doosan: growing through m&as

TRANSCRIPT

1

Doosan: Growing through M&As

Jaeyong Song

Professor, Graduate School of Business, Seoul National University

Hyejun Kim

Master’s candidate, College of Business Administration, Seoul National University

Written in 2009.8.12

2

Doosan: Growing through M&As Since the 1990s, Doosan group has marked continuous growth with aggressive

restructuring and M&As. The company was one of the first Korean family-owned conglomerates who embarked on restructuring, and attracted public attention by desperate disposals and intensive exit strategy, even from its core business. The drastic remedy helped the company get through the financial crisis which threatened Asian economies in late 1990’s, and the sound financial structure enabled the company to successfully transform its major business from consumer goods to industrial goods. The transformation consequently facilitated aggressive growth of the firm, mainly based on decisive M&As.

Keeping in mind that tragic restructuring in the past was triggered by liquidity crisis,

Doosan coped well with most of financing, even large scale acquisitions, strategically employing liquidation and recurring investment. It was not until Doosan acquired Bobcat at $4.9 billion, the highest price ever in Korean M&A history, in 2007 that the liquidity issue emerged. Industry specialists even described the deal as the reckless pursuit of growth which sacrificed substance and stability that Doosan has emphasized.

The growth, however, could not be ceased easily. The group established the objectives for

2015 to reach sales of 100 trillion KRW, operating income of 10 trillion won, and 90% of oversea sales ratio. Considering the history of Doosan’s rapid growth, the objectives do not seem unrealistic. Sales dramatically increased from 5.3 trillion KRW in 1995 from 23 trillion KRW in 2008, and the market capital of 2007 recorded 48 times the price in 1998. Average growth rate of operating income reached 33% (Exhibit 1). Furthermore, the company announced that it will keep acquiring the hopeful companies, and that the only concern is how to manage its M&As, maintaining the speed and solving the matters in hand.1

1. The growth of Doosan group In 1896, the first modern private store in Korean history opened at Baeogae, Seoul.2 The

owner was Park Seung-jik, a 33-year-old famous, rich merchant who ran the textile business in national arena. Owing to his keen business insight, the Park Seung-jik Store became one of the most popular companies in Seoul in the 1920s. Park Too-Pyung, son of the founder, succeeded his business in 1946 and started the brewery and transportation business. He also changed the company name to Doosan Store, which later became the global company with 35,000 employees all over the world and 23 trillion KRW of sales in 2008, 60% from overseas.3

The growth of Doosan began to accelerate in 1952 when it founded OB(Oriental Brewery)

by acquiring a Japanese beer brewery.4 Fortunately, Korean beer market started to grow in

3

the 1960s and recorded a significant increase in demand in the 1970s. The market had maintained a surplus in demand for almost 40 years, the period that awarded victory to Doosan who had won overwhelming shares in Korean beer market. For those years, OB beer had been played as a symbol of Doosan group as well as that of beer itself. To keep in pace with the prosperity of Oriental Brewery, Doosan established Hankuk Bottle & Glass (1969) to manufacture glasses, Dongyang Agriculture (1975) to farm barleys and hops, and Doosan CCK(1979) to produce aluminum cans. To diversify in liquor business, Doosan group also founded Doosan Beverage (1968) to import beverages from the Coca-Cola company for the first time in Korea, set up a joint venture of OB Seagram (1980) to be the first domestic whiskey maker, and acquired Baekhwa Brewery (1985) for refined rice wine and Kyungwol (1993) for Soju, the most popular distilled liquor in Korea. To support the diversified beverage business, Doosan also executed the acquisition of Samhwa Crown & Closure (1994), the leading bottle cap manufacturer.

The liquor-related business, however, was not the only field Doosan focused on. Since

1960s, Doosan aggressively diversified its portfolio to food, construction, trade, press, and engineering, respectively represented by its affiliates of Hanyang Food, Dongsan Construction and Engineering(currently Doosan Engineering and Construction), Doosan Trading Company, Hapdong News Agency(currently Yonhap News), and Yoonhan Machinary(currently Doosan Mecatec). The expansion continued until the 1990s when Doosan was considered the leading domestic company in life and culture. Indeed, Doosan played a major role in domestic life and culture-related market. The firm entered the publication business by acquiring a domestic leading publisher, the restaurant business by licensing global food brands such as KFC, the leisure business by building resorts and country clubs, the fashion business by importing famous brands such as Polo and Guess, and the consumer product business by providing products from Nestle, Kodak, and 3M.

In 1995, after 100 years of continuous growth, Doosan launched a project to review its

