domestic economic conditions

DESCRIPTION

Domestic Economic Conditions. Jeff Fuhrer Director of Research Federal Reserve Bank of Boston Presented to the 495/MetroWest Corridor Partnership’s Economic Forum September 4, 2008 Chart assistance provided by Denny Lie. Overview. Update on the housing crisis: Still going - PowerPoint PPT PresentationTRANSCRIPT

Domestic Economic Domestic Economic Conditions Conditions

Jeff FuhrerJeff FuhrerDirector of ResearchDirector of Research

Federal Reserve Bank of BostonFederal Reserve Bank of Boston

Presented to the Presented to the 495/MetroWest Corridor Partnership’s 495/MetroWest Corridor Partnership’s

Economic ForumEconomic ForumSeptember 4, 2008September 4, 2008

Chart assistance provided by Denny LieChart assistance provided by Denny Lie

OverviewOverview

Update on the housing crisis: Still goingUpdate on the housing crisis: Still going

Update on financial market stresses: Update on financial market stresses: Still goingStill going

Outlook and risks for the real economy: Outlook and risks for the real economy: Weak second halfWeak second half

Outlook and risks for inflationOutlook and risks for inflation

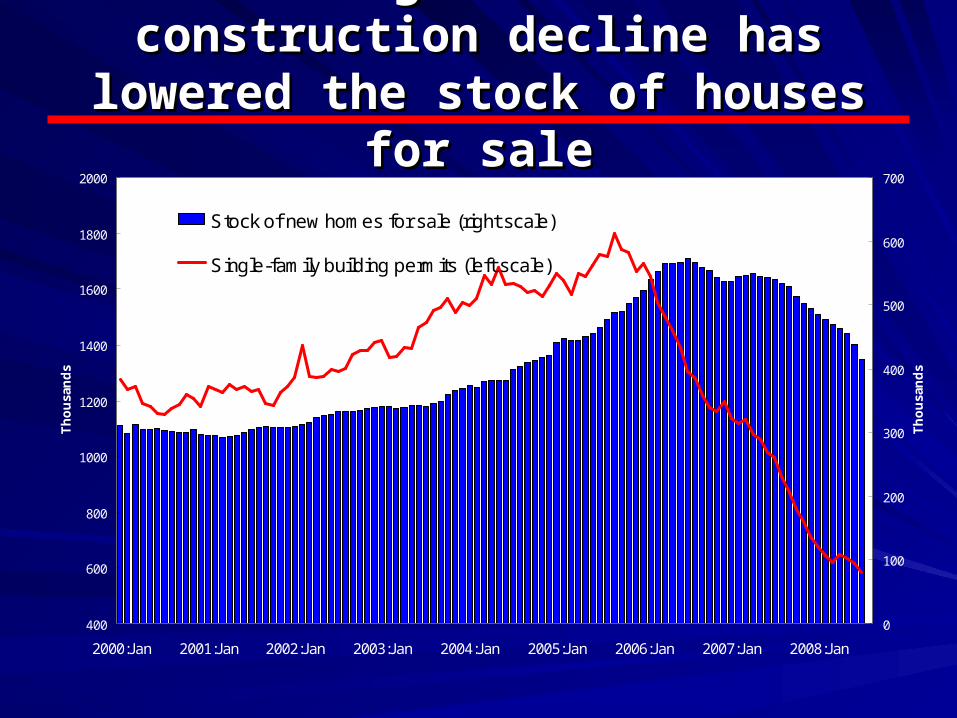

Housing: A massive Housing: A massive construction decline has construction decline has

lowered the stock of houses for lowered the stock of houses for salesale

400

600

800

1000

1200

1400

1600

1800

2000

2000:Jan 2001:Jan 2002:Jan 2003:Jan 2004:Jan 2005:Jan 2006:Jan 2007:Jan 2008:Jan

Th

ou

san

ds

0

100

200

300

400

500

600

700

Th

ou

san

ds

Stock of new homes for sale (right scale)

Single-family building permits (left scale)

