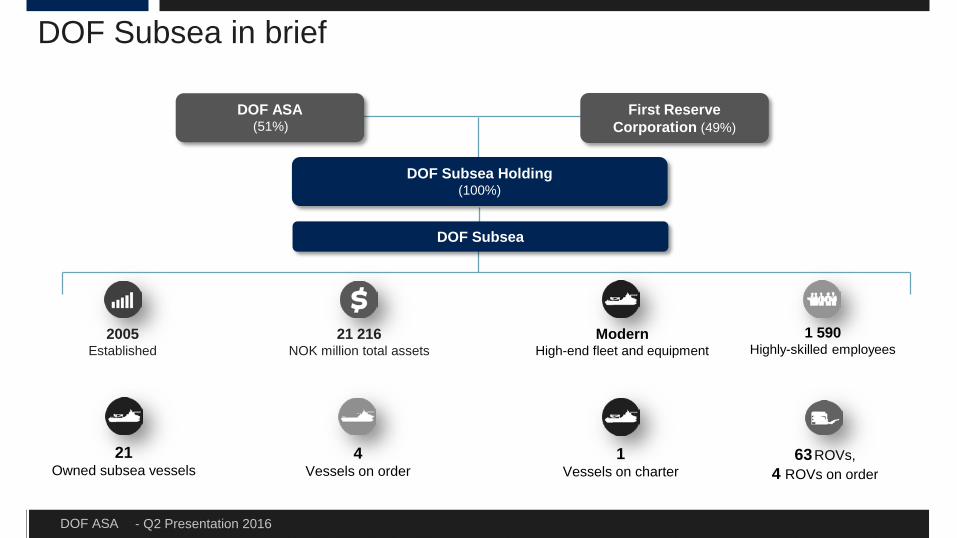

- Q2 Presentation 2016DOF ASA

2005Established

21 216 NOK million total assets

ModernHigh-end fleet and equipment

21Owned subsea vessels

4Vessels on order

1Vessels on charter

63ROVs,4 ROVs on order

First Reserve Corporation (49%)

1 590Highly-skilled employees

DOF Subsea Holding(100%)

DOF ASA(51%)

DOF Subsea in brief

DOF Subsea

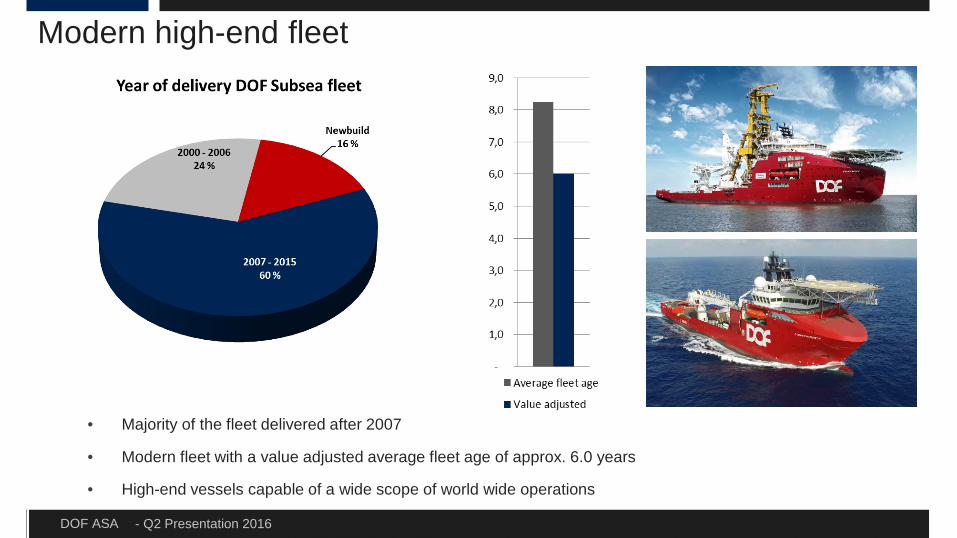

- Q2 Presentation 2016DOF ASA

• Majority of the fleet delivered after 2007

• Modern fleet with a value adjusted average fleet age of approx. 6.0 years

• High-end vessels capable of a wide scope of world wide operations

Modern high-end fleet

- Q2 Presentation 2016DOF ASA

DOF Subsea ranked as IMCA International Contractor

Tier 1

Tier 2

Tier 3

IMCA Membership

Surf / IMR / Construction

Heavy lift / trunkline / FPSO / Intervention

Vessel operators

GlobalContractor (6)