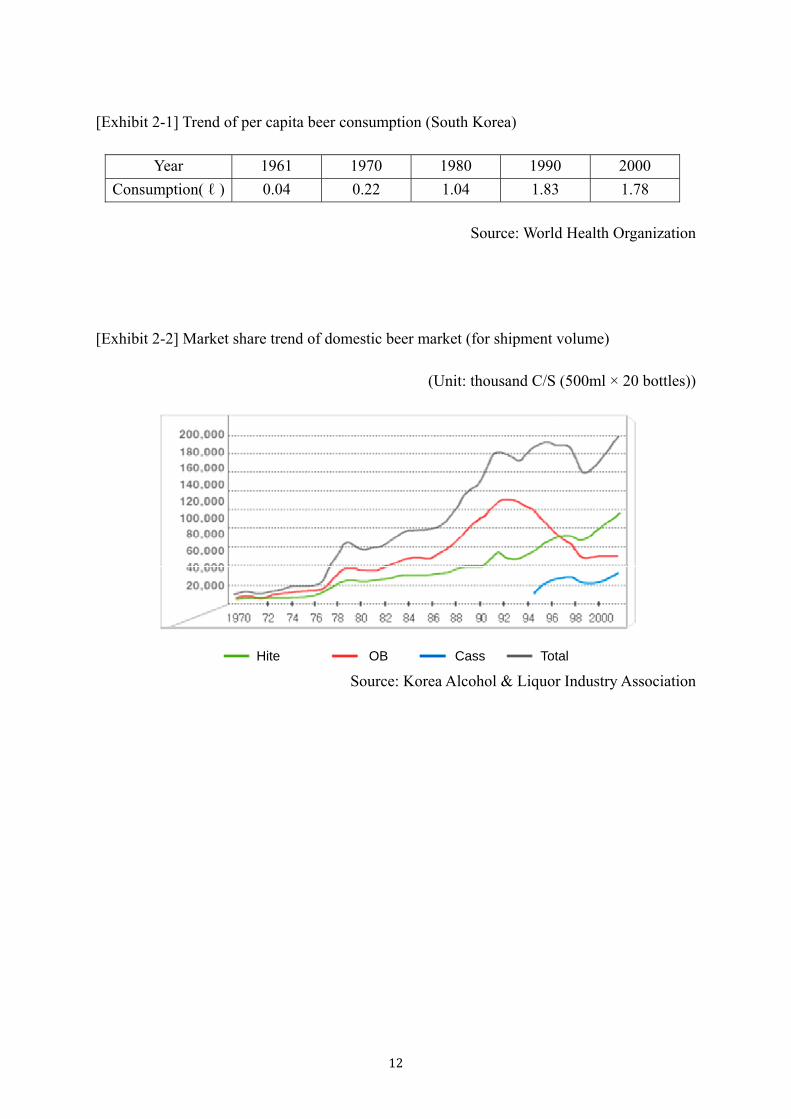

past 100 years and draw a blueprint for the next 100 years.5 What the project revealed, however, was not the rosy future but the deadly financial structure. Inside the glorious history was a mess. A cumulated loss reached 908 billion KRW(1995), putting the firm in need of additional loan to make up the loss. But the loan already amounted to 1 trillion won, with the debt ratio of 624% and ROIC(Return on invested capital) of -1%.6 Moreover, the gap between planned performance and realized one was widening. Even its beer business which had been highly profitable for decades was not safe. Hite, a competitor’s new beer brand which stressed mineral water base, made a big hit in the market. The unexpected victory of competitor pulled OB down to second place for the first time in its 40-year history, exposing all the beer related business, from barely to bottle cap, to danger (Exhibit 2).

2. Restructuring In December 1995, Doosan launched the first restructuring plan for the next 100 years. A

4

small numbers of exceptional talents, including former consultants, was gathered in a team called ‘Tri-C(Challenge, Create, Change)’. The team’s first goal was to secure cash flow and profit. That is, the team had to switch cash flow from huge loss to gain. To this purpose, team disposed all the unnecessary assets that could bring cash right away, starting from real estates to shares in joint venture. Doosan sold the OB beer factory in Seoul and ended joint venture businesses with its crucial partners such as Nestle, Kodak, 3M, and Coca Cola (Exhibit 3). It was not an easy process. The OB Seoul beer factory was where the founder first started the business, and all of the joint ventures it ended were its substantial businesses. In reward for the painful disposals, loss in cash flow decreased to 590 billion KRW in a year and turned to 13 billion KRW gain in the next year (Exhibit 4).

Unfortunately, the company was hit by the Asian economic crisis in 1997. Debt ratio that

seemed to be decreasing reached 600% again, and its remaining weak businesses were uncovered by depression. In the second restructuring program, Doosan had to build a truly sound financial structure by strategically evaluating, selecting, and integrating all of its working businesses. 7 It merged 23 affiliates to 5 main business units and sold off unprofitable businesses. To invite a foreign capital, it established a joint venture by disposing 50% shares of OB beers, one of the main businesses, to Interbrew in Belgium. The result came out to be successful, improving the debt ratio from over 600% in 1997 to 332% in 1998, and 159% in 1999.8

The third restructuring program in 1999, based on a sound financial structure, was focused

on improving the management system. A series of efforts-including manufacturing process reform, efficient outsourcing, and management infrastructure arrangement such as ERP- brought an improvement in profitability. Operating income, which had been remained around 5%, increased to 11.5%.

The next step for Doosan who endured three stages of restructuring was to discover a

growth engine. Having plenty of money in its pocket, Doosan seriously began to change its business portfolio by fully utilizing M&As. The CFP (Corporate Financing Project) team, a spin-off team from the Tri-C team, specialized in M&A and actively searched targets for acquisition.9 The group was in need of new driving forces that can revitalize the organization which was exhausted by painful rationalization and eventually undertake the group’s future.

“What we were holding after harsh disposals in 1990s, including disposal of beer

business which had been our main business, was very limited for the further growth. A few percent of organic growth was never enough to fulfill our ambition. To be the global enterprise sooner, we needed to build staircases to growth that required consequent steps of adding new platforms. Acquiring Hankuk Heavy Industry, we set our direction to ISB(Infrastructure Support Business) and concentrated on the area by acquiring related firms such as Dafewoo Machinery.”10

2009.6.3 Yongman Park, current CEO

5

3. Transformation into an infrastructure company The IMF(International Monetary Fund) bailout in 1997 brought about many changes to

Korea. Several large conglomerates failed in an instant and the whole nation suffered from severe rationalization. Bankruptcy occurred in succession, large-scale layoff prevailed, and irresponsible public organizations privatized. Hankuk Heavy Industry was also one of the privatized organizations who announced open tender in 1999.