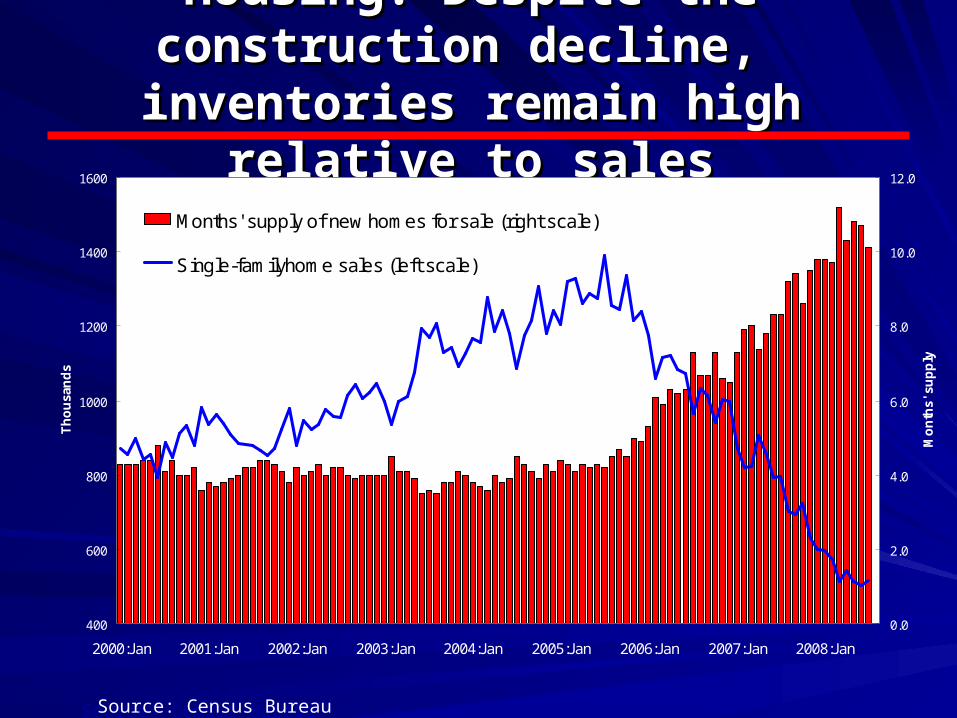

Housing: Despite the Housing: Despite the construction decline, construction decline,

inventories remain high relative inventories remain high relative to salesto sales

400

600

800

1000

1200

1400

1600

2000:Jan 2001:Jan 2002:Jan 2003:Jan 2004:Jan 2005:Jan 2006:Jan 2007:Jan 2008:Jan

Th

ou

san

ds

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Mo

nth

s' s

up

ply

Months' supply of new homes for sale (right scale)

Single-familyhome sales (left scale)