Saipem, Technip,Subsea 7

Allseas, Hereema, McDermott

International Contractor(6)

DOF, EMAS,Fugro

Helix, BW, SBM

Contractor Ocean Installer, Bibby, several others

Several Farstad, Eidesvik, Havila, Island Offshore, Olympic, Solstad

Typically lump sum projects driven by E&P spending

Typically day rate projects, OPEX driven within IMR/Light construction

37

- Q2 Presentation 2016DOF ASA

DOF Subsea - a leading subsea IMR provider

38

Awarded IMR contracts with total value of NOK 6.5 billion in 2015

Continues with Shell IMR contract award July 2016 – 5+2+2 year contract

Combination of vessel expertise, subsea operations and low overhead makes DOF competitive

Historical margins approx. 10-15 %, and typically 3-10 year contracts + vessel EBITDA

Highly competitive today, but still positive margins 2-7 % + vessel EBITDA

Several opportunities with key clients (APAC, Atlantic, Brazil and North America)

Stable/improving IMR market going forward

Increased demand for one supplier of vessel andIMR services, with ability to deliver light construction

DOF is well positioned to capture more contracts in this market

- Q2 Presentation 2016DOF ASA

DOF Subsea - a leading subsea IMR provider

Shell Australia awarded DOF Subsea a 5 year + 2 x 2 year options for fulltime Underwater Services and Multi-Purpose Supply Vessel (MPSV) Services to the Prelude FLNG facility, offshore Australia

Combination of vessel expertise, subsea operations track-record and shared safety, environmental and local-content objectives made DOF Subsea competitive

Established local presence and organisational expertise - combination of Australian and Norwegian teams

Client opted for an integrated solution with one supplier

Differentiated offering from DOF resulted in contract award

Integrated work scope:• Provision of MPSV and substitute

MPSV with associated marine crew; • Project Management and Engineering• IMR program services • Subsea inspection/intervention services• Survey Services• Data Management / Reporting services • ROV and tooling services • Asset management• Platform Supply services • Non-planned maintenance • Emergency response

Client and location:Shell Australia is part of The Shell Group, a global group of energy and petrochemical companies. Shell’s world-leading FLNG technology is to be deployed at the Prelude FLNG facility – it is the largest floating facility ever built, it will produce, liquefy, store and transfer LNG at sea. The facility will be located 475 kilometres north-north east of Broome, in Western Australia.

39

- Q2 Presentation 2016DOF ASA 40

According to management reporting

DOF Subsea quarterly performance (excl. asset sales)

NOK Million Q2 2013 Q2 2014 Q2 2015 Q2 2016Operating revenue 1 679 1 963 1 962 1 660 EBITDA 471 543 515 510 EBITDA margin 28% 28% 26% 31%

Non-current assets 16 344 16 151 16 578 18 206 Current assets 3 319 3 252 3 414 3 010 Total assets 19 663 19 403 19 992 21 216

Equity 4 996 5 962 6 405 6 330 Non-current debt 11 862 9 701 9 009 11 864 Current debt 2 805 3 741 4 577 3 022 Total Equity and Debts 19 663 19 404 19 991 21 216

0%

5%

10%

15%

20%

25%

30%

35%

40%

-

500

1 000

1 500

2 000

2 500

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016

EBIT

DA m

argi

n

NO

K m

illio

n

Operating income EBITDA EBITDA margin

- Q2 Presentation 2016DOF ASA

In general, weak global markets within supply and subsea, however still differences in regional opportunitiesSubsea: APAC market

Reduced spending from operators leading to low activity Competition scene changing with the bigger contractors now interested in IMR as

construction work dries up

DOF SUB: Still long and short term opportunities, but downward pressure on rates and slower tender activities

Brazil market We expect a slow market, with few new tenders, strong pressure on rates and “blocking activity” leading to termination and renegotiation of contracts (DOF is benefiting from blockings).