Hankuk Heavy Industry was an integrated power generation supplier who served

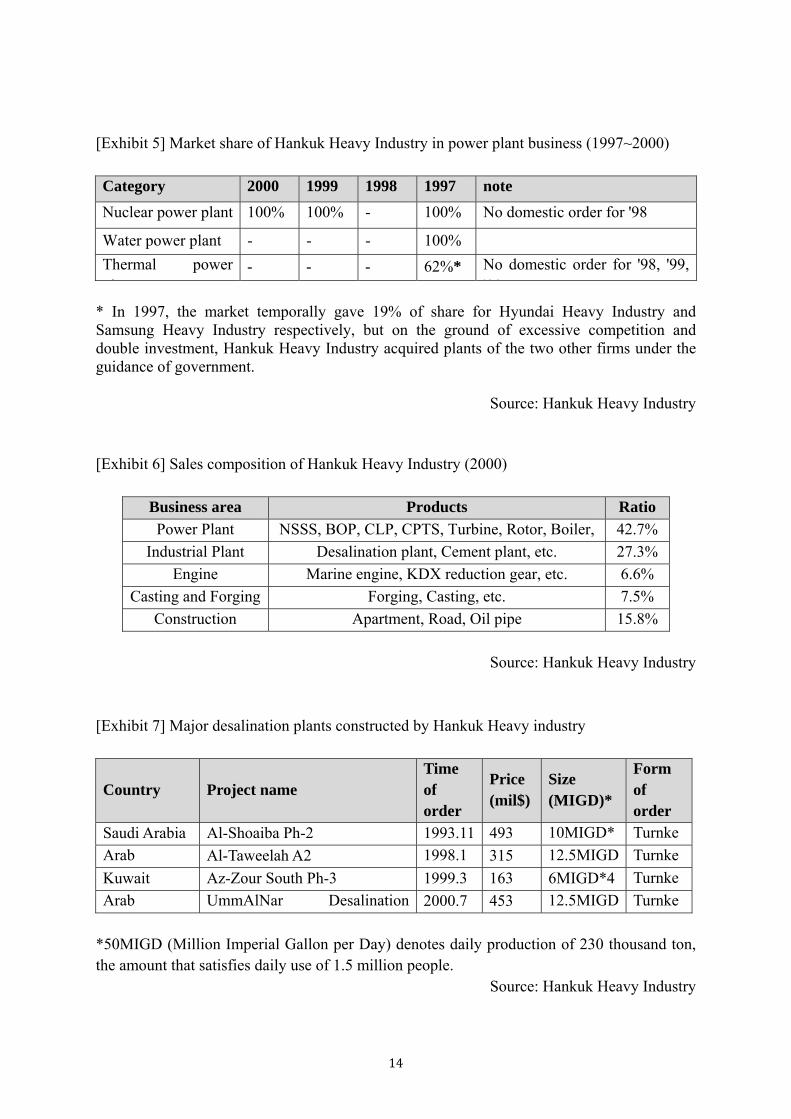

everything from raw material production to design, manufacturing, construction, test, and maintenance. In addition, it was the only supplier in Korea, producing most of nuclear, water, and thermal power plant with its own technologies. Since 1991 when power plant construction initiated, the organization had kept its balance in the black and became a blue chip company that maintained a low debt ratio (139% in 1999). Although it recorded losses in net profit in 2000, construction orders that had been in slump during the economic crisis were on the way to recovery. Since the market was still monopolistic, growth naturally guaranteed high profit (Exhibit 5).

Besides power plant, Hankuk Heavy Industry also produced industrial plant for cement,

iron, chemicals, and desalination business, and participated in construction business including casting and forging of industrial material, and civil engineering (Exhibit 6). Especially for desalination plant that converts sea water to fresh water, the organization’s technological excellence invited a series of orders from Mideast region including Saudi Arabia and the United Arab Emirates (Exhibit 7).

Hankuk Heavy Industry, despite its attractiveness, was highly underestimated in the

market. It was no wonder that a myriad of companies were anxious to acquire the target. Samsung Heavy Industry and Hyundai Heavy Industry were no exception, but the government restricted the acquisition by Korean big 4 conglomerate (Samsung, LG, SK, and Hyundai) in order to restrain the economic concentration of Chaebols.11 Many small and medium enterprises also participated in the acquisition race, but no one was better prepared than Doosan who completed the three steps of restructuring. Furthermore, Doosan’s capability in restructuring was considered to be perfect in solving the problems of Hankuk Heavy Industry who suffered from chronic issues of public organization. In December 2000, Doosan finally succeeded in acquiring of Hankuk Heavy Industry (currently Doosan Heavy Industries & Construction), whose asset amounts up 3.5 trillion KRW.

After the acquisition, Doosan could build a new, big support for the group. Although

heavy industry was neither close to the consumer business where Doosan had been concentrated on, nor supposed to create the direct synergy with its existing businesses such as machineries or construction, the business was to be managed by a long-term steady perspective, which fitted Doosan’s characteristics.12 The big deal experience also encouraged the group to be confident of M&As. After being acquired to Doosan, Hankuk Heavy Industry

6

went through several steps of restructuring and then began to grow vigorously. Depending on its two main businesses-power plant and desalination plant, Doosan Heavy Industries & Construction played major role in globalization that the group pursued since 1990s. (Exhibit 8)

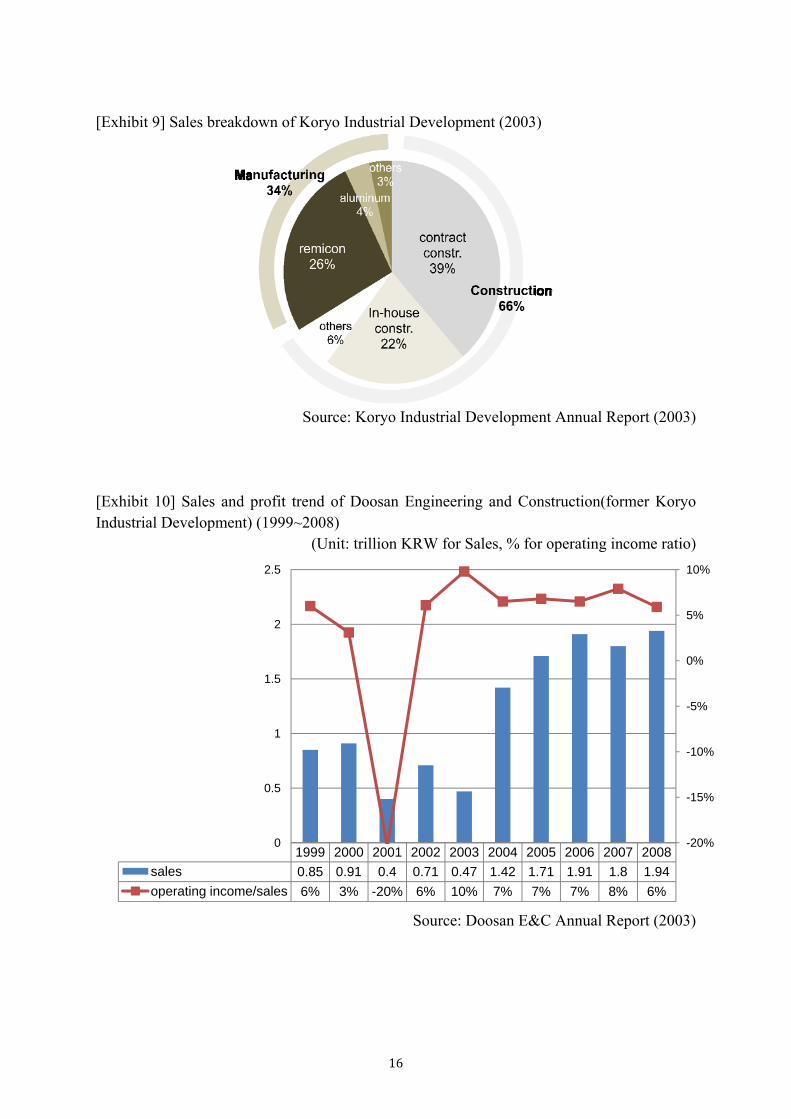

Doosan grew further after the big deal, setting its way to heavy industries. In 2003,

Doosan Engineering and Construction (Doosan E&C) acquired Koryo Industrial Development. While Doosan E&C had focused on apartment business with its representative brand ‘We’ve’, Koryo Industrial Development covered all the construction related business ranging from apartment to civil engineering, SOC(Social Overhead Capital) construction, and remicon(ready mix concrete) manufacturing (Exhibit 9).13 Although reckless management drove the company to bankruptcy, its core business was sustaining the competitiveness.14

Doosan E&C, formerly ranked 21st in the domestic construction market, jumped up to 10th

position by acquiring Koryo Industrial Development. Supported by resources acquired, its SOC business began expanding rigorously, executing most of the country’s public facilities including subways, highways, tunnels, reclamations, sewerages, and energy facilities. It also raised the apartment brand “we’ve” to major prestige brand. Focusing on construction business, Doosan E&C separated and transferred other businesses of Koryo Industrial Development such as remicon, aluminum, and emulsification businesses. Doosan E&C still sustains the top position in domestic construction market with its experiences and capabilities in planning, PF(Project Financing), and construction (Exhibit 10).