Source: Census BureauSource: Census Bureau

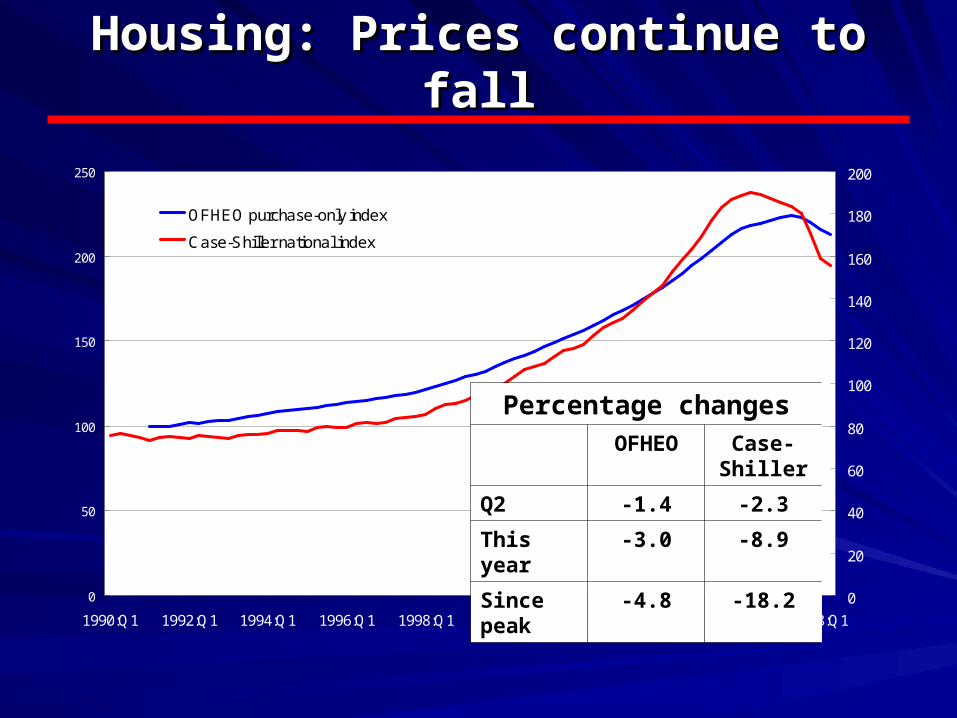

Housing: Prices continue to Housing: Prices continue to fallfall

0

50

100

150

200

250

1990:Q1 1992:Q1 1994:Q1 1996:Q1 1998:Q1 2000:Q1 2002:Q1 2004:Q1 2006:Q1 2008:Q1

0

20

40

60

80

100

120

140

160

180

200

OFHEO purchase-only index

Case-Shiller national index

Percentage changesOFHEO Case-

Shiller

Q2 -1.4 -2.3

This year

-3.0 -8.9

Since peak

-4.8 -18.2

Financial market conditions:Financial market conditions:Continued liquidity pressuresContinued liquidity pressures