DOF SUB: Challenging and time-consuming for vessels that are up for renewal

Important with Brazilian flag

Market and outlook

41

- Q2 Presentation 2016DOF ASA

Market and outlook

42

Subsea: North America market We still see a reasonable level of activities in the IMR and Tie-back, however prices

are lower due to cost saving approach by the Operators Added opportunities following fewer competitors in market Better opportunity in Canada, where local presence is minimum

DOF SUB: Maintaining our position. We expect to see a gradual increase in market share in the medium

term, as target clients provide access to opportunities. Flexible business model with chartered-in vessels.

Atlantic market We expect Norway to be weak in 2016 We expect UK to be weak in 2016

DOF SUB: Normand Reach redelivered

- Q2 Presentation 2016DOF ASA

Market and outlook

43

Supply: Brazil: Slow market continues, with few new tenders, increased competition and lower rates. Petrobras redelivering vessels in order to reduce current fleet size, but at slower pace. DOF: Few vessels up for renewal. There are some opportunities for Brazilian flagged and international

vessels using “REB flag import capacity”, through blocking. Slow progress on negotiations and risk of idle time.

North Sea: We expect the North Sea market for both AHTS and PSV to be weak.DOF: Low market exposure in Q3, but gradually higher exposure going forward.Asia Pacific: We see low tender activity in the region within supply. Downward pressure on rates and over-supply of tonnage.DOF: 3 vessels in the region, two on term contracts and one in the spot market.

- Q2 Presentation 2016DOF ASA

Operational EBITDA for Q3 2016 to be weaker than Q2 2016, however no change in full year guidance

Refinancing plan completed and DOF has secured sufficient liquidity to sustain a downturn until 2020 and is well positioned for healthy earnings when the marketrecovers

Challenging markets expected to continue

Outlook

44

Thank youPresented by Mons Aase - CEOHilde Drønen - CFO

- Q2 Presentation 2016DOF ASA

DISCLAIMER

This presentation by DOF ASA designed to provide a high level overview of aspects of the operations of the DOF ASA Group.The material set out in the presentation is current as at 17 August 2016.This presentation contains forward-looking statements relating to operations of the DOF ASA Group that are based onmanagement’s own current expectations, estimates and projections about matters relevant to DOF ASA‘s future financialperformance. Words such as “likely”, “aims”, “looking forward”, “potential”, “anticipates”, “expects”, “predicts”, “plans”, “targets”,“believes” and “estimates” and similar expressions are intended to identify forward-looking statements.References in the presentation to assumptions, estimates and outcomes and forward-looking statements about assumptions,estimates and outcomes, which are based on internal business data and external sources, are uncertain given the nature of theindustry, business risks, and other factors. Also, they may be affected by internal and external factors that may have a materialeffect on future business performance and results.No assurance or guarantee is, or should be taken to be, given in relation to the future business performance or results of theDOF ASA Group or the likelihood that the assumptions, estimates or outcomes will be achieved.While management has taken every effort to ensure the accuracy of the material in the presentation, the presentation is providedfor information only. DOF ASA , its officers and management exclude and disclaim any liability in respect of anything done inreliance on the presentation.All forward-looking statements made in this presentation are based on information presently available to management and DOFASA assumes no obligation to update any forward looking- statements. Nothing in this presentation constitutes investmentadvice and this presentation shall not constitute an offer to sell or the solicitation of any offer to buy any securities or otherwiseengage in any investment activity.You should make your own enquiries and take your own advice (including financial and legal advice) before making aninvestment in the company's shares or in making a decision to hold or sell your shares.

46