After acquiring Doosan Heavy Industries & Engineering and Doosan Engineering and

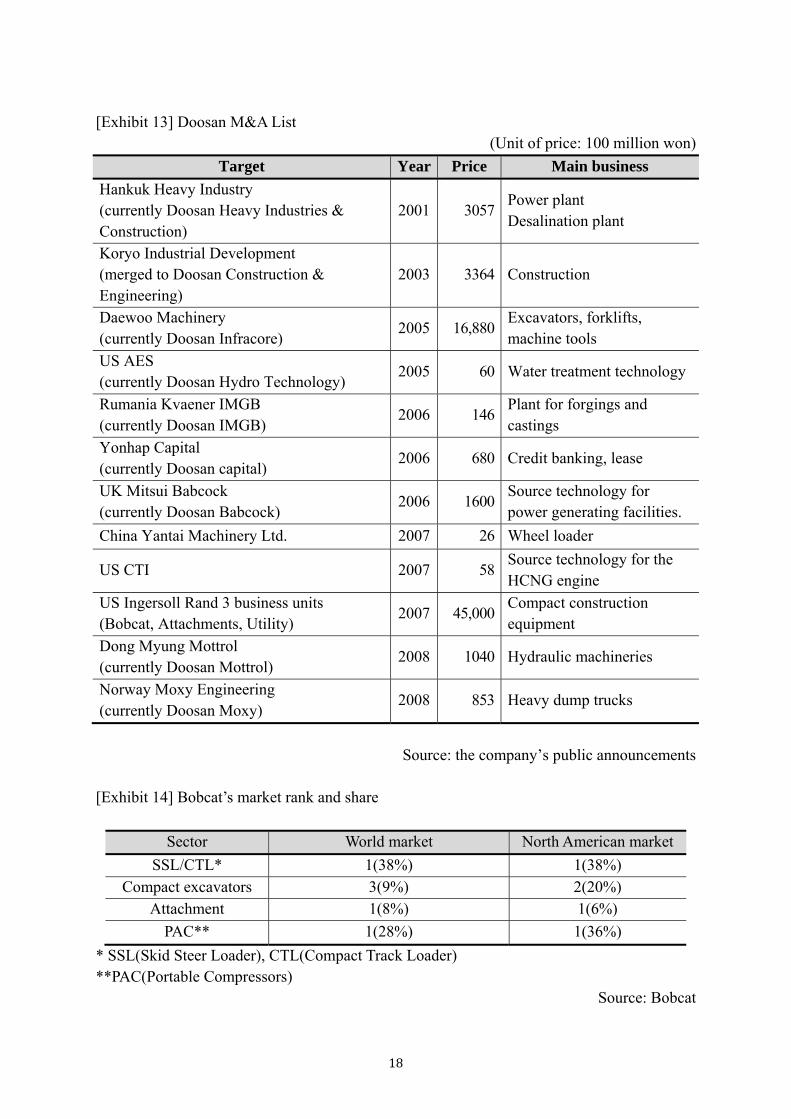

Construction, Doosan tried another reap by M&A in its way to infrastructure support business. Daewoo Machinery, currently Doosan Infracore, was timely put up for sale in the M&A market. Since Daewoo Group collapsed in 2001 by Asian economic crisis, Daewoo Heavy Industry was separated into Daewoo Machinery and Daewoo Shipbuilding & Marine Engineering. In spite of 6 years of restructuring which greatly improved economic performance of Daewoo Machinery, the company faced a crisis of being sold. 15 7 consortiums and 10 competitive companies were eager to acquire the company, but Doosan left all the competitors by presenting 1.7 trillion KRW.16

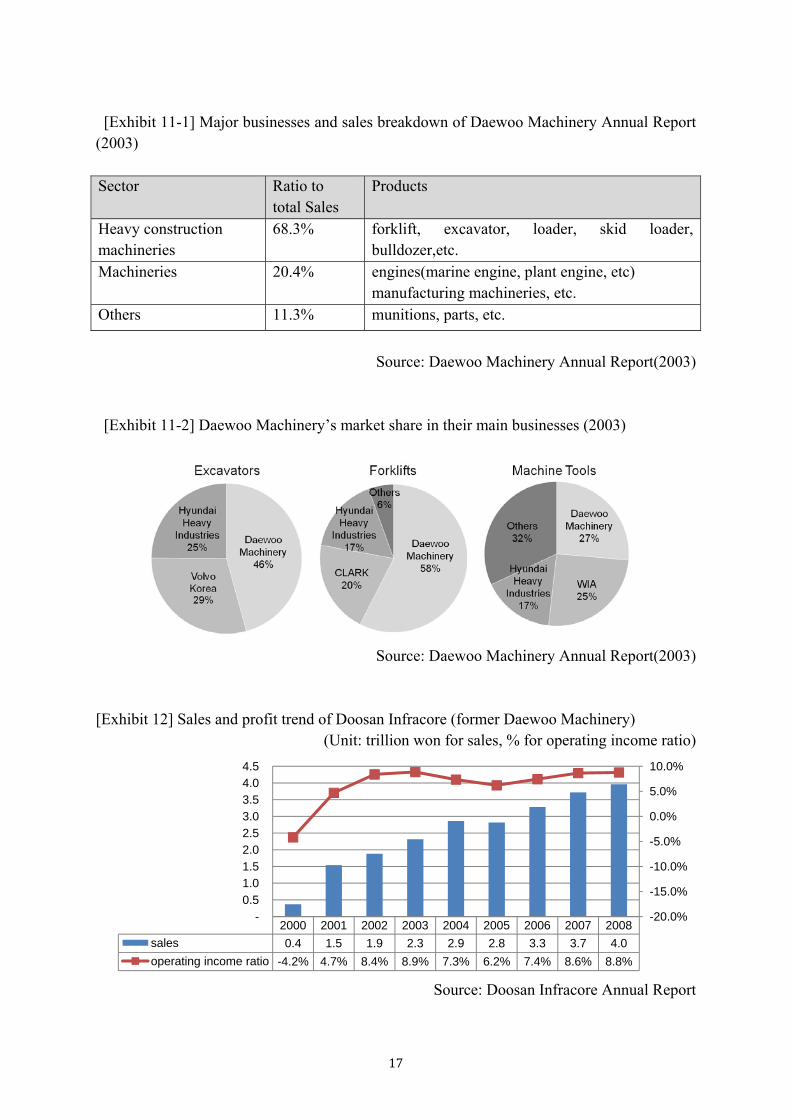

Deawoo Machinery was a leading manufacturer in three of its main markets: construction

equipment (excavators), machine tools, and forklifts (Exhibit 11). The company had a delicate equipment technology which had granted the company various technology related honors for several years, and sales also had shown a steady increase (Exhibit 12). In addition, it had established a local production in China and local sales branches in European countries including German and UK, the ventures which made Daewoo Machinery have a relatively high recognition in Chinese and European market. For Doosan who had many experiences only in the Middle East, Daewoo Machinery was a great target for the overseas market portfolio as well.