Significant improvement in liquidity in markets

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2007

0101

2007

0214

2007

0330

2007

0515

2007

0628

2007

0813

2007

0926

2007

1109

2007

1225

2008

0207

2008

0324

2008

0507

2008

0620

2008

0805

Spread, 3-mo. $ Libor over 3-mo. OIS

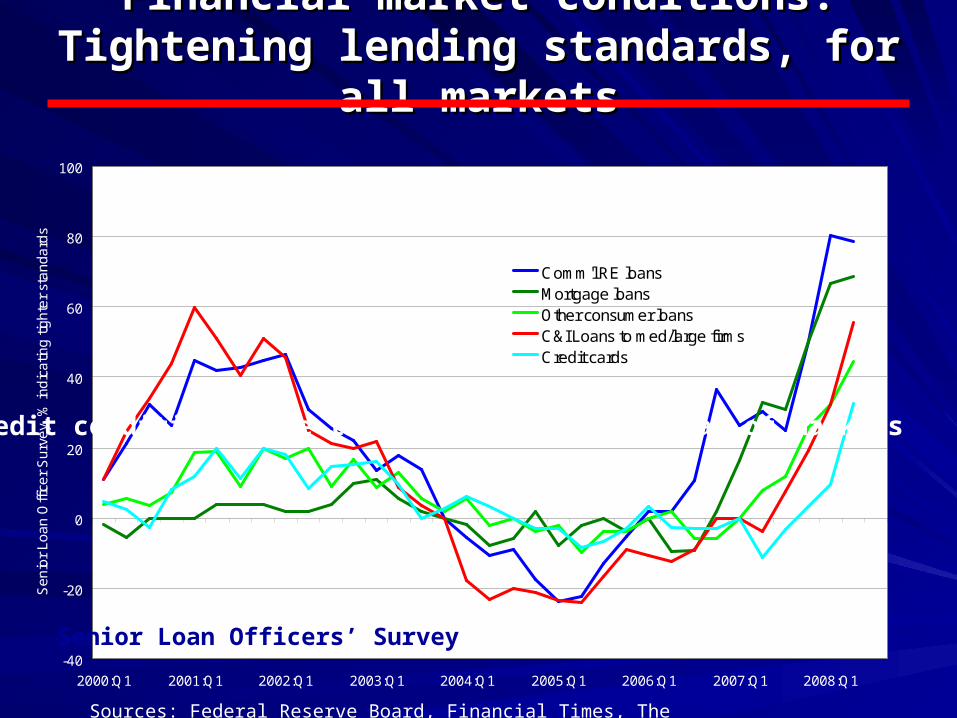

After improvement earlierthis year, conditions havecontinued to deteriorate

-40

-20

0

20

40

60

80

100

2000:Q1 2001:Q1 2002:Q1 2003:Q1 2004:Q1 2005:Q1 2006:Q1 2007:Q1 2008:Q1

Se

nio

r L

oa

n O

ffic

er

Su

rve

y, %

ind

ica

ting

tig

hte

r st

an

da

rds

Comm'l RE loansMortgage loansOther consumer loansC&I Loans to med/large firmsCredit cards

Credit conditions have tightened in a wide array of markets

Sources: Federal Reserve Board, Financial Times, The Wall Street Journal

Senior Loan Officers’ Survey

Financial market conditions:Financial market conditions:Tightening lending standards, for Tightening lending standards, for

all marketsall markets

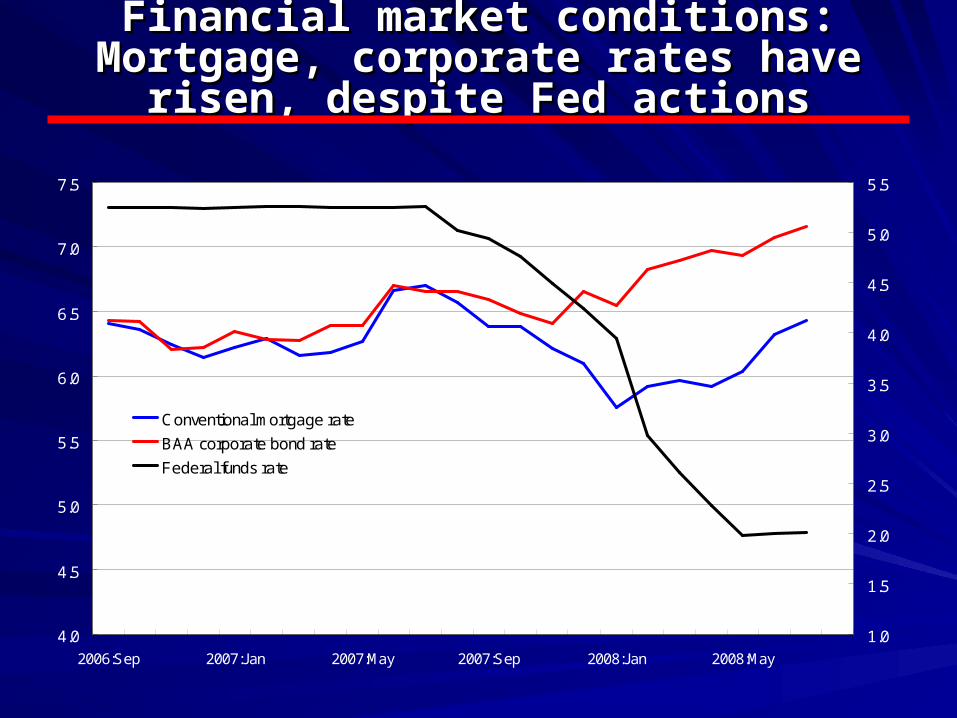

Financial market conditions:Financial market conditions:Mortgage, corporate rates have Mortgage, corporate rates have