7

Thus far, the fourth step of restructuring for discovering a new growth engine and business transformation showed a favorable result to some extent. Three major deals successfully transformed the contracted consumer goods company into a confident infrastructure company. On its way to transformation, Doosan additionally sold off shares of of Oriental Brewery, the original business for the group, to be left only 5% in 2001, indicating the practical exit from the beer business. 74:26, the ratio of consumer goods to industrial goods of Doosan group in 1997, underwent a dramatic change and reversed to 15:80 in 2007.

The ISB(Infrastructure Support Business) field has become Doosan’s core business as well

as a growth engine. In addition to three acquired company-Doosan Heavy Industries & Construction, Doosan E&C, and Doosan Infracore, two existing businesses-Doosan Mechatech(former Doosan Machinery) and Doosan Engine- also set their courses to ISB, constituting Doosan’s major five ISB affiliates. The booming stage of construction industry in China and Middle East was also seen as an opportunity for Doosan. Nothing hindered Doosan’s growth. It was time to look further.

Yongman Park, current CEO and grandson of the founder, clarified that “Doosan is going

to foster ISB intensively as strategic industries”, announcing the acquisition of Daewoo Machinery. He also stated that “We will invest heavily in R&D, production facilities, and global networks for such purpose, and Daewoo Machinery (currently Doosan Infracore) will be at the center of the move.” His statement was realized by the fastest, most skillful way, M&A (Exhibit 13).

4. The beginning of global M&A In 2005, Doosan acquired the water treatment business of AES in US (currently Doosan

Hydro Technology) for 6 billion KRW. Through the acquisition, Doosan could obtain source technologies for the desalination key parts and RO (Reverse Osmosis) area. Soon after in June 2006, Doosan Heavy Industries & Construction acquired Kvaener IMGB (currently Doosan IMGB), the largest materials company for power generation facilities in Romania. Even though it was uncommon for Korean company to acquire finished oversea plant, Doosan noticed that the forgings and castings facilities in Kvaener IMGB were exactly the same as those of Doosan.17 That was because a German company produced two biggest press facilities 30 years ago and each of them was sent to Korea and Romania respectively.18 The Romanian plant that was laid almost in ruins at the time of acquisition improved remarkably by Doosan’s maintenance and reeducation, and soon played its role to meet the flourishing demand. Doosan could not only reinforce its plant facilities but also pave the way to the Middle East and European markets nearby.

In only 6 months, Doosan made another deal at 160billion KRW to acquire UK based

Mitsui Babcock (currently Doosan Babcock), one of the leading technology companies for power generating facilities. Overseas boiler market was almost dominated by source

8

technology companies, and B&W(US), Foster Wheeler(US), Alstom(France), and Mitsui Babcock(UK) were the only four companies who had the technology.19 With this acquisition, Doosan could not only achieve technological independence, a long desire, but also attain the global networks. Mitsui Babcock had been supplying boilers to 30 countries over the world, including North America, Europe, and China, and was in license contract with the biggest Chinese manufacturer, Harbin Boiler Company.20

In March 2007, the next year, Doosan Infracore acquired Yantai Machinery Ltd., a Chinese

wheel loader company, at 2.6 billion KRW. Located in Shandong, the target company provided both the production base and the permission to immediately enter the Chinese wheel loader market at a low cost.21 Since clients of wheel loader were overlapped with those of excavators, the acquisition enabled a full exploitation of sales and A/S network for the excavator business where Doosan led the market share.

In April of the same year, Doosan acquired CTI (Collier Technologies Inc., US) for 5.8

billion KRW. CTI had the source technology and patent for HCNG (Hydrogen Blended Compressed Natural Gas), which compounded CNG (Compressed Natural Gas) and Hydrogen.22 Its HCNG engine technology could meet the upcoming California 2007 heavy-duty emissions standard most efficiently, the capability guaranteeing competitive technological advantage.23 That is, Doosan could obtain the world class eco-friendly source technology, and also successfully entered the high value-added, rapidly growing engine market in North America. Other emerging economies such as South Korea, China, and India were also expected to create considerable demands for the low-emission automobile engine.

5. Acquisition of Bobcat and the expectations24 Since the acquisition of Daewoo Machinery in 2005, Doosan had followed the clear vision

of global brand and core technology in machine industries. All the acquisitions of AES, IMGB, Mitsui Babcock, Yantai Machinery, and CTI were strategically focused for the vision. To be a globally competent player, however, Doosan still needed something more. Doosan’s management team and CFP team were also aware of the need, naturally preparing the next big deal they must accomplish. Then Bobcat came up as a prospective candidate.

Bobcat started with the small factory established in 1947 by E.G Melroe, an American

farmer and inventor, with his four sons to manufacture combine (combiné hàrverster). After the serial hits of Melroe Self-Propelled Loader in 1958 and Skid loader (one of compact construction equipment) M-440 in 1962, the company switched its core business from agriculture to machinery and led Skid Loader business. The unprecedented hit of skid loader even made Bobcat as the synonyms to skid loader, the product.

Breaking the production record, Bobcat ventured to the European market in 1965. In 1969,

Melroe’s four brothers sold the company to Clark Equipment Company who could provide

9

more opportunities by giving access to the large capital and better human resources. Until 1970s, the company laid down the foundation in Europe around Belgium, and the accumulated capability later enabled its entry to Latin America and Japan. In 1988, Bobcat’s skid loader was selected by Fortune magazine as one of “America’s Best 100 Products”, and the honor was given once again in 1991. In 2004, Bobcat’s total production of skid loader recorded 600 thousand units, outnumbering the sum of all the other brands.

In 1995, Bobcat was acquired by Ingersoll-Rand Company and became the leading

compact equipment company with 135 years of history and 11.4 billion dollars of sales, covering production and service in transportation, construction, and agriculture related equipments. Continuously introducing various innovative compact equipments to the market, Bobcat grew to a global company with 5,600 employees and 73 local subsidiaries in 27 countries.25 By 2007, Bobcat recorded market share of 38% and 43% for US and European market respectively, global network of 2,700 dealer units, 16 production plants, and 9 R&D centers, sales of 2.85 billion dollars, and EBITDA of 440 million dollars.26 (Exhibit 14)

Then the subprime mortgage crisis occurred and put the US economy into the worst

recession in 2007. Construction industry was the first target as housing bubble burst, and the situation eventually affected Bobcat. Ingersoll-Rand Company, the parent company of Bobcat, tried to rationalize its business portfolio and decided to sell Bobcat in May 2007.

Doosan quickly prepared the acquisition of Bobcat and completed the deal in July 2007.

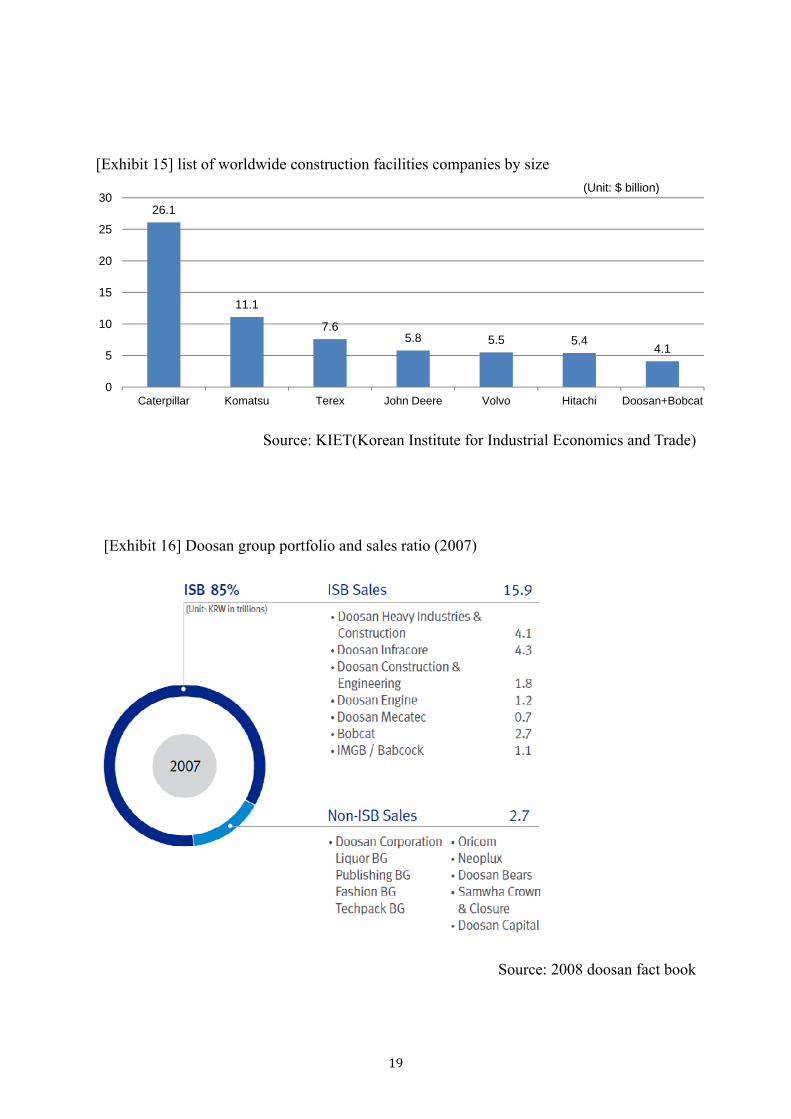

The acquisition price was 4.9 billion dollar (approx. 4.5 trillion KRW), the highest price ever in the Korean M&A history. The price reached almost a fourth of Doosan group’s total asset and double the total asset of the acquirer, Doosan Infracore. Park described the acquisition as “the most important and the last deal that will change the game of global construction equipment industry”. In his e-mail to the employees, he stated that “this acquisition will help Doosan achieve the 2015 goal of global top 5 in heavy industry and sales of 200 trillion won”. 27 He also expected “a big synergy which might help Doosan gain a global competitiveness at a stretch”. (Exhibit 15)

In fact, Bobcat was not a new target for 2007. Since 2005, the acquisition of Bobcat had

already been considered a prospective strategic option for becoming a top player in the equipment industry. 28 Park and CFP team were just waiting for the opportunity, preparing the acquisition plan and simulating the acquisition scenarios.29 Bobcat was expected to be an excellent target in terms of the product and market portfolio, because Bobcat was the world’s best compact equipment company while Doosan Infracore was competent in heavy equipment.30

Doosan’s accumulated experience in M&A was proved in the post-merger integration

(PMI) process as well as the pre-acquisition process. Doosan’s PMI philosophy could be explained by the statement of Park: “Why should I change the brand name after paying so much money for the brand? The destiny of brand is determined not by me, but by the

10

customers.”31 Doosan learned from past M&A experiences that full exploitation of focal employees with minimum expatriates is good for organizational and cultural integration. The company also learned that anxiety and uncertainty could drive out the core talents and hinder the organizational integration, leading the acquisition to failure at a heavy cost. Doosan indeed minimized the expatriates to 5 for Bobcat with 5,800 employees, showing its belief toward the PMI philosophy.32

Despite Doosan’s rich experiences in M&A, however, the voices of worry was getting

louder after the acquisition. People first worried about the high acquisition price.33 In most deals, Doosan bid higher than its competitors, and the premium ranged from hundreds of a million KRW to almost double the price of others. Especially under the subprime crisis which critically affected financial industry, a large amount of loan for M&A was considered to be a risky option. Others worried about the possibility of prolonged recession in the construction industry, which may critically threaten the future of Bobcat. There were also other voices that were skeptical about cross-border M&As. They pointed out that tens of cross-border M&A cases recently acquired by Korean firms were suffering from cross-cultural issues. Last worry reflected the general skepticism toward M&A’s. Considering empirical researches that indicate that only 30% of M&A can lead to successful result, Doosan’s rigorous M&A strategy seemed too risky.

6. Continuing M&As Despite public worries about the aggressive financing that Doosan has been pursuing

regardless of global economic recession, Doosan has kept a good pace with confidence accumulated by abundant experiences. Firmly setting its way to ISB, the current M&A strategy is steadily filling the empty spaces of ISB portfolio in product and region. (Exhibit 16) When announcing serial disposals of affiliates in order to finance M&As in 2009, Doosan declared its position: “We are keeping our eyes open to a new target. Our M&A strategy will never stop, unless there exists the target that can bring us the source technology or to help us venture to the new market.”34

11

[Exhibit 1-1] Sales trend of Doosan (1995~2007) (Unit: trillion KRW)

Source: 2008 doosan fact book

[Exhibit 1-2] Market capital trend of Doosan (1998~2007)

(Unit: trillion KRW)

Source: 2008 doosan fact book

5.3 4.93.4 3.4

6.9 7.2

14.2

18.6

0

5

10

15

20

1995 1996 1998 2000 2002 2004 2006 2007

0.5 0.92.1

10.8

24.1

0

5

10

15

20

25

30

1998 2002 2004 2006 2007

12

[Exhibit 2-1] Trend of per capita beer consumption (South Korea)