risen, despite Fed actionsrisen, despite Fed actions

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

2006:Sep 2007:Jan 2007:May 2007:Sep 2008:Jan 2008:May

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Conventional mortgage rate

BAA corporate bond rate

Federal funds rate

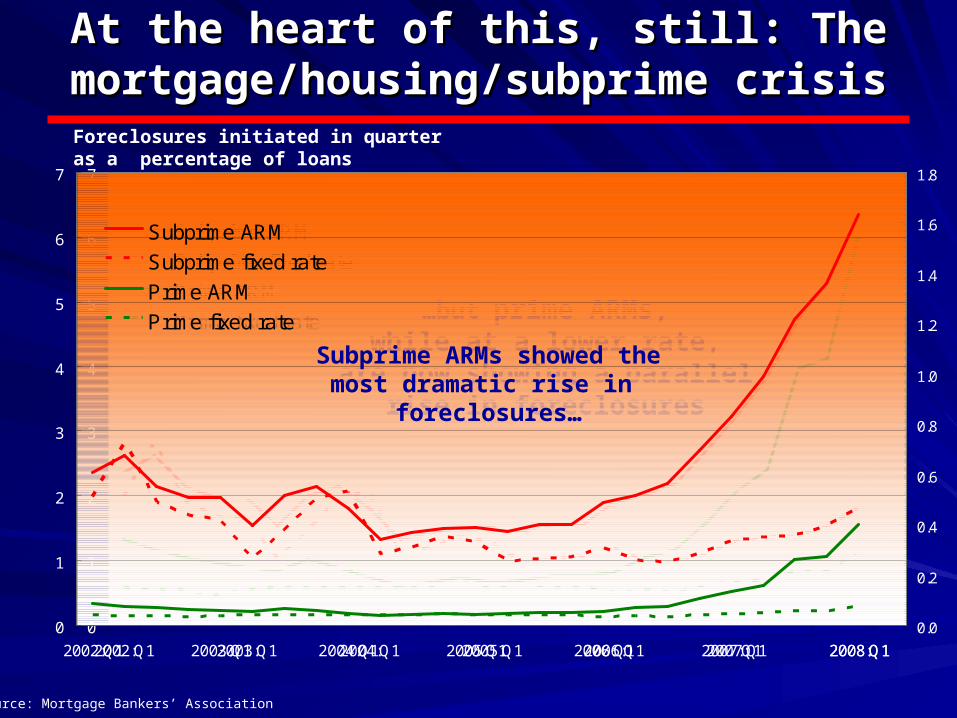

At the heart of this, still: The At the heart of this, still: The mortgage/housing/subprime crisismortgage/housing/subprime crisisForeclosures initiated in quarter as a percentage of loans

0

1

2

3

4

5

6

7

2002:Q1 2003:Q1 2004:Q1 2005:Q1 2006:Q1 2007:Q1 2008:Q1

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Subprime ARM

Subprime fixed rate

Prime ARM

Prime fixed rate …but prime ARMs,while at a lower rate,

are now showing a parallel rise in foreclosures

Source: Mortgage Bankers’ Association

0

1

2

3

4

5

6

7

2002:Q1 2003:Q1 2004:Q1 2005:Q1 2006:Q1 2007:Q1 2008:Q1

Subprime ARM

Subprime fixed rate

Prime ARM

Prime fixed rate

Subprime ARMs showed themost dramatic rise in

foreclosures…

Fed responses to financial market Fed responses to financial market problemsproblems

Liquidity measures (Goal: to restore flow of Liquidity measures (Goal: to restore flow of short-term lending)short-term lending)– Term Auction Facility (TAF)Term Auction Facility (TAF)

Take MBS as collateral in bids for short-term fundingTake MBS as collateral in bids for short-term funding

– Other lending facilities (to “primary dealers,” for Other lending facilities (to “primary dealers,” for longer terms, expand list of collateral, lend to longer terms, expand list of collateral, lend to used-car dealers, hot-dog stands, etc.)used-car dealers, hot-dog stands, etc.)

– Bear-Stearns—we could spend all day on this oneBear-Stearns—we could spend all day on this one

Underlying credit problems: Harder to Underlying credit problems: Harder to addressaddressMonetary policy responseMonetary policy response– Cut three 3-¼ percentage points since August Cut three 3-¼ percentage points since August

20072007

Lessons learned from financial Lessons learned from financial marketsmarkets

What have we learned?What have we learned?– We are infinitely capable of getting We are infinitely capable of getting

ourselves in trouble.ourselves in trouble.– That’s probably here to stay.That’s probably here to stay.– Regulation is to self-regulation as Regulation is to self-regulation as

important is to self-importantimportant is to self-importanta.a.