Year 1961 1970 1980 1990 2000

Consumption( ℓ ) 0.04 0.22 1.04 1.83 1.78

Source: World Health Organization

[Exhibit 2-2] Market share trend of domestic beer market (for shipment volume)

(Unit: thousand C/S (500ml × 20 bottles))

Source: Korea Alcohol & Liquor Industry Association

Hite OB Cass Total

13

[Exhibit 3] Doosan’s disposal list

Disposal list Year Price (100 million

KRW)

Nestle (1,539,000 shares) 1996 235

3M Korea (960,000 shares) 1996 900

Kodak Korea (423,000 shares) 1996 500

OB beers factory at Yeong deung po in Seoul 1996 1124

Beverage business (to Coca Cola) 1997 4322

Doosan Building (where the group’s headquarter located)

1998 690

Oricom Cable TV business goodwill 1998 55

Doosan Seagram shares 1998 1275

Joint venture with Interbrew regarding OB beers 1998 3500

OB beers (45% of shares) 2001 5600

Doosan Chongga Kimchi business unit (to Daesang) 2006 1050

Doosan Techpack (to MBK Partners) 2008 4000

Doosan Alcohol business unit(to Lotte) 2009 5030

Doosan DST, Korea Aerospace Industries, Samhwa Crown & Closure Company, SRS Korea

2009 7808

Source: the company’s public announcements

[Exhibit 4] Doosan’s cash flow trend (Unit: 100 mil KRW)

Source: Doosan

-9,080

-6,900

130

3,500

7,700

1995 1996 1997 1998 1999

14

[Exhibit 5] Market share of Hankuk Heavy Industry in power plant business (1997~2000) Category 2000 1999 1998 1997 note

Nuclear power plant 100% 100% - 100% No domestic order for '98

Water power plant - - - 100%

Thermal power l

- - - 62%* No domestic order for '98, '99, '00

* In 1997, the market temporally gave 19% of share for Hyundai Heavy Industry and Samsung Heavy Industry respectively, but on the ground of excessive competition and double investment, Hankuk Heavy Industry acquired plants of the two other firms under the guidance of government.

Source: Hankuk Heavy Industry

[Exhibit 6] Sales composition of Hankuk Heavy Industry (2000)

Business area Products Ratio

Power Plant NSSS, BOP, CLP, CPTS, Turbine, Rotor, Boiler, 42.7%

Industrial Plant Desalination plant, Cement plant, etc. 27.3%

Engine Marine engine, KDX reduction gear, etc. 6.6%

Casting and Forging Forging, Casting, etc. 7.5%

Construction Apartment, Road, Oil pipe 15.8%

Source: Hankuk Heavy Industry

[Exhibit 7] Major desalination plants constructed by Hankuk Heavy industry

Country Project name Time of order

Price (mil$)

Size (MIGD)*

Form of order

Saudi Arabia Al-Shoaiba Ph-2 1993.11 493 10MIGD* Turnke

Arab Al-Taweelah A2 1998.1 315 12.5MIGD Turnke

Kuwait Az-Zour South Ph-3 1999.3 163 6MIGD*4 Turnke

Arab UmmAlNar Desalination 2000.7 453 12.5MIGD Turnke

*50MIGD (Million Imperial Gallon per Day) denotes daily production of 230 thousand ton, the amount that satisfies daily use of 1.5 million people.

Source: Hankuk Heavy Industry

15

[Exhibit 8-1] Market capital trend of Doosan Heavy Industries & Construction (former Hankuk Heavy Industry) (2001~2007)

(Unit: trillion KRW)

Source: 2008 doosan fact book

[Exhibit 8-2] Doosan Heavy Industry (former Hankuk Heavy industry) sales and operating income trend since the acquisition (2000~2007)

(Unit: trillion won for sales, % for operating income ratio)

Source: Doosan Heavy Industry Annual Report

1 0.6

4

13.2

0

5

10

15

2001 2002 2005 2007

2000 2001 2002 2003 2004 2005 2006 2007 2008

sales 2.4 2.5 2.8 2.1 2.5 3.3 3.5 4.1 5.7

operating income to sales 3.4% 3.8% 5.4% 3.3% 8.5% 6.7% 5.9% 6.9% 8.3%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

0

1

2

3

4

5

6

16

[Exhibit 9] Sales breakdown of Koryo Industrial Development (2003)

Source: Koryo Industrial Development Annual Report (2003)

[Exhibit 10] Sales and profit trend of Doosan Engineering and Construction(former Koryo Industrial Development) (1999~2008)

(Unit: trillion KRW for Sales, % for operating income ratio)

Source: Doosan E&C Annual Report (2003)

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

sales 0.85 0.91 0.4 0.71 0.47 1.42 1.71 1.91 1.8 1.94

operating income/sales 6% 3% -20% 6% 10% 7% 7% 7% 8% 6%

-20%

-15%

-10%

-5%

0%

5%

10%

0

0.5

1

1.5

2

2.5

17

[Exhibit 11-1] Major businesses and sales breakdown of Daewoo Machinery Annual Report (2003) Sector Ratio to

total Sales Products

Heavy construction machineries

68.3% forklift, excavator, loader, skid loader, bulldozer,etc.

Machineries 20.4% engines(marine engine, plant engine, etc) manufacturing machineries, etc.

Others 11.3% munitions, parts, etc.

Source: Daewoo Machinery Annual Report(2003)

[Exhibit 11-2] Daewoo Machinery’s market share in their main businesses (2003)

Source: Daewoo Machinery Annual Report(2003)

[Exhibit 12] Sales and profit trend of Doosan Infracore (former Daewoo Machinery)

(Unit: trillion won for sales, % for operating income ratio)

Source: Doosan Infracore Annual Report

2000 2001 2002 2003 2004 2005 2006 2007 2008

sales 0.4 1.5 1.9 2.3 2.9 2.8 3.3 3.7 4.0

operating income ratio -4.2% 4.7% 8.4% 8.9% 7.3% 6.2% 7.4% 8.6% 8.8%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

-0.5

1.0 1.5 2.0 2.5

3.0 3.5 4.0 4.5

18

[Exhibit 13] Doosan M&A List (Unit of price: 100 million won)

Target Year Price Main business

Hankuk Heavy Industry (currently Doosan Heavy Industries & Construction)

2001 3057Power plant Desalination plant

Koryo Industrial Development (merged to Doosan Construction & Engineering)

2003 3364 Construction

Daewoo Machinery (currently Doosan Infracore)

2005 16,880Excavators, forklifts, machine tools

US AES (currently Doosan Hydro Technology)

2005 60 Water treatment technology

Rumania Kvaener IMGB (currently Doosan IMGB)

2006 146Plant for forgings and castings

Yonhap Capital (currently Doosan capital)

2006 680 Credit banking, lease

UK Mitsui Babcock (currently Doosan Babcock)

2006 1600Source technology for power generating facilities.