– A “AAA” rating for a fancy new asset A “AAA” rating for a fancy new asset really means “Could be pretty good stuff, really means “Could be pretty good stuff, who am I to say no?”who am I to say no?”bb

– When it comes right down to it, there’s When it comes right down to it, there’s only one institution you can trust:only one institution you can trust:

aWillem Buiter, 2008

THE FEDTHE FED

bEspecially if you’re willing to pay me a very large fee if I call it AAA

The Real EconomyThe Real Economy

Weak second half expectedWeak second half expected– Consumer supports not goodConsumer supports not good

Wage growth slowingWage growth slowingWealth decliningWealth decliningOil prices are “taxing”—some respite latelyOil prices are “taxing”—some respite latelyInterest rates not particularly lowInterest rates not particularly low

– Housing moribundHousing moribund– Commercial real estate—weakeningCommercial real estate—weakening– Exports—foreign growth stallingExports—foreign growth stalling

May well muddle through at low May well muddle through at low growth ratesgrowth rates– But weaker outcomes are possibleBut weaker outcomes are possible

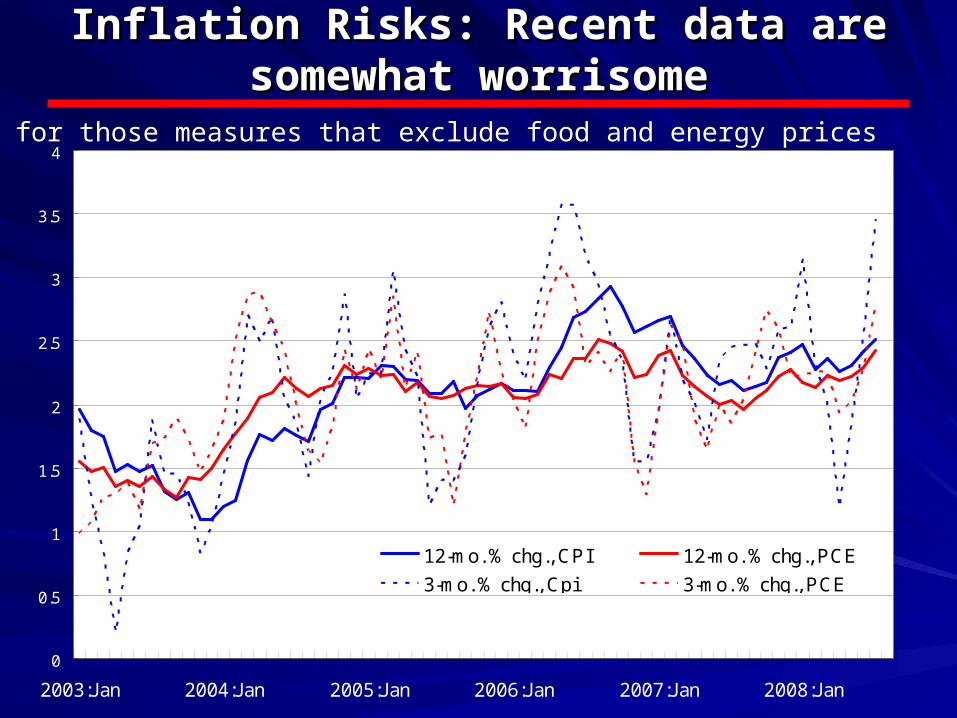

Inflation Risks: Recent data are Inflation Risks: Recent data are somewhat worrisomesomewhat worrisome

0

0.5

1

1.5

2

2.5

3

3.5

4

2003:Jan 2004:Jan 2005:Jan 2006:Jan 2007:Jan 2008:Jan

12-mo. % chg., CPI 12-mo. % chg., PCE

3-mo. % chg., Cpi 3-mo. % chg., PCE

Even for those measures that exclude food and energy prices

Inflation risks:Inflation risks: Some comfort— Some comfort— A slowing economy will helpA slowing economy will help

Sources: Bureau of Labor Statistics

CPI inflation (4-qtr. % chg.)