China Yantai Machinery Ltd. 2007 26 Wheel loader

US CTI 2007 58Source technology for the HCNG engine

US Ingersoll Rand 3 business units (Bobcat, Attachments, Utility)

2007 45,000Compact construction equipment

Dong Myung Mottrol (currently Doosan Mottrol)

2008 1040 Hydraulic machineries

Norway Moxy Engineering (currently Doosan Moxy)

2008 853 Heavy dump trucks

Source: the company’s public announcements

[Exhibit 14] Bobcat’s market rank and share

Sector World market North American market

SSL/CTL* 1(38%) 1(38%) Compact excavators 3(9%) 2(20%)

Attachment 1(8%) 1(6%)

PAC** 1(28%) 1(36%)

* SSL(Skid Steer Loader), CTL(Compact Track Loader) **PAC(Portable Compressors)

Source: Bobcat

19

[Exhibit 15] list of worldwide construction facilities companies by size

Source: KIET(Korean Institute for Industrial Economics and Trade)

[Exhibit 16] Doosan group portfolio and sales ratio (2007)

Source: 2008 doosan fact book

26.1

11.1

7.65.8 5.5 5.4

4.1

0

5

10

15

20

25

30

Caterpillar Komatsu Terex John Deere Volvo Hitachi Doosan+Bobcat

(Unit: $ billion)

20

Endnote

1 Jang C., Yongsung Park, CEO of Doosan Heavy Industries and Construction said “We will continue the M&A strategy”, The Korean Economic Daily, 2007/08/01. (In Korean) (http://www.hankyung.com/news/app/newsview.php?aid=2007080147011) 2 Kim (2001), <Park Seung Jik Store, 1882-1951>, Seoul: Hye An. (In Korean) 3 Doosan History, Doosan official homepage. (http://www.doosan.com/en/about/doosan_history.page?) 4 Ibid for this information and for most of the remaining information about history of Doosan 5 Kwon, S., et al.(2002), CEO Study: Doosan CEO Yongman Park, N-CEO (In Korean) 6 Kim, J.,(2001), ‘How we succeeded restructuring’, Nara Economies, April, 2001 (In Korean) 7 Kwak, S.,(2009), Doosan Restructuring Case, Strategic Management Case Presentation (In Korean) 8 Kim, J.,(2001), Ibid 9 Kim, M., 0.03% under the veil open the future for ‘New Doosan, 2008/05/20), Seoul Economic Daily. (In Korean) (http://economy.hankooki.com/lpage/industry/200805/e2008052017391747580.htm) 10 Kim, Y., Dukhan Kim, How to revitalize the old company: Court the attractive companies, Weekly Biz, Choson Ilbo, 2007.11.23. (In Korean) (http://news.chosun.com/site/data/html_dir/2007/11/23/2007112300619.html) 11 Kwon, S., et al.(2002), Ibid 12 Kwon, S., et al.(2002), Ibid 13 Kong, D.,, [Doosan Industrial Development] Growing as a blue chip company since the merger, The Korea Securities News, 2005/06/20. (In Korean) (http://ksdaily.co.kr/news/article.html?no=8955) 14 Ibid for this information and for most of the remaining information about the acquisition of Koryo Industrial Development 15 Cho, J., Daewoo Machinery, Corporate Research 03-37, SK research, 2003/10/23. (In Korean) (http://www.priden.com/data1/research/qna_file/(03-37)daewoomachine(1023).PDF) 16 Kim, M., Daewoo Machinery finally acquired by Doosan Heavy Industries, Seoul Economic Daily, 2005-04-29. (In Korean) (http://economy.hankooki.com/lpage/industry/200504/e2005042917244447580.htm) 17 Kim, T., Doosan Heavy Industries acquired Romanian factory, Maeil Buisness News Paper, 2007.11.23. (In Korean) (http://news.mk.co.kr/v3/view.php?year=2007&no=641560) 18 Ibid for this information and for most of the remaining information about the acquisition of Kveaner IMGB 19 Samil Price Waterhouse Coopers, Trend and Issues in Domestic and International M&A market, Issue report, Vol. 1, September 2009 (In Korean) 20 Park, K., Doosan Heavy Industries acquired U.K. based Mitsui Bobcock at 160 billion KRW, Construction Daily, 2006.11.08. (In Korean) 21 Cho, Y., Doosan Infracore acquired Chinese Wheel Loader company, financial news, 2007-03-19. (In Korean) (http://www.fnnews.com/view?ra=Sent0601m_View&corp=fnnews&arcid=00000920953741&cDateYear=2007&cDateMonth=03&cDateDay=19)

21

22 Park, M., [KORUS FTA] New business way/Doosan, Financial news, 2007-04-17(In Korean) (http://www.fnnews.com/view?ra=Sent0601m_View&corp=fnnews&arcid=0920975341&cDateYear=2007&cDateMonth=04&cDateDay=17) 23 Ibid for this information and for most of the remaining information about the acquisition of CTI 24 This part is written on the basis of the prior article, Shin, K. et al.,(2008), Doosan M&A Case. Seoul National Univeristy (In Korean) 25 Kim, M., [To the global stage] Doosan Infracore gears up to the world with international production networks, Seoul Economic Daily, 2008/08/13. (In Korean) (http://economy.hankooki.com/lpage/industry/200808/e2008081313042347580.htm) 26 Kim, D., Doosan, growing rapidly after changing its main business through M&A, Choson Ilbo, 2007/07/30. (In Korean) (http://news.choson.com/site/data/html_dir/2007/07/30/2007073001304.html) 27 Ibid 28 Chae, M., Power of Doosan’s M&A..pre-merger preparation from A to Z, Asiaeconomy Newpaper, 2009/06/11. (In Korean) (http://www.asiae.co.kr/news/view.htm?idxno=2009061110474877274&nvr=) 29 Ibid 30 Kim, Y., Dukhan Kim, Ibid 31 Kim, M., [To the global stage…] Doosan’s M&A philosophy, Seoul Economic Daily, 2008/08/13. (In Korean) (http://economy.hankooki.com/lpage/industry/200808/e2008081313093747580.htm) 32 Ibid 33 Doosan acquired Bobcat at about 13.1 times of its 2007 EBITDA, while Volvo acquired road equipment business of Ingersoll rand at 11 to 12 times of its EBITDA. Samsung Securities (2007.7.31) 34 Chae, M., Global Doosan’s Challenge without rest “find the new target for the growth”, Asiaeconomy Newpaper, 2009/06/12. (In Korean) (http://www.asiae.co.kr/news/view.htm?idxno=2009061211192524630&nvr=y)