0

2

4

6

8

10

12

14

16

1955:Q1 1961:Q1 1967:Q1 1973:Q1 1979:Q1 1985:Q1 1991:Q1 1997:Q1 2003:Q1

Contrary to some analysts’ assertions, inflation always

falls during slowdowns

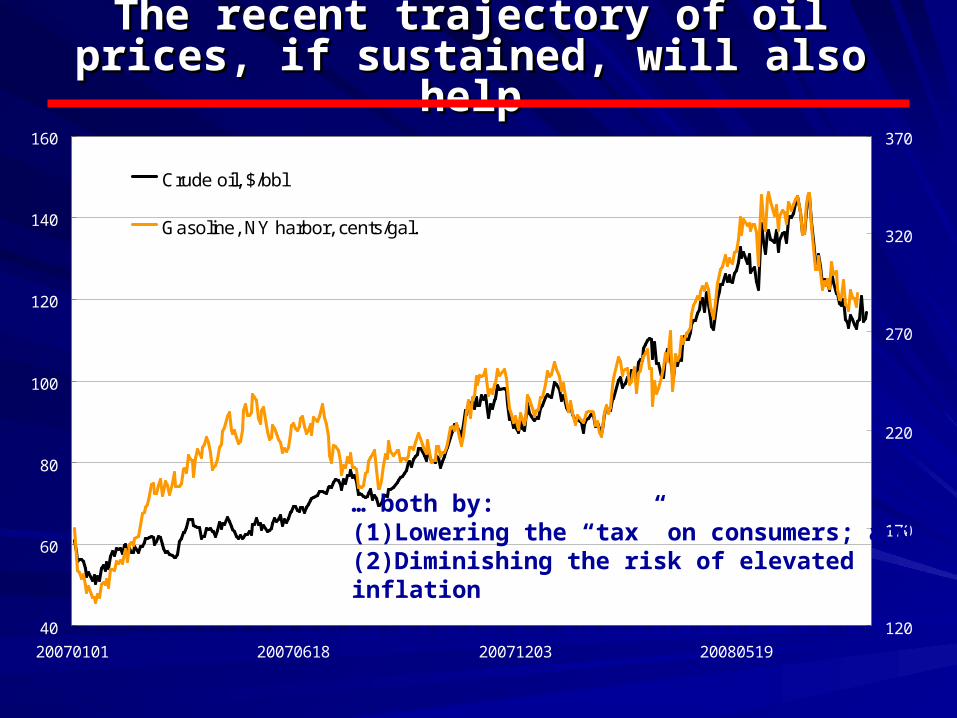

The recent trajectory of oil prices, The recent trajectory of oil prices, if sustained, will also helpif sustained, will also help

40

60

80

100

120

140

160

20070101 20070618 20071203 20080519

120

170

220

270

320

370

Crude oil, $/bbl

Gasoline, NY harbor, cents/gal.

… both by:(1)Lowering the “tax” on consumers; and(2)Diminishing the risk of elevatedinflation

SummarySummary

The housing slowdown continuesThe housing slowdown continues– Sales may flatten, but still inventory to work Sales may flatten, but still inventory to work

off, and prices continue to declineoff, and prices continue to decline

Financial markets remain somewhat Financial markets remain somewhat fragilefragile– Tightened lending standards, liquidity issuesTightened lending standards, liquidity issues

Expecting weak second-half growth, Expecting weak second-half growth, rising unemploymentrising unemploymentInflation a riskInflation a risk– Has been high latelyHas been high lately– Largely lagged effects of food, energy pricesLargely lagged effects of food, energy prices– Likely to retreat in coming monthsLikely to retreat in coming months